Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Infor, Inc. | d17720d8k.htm |

| EX-99.1 - EX-99.1 - Infor, Inc. | d17720dex991.htm |

Exhibit 99.2

First excerpt from offering memorandum:

On August 10, 2015, we entered into an Agreement and Plan of Merger (the “Acquisition Agreement”) to acquire GT Nexus for $675 million. Pursuant to the Acquisition Agreement, Apollo Acquisition Sub, Inc. will be merged with and into GT Nexus, with GT Nexus as the surviving corporation (the “Acquisition”). We intend to finance the Acquisition with a combination of approximately $175 million of cash on hand and the net proceeds from the Notes offered hereby. The $675 million acquisition consideration also includes $125 million of equity that we expect to issue as part of a GTN shareholder and management equity rollover. The closing of the Acquisition is subject to customary closing conditions, including regulatory approvals. There can be no assurance that the Acquisition will be consummated on the expected schedule, pursuant to the agreed upon terms or at all.

GT Nexus operates an on-demand, cloud-based global supply chain management platform, which provides its customers with a rapid, low-cost way to enable and automate hundreds of inter-company supply chain processes on a global scale, and across entire trading communities, to drive operational efficiency and business agility. GTN’s platform manages over $100 billion of global trade annually and is utilized by over 28,000 businesses and over 100,000 users in 66 countries. We believe GTN’s platform and our ERP applications are highly complementary. Our ERP applications track orders within the walls of an enterprise, while GTN’s platform tracks orders outside of the enterprise. Combined, our solutions will provide users with end-to-end order tracking capability. Furthermore, we believe our applications would add another dimension by extending order visibility through sales, marketing, quoting and merchandise planning. We also anticipate the Acquisition to create attractive cross-selling opportunities.

For the twelve month period ended December 31, 2014, GT Nexus generated approximately $133.2 million in revenue and approximately $10.0 million of EBITDA, adjusted to exclude certain non-recurring items (“GTN EBITDA”), and as of December 31, 2014, GT Nexus had total assets of approximately $222.6 million, of which approximately $166.5 million were intangible assets (which includes goodwill). The GTN revenue, total assets and intangible assets are derived from audited financial statements of GTN that have been provided to us. GTN EBITDA is based on information provided to us by management of GTN and has not been independently verified by our management.

PricewaterhouseCoopers LLP has not audited, reviewed, compiled or performed any procedures with respect to any data of GTN. Accordingly, PricewaterhouseCoopers LLP does not express an opinion or any other form of assurance with respect thereto.

The information presented above should not be considered a substitute for audited or unaudited financial statements. See “Risk Factors—Risks Related to Our Business—This offering memorandum includes financial information prepared by other entities, which our management cannot independently verify.” and “Risk Factors—We have not provided you with historical financial statements for GTN or pro forma financial statements giving effect to the Acquisition.”

We expect to realize approximately $8.7 million in annualized operating synergies, consisting of reductions in GTN’s headcount and employee-related costs, general and administrative costs and

facilities costs. These synergies are focused on areas outside of the development and sales staff so as to avoid any impact on growth potential. These expected synergies constitute forward-looking statements and are not indicative of the results of the Acquisition. Additionally, such information was not prepared in accordance with (i) GAAP, (ii) the requirements of Regulation S-X under the Exchange Act, including Article 11 thereto, or (iii) any other securities laws relating to the presentation of pro forma financial information. Accordingly, you should not place undue reliance upon these estimates. Please refer to “Forward-Looking Statements” in this offering memorandum for additional information. These preliminary results should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “—Summary Historical Consolidated Financial Data” and the related notes thereto, and the consolidated financial statements and the related notes thereto, included or incorporated by reference elsewhere in this offering memorandum. For additional information, please see “Risk Factors.”

Second excerpt from offering memorandum:

| Lender Reported 12 Months Ended April 30, 2015 |

||||

| Credit Statistics As Adjusted for the Notes Offered Hereby: |

||||

| Ratio of Pro Forma total net debt to Adjusted EBITDA(11) |

6.9x | |||

| Ratio of Adjusted EBITDA to Cash Interest Expense(11) |

2.4x | |||

| (11) | The Credit Statistics As Adjusted for the Notes Offered Hereby presented in this offering memorandum are derived in part from the historical consolidated financial statements of Infor as modified to reflect: (i) adjustments to include the indebtedness and assumed interest expense resulting from the issuance of the notes, (ii) the intended use of an estimated $175.0 million of cash on hand to fund a portion of the Acquisition and (iii) an estimate of cash interest expense based on current interest rates on Infor’s debt, including the Credit Agreement (as defined herein) and the indentures governing our Existing OpCo Notes and the HoldCo Notes. The Credit Statistics As Adjusted for the Notes Offered Hereby excludes deferred financing fees, debt discounts and premiums, net, in connection with the issuance of the Existing OpCo Notes and the existing term loans. Credit Statistics As Adjusted for the Notes Offered Hereby represent non-GAAP financial measures. See “Non-GAAP Financial Measures.” If cash interest expense under the indenture governing our HoldCo Notes is excluded, our Ratio of Adjusted EBITDA to Cash Interest Expense would be 2.8x for the lender reported twelve months ended April 30, 2015. |

2

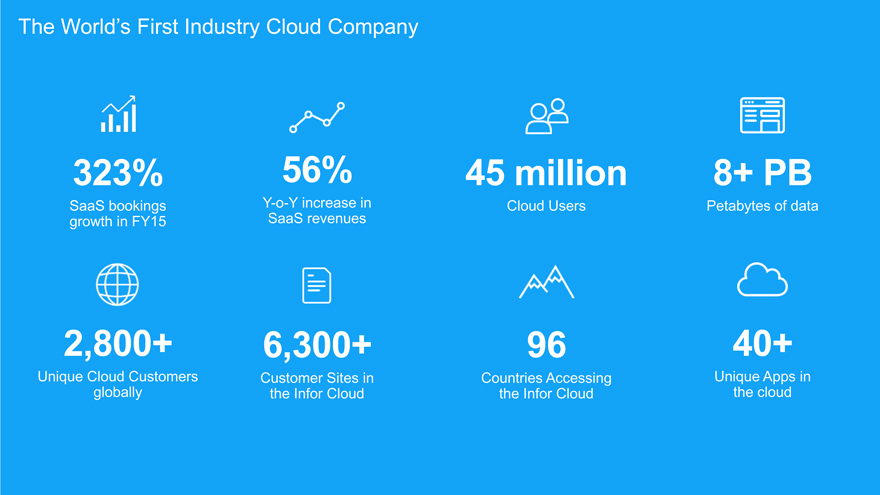

First excerpt from investor presentation:

3

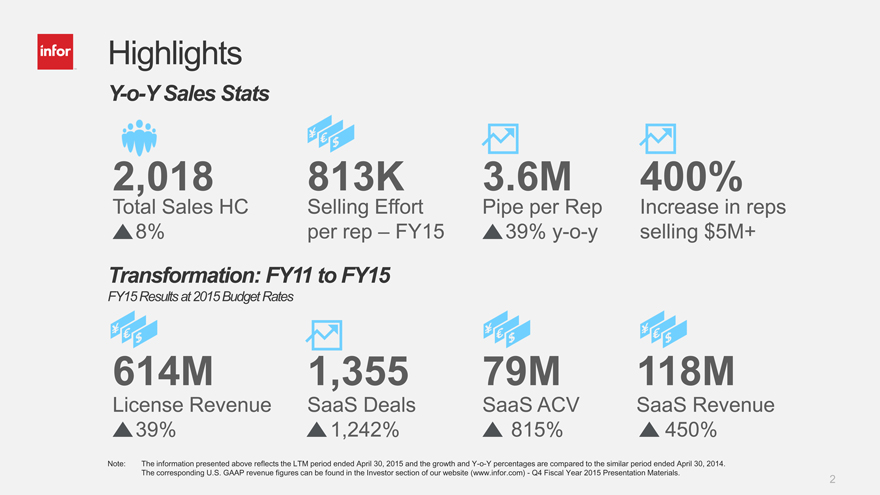

Second excerpt from investor presentation:

4