Attached files

Table of Contents

Index to Financial Statements

As filed with the Securities and Exchange Commission on August 10, 2015

Registration No. 333-205170

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Freeport-McMoRan Oil & Gas Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 1311 | 47-4274520 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

700 Milam, Suite 3100

Houston, Texas 77002

(713) 579-6000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

John F. Wombwell

Executive Vice President, General Counsel and Secretary

700 Milam, Suite 3100

Houston, Texas 77002

(713) 579-6000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Michael E. Dillard Sean T. Wheeler Latham & Watkins LLP 811 Main Street, Suite 3700 Houston, Texas 77002 (713) 546-5400 |

G. Michael O’Leary Henry Havre Andrews Kurth LLP 600 Travis Street, Suite 4200 Houston, Texas 77002 (713) 220-4200 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

Index to Financial Statements

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, dated August 10, 2015

PROSPECTUS

Shares

Freeport-McMoRan Oil & Gas Inc.

Class A Common Stock

This is the initial public offering of the Class A common stock of Freeport-McMoRan Oil & Gas Inc. We are offering shares of our Class A common stock. No public market currently exists for our Class A common stock.

We intend to apply to list our Class A common stock on the New York Stock Exchange under the symbol “FMOG.”

We anticipate that the initial public offering price will be between $ and $ per share.

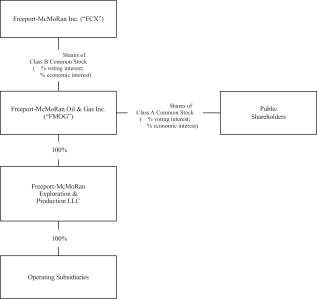

Following this offering, we will have two classes of authorized common stock: Class A common stock and Class B common stock. Each share of our Class A common stock entitles its holder to one vote on all matters to be voted on by stockholders, generally. Each share of our Class B common stock entitles its holder to five votes on all matters to be voted on by stockholders, generally. Holders of our Class A and Class B common stock vote together as a single class on all matters presented to our stockholders for their vote or approval, except as otherwise required by applicable law. Our parent company, Freeport-McMoRan Inc., will hold shares of Class B common stock, representing percent of our total outstanding shares of common stock, 100 percent of our total outstanding shares of Class B common stock, and percent of the combined voting power of our outstanding common stock upon completion of this offering, assuming that the underwriters do not exercise their option to purchase additional shares of Class A common stock from us. The shares being sold in this offering will represent percent of our total outstanding shares of common stock immediately following this offering assuming that the underwriters do not exercise their option to purchase additional shares of Class A common stock from us.

Investing in our Class A common stock involves certain risks. See “Risk Factors” beginning on page 25 of this prospectus.

| Per Share | Total | |||||||

| Price to the public |

$ | $ | ||||||

| Underwriting discounts and commissions(1) |

$ | $ | ||||||

| Proceeds to us (before expenses) |

$ | $ | ||||||

| (1) | See “Underwriting” for a description of all underwriting compensation payable in connection with this offering. |

We have granted the underwriters the option to purchase additional shares of Class A common stock from us on the same terms and conditions set forth above if the underwriters sell more than shares of Class A common stock in this offering.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Barclays expects to deliver the shares on or about , 2015 through the book-entry facilities of The Depository Trust Company.

| Barclays |

Prospectus dated , 2015

Table of Contents

Index to Financial Statements

| 1 | ||||

| 1 | ||||

| Deepwater GOM Producing Assets, Sanctioned Discoveries and Associated Drilling Inventory |

2 | |||

| Deepwater GOM Discoveries in Pre-Sanction Stage with Potential Development Opportunities |

6 | |||

| 6 | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

| 9 | ||||

| 10 | ||||

| 10 | ||||

| 11 | ||||

| 13 | ||||

| 13 | ||||

| 14 | ||||

| 15 | ||||

| 17 | ||||

| 18 | ||||

| 19 | ||||

| 20 | ||||

| 24 | ||||

| 25 | ||||

| 25 | ||||

| 49 | ||||

| 57 | ||||

| 59 | ||||

| 59 | ||||

| 60 | ||||

| 61 | ||||

| 62 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

64 | |||

| 64 | ||||

| 65 | ||||

| 66 | ||||

| 72 | ||||

| 78 | ||||

| 81 | ||||

| 82 | ||||

| 85 | ||||

| 86 | ||||

| 89 | ||||

| 89 | ||||

| 90 | ||||

| 105 | ||||

| 105 | ||||

| 107 | ||||

| Select Producing Fields and Development Projects in the Deepwater GOM |

108 | |||

| 109 |

i

Table of Contents

Index to Financial Statements

| 111 | ||||

| 111 | ||||

| Deepwater GOM Producing Assets, Sanctioned Discoveries and Associated Drilling Inventory |

112 | |||

| Deepwater GOM Discoveries in Pre-Sanction Stage with Potential Development Opportunities |

118 | |||

| 120 | ||||

| 124 | ||||

| 126 | ||||

| 127 | ||||

| 128 | ||||

| 129 | ||||

| 130 | ||||

| 131 | ||||

| 133 | ||||

| 139 | ||||

| 144 | ||||

| 146 | ||||

| 153 | ||||

| 154 | ||||

| 154 | ||||

| 154 | ||||

| 155 | ||||

| 155 | ||||

| 156 | ||||

| 156 | ||||

| 156 | ||||

| 157 | ||||

| 157 | ||||

| 157 | ||||

| 158 | ||||

| 171 | ||||

| 172 | ||||

| 177 | ||||

| 180 | ||||

| 180 | ||||

| 181 | ||||

| 181 | ||||

| 182 | ||||

| 182 | ||||

| 182 | ||||

| 182 | ||||

| 183 | ||||

| Policies and Procedures for Review of Related Party Transactions |

184 | |||

| 185 | ||||

| 187 | ||||

| 188 | ||||

| 188 | ||||

| 188 | ||||

| 189 | ||||

| Certain Provisions of Our Amended and Restated Certificate of Incorporation and By-laws |

189 |

ii

Table of Contents

Index to Financial Statements

| 193 | ||||

| 193 | ||||

| 193 | ||||

| 193 | ||||

| 194 | ||||

| 194 | ||||

| MATERIAL U.S. FEDERAL INCOME TAX CONSEQUENCES TO NON-U.S. HOLDERS OF OUR CLASS A COMMON STOCK |

195 | |||

| 196 | ||||

| 196 | ||||

| 197 | ||||

| 197 | ||||

| Additional Withholding Tax on Payments Made to Foreign Accounts |

198 | |||

| 199 | ||||

| 199 | ||||

| 199 | ||||

| 200 | ||||

| 201 | ||||

| 201 | ||||

| 201 | ||||

| 201 | ||||

| 202 | ||||

| 202 | ||||

| 202 | ||||

| 203 | ||||

| 203 | ||||

| 203 | ||||

| 207 | ||||

| 207 | ||||

| 207 | ||||

| 208 |

You should rely only on the information contained in this prospectus and any free writing prospectus prepared by or on behalf of us or to which we have referred you. Neither we nor the underwriters have authorized anyone to provide you with information different from that contained in this prospectus and any free writing prospectus. We are offering to sell shares of Class A common stock and seeking offers to buy shares of Class A common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus regardless of the time of delivery of this prospectus or any sale of the Class A common stock.

Industry and Market Data

The market data and certain other statistical information used throughout this prospectus are based on independent industry publications, government publications or other independent published sources. Some data is also based on our good faith estimates. Such data involve a number of assumptions and limitations, and you are cautioned not to give undue weight to such information. The industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the section entitled “Risk Factors.” These and other factors could cause results to differ materially from those expressed in these publications.

iii

Table of Contents

Index to Financial Statements

This summary provides a brief overview of information contained elsewhere in this prospectus and does not contain all of the information that you should consider before investing in our Class A common stock. You should read the entire prospectus carefully before making an investment decision, including the information presented under the headings “Risk Factors,” “Cautionary Note Regarding Forward-Looking Statements” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Unless otherwise indicated, the information presented in this prospectus assumes that the underwriters’ option to purchase additional shares of Class A common stock from us is not exercised. Several terms used in this prospectus are defined in the “Glossary.” References to our estimated proved, probable and possible reserves, standardized measure and PV-10 are derived from our reserve reports prepared by our external, independent petroleum engineering firms Netherland, Sewell & Associates, Inc., which we refer to as NSAI, and Ryder Scott Company, L.P., which we refer to as Ryder Scott.

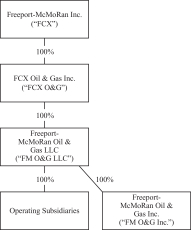

In this prospectus, unless the context otherwise requires, the terms “we,” “us,” “our,” and “FCX O&G” refer to FCX Oil & Gas Inc. and its subsidiaries before the completion of our corporate reorganization prior to the closing of this offering, and Freeport-McMoRan Oil & Gas Inc., which we refer to as “FM O&G Inc.” and its subsidiaries as of the completion of our corporate reorganization and thereafter. The term “FCX” refers to Freeport-McMoRan Inc., our direct parent after completion of our corporate reorganization. See “Corporate Reorganization.”

We are an upstream oil and gas energy company primarily engaged in acquiring, exploring for, developing and producing oil and gas properties. We are focused on growing our strategic position in the Deepwater U.S. Gulf of Mexico, which we refer to as the Deepwater GOM. Our Deepwater GOM position has significant current oil production, strong cash margins and existing infrastructure with excess production and handling capacity. We expect this existing infrastructure and our extensive inventory of drilling opportunities will allow us to grow our Deepwater GOM production with comparatively low capital expenditures. In addition, our onshore and offshore properties in California are characterized as low-decline properties with stable production and long-lived reserves. We also have a large, onshore gas position in the Haynesville shale and the Inboard Lower Tertiary/Cretaceous gas trend located onshore in South Louisiana. Our Madden field in Central Wyoming also provides us with additional predictable cash flows, low-decline production and long-lived gas reserves. Our gas-weighted assets position us to benefit from a recovery in gas prices. We are currently focused on growing our proved reserves and production by developing our oil-weighted properties in the Deepwater GOM with a prudent capital profile for the current commodity price environment.

We believe our portfolio of oil and gas properties delivers financially attractive investment opportunities with growth potential in terms of production, cash margin and reserves. For the six months ended June 30, 2015, 88 percent of our oil and gas revenues, excluding the impact of derivative contracts, was from oil and NGLs. Our oil and gas business has significant proved, probable and possible reserves and a broad range of additional development opportunities, including discoveries and identified prospects in the Deepwater GOM. A significant portion of our planned capital expenditures are expected to be focused on converting our probable and possible reserves and prospective resources to the proved reserves category as we are focused on developing our relatively low-risk near-term Deepwater GOM inventory. We strive to manage our business to reinvest cash flows in projects with attractive risk-adjusted rates of return.

1

Table of Contents

Index to Financial Statements

Based on data derived from reserve reports prepared by our external, independent petroleum engineering firms, our estimated oil and gas reserves at December 31, 2014 were as follows:

| Oil (MMBbls) |

NGLs (MMBbls) |

Gas (Bcf)(1) |

Total (MMBoe)(1) |

PV-10(2) | ||||||||||||||||

| Proved Reserves(3) |

278 | 10 | 610 | 390 | $ | 8.1 billion | ||||||||||||||

| Probable Reserves(3) |

192 | 7 | 278 | 245 | $ | 4.8 billion | ||||||||||||||

| Possible Reserves(3) |

230 | 9 | 592 | 338 | $ | 6.7 billion | ||||||||||||||

| (1) | Excludes 19 Bcf of proved reserves, 25 Bcf of probable reserves and 53 Bcf of possible reserves as of December 31, 2014, related to the Highlander gas discovery well located in the Inboard Lower Tertiary/Cretaceous trend, for which external reserve estimates were completed in March 2015. |

| (2) | PV-10 is a non-GAAP financial measure. Standardized Measure is the most directly comparable GAAP measure, which was $6.5 billion for proved reserves at December 31, 2014. GAAP does not provide a measure of estimated future net cash flows for reserves other than proved reserves. Therefore, a reconciliation between PV-10 and Standardized Measure for probable and possible reserves is not subsequently provided. Because PV-10 estimates of probable and possible reserves are more uncertain than the PV-10 and Standardized Measure of proved reserves, but have not been adjusted for risk due to that uncertainty, they may not be comparable with each other. For additional information about PV-10 and how it differs from the Standardized Measure, see “Summary Consolidated Financial, Reserve and Operating Data—Non-GAAP Financial Measures.” |

| (3) | At December 31, 2014, proved undeveloped reserves were composed of 104 MMBbls of oil and NGLs and 241 Bcf of gas for a total of 144 MMBoe, which comprised 37 percent of our total proved reserves. Volumes and values were determined in accordance with the U.S. Securities and Exchange Commission, which we refer to as the SEC, rules using reference prices for oil and gas of $94.99 per Bbl and $4.35 per MMBtu, respectively. Our probable and possible reserves include 70 MMBoe and 182 MMBoe, respectively, related to our Deepwater GOM producing assets and discoveries attributable to incremental increases in recovery factor or volumetric drainage areas. Our probable and possible reserves are based upon observed well production performance, reservoir simulation modeling and volumetric calculations. See “Risk Factors—Risks Related to Our Business—Our estimated reserves are based on many assumptions that may turn out to be inaccurate. Significant inaccuracies in these underlying assumptions will materially affect the quantities and present value of our proved reserves.” |

Our acreage position was 1,022,537 gross (436,189 net) developed acres and 4,017,361 gross (2,458,424 net) undeveloped acres at December 31, 2014. At December 31, 2014, we owned working interests in 3,069 gross (2,991 net) active producing oil wells and 1,710 gross (211 net) active producing gas wells. For the six months ended June 30, 2015, we generated sales volumes of 142 MBoe/d with realized revenues, including cash gains on derivatives, of $46.95 per Boe and cash production costs of $19.62 per Boe. Realized revenue and cash production costs are non-GAAP financial measures. Revenue and production costs, respectively, are the most directly comparable GAAP measure, which were $41.35 per Boe and $22.01 per Boe, respectively, for the six months ended June 30, 2015. See “Summary Consolidated Financial, Reserve and Operating Data—Non-GAAP Financial Measures.”

Deepwater GOM Producing Assets, Sanctioned Discoveries and Associated Drilling Inventory

We have a large strategic position in the Deepwater GOM with significant current oil production, strong cash margins and existing infrastructure with excess production and handling capacity. These assets, combined with our large leasehold interests, provide financially attractive near-term drilling opportunities for growth in oil production and cash margins. Our properties and activities are principally located in four focus areas, which we refer to as Atwater Valley, Green Canyon, Mississippi Canyon and Keathley Canyon. Furthermore, our capital allocation strategy is principally focused on drilling wells that can be tied back expeditiously to our existing facilities. We have adopted a prudent capital profile for the current commodity price environment in which we have deferred certain capital associated with completion and infrastructure spending and are electing to defer production growth for potentially more favorable market conditions. We believe our existing infrastructure provides us with a competitive advantage by allowing for flexibility to control the pace of our development and production activities for relatively low amounts of investment capital as compared to competitors who lack access to such facilities. In addition, we expect to apply existing technologies in subsea pumping and lifting technology to our properties. This technology can provide the potential for increasing hydrocarbon recovery by boosting pressure required for delivery at the existing host platform.

2

Table of Contents

Index to Financial Statements

The following is a summary of our Deepwater GOM platforms and currently producing fields at June 30, 2015:

| Avg. Daily Net Sales Volumes for the Six Months Ended June 30, 2015 (MBoe/d) |

||||||||||||||||||||||||||||||||

| Platform |

Working Interest |

Operator | Type of Platform | Production Commenced |

Water Depth (Feet) |

Gross |

Gross Oil Capacity Utilization %(1) |

|||||||||||||||||||||||||

| Oil (MBbls) |

Gas (MMcf) |

|||||||||||||||||||||||||||||||

| Holstein |

100 | % | FCX O&G | Truss Spar | 2004 | 4,300 | 13 | 113 | 142 | 11 | % | |||||||||||||||||||||

| Marlin Hub(2) |

100 | % | FCX O&G | Tension Leg | 2000 | 3,200 | 24 | 60 | 235 | 37 | % | |||||||||||||||||||||

| Horn Mountain |

100 | % | FCX O&G | Truss Spar | 2002 | 5,400 | 9 | 75 | 72 | 11 | % | |||||||||||||||||||||

| Lucius |

25.1 | % | Anadarko | Truss Spar | 2015 | 7,200 | 13 | 80 | 450 | 59 | % | |||||||||||||||||||||

| Ram Powell |

31.0 | % | Shell | Tension Leg | 1997 | 3,200 | 3 | 70 | 310 | 7 | % | |||||||||||||||||||||

| Hoover |

33.3 | % | ExxonMobil | Deep Draft Caisson Vessel |

2000 | 4,800 | 2 | 100 | 325 | 6 | % | |||||||||||||||||||||

|

|

|

|||||||||||||||||||||||||||||||

| Total | 64 | |||||||||||||||||||||||||||||||

| (1) | Represents average daily gross oil production for the six months ended June 30, 2015 as a percentage of total production capacity during such period. |

| (2) | The Marlin Hub is the production facility for three fields: Marlin, Dorado and King. |

Since the acquisition of our Holstein, Marlin Hub and Horn Mountain properties from subsidiaries of BP p.l.c., which we refer to as BP, and Royal Dutch Shell p.l.c., which we refer to as Shell, in November 2012, we have been active in optimizing production from existing wells through well workover and stimulation activities in previously developed formations. The significant production history from these assets, together with extensive reservoir modeling and multiple series of seismic evaluation and interpretation, gives us high confidence in achieving positive results in our planned near-term development drilling activities.

Our planned development activities associated with our Deepwater GOM producing assets targeting known productive pay sand in these fields are listed below.

| Focus Area | Working Interest |

Operator | Number of Currently Producing Wells |

Identified Undeveloped Locations(1) |

||||||||||||||||

| Producing Field |

Number | Projected First Spud |

||||||||||||||||||

| Holstein |

Green Canyon | 100 | % | FCX O&G | 11 | 9 | 2016 | |||||||||||||

| Marlin Hub |

Mississippi Canyon | |||||||||||||||||||

| Dorado |

100 | % | FCX O&G | 4 | 2 | 2016 | ||||||||||||||

| King |

100 | % | FCX O&G | 4 | 5 | (2) | 2015 | |||||||||||||

| Horn Mountain |

Mississippi Canyon | 100 | % | FCX O&G | 6 | 7 | (3) | 2015 | ||||||||||||

| Lucius |

Keathley Canyon | 25.1 | % | Anadarko | 6 | 10 | 2016 | |||||||||||||

| Ram Powell |

Mississippi Canyon | 31.0 | % | Shell | 8 | 1 | 2015 | |||||||||||||

|

|

|

|

|

|||||||||||||||||

| Total | 39 | 34 | ||||||||||||||||||

| (1) | Of our 34 identified undeveloped locations associated with our Deepwater GOM producing assets, 19 are included in our reserve reports, 15 of which were classified as proved undeveloped locations, prepared by our external, independent petroleum engineering firms as of December 31, 2014. The drilling locations on which we ultimately drill will depend on the availability of capital, regulatory approvals, commodity prices, costs, actual drilling results and other factors. Any drilling activities on these identified undeveloped locations may not be successful and may not result in additions to our existing proved reserves. Successful drilling activities could require substantial additional capital expenditures. For more information, see “Risk Factors—Risks Related to Our Business—Our business plan requires |

3

Table of Contents

Index to Financial Statements

| substantial additional capital, which we may be unable to raise on acceptable terms in the future, which may in turn limit our ability to execute our business plan and could lead to a loss of properties and have a material adverse effect on our production, reserves and results of operations.” |

| (2) | Includes a development well drilled in January 2015. |

| (3) | Includes a development well drilled in June 2015 and two development wells drilled in July 2015. |

Holstein. In 2014, we commenced a program to redevelop Holstein and successfully drilled two sidetrack wells utilizing our owned platform drilling rig. Our future plans for Holstein include additional sidetracks and drilling activities. In addition, we have made a significant discovery in deeper subsalt Miocene reservoirs at Holstein, which we refer to as Holstein Deep, and we are developing this discovery by means of a subsea tieback with the potential to apply existing subsea enhancement technologies that could increase total recovery efficiencies for the project.

Marlin Hub. Activities in the Marlin Hub area have focused on infield drilling at the Dorado and King fields, which are produced through subsea tie back to the Marlin platform. In December 2014, we successfully drilled a development well at Dorado that encountered 245 net feet of Miocene oil pay. This well was placed on production in March 2015 after a successful production test with gross volumes in excess of seven MBbls of oil per day and eight MMcf of gas per day and continues to produce at strong rates. At King, we drilled a development well in January 2015 and logged 63 net feet of Miocene oil pay. We subsequently sidetracked and completed this well for an optimum oil take point, and we expect to place this well on production in 2015. Our future plans at Dorado and King include additional drilling in the same Miocene horizons in the second half of 2015 and in 2016. In addition, we have identified prospective drilling at King in deeper horizons, which we refer to as King West Deep. Future wells in the Marlin Hub area can be brought on-line expeditiously through our existing infrastructure and future subsea tiebacks have the potential to utilize existing subsea enhancement technologies that could increase total recovery efficiencies. In second-quarter 2015, we completed maintenance activities, including installation of new export flow line flex joints, which will extend the life of the Marlin platform.

Horn Mountain. Our producing wells in the Horn Mountain field target formations similar to those in the Marlin Hub area and are located in the same geologic setting as our production from the Dorado and King fields. The currently producing wells use dry trees to connect to the Horn Mountain spar. To enhance our recovery of remaining oil in place, our future development plan anticipates utilizing subsea tieback wells targeting multiple stacked sands. During the three months ended June 30, 2015, the Quebec/Victory well, the first location of this program, was drilled to 14,780 feet and we have logged 355 net feet of oil and gas pay. Upon completion, we plan to put this well on production in 2016. In June 2015, drilling operations commenced at the Kilo/Oscar and Horn Mountain Updip wells. At Kilo/Oscar, the well was drilled to a total depth of 14,250 feet and successfully logged 166 net feet of oil pay. At Horn Mountain Updip, the well was drilled to a total depth of 14,780 feet and successfully logged 112 net feet of oil and gas pay. This infill development drilling program will target hydrocarbon accumulations in the sands found to be productive at Horn Mountain and, in addition to these three wells, consists of the Horn Mountain Northwest, Eland/Zebra, Sable and Lion locations. In addition, we have identified prospective drilling in deeper horizons, which we refer to as Horn Mountain Deep which we plan to spud in third-quarter 2015. All planned and prospective drilling at Horn Mountain has the potential to utilize existing subsea enhancement technologies that could increase total recovery efficiencies.

Lucius. In January 2015, we began production from an initial six-well development in the Lucius field operated by Anadarko Petroleum Corporation, which we refer to as Anadarko. During the three months ended June 30, 2015, the Lucius Oil Facility reached capacity of 80 MBbls of oil per day. Lucius is a world-class subsalt Pliocene and Miocene discovery with high-quality reservoir attributes. We participated in the drilling of the discovery well in 2009 and increased our working interest through an acquisition in 2014. In 2011, we and the other working interest owners sanctioned the spar construction, with initial development focused primarily on the Pliocene-aged sands with average net pay thickness of 469 feet. In addition, we have identified further

4

Table of Contents

Index to Financial Statements

drilling opportunities in the Pliocene and Miocene horizons at Lucius. Our Lucius development is an example of how historically we have partnered with third party capital providers to finance development costs related to our Deepwater GOM properties. In 2011, subsequent to the Lucius discovery well, we raised $450 million through the issuance of convertible preferred stock in one of our subsidiaries that holds a portion of our interest at Lucius.

Ram Powell. In March 2015, Shell successfully drilled a development well at Ram Powell logging 106 feet of pay in above salt Miocene reservoirs. The well has been completed and came online in July 2015.

In addition to our activities on our producing fields we own interests in and have been actively developing two discoveries that have been sanctioned for development. Both of these discoveries are located in our Green Canyon focus area and target subsalt Miocene reservoirs.

The following table provides a summary of our active development projects:

| Discovery |

Working Interest |

Operator | Identified Undeveloped Locations(1) |

Projected First Oil |

Focus Area | |||||||||||

| Holstein Deep |

100 | % | FCX O&G | 10 | (2) | 2016 | Green Canyon | |||||||||

| Heidelberg |

12.5 | % | Anadarko | 9 | (3) | 2016 | Green Canyon | |||||||||

|

|

|

|||||||||||||||

| Total | 19 | |||||||||||||||

| (1) | Of our 19 identified undeveloped locations associated with our Deepwater GOM discoveries sanctioned for development, 12 are included in our reserve reports, 6 of which are classified as proved undeveloped locations, prepared by our external, independent petroleum engineering firms as of December 31, 2014. The drilling locations on which we ultimately drill will depend on the availability of capital, regulatory approvals, commodity prices, costs, actual drilling results and other factors. Any drilling activities on these identified undeveloped locations may not be successful and may not result in adding additional reserves to our existing proved reserves. Successful drilling activities could require substantial additional capital expenditures. For more information, see “Risk Factors—Risks Related to Our Business—Our business plan requires substantial additional capital, which we may be unable to raise on acceptable terms in the future, which may in turn limit our ability to execute our business plan and could lead to a loss of properties and have a material adverse effect on our production, reserves and results of operations.” |

| (2) | Includes three development wells drilled in December 2014, February 2015 and July 2015, respectively. |

| (3) | Includes three development wells drilled by Anadarko in 2014 and through May 31, 2015. |

Holstein Deep. This large, high-quality subsalt Miocene oil discovery has the potential to be a phased development project tied back to the Holstein spar. In December 2014, we achieved successful results from a Holstein Deep delineation well that logged 444 feet of net oil pay. In February 2015, we completed drilling the second delineation well, with positive results. This second well encountered 482 feet of net oil pay. The third delineation well was drilled to 29,440 feet and encountered approximately 200 feet of net oil pay. Drilling results from this initial three-well development program successfully established sand continuity across the primary reservoir. Production from this initial three-well development is expected to begin in 2016 with estimated risk-adjusted gross initial individual well flowrates of 8 MBbls of oil per day. We believe that when fully developed this project could have the potential to produce up to 75 MBbls of oil per day.

Heidelberg. The initial Heidelberg discovery well was drilled in 2009 and encountered more than 200 net feet of oil pay. Log and pressure data from the discovery and delineation wells indicate excellent quality, continuous and pressure-connected reservoirs with subsalt Miocene oil. The Heidelberg working interest owners sanctioned a six well development plan, with a new truss spar facility having a design capacity of 80 MBbls of oil per day. Completion activities on the three initial wells are in progress. Fabrication of the main topsides module is complete, the hull is on location, the mooring lines are completed, and the project remains on track for first production in 2016 with anticipated risk-adjusted gross initial individual well flowrates of 10.4 MBbls of oil per day.

5

Table of Contents

Index to Financial Statements

Deepwater GOM Discoveries in Pre-Sanction Stage with Potential Development Opportunities

In addition to our discoveries that have been sanctioned for development, we own working interests in several additional significant oil discoveries that could provide additional production reserves and drilling opportunities. These discoveries consist of subsalt Miocene and Lower Tertiary formations located in our Atwater Valley and Keathley Canyon focus areas. These discoveries hold significant potential and the timing of their development will be dependent on finalization of development plans and sanctioning by us and our partners.

The following table provides a summary of our discoveries that are in the pre-sanctioning phase:

| Discovery |

Working Interest |

Operator | Identified Undeveloped Locations(1) |

Projected First Oil |

Focus Area | |||||||||||

| Vito |

18.67 | % | Shell | 15 | 2020 | Atwater Valley | ||||||||||

| Power Nap |

50 | % | Shell | 5 | 2020 | Atwater Valley | ||||||||||

| Phobos |

50 | % | Anadarko | 9 | 2020 | Keathley Canyon | ||||||||||

|

|

|

|||||||||||||||

| Total | 29 | |||||||||||||||

| (1) | Of our 29 identified undeveloped locations associated with our Deepwater GOM discoveries in the pre-sanctioning stage, none are included in our reserve reports prepared by our external, independent petroleum engineering firms. The drilling locations on which we ultimately drill will depend on the availability of capital, regulatory approvals, commodity prices, costs, actual drilling results and other factors. Neither the Vito, Power Nap, nor Phobos discoveries have been sanctioned for further development by us or our partners. Any drilling activities on these identified undeveloped locations may not be successful and may not result in adding additional reserves to our existing proved reserves. Successful drilling activities could require substantial additional capital expenditures. For more information, see “Risk Factors—Risks Related to Our Business—Our business plan requires substantial additional capital, which we may be unable to raise on acceptable terms in the future, which may in turn limit our ability to execute our business plan and could lead to a loss of properties and have a material adverse effect on our production, reserves and results of operations.” |

Vito and Power Nap. Vito is a large, deep subsalt Miocene oil discovery made in 2009. Exploration and delineation drilling in recent years confirmed a significant resource in high-quality, subsalt Miocene sands with an average net pay of 457 feet. Development options are under evaluation by the working interest owners, and we expect Shell, as the operator, to propose a sanctioning development plan for 2016. Power Nap is located in close proximity to Vito where we encountered positive drilling results in December 2014 in the same sands as Vito. Delineation drilling activities consisting of two sidetracks have confirmed the findings in the initial well. The working interest owners are currently evaluating development options for Power Nap.

Phobos. In 2013, the initial Phobos discovery well, located in the Sigsbee Escarpment area, was drilled and encountered more than 250 net feet of pay in Lower Tertiary reservoirs. We expect a potential Phobos development to benefit from its close proximity to the Lucius spar. The working interest owners are evaluating future plans for this discovery.

Deepwater GOM Prospect Inventory and Drilling Plans

In addition to the proved, probable and possible reserves and prospective resources associated with our Deepwater GOM producing assets and Deepwater GOM discoveries, we have a large inventory of identified prospects with production and resource potential. Our inventory consists of both above salt and subsalt formations and is focused on resources that, upon success, we plan to tieback to our Holstein, Horn Mountain, Marlin and Lucius platforms or can be developed in conjunction with our Vito and Power Nap discoveries, should those discoveries be sanctioned for development. Our operational control and remaining primary term lease position for these prospects allows us the ability to modify the timing of when we expect to drill the initial well in these prospects. We target resources primarily in Pliocene and Miocene reservoirs but also have large prospects in the Lower Tertiary.

6

Table of Contents

Index to Financial Statements

Our Deepwater GOM prospect inventory consists of interests in 16 prospects, which were identified by seismic imaging and which include 154 undeveloped well locations. The following table provides a summary of prospects and projected spud dates. The commercial success of these prospects would likely lead to a large number of additional drilling opportunities in the future.

| Prospect |

Operator | Working Interest(1) |

Identified Undeveloped Locations(2) |

Projected Spud Year(3) |

Focus Area | |||||||||

| Deep Sleep |

Shell | 50 | % | 10 | 2015 | Atwater Valley | ||||||||

| Horn Mountain Deep |

FCX O&G | 100 | % | 6 | 2015 | Mississippi Canyon | ||||||||

| Sun |

FCX O&G | 100 | % | 14 | 2016 | Atwater Valley | ||||||||

| Spitfire |

FCX O&G | 100 | % | 20 | 2016 | Atwater Valley | ||||||||

| Holstein Wilcox |

FCX O&G | 100 | % | 16 | 2017 | Green Canyon | ||||||||

| Orange |

FCX O&G | 100 | % | 8 | 2017 | Mississippi Canyon | ||||||||

| Sugar |

FCX O&G | 100 | % | 8 | 2017 | Mississippi Canyon | ||||||||

| Rose |

FCX O&G | 100 | % | 6 | 2017 | Mississippi Canyon | ||||||||

| Fiesta |

FCX O&G | 100 | % | 7 | 2017 | Mississippi Canyon | ||||||||

| Gator |

FCX O&G | 100 | % | 4 | 2017 | Mississippi Canyon | ||||||||

| Lionhead |

Anadarko | 50 | % | 11 | 2017 | Keathley Canyon | ||||||||

| King West Deep |

FCX O&G | 100 | % | 8 | 2018+ | Mississippi Canyon | ||||||||

| Platinum |

FCX O&G | 100 | % | 5 | 2018+ | Mississippi Canyon | ||||||||

| Peach |

FCX O&G | 100 | % | 8 | 2018+ | Mississippi Canyon | ||||||||

| Silverfox |

FCX O&G | 100 | % | 16 | 2018+ | Green Canyon | ||||||||

| Tungsten |

FCX O&G | 100 | % | 7 | 2018+ | Green Canyon | ||||||||

|

|

|

|||||||||||||

| Total | 154 | |||||||||||||

| (1) | Our working interests are subject to change as a result of unitization or co-development of the applicable block or area with adjacent acreage. Our working interest may increase or decrease based on the extent and productivity of the discovery. |

| (2) | We work with NSAI in assessing our identified undeveloped locations for our prospects. Of our 154 identified undeveloped locations associated with our Deepwater GOM prospect inventory, none are included in our reserve reports as of December 31, 2014. The drilling locations on which we actually drill will depend on the availability of capital, regulatory approvals, commodity prices, costs, actual drilling results, participation of partners and other factors. Drilling activities on these identified undeveloped locations may not be successful and may not result in our adding additional proved reserves to our existing proved reserves. Successful drilling activities could require substantial additional capital expenditures. For more information, see “Risk Factors—Risks Related to Our Business—Our business plan requires substantial additional capital, which we may be unable to raise on acceptable terms in the future, which may in turn limit our ability to execute our business plan and could lead to a loss of properties and have a material adverse effect on our production, reserves and results of operations.” The number of identified undeveloped locations are based upon our P10 estimates. |

| (3) | See “Risk Factors—Risks Related to Our Business—Drilling for and producing oil and gas are high-risk activities with many uncertainties that may result in a total loss of investment or otherwise adversely affect our business, financial condition or results of operations.” |

Utilizing seismic interpretation, we intend to identify areas for potential hydrocarbon accumulations and add to this undrilled inventory through farm outs, acquisitions and participation in future BOEM lease sales. Also, as part of our exploration efforts, we regularly collaborate with experienced and respected large independent, major integrated and international state owned oil and gas energy companies on geologic and engineering studies covering currently owned leasehold and uncaptured domestic and international acreage. We believe these efforts will enable us to enhance and optimize our undrilled portfolio.

Our prospect generation approach is predicated upon a thorough, basin-wide understanding of the geologic trends within our focus areas through a detailed review of industry drilling results, followed by a rigorous analysis and reprocessing of our basin wide, focused 3-D seismic data. Consistent with our approach and to drive the internal generation and acquisition of new prospects, we have made significant investments in the latest

7

Table of Contents

Index to Financial Statements

seismic data and seismic imaging technology. Since 2006, we have spent in excess of $300 million on the acquisition, reprocessing and analysis of extensive geophysical data in the Deepwater GOM. We currently own or have licensed 3-D seismic data covering over 5,000 blocks in the Deepwater GOM. Our seismic data base includes the most recent advanced technologies, including wide-azimuth 3-D data. Wide-azimuth 3-D seismic data generates substantially more accurate images than traditional 3-D seismic data, helping to reduce exploration risk. Wide-azimuth 3-D seismic data is critical to understanding of a particular reservoir’s characteristics, including trapping mechanics and fluid migration patterns. Additionally, we utilize 4-D seismic data, which is a series of 3-D seismic surveys repeated over a period of time. Our technical team also regularly makes use of advanced seismic imaging technology including pre-stack depth migration, which is a technique that uses advanced processing algorithms to transform seismic data from a scale of time to a scale of depth.

Our Holstein Deep, Phobos, Highlander, Vito and Power Nap discoveries are evidence of a successful prospect generation approach coupled with advanced seismic data that resulted in discoveries of significant hydrocarbon reservoirs. We believe that these discoveries will add to our proved reserve base over time. We expect to add Holstein Deep and Highlander reserves starting this year. Going forward we expect that new prospects generated through our exploration efforts will typically target formations with gross hydrocarbon potential in excess of 100 MMBoe. We expect our exploration process and our collaboration with other companies that have comparable technology and technical expertise to continue to provide significant high-quality prospects. Capri and Eagle are two of our long term exploration prospects and are examples of interests acquired through BOEM lease sales, that are currently being matured. Future drilling decisions for these or other prospects will be driven by the results of our exploration process and capital budget considerations. In the current commodity price environment we intend to significantly reduce spending on our exploration inventory in the near term.

In addition to employing our exploration process and technical capabilities in the U.S., we have in the past explored for hydrocarbons internationally and may do so in the future. Currently, we have licenses to 1,662 square miles of 3-D seismic data covering deepwater areas, offshore Morocco. Further, we have been pre-qualified as a bidder in the upcoming Mexican lease sale and we are in the early stages of evaluating the hydrocarbon potential of Mexico.

Our California assets provide an established oil production base with low-decline production profiles, long-lived reserves and significant exposure to an improving oil market. Our onshore California properties are primarily located in the Los Angeles Basin and San Joaquin Valley. We hold a 100 percent working interest in the substantial majority of our onshore position. The Los Angeles Basin properties are characterized by light crude oil, have well depths ranging from 2,000 feet to over 10,000 feet and include both primary production and secondary recovery using waterflood methods, and produce with high water cuts. The San Joaquin Basin properties are characterized by heavier oil and shallow wells (generally less than 2,000 feet) that require enhanced oil recovery techniques, including steam injection. Our offshore California properties are primarily located in the Point Arguello and Point Pedernales fields, where we hold a 69.3 percent and 100 percent working interest, respectively. In 2015, we plan to focus our operating and capital expenditures in California on high-margin re-completion and well maintenance activities. For the six months ended June 30, 2015, our California assets produced 39.0 MBoe/d. In 2016 we plan to focus our drilling activities in the Cymric field, our largest property in California.

8

Table of Contents

Index to Financial Statements

We own a substantial portfolio of gas-weighted assets, including a large position in the Haynesville shale in Louisiana, a position in the Inboard Lower Tertiary/Cretaceous gas trend located onshore in South Louisiana, producing properties on the shelf of the Gulf of Mexico, which we refer to as the GOM Shelf, and a position in the Madden field located in Central Wyoming. As of December 31, 2014, in the Haynesville shale, we have a non-operated interest in over 1,400 producing wells with an average working interest of 8.5 percent and leases covering 75,000 net acres. We estimate the potential to drill an additional 12,000 gross (1,000 net) wells on our Haynesville shale acreage. In the Lower Tertiary/Cretaceous we have recently experienced success from a production test indicating a flow rate of 75 MMcf/d. The Highlander well, which has been restricted because of limited processing facilities, averaged a gross rate of 22 MMcf/d (approximately 11 MMcf/d net) during the quarter ended June 30, 2015. We are developing additional processing facilities to accommodate the higher flow rates with installation expected by year-end 2015. In July 2015, the Highlander well was shut in for remedial workover operations to address a mechanical issue encountered in the wellbore. A second well location has been identified and future plans are being considered. Our gas-weighted assets in Louisiana are geographically positioned to benefit from the expected growth in gas demand from existing and planned LNG terminals and petrochemical plants along the Gulf Coast. We also own interests in gas-weighted properties in the GOM Shelf in Louisiana. Further, our approximate non-operated 14 percent working interest in the Madden Deep Unit and Lost Cabin Gas Plant in Wyoming provides us with low-decline stable cash flows with long reserve life. Our large resource and acreage position provides us with the opportunity for significant reserve and production growth on a rapidly scalable basis upon a return of a more favorable gas price environment. For the six months ended June 30, 2015, our gas-weighted assets produced 233.8 MMcfe/d.

We estimate our fiscal 2015 capital budget will be $2.8 billion (of which $1.8 billion was spent for the six months ended June 30, 2015). This capital budget reflects our focus on growth of production and reserves, as well as executing on our inventory of discoveries and prospects in the Deepwater GOM. Our 2015 capital budget includes:

| 2015(1) | ||||

| (in billions) | ||||

| Development (Drilling, Completion, Infrastructure and Maintenance) |

$ | 2.5 | ||

| Deepwater GOM |

2.2 | |||

| California |

0.1 | |||

| Gas-weighted assets |

0.2 | |||

| Exploration |

0.1 | |||

| Other items |

0.2 | |||

| (1) | Budget figures were prepared assuming prices of $56.00 per Bbl of oil and $2.50 per MMcf of gas for the second half of 2015. The ultimate amount of capital we will expend may fluctuate materially based on market conditions and the success of our drilling results. |

9

Table of Contents

Index to Financial Statements

We estimate our fiscal 2016 capital budget will be $2.0 billion. This capital budget reflects our conservative strategy of moderate production growth in the current commodity price environment. The majority of capital budget in 2016 will be allocated to operated properties focused on development in the Deepwater GOM, giving us increased flexibility to respond to more favorable commodity pricing. We plan to engage third party investors and industry partners to further delineate our existing discoveries and test our prospects in the Atwater Valley focus area. We have elected to defer capital spending and associated production growth for more favorable market conditions. We also plan to defer exploratory spending to future periods. Our 2016 capital budget includes:

| 2016(1) | ||||

| (in billions) | ||||

| Development (Drilling, Completion, Infrastructure and Maintenance) |

$ | 1.8 | ||

| Deepwater GOM |

1.6 | |||

| California |

0.1 | |||

| Gas-weighted assets |

0.1 | |||

| Other items |

0.2 | |||

| (1) | Budget figures were prepared assuming prices of $61.00 per Bbl of oil and $3.00 per MMcf of gas. The ultimate amount of capital we will expend may fluctuate materially based on market conditions and the success of our drilling results. |

We have made, and expect to make in 2015, 2016 and beyond, substantial capital expenditures in our business and operations for the exploration, development, production and acquisition of reserves, as well as the development and maintenance of necessary infrastructure and other items. We may not have sufficient resources to undertake these activities. For more information, see “Risk Factors—Risks Related to Our Business—Our business plan requires substantial additional capital, which we may be unable to raise on acceptable terms in the future, which may in turn limit our ability to execute our business plan and could lead to a loss of properties and have a material adverse effect on our production, reserves and results of operations.”

We have a number of competitive strengths that we believe will help us to successfully execute our business strategies, including:

| • | We own a world-class asset portfolio and a large inventory of development projects and prospects in the Deepwater GOM. We have a large strategic position in the Deepwater GOM with significant current oil production, strong cash margins and existing infrastructure with excess production and handling capacity. Our Deepwater GOM portfolio includes 310 identified undeveloped locations in the Pliocene, Miocene and Lower Tertiary trends, which we believe offer impactful development and exploration potential. We have focused our capital on high cash margin oil-weighted properties where we receive favorable prices in relation to WTI. We have an extensive inventory of high-quality seismic imaging encompassing our prospects and covering over 5,000 blocks in the Deepwater GOM. |

In addition to current production, we believe that our Deepwater GOM properties have attractive production growth profiles in well-defined areas driven by our key discoveries and identified prospects. Our existing infrastructure enables us to develop resources using subsea tiebacks. This infrastructure position allows us to reduce the time from investment to first production and our capital costs have the potential to be lower when compared to other operators with similar prospects that lack infrastructure capacity. This is evidenced by our recent Dorado well that was brought on-line within five months of spud and our Holstein Deep and Horn Mountain developments, which we expect to begin production in

10

Table of Contents

Index to Financial Statements

2016. Our non-operated interests in the Lucius and Heidelberg are expected to provide additional production growth and our discoveries at Vito and Power Nap have a potential to add value upon their potential sanctioning. Our plan for developing our Deepwater GOM portfolio provides opportunities for near-term cash generation, reserve replacement and long-term production growth.

| • | Our California assets provide significant cash flow from stable production. We believe our long-lived reserve base in California should also provide us with relatively stable production and recurring cash flow with significant exposure to improvements in oil prices. Our inventory consists of more than 4,500 future well operations. Given the maturity of our assets, we believe our drilling and development operations in California are predictable and low risk. Our California production is sold locally under long-term contracts with prices based upon regional benchmarks. In response to current oil market conditions, we plan to focus our 2015 operating and capital expenditures in California on high-margin recompletion and well maintenance activities and conduct a moderate level of drilling in 2016 focused on our Cymric field. |

| • | We own an attractively positioned gas portfolio in Louisiana and Wyoming. We own extensive positions in the Haynesville shale formation in Louisiana, a position in the Inboard Lower Tertiary/Cretaceous gas trend located onshore in South Louisiana and a position in the Madden field located in Central Wyoming. Our gas properties in the Haynesville shale formation and in the Inboard Lower Tertiary/Cretaceous trend are geographically located to benefit from expected gas demand growth at existing and planned LNG terminals and petrochemical plants in the Gulf Coast region. Our position in the Madden field provides us with stable production and cash flows with long reserve life. Our large resource and acreage position provides us with the opportunity for significant reserve and production growth on a rapidly scalable basis upon a return of a more favorable gas price environment. |

| • | Experienced management and technical team with proven offshore and onshore expertise. Our senior management team has extensive expertise in the oil and gas industry, with an average of 33 years of experience, many of which have been spent working together in the Deepwater GOM. We believe this experience, along with widespread industry relationships, allows our senior management team to identify attractive acquisition opportunities and evaluate resource potential. We have also assembled a technical team that includes 135 engineers, 62 geologists/geophysicists and 236 petrotechnical professionals with an average of 26 years of experience. We believe our experienced and cohesive management and technical team will be of strategic importance as we continue to expand our future exploration and development plans. |

| • | Strong financial position. After giving effect to our corporate reorganization and this offering and the use of proceeds therefrom, we will have zero debt, $ million in cash on hand and $ million of available borrowing capacity through bank credit facilities and/or an intercompany loan agreement with our parent FCX. In the future, we will seek to maintain financial flexibility to enable us to most effectively develop our portfolio in the Deepwater GOM, California and other areas. |

Our strategy consists of the following principal elements:

| • | Grow proved reserves and production through measured development of our asset portfolio. We intend to develop our asset portfolio of identified drilling locations at a prudent pace given the current commodity price environment and plan to seek partnerships with third parties to delineate our discoveries and prospects. Capital expenditures for 2015 are currently estimated to total $2.8 billion, with 79 percent of our 2015 capital budget expected to be directed to our focus areas in the Deepwater GOM. We intend to pursue drilling opportunities that offer competitive risk-adjusted rates of return. We believe our near-term investments are low risk based on production history and industry activity in |

11

Table of Contents

Index to Financial Statements

| the area and repeatable as a result of well-defined geological properties over a large area. Through the conversion of our resource base to developed reserves, we will seek to increase our proved reserves, production and cash flow while generating favorable returns on invested capital. |

| • | Focus on our high-margin, oil-weighted Deepwater GOM projects. We focus our capital on high cash margin oil-weighted properties in the Deepwater GOM where we receive favorable prices in relation to WTI. Because we have extensive existing infrastructure and facilities with excess production and handling capacity in the Deepwater GOM, our capital allocation strategy is principally focused on drilling and development opportunities that can be tied back to existing facilities. We expect to continue to maintain and grow our reserve and production base through the development of our existing inventory of projects in the Deepwater GOM. |

| • | Utilize our proven technical experience to optimize results and increase returns in the Deepwater GOM. Our senior management and technical team intend to continue to seek ways to maximize hydrocarbon recovery by enhancing our evaluation, drilling, completion and production techniques. We utilize a variety of techniques to increase returns in the Deepwater GOM, including reservoir modeling, pressure maintenance, flow optimization, subsea pumping, and evaluation of seismic data. Continued reprocessing, new acquisitions and improvement in seismic imaging have allowed us to identify additional hydrocarbon potential in previously producing fields as well as in our exploration drilling. Advancements in subsea pumping as well as existing deepwater wellbore lift mechanisms have the potential to allow us to increase the recovery factors from our properties. We regularly evaluate our operating results in order to optimize our performance and make informed decisions about our capital program. |

| • | Maintain a high degree of operational control in order to improve operating and cost efficiencies and leverage relationships with key partners. We seek operational control of our properties in order to enhance returns through operational and cost efficiencies and increase ultimate hydrocarbon recovery by continuous improvement of our drilling techniques, completion methodologies and reservoir evaluation processes. Operational control allows us to more efficiently manage the pace of development activities and the gathering and marketing of our production. Of our estimated 2015 capital budget, 77 percent is related to projects we operate, allowing us to effectively manage the timing and levels of our development spending, overall well costs and operating costs. For properties we operate, in addition to having the ability to control the timing and method of development, we have the ability to partner with third party investors similar to our financing related to our Lucius development. For wells that we do not operate, we seek to join with other experienced and respected companies in the Deepwater GOM, including Anadarko and Shell, with comparable technology and technical expertise. In addition, we benefit from shared information and technology with our working interest partners and believe this enhances our operational results. |

| • | Maintain a rigorous, ongoing prospect maturation and enhancement process through our technical capabilities. We believe that having seismic data in the Deepwater GOM complemented by an experienced technical team that is capable of reprocessing the data to maximize its benefit is a core requirement for generating and maturing high-quality exploratory prospects. We actively leverage our extensive inventory of seismic data to identify prospects by correlating regional imaging analysis to industry drilling results. We continually enhance our prospect inventory through our technical team’s interpretation and reprocessing of our existing seismic data, our ongoing acquisition of incremental data to augment our data base and our team’s detailed regional sand isopach mapping and analysis and since 2006 have spent in excess of $300 million on acquiring and reprocessing seismic data. We believe these initiatives will allow us to replenish our exploration inventory through maturation of prospects on currently owned leasehold, farmouts or acquisitions from other oil and gas energy companies and participation in future lease sales. In the near term we plan to limit the amount of spending on lease acquisitions and exploration activities. |

12

Table of Contents

Index to Financial Statements

| • | Continue enhancing California operations to realize increased cash flow and grow our reserve base. Our management team is focused on continuous improvement of our California operations, both onshore and offshore, and has significant experience in identifying cost efficiencies while maintaining a stable production profile. Our California development plans are focused principally on maintaining stable production levels through continued drilling of conventional, waterflood and steamflood opportunities in the onshore fields. We believe the nature of our asset portfolio in California will continue to provide us with stable production and recurring cash flows in the foreseeable future. |

| • | Execute strategic acquisitions where our operating experience can be applied. We believe that attractive acquisition opportunities will become available and that our management team’s familiarity with our key operating areas and its contacts with the operators in those regions will enable us to identify high-return acquisition opportunities at attractive prices. We focus our acquisition activity where we believe our operational expertise provides the opportunity for meaningful incremental value creation and where our operational methods are most effective. Historically, this approach has allowed us to enter new areas and capture additional opportunities as evidenced by our acquisitions from BP and Shell of the Holstein, Horn Mountain and Marlin assets in 2012, as well as our recent acquisitions from Apache of an initial interest in Heidelberg and an additional interest in Lucius, our recent acquisition from Anadarko of interests in Vito and surrounding acreage, and our regular participation in the BOEM’s Deepwater GOM lease sales. We may selectively make acquisitions on attractive terms that complement our growth and help us achieve economies of scale. |

| • | Maintain financial flexibility to fund growth. We intend to maintain flexibility to fund our long-term growth plan. We expect our cash flows from operating activities, the net proceeds of this offering and our borrowing availability will be sufficient to fund our capital expenditures and other obligations necessary to execute our business plan in the near term. Substantially all of our lease terms allow us to allocate capital among projects in a manner that optimizes both costs and returns. In addition, our lease terms allow us to adjust our capital spending depending on commodity prices and market conditions. We currently have 84 MBbls/d hedged in 2015 with $90 by $70 put spreads. In the future, we plan to opportunistically hedge a portion of our expected production in order to stabilize our cash flows and maintain liquidity. |

Investing in our Class A common stock involves risks that include the speculative nature of oil and gas exploration, competition, volatile commodity prices and other material factors. For a discussion of these risks and other considerations that could negatively affect us, including risks related to this offering and our common stock, see “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements.”

Our principal stockholder is FCX, a leading international natural resources company with headquarters in Phoenix, Arizona. FCX operates large, long-lived, geographically diverse assets with significant reserves of copper, gold, molybdenum, cobalt, crude oil and gas.

FCX currently owns 100 percent of our Class A and Class B common stock. Upon completion of this offering, FCX will hold shares of Class B common stock, representing percent of our total outstanding shares of common stock, 100 percent of our total outstanding shares of Class B common stock, and percent of the combined voting power of our outstanding common stock upon completion of this offering (or percent, 100 percent and percent, respectively, if the underwriters’ option to purchase additional shares of Class A common stock from us is exercised in full). We also expect to enter into several agreements with FCX at the

13

Table of Contents

Index to Financial Statements

closing of this offering, including a tax matters agreement, an intercompany loan agreement, a shared services agreement, a transaction agreement and a stockholders agreement. For a description of these agreements, see “Certain Relationships and Related Party Transactions.” For more information regarding risks related to our relationship with FCX, see “Risk Factors,” including “Risk Factors—Risks Relating to this Offering and Our Class A Common Stock.”

Our principal executive offices are located at 700 Milam, Suite 3100, Houston, Texas 77002, and our telephone number is (713) 579-6000. Our website is www. .com. We expect to make our periodic reports and other information filed with or furnished to the SEC available free of charge through our website as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Information on our website or any other website is not incorporated by reference herein and does not constitute a part of this prospectus.

14

Table of Contents

Index to Financial Statements

| Issuer |

Freeport-McMoRan Oil & Gas Inc., a Delaware corporation. |

| Class A common stock offered by us |

shares (or shares if the underwriters exercise their option to purchase additional shares in full). |

| Option to purchase additional shares of Class A common stock |

The underwriters have a 30-day option to purchase up to additional shares of Class A common stock from us. |

| Class A common stock to be outstanding after the offering |

shares (or shares if the underwriters exercise their option to purchase additional shares in full). |

| Class B common stock to be outstanding after this offering |

shares. |

| Voting power of Class A common stock outstanding after giving effect to this offering |

percent ( percent if the underwriters exercise their option to purchase additional shares in full). |

| Voting power of Class B common stock outstanding after giving effect to this offering |

percent ( percent if the underwriters exercise their option to purchase additional shares in full). |

| Voting rights |

Following this offering, we will have two classes of authorized common stock: Class A common stock and Class B common stock. Each share of our Class A common stock entitles its holder to one vote on all matters to be voted on by stockholders generally. Each share of our Class B common stock entitles its holder to five votes on all matters to be voted on by stockholders generally. |

| Holders of our Class A and Class B common stock vote together as a single class on all matters presented to our stockholders for their vote or approval, except as otherwise required by applicable law. Please see “Description of Capital Stock.” |

| Use of proceeds |

We expect to receive $ million of net proceeds from the sale of the Class A common stock offered by us, after deducting underwriting discounts and commissions and estimated offering expenses. We intend to use the net proceeds from this offering and any proceeds received pursuant to any exercise by the underwriters of their option to purchase additional shares of our Class A common stock to fund the remainder of our 2015 capital budget and portions of our 2016 capital budget and for general corporate purposes. |

15

Table of Contents

Index to Financial Statements

| Dividend policy |

We do not anticipate paying any cash dividends on our Class A or Class B common stock. |

| Listing |

We intend to apply to list our Class A common stock on the New York Stock Exchange under the symbol “FMOG.” |

| Risk factors |

You should carefully read and consider the information beginning on page 25 of this prospectus set forth under the heading “Risk Factors” and all other information set forth in this prospectus before deciding to invest in our Class A common stock. |

The information above excludes shares of Class A common stock reserved for issuance under the Freeport-McMoRan Oil & Gas Inc. 2015 Incentive Award Plan. See “Management—2015 Incentive Plan.”

16

Table of Contents

Index to Financial Statements

SUMMARY CONSOLIDATED FINANCIAL, RESERVE AND OPERATING DATA

The following summary consolidated financial, reserve and operating data should be read in conjunction with, and are qualified by reference to, “Selected Historical Consolidated Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Corporate Reorganization” and the consolidated financial statements and related notes contained elsewhere in this prospectus.

On May 31, 2013, FCX acquired Plains Exploration & Production Company, which we refer to as the Predecessor or PXP, through a merger into Freeport-McMoRan Oil & Gas LLC, which we refer to as FM O&G LLC, a wholly owned subsidiary of FCX O&G, which we refer to as the Successor. On June 3, 2013, FCX acquired McMoRan Exploration Co., which we refer to as McMoRan, which became a wholly owned subsidiary of FCX O&G. The below selected unaudited pro forma consolidated information as of and for the six months ended June 30, 2015, and for the year ended December 31, 2014, relates to the Successor. The below summary consolidated financial data as of and for the six months ended June 30, 2015, for the six months ended June 30, 2014, as of and for the year ended December 31, 2014, as of December 31, 2013, and for the period from April 23, 2013, to December 31, 2013, relates to the Successor. The results included in the summary financial data for the period from April 23, 2013, to December 31, 2013, include PXP’s results beginning June 1, 2013, and McMoRan’s results beginning June 4, 2013. The Successor’s oil and gas operations commenced on June 1, 2013. The below summary consolidated financial data for the period from January 1, 2013, to May 31, 2013, and as of and for the years ended December 31, 2012, 2011 and 2010, relates to the Predecessor.

The unaudited pro forma information of FCX O&G gives effect to (i) the expected sale of shares of Class A common stock, the use of proceeds from the sale of the Class A common stock and the proposed corporate reorganization (which, among other things will result in the elimination of our revolving notes and other long-term debt, including our senior notes) and (ii) the Eagle Ford shale divestment. The unaudited pro forma condensed consolidated statement of operations for the six months ended June 30, 2015, gives effect to the expected sale of equity securities as if the sale had occurred on January 1, 2014; the unaudited pro forma condensed consolidated statement of operations for the year ended December 31, 2014, gives effect to the expected sale of equity securities and the Eagle Ford shale divestment as if the transactions had occurred on January 1, 2014; and the unaudited pro forma condensed consolidated balance sheet gives effect to the expected sale of Class A common stock securities as if it had occurred on June 30, 2015. This unaudited pro forma condensed consolidated financial data is provided for information purposes only and does not purport to represent what the actual results of operations or financial position would have been if these transactions had occurred on the dates assumed. The unaudited pro forma condensed consolidated financial data should be read together with the historical financial statements and the pro forma condensed consolidated financial statements included elsewhere in this prospectus.

The summary historical consolidated statements of operations data and statements of cash flow data for the six months ended June 30, 2015 and 2014, and the summary historical consolidated balance sheet data as of June 30, 2015, were derived from the unaudited consolidated financial statements of the Successor included elsewhere in this prospectus. These statements have been prepared on a basis consistent with the audited consolidated financial statements of the Successor. In the opinion of management, such unaudited financial data reflects all adjustments, consisting only of normal and recurring adjustments, necessary for a fair presentation of the results for such period. The results of operations for the interim periods are not necessarily indicative of the results to be expected for the full year or any future period.

We derived the summary historical consolidated statements of operations data and statements of cash flow data for the year ended December 31, 2014, and for the period from April 23, 2013, to December 31, 2013, and the summary historical consolidated balance sheet data as of December 31, 2014 and 2013, from the audited consolidated financial statements of the Successor included elsewhere in this prospectus.

17

Table of Contents

Index to Financial Statements

We derived the summary historical consolidated statements of operations data and statements of cash flow data for the period from January 1, 2013, to May 31, 2013, and for the year ended December 31, 2012, from the audited consolidated financial statements of the Predecessor included elsewhere in this prospectus.

Summary Consolidated Financial Data

| FM O&G Inc. Pro Forma |

FCX O&G (Successor) | PXP (Predecessor) | ||||||||||||||||||||||||||||||||

| As of and for the Six Months Ended June 30, 2015 |

For the Year Ended December 31, 2014 |

As of and for the Six Months Ended June 30, 2015 |

For the Six Months Ended June 30, 2014 |

As of and for the Year Ended December 31, 2014 |

April 23 to and as of December 31, 2013(1) |

January 1 to May 31, 2013 |

As of and for the Year Ended December 31, 2012 |

|||||||||||||||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||||||||||||||||

| (in thousands, except outstanding shares) |

(in thousands, except earnings per share) |

|||||||||||||||||||||||||||||||||

| Statement of operations data |

||||||||||||||||||||||||||||||||||

| Revenues(2) |

$ | 1,068,588 | $ | 2,496,998 | $ | 4,709,706 | $ | 2,615,966 | $ | 2,041,802 | $ | 2,565,307 | ||||||||||||||||||||||

| (Loss) income from operations(2)(3) |

(6,400,590 | ) | 508,351 | (4,479,725 | ) | 450,137 | 627,837 | 615,657 | ||||||||||||||||||||||||||

| Net (loss) income |

(4,432,758 | ) | 178,685 | (3,569,611 | ) | 199,475 | 274,523 | 342,787 | ||||||||||||||||||||||||||

| Net (loss) income attributable to common stockholders(4) |

(4,453,060 | ) | 158,925 | (3,609,437 | ) | 177,691 | 256,152 | 306,420 | ||||||||||||||||||||||||||

| (Loss) earnings per common share |

||||||||||||||||||||||||||||||||||

| Basic |