Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - META FINANCIAL GROUP INC | ex99_1.htm |

| 8-K - META FINANCIAL GROUP, INC 8-K 7-30-2015 - META FINANCIAL GROUP INC | form8k.htm |

Exhibit 99.2

Third QUARTER 2015 Investor Update

META Management Chairman and Chief Executive Officer, Meta Financial GroupTyler Haahr has been with Meta Financial Group since March 1997. Previously, he was a partner with the law firm of Lewis and Roca LLP, Phoenix, Arizona. Tyler received his B.S. degree with honors at the University of South Dakota in Vermillion, SD. He graduated with honors from the Georgetown University Law Center, Washington, D.C. President, Meta Financial Group and MetaBankBrad Hanson founded Meta Payment Systems in May 2004. He has more than 20 years of experience in financial services, including numerous banking, card industry and technology-related capacities. During his career Brad has played a significant role in the development of the prepaid card industry. Brad graduated from the University of South Dakota in Vermillion, SD with a degree in Economics. Chief Financial Officer, Meta Financial Group and MetaBank Glen Herrick was appointed EVP & Chief Financial Officer in October 2013, after joining Meta in March 2013. Previously, he served in various finance and risk management roles at Wells Fargo, including as CFO of Wells Fargo’s student loan division. Glen received his B.S. degree in Engineering Management from the United States Military Academy in West Point, N.Y. and MBA from the University of South Dakota. He also graduated from the Stonier Graduate School of Banking. J. Tyler Haahr Brad C. Hanson Glen W. Herrick 2

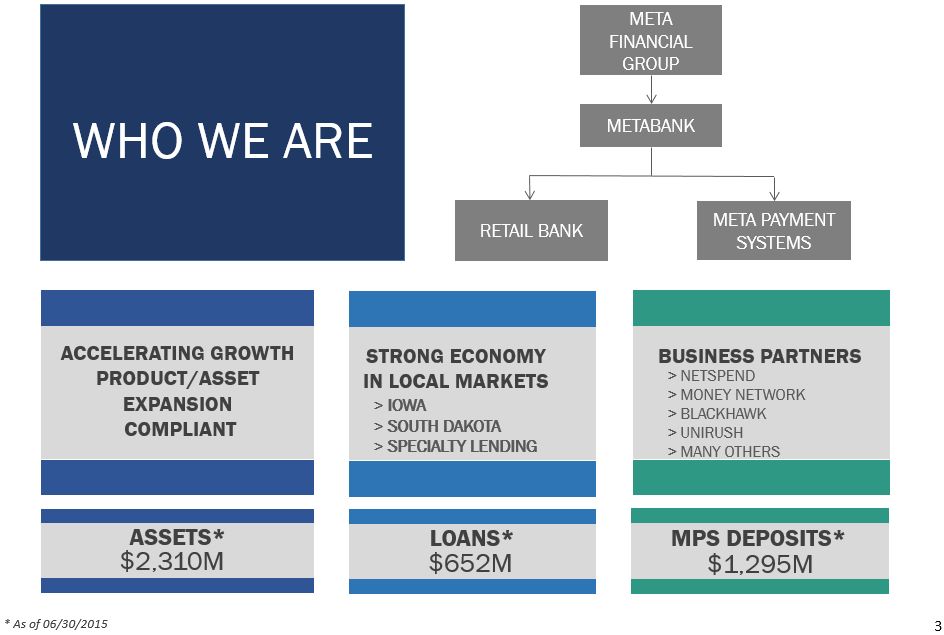

MetaBank Retail Bank Meta Payment Systems Meta Financial Group LOANS* $652M MPS Deposits* $1,295M STRONG ECONOMY IN LOCAL MARKETS BUSINESS PARTNERS > NetSpend> Money Network> Blackhawk> Unirush> Many Others * As of 06/30/2015 WHO WE ARE 3 Accelerating Growth Product/asset Expansion Compliant Assets* $2,310M > IOWA> SOUTH DAKOTA> SPECIALTY LENDING

WHO WE ARE Growing community bank in regions with strong economiesBased in Iowa and South Dakota Strong and high quality commercial & ag loan growthAFS / IBEX asset acquisition completed in December 2014Platform for nationwide expansionHigh quality and accelerating loan growth RETAIL BANK A top prepaid card issuer in U.S.Robust deposit growthNew partners being added & existing partners expandingNew product introductions in 2015 META PAYMENT SYSTEMS 4 Meta financial group: (NASDAQ: CASH) Big company expertise, small company agility

5 MFG evolution Community Bank MPS Start-Up Pre-Recession Regulatory Diversification ($ mil) 2000 2004 2007 2011 2015 Assets $506 $781 $686 $1,275 $2,310 Mkt Cap $23 $55 $103 $59 $298 TBV – not rounded $16.48 $18.98 $18.11 $25.19 $27.01 Net Income $2.3 $4.0 $1.2 $4.6 $13.4 (9 Mos.) Events Expanded to SF MPS issues first prepaid cards MPS deposits $243MMetaBank West Central Sale Consent OrderBegan enhanced compliance & operational multi-year build-out Consent Order TerminatedAFS AcquiredFt. Knox AnnouncedMPS partners addedMPS deposits $1.3B Amounts are at year end, September 30, except for 2015 which is at June 30th

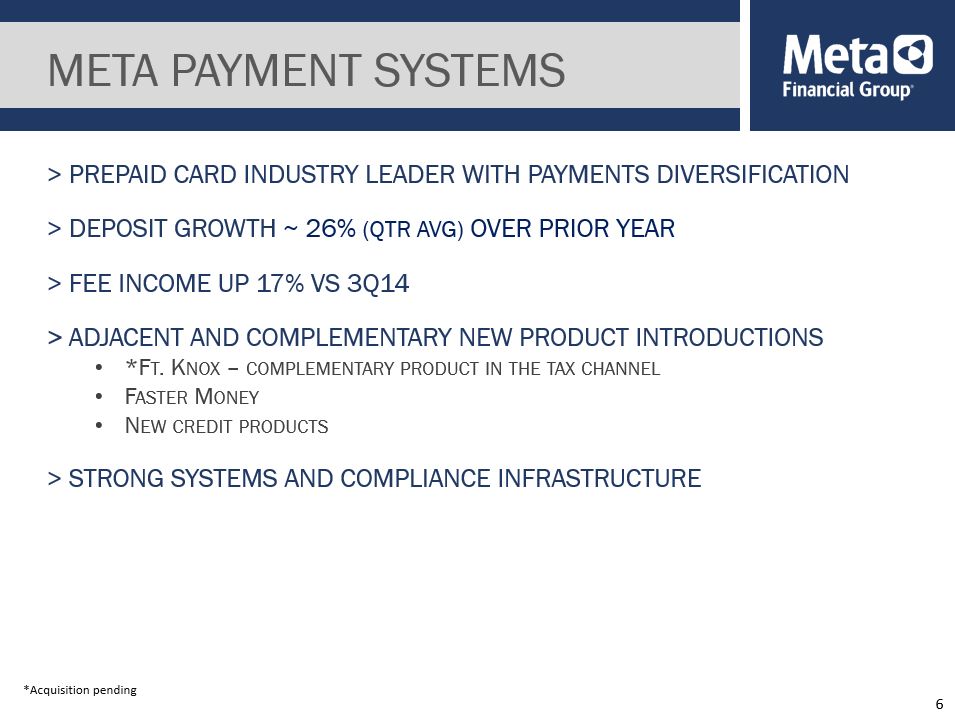

> Prepaid card industry leader with payments diversification> Deposit Growth ~ 26% (qtr avg) over prior year> Fee Income up 17% vs 3Q14> Adjacent and Complementary new product introductions*Ft. Knox – complementary product in the tax channelFaster MoneyNew credit products> Strong systems and compliance infrastructure Meta Payment Systems 6 *Acquisition pending

> Growing Existing relationshipsNetspendMoney NetworkBlackhawkGlobal Cash> New relationships driving accelerating growth, Strong PipelineInComm UnirushStore FinancialHyperwallet Systems Berkley Payment SolutionsUnivision> 9 of the top 10 program managers under contract through 2019 Meta Payment Systems 7

> Successful regional enterprise60 years in business 10 locations in Iowa and South Dakota Growing, profitable operationsLoyal customer base> Diverse customer base Attractive combination of commercial, agricultural & retail> Net Loan growth of 19% ($87M) over the last 12 Months> Expect continued robust loan growth in the next year> Maintained high credit standards resulting in low non-performing assets Retail bank 8

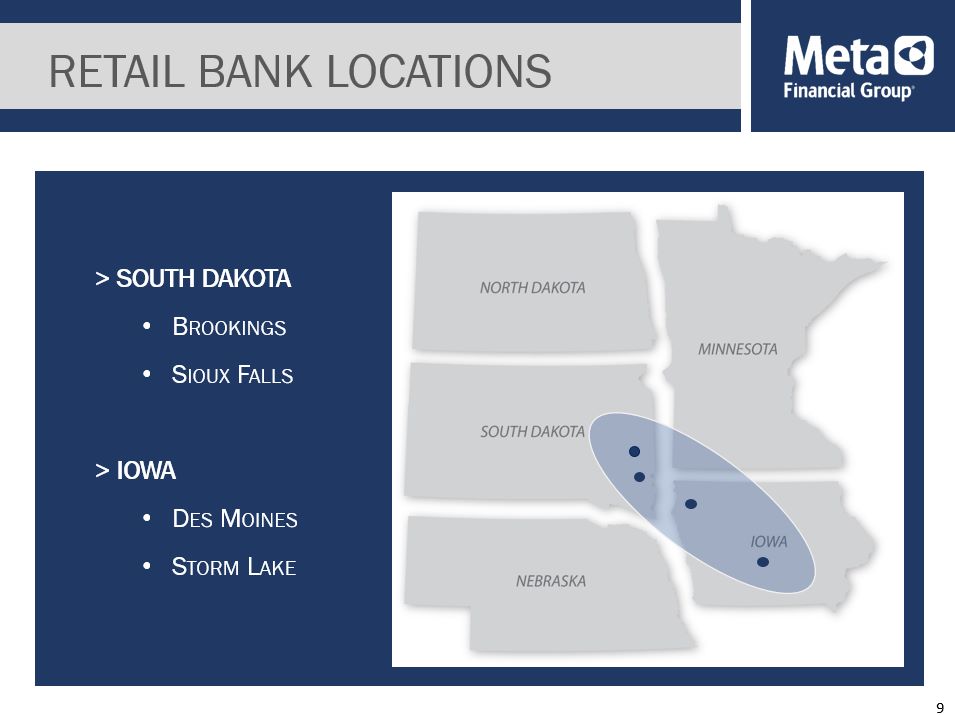

Retail bank locations > South dakotaBrookingsSioux Falls> Iowa Des MoinesStorm Lake 9

Retail bank - AFS/IBEX acquisition 10 7th largest U.S. insurance premium finance company in 2014Loans to commercial businesses fund their property, casualty, and liability insurance premiums. Assisted by > 1,300 independent insurance agencies / brokersHigher yields than alternative investments, particularly for the termSignificant collateralization minimizes credit riskTypically 9-10 month terms ensure rapid portfolio turnover and potential for rate increases in a rising rate environmentAgencies / brokers are underwritten to mitigate potential fraudLoans grew $17.6 million, or 19% (38% annualized), from acquisition in December, 2014 - June 30, 2015, & expected to accelerate going forwardScalable platform will support anticipated robust national growthNew, seasoned sales executives added in fiscal third quarter of 2015

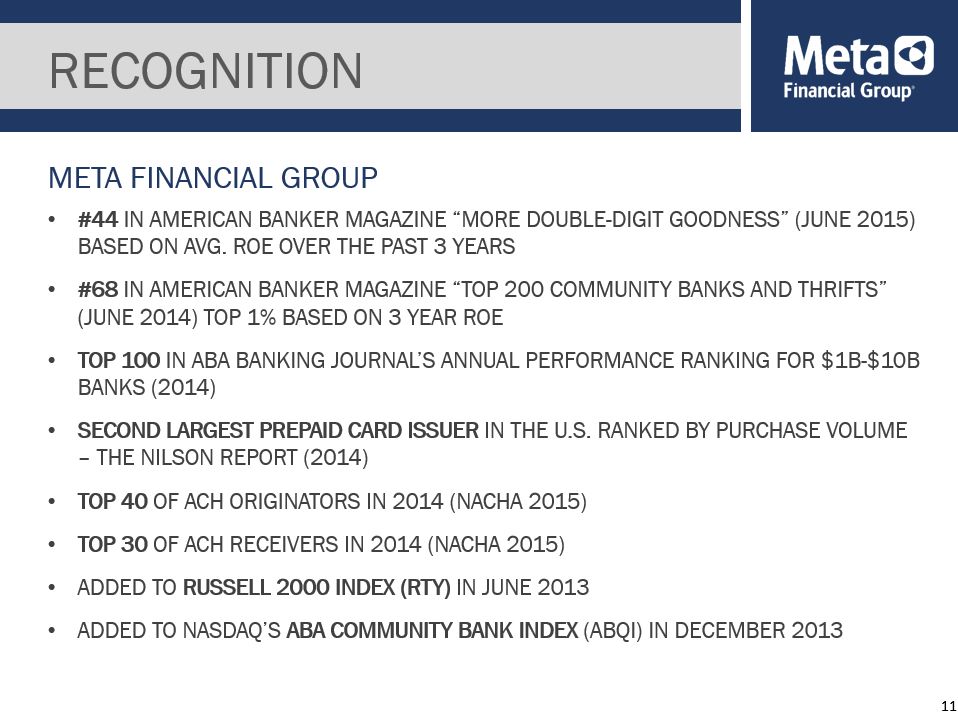

RECOGNITION #44 in American Banker Magazine “More double-digit goodness” (June 2015) based on avg. roe over the past 3 years#68 in American Banker Magazine “Top 200 Community Banks and Thrifts” (June 2014) Top 1% based on 3 year ROETop 100 in ABA Banking Journal’s annual Performance Ranking for $1B-$10B banks (2014)Second largest Prepaid card issuer in the U.S. ranked by purchase volume – The Nilson Report (2014)Top 40 of ACH originators in 2014 (nacha 2015)Top 30 of ACH receivers in 2014 (nacha 2015)Added to Russell 2000 Index (RTY) in June 2013Added to NASDAQ’s ABA Community Bank Index (ABQI) in December 2013 Meta Financial Group 11

Strategic Goals Grow organically and by acquisition to achieve scaleDiversify business linesStrengthen balance sheet and grow revenueCreate a more strategic asset mixHire and develop the right people in the right rolesscalable operating infrastructureVertically integrate to gain more of the economic value chain 12

> Optimize synergies: retail bank and MPSStrong loan growth in local markets and AFS/IBEXLow cost deposits feed increasingly diverse asset mixRising rates expected to increase yields while funding costs remain lowMBS portfolio ($666M) yields & income expected to increase as rates riseAs of June 30, 2015 yield book projects income increases of $4.4M, $5.8M, & $6.8M in a +50, +100, and +200 parallelPortfolio restructuring in 3Q15, expected to increase taxable equivalent income by ~ $1.6M annually> Leverage MPS leadership in payments industryIncreasing market share organically and with new partnersEmergent leader in “virtual cards” for electronic settlementsSponsors ~65% of U.S. “white label” ATMs42 patents with over a dozen pending> Retail bank Entrance into specialty lendingCompleted AFS/IBEX asset acquisition in December 2014Hired executive sales staff and other producers for AFS/IBEX in 3Q15Pending partnership with a health care financing company provides another loan portfolio of historically limited credit risk & solid yields Growth drivers 13

> Early adopter of sophisticated compliance systems> OCC consent order removed in august 2014> Federal reserve bank consent order removed in may 2015> Investments in MPS program design, training and technologyImplemented enhanced bsa/aml technologyEnhanced infrastructure supports growthShifted focus to business development opportunities, while maintaining continuous improvement mindset on systems and compliance> High competitive barriers to enter prepaid IndustryExpertise, Capital, ComplianceOperational infrastructureHigh start-up costs Compliance and oversight systems 14

> Positively leveraged for higher rate environment> OCI volatile relative to peers GAAP does not capture balance sheet true value, particularly low and no-cost depositsMeta mark includes ~65% of assets (securities) vs. typical “peer” at ~20%> Expectation for Continued, increasing Net Interest Margin (NIM)AFS/IBEX loans (wtd avg rate > 8.75%, avg maturities < 6 mos) should adjust higher if rates riseAFS continued loan growth and addition of experienced sales executivesRestructured a portion of securities portfolio that negatively affected margin and income in 3Q15 but is expected to add ~$1.6M in annual taxable equivalent income going forward> reinvestment opportunity leading to increased Nim expansion in an up-rate environmentSecurities cash flow and new MPS deposits deployed at higher ratesMBS portfolio yields & income expected to increase as rates rise. Yield Book projects income increases, as of June 30, 2015, in a +50 and +100 parallel, instantaneous interest rate shock of $4.4M and $5.8M, respectively> Deposit funding cost to remain at low levels due to concentration of MPS-related non-interest bearing deposits Interest Rate Risk Management 15

> Capital enhancementsRecent $26 million private placement supporting pending Fort Knox acquisition2014-15 ATM net proceeds of $25.4 million to support growth$61.0 million in 2012-13 via private placements and an ATM offering> Maintain strong capital ratio goalsCommon equity tier 1 capital at least 8%Risk-based over 15%> Prudent Capital management, flexibility to source future needs Capital Management 16

> Net Income$13.4m in fiscal 2015 (9 months thru 06/30/15)Adjusted $14.9M*, +19% vs. fy14 same period> earnings profileAnnualized ROAA of 0.78% and annualized ROAE of 9.07%Adjusted* annualized ROAA and ROAE of 0.87% and 10.04%Business development & implementation costs from new agreements & products being incurred for future revenue that historically lags 9-12 months after implementation> Very Strong asset qualityNPAs markedly lower than peer group at 0.33% of total assets Mfg FINANCIAL HIGHLIGHTS 17 *$(1.5)M Loss on sale of securities, $(.8)M acquisition costs, $(0.8)M Amortization Expense and $0.9M ins. claim reimbursements less applicable taxes

Earnings power while growing equity 18

Income statement ($000s) * Includes $11.4M gain on sale of GNMA Securities** Includes $2.4M gain on sale of securities*** Includes $(1.5)M loss on sale of securities, $(.8)M acquisition costs, $(0.8)M Amortization Expense and $0.9M ins. claim reimbursements. Meta Financial Group FY10 FY11 FY12* FY13** FY14 3Q14 YTD 3Q15 YTD*** Net Interest Income After Provision 17,299 34,034 32,685 36,022 45,112 33,359 42,176 Total Non Interest Income 97,444 57,491 69,574 55,503 51,738 39,131 43,068 Compensation and Benefits 32,529 30,467 31,104 34,106 38,155 28,288 34,324 Card Processing Expense 38,242 23,286 17,373 15,584 15,487 11,668 12,374 All Other Expense 24,159 29,509 26,986 24,713 24,589 17,685 23,608 Net Income Before Taxes 19,813 8,263 26,796 17,122 18,619 14,849 14,939 Income Tax Expense 7,420 3,623 9,682 3,704 2,906 2,500 1,523 Net Income 12,393 4,640 17,114 13,418 15,713 12,349 13,416 19

Total revenue * Includes $11.4M gain on sale of GNMA Securities** Includes $2.4M gain on sale of securities*** Includes $(1.5)M loss on sale of securities, $(1.6)M acquisition costs, $(0.7)M Amortization Expense and $0.9M ins. claim reimbursements $ millions 20

Balance sheet ($000s) 4Q10 4Q11 4Q12 4Q13 4Q14 3Q14 3Q15 Cash And Cash Equivalents 94,248 132,149 106,067 73,733 100,159 75,120 79,460 Investments and MBS 511,011 615,320 998,826 1,176,811 1,320,364 1,319,198 1,516,948 Loans Receivable Net 369,563 314,484 329,689 364,100 484,690 450,628 634,513 Other Assets 64,037 64,825 61,412 98,760 96,555 143,662 117,161 Assets 1,038,859 1,126,778 1,495,994 1,713,404 2,001,768 1,988,608 2,348,081 Total Deposits 855,383 969,978 1,274,867 1,405,294 1,541,539 1,513,179 1,804,247 Other Liabilities 112,761 77,721 112,355 172,295 289,717 314,296 329,263 Shareholders' Equity 70,715 79,079 108,772 135,815 170,512 161,133 214,571 Liabilities and Equity 1,038,859 1,126,778 1,495,994 1,713,404 2,001,768 1,988,608 2,348,081 (Fiscal Quarter Average) 21

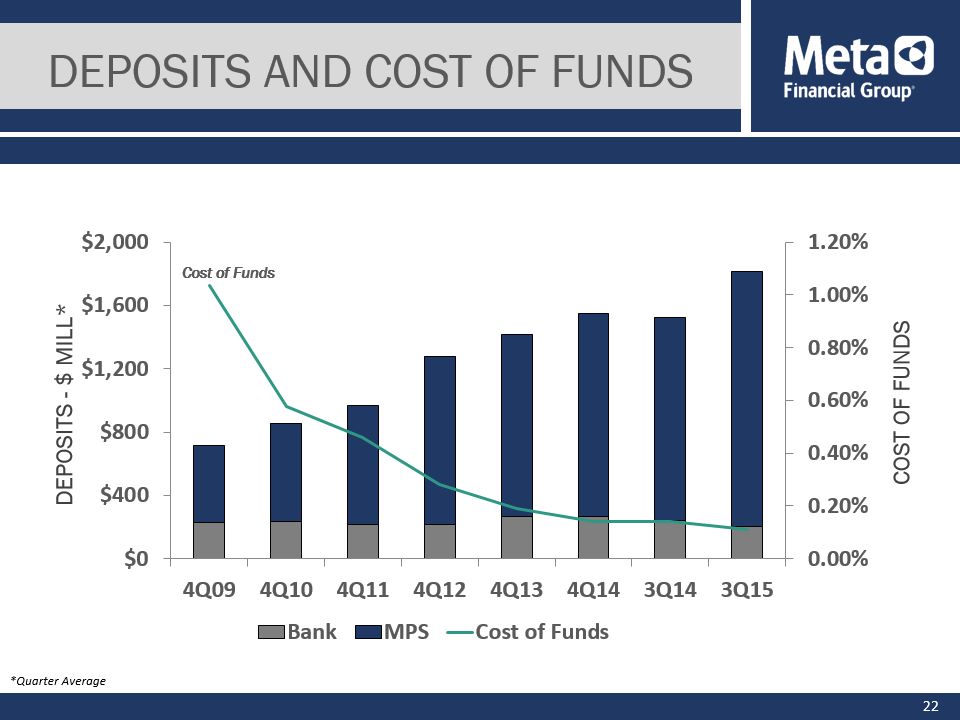

Deposits and cost of funds deposits - $ mill* Cost of Funds 22 *Quarter Average

Total assets* 19.0% CAGR $ millions 23 *Fiscal Quarter average

Total net loans* *Fiscal Quarter average Net of ALLL $ millions 24

Non-performing assets $ millions of non-performing assets % of total assets 25

> A Leading issuer of prepaid debit cardsSpringboard into other products and servicesSignificant growth - current partners' expanding & new partners added> Strong capital positionEarnings and access to capital markets to fund our growth objectivesMFG ratio of tier 1 capital to adj. total assets at June 30, 2015 of 8.91%MFG ratio of tier 1 capital to RWAs at June 30, 2015 of 20.68% > Stable, low-cost funding advantage> Steady dividend policy > Potential for upward trend in earningsHigher/Normalized interest rates Asset diversification with higher yields~90% of deposits are low or no-cost & will remain so in rising ratesLoan & Security yields well positioned to increase with rising rates META VALUE PROPOSITION 26

Forward Looking Statements Meta Financial Group, Inc.®, (“the Company”) and its wholly-owned subsidiary, MetaBank® (the “Bank” or “MetaBank”), may from time to time make written or oral “forward-looking statements,” including statements contained in this investor update, in its filings with the Securities and Exchange Commission (“SEC”), in its reports to stockholders and in other communications by the Company, which are made in good faith by the Company pursuant to the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995.You can identify forward-looking statements by words such as “may,” “hope,” “will,” “should,” “expect,” “plan,” “anticipate,” “intend,” “believe,” “estimate,” “predict,” “potential,” “continue,” “could,” “future” or the negative of those terms or other words of similar meaning. You should carefully read statements that contain these words because they discuss our future expectations or state other “forward-looking” information. These forward-looking statements include statements with respect to the Company’s beliefs, expectations, estimates, and intentions that are subject to significant risks and uncertainties, and are subject to change based on various factors, some of which are beyond the Company’s control. Such statements address, among others, the following subjects: future operating results; customer retention; loan and other product demand; important components of the Company’s balance sheet and income statements; growth and expansion; new products and services, such as those offered by MetaBank or Meta Payment Systems® (“MPS”), a division of the Bank; credit quality and adequacy of reserves; technology; and the Company’s employees. The following factors, among others, could cause the Company’s financial performance and results of operations to differ materially from the expectations, estimates, and intentions expressed in such forward-looking statements: the risk that the Fort Knox transaction may not occur on a timely basis or at all; the risk that the business of the Bank and Fort Knox may not be combined successfully; the strength of the United States’ economy in general and the strength of the local economies in which the Company conducts operations; the effects of, and changes in, trade, monetary, and fiscal policies and laws, including interest rate policies of the Board of Governors of the Federal Reserve System (the “Federal Reserve”), as well as efforts of the United States Treasury in conjunction with bank regulatory agencies to stimulate the economy and protect the financial system; inflation, interest rate, market, and monetary fluctuations; the timely development of and acceptance of new products and services offered by the Company as well as risks (including reputational and litigation) attendant thereto and the perceived overall value of these products and services by users; the risks of dealing with or utilizing third parties; actions which may be initiated by our regulators; the impact of changes in financial services laws and regulations, including, but not limited to, laws and regulations relating to the tax refund industry; our relationship with our primary regulators, the Office of the Comptroller of the Currency and the Federal Reserve; technological changes, including, but not limited to, the protection of electronic files or databases; acquisitions; litigation risk in general, including, but not limited to, those risks involving the MPS division; the growth of the Company’s business, as well as expenses related thereto; continued maintenance by the Bank of its status as a well-capitalized institution; particularly in light of our deposit base, a substantial portion of which has been characterized as “brokered”; changes in consumer spending and saving habits; and the success of the Company at managing and collecting assets of borrowers in default.The foregoing list of factors is not exclusive. Additional discussions of factors affecting the Company’s business and prospects are reflected under the headings “Risk Factors” and in other sections of the Company’s Annual Report on Form 10-K for the fiscal year ended September 30, 2014, Quarterly Reports on Form 10-Q for the fiscal quarters ended December 31,2014, March 31,2015 and June 30,2015, and other filings made with the SEC. The Company expressly disclaims any intent or obligation to update any forward-looking statement, whether written or oral, that may be made from time to time by or on behalf of the Company or its subsidiaries. 27

NASDAQ: CASH