Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Guaranty Bancorp | gbnk-20150727x8k.htm |

Keefe, Bruyette & Woods16th Annual Community Bank Investor Conference New York, NY July 28-29, 2015

Keefe, Bruyette & Woods16th Annual Community Bank Investor Conference New York, NY July 28-29, 2015

forward looking statements This presentation contains forward-looking statements, which are included in accordance with the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “could,” “expects,” “plans,” “intends,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” or “continue,” or the negative of such terms and other comparable terminology. These forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the Company’s actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such factors include, among others, the following: failure to maintain adequate levels of capital and liquidity to support the Company’s operations; general economic and business conditions in those areas in which the Company operates, including the impact of global and national economic conditions on our local economy; demographic changes; competition; fluctuations in interest rates; continued ability to attract and employ qualified personnel; ability to receive regulatory approval for the bank subsidiary to declare dividends to the Company; adequacy of the allowance for loan losses, changes in credit quality and the effect of credit quality on the provision for credit losses and allowance for loan losses; changes in governmental legislation or regulation, including, but not limited to, any increase in FDIC insurance premiums; changes in accounting policies and practices; changes in business strategy or development plans; changes in the securities markets; changes in consumer spending, borrowing and savings habits; the availability of capital from private or government sources; competition for loans and deposits and failure to attract or retain loans and deposits; failure to recognize expected cost savings; changes in the financial performance and/or condition of our borrowers and the ability of our borrowers to perform under the terms of their loans and terms of other credit agreements; changes in oil and natural gas prices; political instability, acts of war or terrorism and natural disasters; and additional “Risk Factors” referenced in the Company’s most recent Annual Report on Form 10-K filed with the Securities and Exchange Commission, as supplemented from time to time. When relying on forward-looking statements to make decisions with respect to the Company, investors and others are cautioned to consider these and other risks and uncertainties. The Company can give no assurance that any goal or plan or expectation set forth in any forward-looking statement can be achieved and readers are cautioned not to place undue reliance on such statements, which speak only as of the date made. The forward-looking statements are made as of the date of this presentation, and, except as may otherwise be required by law, the Company does not intend, and assumes no obligation, to update the forward-looking statements or to update the reasons why actual results could differ from those projected in the forward-looking statements.

forward looking statements This presentation contains forward-looking statements, which are included in accordance with the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “could,” “expects,” “plans,” “intends,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” or “continue,” or the negative of such terms and other comparable terminology. These forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the Company’s actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such factors include, among others, the following: failure to maintain adequate levels of capital and liquidity to support the Company’s operations; general economic and business conditions in those areas in which the Company operates, including the impact of global and national economic conditions on our local economy; demographic changes; competition; fluctuations in interest rates; continued ability to attract and employ qualified personnel; ability to receive regulatory approval for the bank subsidiary to declare dividends to the Company; adequacy of the allowance for loan losses, changes in credit quality and the effect of credit quality on the provision for credit losses and allowance for loan losses; changes in governmental legislation or regulation, including, but not limited to, any increase in FDIC insurance premiums; changes in accounting policies and practices; changes in business strategy or development plans; changes in the securities markets; changes in consumer spending, borrowing and savings habits; the availability of capital from private or government sources; competition for loans and deposits and failure to attract or retain loans and deposits; failure to recognize expected cost savings; changes in the financial performance and/or condition of our borrowers and the ability of our borrowers to perform under the terms of their loans and terms of other credit agreements; changes in oil and natural gas prices; political instability, acts of war or terrorism and natural disasters; and additional “Risk Factors” referenced in the Company’s most recent Annual Report on Form 10-K filed with the Securities and Exchange Commission, as supplemented from time to time. When relying on forward-looking statements to make decisions with respect to the Company, investors and others are cautioned to consider these and other risks and uncertainties. The Company can give no assurance that any goal or plan or expectation set forth in any forward-looking statement can be achieved and readers are cautioned not to place undue reliance on such statements, which speak only as of the date made. The forward-looking statements are made as of the date of this presentation, and, except as may otherwise be required by law, the Company does not intend, and assumes no obligation, to update the forward-looking statements or to update the reasons why actual results could differ from those projected in the forward-looking statements.

Investors and security holders are urged to read the Company’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and other documents filed by the Company with the SEC. The documents filed by the Company with the SEC may be obtained at the Company’s website at www.gbnk.com or at the SEC's website at www.sec.gov. These documents may also be obtained free of charge from the Company by directing a request to: Guaranty Bancorp, 1331 Seventeenth St., Suite 200, Denver, CO 80202, Attention: Christopher Treece/Investor Relations; Telephone 303-675-1194.

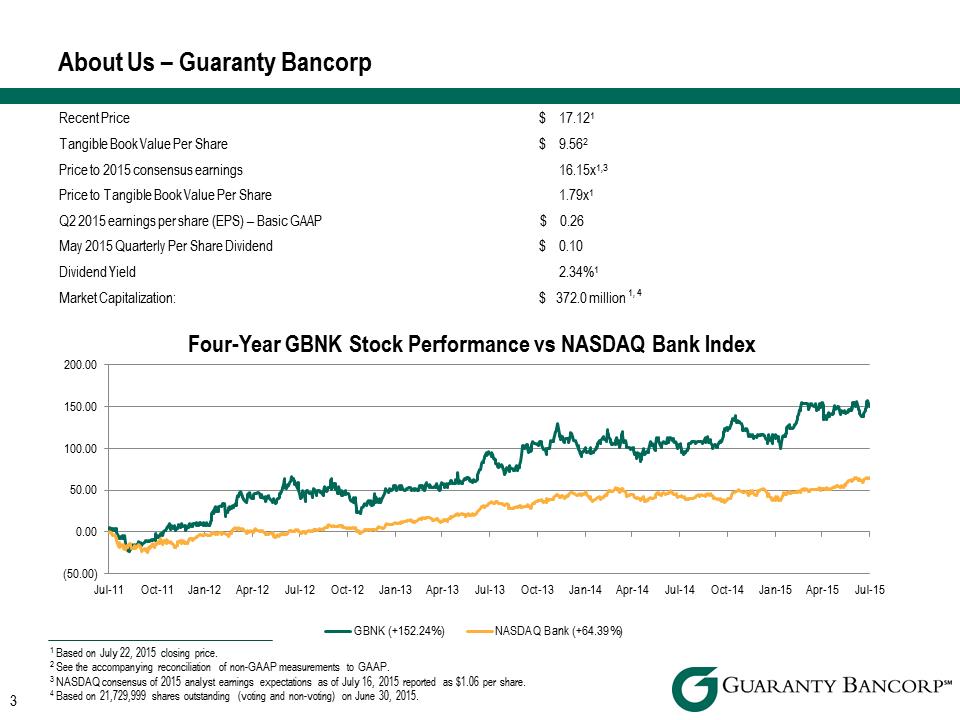

About Us – Guaranty BancorpRecent Price

About Us – Guaranty BancorpRecent Price

Recent Price$ 17.121

Tangible Book Value Per Share $ 9.562

Price to 2015 consensus earnings 16.15x1,3

Price to Tangible Book Value Per Share 1.79x1

Q2 2015 earnings per share (EPS) – Basic GAAP $ 0.26

May 2015 Quarterly Per Share Dividend$ 0.10

Dividend Yield 2.34%1

Market Capitalization: $ 372.0 million 1, 4 Four-Year GBNK Stock Performance vs NASDAQ Bank Index

1 Based on July 22, 2015 closing price.

2 See the accompanying reconciliation of non-GAAP measurements to GAAP.

3 NASDAQ consensus of 2015 analyst earnings expectations as of July 16, 2015 reported as $1.06 per share.

4 Based on 21,729,999 shares outstanding (voting and non-voting) on June 30, 2015.

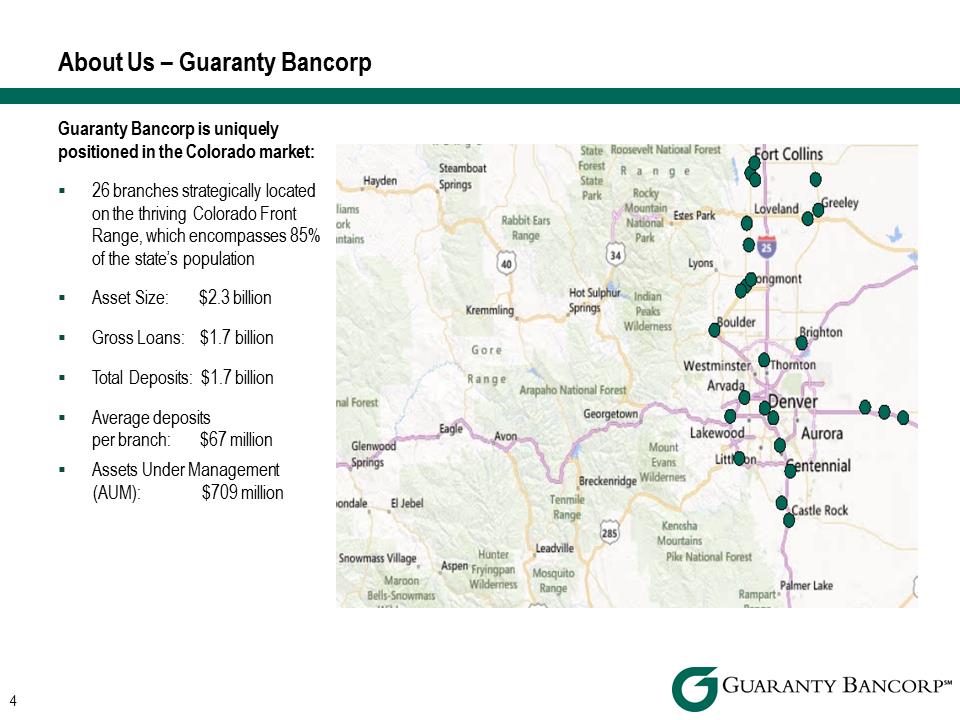

About Us – Guaranty Bancorp

Guaranty Bancorp is uniquely positioned in the Colorado market:

|

§ |

26 branches strategically located on the thriving Colorado Front Range, which encompasses 85% of the state’s population |

|

§ |

Asset Size: $2.3 billion |

|

§ |

Gross Loans: $1.7 billion |

|

§ |

Total Deposits: $1.7 billion |

|

§ |

Average deposits per branch: $67 million |

|

§ |

Assets Under Management |

(AUM): $709 million

|

§ |

Investment Considerations Profitability |

|

" |

Achieved ROAA and ROAE of 1.00% and 10.29% respectively, in the second quarter 2015 |

|

" |

Second quarter 2015 pre-tax operating earnings1 increased $2.4 million, or 40.0%, compared to second quarter 2014 |

|

" |

Net interest margin of 3.67% during the second quarter 2015 as compared to 3.66% in the second quarter 2014 |

|

q |

Stable net interest margin despite competitive interest rate environment |

|

q |

Cost of interest bearing liabilities decreased to 0.25% in the second quarter 2015 compared to 0.37% in the second quarter 2014, benefiting from the fourth quarter 2014 prepayment of $90 million in FHLB term advances |

|

§ |

Doubled quarterly cash dividend to 10 cents per share in February 2015 |

|

" |

Dividend yield of approximately 2.34% |

|

§ |

Loan growth momentum |

|

" |

Loan balances increased $113.5 million, or 29.3% annualized, compared to the first quarter 2015 |

|

" |

Trailing twelve month net loan growth of 16.0% |

|

" |

Trailing twelve month net loan growth in C&I loans of 8.5%, despite proactively reducing energy exposure by $20.6 million |

|

§ |

Strong asset quality (ratios as of June 30, 2015) |

|

" |

Nonperforming assets to total assets of 0.65% |

|

" |

Classified asset ratio of 13.87% |

|

" |

Texas ratio of 5.80% |

|

" |

Allowance to total loans of 1.37% 1 See accompanying reconciliation of non-GAAP financial measurements to GAAP. |

|

§ |

|

|

§ |

|

Investment Considerations Strong core deposit mix

Investment Considerations Strong core deposit mix

|

" |

Noninterest bearing deposits comprised 35.7% of total deposits at June 30, 2015 |

|

" |

Time deposits comprised 13.7% of total deposits at June 30, 2015 |

|

" |

Average cost of deposits remains low at 0.18% during the second quarter 2015 |

|

§ |

Noninterest income growth |

|

" |

Investment advisory fees |

|

q |

Total AUM at June 30, 2015 of $708.6 million, an annualized increase of 7.5%, from December 31, 2014 |

|

q |

Continued focus on growth in investment management and trust fee income through organic growth, fee enhancement and acquisitions |

|

" |

Gains on sale of SBA loans generated $449,000 in noninterest income in the first six months of 2015 compared to $165,000 in the first six months of 2014, an increase of $284,000 or 172% |

|

" |

Treasury management fees grew 11.1% in 2014, followed by a 4.8% growth in treasury management fees through the first six months of 2015, due mostly to growth in our C&I customer base |

|

§ |

|

|

" |

|

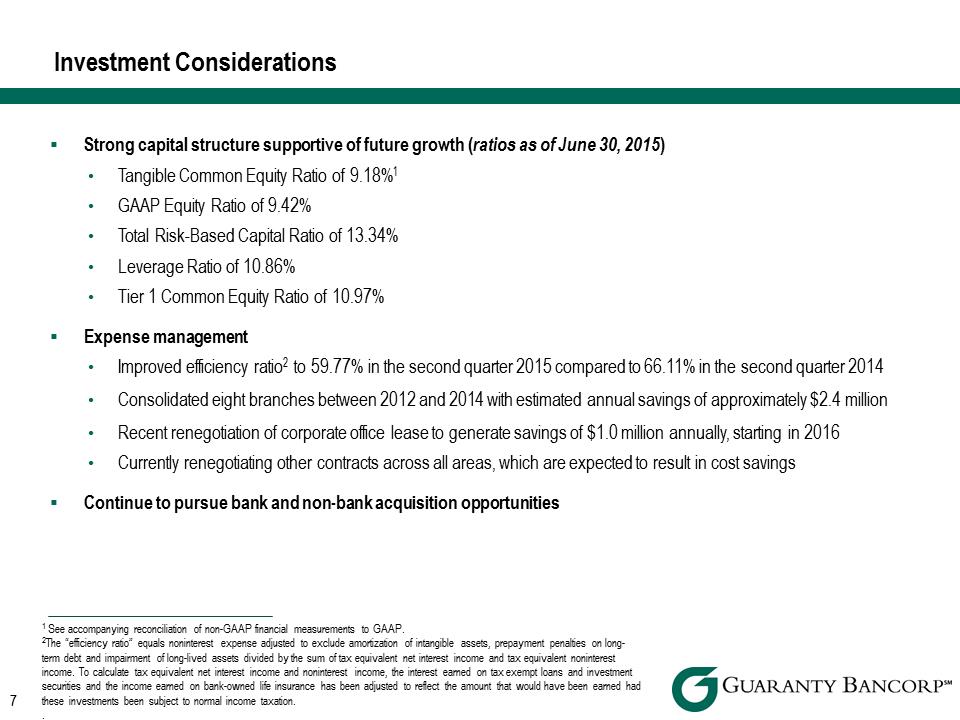

Investment Considerations

Investment Considerations

Strong capital structure supportive of future growth (ratios as of June 30, 2015)

|

" |

Tangible Common Equity Ratio of 9.18%1 |

|

" |

GAAP Equity Ratio of 9.42% |

|

" |

Total Risk-Based Capital Ratio of 13.34% |

|

" |

Leverage Ratio of 10.86% |

|

" |

Tier 1 Common Equity Ratio of 10.97% |

|

§ |

Expense management |

|

" |

Improved efficiency ratio2 to 59.77% in the second quarter 2015 compared to 66.11% in the second quarter 2014 |

|

" |

Consolidated eight branches between 2012 and 2014 with estimated annual savings of approximately $2.4 million |

|

" |

Recent renegotiation of corporate office lease to generate savings of $1.0 million annually, starting in 2016 |

|

" |

Currently renegotiating other contracts across all areas, which are expected to result in cost savings |

|

" |

Continue to pursue bank and non-bank acquisition opportunities |

|

" |

1 See accompanying reconciliation of non-GAAP financial measurements to GAAP. |

|

" |

2The “efficiency ratio” equals noninterest expense adjusted to exclude amortization of intangible assets, prepayment penalties on long-term debt and impairment of long-lived assets divided by the sum of tax equivalent net interest income and tax equivalent noninterest income. To calculate tax equivalent net interest income and noninterest income, the interest earned on tax exempt loans and investment securities and the income earned on bank-owned life insurance has been adjusted to reflect the amount that would have been earned had these investments been subject to normal income taxation. |

|

" |

|

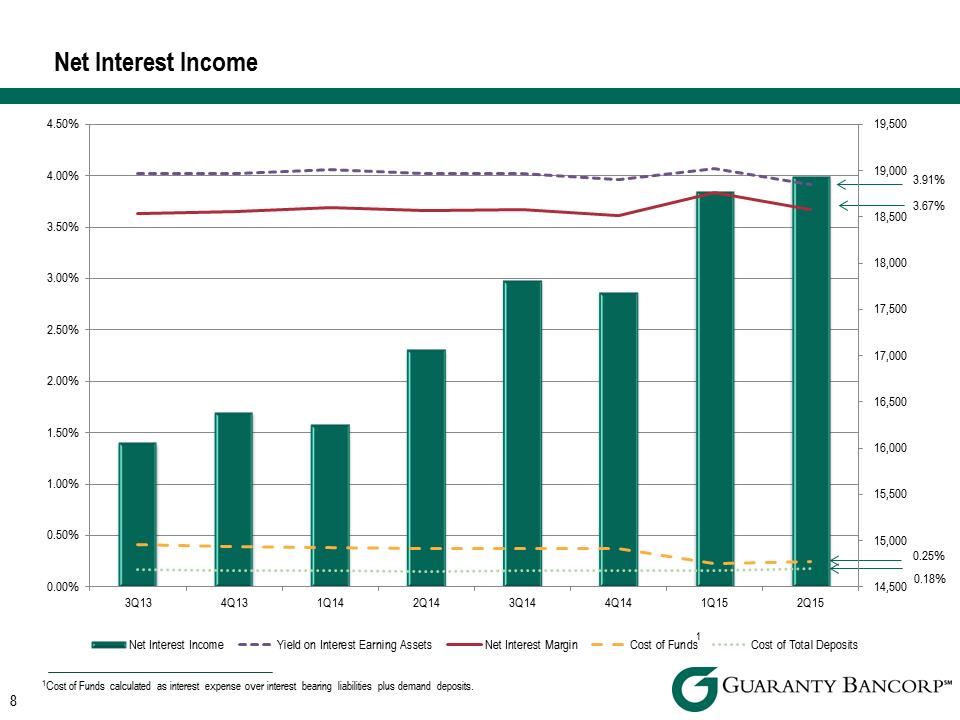

Net Interest Income 4.50% 19,500 19,000 4.00% 3.91% 3.67% 18,500 3.50% 18,000 3.00% 17,500 2.50% 17,000 2.00% 16,500 1.50% 16,000 1.00% 15,500 0.50% 15,000 0.25% 0.18% 0.00% 14,500 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 1 Net Interest Income Yield on Interest Earning Assets Net Interest Margin Cost of Funds Cost of Total Deposits 1Cost of Funds calculated as interest expense over interest bearing liabilities plus demand deposits.

Net Interest Income 4.50% 19,500 19,000 4.00% 3.91% 3.67% 18,500 3.50% 18,000 3.00% 17,500 2.50% 17,000 2.00% 16,500 1.50% 16,000 1.00% 15,500 0.50% 15,000 0.25% 0.18% 0.00% 14,500 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 1 Net Interest Income Yield on Interest Earning Assets Net Interest Margin Cost of Funds Cost of Total Deposits 1Cost of Funds calculated as interest expense over interest bearing liabilities plus demand deposits.

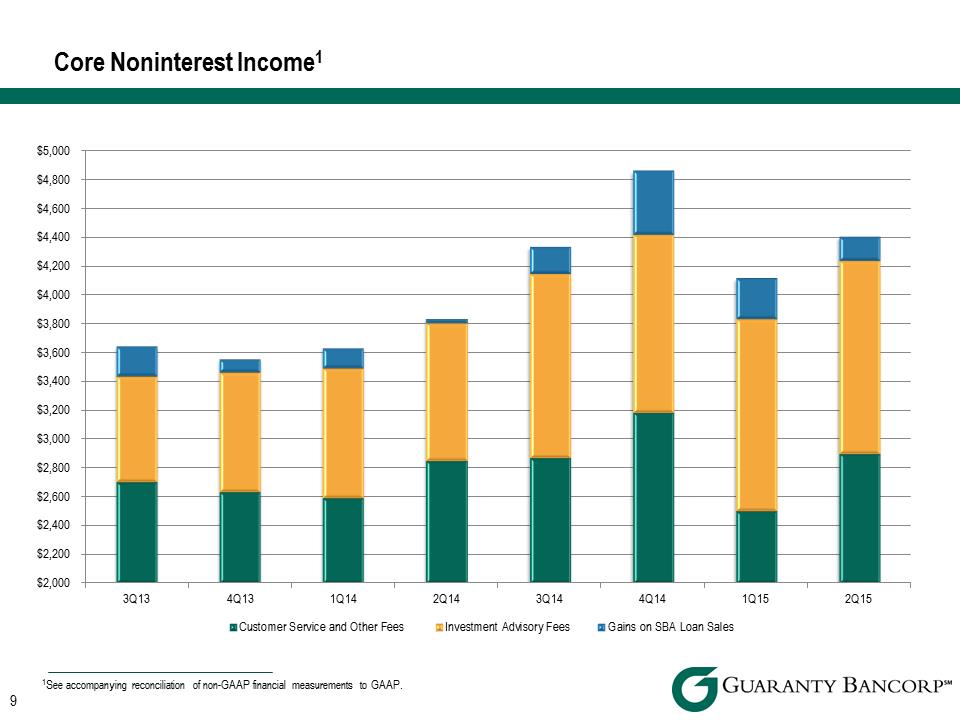

Core Noninterest Income1 $2,000$2,200$2,400$2,600$2,800$3,000$3,200$3,400$3,600$3,800$4,000$4,200$4,400$4,600$4,800$5,0003Q134Q131Q142Q143Q144Q141Q152Q15 Customer Service and Other Fees Investment Advisory Fees Gains on SBA Loan Sales 1See accompanying reconciliation of non-GAAP financial measurements to GAAP.

Core Noninterest Income1 $2,000$2,200$2,400$2,600$2,800$3,000$3,200$3,400$3,600$3,800$4,000$4,200$4,400$4,600$4,800$5,0003Q134Q131Q142Q143Q144Q141Q152Q15 Customer Service and Other Fees Investment Advisory Fees Gains on SBA Loan Sales 1See accompanying reconciliation of non-GAAP financial measurements to GAAP.

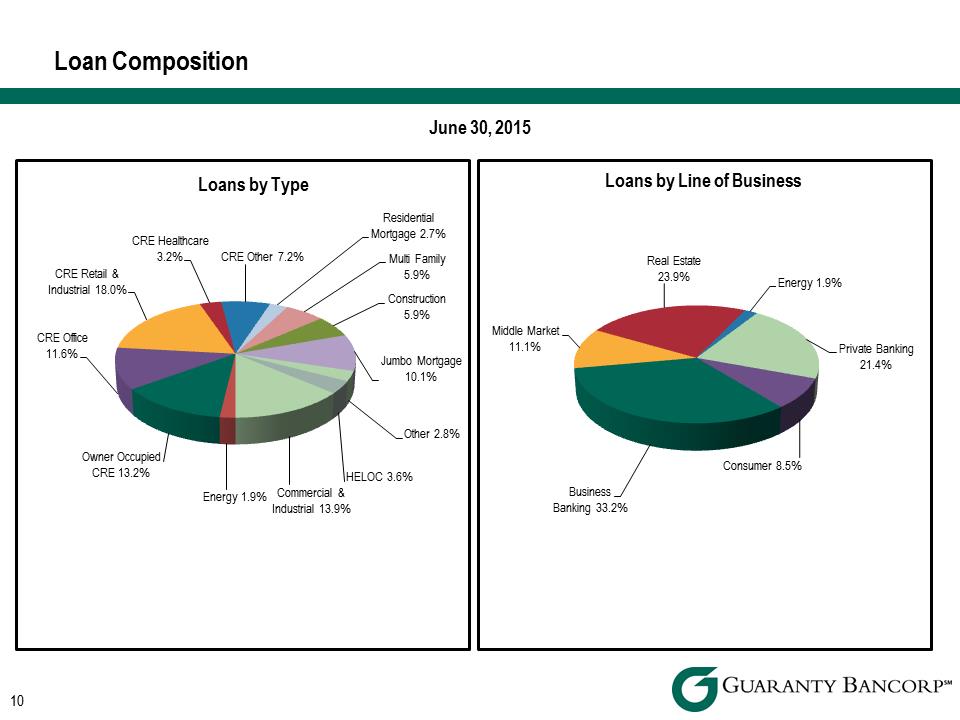

Loan Composition June 30, 2015 Loans by Line of Business Consumer 8.5% Business Banking 33.2% Middle Market 11.1%RealEstate 23.9% Energy 1.9% PrivateBanking21.4% Loans by Line of Business Commercial & Industrial 13.9% Energy1.9% OwnerOccupiedCRE13.2%CRE Office 11.6% CRE Retail & Industrial 18.0% CRE Healthcare 3.2% CRE Other 7.2% Residential Mortgage 2.7% Multi Family 5.9% Construction 5.9% Jumbo Mortgage 10.1% Other 2.8%HELOC3.6%

Loan Composition June 30, 2015 Loans by Line of Business Consumer 8.5% Business Banking 33.2% Middle Market 11.1%RealEstate 23.9% Energy 1.9% PrivateBanking21.4% Loans by Line of Business Commercial & Industrial 13.9% Energy1.9% OwnerOccupiedCRE13.2%CRE Office 11.6% CRE Retail & Industrial 18.0% CRE Healthcare 3.2% CRE Other 7.2% Residential Mortgage 2.7% Multi Family 5.9% Construction 5.9% Jumbo Mortgage 10.1% Other 2.8%HELOC3.6%

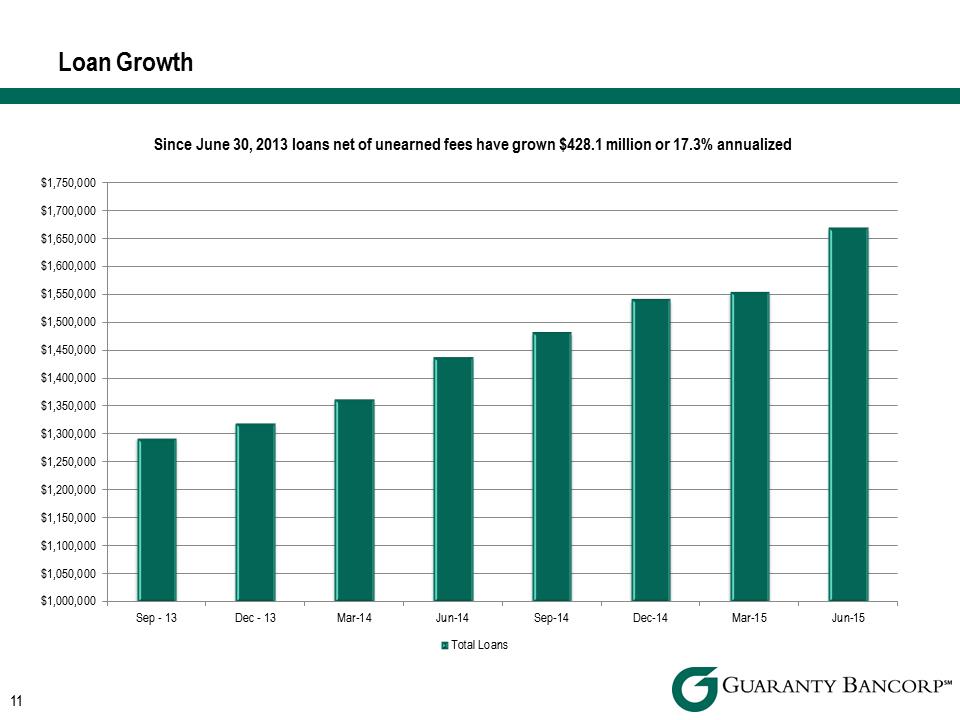

Loan Growth

Loan Growth

$1,000,000$1,050,000$1,100,000$1,150,000$1,200,000$1,250,000$1,300,000$1,350,000$1,400,000$1,450,000$1,500,000$1,550,000$1,600,000$1,650,000$1,700,000$1,750,000

Since June 30, 2013 loans net of unearned fees have grown $428.1 million or 17.3% annualized Sep -13 Dec -13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Total Loans

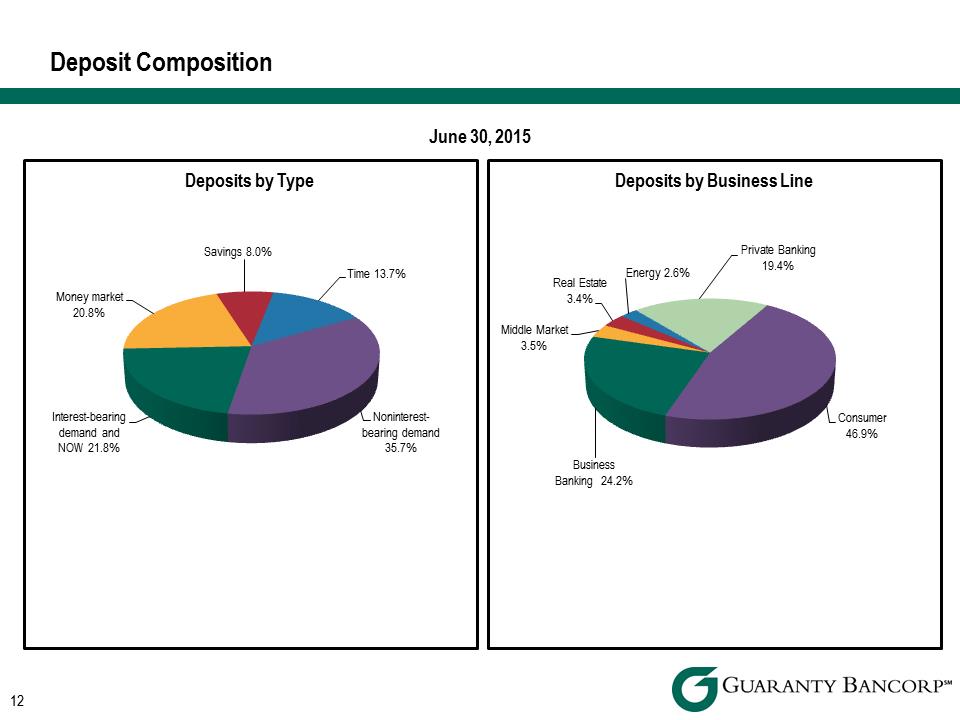

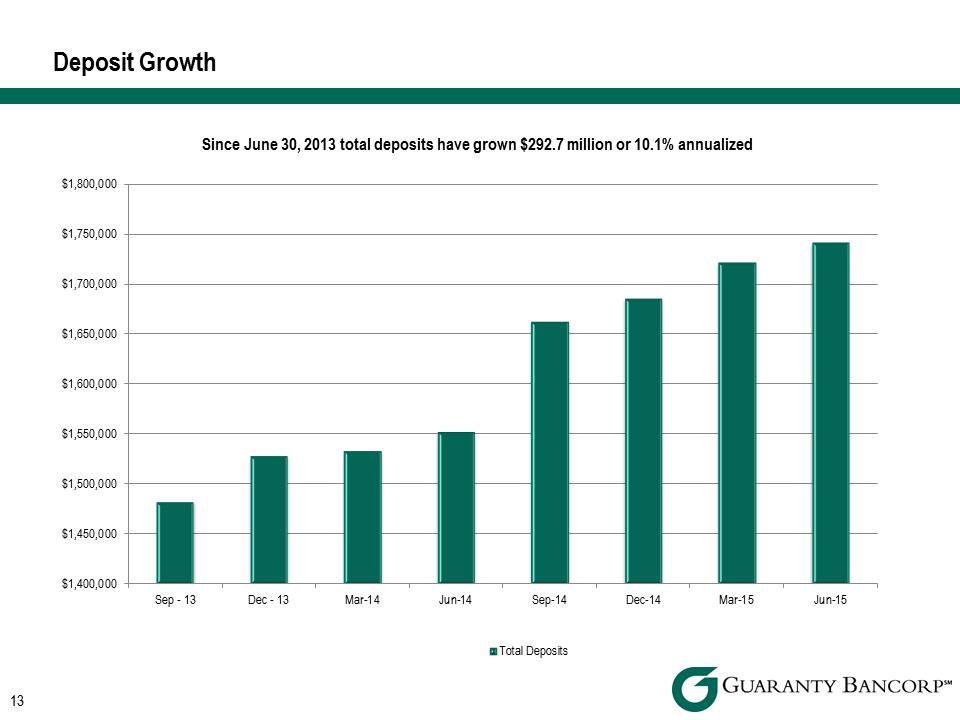

Deposit Composition June 30, 2015 Deposits by Business Line Consumer 46.9% BusinessBanking24.2% Middle Market 3.5% Real Estate 3.4% Energy 2.6% Private Banking 19.4% Deposits by Type Noninterest-bearing demand 35.7% Interest-bearing demand and NOW 21.8% Money market 20.8% Savings 8.0% Time 13.7%Deposit Growth

$1,400,000 $1,450,000 $1,500,000 $1,550,000 $1,600,000 $1,650,000 $1,700,000 $1,750,000 $1,800,000 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Since June 30, 2013 total deposits have grown $292.7 million or 10.1% annualized

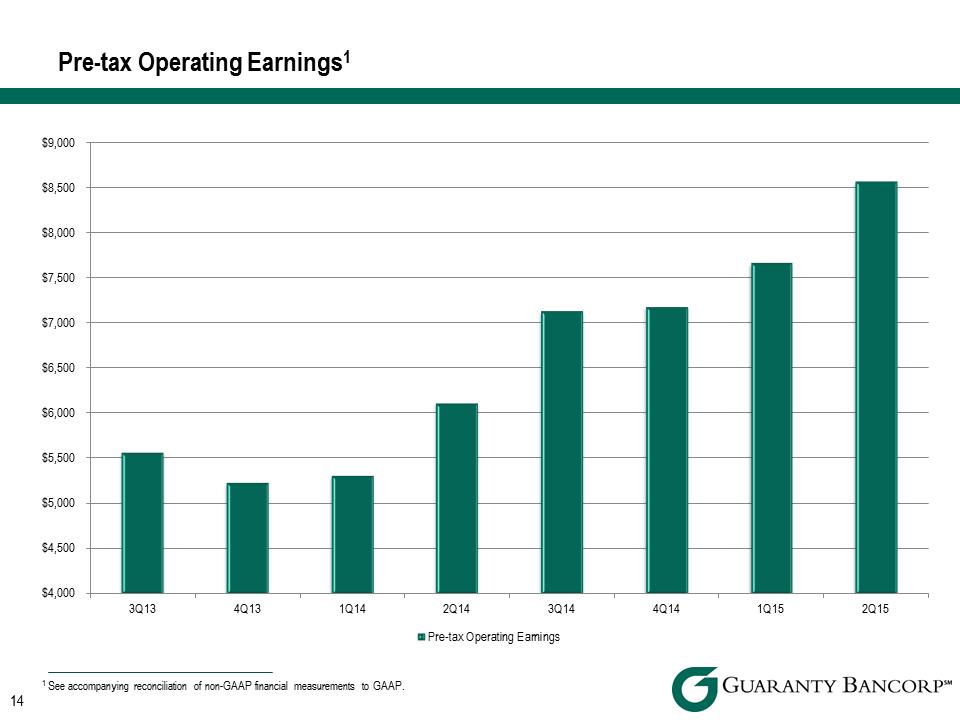

Pre-tax

Pre-tax

Pre-tax Operating Earnings 1

$4,000 $4,500 $5,000 $5,500 $6,000 $6,500 $7,000 $7,500 $8,000 $8,500 $9,000 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 1See accompanying reconciliation of non-GAAP financial measurements to GAAP.

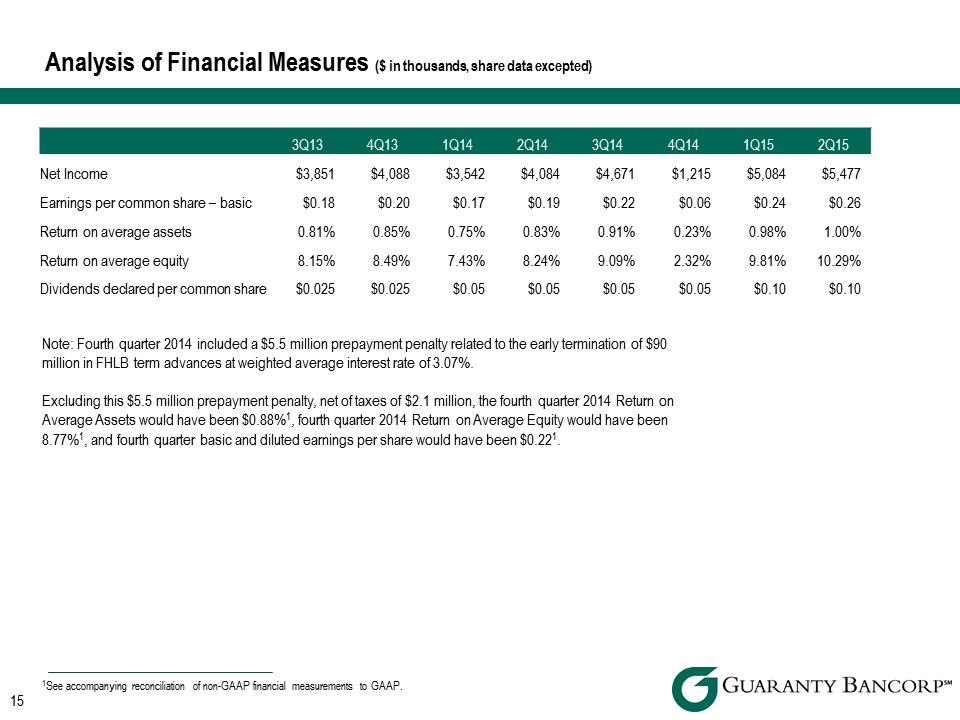

Analysis of Financial Measures ($ in thousands, share data excepted)

Analysis of Financial Measures ($ in thousands, share data excepted)

3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

Net Income $3,851 $4,088 $3,542 $4,084 $4,671 $1,215 $5,084 $5,477 Earnings per common share – basic Return on average assets Return on average equity Dividends declared per common share $0.18 0.81% 8.15% $0.025 $0.20 0.85% 8.49% $0.025 $0.17 0.75% 7.43% $0.05 $0.19 0.83% 8.24% $0.05 $0.22 0.91% 9.09% $0.05 $0.06 0.23% 2.32% $0.05 $0.24 0.98% 9.81% $0.10 $0.26 1.00% 10.29% $0.10 Note: Fourth quarter 2014 included a $5.5 million prepayment penalty related to the early termination of $90 million in FHLB term advances at weighted average interest rate of 3.07%. Excluding this $5.5 million prepayment penalty, net of taxes of $2.1 million, the fourth quarter 2014 Return on Average Assets would have been $0.88%1, fourth quarter 2014 Return on Average Equity would have been 8.77%1, and fourth quarter basic and diluted earnings per share would have been $0.22 1See accompanying reconciliation of non-GAAP financial measurements to GAAP.

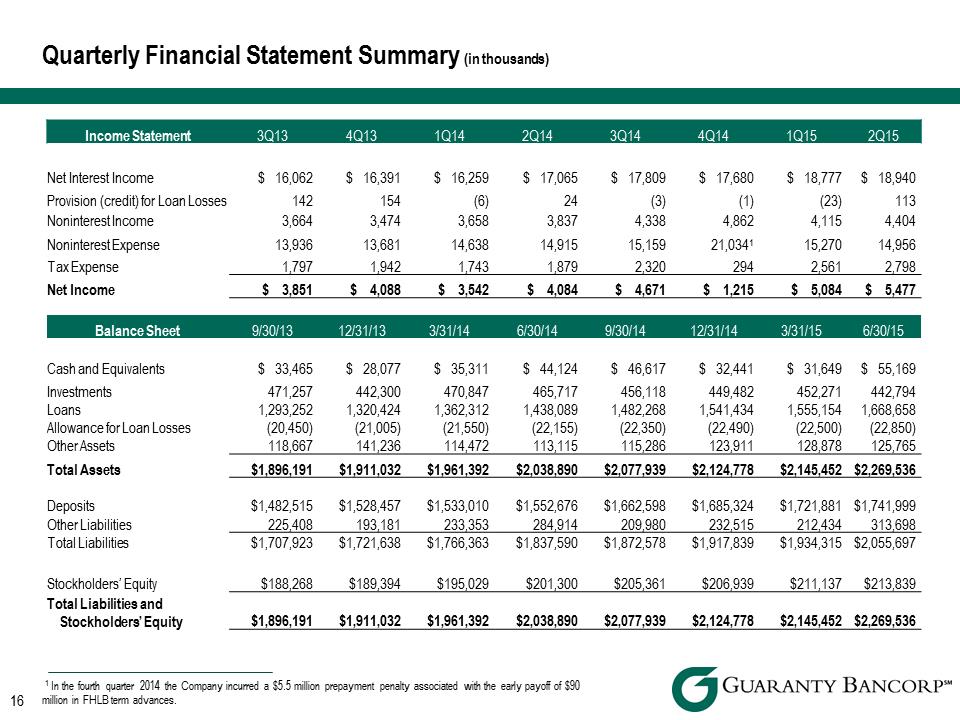

Quarterly Financial Statement Summary (in thousands)

Income Statement 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 Net Interest Income$16,062 $16,391 $16,259 $17,065 $17,809 $17,680 $18,777 $18,940 Provision (credit) for Loan Losses 142 154 (6) 24 (3) (1) (23) 113 Noninterest Income 3,664 3,474 3,658 3,837 4,338 4,862 4,115 4,404 Noninterest Expense 13,936 13,681 14,638 14,915 15,159 21,0341 15,270 14,956 Tax Expense 1,797 1,942 1,743 1,879 2,320 294 2,561 2,798 Net Income $ 3,851 $ 4,088 $ 3,542 $ 4,084 $ 4,671 $ 1,215 $ 5,084 $ 5,477

Balance Sheet 9/30/13 12/31/13 3/31/14 6/30/14 9/30/14 12/31/14 3/31/15 6/30/15 Cash and Equivalents $ 33,465 $28,077 $35,311 $44,124 $46,617 $32,441 $31,649 $55,169 Investments 471,257 442,300 470,847 465,717 456,118 449,482 452,271 442,794 Loans 1,293,252 1,320,424 1,362,312 1,438,089 1,482,268 1,541,434 1,555,154 1,668,658 Allowance for Loan Losses (20,450) (21,005) (21,550) (22,155) (22,350) (22,490) (22,500) (22,850) Other Assets 118,667 141,236 114,472 113,115 115,286 123,911 128,878 125,765 Total Assets $1,896,191 $1,911,032 $1,961,392 $2,038,890 $2,077,939 $2,124,778 $2,145,452 $2,269,536 Deposits $1,482,515 $1,528,457 $1,533,010 $1,552,676 $1,662,598 $1,685,324 $1,721,881 $1,741,999 Other Liabilities 225,408 193,181 233,353 284,914 209,980 232,515 212,434 313,698 Total Liabilities $1,707,923 $1,721,638 $1,766,363 $1,837,590 $1,872,578 $1,917,839 $1,934,315 $2,055,697 Stockholders’ Equity $188,268 $189,394 $195,029 $201,300 $205,361 $206,939 $211,137 $213,839 Total Liabilities and Stockholders’ Equity $1,896,191 $1,911,032 $1,961,392 $2,038,890 $2,077,939 $2,124,778

$2,145,452 $2,269,536 1 In the fourth quarter 2014 the Company incurred a $5.5 million prepayment penalty associated with the early payoff of $90 million in FHLB term advances. Colorado Market

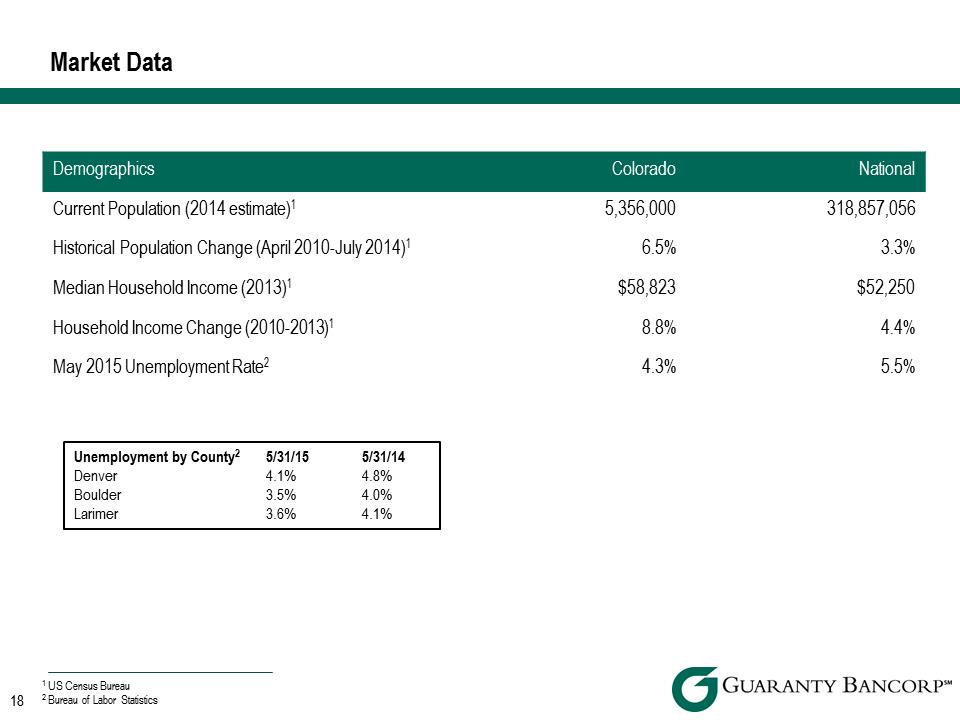

Market Data

Market Data

|

§ |

Demographics Colorado National Current Population (2014 estimate)1 5,356,000 318,857,056 Historical Population Change (April 2010-July 2014)1 6.5% 3.3% Median Household Income (2013)1 $58,823 $52,250 Household Income Change (2010-2013)1 8.8% 4.4% May 2015 Unemployment Rate2 4.3% 5.5% Unemployment by County2 5/31/15 5/31/14 Denver 4.1% 4.8% Boulder 3.5% 4.0% Larimer 3.6% 4.1% 1 US Census Bureau 2 Bureau of Labor Statistics |

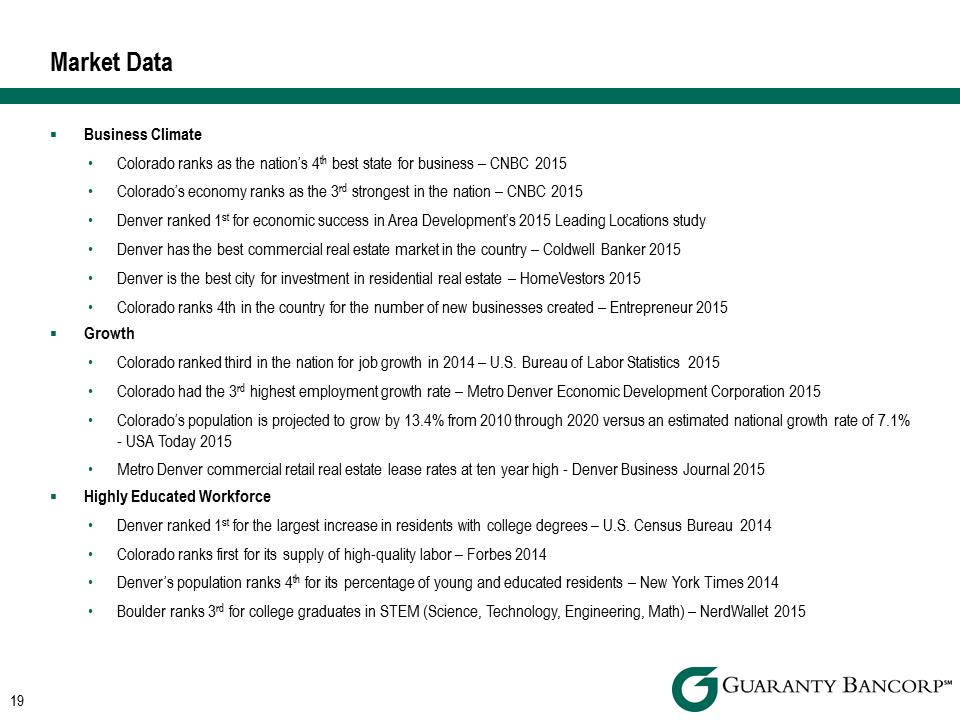

Market Data

Market Data

|

§ |

Business Climate |

|

" |

Colorado ranks as the nation’s 4th best state for business – CNBC 2015 |

|

" |

Colorado’s economy ranks as the 3rd strongest in the nation – CNBC 2015 |

|

" |

Denver ranked 1st for economic success in Area Development’s 2015 Leading Locations study |

|

" |

Denver has the best commercial real estate market in the country – Coldwell Banker 2015 |

|

" |

Denver is the best city for investment in residential real estate – HomeVestors 2015 |

|

" |

Colorado ranks 4th in the country for the number of new businesses created – Entrepreneur 2015 |

|

§ |

Growth |

|

" |

Colorado ranked third in the nation for job growth in 2014 – U.S. Bureau of Labor Statistics 2015 |

|

" |

Colorado had the 3rd highest employment growth rate – Metro Denver Economic Development Corporation 2015 |

|

" |

Colorado’s population is projected to grow by 13.4% from 2010 through 2020 versus an estimated national growth rate of 7.1% - USA Today 2015 |

|

" |

Metro Denver commercial retail real estate lease rates at ten year high - Denver Business Journal 2015 |

|

" |

Highly Educated Workforce |

|

" |

Denver ranked 1st for the largest increase in residents with college degrees – U.S. Census Bureau 2014 |

|

" |

Colorado ranks first for its supply of high-quality labor – Forbes 2014 |

|

" |

Denver’s population ranks 4th for its percentage of young and educated residents – New York Times 2014 |

|

" |

Boulder ranks 3rd for college graduates in STEM (Science, Technology, Engineering, Math) – NerdWallet 2015 |

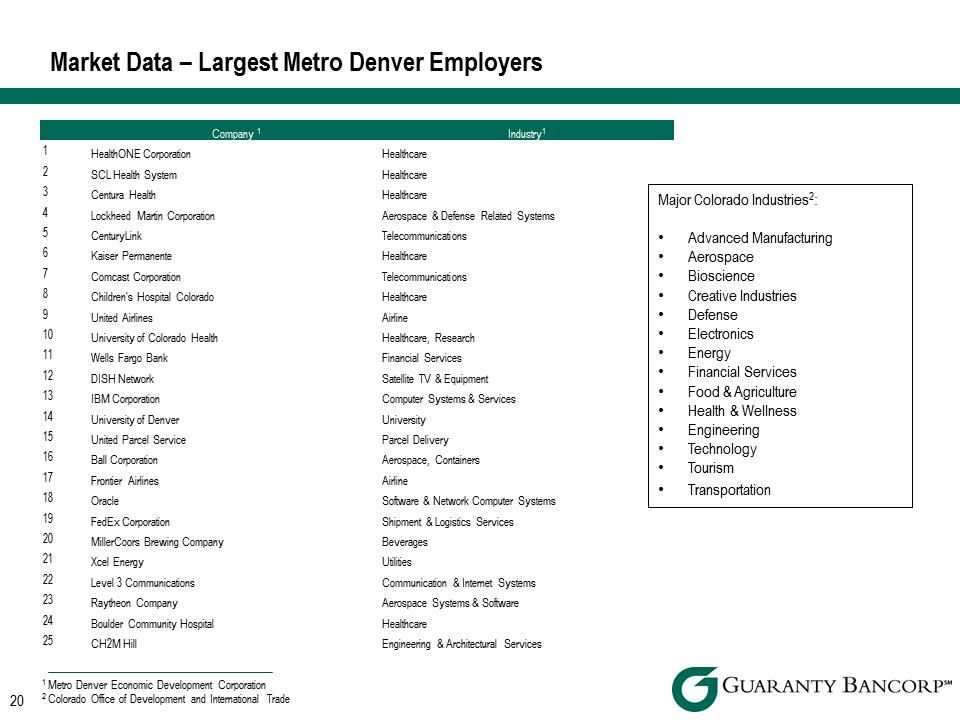

Market Data – Largest Metro Denver Employ

Market Data – Largest Metro Denver Employ

|

|

Company1 |

Industry1 |

|

1 |

HealthONE Corporation |

Healthcare |

|

2 |

SCL Health System |

Healthcare |

|

3 |

Centura Health |

Healthcare |

|

4 |

Lockheed Martin Corporation |

Aerospace & Defense Related Systems |

|

5 |

CenturyLink |

Telecommunications |

|

6 |

Kaiser Permanente |

Healthcare |

|

7 |

Comcast Corporation |

Telecommunications |

|

8 |

Children's Hospital Colorado |

Healthcare |

|

9 |

United Airlines |

Airline |

|

10 |

University of Colorado Health |

Healthcare, Research |

|

11 |

Wells Fargo Bank |

Financial Services |

|

12 |

DISH Network |

Satellite TV & Equipment |

|

13 |

IBM Corporation |

Computer Systems & Services |

|

14 |

University of Denver |

University |

|

15 |

United Parcel Service |

Parcel Delivery |

|

16 |

Ball Corporation |

Aerospace, Containers |

|

17 |

Frontier Airlines |

Airline |

|

18 |

Oracle |

Software & Network Computer Systems |

|

19 |

FedEx Corporation |

Shipment & Logistics Services |

|

20 |

MillerCoors Brewing Company |

Beverages |

|

21 |

Xcel Energy |

Utilities |

|

22 |

Level 3 Communications |

Communication & Internet Systems |

|

23 |

Raytheon Company |

Aerospace Systems & Software |

|

24 |

Boulder Community Hospital |

Healthcare |

|

25 |

CH2M Hill |

Engineering & Architectural Services |

|

Major Colorado Industries2: " Advanced Manufacturing" Aerospace" Bioscience" Creative Industries" Defense" Electronics" Energy" Financial Services" Food & Agriculture" Health & Wellness" Engineering" Technology" Tourism" Transportation

|

|

|

|

1 Metro Denver Economic Development Corporation 2 Colorado Office of Development and International Trade

|

|

|

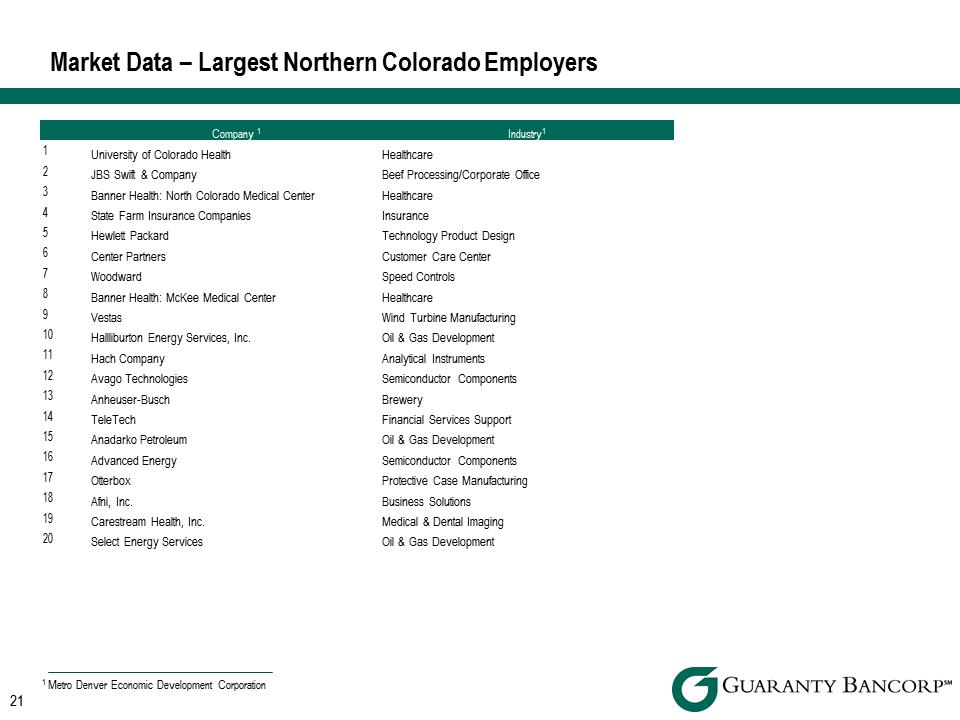

Market Data – Largest Northern Colorado Employers

Market Data – Largest Northern Colorado Employers

Company1 Industry1 1University of Colorado Health Healthcare 2JBS Swift & Company Beef Processing/Corporate Office 3Banner Health: North Colorado Medical Center Healthcare 4State Farm Insurance Companies Insurance 5Hewlett Packard Technology Product Design 6Center Partners Customer Care Center 7Woodward Speed Controls 8 Banner Health: McKee Medical Center Healthcare 9Vestas Wind Turbine Manufacturing 10Hallliburton Energy Services, Inc. Oil & Gas Development 11Hach Company Analytical Instruments 12Avago Technologies Semiconductor Components 13Anheuser-Busch Brewery 14TeleTech Financial Services Support 15Anadarko Petroleum Oil & Gas Development 16Advanced Energy Semiconductor Components 17Otterbox Protective Case Manufacturing 18Afni, Inc. Business Solutions 19Carestream Health, Inc. Medical & Dental Imaging 20 Select Energy Services Oil & Gas Development

1Metro Denver Economic Development Corporation

Reconciliation of Non-GAAP Financial Measures

Reconciliation of Non-GAAP Financial Measures

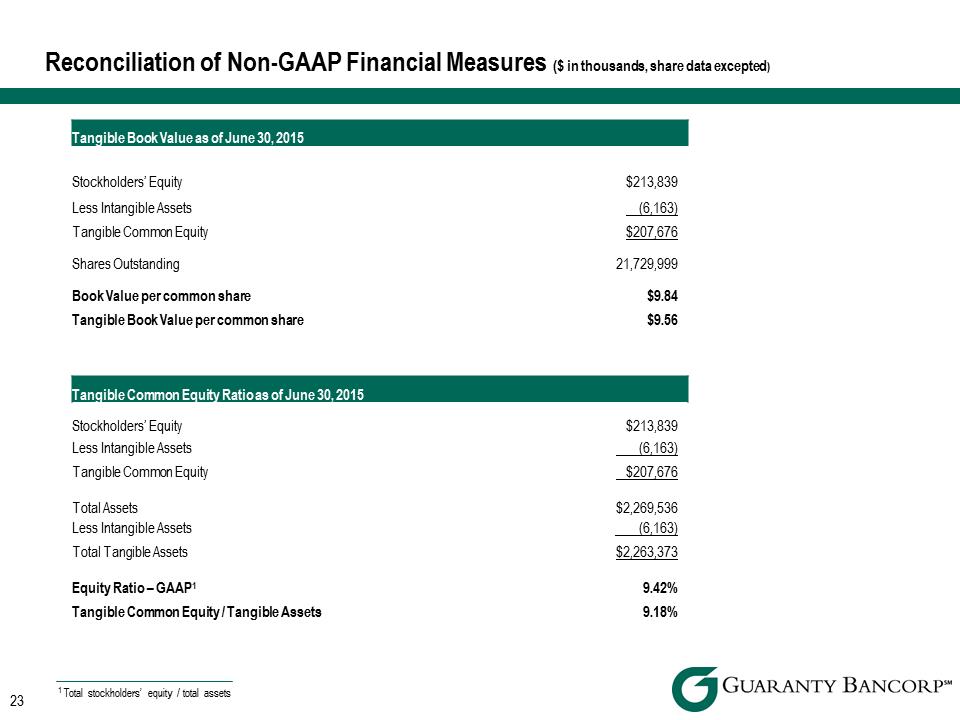

Reconciliation of Non-GAAP Financial Measures ($ in thousands, share data excepted) Tangible Book Value as of June 30,2015 Stockholders’ Equity $213,839 Less Intangible Assets (6,163) Tangible Common Equity $207,676 Shares Outstanding 21,729,999 Book Value per common share $9.84 Tangible Book Value per common share $9.56 Tangible Common Equity Ratio as of June 30, 2015 Stockholders’ Equity $213,839 Less Intangible Assets (6,163) Tangible Common Equity $207,676 Total Assets $2,269,536 Less Intangible Assets (6,163) Total Tangible Assets $2,263,373 Equity Ratio – GAAP1 9.42% Tangible Common Equity / Tangible Assets 9.18% 1 Total stockholders’ equity / total assets

Reconciliation of Non-GAAP Financial Measures ($ in thousands, share data excepted) Tangible Book Value as of June 30,2015 Stockholders’ Equity $213,839 Less Intangible Assets (6,163) Tangible Common Equity $207,676 Shares Outstanding 21,729,999 Book Value per common share $9.84 Tangible Book Value per common share $9.56 Tangible Common Equity Ratio as of June 30, 2015 Stockholders’ Equity $213,839 Less Intangible Assets (6,163) Tangible Common Equity $207,676 Total Assets $2,269,536 Less Intangible Assets (6,163) Total Tangible Assets $2,263,373 Equity Ratio – GAAP1 9.42% Tangible Common Equity / Tangible Assets 9.18% 1 Total stockholders’ equity / total assets

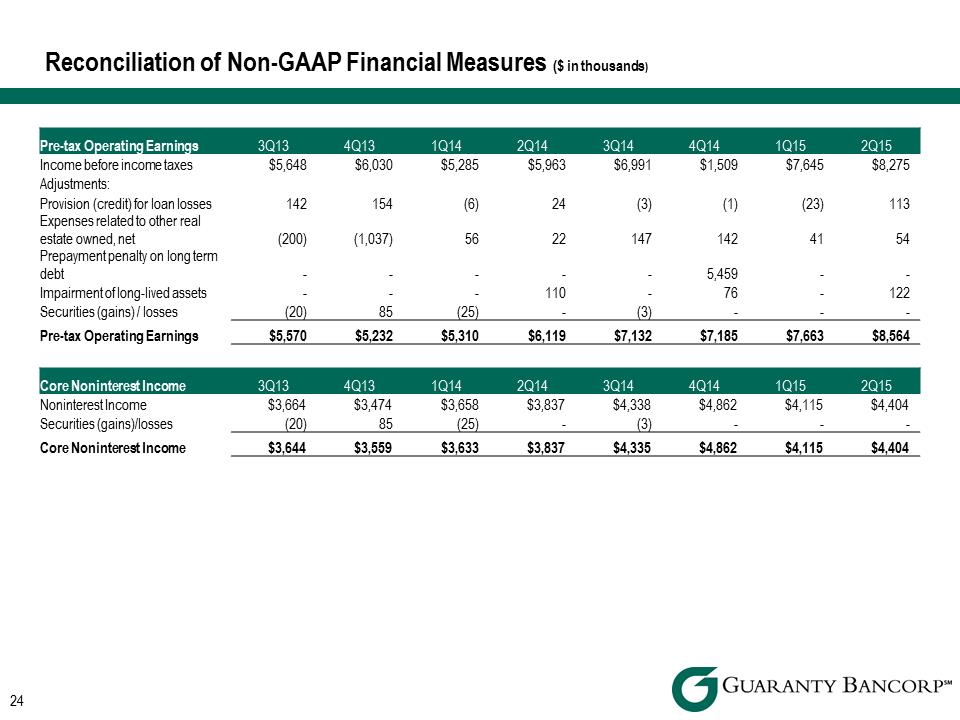

Reconciliation of Non-GAAP Financial Measures ($ in thousands) Pre tax Operating Earnings 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 Income before income taxes $5,648 $6,030 $5,285 $5,963 $6,991 $1,509 $7,645 $8,275 Adjustments: Provision (credit) for loan losses 142 154 (6) 24 (3) (1) (23) 113 Expenses related to other real estate owned, net (200) (1,037) 56 2 147 142 41 54 Prepayment penalty on long term debt -----5,459 --Impairment of long-lived assets ---110 -76 -122 Securities (gains) / losses (20) 85 (25) -(3) ---Pre-tax Operating Earnings $5,570 $5,232 $5,310 6,119 $7,132 $7,185 $7,663 $8,564 Noninterest Income $3,664 $3,474 $3,658 $3,837 $4,338 $4,862 $4,115 $4,404 Securities (gains)/losses (20) 85 (25) -(3) ---Core Noninterest Income $3,644$3,559 $3,633 $3,837 $4,335 $4,862 $4,115 $4,404 Core Noninterest Income 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

Reconciliation of Non-GAAP Financial Measures ($ in thousands) Pre tax Operating Earnings 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 Income before income taxes $5,648 $6,030 $5,285 $5,963 $6,991 $1,509 $7,645 $8,275 Adjustments: Provision (credit) for loan losses 142 154 (6) 24 (3) (1) (23) 113 Expenses related to other real estate owned, net (200) (1,037) 56 2 147 142 41 54 Prepayment penalty on long term debt -----5,459 --Impairment of long-lived assets ---110 -76 -122 Securities (gains) / losses (20) 85 (25) -(3) ---Pre-tax Operating Earnings $5,570 $5,232 $5,310 6,119 $7,132 $7,185 $7,663 $8,564 Noninterest Income $3,664 $3,474 $3,658 $3,837 $4,338 $4,862 $4,115 $4,404 Securities (gains)/losses (20) 85 (25) -(3) ---Core Noninterest Income $3,644$3,559 $3,633 $3,837 $4,335 $4,862 $4,115 $4,404 Core Noninterest Income 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

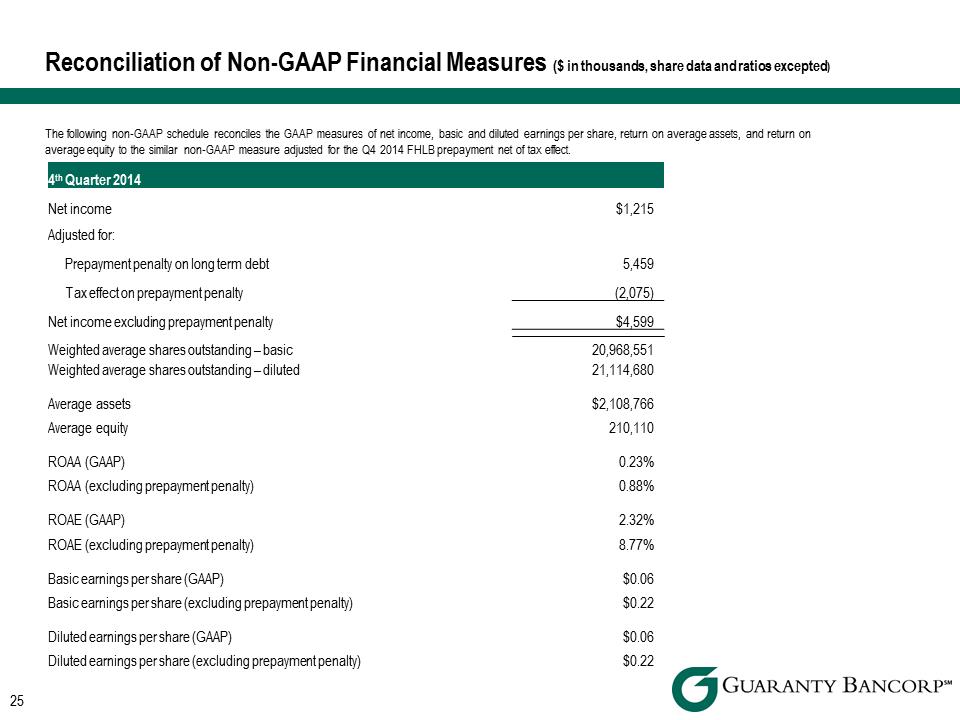

Reconciliation of Non-GAAP Financial Measures ($ in thousands, share data and ratios excepted) The following non-GAAP schedule reconciles the GAAP measures of net income, basic and diluted earnings per share, return on average assets, and return on average equity to the similar non-GAAP measure adjusted for the Q4 2014 FHLB prepayment net of tax effect. 4th Quarter 2014 Net income Adjusted for: $1,215 Prepayment penalty on long term debt 5,459 Tax effect on prepayment penalty (2,075) Net income excluding prepayment penalty $4,599 Weighted average shares outstanding – basic Weighted average shares outstanding – diluted 20,968,551 21,114,680 Average assets Average equity $2,108,766 210,110 ROAA (GAAP) ROAA (excluding prepayment penalty) 0.23% 0.88% ROAE (GAAP) ROAE (excluding prepayment penalty) 2.32% 8.77% Basic earnings per share (GAAP) Basic earnings per share (excluding prepayment penalty) $0.06 $0.22 Diluted earnings per share (GAAP) Diluted earnings per share (excluding prepayment penalty) $0.06 $0.22

Reconciliation of Non-GAAP Financial Measures ($ in thousands, share data and ratios excepted) The following non-GAAP schedule reconciles the GAAP measures of net income, basic and diluted earnings per share, return on average assets, and return on average equity to the similar non-GAAP measure adjusted for the Q4 2014 FHLB prepayment net of tax effect. 4th Quarter 2014 Net income Adjusted for: $1,215 Prepayment penalty on long term debt 5,459 Tax effect on prepayment penalty (2,075) Net income excluding prepayment penalty $4,599 Weighted average shares outstanding – basic Weighted average shares outstanding – diluted 20,968,551 21,114,680 Average assets Average equity $2,108,766 210,110 ROAA (GAAP) ROAA (excluding prepayment penalty) 0.23% 0.88% ROAE (GAAP) ROAE (excluding prepayment penalty) 2.32% 8.77% Basic earnings per share (GAAP) Basic earnings per share (excluding prepayment penalty) $0.06 $0.22 Diluted earnings per share (GAAP) Diluted earnings per share (excluding prepayment penalty) $0.06 $0.22