Attached files

| file | filename |

|---|---|

| 8-K - 8-K - HERCULES OFFSHORE, INC. | d55204d8k.htm |

| EX-99.2 - EX-99.2 - HERCULES OFFSHORE, INC. | d55204dex992.htm |

Exhibit 99.1

THIS IS A SOLICITATION OF VOTES TO ACCEPT OR REJECT A JOINT PREPACKAGED CHAPTER 11 PLAN OF REORGANIZATION OF HERCULES OFFSHORE, INC. AND ITS DEBTOR AFFILIATES. HERCULES OFFSHORE, INC. AND THE COMPANIES LISTED BELOW HAVE NOT FILED FOR RELIEF UNDER CHAPTER 11 OF THE BANKRUPTCY CODE, AND THIS DISCLOSURE STATEMENT HAS NOT BEEN FILED WITH OR APPROVED BY THE BANKRUPTCY COURT OR THE SECURITIES AND EXCHANGE COMMISSION. IN THE EVENT THAT THESE COMPANIES FILE PETITIONS FOR RELIEF UNDER CHAPTER 11 OF THE BANKRUPTCY CODE AND SEEK CONFIRMATION OF THE JOINT PREPACKAGED PLAN OF REORGANIZATION DESCRIBED HEREIN, THIS DISCLOSURE STATEMENT WILL BE SUBMITTED TO THE BANKRUPTCY COURT FOR APPROVAL.

SOLICITATION AND DISCLOSURE STATEMENT FOR THE

JOINT PREPACKAGED CHAPTER 11 PLAN OF REORGANIZATION OF

HERCULES OFFSHORE, INC., et al.,1

From Holders of 7.375% Senior Notes due March 1, 2018 (CUSIP Nos. 74912EAH4 / US74912EAH45);

10.250% Senior Notes due April 1, 2019 (CUSIP Nos. 427093AE9 / U42714AB8);

8.75% Senior Notes due July 15, 2021 (CUSIP Nos. 427093AG4 / U42714AD4);

7.50% Senior Notes due October 1, 2021 (CUSIP Nos. 427093AH2 / U42714AE2);

6.75% Senior Notes due April 1, 2022 (CUSIP Nos. 427093AJ8 / U42714AF9); and

3.375% Convertible Senior Notes due 2038 (CUSIP Nos. 427093AD1 / US427093AD16)

THE DEADLINE TO ACCEPT OR REJECT THE PLAN IS 5:00 P.M., PREVAILING EASTERN TIME, ON AUGUST 12, 2015, UNLESS EXTENDED.

FOR YOUR VOTE TO BE COUNTED, YOUR BALLOT MUST BE ACTUALLY RECEIVED BY PRIME CLERK, THE VOTING AND CLAIMS AGENT, BEFORE THE VOTING DEADLINE AS DESCRIBED HEREIN. HOLDERS OF SENIOR NOTES CLAIMS SHOULD REFER TO THE BALLOTS ENCLOSED FOR INSTRUCTIONS ON HOW TO VOTE ON THE PLAN OF REORGANIZATION. PLEASE NOTE THAT THE DESCRIPTION OF THE PLAN PROVIDED THROUGHOUT THIS DISCLOSURE STATEMENT IS ONLY A SUMMARY PROVIDED FOR CONVENIENCE. IN THE CASE OF ANY INCONSISTENCY BETWEEN THE SUMMARY OF THE PLAN IN THIS DISCLOSURE STATEMENT AND THE PLAN, THE PLAN WILL GOVERN.2

The Debtors hereby solicit from Holders of 7.375% Senior Notes due March 1, 2018; 10.250% Senior Notes due April 1, 2019; 8.75% Senior Notes due July 15, 2021; 7.50% Senior Notes due October 1, 2021; 6.75% Senior Notes due April 1, 2022; and 3.375% Convertible Senior Notes due 2038, votes to accept or reject the Debtors’ Plan under chapter 11 of the Bankruptcy Code. A copy of the Plan is attached hereto as Exhibit A.

| 1 | The debtors in the chapter 11 cases, along with the last four digits of each Debtors’ federal tax identification number, are: Cliffs Drilling Company (8934); Cliffs Drilling Trinidad L.L.C. (5205); FDT LLC (7581); FDT Holdings LLC (4277); Hercules Drilling Company, LLC (2771); Hercules Liftboat Company LLC (0791); Hercules Offshore, Inc. (2838); Hercules Offshore Services LLC (1670); Hercules Offshore Liftboat Company LLC (5303); HERO Holdings, Inc. (5475); SD Drilling LLC (8190); THE Offshore Drilling Company (4465); THE Onshore Drilling Company (1072); TODCO Americas Inc. (0289); and TODCO International Inc. (6326) (collectively, the “Debtors”). |

| 2 | Capitalized terms used but not otherwise defined in this Disclosure Statement will have the meanings set forth in the Plan. |

| Emanuel C. Grillo (pro hac vice pending) Christopher Newcomb (pro hac vice pending) BAKER BOTTS LLP 30 Rockefeller Plaza New York, New York 10112 (212) 892-4000

- and –

James Prince II (pro hac vice pending) C. Luckey McDowell (pro hac vice pending) Meggie S. Gilstrap (pro hac vice pending) BAKER BOTTS LLP 2001 Ross Avenue Dallas, Texas 75201 (214) 953-6500

Proposed Co-Counsel to Debtors and Debtors in Possession |

Robert J. Dehney Matthew B. Harvey Tamara K. Minott MORRIS, NICHOLS, ARSHT & TUNNELL LLP 1201 N. Market Street, 16th Floor Wilmington, Delaware 19801 (302) 658-9200

Proposed Co-Counsel to Debtors and Debtors in Possession |

Dated: July 13, 2015

NOTICE TO EMPLOYEES, TRADE CREDITORS,

AND OTHER HOLDERS OF GENERAL UNSECURED CLAIMS

THE DEBTORS INTEND TO CONTINUE OPERATING THEIR BUSINESSES IN CHAPTER 11 IN THE ORDINARY COURSE OF BUSINESS AND TO SEEK TO OBTAIN THE NECESSARY RELIEF FROM THE COURT TO HONOR ITS OBLIGATIONS AND PAY ITS EMPLOYEES, TRADE CREDITORS, AND OTHER GENERAL UNSECURED CLAIMS IN FULL AND IN ACCORDANCE WITH EXISTING BUSINESS TERMS.

DISCLAIMER

IMPORTANT INFORMATION FOR YOU TO READ

THE DEADLINE TO VOTE ON THE JOINT PREPACKAGED CHAPTER 11 PLAN OF HERCULES OFFSHORE, INC., ET AL. IS AUGUST 12, 2015 AT 5:00 P.M. PREVAILING EASTERN TIME.

FOR YOUR VOTE TO BE COUNTED, YOUR BALLOT MUST BE ACTUALLY RECEIVED BY THE VOTING AND CLAIMS AGENT BEFORE THE VOTING DEADLINE AS DESCRIBED HEREIN.

The information contained in this disclosure statement including the Exhibits annexed hereto (collectively, the “Disclosure Statement”) is included herein for purposes of soliciting acceptances of the Joint Prepackaged Chapter 11 Plan of Reorganization of Hercules Offshore, Inc. and its Debtor Affiliates (the “Plan”) and may not be relied upon for any purpose other than to determine how to vote on the Plan. The Bankruptcy Court has not approved the adequacy of the disclosure contained in this Disclosure Statement or the merits of the Plan. No person is authorized by the Debtors in connection with the Plan or the solicitation of acceptances of the Plan to give any information or to make any representation regarding this Disclosure Statement or the Plan other than as contained in this Disclosure Statement and the Exhibits annexed hereto, incorporated by reference or referred to herein, and if given or made, such information or representation may not be relied upon as having been authorized by the Debtors.

The Disclosure Statement shall not be construed to be advice on the tax, securities, financial, business, or other legal effects of the Plan as to holders of Claims against, or Equity Interests in, the Debtors, the Reorganized Debtors, or any other person. Each holder should consult with its own legal, business, financial, and tax advisors with respect to any matters concerning this Disclosure Statement, the solicitation of votes to accept the Plan, the Plan, and the transactions contemplated hereby and thereby.

The Debtors urge the holders of Senior Notes Claims in Class 3, the only Class of Claims entitled to vote on the Plan, to (1) read the entire Disclosure Statement and Plan carefully; (2) consider all of the information in this Disclosure Statement, including, importantly, the risk factors described in Article XI of this Disclosure Statement; and (3) consult with your own advisors with respect to reviewing this Disclosure Statement, the Plan, and all documents that are attached to the Plan and Disclosure Statement before deciding whether to vote to accept or reject the Plan. Plan summaries and statements made in this Disclosure Statement are qualified in their entirety by reference to the Plan and the Exhibits annexed to the Plan and this Disclosure Statement. Please be advised, however, that the statements contained in this Disclosure Statement are made as of the date hereof unless another time is specified herein, and holders of Claims reviewing this Disclosure Statement should not infer at the time of such review that there has not been any change in the information set forth herein since the date hereof unless so specified. In the event of any conflict between the descriptions set forth in this Disclosure Statement and the terms of the Plan, the terms of the Plan shall govern.

See the Risk Factors in Article XI of the Disclosure Statement for certain risks that you should carefully consider.

The financial information contained in or incorporated by reference into this Disclosure Statement has not been audited, except as specifically indicated otherwise. The Debtors’ management, in consultation with

i

their advisors, has prepared the Financial Projections (as defined below) attached hereto as Exhibit D and described in this Disclosure Statement. The Debtors’ management did not prepare the projections in accordance with Generally Accepted Accounting Principles (“GAAP”) or International Financial Reporting Standards (“IFRS”) or to comply with the rules and regulations of the SEC or any foreign regulatory authority. The financial projections, while presented with numerical specificity, necessarily were based on a variety of estimates and assumptions that are inherently uncertain and may be beyond the control of the Debtors’ management. Important factors that may affect actual results and cause the management forecasts not to be achieved include, but are not limited to, risks and uncertainties relating to the Debtors’ businesses (including their ability to achieve strategic goals, objectives, and targets over applicable periods), industry performance, the regulatory environment, general business and economic conditions and other factors. The Debtors caution that no representations can be made as to the accuracy of these projections or to their ultimate performance compared to the information contained in the forecasts or that the forecasted results will be achieved. Therefore, the financial projections may not be relied upon as a guarantee or other assurance that the actual results will occur.

As to contested matters, existing litigation involving, or possible litigation to be brought by, or against, the Debtors, adversary proceedings, and other actions or threatened actions, this Disclosure Statement and Plan shall not constitute, or be construed as, an admission of any fact or liability, a stipulation, or a waiver, but rather as a statement made without prejudice solely for settlement purposes in accordance with Federal Rule of Evidence 408, with full reservation of rights, and is not to be used for any litigation purpose whatsoever by any person, party, or entity.

The Board of Directors (or equivalent thereof, as applicable) of each of the Debtors has approved the Plan and recommends that the holders of Senior Notes Claims (Class 3) vote to accept the Plan. The Plan has been negotiated with, and has the support of, the Steering Group, an ad hoc group of holders of Senior Notes that together hold in excess of 66 2/3% of the aggregate principal amount of the Senior Notes. This Disclosure Statement, the Plan, and the accompanying documents have been extensively negotiated with the legal and/or financial advisors to the Steering Group. The votes on the Plan are being solicited in accordance with the Restructuring Support Agreement dated as of June 17, 2015 (as may be amended from time to time), which was executed by the Debtors and each of the members of the Steering Group.

The Debtors intend to confirm the Plan and cause the Effective Date to occur promptly after confirmation of the Plan. There can be no assurance, however, as to when and whether confirmation of the Plan and the Effective Date actually will occur. The confirmation and effectiveness of the Plan are subject to material conditions precedent. See Section VIII.A—“Conditions Precedent to Effectiveness.” There is no assurance that these conditions will be satisfied or waived. Procedures for distributions under the Plan are described under Section VII.F—“Distributions Under the Plan.” Distributions will be made only in compliance with these procedures.

If the Plan is confirmed by the Court and the Effective Date occurs, all holders of Claims against, and Equity Interests in, the Debtors (including, without limitation, those holders of Claims and Equity Interests that do not submit ballots to accept or reject the Plan or that are not entitled to vote on the Plan) will be bound by the terms of the Plan and the transactions contemplated thereby.

If the financial restructuring of the indebtedness contemplated by the Plan is not approved and consummated, there can be no assurance that the Debtors will be able to effectuate an alternative restructuring or successfully emerge from its chapter 11 cases, and the Debtors may be forced into a liquidation under chapter 7 of the Bankruptcy Code or under the laws of other countries. As reflected in the Liquidation Analysis (as defined below), the Debtors believe that if operations are terminated and their assets are liquidated under chapter 7 of the Bankruptcy Code or otherwise, the value of the assets available for payment to creditors and interest holders would be significantly lower than the value of the distributions contemplated by and under the Plan.

ii

SPECIAL NOTICE REGARDING FEDERAL AND STATE SECURITIES LAWS

As of the date of distribution, neither this Disclosure Statement nor the Plan has been filed with or reviewed by the Court, and neither this Disclosure Statement nor the Plan has been filed with the United States Securities and Exchange Commission (the “SEC”) or any state authority. The Plan has not been approved or disapproved by the SEC or any state securities commission and neither the SEC nor any state securities commission has passed upon the accuracy or adequacy of this Disclosure Statement or the merits of the Plan. Any representation to the contrary is a criminal offense.

This Disclosure Statement has been prepared pursuant to section 1125 of the Bankruptcy Code and Bankruptcy Rule 3016(b) (but has not yet been approved by the Court as complying with section 1125 of the Bankruptcy Code and Bankruptcy Rule 3016(b)). The securities to be issued under the Plan on or after the Effective Date will not have been the subject of a registration statement filed with the SEC under the Securities Act or any securities regulatory authority of any state under any state securities laws (“Blue Sky Laws”).

Prior to the filing of the chapter 11 cases, the Debtors will rely on the exemption provided by section 4(a)(2) of the Securities Act of 1933, as amended, and applicable exemptions from Blue Sky Laws. After the commencement of the chapter 11 cases, the Debtors intend to rely on the exemption from the Securities Act and Blue Sky Laws registration requirements provided by section 1145(a)(1) of the Bankruptcy Code to exempt the issuance of securities issued under, or in connection with, the Plan.

Each holder of a Senior Notes Claim will be required to certify on its ballot whether it is an Accredited Investor or a Qualified Institutional Buyer. If a holder of Senior Notes Claims is not an Accredited Investor or a Qualified Institutional Buyer, its vote will not be counted.

Neither the Solicitation nor this Disclosure Statement constitutes an offer to sell or the solicitation of an offer to buy securities in any state or jurisdiction in which such offer or solicitation is not authorized.

See the Risk Factors in Article XI of the Disclosure Statement for certain risks that you should carefully consider.

This Disclosure Statement contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements consist of any statement other than a recitation of historical fact and can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “could,” “intend,” “consider,” “expect,” “plan,” “anticipate,” “believe,” “predict,” “estimate,” or “continue” or the negative thereof or other variations thereon or comparable terminology. You are cautioned that all forward-looking statements involve risks and uncertainties that could cause actual events or results to differ materially from those referred to in such forward-looking statements. Important factors that could cause or contribute to such differences include those in Article V: “Certain Risk Factors to be Considered,” generally and in particular “Additional Factors to be Considered—Forward-Looking Statements are not Assured, and Actual Results May Vary.” The Liquidation Analysis set forth in Exhibit E, distribution projections and other information contained herein and annexed hereto are estimates only, and the timing and amount of actual distributions to Holders of Allowed Claims and Allowed Equity Interests may be affected by many factors that cannot be predicted. Any analyses, estimates or recovery projections may or may not turn out to be accurate.

iii

QUESTIONS AND ADDITIONAL INFORMATION

If you would like to obtain copies of this Disclosure Statement, the Plan, or any of the documents attached hereto or referenced herein, or if you have questions about the solicitation and voting process or these Chapter 11 Cases generally, please contact Prime Clerk, LLC (the “Voting and Claims Agent” or “Prime Clerk”), by (i) calling 844-241-2770 (Toll Free) or 929-342-0757 (International), (ii) emailing herculesballots@primeclerk.com, or (iii) visiting cases.primeclerk.com/hercules.

HERO files annual, quarterly, and other reports, proxy and information statements and other information with the SEC. You may read and copy any document HERO files at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for information regarding the Public Reference Room and its copying charges. You can also find Company filings on the SEC’s website at http://www.sec.gov and on HERO’s website at http://www.herculesoffshore.com. Information contained on HERO’s website, except for the SEC filings referred to below, is not a part of, and shall not be deemed to be incorporated by reference into, this Disclosure Statement.

By “incorporating by reference” the information HERO has filed with the SEC, HERO is disclosing information to you by referring you to those documents without actually including the specific information in this Disclosure Statement. The information incorporated by reference is an important part of this Disclosure Statement, and information that HERO files later with the SEC will automatically update and may replace this information and information previously filed with the SEC. Any statement contained in the filings (or portions of filings) incorporated by reference into this Disclosure Statement will be deemed to be modified or superseded for purposes of this Disclosure Statement to the extent that a statement contained in this Disclosure Statement or in any filing by HERO with the SEC prior to the completion of this solicitation modifies, conflicts with, or supersedes such statement.

HERO also incorporates by reference into this Disclosure Statement any future filings made with the SEC under sections 13(a), 13(c), 14 or 15(d) of the Securities Exchange Act of 1934, as amended, other than information furnished to the SEC under Items 2.02 or 7.01, or the exhibits related thereto under Item 9.01, of Form 8-K, which information is not deemed filed under the Exchange Act and is not incorporated by reference into this Disclosure Statement.

iv

TABLE OF CONTENTS

| I. |

INTRODUCTION AND EXECUTIVE SUMMARY |

1 | ||||||

| II. |

SUMMARY OF THE CLASSIFICATION AND TREATMENT OF CLAIMS AND EQUITY INTERESTS UNDER THE PLAN |

3 | ||||||

| III. |

VOTING PROCEDURES AND REQUIREMENTS |

6 | ||||||

| A. | Classes Entitled to Vote on the Plan |

6 | ||||||

| B. | Votes Required for Acceptance by a Class |

6 | ||||||

| C. | Certain Factors To Be Considered Prior to Voting |

7 | ||||||

| D. | Classes Not Entitled To Vote on the Plan |

7 | ||||||

| E. | Cramdown |

8 | ||||||

| F. | Allowed Claims |

8 | ||||||

| G. | Impairment generally |

8 | ||||||

| H. | Solicitation and Voting Process |

8 | ||||||

| The “Solicitation Package.” |

8 | |||||||

| Voting Deadlines |

9 | |||||||

| Voting Instructions |

9 | |||||||

| Beneficial Owners of the Senior Notes |

12 | |||||||

| Brokerage Firms, Banks, and Other Nominees |

13 | |||||||

| I. | The Confirmation Hearing |

13 | ||||||

| IV. |

COMPANY BACKGROUND |

13 | ||||||

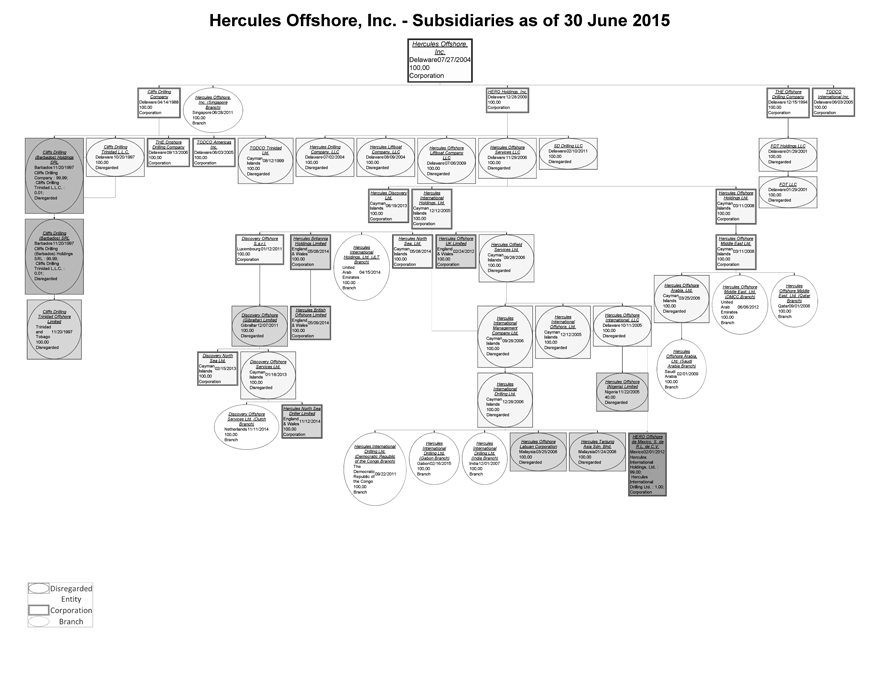

| A. | Business Segments and Organizational Structure |

13 | ||||||

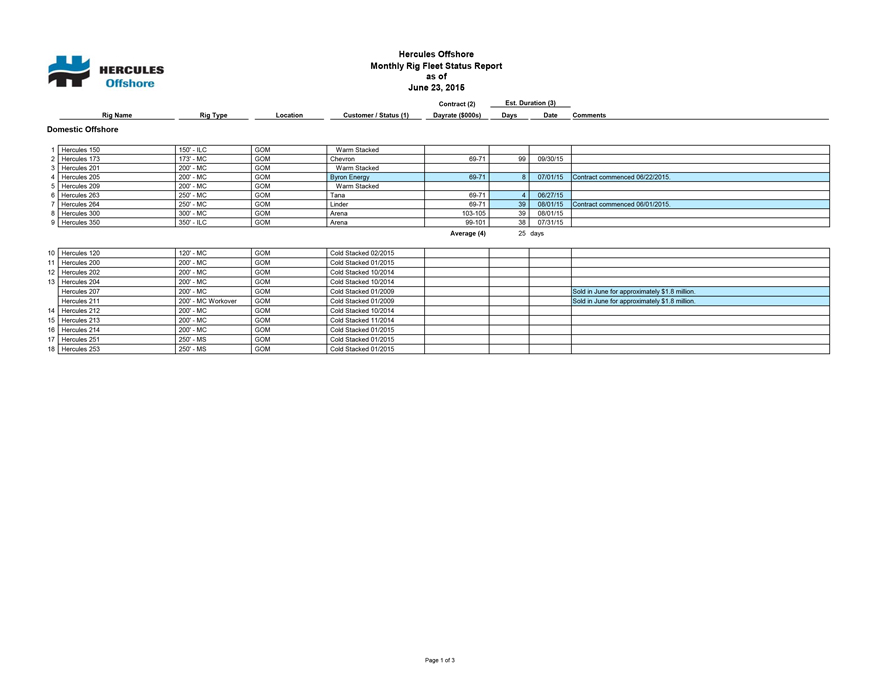

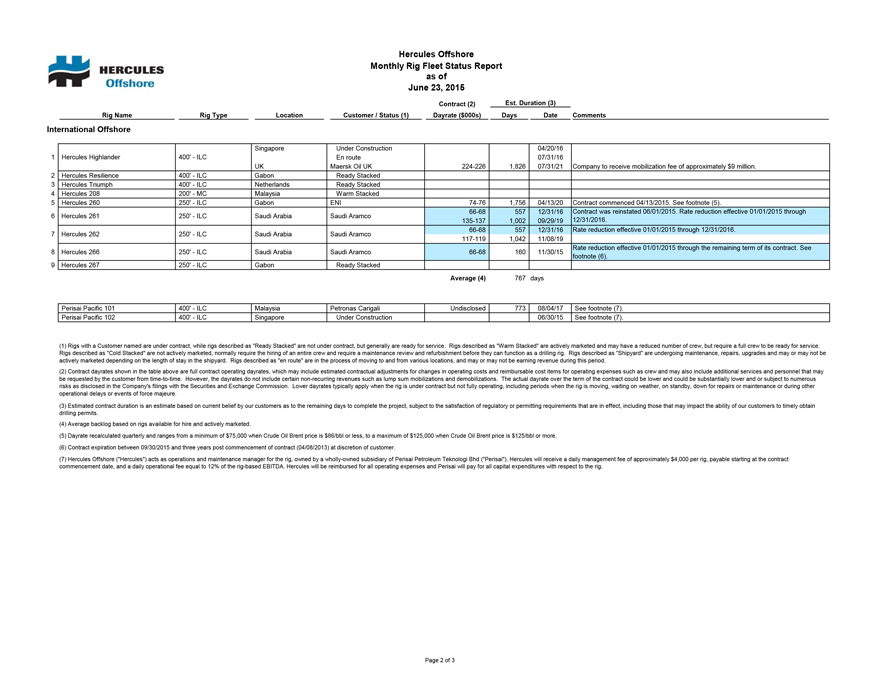

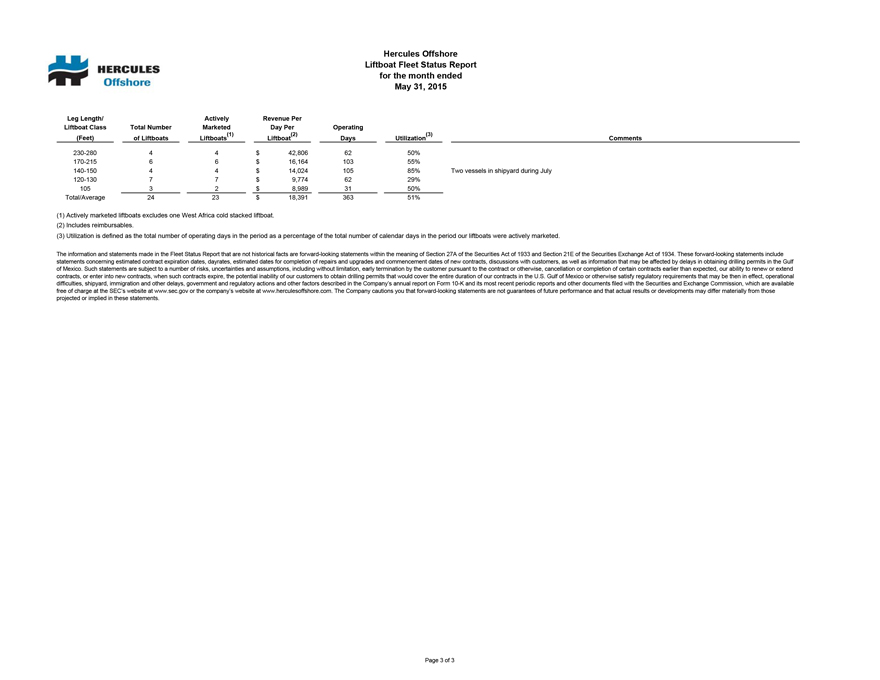

| B. | Fleet Status |

14 | ||||||

| C. | Competition and Marketing |

14 | ||||||

| D. | Backlog |

14 | ||||||

| E. | Regulation |

15 | ||||||

| F. | Properties |

18 | ||||||

| G. | Employees |

18 | ||||||

| H. | The Debtors’ Pre-Petition Capital Structure |

19 | ||||||

| I. | Significant Pre-Petition Contracts and Leases |

20 | ||||||

| J. | Pre-Petition Litigation |

22 | ||||||

| V. |

EVENTS LEADING TO THE COMMENCEMENT OF THE CHAPTER 11 CASES |

23 | ||||||

| A. | Mobile Drilling Rig and Liftboat Market |

23 | ||||||

| B. | Certain Events that Set the Stage for the Restructuring and the Chapter 11 Cases |

23 | ||||||

| C. | Prepetition Restructuring Initiatives |

24 | ||||||

| D. | The Restructuring Support Agreement |

25 | ||||||

| VI. |

THE ANTICIPATED CHAPTER 11 CASES |

27 | ||||||

| A. | Expected Timetable of the Chapter 11 Case |

27 | ||||||

| B. | Significant First Day Motions and Retention of Professionals |

27 | ||||||

| Approval of Solicitation Procedures and Scheduling of Confirmation Hearing |

28 | |||||||

| Stabilizing Operations |

28 | |||||||

| Procedural Motions and Professional Retention Applications |

29 | |||||||

| VII. |

SUMMARY OF THE PLAN |

30 | ||||||

| A. | Unclassified Claims |

30 | ||||||

| Unclassified Claims Summary |

30 | |||||||

| B. | Classified Claims and Equity Interests |

31 | ||||||

| Special Provision Regarding Unimpaired and Reinstated Claims |

35 | |||||||

| C. | Means for Implementation of the Plan |

35 | ||||||

| Operations Between the Confirmation Date and Effective Date |

35 | |||||||

| First Lien Exit Facility |

35 | |||||||

| Nonconsensual Confirmation |

36 | |||||||

| Cancellation of Certain Indebtedness, Agreements, and Existing Securities |

36 | |||||||

| Issuance of New HERO Common Stock and Warrants |

36 | |||||||

| The New HERO Warrants |

37 | |||||||

| Continued Corporate Existence and Vesting of Assets |

38 | |||||||

| Claims Against Non-Debtor Subsidiaries |

39 | |||||||

v

| Intercompany Interests |

39 | |||||||

| Corporate Action |

39 | |||||||

| Steering Group Fees and Expenses |

39 | |||||||

| Senior Notes Indenture Trustee Fees and Expenses |

39 | |||||||

| D. | Provisions Regarding Corporate Governance of the Reorganized Debtor |

40 | ||||||

| Organizational Documents |

40 | |||||||

| Appointment of Officers and Directors |

40 | |||||||

| Powers of Officers |

40 | |||||||

| Indemnification of Directors, Officers, and Employees |

40 | |||||||

| Existing Benefits Agreements and Retiree Benefits |

41 | |||||||

| New HERO Management Incentive Program |

41 | |||||||

| E. | Effect of Confirmation of the Plan |

41 | ||||||

| Compromise and Settlement |

41 | |||||||

| Subordination of Claims |

41 | |||||||

| Discharge of the Debtors |

42 | |||||||

| Injunction |

42 | |||||||

| Preservation of Causes of Action |

43 | |||||||

| Claims Incurred After the Effective Date |

43 | |||||||

| Releases, Exculpations, and Injunctions of Released Parties |

43 | |||||||

| F. | Distributions Under the Plan |

46 | ||||||

| Filing Proofs of Claim |

46 | |||||||

| Disputed Claims Process |

46 | |||||||

| Prosecution of Objections to Claims and Equity Interests |

46 | |||||||

| No Interest |

46 | |||||||

| Allocation of Consideration |

46 | |||||||

| Disallowance of Certain Claims and Equity Interests |

47 | |||||||

| Estimation |

47 | |||||||

| Insured Claims |

47 | |||||||

| Allowed Claims |

47 | |||||||

| G. | Retention of Jurisdiction |

48 | ||||||

| H. | Executory Contracts and Unexpired Leases |

50 | ||||||

| Assumption of Executory Contracts and Unexpired Leases |

50 | |||||||

| Cure Claims |

50 | |||||||

| Reservation of Rights |

51 | |||||||

| Assignment |

51 | |||||||

| Insurance Policies |

52 | |||||||

| I. | Miscellaneous Provisions |

52 | ||||||

| Immediate Binding Effect |

52 | |||||||

| Governing Law |

52 | |||||||

| Filing or Execution of Additional Documents |

52 | |||||||

| Reservation of Rights |

52 | |||||||

| Successors and Assigns |

52 | |||||||

| Term of Injunctions or Stays |

52 | |||||||

| Withholding and Reporting Requirements |

53 | |||||||

| Exemption From Transfer Taxes |

53 | |||||||

| Plan Supplement |

53 | |||||||

| Conflicts |

53 | |||||||

| VIII. |

CONFIRMATION AND EFFECTIVENESS OF THE PLAN |

53 | ||||||

| A. | Conditions Precedent to Effectiveness |

53 | ||||||

| B. | Waiver of Conditions Precedent to Effectiveness |

54 | ||||||

| C. | Effect of Failure of Condition |

54 | ||||||

| D. | Vacatur of Confirmation Order |

55 | ||||||

| E. | Modification of the Plan |

55 | ||||||

| F. | Revocation, Withdrawal, or Non-Consummation |

55 | ||||||

| Right to Revoke or Withdraw |

55 | |||||||

| Effect of Withdrawal, Revocation, or Non-Consummation |

55 | |||||||

vi

| IX. |

CONFIRMATION PROCEDURES |

55 | ||||||

| A. | Combined Disclosure Statement and Confirmation Hearing |

55 | ||||||

| B. | Standards for Confirmation |

56 | ||||||

| Confirmation Without Acceptance by All Impaired Classes | 57 | |||||||

| C. | Alternatives to Confirmation and Consummation of the Plan |

60 | ||||||

| X. |

LIQUIDATION ANALYSIS, VALUATION AND FINANCIAL PROJECTIONS |

60 | ||||||

| A. | Liquidation Analysis |

60 | ||||||

| B. | Valuation Analysis |

61 | ||||||

| C. | Financial Projections |

61 | ||||||

| D. | Other Available Information |

61 | ||||||

| XI. |

CERTAIN RISK FACTORS TO BE CONSIDERED |

62 | ||||||

| A. | General |

62 | ||||||

| B. | Certain Bankruptcy Law Considerations |

62 | ||||||

| Parties in Interest May Object to the Debtors’ Classification of Claims and Interests |

62 | |||||||

| Contingencies Not to Affect Votes of Impaired Classes to Accept or Reject the Plan |

62 | |||||||

| The Debtors May Fail to Satisfy the Solicitation Requirements Requiring a Re-Solicitation |

63 | |||||||

| The Restructuring Support Agreement Could be Terminated |

63 | |||||||

| Risk of Non-Confirmation, Non-Occurrence, or Delay of the Plan |

63 | |||||||

| Risk of Non-Occurrence of the Effective Date |

64 | |||||||

| Impact of the Chapter 11 Cases on the Debtors |

64 | |||||||

| The Plan is Based Upon Assumptions the Debtors Developed which May Prove Incorrect and Could Render the Plan Unsuccessful |

65 | |||||||

| C. | Certain Risks Related to the Debtors’ Business and Operations |

65 | ||||||

| The Company’s Business Depends on the Level of Activity in the Oil and Natural Gas Industry, which is Significantly Affected by Volatile Oil and Natural Gas Prices |

65 | |||||||

| The Offshore Service Industry is Highly Cyclical and Experiences Periods of Low Demand and Low Dayrates. The Volatility of the Industry has in the Past Resulted and Could Again Result in Sharp Declines in the Company’s Profitability |

66 | |||||||

| Maintaining Idle Assets or the Sale of Assets Below Their Then Carrying Value May Cause the Company to Experience Losses and May Result in Impairment Charges |

66 | |||||||

| HERO is a Holding Company, and it is Dependent Upon Cash Flow From Subsidiaries to Meet Financial Obligations |

66 | |||||||

| Many Customer Contracts are Short Term, and Customers May Seek to Terminate, Renegotiate or Decline to Renew Contracts During Depressed Market Conditions, Which Will Result in Reduced Revenue and Profitability |

67 | |||||||

| Hercules can Provide No Assurance That its Current Backlog of Contract Revenue and Receivables Will be Ultimately Realized |

67 | |||||||

| A Significant Portion of The Company’s Business is Conducted in Shallow-Water Areas of the U.S. Gulf of Mexico. The Mature Nature of This Region Could Result in Less Drilling Activity in the Area, Thereby Reducing Demand for the Company’s Services and Requiring Hercules to Cold Stack Additional Rigs |

68 | |||||||

| The Debtors’ Industry is Highly Competitive, With Intense Price Competition. The Debtors’ Inability to Compete Successfully may Reduce Profitability |

68 | |||||||

| An Increase in Supply of Rigs or Liftboats Could Adversely Affect the Debtors’ Financial Condition and Results of Operations |

68 | |||||||

| Asset Sales Have Been an Important Component of the Company’s Business Strategy. Hercules may be Unable to Identify Appropriate Buyers With Access to Financing or to Complete any Sales on Acceptable Terms |

69 | |||||||

| The First Lien Exit Facility Will Impose Significant Additional Costs and Operating and Financial Restrictions on the Company, Which May Prevent Hercules From Capitalizing on Business Opportunities and Taking Certain Actions |

69 | |||||||

| The Company’s International Operations are Subject to Additional Political, Economic, and Other Uncertainties not Generally Associated With Domestic Operations |

70 | |||||||

vii

| More of the Company’s Existing Jackup Rigs are at a Relative Disadvantage to Higher Specification Rigs, Which May be More Likely to Obtain Contracts Than Lower Specification Jackup Rigs Such as the Company’s |

71 | |||||||

| A Small Number of Customers Account for a Significant Portion of the Company’s Revenue, and the Loss of One or More of These Customers Could Adversely Affect the Company’s Financial Condition and Results of Operations |

72 | |||||||

| The Company’s Business Involves Numerous Operating Hazards and Exposure to Extreme Weather and Climate Risks, and the Company’s Insurance may not be Adequate to Cover its Losses |

72 | |||||||

| The Company’s Insurance Coverage has Become More Expensive, May Become Unavailable in the Future and May be Inadequate to Cover its Losses |

72 | |||||||

| The Company’s Customers may be Unable or Unwilling to Indemnify It |

73 | |||||||

| HERO Expects That its Common Stock Will Become Delisted from Trading on NASDAQ Following the Petition Date |

73 | |||||||

| Any Violation of the Foreign Corrupt Practices Act (“FCPA”) or Similar Laws and Regulations Could Result in Significant Expenses, Divert Management Attention, and Otherwise Have a Negative Impact |

73 | |||||||

| The Company’s International Operations May Subject it to Political and Regulatory Risks and Uncertainties |

74 | |||||||

| Public Health Threats Could Have a Material Adverse Effect on the Company’s Operations and its Financial Results |

74 | |||||||

| Hercules Cannot Guarantee the Timely Completion and Delivery of its Newbuild Rig that is Being Constructed And that is Currently Scheduled for Delivery in April 2016 |

74 | |||||||

| Hercules Cannot Guarantee that Hercules Highlander Will be Completed or Pass the Acceptance Tests |

75 | |||||||

| Failure to Retain or Attract Skilled Workers Could Hurt the Company’s Operations |

75 | |||||||

| Governmental Laws and Regulations, Including Those Arising Out of the Macondo Well Incident and Those Related to Climate Change and Emissions of Greenhouse Gases, May Add to the Company’s Costs or Limit Drilling Activity |

75 | |||||||

| Compliance With or a Breach of Environmental Laws and Regulations can be Costly and Could Limit the Company’s Operations |

76 | |||||||

| Hercules May Not Be Able to Maintain or Replace its Rigs and Liftboats as They Age |

76 | |||||||

| The Company’s Operating and Maintenance Costs With Respect to its Rigs Include Fixed Costs That Will Not Decline in Proportion to Decreases in Dayrates |

76 | |||||||

| Upgrade, Refurbishment and Repair Projects are Subject to Risks, Including Delays and Cost Overruns, Which Could Have an Adverse Impact on the Company’s Available Cash Resources and Results of Operations |

77 | |||||||

| Hercules is Subject to Litigation That Could Have an Adverse Effect on its Business |

78 | |||||||

| The Company’s Operations Present Hazards and Risks That Require Significant and Continuous Oversight, and it Depends Upon the Security and Reliability of its Technologies, Systems and Networks in Numerous Locations Where it Conducts Business |

78 | |||||||

| Changes in Effective Tax Rates, Taxation of the Company’s Foreign Subsidiaries, Limitations on Utilization of the Company’s Net Operating Losses or Adverse Outcomes Resulting From Examination of the Company’s Tax Returns Could Adversely Affect its Operating Results and Financial Results |

78 | |||||||

| Discharge of Prepetition Claims and Related Legal Proceedings |

78 | |||||||

| D. | Certain Risks Relating to HERO Equity Interests related to the Plan and Bankruptcy Filing |

79 | ||||||

| Lack of Established Market for HERO Equity Interests as a Consequence of Plan and Bankruptcy Filing |

79 | |||||||

| E. | Certain Risks Relating to the Shares of New HERO Common Stock and the New HERO Warrants Under the Plan |

79 | ||||||

| Significant Holders |

79 | |||||||

| Restrictions on Transfer of New HERO Common Stock |

79 |

viii

| Lack of Established Market for New HERO Common Stock and the New HERO Warrants |

79 | |||||||

| The Anti-Dilution Protection for the New HERO Warrants Does Not Cover All Transactions that Could Adversely Affect Such Warrants |

80 | |||||||

| Historical Financial Information of the Debtors May Not Be Comparable to the Financial Information of the Reorganized Debtor |

80 | |||||||

| The Financial Projections Set forth in this Disclosure Statement May Not Be Achieved |

80 | |||||||

| F. | Additional Factors to Be Considered |

80 | ||||||

| The Debtors Have No Duty to Update |

80 | |||||||

| No Representations Made Outside this Disclosure Statement Are Authorized |

81 | |||||||

| The Debtors Relied on Certain Exemptions from Registration under the Securities Act |

81 | |||||||

| The Information Herein Was Provided by the Debtors and Relied upon by Their Advisors |

81 | |||||||

| No Legal or Tax Advice Is Provided to You by this Disclosure Statement |

81 | |||||||

| No Admissions Are Made by this Disclosure Statement |

82 | |||||||

| Forward-Looking Statements in this Disclosure Statement |

82 | |||||||

| XII. |

SECURITIES LAW MATTERS |

83 | ||||||

| A. | Bankruptcy Code Exemptions from Registration Requirements |

83 | ||||||

| Subsequent Transfers of the New HERO Common Stock and New HERO Warrants Issued to Affiliates |

85 | |||||||

| XIII. |

CERTAIN UNITED STATES FEDERAL INCOME TAX CONSEQUENCES OF THE PLAN |

86 | ||||||

| A. | Introduction |

86 | ||||||

| B. | Certain U.S. Federal Income Tax Consequences of the Plan to the Debtors |

87 | ||||||

| Cancellation of Debt and Reduction of Tax Attributes |

87 | |||||||

| Limitation of NOL Carryforwards and Other Tax Attributes |

88 | |||||||

| Alternative Minimum Tax |

89 | |||||||

| C. | Certain U.S. Federal Income Tax Consequences of the Plan to U.S. Holders of Allowed Class 3 Senior Notes Claims |

90 | ||||||

| Distributions After the Effective Date |

92 | |||||||

| Accrued But Unpaid Interest |

92 | |||||||

| Market Discount |

92 | |||||||

| Medicare Tax |

93 | |||||||

| D. | Certain U.S. Federal Income Tax Considerations for Non-U.S. Holders of Allowed Class 3 Senior Notes Claims |

93 | ||||||

| Gain Recognition |

93 | |||||||

| U.S. Federal Income Tax Consequences to Non-U.S. Holders of Owning and Disposing of New HERO Common Stock |

93 | |||||||

| FATCA |

94 | |||||||

| E. | Information Reporting and Backup Withholding |

95 | ||||||

| F. | Importance of Obtaining Professional Tax Assistance |

95 | ||||||

| XIV. |

RECOMMENDATION AND CONCLUSION |

95 | ||||||

ix

TABLE OF EXHIBITS

| Exhibit A: | Debtors’ Joint Prepackaged Plan of Reorganization Pursuant to Chapter 11 of the Bankruptcy Code | |

| Exhibit B: | Restructuring Support Agreement | |

| Exhibit C: | Hercules’ Prepetition Corporate Structure | |

| Exhibit D: | Financial Projections | |

| Exhibit E: | Liquidation Analysis | |

| Exhibit F: | Valuation Analysis | |

| Exhibit G: | Fleet Status Report as of June 23, 2015 | |

| Exhibit H: | First Lien Exit Facility Commitment Letter. | |

THE DEBTORS HEREBY ADOPT AND INCORPORATE EACH EXHIBIT ANNEXED TO THIS DISCLOSURE STATEMENT BY REFERENCE AS THOUGH FULLY SET FORTH HEREIN.

x

I. INTRODUCTION AND EXECUTIVE SUMMARY

Hercules Offshore, Inc., a Delaware corporation (“HERO”) and certain of its direct and indirect subsidiaries (the “Debtor Subsidiaries,”) which intend to become chapter 11 debtors and debtors in possession (the “Debtors”) in chapter 11 cases to be filed (the “Chapter 11 Cases”), submit this Disclosure Statement pursuant to section 1126 of title 11 of the United States Code (the “Bankruptcy Code”) for use in the solicitation of votes on the Plan. A copy of the Plan is annexed as Exhibit A to this Disclosure Statement. Capitalized terms used but not otherwise defined herein have the meanings ascribed to such terms in the Plan. For the avoidance of doubt, the Debtors’ foreign direct and indirect subsidiaries are not presently contemplated to be debtors in the Chapter 11 Cases.

HERO provides shallow-water drilling and marine services to the oil and natural gas exploration and production industry globally through its Domestic Offshore, International Offshore and International Liftboats segments (as discussed further below). At June 23, 2015, the Debtors and their Non-Debtor Subsidiaries (collectively, “Hercules” or the “Company”) operated a fleet of 27 jackup rigs, including one rig under construction, and 24 liftboat vessels. Hercules’ diverse fleet is capable of providing services such as oil and gas exploration and development drilling, well service, platform inspection, maintenance and decommissioning operations in several key shallow-water provinces around the world.

The purpose of this Disclosure Statement is to provide information of a kind, and in sufficient detail, to enable creditors of the Debtors that are entitled to vote on the Plan to make informed decisions on whether to vote to accept or reject the Plan. This Disclosure Statement sets forth certain information regarding the Debtors’ prepetition operating and financial history, the Debtors’ need to seek chapter 11 protection, significant events that are expected to occur during the Chapter 11 Cases, and the Debtors’ anticipated organization, operations, and liquidity upon successful emergence from chapter 11 protection.

The Plan and this Disclosure Statement are the result of extensive and vigorous negotiations among the Debtors and the Steering Group, which is an ad hoc group of holders of Senior Notes that collectively hold in excess of 66 2/3% of the Senior Notes. The culmination of such negotiations was the entry into the Restructuring Support Agreement (as may be amended from time to time, the “Restructuring Support Agreement”), a copy of which is attached hereto as Exhibit B. The Restructuring Support Agreement sets forth the material terms and conditions of the restructuring provided for in the Plan and described herein (the “Restructuring”). As described in more detail below, the Plan substantially deleverages the Debtors’ balance sheet by converting approximately $1.2 billion of debt under the Senior Notes into 96.9% of the equity in Reorganized HERO. As part of the overall settlement embodied in the Restructuring Support Agreement and the Plan, the holders of Senior Notes are voluntarily forgoing their right to part of the distributions under the Plan that they are otherwise entitled to receive so that the Debtors can (i) pay in full allowed general unsecured claims, such as the claims of suppliers and vendors, in the ordinary course according to existing business terms and (ii) provide a pro rata distribution of a portion of the New HERO Common Stock and the New HERO Warrants to holders of HERO Equity Interests in exchange for the surrender or cancellation of their Equity Interests.

The key components of the Plan are as follows:

| • | Holders of Allowed General Unsecured Claims, including Allowed Claims of trade vendors, suppliers, and customers, will not be affected by the filing of the Chapter 11 Cases and, subject to Court approval, are anticipated to be paid in full in the ordinary course of business during the pendency of the Chapter 11 Cases or reinstated and left unimpaired under the Plan in accordance with their terms as part of the overall compromise embodied in the Plan. |

| • | Payment in full, in cash, of all Allowed Administrative Claims, Fee Claims, Priority Tax Claims, statutory fees, Other Priority Claims, and Other Secured Claims. |

| • | Holders of Allowed Senior Notes Claims will receive their Pro Rata share of 96.9% on a fully diluted basis (subject only to the New HERO Warrants and the New HERO Management Incentive Program Equity) of the New HERO Common Stock outstanding as of the Effective Date. |

1

| • | In addition, each holder of an Allowed Senior Notes Claim that is an Eligible Noteholder shall have the opportunity to participate, on a Pro Rata basis, in the First Lien Exit Facility in accordance with the terms and conditions set forth in the First Lien Exit Facility Subscription Procedures during the period from the Petition Date through the date of the Confirmation Hearing. |

| • | HERO Equity Interests shall be cancelled and discharged and shall be of no further force or effect, whether surrendered for cancellation or otherwise, and holders of HERO Equity Interests shall not receive or retain any property under the Plan on account of such HERO Equity Interests; provided, however, that on the Effective Date, holders of HERO Equity Interests shall receive, in exchange for the surrender or cancellation of their HERO Equity Interests and for the releases by such holders of the Released Parties, their Pro Rata share of (1) 3.1% of the New HERO Common Stock on a fully diluted basis (subject only to the New HERO Warrants and the Management Incentive Program Equity) and (2) the New HERO Warrants; provided, further, that holders of HERO Equity Interests that opt not to grant the voluntary releases contained in the Plan shall not be entitled to receive their Pro Rata share of such New HERO Common Stock and the New HERO Warrants and shall not receive any consideration in exchange for the surrender or cancellation of their HERO Equity Interests. |

| • | Entry into the new $450 million First Lien Exit Facility, which will be used (i) to pay for the construction and purchase of the Hercules Highlander, a newbuild jackup rig that is expected to be delivered in April 2016, (ii) to pay all restructuring fees and costs and other payments required under the Plan, and (iii) for working capital and general corporate purposes on and after the Effective Date. |

The Debtors and the other parties to the Restructuring Support Agreement believe that the restructuring contemplated by the Plan is in the best interests of all stakeholders because it (i) achieves a substantial deleveraging of the Debtors’ balance sheet through consensus with the overwhelming majority of the holders of Senior Notes, (ii) provides for a reduction of approximately $50 million of the Debtors’ pre-Restructuring annual interest burden on previously funded debt, (iii) provides $450 million of new financing in the form of the First Lien Exit Facility, and (iv) eliminates potential deterioration of value—and disruptions to worldwide operations—that could otherwise result from protracted and contentious bankruptcy cases. Importantly, the Debtors would not be able to implement the conversion of debt-to-equity contemplated by the Plan without the support of the Steering Group. In sum, the Plan embodies a global settlement as part of an expeditious and consensual restructuring. This avoids potential litigation that could decrease value for all stakeholders and delay (and possibly derail) the restructuring process. The significant support obtained by the Debtors pursuant to the Restructuring Support Agreement provides a fair and reasonable path for an expeditious consummation of the Plan and the preservation of Hercules’ ordinary course of business.

As of the Effective Date, Reorganized HERO will be a reporting company under the Securities Exchange Act of 1934, as amended. As of July 13, 2015, HERO common stock was listed for trading on The Nasdaq Global Select Market (“NASDAQ”) under the ticker “HERO.” In March 2015, HERO received a letter from NASDAQ informing HERO that its common stock was below the minimum bid price requirement for continued listing on NASDAQ. Hercules expects that its common stock will become delisted from trading on NASDAQ following the Petition Date and will then be traded on the OTC Pink market. Reorganized HERO will use reasonable efforts to cause the listing on NASDAQ of the New HERO Common Stock on or as soon as reasonably practicable after the Effective Date.

Additionally, as described in Section VII.E herein, the Plan provides for certain releases of Claims against, among others, the Debtors, the Reorganized Debtors, the Non-Debtor Subsidiaries, the parties to the Restructuring Support Agreement, the Senior Notes Indenture Trustees, and each of their professionals, employees, officers, and directors. Because holders of HERO Equity Interests are substantially

2

out of the money under absolute priority principles, the Plan further provides that any holder of HERO Equity Interests that opts not to grant the voluntary releases contained in the Plan shall not receive the New HERO Equity Interests and New HERO Warrants that it would otherwise be entitled to receive under the Plan and shall not receive any distribution whatsoever under the Plan.

FOR A COMPLETE UNDERSTANDING OF THE PLAN, YOU SHOULD READ THIS DISCLOSURE STATEMENT, THE PLAN, AND THE EXHIBITS THERETO IN THEIR ENTIRETY. IF ANY INCONSISTENCY EXISTS BETWEEN THE PLAN AND THIS DISCLOSURE STATEMENT, THE TERMS OF THE PLAN ARE CONTROLLING. ALL EXHIBITS TO THIS DISCLOSURE STATEMENT ARE INCORPORATED INTO AND ARE A PART OF THIS DISCLOSURE STATEMENT AS IF SET FORTH IN FULL HEREIN.

THE DEBTORS HAVE NOT YET COMMENCED BANKRUPTCY CASES UNDER CHAPTER 11 OF THE BANKRUPTCY CODE. THE DEBTORS EXPECT TO FILE THEIR BANKRUPTCY CASES AFTER THEY SOLICIT THE VOTES OF THE IMPAIRED CLASS OF CLAIMS ENTITLED TO VOTE ON THE PLAN.

BECAUSE NO BANKRUPTCY CASES HAVE YET BEEN COMMENCED, THIS DISCLOSURE STATEMENT HAS NOT YET BEEN APPROVED BY ANY COURT WITH RESPECT TO WHETHER IT CONTAINS ADEQUATE INFORMATION WITHIN THE MEANING OF SECTION 1125(a) OF THE BANKRUPTCY CODE. NONETHELESS, ONCE THE CHAPTER 11 CASES ARE COMMENCED, THE DEBTORS EXPECT TO PROMPTLY SEEK ENTRY OF AN ORDER OF THE COURT APPROVING THIS DISCLOSURE STATEMENT PURSUANT TO SECTION 1125 OF THE BANKRUPTCY CODE AND DETERMINING THAT THE SOLICITATION OF VOTES ON THE PLAN BY MEANS OF THIS DISCLOSURE STATEMENT WAS IN COMPLIANCE WITH SECTION 1125(a) OF THE BANKRUPTCY CODE.

Each holder of a Claim entitled to vote on the Plan should read this Disclosure Statement, the Plan, and the instructions accompanying the Ballots in their entirety before voting on the Plan. These documents contain, among other things, important information concerning the classification of Claims for voting purposes and the tabulation of votes. The statements contained in this Disclosure Statement are made only as of the date hereof unless otherwise specified, and there can be no assurance that the statements contained herein will be correct at any time hereafter.

All creditors should also carefully read Article XI of this Disclosure Statement—“Certain Risk Factors to be Considered”—before voting to accept or reject the Plan.

THE DEBTORS BELIEVE THAT IMPLEMENTATION OF THE PLAN IS IN THE BEST INTERESTS OF THE DEBTORS, THEIR ESTATES, AND ALL STAKEHOLDERS. FOR ALL OF THE REASONS DESCRIBED IN THIS DISCLOSURE STATEMENT, THE DEBTORS URGE YOU TO RETURN YOUR BALLOT ACCEPTING THE PLAN BY THE VOTING DEADLINE (I.E., THE DATE BY WHICH YOUR BALLOT MUST BE ACTUALLY RECEIVED), WHICH IS AUGUST 12, 2015 AT 5:00 P.M. (PREVAILING EASTERN TIME).

II. SUMMARY OF THE CLASSIFICATION AND TREATMENT OF CLAIMS AND EQUITY INTERESTS UNDER THE PLAN

The Plan establishes a comprehensive classification of Claims and Equity Interests.3 The following table summarizes the classification and treatment of Claims and Equity Interests against each Debtor under the Plan and the estimated distributions to be received by the holders of Allowed Claims under the Plan thereunder. Amounts assumed for purposes of projected recoveries are estimates only; actual recoveries received under the Plan may differ materially from the projected recoveries.

| 3 | In accordance with section 1123(a)(1) of the Bankruptcy Code, the Plan does not classify Administrative Claims, Priority Tax Claims, U.S. Trustee Fees and Fee Claims. |

3

The summaries in this table are qualified in their entirety by the description of the treatment of such Claims in Article III of the Plan. All claims and interests against a particular Debtor are placed in classes for each of the Debtors (as designated by subclasses a through o for each of the 15 Debtors). Specifically, such subclasses represent Claims against and Equity Interests in the Debtors as follows: Cliffs Drilling Company (subclass a); Cliffs Drilling Trinidad LLC (subclass b); FDT LLC (subclass c); FDT Holdings LLC (subclass d); Hercules Drilling Company LLC (subclass e); Hercules Liftboat Company LLC (subclass f); Hercules Offshore, Inc. (subclass g); Hercules Offshore Services LLC (subclass h); Hercules Offshore Liftboat Company LLC (subclass i); HERO Holdings, Inc. (subclass j); SD Drilling LLC (subclass k); THE Offshore Drilling Company (subclass l); THE Onshore Drilling Company (subclass m); TODCO Americas, Inc. (subclass n); and TODCO International, Inc. (subclass o).

| Class |

Claim or Interest |

Treatment of Allowed Claims |

Voting Rights |

Projected Plan Recovery |

||||||

| 1 |

Other Priority Claims | Except to the extent that a holder of an Allowed Other Priority Claim and the Debtors (with the consent of the Steering Group) agree in writing to less favorable treatment, in full and final satisfaction, settlement, release, and discharge of, and in exchange for, each Allowed Other Priority Claim, each holder of an Allowed Other Priority Claim shall receive (i) payment in Cash in an amount equal to such Allowed Other Priority Claim as soon as practicable after the later of (a) the Effective Date and (b) thirty (30) days after the date when such Other Priority Claim becomes an Allowed Other Priority Claim or (ii) such other treatment, as determined by the Debtors (with the consent of the Steering Group), that will render it Unimpaired pursuant to section 1124 of the Bankruptcy Code. |

Unimpaired / Deemed to Accept |

100 | % | |||||

| 2 |

Other Secured Claims | Except to the extent that a holder of an Allowed Other Secured Claim and the Debtors (with the consent of the Steering Group) agree in writing to less favorable treatment, in full and final satisfaction, settlement, release and discharge of and in exchange for such Other Secured Claim, each holder of an Allowed Other Secured Claim shall, as determined by the Debtors (with the consent of the Steering Group), receive (i) Cash in an amount equal to such Allowed Other Secured Claim, including any interest on such Allowed Other Secured Claim, if such interest is required to be paid pursuant to sections 506(b) and/or 1129(a)(9) of the Bankruptcy Code, as soon as practicable after the later of (a) the Effective Date, and (b) thirty (30) days after the date such Other Secured Claim becomes an Allowed Other Secured Claim, (ii) the Collateral securing its Allowed Other Secured Claim as soon as practicable after the later of (a) the Effective Date and (b) thirty (30) days after the date such Other Secured Claim becomes an Allowed Other Secured Claim, or (iii) such other treatment, as determined by the Debtors (with the consent of the Steering Group), that will render it Unimpaired pursuant to section 1124 of the Bankruptcy Code. |

Unimpaired / Deemed to Accept |

100 | % | |||||

| 3 |

Senior Notes Claims | Except to the extent that a holder of an Allowed Senior Notes Claim and the Debtors (with the consent of the Steering Group) agree in writing to less favorable treatment, in full and final satisfaction, settlement, release, and discharge of, and in exchange for, each Senior Notes Claim, on or as soon as practicable after the Effective Date, each holder of an Allowed Senior Notes Claim shall receive its Pro Rata share of the Senior Notes Equity Distribution. |

Impaired / Entitled to Vote | 41 | %4 | |||||

| 4 | For the avoidance of doubt, the projected recovery for holders of Senior Notes Claims does not include any recovery attributable to the right of holders of Senior Notes Claims who are Eligible Noteholders to participate in the First Lien Exit Facility. |

4

| In addition to the foregoing, each holder of an Allowed Senior Notes Claim that is an Eligible Noteholder shall have the opportunity to participate, on a Pro Rata basis, in the First Lien Exit Facility in accordance with the terms and conditions set forth in the First Lien Exit Facility Subscription Procedures during the period from the Petition Date through the date of the Confirmation Hearing. The opportunity to participate in the First Lien Exit Facility does not constitute a distribution to the holders of Allowed Senior Notes Claims on account of their Claims. |

||||||||||

| 4 |

General Unsecured Claims5 | In full and final satisfaction, settlement, release, and discharge of, and in exchange for, each Allowed General Unsecured Claim, on the Effective Date, each holder of an Allowed General Unsecured Claim shall, at the discretion of the Debtors (with the consent of the Steering Group), and only to the extent such holder’s Allowed General Unsecured Claim was not previously paid in the ordinary course of business, pursuant to an order of the Court, or otherwise: (i) have its Allowed General Unsecured Claim Reinstated as an obligation of the applicable Reorganized Debtor, and be paid in accordance with ordinary course terms, (ii) receive such other treatment as may be agreed between such holder and the Debtors (with the consent of the Steering Group) or (iii) receive such other treatment, as determined by the Debtors (with the consent of the Steering Group), that will render it Unimpaired pursuant to section 1124 of the Bankruptcy Code. Payment of an Allowed General Unsecured Claim is subject to the rights of the Debtors, Reorganized Debtors or any other party in interest to dispute such Claim as if the Chapter 11 Cases had not been commenced in accordance with applicable nonbankruptcy law. |

Unimpaired / Deemed to Accept |

100 | % | |||||

| 5 |

Intercompany Claims | In full and final satisfaction, settlement, release, and discharge of, and in exchange for, each Allowed Intercompany Claim, on the Effective Date, each Intercompany Claim shall be Reinstated. On and after the Effective Date, the Reorganized Debtors and the Non-Debtor Subsidiaries will be permitted to transfer funds between and among themselves as they determine to be necessary or appropriate to enable the Reorganized Debtors to satisfy their obligations under the Plan. Except as set forth herein, any changes to intercompany account balances resulting from such transfers will be accounted for and settled in accordance with the Debtors’ and the Non-Debtor Subsidiaries’ historical intercompany account settlement practices. |

Unimpaired / Deemed to Accept |

100 | % | |||||

| 6 |

Intercompany Interests | On the Effective Date, Intercompany Interests shall be Reinstated. |

Unimpaired / Deemed to Accept |

100 | % | |||||

| 5 | At May 31, 2015, the Company’s accounts payable was approximately $52 million on a consolidated basis. The Company’s accounts payable balances fluctuate from month to month depending upon business activity and other factors. The Debtors estimate Class 4 General Unsecured Claims in the range of approximately $40 million. |

5

| 7 |

HERO Equity Interests | On the Effective Date, HERO Equity Interests shall be cancelled and discharged and shall be of no further force or effect, whether surrendered for cancellation or otherwise, and holders of HERO Equity Interests shall not receive or retain any property under the Plan on account of such HERO Equity Interests. Notwithstanding the foregoing, on or as soon as practicable after the Effective Date, holders of HERO Equity Interests shall receive, in exchange for the surrender or cancellation of their HERO Equity Interests and for the releases by such holders of the Released Parties, their Pro Rata share of (1) the Shareholder Equity Distribution and (2) the New HERO Warrants; provided, however, that any holder of a HERO Equity Interest that opts not to grant the voluntary releases contained in Article VII.F of the Plan shall not be entitled to receive its Pro Rata share of the Shareholder Equity Distribution and the New HERO Warrants and shall not receive any consideration in exchange for the surrender or cancellation of its HERO Equity Interests or any distribution whatsoever under the Plan; and provided, further, that, notwithstanding Article VIII.B.8, the Debtors (with the consent of the Steering Group) may provide any holder of a HERO Equity Interest that would otherwise be entitled to receive a distribution of less than one (1) share of the New HERO Common Stock under Article III.D.7.(b) of the Plan with a distribution of one (1) share of New HERO Common Stock. |

Impaired / Deemed to Reject | 0 | %6 |

III. VOTING PROCEDURES AND REQUIREMENTS

| A. | Classes Entitled to Vote on the Plan |

The following Class is the only Class entitled to vote to accept or reject the Plan (the “Voting Class”):

| Class |

Claim or Interest |

Status | ||

| 3 | Senior Note Claims | Impaired7 |

If your Claim or Equity Interest is not included in the Voting Class, you are not entitled to vote. If your Claim is included in the Voting Class, you should read your ballot and carefully follow the instructions included in the ballot. Please use only the ballot that accompanies the Disclosure Statement or the ballot that the Debtors, or the Voting and Claims Agent on behalf of the Debtors, otherwise provided to you.

| B. | Votes Required for Acceptance by a Class |

Under the Bankruptcy Code, acceptance of a plan of reorganization by a class of claims or interests is determined by calculating the amount and, if a class of claims, the number, of claims and interests voting to accept, as a percentage of the allowed claims or interests, as applicable, that have voted. Acceptance by a class of claims requires an affirmative vote of (i) at least two-thirds in dollar amount of the total allowed claims that have voted and (ii) more than one-half in number of the total allowed claims that have voted. Your vote on the Plan is important. The Bankruptcy Code requires as a condition to confirmation of a plan of reorganization that each class that is impaired and entitled to vote under a plan votes to accept such plan, unless the plan is being confirmed under the “cram down” provisions of section 1129(b) of the Bankruptcy Code.

| 6 | As discussed above, holders of Class 7 Equity Interests will receive no distribution on account of their HERO Equity Interests, provided, however, that such holders that do not opt out of the Releases contained in Article VII of the Plan shall receive their Pro Rata share of (i) 3.1% of the New HERO Common Stock, and (ii) the New HERO Warrants. |

| 7 | Eligible Noteholders are entitled to vote to accept or reject the Plan. Any votes cast by Non-Eligible Noteholders will not be counted. |

6

| C. | Certain Factors To Be Considered Prior to Voting |

There are a variety of factors that all holders of Claims entitled to vote on the Plan should consider prior to voting to accept or reject the Plan. These factors may impact recoveries under the Plan and include:

| • | unless otherwise specifically indicated, the financial information contained in the Disclosure Statement has not been audited and is based on an analysis of data available at the time of the preparation of the Plan and the Disclosure Statement; |

| • | although the Debtors believe that the Plan complies with all applicable provisions of the Bankruptcy Code, the Debtors can neither assure such compliance nor that the Bankruptcy Court will confirm the Plan; |

| • | the Debtors may request Confirmation without the acceptance of all Impaired Classes in accordance with section 1129(b) of the Bankruptcy Code; and |

| • | any delays of either Confirmation or Consummation could result in, among other things, increased Administrative Claims and Fee Claims. |

While these factors could affect distributions available to holders of Allowed Claims under the Plan, the occurrence or impact of such factors will not necessarily affect the validity of the vote of the Voting Class or necessarily require a re-solicitation of the votes of holders of Claims in such Voting Class.

For a discussion of certain risk factors, please refer to ARTICLE XI, entitled “Certain Risk Factors to Be Considered,” of this Disclosure Statement.

| D. | Classes Not Entitled To Vote on the Plan |

Under the Bankruptcy Code, holders of claims and interests are not entitled to vote if their contractual rights are unimpaired by the proposed plan or if they will receive no property under the proposed plan on account of their claims or interests, as applicable, or are otherwise deemed to reject. As holders of HERO Equity Interests are not entitled to receive any distributions on account of the valuation of the Debtors, the votes of holders of HERO Equity Interests will not be solicited and such holders will be deemed to reject. In addition, because holders of HERO Equity Interests are substantially out of the money under absolute priority principles, holders of HERO Equity Interests that opt not to grant the releases contained in Article VII of the Plan shall not receive the New HERO Equity Interests and New HERO Warrants that they would otherwise be entitled to receive under the Plan and shall not receive any distribution whatsoever under the Plan. Accordingly, the following Classes of Claims and Equity Interests are not entitled to vote to accept or reject the Plan:

| Class |

Claim or Interest |

Status |

Voting Rights | |||

| 1 | Other Priority Claims | Unimpaired | Deemed to Accept | |||

| 2 | Other Secured Claims | Unimpaired | Deemed to Accept | |||

| 4 | General Unsecured Claims | Unimpaired | Deemed to Accept | |||

| 5 | Intercompany Claims | Unimpaired | Deemed to Accept | |||

| 6 | Intercompany Interests | Unimpaired | Deemed to Accept | |||

| 7 | HERO Equity Interests | Impaired | Deemed to Reject | |||

7

| E. | Cramdown |

Section 1129(b) permits confirmation of a plan of reorganization notwithstanding the non-acceptance of the plan by one or more impaired classes of claims or equity interests, so long as at least one impaired class of claims or interests votes to accept a proposed plan. Under that section, a plan may be confirmed by a bankruptcy court if it does not “discriminate unfairly” and is “fair and equitable” with respect to each non-accepting class.

The Debtors intend to pursue a “cram down” of the holders of HERO Equity Interests in Class 7, who are deemed to have rejected the Plan for the reasons described in subsection D above.

| F. | Allowed Claims |

Only administrative expenses, claims, and equity interests that are “allowed” may receive distributions under a chapter 11 plan. An “allowed” administrative expense, claim or equity interest means that a debtor agrees, or in the event of a dispute, that the Bankruptcy Court determines by Final Order, that the administrative expense, claim or equity interest, including the amount thereof, is in fact a valid obligation of, or equity interest in, a debtor.

| G. | Impairment generally |

Under section 1124 of the Bankruptcy Code, a class of claims or equity interests is “impaired” unless, with respect to each claim or interest of such class, the plan of reorganization (i) does not alter the legal, equitable or contractual rights of the holders of such claims or interests or (ii) irrespective of the holders’ right to receive accelerated payment of such claims or interests after the occurrence of a default, cures all defaults (other than those arising from, among other things, the debtor’s insolvency or the commencement of a bankruptcy case), reinstates the maturity of the claims or interests in the class, compensates the holders of such claims or interests for any damages incurred as a result of their reasonable reliance upon any acceleration rights and does not otherwise alter their legal, equitable or contractual rights.

Only holders of allowed claims or equity interests in impaired classes of claims or equity interests that receive or retain property under a proposed plan of reorganization, but are not otherwise deemed to reject the plan (such as Class 7 HERO Equity Interests in these cases), are entitled to vote on such a plan. Holders of unimpaired claims or equity interests are deemed to accept the plan under section 1126(f) of the Bankruptcy Code and are not entitled to vote. Holders of claims or equity interests that do not receive or retain any property on account of such claims or equity interests are deemed to reject the plan under section 1126(g) of the Bankruptcy Code and are not entitled to vote.

| H. | Solicitation and Voting Process |

Each holder of a Senior Notes Claim as of July 9, 2015 (the “Voting Record Date”) that is an Eligible Noteholder is entitled to vote to accept or reject the Plan and shall receive the Solicitation Package in accordance with the solicitation procedures. Except as otherwise set forth herein, the Voting Record Date and all of the Debtors’ solicitation and voting procedures shall apply to all holders of Claims or Equity Interests and other parties in interest.

The following summarizes the procedures for voting to accept or reject the Plan. Holders of Senior Notes Claims, the only Voting Class under the Plan, are encouraged to review the relevant provisions of the Bankruptcy Code and Bankruptcy Rules and/or to consult their own attorneys.

The “Solicitation Package.”

The following materials are provided to each holder of a Senior Notes Claim that is entitled to vote on the Plan:

| • | the applicable Ballot and voting instructions; |

| • | this Disclosure Statement with all exhibits; and |

| • | the Plan. |

8

If you (a) did not receive a Ballot and believe you are entitled to one; (b) received a damaged Ballot; (c) lost your Ballot; (d) have any questions concerning this Disclosure Statement, the Plan, or the procedures for voting on the Plan, or the Solicitation Package you received; or (e) wish to obtain a paper copy of the Plan, this Disclosure Statement or any exhibits to such documents, please contact Prime Clerk, LLC, the Debtors’ Voting and Claims Agent, at Hercules Balloting, c/o Prime Clerk, LLC, 830 Third Ave., 9th Floor, New York, NY 10022, by calling 844-241-2770 (Toll Free) or 929-342-0757 (International), or by email at herculesballots@primeclerk.com.

Before the deadline to object to Confirmation of the Plan, the Debtors intend to file the Plan Supplement. If the Plan Supplement is updated or otherwise modified, such modified or updated documents will be made available on the Debtors’ restructuring website: cases.primeclerk.com/hercules. The Debtors will not distribute paper or CD-ROM copies of the Plan Supplement; however, parties may obtain a copy of the Plan Supplement by visiting the Debtors’ restructuring website, cases.primeclerk.com/hercules; and/or by calling 844-241-2770 (Toll Free) or 929-342-0757 (International).

Voting Deadlines.

To be counted, your Ballot(s) must be actually received by the Voting and Claims Agent no later than:

| • | August 12, 2015 at 5:00 p.m. (Prevailing Eastern Time) for Holders of Senior Notes Claims entitled to vote on the Plan. This is the “Voting Deadline.” If you do not return your Ballot prior to the Voting Deadline or if you are not an Eligible Noteholder, your vote will not be counted. |

Voting Instructions.

If you are a holder of a Class 3 Senior Notes Claim, a Ballot is enclosed for the purpose of voting on the Plan. BALLOTS ARE ONLY BEING SOLICITED FROM HOLDERS OF CLASS 3 CLAIMS THAT ARE ACCREDITED INVESTORS OR QUALIFIED INSTITUTIONAL BUYERS. THE VOTE OF ANY HOLDER OF A CLASS 3 CLAIM THAT DOES NOT CERTIFY THAT IT IS AN ACCREDITED INVESTOR OR QUALIFIED INSTITUTIONAL BUYER WILL NOT BE COUNTED. IF YOU ARE NOT AN ACCREDITED INVESTOR OR QUALIFIED INSTITUTIONAL BUYER, PLEASE DO NOT COMPLETE THE BALLOT. HOWEVER, PLEASE READ THE NON-ELIGIBLE NOTEHOLDER ELECTION ATTACHED TO THE BALLOT AS EXHIBIT A AND FOLLOW THE INSTRUCTIONS SET FORTH THEREIN IF YOU ELECT TO OPT OUT OF THE RELEASES IN ARTICLE VII.F OF THE PLAN. IF YOU DO NOT COMPLETE AND RETURN THE BENEFICIAL HOLDER ELECTION BY THE VOTING DEADLINE, YOU WILL BE DEEMED TO HAVE GRANTED THE RELEASES IN ARTICLE VII.F OF THE PLAN.

Except as provided below, holders of Claims are required to vote all of their Claims within a Class either to accept or reject the Plan and may not split their votes. Any Ballot received that does not indicate either an acceptance or rejection of the Plan or that indicates both acceptance and rejection of the Plan will be counted as an acceptance. Any Ballot received that is not signed or that contains insufficient information to permit the identification of the holder will be an invalid Ballot and will not be counted.

If you are the record holder of Claims that are beneficially owned by another party, you may submit a separate Ballot with respect to such portion of Claims that are beneficially owned by such third party, and the vote indicated on such separate Ballot may differ from the vote indicated on Ballots submitted with respect to Claims that you beneficially own yourself or that are beneficially owned by other parties. In no event may you submit Ballots with respect to Claims in excess of the amount of Claims for which you are the record holder as of the Voting Record Date.

9

Please sign and complete a separate Ballot with respect to each Claim, and return your Ballot(s) in accordance with the instructions provided by your Nominee (as defined below), so that your Pre-Validated Ballot (as defined below) or the Master Ballot reflecting your vote is received by Prime Clerk by the Voting Deadline. Pre-Validated Ballots or Master Ballots reflecting your vote should be returned to the Debtors’ voting agent, Prime Clerk, by hand delivery, overnight courier, or first class mail to:

Hercules Ballot Processing

c/o Prime Clerk, LLC

830 Third Avenue, 9th Floor

New York, NY 10022

If you are the beneficial owner of a Senior Note Claim, please follow the directions listed on your Ballot and read the Section below titled “Beneficial Owners of the Senior Notes”.

Only Ballots with an original signature will be counted. Email submission of ballots is not permitted. Only Ballots (including Master Ballots submitted by a Nominee) received by Prime Clerk by the Voting Deadline will be counted.

If delivery of a Ballot is by mail, it is recommended that voters use an air courier with guaranteed next day delivery or registered mail, properly insured, with return receipt requested. In all cases, sufficient time should be allowed to ensure timely delivery. The method of such delivery is at the election and risk of the voter.

A Ballot may be withdrawn by delivering a written notice of withdrawal to Prime Clerk, so that Prime Clerk receives the notice before the Voting Deadline. In order to be valid, a notice of withdrawal must (a) specify the name of the creditor who submitted the Ballot to be withdrawn, (b) contain a description of the Claim(s) to which it relates, and (c) be signed by the creditor in the same manner as on the Ballot. The Debtors expressly reserve the right to contest the validity of any withdrawals of votes on the Plan.

After the Voting Deadline, any creditor who has timely submitted a properly completed Ballot to Prime Clerk or a Nominee (defined below), which is then timely delivered to Prime Clerk by the Voting Deadline, may change or withdraw its vote only with the approval of the Bankruptcy Court or the consent of the Debtors (with the consent of the Steering Group). If more than one timely, properly completed Ballot is received with respect to the same Claim and no order of the Bankruptcy Court allowing the creditor to change its vote has been entered before the Voting Deadline, the Ballot that will be counted for purposes of determining whether sufficient acceptances required to confirm the Plan have been received will be the timely, properly-completed Ballot determined by Prime Clerk to have been received last.

Nominees are required to retain for inspection by the Court for one year following the Voting Deadline the Ballots cast by their beneficial holders.

Nominees may elect to pre-validate the Beneficial Holder Ballot (a “Pre-Validated Ballot”) by (i) signing the applicable Beneficial Holder Ballot and including its DTC Participant Number, (ii) indicating on the Beneficial Holder Ballot the account number of such holder, and the principal amount of Notes held by the Nominee for such beneficial holder, and (iii) forwarding the Beneficial Holder Ballot (together with the full Solicitation Package) to the beneficial holder for voting. The beneficial holder must then complete the information requested in the Beneficial Holder Ballot (including indicating a vote to accept or reject the Plan), review the certifications contained therein, and return the Beneficial Holder Ballot directly to the Voting Agent in the pre-addressed, postage paid envelope included with the Solicitation Package so that it is actually received by the Voting Agent on or before the Voting Deadline. A list of beneficial holders to whom the Nominee sent Pre-Validated Ballots should be maintained by the Nominee for inspection for at least one year following the Voting Deadline.

10

Votes cast by the beneficial holders through a Nominee and transmitted by means of a Master Ballot or a Pre-Validated Ballot will be applied against the positions held by such Nominee as evidenced by the list of record holders of Notes provided by the applicable securities depository. The Debtors further propose that votes submitted by a Nominee on a Master Ballot will not be counted in excess of the position maintained by the respective Nominee on the Voting Record Date.8

To the extent that conflicting, double or over-votes are submitted on Master Ballots, the Voting Agent shall attempt to resolve such votes prior to the vote certification in order to ensure that the votes of beneficial holders of Notes are accurately tabulated.

To the extent that such conflicting double or over-votes are not reconcilable prior to the vote certification, the Voting Agent is directed to count votes in respect of each Master Ballot in the same proportion as the votes of the beneficial holders or entitlement holders to accept or reject the Plan submitted on such Master Ballot, but only to the extent of the applicable Nominee’s position on the Voting Record Date in the Notes.

For the purposes of tabulating votes, each beneficial holder shall be deemed (regardless of whether such holder includes interest in the amount voted on its Ballot) to have voted only the principal amount of its securities; any principal amounts thus voted may be thereafter adjusted by the Voting Agent, on a proportionate basis to reflect the corresponding claim amount, including any accrued but unpaid prepetition interest, with respect to the securities this voted.

EACH BALLOT ADVISES HOLDERS OF CLAIMS THAT, IF THEY (1) (A) VOTE TO REJECT THE PLAN OR (B) DO NOT CERTIFY ON THEIR BALLOT THAT THEY ARE AN ACCREDITED INVESTOR OR QUALIFIED INSTITUTIONAL INVESTOR AND (2) DO NOT ELECT TO OPT OUT OF THE RELEASE PROVISIONS CONTAINED IN ARTICLE VII OF THE PLAN, THEY SHALL BE DEEMED TO HAVE CONCLUSIVELY, ABSOLUTELY, UNCONDITIONALLY, IRREVOCABLY AND FOREVER RELEASED AND DISCHARGED ALL CLAIMS AND CAUSES OF ACTION AGAINST THE RELEASED PARTIES IN ACCORDANCE WITH THE PLAN. ACCORDINGLY, IF YOU (1)(A) VOTE TO REJECT THE PLAN OR (B) DO NOT CERTIFY THAT YOU ARE AN ACCREDITED INVESTOR OR QUALIFIED INSTITUTIONAL BUYER AND (2) DO NOT ELECT TO OPT OUT OF THE RELEASE PROVISIONS CONTAINED IN ARTICLE VII OF THE PLAN, YOU WILL BE DEEMED TO HAVE GRANTED THE RELEASES CONTEMPLATED BY SUCH RELEASE PROVISIONS.