Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - PATTERSON UTI ENERGY INC | d942517d8k.htm |

Tudor, Pickering, Holt & Co.

2015 Hotter ‘N Hell Conference

June 17, 2015 Exhibit 99.1 |

Forward Looking Statements

2 This material and any oral statements made in connection with this material

include "forward-looking statements" within the meaning of the

Securities Act of 1933 and the Securities Exchange Act of

1934. Statements made which provide the Company’s or

management’s intentions, beliefs, expectations or predictions

for the future are forward-looking statements and are inherently

uncertain. The opinions, forecasts, projections or other statements other than

statements of historical fact, including, without limitation,

plans and objectives of management of the Company are

forward-looking statements. It is important to note that

actual results could differ materially from those discussed in

such forward-looking statements. Important factors that could cause actual results to differ materially include the risk factors and other

cautionary statements contained from time to time in the Company’s SEC

filings, which may be obtained by contacting the Company or the

SEC. These filings are also available through the Company’s

web site at http://www.patenergy.com

or through the SEC’s Electronic Data Gathering and

Analysis Retrieval System (EDGAR) at http://www.sec.gov.

We

undertake no obligation to publicly update or revise any forward-looking statement.

Statements made in this presentation include non-GAAP financial

measures. The required reconciliation to GAAP financial

measures are included on our website and at the end of this

presentation. |

Patterson-UTI Energy is a leading

provider of contract drilling and

pressure pumping services

3 |

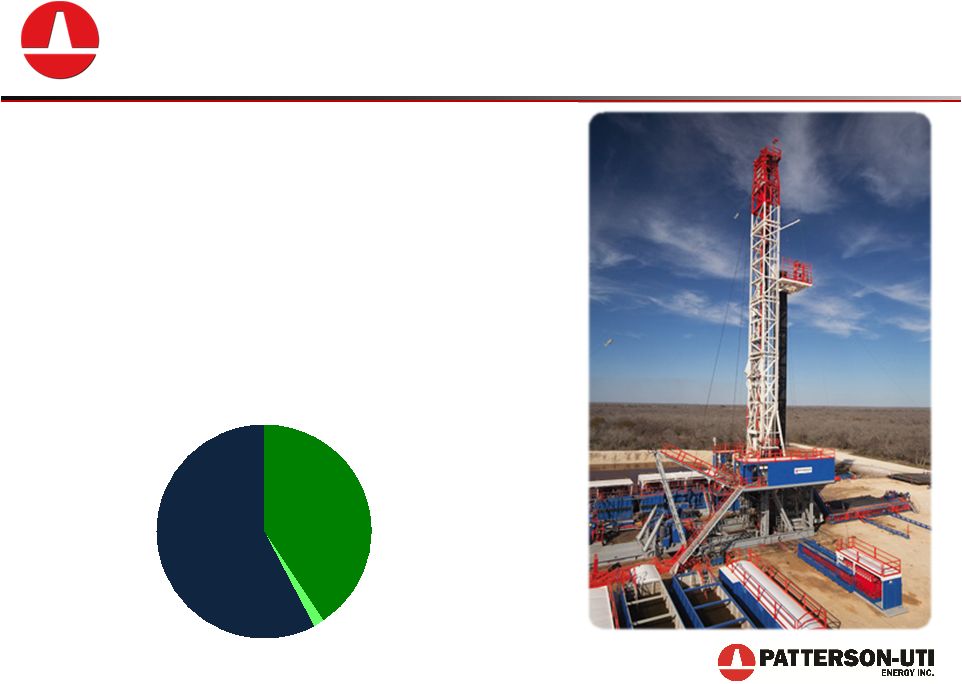

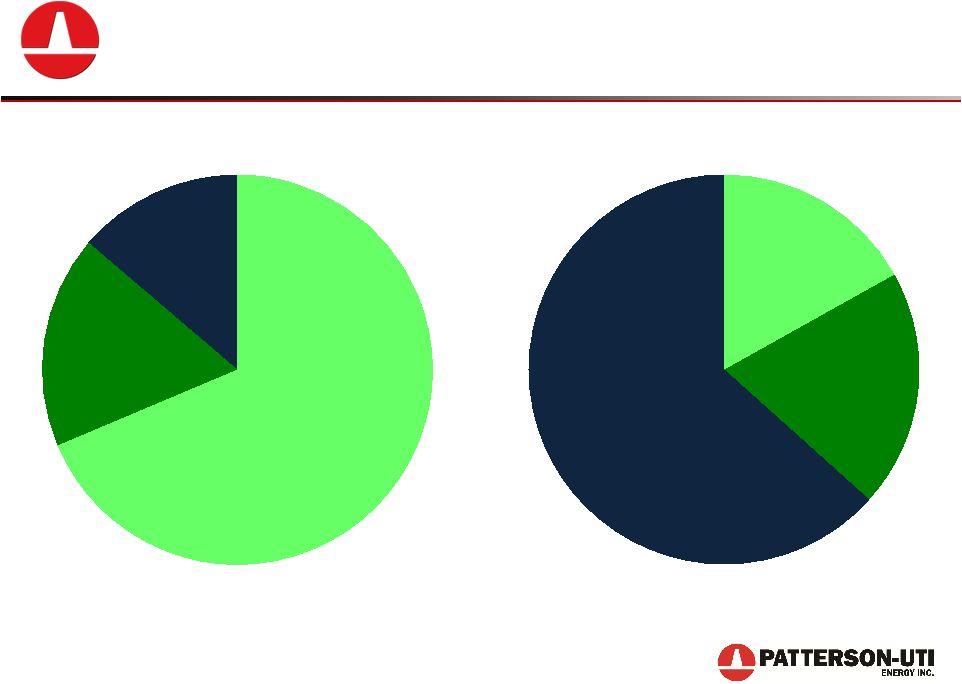

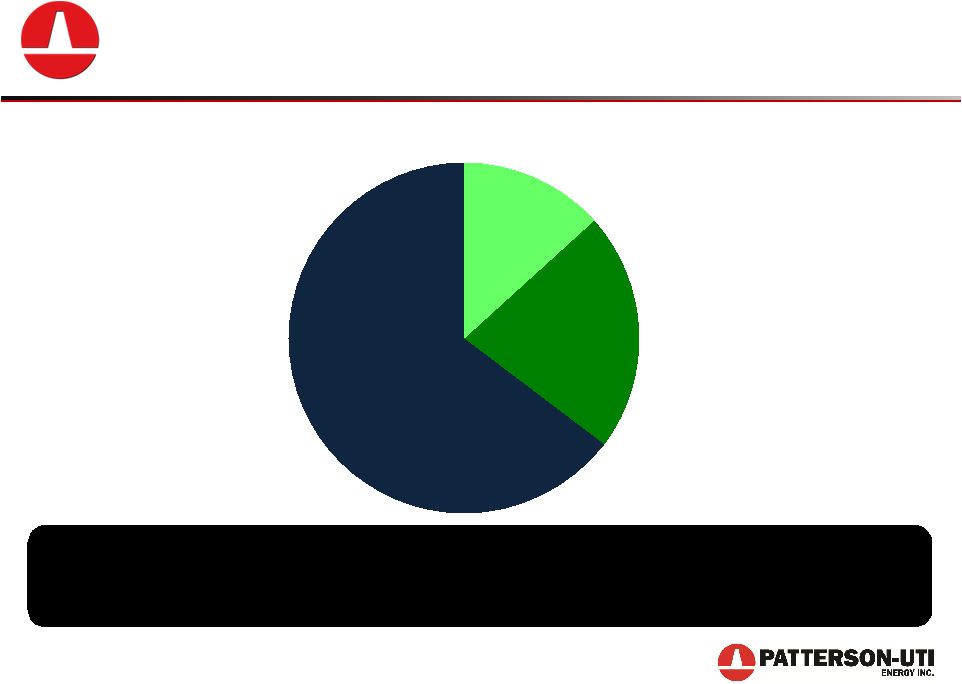

Contract Drilling

• High quality fleet of land drilling rigs including 156 APEX ® rigs • Leader in walking rig technology for pad drilling applications • Large footprint across North American drilling markets Pressure Pumping 41% Oil & Natural Gas 1% Contract Drilling 58% Components of Revenue Patterson-UTI reported results for the year ended December 31, 2014 4 |

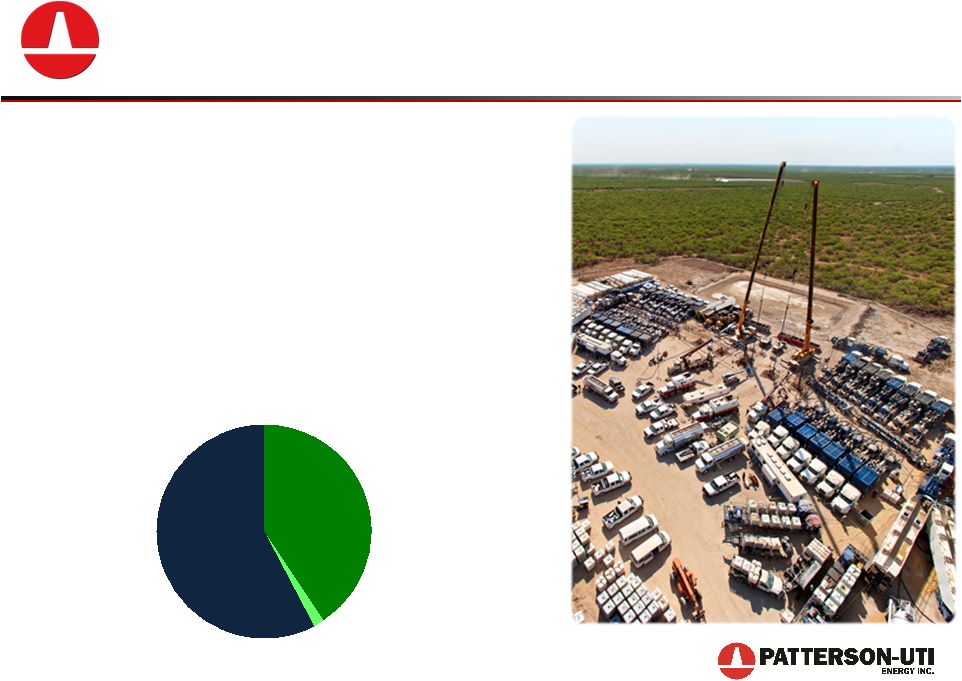

Pressure Pumping

• High quality fleet of modern pressure pumping equipment • A leader in natural gas bi-fuel technology • Strong reputation for regional knowledge and efficient operations Patterson-UTI reported results for the year ended December 31, 2014 5 Pressure Pumping 41% Oil & Natural Gas 1% Contract Drilling 58% Components of Revenue |

Contract Drilling |

Improved Performance

0%

20%

40%

60%

80%

100%

120%

U.S. Rig Count Downturn

0%

20%

40%

60%

80%

100%

120%

2008 - 2009 Total Baker Hughes U.S. Land Rig Count: -53% Total PTEN U.S. Rig Count: -77% 2014 - 2015 Total PTEN U.S. Rig Count: -47% Total Baker Hughes U.S. Land Rig Count: -56% Baker Hughes and Patterson-UTI U.S. Land Rig Counts as of June 12, 2015

7 |

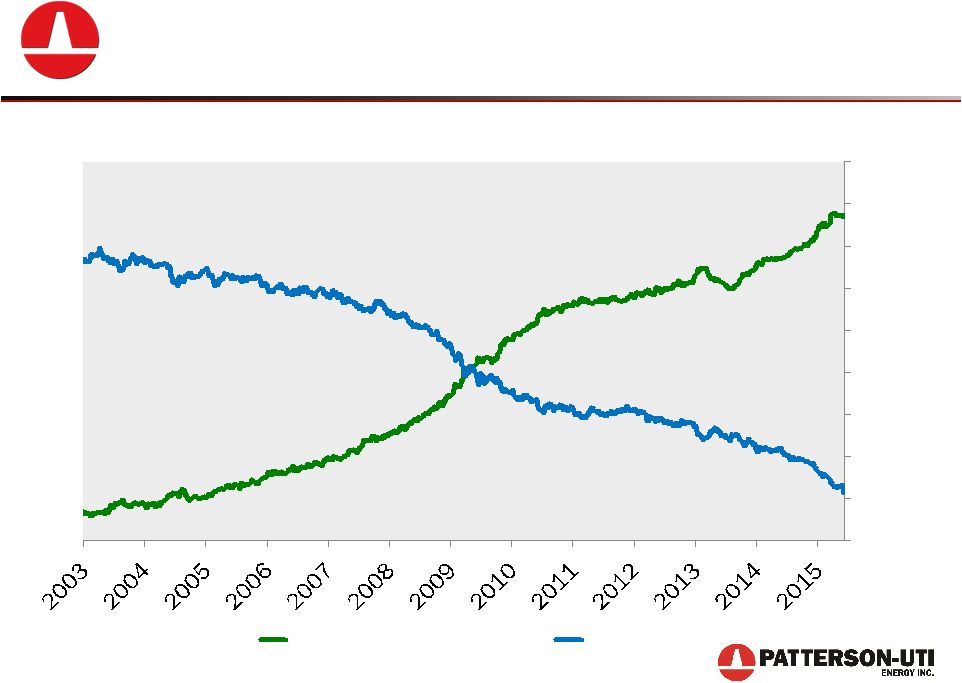

A

Rig Fleet Transformation 8

Other

Electric

APEX®

Mechanical Patterson-UTI Energy Total Rig Fleet Other Electric APEX® Mechanical December 2009 Projected December 2015 |

…and Expected as of December 31, 2015

APEX-XK 1500

® APEX-XK 1000™ APEX WALKING ® APEX 1500 ® APEX 1000 ® Total APEX ® Rigs Class APEX ® Rigs as of June 12, 2015 53 4 49 44 11 161 12/31/2015 A leader in high specification drilling rigs 48 4 49 44 11 156 6/12/2015 APEX ® Rig Fleet 9 |

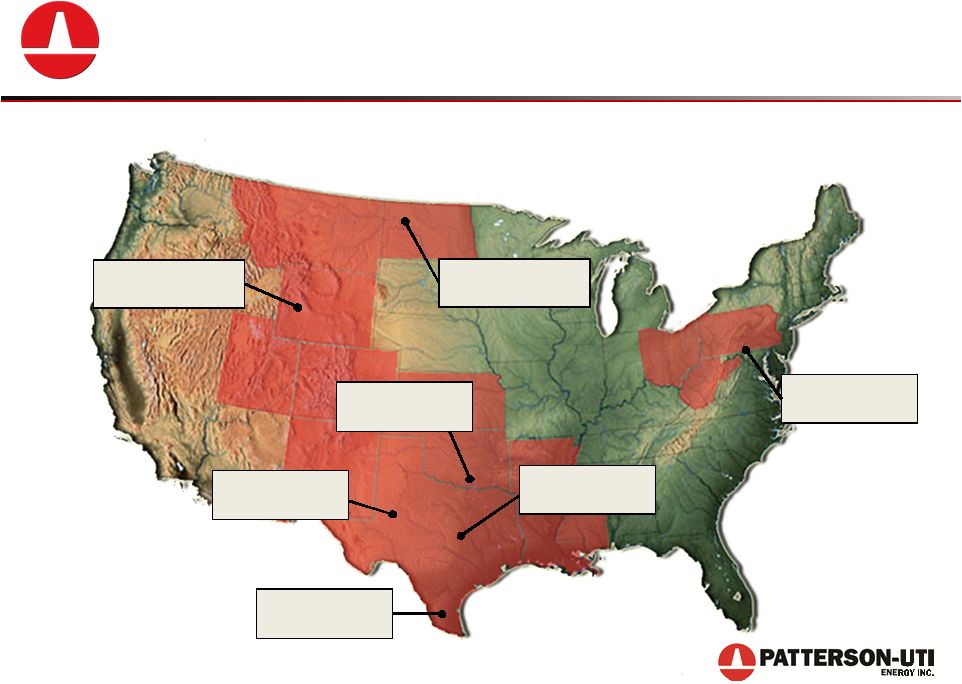

West Texas 24 Rigs Large Geographic Footprint 10 PTEN’s Active U.S. Land Drilling Rigs as of June 12, 2015 Appalachia 23 Rigs East Texas 15 Rigs Mid-Continent 8 Rigs Mid-Continent 8 Rigs Rockies 9 Rigs South Texas 21 Rigs North Dakota 13 Rigs |

Patterson-UTI Energy

…the impact of APEX ® rigs has been transformative! |

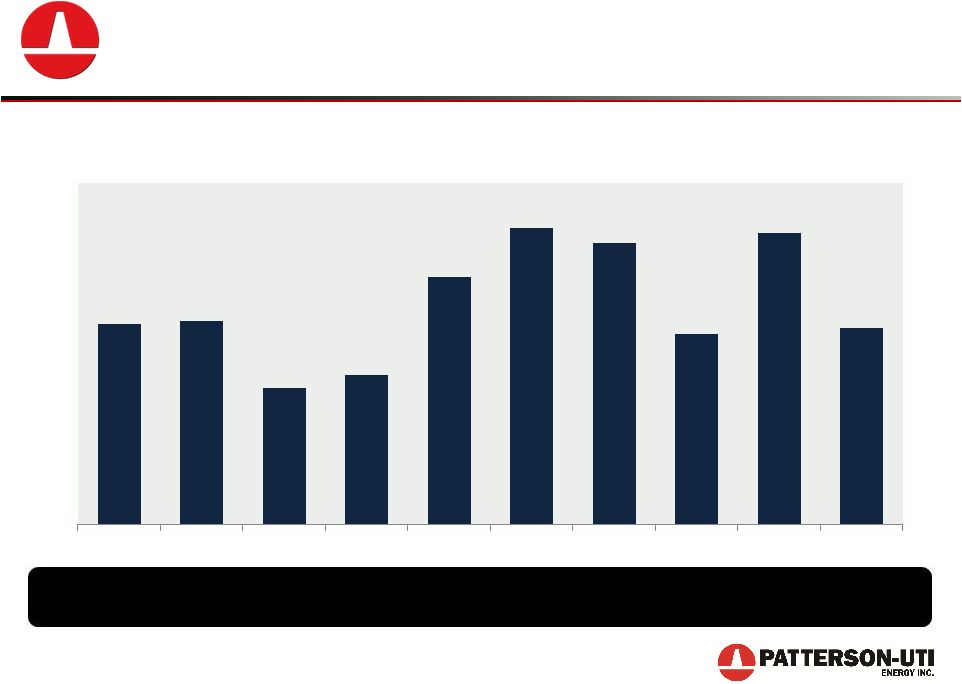

Increasing APEX

® Drilling Activity 12 0 20 40 60 80 100 120 140 160 Active APEX ® Rig Count |

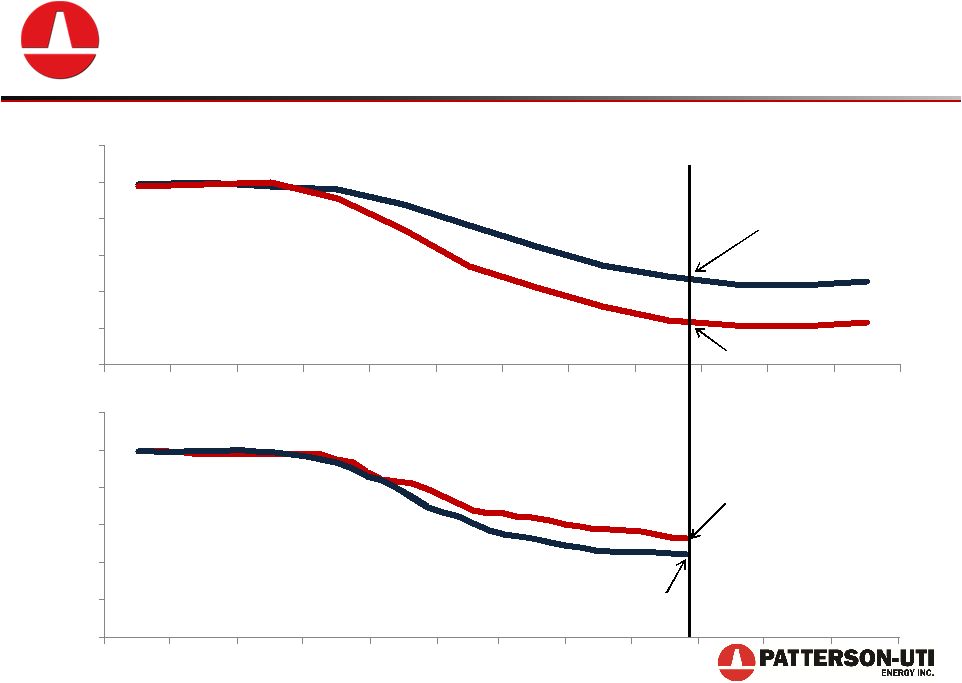

PTEN Relative Active Rig Count by Rig Class

13 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% APEX® Other Electric Mechanical |

Greater Stability of Utilization

14 0% 20% 40% 60% 80% 100% 120% APEX ® Rig Utilization |

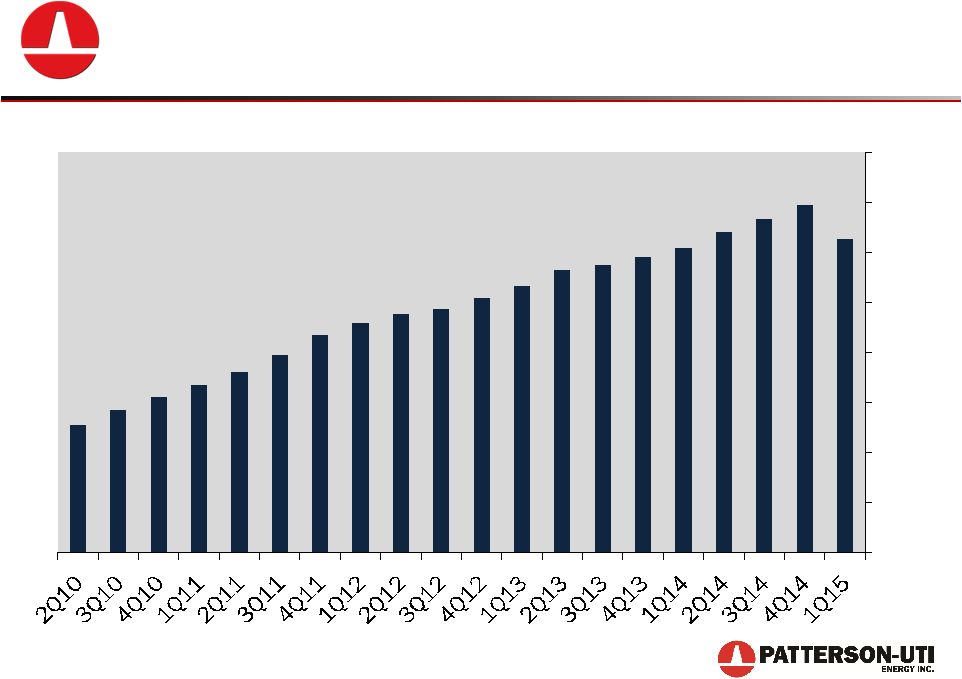

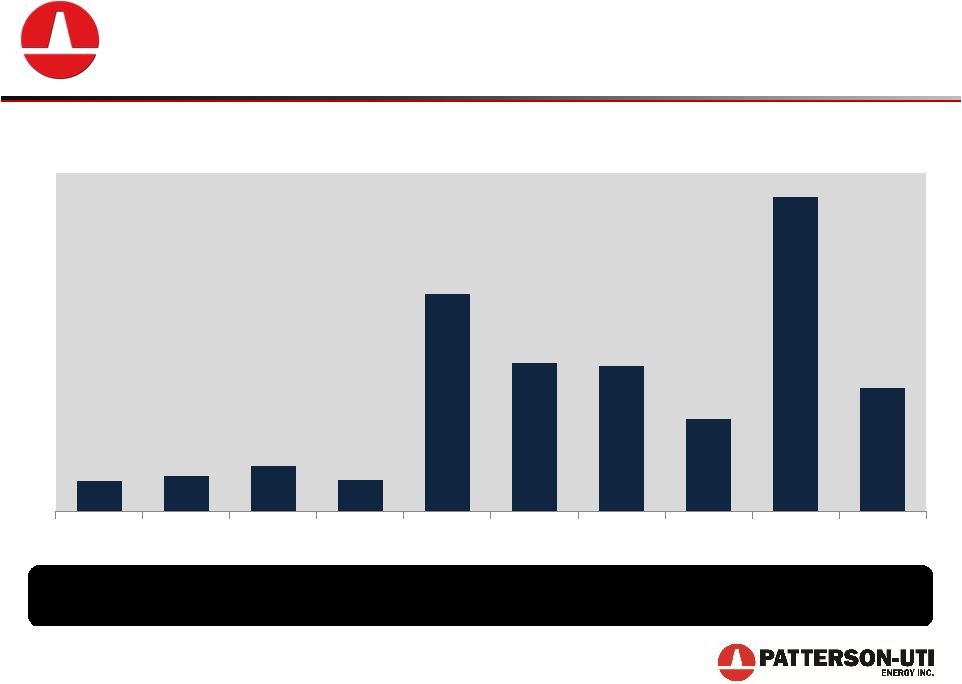

Improving Average Rig Revenue Per Day

15 10,000 12,000 14,000 16,000 18,000 20,000 22,000 24,000 26,000 Patterson-UTI Total Average Rig Revenue Per Day Excludes early-termination revenues during the third and fourth quarter of 2013 of $3,600 per day and $130 per

day, respectively, and early-termination revenues during the first quarter

of 2015 of $1,020 per day. |

Adjusted EBITDA Contribution from

High Specification Rigs

16 2010 2011 2012 2013 2014 2015 APEX® & Other Electric Mechanical Preferred rigs account for approximately 91% of Adjusted EBITDA in Contract Drilling Excludes early-termination revenues during the third and fourth quarter of 2013 of $62.8 million and $2.4 million,

respectively, and early-termination revenue during the first quarter of 2015

of $15.8 million. |

Patterson-UTI Energy

…the APEX ® rig outlook remains strong! |

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% % Horizontal % Vertical 18 U.S. Rig Count % by Drilling Type Continued Demand for APEX ® Rigs Source: Baker Hughes North America Rotary Rig Count |

SCR AC Mechanical AC-powered rigs have increased as a percentage of the horizontal rig count Total U.S. Horizontal Rig Count by Power Type Continued Demand for APEX ® Rigs Analysis from Patterson-UTI Energy based on data from RigData and company filings. 19 |

Patterson-UTI Energy

…Patterson-UTI is a technology leader!

|

APEX WALKING ® Rigs 21 • Capable of walking with drill pipe and collars racked in the mast • Full multi-directional walking capability • Walking times average 45 minutes for 10’ – 15’ well spacing http://patenergy.com/drilling/technology/apexwalk 21 |

Strong Demand for Pad Drilling

22 • Pad drilling is contributing to increasing rig efficiency • Pad drilling capable rigs are highly utilized • Most new APEX ® rigs are expected to have walking systems http://patenergy.com/drilling/technology 22 |

APEX-XK ® Rig Walking on Pad 23 http://patenergy.com/drilling/technology/apexwalk/ Video of APEX-XK ® Rig 23 |

The APEX-XK ® 24 • Enhanced mobility including more efficient rig up and rig down • Greater clearance under rig floor for optional walking system • Advanced environmental spill control integrated into drilling floor • Minimized number of truck loads for rig moves • Available in both 1500 HP and 1000 HP http://patenergy.com/drilling/technology 24 |

Enhancing our Position in Pad Drilling

25 Walking Systems Can be Added to Any Rig in Our Fleet… …Allowing for True Multi-Directional Pad Drilling Capabilities 25 |

Enhancing our Position in Pad Drilling

26 http://patenergy.com/drilling/technology 26 |

Early Adopter of Natural Gas Engines

27 http://patenergy.com/drilling/technology 27 |

Pressure Pumping |

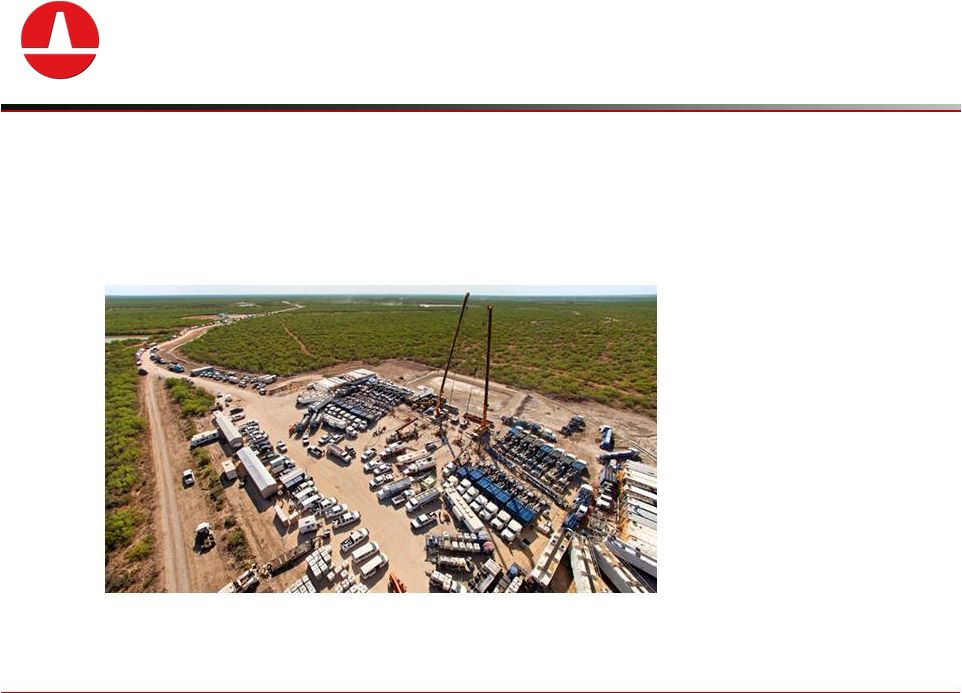

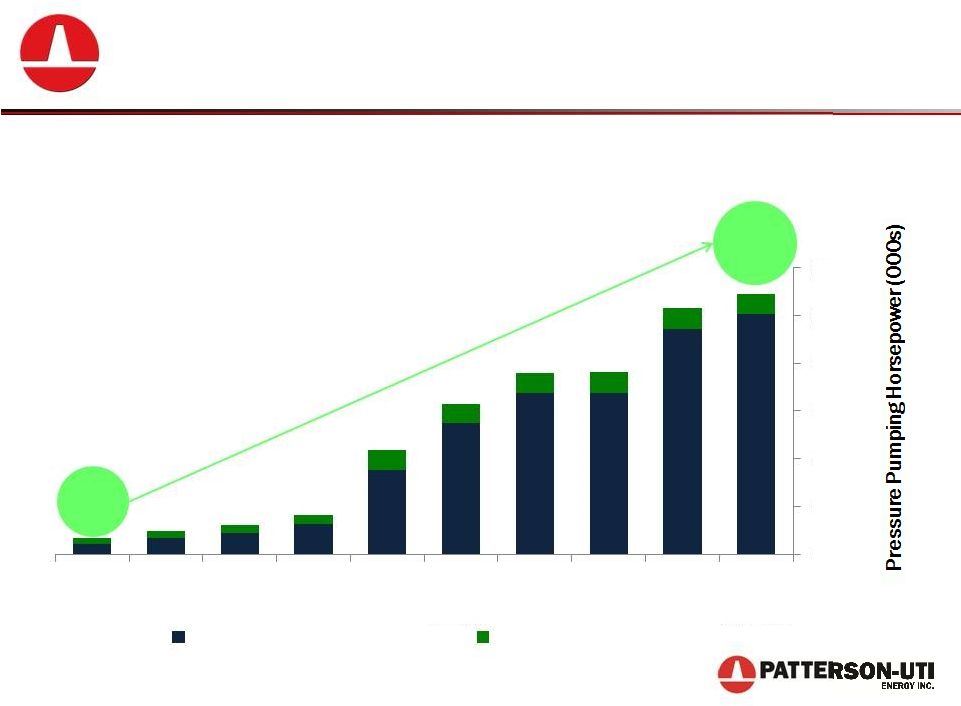

Growing Pressure Pumping Business

29 Investments in Pressure Pumping… …Have Increased Fleet Size and Quality 65 1,100 2006 2007 2008 2009 2010 2011 2012 2013 2014 June 0 200 400 600 800 1000 1200 Fracturing Horsepower Other Horsepower Period End 2015E |

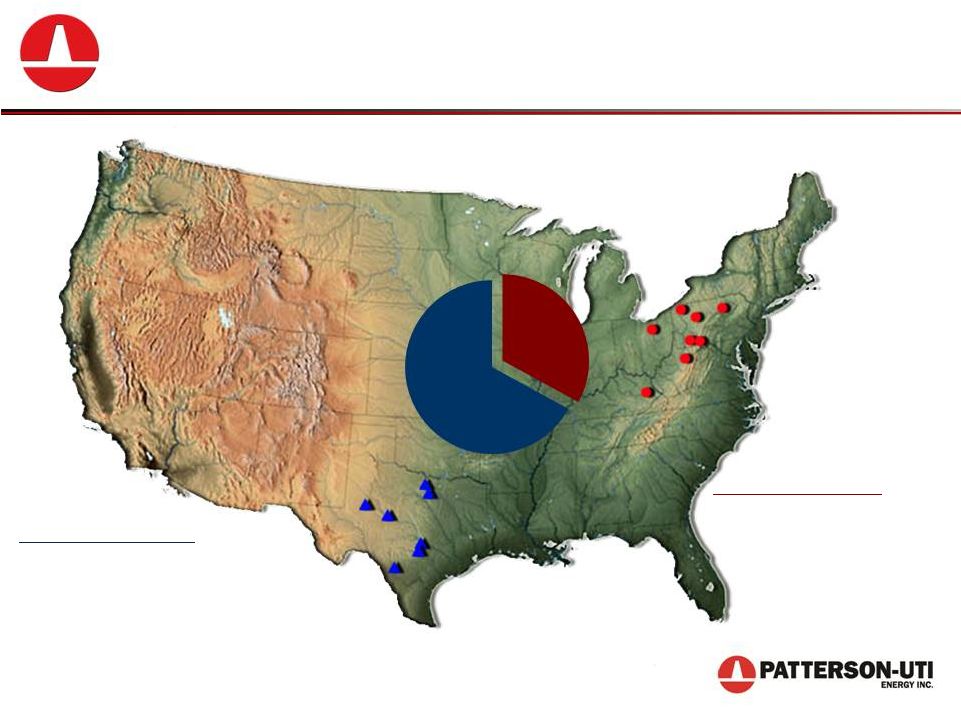

Southwest Region:

Northeast Region:

Fracturing horsepower: 663,800

Other horsepower: 32,165

Fracturing horsepower: 326,30

Other horsepower: 55,400

A Significant Player in Regional Markets

Pressure Pumping Areas

30 Horsepower distribution as of March 31, 2015 Fracturing Horsepower 33% 67% |

A Leader in Bi-Fuel Technology

• Engines can burn a fuel mix comprised of up to 70% natural gas • Comparable torque and horsepower to an all diesel engine • Reduces operating costs by lowering fuel costs • Good for environmental sustainability http://patenergy.com/pressurepumping/services 31 |

A Leader in Bi-Fuel Technology

32 http://patenergy.com/pressurepumping/services 32 |

A Leader in Bi-Fuel Technology

33 • One of the largest bi-fuel frac fleets in the Marcellus • Approximately 1,950 stages completed using natural gas as a fuel source • Replaced approximately 1.3 million gallons of diesel with cleaner burning natural gas • Eliminated 9.6 million pounds of transportation loads on local roads http://patenergy.com/pressurepumping/services 33 |

Comprehensive Lab Services

http://patenergy.com/pressurepumping/services

34 |

Financial Flexibility |

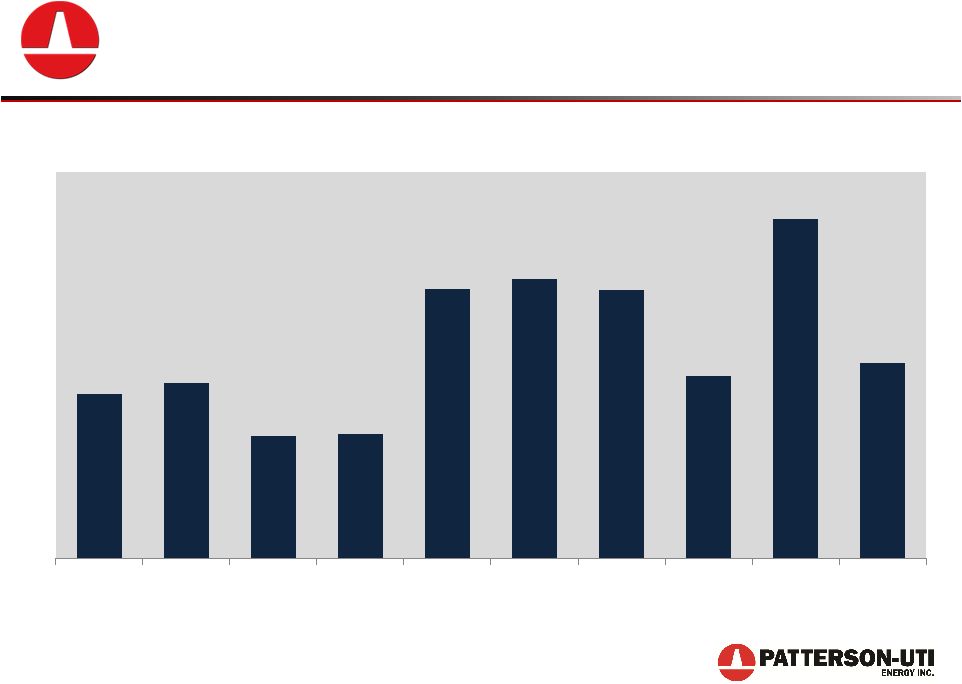

Investing in Our Company

36 $598 $637 $445 $453 $976 $1,012 $974 $662 $1,229 $710 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E Year End Capital Expenditures and Acquisitions ($ in millions) 2015 Capital expenditure forecast as of April 23, 2015 |

Strong Financial Position

37 • History of returning capital to investors – Cash Dividend • Initiated cash dividend in 2004 • Doubled quarterly cash dividend to $0.10 per share in February 2014 – Stock Buyback • Total of $857 million repurchased since 2005 • Approximately $187 million remaining authorization as of March 31, 2015 • Returned approximately $1.3 billion to shareholders since 2005 |

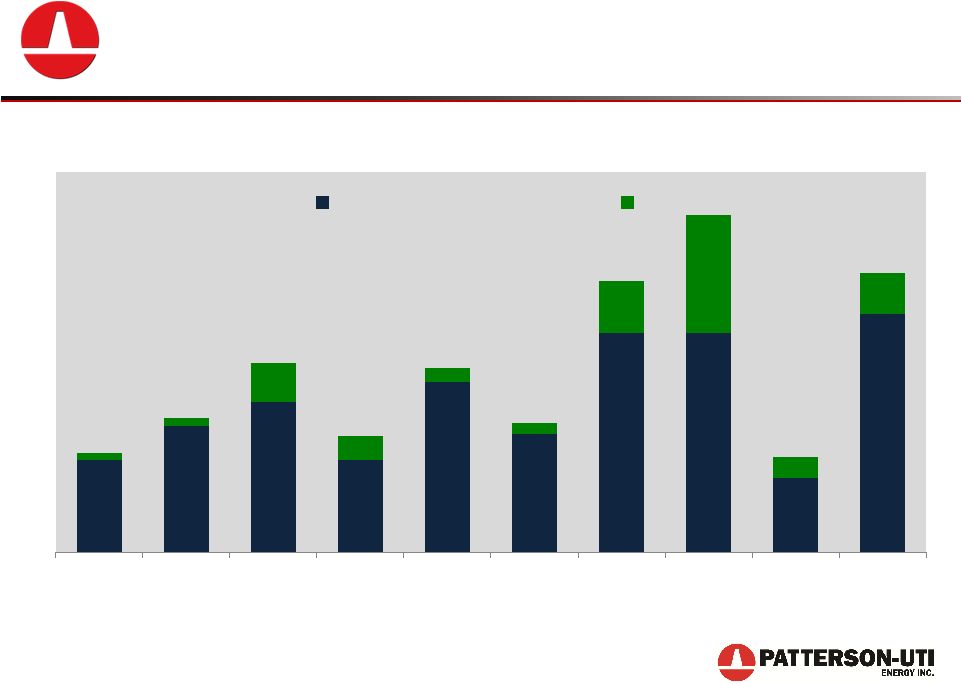

Strong Financial Position

38 2006 2007 2008 2009 2010 2011 2012 2013 2014 1Q15 Period End Line of Credit Availability Cash Total Liquidity ($ in millions) Liquidity defined as end of period cash plus availability under revolving line of credit |

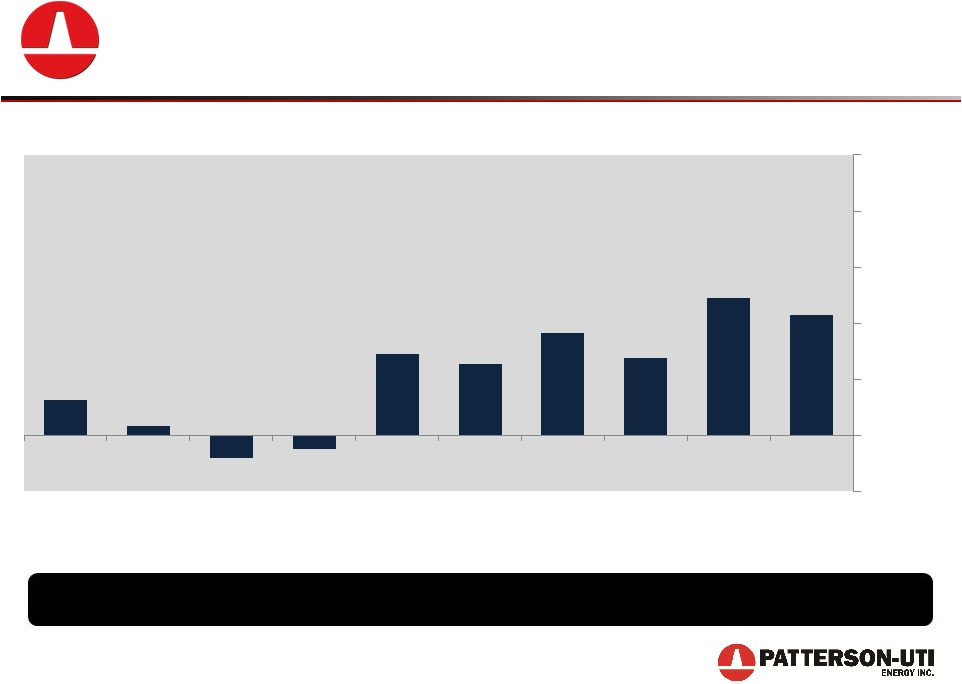

Strong Financial Position

39 6% 2% -4% -2% 15% 13% 18% 14% 24% 21% -10% 0% 10% 20% 30% 40% 50% 2006 2007 2008 2009 2010 2011 2012 2013 2014 1Q15 Period End Net Debt to Capital Ratio $600 million of debt not due until at least 2020 |

Why Invest in Patterson-UTI Energy?

• Continuing Transformation – Committed to high-spec land rigs where demand remains strong – Creating value through focus on well site execution • Technology leader – Leader in walking rigs for pad drilling – Innovator in use of natural gas as a fuel source for both drilling and pressure pumping • Financially flexible – Strong balance sheet – History of share buybacks – Dividends 40 |

Additional References |

42 Contract Drilling Capital Expenditures and Acquisitions ($ in millions) Investing in Our Drilling Rig Fleet 2015 Capital expenditure forecast as of April 23, 2015 $531 $540 $361 $395 $656 $785 $745 $505 $772 $520 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E More than $5 billion invested since 2005 |

Investing in Pressure Pumping

43 $41 $48 $61 $43 $289 $198 $194 $123 $418 $165 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E Pressure Pumping Capital Expenditures and Acquisitions ($ in millions) More Than $1.4 billion invested since 2005 2015 Capital expenditure forecast as of April 23, 2015 |

Strong Financial Position • Total liquidity of approximately $587 million – $86.9 million of cash at March 31, 2015 – $500 million revolver availability at April 27, 2015 • $793.1 million net debt at March 31, 2015 – 21.5% Net Debt/Total Capitalization – $300 million of 4.97% Series A notes due October 5, 2020 – $300 million of 4.27% Series B notes due June 14, 2022 – $280 million of term loans maturing September 27, 2017 • No equity sales in last 14 years • Reduced share count by 25.6 million shares since 2005 44 |

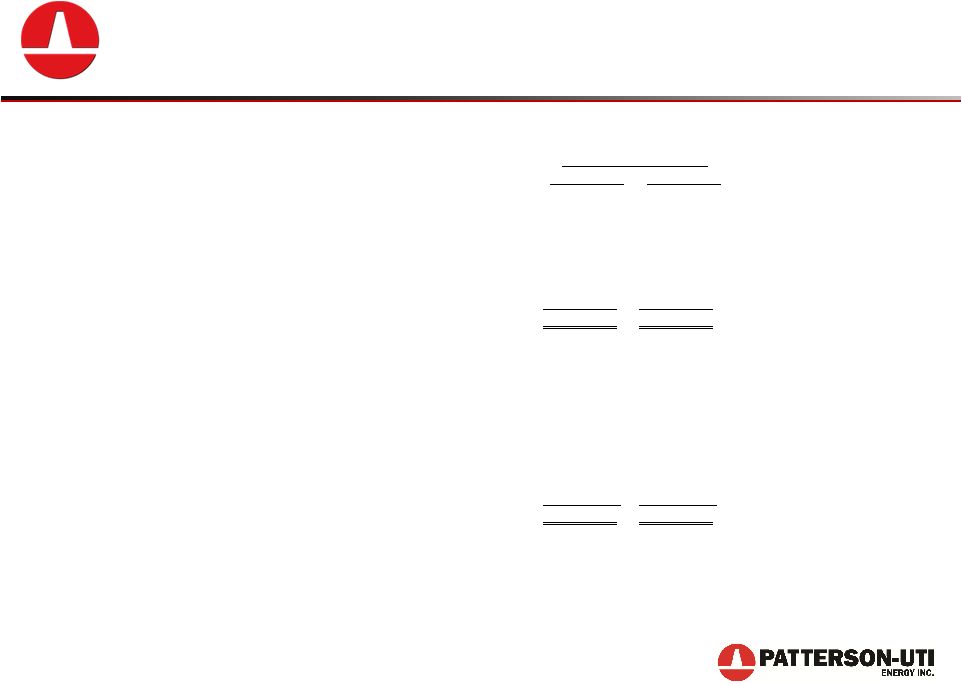

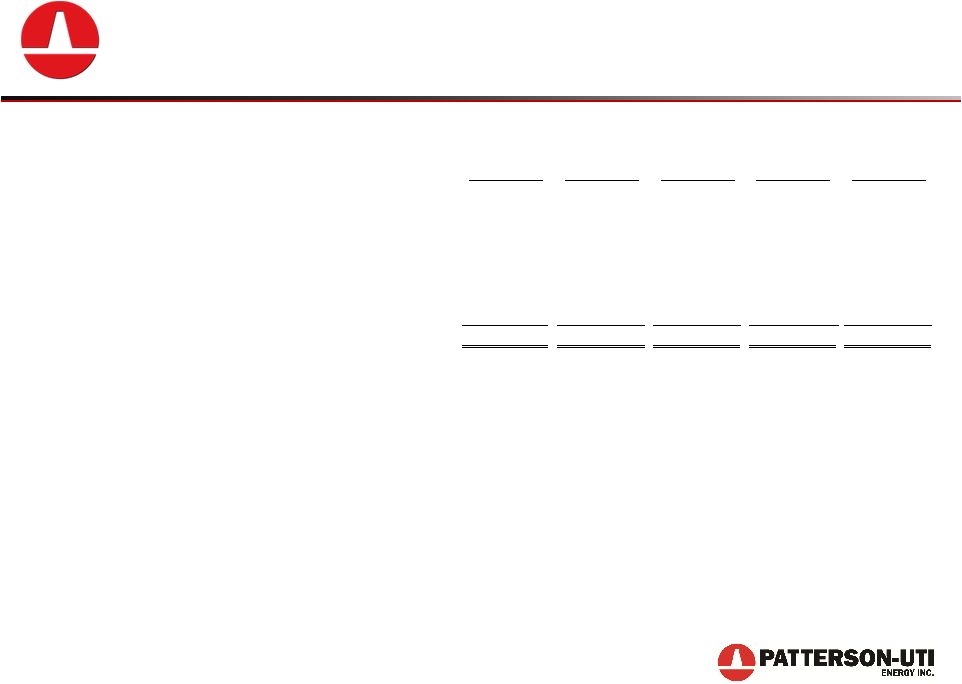

Three Months Ended March 31, Twelve Months Ended December 31, 2015 2014 2014 2013 Adjusted Earnings Before Interest, Taxes, Depreciation and Amortization

(Adjusted EBITDA)(1):

Net income

$

9,125

$

34,822

$

162,664

$

188,009

Income tax expense

6,720

16,942

91,619

108,432

Net interest expense

8,258

7,012

28,846

27,441

Depreciation, depletion, amortization and

impairment 175,382

147,322

718,730

597,469

Adjusted EBITDA

$

199,485

$

206,098

$1,001,859

$

921,351

Total revenue

$

657,699

$

678,168

$3,182,291

$2,716,034

Adjusted EBITDA margin

31.5%

33.9%

Adjusted EBITDA by operating segment:

Contract drilling

$

765,874

$

704,990

Pressure pumping

31,903

35,585

236,676

217,228

Oil and natural gas

3,702

8,730

37,094

44,348

Corporate and other

(11,090)

(11,413)

(37,785)

(45,215)

Consolidated Adjusted EBITDA

$

199,485

$

206,098

$1,001,859

$

921,351

(1)

The company makes use of financial measures that are not

calculated in accordance with U.S. generally accepted accounting principles (“GAAP”) to help in the assessment of ongoing operating performance. These non-GAAP financial measures are reconciled to their most directly

comparable GAAP measures in the tables above. We

define Adjusted EBITDA as net income plus net interest expense, income tax expense and depreciation, depletion, amortization and impairment expense. We present Adjusted EBITDA because we believe it provides additional information with respect to both the performance of

our fundamental business activities and our

ability to meet our capital expenditures and working capital requirements. Adjusted EBITDA is not defined by GAAP and, as such, should not be construed as an

alternative to net income (loss) or operating cash flow. We

define margin as revenues less direct operating costs. We present margin because we believe it to be the component of our earnings most impacted by the variability in our contract drilling and pressure pumping operations.

Margin is not defined by GAAP and, as such, should

not be construed as an alternative to net income (loss). PATTERSON-UTI

ENERGY, INC. Non-GAAP Financial Measures (Unaudited)

(dollars in thousands)

Non-GAAP Financial Measures

45

$

174,970

$

173,196

30.3%

30.4% |

Non-GAAP Financial Measures 46 2014 2013 2012 2011 2010 Adjusted Earnings Before Interest, Taxes, Depreciation and Amortization

(Adjusted EBITDA)(1):

Net income (loss)

$

162,664

$

188,009

$

299,477

$

322,413

$

116,942

Income tax expense (benefit)

91,619

108,432

176,196

187,938

72,856

Net interest expense (income)

28,846

27,441

22,196

15,465

11,098

Depreciation, depletion, amortization and

impairment 718,730

597,469

526,614

437,279

333,493

Net

impact of discontinued operations

(209)

1,778

Adjusted EBITDA

$

1,001,859

$

921,351

$

1,024,483

$

962,886

$

536,167

Total revenue

$

3,182,291

$

2,716,034

$

2,723,414

$

2,565,943

$

1,462,931

Adjusted EBITDA margin

31.5%

33.9%

37.6%

37.5%

36.7%

(1) The company makes use of

financial measures that are not calculated in accordance with U.S. generally accepted accounting principles (“GAAP”) to help in the assessment of

ongoing operating performance. These

non-GAAP financial measures are reconciled to their most directly comparable GAAP measures in the tables above. We define Adjusted EBITDA as net income plus net interest expense, income tax expense and depreciation, depletion, amortization and

impairment expense. We present Adjusted EBITDA because we believe it provides additional information with respect to both the performance of our fundamental business activities

and our ability to meet our capital expenditures

and working capital requirements.

Adjusted EBITDA is not defined by GAAP and, as such, should not

be construed as an alternative to net income

(loss) or operating cash flow. We define margin as

revenues less direct operating costs. We present

margin because we believe it to be the component of our earnings most impacted by the variability in our contract drilling and pressure pumping operations. Margin is not defined by GAAP and, as such, should not be construed as

an alternative to net income (loss). PATTERSON-UTI ENERGY,

INC. Non-GAAP Financial Measures (Unaudited)

(dollars in thousands)

-

-

- |