Attached files

| file | filename |

|---|---|

| 8-K - 8-K - RYLAND GROUP INC | d942671d8k.htm |

| EX-3.1 - EX-3.1 - RYLAND GROUP INC | d942671dex31.htm |

| EX-2.1 - EX-2.1 - RYLAND GROUP INC | d942671dex21.htm |

| EX-10.1 - EX-10.1 - RYLAND GROUP INC | d942671dex101.htm |

| EX-99.3 - EX-99.3 - RYLAND GROUP INC | d942671dex993.htm |

| EX-99.1 - EX-99.1 - RYLAND GROUP INC | d942671dex991.htm |

| Exhibit 99.2

|

Standard Pacific and Ryland merge nearly a century of experience to form an all-new leading homebuilder

June 15, 2015

|

|

DISCLAIMER

Cautionary Statement Regarding Forward-Looking Statements

This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are typically identified by words or phrases such as “may,” “will,” “could,” “should,” “would,” “anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “believe,” “target,” “prospects,” “potential” and “forecast,” and other words, terms and phrases of similar meaning. Forward-looking statements involve estimates, expectations, projections, goals, forecasts, assumptions, risks and uncertainties. The Ryland Group, Inc. (“Ryland”) and Standard Pacific Corp. (“Standard Pacific”) caution readers that any forward-looking statement is not a guarantee of future performance and that actual results could differ materially from those contained in the forward-looking statement. Such forward-looking statements include, but are not limited to, statements regarding the anticipated closing date of the transaction, the ability to obtain stockholder approvals and satisfy the other conditions to the closing of the transaction, the successful closing of the transaction and the integration of Ryland and Standard Pacific as well as opportunities for operational improvement including but not limited to cost reduction and capital investment, the strategic opportunity and perceived value to Ryland’s and Standard Pacific’s respective stockholder of the transaction, the transaction’s impact on, among other things, the combined company’s prospective business mix, margins, transitional costs and integration to achieve the synergies and the timing of such costs and synergies and earnings.

With respect to these statements, Ryland and Standard Pacific have made assumptions regarding, among other things, whether and when the proposed transaction will be approved; whether and when the proposed transaction will close; the results and impacts of the proposed transaction; competitive conditions in Ryland’s and Standard Pacific’s businesses and possible adverse actions of their respective customers, competitors and suppliers. Further, Ryland’s and Standard Pacific’s businesses are subject to a number of general risks that would affect any such forward-looking statements including, among others, decreases in demand for their products; increases in energy, raw materials, shipping and capital equipment costs; reduced supply of raw materials; fluctuations in selling prices and volumes; intense competition; the potential loss of certain customers; and adverse changes in general market and industry conditions. Such risks and other factors that may impact management’s assumptions are more particularly described in Ryland’s and Standard Pacific’s filings with the Securities and Exchange Commission (the “SEC”). The information contained herein speaks as of the date hereof and neither Ryland nor Standard Pacific have or undertake any obligation to update or revise their forward-looking statements, whether as a result of new information, future events or otherwise.

Additional Information and Where to Find It

In connection with the proposed merger, Standard Pacific plans to file with the SEC a registration statement on Form S-4 that will include a joint proxy statement of Ryland and Standard Pacific that also constitutes a prospectus of the surviving corporation. Ryland and Standard Pacific will make the joint proxy statement/prospectus available to their respective stockholders. Investors are urged to read the joint proxy statement/prospectus when it becomes available, because it will contain important information. The registration statement, definitive joint proxy statement/prospectus and other documents filed by Ryland and Standard Pacific with the SEC will be available free of charge at the SEC’s website (www.sec.gov) and from Ryland and Standard Pacific. In addition, security holders will be able to obtain free copies of the Registration Statement and the joint proxy statement/prospectus from Ryland by going to its investor relations page of its corporate website at http://www.ryland.com and from Standard Pacific on its investor relations pages of its corporate website at http://www. standardpacifichomes.com.

Participants in the Solicitation

Ryland, Standard Pacific, their respective directors, executive officers and employees may be deemed to be participants in the solicitation of proxies from Ryland’s and Standard Pacific’s stockholders in connection with the proposed transaction. Information about the directors and executive officers of Ryland and their ownership of Ryland stock is set forth in Ryland’s annual report on Form 10-K for the fiscal year ended December 31, 2014, which was filed with the SEC on February 25, 2015 and its proxy statement for its 2015 annual meeting of stockholders, which was filed with the SEC on March 13, 2015. Information regarding Standard Pacific’s directors and executive officers is contained in Standard Pacific’s annual report on Form 10-K for the fiscal year ended December 31, 2014, which was filed with the SEC on February 23, 2015, and its proxy statement for its 2015 annual general meeting of stockholders, which was filed with the SEC on April 24, 2015. These documents can be obtained free of charge from the sources indicated above. Certain directors, executive officers and employees of Ryland and Standard Pacific may have direct or indirect interest in the transaction due to securities holdings, vesting of equity awards and rights to severance payments. Additional information regarding the participants in the solicitation of Ryland and Standard Pacific stockholders will be included in the joint proxy statement/prospectus.

No Offer or Solicitation

This presentation shall not constitute an offer to sell or the solicitation of an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended.

| 2 |

|

|

|

WELCOME

E

Today’s announcement and call presented by:

Scott Stowell Larry Nicholson

President & CEO President & CEO Standard Pacific Ryland

Jeff McCall Gordon Milne

EVP & CFO EVP & CFO Standard Pacific Ryland

3

|

|

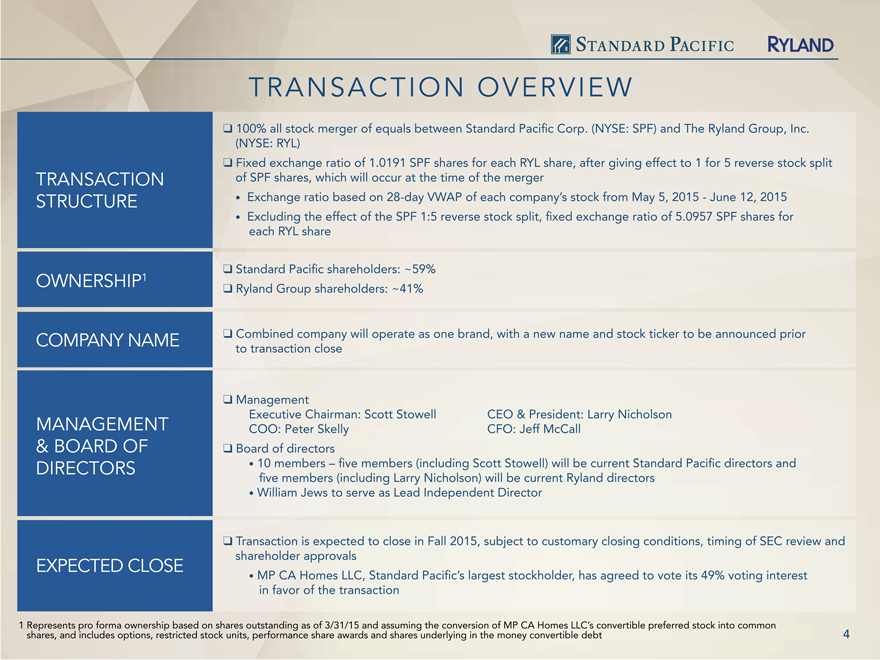

TRANSACTION OVERVIEW

q 100% all stock merger of equals between Standard Pacific Corp. (NYSE: SPF) and The Ryland Group, Inc. (NYSE: RYL) q Fixed exchange ratio of 1.0191 SPF shares for each RYL share, after giving effect to 1 for 5 reverse stock split TRANSACTION of SPF shares, which will occur at the time of the merger STRUCTURE • Exchange ratio based on 28-day VWAP of each company’s stock from May 5, 2015—June 12, 2015 • Excluding the effect of the SPF 1:5 reverse stock split, fixed exchange ratio of 5.0957 SPF shares for each RYL share

q Standard Pacific shareholders: ~59%

OWNERSHIP1

q Ryland Group shareholders: ~41%

COMPANY NAME q Combined company will operate as one brand, with a new name and stock ticker to be announced prior to transaction close

q Management

Executive Chairman: Scott Stowell CEO & President: Larry Nicholson MANAGEMENT COO: Peter Skelly CFO: Jeff McCall

& BOARD OF q Board of directors

DIRECTORS • 10 members – five members (including Scott Stowell) will be current Standard Pacific directors and five members (including Larry Nicholson) will be current Ryland directors • William Jews to serve as Lead Independent Director

q Transaction is expected to close in Fall 2015, subject to customary closing conditions, timing of SEC review and shareholder approvals

EXPECTED CLOSE

• MP CA Homes LLC, Standard Pacific’s largest stockholder, has agreed to vote its 49% voting interest in favor of the transaction

1 Represents pro forma ownership based on shares outstanding as of 3/31/15 and assuming the conversion of MP CA Homes LLC’s convertible preferred stock into common shares, and includes options, restricted stock units, performance share awards and shares underlying in the money convertible debt 4

|

|

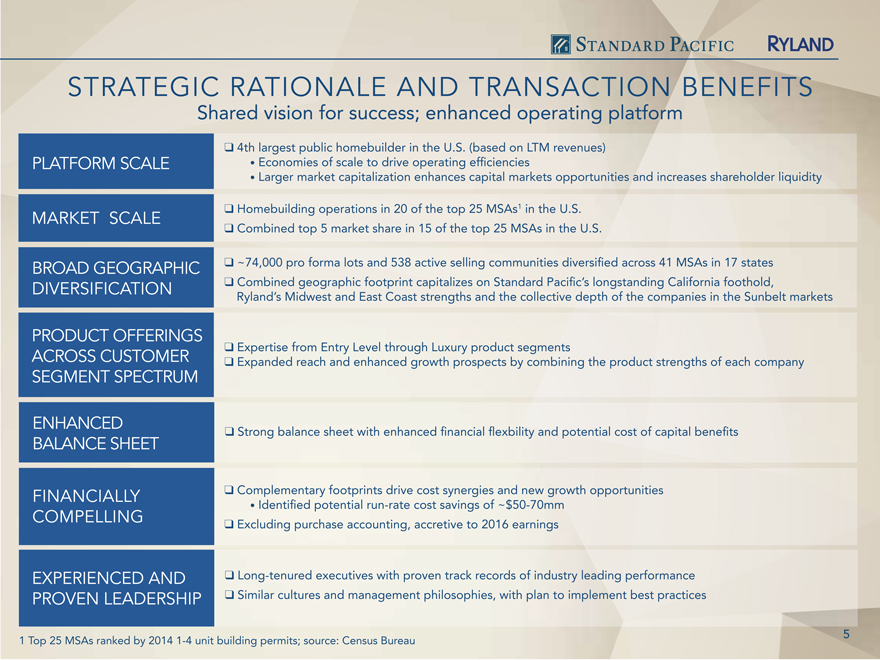

STRATEGIC RATIONALE AND TRANSACTION BENEFITS

Shared vision for success; enhanced operating platform

q 4th largest public homebuilder in the U.S. (based on LTM revenues) PLATFORM SCALE • Economies of scale to drive operating efficiencies

• Larger market capitalization enhances capital markets opportunities and increases shareholder liquidity

q Homebuilding operations in 20 of the top 25 MSAs1 in the U.S.

MARKET SCALE

q Combined top 5 market share in 15 of the top 25 MSAs in the U.S.

BROAD GEOGRAPHIC q ~74,000 pro forma lots and 538 active selling communities diversified across 41 MSAs in 17 states DIVERSIFICATION q Combined geographic footprint capitalizes on Standard Pacific’s longstanding California foothold, Ryland’s Midwest and East Coast strengths and the collective depth of the companies in the Sunbelt markets

PRODUCT OFFERINGS

q Expertise from Entry Level through Luxury product segments

ACROSS CUSTOMER q Expanded reach and enhanced growth prospects by combining the product strengths of each company

SEGMENT SPECTRUM

ENHANCED

q Strong balance sheet with enhanced financial flexbility and potential cost of capital benefits

BALANCE SHEET

FINANCIALLY q Complementary footprints drive cost synergies and new growth opportunities • Identified potential run-rate cost savings of ~$50-70mm

COMPELLING

q Excluding purchase accounting, accretive to 2016 earnings

EXPERIENCED AND q Long-tenured executives with proven track records of industry leading performance PROVEN LEADERSHIP q Similar cultures and management philosophies, with plan to implement best practices

1 Top 25 MSAs ranked by 2014 1-4 unit building permits; source: Census Bureau 5

|

|

MERGER CREATES A LEADING NATIONAL HOMEBUILDING PLATFORM

Standard Pacific Ryland Combined

COMPANY INCEPTION 1965 1967 Fall 2015

MSAs SERVED 26 29 41

TOTAL LOTS OWNED

~35,000 ~39,000 ~74,000

& CONTROLLED

YEARS’ SUPPLY

1 7.1 years 5.1 years 5.9 years

OF LOTS

LTM REVENUES $2.4bn $2.6bn $5.1bn

LTM PRE-TAX $337mm $288mm $625mm EARNINGS

1Q ‘15 ASP ($000s) $482 $343 $398

1Q ’15 BACKLOG $1.3bn $1.2bn $2.5bn

VALUE

Source: Company filings as of 3/31/15 6 1 Total owned and controlled lots divided by total closings for 12 months ended 3/31/15

|

|

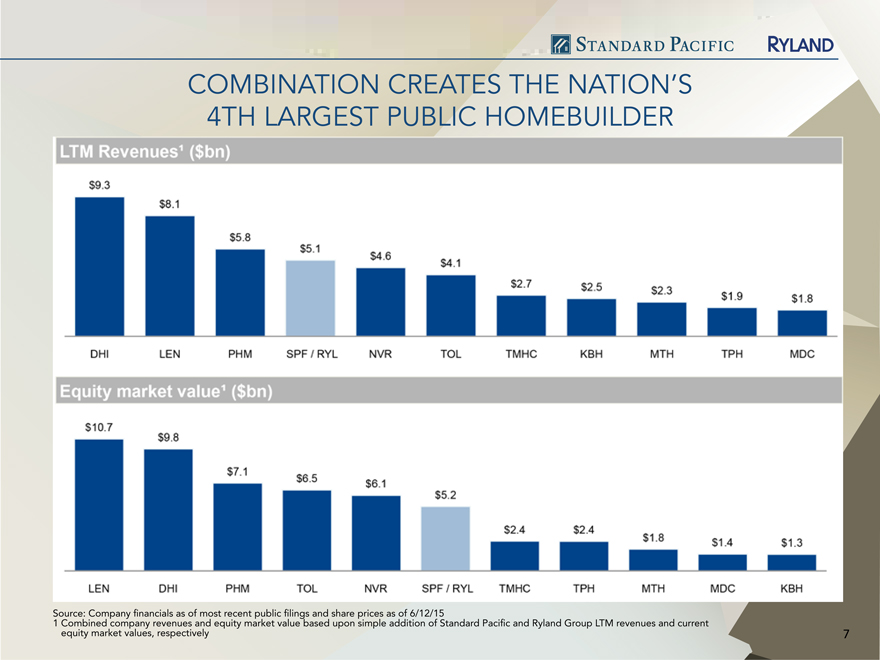

COMBINATION CREATES THE NATION’S 4TH LARGEST PUBLIC HOMEBUILDER

Source: Company financials as of most recent public filings and share prices as of 6/12/15

1 Combined company revenues and equity market value based upon simple addition of Standard Pacific and Ryland Group LTM revenues and current equity market values, respectively 7

LTM Revenues1 ($bn0

$9.3

$8.1 $5.8 $5.1 $4.6 $4.1 $2.7 $2.5 $2.3 $1.9 $1.8

DHI LEN PHM SPF/RYL NVR TOL TMHC KBH MTH TPH MDC

LEN DHI PHM TOL NVR SPF/RYL TMHC TPH MTH MDC KBH

$10.7 $9.8 $7.1 $6.5 $6.1 $5.2 $2.4 $2.4 $1.8 $1.4 $1.3

|

|

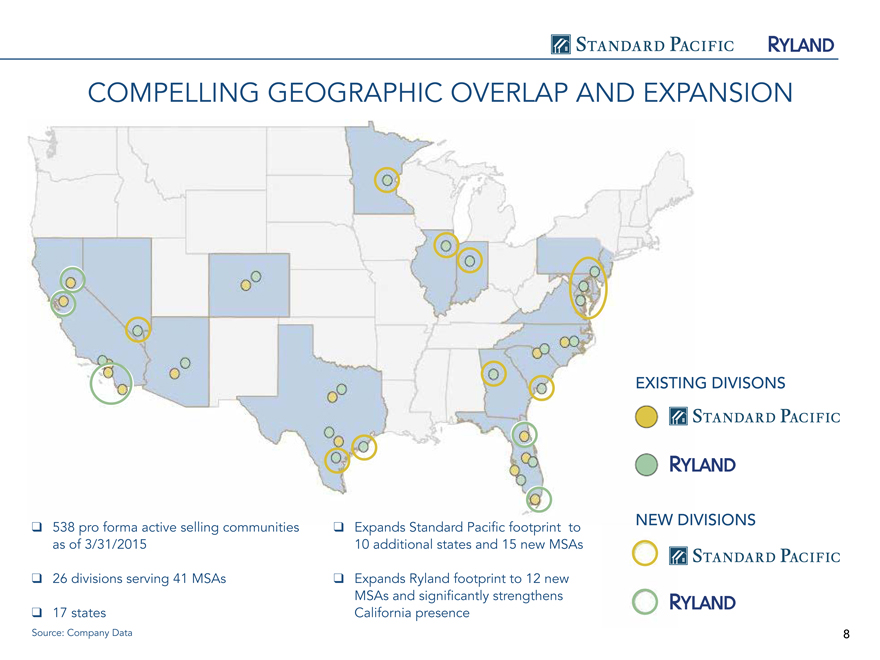

COMPELLING GEOGRAPHIC OVERLAP AND EXPANSION

EXISTING DIVISONS

NEW DIVISIONS

q 538 pro forma active selling communities q Expands Standard Pacific footprint to as of 3/31/2015 10 additional states and 15 new MSAs

q 26 divisions serving 41 MSAs q Expands Ryland footprint to 12 new MSAs and significantly strengthens q 17 states California presence

Source: Company Data 8

|

|

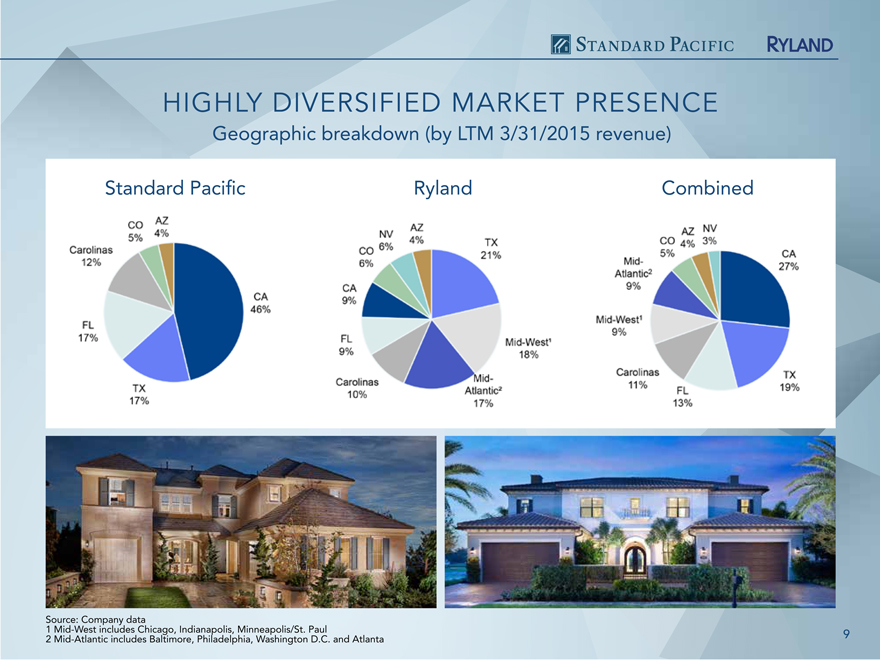

HIGHLY DIVERSIFIED MARKET PRESENCE

Geographic breakdown (by LTM 3/31/2015 revenue)

Standard Pacific Ryland Combined

Source: Company data

1 Mid-West includes Chicago, Indianapolis, Minneapolis/St. Paul 9 2 Mid-Atlantic includes Baltimore, Philadelphia, Washington D.C. and Atlanta

CO 5% AZ 4% Carolinas 12% FL 17% TX 17% CA 46%

CO 6% AZ 4% Carolinas 10% FL 9% TX 21% CA 46% Mid- WEST1 18% Mid-Atlantic2 17%

CO5% AZ 4% Carolinas 11% FL 13% TX 19% CA 27% Mid- WEST1 18% Mid-Atlantic2 9%

NV3%

|

|

LEADING MARKET SHARE POSITIONS

q Homebuilding operations in 20 of the top 251 MSAs in the U.S. q Combined top 5 market share in 15 of the top 25 MSAs

PF RANK TOP 3 MARKET SHARE MARKETS PF RANK OTHER TOP 10 MARKET SHARE MARKETS

Raleigh-Durham, NC Charlotte, NC

#1 San Diego, CA Las Vegas, NV Chicago, IL #4 Denver, CO

Phoenix, AZ

Central Valley, CA Orange County, CA Baltimore, MD Ventura, CA

#2 Tampa, FL Bakersfield, CA Minneapolis-St.Paul, MN #5 Sarasota, FL

Dallas-Ft. Worth, TX

Charleston, SC South Florida Austin, TX #7 Orlando, FL San Antonio, TX

#3 Indianapolis, IN #8 San Francisco Bay Area, CA

Atlanta, GA

Riverside-San Bernardino, CA

#9 Jacksonville, FL

Sacramento, CA

Houston, TX

Philadelphia, PA

15 TOP 3 POSITIONS 14 ADDITIONAL TOP 10 POSITIONS

Source: MetroStudy, based on combined 2014 Standard Pacific and Ryland closings

1 Top 25 MSAs ranked by 2014 1-4 unit building permits; source: Census Bureau 10

|

|

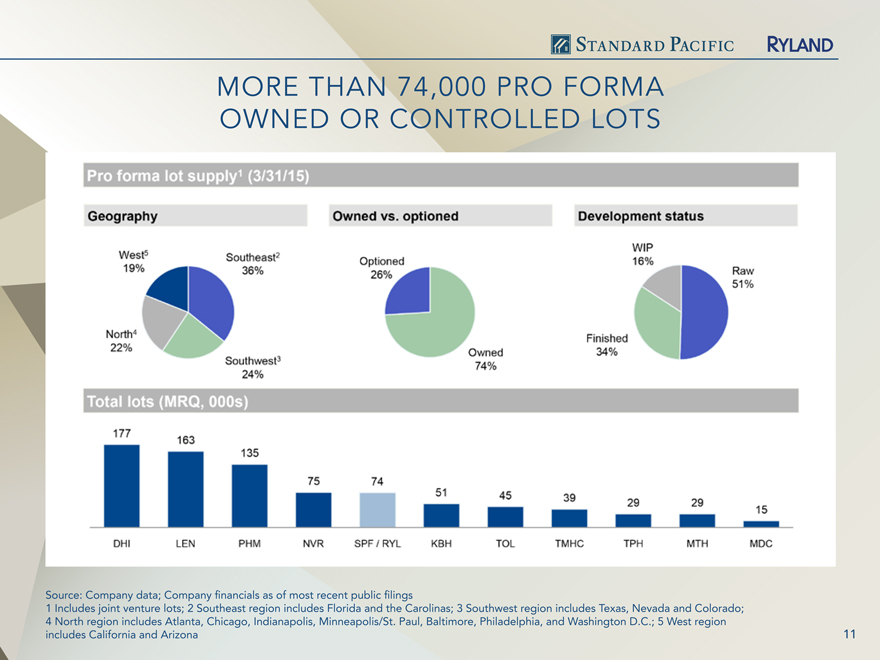

MORE THAN 74,000 PRO FORMA OWNED OR CONTROLLED LOTS

Source: 1 Includes Company joint venture data; lots; Company 2 Southeast financials region as of includes most recent Florida public and filings the Carolinas; 3 Southwest region includes Texas, Nevada and Colorado; 4 North region includes Atlanta, Chicago, Indianapolis, Minneapolis/St. Paul, Baltimore, Philadelphia, and Washington D.C.; 5 West region includes California and Arizona 11

Geopraphy West5 19%

Sotheast2 36%

North4 22% Southwest3 24% Owned VS.OPTIONED Optioned 26% owned 74% Develpoment status WIP 16% Raw 51% Finished 34%

Total lots (MRQ,000S)

177 163 135 75 74 51 45 39 29 29 15

DHI LEN PHM NVR SPF/RYL KBH TOL TMHC TPH MTH MDC

|

|

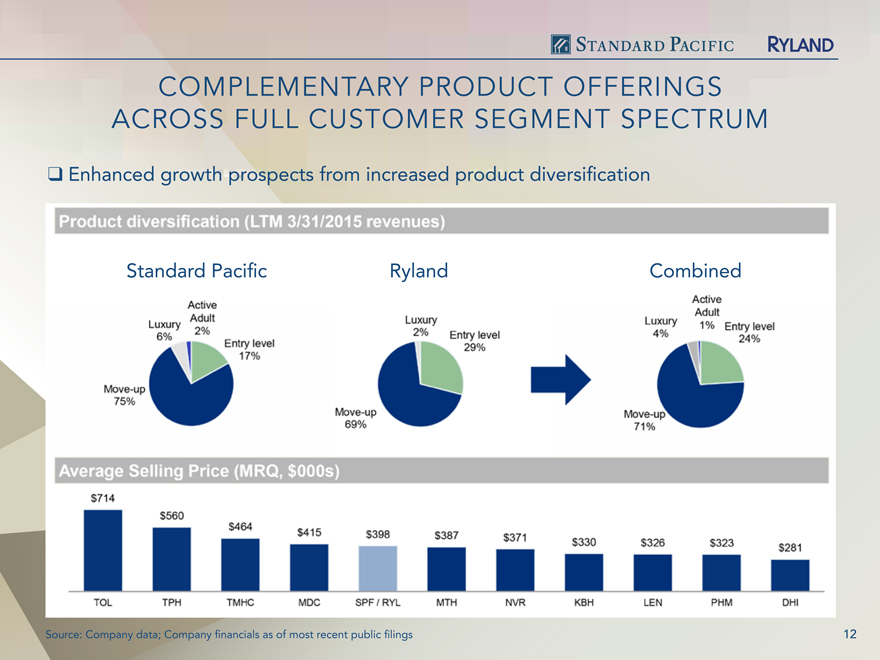

COMPLEMENTARY PRODUCT OFFERINGS ACROSS FULL CUSTOMER SEGMENT SPECTRUM

q Enhanced growth prospects from increased product diversification

Standard Pacific Ryland Combined

Source: Company data; Company financials as of most recent public filings 12

Product diversification (LTM3/31/2015 revenues)

Luxury 6% Active Adult 2% Entry level 17% Move-up 75%

Luxury 2% Entry level 29% Move-up 69%

Luxury 4% Active Adult 1% Entry level 24% Move-up 71%

Average Selling Price (MRQ-$000S)

$714 $560 $464 $415 $398 $387 $371 $330 $326 $323 $281 TOL TPH TMHC MDC SPF/RYL MTH NVR KBH LEN PHM DHI

|

|

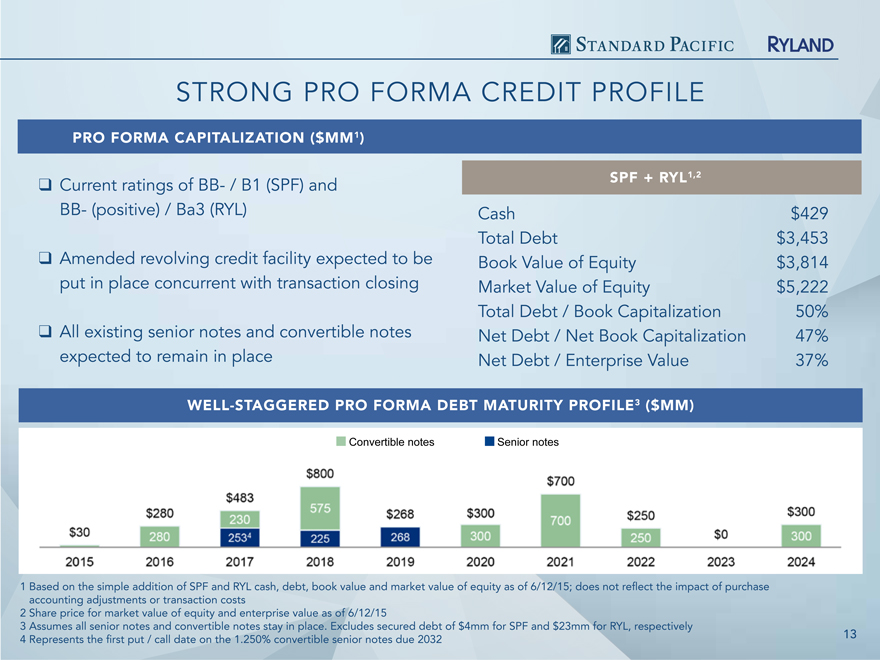

STRONG PRO FORMA CREDIT PROFILE

PRO FORMA CAPITALIZATION ($MM1)

SPF + RYL1,2

q Current ratings of BB- / B1 (SPF) and

BB- (positive) / Ba3 (RYL) Cash $429 Total Debt $3,453 q Amended revolving credit facility expected to be Book Value of Equity $3,814 put in place concurrent with transaction closing Market Value of Equity $5,222 Total Debt / Book Capitalization 50% q All existing senior notes and convertible notes Net Debt / Net Book Capitalization 47% expected to remain in place Net Debt / Enterprise Value 37%

WELL-STAGGERED PRO FORMA DEBT MATURITY PROFILE3 ($MM)

Convertible notes Senior notes

$30 $280 280 $483 $800 $268 $300 $700 $250 $0 $300

280 230 230 2534 575 225 268 300 700 250 300

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

1 accounting Based on the adjustments simple addition or transaction of SPF and costs RYL cash, debt, book value and market value of equity as of 6/12/15; does not reflect the impact of purchase 3 2 Assumes Share price all for senior market notes value and of convertible equity and notes enterprise stay in value place. as Excludes of 6/12/15 secured debt of $4mm for SPF and $23mm for RYL, respectively

4 Represents the first put / call date on the 1.250% convertible senior notes due 2032 13

|

|

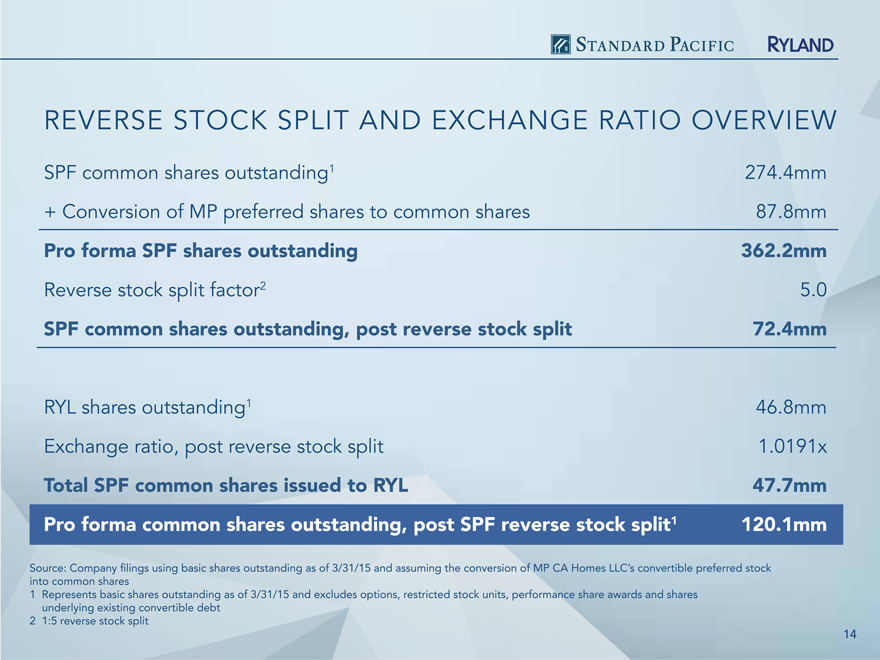

REVERSE STOCK SPLIT AND EXCHANGE RATIO OVERVIEW

SPF common shares outstanding1 274.4mm

+ Conversion of MP preferred shares to common shares 87.8mm

Pro forma SPF shares outstanding 362.2mm

Reverse stock split factor2 5.0

SPF common shares outstanding, post reverse stock split 72.4mm

RYL shares outstanding1 46.8mm

Exchange ratio, post reverse stock split 1.0191x

Total SPF common shares issued to RYL 47.7mm Pro forma common shares outstanding, post SPF reverse stock split1 120.1mm

Source: into common Company shares filings using basic shares outstanding as of 3/31/15 and assuming the conversion of MP CA Homes LLC’s convertible preferred stock

1 Represents underlying existing basic shares convertible outstanding debt as of 3/31/15 and excludes options, restricted stock units, performance share awards and shares 2 1:5 reverse stock split

14

|

|

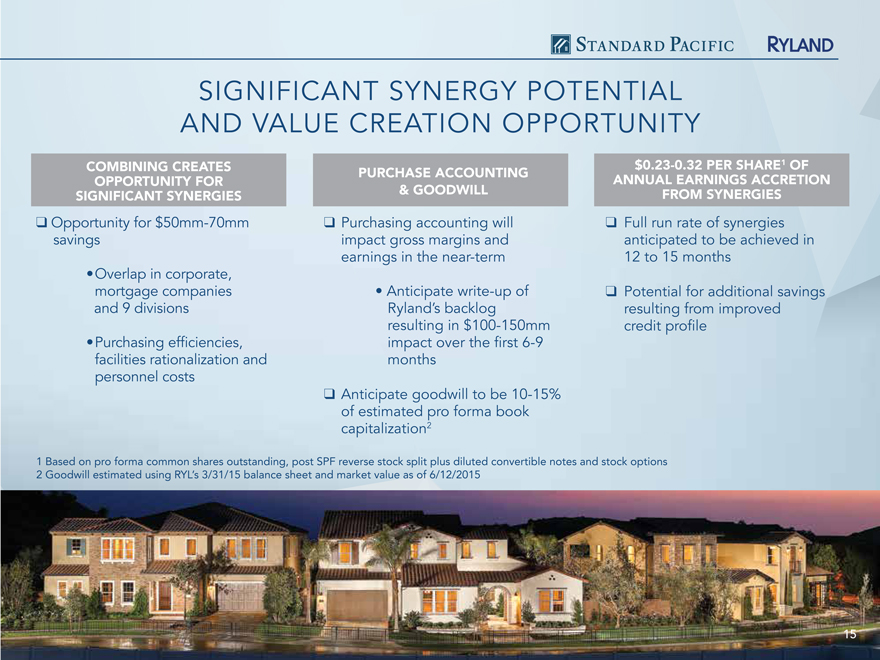

SIGNIFICANT SYNERGY POTENTIAL AND VALUE CREATION OPPORTUNITY

COMBINING CREATES $0.23-0.32 PER SHARE1 OF PURCHASE ACCOUNTING ANNUAL EARNINGS ACCRETION

OPPORTUNITY FOR

SIGNIFICANT SYNERGIES & GOODWILL FROM SYNERGIES q Opportunity for $50mm-70mm q Purchasing accounting will q Full run rate of synergies savings impact gross margins and anticipated to be achieved in earnings in the near-term 12 to 15 months

•Overlap in corporate, mortgage companies • Anticipate write-up of q Potential for additional savings and 9 divisions Ryland’s backlog resulting from improved resulting in $100-150mm credit profile

•Purchasing efficiencies, impact over the first 6-9 facilities rationalization and months personnel costs q Anticipate goodwill to be 10-15% of estimated pro forma book capitalization2

1 2 Based Goodwill on estimated pro forma using common RYL’s shares 3/31/15 outstanding, balance sheet post and SPF market reverse value stock as split of 6/12/2015 plus diluted convertible notes and stock options

15

|

|

EXPERIENCED AND PROVEN LEADERSHIP

Scott Stowell Larry Nicholson Executive Chairman President and CEO

Chief Executive Officer of Standard Pacific since January 2012 and President since Chief Executive Officer of The Ryland Group since March 2011 May 2009 and President since October 2008 Chief Operating Officer of Standard Pacific Chief Operating Officer of The Ryland Group from from May 2007 to March 2011 June 2007 to May 2009 President of Standard Pacific’s Southern Senior Vice President of The Ryland Group from

California Region from September 2002 2005 to 2007, and Executive Vice President from to May 2007 2007 to October 1, 2008

Jeff McCall Peter Skelly

EVP and CFO EVP and COO

Executive Vice President and Chief Operating Executive Vice President and Chief Financial Officer of The Ryland Group since June 2013 Officer of Standard Pacific since June 2011 Senior Vice President of The Ryland Group from

Chief Financial Officer–Americas at Regus plc, 2006 to 2013 from August 2004 to May 2011 28 year veteran of the real estate business and Chief Financial Officer and Executive Vice President joined The Ryland Group in 1988 as an Assistant of HQ Global Workplaces, from Controller December 2003 to August 2004

16

|

|

LEADERSHIP AND GOVERNANCE

q Executive Chairman to lead strategy and work with CEO in conceptualizing and communicating the Company’s purpose, vision, core values and culture

• Chair of Land Investment Committee

• Strategic guidance with respect to California operations

• Responsible for leading integration of the two companies

• Board governance and facilitation

q CEO to lead day-to-day operations and to serve as lead voice for the combined company

• Work with Executive Chairman in setting strategy • Responsible for land acquisition and land strategy • Capital allocation and capital markets decisions • Managing the mortgage company q 10 member Board with 8 highly qualified independent directors

17

|

|

DRIVING SHAREHOLDER VALUE THROUGH COMBINATION OF TWO INDUSTRY LEADERS

q Combined strength of two industry leading companies with proud legacies and nearly

100 years of aggregate homebuilding expertise q Experienced and proven leadership with shared visions and passions for success q Positioned to take advantage of opportunities and efficiencies while accelerating both companies’ growth strategies q Better navigation of industry cyclicality through broader market and product diversification and greater economies of scale q Significant synergy potential and efficient integration resulting from compatibility of businesses q All-stock transaction allows all shareholders to participate in potential upside

18