Attached files

| file | filename |

|---|---|

| EX-23.2 - EX-23.2 - Wingstop Inc. | d880866dex232.htm |

Table of Contents

As filed with the Securities and Exchange Commission on June 9, 2015

Registration No. 333-203891

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 3

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

WINGSTOP INC.

(Exact name of registrant as specified in its charter)

| Delaware | 5812 | 47-3494862 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(IRS Employer Identification No.) |

5501 LBJ Freeway, 5th Floor,

Dallas, Texas 75240

(972) 686-6500

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Charles R. Morrison

President and Chief Executive Officer

Wingstop Inc.

5501 LBJ Freeway, 5th Floor,

Dallas, Texas 75240

(972) 686-6500

(Name, address, including zip code, and telephone number, including area code, of agent for service)

with copies to:

| Keith M. Townsend, Esq. | Marc D. Jaffe, Esq. | |

| King & Spalding LLP | Ian D. Schuman, Esq. | |

| 1180 Peachtree Street, N.E. | Latham & Watkins LLP | |

| Atlanta, GA 30309 | 885 Third Avenue | |

| Telephone: (404) 572-4600 | New York, NY 10022 | |

| Facsimile: (404) 572-5100 | Telephone: (212) 906-1200 | |

| Facsimile: (212) 751-4864 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (check one):

| Larger accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of each class of securities to be registered |

Amount to be |

Proposed Per Share (2) |

Proposed Maximum Aggregate Offering Price (1)(2) |

Amount of Registration Fee (3) | ||||

| Common Stock, par value $0.01 per share |

6,670,000 | $18.00 | $120,060,000 | $13,950.97 | ||||

|

| ||||||||

|

| ||||||||

| (1) | Includes 870,000 shares of common stock that may be sold if the underwriters’ exercise their option to purchase additional shares. See “Underwriters (Conflicts of Interest).” |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(a) under the Securities Act. |

| (3) | The Registrant previously paid $10,850.76 in connection with prior filings of this Registration Statement. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS (Subject to Completion)

Issued June 9, 2015

5,800,000 shares

Common stock

This is the initial public offering of Wingstop Inc. We are offering 2,150,000 shares of common stock and the selling stockholders identified in this prospectus are offering 3,650,000 shares of common stock. We will not receive any of the proceeds from the sale of shares being sold by the selling stockholders in this offering.

No public market currently exists for our shares. Our common stock has been approved for listing on The Nasdaq Global Select Market, or Nasdaq, under the symbol “WING.” The estimated initial public offering price is expected to be between $16.00 and $18.00 per share.

We are an “emerging growth company” as that term is used in the Jumpstart Our Business Startups Act of 2012 and will be subject to reduced public company reporting requirements. See “Prospectus Summary—Emerging Growth Company Status.”

Investing in our common stock involves risks. See “Risk Factors” beginning on page 18.

| Price to public |

Underwriting discounts and commissions |

Proceeds, before expenses to us (1) |

Proceeds, before expenses to the selling stockholders |

|||||||||||||

| Per share |

$ | $ | $ | $ | ||||||||||||

| Total |

$ | $ | $ | $ | ||||||||||||

| (1) | We have agreed to reimburse the underwriters for certain FINRA-related expenses. See “Underwriters (Conflicts of Interest).” |

The underwriters may also exercise their option to purchase up to an additional 870,000 shares of common stock from one of the selling stockholders identified in this prospectus. The underwriters can exercise this option at any time within 30 days from the date of this prospectus.

Neither the Securities and Exchange Commission, or SEC, nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock on or about , 2015.

| Morgan Stanley | Jefferies | Baird | ||

| Goldman, Sachs & Co. | Barclays | Wells Fargo Securities | ||

, 2015

Table of Contents

WELCOME TO WINGSTOP

We’re not in the wing business. We’re in the flavor business. It’s been our mission to serve the world flavor since we first opened shop in ‘94, and we’re just getting started.

It’s flavor that defines us. It inspires our fans and fuels their crave. It’s our unfair advantage and has made Wingstop one of the fastest growing brands in the restaurant industry. We’re tough to forget. Because when you crave wings, ordinary just won’t do.

Table of Contents

Table of Contents

| Page | ||||

| 1 | ||||

| 18 | ||||

| 41 | ||||

| 43 | ||||

| 44 | ||||

| 45 | ||||

| 46 | ||||

| 48 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

51 | |||

| 75 | ||||

| 96 | ||||

| 104 | ||||

| 118 | ||||

| 121 | ||||

| 123 | ||||

| 128 | ||||

| MATERIAL U.S. FEDERAL INCOME TAX CONSEQUENCES TO NON-U.S. HOLDERS |

131 | |||

| 135 | ||||

| 142 | ||||

| 142 | ||||

| 142 | ||||

| 143 | ||||

| F-1 | ||||

You should rely only on the information contained in this prospectus or in any free-writing prospectus we may specifically authorize to be delivered or made available to you. Neither we, the selling stockholders, nor the underwriters (or any of our or their respective affiliates) authorized anyone to provide you with additional or different information. Neither we, the selling stockholders, nor the underwriters (or any of our or their respective affiliates) take any responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We, the selling stockholders and the underwriters are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where such offers and sales are permitted. The information in this prospectus or any free-writing prospectus is accurate only as of its date, regardless of its time of delivery or the time of any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

Until , 2015 (25 days after the date of this prospectus), all dealers that buy, sell or trade shares of our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the dealers’ obligation to deliver a prospectus when acting as an underwriter and with respect to their unsold allotments or subscriptions.

i

Table of Contents

MARKET DATA AND FORECASTS

Unless otherwise indicated, information in this prospectus concerning economic conditions, our industry, our markets and our competitive position is based on a variety of sources, including information from independent industry analysts and publications, as well as our own estimates and research. The term “designated market area,” or “DMA,” refers to a geographic area as defined by Nielsen Media Research Company as a group of counties that make up a particular media market. Technomic, Inc. is a leading restaurant industry consulting and researching firm.

Our estimates are derived from publicly available information released by third-party sources, as well as data from our internal research, and are based on such data and our knowledge of our industry, which we believe to be reasonable. None of the independent industry publications used in this prospectus were prepared on our behalf.

TRADEMARKS AND TRADE NAMES

This prospectus includes our trademarks, such as WING-STOP®; Wing-Stop—The Wing Experts; WINGSTOP; THE WING EXPERTS and THE BONELESS WING EXPERTS, which are protected under applicable intellectual property laws and are the property of Wingstop Inc. or its subsidiaries. Solely for convenience, trademarks, service marks and trade names referred to in this prospectus may appear without the ®, TM or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks, service marks and trade names. This prospectus may also contain trademarks, service marks, trade names and copyrights of other companies, which are the property of their respective owners.

BASIS OF PRESENTATION

Except where the context otherwise requires or where otherwise indicated, the terms “Wingstop,” “we,” “us,” “our,” “our company” and “our business” refer collectively to, prior to the completion of the reorganization described in this prospectus, Wing Stop Holding Corporation and its consolidated subsidiaries and, after the completion of the reorganization, Wingstop Inc. and its consolidated subsidiaries. On May 28, 2015, Wing Stop Holding Corporation merged with and into Wingstop Inc., a newly formed, wholly owned Delaware subsidiary of Wing Stop Holding Corporation, with Wingstop Inc. as the surviving corporation in the merger. Wingstop Restaurants Inc. is an indirect wholly owned subsidiary of Wingstop Inc. and is the franchisor of all Wingstop franchised restaurants and the lessee, owner and operator of all company-owned restaurants. Accordingly, any references to “Wingstop,” “we,” “us,” “our,” “our company” or “our business” in the context of domestic and international franchising activities, domestic and international franchised restaurants and the leasing, ownership or operations of company-owned restaurants should be read as a reference to Wingstop Restaurants Inc. The term “selling stockholders” refers to the entities named herein (other than the company) that intend to sell shares in this offering. RC II WS LLC, a Georgia limited liability company, or RC II WS, is our majority stockholder.

Throughout this prospectus, we provide a number of key performance indicators used by management and typically used by our competitors in the restaurant industry, including same store sales, system-wide sales and average unit volume. Same store sales reflect the change in year-over-year sales for the same store base, which includes restaurants open for at least 52 weeks. System-wide sales include restaurant net sales at all company-owned restaurants and at all franchised restaurants, as reported by franchisees. While we do not record franchised restaurant sales as revenue, our royalty revenue is calculated based on a percentage of franchised restaurant sales, which generally range from 5.0% to 6.0% of gross sales net of discounts. Average unit volume, or AUV, consists of the average annual sales of all restaurants that have been open for a trailing 52-week period or longer. This measure is calculated by dividing sales during the applicable period for all restaurants being measured by the

ii

Table of Contents

number of restaurants being measured. In this prospectus, we provide AUV for domestic restaurants and company-owned restaurants. Domestic AUV includes revenue from both company-owned and franchised restaurants, which are not owned by us. Unless otherwise indicated, references to domestic same store sales and domestic AUV include both domestic franchised restaurants and domestic company-owned restaurants. These and other key performance indicators are discussed in more detail in the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Performance Indicators.” In this prospectus, we also reference EBITDA and Adjusted EBITDA, which are non-GAAP financial measures. See “Prospectus Summary—Selected Historical Consolidated Financial and Other Data” for a discussion of EBITDA and Adjusted EBITDA, as well as a reconciliation of those measures to net income, the most directly comparable financial measure required by, or presented in accordance with, generally accepted accounting principles in the United States, or U.S. GAAP.

Our fiscal year ends on the last Saturday of each calendar year. Our most recent fiscal year ended on December 27, 2014. Fiscal years 2014, 2013 and 2012 were 52-week years, fiscal year 2011 was a 53-week year and fiscal years 2015 and 2016 are 52-week and 53-week years, respectively. References to fiscal years 2014, 2013 and 2012 and references to 2014, 2013 and 2012 are references to the fiscal years ended December 27, 2014, December 28, 2013 and December 29, 2012, respectively. Our fiscal quarters are comprised of 13 weeks each, except for 53-week fiscal years for which the fourth quarter will be comprised of 14 weeks, and end on the 13th Saturday of each quarter (14th Saturday of the fourth quarter, when applicable). For purposes of same store sales and AUV calculations in 53-week fiscal years, we do not include the 53rd week of the fiscal year.

iii

Table of Contents

This summary highlights significant aspects of our business and this offering that appear later in this prospectus, but it is not complete and does not contain all of the information that you should consider before making your investment decision. You should read carefully the entire prospectus, especially the information set forth under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the financial statements and related notes included elsewhere in this prospectus, before making an investment decision.

OVERVIEW

#TheWingExperts

Wingstop is a high-growth franchisor and operator of restaurants that specialize in cooked-to-order, hand-sauced and tossed chicken wings. Founded in 1994 in Garland, Texas, we believe we pioneered the concept of wings as a “center-of-the-plate” item for all of our meal occasions. We offer our guests 11 bold, distinctive and craveable flavors on our bone-in and boneless chicken wings paired with hand-cut, seasoned fries and sides made fresh daily. Our menu is highly customizable for different dining occasions, and we believe it delivers a compelling value proposition for groups, families, and individuals. Our average transaction size in 2014 was $15.61, as a result of our large, value-oriented family packs, as well as meals for two and individual combo meals, which start at approximately $8. Additionally, carry-out orders constituted approximately 75% of our sales during the same time period. Our concept has received numerous accolades, including recognition in 2014 as the “Best Chicken Wings” in the U.S. by Food and Wine, the “#3 Fastest-Growing Chain” by Nation’s Restaurant News, and the “Best Franchise Deal in North America” by QSR Magazine.

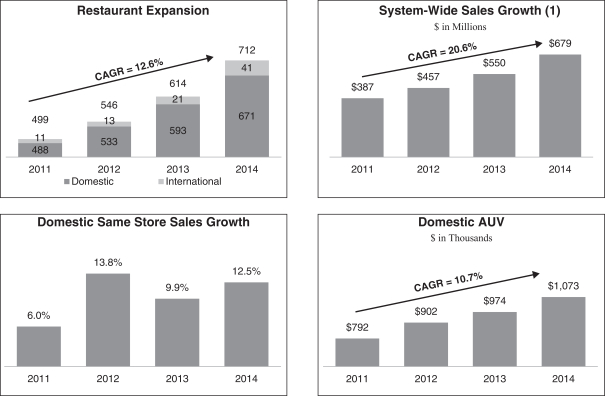

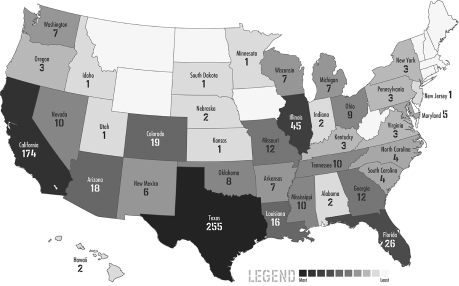

We are the largest fast casual chicken wings-focused restaurant chain in the world, and have demonstrated strong, consistent growth on a national scale. We have sold approximately 4 billion wings over the last 20 years, as we grew to 745 restaurants across 37 states and 6 countries, as of March 28, 2015. Wings are our “center-of-the-plate” specialty. While other concepts include wings as add-on menu items or focus on wings in a bar or sports-centric setting, we are singularly focused on wings, fries and sides, which generate approximately 90% of our sales. We have broad and growing consumer appeal anchored by a sought after core demographic of 18-34 year old Millennials, which we believe is a loyal consumer group that dines at fast casual restaurants more frequently. Increasing customer loyalty and brand awareness have enabled us to deliver positive domestic same store sales for 11 consecutive years through 2014, while growing our restaurant count at a 15.3% compound annual growth rate, or CAGR, over the same timeframe.

As of March 28, 2015, our restaurant base was 97% franchised, with 726 franchised locations (including 45 international locations) and 19 company-owned restaurants. We believe our simple and efficient restaurant operating model, low initial cash investment and compelling restaurant economics help drive continued system growth through both existing and new franchisees. Our “wings, fries, sides, repeat” restaurant operating model requires few ingredients and easy preparation within a small, flexible real estate footprint. We believe we offer an attractive investment opportunity for our franchisees as evidenced by our domestic average sales-to-investment ratio of 2.9x and the 43.4% increase in domestic restaurant count since the end of 2011. We believe our asset-light, highly-franchised business model generates strong operating margins and requires low capital expenditures, creating shareholder value through strong and consistent free cash flow and capital-efficient growth.

1

Table of Contents

#ExceptionalFinancialPerformance

We believe our bold flavors, compelling value proposition, strong base of franchisees, growing brand awareness and focused development strategy drive strong operating results, as illustrated by the following:

| • | Domestic restaurant count has increased 43.4% since the end of 2011, with the pace of restaurant openings increasing each year; |

| • | We have grown domestic same store sales 11 consecutive years through 2014, which includes three-year cumulative domestic same store sales growth of 36.2% since 2011; and |

| • | On a year-over-year basis, for fiscal year 2014, our total revenue increased by 14.3% to $67.4 million, our Adjusted EBITDA increased by 25.0% to $24.4 million, our Adjusted EBITDA margin increased 310 basis points to 36.1%, and our net income increased by 19.3% to $9.0 million. For a reconciliation of Adjusted EBITDA, a non-GAAP metric, to net income, see “Summary Historical Consolidated Financial and Other Data.” |

The graphs below highlight the consistency of our exceptional performance and growth across our key metrics, including restaurant expansion and system-wide sales, domestic same store sales and domestic AUV. Each of the graphs below include information regarding franchised restaurants and company-owned restaurants.

| (1) | The percentage of system-wide sales attributable to company-owned restaurants for the fiscal years ended December 31, 2011, December 29, 2012, December 28, 2013 and December 27, 2014 was 6.0%, 5.8%, 5.2% and 4.3%, respectively. The remainder was generated by franchised restaurants, as reported by our franchisees. Our total revenue during the fiscal years ended December 31, 2011, December 29, 2012, December 28, 2013 and December 27, 2014 was $46.1 million, $51.6 million, $59.0 million and $67.4 million, respectively. |

2

Table of Contents

OUR STRENGTHS

#UnleashTheFlavor

Wingstop is the destination when our guests crave fresh, cooked-to-order wings with bold, layered flavors that touch all of the senses. People who prioritize flavor prioritize Wingstop—because it is more than a meal, it is a flavor experience. We speak in bold, distinctive and craveable flavors. Our dialect is our 11 proprietary flavors, presented here in order from most spicy to least:

3

Table of Contents

Our diverse flavor offerings allow our guests to customize their experience. All of our wings are cooked-to-order, hand-sauced and tossed and served fresh to our guests for dine-in or carry-out. We never use heat lamps or microwaves in the preparation of our food. To complement our wings, we serve hand-cut, freshly-prepared seasoned fries, crafted from carefully-selected whole Russet potatoes. We complete the flavor experience with fresh carrots and celery and ranch and bleu cheese dips made from buttermilk in-house daily, as well as freshly-prepared side items, including coleslaw, bourbon baked beans, potato salad and freshly-baked yeast rolls. We believe our bold and distinctive flavors leave our guests craving more and create a differentiated and tailor-made flavor experience that drives repeat business and brand loyalty.

Our customizable menu and craveable flavors drive demand across multiple day-parts and occasions. Our 11 flavors, signature fries, freshly-prepared sides and numerous order options (eat-in / to go, individual / combo meals / family packs) allow guests to eat Wingstop during any occasion, whether it is a quick carry-out snack, dine-in dinner with friends or picking up a party size order for their favorite sporting event. Since our inception, we have received numerous accolades from both consumers and industry-leading publications for the quality of our food offering and strong brand appeal, including:

| • | “Best Chicken Wings in the U.S.,” Food and Wine (2014); and |

| • | “Best Menu Variety and Best Craveability,” Nation’s Restaurant News (2014). |

#CompellingUnitEconomics

We believe the growing popularity of the Wingstop experience and the operational simplicity of our restaurants translate into attractive economics at our franchised and company-owned locations. Our compelling franchisee investment opportunity has been recognized across the industry, including by QSR magazine, which in 2014 named us “The Best Franchise Deal in North America” amongst fast casual and QSR brands. Additionally, existing franchisees accounted for approximately 69% of franchised restaurants opened in 2013 and 2014, which we believe further underscores our restaurant model’s financial appeal.

Our restaurants do not generally experience a “honeymoon” period of higher sales upon opening, but instead typically build year over year. Our domestic AUV has grown consistently, achieving $1.07 million during fiscal year 2014. In addition, new restaurant sales volumes in the first year of operation have improved 43% since 2006, with the 2013 new restaurants openings averaging approximately $820,000 during their first 52 weeks of operations, accelerating our franchisees’ return on investment. Our restaurants are approximately 1,700 square feet on average and yield average sales per square foot of $631 based on 2014 domestic AUV due to the high average domestic carry-out mix of 75% in 2014. Our operational simplicity results in low labor costs, further improving the profitability of our concept. Our operating model targets a low average estimated initial investment of approximately $370,000, excluding real estate purchase or lease costs and pre-opening expenses. In year two of operation, we believe that, on average, our franchisees can achieve an unlevered cash-on-cash return, which is defined as restaurant-level operating profit after royalties and advertising fund contributions, divided by initial investment costs, of approximately 35% to 40%. We believe low entry costs and high returns provide a compelling investment opportunity for our franchisees that has helped drive the continued growth of our system.

#ProvenPortability

Our concept is successful across the United States, with restaurants operating in 37 states across varying geographic regions, population densities and real estate settings. We have had positive same store sales growth across a wide variety of major markets over the last three years, including Dallas / Ft. Worth, Los Angeles, the San Francisco Bay area, Chicago, Houston, San Antonio, Miami, Denver, Sacramento and Memphis. Broad appeal and the simplicity of our restaurant operating model have supported our success across the country. While our concept has succeeded in a variety of real estate formats and locations, our preferred real estate site is an

4

Table of Contents

in-line or end-cap retail strip center location available in most shopping centers. The flexibility of our real estate model coupled with the broad appeal of our food has enabled us and our franchisees to locate profitable restaurants in both urban and suburban areas throughout the country. Accordingly, we believe our concept is well-positioned for continued system growth in both existing and new markets.

#SocialEngagement

We believe we have developed a broad, loyal and diverse guest base which is attracted to Wingstop by the unique flavor experience, product quality, brand personality and the convivial nature of eating wings. While we appeal to a broad demographic, we have been particularly successful at actively engaging the coveted Millennial consumer. Millennials leverage technology via smartphones and social media to connect with each other, search out dining experiences and voice their opinions, and we engage them on all of these fronts. We take pride in connecting with our guests, both inside and outside of our restaurants.

We believe much of our growth is attributable to our focus on meaningful consumer engagement, fueled by social media. We actively engage our core audience in conversation through key social media channels, which in turn drives our editorial calendar and advertising content. As of March 28, 2015, we had 908,196 Facebook followers, 93,942 Twitter followers and 26,705 Instagram followers, representing year-over-year growth of 220%, 137% and 425%, respectively. According to a report published by Forbes in November 2014, 30% of our almost 1 million followers across all social media platforms engage with our content over a period of 30 days, compared to an average 3% for the top 25 restaurants in social media cited in the same study. Our social game is just as strong as our wing game and we believe that this continues to inspire brand loyalty and repeat visits to our restaurants.

#StrengthInNumbers

We have demonstrated a consistent track record of strong financial performance:

| • | Domestic same store sales increased 13.8% in 2012, 9.9% in 2013 and 12.5% in 2014, representing three year cumulative domestic same store sales growth of 36.2%, driven primarily by an increase in transactions, which demonstrates the growing awareness and popularity of our brand; |

| • | Our domestic same store sales growth is even more meaningful given that we have had 11 consecutive years of positive same store sales; |

| • | From 2012 to 2014, our system-wide sales increased from $457 million to $679 million, which represents growth of 48.4% over the period; |

| • | Total revenue increased from $51.6 million in 2012, to $59.0 million in 2013, to $67.4 million in 2014, our Adjusted EBITDA increased from $15.6 million, to $19.5 million, to $24.4 million, respectively, and our net income grew from $3.6 million, to $7.5 million, to $9.0 million, respectively; and |

| • | From 2012 to 2014, our Adjusted EBITDA margin increased from 30.3% in 2012, to 33.0% in 2013, to 36.1% in 2014, while our capital expenditures were 3.1%, 3.6% and 2.2% of revenue, respectively, leading to high cash flow conversion. |

#OurCrew

Our strategic vision and results-driven culture are directed by our executive management team under the leadership of our President and Chief Executive Officer, Charlie Morrison. Charlie joined Wingstop in 2012, bringing more than 20 years of experience in the restaurant and multi-unit retail industry, including leadership positions at Pizza Hut, Boston Market, Kinko’s, Steak & Ale and, most recently, Rave Restaurant Group, where

5

Table of Contents

he served as Chief Executive Officer and led the creation of the award winning Pie Five restaurant concept. Charlie is supported by a strong executive team with significant retail and restaurant experience. Bill Engen, our Chief Operating Officer, previously was the Senior Vice President of Eastern Operations at 7-Eleven, overseeing approximately 4,000 stores. Our Chief Financial Officer, Mike Mravle, came to us from Bloomin’ Brands, where he was the Chief Financial Officer of the U.S. segment. Heading up our marketing efforts is Flynn Dekker, who has over 20 years of experience and was previously the Chief Marketing Officer of Fogo de Chao and Rave Restaurant Group. Dave Vernon, our Chief Development Officer, joined us from Sonic Corporation, where he was Vice President of Franchise Sales, and brings 25 years of experience in the restaurant industry to oversee our franchise development efforts. Jay Young, our General Counsel, joined us from CEC Entertainment Inc., the parent company of Chuck E. Cheese, where he was Senior Vice President and General Counsel. Completing our executive team is Stacy Peterson, our Chief Information Officer, who has over 15 years of information technology experience at multi-unit retailers, including Blockbuster and Kinko’s. We believe our management team is a key driver of our success and positions us well for long-term growth.

OUR GROWTH STRATEGY

#SpreadOurWings

We believe that there is significant opportunity to expand in the United States, and we intend to focus our efforts on increasing our geographic penetration in both existing and new markets. We believe our highly-franchised model positions us for continued strong unit growth over the medium and long-term. We expect high franchisee demand for our brand, supported by compelling unit economics, operational simplicity, low entry costs and flexible real estate profile, to drive domestic restaurant growth. Based on our internal analysis, we believe there is opportunity for our brand to grow to approximately 2,500 restaurants across the United States.

We intend to achieve our domestic restaurant potential by expanding in our existing markets, where we believe we have the opportunity to more than double our current restaurant count. In addition, we will continue to expand into new markets. Our “inside out” domestic market expansion strategy focuses our initial development in urban centers where our core demographic is most densely populated and then builds outward into suburban areas as our brand awareness grows in the market. We have a robust domestic development pipeline including 503 total commitments to open new franchised restaurants as of December 27, 2014. Approximately 63% of our current domestic commitments are from existing franchisees, supporting the attractiveness of our restaurant business model as well as our positive franchisor / franchisee relationships. We believe that our highly-franchised business model provides a platform for continued growth as it allows us to focus on our core strengths of flavor innovation, marketing and guest engagement, and franchisee selection and support, while growing our restaurant presence and brand recognition with limited capital investment by us.

We also believe that there is significant international growth opportunity. We opened our first international location in Mexico in 2009. As of March 28, 2015, we had 45 international restaurants located in Indonesia, Mexico, the Philippines, Russia and Singapore, all of which were franchised. In 2014, we opened 20 international locations. We had 310 international restaurant commitments as of December 27, 2014, and our first location in the United Arab Emirates opened in April 2015. We believe that our restaurant operating model will translate well internationally based on our small real estate footprint, our simplicity of operations, the universal and broad appeal of chicken, and our ability to customize our wide variety of flavors to local tastes.

#KeepItGrowing

| • | Flavor Innovation |

We plan to leverage flavor innovation to drive restaurant traffic and social media engagement. We do not have limited time offers; instead, we have limited time “flavor events” that pique our guests’ interest and drive

6

Table of Contents

frequency of visit. We approach additions to our menu as a conversation between us and our guests and make changes only after intense scrutiny in our test kitchen. For example, our Mango Habanero flavor was introduced as a limited time flavor event. When the flavor event ended, overwhelming demand from our highly-engaged social following to bring it back influenced us to return it to the menu as a permanent flavor. We do not believe in “off-the-shelf” flavors and are careful not to crowd the menu with too many flavors or any flavors the development of which has not received the attention and care that our guests expect. We anticipate that our powerful and selective flavor innovation will continue to drive domestic same store sales growth.

| • | Improve Efficiency to Drive Sales |

We are making focused investments in technology and restaurant design to increase the efficiency of our model and drive increased revenue. We are in the process of rolling out a single integrated point-of-sale system, or POS system. We also launched an updated online ordering system and mobile ordering application, or app, in 2014, that simplifies the ordering process and integrates into our POS system, uniting online and register ordering across our system for the first time. We believe that we can continue to grow sales through integration of orders through our website and app. As an example, since the implementation of our new online ordering platform and app in September 2014, online ordering increased from less than 7% of sales during the nine months preceding the launch of the new online ordering platform and app to over 11% of sales during the first quarter of 2015. Additionally, average transaction size for online orders is approximately $4 higher than the average for all other orders. As guests’ ordering preferences continue to shift online, we will implement a new front counter design in our existing and new restaurants, creating a dedicated queuing area for guests to efficiently pick up their prepaid online orders.

| • | Grow Brand Awareness |

We believe our strong domestic same store sales growth has been supported by growing brand awareness as our concept has expanded. Franchisees in our 13 most penetrated markets have formed advertising co-ops at our direction to leverage their collective local marketing spend to buy traditional and digital media more efficiently. As our restaurant base continues to grow and we further penetrate existing and new markets, we expect to add more advertising co-ops in markets where efficient media purchasing can be achieved. Over time, we believe increased marketing funds contributed to our ad fund combined with local co-op spending will yield sufficient funds to efficiently purchase traditional and digital media nationally to further expand our brand recognition.

| • | Leverage Social Media |

We expect that our advertising will become more cost-effective and drive system-wide revenue more efficiently as we grow in scale and further increase our use of social media to activate interest from our guests. We believe social media is a cost-effective way of targeting existing and new guests, as we do not have to purchase as much advertising through more expensive forms of traditional media. Furthermore, we believe that our strong and growing social media presence will drive more orders through our online portals.

#CreateShareholderValue

We expect our asset-light, highly-franchised business model to generate strong operating margins and consistent free cash flow as a result of low capital expenditures and working capital needs. As we execute our growth strategy, we believe we will continue to grow revenue and leverage our cost infrastructure, generating continued earnings growth and strong free cash flow, which will create additional equity value for our shareholders.

7

Table of Contents

CORPORATE AND OTHER INFORMATION

The first Wingstop restaurant opened in July 1994. Our operating company, Wingstop Restaurants Inc., was incorporated in November 1996 and began offering franchises for Wingstop restaurants in May 1997. The first franchised restaurant opened in April 1998. On April 9, 2010, Wingstop Holdings, Inc., the holding company for Wingstop Restaurants Inc., was acquired by Wing Stop Holding Corporation. As of March 28, 2015, we were the franchisor of 726 restaurants and owned and operated 19 restaurants for a total of 745 system-wide restaurants in 37 states and 6 countries.

Our principal executive offices are located at 5501 LBJ Freeway, 5th Floor, Dallas, Texas 75240, and our telephone number at that address is (972) 686-6500. Our website is located at www.wingstop.com. Our website, and the information on our website, is neither part of this prospectus nor incorporated by reference herein.

THE REORGANIZATION

Wingstop Inc. was incorporated in Delaware on March 18, 2015, as a wholly owned subsidiary of Wing Stop Holding Corporation. On May 28, 2015, Wing Stop Holding Corporation merged with and into Wingstop Inc., with Wingstop Inc. as the surviving corporation in the merger.

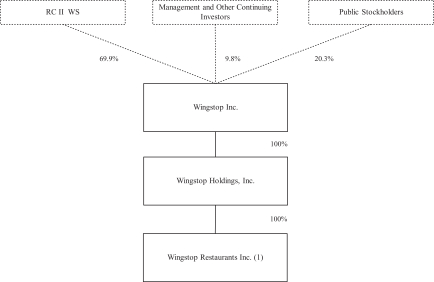

Pursuant to the merger, each holder of Wing Stop Holding Corporation common stock received 0.545 shares of common stock of Wingstop Inc. for each one share of Wing Stop Holding Corporation with fractional shares being cashed out and each option to purchase common stock of Wing Stop Holding Corporation was assumed by Wingstop Inc. and converted into an option to purchase 0.545 shares of common stock of Wingstop Inc. for each one share of Wing Stop Holding Corporation with the remaining terms of each such option remaining unchanged, except as was necessary to reflect the reorganization. 48,497,594 shares of Wing Stop Holding Corporation common stock were converted into 26,431,182 shares of common stock of Wingstop Inc. in connection with the reorganization. The Wing Stop Holding Corporation shares were then cancelled and retired. The following chart illustrates our organizational structure upon completion of this offering, assuming no exercise of the underwriters’ option to purchase additional shares of common stock:

| (1) | The franchisor of all Wingstop franchised restaurants and the lessee, owner and operator of all company-owned restaurants. |

8

Table of Contents

RISK FACTORS

Investing in our common stock involves substantial risk, and our ability to successfully operate our business is subject to numerous risks, including those that are generally associated with our industry. Any of the risks set forth in this prospectus under the heading “Risk Factors” may limit our ability to successfully execute our business strategy. You should carefully consider all of the information set forth in this prospectus and, in particular, should evaluate the specific risks set forth in this prospectus under the heading “Risk Factors” in deciding whether to invest in our common stock. The following is a summary of some of the principal risks we face:

| • | if we fail to successfully implement our growth strategy, which includes opening new domestic and international restaurants, our ability to increase our revenue and operating profits could be adversely affected; |

| • | our financial results are affected by the operating results of our and our franchisees existing restaurants; |

| • | our results of operations and growth strategy depend in significant part on the success of our franchisees, and we are subject to a variety of additional risks associated with our franchisees; |

| • | if we fail to identify, recruit and contract with a sufficient number of qualified franchisees, our ability to open new franchise restaurants and increase our revenue could be materially adversely affected; |

| • | our franchisees could take actions that could harm our business; |

| • | interruptions in the supply of product to company-owned restaurants and franchisees could adversely affect our revenue; |

| • | our success depends on our ability to compete with many other restaurants; |

| • | reliance on past increases in our domestic same store sales or our average weekly sales as an indication of our future results of operations; |

| • | our quarterly operating results may fluctuate significantly, resulting in a decline in our stock price; and |

| • | expansion into new markets presents increased risks. |

EMERGING GROWTH COMPANY STATUS

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act, which permits us to elect not to be subject to certain disclosure and other requirements that otherwise would have been applicable to us had we not been an “emerging growth company.” These provisions include:

| • | only two years of audited financial statements, in addition to any required unaudited interim financial statements, with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure in this prospectus; |

| • | reduced disclosure about our executive compensation arrangements; |

| • | no requirement for non-binding advisory votes on executive compensation or golden parachute arrangements; and |

| • | exemption from the auditor attestation requirement in the assessment of our internal controls over financial reporting. |

We may take advantage of these exemptions for up to five years or such earlier time as we are no longer an “emerging growth company.” We will qualify as an “emerging growth company” until the earliest of (1) the last

9

Table of Contents

day of our fiscal year following the fifth anniversary of the date of completion of this offering, (2) the last day of our fiscal year in which we have annual gross revenue of $1.0 billion or more, (3) the date on which we have, during the previous three-year period, issued more than $1.0 billion in non-convertible debt, and (4) the last day of the fiscal year in which we become a “large accelerated filer” as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended, or the Exchange Act. Under this definition, we will be an “emerging growth company” upon completion of this offering and could remain an “emerging growth company” until as late as December 26, 2020.

In addition, the JOBS Act provides that an emerging growth company can take advantage of an extended transition period for complying with new or revised accounting standards. This allows an emerging growth company to delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have irrevocably elected not to avail ourselves of this exemption from new or revised accounting standards and, therefore, we will be subject to the same new or revised accounting standards as other public companies that are not emerging growth companies.

PRINCIPAL STOCKHOLDER

Roark Capital Partners II, LP and Roark Capital Partners Parallel II, LP, which we refer to in this prospectus, along with RC II WS (but excluding us and other companies that they own as a result of their investment activity), as Roark, are part of an Atlanta-based private equity firm with over $6 billion in equity capital commitments raised since inception. Roark and its affiliates invest primarily in consumer, business and environmental service companies with a specialization around franchised and multi-unit business models in the retail, restaurant and consumer services sectors. Immediately prior to this offering, Roark beneficially owned 84.5% of our outstanding common stock, and will beneficially own approximately 69.9% of our common stock immediately following consummation of this offering, assuming no exercise of the underwriters’ option to purchase additional shares of common stock. Therefore, Roark will be able to have a significant effect over fundamental and significant corporate matters and transactions. For example, we currently expect that, following this offering, four of the seven members of our board of directors will be employees of Roark Capital Management, LLC, which is an affiliate of Roark, and that our amended and restated certificate of incorporation will provide that the doctrine of corporate opportunity will not apply against Roark, or any of our directors who are employees of or affiliated with Roark. Accordingly, the interests of Roark may supersede ours, causing it or its affiliates to compete against us or to pursue opportunities instead of us, for which we have no recourse. We also expect to be a “controlled company” under Nasdaq corporate governance standards and to take advantage of the corporate governance exceptions related thereto. See “Risk Factors—Risks Related to this Offering and Ownership of our Common Stock.”

10

Table of Contents

THE OFFERING

| Common stock offered by us |

2,150,000 shares. |

| Common stock offered by the selling stockholders |

3,650,000 shares (or 4,520,000 shares if the underwriters’ option to purchase additional shares from one of the selling stockholders identified in this prospectus is exercised in full). |

| Common stock to be outstanding immediately after this offering |

28,581,182 shares. |

| Underwriters’ option to purchase additional shares of common stock |

The underwriters may also exercise their option to purchase up to an additional 870,000 shares of common stock from one of the selling stockholders identified in this prospectus. The underwriters can exercise this option at any time within 30 days from the date of this prospectus. |

| Use of proceeds |

We estimate, based upon an assumed initial public offering price of $17.00 per share (which is the midpoint of the price range set forth on the cover page of this prospectus) we will receive proceeds from the offering of approximately $30.9 million after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. We intend to use the proceeds from this offering (i) for the repayment of debt, (ii) to pay a fee in connection with the termination of our management agreement with Roark Capital Management, LLC and (iii) other general corporate purposes. See “Use of Proceeds.” We will not receive any of the proceeds from the sale of shares of common stock by the selling stockholders. |

| Principal stockholder |

Upon completion of this offering, RC II WS will continue to own a controlling interest in us. Accordingly, we currently intend to avail ourselves of the “controlled company” exemption under the corporate governance rules of Nasdaq. |

| Dividend policy |

We currently expect to retain all future earnings, if any, for use in the operation and expansion of our business and repayment of debt; therefore, we do not anticipate paying cash dividends on our common stock in the foreseeable future. See “Dividend Policy” below. |

| Directed share program |

At our request, the underwriters have reserved 5.0% of the shares of common stock offered by this prospectus for sale, at the initial public offering price, to our directors, officers, employees, business associates and related persons. If these persons purchase shares, this will reduce the number of shares available for sale to the public. |

11

Table of Contents

| Risk factors |

You should carefully read and consider the information set forth under the heading “Risk Factors” of this prospectus and all other information set forth in this prospectus before investing in our common stock. |

| Conflicts of Interest |

The net proceeds from this offering will be used to repay borrowings under our senior secured credit facility. Because an affiliate of Wells Fargo Securities, LLC is a lender under our senior secured credit facility and will receive 5% or more of the net proceeds of this offering, Wells Fargo Securities, LLC is deemed to have a “conflict of interest” under Rule 5121 of the Financial Industry Regulatory Authority, Inc., or FINRA. As a result, this offering will be conducted in accordance with FINRA Rule 5121. Pursuant to that rule, the appointment of a “qualified independent underwriter” is not required in connection with this offering as the members primarily responsible for managing the public offering do not have a conflict of interest, are not affiliates of any member that has a conflict of interest and meet the requirements of paragraph (f)(12)(E) of FINRA Rule 5121. See “Use of Proceeds” and “Underwriters (Conflicts of Interest).” |

| Proposed Nasdaq ticker symbol |

“WING” |

Unless otherwise indicated, all information in this prospectus relating to the number of shares of common stock that will be outstanding following this offering:

| • | gives effect to the reorganization; |

| • | excludes, as of March 28, 2015, 1,356,262 shares issuable upon the exercise of outstanding stock options at a weighted-average exercise price of $3.03 per share; |

| • | excludes 2,143,589 shares reserved for future issuance under our new equity compensation plan, assuming the number of shares offered, as set forth on the cover page of this prospectus, remains the same; |

| • | assumes no exercise of the underwriters’ option to purchase additional shares from one of the selling stockholders identified in this prospectus; and |

| • | an initial public offering price of $17.00 per share (which is the midpoint of the price range set forth on the cover page of this prospectus). |

12

Table of Contents

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL AND OTHER DATA

Wingstop Inc. was incorporated in Delaware on March 18, 2015. On May 28, 2015, Wing Stop Holding Corporation merged with and into Wingstop Inc., with Wingstop Inc. as the surviving corporation in the merger. Pursuant to the merger, each holder of Wing Stop Holding Corporation common stock received 0.545 shares of common stock of Wingstop Inc. for each one share of Wing Stop Holding Corporation and each option to purchase common stock of Wing Stop Holding Corporation was assumed by Wingstop Inc. and converted into an option to purchase 0.545 shares of common stock of Wingstop Inc. for each one share of Wing Stop Holding Corporation with the remaining terms of each such option remaining unchanged, except as was necessary to reflect the reorganization. The following tables set forth the financial statements of Wingstop Inc., giving effect to the reorganization. All references to per share amounts in the table below have been adjusted to reflect the reorganization retrospectively.

We derived the financial information for the thirteen weeks ended March 28, 2015 and March 29, 2014 from our unaudited consolidated financial statements, which are included elsewhere in this prospectus. We derived the financial information for the fiscal years ended December 27, 2014, December 28, 2013 and December 29, 2012 from our audited consolidated financial statements, which are included elsewhere in this prospectus.

Wingstop utilizes a 52- or 53-week fiscal year that ends on the last Saturday of the calendar year. The fiscal years ended December 27, 2014, December 28, 2013 and December 29, 2012 included 52 weeks. The first three quarters of our fiscal year consist of 13 weeks and our fourth quarter consists of 13 weeks for 52-week fiscal years and 14 weeks for 53-week fiscal years.

The historical results presented below are not necessarily indicative of the results to be expected for any future period. This information should be read in conjunction with “Risk Factors,” “Selected Historical Consolidated Financial and Other Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and each of their related notes included elsewhere in this prospectus.

| Thirteen weeks ended | Year ended | |||||||||||||||||||

| (in thousands) | March 28, 2015 |

March 29, 2014 |

December 27, 2014 |

December 28, 2013 |

December 29, 2012 |

|||||||||||||||

| Consolidated Statements of Operations Data: |

||||||||||||||||||||

| Revenue: |

||||||||||||||||||||

| Royalty revenue and franchise fees |

$ | 11,157 | $ | 8,659 | $ | 38,032 | $ | 30,202 | $ | 25,057 | ||||||||||

| Company-owned restaurant sales |

7,869 | 8,015 | 29,417 | 28,797 | 26,534 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total revenue |

19,026 | 16,674 | 67,449 | 58,999 | 51,591 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Cost and expenses: |

||||||||||||||||||||

| Cost of sales |

5,736 | 5,311 | 20,473 | 22,176 | 21,262 | |||||||||||||||

| Selling, general and administrative |

7,676 | 4,761 | 26,006 | 18,913 | 15,896 | |||||||||||||||

| Depreciation and amortization |

663 | 815 | 2,904 | 3,030 | 2,930 | |||||||||||||||

| Earn-out obligation |

— | — | — | — | 2,500 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total costs and expenses |

14,075 | 10,887 | 49,383 | 44,119 | 42,588 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating income |

4,951 | 5,787 | 18,066 | 14,880 | 9,003 | |||||||||||||||

| Interest expense, net |

787 | 1,016 | 3,684 | 2,863 | 2,431 | |||||||||||||||

| Other (income) expense, net |

29 | 23 | 84 | (6 | ) | (8 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income before income tax expense |

4,135 | 4,748 | 14,298 | 12,023 | 6,580 | |||||||||||||||

| Income tax expense |

1,581 | 1,764 | 5,312 | 4,493 | 3,000 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

$ | 2,554 | $ | 2,984 | $ | 8,986 | $ | 7,530 | $ | 3,580 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Consolidated Statement of Cash Flows Data: |

||||||||||||||||||||

| Net cash provided by operating activities |

2,520 | 5,763 | $ | 14,370 | $ | 10,906 | $ | 10,421 | ||||||||||||

| Net cash provided by (used in) investing activities |

(99 | ) | 707 | (363 | ) | (2,144 | ) | (1,447 | ) | |||||||||||

| Net cash provided by (used in) financing activities |

(9,242 | ) | 198 | (7,457 | ) | (9,842 | ) | (6,902 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net increase (decrease) in cash and cash equivalents |

$ | (6,821 | ) | $ | 6,668 | $ | 6,550 | $ | (1,080 | ) | $ | 2,072 | ||||||||

13

Table of Contents

| Thirteen weeks ended | Year ended | |||||||||||||||||||

| (in thousands, except share, per share and unit data) | March 28, 2015 |

March 29, 2014 |

December 27, 2014 |

December 28, 2013 |

December 29, 2012 |

|||||||||||||||

| Per Share Data: |

||||||||||||||||||||

| Earnings per share: |

||||||||||||||||||||

| Basic |

$ 0.10 | $ | 0.12 | $ | 0.35 | $ | 0.30 | $ | 0.14 | |||||||||||

| Diluted |

$ 0.10 | $ | 0.11 | 0.34 | 0.29 | 0.14 | ||||||||||||||

| Weighted average shares outstanding: |

||||||||||||||||||||

| Basic |

26,290 | 25,621 | 25,846 | 25,168 | 24,746 | |||||||||||||||

| Diluted |

26,607 | 26,053 | 26,204 | 25,648 | 25,338 | |||||||||||||||

| Pro forma earnings per share (1): |

||||||||||||||||||||

| Basic |

0.09 | 0.32 | ||||||||||||||||||

| Diluted |

0.09 | 0.32 | ||||||||||||||||||

| Selected Other Data (2): |

||||||||||||||||||||

| Number of system-wide restaurants open at end of period |

745 | 627 | 712 | 614 | 546 | |||||||||||||||

| Number of domestic company restaurants open at end of period |

19 | 19 | 19 | 24 | 23 | |||||||||||||||

| Number of domestic franchise restaurants open at end of period |

681 | 587 | 652 | 569 | 510 | |||||||||||||||

| Number of international franchise restaurants open at end of period |

45 | 21 | 41 | 21 | 13 | |||||||||||||||

| System-wide sales (3) |

$199,217 | $ | 162,764 | $ | 678,771 | $ | 549,904 | $ | 457,315 | |||||||||||

| Domestic restaurant AUV |

N/A | N/A | $ | 1,073 | $ | 974 | $ | 902 | ||||||||||||

| Company-owned domestic AUV |

N/A | N/A | $ | 1,504 | $ | 1,206 | $ | 1,126 | ||||||||||||

| Number of restaurants opened (during period) |

34 | 14 | 102 | 74 | 57 | |||||||||||||||

| Number of restaurants closed (during period) |

1 | 1 | 4 | 6 | 10 | |||||||||||||||

| Company-owned restaurants refranchised (during period) |

— | — | 5 | — | 1 | |||||||||||||||

| EBITDA (4) |

$ 5,585 | $ | 6,579 | $ | 20,886 | $ | 17,916 | $ | 11,941 | |||||||||||

| Adjusted EBITDA (4) |

$ 7,194 | $ | 6,715 | $ | 24,378 | $ | 19,495 | $ | 15,615 | |||||||||||

| Adjusted EBITDA margin (5) |

37.8 | % | 40.3 | % | 36.1 | % | 33.0 | % | 30.3 | % | ||||||||||

| Same Store Sales Data (6): |

||||||||||||||||||||

| Domestic same store base (end of period) |

603 | 538 | 589 | 527 | 482 | |||||||||||||||

| Change in domestic same store sales |

10.7 | % | 9.7 | % | 12.5 | % | 9.9 | % | 13.8 | % | ||||||||||

| As of March 28, 2015 | ||||||||

| (unaudited) | ||||||||

| (in thousands) | Actual | Pro forma (7)(8) | ||||||

| Consolidated Balance Sheet Data: |

||||||||

| Cash and cash equivalents |

$ | 2,902 | $ | 2,902 | ||||

| Total assets |

114,071 | 114,071 | ||||||

| Total long-term debt (including current portion) |

132,500 | 104,862 | ||||||

| Total stockholders’ equity (deficit) |

(54,048 | ) | (23,098 | ) | ||||

| (1) | See note 18 to our audited consolidated financial statements and note 13 to our unaudited consolidated financial statements. |

| (2) | See the definitions of key performance indicators under “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Performance Indicators.” |

14

Table of Contents

| (3) | The percentage of system-wide sales attributable to company-owned restaurants was 3.9% and 4.9% for the thirteen weeks ended March 28, 2015 and March 29, 2014, respectively, and was 4.3%, 5.2% and 5.8% for the fiscal years ended December 27, 2014, December 28, 2013 and December 29, 2012, respectively. The remainder was generated by franchised restaurants, as reported by our franchisees. |

| (4) | EBITDA and Adjusted EBITDA are supplemental measures of our performance that are not required by, or presented in accordance with, U.S. GAAP. EBITDA and Adjusted EBITDA are not measurements of our financial performance under U.S. GAAP and should not be considered as an alternative to net income or any other performance measure derived in accordance with U.S. GAAP, or as an alternative to cash flows from operating activities as a measure of our liquidity. |

We define “EBITDA” as net income before interest expense, net, income tax expense, and depreciation and amortization. We define “Adjusted EBITDA” as EBITDA further adjusted for management fees and expense reimbursement, transaction costs, gains and losses on the disposal of assets, stock-based compensation expense and earn-out obligation. We caution investors that amounts presented in accordance with our definitions of EBITDA and Adjusted EBITDA may not be comparable to similar measures disclosed by our competitors, because not all companies and analysts calculate EBITDA and Adjusted EBITDA in the same manner. We present EBITDA and Adjusted EBITDA because we consider them to be important supplemental measures of our performance and believe they are frequently used by securities analysts, investors and other interested parties in the evaluation of companies in our industry. Management believes that investors’ understanding of our performance is enhanced by including these non-GAAP financial measures as a reasonable basis for comparing our ongoing results of operations. Many investors are interested in understanding the performance of our business by comparing our results from ongoing operations period over period and would ordinarily add back non-cash expenses such as depreciation and amortization, as well as items that are not part of normal day-to-day operations of our business.

Management uses EBITDA and Adjusted EBITDA:

| • | as a measurement of operating performance because they assist us in comparing the operating performance of our restaurants on a consistent basis, as they remove the impact of items not directly resulting from our core operations; |

| • | for planning purposes, including the preparation of our internal annual operating budget and financial projections; |

| • | to evaluate the performance and effectiveness of our operational strategies; |

| • | to evaluate our capacity to fund capital expenditures and expand our business; and |

| • | to calculate incentive compensation payments for our employees, including assessing performance under our annual incentive compensation plan and determining the vesting of performance shares. |

By providing these non-GAAP financial measures, together with a reconciliation to the most comparable GAAP measure, we believe we are enhancing investors’ understanding of our business and our results of operations, as well as assisting investors in evaluating how well we are executing our strategic initiatives. Items excluded from these non-GAAP measures are significant components in understanding and assessing financial performance. In addition, the instruments governing our indebtedness use EBITDA (with additional adjustments) to measure our compliance with covenants such as fixed charge coverage, lease adjusted leverage and debt incurrence. EBITDA and Adjusted EBITDA have limitations as analytical tools, and should not be considered in isolation, or as an alternative to, or a substitute for net income or other financial statement data presented in our consolidated financial statements as indicators of financial performance. Some of the limitations are:

| • | such measures do not reflect our cash expenditures, or future requirements for capital expenditures or contractual commitments; |

| • | such measures do not reflect changes in, or cash requirements for, our working capital needs; |

15

Table of Contents

| • | such measures do not reflect the interest expense, or the cash requirements necessary to service interest or principal payments on our debt; |

| • | such measures do not reflect our tax expense or the cash requirements to pay our taxes; |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future and such measures do not reflect any cash requirements for such replacements; and |

| • | other companies in our industry may calculate such measures differently than we do, limiting their usefulness as comparative measures. |

Due to these limitations, EBITDA and Adjusted EBITDA should not be considered as measures of discretionary cash available to us to invest in the growth of our business. We compensate for these limitations by relying primarily on our U.S. GAAP results and using these non-GAAP measures only supplementally. As noted in the table below, Adjusted EBITDA includes adjustments for transaction costs, gains and losses on disposal of assets and stock-based compensation, among other items. It is reasonable to expect that these items will occur in future periods. However, we believe these adjustments are appropriate because the amounts recognized can vary significantly from period to period, do not directly relate to the ongoing operations of our restaurants and complicate comparisons of our internal operating results and operating results of other restaurant companies over time. In addition, Adjusted EBITDA includes adjustments for other items that we do not expect to regularly record following this offering, such as management fees and expense reimbursement. Each of the normal recurring adjustments and other adjustments described in this paragraph and in the reconciliation table below help management with a measure of our core operating performance over time by removing items that are not related to day-to-day operations.

The following table reconciles EBITDA and Adjusted EBITDA to the most directly comparable U.S. GAAP financial performance measure, which is net income:

| Thirteen weeks ended | Year ended | |||||||||||||||||||

| (in thousands) | March 28, 2015 |

March 29, 2014 |

December 27, 2014 |

December 28, 2013 |

December 29, 2012 |

|||||||||||||||

| Net income |

$2,554 | $2,984 | $ | 8,986 | $ | 7,530 | $ | 3,580 | ||||||||||||

| Interest expense, net |

787 | 1,016 | 3,684 | 2,863 | 2,431 | |||||||||||||||

| Income tax expense |

1,581 | 1,764 | 5,312 | 4,493 | 3,000 | |||||||||||||||

| Depreciation and amortization |

663 | 815 | 2,904 | 3,030 | 2,930 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| EBITDA |

$5,585 | $6,579 | $ | 20,886 | $ | 17,916 | $ | 11,941 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Management fees (a) |

117 | 114 | 449 | 436 | 422 | |||||||||||||||

| Transaction costs (b) |

1,303 | 5 | 2,169 | 395 | 308 | |||||||||||||||

| Gains and losses on disposal of assets (c) |

— | (86) | (86 | ) | — | (20 | ) | |||||||||||||

| Stock-based compensation expense (d) |

189 | 103 | 960 | 748 | 464 | |||||||||||||||

| Earn-out obligation (e) |

— | — | — | — | 2,500 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted EBITDA |

$7,194 | $6,715 | $ | 24,378 | $ | 19,495 | $ | 15,615 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (a) | Includes management fees and other out-of-pocket expenses paid to Roark Capital Management, LLC. |

| (b) | Represents costs and expenses related to refinancings of our credit agreement and our initial public offering. |

| (c) | Represents non-cash gains and losses resulting from the sale of company-owned restaurants to a franchisee and associated goodwill impairment. |

16

Table of Contents

| (d) | Includes non-cash, stock-based compensation. |

| (e) | Represents an earn-out payment made to our prior owner based on us achieving revenue benchmarks specified in the acquisition agreement governing our purchase. There are no further obligations related to the earn-out remaining under the acquisition agreement. |

| (5) | Adjusted EBITDA margin is defined as the ratio of Adjusted EBITDA to total revenue. We present Adjusted EBITDA margin because it is used by management as a performance measurement of Adjusted EBITDA generated from total revenue. See footnote 4 above for a discussion of Adjusted EBITDA as a non-GAAP measure and a reconciliation of net income to EBITDA and Adjusted EBITDA. |

| (6) | We define the domestic same store base to include those domestic restaurants open for at least 52 full weeks. Change in domestic same store sales reflects the change in year-over-year sales for the domestic same store base. |

| (7) | The pro forma balance sheet data gives effect to (i) the sale by us of 2,150,000 shares of our common stock in this offering at an assumed initial public offering price of $17.00 per share (which is the midpoint of the price range set forth on the cover page of this prospectus) after deducting estimated underwriting discounts and commissions and offering expenses paid by us and (ii) the application of the net proceeds from this offering to us as described under “Use of Proceeds.” |

| (8) | Each $1.00 increase or decrease in the assumed initial public offering price of $17.00 per share (which is the midpoint of the price range set forth on the cover page of this prospectus) would increase or decrease each of cash and cash equivalents and total stockholders’ equity (deficit) on a pro forma basis by approximately $2.0 million, assuming the number of shares offered, as set forth on the cover page of this prospectus, remains the same, and after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

17

Table of Contents

Risks Related to Our Business

If we fail to successfully implement our growth strategy, which includes opening new restaurants, our ability to increase our revenue and operating profits could be adversely affected.

Our growth strategy relies substantially upon new restaurant development by existing and new franchisees. While we believe there is opportunity for our brand to grow to up to approximately 2,500 domestic restaurants over the long term, we do not currently target a specific number of annual new restaurant openings over a multi-year period. Therefore, we cannot predict the time period over which we can achieve this level of domestic restaurant growth or whether we will achieve this level of growth at all. In addition, we and our franchisees face many challenges in opening new restaurants, including:

| • | availability of financing; |

| • | selection and availability of suitable restaurant locations; |

| • | competition for restaurant sites; |

| • | negotiation of acceptable lease and financing terms; |

| • | securing required governmental permits and approvals; |

| • | consumer tastes in new geographic regions and acceptance of our products; |

| • | employment and training of qualified personnel; |

| • | impact of inclement weather, natural disasters, and other acts of nature; |

| • | general economic and business conditions; and |

| • | the general legal and regulatory landscape in which we and our restaurants operate. |

In particular, because the majority of our new restaurant development is funded by franchisee investment, our growth strategy is dependent on our franchisees’ (or prospective franchisees’) ability to access funds to finance such development. We do not provide our franchisees with direct financing and therefore their ability to access borrowed funds generally depends on their independent relationships with various financial institutions. Some of our existing franchisees utilize loans guaranteed by the U.S. Small Business Administration, or SBA, which guarantees loans made by financial institutions to small businesses in the U.S., including franchisees. If SBA guaranteed loans are no longer available to our franchisees (or potential franchisees), their ability to obtain the requisite financing at attractive rates, or at all, could be adversely affected. Moreover, if our franchisees (or prospective franchisees) are not able to obtain financing from any source at commercially reasonable rates, or at all, they may be unwilling or unable to invest in the development of new restaurants, and our future growth could be adversely affected.

To the extent our franchisees are unable to open new restaurants as we anticipate, our revenue growth would come primarily from growth in comparable store sales. Our failure to add a significant number of new restaurants or grow domestic same store sales would adversely affect our ability to increase our revenue and operating income and could materially and adversely harm our business and operating results.

Our business and results of operations depend significantly upon the success of our and our franchisees’ existing restaurants.

Our business and results of operations are significantly dependent upon the success of our franchisees and our company-owned restaurants. We and our franchisees may be adversely affected by:

| • | declining economic conditions; |

| • | increased competition in the restaurant industry; |

18

Table of Contents

| • | changes in consumer tastes and preferences; |

| • | demographic trends; |

| • | customers’ budgeting constraints; |

| • | customers’ willingness to accept menu price increases; |

| • | adverse weather conditions; |

| • | our reputation and consumer perception of our concepts’ offerings in terms of quality, price, value and service; and |

| • | customers’ experiences in our restaurants. |

Our company-owned restaurants and our franchisees are also susceptible to increases in certain key operating expenses that are either wholly or partially beyond our control, including:

| • | food, particularly bone-in chicken wings, which we do not or cannot effectively hedge; |

| • | labor costs, including wage, workers’ compensation, minimum wage requirements, health care and other benefits expenses; |

| • | rent expenses and construction, remodeling, maintenance and other costs under leases for our existing and new restaurants; |

| • | compliance costs as a result of changes in legal, regulatory or industry standards; |

| • | energy, water and other utility costs; |

| • | insurance costs; |

| • | information technology and other logistical costs; and |

| • | expenses associated with legal proceedings and regulatory compliance. |

Our business and results of operations depend in significant part on the future performance of existing and new franchise restaurants, and we are subject to a variety of additional risks associated with our franchisees.

A substantial portion of our revenue comes from royalties generated by our franchised restaurants. We anticipate that franchise royalties will represent a substantial part of our revenue in the future. As of March 28, 2015, we had 264 domestic franchisees operating 681 domestic restaurants and 6 international franchisees operating 45 international restaurants. Our largest franchisee operated 46 restaurants and our top 10 franchisees operated a total of 186 restaurants as of March 28, 2015. Accordingly, we are reliant on the performance of our franchisees in successfully operating their restaurants and paying royalties to us on a timely basis. Our franchise system subjects us to a number of risks, any one of which may impact our ability to collect royalty payments from our franchisees, may harm the goodwill associated with our franchise, and may materially adversely affect our business and results of operations.

Our franchisees are an integral part of our business. We may be unable to successfully implement our growth strategy without the participation of our franchisees. Franchisees may fail to participate in our marketing initiatives, which could materially adversely affect their sales trends, average weekly sales and results of operations. The failure of our franchisees to focus on the fundamentals of restaurant operations, such as quality, service and cleanliness, would have a negative impact on our success. In addition, if our franchisees fail to renew their franchise agreements, our royalty revenue may decrease which in turn could materially and adversely affect our business and operating results. It also may be difficult for us to monitor our international franchisees’ implementation of our growth strategy due to our lack of personnel in the markets served by such franchisees.

Furthermore, a bankruptcy of any multi-unit franchisee could negatively impact our ability to collect payments due under such franchisee’s franchise agreements. In a franchisee bankruptcy, the bankruptcy trustee

19

Table of Contents