Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Synchrony Financial | d932928d8k.htm |

|

|

Bernstein Strategic Decisions Conference

May 28, 2015

|

|

Disclaimers

Cautionary Statement Regarding Forward-Looking Statements

The following slides are part of a presentation by Synchrony Financial and are intended to be viewed as part of that presentation.

This presentation contains certain forward-looking statements as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, which are subject to the “safe harbor” created by those sections. Forward-looking statements may be identified by words such as “outlook,” “expects,” “intends,” “anticipates,” “plans,” “believes,” “seeks,” “targets,” “estimates,” “will,” “should,” “may” or words of similar meaning, but these words are not the exclusive means of identifying forward-looking statements. Forward-looking statements are based on management’s current expectations and assumptions, and are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. As a result, actual results could differ materially from those indicated in these forward-looking statements. Factors that could cause actual results to differ materially include global political, economic, business, competitive, market, regulatory and other factors and risks, such as: the impact of macroeconomic conditions and whether industry trends we have identified develop as anticipated; retaining existing partners and attracting new partners, concentration of our platform revenue in a small number of Retail Card partners, promotion and support of our products by our partners, and financial performance of our partners; our need for additional financing, higher borrowing costs and adverse financial market conditions impacting our funding and liquidity, and any reduction in our credit ratings; our ability to securitize our loans, occurrence of an early amortization of our securitization facilities, loss of the right to service or subservice our securitized loans, and lower payment rates on our securitized loans; our reliance on dividends, distributions and other payments from Synchrony Bank; our ability to grow our deposits in the future; changes in market interest rates and the impact of any margin compression; effectiveness of our risk management processes and procedures, reliance on models which may be inaccurate or misinterpreted, our ability to manage our credit risk, the sufficiency of our allowance for loan losses and the accuracy of the assumptions or estimates used in preparing our financial statements; our ability to offset increases in our costs in retailer share arrangements; competition in the consumer finance industry; our concentration in the U.S. consumer credit market; our ability to successfully develop and commercialize new or enhanced products and services; our ability to realize the value of strategic investments; reductions in interchange fees; fraudulent activity; cyber-attacks or other security breaches; failure of third parties to provide various services that are important to our operations; disruptions in the operations of our computer systems and data centers; international risks and compliance and regulatory risks and costs associated with international operations; alleged infringement of intellectual property rights of others and our ability to protect our intellectual property; litigation and regulatory actions; damage to our reputation; our ability to attract, retain and motivate key officers and employees; tax legislation initiatives or challenges to our tax positions and state sales tax rules and regulations; significant and extensive regulation, supervision, examination and enforcement of our business by governmental authorities, the impact of the Dodd-Frank Act and the impact of the CFPB’s regulation of our business; changes to our methods of offering our CareCredit products; impact of capital adequacy rules; restrictions that limit Synchrony Bank’s ability to pay dividends; regulations relating to privacy, information security and data protection; use of third-party vendors and ongoing third-party business relationships; failure to comply with anti-money laundering and anti-terrorism financing laws; effect of General Electric Capital Corporation being subject to regulation by the Federal Reserve Board both as a savings and loan holding company and as a systemically important financial institution; General Electric Company (GE) not completing the separation from us as planned or at all, GE’s inability to obtain savings and loan holding company deregistration (GE SLHC Deregistration) and GE continuing to have significant control over us; completion by the Federal Reserve Board of a review (with satisfactory results) of our preparedness to operate on a standalone basis, independently of GE, and Federal Reserve Board approval required for us to continue to be a savings and loan holding company, including the timing of the approval and the imposition of any significant additional capital or liquidity requirements; our need to establish and significantly expand many aspects of our operations and infrastructure; delays in receiving or failure to receive Federal Reserve Board agreement required for us to be treated as a financial holding company after the GE SLHC Deregistration; loss of association with GE’s strong brand and reputation; limited right to use the GE brand name and logo and need to establish a new brand; GE has significant control over us; terms of our arrangements with GE may be more favorable than what we will be able to obtain from unaffiliated third parties; obligations associated with being a public company; our incremental cost of operating as a standalone public company could be substantially more than anticipated; GE could engage in businesses that compete with us, and conflicts of interest may arise between us and GE; and failure caused by us of GE’s distribution of our common stock to its stockholders in exchange for its common stock to qualify for tax-free treatment, which may result in significant tax liabilities to GE for which we may be required to indemnify GE. For the reasons described above, we caution you against relying on any forward-looking statements, which should also be read in conjunction with the other cautionary statements that are included elsewhere in this presentation and in our public filings, including under the heading “Risk Factors” in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2014, as filed on February 23, 2015. You should not consider any list of such factors to be an exhaustive statement of all of the risks, uncertainties, or potentially inaccurate assumptions that could cause our current expectations or beliefs to change. Further, any forward-looking statement speaks only as of the date on which it is made, and we undertake no obligation to update or revise any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events, except as otherwise may be required by law.

Non-GAAP Measures

The information provided herein includes measures we refer to as “platform revenue” and “platform revenue excluding retailer share arrangements” and certain capital ratios, which are not prepared in accordance with U.S. generally accepted accounting principles (“GAAP”). The reconciliations of such measures to the most directly comparable GAAP measures are included in the appendix of this presentation.

| 1 |

|

|

|

Synchrony Financial Overview

Leading Consumer Finance Business

Largest PLCC provider in US (a)

A leader in financing for major consumer purchases and healthcare services

Long-standing and diverse partner base

Strong Value Proposition for Partners and Consumers

Deep partner integration enables customized loyalty products, across channels

Advanced data analytics and targeted marketing capabilities

Dedicated team members support partners to help maximize program effectiveness

Partner and cardholder focused mobile payments and e-commerce strategies

Attractive Growth and Ample Opportunities

Strong receivables growth

Significant opportunity to leverage long-standing partnerships to increase penetration

Opportunity to attract new partners

Developing broad product suite to support efforts to build a leading, full-scale online bank

Strong Financial Profile and Operating Performance

Solid fundamentals with attractive returns

Strong capital and liquidity with diverse funding profile

Positioned for future capital return post separation

(a) Source: The Nilson Report (April 2015 Issue #1062)

2

|

|

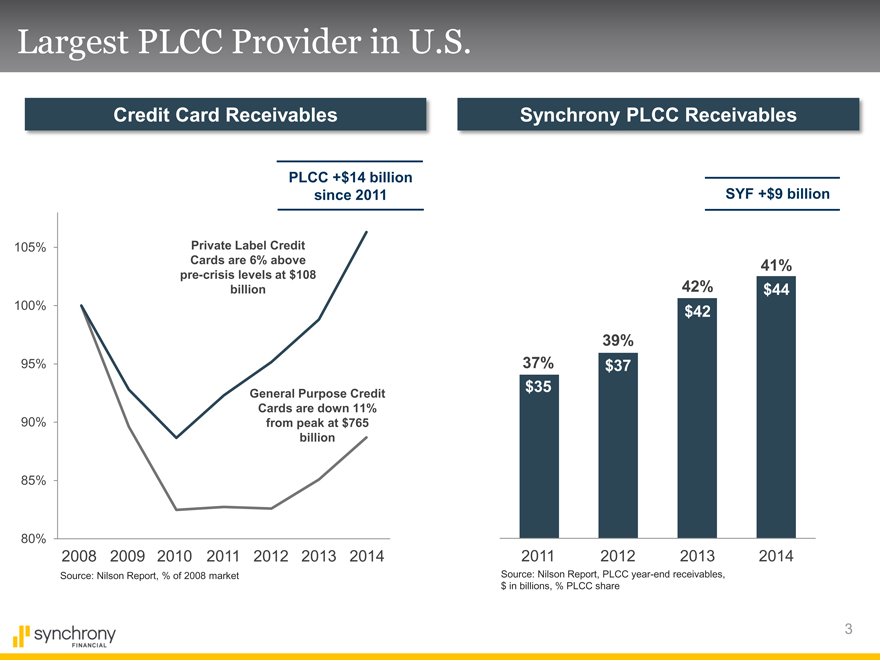

Largest PLCC Provider in U.S.

Credit Card Receivables

Synchrony PLCC Receivables

PLCC +$14 billion since 2011

Private Label Credit Cards are 6% above pre-crisis levels at $108 billion

General Purpose Credit Cards are down 11% from peak at $765 billion

105% 100% 95% 90% 85% 80%

2008 2009 2010 2011 2012 2013 2014

Source: Nilson Report, % of 2008 market

SYF +$9 billion

37% $35

39% $37

42% $42

41% $44

2011 2012 2013 2014

Source: Nilson Report, PLCC year-end receivables, $ in billions, % PLCC share

3

|

|

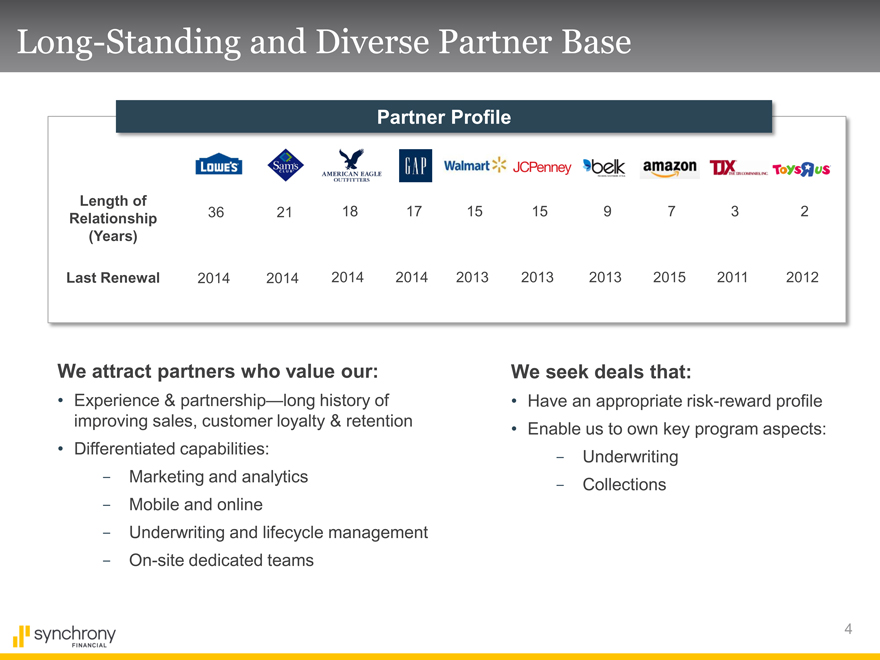

Long-Standing and Diverse Partner Base

Partner Profile

Length of Relationship (Years)

Last Renewal

36 21 18 17 15 15 9 7 3 2

2014 2014 2014 2014 2013 2013 2013 2015 2011 2012

We attract partners who value our:

Experience & partnership—long history of improving sales, customer loyalty & retention

Differentiated capabilities:

- Marketing and analytics

- Mobile and online

- Underwriting and lifecycle management

- On-site dedicated teams

We seek deals that:

Have an appropriate risk-reward profile

Enable us to own key program aspects:

- Underwriting

- Collections

4

|

|

Product Offerings

Credit Products

Retail Card

Private Label Dual Card

Retailer only Accepted at acceptance network locations

Affinity to retailer, provides customized benefits & features

Cash back, discounts

Credit events & promotions

Payment Solutions

Private Label

Retailer only acceptance

CareCredit

Private Label

Accepted at provider network locations

Big ticket focus, offering promotional financing options

Home

Furniture

Electronics luxury

power sports

Dental

Vision

Cosmetic

Veterinary

Deposit Products

Synchrony Bank

Deposits

Fast growing online bank

FDIC insured products

Certificates of Deposit

Money Market Accounts

Savings Accounts

IRA Money Market Accounts

IRA Certificates of Deposit

5

|

|

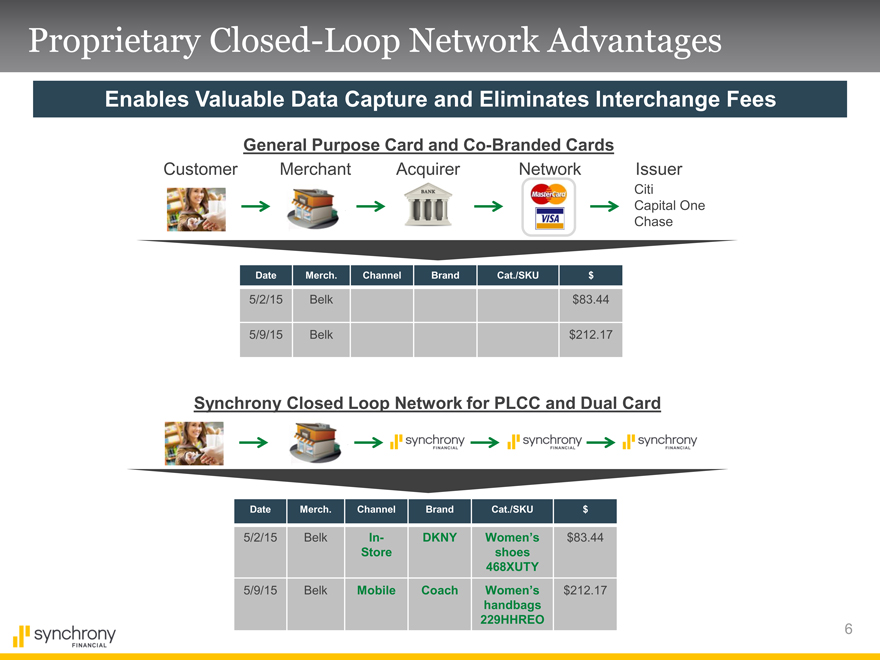

Proprietary Closed-Loop Network Advantages

Enables Valuable Data Capture and Eliminates Interchange Fees

General Purpose Card and Co-Branded Cards

Customer Merchant Acquirer Network Issuer

Citi

Capital One Chase

Date Merch. Channel Brand Cat./SKU $

5/2/15 Belk $83.44

5/9/15 Belk $212.17

Synchrony Closed Loop Network for PLCC and Dual Card

Date Merch. Channel Brand Cat./SKU $

5/2/15 Belk In- DKNY Women’s $83.44

Store shoes

468XUTY

5/9/15 Belk Mobile Coach Women’s $212.17

handbags

229HHREO

6

|

|

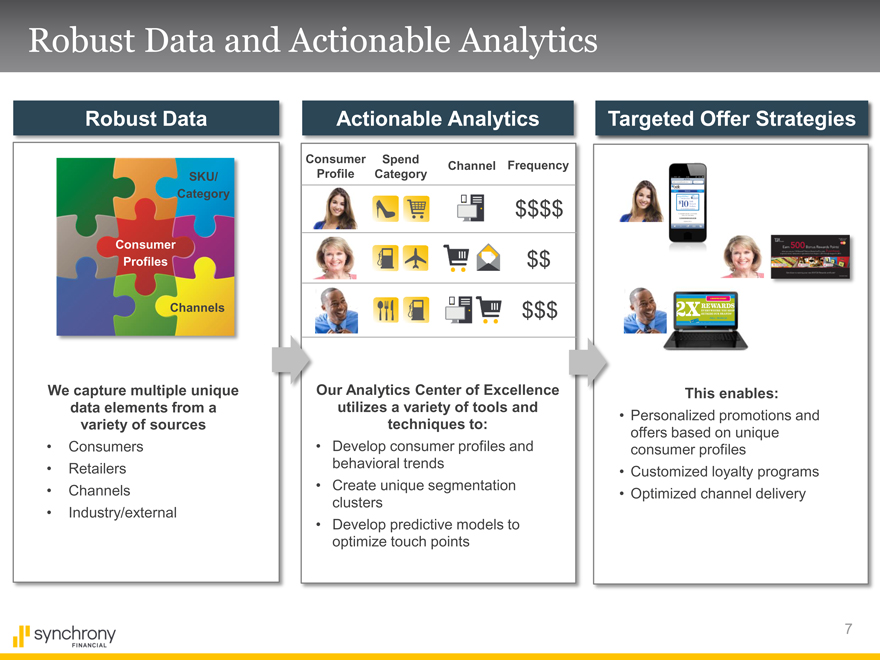

Robust Data and Actionable Analytics

Robust Data

SKU/ Category

Consumer

Profiles

Channels

We capture multiple unique data elements from a variety of sources

Consumers

Retailers

Channels

Industry/external

Actionable Analytics

Consumer Spend

Channel Frequency Profile Category

$$$$ $$ $$$

Our Analytics Center of Excellence utilizes a variety of tools and techniques to:

Develop consumer profiles and behavioral trends

Create unique segmentation clusters

Develop predictive models to optimize touch points

Targeted Offer Strategies

This enables:

Personalized promotions and offers based on unique consumer profiles

Customized loyalty programs

Optimized channel delivery

7

|

|

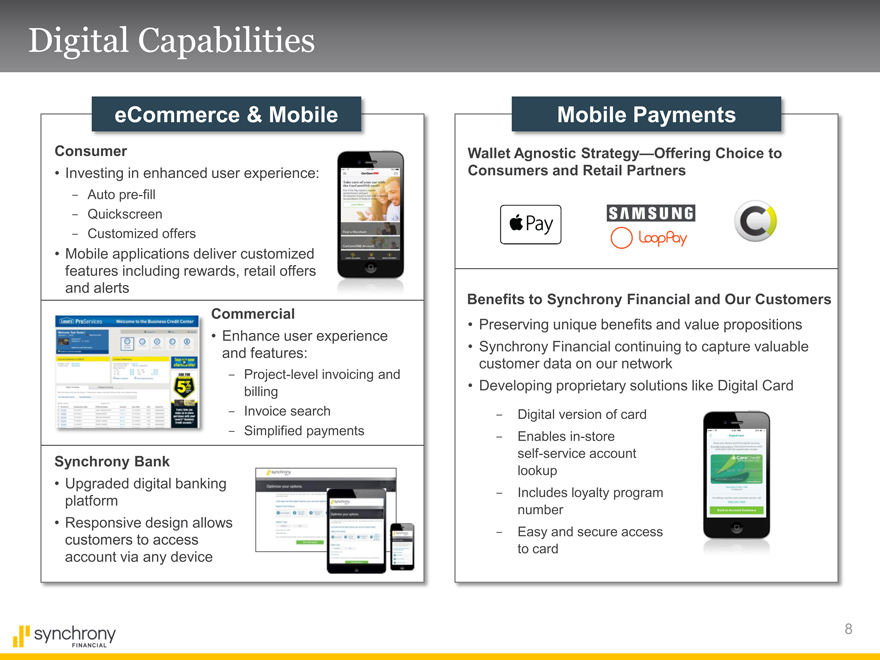

Digital Capabilities

eCommerce & Mobile

Consumer

Investing in enhanced user experience:

- Auto pre-fill

- Quickscreen

- Customized offers

Mobile applications deliver customized features including rewards, retail offers and alerts

Commercial

Enhance user experience and features:

- Project-level invoicing and billing

- Invoice search

- Simplified payments

Synchrony Bank

Upgraded digital banking platform

Responsive design allows customers to access account via any device

Mobile Payments

Wallet Agnostic Strategy—Offering Choice to Consumers and Retail Partners

Benefits to Synchrony Financial and Our Customers

Preserving unique benefits and value propositions

Synchrony Financial continuing to capture valuable customer data on our network

Developing proprietary solutions like Digital Card

- Digital version of card

- Enables in-store self-service account lookup

- Includes loyalty program number

- Easy and secure access to card

8

|

|

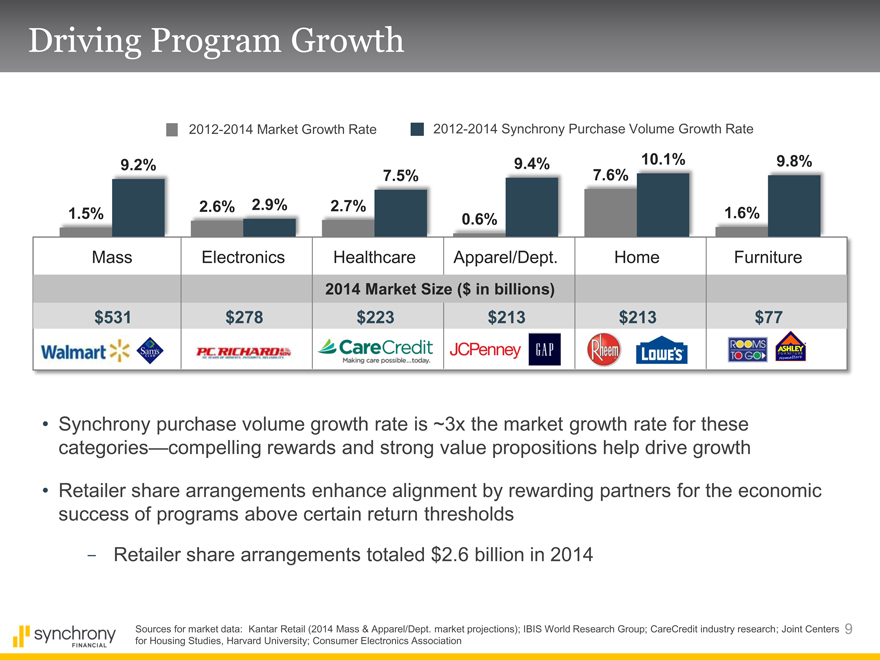

Driving Program Growth

2012-2014 Market Growth Rate

2012-2014 Synchrony Purchase Volume Growth Rate

9.2% 9.4% 10.1% 9.8%

7.5% 7.6%

1.5% 2.6% 2.9% 2.7% 1.6%

0.6%

Mass Electronics Healthcare Apparel/Dept. Home Furniture

2014 Market Size ($ in billions) $531 $278 $223 $213 $213 $77

Synchrony purchase volume growth rate is ~3x the market growth rate for these categories—compelling rewards and strong value propositions help drive growth

Retailer share arrangements enhance alignment by rewarding partners for the economic success of programs above certain return thresholds

- Retailer share arrangements totaled $2.6 billion in 2014

Sources for market data: Kantar Retail (2014 Mass & Apparel/Dept. market projections); IBIS World Research Group; CareCredit industry research; Joint Centers 9 for Housing Studies, Harvard University; Consumer Electronics Association

9

|

|

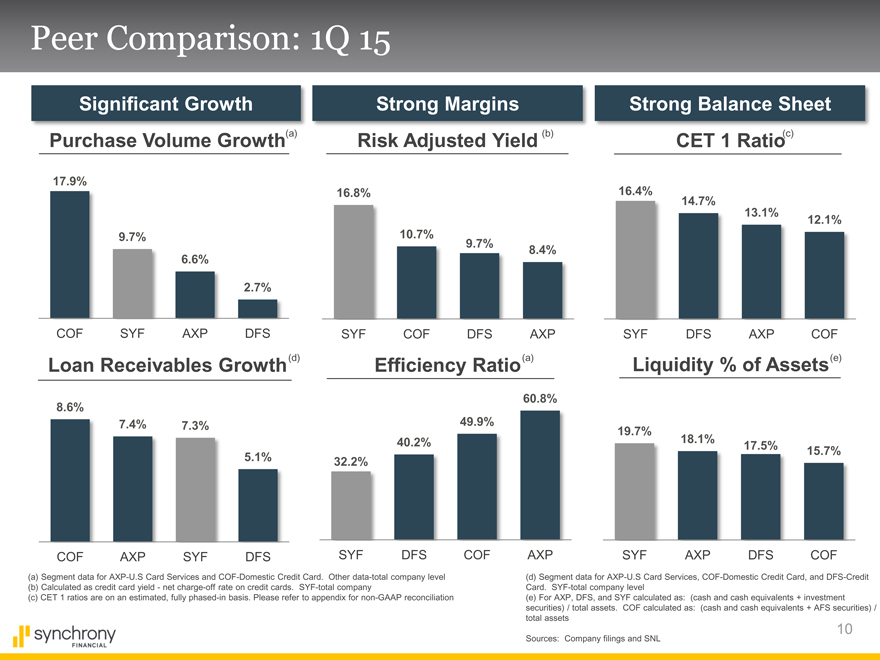

Peer Comparison: 1Q 15

Significant Growth Purchase Volume Growth (a)

Strong Margins Risk Adjusted Yield (b)

Strong Balance Sheet CET 1 Ratio(c)

17.9%

9.7%

6.6%

2.7%

COF SYF AXP DFS

16.8%

10.7%

9.7%

8.4%

SYF COF DFS AXP

(a)

16.4%

14.7%

13.1%

12.1%

SYF DFS AXP COF

Loan Receivables Growth (d) Efficiency Ratio (a) Liquidity % of Assets (e)

8.6%

7.4% 7.3%

5.1%

COF AXP SYF DFS

60.8% 49.9% 40.2% 32.2%

SYF DFS COF AXP

19.7%

18.1%

17.5% 15.7%

SYF AXP DFS COF

(a) Segment data for AXP-U.S Card Services and COF-Domestic Credit Card. Other data-total company level (b) Calculated as credit card yield—net charge-off rate on credit cards. SYF-total company (c) CET 1 ratios are on an estimated, fully phased-in basis. Please refer to appendix for non-GAAP reconciliation

(d) Segment data for AXP-U.S Card Services, COF-Domestic Credit Card, and DFS-Credit Card. SYF-total company level (e) For AXP, DFS, and SYF calculated as: (cash and cash equivalents + investment securities) / total assets. COF calculated as: (cash and cash equivalents + AFS securities) / total assets

Sources: Company filings and SNL

10

|

|

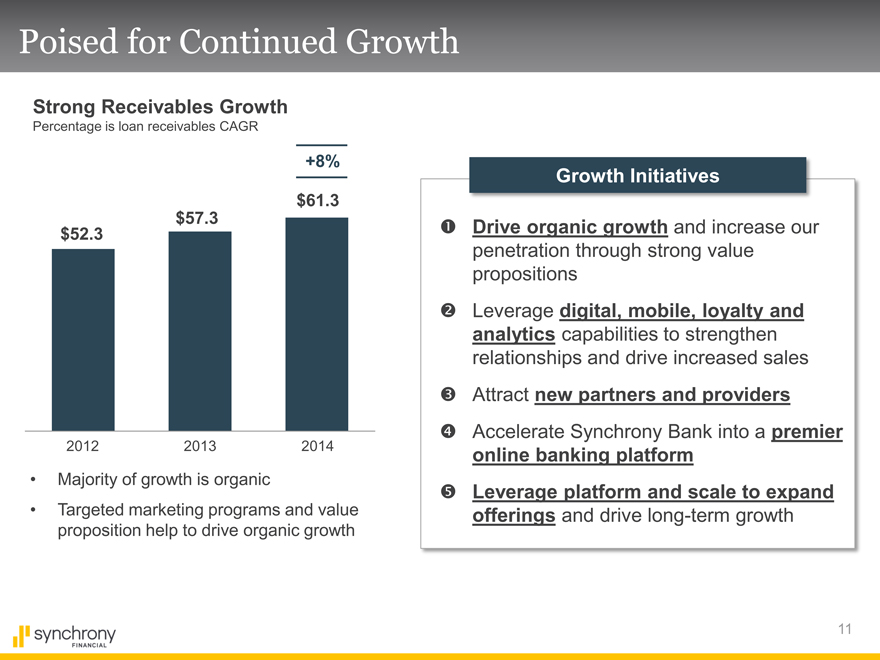

Poised for Continued Growth

Strong Receivables Growth

Percentage is loan receivables CAGR

+8%

$61.3

$57.3

$52.3

2012 2013 2014

Majority of growth is organic

Targeted marketing programs and value proposition help to drive organic growth

Growth Initiatives

? Drive organic growth and increase our penetration through strong value propositions

? Leverage digital, mobile, loyalty and analytics capabilities to strengthen relationships and drive increased sales

? Attract new partners and providers

? Accelerate Synchrony Bank into a premier online banking platform ? Leverage platform and scale to expand offerings and drive long-term growth

11

|

|

Summary

Premier consumer finance company well-positioned to capitalize on deep partner integration

Differentiated business model with solid value proposition for both partners and consumers

Attractive growth opportunities, particularly to further leverage data analytics, loyalty, mobile and e-capabilities

Growth supported by online bank with strong deposit growth

Solid fundamentals with strong returns

12

|

|

Engage with us.

|

|

Appendix: Non-GAA

In order to assess and internally report the revenue performance of our three sales platforms, we use measures we refer to as “platform revenue” and “platform revenue excluding retailer share arrangements.” Platform revenue is the sum of three line items in our Condensed Consolidated and Combined Statements of Earnings prepared in accordance with GAAP: “interest and fees on loans,” plus “other income,” less “retailer share arrangements.” Platform revenue and platform revenue excluding retailer share arrangements are not measures presented in accordance with GAAP. To calculate platform revenue we deduct retailer share arrangements but do not deduct other line item expenses, such as interest expense, provision for loan losses and other expense, because those items are managed for the business as a whole. We believe that platform revenue is a useful measure to investors because it represents management’s view of the net revenue contribution of each of our platforms. Platform revenue excluding retailer share arrangements represents management’s view of the gross revenue contribution of each of our platforms. These measures should not be considered a substitute for interest and fees on loans or other measures of performance we have reported in accordance with GAAP.

We present certain capital ratios. As a new savings and loan holding company, we historically have not been required by regulators to disclose capital ratios, and therefore these capital ratios are non-GAAP measures. We believe these capital ratios are useful measures to investors because they are widely used by analysts and regulators to assess the capital position of financial services companies, although our Basel I Tier 1 common ratio is not a Basel I defined regulatory capital ratio, and our Basel I and Basel III Tier 1 common ratios may not be comparable to similarly titled measures reported by other companies. Our Basel I Tier 1 common ratio is the ratio of Tier 1 common equity (as calculated below) to total risk-weighted assets as calculated in accordance with the U.S. Basel I capital rules. Our Basel III Tier 1 common ratio is the ratio of common equity Tier 1 capital to total risk-weighted assets, each as calculated in accordance with the U.S. Basel III capital rules (on a fully phased-in basis). Our Basel III Tier 1 common ratio is a preliminary estimate reflecting management’s interpretation of the final Basel III capital rules adopted in July 2013 by the Federal Reserve Board, which have not been fully implemented, and our estimate and interpretations are subject to, among other things, ongoing regulatory review and implementation guidance.

|

|

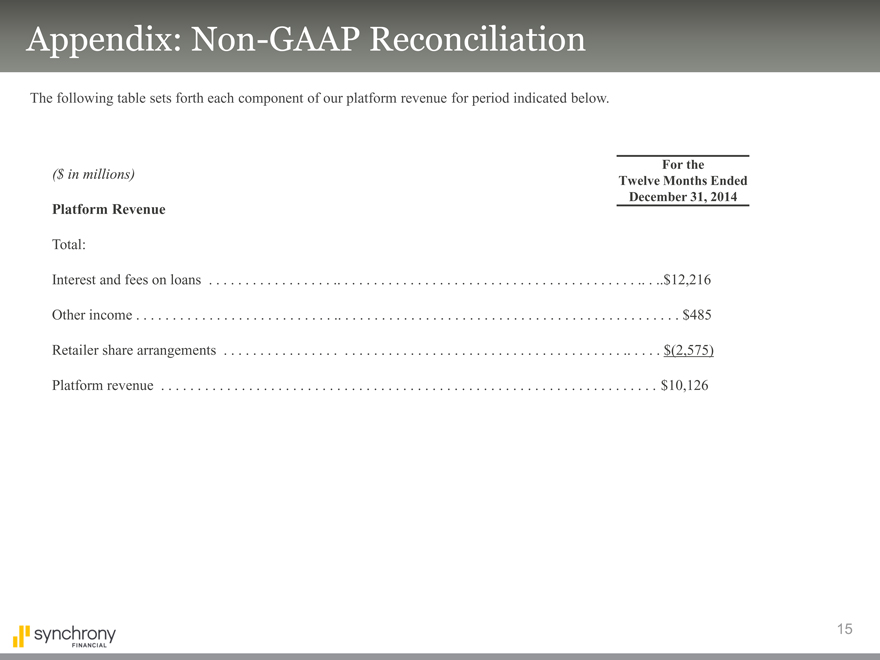

Appendix: Non-GAAP Reconciliation

The following table sets forth each component of our platform revenue for period indicated below.

($ in millions)

Platform Revenue

Total:

Interest and fees on $12,216

Other income $485

Retailer share arrangements $(2,575)

Platform revenue $10,126

For the

Twelve Months Ended

December 31, 2014

|

|

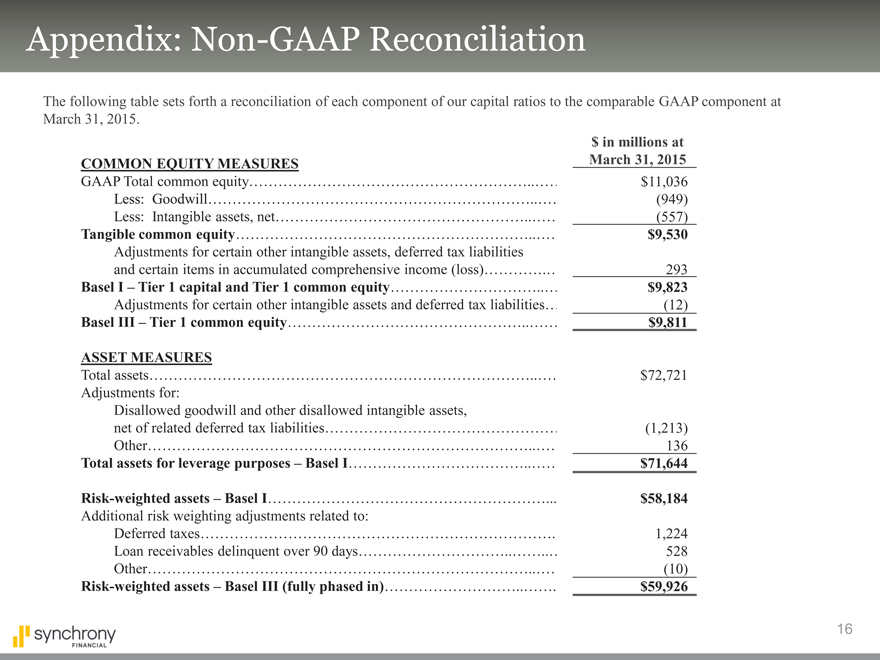

$ in millions at

COMMON EQUITY MEASURES March 31, 2015

GAAP Total common equity$11,036

Less: Goodwill (949)

Less: Intangible assets, net (557)

Tangible common equity $9,530

Adjustments for certain other intangible assets, deferred tax liabilities

and certain items in accumulated comprehensive income (loss) 293

Basel I – Tier 1 capital and Tier 1 common equity $9,823

Adjustments for certain other intangible assets and deferred tax liabilities (12)

Basel III – Tier 1 common equity $9,811

ASSET MEASURES

Total assets $72,721

Adjustments for:

Disallowed goodwill and other disallowed intangible assets,

net of related deferred tax liabilities(1,213)

Other 136

Total assets for leverage purposes – Basel I $71,644

Risk-weighted assets – Basel I $58,184

Additional risk weighting adjustments related to:

Deferred taxes 1,224

Loan receivables delinquent over 90 days 528

Other (10)

Risk-weighted assets – Basel III (fully phased in) $59,926

The following table sets forth a reconciliation of each component of our capital ratios to the comparable GAAP component at March 31, 2015.

Appendix: Non-GAAP Reconciliation