Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SPECTRUM MANAGEMENT HOLDING COMPANY, LLC | eh1500700_8k.htm |

| EX-99 - EXHIBIT 99.1 - SPECTRUM MANAGEMENT HOLDING COMPANY, LLC | eh1500700_ex9901.htm |

EXHIBIT 99.2

Charter to Merge with Time Warner Cable and Acquire Bright House Networks Combinations Benefit Shareholders, Consumers and Cable Industry May 26, 2015

2 Cautionary Statement Regarding Forward - Looking Statements Certain statements in this communication regarding the proposed transaction between Charter and Time Warner Cable and the proposed transaction between Bright House and Charter, including any statements regarding the expected timetable for completing the transaction, benefits and synergies of the transaction, future opportunities for the respective companies and products, and any other statements regarding Charter’s, Time Warner Cable’s and Bright House’s future expectations, beliefs, plans, objectives, financial conditions, assumptions or future events or performance that are not historical facts are “forward - looking” statements made within the meaning of Section 27 A of the Securities Act of 1933 , as amended, and Section 21 E of the Securities Exchange Act of 1934 , as amended . These statements are often, but not always, made through the use of words or phrases such as “believe,” “expect,” “anticipate,” “should,” “planned,” “will,” “may,” “intend,” “estimated,” “aim,” “on track,” “target,” “opportunity,” “tentative,” “positioning,” “designed,” “create,” “predict,” “project,” “seek,” “would,” “could,” “potential,” “continue,” “ongoing,” “upside,” “increases,” and “potential” and similar expressions . All such forward - looking statements involve estimates and assumptions that are subject to risks, uncertainties and other factors that could cause actual results to differ materially from the results expressed in the statements . Among the key factors that could cause actual results to differ materially from those projected in the forward - looking statements are the following : the timing to consummate the proposed transactions ; the risk that a condition to closing the proposed transactions may not be satisfied ; the risk that a regulatory approval that may be required for the proposed transactions is not obtained or is obtained subject to conditions that are not anticipated ; Charter’s ability to achieve the synergies and value creation contemplated by the proposed transactions ; Charter’s ability to promptly, efficiently and effectively integrate acquired operations into its own operations ; and the diversion of management time on transaction - related issues . Additional information concerning these and other factors can be found in Charter’s and Time Warner Cable’s respective filings with the SEC, including Charter’s and Time Warner Cable’s most recent Annual Reports on Form 10 - K, Quarterly Reports on Form 10 - Q and Current Reports on Form 8 - K . Charter and Time Warner Cable assume no obligation to update any forward - looking statements . Readers are cautioned not to place undue reliance on these forward - looking statements that speak only as of the date hereof .

3 Important Information for Investors and Shareholders This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitati on of any vote or approval. In connection with the transactions referred to in this material, Charter Communications, Inc. (“Charter”), expects to file a re gis tration statement on Form S - 4 with the Securities and Exchange Commission (“SEC”) containing a preliminary joint proxy statement of Charter and Time Warn er Cable, Inc. (“Time Warner Cable”) that also constitutes a preliminary prospectus of Charter. After the registration statement is declared effect ive , Charter and Time Warner Cable will mail a definitive proxy statement/prospectus to stockholders of Charter and stockholders of Time Warner Cable. Th is material is not a substitute for the joint proxy statement/prospectus or registration statement or for any other document that Charter or Time War ner Cable may file with the SEC and send to Charter’s and/or Time Warner Cable’s stockholders in connection with the proposed transactions. INVESTOR S A ND SECURITY HOLDERS OF CHARTER AND TIME WARNER CABLE ARE URGED TO READ THE PROXY STATEMENT/PROSPECTUS AND OTHER DOCUMENTS FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Investors and security holders will be able to obtain free copies of the proxy statement/prosp ect us (when available) and other documents filed with the SEC by Charter or Time Warner Cable through the website maintained by the SEC a t h ttp://www.sec.gov. Copies of the documents filed with the SEC by Charter will be available free of charge on Charter’s website at charter.com, i n t he “Investor and News Center” near the bottom of the page, or by contacting Charter’s Investor Relations Department at 203 - 905 - 7955. Copies of the doc uments filed with the SEC by Time Warner Cable will be available free of charge on Time Warner Cable’s website at http://ir.timewarnercable.com or by contacting Time Warner Cable’s Investor Relations Department at 877 - 446 - 3689. Charter and Time Warner Cable and their respective directors and certain of their respective executive officers may be consid ere d participants in the solicitation of proxies with respect to the proposed transactions under the rules of the SEC. Information about the directors an d executive officers of Charter is set forth in its Annual Report on Form 10 - K for the year ended December 31, 2014, which was filed with the SEC on Feb ruary 24, 2015, and its proxy statement for its 2015 annual meeting of stockholders, which was filed with the SEC on March 18, 2015. Information abo ut the directors and executive officers of Time Warner Cable is set forth in its Annual Report on Form 10 - K for the year ended December 31, 2014, whi ch was filed with the SEC on February 13, 2015, as amended April 27, 2015, and its proxy statement for its 2015 annual meeting of stockholders, whi ch was filed with the SEC on May 18, 2015. These documents can be obtained free of charge from the sources indicated above. Additional information reg arding the participants in the proxy solicitations and a description of their direct and indirect interests, by security holdings or oth erw ise, will also be included in any proxy statement and other relevant materials to be filed with the SEC when they become available. New Charter In connection with the closing of the transaction with Time Warner Cable, Charter will undergo a tax - free reorganization that wi ll result in a current subsidiary of Charter, CCH I, LLC ("New Charter") becoming the new holding company owning 100% of Charter. The terms Charter and New Charter are used interchangeably throughout this presentation.

Thomas M. Rutledge President and CEO, Charter Communications

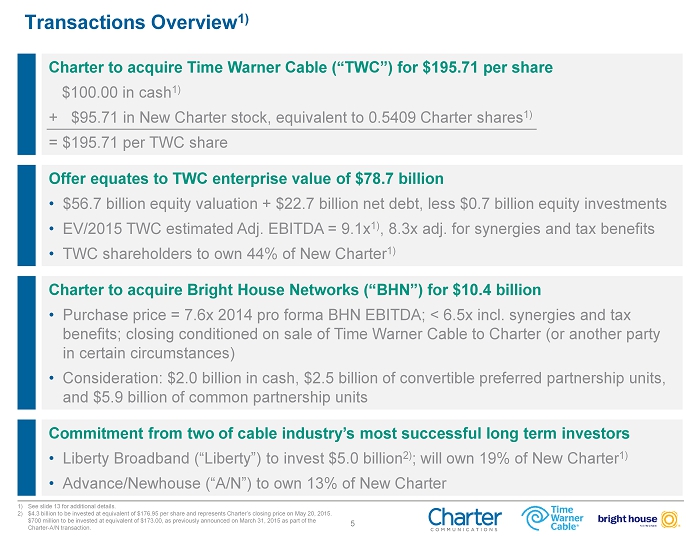

5 Transactions Overview 1) 1) See slide 13 for additional details. 2) $4.3 billion to be invested at equivalent of $176.95 per share and represents Charter’s closing price on May 20, 2015. $700 million to be invested at equivalent of $173.00, as previously announced on March 31, 2015 as part of the Charter - A/N transaction. Charter to acquire Time Warner Cable (“TWC”) for $195.71 per share $100.00 in cash 1) + $95.71 in New Charter stock, equivalent to 0.5409 Charter shares 1) = $195.71 per TWC share Offer equates to TWC enterprise value of $78.7 billion • $56.7 billion equity valuation + $22.7 billion net debt, less $0.7 billion equity investments • EV/2015 TWC estimated Adj. EBITDA = 9.1x 1) , 8.3x adj. for synergies and tax benefits • TWC shareholders to own 44% of New Charter 1) Charter to acquire Bright House Networks (“BHN”) for $10.4 billion • Purchase price = 7.6x 2014 pro forma BHN EBITDA; < 6.5x incl. synergies and tax benefits ; closing conditioned on sale of Time Warner Cable to Charter (or another party in certain circumstances) • Consideration: $2.0 billion in cash, $2.5 billion of convertible preferred partnership units, and $5.9 billion of common partnership units Commitment from two of cable industry’s most successful long term investors • Liberty Broadband (“Liberty”) to invest $5.0 billion 2) ; will own 19% of New Charter 1) • Advance/Newhouse (“A/N”) to own 13% of New Charter

6 0 Accelerate growth by building on TWC momentum and Charter operating strategy • Combine TWC’s recent operating momentum with Charter’s proven track record of investing in, and offering, highly competitive products to drive growth • Continue to remove analog signals in TWC and Bright House networks to free capacity to offer faster Internet products, more HD content and other advanced products Greater scale and enhanced footprint drives competitiveness and innovation • Enhances sales, marketing and branding capabilities vs. national competitors • Scale enables and accelerates product development and innovation • New footprint provides larger opportunity to compete in medium/large commercial market Cost synergies, levered and tax - efficient equity returns • Unlock value through cost synergies inherent in Charter’s operating model, and via combined purchasing and elimination of duplicate costs • Transaction structure designed to provide long - dated and low - cost financing, and enable unified operations which achieves operating cost and tax objectives • Moderate leverage at closing to facilitate transaction and significant tax assets offer attractive equity returns Superior Value Creation For All Shareholders

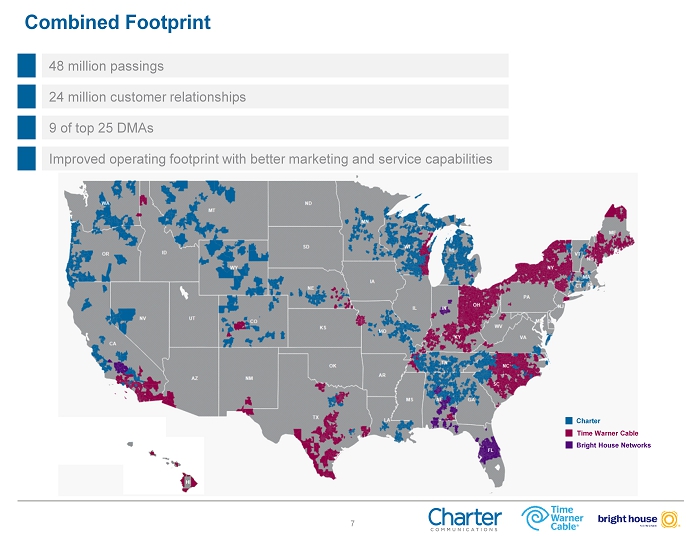

7 Combined Footprint Charter Time Warner Cable Bright House Networks 48 million passings 24 million customer relationships 9 of top 25 DMAs Improved operating footprint with better marketing and service capabilities HI

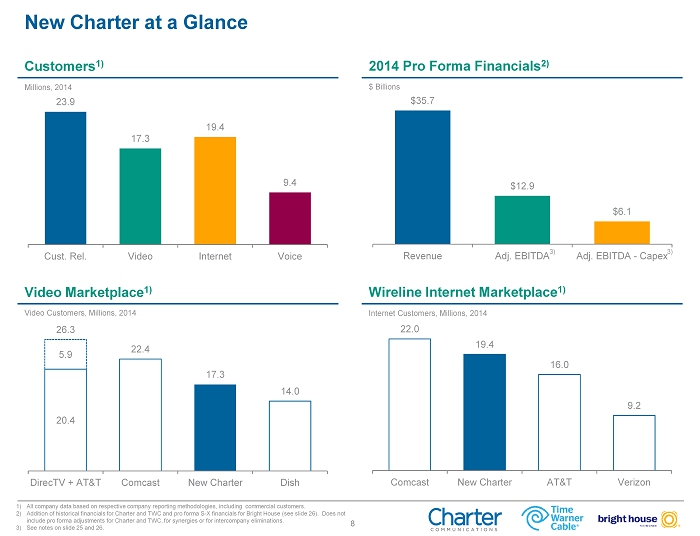

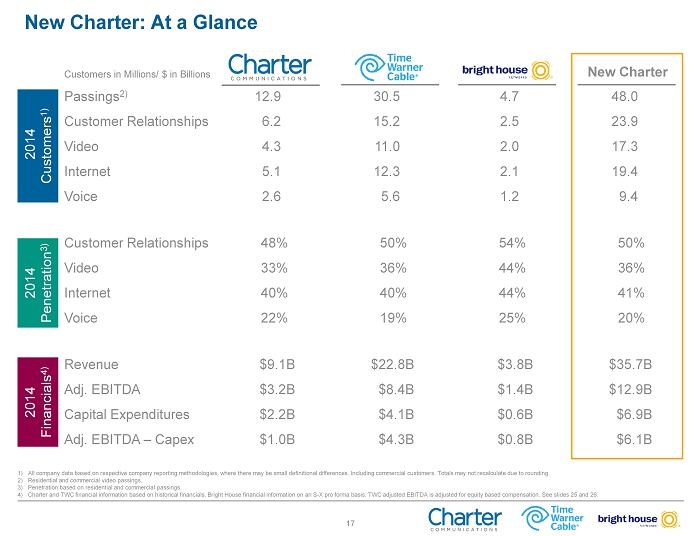

8 New Charter at a Glance Millions, 2014 Video Customers, Millions, 2014 $ Billions Video Marketplace 1) 1) All company data based on respective company reporting methodologies, including commercial customers. 2) Addition of historical financials for Charter and TWC and pro forma S - X financials for Bright House (see slide 26). Does not include pro forma adjustments for Charter and TWC, for synergies or for intercompany eliminations. 3) See notes on slide 25 and 26. Wireline Internet Marketplace 1) Internet Customers, Millions, 2014 Customers 1 ) 2014 Pro Forma Financials 2) 23.9 17.3 19.4 9.4 Cust. Rel. Video Internet Voice $35.7 $12.9 $6.1 Revenue Adj. EBITDA Adj. EBITDA - Capex 3) 3) 20.4 5.9 26.3 22.4 17.3 14.0 DirecTV + AT&T Comcast New Charter Dish 22.0 19.4 16.0 9.2 Comcast New Charter AT&T Verizon

9 A win for consumers and commercial c ustomers • Continued network investments will drive faster broadband speeds, better video products and more competition • Scale will drive greater product innovation, bringing new and advanced services to consumers • Investments in insourcing will drive better customer service, higher customer satisfaction • Medium and large commercial customers will have access to better products, services and enterprise solutions Offers s ignificant benefits to employees and vendors • Charter’s commitment to superior products and customer service, and its strategy of investing in insourcing, drives opportunities for all employees • Drives incentives for vendors to invest in, and develop new technologies, business lines and alternative video programming platforms Combination in Best Interest of All Stakeholders

Robert D. Marcus Chairman and CEO, Time Warner Cable

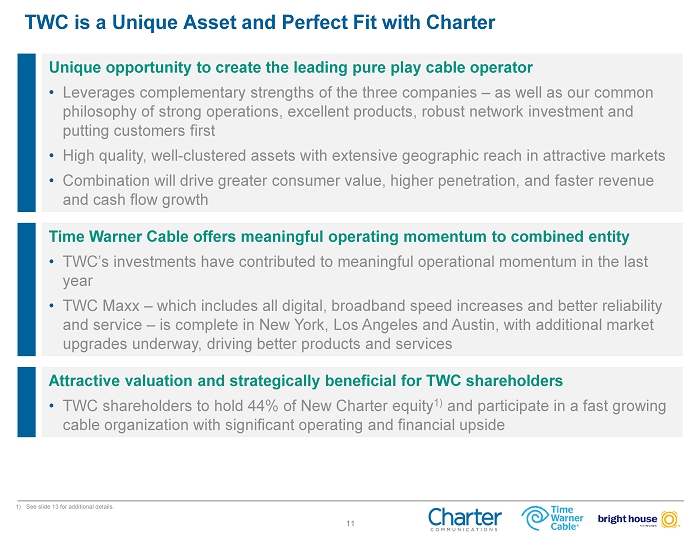

11 TWC is a Unique Asset and Perfect Fit with Charter Unique opportunity to create the leading pure play cable operator • Leverages complementary strengths of the three companies – as well as our common philosophy of strong operations, excellent products, robust network investment and putting customers first • High quality, well - clustered assets with extensive geographic reach in attractive markets • Combination will drive greater consumer value, higher penetration, and faster revenue and cash flow growth Time Warner Cable o ffers meaningful operating momentum to combined entity • TWC’s investments have contributed to meaningful operational momentum in the last year • TWC Maxx – which includes all digital, broadband speed increases and better reliability and service – is complete in New York, Los Angeles and Austin, with additional market upgrades underway, driving better products and services Attractive valuation and strategically beneficial for TWC shareholders • TWC shareholders to hold 44% of New Charter equity 1) and participate in a fast growing cable organization with significant operating and financial upside 1) See slide 13 for additional details.

Christopher L. Winfrey Executive Vice President and CFO, Charter Communications

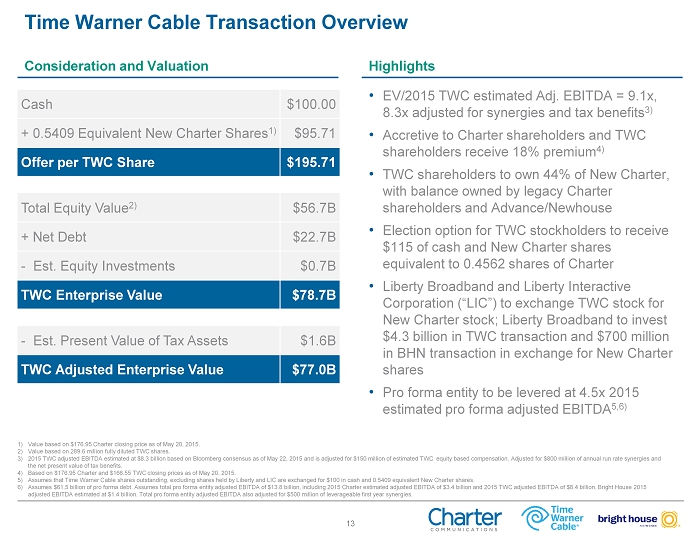

13 Time Warner Cable Transaction Overview Consideration and Valuation Highlights • EV/2015 TWC estimated Adj. EBITDA = 9.1x , 8.3x adjusted for synergies and tax benefits 3) • Accretive to Charter shareholders and TWC shareholders receive 18% premium 4) • TWC shareholders to own 44% of New Charter, with balance owned by legacy Charter shareholders and Advance/Newhouse • Election option for TWC stockholders to receive $115 of cash and New Charter shares equivalent to 0.4562 shares of Charter • Liberty Broadband and Liberty Interactive Corporation (“LIC”) to exchange TWC stock for New Charter stock; Liberty Broadband to invest $4.3 billion in TWC transaction and $700 million in BHN transaction in exchange for New Charter shares • Pro forma entity to be levered at 4.5x 2015 estimated pro forma adjusted EBITDA 5,6 ) Cash $100.00 + 0.5409 Equivalent New Charter Shares 1) $95.71 Offer per TWC Share $195.71 Total Equity Value 2) $56.7B + Net Debt $22.7B - Est. Equity Investments $0.7B TWC Enterprise Value $78.7B - Est. Present Value of Tax Assets $1.6B TWC Adjusted Enterprise Value $77.0B 1) Value based on $176.95 Charter closing price as of May 20, 2015. 2) Value based on 289.6 million fully diluted TWC shares. 3) 2015 TWC adjusted EBITDA estimated at $8.3 billion based on Bloomberg consensus as of May 22, 2015 and is adjusted for $150 m ill ion of estimated TWC equity based compensation. Adjusted for $800 million of annual run rate synergies and the net present value of tax benefits. 4) Based on $176.95 Charter and $166.55 TWC closing prices as of May 20, 2015. 5) Assumes that Time Warner Cable shares outstanding, excluding shares held by Liberty and LIC are exchanged for $100 in cash an d 0 .5409 equivalent New Charter shares. 6) Assumes $61.5 billion of pro forma debt. Assumes total pro forma entity adjusted EBITDA of $13.8 billion, including 2015 Char ter estimated adjusted EBITDA of $3.4 billion and 2015 TWC adjusted EBITDA of $8.4 billion. Bright House 2015 adjusted EBITDA estimated at $1.4 billion. Total pro forma entity adjusted EBITDA also adjusted for $500 million of leveragea ble first year synergies.

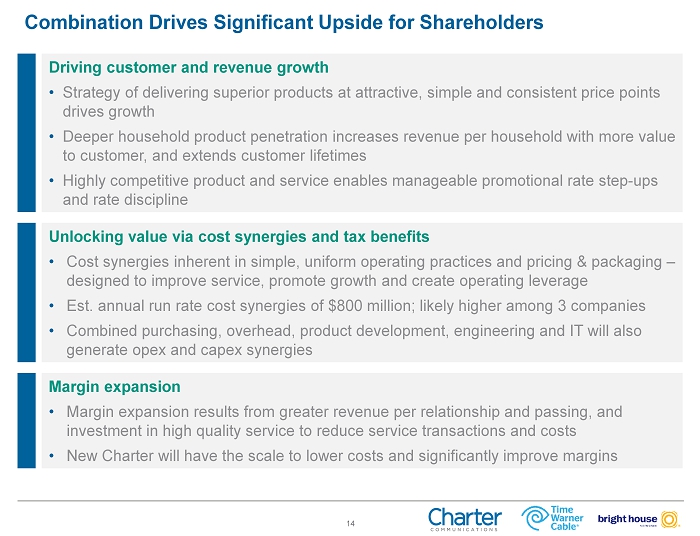

14 0 Driving customer and revenue growth • Strategy of delivering superior products at attractive, simple and consistent price points drives growth • Deeper household product penetration increases revenue per household with more value to customer, and extends customer lifetimes • Highly competitive product and service enables manageable promotional rate step - ups and rate discipline Unlocking value via cost synergies and tax benefits • Cost synergies inherent in simple, uniform operating practices and pricing & packaging – designed to improve service, promote growth and create operating leverage • Est. annual run rate cost synergies of $800 million; likely higher among 3 companies • Combined purchasing, overhead, product development, engineering and IT will also generate opex and capex synergies Margin expansion • Margin expansion results from greater revenue per relationship and passing, and investment in high quality service to reduce service transactions and costs • New Charter will have the scale to lower costs and significantly improve margins Combination Drives Significant Upside for Shareholders

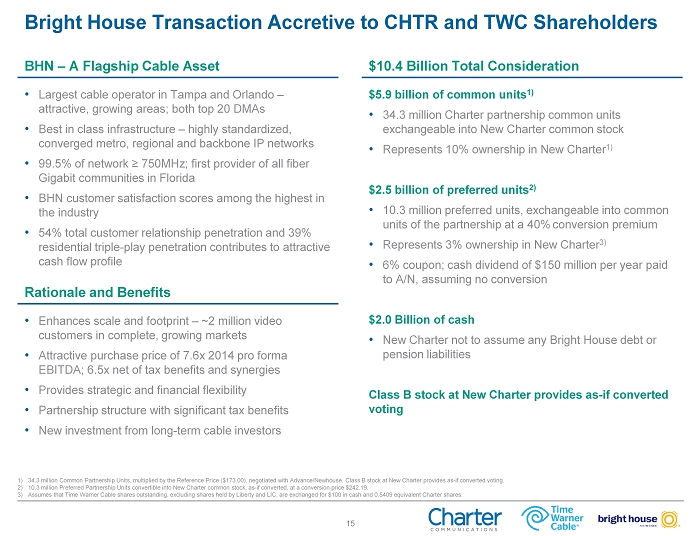

15 Bright House Transaction Accretive to CHTR and TWC Shareholders BHN – A Flagship Cable Asset $10.4 Billion Total Consideration Rationale and Benefits $5.9 billion of common units 1) • 34.3 m illion Charter partnership common units exchangeable into New Charter common stock • Represents 10% ownership in New Charter 1 ) $2.5 billion of preferred units 2) • 10.3 million preferred units, exchangeable into common units of the partnership at a 40% conversion premium • Represents 3 % ownership in New Charter 3 ) • 6% coupon; cash dividend of $150 million per year paid to A/N, assuming no conversion $ 2.0 Billion of cash • New Charter not to assume any Bright House debt or pension liabilities Class B stock at New Charter provides as - if converted voting • Largest cable operator in Tampa and Orlando – attractive, growing areas; both top 20 DMAs • Best in class infrastructure – h ighly standardized, c onverged metro, regional and backbone IP networks • 99.5% of network ≥ 750MHz; first provider of all fiber Gigabit communities in Florida • BHN customer satisfaction scores among the highest in the industry • 54% total customer relationship penetration and 39% residential triple - play penetration contributes to attractive cash flow profile • Enhances scale and footprint – ~2 million video customers in complete, growing markets • Attractive purchase price of 7.6x 2014 pro forma EBITDA; 6.5x net of tax benefits and synergies • Provides strategic and financial flexibility • Partnership structure with significant tax benefits • New investment from long - term cable investors 1) 34.3 million Common Partnership Units, multiplied by the Reference Price ($173.00), negotiated with Advance/Newhouse. Class B st ock at New Charter provides as - if converted voting. 2) 10.3 million Preferred Partnership Units convertible into New Charter common stock, as - if converted, at a conversion price $242. 19. 3) Assumes that Time Warner Cable shares outstanding, excluding shares held by Liberty and LIC, are exchanged for $100 in cash a nd 0.5409 equivalent Charter shares.

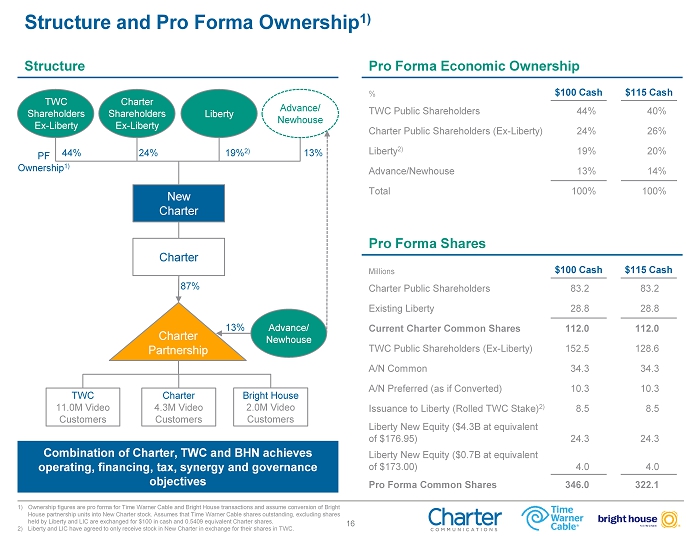

16 Structure and P ro Forma Ownership 1) Structure Pro Forma Economic Ownership Pro Forma Shares Millions $100 Cash $115 Cash Charter Public Shareholders 83.2 83.2 Existing Liberty 28.8 28.8 Current Charter Common Shares 112.0 112.0 TWC Public Shareholders (Ex - Liberty) 152.5 128.6 A/N Common 34.3 34.3 A/N Preferred (as if Converted) 10.3 10.3 Issuance to Liberty (Rolled TWC Stake) 2) 8.5 8.5 Liberty New Equity ($4.3B at equivalent of $176.95) 24.3 24.3 Liberty New Equity ($0.7B at equivalent of $173.00) 4.0 4.0 Pro Forma Common Shares 346.0 322.1 Combination of Charter, TWC and BHN achieves operating, financing, tax, synergy and governance objectives % $100 Cash $115 Cash TWC Public Shareholders 44% 40% Charter Public Shareholders (Ex - Liberty) 24% 26% Liberty 2) 19% 20% Advance/Newhouse 13% 14% Total 100% 100% Charter Charter Partnership Advance/ Newhouse TWC 11.0M Video Customers Bright House 2.0M Video Customers 87% 1 3% New Charter Advance/ Newhouse 44% Liberty Charter 4.3M Video Customers PF Ownership 1) 24% 19% 2) 13% 1) Ownership figures are pro forma for Time Warner Cable and Bright House transactions and assume conversion of Bright House partnership units into New Charter stock. Assumes that Time Warner Cable shares outstanding, excluding shares held by Liberty and LIC are exchanged for $100 in cash and 0.5409 equivalent Charter shares. 2) Liberty and LIC have agreed to only receive stock in New Charter in exchange for their shares in TWC. TWC Shareholders Ex - Liberty Charter Shareholders Ex - Liberty

17 New Charter: At a Glance Customers in Millions / $ in Billions New Charter Passings 2) 12.9 30.5 4.7 48.0 Customer Relationships 6.2 15.2 2.5 23.9 Video 4.3 11.0 2.0 17.3 Internet 5.1 12.3 2.1 19.4 Voice 2.6 5.6 1.2 9.4 Customer Relationships 48% 50% 54% 50% Video 33% 36% 44% 36% Internet 40% 40% 44% 41% Voice 22% 19% 25% 20% Revenue $9.1B $22.8B $3.8B $35.7B Adj. EBITDA $3.2B $8.4B $1.4B $12.9B Capital Expenditures $2.2B $4.1B $0.6B $6.9B Adj. EBITDA – Capex $1.0B $4.3B $0.8B $6.1B 2014 Customers 1) 2014 Financials 4) 1) All company data based on respective company reporting methodologies, where there may be small definitional differences. Incl udi ng commercial customers. Totals may not recalculate due to rounding. 2) Residential and commercial video passings. 3) Penetration based on residential and commercial passings. 4) Charter and TWC financial information based on historical financials. Bright House financial information on an S - X pro forma bas is. TWC adjusted EBITDA is adjusted for equity based compensation. See slides 25 and 26. 2014 Penetration 3)

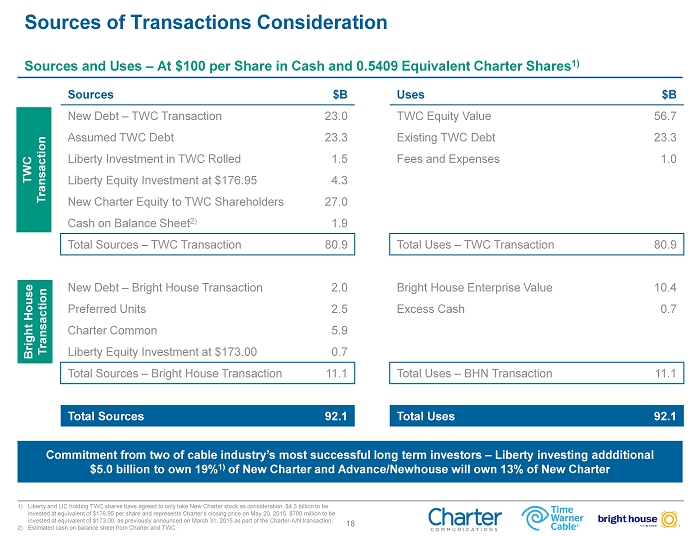

18 Sources of Transactions Consideration Sources and Uses – At $100 per Share in Cash and 0.5409 Equivalent Charter Shares 1) Sources $B Uses $B New Debt – TWC Transaction 23.0 TWC Equity Value 56.7 Assumed TWC Debt 23.3 Existing TWC Debt 23.3 Liberty Investment in TWC Rolled 1.5 Fees and Expenses 1.0 Liberty Equity Investment at $176.95 4.3 New Charter Equity to TWC Shareholders 27.0 Cash on Balance Sheet 2) 1.9 Total Sources – TWC Transaction 80.9 Total Uses – TWC Transaction 80.9 New Debt – Bright House Transaction 2.0 Bright House Enterprise Value 10.4 Preferred Units 2.5 Excess Cash 0.7 Charter Common 5.9 Liberty Equity Investment at $173.00 0.7 Total Sources – Bright House Transaction 11.1 Total Uses – BHN Transaction 11.1 Total Sources 92.1 Total Uses 92.1 TWC Transaction Bright House Transaction Commitment from two of cable industry’s most successful long term investors – Liberty investing addditional $5.0 billion to own 19% 1) of New Charter and Advance/Newhouse will own 13% of New Charter 1) Liberty and LIC holding TWC shares have agreed to only take New Charter stock as consideration. $4.3 billion to be invested at equivalent of $176.95 per share and represents Charter’s closing price on May 20, 2015. $700 million to be invested at equivalent of $173.00, as previously announced on March 31, 2015 as part of the Charter - A/N transaction. 2) Estimated cash on balance sheet from Charter and TWC.

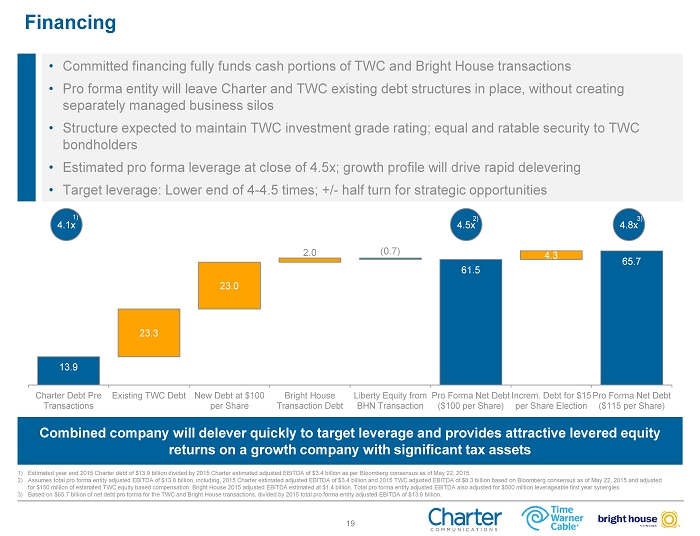

19 4.8x 4.5x 4.1x Financing Combined company will delever quickly to target leverage and provides attractive levered equity returns on a growth company with significant tax assets 1) Estimated year end 2015 Charter debt of $13.9 billion divided by 2015 Charter estimated adjusted EBITDA of $3.4 billion as pe r B loomberg consensus as of May 22, 2015. 2) Assumes total pro forma entity adjusted EBITDA of $13.8 billion, including, 2015 Charter estimated adjusted EBITDA of $3.4 bi lli on and 2015 TWC adjusted EBITDA of $8.3 billion based on Bloomberg consensus as of May 22, 2015 and adjusted for $150 million of estimated TWC equity based compensation. Bright House 2015 adjusted EBITDA estimated at $1.4 billion. Tot al pro forma entity adjusted EBITDA also adjusted for $500 million leverageable first year synergies. 3) Based on $65.7 billion of net debt pro forma for the TWC and Bright House transactions, divided by 2015 total pro forma entit y a djusted EBITDA of $13.8 billion. • Committed financing fully funds cash portions of TWC and Bright House transactions • Pro forma entity will leave Charter and TWC existing debt structures in place, without creating separately managed business silos • Structure expected to maintain TWC investment grade rating; equal and ratable security to TWC bondholders • Estimated pro forma leverage at close of 4.5x; growth profile will drive rapid delevering • Target leverage: Lower end of 4 - 4.5 times; +/ - half turn for strategic opportunities 2) 1) 3) 13.9 61.5 65.7 23.3 23.0 2.0 4.3 (0.7) Charter Debt Pre Transactions Existing TWC Debt New Debt at $100 per Share Bright House Transaction Debt Liberty Equity from BHN Transaction Pro Forma Net Debt ($100 per Share) Increm. Debt for $15 per Share Election Pro Forma Net Debt ($115 per Share)

20 Tax Assets are Preserved and Enhanced Benefit from enhanced NOL usage • Current NPV of $3 billion of existing Charter NOLs enhanced by over $400 million, as they will be applied to larger base of operating income • Outsized tax basis of $9.1 billion as of 12/31/14 remain intact; likely section 382 ownership change, not expected to impact value of NOLs on an NPV basis • Value of existing NOLs benefit Charter/TWC shareholders only, until A/N’s conversion of partnership units into New Charter stock Tax receivables agreement with Advance/Newhouse drives additional value • New Charter will receive additional tax basis step - up upon any future A/N’s conversion of partnership units into New Charter stock • New Charter retains 50% of the cash tax savings value associated with the tax basis step - up received if and when A/N exchanges partnership units for shares in New Charter • A/N compensated on 50% of the net cash tax savings value associated with the tax basis step - up received by Charter, on a with and without FIFO basis, when the step - up benefits are used by Charter

21 0 Board representation and structure • 13 directors at closing • A/N designates 2 directors and Liberty designates 3 directors Proxy and voting • For 5 years after closing, A/N to grant Liberty a proxy, capped at 7%, giving Liberty total voting power of up to 25.01%; proxy excludes votes on certain matters • A/N voting cap of 23.5%, increased 1:1, to max 35%, to the extent Liberty ownership falls permanently below 15% • Liberty voting cap greater of: • 25.01% and 0.01% above highest voting % of any other person and • 23.5%, increased 1:1, to max 33.5%, if A/N ownership is permanently below 15% Preemptive rights • A/N and Liberty receive preemptive rights to maintain certain ownership thresholds • Liberty ownership capped at the greater of 26% and its voting cap. A/N capped at the greater of its ownership percentage at closing, 25% and its voting cap • Liberty and A/N required to participate in any share repurchase so as not to exceed their respective ownership caps, and transfer rights are generally restricted Governance Structure

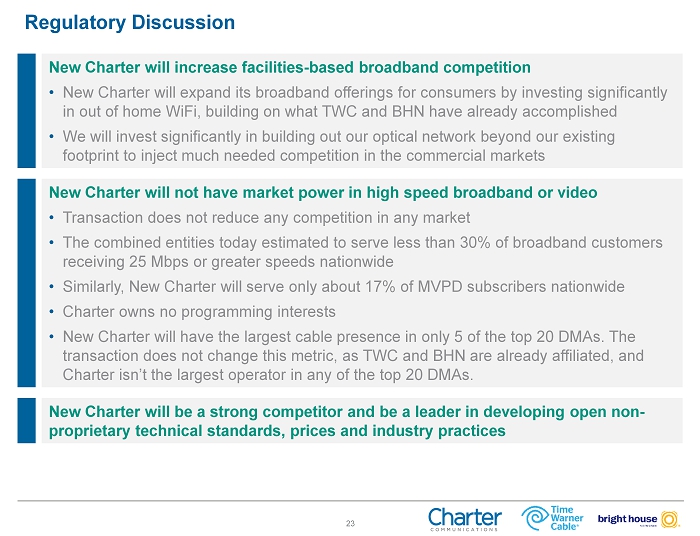

22 Consumers will benefit from a broadband service that makes watching online video, gaming, etc. a great experience – including at peak times – for a great value • Charter’s slowest speed tier (60 Mbps downstream) is considerably faster and less expensive than TWC’s comparable tiers, with no data caps or usage based pricing • Charter will bring these products and pricing to TWC and BHN customers, while embracing TWC’s and BHN’s rollouts of a 300 Mbps tier • Charter will continue to invest in interconnection to minimize likelihood of congestion • Regardless of Title II litigation, we have no plans to block, throttle or engage in paid prioritization because our customers demand an open Internet We will deliver superior customer care, adding U.S. jobs • Charter has added 7,000 new jobs since 2012, most of which have been in customer service fields • New Charter will bring TWC’s customer care jobs back from overseas, too, training new employees to provide superior service while adding jobs to the U.S. economy • New Charter will build on BHN’s reputation for quality customer service Regulatory Discussion

23 0 New Charter will increase facilities - based broadband competition • New Charter will expand its broadband offerings for consumers by investing significantly in out of home WiFi , building on what TWC and BHN have already accomplished • We will invest significantly in building out our optical network beyond our existing footprint to inject much needed competition in the commercial markets New Charter will not have market power in high speed broadband or video • Transaction does not reduce any competition in any market • The combined entities today estimated to serve less than 30% of broadband customers receiving 25 Mbps or greater speeds nationwide • Similarly, New Charter will serve only about 17% of MVPD subscribers nationwide • Charter owns no programming interests • New Charter will have the largest cable presence in only 5 of the top 20 DMAs. The transaction does not change this metric, as TWC and BHN are already affiliated, and Charter isn’t the largest operator in any of the top 20 DMAs. New Charter will be a strong competitor and be a leader in developing open non - proprietary technical standards, prices and industry practices Regulatory Discussion

Appendix

25 Use of Non - GAAP Financial Metrics 3) 1) The Company uses certain measures that are not defined by Generally Accepted Accounting Principles (“GAAP”) to evaluate vario us aspects of its business. Adjusted EBITDA, pro forma adjusted EBITDA, adjusted EBITDA less capital expenditures, and free cash flow are non - GAAP financial measures and should be considered in addition to, not as a substitute for, net income (loss) or cash flows from operating act ivi ties reported in accordance with GAAP. These terms, as defined by Charter, may not be comparable to similarly titled measures used by other co mpa nies. Adjusted EBITDA is reconciled to net income (loss) and free cash flow is reconciled to net cash flows from operating activities in the ap pendix of this presentation. Adjusted EBITDA is defined as net income (loss) plus net interest expense, income taxes, depreciation and amortization, stock co mpensation expense, loss on extinguishment of debt, (gain) loss on derivative instruments, net and other operating expenses, such as merger and a cqu isition costs, special charges and (gain) loss on sale or retirement of assets. As such, it eliminates the significant non - cash depreciation and amort ization expense that results from the capital - intensive nature of the Company's businesses as well as other non - cash or special items, and is unaffec ted by the Company's capital structure or investment activities. However, this measure is limited in that it does not reflect the periodic costs o f c ertain capitalized tangible and intangible assets used in generating revenues and the cash cost of financing. These costs are evaluated through other financi al measures. Free cash flow is defined as net cash flows from operating activities, less purchases of property, plant and equipment and ch ang es in accrued expenses related to capital expenditures. Management and the Company’s Board use adjusted EBITDA and free cash flow to assess Charter's performance and its ability to ser vice its debt, fund operations and make additional investments with internally generated funds. In addition, adjusted EBITDA generally correlates to the leverage ratio calculation under the Company's credit facilities or outstanding notes to determine compliance with the covenants contained i n t he credit facilities and notes (all such documents have been previously filed with the United States Securities and Exchange Commission). For the purp ose of calculating compliance with leverage covenants, we use adjusted EBITDA, as presented, excluding certain expenses paid by our operating su bsi diaries to other Charter entities. Our debt covenants refer to these expenses as management fees which fees were in the amount of $76 million and $64 million for the three months ended March 31, 2015 and 2014, respectively. For a reconciliation of adjusted EBITDA to the most directly comparable GAAP financial measure, see slide 26.

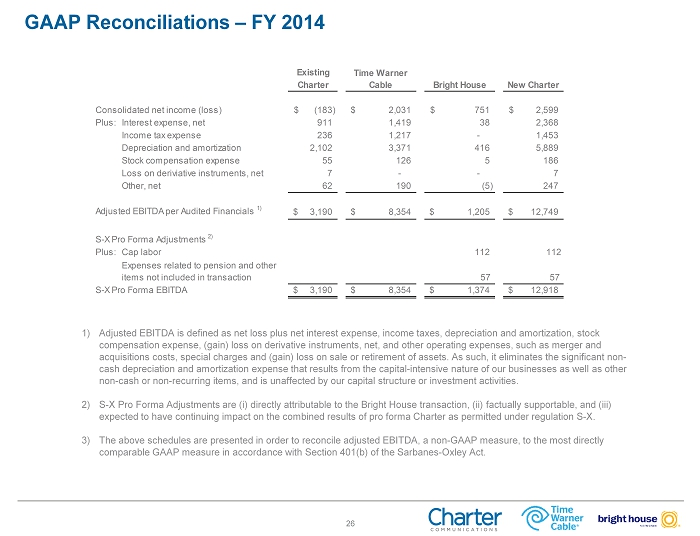

26 3) 1) GAAP Reconciliations – FY 2014 1) Adjusted EBITDA is defined as net loss plus net interest expense, income taxes, depreciation and amortization, stock compensation expense, (gain) loss on derivative instruments, net, and other operating expenses, such as merger and acquisitions costs, special charges and (gain) loss on sale or retirement of assets. As such, it eliminates the significant n on - cash depreciation and amortization expense that results from the capital - intensive nature of our businesses as well as other non - cash or non - recurring items, and is unaffected by our capital structure or investment activities. 2) S - X Pro Forma Adjustments are (i) directly attributable to the Bright House transaction, (ii) factually supportable, and (iii) expected to have continuing impact on the combined results of pro forma Charter as permitted under regulation S - X. 3) The above schedules are presented in order to reconcile adjusted EBITDA, a non - GAAP measure, to the most directly comparable GAAP measure in accordance with Section 401(b) of the Sarbanes - Oxley Act. Existing Charter Bright House New Charter Consolidated net income (loss) (183)$ 2,031$ 751$ 2,599$ Plus: Interest expense, net 911 1,419 38 2,368 Income tax expense 236 1,217 - 1,453 Depreciation and amortization 2,102 3,371 416 5,889 Stock compensation expense 55 126 5 186 Loss on deriviative instruments, net 7 - - 7 Other, net 62 190 (5) 247 Adjusted EBITDA per Audited Financials 1) 3,190$ 8,354$ 1,205$ 12,749$ S-X Pro Forma Adjustments 2) Plus: Cap labor 112 112 S-X Pro Forma EBITDA 3,190$ 8,354$ 1,374$ 12,918$ 57 Time Warner Cable Expenses related to pension and other items not included in transaction 57