Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Benefit Street Partners Realty Trust, Inc. | Financial_Report.xls |

| EX-31.2 - EXHIBIT 31.2 - Benefit Street Partners Realty Trust, Inc. | rft-exhibit312x2015q1.htm |

| EX-31.1 - EXHIBIT 31.1 - Benefit Street Partners Realty Trust, Inc. | rft-exhibit311x2015q1.htm |

| EX-32 - EXHIBIT 32 - Benefit Street Partners Realty Trust, Inc. | rft-exhibit32x2015q1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One) | |

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2015

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 000-55188

REALTY FINANCE TRUST, INC.

(Exact name of registrant as specified in its charter)

Maryland | 46-1406086 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

405 Park Avenue, 14th Floor New York, New York | 10022 | |

(Address of Principal Executive Office) | (Zip Code) | |

(212) 415-6500

(Registrant’s Telephone Number, Including Area Code)

Not applicable

(Former Name, Former Address and Former Fiscal Year, if Changed Since Last Report)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (check one):

Large accelerated filer o | Accelerated filer o |

Non-accelerated filer o | Smaller reporting company x |

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The number of shares of the registrant's common stock, $0.01 par value, outstanding as of April 30, 2015 was 21,214,570.

TABLE OF CONTENTS

Page | |

PART I | |

PART II | |

PART I

Item 1. Condensed Consolidated Financial Statements.

REALTY FINANCE TRUST, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(In thousands, except for share and per share data)

March 31, 2015 | December 31, 2014 | ||||||

ASSETS | (Unaudited) | ||||||

Cash and cash equivalents | $ | 17,155 | $ | 386 | |||

Restricted cash | 68 | 68 | |||||

Commercial mortgage loans, held for investment, net | 559,058 | 456,884 | |||||

Real estate securities, at fair value | 58,375 | 50,234 | |||||

Accrued interest receivable | 2,306 | 2,866 | |||||

Prepaid expenses and other assets | 5,009 | 3,782 | |||||

Total assets | $ | 641,971 | $ | 514,220 | |||

LIABILITIES AND STOCKHOLDERS' EQUITY | |||||||

Repurchase agreements - commercial mortgage loans | $ | 182,307 | $ | 150,169 | |||

Repurchase agreements - real estate securities | 37,734 | 26,269 | |||||

Interest payable | 257 | 232 | |||||

Distributions payable | 3,269 | 2,623 | |||||

Accounts payable and accrued expenses | 2,151 | 2,385 | |||||

Due to affiliate | 3,223 | 2,035 | |||||

Total liabilities | 228,941 | 183,713 | |||||

Preferred stock, $0.01 par value, 50,000,000 authorized, none issued and outstanding as of March 31, 2015 and December 31, 2014 | — | — | |||||

Convertible stock; $0.01 par value, 1,000 shares authorized, issued and outstanding as of March 31, 2015 and December 31, 2014, respectively | 1 | 1 | |||||

Common stock, $0.01 par value, 949,999,000 shares authorized, 19,406,761 and 15,472,192 shares issued and outstanding as of March 31, 2015 and December 31, 2014, respectively | 194 | 155 | |||||

Additional paid-in capital | 427,373 | 340,874 | |||||

Accumulated other comprehensive loss | (166 | ) | (307 | ) | |||

Accumulated deficit | (14,372 | ) | (10,216 | ) | |||

Total stockholders' equity | 413,030 | 330,507 | |||||

Total liabilities and stockholders' equity | $ | 641,971 | $ | 514,220 | |||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

1

REALTY FINANCE TRUST, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(In thousands, except for share and per share data)

(Unaudited)

Three Months Ended March 31, | |||||||

2015 | 2014 | ||||||

Interest Income: | |||||||

Interest income | $ | 9,605 | $ | 977 | |||

Less: Interest expense | 1,933 | 21 | |||||

Net interest income | 7,672 | 956 | |||||

Expenses: | |||||||

Acquisition fees | 1,032 | 259 | |||||

Subordinated performance fee | 362 | — | |||||

Professional fees | 1,379 | 113 | |||||

Other expenses | 123 | 272 | |||||

Loan loss provision | 144 | 86 | |||||

Total expenses | 3,040 | 730 | |||||

Net income | $ | 4,632 | $ | 226 | |||

Basic net income per share | $ | 0.27 | $ | 0.11 | |||

Diluted net income per share | $ | 0.27 | $ | 0.11 | |||

Basic weighted average shares outstanding | 17,279,713 | 2,025,934 | |||||

Diluted weighted average shares outstanding | 17,284,086 | 2,030,023 | |||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

2

REALTY FINANCE TRUST, INC.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(In thousands)

(Unaudited)

Three Months Ended March 31, | |||||||

2015 | 2014 | ||||||

Net income | $ | 4,632 | $ | 226 | |||

Unrealized gain on available-for-sale securities | 141 | 5 | |||||

Comprehensive income attributable to Realty Finance Trust, Inc. | $ | 4,773 | $ | 231 | |||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

3

REALTY FINANCE TRUST, INC.

CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS' EQUITY

(In thousands, except for share data)

Common Stock | Convertible Stock | ||||||||||||||||||||||||||||

Number of Shares | Par Value | Number of Shares | Amount | Additional Paid-In Capital | Accumulated Other Comprehensive Loss | Accumulated Deficit | Total Stockholders' Equity | ||||||||||||||||||||||

Balance, December 31, 2014 | 15,472,192 | $ | 155 | 1,000 | $ | 1 | $ | 340,874 | $ | (307 | ) | $ | (10,216 | ) | $ | 330,507 | |||||||||||||

Issuance of common stock | 3,795,148 | 38 | — | — | 94,583 | — | — | 94,621 | |||||||||||||||||||||

Common stock repurchases | (5,752 | ) | — | — | — | (144 | ) | — | — | (144 | ) | ||||||||||||||||||

Net income | — | — | — | — | — | — | 4,632 | 4,632 | |||||||||||||||||||||

Distributions declared | — | — | — | — | — | — | (8,788 | ) | (8,788 | ) | |||||||||||||||||||

Common stock issued through distribution reinvestment plan | 145,173 | 1 | — | — | 3,444 | — | — | 3,445 | |||||||||||||||||||||

Share-based compensation | — | — | — | — | 6 | — | — | 6 | |||||||||||||||||||||

Common stock offering costs, commissions and dealer manager fees | — | — | — | — | (11,390 | ) | — | — | (11,390 | ) | |||||||||||||||||||

Other comprehensive income | — | — | — | — | — | 141 | — | 141 | |||||||||||||||||||||

Balance, March 31, 2015 (Unaudited) | 19,406,761 | $ | 194 | 1,000 | $ | 1 | $ | 427,373 | $ | (166 | ) | $ | (14,372 | ) | $ | 413,030 | |||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

4

REALTY FINANCE TRUST, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(In thousands)

(Unaudited)

Three Months Ended March 31, | |||||||

2015 | 2014 | ||||||

Cash flows from operating activities: | |||||||

Net income | $ | 4,632 | $ | 226 | |||

Adjustments to reconcile net income to net cash provided by (used in) operating activities: | |||||||

Discount accretion and premium amortization, net | (189 | ) | (52 | ) | |||

Accretion of loan exit fees | (145 | ) | — | ||||

Amortization of deferred financing costs | 479 | — | |||||

Share-based compensation | 6 | 4 | |||||

Loan loss provision | 144 | 86 | |||||

Changes in assets and liabilities: | |||||||

Accrued interest receivable | 705 | (198 | ) | ||||

Prepaid expenses and other assets | 859 | (1,194 | ) | ||||

Accounts payable and accrued expenses | (364 | ) | 92 | ||||

Due to affiliate | (894 | ) | — | ||||

Interest payable | 25 | (2 | ) | ||||

Net cash provided by (used in) operating activities | $ | 5,258 | $ | (1,038 | ) | ||

Cash flows from investing activities: | |||||||

Origination and purchase of commercial mortgage loans | $ | (116,434 | ) | $ | (24,066 | ) | |

Purchase of real estate securities | (8,016 | ) | (9,497 | ) | |||

Principal repayments received on commercial mortgage loans | 14,321 | 38 | |||||

Net cash used in investing activities | $ | (110,129 | ) | $ | (33,525 | ) | |

Cash flows from financing activities: | |||||||

Proceeds from issuances of common stock | $ | 92,806 | $ | 40,844 | |||

Common stock repurchases | (144 | ) | — | ||||

Payments of offering costs and fees related to common stock issuances | (9,178 | ) | (4,501 | ) | |||

Borrowings on revolving line of credit with affiliate | — | 3,300 | |||||

Repayments of revolving line of credit with affiliate | — | (7,305 | ) | ||||

Borrowings on repurchase agreements - commercial mortgage loans | 38,376 | — | |||||

Repayments of repurchase agreements - commercial mortgage loans | (6,238 | ) | — | ||||

Borrowings on repurchase agreements - real estate securities | 99,560 | 4,010 | |||||

Repayments of repurchase agreements - real estate securities | (88,095 | ) | (10 | ) | |||

Advances from affiliate | — | (1,078 | ) | ||||

Payments of deferred financing costs | (750 | ) | — | ||||

Distributions paid | (4,697 | ) | (523 | ) | |||

Net cash provided by financing activities | $ | 121,640 | $ | 34,737 | |||

Net change in cash | $ | 16,769 | $ | 174 | |||

Cash, beginning of period | 386 | 178 | |||||

Cash, end of period | $ | 17,155 | $ | 352 | |||

5

REALTY FINANCE TRUST, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(In thousands)

(Unaudited)

Three Months Ended March 31, | |||||||

2015 | 2014 | ||||||

Supplemental disclosures of cash flow information: | |||||||

Escrow deposits payable related to commercial mortgage loans | $ | 295 | $ | — | |||

Income taxes paid | 9 | — | |||||

Interest paid | 2,471 | 24 | |||||

Supplemental disclosures of non-cash flow information: | |||||||

Distributions payable | $ | 3,269 | $ | 469 | |||

Common stock issued through distribution reinvestment plan | 3,445 | 266 | |||||

Receivable for common stock issued | 3,006 | — | |||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

6

REALTY FINANCE TRUST, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2015

(Unaudited)

Note 1 - Organization and Business Operations

Realty Finance Trust, Inc. (formerly known as ARC Realty Finance Trust, Inc.) (the "Company") was incorporated in Maryland on November 15, 2012 and conducts its operations to qualify as a real estate investment trust ("REIT") for U.S. federal income tax purposes beginning with the filing of its tax return for the taxable year ended December 31, 2013. The Company is offering for sale a maximum of $2.0 billion of common stock, $0.01 par value per share, on a reasonable best efforts basis, pursuant to a registration statement on Form S-11 (the "Offering") filed with the U.S. Securities and Exchange Commission under the Securities Act of 1933, as amended. The Offering also covers the offer and sale of up to approximately $400.0 million in shares of common stock pursuant to a distribution reinvestment plan (the "DRIP") under which common stockholders may elect to have their distributions reinvested in additional shares of the Company’s common stock. On May 14, 2013, the Company commenced business operations after raising in excess of $2.0 million of equity, the amount required for the Company to release equity proceeds from escrow.

Prior to the filing of the Company's second Quarterly Report on Form 10-Q following February 12, 2015 (the "NAV Pricing Date"), the per share purchase price in the Offering will be up to $25.00 per share (including the maximum allowed to be charged for commissions and fees and subject to certain discounts) and the per share purchase price for shares issued under the DRIP will be $23.75 per share, which is 95% of the purchase price per share in the Offering. As of March 31, 2015, the aggregate value of all the common stock outstanding was $484.7 million based on a per share value of $25.00 (or $23.75 for shares issued under DRIP). After the NAV Pricing Date, the Company will begin offering shares in the Offering and the DRIP at a per share purchase price that will vary quarterly and will be equal to the net asset value ("NAV") divided by the number of shares outstanding as of the end of the business day immediately preceding the day on which the Company makes its quarterly periodic filing ("Per Share NAV"). Applicable selling commissions and dealer manager fees will be added to the per share price for shares in the Company’s primary offering but not for the DRIP.

On December 30, 2014, the Company filed with the Maryland State Department of Assessments and Taxation articles supplementary to its charter that reclassified 1,000 authorized but unissued shares of the Company’s common stock as shares of convertible stock and set the terms of such convertible shares. The Company then issued 1,000 convertible shares to Realty Finance Advisors, LLC (the "Advisor") for $1.00 per share. The convertible shares will automatically convert to shares of common stock upon the first occurrence of any of following triggering events (the "Triggering Events"): (i) the Company has paid total distributions on the then-outstanding shares of common stock in an amount equal to or in excess of the sum of the invested capital (as defined in the Company’s charter) plus an aggregate 6.0% cumulative, pre-tax, non-compounded, annual return on such invested capital, (ii) a listing of the Company’s shares of common stock on a national securities exchange and (iii) the termination of the Company’s advisory agreement under certain circumstances. In general, but with certain exceptions as outlined in the articles supplementary, each convertible share will convert into a number of common shares equal to 1/1000 of the quotient of (a) the conversion product (the product of 0.15 times the amount, if any, by which (i) the sum of the enterprise value as of the date of the Triggering Event plus total distributions paid to the Company’s stockholders through the date of the Triggering Event exceeds (ii) the sum of the Company's stockholders’ invested capital plus a 6.0% return as of the date of the Triggering Event) divided by (b) the quotient of the enterprise value divided by the number of shares of the Company’s common stock outstanding (on an as-converted basis) on the date of the Triggering Event. The conversion product will be reduced by the amounts payable pursuant to the annual subordinated performance fee as realized appreciation in the Company’s assets during the time that the Advisor or one of its affiliates acts as the Company’s advisor.

The Company was formed to originate, acquire and manage a diversified portfolio of commercial real estate debt investments secured by properties located both within and outside of the United States. The Company may also invest in commercial real estate securities and commercial real estate properties. Commercial real estate debt investments may include first mortgage loans, subordinated mortgage loans, mezzanine loans and participations in such loans. Commercial real estate securities may include commercial mortgage-backed securities ("CMBS"), senior unsecured debt of publicly traded REITs, debt or equity securities of other publicly traded real estate companies and collateralized debt obligations ("CDOs").

The Company has no direct employees. The Company has retained the Advisor to manage the Company's affairs on a day-to-day basis. Realty Capital Securities, LLC (the "Dealer Manager") serves as the dealer manager of the Offering. The Advisor and Dealer Manager are under common control with the parent of American Realty Capital VIII, LLC (the "Sponsor"), as a result of which they are related parties and each of them have or will receive compensation and fees for services related to the Offering, the investment and management of the Company's assets, the operations of the company and the liquidation of the Company.

7

REALTY FINANCE TRUST, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2015

(Unaudited)

Note 2 - Summary of Significant Accounting Policies

Basis of Accounting

The accompanying condensed consolidated financial statements and related footnotes are unaudited and have been prepared on the accrual basis of accounting in conformity with accounting principles generally accepted in the United States of America (“GAAP”) for interim financial statements. The accompanying condensed consolidated financial statements include the accounts of the Company, Realty Finance Operating Partnership, L.P. (the "OP") and its subsidiaries. All intercompany accounts and transactions have been eliminated in consolidation.

Interim financial statements are prepared in accordance with GAAP for interim financial information and pursuant to the requirements for reporting on Form 10-Q and Regulation S-X, as appropriate. Accordingly, the condensed consolidated financial statements may not include all of the information and notes required by GAAP for annual consolidated financial statements. GAAP requires management to make estimates and assumptions that affect the reported amount of assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reported periods. Changes in the economic environment, financial markets and any other parameters used in determining these estimates could cause actual results to differ materially. In the opinion of management, the interim data includes all adjustments, of a normal and recurring nature, necessary for a fair statement of the results for the periods presented. The current period’s results of operations will not necessarily be indicative of results that ultimately may be achieved for the fiscal year ending on December 31, 2015.

Allowance for Loan Losses

The allowance for loan losses reflects management's estimate of loan losses inherent in the loan portfolio as of the balance sheet date. The reserve is increased through the loan loss provision on the Company's consolidated statement of operations and is decreased by charge-offs when losses are confirmed through the receipt of assets, such as cash in a pre-foreclosure sale or upon ownership control of the underlying collateral in full satisfaction of the loan upon foreclosure or when significant collection efforts have ceased. The Company uses a uniform process for determining its allowance for loan losses. The allowance for loan losses includes a general, formula-based component and an asset-specific component.

General reserves are recorded when (i) available information as of each balance sheet date indicates that it is probable a loss has occurred in the portfolio and (ii) the amount of the loss can be reasonably estimated. The Company currently estimates loss rates based on historical realized losses experienced in the industry and takes into account current collateral and economic conditions affecting the probability or severity of losses when establishing the allowance for loan losses. The Company performs a comprehensive analysis of its loan portfolio and assigns risk ratings to loans that incorporate management's current judgments about their credit quality based on all known and relevant internal and external factors that may affect collectability. The Company considers, among other things, payment status, lien position, borrower financial resources and investment in collateral, collateral type, project economics and geographical location as well as national and regional economic factors. This methodology results in loans being segmented by risk classification into risk rating categories that are associated with estimated probabilities of default and principal loss. Ratings range from "1" to "5" with "1" representing the lowest risk of loss and "5" representing the highest risk of loss.

The asset-specific reserve component relates to reserves for losses on individual impaired loans. The Company considers a loan to be impaired when, based upon current information and events, it believes that it is probable that the Company will be unable to collect all amounts due under the contractual terms of the loan agreement. This assessment is made on an individual loan basis each quarter based on such factors as payment status, lien position, borrower financial resources and investment in collateral, collateral type, project economics and geographical location as well as national and regional economic factors. A reserve is established for an impaired loan when the present value of payments expected to be received, observable market prices or the estimated fair value of the collateral (for loans that are dependent on the collateral for repayment) is lower than the carrying value of that loan.

For collateral dependent impaired loans, impairment is measured using the estimated fair value of collateral less the estimated cost to sell. Valuations are performed or obtained at the time a loan is determined to be impaired and designated non-performing, and they are updated if circumstances indicate that a significant change in value has occurred. The Advisor generally will use the income approach through internally developed valuation models to estimate the fair value of the collateral for such loans. In more limited cases, the Advisor will obtain external "as is" appraisals for loan collateral, generally when third party participations exist.

A loan is also considered impaired if its terms are modified in a troubled debt restructuring ("TDR"). A TDR occurs when a

8

REALTY FINANCE TRUST, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2015

(Unaudited)

concession is granted and the debtor is experiencing financial difficulties. Impairments on TDR loans are generally measured based on the present value of expected future cash flows discounted at the effective interest rate of the original loans.

The Company designates non-performing loans at such time as (i) loan payments become 90-days past due; (ii) the loan has a maturity default; or (iii) when, in the opinion of the Company, it is probable the Company will be unable to collect all amounts due according to the contractual terms of the loan. Income recognition will be suspended when a loan is designated non-performing and resumed only when the suspended loan becomes contractually current and performance is demonstrated to have resumed. A loan will be written off when it is no longer realizable and legally discharged.

As of March 31, 2015 and December 31, 2014, the Company had 46 and 38 loan investments, respectively, all of which were current on their interest and scheduled principal payments. The Company has established a $0.7 million and $0.6 million allowance for loan losses as of March 31, 2015 and December 31, 2014, respectively. There are no specifically reserved loans in the portfolio as of March 31, 2015 and December 31, 2014.

Per Share Data

The Company calculates basic earnings per share by dividing net income attributable to the Company for the period by the weighted-average number of shares of common stock outstanding for that period. Diluted earnings per share reflects the potential dilution that that could occur from shares issuable in connection with the restricted stock plan and if convertible shares were exercised, except when doing so would be anti-dilutive.

Reportable Segments

The Company conducts its business through the following segments:

• | The real estate debt business which is focused on originating, acquiring and asset managing commercial real estate debt investments, including first mortgage loans, subordinate mortgages, mezzanine loans and participations in such loans. |

• | The real estate securities business which is focused on investing in and asset managing commercial real estate securities primarily consisting of CMBS and may include unsecured REIT debt, CDO notes and other securities. |

See Note 12 - Segment Reporting for further information regarding the Company's segments.

New Accounting Pronouncements

In May 2014, the FASB issued revised guidance relating to revenue recognition. Under the revised guidance, an entity is required to recognize revenue when it transfers promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. The revised guidance is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2017. The Company has not yet selected a transition method and is currently evaluating the impact of the new guidance.

In June 2014, the FASB issued Accounting Standards Update ("ASU") No. 2014-11 "Repurchase-to-Maturity Transactions, Repurchase Financings and Disclosures." ASU No. 2014-11 makes limited changes to the accounting for repurchase agreements, clarifies when repurchase agreements and securities lending transactions should be accounted for as secured borrowings and requires additional disclosures regarding these types of transactions. The Company currently records repurchase arrangements as secured borrowings and does not anticipate this guidance will have an impact on the Company's condensed consolidated financial statements.

In April 2015, the FASB issued guidance that simplifies the presentation of debt issuance costs by amending the accounting guidance to require that debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct deduction from the carrying amount of the related debt liability. The amendments are consistent with the accounting guidance related to debt discounts. This guidance is effective for the first interim or annual period beginning after December 15, 2015. Early adoption is permitted, and the Company is currently assessing the impact of this guidance on its condensed consolidated financial statements.

9

REALTY FINANCE TRUST, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2015

(Unaudited)

Note 3 - Commercial Mortgage Loans

The following table is a summary of the Company's commercial mortgage loans by class (in thousands):

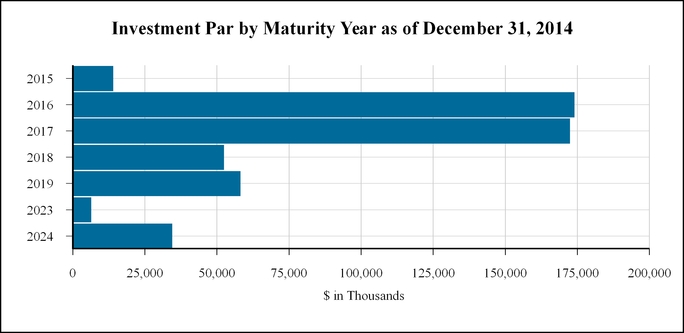

March 31, 2015 | December 31, 2014 | ||||||

Senior loans | $ | 342,870 | $ | 250,093 | |||

Mezzanine loans | 206,902 | 191,863 | |||||

Subordinated loans | 10,000 | 15,498 | |||||

Total gross carrying value of loans | 559,772 | 457,454 | |||||

Less: Allowance for loan losses | 714 | 570 | |||||

Total commercial mortgage loans | $ | 559,058 | $ | 456,884 | |||

As of March 31, 2015, the Company's commercial mortgage loan portfolio was comprised of 46 loans with a par value of $563.9 million. For the three months ended March 31, 2015, the Company received scheduled and unscheduled principal repayments of $14.3 million on the loans.

The following table presents the activity in the Company's allowance for loan losses (in thousands):

Three Months Ended March 31, 2015 | Year Ended December 31, 2014 | ||||||

Beginning of period | $ | 570 | $ | — | |||

Provision for loan losses | 144 | 570 | |||||

Charge-offs | — | — | |||||

Recoveries | — | — | |||||

End of period | $ | 714 | $ | 570 | |||

The Company's commercial mortgage loan portfolio was comprised of the following as of March 31, 2015 (in thousands):

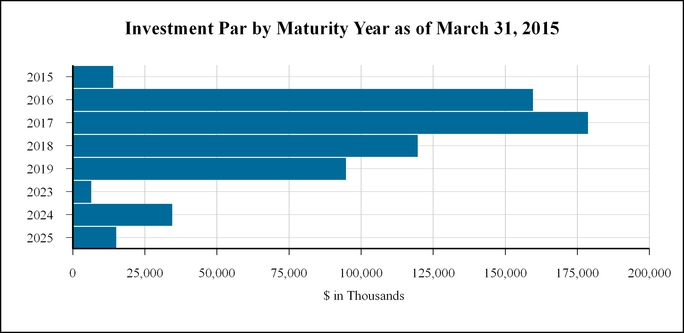

Loan Type | Property Type | Par Value | Premium (Discount)(1) | Carrying Value | Interest Rate | Effective Yield | Loan to Value (2) | Maturity Date | ||||||||||||||||

Senior 1 | Office | $ | 11,450 | $ | (61 | ) | $ | 11,389 | 5.00% +1M LIBOR | 5.5 | % | 70.0 | % | June 2017 | ||||||||||

Senior 2 | Retail | 3,389 | (27 | ) | 3,362 | 5.40% +1M LIBOR | 6.3 | % | 73.9 | % | July 2016 | |||||||||||||

Senior 3 | Mixed Use | 14,000 | (96 | ) | 13,904 | 8.00% +1M LIBOR | 10.9 | % | 70.0 | % | July 2015 | |||||||||||||

Senior 4 | Office | 5,750 | (7 | ) | 5,743 | 4.90% +1M LIBOR | 5.1 | % | 80.0 | % | August 2017 | |||||||||||||

Senior 5 | Mixed Use | 31,250 | (147 | ) | 31,103 | 4.50% +1M LIBOR | 4.9 | % | 75.0 | % | September 2017 | |||||||||||||

Senior 6 | Mixed Use | 32,272 | (119 | ) | 32,153 | 5.50% +1M LIBOR | 5.8 | % | 55.3 | % | September 2019 | |||||||||||||

Senior 7 | Retail | 9,450 | (40 | ) | 9,410 | 4.90% +1M LIBOR | 5.3 | % | 70.0 | % | September 2017 | |||||||||||||

Senior 8 | Mixed Use | 7,460 | (42 | ) | 7,418 | 4.75% +1M LIBOR | 5.2 | % | 78.0 | % | October 2017 | |||||||||||||

Senior 9 | Hotel | 10,171 | (41 | ) | 10,130 | 5.75% +1M LIBOR | 6.1 | % | 60.0 | % | October 2017 | |||||||||||||

Senior 10 | Retail | 11,800 | (56 | ) | 11,744 | 4.75% +1M LIBOR | 5.1 | % | 79.4 | % | November 2017 | |||||||||||||

Senior 11 | Office | 22,150 | (249 | ) | 21,901 | 4.65% +1M LIBOR | 5.3 | % | 80.0 | % | November 2017 | |||||||||||||

Senior 12 | Office | 9,150 | (53 | ) | 9,097 | 5.50% +1M LIBOR | 6.1 | % | 75.0 | % | November 2016 | |||||||||||||

Senior 13 | Office | 14,200 | (19 | ) | 14,181 | 5.20% +1M LIBOR | 5.5 | % | 75.0 | % | November 2017 | |||||||||||||

Senior 14 | Office | 34,500 | (343 | ) | 34,157 | 5.25% +1M LIBOR | 5.7 | % | 75.0 | % | December 2018 | |||||||||||||

Senior 15 | Office | 11,400 | (12 | ) | 11,388 | 4.80% +1M LIBOR | 5.0 | % | 75.0 | % | December 2017 | |||||||||||||

Senior 16 | Mixed Use | 9,600 | (70 | ) | 9,530 | 5.10% +1M LIBOR | 5.6 | % | 75.0 | % | January 2018 | |||||||||||||

Senior 17 | Office | 9,180 | (97 | ) | 9,083 | 5.00% +1M LIBOR | 5.6 | % | 75.0 | % | January 2018 | |||||||||||||

Senior 18 | Multifamily | 6,611 | (48 | ) | 6,563 | 4.75% +1M LIBOR | 5.2 | % | 78.3 | % | February 2018 | |||||||||||||

Senior 19 | Office | 24,500 | (188 | ) | 24,312 | 4.60% +1M LIBOR | 5.0 | % | 65.0 | % | February 2019 | |||||||||||||

Senior 20 | Retail | 11,450 | (66 | ) | 11,384 | 4.50% +1M LIBOR | 4.8 | % | 74.8 | % | February 2019 | |||||||||||||

Senior 21 | Multifamily | 12,840 | (80 | ) | 12,760 | 5.00% +1M LIBOR | 5.4 | % | 76.7 | % | February 2018 | |||||||||||||

Senior 22 | Multifamily | 8,600 | (55 | ) | 8,545 | 4.70% +1M LIBOR | 5.1 | % | 68.8 | % | February 2018 | |||||||||||||

Senior 23 | Retail | 9,850 | (67 | ) | 9,783 | 5.25% +1M LIBOR | 5.7 | % | 80.0 | % | March 2018 | |||||||||||||

Senior 24 | Multifamily | 10,450 | (57 | ) | 10,393 | 4.75% +1M LIBOR | 5.1 | % | 75.0 | % | April 2018 | |||||||||||||

10

REALTY FINANCE TRUST, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2015

(Unaudited)

Loan Type | Property Type | Par Value | Premium (Discount)(1) | Carrying Value | Interest Rate | Effective Yield | Loan to Value (2) | Maturity Date | ||||||||||||||||

Senior 25 | Retail | 13,500 | (63 | ) | 13,437 | 5.00% +1M LIBOR | 5.4 | % | 78.0 | % | April 2017 | |||||||||||||

Mezzanine 1 | Hotel | 6,344 | (2,222 | ) | 4,122 | 5.50% | 12.7 | % | 76.7 | % | May 2023 | |||||||||||||

Mezzanine 2 | Multifamily | 5,000 | 40 | 5,040 | 9.00% | 8.7 | % | 73.9 | % | September 2018 | ||||||||||||||

Mezzanine 3 | Office | 9,000 | 48 | 9,048 | 11.00% +3M LIBOR | 10.9 | % | 77.9 | % | September 2016 | ||||||||||||||

Mezzanine 4 | Office | 5,000 | 69 | 5,069 | 11.00% | 10.8 | % | 63.6 | % | January 2024 | ||||||||||||||

Mezzanine 5 | Student Housing | 4,000 | 56 | 4,056 | 12.00% | 11.7 | % | 74.5 | % | January 2024 | ||||||||||||||

Mezzanine 6 | Hotel | 11,000 | 25 | 11,025 | 7.05% +1M LIBOR | 7.0 | % | 70.0 | % | March 2016 | ||||||||||||||

Mezzanine 7 | Hotel | 3,000 | 19 | 3,019 | 11.00% | 10.8 | % | 81.8 | % | August 2018 | ||||||||||||||

Mezzanine 8 | Office | 7,000 | 30 | 7,030 | 12.00% | 11.9 | % | 78.3 | % | May 2019 | ||||||||||||||

Mezzanine 9 | Retail | 1,962 | 9 | 1,971 | 13.00% | 12.9 | % | 85.0 | % | June 2024 | ||||||||||||||

Mezzanine 10 | Office | 10,000 | 16 | 10,016 | 8.00% +1M LIBOR | 8.0 | % | 80.0 | % | May 2016 | ||||||||||||||

Mezzanine 11 | Multifamily | 3,480 | 17 | 3,497 | 9.50% | 9.4 | % | 84.5 | % | July 2024 | ||||||||||||||

Mezzanine 12 | Hotel | 35,000 | 112 | 35,112 | 8.40% +1M LIBOR | 8.3 | % | 70.1 | % | June 2016 | ||||||||||||||

Mezzanine 13 | Mixed Use | 7,000 | (29 | ) | 6,971 | 10.50% +1M LIBOR | 11.0 | % | 84.0 | % | July 2017 | |||||||||||||

Mezzanine 14 | Hotel | 12,000 | 46 | 12,046 | 9.00% +1M LIBOR | 8.9 | % | 74.2 | % | September 2016 | ||||||||||||||

Mezzanine 15 | Student Housing | 5,000 | 19 | 5,019 | 8.00% +1M LIBOR | 7.9 | % | 71.0 | % | August 2016 | ||||||||||||||

Mezzanine 16 | Office | 45,000 | 170 | 45,170 | 7.25% +1M LIBOR | 7.1 | % | 76.0 | % | August 2016 | ||||||||||||||

Mezzanine 17 | Office | 9,000 | 42 | 9,042 | 10.50% | 10.4 | % | 85.0 | % | October 2019 | ||||||||||||||

Mezzanine 18 | Office | 5,100 | — | 5,100 | 10.00% +3M LIBOR | 10.3 | % | 79.5 | % | October 2017 | ||||||||||||||

Mezzanine 19 | Office | 10,000 | (537 | ) | 9,463 | 10.00% | 10.9 | % | 79.0 | % | September 2024 | |||||||||||||

Mezzanine 20 | Office | 15,000 | 86 | 15,086 | 11.00% | 10.9 | % | 80.0 | % | April 2025 | ||||||||||||||

Subordinated 1 | Net Lease Retail | 10,000 | — | 10,000 | 11.00% | 11.0 | % | 50.1 | % | April 2024 | ||||||||||||||

$ | 563,859 | $ | (4,087 | ) | $ | 559,772 | 7.0 | % | 73.3 | % | ||||||||||||||

________________________

(1) Includes acquisition fees and acquisition expenses where applicable.

(2) Loan to value percentage is from metrics at origination.

Credit Characteristics

As part of the Company's process for monitoring the credit quality of its loans, it performs a quarterly loan portfolio assessment and assigns risk ratings to each of its performing loans. The loans are scored on a scale of 1 to 5 as follows:

Investment Rating | Summary Description | |

1 | Investment exceeding fundamental performance expectations and/or capital gain expected. Trends and risk factors since time of investment are favorable. | |

2 | Performing consistent with expectations and a full return of principal and interest expected. Trends and risk factors are neutral to favorable. | |

3 | Performing investments requiring closer monitoring. Trends and risk factors show some deterioration. | |

4 | Underperforming investment with some loss of interest or dividend expected but still expecting a positive return on investment. Trends and risk factors are negative. | |

5 | Underperforming investment with expected loss of interest and some principal. | |

All commercial mortgage loans are assigned an initial risk rating of 2. As of March 31, 2015 and December 31, 2014, the weighted average risk rating of loans was 1.9 and 2.0, respectively. As of March 31, 2015, the Company did not have any loans that were past due on their payments, in non-accrual status or impaired.

11

REALTY FINANCE TRUST, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2015

(Unaudited)

For the three months ended March 31, 2015 and year ended December 31, 2014, the activity in the Company's loan portfolio was as follows (in thousands):

Three Months Ended March 31, 2015 | Year Ended December 31, 2014 | ||||||

Beginning balance | $ | 456,884 | $ | 30,832 | |||

Acquisitions and originations | 116,434 | 429,941 | |||||

Dispositions | — | (3,580 | ) | ||||

Principal repayments | (14,321 | ) | (136 | ) | |||

Discount accretion and premium amortization* | 205 | 397 | |||||

Provision for loan losses | (144 | ) | (570 | ) | |||

Ending balance | $ | 559,058 | $ | 456,884 | |||

________________________

* Includes amortization of capitalized acquisition fees and expenses.

During the three months ended March 31, 2015, the Company invested approximately $116.4 million in 10 loans including $0.7 million of capitalized acquisition fees and expenses.

Note 4 - Real Estate Securities

The following is a summary of the Company's real estate securities, CMBS (in thousands):

Weighted Average | |||||||||||||||

Number of Investments | Interest Rate | Maturity | Par Value | Fair Value | |||||||||||

March 31, 2015 | 9 | 1M LIBOR + 3.237% | September 2017 | $ | 58,447 | $ | 58,375 | ||||||||

December 31, 2014 | 8 | 1M LIBOR + 3.124% | November 2017 | 50,447 | 50,234 | ||||||||||

The Company classified its CMBS investments as available-for-sale as of March 31, 2015 and December 31, 2014. These investments are reported at fair value in the balance sheet with changes in fair value recorded in accumulated other comprehensive income or loss. The following table shows the changes in fair value of the Company's CMBS investments (in thousands):

Amortized Cost | Unrealized Gains | Unrealized Losses | Fair Value | |||||||||||||

March 31, 2015 | $ | 58,542 | $ | 49 | $ | (216 | ) | $ | 58,375 | |||||||

December 31, 2014 | 50,541 | 14 | (321 | ) | 50,234 | |||||||||||

Note 5 - Debt

Repurchase Agreements - Commercial Mortgage Loans

The Company entered into repurchase facilities with JP Morgan Chase Bank, National Association (the "JPM Repo Facility") and Barclays Bank PLC (the "Barclays Repo Facility"). The JPM Repo Facility and Barclays Repo Facility each provide up to $150.0 million in advances, subject to adjustment, which the Company expects to use to finance the acquisition or origination of eligible loans, including first mortgage loans, subordinated mortgage loans, mezzanine loans and participation interests therein. The initial maturity date of the JPM Repo Facility is June 18, 2016, with a one-year extension at the Company’s option, which may be exercised upon the satisfaction of certain conditions. The initial maturity date of the Barclays Repo Facility is September 3, 2015, with four six-month extensions at the Company’s option, which may be exercised upon the satisfaction of certain conditions.

As of March 31, 2015 and December 31, 2014, the Company had $75.9 million and $76.5 million outstanding under the JPM Repo Facility, respectively. Advances under the JPM Repo Facility accrue interest at per annum rates equal to the sum of (i) the applicable LIBOR index rate plus (ii) a margin between 2.25% to 4.50%, depending on the attributes of the purchased assets. As of March 31, 2015 and December 31, 2014, the weighted average interest rate on advances was 3.755% and 3.841%, respectively. The Company incurred $0.7 million and $0 in interest expense on the JPM Repo Facility for the three months ended March 31, 2015 and 2014, respectively.

As of March 31, 2015 and December 31, 2014, the Company had $106.4 million and $73.7 million outstanding under the Barclays Repo Facility, respectively. Advances under the Barclays Repo Facility accrue interest at per annum rates equal to the

12

REALTY FINANCE TRUST, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2015

(Unaudited)

sum of (i) the applicable LIBOR index rate plus (ii) a margin between 2.00% to 2.50%, depending on the attributes of the purchased assets. As of March 31, 2015 and December 31, 2014, the weighted average interest rate on advances was 2.172% and 2.155%, respectively. The Company incurred $0.5 million and $0 in interest expense on the Barclays Repo Facility for the three months ended March 31, 2015 and 2014, respectively.

Repurchase Agreements - Real Estate Securities

The Company has entered into various Master Repurchase Agreements (the "MRAs") that allow the Company to sell real estate securities while providing a fixed repurchase price for the same real estate securities in the future. The repurchase contracts on each security under an MRA generally mature in 30-90 days and terms are adjusted for current market rates as necessary. As of March 31, 2015 and December 31, 2014, the Company was entered into six MRAs, of which three were in use, see below (in thousands):

Weighted Average | |||||||||||||

Counterparty | Amount Outstanding | Accrued Interest | Interest Rate | Days to Maturity | |||||||||

As of March 31, 2015 | |||||||||||||

Citigroup Global Markets, Inc. | $ | 4,010 | $ | 2 | 1.48 | % | 20 | ||||||

J.P. Morgan Securities LLC | 29,993 | 14 | 1.38 | % | 20 | ||||||||

Wells Fargo Securities, LLC | 3,731 | 2 | 1.53 | % | 20 | ||||||||

Total/Weighted Average | $ | 37,734 | $ | 18 | 1.41 | % | 20 | ||||||

As of December 31, 2014 | |||||||||||||

Citigroup Global Markets, Inc. | $ | 4,010 | $ | 2 | 1.46 | % | 20 | ||||||

J.P. Morgan Securities LLC | 18,528 | 8 | 1.44 | % | 20 | ||||||||

Wells Fargo Securities, LLC | 3,731 | 2 | 1.52 | % | 20 | ||||||||

Total/Weighted Average | $ | 26,269 | $ | 12 | 1.46 | % | 20 | ||||||

As of March 31, 2015 and December 31, 2014, the Company's $37.7 million and $26.3 million of borrowings under repurchase agreements were collaterlized by CMBS with a fair value of $50.4 million and $33.8 million, respectively.

Note 6 - Net Income Per Share

The following table is a summary of the basic and diluted net income per share computation for the three months ended March 31, 2015 and 2014, respectively:

Three Months Ended March 31, | |||||||

2015 | 2014 | ||||||

Net income (in thousands) | $ | 4,632 | $ | 226 | |||

Basic weighted average shares outstanding | 17,279,713 | 2,025,934 | |||||

Unvested restricted shares | 4,373 | 4,089 | |||||

Diluted weighted average shares outstanding | 17,284,086 | 2,030,023 | |||||

Basic net income per share | $ | 0.27 | $ | 0.11 | |||

Diluted net income per share | $ | 0.27 | $ | 0.11 | |||

Note 7 - Common Stock

As of March 31, 2015 and December 31, 2014, the Company had approximately 19,406,761 and 15,472,192 shares of common stock outstanding, respectively, including shares issued pursuant to the DRIP and unvested restricted shares. As of March 31, 2015 and December 31, 2014, the Company had received total proceeds of approximately $482.2 million and $384.2 million, respectively, including shares issued pursuant to the DRIP and share-based compensation.

On December 30, 2014, the Company filed with the Maryland State Department of Assessments and Taxation articles supplementary to its charter that reclassified 1,000 authorized but unissued shares of the Company’s common stock as shares of convertible stock and set the terms of such convertible shares. The Company then issued 1,000 convertible shares to the

13

REALTY FINANCE TRUST, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2015

(Unaudited)

Advisor for $1.00 per share. The convertible shares will automatically convert to shares of common stock upon the first occurrence of any of the Triggering Events.

Distributions

In order to maintain its election to qualify as a REIT, the Company must currently distribute, at a minimum, an amount equal to 90% of its taxable income, without regard to the deduction for distributions paid and excluding net capital gains. The Company must distribute 100% of its taxable income (including net capital gains) to avoid paying corporate federal income taxes.

On May 13, 2013, the Company's board of directors authorized, and the Company declared a distribution, which is calculated based on stockholders of record each day during the applicable period at a rate of $0.00565068493 per day, based on a price of $25.00 per share of common stock. The Company's distributions are payable by the fifth day following each month end to stockholders of record at the close of business each day during the prior month. The first distribution payment was made on June 3, 2013, relating to the period from May 30, 2013 (15 days after the date of the first asset acquisition) through May 31, 2013. Distributions payments are dependent on the availability of funds. The board of directors may reduce the amount of distributions paid or suspend distribution payments at any time, and therefore, distributions payments are not assured.

The below table shows the distributions paid during the three months ended March 31, 2015 and year ended December 31, 2014 (in thousands, except for shares):

Three Months Ended March 31, 2015 Payment Date | Weighted Average Shares Outstanding (1) | Amount Paid in Cash | Amount Issued under DRIP | ||||||||

January 2, 2015 | 16,006,444 | $ | 1,512 | $ | 1,109 | ||||||

February 2, 2015 | 17,192,517 | 1,618 | 1,182 | ||||||||

March 2, 2015 | 18,644,252 | 1,567 | 1,154 | ||||||||

Total | $ | 4,697 | $ | 3,445 | |||||||

Year Ended December 31, 2014 Payment Date | Weighted Average Shares Outstanding (1) | Amount Paid in Cash | Amount Issued under DRIP | ||||||||

January 2, 2014 | 1,219,825 | $ | 141 | $ | 74 | ||||||

February 3, 2014 | 1,463,829 | 171 | 85 | ||||||||

March 3, 2014 | 1,979,935 | 213 | 106 | ||||||||

April 1, 2014 | 2,644,003 | 305 | 163 | ||||||||

May 1, 2014 | 3,277,803 | 353 | 206 | ||||||||

June 2, 2014 | 4,126,746 | 452 | 282 | ||||||||

July 2, 2014 | 5,372,322 | 571 | 356 | ||||||||

August 2, 2014 | 6,956,879 | 759 | 485 | ||||||||

September 2, 2014 | 8,925,637 | 951 | 628 | ||||||||

October 2, 2014 | 10,575,893 | 1,073 | 736 | ||||||||

November 2, 2014 | 12,253,800 | 1,249 | 905 | ||||||||

December 1, 2014 | 13,880,235 | 1,354 | 1,001 | ||||||||

Total | $ | 7,592 | $ | 5,027 | |||||||

________________________

(1) Represents the weighted average shares outstanding for the period related to the respective payment date.

For the three months ended March 31, 2015, the Company paid cash distributions of $4.7 million and had net income of $4.6 million. As of March 31, 2015, the Company had a distribution payable of $3.3 million for distributions accrued in the month of March 2015. For the three months ended March 31, 2014, the Company paid cash distributions of $0.5 million and had net income of $0.2 million. As of December 31, 2014, the Company had a distribution payable of $2.6 million for distributions accrued in the month of December 2014.

14

REALTY FINANCE TRUST, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2015

(Unaudited)

Share Repurchase Program

The Company's board of directors has adopted a Share Repurchase Program ("SRP") that enables stockholders to sell their shares to the Company in limited circumstances. The SRP permits investors to sell their shares back to the Company after they have held them for at least one year, subject to the significant conditions and limitations described below.

The repurchase price per share depends on the length of time investors have held such shares as follows: after one year from the purchase date - the lower of $23.13 or 92.5% of the amount they actually paid for each share; after two years from the purchase date - the lower of $23.75 or 95.0% of the amount they actually paid for each share; after three years from the purchase date - the lower of $24.38 or 97.5% of the amount they actually paid for each share; and after four years from the purchase date - the lower of $25.00 or 100% of the amount they actually paid for each share (in each case, as adjusted for any stock distributions, combinations, splits and recapitalizations).

The Company is only authorized to repurchase shares pursuant to the SRP using the proceeds received from the DRIP and will limit the amount spent to repurchase shares in a given quarter to the amount of proceeds received from the DRIP in that same quarter. In addition, the board of directors may reject a request for redemption at any time. Due to these limitations, the Company cannot guarantee that it will be able to accommodate all repurchase requests. Purchases under the SRP by the Company will be limited in any calendar year to 5% of the weighted average number of shares outstanding on December 31 of the previous calendar year.

When a stockholder requests redemption and the redemption is approved, the Company will reclassify such obligation from equity to a liability based on the settlement value of the obligation. Shares purchased under the SRP will have the status of authorized but unissued shares. The following table reflects the number of shares repurchased cumulatively through March 31, 2015:

Number of Requests | Number of Shares Repurchased | Average Price per Share | ||||||||

Cumulative repurchases as of December 31, 2014 | 9 | 20,355 | $ | 23.99 | ||||||

Three Months Ended March 31, 2015 (1) | 8 | 5,752 | 24.97 | |||||||

Cumulative repurchases as of March 31, 2015 (1) | 17 | 26,107 | $ | 24.21 | ||||||

________________________

(1) Includes 8 unfulfilled repurchase requests consisting of 5,752 shares at an average repurchase price per share of $24.97, which were approved but not completed as of March 31, 2015.

Note 8 - Commitments and Contingencies

Unfunded Commitments Under Commercial Mortgage Loans

As of March 31, 2015 and December 31, 2014, the Company had unfunded commitments of $84.2 million and $63.5 million related to 20 and 14 commercial mortgage loans, respectively, which amounts will generally be funded to finance capital expenditures by the Company's borrowers. These future commitments will expire over the next five years.

Litigation and Regulatory Matters

In the ordinary course of business, the Company may become subject to litigation, claims and regulatory matters. The Company has no knowledge of material legal or regulatory proceedings pending or known to be contemplated against the Company at this time.

Note 9 - Related Party Transactions and Arrangements

As of March 31, 2015, an entity wholly-owned by the Sponsor owned 8,888 shares of the Company’s outstanding common stock and the Advisor owned 1,000 shares of the Company's convertible stock.

15

REALTY FINANCE TRUST, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2015

(Unaudited)

Fees Paid in Connection with the Offering

The Dealer Manager receives fees and compensation in connection with the sale of the Company’s common stock in the Offering. The Dealer Manager receives a selling commission of up to 7.0% of the per share purchase price of the Company's offering proceeds before reallowance of commissions earned by soliciting dealers. In addition, the Dealer Manager receives up to 3.0% of the gross proceeds from the sale of shares, before reallowance to soliciting dealers, as a dealer manager fee. The Dealer Manager may reallow its dealer manager fee to such soliciting dealers. A soliciting dealer may elect to receive a fee equal to 7.5% of the gross proceeds from the sale of shares (not including selling commissions and dealer manager fees) by such soliciting dealer, with 2.5% thereof paid at the time of such sale and 1.0% thereof paid on each anniversary of the closing of such sale up to and including the fifth anniversary of the closing of such sale. If this option is elected, the dealer manager fee will be reduced to 2.5% of gross proceeds (not including selling commissions and dealer manager fees).

The table below shows the fees incurred from the Dealer Manager associated with the Offering during the three months ended March 31, 2015 and 2014, respectively, and the associated payable as of March 31, 2015 and December 31, 2014, respectively (in thousands):

Three Months Ended March 31, | Payable as of | |||||||||||||||

2015 | 2014 | March 31, 2015 | December 31, 2014 | |||||||||||||

Total commissions and fees incurred from the Dealer Manager | $ | 9,247 | $ | 3,851 | $ | 295 | $ | 119 | ||||||||

The Advisor, its affiliates, entities under common control with the Advisor and the Dealer Manager receive compensation and reimbursement for services relating to the Offering.

An affiliate of the Company, RCS Advisory Services, LLC ("RCS"), is an entity under common control with the Sponsor. RCS performs legal, compliance and marketing services for the Company.

American National Stock Transfer, LLC (the "Transfer Agent"), an entity under common control with the Sponsor, provides the Company with transfer agent, registrar and supervisory services for the Company.

An affiliate of the Company, SK Research, LLC ("SK Research"), is an entity under common control with the Sponsor. SK Research provides broker-dealers and financial advisors with the research, critical thinking and analytical resources necessary to evaluate the viability, utility and performance of investment programs.

The table below shows the compensation and reimbursement to the Advisor, its affiliates, entities under common control with the Advisor and the Dealer Manager incurred for services relating to the Offering during the three months ended March 31, 2015 and 2014, respectively, and the associated payable as of March 31, 2015 and December 31, 2014, respectively (in thousands):

Three Months Ended March 31, | Payable as of | |||||||||||||||

2015 | 2014 | March 31, 2015 | December 31, 2014 | |||||||||||||

Total compensation and reimbursement for services provided by the Advisor, its affiliates, entities under common control with the Advisor and the Dealer Manager | $ | 1,962 | $ | 360 | $ | 1,786 | $ | 1,725 | ||||||||

The payables as of March 31, 2015 and December 31, 2014 in the table above are included in due to affiliate on the Company's consolidated balance sheets.

The Company is responsible for organizational and offering costs from the ongoing Offering, excluding commissions and dealer manager fees, up to a maximum of 2.0% of gross proceeds from its ongoing Offering of common stock, measured at the end of the Offering. Organizational and offering costs in excess of the 2.0% cap as of the end of the Offering are the Advisor's responsibility. As of March 31, 2015, organizational and offering costs did not exceed the 2.0% cap of gross proceeds received from the Offering.

16

REALTY FINANCE TRUST, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2015

(Unaudited)

Fees Paid in Connection with the Operations of the Company

The Advisor receives an acquisition fee of 1.0% of the principal amount funded by the Company to originate or acquire commercial mortgage loans and 1.0% of the anticipated net equity funded by the Company to acquire real estate securities. The Company reimburses the Advisor for expenses incurred by the Advisor on behalf of the Company related to selecting, evaluating, originating and acquiring investments in an amount up to 0.5% of the principal amount funded by the Company to originate or acquire commercial mortgage loans and up to 0.5% of the anticipated net equity funded by the Company to acquire real estate securities investments. In no event will the total of all acquisition fees and acquisition expenses exceed 4.5% of the principal amount funded with respect to the Company's total portfolio including subsequent fundings to investments in the Company's portfolio. During the three months ended March 31, 2015 and 2014, acquisition fees of $1.0 million and $0.3 million, respectively, have been recognized in the consolidated statement of operations. In addition, over the same periods, the Company capitalized $0.7 million and $0.1 million, respectively, of acquisition expenses to the Company's consolidated balance sheets, which will be amortized over the life of each investment using the effective interest method.

The Company will pay the Advisor, or its affiliates, a monthly asset management fee equal to one-twelfth of 0.75% of the cost of the Company's assets. Commencing on the NAV Pricing Date, the asset management fee will be based on the lower of the cost of the Company's assets and the fair value of the Company's assets (fair value will consist of the market value of each portfolio investment as determined in accordance with the Company's valuation guidelines). The amount of the asset management fee will be reduced to the extent that funds from operations as defined by the National Association of Real Estate Investment Trusts ("FFO"), as adjusted, during the six month period ending on the last day of the calendar quarter immediately preceding the date such asset management fee is payable, is less than distributions declared during the same period. For purposes of this determination, FFO, as adjusted, is FFO adjusted to (i) include acquisition fees and acquisition expenses; (ii) include non-cash restricted stock grant amortization, if any; and (iii) impairments and loan loss reserves on investments, if any (including commercial mortgage loans and other debt investments). FFO, as adjusted, is not the same as FFO. During the three months ended March 31, 2015 and 2014, no asset management fees were incurred.

The Company will pay the Advisor, or its affiliates, an annual subordinated performance fee calculated on the basis of total return to stockholders, payable monthly in arrears, such that for any year in which total return on stockholders’ capital exceeds 6.0% per annum, the Advisor will be entitled to 15.0% of the excess total return; provided that in no event will the annual subordinated performance fee payable to the Advisor exceed 10.0% of the aggregate total return for such year. This fee will be payable only upon the sale of assets, distributions or other event which results in the Company's return on stockholders’ capital exceeding 6.0% per annum. During the three months ended March 31, 2015 and 2014, the Company incurred an annual subordinated performance fee of $0.4 million and $0, respectively.

Effective June 1, 2013, the Company entered into an agreement with the Dealer Manager to provide strategic advisory services and investment banking services required in the ordinary course of the Company's business, such as performing financial analysis, evaluating publicly traded comparable companies and assisting in developing a portfolio composition strategy, a capitalization structure to optimize future liquidity options and structuring operations. The Company prepaid the cost of $0.9 million associated with this agreement and amortizes the cost over the estimated life of the Offering into "Other expense" on the Company's consolidated statement of operations. The unamortized cost associated with this agreement is included in "Prepaid expenses and other assets" on the Company's consolidated balance sheet.

The table below depicts related party fees and reimbursements in connection with the operations of the Company for the three months ended March 31, 2015 and 2014 and the associated payable as of March 31, 2015 and December 31, 2014 (in thousands):

Three Months Ended March 31, | Payable as of | |||||||||||||||

2015 | 2014 | March 31, 2015 | December 31, 2014 | |||||||||||||

Acquisition fees and acquisition expenses | $ | 1,781 | $ | 397 | $ | 155 | $ | — | ||||||||

Advisory and investment banking fee | 14 | 135 | — | — | ||||||||||||

Subordinated performance fee | 362 | — | 965 | 191 | ||||||||||||

Other related party expenses | 21 | — | 21 | — | ||||||||||||

Total related party fees and reimbursements | $ | 2,178 | $ | 532 | $ | 1,141 | $ | 191 | ||||||||

The payables as of March 31, 2015 and December 31, 2014 in the table above are included in due to affiliate on the Company's consolidated balance sheets.

17

REALTY FINANCE TRUST, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2015

(Unaudited)

In order to improve operating cash flows and the ability to pay distributions from operating cash flows, the Advisor may elect to waive certain fees. Because the Advisor may waive certain fees, cash flows from operations that would have been paid to the Advisor may be available to pay distributions to stockholders. The fees that may be forgiven are not deferrals and accordingly, will not be paid to the Advisor. The Advisor permanently waived a portion of the acquisition fees and expenses earned on the acquisition of the Company's CMBS in the amount of $0.1 million and $0.1 million for the three months ended March 31, 2015 and 2014, respectively.

Subject to the limitations outlined below, the Company will reimburse the Advisor's cost of providing administrative services and personnel costs in connection with other services during the operational stage, in addition to paying an asset management fee; however, the Company will not reimburse the Advisor for personnel costs in connection with services for which the Advisor receives acquisition fees or disposition fees. For the three months ended March 31, 2015 and 2014, no administrative costs of the Advisor were reimbursed for any period in connection with the operations of the Company.

The Advisor must pay any expenses in which the Company's operating expenses as defined by North American Securities Administrators Association at the end of the four preceding fiscal quarters exceeds the greater of (i) 2.0% of average invested assets or (ii) 25.0% of net income other than any additions to reserves for depreciation, bad debt or other similar non-cash reserves and excluding any gain from the sale of assets for that period, unless a majority of the Company's independent directors determine the excess expenses were justified based on unusual and nonrecurring factors.

The Advisor at its election may also contribute capital to enhance the Company’s cash position for working capital and distribution purposes. Any contributed capital amounts are not reimbursable to the Advisor. Further, any capital contributions are made without any corresponding issuance of common or preferred shares. The Advisor did not contribute capital to enhance the Company's cash position for working capital or distribution purposes during the three months ended March 31, 2015 or 2014.

Fees Paid in Connection with the Liquidation of Assets, Listing of the Company's Common Stock or Termination of the Advisory Agreement

The Company will pay a disposition fee of 1.0% of the contract sales price of each commercial mortgage loans or other investment sold, including real estate securities or CDOs issued by a subsidiary of the Company as part of a securitization transaction. The Company will not be obligated to pay a disposition fee upon the maturity, prepayment, workout, modification or extension of commercial real estate debt unless there is a corresponding fee paid by the borrower, in which case the disposition fee will be the lesser of (i) 1.0% of the principal amount of the debt prior to such transaction; or (ii) the amount of the fee paid by the borrower in connection with such transaction. If the Company takes ownership of a property as a result of a workout or foreclosure of a loan, it will pay a disposition fee upon the sale of such property.

During the year ended December 31, 2014, the Company changed the structure of its incentive compensation in order to eliminate the susceptibility of the OP to certain taxes. On December 31, 2014, the OP redeemed all of the special limited partnership interests held by the Realty Finance Special Limited Partnership, LLC (the "Special Limited Partner"), an entity controlled by the Sponsor. In addition, the Special Limited Partner transferred all of its common limited partnership interests in the OP to Realty Finance Trust LP, LLC ("RFT LP"), the Company's wholly-owned subsidiary. As a result of these transactions, the Special Limited Partner no longer owns any interest in the OP and RFT LP is the sole limited partner of the OP.

On December 30, 2014, the Company filed with the Maryland State Department of Assessments and Taxation articles supplementary to its charter that reclassified 1,000 authorized but unissued shares of its common stock as shares of convertible stock and set the terms of such convertible shares. The Company then issued 1,000 convertible shares to the Advisor for $1.00 per share. The convertible shares issued to the Advisor will automatically convert to shares of the Company’s common stock upon the first to occur of any of the Triggering Events. In general, but with certain exceptions as outlined in the Articles Supplementary, each convertible share will convert into a number of common shares equal to 1/1000 of the quotient of (a) the conversion product (the product of 0.15 times the amount, if any, by which (i) the sum of the enterprise value as of the date of the Triggering Event plus total distributions paid to the Company’s stockholders through the date of the Triggering Event exceeds (ii) the sum of the Company's stockholders’ invested capital plus a 6.0% return as of the date of the Triggering Event) divided by (b) the quotient of the enterprise value divided by the number of shares of the Company’s common stock outstanding (on an as-converted basis) on the date of the Triggering Event. The conversion product will be reduced by the amounts payable pursuant to the annual subordinated performance fee as realized appreciation in the Company’s assets during the time that the Advisor or one of its affiliates acts as the Company’s advisor.

18

REALTY FINANCE TRUST, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2015

(Unaudited)

During the three months ended March 31, 2015 and 2014, no fees were paid for any period in connection with the liquidation of assets, listing of the Company's common stock or termination of the advisory agreement.

The Company has also established a restricted share plan for the benefit of employees (if the Company ever has employees), directors, employees of the Advisor and its affiliates.

Note 10 - Fair Value of Financial Instruments

GAAP establishes a hierarchy of valuation techniques based on the observability of inputs used in measuring financial instruments at fair values. GAAP establishes market-based or observable inputs as the preferred source of values, followed by valuation models using management assumptions in the absence of market inputs. The three levels of the hierarchy are described below:

• | Level I - Inputs are unadjusted, quoted prices in active markets for identical assets or liabilities at the measurement date. |

• | Level II - Inputs (other than quoted prices included in Level I) are either directly or indirectly observable for the asset or liability through correlation with market data at the measurement date and for the duration of the instrument’s anticipated life. |

• | Level III - Inputs reflect management’s best estimate of what market participants would use in pricing the asset or liability at the measurement date. Consideration is given to the risk inherent in the valuation technique and the risk inherent in the inputs to the model. |

The determination of where an asset or liability falls in the above hierarchy requires significant judgment and factors specific to the asset or liability. In instances where the determination of the fair value measurement is based on inputs from different levels of the fair value hierarchy, the level in the fair value hierarchy within which the entire fair value measurement falls is based on the lowest level input that is significant to the fair value measurement in its entirety. The Company evaluates its hierarchy disclosures each quarter and depending on various factors, it is possible that an asset or liability may be classified differently from quarter to quarter.

The Company has implemented valuation control processes to validate the fair value of the Company's financial instruments measured at fair value including those derived from pricing models. These control processes are designed to assure that the values used for financial reporting are based on observable inputs wherever possible. In the event that observable inputs are not available, the control processes are designed to assure that the valuation approach utilized is appropriate and consistently applied and the assumptions are reasonable.

Real estate securities or CMBS, are valued utilizing both observable and unobservable market inputs. These factors include projected future cash flows, ratings, subordination levels, vintage, remaining lives, credit issues, recent trades of similar real estate securities and the spreads used in the prior valuation. The Company obtains current market spread information where available and uses this information in evaluating and validating the market price of all real CMBS. Depending upon the significance of the fair value inputs used in determining these fair values, these real estate securities are classified in either Level II or Level III of the fair value hierarchy. As of March 31, 2015 and December 31, 2014, the Company received broker quotes on each CMBS investment used in determining the fair value. As of March 31, 2015 and December 31, 2014, the Company's CMBS investments have been classified as Level II due to the observable nature of many of the market inputs.

The following table presents the Company's financial instrument carried at fair value on a recurring basis in the condensed consolidated balance sheet by its level in the fair value hierarchy as of March 31, 2015 and December 31, 2014 (in thousands):

Total | Level I | Level II | Level III | ||||||||||||

March 31, 2015 | |||||||||||||||

Real estate securities | $ | 58,375 | $ | — | $ | 58,375 | $ | — | |||||||

Repurchase agreements - commercial mortgage loans | 182,307 | — | 182,307 | — | |||||||||||

Repurchase agreements - real estate securities | 37,734 | — | 37,734 | — | |||||||||||

December 31, 2014 | |||||||||||||||

Real estate securities | 50,234 | — | 50,234 | — | |||||||||||

Repurchase agreements - commercial mortgage loans | 150,169 | — | 150,169 | — | |||||||||||

Repurchase agreements - real estate securities | 26,269 | — | 26,269 | — | |||||||||||

19

REALTY FINANCE TRUST, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2015

(Unaudited)

A review of the fair value hierarchy classification is conducted on a quarterly basis. Changes in the type of inputs may result in a reclassification for certain assets. There were no transfers between levels within fair value hierarchy during the three months ended March 31, 2015 and 2014.

The fair value of cash and cash equivalents and restricted cash measured using observable quoted market prices, or Level I inputs. The fair value of short-term financial instruments, such as accrued interest receivable, prepaid expenses and other assets, accounts payable and accrued expenses, distributions payable, interest payable and due to affiliate are approximated by their carrying value on the consolidated balance sheets due to their short-term nature, and are measured using Level II inputs.

The fair values of the Company's remaining commercial mortgage loans, which are not reported at fair value on the condensed consolidated balance sheets are reported below as of March 31, 2015 and December 31, 2014 (in thousands):

Level | Carrying Value | Fair Value | |||||||

March 31, 2015 | III | $ | 559,772 | $ | 569,174 | ||||

December 31, 2014 | III | 457,454 | 474,932 | ||||||

The fair value of the commercial mortgage loans is estimated using a discounted cash flow analysis, based on the Advisor's experience with similar types of investments.

Note 11 - Offsetting Assets and Liabilities

The Company's condensed consolidated balance sheets used a gross presentation of repurchase agreements. The table below provides a gross presentation, the effects of offsetting and a net presentation of the Company's repurchase agreements within the scope of ASC 210-20, Balance Sheet—Offsetting, as of March 31, 2015 and December 31, 2014, respectively (in thousands):

Gross Amounts Not Offset on the Balance Sheet | ||||||||||||||||||||||||

Repurchase Agreements | Gross Amounts of Recognized Liabilities | Gross Amounts Offset on the Balance Sheet | Net Amount of Liabilities Presented on the Balance Sheet | Financial Instruments | Cash Collateral Pledged | Net Amount | ||||||||||||||||||

As of March 31, 2015 | ||||||||||||||||||||||||

Commercial mortgage loans | $ | 182,307 | $ | — | $ | 182,307 | $ | 363,971 | $ | — | $ | — | ||||||||||||

Real estate securities | 37,734 | — | 37,734 | 50,376 | 68 | — | ||||||||||||||||||

As of December 31, 2014 | ||||||||||||||||||||||||

Commercial mortgage loans | 150,169 | — | 150,169 | 301,704 | — | — | ||||||||||||||||||

Real estate securities | 26,269 | — | 26,269 | 38,834 | 68 | — | ||||||||||||||||||

Note 12 - Segment Reporting

The Company conducts its business through the following segments:

• | The real estate debt business focuses on originating, acquiring and asset managing commercial real estate debt investments, including first mortgage loans, subordinate mortgages, mezzanine loans and participations in such loans. |

• | The real estate securities business focuses on investing in and asset managing commercial real estate securities primarily consisting of CMBS and may include unsecured REIT debt, CDO notes and other securities. |

20

REALTY FINANCE TRUST, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2015

(Unaudited)

The following table represents the Company's operations by segment for the three months ended March 31, 2015 and 2014 (in thousands):

Three Months Ended March 31, 2015 | Total | Real Estate Debt | Real Estate Securities | |||||||||

Interest income | $ | 9,605 | $ | 9,196 | $ | 409 | ||||||

Interest expense | 1,933 | 1,804 | 129 | |||||||||

Net income | 4,632 | 4,546 | 86 | |||||||||

Total assets | 641,971 | 582,976 | 58,995 | |||||||||

Three Months Ended March 31, 2014 | ||||||||||||

Interest income | 977 | 940 | 37 | |||||||||

Interest expense | 21 | 9 | 12 | |||||||||

Net income (loss) | 226 | 349 | (123 | ) | ||||||||

Total assets | 71,431 | 56,913 | 14,518 | |||||||||

For the purposes of the table above, any expenses unallocable to specific segments have been allocated to the business segments using a percentage derived by using the sum of commercial mortgage loans, net and real estate securities, at fair value as the denominator and commercial mortgage loans, net and real estate securities, at fair value as the numerators.

Note 13 - Subsequent Events

The Company has evaluated subsequent events through the filing of this Quarterly Report on Form 10-Q and determined that there have not been any events that have occurred that would require adjustments to disclosures in the condensed consolidated financial statements except for the following transactions:

Sales of Common Stock

As of April 30, 2015, the Company had 21,214,570 shares of common stock outstanding, including shares issued under the DRIP and unvested restricted shares and has raised total proceeds from the Offering of $526.7 million. As of April 30, 2015, the aggregate value of all share issuances in the Offering was $529.8 million based on a per share value of $25.00 (or $23.75 per share for shares issued under the DRIP).

Total capital raised through April 30, 2015, including shares issued under the DRIP and unvested restricted shares, is as follows (in thousands):

Source of Capital | Inception to March 31, 2015 | April 1, 2015 to April 30, 2015 | Total | |||||||||

Common stock | $ | 482,202 | $ | 44,479 | $ | 526,681 | ||||||

Distributions Paid

On April 1, 2015, the Company paid a distribution of $3.3 million to stockholders of record during the month of March 2015. Approximately $1.9 million of the distribution was paid in cash, while $1.4 million was used to purchase 58,714 shares for those stockholders that chose to reinvest distributions through the DRIP.

Commercial Mortgage Loans

For the period from April 1, 2015 to April 30, 2015 the Company has originated and acquired commercial mortgage loans and CMBS with a total par value of $53.3 million and $18.0 million, respectively.

21

Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations

The following discussion should be read in conjunction with the accompanying condensed consolidated financial statements of Realty Finance Trust, Inc. the notes thereto and other financial information included elsewhere in this Quarterly Report on Form 10-Q as well as our Annual Report on Form 10-K for the fiscal year ended December 31, 2014 filed with the U.S. Securities and Exchange Commission ("the "SEC") on April 24, 2015, as amended by the Form 10-K/A filed with the SEC on April 29, 2015.