Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - UNITIL CORP | d924068d8k.htm |

American Gas Association

Financial Forum

May 2015

Exhibit 99.1 |

1

Safe Harbor Provision

This

presentation

contains

“forward-looking

statements”

made

pursuant

to

the

safe

harbor

provisions of the Private Securities Litigation Reform Act of 1995. These

forward-looking statements include statements regarding Unitil

Corporation’s (“Unitil”) financial condition, results of

operations, capital expenditures, business strategy, regulatory strategy, market opportunities,

and other plans and objectives. In some cases, forward-looking statements

can be identified by terminology such as “may,”

“will,”

“should,”

“expects,”

“plans,”

“anticipates,”

“believes,”

“estimates,”

“predicts,”

“potential”

or “continue”, the negative of such terms, or other comparable

terminology.

These forward-looking statements are neither promises nor guarantees, but

involve risks and uncertainties that could cause the actual results to

differ materially from those set forth in the forward-looking

statements. Those risks and uncertainties include: Unitil’s regulatory

environment (including regulations relating to climate change, greenhouse gas

emissions and other environmental matters); fluctuations in the supply of,

demand for, and the prices of energy commodities and transmission capacity

and Unitil’s ability to recover energy commodity costs in its rates;

customers’ preferred energy sources; severe storms and Unitil’s

ability to recover storm costs in its rates; general economic conditions;

variations in weather; long-term global climate change; Unitil’s

ability to retain its existing customers and attract new customers; Unitil’s

energy brokering customers’

performance and energy used under multi-year energy brokering

contracts; increased competition; integrity and security of operational and

information systems; publicity and reputational risks; and other risks

detailed in Unitil's filings with the Securities and Exchange

Commission,

including

those

appearing

under

the

caption

"Risk

Factors"

in

Unitil's

Annual Report on Form 10-K for the year ended December 31, 2014.

Readers should not place undue reliance on any forward looking statements, which

speak only as of the date they are made. Unitil undertakes no

obligation to update any forward- looking statements to reflect any

change in Unitil’s expectations or in events, conditions, or

circumstances

on

which

any

such

statements

may

be

based,

or

that

may

affect

the

likelihood

that actual results will differ from those set forth in the forward-looking

statements. |

2

Unitil Overview

Unitil Service Areas

•

Natural gas and electric utility with

operations in Maine, New Hampshire

and Massachusetts

•

Serving approximately 181,000 gas

and electric customers

•

Utility operations sales margin split

55% gas and 45% electric

•

Regulated T&D utility business model

•

Growing operations and customers

•

Regulated electric and gas rate base

growth

•

Robust natural gas system

expansion

•

Constructive rate plans and cost

trackers

•

Attractive dividend yield

•

Experienced management team |

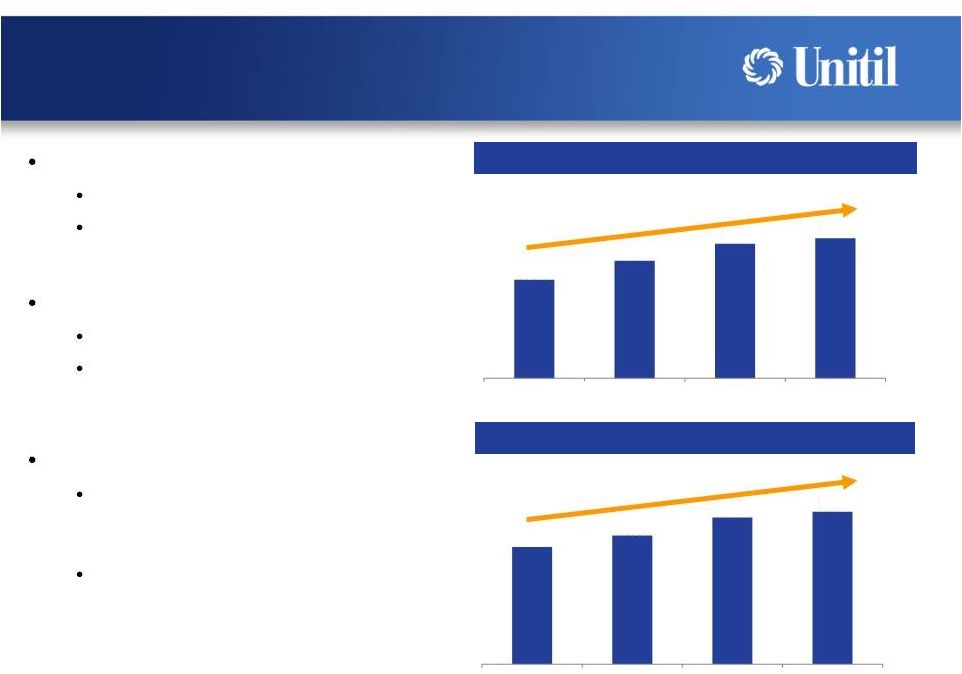

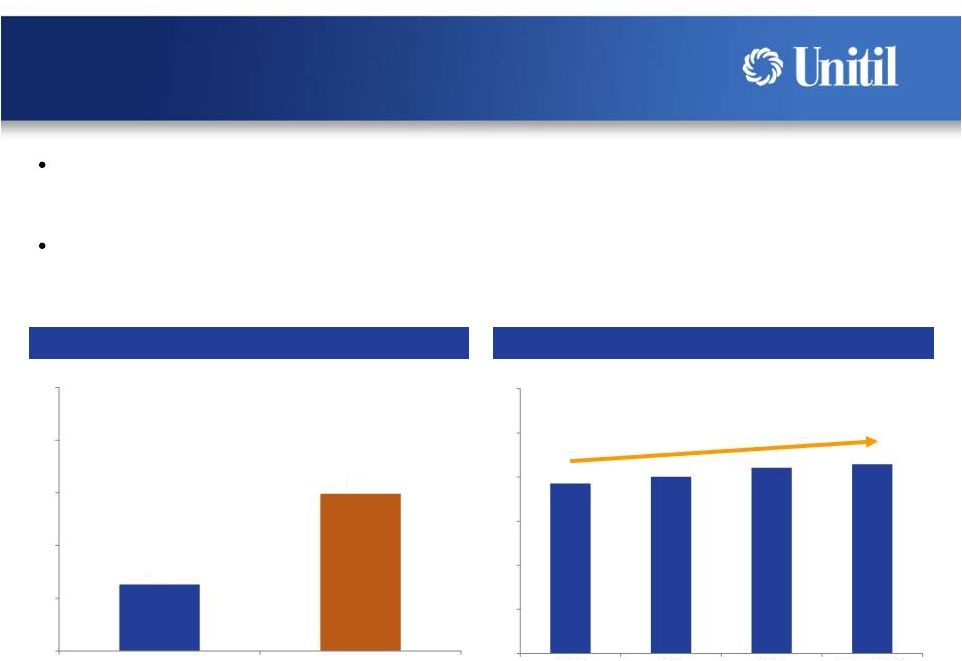

Generating Financial Results

3

Net Income

17% CAGR

($ in millions)

Earnings Per Share

12% CAGR

Robust business fundamentals

Improving economy

Strong demand for natural gas

Utility rate base growth

Significant gas growth potential

Infrastructure replacement and

upgrade projects

Constructive regulation

Rate relief has provided ~50%

increase to sales margin since

2010

High fixed component of rates

and decoupling reduces weather

volatility to earnings

$18.1

$21.6

$24.7

$25.7

2012

2013

2014

LTM Q1 2015

$1.43

$1.57

$1.79

$1.86

2012

2013

2014

LTM Q1 2015 |

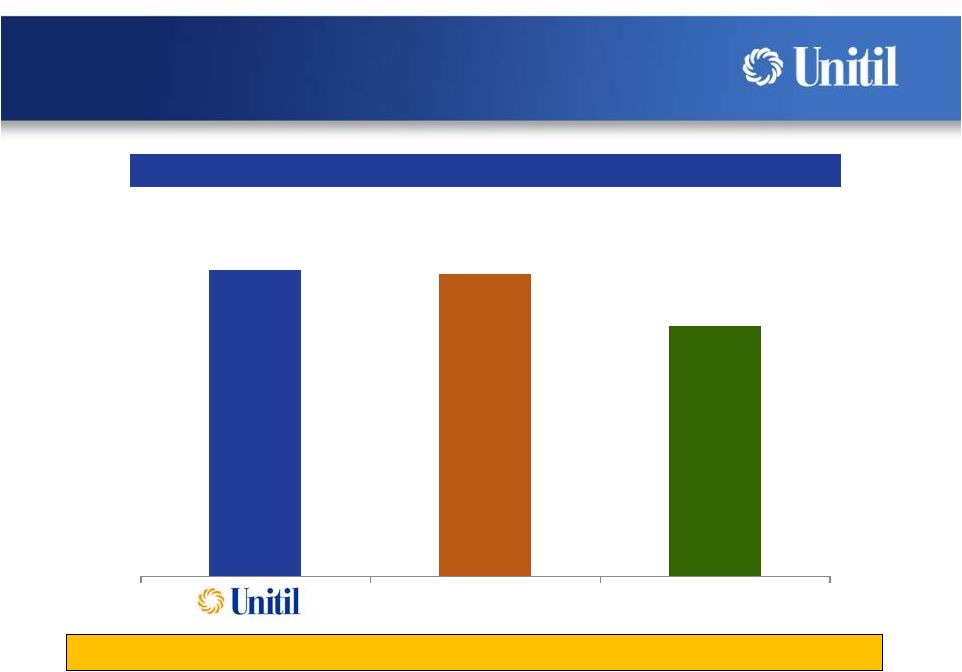

5-Year Total Shareholder Return (2010 -

2014)

Market Performance

4

Unitil 5-year total return of 106% versus 105% for S&P 500 and 87% for

S&P Utility 106%

105%

87%

S&P 500

S&P Utility Index |

Approximately 100+ years of domestic natural gas supply

U.S. Shale Plays

Domestic Natural Resources

5 |

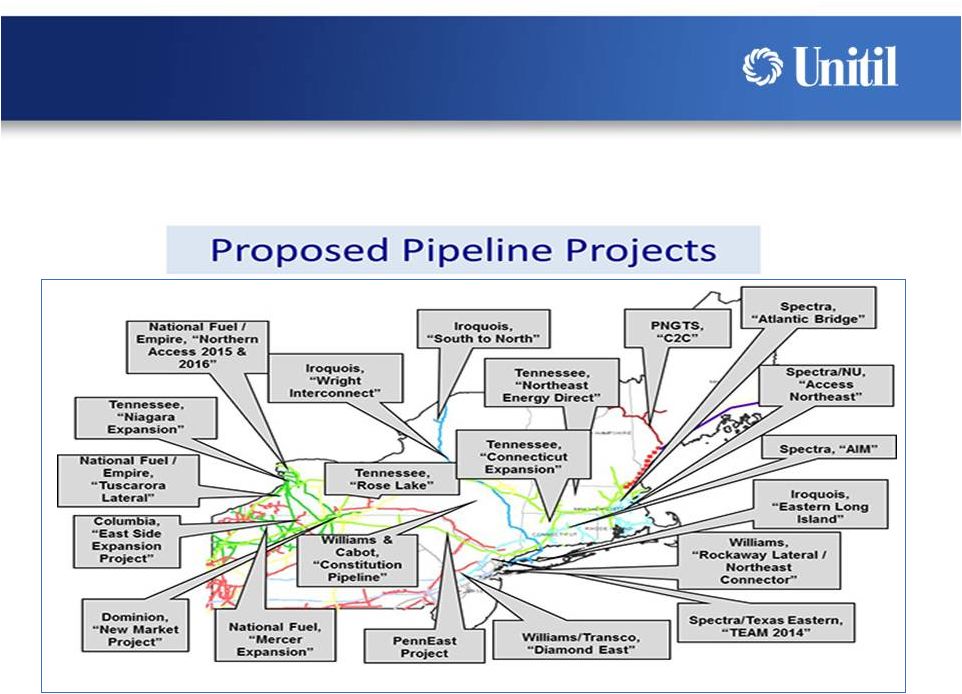

•

Numerous pipeline projects are in development to expand the Northeast pipeline

system, to transport supplies from the Marcellus and Utica shale gas

basins 6

Proposed Northeast

Natural Gas Pipeline Projects

Prepared by Northeast Gas Association based on publicly available information

(2014). Locations approximate. |

Gas

Growth Potential 7

•

The increasing demand for natural gas in

our service areas provides favorable

conditions for growth

•

Only 60% penetration on existing distribution

system means more room to grow

•

Expansion in adjacent service areas provides

new opportunities for growth each year

•

Convenient, clean, efficient and low cost

natural gas is attracting more and more

commercial and industrial high volume users

Current On-the-Main Penetration

77,900

(60%)

~50,000

(40%)

Current Customers

On-the-Main Prospects |

The

total

number

of

gas

customers

served

grew

3%

in

2014

–

triple

the

New

England peer group average growth

Weather-normalized gas unit sales have grown at a 5% annual rate since

2012

Customer Growth and Gas Sales

8

Gas Customer Growth

(therms, in millions)

Weather-Normalized Gas Sales

5% CAGR

1%

3%

0%

1%

2%

3%

4%

5%

New England Peers

Unitil

0

50

100

150

200

250

300

2012

2013

2014

LTM Q1 2015 |

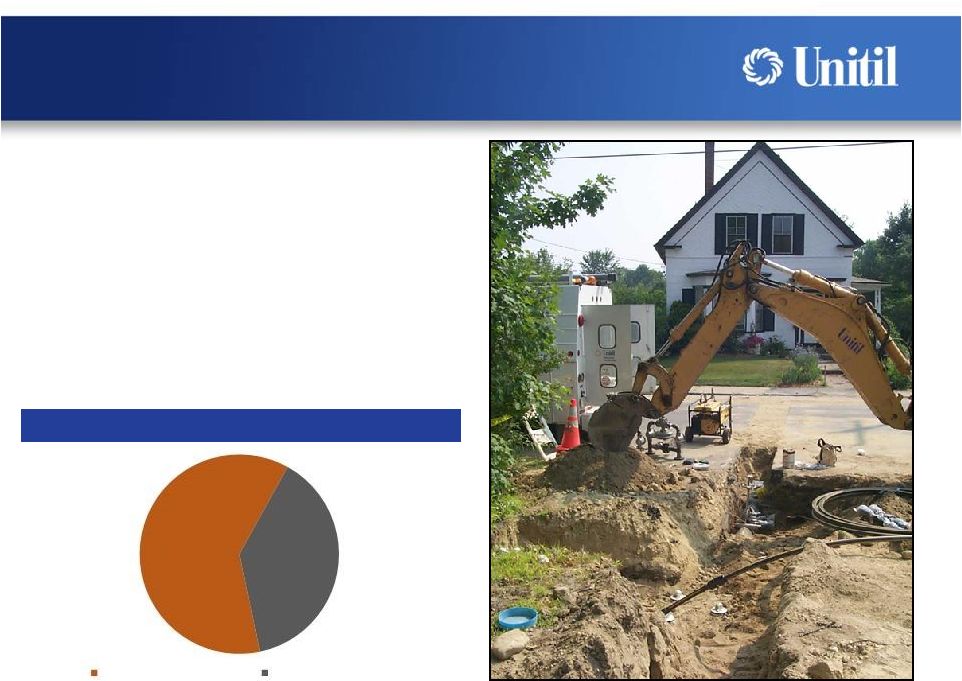

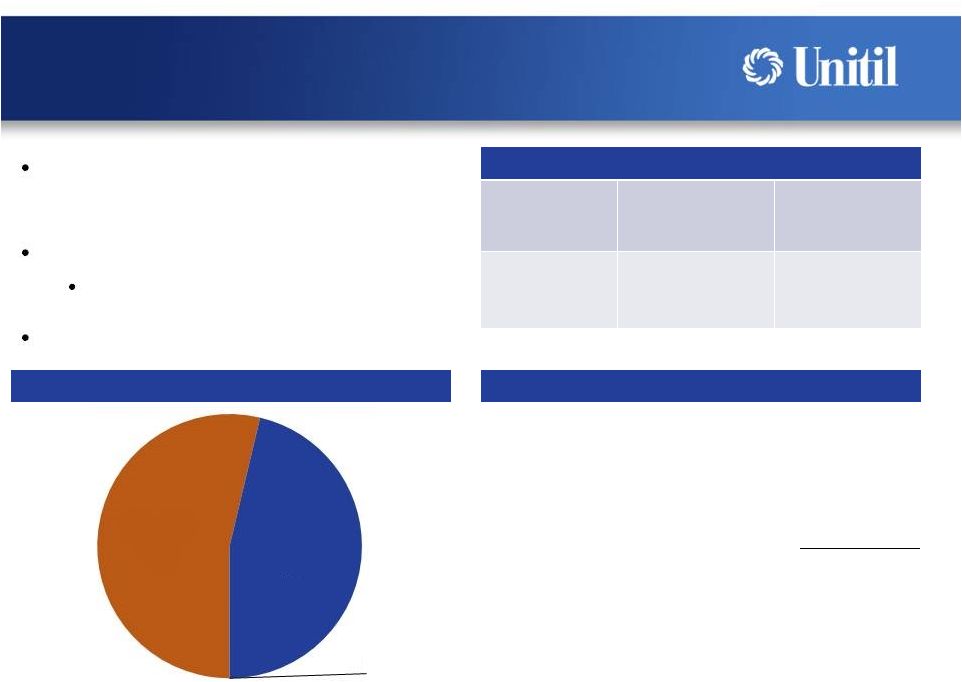

•

Recent rate design changes

have reduced weather volatility

•

25% of gas margin is fixed (i.e.

customer charge) which levels

customers bills throughout the

year

•

17% of gas margin is decoupled

–

margin is unaffected by

weather

2014 Gas Margin

9

Stability of Gas Margin

Fixed

25%

Decoupled

17%

Variable

58% |

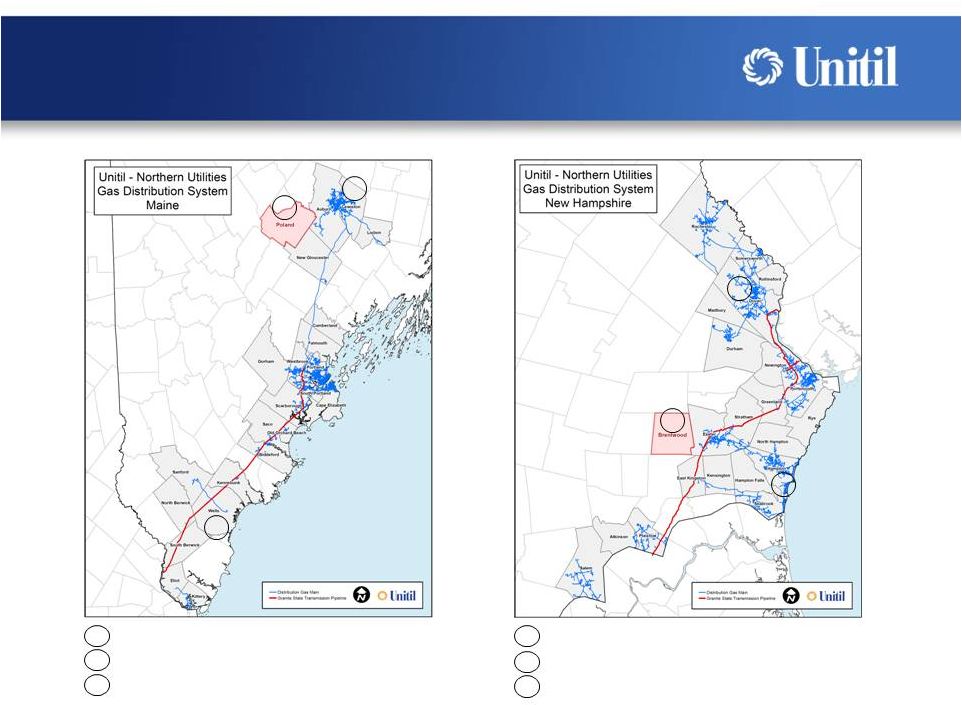

4

Brentwood New Service Area

5

Dover Extension

6

Hampton Extension

1

Poland New Service Area

2

Wells Extension

3

Lewiston Extension

10

New Service Area Expansion

1

2

3

4

5

6 |

0

4

8

12

16

20

2012

2013

2014

2015 F

2016 F

2017 F

ME

NH

MA

Infrastructure Replacement

11

Modern

gas

infrastructure

–

Approximately

70%

of

gas

mains

are

contemporary

materials

-

polyethylene plastic and protected steel

Replacing

~14

miles

of

remaining

older

leak

prone

mains

annually

across

all

three

states

to

achieve continuous improvement and modernization of entire natural gas delivery

system Cast Iron / Bare Steel Miles Replaced |

Electric Substation Projects

12

Construction of two major electric distribution

substations in New Hampshire began in 2014

Provides capacity to meet forecasted load growth

in New Hampshire

Enhances reliability and addresses capacity

constraints at existing substations

Kingston Project:

Kingston, NH (Seacoast Region)

Construction began 2014; in service 2016

Total cost of ~$12 million

Broken Ground Project:

Concord, NH (Capital Region)

Construction to begin 2015; in service 2017

Total cost of ~$11 million |

Capital Budget and Rate Base

13

($ in millions)

($ in millions)

Electric Rate Base

2015 Capital Budget $98 million

Gas Rate Base

3%

10%

($ in millions)

Total capital budget of $98 million

in 2015

Gas

–

$58

million

Electric

–

$31

million

Information

technology

–

$9

million

Gas rate base has grown at an

annual rate of 10% since 2009

Gas

Distribution

Expansion

$21

Electric

Distribution

Expansion

$14

Information

Technology

$9

Infrastructure

Replacement

$22

Gas & Electric

Other

Requirements

$32

$0

$75

$150

$225

$300

$375

2009

2010

2011

2012

2013

2014

$0

$75

$150

$225

$300

$375

2009

2010

2011

2012

2013

2014 |

14

Balanced Capital Structure

3/31/15 Liquidity

3/31/15 Capitalization

Standard and Poor’s corporate

rating of BBB+

Balanced capital structure

46% equity capitalization

Significant liquidity to fund growth

($ in millions)

Credit Facility Limit

120.0

$

Less: Current Balance

32.0

Liquidity

88.0

$

S&P Credit Rating

Unitil

Consolidated

Unitil Utility

Subsidiaries

Corporate

Rating

BBB+

BBB+

Long Term

Debt

54%

Common

Equity

46%

Preferred

Stock

<0.1% |

Sales and customer growth combined with constructive rate case results and

cost trackers continue to drive increases in return on equity

Constructive Regulation

15

Return on Equity

Achieved ~$60 million (~50% increase to sales margin) in rate relief since

2010 8.0%

8.2%

9.2%

9.2%

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

2012

2013

2014

LTM Q1 2015 |

16

Dividend Strength

Recently increased dividend in Q1 2015

Current quarterly dividend of $0.35 (annual dividend of

$1.40 per share)

Current dividend yield of ~4%

Since incorporation in 1984, Unitil has continuously paid

quarterly dividends and has never reduced its dividend

rate |

17

Key Investment Highlights

Regulated local distribution utility

business model

Diversified natural gas and electric sales

Growing operations and customer base

Regulated rate base growth

Robust natural gas system expansion

Constructive rate plans and cost trackers

Dividend strength

Experienced management team |