Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Western Refining, Inc. | Financial_Report.xls |

| EX-31.1 - EXHIBIT 31.1 - Western Refining, Inc. | exhibit311-wnrx33115.htm |

| EX-32.1 - EXHIBIT 32.1 - Western Refining, Inc. | exhibit321-wnrx33115.htm |

| EX-32.2 - EXHIBIT 32.2 - Western Refining, Inc. | exhibit322-wnrx33115.htm |

| EX-31.2 - EXHIBIT 31.2 - Western Refining, Inc. | exhibit312-wnrx33115.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the quarterly period ended March 31, 2015 | ||

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from _____ to _____ | ||

Commission File Number: 001-32721

WESTERN REFINING, INC.

(Exact name of registrant as specified in its charter)

Delaware | 20-3472415 | |

(State or other jurisdiction of | (I.R.S. Employer | |

incorporation or organization) | Identification No.) | |

123 W. Mills Ave., Suite 200 | 79901 | |

El Paso, Texas | (Zip Code) | |

(Address of principal executive offices) | ||

Registrant’s telephone number, including area code: (915) 534-1400

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

As of May 1, 2015, there were 95,517,605 shares outstanding, par value $0.01, of the registrant’s common stock.

WESTERN REFINING, INC. AND SUBSIDIARIES

INDEX

Item 1. Financial Statements (Unaudited) | |

EX-31.1 | |

EX-31.2 | |

EX-32.1 | |

EX-32.2 | |

EX-101 | |

Forward-Looking Statements

As provided by the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, certain statements included throughout this Quarterly Report on Form 10-Q and in particular under the section entitled Part I — Item 2, Management’s Discussion and Analysis of Financial Condition and Results of Operations relating to matters that are not historical fact should be deemed forward-looking statements that represent management’s beliefs and assumptions based on currently available information. These forward-looking statements relate to matters such as our industry, including the regulation of our industry, business strategy, future operations, our expectations for margins and crack spreads, the discount between West Texas Intermediate ("WTI") crude oil and Dated Brent crude oil as well as the discount between WTI Cushing and WTI Midland crude oils, volatility of crude oil prices, additions to pipeline capacity in the Permian Basin and at Cushing, Oklahoma, expected share repurchases and dividends, volatility in pricing of Renewable Identification Numbers ("RINs"), taxes, capital expenditures, liquidity and capital resources and other financial and operating information. Forward-looking statements also include those regarding the timing of completion of certain operational and maintenance improvements we are making at our refineries, future operational and refinery efficiencies and cost savings, timing of future maintenance turnarounds, the amount or sufficiency of future cash flows and earnings growth, future expenditures, future contributions related to pension and postretirement obligations, our ability to manage our inventory price exposure through commodity hedging instruments, the impact on our business of existing and future state and federal regulatory requirements, environmental loss contingency accruals, projected remediation costs or requirements and the expected outcomes of legal proceedings in which we are involved. We have used the words “anticipate,” “assume,” “believe,” “budget,” “continue,” “could,” “estimate,” “expect,” “forecast,” “intend,” “may,” “plan,” “position,” “potential,” “predict,” “project,” “strategy,” “will,” “future” and similar terms and phrases to identify forward-looking statements in this report.

Forward-looking statements reflect our current expectations regarding future events, results or outcomes. These expectations may or may not be realized. Some of these expectations may be based upon assumptions or judgments that prove to be incorrect or that are affected by unknown risks or uncertainties. Consequently, no forward-looking statements can be guaranteed. In addition, our business and operations involve numerous risks and uncertainties, many that are beyond our control, that could result in our expectations not being realized or otherwise materially affect our financial condition, results of operations and cash flows.

When considering these forward-looking statements, you should keep in mind the risk factors and other cautionary statements in this quarterly report on Form 10-Q. Actual events, results and outcomes may differ materially from our expectations due to a variety of factors. Although it is not possible to predict or identify all of these factors, they include, among others, the following:

• | changes in crack spreads; |

• | changes in the spread between WTI crude oil and West Texas Sour crude oil, also known as the sweet/sour spread; |

• | changes in the spread between WTI crude oil and Dated Brent crude oil and between WTI Cushing crude oil and WTI Midland crude oil; |

• | availability, costs and price volatility of crude oil, other refinery feedstocks and refined products; |

• | effects of and exposure to risks related to our commodity hedging strategies and transactions; |

• | availability and costs of renewable fuels for blending and RINs to meet Renewable Fuel Standards ("RFS") obligations; |

• | construction of new, or expansion of existing, product or crude oil pipelines, including in the Permian Basin, in the San Juan Basin and at Cushing, Oklahoma; |

• | changes in the underlying demand for our refined products; |

• | instability and volatility in the financial markets, including as a result of potential disruptions caused by economic uncertainties in Europe; |

• | a potential economic recession in the United States and/or abroad; |

• | adverse changes in the credit ratings assigned to our and our subsidiaries' debt instruments; |

• | changes in the availability and cost of capital; |

• | actions of customers and competitors; |

• | successful integration and future performance of acquired assets, businesses or third-party product supply and processing relationships; |

• | actions of third-party operators, processors and transporters; |

i

• | changes in fuel and utility costs incurred by our refineries; |

• | the effect of weather-related problems on our operations; |

• | disruptions due to equipment interruption, pipeline disruptions or failure at our or third-party facilities; |

• | execution of planned capital projects, cost overruns relating to those projects and failure to realize the expected benefits from those projects; |

• | effects of and costs relating to compliance with current and future local, state and federal environmental, economic, climate change, safety, tax and other laws, policies and regulations and enforcement initiatives; |

• | rulings, judgments or settlements in litigation, tax or other legal or regulatory matters, including unexpected environmental remediation costs in excess of any reserves or insurance coverage; |

• | the price, availability and acceptance of alternative fuels and alternative fuel vehicles; |

• | labor relations; |

• | operating hazards, natural disasters, casualty losses, acts of terrorism including cyber-attacks and other matters beyond our control; and |

• | other factors discussed in more detail under Part I — Item 1A. Risk Factors in our Annual Report on Form 10-K for the year ended December 31, 2014 ("2014 10‑K") that are incorporated herein by this reference. |

Any one of these factors or a combination of these factors could materially affect our financial condition, results of operations or cash flows and could influence whether any forward-looking statements ultimately prove to be accurate. You are urged to consider these factors carefully in evaluating any forward-looking statements and are cautioned not to place undue reliance on these forward-looking statements.

Although we believe the forward-looking statements we make in this report related to our plans, intentions and expectations are reasonable, we can provide no assurance that such plans, intentions or expectations will be achieved. These statements are based on assumptions made by us based on our experience and perception of historical trends, current conditions, expected future developments and other factors that we believe are appropriate in the circumstances. Such statements are subject to a number of risks and uncertainties, many of which are beyond our control. The forward-looking statements included herein are made only as of the date of this report and we are not required to (and will not) update any information to reflect events or circumstances that may occur after the date of this report, except as required by applicable law.

ii

Part I

Financial Information

Item 1. | Financial Statements |

WESTERN REFINING, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(Unaudited)

(In thousands, except share and per share data)

March 31, 2015 | December 31, 2014 | ||||||

ASSETS | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 463,074 | $ | 431,159 | |||

Accounts receivable, trade, net of a reserve for doubtful accounts of $547 and $484, respectively | 452,297 | 467,527 | |||||

Inventories | 673,088 | 629,237 | |||||

Prepaid expenses | 76,506 | 88,415 | |||||

Other current assets | 159,566 | 152,125 | |||||

Total current assets | 1,824,531 | 1,768,463 | |||||

Restricted cash | 123,609 | 167,009 | |||||

Equity method investment | 95,899 | 96,080 | |||||

Property, plant and equipment, net | 2,177,786 | 2,153,189 | |||||

Goodwill | 1,289,443 | 1,289,443 | |||||

Intangible assets, net | 85,261 | 85,952 | |||||

Other assets, net | 133,340 | 122,422 | |||||

Total assets | $ | 5,729,869 | $ | 5,682,558 | |||

LIABILITIES AND EQUITY | |||||||

Current liabilities: | |||||||

Accounts payable | $ | 592,332 | $ | 681,803 | |||

Accrued liabilities | 260,697 | 268,449 | |||||

Deferred income tax liability, net | 28,548 | 57,949 | |||||

Current portion of long-term debt | 5,500 | 5,500 | |||||

Total current liabilities | 887,077 | 1,013,701 | |||||

Long-term liabilities: | |||||||

Long-term debt, less current portion | 1,544,391 | 1,515,037 | |||||

Lease financing obligations | 46,266 | 27,489 | |||||

Deferred income tax liability, net | 331,250 | 296,860 | |||||

Other liabilities | 41,727 | 41,827 | |||||

Total long-term liabilities | 1,963,634 | 1,881,213 | |||||

Commitments and contingencies | |||||||

Equity: | |||||||

Western shareholders' equity: | |||||||

Common stock, par value $0.01, 240,000,000 shares authorized; 102,700,347 and 102,642,540 shares issued, respectively | 1,026 | 1,026 | |||||

Preferred stock, par value $0.01, 10,000,000 shares authorized; no shares issued or outstanding | — | — | |||||

Additional paid-in capital | 489,086 | 487,748 | |||||

Retained earnings | 967,744 | 890,393 | |||||

Accumulated other comprehensive loss, net of tax | (1,283 | ) | (1,291 | ) | |||

Treasury stock, 7,182,742 and 6,441,883 shares, respectively at cost | (283,168 | ) | (258,168 | ) | |||

Total Western shareholders' equity | 1,173,405 | 1,119,708 | |||||

Non-controlling interests | 1,705,753 | 1,667,936 | |||||

Total equity | 2,879,158 | 2,787,644 | |||||

Total liabilities and equity | $ | 5,729,869 | $ | 5,682,558 | |||

The accompanying notes are an integral part of these condensed consolidated financial statements.

1

WESTERN REFINING, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

(In thousands, except per share data)

Three Months Ended | |||||||

March 31, | |||||||

2015 | 2014 | ||||||

Net sales | $ | 2,318,730 | $ | 3,725,143 | |||

Operating costs and expenses: | |||||||

Cost of products sold (exclusive of depreciation and amortization) | 1,741,310 | 3,160,737 | |||||

Direct operating expenses (exclusive of depreciation and amortization) | 215,311 | 198,349 | |||||

Selling, general and administrative expenses | 55,803 | 58,732 | |||||

Affiliate severance costs | — | 9,399 | |||||

Loss on disposal of assets, net | 282 | 886 | |||||

Maintenance turnaround expense | 105 | 46,446 | |||||

Depreciation and amortization | 49,926 | 46,410 | |||||

Total operating costs and expenses | 2,062,737 | 3,520,959 | |||||

Operating income | 255,993 | 204,184 | |||||

Other income (expense): | |||||||

Interest income | 163 | 195 | |||||

Interest expense and other financing costs | (24,957 | ) | (28,957 | ) | |||

Loss on extinguishment of debt | — | (8 | ) | ||||

Other, net | 3,206 | 1,482 | |||||

Income before income taxes | 234,405 | 176,896 | |||||

Provision for income taxes | (59,437 | ) | (49,199 | ) | |||

Net income | 174,968 | 127,697 | |||||

Less net income attributable to non-controlling interests | 68,979 | 42,151 | |||||

Net income attributable to Western Refining, Inc. | $ | 105,989 | $ | 85,546 | |||

Net earnings per share: | |||||||

Basic | $ | 1.11 | $ | 1.07 | |||

Diluted | 1.11 | 0.88 | |||||

Weighted average common shares outstanding: | |||||||

Basic | 95,567 | 79,729 | |||||

Diluted | 95,682 | 102,522 | |||||

Cash dividends declared per common share | $ | 0.30 | $ | 0.26 | |||

The accompanying notes are an integral part of these condensed consolidated financial statements.

2

WESTERN REFINING, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited)

(In thousands)

Three Months Ended | |||||||

March 31, | |||||||

2015 | 2014 | ||||||

Net income | $ | 174,968 | $ | 127,697 | |||

Other comprehensive income items: | |||||||

Benefit plans: | |||||||

Amortization of net prior service cost | — | 81 | |||||

Reclassification of loss to income | 13 | 5 | |||||

Other comprehensive income before tax | 13 | 86 | |||||

Income tax | (5 | ) | (2 | ) | |||

Other comprehensive income, net of tax | 8 | 84 | |||||

Comprehensive income | 174,976 | 127,781 | |||||

Less comprehensive income attributable to non-controlling interests | 68,979 | 42,201 | |||||

Comprehensive income attributable to Western Refining, Inc. | $ | 105,997 | $ | 85,580 | |||

The accompanying notes are an integral part of these condensed consolidated financial statements.

3

WESTERN REFINING, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

(In thousands)

Three Months Ended | |||||||

March 31, | |||||||

2015 | 2014 | ||||||

Cash flows from operating activities: | |||||||

Net income | $ | 174,968 | $ | 127,697 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 49,926 | 46,410 | |||||

Changes in fair value of commodity hedging instruments | 20,057 | (73,972 | ) | ||||

Reserve for doubtful accounts | (46 | ) | 258 | ||||

Amortization of loan fees and original issue discount | 1,515 | 6,020 | |||||

Loss on extinguishment of debt | — | 8 | |||||

Stock-based compensation expense | 4,010 | 8,812 | |||||

Deferred income taxes | 4,989 | 35,839 | |||||

Excess tax benefit from stock-based compensation | (337 | ) | (254 | ) | |||

Income from equity method investment | (3,619 | ) | (1,512 | ) | |||

Loss on disposal of assets, net | 282 | 886 | |||||

Changes in operating assets and liabilities: | |||||||

Accounts receivable | 19,016 | (33,413 | ) | ||||

Inventories | (43,851 | ) | (58,900 | ) | |||

Prepaid expenses | 11,909 | (22,369 | ) | ||||

Other assets | (33,451 | ) | 2,141 | ||||

Accounts payable and accrued liabilities | (99,041 | ) | 27,601 | ||||

Other long-term liabilities | (1,349 | ) | (1,220 | ) | |||

Net cash provided by operating activities | 104,978 | 64,032 | |||||

Cash flows from investing activities: | |||||||

Capital expenditures | (53,195 | ) | (50,598 | ) | |||

Decrease in restricted cash | 43,400 | — | |||||

Proceeds from the sale of assets | 624 | 149 | |||||

Net cash used in investing activities | (9,171 | ) | (50,449 | ) | |||

Cash flows from financing activities: | |||||||

Additions to long-term debt | 300,000 | — | |||||

Payments on long-term debt | (1,375 | ) | (1,680 | ) | |||

Payments on revolving credit facility | (269,000 | ) | — | ||||

Deferred financing costs | (6,551 | ) | — | ||||

Purchase of treasury stock | (25,000 | ) | — | ||||

Distribution to non-controlling interest holders | (33,665 | ) | (27,072 | ) | |||

Dividends paid | (28,638 | ) | (20,730 | ) | |||

Convertible debt redemption | — | (788 | ) | ||||

Excess tax benefit from stock-based compensation | 337 | 254 | |||||

Net cash used in financing activities | (63,892 | ) | (50,016 | ) | |||

Net increase (decrease) in cash and cash equivalents | 31,915 | (36,433 | ) | ||||

Cash and cash equivalents at beginning of period | 431,159 | 468,070 | |||||

Cash and cash equivalents at end of period | $ | 463,074 | $ | 431,637 | |||

The accompanying notes are an integral part of these condensed consolidated financial statements.

4

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. Organization

"Western," "we," "us," "our" and the "Company" refer to Western Refining, Inc. and, unless the context otherwise requires, our subsidiaries. Western Refining, Inc. was formed on September 16, 2005 as a holding company prior to our initial public offering and is incorporated in Delaware.

We produce refined products at three refineries: one in El Paso, Texas, one near Gallup, New Mexico and one in St. Paul Park, Minnesota. We sell refined products primarily in Arizona, Colorado, Minnesota, New Mexico, Wisconsin, West Texas, the Mid-Atlantic region and Mexico; and through bulk distribution terminals and wholesale marketing networks and we sell refined products through two retail networks with a total of 521 company-owned and franchised retail sites in the U.S.

At March 31, 2015, we owned a 38.4% limited partner interest, and 100% of the general partner that grants us control, of Northern Tier Energy LP ("NTI"). NTI owns and operates a refinery in St. Paul Park, Minnesota. NTI has a retail-marketing network of 260 convenience stores. NTI directly operates 165 of these stores and supports 95 stores through franchise agreements. NTI's primary areas of operation include Minnesota and Wisconsin.

At March 31, 2015, we owned a 66.1% limited partner interest in Western Refining Logistics, LP ("WNRL") and the public held a 33.9% limited partner interest. We control WNRL through our 100% ownership of the general partner of WNRL and our majority ownership of WNRL's limited partnership interests. We formed WNRL as a Delaware master limited partnership to own, operate, develop and acquire terminals, storage tanks, pipelines and other logistics assets and related businesses.

On October 15, 2014, in connection with a Contribution, Conveyance and Assumption Agreement (the "Contribution Agreement") dated September 25, 2014, we sold all of the outstanding limited liability company interests of Western Refining Wholesale, LLC ("WRW") to WNRL. The sale of WRW to WNRL was a reorganization of entities under common control. We have recast historical financial and operational data of WNRL, for all periods presented, to reflect the purchase and consolidation of WRW into WNRL. We refer to this transaction as the "Wholesale Acquisition."

We changed our reportable segments during the fourth quarter of 2014 due to changes in our organization. Our operations include four business segments: refining, NTI, WNRL and retail. See Note 3, Segment Information, for further discussion of our business segments.

2. Basis of Presentation and Significant Accounting Policies

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles ("GAAP") for interim consolidated financial information and with the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, these unaudited condensed consolidated financial statements do not include all of the information and footnotes required by GAAP for complete financial statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered necessary for a fair presentation have been included. Operating results for the three months ended March 31, 2015, are not necessarily indicative of the results that may be expected for the year ending December 31, 2015, or for any other period.

The Condensed Consolidated Balance Sheet at December 31, 2014, has been derived from the audited financial statements at that date but does not include all of the information and footnotes required by GAAP for complete financial statements. The accompanying condensed consolidated financial statements should be read in conjunction with the consolidated financial statements and notes thereto included in our Annual Report on Form 10-K for the year ended December 31, 2014.

The condensed consolidated financial statements include the accounts of Western Refining, Inc. and subsidiaries in which we have a controlling interest. We own a 38.4% limited partner interest in NTI and we own a 66.1% limited partner interest in WNRL. We own 100% of NTI's and WNRL's respective general partners. As the general partner of NTI and WNRL, we have the ability to direct the activities of NTI and WNRL that most significantly impact their respective economic performance.

Demand for gasoline is generally higher during the summer months than during the winter months. As a result, our operating results for the first and fourth calendar quarters are generally lower than those for the second and third calendar quarters of each year. During 2014 and continuing into 2015, the volatility in crude oil prices and refining margins contributed to the variability of our results of operations.

5

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Principles of Consolidation

The accompanying condensed consolidated financial statements include the accounts of Western and subsidiaries in which we have a controlling interest. All intercompany accounts and transactions have been eliminated for all periods presented. Investments in significant non-controlled entities are accounted for using the equity method.

We have reported non-controlling interests for NTI and WNRL of $1,705.8 million in our Condensed Consolidated Balance Sheet as of March 31, 2015. We have reported non-controlling interest for NTI and WNRL of $1,667.9 million in our Condensed Consolidated Balance Sheet as of December 31, 2014.

Use of Estimates

The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Recent Accounting Pronouncements

Effective January 1, 2015, we adopted the accounting and reporting requirements included in the Accounting Standards Codification ("ASC") for disposals when such disposal represents a strategic shift that will have a significant impact on the entity’s operations and financial results. These requirements have been applied prospectively. Our adoption of these changes effective January 1, 2015 had no impact on our financial position, results of operations or cash flows.

From time to time, new accounting pronouncements are issued by various standard setting bodies that may have an impact on our accounting and reporting. We are currently evaluating the effect that certain of these new accounting requirements may have on our accounting and related reporting and disclosures in our consolidated financial statements.

• | Recognition and reporting of revenues - the requirements were amended to remove inconsistencies in revenue requirements and to provide a more complete framework for addressing revenue issues across a broad range of industries and transaction types. The revised standard’s core principle is that a company should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. These provisions are effective January 1, 2017, and are to be applied retrospectively, with early adoption not permitted. |

• | Evaluation of going concern - management of an entity is required to evaluate whether there is substantial doubt about the entity’s ability to continue as a going concern and to provide related footnote disclosures. The new requirements will become effective for annual periods beginning after December 15, 2016, and interim periods thereafter with early application permitted. The changed requirements are intended to reduce diversity in the timing and content of footnote disclosures. |

• | Consolidation considerations - reporting entities are required to evaluate whether certain legal entities should be consolidated effective for interim and annual periods beginning after December 15, 2015. |

• | Presentation of debt issuance costs - debt issuance costs are presented as an offset to the related debt and will become effective for interim and annual periods beginning after December 15, 2015. |

3. Segment Information

We changed our reportable segments during the fourth quarter of 2014 due to changes in our organization. Assets transferred from Western in the Wholesale Acquisition were treated as a transfer of assets between entities under common control. Accordingly, the financial information for the affected reporting segments has been retrospectively adjusted to include or exclude the historical results of the transferred WRW assets for periods prior to the effective date of the transaction. The primary effects of this reporting reorganization were:

• | Other than unmanned fleet fueling ("cardlock") related activities and product sales activity in the Mid-Atlantic region, the wholesale segment was moved to WNRL; |

•Product sales activity in the Mid-Atlantic region was moved to the refining segment; and

•Cardlock related activities were moved to the retail segment.

Our operations are organized into four reportable segments based on manufacturing and marketing criteria, the nature of our products and services, our production processes and our types of customers. Our reportable segments are refining, NTI, WNRL and retail. A description of each segment's activities and principal products follows:

6

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

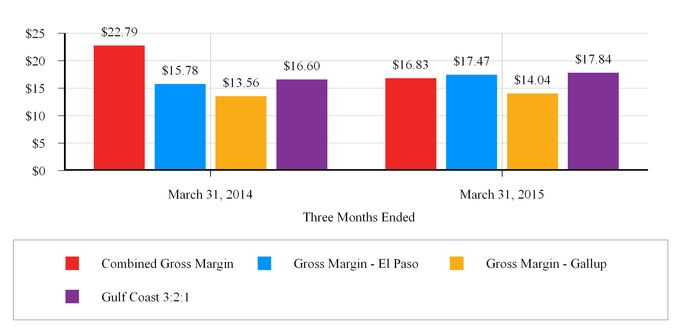

Refining. We report the operations of two refineries in our refining segment: one in El Paso, Texas (the "El Paso refinery") with a 131,000 barrel per day ("bpd") capacity and one near Gallup, New Mexico (the "Gallup refinery") with a 25,000 bpd capacity. Our refineries make various grades of gasoline, diesel fuel and other products from crude oil, other feedstocks and blending components. We purchase crude oil, other feedstocks and blending components from various third-party suppliers. We also acquire refined products through exchange agreements and from various third-party suppliers to supplement supply to our customers. We sell these products through WNRL's wholesale business and our retail business, other independent wholesalers and retailers, commercial accounts and sales and exchanges with major oil companies.

We have an exclusive supply and marketing agreement with a third party covering activities related to our refined product supply, sales and hedging in the Mid-Atlantic region. We recorded $0.3 million and $0.1 million in assets at March 31, 2015, and December 31, 2014, respectively, related to this supply agreement in our Condensed Consolidated Balance Sheets. The revenues and costs recorded under the supply agreement included $21.5 million and $0.1 million in net hedging gains for the three months ended March 31, 2015 and 2014, respectively.

NTI. NTI is an independent crude oil refiner and marketer of refined products with one 97,800 bpd refinery that also operates a network of retail convenience stores selling various grades of gasoline, diesel fuel and convenience store merchandise, primarily in Minnesota and Wisconsin. NTI's operations are separate from those of Western. At March 31, 2015, NTI included the operations of 165 retail convenience stores and supported 95 franchised retail convenience stores. These retail convenience stores are located primarily in Minnesota and Wisconsin. NTI's refinery supplies the majority of the gasoline and diesel fuel sold through its retail convenience stores.

WNRL. WNRL owns and operates certain logistics assets that consist of pipeline and gathering, terminalling, storage and transportation assets, providing related services primarily to our refining segment in the Southwest, including approximately 300 miles of pipelines and approximately 8.1 million barrels of active storage capacity. WNRL also owns a wholesale business that operates primarily in the Southwest. The majority of WNRL's logistics assets are integral to the operations of the El Paso and Gallup refineries. WNRL's wholesale business includes the operations of several lubricant and bulk petroleum distribution plants and a fleet of crude oil, refined product and lubricant delivery trucks. WNRL distributes commercial wholesale petroleum products primarily in Arizona, California, Colorado, Nevada, New Mexico and Texas. WNRL purchases petroleum fuels and lubricants from our refining segment and from third-party suppliers.

In the Wholesale Acquisition, WNRL purchased substantially all of Western’s southwest wholesale assets including assets and related inventories of WRW's lubricant distributions, southwest bulk petroleum fuels distribution, and crude oil and products transportation businesses.

Retail. Our retail segment located in the Southwest sells various grades of gasoline, diesel fuel, convenience store merchandise and beverage and food products to the general public through retail convenience stores and various grades of gasoline and diesel fuel to commercial vehicle fleets through cardlocks. WNRL supplies the majority of gasoline and diesel fuel that our retail segment sells. We purchase general merchandise and beverage and food products from various third-party suppliers. At March 31, 2015, the retail segment operated 261 service stations and convenience stores or kiosks located in Arizona, Colorado, New Mexico and Texas compared to 229 service stations and convenience stores or kiosks at March 31, 2014. The additional stores were added under various operating and capital leases. At March 31, 2015, the retail segment operated 50 cardlocks located in Arizona, California and New Mexico compared to 52 cardlocks at March 31, 2014.

Segment Accounting Principles. Operating income for each segment consists of net revenues less cost of products sold; direct operating expenses; selling, general and administrative expenses; net impact of the disposal of assets; maintenance turnaround expense and depreciation and amortization. Cost of products sold includes net realized and unrealized gains and losses related to our commodity hedging activities and reflects current costs adjusted, where appropriate, for "last-in, first-out" ("LIFO") and lower of cost or market ("LCM") inventory adjustments. Intersegment revenues are reported at prices that approximate market.

Activities of our business that are not included in the four segments mentioned above are included in the "Other" category. These activities consist primarily of corporate staff operations and other items that are not specific to the normal business of any one of our four operating segments. We do not allocate certain items of other income and expense, including income taxes, to the individual segments. NTI and WNRL are primarily pass-through entities with respect to income taxes.

The total assets of each segment consist primarily of cash and cash equivalents; inventories; net accounts receivable; net property, plant and equipment and other assets directly associated with the individual segment’s operations. Included in the total assets of the corporate operations are cash and cash equivalents; various net accounts receivable; prepaid expenses; other current assets; net deferred income tax items; net property, plant and equipment and other long-term assets.

7

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Disclosures regarding our reportable segments with reconciliations to consolidated totals for the three months ended March 31, 2015 and 2014, are presented below:

Three Months Ended March 31, 2015 | |||||||||||||||||||||||

Refining | NTI | WNRL | Retail | Other | Consolidated | ||||||||||||||||||

(In thousands) | |||||||||||||||||||||||

Net sales to external customers | $ | 948,899 | $ | 684,786 | $ | 429,147 | $ | 255,898 | $ | — | $ | 2,318,730 | |||||||||||

Intersegment sales (1) | 542,542 | 12,990 | 178,249 | 2,704 | — | ||||||||||||||||||

Operating income (loss) (2) | $ | 146,724 | $ | 107,987 | $ | 19,473 | $ | (441 | ) | $ | (17,750 | ) | $ | 255,993 | |||||||||

Other income (expense), net | (21,588 | ) | |||||||||||||||||||||

Income before income taxes | $ | 234,405 | |||||||||||||||||||||

Depreciation and amortization | $ | 21,638 | $ | 19,365 | $ | 4,738 | $ | 3,286 | $ | 899 | $ | 49,926 | |||||||||||

Capital expenditures | 35,908 | 6,673 | 7,914 | 1,402 | 1,298 | 53,195 | |||||||||||||||||

Goodwill at March 31, 2015 | — | 1,289,443 | — | — | — | 1,289,443 | |||||||||||||||||

Total assets at March 31, 2015 | 1,763,116 | 2,263,632 | 378,395 | 249,318 | 1,075,408 | 5,729,869 | |||||||||||||||||

(1) | Intersegment sales of $736.5 million have been eliminated in consolidation. |

(2) | The effect of our economic hedging activity is included within operating income of our refining and NTI segments as a component of cost of products sold. The cost of products sold within our refining segment includes $3.7 million in net realized and unrealized economic hedging losses. NTI cost of products sold includes $1.2 million in net realized and unrealized economic hedging gains. |

Three Months Ended March 31, 2014 | |||||||||||||||||||||||

Refining | NTI | WNRL (3) | Retail (3) | Other (3) | Consolidated | ||||||||||||||||||

(In thousands) | |||||||||||||||||||||||

Net sales to external customers | $ | 1,510,109 | $ | 1,256,394 | $ | 628,026 | $ | 330,371 | $ | 243 | $ | 3,725,143 | |||||||||||

Intersegment sales (1) | 815,705 | 984 | 236,584 | 4,913 | — | ||||||||||||||||||

Operating income (loss) (2) | $ | 139,007 | $ | 67,330 | $ | 16,761 | $ | (830 | ) | $ | (18,084 | ) | $ | 204,184 | |||||||||

Other income (expense), net | (27,288 | ) | |||||||||||||||||||||

Income before income taxes | $ | 176,896 | |||||||||||||||||||||

Depreciation and amortization | $ | 19,468 | $ | 18,985 | $ | 4,152 | $ | 2,935 | $ | 870 | $ | 46,410 | |||||||||||

Capital expenditures | 33,620 | 7,181 | 8,379 | 1,341 | 77 | 50,598 | |||||||||||||||||

Goodwill at March 31, 2014 | — | 1,297,043 | — | — | — | 1,297,043 | |||||||||||||||||

Total assets at March 31, 2014 | 1,807,484 | 2,949,498 | 397,887 | 207,293 | 268,569 | 5,630,731 | |||||||||||||||||

(1) | Intersegment sales of $1,058.2 million have been eliminated in consolidation. |

(2) | The effect of our economic hedging activity is included within operating income of our refining and NTI segments as a component of cost of products sold. The cost of products sold within our refining segment includes $90.6 million in net realized and unrealized economic hedging gains. NTI cost of products sold includes $0.9 million in net realized and unrealized economic hedging losses. |

(3) | WNRL's financial data includes the Predecessor's historical financial results and an allocated portion of corporate general and administrative expenses, previously reported as Other, for the three months ended March 31, 2014. Net sales to external customers and intersegment sales for our retail segment include the operating results of cardlock stations that were formerly recorded in our wholesale segment. Other operating results include activity of the wholesale fleet service department that was previously recorded within our wholesale segment. |

8

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

4. Fair Value Measurement

We utilize the market approach when measuring fair value of our financial assets and liabilities. The market approach uses prices and other relevant information generated by market transactions involving identical or comparable assets or liabilities.

The fair value hierarchy consists of the following three levels:

Level 1 | Inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities. |

Level 2 | Inputs are quoted prices for similar assets or liabilities in an active market, quoted prices for identical or similar assets or liabilities in markets that are not active, inputs other than quoted prices that are observable and market-corroborated inputs that are derived principally from or corroborated by observable market data. |

Level 3 | Inputs are derived from valuation techniques in which one or more significant inputs or value drivers are unobservable and cannot be corroborated by market data or other entity-specific inputs. |

The carrying amounts of cash and cash equivalents, which we consider Level 1 assets and liabilities, approximated their fair values at March 31, 2015 and December 31, 2014, due to their short-term maturities. Our fair value assessment incorporates a variety of considerations, including the short-term duration of the instruments and an evaluation of counterparty credit risk. Cash equivalents totaling $70.0 million, consisting of short-term money market deposits and commercial paper, were included in the Condensed Consolidated Balance Sheets as of March 31, 2015 and December 31, 2014, respectively.

We maintain cash deposits with various counterparties in support of our hedging and trading activities. These deposits are required by counterparties as collateral and cannot be offset against the fair value of open contracts except in the event of default. Certain of our commodity derivative contracts under master netting arrangements include both asset and liability positions. We have elected to offset the fair value amounts recognized for multiple similar derivative instruments executed with the same counterparty under the column "Netting Adjustments" below; however, fair value amounts by hierarchy level are presented on a gross basis in the tables below. See Note 13, Crude Oil and Refined Product Risk Management, for further discussion of master netting arrangements.

The following tables represent our assets and liabilities measured at fair value on a recurring basis as of March 31, 2015 and December 31, 2014 and the basis for that measurement:

Carrying Value at March 31, 2015 | Fair Value Measurement Using | Netting Adjustments | Net Fair Value at March 31, 2015 | ||||||||||||||||||||

Level 1 | Level 2 | Level 3 | |||||||||||||||||||||

(In thousands) | |||||||||||||||||||||||

Gross financial assets: | |||||||||||||||||||||||

Other current assets - commodity hedging contracts | $ | 81,813 | $ | — | $ | 80,794 | $ | 1,019 | $ | (7,200 | ) | $ | 74,613 | ||||||||||

Other assets - commodity hedging contracts | 41,103 | — | 40,412 | 691 | (1,689 | ) | 39,414 | ||||||||||||||||

Gross financial liabilities: | |||||||||||||||||||||||

Accrued liabilities - commodity hedging contracts | (9,573 | ) | — | (9,573 | ) | — | 7,200 | (2,373 | ) | ||||||||||||||

Other long-term liabilities - commodity hedging contracts | (3,435 | ) | — | (3,435 | ) | — | 1,689 | (1,746 | ) | ||||||||||||||

$ | 109,908 | $ | — | $ | 108,198 | $ | 1,710 | $ | — | $ | 109,908 | ||||||||||||

9

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Carrying Value at December 31, 2014 | Fair Value Measurement Using | Netting Adjustments | Net Fair Value at December 31, 2014 | ||||||||||||||||||||

Level 1 | Level 2 | Level 3 | |||||||||||||||||||||

(In thousands) | |||||||||||||||||||||||

Gross financial assets: | |||||||||||||||||||||||

Other current assets - commodity hedging contracts | $ | 86,659 | $ | — | $ | 86,329 | $ | 330 | $ | (6,937 | ) | $ | 79,722 | ||||||||||

Other assets - commodity hedging contracts | 58,182 | — | 58,182 | — | (1,649 | ) | 56,533 | ||||||||||||||||

Gross financial liabilities: | |||||||||||||||||||||||

Accrued liabilities - commodity hedging contracts | (11,826 | ) | — | (11,826 | ) | — | 6,937 | (4,889 | ) | ||||||||||||||

Other long-term liabilities - commodity hedging contracts | (3,049 | ) | — | (3,049 | ) | — | 1,649 | (1,400 | ) | ||||||||||||||

$ | 129,966 | $ | — | $ | 129,636 | $ | 330 | $ | — | $ | 129,966 | ||||||||||||

Commodity hedging contracts designated as Level 3 financial assets consist of jet fuel crack spread swaps. Ultra-low sulfur diesel ("ULSD") pricing has had a strong historical correlation to jet fuel crack spread swaps. We estimate the fair value of our Level 3 instruments based on the differential between quoted market settlement prices on ULSD futures and quoted market settlement prices on jet fuel futures for settlement dates corresponding to each of our outstanding Level 3 jet fuel crack spread swaps. As quoted prices for similar assets or liabilities in an active market are available, we reclassify the underlying financial asset or liability and designate them as Level 2 prior to final settlement.

Carrying amounts of commodity hedging contracts reflected as financial assets are included in both current and non-current other assets in the Condensed Consolidated Balance Sheets. Carrying amounts of commodity hedging contracts reflected as financial liabilities are included in both accrued and other long-term liabilities in the Condensed Consolidated Balance Sheets. Fair value adjustments referred to as credit valuation adjustments ("CVA") are included in the carrying amounts of commodity hedging contracts. CVAs are intended to adjust the fair value of counterparty contracts as a function of a counterparty's credit rating and reflect the credit quality of each counterparty to arrive at contract fair values.

The following table presents the changes in fair value of our Level 3 assets and liabilities (all related to commodity price swap contracts) for the three months ended March 31, 2015 and 2014.

Three Months Ended | |||||||

March 31, | |||||||

2015 | 2014 | ||||||

(In thousands) | |||||||

Asset (liability) balance at beginning of period | $ | 330 | $ | (1,935 | ) | ||

Change in fair value | — | 5,232 | |||||

Fair value of trades entered into during the period | 1,462 | — | |||||

Fair value reclassification from Level 3 to Level 2 | (82 | ) | (65 | ) | |||

Asset balance at end of period | $ | 1,710 | $ | 3,232 | |||

A hypothetical change of 10% to the estimated future cash flows attributable to our Level 3 commodity price swaps would result in a $0.2 million change in the estimated fair value.

10

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

As of March 31, 2015 and December 31, 2014, the carrying amount and estimated fair value of our debt was as follows:

March 31, 2015 | December 31, 2014 | ||||||

(In thousands) | |||||||

Western obligations: | |||||||

Carrying amount | $ | 893,125 | $ | 894,500 | |||

Fair value | 892,159 | 878,360 | |||||

NTI obligations: | |||||||

Carrying amount | $ | 356,766 | $ | 357,037 | |||

Fair value | 362,250 | 351,313 | |||||

WNRL obligations: | |||||||

Carrying amount | $ | 300,000 | $ | 269,000 | |||

Fair value | 309,000 | 269,000 | |||||

The carrying amount of our debt is the amount reflected in the Condensed Consolidated Balance Sheets, including the current portion. The fair value of the debt was determined using Level 2 inputs.

There have been no transfers between assets or liabilities whose fair value is determined through the use of quoted prices in active markets (Level 1) and those determined through the use of significant other observable inputs (Level 2).

5. Inventories

Inventories were as follows:

March 31, 2015 | December 31, 2014 | ||||||

(In thousands) | |||||||

Refined products (1) (2) | $ | 274,306 | $ | 257,476 | |||

Crude oil and other raw materials (2) | 343,194 | 318,565 | |||||

Lubricants | 14,855 | 14,265 | |||||

Retail store merchandise | 40,733 | 38,931 | |||||

Inventories | $ | 673,088 | $ | 629,237 | |||

(1) | Includes $17.7 million and $18.2 million of inventory valued using the first-in, first-out ("FIFO") valuation method at March 31, 2015, and December 31, 2014, respectively. |

(2) | At March 31, 2015, in order to state our inventories at market prices that were lower than our LIFO cost, we reduced the carrying value of our inventory through a non-cash LCM inventory adjustment of $62.8 million. At December 31, 2014, in order to state our inventories at market prices that were lower than our LIFO cost, we reduced the carrying value of our inventory through a non-cash LCM adjustment of $78.6 million. |

We value our refinery inventories of crude oil, other raw materials and asphalt inventories at the lower of cost or market under the LIFO valuation method. Other than refined products inventories held by WNRL and our retail segment, refined products inventories are valued under the LIFO valuation method. WNRL's wholesale refined product, lubricants and related inventories are determined using the FIFO inventory valuation method. Retail refined product inventory values are determined using the FIFO inventory valuation method. Retail merchandise inventory value is determined under the retail inventory method.

As of March 31, 2015, and December 31, 2014, refined products valued under the LIFO method and crude oil and other raw materials totaled 9.9 million barrels and 9.3 million barrels, respectively. At March 31, 2015 and December 31, 2014, the excess of the LIFO cost over the current cost of these crude oil, refined product and other feedstock and blendstock inventories was $142.0 million and $28.4 million, respectively.

11

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

During the three months ended March 31, 2015, cost of products sold included net non-cash credits of $113.6 million from changes in our LIFO reserves. During the three months ended March 31, 2014, cost of products sold included net non‑cash charges of $18.6 million from changes in our LIFO reserves.

Average LIFO cost per barrel of our refined products and crude oil and other raw materials inventories as of March 31, 2015, and December 31, 2014, was as follows:

March 31, 2015 | December 31, 2014 | ||||||||||||||||||||

Barrels | LIFO Cost | Average LIFO Cost Per Barrel | Barrels | LIFO Cost | Average LIFO Cost Per Barrel | ||||||||||||||||

(In thousands, except cost per barrel) | |||||||||||||||||||||

Refined products | 3,911 | $ | 289,942 | $ | 74.14 | 3,707 | $ | 283,333 | $ | 76.43 | |||||||||||

Crude oil and other | 5,971 | 372,698 | 62.42 | 5,577 | 355,470 | 63.74 | |||||||||||||||

9,882 | $ | 662,640 | 67.06 | 9,284 | $ | 638,803 | 68.81 | ||||||||||||||

6. Equity Method Investment

NTI owns a 17% common equity interest in Minnesota Pipe Line Company, LLC ("MPL"). The carrying value of this equity method investment was $95.9 million and $96.1 million at March 31, 2015 and December 31, 2014, respectively.

As of March 31, 2015 and December 31, 2014, the carrying amount of the equity method investment was $21.5 million and $21.6 million higher, respectively, than the underlying net assets of the investee. We are amortizing this difference over the remaining life of MPL’s primary asset (the fixed asset life of the pipeline).

During the three months ended March 31, 2015, we recognized $3.7 million in declared but unpaid distributions from MPL. There were no distributions received from MPL during the three months ended March 31, 2014. Equity income from MPL for the three months ended March 31, 2015, and 2014 was $3.6 million and $1.5 million, respectively. Equity income has been included in other, net in the accompanying Condensed Consolidated Statement of Operations.

7. Property, Plant and Equipment, Net

Property, plant and equipment, net was as follows:

March 31, 2015 | December 31, 2014 | ||||||

(In thousands) | |||||||

Refinery facilities and related equipment | $ | 2,229,195 | $ | 2,217,013 | |||

Pipelines, terminals and transportation equipment | 404,840 | 369,080 | |||||

Retail facilities and related equipment | 308,437 | 288,338 | |||||

Wholesale facilities and related equipment | 59,434 | 57,158 | |||||

Corporate | 49,464 | 48,871 | |||||

3,051,370 | 2,980,460 | ||||||

Accumulated depreciation | (873,584 | ) | (827,271 | ) | |||

Property, plant and equipment, net | $ | 2,177,786 | $ | 2,153,189 | |||

Depreciation expense was $48.9 million and $45.3 million for the three months ended March 31, 2015 and March 31, 2014, respectively.

12

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

8. Intangible Assets, Net

Intangible assets, net was as follows:

March 31, 2015 | December 31, 2014 | Weighted Average Amortization Period (Years) | |||||||||||||||||||||||

Gross Carrying Value | Accumulated Amortization | Net Carrying Value | Gross Carrying Value | Accumulated Amortization | Net Carrying Value | ||||||||||||||||||||

(In thousands) | |||||||||||||||||||||||||

Amortizable assets: | |||||||||||||||||||||||||

Licenses and permits | $ | 20,427 | $ | (12,544 | ) | $ | 7,883 | $ | 20,427 | $ | (12,148 | ) | $ | 8,279 | 5.0 | ||||||||||

Customer relationships | 7,551 | (3,505 | ) | 4,046 | 7,551 | (3,366 | ) | 4,185 | 7.3 | ||||||||||||||||

Rights-of-way and other | 7,878 | (3,769 | ) | 4,109 | 7,878 | (3,613 | ) | 4,265 | 9.3 | ||||||||||||||||

35,856 | (19,818 | ) | 16,038 | 35,856 | (19,127 | ) | 16,729 | ||||||||||||||||||

Unamortizable assets: | |||||||||||||||||||||||||

Franchise rights and trademarks | 50,500 | — | 50,500 | 50,500 | — | 50,500 | |||||||||||||||||||

Liquor licenses | 18,723 | — | 18,723 | 18,723 | — | 18,723 | |||||||||||||||||||

Intangible assets, net | $ | 105,079 | $ | (19,818 | ) | $ | 85,261 | $ | 105,079 | $ | (19,127 | ) | $ | 85,952 | |||||||||||

Intangible asset amortization expense for the three months ended March 31, 2015, was $0.7 million based on estimated useful lives ranging from 1 to 23 years. Intangible asset amortization expense for the three months ended March 31, 2014 was $0.7 million based on estimated useful lives ranging from 5 to 23 years.

Estimated amortization expense for the indicated periods is as follows (in thousands):

Remainder of 2015 | $ | 1,973 | |

2016 | 2,620 | ||

2017 | 2,679 | ||

2018 | 2,678 | ||

2019 | 2,011 | ||

2020 | 1,066 | ||

13

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

9. Long-Term Debt

Long-term debt was as follows:

March 31, 2015 | December 31, 2014 | ||||||

(In thousands) | |||||||

Western obligations: | |||||||

Revolving Credit Facility due 2019 | $ | — | $ | — | |||

Term Loan Credit Facility due 2020 | 543,125 | 544,500 | |||||

6.25% Senior Unsecured Notes due 2021 | 350,000 | 350,000 | |||||

Total Western obligations | 893,125 | 894,500 | |||||

NTI obligations: | |||||||

Revolving Credit Facility due 2018 | — | — | |||||

7.125% Senior Secured Notes due 2020, net of unamortized premium of $6,766 and $7,037, respectively | 356,766 | 357,037 | |||||

Total NTI obligations | 356,766 | 357,037 | |||||

WNRL obligations: | |||||||

Revolving Credit Facility due 2018 | — | 269,000 | |||||

7.5% Senior Notes due 2023 | 300,000 | — | |||||

Total WNRL obligations | 300,000 | 269,000 | |||||

Long-term debt | 1,549,891 | 1,520,537 | |||||

Current portion of long-term debt | (5,500 | ) | (5,500 | ) | |||

Long-term debt, net of current portion | $ | 1,544,391 | $ | 1,515,037 | |||

As of March 31, 2015, annual maturities of long-term debt for the remainder of 2015 are $4.1 million. From 2016 through 2019, long-term debt maturities are $5.5 million. Thereafter, total long-term debt maturities are $1,517.0 million.

Interest expense and other financing costs were as follows:

Three Months Ended | |||||||

March 31, | |||||||

2015 | 2014 | ||||||

(In thousands) | |||||||

Contractual interest: | |||||||

Western obligations | $ | 12,007 | $ | 15,267 | |||

NTI obligations | 6,591 | 5,335 | |||||

WNRL obligations | 3,726 | 225 | |||||

22,324 | 20,827 | ||||||

Amortization of loan fees | 1,786 | 2,097 | |||||

Amortization of original issuance discount | — | 4,044 | |||||

Other interest expense | 1,075 | 2,205 | |||||

Capitalized interest | (228 | ) | (216 | ) | |||

Interest expense and other financing costs | $ | 24,957 | $ | 28,957 | |||

We amortize original issue discounts and financing fees using the effective interest method over the respective term of the debt. Our creditors have no recourse to the assets owned by either of NTI or WNRL, and the creditors of NTI and WNRL have no recourse to our assets or those of our other subsidiaries.

14

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Western Obligations

Revolving Credit Facility

On October 2, 2014, we entered into the Third Amended and Restated Revolving Credit Agreement ("Western 2019 Revolving Credit Facility"). Lenders committed $900.0 million, all of which will mature on October 2, 2019. The commitments under the Western 2019 Revolving Credit Facility may be increased in the future to $1.4 billion, subject to certain conditions (including the agreement of financial institutions, in their sole discretion, to provide such additional commitments). The amended terms of the agreement include revised borrowing rates. Borrowings can be either base rate loans plus a margin ranging from 0.50% to 1.00% or LIBOR loans plus a margin ranging from 1.50% to 2.00%, subject to adjustment based upon the average excess availability. The Western 2019 Revolving Credit Facility also provides for a quarterly commitment fee ranging from 0.25% to 0.375% per annum, subject to adjustment based upon the average utilization ratio, and letter of credit fees ranging from 1.50% to 2.00% per annum payable quarterly, subject to adjustment based upon the average excess availability. Borrowing availability under the Western 2019 Revolving Credit Facility is tied to the amount of our and our restricted subsidiaries' eligible accounts receivable and inventory. The Western 2019 Revolving Credit Facility is guaranteed, on a joint and several basis, by certain of our subsidiaries and will be guaranteed by certain newly acquired or formed subsidiaries, subject to certain limited exceptions. The Western 2019 Revolving Credit Facility is secured by our cash and cash equivalents, accounts receivable and inventory. The Western 2019 Revolving Credit Facility contains certain covenants, including but not limited to, limitations on debt, investments, and dividends and the maintenance of a minimum fixed charge coverage ratio in certain circumstances.

As of and during the three month period ended March 31, 2015, we had no direct borrowings under the Western 2019 Revolving Credit Facility, with availability of $358.4 million. This availability is net of $67.0 million in outstanding letters of credit.

Term Loan Credit Agreement

On November 12, 2013, we entered into a term loan credit agreement (the "Western 2020 Term Loan Credit Facility"). The Western 2020 Term Loan Credit Facility provides for loans of $550.0 million, matures on November 12, 2020 and provides for quarterly principal payments of $1.4 million until September 30, 2020, with the remaining balance then outstanding due on the maturity date. The Western 2020 Term Loan Credit Facility bears interest at a rate based either on the base rate (as defined in the Western 2020 Term Loan Credit Facility) plus 2.25% or the Eurodollar Rate (as defined in the Western 2020 Term Loan Credit Facility) plus 3.25% (with a Eurodollar Rate floor of 1.00%). The Western 2020 Term Loan Credit Facility is secured by both the El Paso and Gallup refineries and is fully and unconditionally guaranteed on a joint and several basis by substantially all of Western's material subsidiaries. The Western 2020 Term Loan Credit Facility contains customary restrictive covenants including limitations of debt, investments and dividends, and does not contain any financial maintenance covenants.

6.25% Senior Unsecured Notes

On March 25, 2013, we entered into an indenture (the "Western 2021 Indenture") for the issuance of $350.0 million in aggregate principal amount of 6.25% Senior Unsecured Notes due 2021 (the "Western 2021 Senior Unsecured Notes"). The Western 2021 Senior Unsecured Notes are guaranteed on a senior unsecured basis by each of our wholly-owned domestic restricted subsidiaries. We pay interest on the Western 2021 Senior Unsecured Notes semi-annually in arrears on April 1 and October 1 of each year. The Western 2021 Senior Unsecured Notes mature on April 1, 2021.

5.75% Convertible Senior Unsecured Notes

On March 7, 2014, we provided notice to the Trustee and the holders (the “Noteholders”) of our 5.75% Convertible Senior Unsecured Notes (the "Western Convertible Notes") informing the Trustee and the Noteholders of our election, with respect to all conversions requested by Noteholders in accordance with the terms of the Indenture received by the conversion agent on or after March 20, 2014, to settle conversions of the Western Convertible Notes through the issuance of shares of our common stock. On various dates between March 26, 2014, and June 2, 2014, we delivered an aggregate of 9,155 shares of common stock to Noteholders to satisfy the conversion of $87,000 aggregate principal amount of Western Convertible Notes based on conversion rates, dependent on conversion date, of 105.2394 or 105.8731 shares of common stock for each $1,000 of principal amount of Western Convertible Notes converted. On June 16, 2014, we delivered 22,750,088 shares of common stock to Noteholders, to satisfy the conversion of $214,881,000 aggregate principal amount of Western Convertible Notes, based on a conversion rate of 105.8731 shares of common stock for each $1,000 of principal amount of Western Convertible Notes converted.

In addition to these conversions, we paid cash for the remainder of the outstanding amount of the Western Convertible Notes with a nominal loss on extinguishment of debt.

15

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Our payment of dividends is limited under the terms of our Revolving Credit Agreement, our Senior Unsecured Notes and our Term Loan Credit Facility, and in part, depends on our ability to satisfy certain financial covenants. Note guarantors will be released if they cease to be a Restricted Subsidiary as the result of a transaction permitted under the terms of the indenture, including through the disposition of capital stock of the guarantor.

NTI Obligations

Revolving Credit Facility

On September 29, 2014, NTI amended its senior secured Revolving Credit Facility (the "NTI Revolving Credit Facility"), increasing the aggregate principal amount available prior to the amendment from $300.0 million to $500.0 million. The NTI Revolving Credit Facility, which matures on September 29, 2019, incorporates a borrowing base tied to eligible accounts receivable and inventory and provides for up to $500.0 million for the issuance of letters of credit and up to $45.0 million for swing line loans. The NTI Revolving Credit Facility may be increased up to a maximum aggregate principal amount of $750.0 million, subject to certain conditions. Obligations under the NTI Revolving Credit Facility are secured by substantially all of NTI’s assets. Indebtedness under the NTI Revolving Credit Facility is recourse to Northern Tier Energy GP LLC, its general partner, and is guaranteed by NTI and certain of its subsidiaries. Borrowings under the NTI Revolving Credit Facility bear interest at either (a) an alternative base rate plus an applicable margin (ranging between 0.50% and 1.00%) or (b) a LIBOR rate plus an applicable margin (ranging between 1.50% and 2.00%), in each case based upon the average excess availability. In addition to paying interest on outstanding borrowings, NTI is also required to pay quarterly commitment fees ranging from 0.250% to 0.375% and letter of credit fees ranging from 1.50% to 2.00%. The NTI Revolving Credit Facility contains certain covenants, including but not limited to, limitations on debt, investments and dividends and the maintenance of a minimum fixed charge coverage ratio in certain circumstances. NTI incurred financing costs of $2.6 million associated with the amended NTI Revolving Credit Facility.

As of March 31, 2015, the availability under the NTI Revolving Credit Facility was $194.6 million. This availability is net of $32.0 million in outstanding letters of credit. There were no borrowings under the NTI Revolving Credit Facility during the three month period ended March 31, 2015.

7.125% Secured Notes

On November 8, 2012, Northern Tier Energy LLC, its wholly owned subsidiary ("NTI LLC"), and Northern Tier Finance Corporation issued $275.0 million in aggregate principal amount of 7.125% senior secured notes due 2020 (the "NTI 2020 Secured Notes").

NTI increased the principal amount of the NTI 2020 Secured Notes in September 2014 through issuance of a private placement of an additional $75.0 million in principal value. This offering was issued under the same indenture and under the same terms as the existing NTI 2020 Secured Notes. The offering generated total cash proceeds of $79.2 million including an issuance premium of $4.2 million. NTI incurred financing costs of $2.5 million associated with this offering. The issuance premium and financing costs will be amortized to interest expense over the remaining life of the notes.

The obligations under the NTI 2020 Secured Notes are fully and unconditionally guaranteed, jointly and severally, on a senior unsecured basis by Northern Tier Energy LP and on a senior secured basis by (i) all of NTI LLC’s restricted subsidiaries that borrow, or guarantee obligations, under the NTI Revolving Credit Facility or any other indebtedness of NTI LLC or another subsidiary of NTI LLC that guarantees the NTI 2020 Secured Notes and (ii) all other material wholly owned domestic subsidiaries of NTI LLC. The indenture governing the NTI 2020 Secured Notes contains covenants that limit or restrict dividends or other payments from restricted subsidiaries. Indebtedness under the NTI 2020 Secured Notes is guaranteed by NTI and certain of their subsidiaries.

16

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

WNRL Obligations

Revolving Credit Facility

On October 16, 2013, WNRL entered into a $300.0 million senior secured revolving credit facility ("WNRL Revolving Credit Facility"). WNRL has the ability to increase the total commitment of the WNRL Revolving Credit Facility by up to $200.0 million for a total facility size of up to $500.0 million, subject to certain conditions. The WNRL Revolving Credit Facility includes a $25.0 million sub-limit for standby letters of credit and a $10.0 million sub-limit for swing line loans. Obligations under the WNRL Revolving Credit Facility and certain cash management and hedging obligations are guaranteed by all of WNRL's subsidiaries. Obligations under the WNRL Revolving Credit Facility are secured by a first priority lien on substantially all of WNRL's and its subsidiaries' significant assets. WNRL creditors under the WNRL Revolving Credit Facility have no recourse to Western's assets, except to the extent of the assets of Western Refining Logistics GP, LLC, the general partner of WNRL that Western wholly owns. The WNRL Revolving Credit Facility will mature on October 16, 2018. Borrowings under the WNRL Revolving Credit Facility bear interest at either a base rate plus an applicable margin ranging from 0.75% to 1.75%, or at LIBOR plus an applicable margin ranging from 1.75% to 2.75%. The applicable margin will vary based upon WNRL's Consolidated Total Leverage Ratio, as defined in the WNRL Revolving Credit Facility.

During the three months ended March 31, 2015, WNRL repaid its outstanding direct borrowings under the WNRL Revolving Credit Facility with a portion of the proceeds from the issuance of its 7.5% Senior Notes, discussed below, resulting in no direct or swing line borrowings under the WNRL Revolving Credit Facility as of March 31, 2015. As of March 31, 2015, the availability under the WNRL Revolving Credit Facility was $299.3 million. This availability is net of $0.7 million in outstanding letters of credit.

The WNRL Revolving Credit Facility contains covenants that limit or restrict WNRL's ability to make cash distributions. WNRL is required to maintain certain financial ratios that are tested on a quarterly basis for the immediately preceding four quarter period.

7.5% Senior Notes

On February 11, 2015, WNRL entered into an indenture (the “WNRL Indenture”) among WNRL, WNRL Finance Corp., a Delaware corporation and wholly-owned subsidiary of WNRL (“Finance Corp.” and together with WNRL, the “Issuers”), the guarantors named therein and U.S. Bank National Association, as trustee under which the Issuers issued $300.0 million in aggregate principal amount of 7.5% Senior Notes due 2023 (the "WNRL 2023 Senior Notes"). WNRL will pay interest on the WNRL 2023 Senior Notes semi-annually in cash in arrears on February 15 and August 15 of each year, beginning on August 15, 2015. The WNRL 2023 Senior Notes will mature on February 15, 2023. WNRL used the proceeds from the notes to repay the full balance due under the WNRL Revolving Credit Facility on February 11, 2015.

The WNRL Indenture contains covenants that limit WNRL’s and its restricted subsidiaries’ ability to, among other things: (i) incur, assume or guarantee additional indebtedness or issue preferred units, (ii) create liens to secure indebtedness, (iii) pay distributions on equity securities, repurchase equity securities or redeem subordinated indebtedness, (iv) make investments, (v) effect distributions, loans or other asset transfers from WNRL’s restricted subsidiaries, (vi) consolidate with or merge with or into, or sell substantially all of WNRL’s properties to, another person, (vii) sell or otherwise dispose of assets, including equity interests in subsidiaries and (viii) enter into transactions with affiliates. These covenants are subject to a number of limitations and exceptions. The WNRL Indenture also provides for events of default, which, if any of them occurs, would permit or require the principal, premium, if any, and interest on all the then outstanding WNRL 2023 Senior Notes to be due and payable immediately.

17

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

10. Equity

Changes to equity during the three months ended March 31, 2015, were as follows:

Western Shareholders' Equity | Non-controlling Interest | Total Equity | |||||||||

(In thousands) | |||||||||||

Balance at December 31, 2014 | $ | 1,119,708 | $ | 1,667,936 | $ | 2,787,644 | |||||

Net income | 105,989 | 68,979 | 174,968 | ||||||||

Other comprehensive income, net of tax | 8 | — | 8 | ||||||||

Dividends | (28,638 | ) | — | (28,638 | ) | ||||||

Stock-based compensation | 1,001 | 2,503 | 3,504 | ||||||||

Excess tax benefit from stock-based compensation | 337 | — | 337 | ||||||||

Distributions to non-controlling interests | — | (33,665 | ) | (33,665 | ) | ||||||

Treasury stock purchases | (25,000 | ) | — | (25,000 | ) | ||||||

Balance at March 31, 2015 | $ | 1,173,405 | $ | 1,705,753 | $ | 2,879,158 | |||||

Changes to equity during the three months ended March 31, 2014, were as follows:

Western Shareholders' Equity | Non-controlling Interest | Total Equity | |||||||||

(In thousands) | |||||||||||

Balance at December 31, 2013 | $ | 894,052 | $ | 1,676,535 | $ | 2,570,587 | |||||

Net income | 85,546 | 42,151 | 127,697 | ||||||||

Convertible debt redemption | (807 | ) | — | (807 | ) | ||||||

Convertible debt settlement - treasury stock issuance in additional paid-in capital | 6 | — | 6 | ||||||||

Other comprehensive income, net of tax | 34 | 50 | 84 | ||||||||

Dividends | (20,730 | ) | — | (20,730 | ) | ||||||

Stock-based compensation | 1,151 | 7,661 | 8,812 | ||||||||

Excess tax benefit from stock-based compensation | 254 | — | 254 | ||||||||

Distributions to non-controlling interests | — | (27,072 | ) | (27,072 | ) | ||||||

Offering costs | — | 66 | 66 | ||||||||

Treasury stock issuance | 19 | — | 19 | ||||||||

Balance at March 31, 2014 | $ | 959,525 | $ | 1,699,391 | $ | 2,658,916 | |||||

Share Repurchase Programs

Since 2012, our board of directors has approved four separate share repurchase programs, authorizing us to repurchase up to $200 million, per program, of our outstanding common stock. Our board of directors approved our current share repurchase program in November of 2014 (the "November 2014 Program") that will expire in November of 2015.

Subject to market conditions as well as corporate, regulatory and other considerations, we will repurchase shares from time-to-time through open market transactions, block trades, privately negotiated transactions or otherwise. Our board of directors may discontinue the share repurchase program at any time.

18

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

The following table summarizes our share repurchase activity for the November 2014 Program:

Number of shares purchased | Cost of share purchases (In thousands) | |||||

Shares purchased at December 31, 2014 | 1,492,874 | $ | 59,222 | |||

Shares purchased during Q1, 2015 | 740,859 | 25,000 | ||||

Shares purchased at March 31, 2015 | 2,233,733 | $ | 84,222 | |||

As of March 31, 2015, we had $115.8 million remaining in authorized expenditures under the November 2014 Program.

Dividends

The table below summarizes our 2015 cash dividend declarations, payments and scheduled payments through May 1, 2015:

2015 | |||||||||||||

Declaration Date | Record Date | Payment Date | Dividend per Common Share | Total Payment (In thousands) | |||||||||

First quarter | February 6 | February 20 | March 6 | $ | 0.30 | $ | 28,638 | ||||||

Second quarter (1) | April 21 | May 5 | May 20 | 0.34 | — | ||||||||

Total | $ | 28,638 | |||||||||||

(1) The second quarter 2015 cash dividend of $0.34 per common share will result in an aggregate payment of approximately $32.5 million.

Total dividends declared were $0.30 and $0.26 per common share, including those declared related to participating securities, for the three months ended March 31, 2015 and 2014, respectively.

NTI Distributions

On February 5, 2015, NTI declared a quarterly cash distribution of $0.49 per unit for the period October 1, 2014 through December 31, 2014. NTI paid the distribution on February 27, 2015 to all unitholders of record on February 21, 2015.

The table below summarizes NTI's 2015 quarterly distribution declarations, payments and scheduled payments through May 1, 2015:

2015 | |||||||||

Declaration Date | Record Date | Payment Date | Distribution per Unit | ||||||

First quarter | May 5 | May 18 | May 29 | $ | 1.08 | ||||

Total | $ | 1.08 | |||||||

WNRL Distributions

On January 30, 2015, WNRL's general partner's board of directors declared a quarterly cash distribution of $0.3325 per unit for the period October 1, 2014 through December 31, 2014. WNRL paid the distribution on February 23, 2015 to all unitholders of record on February 13, 2015.

The table below summarizes WNRL's 2015 quarterly distribution declarations, payments and scheduled payments through May 1, 2015:

2015 | |||||||||

Declaration Date | Record Date | Payment Date | Distribution per Common and Subordinated Unit | ||||||

First quarter | May 1 | May 15 | May 26 | $ | 0.3475 | ||||

Total | $ | 0.3475 | |||||||

19

WESTERN REFINING, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

11. Income Taxes

Compared to the federal statutory rate of 35%, our effective tax rates for the three months ended March 31, 2015, and March 31, 2014 were 25.4% and 27.8%, respectively. The effective tax rates for the three months ended March 31, 2015, and March 31, 2014 were lower than the statutory rate primarily due to the reduction of taxable income associated with the non-controlling interests in WNRL and NTI and recognizing a benefit relating to various federal tax credits at March 31, 2014.

We are subject to examination by the Internal Revenue Service for tax years ending December 31, 2012 or after and by various state and local taxing jurisdictions for tax years ending December 31, 2011 or after.

We believe that it is more likely than not that the benefit from certain state net operating loss ("NOL") carryforwards related to the Yorktown refinery will not be realized. Accordingly, a valuation allowance of $20.8 million was provided against the deferred tax assets relating to these NOL carryforwards at March 31, 2015. There was no change in the valuation allowance for the Yorktown NOL carryforwards from December 31, 2014.

As of March 31, 2015, we have recorded a liability of $13.8 million for unrecognized tax benefits, of which $13.8 million would affect our effective tax rate if recognized. We recognized a net change of $0.1 million for unrecognized benefits, which includes $0.1 million in interest and penalties for the three months ended March 31, 2015.

12. Retirement Plans

We fully recognize the obligations associated with our retiree healthcare and other postretirement plans and NTI's single-employer defined benefit cash balance plan in our financial statements.

Pensions

The net periodic benefit cost associated with NTI's cash balance plan for the three months ended March 31, 2015 and 2014 was $0.6 million and $0.5 million, respectively.

Postretirement Obligations

The net periodic benefit cost associated with our postretirement medical benefit plans for both the three months ended March 31, 2015 and 2014 was $0.2 million, respectively.

Our benefit obligation at December 31, 2014, for our postretirement medical benefit plans was $9.8 million. We fund our medical benefit plans on an as-needed basis.