Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT - Wendy's Co | d920177d8k.htm |

©

2013 Oldemark LLC

First-Quarter 2015

Conference Call

May 6, 2015

Exhibit 99.1

©

2013 Oldemark LLC |

©

2013 Oldemark LLC

DAVID POPLAR

Vice President

Investor Relations

2

©

2013 Oldemark LLC |

Today’s Agenda

CEO Overview

Emil Brolick

Financial Update

Todd Penegor

Q&A

3 |

4

Forward-Looking Statements and Non-GAAP Financial Measures

This presentation, and certain information that management may discuss in connection with

this presentation, contains certain statements that are not historical facts,

including information concerning possible or assumed future results of our

operations. Those statements constitute “forward-looking statements” within the meaning

of the Private Securities Litigation Reform Act of 1995 (The “Reform Act”). For

all forward-looking statements, we claim the protection of the safe harbor for

forward-looking statements contained in the Reform Act. Many important factors could affect our future results and could cause those

results to differ materially from those expressed in or implied by our

forward-looking statements. Such factors, all of which are difficult or

impossible to predict accurately, and many of which are beyond our control, include but

are not limited to those identified under the caption “Forward-Looking

Statements” in our news release issued on May 6, 2015 and in the

“Special Note Regarding Forward-Looking Statements and Projections” and “Risk Factors” sections

of our most recent Form 10-K / Form 10-Qs.

In addition, this presentation and certain information management may discuss in

connection with this presentation reference non-GAAP financial measures, such

as adjusted earnings before interest, taxes, depreciation and amortization (or

adjusted EBITDA), adjusted EBITDA margin and adjusted earnings per share. Adjusted

EBITDA, adjusted EBITDA margin and adjusted earnings per share exclude certain expenses,

net of certain benefits. Reconciliations of non-GAAP financial measures to the most

directly comparable GAAP financial measures are provided in the Appendix to this

presentation, and are included in our news release issued on May 6, 2015 and

posted on www.aboutwendys.com. |

©

2013 Oldemark LLC

EMIL BROLICK

President & CEO

5

©

2013 Oldemark LLC |

HOW WE

GROW BRAND RELEVANCE + ECONOMIC RELEVANCE = GROWTH

Shareholder

Value-Enhancing

Initiatives

Core Organic

Growth

Strategies

6

System Optimization

Financial Management

Global Growth

Restaurant Utilization &

Brand Access

New Restaurant Growth

Image / Experience Activation

North America Same-Restaurant Sales Growth |

HIGH

LOW

FUNCTIONAL

EMOTIONAL

Wendy’s: New QSR Quality, QSR Price

7

Traditional

QSR

B

A

C

New

QSR

EXPERIENCE |

PEOPLE

5-Star Talent

PRICE

New QSR Quality / QSR Price

PRODUCT

Playing a Different Game

PROMOTION

Tactically Brilliant / Strategically Directed

PLACE

Total Brand Experience

PERFORMANCE

Keeping Brand Promise

Recipe to Win

8 |

©

2013 Oldemark LLC

NORTH AMERICA COMPANY-OPERATED

RESTAURANT MARGIN INCREASES 160 BPS

IMPROVEMENT OF 360 BPS IN ADJUSTED

EBITDA MARGIN*

9

ADJ. EBITDA & ADJ. EPS GROWTH IN LINE

WITH EXPECTATIONS

RECAP ON SCHEDULE; COMPANY TO

PROVIDE UPDATED GUIDANCE ON JUNE 3

NORTH AMERICA SYSTEMWIDE SRS

INCREASE OF 3.2 PERCENT

*See Reconciliation of Adjusted EBITDA, Adjusted EBITDA Margin and Adjusted EPS in

the Appendix ©

2013 Oldemark LLC |

2015

Balanced Across Core, LTO & Price/Value LTO

Price/Value

Core

10 |

Menu

Vision: Limited Time Offerings + Core 11

CORE

CORE

LTO |

Jalapeno

Fresco Chicken & Ghost Pepper Fries 12 |

Brand

Access: Image Activation 13 |

Image

Activation New Build AUV ~$300K Higher than Previous Design 14

$1.6M

2010

$1.9M

2014

Brand Access: New Restaurant Growth |

Brand

Access: Consumer-Facing Technology 15

Mobile Order

Mobile Pay

Customer Self

Order Kiosk |

Financial

Management Strategies On Track DEBT REFINANCING

•

On schedule for June 1

completion

•

Targeting leverage ratio

of 5-6x net debt to

2014 Adj. EBITDA

SHARE REPURCHASE

•

Intend to return

refinancing net

proceeds to

shareholders via share

repurchase program

16 |

System

Optimization Phase III Update 17

Process on track with dispositions commencing in Q3 2015;

Expect ~280 to be sold in 2015 with the remaining ~260 in 2016

Process to identify markets to be sold has been completed;

Engaged The Cypress Group to assist with divestitures

~ 540

~ 5% of System

U.S. Company Restaurants to Sell

Ongoing Transition to Own |

Sale of

Bakery Operations Expect Transaction to Close in Q2 of 2015

Allows for Greater Sourcing Flexibility

Focus on Core Restaurant Operations

Eliminate Future Bakery Capital Expenditures

18 |

Reasons

to Believe 19

Transforming the System by Facilitating

Growth through Image Activation

& New Restaurant Development

Strengthening the

Franchise System through

Concentrated Ownership

Improving the

Company & Franchisees

Economic Models

Growth Pyramid

Continue to Execute Against our Strategic Growth Priorities

“A Cut Above”

Brand Positioning

Recipe to Win

Enhancing Our Quality of Earnings &

Adjusted EBITDA Margins

Adjusting our Capital Structure &

Accelerating Long-Term Adj. EPS Growth

Creating Flexibility

for Sustainable, Predictable

Long-Term Income & Growth |

©

2013 Oldemark LLC

TODD PENEGOR

Chief Financial Officer

20

©

2013 Oldemark LLC |

$Mils

First Quarter Financial Highlights

N.A. Systemwide SRS

3.2%

0.7%

2-Year 3.9%

N.A. Company SRS

2.6%

1.3%

2-Year 3.9%

N.A. Co. Rest. Margin

14.7%

13.1%

+160 bps

G&A

$60.3

$70.4

$10.1

Adjusted EBITDA*

$84.0

$75.3

11.6%

Adjusted EBITDA Margin*

18.0%

14.4%

+360 bps

Adjusted EPS*

$0.06

$0.05

20.0%

2015

2014**

B/(W)

*See Reconciliation of Adjusted EBITDA, Adjusted EBITDA Margin and Adjusted EPS in

the Appendix. ** The Company has provided reclassified quarterly 2014

statements of operations on its website to conform to its current-year presentation.

21 |

Q1 2015

vs. Q1 2014: Adjusted EBITDA 22

* See reconciliation in appendix.

(Unaudited)

$ in millions

$87.3

$75.3

$84.0

($8.4)

($12.0)

$10.1

$4.8

$3.9

$2.2

$1.2

($5.1)

2014 Q1 Reported

Adj. EBITDA *

LY Gains on

Rest. Sales &

Surplus Property

2014 Q1 Revised

Adj. EBITDA *

G&A

Savings

Royalties & Net

Rental Income

Core Restaurant

EBITDA

IA Impact

Other

Franchise

Fees

Disposed Rest.

EBITDA

(SO I & II)

2015 Q1

Adj. EBITDA * |

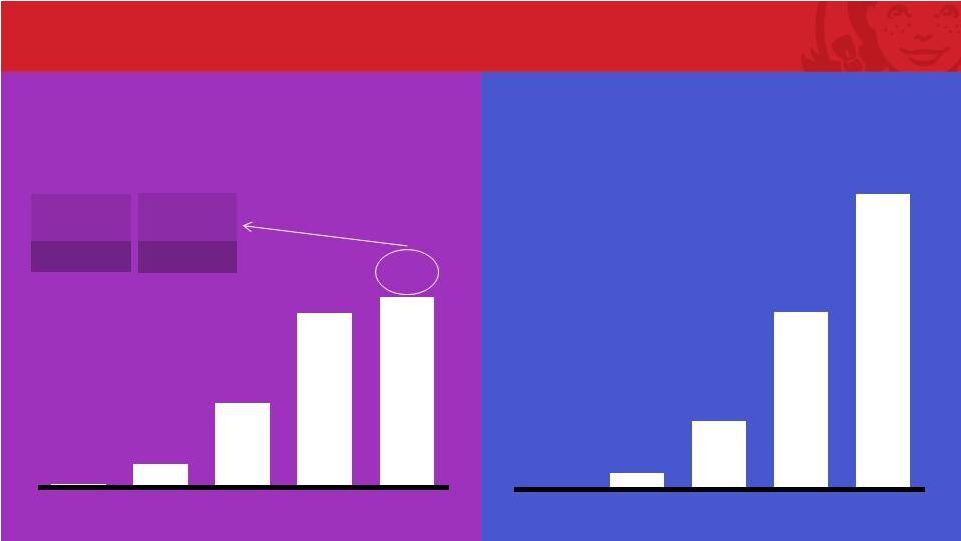

Image

Activation Accelerating Total System Annual

Reimages & New Builds

Total System Cumulative

Reimages & New Builds

450

Reimages

80

New

23

10

64

234

486

530

2011A

2012A

2013A

2014A

2015E

10

74

308

794

1,324

2011A

2012A

2013A

2014A

2015E |

Facilitating Franchisee Commitments for Reimages and New Builds

24

60% Image Activation Requirement by 2020

Canadian Build-to-Suit program

Multi-Year Incentives

Turnkey Services

Construction Support

Multi-Year Investment Plan

Market & Joint Capital Planning |

System

Optimization Update Canada System

Optimization

•

Plan to sell all 131 restaurants

•

Expect to sell remaining restaurants by the

end of Q2

•

Expect to be EBITDA-dilutive in near term,

but EBITDA-accretive longer-term with

build-to-suit restaurant development

U.S. System

Optimization

•

Plan to sell an additional ~540 restaurants:

~280 in 2015 and ~260 in 2016

•

Strong initial interest

System Optimization II

System Optimization III

25 |

Company

Reaffirms 2015 Adj. EBITDA & Adj. EPS

Outlook

To provide updated guidance June 3 after completion of debt refinancing

26

•

Reaffirming G&A expense of approximately $250 million

•

Revising:

•

Company-operated SRS growth of 2.5 to 3.0 percent

•

Capital Expenditures of $250 to $260 million, including approximately $165

million for Company-operated Image Activation restaurants

•

Company-operated restaurant margin outlook of 16.5 to 17.0 percent

•

Reported effective tax rate of 41 to 42%

Adjusted EBITDA of $390 to $400 million

Adjusted EPS of $0.33 to $0.35

26 |

Debt

Refinancing on Schedule to Close June 1 Recapitalization to Target Five to Six

Times Net Debt to 2014 Adjusted EBITDA

Intend to use the Net Proceeds to Return Cash to

Shareholders Via a Share Repurchase Program

Company to Update Guidance on June 3 to Reflect

Expected Completion of Refinancing, Anticipated Share

Repurchase Program, and Planned Sale of Bakery

27 |

Transformation of Company Economic Model

Transformation of Company Economic Model

28

System Optimization Provides a Stronger Platform to Return Cash to Shareholders

Supports Long-Term Income and Growth Commitment

Leveraging Our Balance Sheet

Less Capital Intensive

Enhances Quality of Earnings

Generates Higher Adj. EBITDA Margins

More Predictable and Sustainable Earnings Growth

More Predictable and Sustainable Earnings Growth |

©

2013 Oldemark LLC

DAVID POPLAR

Vice President

Investor Relations

29

©

2013 Oldemark LLC |

30

2015 Investor Relations Calendar: Key Dates

June 1

Annual Meeting

June 3

Company to Issue Updated Outlook

June 22

Stifel Conference (Baltusrol, NJ)

June 23

New York Road Show

August 5

2Q Earnings Release

September 10

CL King (NYC) Conference

November 4

3Q Earnings Release |

Q&A

31 |

Appendix

32 |

Reconciliation of Adjusted EBITDA to Net Income

33

2015

2014

1

Adjusted EBITDA

84,027

$

75,283

$

Plus (less):

Reversal of pension withdrawal liability in cost of sales

12,486

-

Depreciation and amortization

(36,880)

(42,021)

System optimization losses (gains), net

(813)

72,992

Reorganization and realignment costs

(4,613)

(14,711)

Impairment of long-lived assets

(1,937)

(2,529)

Operating profit

52,270

89,014

Interest expense

(12,757)

(12,994)

Other income, net

239

523

Income before income taxes

39,752

76,543

Provision for income taxes

(12,245)

(30,240)

Net income

27,507

$

46,303

$

Adjusted EBITDA margin

18.0%

14.4%

Previously reported Adjusted EBITDA

1

87,334

$

Change

1

(12,051)

1

2014 Adjusted EBITDA updated to exclude net gain on disposal of assets to conform

to the current year presentation. Three Months |

34

Reconciliation of Adjusted Income and Adjusted Earnings Per

Share to Net Income and Earnings Per Share

Per share

Per share

Adjusted income and adjusted earnings per share

23,912

$

0.06

$

18,814

$

0.05

$

Plus (less):

Reversal of pension withdrawal liability in cost of sales

7,816

0.02

-

-

Depreciation of assets that will be replaced as part of the Image Activation

initiative 109

0.00

(5,897)

(0.02)

Reorganization and realignment costs

(2,846)

(0.01)

(8,738)

(0.02)

Impairment of long-lived assets

(1,195)

(0.00)

(1,510)

(0.00)

System optimization losses (gains), net

(289)

(0.00)

43,634

0.11

Total adjustments

3,595

0.01

27,489

0.07

Net income

27,507

$

0.07

$

46,303

$

0.12

$

Previously

reported

adjusted

income

and

adjusted

earnings

per

share

1

26,249

$

0.07

$

Change

1

(7,435)

(0.02)

1

2014

Adjusted

income

and

adjusted

earnings

per

share

updated

to

exclude

net

gain

on

disposal

of

assets

to

conform

to

the

current

year

presentation.

2015

2014

1

Three Months |

35

Notice Regarding Debt Recapitalization

The information in this presentation regarding a debt

recapitalization does not constitute an offer to sell or the

solicitation of an offer to buy any notes or other securities that

could be issued in such transaction. |

36 |