Attached files

| file | filename |

|---|---|

| 8-K - AXALTA COATING SYSTEMS LTD. 8-K - Axalta Coating Systems Ltd. | a51096085.htm |

| EX-99.1 - EXHIBIT 99.1 - Axalta Coating Systems Ltd. | a51096085ex99_1.htm |

Exhibit 99.2

Axalta Coating Systems Ltd.

Q1 2015 Conference Call May 6, 2015

Axalta Coating Systems Ltd.

Q1 2015 Conference Call May 6, 2015

Notice Regarding Forward

Looking Statements, Non-GAAP Financial Measures and Defined Terms

Forward-Looking Statements This presentation and the oral remarks made

in connection herewith may contain “forward-looking statements” within

the meaning of the U.S. Private Securities Litigation Reform Act of

1995, including those relating to 2015 net sales, Adjusted EBITDA, tax

rate, capital expenditures, plant expansions and net working capital.

Any forward-looking statements involve risks, uncertainties and

assumptions. These statements often include words such as “believe,”

“expect,” “anticipate,” “intend,” “plan,” “estimate,” “target,”

“project,” “forecast,” “seek,” “will,” “may,” “should,” “could,”

“would,” or similar expressions. These statements are based on certain

assumptions that we have made in light of our experience in the industry

and our perceptions of historical trends, current conditions, expected

future developments and other factors we believe are appropriate under

the circumstances as of the date hereof. Although we believe that the

assumptions and analysis underlying these statements are reasonable as

of the date hereof, investors are cautioned not to place undue reliance

on these statements. We do not have any obligation to and do not intend

to update any forward-looking statements included herein, which speak

only as of the date hereof. You should understand that these statements

are not guarantees of future performance or results. Actual results

could differ materially from those described in any forward-looking

statements contained herein or the oral remarks made in connection

herewith as a result of a variety of factors, including known and

unknown risks and uncertainties, many of which are beyond our control.

Non-GAAP Financial Measures The historical financial information

included in this presentation includes financial information that is not

presented in accordance with generally accepted accounting principles in

the United States (“GAAP”), including EBITDA, Adjusted EBITDA and Net

Debt. Management uses these non-GAAP financial measures in the analysis

of our financial and operating performance because they assist in the

evaluation of underlying trends in our business. Our use of the terms

EBITDA, Adjusted EBITDA and Net Debt may differ from that of others in

our industry. EBITDA and Adjusted EBITDA should not be considered as

alternatives to net income (loss), operating income or any other

performance measures derived in accordance with GAAP as measures of

operating performance or operating cash flows or as measures of

liquidity. EBITDA, Adjusted EBITDA and Net Debt have important

limitations as analytical tools and should be considered in conjunction

with, and not as substitutes for, our results as reported under GAAP.

This presentation includes a reconciliation of certain non-GAAP

financial measures with the most directly comparable financial measures

calculated in accordance with GAAP. Defined Terms All capitalized terms

contained within this presentation have been previously defined in our

filings with the United States Securities and Exchange Commission.

Axalta Coating Systems Ltd. 2

Notice Regarding Forward

Looking Statements, Non-GAAP Financial Measures and Defined Terms

Forward-Looking Statements This presentation and the oral remarks made

in connection herewith may contain “forward-looking statements” within

the meaning of the U.S. Private Securities Litigation Reform Act of

1995, including those relating to 2015 net sales, Adjusted EBITDA, tax

rate, capital expenditures, plant expansions and net working capital.

Any forward-looking statements involve risks, uncertainties and

assumptions. These statements often include words such as “believe,”

“expect,” “anticipate,” “intend,” “plan,” “estimate,” “target,”

“project,” “forecast,” “seek,” “will,” “may,” “should,” “could,”

“would,” or similar expressions. These statements are based on certain

assumptions that we have made in light of our experience in the industry

and our perceptions of historical trends, current conditions, expected

future developments and other factors we believe are appropriate under

the circumstances as of the date hereof. Although we believe that the

assumptions and analysis underlying these statements are reasonable as

of the date hereof, investors are cautioned not to place undue reliance

on these statements. We do not have any obligation to and do not intend

to update any forward-looking statements included herein, which speak

only as of the date hereof. You should understand that these statements

are not guarantees of future performance or results. Actual results

could differ materially from those described in any forward-looking

statements contained herein or the oral remarks made in connection

herewith as a result of a variety of factors, including known and

unknown risks and uncertainties, many of which are beyond our control.

Non-GAAP Financial Measures The historical financial information

included in this presentation includes financial information that is not

presented in accordance with generally accepted accounting principles in

the United States (“GAAP”), including EBITDA, Adjusted EBITDA and Net

Debt. Management uses these non-GAAP financial measures in the analysis

of our financial and operating performance because they assist in the

evaluation of underlying trends in our business. Our use of the terms

EBITDA, Adjusted EBITDA and Net Debt may differ from that of others in

our industry. EBITDA and Adjusted EBITDA should not be considered as

alternatives to net income (loss), operating income or any other

performance measures derived in accordance with GAAP as measures of

operating performance or operating cash flows or as measures of

liquidity. EBITDA, Adjusted EBITDA and Net Debt have important

limitations as analytical tools and should be considered in conjunction

with, and not as substitutes for, our results as reported under GAAP.

This presentation includes a reconciliation of certain non-GAAP

financial measures with the most directly comparable financial measures

calculated in accordance with GAAP. Defined Terms All capitalized terms

contained within this presentation have been previously defined in our

filings with the United States Securities and Exchange Commission.

Axalta Coating Systems Ltd. 2

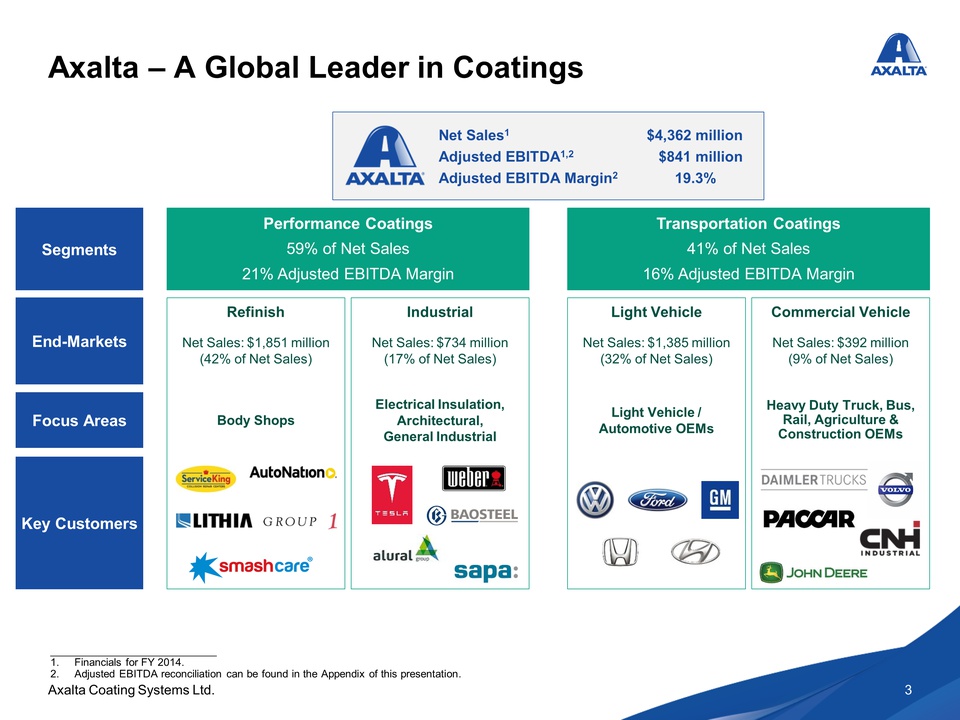

Axalta – A Global Leader in

Coatings Net Sales 1 $4,362 million Adjusted EBITDA 1,2 $841 million

Adjusted EBITDA Margin 2 19.3% Segments Performance Coatings 59% of Net

Sales 21% Adjusted EBITDA Margin Transportation Coatings 41% of Net

Sales 16% Adjusted EBITDA Margin End-Markets Focus Areas Key Customers

Body Shops Electrical Insulation, Architectural, General Industrial

Light Vehicle / Automotive OEMs Heavy Duty Truck, Bus, Rail, Agriculture

& Construction OEMs Net Sales: $1,851 million (42% of Net Sales) Net

Sales: $734 million (17% of Net Sales) Net Sales: $1,385 million (32% of

Net Sales) Net Sales: $392 million (9% of Net Sales) Refinish Industrial

Light Vehicle Commercial Vehicle 1. Financials for FY 2014. 2. Adjusted

EBITDA reconciliation can be found in the Appendix of this presentation.

Axalta Coating Systems Ltd. 3

Axalta – A Global Leader in

Coatings Net Sales 1 $4,362 million Adjusted EBITDA 1,2 $841 million

Adjusted EBITDA Margin 2 19.3% Segments Performance Coatings 59% of Net

Sales 21% Adjusted EBITDA Margin Transportation Coatings 41% of Net

Sales 16% Adjusted EBITDA Margin End-Markets Focus Areas Key Customers

Body Shops Electrical Insulation, Architectural, General Industrial

Light Vehicle / Automotive OEMs Heavy Duty Truck, Bus, Rail, Agriculture

& Construction OEMs Net Sales: $1,851 million (42% of Net Sales) Net

Sales: $734 million (17% of Net Sales) Net Sales: $1,385 million (32% of

Net Sales) Net Sales: $392 million (9% of Net Sales) Refinish Industrial

Light Vehicle Commercial Vehicle 1. Financials for FY 2014. 2. Adjusted

EBITDA reconciliation can be found in the Appendix of this presentation.

Axalta Coating Systems Ltd. 3

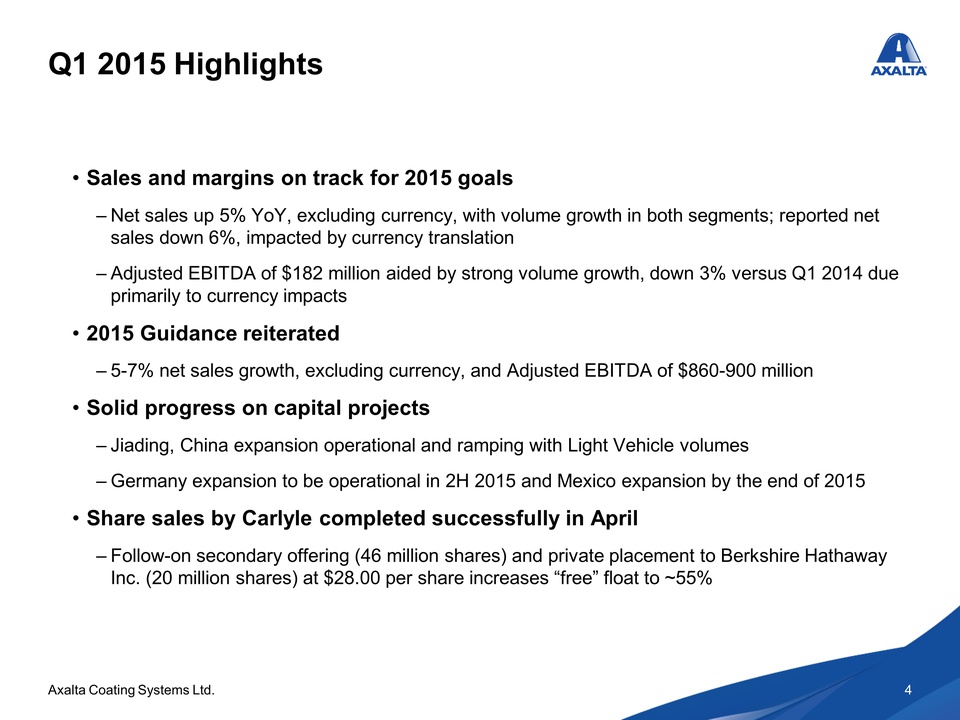

Q1 2015 Highlights Sales

and margins on track for 2015 goals – Net sales up 5% YoY, excluding

currency, with volume growth in both segments; reported net sales down

6%, impacted by currency translation – Adjusted EBITDA of $182 million

aided by strong volume growth, down 3% versus Q1 2014 due primarily to

currency impacts 2015 Guidance reiterated – 5-7% net sales growth,

excluding currency, and Adjusted EBITDA of $860-900 million Solid

progress on capital projects – Jiading, China expansion operational and

ramping with Light Vehicle volumes – Germany expansion to be operational

in 2H 2015 and Mexico expansion by the end of 2015 Share sales by

Carlyle completed successfully in April – Follow-on secondary offering

(46 million shares) and private placement to Berkshire Hathaway Inc. (20

million shares) at $28.00 per share increases “free” float to ~55%

Axalta Coating Systems Ltd. 4

Q1 2015 Highlights Sales

and margins on track for 2015 goals – Net sales up 5% YoY, excluding

currency, with volume growth in both segments; reported net sales down

6%, impacted by currency translation – Adjusted EBITDA of $182 million

aided by strong volume growth, down 3% versus Q1 2014 due primarily to

currency impacts 2015 Guidance reiterated – 5-7% net sales growth,

excluding currency, and Adjusted EBITDA of $860-900 million Solid

progress on capital projects – Jiading, China expansion operational and

ramping with Light Vehicle volumes – Germany expansion to be operational

in 2H 2015 and Mexico expansion by the end of 2015 Share sales by

Carlyle completed successfully in April – Follow-on secondary offering

(46 million shares) and private placement to Berkshire Hathaway Inc. (20

million shares) at $28.00 per share increases “free” float to ~55%

Axalta Coating Systems Ltd. 4

Delivering On Our Goals

Stated Objective Results Delivered Grow the Business Continue New

Business Wins Increase Emerging Markets Presence Cost Structure &

Commercial Alignment Improvement Pursue High IRR Opportunities Volumes

up 5% in Q1 2015 YoY after 1% in Q4 2014 Adjusted EBITDA on track for

mid to high single digit growth in 2015 Light vehicle wins ramping

significantly over balance of 2015 as planned Axalta Asia Pacific

Transportation Coatings growth over 20% in Q1 Fit-For-Growth savings

remain ahead of plan Axalta Way taking shape and on track Axalta Coating

Systems Ltd . 5 Jiading, China plant ramping, other projects on track.

~$90 million growth capex in 2015 Axalta Coating Systems Ltd. 5

Delivering On Our Goals

Stated Objective Results Delivered Grow the Business Continue New

Business Wins Increase Emerging Markets Presence Cost Structure &

Commercial Alignment Improvement Pursue High IRR Opportunities Volumes

up 5% in Q1 2015 YoY after 1% in Q4 2014 Adjusted EBITDA on track for

mid to high single digit growth in 2015 Light vehicle wins ramping

significantly over balance of 2015 as planned Axalta Asia Pacific

Transportation Coatings growth over 20% in Q1 Fit-For-Growth savings

remain ahead of plan Axalta Way taking shape and on track Axalta Coating

Systems Ltd . 5 Jiading, China plant ramping, other projects on track.

~$90 million growth capex in 2015 Axalta Coating Systems Ltd. 5

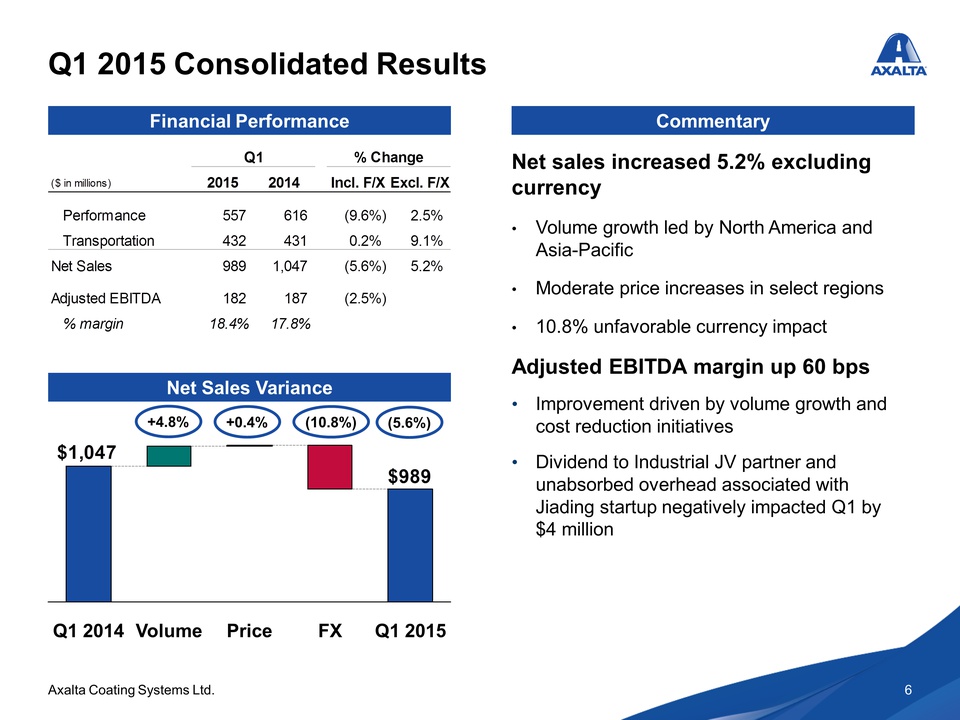

Q1 2015 Consolidated

Results Financial Performance Q1 % Change ($ in millions) 2015 2014

Incl. F/X Excl. F/X Performance 557 616 (9.6%) 2.5% Transportation 432

431 0.2% 9.1% Net Sales 989 1,047 (5.6%) 5.2% Adjusted EBITDA 182 187

(2.5%) % margin 18.4% 17.8% Commentary Net sales increased 5.2%

excluding currency Volume growth led by North America and Asia-Pacific

Moderate price increases in select regions 10.8% unfavorable currency

impact Adjusted EBITDA margin up 60 bps Improvement driven by volume

growth and cost reduction initiatives Dividend to Industrial JV partner

and unabsorbed overhead associated with Jiading startup negatively

impacted Q1 by $4 million Net Sales Variance $1,047 +4.8% +0.4% (10.8%)

(5.6%) $989 Q1 2014 Volume Price FX Q1 2015 Axalta Coating Systems Ltd. 6

Q1 2015 Consolidated

Results Financial Performance Q1 % Change ($ in millions) 2015 2014

Incl. F/X Excl. F/X Performance 557 616 (9.6%) 2.5% Transportation 432

431 0.2% 9.1% Net Sales 989 1,047 (5.6%) 5.2% Adjusted EBITDA 182 187

(2.5%) % margin 18.4% 17.8% Commentary Net sales increased 5.2%

excluding currency Volume growth led by North America and Asia-Pacific

Moderate price increases in select regions 10.8% unfavorable currency

impact Adjusted EBITDA margin up 60 bps Improvement driven by volume

growth and cost reduction initiatives Dividend to Industrial JV partner

and unabsorbed overhead associated with Jiading startup negatively

impacted Q1 by $4 million Net Sales Variance $1,047 +4.8% +0.4% (10.8%)

(5.6%) $989 Q1 2014 Volume Price FX Q1 2015 Axalta Coating Systems Ltd. 6

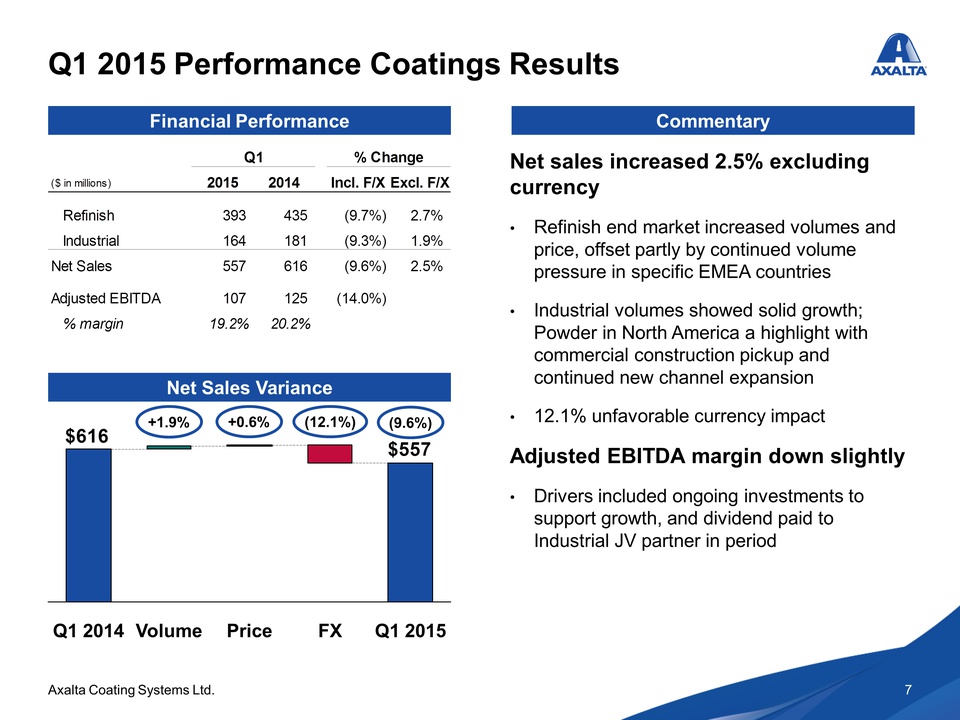

Q1 2015 Performance

Coatings Results Financial Performance Q1 % Change ($ in millions) 2015

2014 Incl. F/X Excl. F/X Refinish 393 435 (9.7%) 2.7% Industrial 164 181

(9.3%) 1.9% Net Sales 557 616 (9.6%) 2.5% Adjusted EBITDA 107 125

(14.0%) % margin 19.2% 20.2% Commentary Net sales increased 2.5%

excluding currency Refinish end market increased volumes and price,

offset partly by continued volume pressure in specific EMEA countries

Industrial volumes showed solid growth; Powder in North America a

highlight with commercial construction pickup and continued new channel

expansion 12.1% unfavorable currency impact Adjusted EBITDA margin down

slightly Drivers included ongoing investments to support growth, and

dividend paid to Industrial JV partner in period Net Sales Variance $616

+1.9% +0.6% (12.1%) (9.6%) $557 Q1 2014 Volume Price FX Q1 2015 Axalta

Coating Systems Ltd. 7

Q1 2015 Performance

Coatings Results Financial Performance Q1 % Change ($ in millions) 2015

2014 Incl. F/X Excl. F/X Refinish 393 435 (9.7%) 2.7% Industrial 164 181

(9.3%) 1.9% Net Sales 557 616 (9.6%) 2.5% Adjusted EBITDA 107 125

(14.0%) % margin 19.2% 20.2% Commentary Net sales increased 2.5%

excluding currency Refinish end market increased volumes and price,

offset partly by continued volume pressure in specific EMEA countries

Industrial volumes showed solid growth; Powder in North America a

highlight with commercial construction pickup and continued new channel

expansion 12.1% unfavorable currency impact Adjusted EBITDA margin down

slightly Drivers included ongoing investments to support growth, and

dividend paid to Industrial JV partner in period Net Sales Variance $616

+1.9% +0.6% (12.1%) (9.6%) $557 Q1 2014 Volume Price FX Q1 2015 Axalta

Coating Systems Ltd. 7

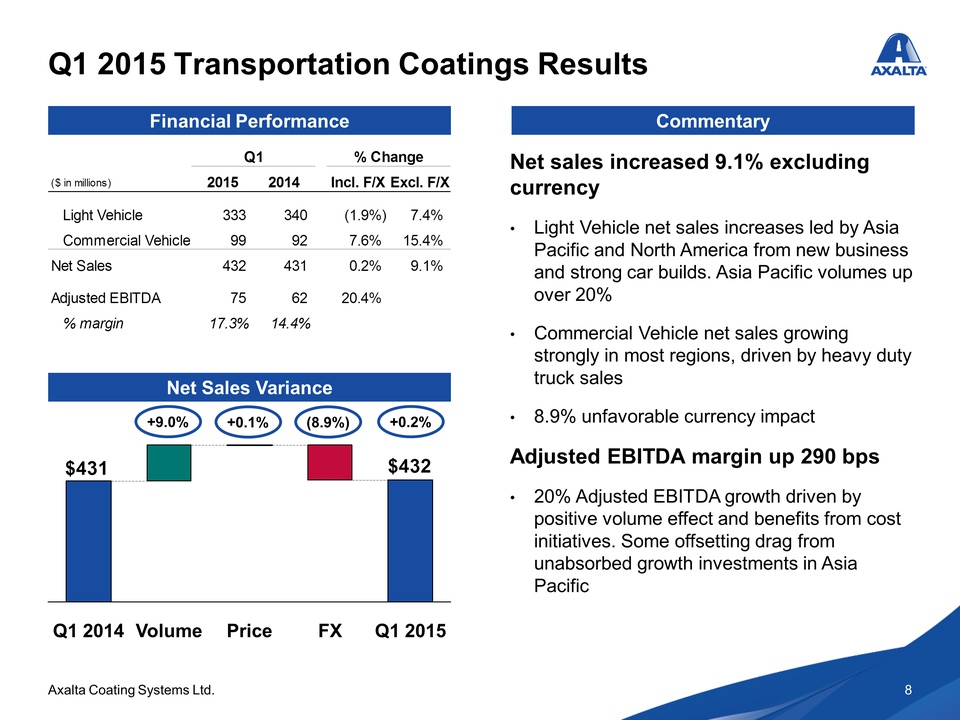

Q1 2015 Transportation Coatings Results Financial Performance Q1 % Change ($ in millions) 2015 2014 Incl. F/X Excl. F/X Light Vehicle 333 340 (1.9%) 7.4% Commercial Vehicle 99 92 7.6% 15.4% Net Sales 432 431 0.2% 9.1% Adjusted EBITDA 75 62 20.4% % margin 17.3% 14.4% Commentary Net sales increased 9.1% excluding currency Light Vehicle net sales increases led by Asia Pacific and North America from new business and strong car builds. Asia Pacific volumes up over 20% Commercial Vehicle net sales growing strongly in most regions, driven by heavy duty truck sales 8.9% unfavorable currency impact Adjusted EBITDA margin up 290 bps 20% Adjusted EBITDA growth driven by positive volume effect and benefits from cost initiatives. Some offsetting drag from unabsorbed growth investments in Asia Pacific Net Sales Variance $431 +9.0% +0.1% (8.9%) +0.2% $432 Q1 2014 Volume Price FX Q1 2015 Axalta Coating Systems Ltd. 8

Cost Optimization Initiatives Progressing Well Fit-For-Growth: $100 million savings plan is on budget – Methodically tracking progress towards remainder of program – Expect $60 million cumulative savings to be realized by the end of 2015 Axalta Way: $100 million savings targeted – Detailed planning and execution began in Q1 – Opportunities in procurement, operations, commercial practices, and SG&A One Time Costs: Minor with independent company transition costs now complete – Q1 saw $4 million for termination benefits, $3 million for consulting and advisory fees Axalta Coating Systems Ltd. 9

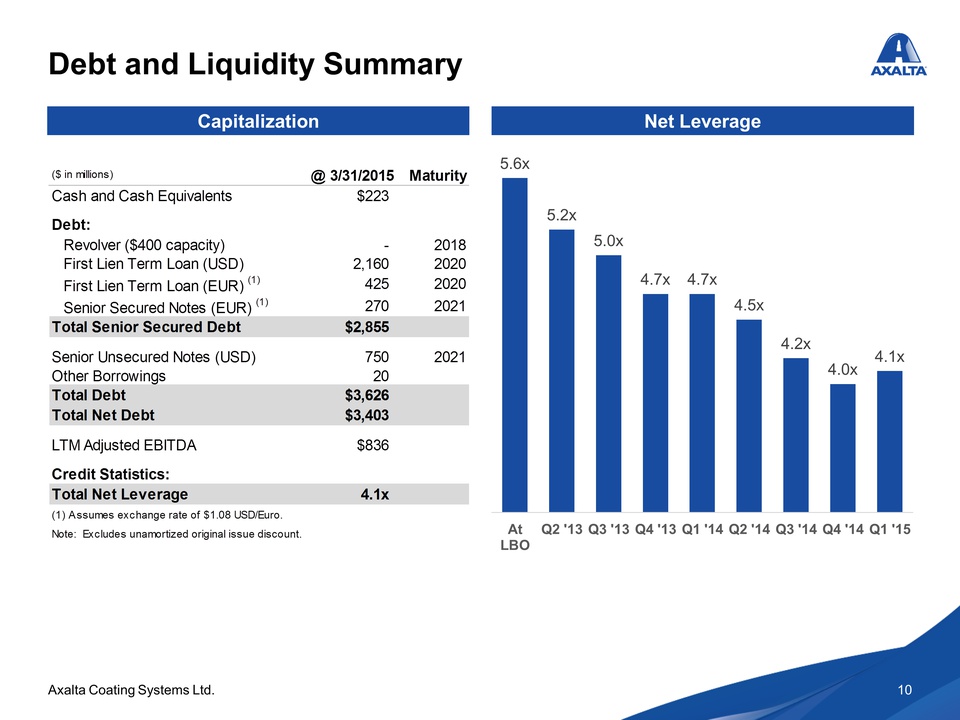

Debt and Liquidity Summary Net Leverage 5.6x 5.2x 5.0x 4.7x 4.7x 4.5x 4.2x 4.0x 4.1x At LBO Q2 '13 Q3 '13 Q4 '13 Q1 '14 Q2 '14 Q3 '14 Q4 '14 Q1 '15 Capitalization ($ in millions) @ 3/31/2015 Maturity Cash and Cash Equivalents $223 Debt: Revolver ($400 capacity) - 2018 First Lien Term Loan (USD) 2,160 2020 First Lien Term Loan (EUR) (1) 425 2020 Senior Secured Notes (EUR) (1) 270 2021 Total Senior Secured Debt $2,855 Senior Unsecured Notes (USD) 750 2021 Other Borrowings 20 Total Debt $3,626 Total Net Debt $3,403 LTM Adjusted EBITDA $836 Credit Statistics: Total Net Leverage 4.1x (1) Assumes exchange rate of $1.08 USD/Euro. Note: Excludes unamortized original issue discount. Axalta Coating Systems Ltd. 10

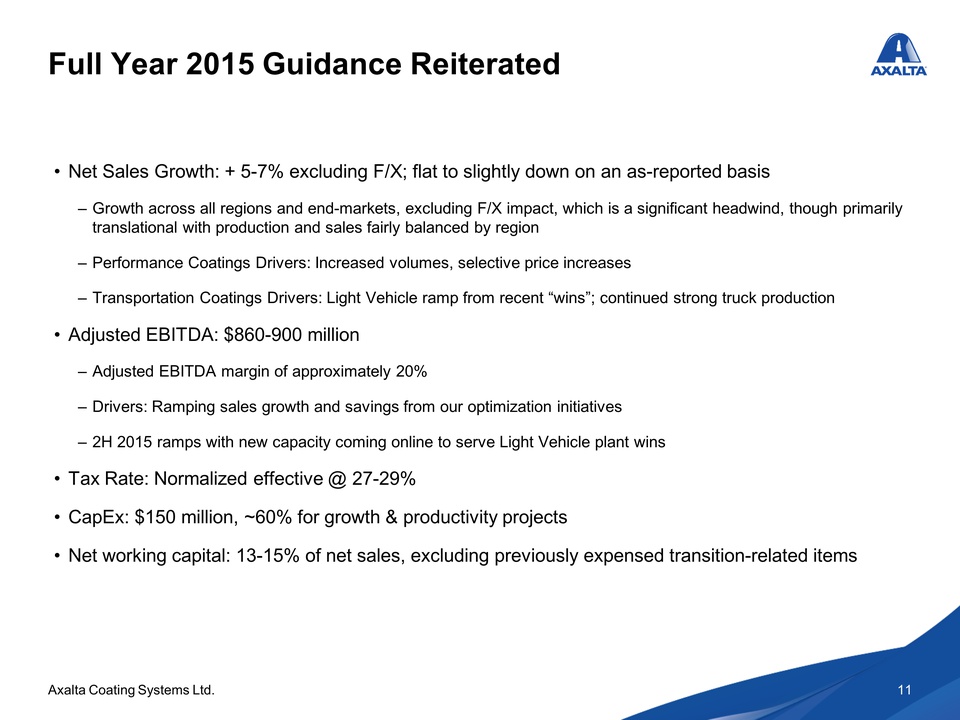

Full Year 2015 Guidance Reiterated Net Sales Growth: + 5-7% excluding F/X; flat to slightly down on an as-reported basis – Growth across all regions and end-markets, excluding F/X impact, which is a significant headwind, though primarily translational with production and sales fairly balanced by region – Performance Coatings Drivers: Increased volumes, selective price increases – Transportation Coatings Drivers: Light Vehicle ramp from recent “wins”; continued strong truck production Adjusted EBITDA: $860-900 million – Adjusted EBITDA margin of approximately 20% – Drivers: Ramping sales growth and savings from our optimization initiatives – 2H 2015 ramps with new capacity coming online to serve Light Vehicle plant wins Tax Rate: Normalized effective @ 27-29% CapEx: $150 million, ~60% for growth & productivity projects Net working capital: 13-15% of net sales, excluding previously expensed transition-related items Axalta Coating Systems Ltd. 11

Appendix

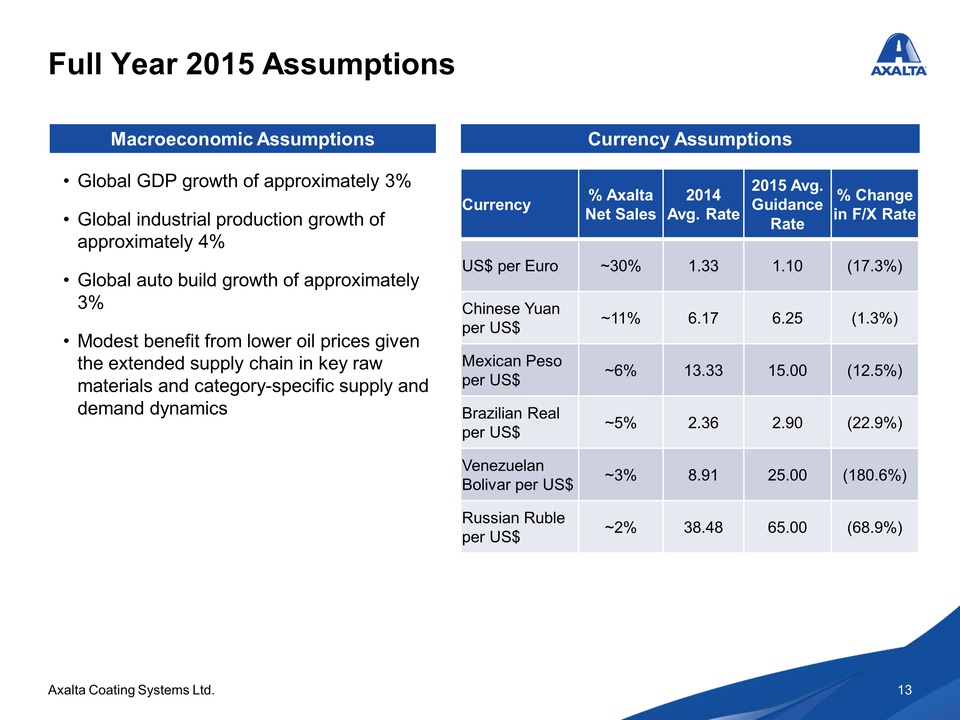

Full Year 2015 Assumptions Currency Assumptions Currency % Axalta Net Sales 2014 Avg. Rate 2015 Avg. Guidance Rate % Change in F/X Rate US$ per Euro ~30% 1.33 1.10 (17.3%) Chinese Yuan per US$ ~11% 6.17 6.25 (1.3%) Mexican Peso per US$ ~6% 13.33 15.00 (12.5%) Brazilian Real per US$ ~5% 2.36 2.90 (22.9%) Venezuelan Bolivar per US$ ~3% 8.91 25.00 (180.6%) Russian Ruble per US$ ~2% 38.48 65.00 (68.9%) Macroeconomic Assumptions Global GDP growth of approximately 3% Global industrial production growth of approximately 4% Global auto build growth of approximately 3% Modest benefit from lower oil prices given the extended supply chain in key raw materials and category-specific supply and demand dynamics Axalta Coating Systems Ltd. 13

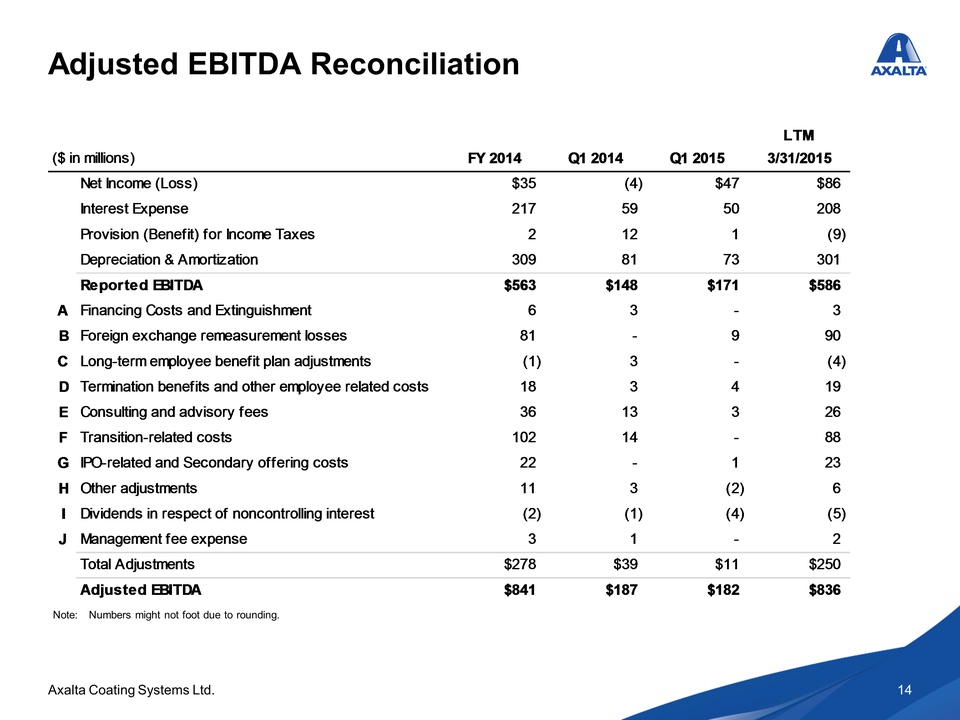

Adjusted EBITDA Reconciliation ($ in millions) FY 2014 Q1 2014 Q1 2015 LTM 3/31/2015 Net Income (Loss) $35 (4) $47 $86 Interest Expense 217 59 50 208 Provision (Benefit) for Income Taxes 2 12 1 (9) Depreciation & Amortization 309 81 73 301 Reported EBITDA $563 $148 $171 $586 A Financing Costs and Extinguishment 6 3 - 3 B Foreign exchange remeasurement losses 81 - 9 90 C Long-term employee benefit plan adjustments (1) 3 - (4) D Termination benefits and other employee related costs 18 3 4 19 E Consulting and advisory fees 36 13 3 26 F Transition-related costs 102 14 - 88 G IPO-related and Secondary offering costs 22 - 1 23 H Other adjustments 11 3 (2) 6 I Dividends in respect of noncontrolling interest (2) (1) (4) (5) J Management fee expense 3 1 - 2 Total Adjustments $278 $39 $11 $250 Adjusted EBITDA $841 $187 $182 $836 Note: Numbers might not foot due to rounding. Axalta Coating Systems Ltd. 14

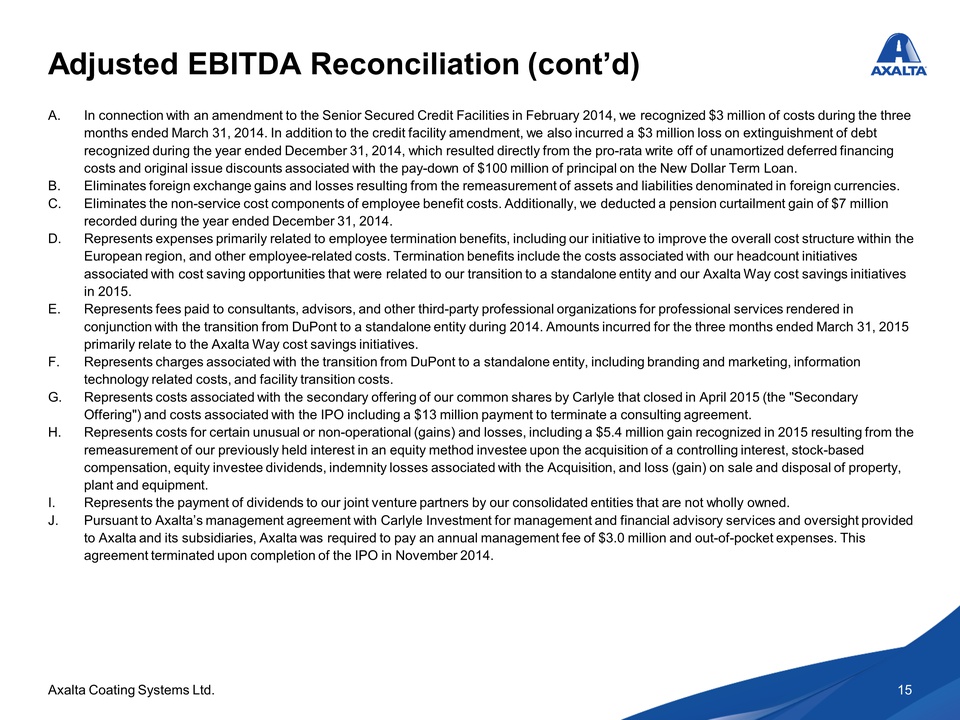

Adjusted EBITDA Reconciliation (cont’d) A. In connection with an amendment to the Senior Secured Credit Facilities in February 2014, we recognized $3 million of costs during the three months ended March 31, 2014. In addition to the credit facility amendment, we also incurred a $3 million loss on extinguishment of debt recognized during the year ended December 31, 2014, which resulted directly from the pro-rata write off of unamortized deferred financing costs and original issue discounts associated with the pay-down of $100 million of principal on the New Dollar Term Loan. B. Eliminates foreign exchange gains and losses resulting from the remeasurement of assets and liabilities denominated in foreign currencies. C. Eliminates the non-service cost components of employee benefit costs. Additionally, we deducted a pension curtailment gain of $7 million recorded during the year ended December 31, 2014. D. Represents expenses primarily related to employee termination benefits, including our initiative to improve the overall cost structure within the European region, and other employee-related costs. Termination benefits include the costs associated with our headcount initiatives associated with cost saving opportunities that were related to our transition to a standalone entity and our Axalta Way cost savings initiatives in 2015. E. Represents fees paid to consultants, advisors, and other third-party professional organizations for professional services rendered in conjunction with the transition from DuPont to a standalone entity during 2014. Amounts incurred for the three months ended March 31, 2015 primarily relate to the Axalta Way cost savings initiatives. F. Represents charges associated with the transition from DuPont to a standalone entity, including branding and marketing, information technology related costs, and facility transition costs. G. Represents costs associated with the secondary offering of our common shares by Carlyle that closed in April 2015 (the "Secondary Offering") and costs associated with the IPO including a $13 million payment to terminate a consulting agreement. H. Represents costs for certain unusual or non-operational (gains) and losses, including a $5.4 million gain recognized in 2015 resulting from the remeasurement of our previously held interest in an equity method investee upon the acquisition of a controlling interest, stock-based compensation, equity investee dividends, indemnity losses associated with the Acquisition, and loss (gain) on sale and disposal of property, plant and equipment. I. Represents the payment of dividends to our joint venture partners by our consolidated entities that are not wholly owned. J. Pursuant to Axalta’s management agreement with Carlyle Investment for management and financial advisory services and oversight provided to Axalta and its subsidiaries, Axalta was required to pay an annual management fee of $3.0 million and out-of-pocket expenses. This agreement terminated upon completion of the IPO in November 2014. Axalta Coating Systems Ltd. 15