Attached files

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE

ACT OF 1934

For the Fiscal Year Ended December 31, 2014

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition Period From ______________ to________________

Commission file number 000-21864

Vu1 Corporation

(Exact name of registrant as specified in its charter)

|

California

|

84-0672714

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

1001 Camelia Street

|

|

|

Berkeley, California

|

94710

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code: (855) 881-2852

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, no par value

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yeso No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yeso No x

Indicate by check mark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer

|

o

|

Accelerated filer

|

o |

|

Non-accelerated filer

|

o

|

Smaller reporting company

|

x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yeso Nox

The aggregate market value of the issuer’s stock held by non-affiliates on June 30, 2013, the last business day of the registrant’s most recently completed second fiscal quarter, was $8,744,853, based on the average of the bid and ask prices of such stock on that date of $1.29 per share, as reported by the OTC Bulletin Board.

On April 16, 2015, there were 14,173,093 shares of registrant’s common stock issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None

Vu1 Corporation

2013 ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

|

Page No.

|

||

|

PART I

|

||

|

Item 1.

|

Business

|

1

|

|

Item 1A.

|

Risk Factors

|

8

|

|

Item 1B.

|

Unresolved Staff Comments

|

15

|

|

Item 2.

|

Properties

|

15

|

|

Item 3.

|

Legal Proceedings

|

15

|

|

Item 4.

|

Mine Safety Disclosures

|

15

|

|

PART II

|

||

|

Item 5.

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

16

|

|

Item 6.

|

Selected Financial Data

|

17

|

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

17

|

|

Item 7A.

|

Quantitative and Qualitative Disclosures About Market Risk

|

21

|

|

Item 8.

|

Financial Statements and Supplementary Data

|

21

|

|

Item 9.

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

21

|

|

Item 9A.

|

Controls and Procedures

|

22

|

|

Item 9B.

|

Other Information

|

22

|

|

PART III

|

||

|

Item 10.

|

Directors, Executive Officers and Corporate Governance

|

23

|

|

Item 11.

|

Executive Compensation

|

28

|

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

32

|

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence

|

34

|

|

Item 14.

|

Principal Accountant Fees and Services

|

34

|

|

PART IV

|

||

|

Item 15.

|

Exhibits and Financial Statement Schedules

|

35

|

|

Signatures

|

38

|

EXPLANATORY NOTE

Unless otherwise indicated or the context otherwise requires, all references in this Annual Report on Form 10-K to “we,” “us,” “our” and the “Company” are to Vu1 Corporation, Sendio, s.r.o., our former Czech subsidiary, and our inactive subsidiary Telisar Corporation.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

We are including the following cautionary statement in this Annual Report to make applicable and take advantage of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 for any forward-looking statements. All statements other than statements of historical fact, including statements concerning plans, objectives, goals, strategies, future events or performance and underlying assumptions, future results of operations or financial position, made in this Annual Report are forward looking. In particular, the words “believe,” “expect,” “intend,” “anticipate,” “estimate,” “may,” “will,” “target,” variations of such words, and similar expressions identify forward-looking statements, but are not the exclusive means of identifying such statements and their absence does not mean that the statement is not forward-looking.

The forward-looking statements contained herein involve risks and uncertainties which could cause actual results or outcomes to differ materially from those expressed in the forward-looking statements. Our expectations, beliefs and projections are expressed in good faith and are believed by management to have a reasonable basis, including without limitation, management’s examination of historical operating trends, data contained in our records and other data available from third parties; however, management’s expectations, beliefs and projections may not be achieved or accomplished. In addition to other factors and matters discussed elsewhere herein, the following are important factors that, in our view, could cause actual results to differ materially from those discussed in the forward-looking statements:

|

·

|

our lack of working capital and lack of revenues;

|

|

·

|

the availability of capital to us, in the amount and time needed, to fund our development programs and operations, and the terms and dilutive effect of any such financings;

|

|

·

|

our ability to be successful in our product development and testing efforts;

|

|

·

|

our ability to obtain commercial development for our products;

|

|

·

|

our ability to obtain manufacturing capability for our products in a cost-effective manner and at the times and in the volumes required, while maintaining quality assurance;

|

|

·

|

market demand for and acceptance of our products and planned products, and other factors affecting market conditions;

|

|

·

|

technological advances and competitive pressure by our competitors;

|

|

·

|

governmental regulations imposed on us in the United States and European Union; and

|

|

·

|

the loss of any of our key employees or consultants.

|

For a discussion of these and other factors that may affect our business, results and prospects, see “Item 1. Business” and “Item 1A. Risk Factors.” Readers are urged to carefully review and consider the various disclosures made by us in this Annual Report and in our other reports filed with the Securities and Exchange Commission, and those described from time to time in our press releases and other communications, which attempt to advise interested parties of the risks and factors that may affect our business, prospects and results of operations. Except as required by U.S. federal securities laws, we do not undertake any obligation to update or revise any forward-looking statements to reflect any future events or circumstances.

PART I

ITEM 1. BUSINESS

We design, develop and market mercury-free lighting products using our proprietary Electron Stimulated Luminescence™, or ESL, technology. Our ESL lights use a form of cathode-ray tube technology in which accelerated electrons stimulate phosphor to create light, making the surface of our lights glow in a highly energy-efficient manner and with a warm white natural light. In December 2010, we released our first product, the R30 reflector light for recessed fixtures (a direct replacement for the 65-watt incandescent flood light), which we believe will capture a growing share of the general illumination market in 2014 and over the next several years. We believe our current and planned ESL lighting products offer advantages over competing technologies including increased energy efficiency, longer product lifetime, environmentally safer and toxin-free disposal, superior light quality and lower cost of usage. We also believe that our ESL lights have the potential to replace traditional incandescent light bulbs, compact fluorescent light bulbs (CFLs) and solid-state light emitting diodes (LEDs) in the future because of these competitive advantages. Our technology, intellectual property position and strategic manufacturing relationships should enable us to share in the revenues from the worldwide general lighting products market when our current and planned ESL lights enter mainstream consumer, commercial and industrial markets.

Our primary growth strategy is to accelerate the introduction of our lighting products into the commercial and residential general illumination market with the goal of obtaining widespread marketplace adoption over the next two years. In support of this objective, we are pursuing a multi-channel sales, marketing and distribution strategy, which includes efforts to establish business relationships with “big box” retailers, electrical and lighting distributors and municipal utilities.

In addition to our R30 reflector light, which received certification from Underwriters Laboratories Inc. (UL®) in October 2010, we are currently developing our version of the standard Edisonian A19 screw-in light (and its European equivalent, the A60), the most common general purpose electric light in the world. In June 2011, we submitted our A19 light to UL for certification and, in August 2011, received that certification. We are also planning to develop an R40 flood light for the United States commercial market and a smaller R63 light for the European market to be used in currently-installed recessed lighting fixtures. According to Strategies Unlimited, an independent research firm, the worldwide lighting market accounts for approximately $90 billion in annual sales.

We believe a significant contributing factor to our prospects are government regulations mandating the use of energy-efficient lighting, including the elimination of the production of traditional incandescent light bulbs in Europe by 2012 and in the United States in 2014, and regulations restricting the use of hazardous substances such as the mercury contained in CFLs. We believe these developments disrupt the well-entrenched lighting industry of past decades and, given the energy conservation and eco-friendly characteristics of our ESL lighting products, create significant opportunities for us to introduce our products into the market in place of incandescent bulbs, as well as CFLs and LEDs.

In February, 2014 we established a research and development facility in Berkeley, California to continue our manufacturing and development efforts. The facility also serves as our corporate headquarters.

In October 2011, we established a key strategic business relationship with Huayi Lighting Company Ltd. (“Huayi Lighting”), an experienced lighting products manufacturer. Under a manufacturing agreement, Huayi Lighting had agreed, under our direction, to produce substantially all of our ESL lighting products for resale to our customers over the next five years. In October, 2014 we terminated this relationship and executed a manufacturing agreement with Shenzhen Jinyi Display Units CO. LTD. (“Shenzhen”), a different outsourced manufacturer in China. Through this relationship, the manufacturer is responsible for sourcing, fabricating and assembling the required electronic components of our lights, sourcing the glass components from its suppliers and using its processes to assemble and package finished products. We have introduced our own manufacturing and quality control processes, as well as provided assistance regarding the sourcing of components and subassemblies during the development of the lines. In the first quarter of 2015, we successfully produced and shipped a limited supply of our R30 bulbs to a customer. Through our development efforts, we have filed eleven U.S. and related foreign patent applications, of which eleven patents have been granted covering important features of our current and planned lighting technology and products, and have accumulated over the years a substantial amount of technical know-how relating to our ESL technology.

1

During 2014, we focused on initiatives to continue the development of our manufacturing operations with Shenzhen. These initiatives also included continued efforts to work with Shenzhen to refine the manufacturing processes, raw materials sourcing and developing quality control testing necessary for quantity manufacturing. Our progress has been limited, primarily due to lack of adequate funding necessary to execute our business plan. These initiatives are ongoing and, as a result, we had no revenues in 2014 and 2013. We anticipate recognizing limited revenues in 2015.

As of April 15, 2015, we operate through the services of consultants to us, including our Chief Executive Officer and Chief Financial Officer as well as sales, marketing and engineering consultants.

Corporate Information

We were incorporated under the laws of the State of California in August 1996 under the name of Telegen Corporation. In late 2004, we began research and product development on our lighting technology and, in May 2008, changed our name to Vu1 Corporation to better reflect this business focus. Our principal executive offices are located at 1001 Camelia Street Berkeley, California 94710 and our telephone number is (855) 881-2852. Our Internet website address is http://www.vu1.com. The information on our website is not incorporated by reference into this Annual Report.

Overview of the Lighting Market

Traditional incandescent light bulbs are inefficient because they convert only about 5% of the energy they consume into visible light, with the rest emerging as heat. CFLs use excited gases, or plasmas, to achieve a higher energy conversion efficiency of about 20%. However, the color rendering index, or CRI, of most fluorescent bulbs – in other words, how good their color is compared to an ideal light source – is inferior to that of an incandescent bulb. CFLs also pose environmental concerns because they have historically contained mercury. By avoiding the heat and plasma-producing processes of incandescent bulbs and CFLs, LEDs can have substantially higher energy conversion efficiencies. Current LEDs are very small in size (about one square millimeter) and are extremely bright. Having been developed in the 1980s, they are already employed in various specialty lighting products, such as traffic lights, billboards, replacements for neon lighting and as border or accent lighting. However, the high operating temperatures and intense brightness of LEDs may make them less desirable for general illumination and diffuse lighting applications.

The key design features of our ESL lighting products, on the other hand, are that they are energy efficient, fully dimmable, illuminate immediately when switched on and have a color quality or CRI that is warm and similar to incandescent light. In addition, our lights do not contain mercury, a feature which will ease disposal. If our efforts are successful, we believe that our lighting products could begin to be used for applications currently addressed by incandescent bulbs, CFLs and LEDs.

We believe a significant contributing factor to our prospects are government regulations mandating the use of energy-efficient lighting, including the elimination of the production of traditional incandescent light bulbs in Europe by 2012 and in the United States by 2014, and regulations restricting the use of hazardous substances such as the mercury contained in CFLs. We believe these developments disrupt the well-entrenched lighting industry of past decades and, given the energy conservation and eco-friendly characteristics of our ESL lighting products, create significant opportunities for us to introduce our products into the market in place of incandescent bulbs, as well as CFLs and LEDs. Unlike LEDs, our lights also work with existing lighting fixtures without modification.

Our Competitive Advantages

We believe our position in the lighting market is the direct result of our technological innovation. We have built an intellectual property portfolio around our ESL technology and are working with our strategic product manufacturer to prepare for large scale commercial production and to launch our lighting products into the marketplace. Our key competitive advantages include:

2

Lighting Qualities. We believe our current and planned ESL lighting products offer potential advantages over competing lighting technologies including increased energy efficiency, longer product lifetime, environmentally safer and toxin-free disposal, superior light quality and lower usage cost as a percentage of the lights’ extended lifetime.

Proprietary Technology. Through our internal development efforts, we have filed eleven U.S. and related foreign patent applications, of which nine patents have been granted covering important features of our current and planned lighting technology and products, and have accumulated over the years a substantial amount of technical know-how relating to our ESL technology.

Strategic Manufacturing Relationship. We have established a key strategic relationship with Shenzhen, an experienced lighting products manufacturer. Under a manufacturing agreement executed in 2014, Shenzhen has agreed, under our direction, to produce substantially all of our ESL lighting products for resale to our customers.

Experienced Management. Our executive officers and directors have significant experience in developing and executing a “go-to-market” business model in a competitive, high growth industry. In addition, our management team has assembled highly-skilled technical personnel in the United States to conduct ongoing research and product development of new lighting products and next-generation technologies.

Our Growth Strategy

Our primary growth strategy is to accelerate the introduction of our lighting products into the commercial and residential general illumination market with the goal of obtaining widespread marketplace adoption over the next two years. In support of this objective, we are pursuing a multi-channel sales, marketing and distribution strategy, which includes efforts to establish business relationships with “big box” retailers, electrical and lighting distributors and municipal utilities.

In addition to our R30 reflector light, which received UL certification in October 2010, we are currently developing our version of the standard Edisonian A19 screw-in light (and its European equivalent, the A60), the most common general purpose electric light in the world. In June 2011, our A19 light was submitted to UL for safety certification and, in August 2011, received that certification. We are also developing an R40 flood light for the United States commercial market and a smaller R63 light for the European market to be used in currently-installed recessed lighting fixtures. According to Strategies Unlimited, an independent research firm, the worldwide lighting market accounts for approximately $90 billion in annual sales.

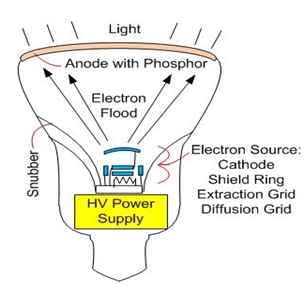

Our Lighting Technology

Our light uses a form of cathode-ray tube. It has an electron source and a power supply that supplies power to the electron source, as well as high voltage to accelerate the electrons toward the anode, where the electrons stimulate light emission from phosphors.

Electron Source. Our light generates a broad flood of high-energy electrons for evenly exciting the anode. The lights use a hot (thermionic) cathode having a flat disc emissive surface surrounded by a cold shield ring. A positively-biased extraction grid close to the cathode surface provides a high field to extract electrons from the cathode. A diffusion grid above the extraction grid provides a low-field zone allowing the electrons to be distributed evenly across the anode.

Power Supply. The power supply transforms power received through a connector from a fixture into three voltages. One voltage powers a heating filament that heats the cathode to a desired temperature to enhance electron emission. A second voltage biases both the extraction and diffusion grids, providing the high field that pulls electrons from the cathode and a low field that spreads the electrons. The third voltage is the several thousand volts provided through a snubber and a conductive coating inside the glass light structure to the anode; this voltage accelerates the electrons so the electrons can stimulate phosphors into emitting light. The power supply is able to respond to dimmers by reducing the anode voltage, thereby reducing phosphor stimulation and light output.

3

Anode. The anode is a thin conductive layer of aluminum, with a phosphor layer. Accelerated electrons stimulate light emission from the phosphors. Our white lights have a mixture of three phosphors, two of which (blue and green) are zinc-based, and a third (red) is a europium-doped phosphor. Virtually any color can be produced by choosing an appropriate mix of one or more known phosphors.

Our Lighting Products

The key design features of our current and planned lighting products are that they are energy efficient, fully dimmable, illuminate immediately when switched on and have a color quality that is warm and similar to incandescent light. Our lighting products do not contain mercury, a feature which will ease disposal.

We are continuing to refine the design of our planned products to maximize their efficiency, and we expect there will be adjustments to our current designs. If these efforts are successful, we believe that our lighting products could begin to be used for applications currently addressed by incandescent bulbs, CFLs and LEDs.

A list and description of each of our current and planned lighting products is set forth below:

|

Model Shape/Size

|

General Description

|

|

R30

|

U.S. reflector light for recessed lighting fixtures. This is the most popular size reflector.

|

|

A19

|

U.S. standard Edisonian screw-in light. This is the most common general purpose electric light in the world.

|

|

R40

|

U.S. reflector flood light for recessed lighting fixtures. This is the second largest selling reflector.

|

|

R95

|

European version of R30 reflector (220 volt).

|

|

A60

|

European standard version of A19 Edisonian screw-in light (220 volt).

|

|

R125

|

European version of R40 reflector flood light (220 volt).

|

|

R20/R63

|

U.S. and European reflector.

|

|

PAR38

|

U.S. and European spot reflector primarily for outdoor use.

|

In the future, we expect the retail price of our R30 reflector light and our other lighting products to be established by “big box” retailers and electrical and lighting distributors.

Product Development

In February, 2014, we established our product, manufacturing and quality control development efforts in the United States and focused on the application of ESL technology on the requirements of our initial product, an R30 size light. The R30 size light is used primarily in lighting fixtures that are recessed in the ceiling of commercial and residential buildings and are commonly referred to as “recessed can fixtures.” We continued our development work on the technology to refine the prototype with the miniaturization of the electronics and improvements to the efficiency of the product and the design and implementation of the processes required for manufacturing the light. We also focused on the development of quality control over the sourcing and manufacturing processes of Shenzhen. We continue to work with Shenzhen to refine the production processes and develop the supply chain for the components used in the manufacturing of our bulbs. We have also hired consultants in the United States and in China to assist Shenzhen with the manufacturing processes and quality control of the manufacturing. This effort will continue in 2015.

4

During the second quarter of 2010, we submitted the R30 light for safety certification to UL and, in October 2010, we received certification. We are continuing to refine the size of the light, further miniaturize the electronics and improve the manufacturing processes to enable us to produce the product at commercially viable levels.

During the fourth quarter of 2010, we began developing our version of the standard Edisonian A19 screw-in light (and its European equivalent, the A60), the most common general purpose electric light in the world. This size light is used in ordinary household lamps and non-recessed ceiling fixtures. In December 2010, we successfully developed a working prototype of this light. We are continuing to refine the prototype with the miniaturization of the electronics and improvements to the efficiency of the product. In June 2011, we submitted our A19 light to UL for safety certification and, in August 2011, received that certification. We are also developing an R40 flood light for the United States commercial market and a smaller R63 light for the European market to be used in currently-installed recessed lighting fixtures.

Our emphasis on the development of our planned products, the additional manufacturing processes required by our product manufacturer, the distribution, marketing and branding of products and the development of sales channels relating to our lighting products will command management’s primary attention during the next 12 months. It will also comprise the primary use of our financial resources. In 2015, our success will depend on our ability to reach commercial manufacturing levels for our R30 and A19 lights, generate market awareness and acceptance of our current and planned lighting products, protect our technology through patents and trade secrets, and develop our planned products to meet industry standards. If we are unable for technological, financial, competitive or other reasons to successfully take these steps, our business and operations will be adversely affected.

Target Markets and Customers

We are initially targeting the U.S. R30 and R40 reflector lighting market. According to recent reports, the U.S. residential market is comprised of 800 million recessed can lights with more than 140 million bulbs sold per year (“CFL Market Profile,” U.S. Department of Energy, March 2009, and “A Review of the Reflector Compact Fluorescent Lamps Technology Procurement Program: Conclusions and Results,” Pacific Northwest National Laboratory, May 2008). We intend to target the A19 standard Edisonian screw-in lighting market when our technology and manufacturing capabilities are fully established for large scale commercial production.

Significant lighting market drivers are product size, shape, cost, brightness, color rendering, mercury content, dimming capability and energy efficiency. As indicated above, we are directing our product development efforts with awareness of these features. Distribution in this market segment is primarily through electrical and lighting distributors (typically on a regional level) or directly from manufacturers to “big box” retailers.

Strategic Relationship with Product Manufacturer

In October 2011, we entered into a manufacturing agreement with Huayi Lighting, an experienced lighting products manufacturer. In October, 2014 we terminated this relationship and executed a manufacturing agreement with Shenzhen in China. Under this agreement, the manufacturer has agreed to produce substantially all of our R30 lights and future lighting products for resale to our customers. Through this agreement, the manufacturer is responsible for fabricating the required electronic components of our lights, sourcing the glass components from its multiple approved suppliers and using its established automated processes to assemble and package finished products. We are required to provide estimated volume requirements to the manufacturer during the term of the agreement. We are responsible to pay the upfront costs of specialized production tooling required by the manufacturer, and for the cost of additional machinery needed for its assembly lines, to produce our ESL lighting products. Payments to the manufacturer under the agreement are based on a negotiated price to source raw materials and manufacture the product, and payments are made by us in U.S. dollars when the products are delivered to the loading dock in Guangzhou, China for shipment to the United States. Our products will be transported to us in bulk via ocean by fully-insured logistics companies. For all lighting products manufactured by our third party manufacturer, the products are warranted to have been made to our required technical specifications and to fully meet applicable quality standards. In connection with the agreement, we granted our manufacturing partner limited license rights to use our technologies and intellectual property for the manufacture of our lights. The manufacturing agreement may be terminated at any time by the parties’ mutual agreement or by us in the event of a material breach under the agreement or failure to deliver products on a timely basis.

5

We expect to pay a duty on all lighting products that we import from China. This duty is expected to represent a 3.9% mark-up to factory invoice.

Sales, Marketing and Distribution

During 2014, we continued our marketing initiatives to determine our initial marketing strategy and begin branding and corporate positioning. Our marketing efforts have included market research to determine market size, competition, product features, consumer attitudes, pricing, certifications, government agencies, grants, target sales channels and retailers, branding and creation of initial marketing collateral. We have also had strategic and pre-contractual meetings with certain retailers and potential channel and distribution partners to determine levels of interest in our lighting products and ESL technology. We believe that the results of these meetings were positive, but no significant customer agreements have been entered into to date.

We intend to adopt inventory-carrying practices, together with the terms under which we sell our lighting products (including payment and delivery terms), that are customary in the lighting products markets.

Twenty states have enacted Conservation Improvement Programs (CIP). Through a CIP, electric and natural gas utilities are required to invest a portion of their state revenues in projects designed to reduce their customers' consumption of electricity and natural gas, and to generally improve resource efficiency. One form of CIP investment is conducting “give-aways” of energy efficient lighting products. Alternatively, some states provide cash rebates to lighting manufacturers, stores or directly to the consumer. We have met with a number of utilities and utility groups to determine interest in the promotion of ESL energy efficient lighting products. We believe that the results of these meetings were positive, but no agreements in this regard have been entered into to date.

Our technology has been featured on the Discovery Channel website, Popular Science magazine and website, CNET website and on The New York Times website.

Intellectual Property, Patents and Proprietary Rights

We have filed eleven U.S. and related foreign patent applications, of which nine patents have been granted. These patents cover important features of our current and planned lighting technology and products. We expect to apply for additional patent protection on our ESL technology and our manufacturing processes both domestically and internationally in the future. We believe that our technology has unique aspects that are patentable; however, there can be no assurance that any patent application will be granted or, if granted, that it will be defensible.

We protect our intellectual property rights through a combination of patent, trademark, trade secret laws and other methods of restricting disclosure, and requiring our independent consultants, strategic vendors and suppliers to sign non-disclosure agreements, as well as assignment of inventions agreements, when appropriate.

Raw Materials and Supplies

Development and production of our lighting products will require certain raw materials, including glass, electronics, coatings, certain chemicals and chemical compounds, plastic and packaging. Pursuant to our manufacturing agreement, our manufacturing partner assumed sole responsibility for sourcing these raw materials. Our manufacturing partner has advised us that it has multiple dedicated supply agreements with glass and other suppliers, and maintains relationships with alternative suppliers for raw materials and specialized component needs. We do not anticipate raw material shortages in the foreseeable future.

6

Research and Product Development

We spent approximately $798,000 during fiscal 2014 and approximately $647,000 during fiscal 2013, in our product development efforts.

During 2012, we established a U.S. based research and development team, and in February, 2014 we established a research and development center in the U.S. to develop new products for the lighting industry by taking advantage of the latest technology advancements. We expect to collaborate closely with our manufacturing partner and other subcontractors which use standard production processes to ensure that new lighting products can be produced quickly, and at the lowest cost and highest quality.

Government Regulation and Industry Certification

In October 2010, we obtained safety certification from UL for our R30 reflector light. This certification enables us to sell our ESL lighting products in the United States and Canada. In June 2011, we submitted our A19 light to UL for safety certification and, in August 2011, received that certification.

Any commercial lighting products that we develop in the future will require certifications from an independent third party testing laboratory prior to their sale. There is presently no Energy Star® certification standard for our products. In addition, we may be subject to other certifying agencies and other regulatory approvals. The approvals and certifications required will be determined based upon the markets that we enter. We are designing our lighting products to meet the standards for certification from independent third party laboratories, and we intend to submit an application to the appropriate testing laboratory once we have completed the necessary development and manufacturing processes required to obtain certification. We cannot predict whether we will obtain any future required certification from an independent third party testing laboratory or any other regulatory agency.

Our activities currently are subject to no particular regulation by governmental agencies other than that routinely imposed on corporate businesses, and no such regulation is now anticipated.

Competition

Our market segment is highly competitive and traditionally dominated by several large competitors such as General Electric Company, Philips Electronics NV and Osram Sylvania. These entities possess far more substantial financial, human and other resources than we do. There are also hundreds of small manufacturers of low-end products – many inexpensive and often poor performing compact fluorescent lamps. Many companies are now developing products utilizing solid-state LED technology. As energy efficient technologies are adopted, it is likely that the industry will continue to be dominated by large competitors who will often outsource manufacturing to smaller companies. Research will continue on incandescent type technologies such as halogen infrared reflecting. Abandoned technologies such as induction lighting may temporarily re-emerge. Based on meetings over the last four years with electric utilities, U.S. Department of Energy consultants, electrical distributors and major retailers, we have not identified any competitors with a similar technology to ESL.

Environmental Compliance

We are not aware of any material effects that compliance with federal, state, local or foreign environmental protection laws or regulations will have on our business. We have not expended material amounts to comply with any environmental protection laws or regulations and do not anticipate having to do so in the foreseeable future.

7

Employees

As of December 31, 2014, we had no employees. We have routinely used consultants in our U.S. operations and strategic vendors on a work-for-hire contract basis. We do not have any collective bargaining agreements in place and we consider relations with our key consultants to be good.

ITEM 1A. RISK FACTORS

Risks Related to Our Business and Industry

We have historically been a research and product development company. We have a limited operating history with minimal revenue to date, so it may be difficult to evaluate our business and prospects. We also received a going concern qualification in our 2014 audit.

We have been primarily engaged during the last eight years in the research and development of our lighting products, and have incurred significant operating losses. During 2014, we focused on initiatives to develop our manufacturing operations with Shenzhen. These initiatives also included continued efforts to work with the manufacturer to refine the manufacturing processes and developing quality control testing necessary for quantity manufacturing. Our progress has been limited, primarily due to lack of adequate funding necessary to execute our business plan. These initiatives are ongoing and, as a result, we had no revenues in 2014 or 2013. We currently depend on third-party financing to fund our operations. We have a very limited operating history upon which an investor can evaluate our business and prospects, and we may never generate significant revenue or achieve net income. Peterson Sullivan, LLP, our independent registered public accounting firm, in its opinion on our financial statements for the year ended December 31, 2014, raised substantial doubt about our ability to continue as a going concern due to our net losses and negative cash flows from operations and other factors.

We have incurred historical losses and, as a result, may not be able to generate profits, support our operations or establish a return on invested capital, which can have a detrimental effect on the long-term capital appreciation of our common stock.

We incurred a net loss in 2014 of $3.0 million and had an accumulated deficit of $91.4 million as of December 31, 2014. We cannot predict when or whether we will ever realize a profit or otherwise establish a return on invested capital. Our business strategies may not be successful and we may never generate significant revenues or profitability, in any future fiscal period or at all.

Creditors have obtained legally enforceable judgments against us on approximately $1.3 million related to the unsecured Convertible Debenture formally held by the judgment holders.

On June 11, 2014, four holders of our Convertible Debentures totaling $705,900 in principal plus accrued interest of $218,215 as of December 31, 2014 filed a motion seeking summary judgment with the Supreme Court of the State of New York. The case was heard on July 31, 2014 and the court granted their request and on August 20, 2014 issued a judgment in their favor for the full amount of principal and interest, plus certain expenses. We have made attempt to work with the judgment holders and their attorney to attempt to find a settlement agreeable to both parties, but no agreement has been reached. The judgment holders have the right to levy the judgment on our bank accounts, intellectual property and patents and other assets at any time. In April, 2015 the judgment holders placed a levy on all of our intellectual property, demanding that we turn over our patents, trade secrets, manufacturing methods and other intellectual property.

On December 22, 2014, one of the holders of our Convertible Debentures totaling $294,125 plus accrued interest and costs of $77,681 obtained a judgment in their favor for the full amount of principal, interest and costs.

8

We are presently in default on approximately $0.24 million of principal of our unsecured, Convertible Debentures.

As of the date of this annual report, the outstanding principal amount of approximately $0.24 million plus accrued interest and penalties under our original issue discount convertible debentures is due and owing by us. We have been in default to the holders of the debentures since June 22, 2013, when the debentures matured. We continue to not have sufficient financial resources, or the ability to arrange financing, to pay the outstanding amount of the debentures at this time. Our failure to pay the outstanding amount when due last year has resulted in our obligation to pay holders interest at the default rate of 18% per year and to pay a mandatory default amount of an additional 10% of the outstanding principal amount of the debentures. Although we have periodically discussed a work-out with some debenture holders, no such agreement currently exists. There can be no assurance that debenture holders have not already or will not in the future take legal action against us to collect the indebtedness due and owing under the debentures or initiate or join in a bankruptcy or insolvency case or proceeding relating to us. Should debenture holders take any such actions, our company will be seriously impacted and we may not be able to continue in business. See Footnote 5 in the Notes to the Consolidated Financial Statements contained elsewhere in this report.

We have a number of technology issues to resolve before we will be able to successfully manufacture a full line of commercially viable lighting products.

Although we have completed initial engineering and obtained UL certification of our initial R30 reflector light, further development work and third-party testing will be necessary before the technology can be deployed and production of a full line of lighting products can be commenced. If we are unable to solve current and future technology issues, we may not be able to offer commercially viable products. In addition, if we encounter difficulty in solving technology issues, our research and development costs could increase substantially and our development and production schedules could be significantly delayed.

We have experienced delays in executing our business plan, and further delays will reduce the likelihood that we will be able to manufacture lighting products or generate sufficient revenue to stay in business.

We have previously experienced delays in executing our business plan. These delays are attributable to a number of factors, including:

|

·

|

unanticipated difficulties and increased expenses in developing our ESL technology,

|

|

·

|

unanticipated difficulties in establishing large scale commercial manufacturing, quality control and sourcing processes, and

|

|

·

|

our inability to obtain funding in a timely manner.

|

In the future, we may experience delays caused by these and other factors. Our business must be viewed in light of the problems, expenses, complications and delays frequently encountered in connection with the development of new technologies, products, markets and operations. If we are unable to anticipate or manage challenges confronting our business in a timely manner, we may be unable to continue our operations.

We must successfully develop, introduce, market and sell lighting products and manage our operating expenses.

To be a viable business, we must successfully develop, introduce, market and sell products and manage our operating expenses. Many of our lighting products are still in development and are subject to the risks inherent in the development of technology products, including unforeseen delays, expenses, patent challenges and complications frequently encountered in the development and commercialization of technology products, the dependence on and attempts to apply new and rapidly changing technology, and the competitive environment of the industry. Many of these events are beyond our control, such as unanticipated development requirements, delays and difficulties with obtaining third-party certification, delays in submitting documentation for and being granted patents and establishing manufacturing and distribution relationships. Our success also depends on our ability to maintain high levels of employee utilization, manage our production costs, sales and marketing costs and general and administrative expenses, and otherwise execute on our business plan. We may not be able to effectively and efficiently manage our development and growth. Any inability to do so could increase our expenses and negatively impact our results of operations.

9

We rely solely on third party manufacturers to manufacture the ESL lighting products we sell to customers and to source the required raw materials.

Our business prospects depend significantly on our ability to obtain ESL lighting products for sale to our customers. Our manufacturing agreement with our manufacturing partner provided us with a single source for our ESL lights. Through this agreement, Shenzhen is responsible for fabricating the required electronic components of our lights, sourcing the glass components from its suppliers and using its established automated processes to assemble and package finished products. Our outsourced manufacturing partner is located in the People’s Republic of China, where shipments of product to us could be delayed, rerouted, lost or damaged. Our inability to obtain finished products from our third party manufacturer in accordance with our required technical specifications and on a timely basis due to shipping delays, manufacturing problems or its failure to obtain required raw materials would have a material adverse effect on our revenue from product sales, as well as on our ability to support our customers’ purchase requirements, which could result in loss of customers and damage to our reputation. We may also be subject to the risk of fluctuations in raw material prices, since our arrangement with our manufacturing partner provides that increases and decreases in the prices will affect the negotiated prices of purchase orders placed.

We may face additional barriers and tariffs as a result of importing our lighting products from China, which could increase our prices and make our products less desirable.

We expect to pay a duty on all lighting products that we import from China. This duty is expected to represent a 3.9% mark-up to factory invoice. We will also bear related importing costs such as customs inspection fees and ocean freight charges. In the future, China and the United States may create additional barriers to business between our China-based product manufacturer and us, including new tariffs, costs, restrictions, controls or embargos that could negatively impact our business and operating results. New or increased tariffs would likely result in higher prices (and potentially lower sales volumes) and lower operating margins on our products.

We rely heavily on a few consultants, the loss of whom could have a material adverse effect on our business, operating results and financial condition.

Our future success will depend in significant part upon the continued services of our executive officers and directors and certain key consultants, and our ability to attract, assimilate and retain highly qualified technical, managerial and sales and marketing personnel when needed. Competition for quality personnel is intense, and there can be no assurance that we can retain our existing key personnel or that we will be able to attract, assimilate and retain such employees in the future when needed. The loss of key personnel or the inability to hire, assimilate or retain qualified personnel in the future could have a material adverse effect on our business.

We rely on outside vendors to manage certain key business processes, and any failure by them to perform will negatively affect our business.

We have outsourced certain of our key business processes. If any of our service providers fail to perform at a satisfactory level, our business development will be negatively affected and delayed, and our reputation may be harmed.

Our future operating results are difficult to predict; thus, the future of our business is uncertain.

Due to our limited operating history and the significant development and manufacturing objectives that we must achieve to be successful, our quarterly and annual operating results are difficult to predict and are expected to vary significantly from period to period. In addition, the amount and duration of losses will be extended if we are unable to develop and manufacture our products in a timely manner. Factors that could inhibit our product development, manufacturing and future operating results include:

10

|

·

|

failure to solve existing or future technology-related issues in a timely manner,

|

|

·

|

failure to obtain sufficient financing when needed,

|

|

·

|

failure to secure key manufacturing or other strategic business relationships, and

|

|

·

|

competitive factors, including the introduction of new products, product enhancements and the introduction of new or improved technologies by our competitors, the entry of new competitors into the lighting markets and pricing pressures.

|

We face currency risks associated with fluctuating foreign currency valuations.

Although we use U.S. dollars to pay our outsourced manufacturing partner, increases in the value of the Chinese Yuan Renminbi would have an adverse affect on their manufacturing costs and therefore our bulb cost may be adversely affected. To date, we have not entered into foreign currency contracts or other currency-related derivatives to mitigate the potential impact of foreign currency fluctuations.

Because we are smaller and have fewer financial resources than most of our competitors, we may not be able to successfully compete in the very competitive lighting industry.

The lighting industry is very competitive and we expect this competition to continue to increase. The general illumination market segment within the lighting industry is dominated by a number of well-funded multi-national companies such as General Electric Company, Phillips Electronics NV and Osram Sylvania, that have established products and are developing new products that compete with our current and planned lighting products. We may not be able to compete effectively against these or other competitors, most of whom have substantially greater financial resources and operating experience than we do. Many of our current and future competitors may have advantages over us, including:

|

·

|

well established products that dominate the market,

|

|

·

|

longer operating histories,

|

|

·

|

established customer bases,

|

|

·

|

substantially greater financial resources,

|

|

·

|

well established and significantly greater technical, research and development, manufacturing, sales and marketing resources, capabilities and experience, and

|

|

·

|

greater name recognition.

|

Our current and potential competitors have established, and may continue to establish in the future, cooperative relationships among themselves or with third parties that would increase their market dominance and negatively impact our ability to compete with them. In addition, competitors may be able to adapt more quickly than we can to new or emerging technologies and changes in customer needs, or to devote more resources to promoting and selling their products. If we fail to adapt to market demands and to compete successfully with existing and new competitors, our results of operations could be materially adversely affected. The market for lighting technology is changing rapidly and there can be no assurance that we will be able to compete, especially in light of our limited resources. There can be no assurance that any of our current or planned lighting products can compete successfully on a cost, quality or market acceptance basis with competitors’ products and technologies.

11

We depend on our intellectual property. If we are unable to protect our intellectual property, we may be unable to compete and our business may fail.

Our success and ability to develop our technology and create products and become competitive depend to a significant degree on our ability to protect our proprietary technology, particularly any patentable material. We rely on a combination of patent, trademark, trade secret and other intellectual property laws, nondisclosure agreements and other protective measures to preserve our rights to our technology. In addition, any intellectual property protection we seek may not preclude competitors from developing products similar to ours. In addition, the laws of certain foreign countries do not protect intellectual property rights to the same extent as do the laws of the United States.

We do not currently have sufficient available resources to defend a lawsuit challenging our intellectual property rights or to prosecute others who may be infringing our rights. Accordingly, even if we have strong intellectual property rights and patent rights, we may not be able to afford to engage in the necessary litigation to enforce our rights.

In April, 2015 certain judgment holders placed a levy on all of our intellectual property, demanding that we turn over our patents, trade secrets, manufacturing methods and other intellectual property.

We compete in industries where competitors pursue patent prosecution worldwide and patent litigation is customary. At any given time, there may be one or more patent applications filed or patents that are the subject of litigation, which, if granted or upheld, could impair our ability to conduct our business without first obtaining licenses or granting cross-licenses, which may not be available on commercially reasonable terms, if at all. We have several patent applications pending in the United States and internationally and we expect to file additional patent applications; however, none of these patents may ever be issued. We do not perform worldwide patent searches as a matter of custom and, at any given time, there could be patent applications pending or patents issued that may have an adverse impact on our business, financial condition and results of operations.

Other parties may assert intellectual property infringement claims against us, and our products may infringe on the intellectual property rights of third parties. Intellectual property litigation is expensive and time consuming and could divert management’s attention from our business and could result in the loss of significant rights. If there is a successful claim of infringement, we may be required to develop non-infringing technology or enter into royalty or license agreements which may not be available on acceptable terms, if at all. In addition, we could be required to cease selling any of our products that infringe on the intellectual property rights of others. Successful claims of intellectual property infringement against us may have a material adverse effect on our business, financial condition and results of operations. Even successful defense and prosecution of patent suits is costly and time consuming.

We rely in part on unpatented proprietary technology, and others may independently develop the same or similar technology or otherwise obtain access to our unpatented technology. To protect our trade secrets and other proprietary information, we require employees, consultants, advisors and strategic partners to enter into confidentiality agreements. These agreements may not provide meaningful protection for our trade secrets, know-how or other proprietary information in the event of any unauthorized use, misappropriation or disclosure of those trade secrets, know-how or other proprietary information. In particular, we may not be able to protect our proprietary information as we conduct discussions with potential strategic partners. If we are unable to protect the proprietary nature of our technologies, it may have an adverse impact on our business, financial condition and results of operations.

Failure to obtain and maintain industry certification for our lighting products could cause an erosion of our current competitive strengths.

We are designing our lighting products to be UL or ETL (an Intertek listed mark for product compliance to North American safety standards) compliant and intend to seek Energy Star certification, as well as appropriate certifications in the European Union and in other countries. UL or ETL compliance certification is a key standard in the lighting industry, and if we fail to obtain or maintain this standard we may not have any market interest for our products. We may not obtain this certification or we may be required to make changes to our lights, which would delay our commercialization efforts and would negatively harm our business and our results of operations.

12

Rapid technological changes and evolving industry standards could result in our lighting products becoming obsolete and no longer in demand.

The lighting industry is characterized by rapid technological change and evolving industry standards and is highly competitive with respect to timely product innovation. The introduction of lighting products embodying new technology and the emergence of new industry standards can render existing products and technologies obsolete and unmarketable. Our success will depend in part on our ability to successfully develop commercial applications for our technology, anticipate and respond to technology developments and changes in industry standards, and obtain market acceptance on any products we introduce. We may not be successful in the development of our ESL technology, and we may encounter technical or other serious difficulties in our development or commercialization efforts that would materially and adversely affect our results of operations.

If we fail to maintain proper and effective internal controls in the future, our ability to produce accurate and timely financial statements could be impaired, which could harm our operating results, investors’ views of us and, as a result, the value of our common stock.

Ensuring that we have effective internal control over financial reporting and disclosure controls and procedures in place is a costly and time-consuming effort that needs to be frequently evaluated. As a public company, we conduct an annual management assessment of the effectiveness of our internal controls over financial reporting in compliance with Section 404 of the Sarbanes-Oxley Act of 2002. As a smaller reporting company, we are not currently required to receive a report from our independent registered public accounting firm addressing the effectiveness of our internal controls over financial reporting. As we grow, it may be necessary in the future to update our internal controls over financial reporting on the basis of periodic reviews. If we are not able to comply with the requirements of Section 404, or if we (or our independent registered public accounting firm) identify deficiencies in our internal controls over financial reporting that could rise to the level of a material weakness, we may not be able to complete our evaluation, testing and any required remediation in a timely fashion. During the evaluation and testing process, if we identify one or more material weaknesses in our internal controls over financial reporting, we will be unable to assert that our internal controls over financial reporting are effective. If we are unable to assert that they are effective (or if our independent registered public accounting firm is unable in the future to express an opinion on the effectiveness of our internal controls over financial reporting), we could be subject to investigations or sanctions by the SEC or other regulatory authorities, and we could lose investor confidence in the accuracy and completeness of our financial reports, which could cause an adverse effect on the market price of our common stock, our business, reputation, financial position and results of operation. In addition, we could be required to expend significant management time and financial resources to correct any material weaknesses that may be identified or to respond to any regulatory investigations or proceedings.

Risks Related to our Securities

Our historic stock price has been volatile and the future market price for our common stock is likely to continue to be volatile. This may make it difficult for you to sell our common stock for a positive return on your investment.

The public market for our common stock has historically been volatile. Any future market price for our shares is likely to continue to be volatile. This price volatility may make it more difficult for you to sell shares when you want at prices you find attractive. The stock market in general has experienced extreme price and volume fluctuations that have often been unrelated or disproportionate to the operating performance of specific companies. Broad market factors and the investing public’s negative perception of our business may reduce our stock price, regardless of our operating performance. Further, the market for our common stock is limited and we cannot assure you that a larger market will ever be developed or maintained. Market fluctuations and volatility, as well as general economic, market and political conditions, could reduce our market price. As a result, these factors may make it more difficult or impossible for you to sell our common stock for a positive return on your investment.

13

Our management and SAM Special Opportunities Fund, L.P. own a substantial amount of our stock and are capable of influencing our affairs.

As of December 31, 2014, our executive officers and directors (and their respective affiliates) beneficially owned approximately 16.3% of our outstanding common stock, with SAM Advisors, LLC, an investment advisor controlled by William B. Smith, our Chairman, beneficially owning approximately 8.1% of our outstanding common stock. As a result, these shareholders substantially influence our management and affairs and, if acting together, control most matters requiring the approval by our shareholders including the election of directors, any merger, consolidation or sale of all or substantially all of our assets and any other significant corporate transactions. The concentration of ownership may delay or prevent a change of control at a premium price.

Our articles of incorporation contain authorized, unissued preferred stock which, if issued, may inhibit a takeover at a premium price that may be beneficial to you.

Our articles of incorporation allow us to issue up to 10,000,000 shares of preferred stock without further stockholder approval and upon such terms and conditions, and having such rights, preferences, privileges and restrictions as the board of directors may determine. The rights of the holders of common stock will be subject to, and may be adversely affected by, the rights of holders of any preferred stock that may be issued in the future. In addition, the issuance of preferred stock could have the effect of making it more difficult for a third party to acquire control of, or of discouraging bids for control of our company. This could limit the price that certain investors might be willing to pay in the future for shares of common stock. We have no current plans to issue any shares of preferred stock.

Shares of stock issuable pursuant to our stock options, warrants, convertible debentures and underwriters’ warrants may adversely affect the market price of our common stock.

As of December 31, 2014, we have outstanding under our 2007 Stock Incentive Plan stock options to purchase 829,936 shares of common stock, outstanding warrants to purchase 6,222,228 shares of common stock and outstanding convertible debentures to acquire 1,304,631 shares of common stock. The exercise or conversion of these securities and sales of common stock issuable pursuant to them, would reduce a stockholder’s percentage voting and ownership interest.

The stock options, warrants and convertible debentures are likely to be exercised when our common stock is trading at a price that is higher than the exercise or conversion price of these securities, and we would be able to obtain a higher price for our common stock than we will receive under such securities. The exercise or conversion, or potential exercise or conversion, of these stock options, warrants and convertible debentures could adversely affect the market price of our common stock and adversely affect the terms on which we could obtain additional financing, if needed.

The large number of shares eligible for future sale may adversely affect the market price of our common stock.

The sale, or availability for sale, of a substantial number of shares of common stock in the public market could materially and adversely affect the market price of our common stock and could impair our ability to raise additional capital through the sale of our equity securities. At December 31, 2014, there were 12,950,384 shares of common stock issued and outstanding. Of these shares, approximately 12,187,734 are freely transferable. Our executive officers and directors beneficially own 2,304,174 shares, which would be eligible for resale, subject to the volume and manner of sale limitations of Rule 144 under the Securities Act. An additional 762,650 shares are “restricted shares,” as that term is defined in Rule 144, and are eligible for sale under the provisions of Rule 144.

Our common stock is currently considered a “penny stock” and may be difficult to sell unless we obtain a Nasdaq listing.

Our common stock is subject to certain rules and regulations relating to “penny stock.” A “penny stock” is generally defined as any equity security that has a price less than $5.00 per share and that is not quoted on a national securities exchange such as Nasdaq. Being a penny stock generally means that any broker who wants to trade in our shares (other than with established clients and certain institutional investors) must comply with certain “sales practice requirements,” including delivery to the prospective purchaser of the penny stock a risk disclosure document describing the penny stock market and the risks associated with it. These penny stock rules make it more difficult for broker-dealers to recommend our common stock and, as a result, our stockholders may have difficulty in selling their shares in the secondary trading market. This lack of liquidity may also make it more difficult for us to raise capital in the future through the sale of our equity securities.

14

We do not intend to pay cash dividends on our common stock, so any return on investment must come from appreciation.

We have never declared or paid any cash dividends on our common stock and do not intend to pay cash dividends in the foreseeable future. We intend to invest all future earnings, if any, to fund our growth. Therefore, any investment return in our common stock must come from increases in the trading price of our common stock.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable

ITEM 2. PROPERTIES

We do not own any real property.

Effective February 1, 2014 we entered into a two year lease for our research and development facility and corporate headquarters, consisting of approximately 4,600 square feet of office and light industrial space located in Berkeley, California in the United States. Our lease obligations are $60,000 and $5,000 for the years ended December 31, 2015 and 2016, respectively.

As of December 31, 2013, our corporate headquarters consisted of approximately 200 square feet, located in New York, New York, for total rent per month of $2,035.

ITEM 3. LEGAL PROCEEDINGS

On June 11, 2014, four holders of our Convertible Debentures totaling $705,900 in principal plus accrued interest of $218,215 as of December 31, 2014 filed a motion seeking summary judgment with the Supreme Court of the State of New York. The case was heard on July 31, 2014 and the court granted their request and on August 20, 2014 issued a judgment in their favor for the full amount of principal and interest, plus certain expenses. We have made attempt to work with the judgment holders and their attorney to attempt to find a settlement agreeable to both parties, but no agreement has been reached. The judgment holders have the right to levy the judgment on our bank accounts, intellectual property and patents and other assets at any time. In April, 2015 the judgment holders placed a levy on all of our intellectual property, demanding that we turn over our patents, trade secrets, manufacturing methods and other intellectual property. The principal and accrued interest have been reclassified on the balance sheet from Convertible Debentures and accrued interest to Judgment payable on the accompanying balance sheet at December 31, 2014.

On December 22, 2014, one of the holders of our Convertible Debentures totaling $294,125 plus accrued interest and costs of $77,681 obtained a judgment in their favor for the full amount of principal, interest and costs. The principal and accrued interest have been reclassified on the balance sheet from Convertible Debentures and accrued interest to Judgment payable on the accompanying balance sheet at December 31, 2014.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable

15

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

PRICE RANGE OF COMMON STOCK

Our common stock is quoted on the OTC Bulletin Board under the trading symbol VUOC. The following table sets forth the range of high and low trading prices as reported by the OTC Bulletin Board for the periods indicated.

|

Year ended December 31,

|

||||||||||||||||

|

Quarter

|

2013

|

2014 | ||||||||||||||

|

High

|

Low

|

High

|

Low

|

|||||||||||||

|

First

|

$ | 2.75 | $ | 0.62 | $ | 1.38 | $ | 0.80 | ||||||||

|

Second

|

$ | 1.72 | $ | 1.16 | $ | 1.06 | $ | 0.67 | ||||||||

|

Third

|

$ | 1.78 | $ | 1.00 | $ | 0.90 | $ | 0.46 | ||||||||

|

Fourth

|

$ | 1.45 | $ | 1.00 | $ | 1.49 | $ | 0.55 | ||||||||

These quotations reflect inter-dealer prices, without retail mark-up, mark-down or commissions, and may not represent actual transactions.

The closing price of our common stock on April 15, 2015 was $0.62 per share.

As of April 15, 2015, we had 244 stockholders of record and approximately 2,800 beneficial owners of common stock.

Securities Authorized for Issuance Under Equity Compensation Plans

On October 26, 2007, our board of directors approved the Vu1 Corporation 2007 Stock Incentive Plan (the “Plan”). The stockholders approved the Plan on May 22, 2008. In March 2011, the board of directors increased the number of shares authorized for issuance under the Plan from 500,000 to a total of 1,000,000 shares. A majority of our stockholders approved the amendment to the Plan on October 10, 2011. On August 26, 2013 the board of directors increased the number of shares authorized for issuance under the 2007 Stock Incentive Plan by 1,500,000 shares to a total of 2,500,000 shares. We intend to seek stockholder approval in 2015. The following table gives information as of December 31, 2014, the end of our most recently completed fiscal year, about shares of common stock that may be issued upon the exercise of options, warrants and rights under the Plan.

|

Equity Compensation Plan Information

|

||||||||||||

|

Plan category

|

Number of

securities to

be issued upon

exercise of

outstanding

options, warrants

and rights

|

Weighted-average

exercise price

of outstanding

options, warrants

and rights

|

Number of

securities

remaining available

for future

issuance

under equity

compensation

plans

(excluding

securities

reflected in

column (a))

|

|||||||||

|

(a)

|

(b)

|

(c)

|

||||||||||

|

Equity compensation plans not approved by security holders

|

392,570 | $ | 0.73 | 750,000 | ||||||||

|

Equity compensation plans approved by security holders

|

595,088 | $ | 6.15 | 133,451 | ||||||||

|

Totals

|

595,088 | $ | 6.15 | 883,451 | ||||||||

A description of the Plan can be found in Note 9 to the Notes to Consolidated Financial Statements contained in this Annual Report.

16

Sales of Unregistered Securities

The following provides information regarding sales of equity securities by us during the fiscal year ended December 31, 2014, which were not registered under the Securities Act.

2014 Unit Offerings

From January 31, 2014 to July 10, 2014 we received gross proceeds of $680,000 from accredited investors at a price of $1.00 per unit and issued 680,000 shares of common stock and two-year warrants to purchase 680,000 shares of common stock at an exercise price of $1.25 per share.

From August 4 to December 17, 2014 we received gross proceeds of $585,000 from accredited investors at a price of $0.50 per unit and issued 1,170,000 shares of common stock and two-year warrants to purchase 1,170,000 shares of common stock at an exercise price of $0.75 per share.

On June 30, 2014 we issued 267,191 shares to an accredited investor upon the conversion of a Convertible Promissory Note as discussed in Note 8.

On June 22, 2014 we issued 125,160 shares of the Company's common stock to the holder in payment of accrued, unpaid interest under the Debenture for the period from December 23, 2013 to June 22, 2014.

On October 24, 2014 we issued 14,286 shares of the Company's common stock to the holder in payment of accrued, unpaid interest under the Debenture for the period from December 23, 2013 to June 22, 2014.

On December 22, 2014 we issued 117,650 shares of the Company's common stock to the holder in payment of accrued, unpaid interest under the Debenture for the period from June 23, 2014 to December 22, 2014.