Attached files

| file | filename |

|---|---|

| EX-5.1 - EX-5.1 - TRIBUNE MEDIA CO | d900252dex51.htm |

| EX-1.1 - EX-1.1 - TRIBUNE MEDIA CO | d900252dex11.htm |

| EX-23.1 - EX-23.1 - TRIBUNE MEDIA CO | d900252dex231.htm |

| EX-23.2 - EX-23.2 - TRIBUNE MEDIA CO | d900252dex232.htm |

Table of Contents

As filed with the Securities and Exchange Commission on April 20, 2015

Registration No. 333-203286

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT

UNDER THE

SECURITIES ACT OF 1933

Tribune Media Company

(Exact name of registrant as specified in its charter)

| Delaware | 4833 | 36-1880355 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

435 North Michigan Avenue

Chicago, Illinois 60611

(312) 994-9300

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Steven Berns

Executive Vice President and Chief Financial Officer

Tribune Media Company

220 East 42nd Street, 10th Floor

New York, New York 10017

(212) 210-2786

(Name, address, including zip code, and telephone number, including area code, of agent for service)

with copies to:

| Peter J. Loughran, Esq. Debevoise & Plimpton LLP 919 Third Avenue New York, NY 10022 (212) 909-6000 |

Michael W. Benjamin, Esq. Merritt S. Johnson, Esq. Shearman & Sterling LLP 599 Lexington Avenue New York, NY 10022 (212) 848-4000 |

Approximate date of commencement of proposed sale of the securities to the public:

As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of Each Class of Securities to be Registered |

Amount to be Registered(1) |

Proposed Aggregate |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee(3) | ||||

| Class A common stock, $0.001 par value per share |

10,626,083 | $61.53 | $653,822,887 | $75,975 | ||||

|

| ||||||||

|

| ||||||||

| (1) | Includes shares/offering price of shares that may be sold upon exercise of the underwriters’ option to purchase additional shares. |

| (2) | This amount represents the proposed maximum aggregate offering price of the securities registered hereunder. These figures are estimated solely for the purpose of calculating the amount of the registration fee pursuant to Rule 457(c) under the Securities Act of 1933. The price shown is the average of the high and low sales price for the registrant’s Class A common stock on April 6, 2015 as reported on the New York Stock Exchange. |

| (3) | Previously paid. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. The selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and neither we nor the selling stockholders are soliciting offers to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED APRIL 20, 2015

9,240,073 Shares

Tribune Media Company

Class A Common Stock

9,240,073 shares of Tribune Media Company Class A common stock are being sold by the selling stockholders identified in this prospectus. Tribune Media Company will not receive any of the proceeds from the sale of the shares being sold by the selling stockholders.

The Class A common stock of Tribune Media Company is listed on the New York Stock Exchange under the symbol TRCO. The last reported sale price of the Class A common stock on April 17, 2015 was $57.60 per share.

Investing in our common stock involves risks. See “Risk Factors” beginning on page 19 of this prospectus.

| Per Share |

Total | |||||||

| Public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions (1) |

$ | $ | ||||||

| Proceeds, before expenses, to the selling stockholders |

$ | $ | ||||||

| (1) | The underwriters will receive compensation in addition to the underwriting discount. See “Underwriting (Conflicts of Interest).” |

To the extent the underwriters sell more than 9,240,073 shares of Class A common stock, the underwriters have the option to purchase up to an additional 1,386,010 shares of Class A common stock from the selling stockholders at the public offering price less the underwriting discount.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares to purchasers on or about , 2015.

| Morgan Stanley | J.P. Morgan | |||

| Goldman, Sachs & Co. | Deutsche Bank Securities |

| BofA Merrill Lynch | Credit Suisse | Evercore ISI | Guggenheim Securities |

Prospectus dated , 2015

Table of Contents

| 1 | ||||

| 19 | ||||

| 43 | ||||

| 45 | ||||

| 46 | ||||

| 47 | ||||

| 48 | ||||

| 49 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

50 | |||

| 95 | ||||

| 115 | ||||

| 122 | ||||

| 145 | ||||

| 147 | ||||

| 149 | ||||

| 152 | ||||

| 158 | ||||

| Material U.S. Federal Tax Considerations for Non-U.S. Holders |

160 | |||

| 164 | ||||

| 173 | ||||

| 173 | ||||

| 173 | ||||

| F-1 | ||||

| F-2 | ||||

| F-4 |

Neither we, the selling stockholders nor the underwriters have authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectus we have prepared. Neither we, the selling stockholders nor the underwriters take responsibility for, nor can provide any assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date.

Table of Contents

This summary highlights certain information contained elsewhere in this prospectus. Because this is only a summary, it does not contain all of the information that may be important to you. For a more complete understanding of this offering, you should read the entire prospectus, including the consolidated financial statements and the related notes and the section entitled “Risk Factors” included elsewhere in this prospectus.

Unless otherwise indicated or the context otherwise requires, in this prospectus, references to “Tribune,” “Tribune Media,” the “Company,” “we,” “us” and “our” mean Tribune Media Company and its consolidated subsidiaries.

Company Overview

Tribune Media Company is a diversified media and entertainment business. It is comprised of 42 television stations that are either owned by us or owned by others, but to which we provide certain services, which we refer to as “our television stations,” along with a national general entertainment cable network, a radio station, a production studio, a digital and data technology business, a portfolio of real estate assets and investments in a variety of media, websites and other related assets. We believe our diverse portfolio of assets distinguishes us from traditional pure-play broadcasters through our ownership of high-quality original and syndicated programming, our ability to capitalize on revenue growth from our digital and data assets, cash distributions from our equity investments and revenues from our real estate assets.

Our business operates in the following two reportable segments:

| • | Television and Entertainment: Provides audiences across the country with news, entertainment and sports programming on Tribune Broadcasting local television stations and distinctive, high quality television series and movies on WGN America, including through content produced by Tribune Studios and its production partners. |

| • | Digital and Data: Provides innovative technology and services that collect and distribute video, music and entertainment data primarily through wholesale distribution channels to consumers globally. |

We also currently hold a variety of investments in cable and digital assets, including equity investments in Television Food Network, G.P. (“TV Food Network”) and CareerBuilder, LLC (“CareerBuilder”). In addition, we report and include under Corporate and Other the management of certain of our real estate assets, including revenues from leasing office and production facilities, as well as certain administrative activities associated with operating our corporate office functions and managing our predominantly frozen company-sponsored defined benefit pension plans.

Competitive Strengths

We believe that we benefit from the following competitive strengths:

Geographically diversified media properties in attractive U.S. markets.

We are one of the largest independent station owner groups in the United States based on household reach, and we own or operate local television stations in each of the nation’s top five markets and seven of the top ten markets by population. We have network affiliations with all of the major over-the-air networks, including American Broadcasting Company (“ABC”), CBS Corporation (“CBS”), FOX Broadcasting Company (“FOX”), National Broadcasting Company (“NBC”) and The CW Network, LLC (“CW”). We provide must-see programming, including the National Football League and other live sports, on many of our stations and local news to over 50 million U.S. households in the aggregate, as measured by Nielsen Media Research (“Nielsen”), representing approximately 44% of all U.S. households.

1

Table of Contents

In addition, we own a national general entertainment cable network, WGN America, which is distributed to approximately 73 million households nationally, as measured by Nielsen. WGN America provides us with a platform for launching original programming and exclusive syndication content. We believe that the combination of our broadcast stations and WGN America creates a differentiated distribution platform.

Core competency in metadata.

Our metadata powers the television listings and schedules for on-screen Electronic Program Guides (“EPG”) through cable and satellite providers via set-top boxes or other means and makes it possible to search for specific television episodes and series and set digital video recorder (“DVR”) recordings. It also powers the algorithms that make movie and music recommendations possible for popular on-demand video and streaming music services.

The demand from consumers and, therefore, distributors has grown for the metadata that we provide through Gracenote Video and Gracenote Music. Data is becoming more vital to businesses as it is used to make smarter decisions about investing in content and to provide enhanced measurement tools to drive advertising efficiency and effectiveness.

As consumer demand continues to increase, we believe we are well positioned to take advantage of this trend by adding scale to our existing business. The industry is highly fragmented by data set, region and service layer.

Strong cash flow generation.

Our core businesses have historically generated strong cash flows from operations. In 2014, our net cash provided by operating activities was $378 million, which includes $190 million of cash distributions received from our equity investments. In addition to the cash distributions accounted for within net cash provided by operating activities, cash flows from investing activities included $181 million of cash distributions from our equity investments, of which $160 million was from Classified Ventures, LLC (“CV”) related to the sale of its Apartments.com business. Our equity investments have historically provided substantial cash distributions annually. These strong cash flows provide us with the financial flexibility to pursue our strategies both through organic investments in our existing businesses and through accretive acquisition opportunities. We are making investments across our businesses, including in the acquisition of original content and the expansion of our digital and data businesses.

Opportunistically deploying capital to drive stockholder returns.

Our capital allocation policy is focused on driving returns for stockholders and investing in areas that are intended to drive growth in our profitability. In October 2014, we announced a $400 million stock repurchase program, under which we may repurchase from time to time up to a remaining $167 million of our outstanding Class A common stock. We have also announced an intention to pay regular quarterly cash dividends on our common stock of $0.25 per share, starting in the second fiscal quarter of 2015. See “Dividend Policy.”

Valuable minority investments, spectrum and real estate holdings.

We currently hold a variety of investments in cable and digital assets, including equity investments in TV Food Network and Career Builder. TV Food Network, of which we have a 31% interest, operates two 24-hour television networks, Food Network and Cooking Channel, as well as their related websites. Food Network is a fully distributed network in the United States with content distributed internationally. Cooking Channel is a digital-tier network, available nationally and airs popular off-Food Network programming as well as originally produced programming. Career Builder, of which we have a 32% interest, is a global leader in human capital solutions, helping companies target, attract and retain talent. Its website, CareerBuilder.com, is the largest job website in North America on the basis of both traffic and revenue. CareerBuilder operates websites in the United States, Europe, Canada, Asia and South America.

2

Table of Contents

We have spectrum holdings in numerous markets where there is expected to be high demand in the anticipated upcoming FCC auction of spectrum currently used by broadcast television stations. We are actively exploring our options to monetize our spectrum in that auction through potential sale, channel sharing arrangements, or relocation. The FCC has stated that it expects the auction to occur in 2016, though the timing of the auction and exactly how it will be administered is uncertain at this time.

We also own attractive real estate in key markets, including development rights for certain of our real estate assets. We actively manage our portfolio of real estate assets to drive value through the following initiatives:

| • | Maximize utility of our existing real estate footprint; |

| • | Generate revenues on excess space by leasing to third parties; |

| • | Opportunistically dispose of underutilized or non-essential properties; and |

| • | Develop vacant properties or properties with redevelopment options. |

Experienced management team with demonstrated industry experience.

Our senior management team has broad and diverse experience across their respective disciplines, with proven track records of success in the industry. Peter Liguori, our President and Chief Executive Officer, is an experienced media industry leader with a background in developing successful programming. Our organization consists of talented executives with expertise across finance, strategy, operations, regulatory matters and human resources. Our management team has a unified vision for the Company, which includes capitalizing on our current strengths and strategically investing in new initiatives and businesses to generate increased value for our stockholders.

Strategies

Our mission is to create, produce and distribute outstanding entertainment, news and sports content and digital data that inform, entertain, engage, and inspire millions of people every day. To achieve this mission, we are pursuing the following strategies:

Utilize the scale and quality of our operating businesses to increase value to our partners, advertisers, MVPDs, network affiliates, consumers and stockholders.

Our television station group reaches over 50 million households nationally, as measured by Nielsen, representing approximately 44% of all U.S. households. WGN America, our national general entertainment cable network, reaches approximately 62% of U.S. households and the digital networks we operate, Antenna TV and THIS TV, collectively reach approximately 90% of U.S. households. We also operate approximately 50 websites primarily associated with our television stations, which, in 2014, reached an average of 63 million unique visitors monthly, which increased to 87 million unique visitors in March 2015. Our metadata businesses feature information and content for approximately 6.7 million TV shows and movies and 200 million song tracks.

Through our extensive distribution network, we can deliver content through a multitude of channels. This ability to reach consumers across a broad geographical footprint is valuable for advertisers, multichannel video programming distributors (“MVPDs”) and affiliates alike as we connect consumers with their messaging and quality content.

WGN America is currently undergoing a transformation from a superstation to a fully distributed general entertainment cable network. Our strategy is to build a network that combines high quality, original programming as well as exclusive, highly-rated syndicated programming and feature films.

3

Table of Contents

Be the most valued source of local news and information in the markets in which we operate.

Local news is a cornerstone of our local television stations. We believe local news enjoys a competitive advantage relative to national news outlets due to its ability to generate immediate reporting, which is especially valuable when a breaking news story develops in a local market. We are also able to utilize our breadth of coverage to distribute local content on a national scale by sharing news stories on-air and digitally across Tribune-covered markets. Annually, we produce approximately 75,000 hours of news in our 33 U.S. markets. We also operate approximately 50 websites and approximately 125 mobile applications.

Continue to shift to a content ownership model that is designed to result in both the retention of a greater share of advertising revenue and allow us to participate in the longer tail of programming monetization.

As competition for media advertising spend continues to increase, we are focused on developing our Tribune Studios business to drive future growth by creating original content to be distributed across our WGN America and television station platforms, as well as on other streaming platforms such as Hulu or Netflix. We believe that retaining the rights associated with our content will provide us with a competitive advantage relative to broadcasters that rely primarily on licensed programming acquired from third-party syndicators. A shift away from licensing content from third parties to content ownership will provide us with new outlets, such as over-the-top (“OTT”), subscription video on demand (“SVOD”) and international rights through which to monetize programming. Owned programming that airs across our station group further allows us to retain a greater share of overall advertising revenue generated from such content.

Develop a leading global metadata business.

Having started with Tribune Media Services as our core metadata asset, we have been selectively acquiring both domestic and foreign metadata businesses in order to capitalize on our core competency in data and technology by driving increased scale in our business and providing deeper and richer global content solutions. Through such acquisitions, we expect to be able to provide improved services for current domestic customers and to compete for international customers through the use of innovative technologies that we anticipate will generate increased monetization opportunities of our data assets.

Disciplined management of operating costs and capital investment.

Our management team is focused on maintaining a disciplined cost management program, while ensuring that the Company is investing in the areas that are expected to continue to drive profitability growth.

Strategically identify and pursue acquisition opportunities to complement our organic growth strategy.

As a complement to our organic growth initiatives, we intend to continue to pursue a selective acquisition strategy that seeks to enhance our offerings and increase our scale. In evaluating prospective investment decisions, we assess the strategic fit, including application of our core competencies and projected cash returns, taking into consideration relevant regulations applicable to owners of broadcast television stations, but which do not apply to cable networks. We also believe there will be opportunities for us to continue to build scale and technology capabilities in our data businesses.

Maximize the long term value of our real estate assets.

We intend to maximize the long term value of our real estate assets primarily by employing best practices in the operation and management of our holdings and selectively forming strategic partnerships with knowledgeable local developers in certain markets where our assets are located.

4

Table of Contents

Recent Developments

Preliminary First Quarter 2015 Results

Our financial results for the first quarter of 2015 are not yet finalized. However, the following information reflects management’s current expectations with respect to our first quarter 2015 results.

Operating Revenues

We expect consolidated operating revenues for the three months ended March 29, 2015 to be approximately $472 million, an increase of $26 million, or 6%, as compared to the three months ended March 30, 2014.

Television and Entertainment segment revenues are expected to be approximately $410 million for the three months ended March 29, 2015, an increase of $10 million, or 2%, as compared to the three months ended March 30, 2014. This increase was primarily due to an expected increase in retransmission consent revenues and carriage fees of approximately $21 million, partially offset by an expected decline in core advertising revenues (local and national advertising revenues, excluding political revenues) of approximately $6 million. The decline in core advertising revenues was primarily impacted by an approximate $10 million decline in revenues associated with airing the Super Bowl on two NBC-affiliated stations in 2015 as compared to 14 FOX-affiliated stations in 2014. Excluding this impact, core advertising revenues are expected to increase by 1.4% in the three months ended March 29, 2015 as compared to the three months ended March 30, 2014.

Digital and Data segment revenues are expected to be approximately $50 million for the three months ended March 29, 2015, an increase of $18 million, or 59%, as compared to the three months ended March 30, 2014. This increase is primarily attributable to the acquisition of Gracenote, which was consummated January 31, 2014, and the acquisitions of HWW, Baseline and What’s ON, which were consummated in the second half of 2014. For a discussion of these acquisitions, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Significant Events—Acquisitions.”

Real estate revenues within Corporate and Other are expected to be approximately $12 million for the three months ended March 29, 2015, a decrease of approximately $2 million as compared to the three months ended March 30, 2014.

Adjusted EBITDA

We expect consolidated Adjusted EBITDA for the three months ended March 29, 2015 to be approximately $129 million, a decrease of approximately $9 million, or 6.5%, compared to the three months ended March 30, 2014.

Television and Entertainment Adjusted EBITDA is expected to be approximately $135 million for the three months ended March 29, 2015, a decrease of $5 million, or 3%, as compared to the three months ended March 30, 2014. This decrease is primarily attributable to higher programming costs including original and syndicated content.

Digital and Data Adjusted EBITDA is expected to be approximately $12 million for the three months ended March 29, 2015, an increase of approximately $7 million as compared to the three months ended March 30, 2014. This increase is primarily attributable to the operating impact of the acquisitions of Gracenote, HWW, Baseline and What’s ON in 2014.

Corporate and Other Adjusted EBITDA is an expected loss of approximately $18 million for the three months ended March 29, 2015, compared to a loss of $7 million for the three months ended March 30, 2014. These additional losses were a result of increased expenses primarily attributable to higher corporate costs driven by increased compensation expense and costs associated with the implementation of improved business and technology applications.

5

Table of Contents

Cautionary Statement Regarding Preliminary Results for the First Quarter of 2015

The estimated first quarter of 2015 results are preliminary, unaudited and subject to completion, reflect management’s current views and may change as a result of management’s review of results and other factors, including a wide variety of significant business, economic and competitive risks and uncertainties. Such preliminary results are subject to the closing of the first quarter of 2015 and finalization of first quarter financial and accounting procedures (which have yet to be performed) and should not be viewed as a substitute for full quarterly financial statements prepared in accordance with accounting principles generally accepted in the U.S. (“GAAP”). We caution you that the first quarter 2015 estimates are not guarantees of future performance or outcomes and that actual results may differ materially from those described above. Factors that could cause actual results to differ from those described above are set forth in “Risk Factors” and “Disclosure Regarding Forward-Looking Statements.” We assume no obligation to update any forward-looking statement as a result of new information, future events or other factors. You should read this information together with the financial statements and the related notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for prior periods included elsewhere in this prospectus. Neither our independent registered public accounting firm nor any other independent registered public accounting firm has audited, reviewed or compiled, examined or performed any procedures with respect to the preliminary results, nor have they expressed any opinion or any other form of assurance on the preliminary results.

Adjusted EBITDA Description and Reconciliations

We present Adjusted EBITDA because, among other reasons, we believe it creates for investors a greater understanding of, and an enhanced level of transparency into, the means by which our management operates our company. Adjusted EBITDA is a supplemental measure of our performance that is not required by, or presented in accordance with, GAAP. Adjusted EBITDA has limitations as an analytical tool and should not be considered as an alternative to net income, operating profit, revenues or any other performance measures derived in accordance with GAAP as measures of our or our segments’ operating performance. See “—Summary Historical Consolidated Financial Data” for a discussion of some of these limitations and the definition of Adjusted EBITDA on a consolidated and a segment basis.

6

Table of Contents

Consolidated Adjusted EBITDA

The following table reconciles Adjusted EBITDA to net income for the periods presented.

| Three months ended | ||||||||

| Mar. 29, 2015 (preliminary) |

Mar. 30, 2014 (actual) |

|||||||

| (in millions of dollars, unaudited) | ||||||||

| Net Income |

$ | 36 | $ | 41 | ||||

| Income from discontinued operations, net of taxes |

— | 13 | ||||||

|

|

|

|

|

|||||

| Income from Continuing Operations |

36 | 28 | ||||||

|

|

|

|

|

|||||

| Income tax expense |

22 | 18 | ||||||

| Reorganization items, net |

1 | 2 | ||||||

| Gain on investment transactions, net |

(1 | ) | — | |||||

| Interest expense |

39 | 41 | ||||||

| Income on equity investments, net |

(37 | ) | (38 | ) | ||||

|

|

|

|

|

|||||

| Operating Profit |

61 | 50 | ||||||

| Depreciation |

17 | 17 | ||||||

| Amortization |

48 | 61 | ||||||

| Stock-based compensation |

8 | 8 | ||||||

| Severance and related charges(1) |

1 | 2 | ||||||

| Transaction-related costs(2) |

2 | 6 | ||||||

| Other |

— | 2 | ||||||

| Pension (credit) |

(7 | ) | (8 | ) | ||||

|

|

|

|

|

|||||

| Adjusted EBITDA |

$ | 129 | $ | 138 | ||||

|

|

|

|

|

|||||

| (1) | Severance and related charges represent charges related to reductions in staffing levels. |

| (2) | Transaction-related costs primarily include professional fees and integration costs incurred in connection with acquisitions made in the relevant period. |

| * | Totals may not sum due to rounding. |

Operating Segments Adjusted EBITDA

Television and Entertainment Adjusted EBITDA

The following table reconciles Television and Entertainment Adjusted EBITDA to Television and Entertainment operating profit for the periods presented.

| Three months ended | ||||||||

| Mar. 29, 2015 (preliminary) |

Mar. 30, 2014 (actual) |

|||||||

| (in millions of dollars, unaudited) | ||||||||

| Operating Profit |

$ | 79 | $ | 65 | ||||

| Depreciation |

11 | 12 | ||||||

| Amortization |

42 | 57 | ||||||

| Stock-based compensation |

2 | 3 | ||||||

| Severance and related charges(1) |

— | 1 | ||||||

| Other |

— | 2 | ||||||

|

|

|

|

|

|||||

| Adjusted EBITDA |

$ | 135 | $ | 140 | ||||

|

|

|

|

|

|||||

| (1) | Severance and related charges represent charges related to reductions in staffing levels. |

| * | Totals may not sum due to rounding. |

7

Table of Contents

Digital and Data Adjusted EBITDA

The following table reconciles Digital and Data Adjusted EBITDA to Digital and Data operating profit (loss) for the periods presented.

| Three months ended | ||||||||

| Mar. 29, 2015 (preliminary) |

Mar. 30, 2014 (actual) |

|||||||

| (in millions of dollars, unaudited) | ||||||||

| Operating Profit (Loss) |

$ | 4 | $ | (2 | ) | |||

| Depreciation |

2 | 2 | ||||||

| Amortization |

6 | 4 | ||||||

| Stock-based compensation |

1 | 1 | ||||||

| Severance and related charges(1) |

— | 1 | ||||||

|

|

|

|

|

|||||

| Adjusted EBITDA |

$ | 12 | $ | 5 | ||||

|

|

|

|

|

|||||

| (1) | Severance and related charges represent charges related to reductions in staffing levels. |

| * | Totals may not sum due to rounding. |

Corporate and Other Adjusted EBITDA

The following table reconciles Corporate and Other Adjusted EBITDA to Corporate and Other operating loss for the periods presented.

| Three months ended | ||||||||

| Mar. 29, 2015 (preliminary) |

Mar. 30, 2014 (actual) |

|||||||

| (in millions of dollars, unaudited) | ||||||||

| Operating Loss |

$ | (22 | ) | $ | (12 | ) | ||

| Depreciation |

4 | 3 | ||||||

| Stock-based compensation |

5 | 5 | ||||||

| Severance and related charges(1) |

1 | — | ||||||

| Transaction-related costs(2) |

2 | 5 | ||||||

| Pension (credit) |

(7 | ) | (8 | ) | ||||

|

|

|

|

|

|||||

| Adjusted EBITDA |

$ | (18 | ) | $ | (7 | ) | ||

|

|

|

|

|

|||||

| (1) | Severance and related charges represent charges related to reductions in staffing levels. |

| (2) | Transaction-related costs primarily include professional fees and integration costs incurred in connection with acquisitions made in the relevant period. |

| * | Totals may not sum due to rounding. |

Full Year 2015 Outlook

In 2015, we continue to expect solid revenue growth despite it being an off-cycle political year. We anticipate that Adjusted EBITDA in 2015 will be impacted by the cyclical loss of political advertising, continued measured programming investment in WGN America and increased operational costs in our Digital and Data segment. We continue to expect the following financial results as it relates to full year 2015:

| • | Consolidated Net Revenues: $2.00 billion to $2.03 billion; |

| • | Consolidated Adjusted EBITDA: $480 million to $495 million; |

8

Table of Contents

| • | Television and Entertainment Adjusted EBITDA: $500 million to $515 million; |

| • | Digital and Data Adjusted EBITDA: $46 million to $48 million; and |

| • | Corporate and Other Adjusted EBITDA: $(66) million to $(68) million. |

In our Television and Entertainment segment, programming expenses for WGN America and Tribune Studios in 2015 are currently expected to be approximately $14 million higher than the previous guidance of approximately $130 million primarily as a result of a change in the timing of the amortization of original programming expenses, which will result in a shift of expenses from 2016 into 2015. We expect that this increase in programming expense will be offset in 2015 by, among other things, an acceleration of cost savings actions.

These estimated results for full year 2015 are forward-looking statements based on management’s estimates as of the date hereof, and our actual results may be materially different from these estimated results. They are preliminary, unaudited and reflect management’s current views with respect to future results and may change as a result of industry or other developments through year-end 2015, management’s review of our actual results and other factors, including, among others, delays in the anticipated timing of activities related to our cost savings actions, unexpected costs associated with operating our business and the performance of our business. These expected financial results are based upon a number of assumptions and estimates that are in turn based on our analysis of the various factors which currently, and could in the future, impact our business. These assumptions and estimates are inherently uncertain and subject to significant business, operational, economic and competitive uncertainties and contingencies. Certain of the assumptions relate to business decisions that are subject to change, including, among others, our anticipated business strategies, our marketing strategies, our program development strategies and our ability to anticipate and react to business trends. Other assumptions relate to risks and uncertainties beyond our control, including, among others, the economic environment in which we operate, government regulation and other developments in our industry. Our actual results for the full year 2015 may differ materially from the estimates set out in this prospectus if any of these assumptions prove incorrect. We assume no obligation to update any forward-looking statement as a result of new information, future events or other factors. Accordingly, you should not place undue reliance on these estimated results and they should not be viewed as a substitute for our historical financial information presented elsewhere in this prospectus, including our audited consolidated financial statements and the related notes. Our independent registered public accounting firm has not audited, reviewed or performed any procedures with respect to these estimated results and does not express any opinion or any other form of assurance with respect thereto.

Reconciliations of the forecasted ranges for Adjusted EBITDA for fiscal 2015 are not included in this prospectus due to the number of variables in the projected ranges for full year 2015 Adjusted EBITDA and because we are currently unable to quantify accurately certain amounts that would be required to be included in the GAAP measures or the individual adjustments for such reconciliations. In addition, we believe such reconciliations would imply a degree of precision that would be confusing or misleading to investors.

9

Table of Contents

Corporate Information

We are incorporated in Delaware and our corporate offices are located at 435 North Michigan Avenue, Chicago, Illinois 60611. Our website address is www.tribunemedia.com, and our corporate telephone number is (312) 994-9300. None of the information contained on, or that may be accessed through, our websites or any other website identified herein is part of, or incorporated into, this registration statement. All website addresses in this registration statement are intended to be inactive textual references only.

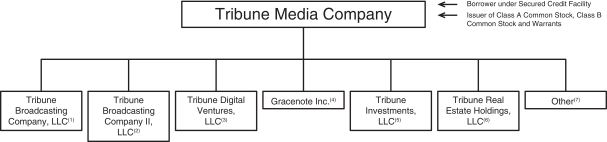

Tribune Media Company is a holding company that does business through its direct and indirect operating subsidiaries. The following chart illustrates our organizational structure as of the date hereof:

| (1) | This entity and its direct and indirect subsidiaries hold our broadcasting business, including WGN America (with the exception of the broadcasting business that we acquired through our acquisition of Local TV). |

| (2) | This entity and its direct and indirect subsidiaries hold our broadcasting business that we acquired through our acquisition of Local TV. |

| (3) | This entity and its direct and indirect subsidiaries hold our digital and data businesses (with the exception of our Gracenote businesses). |

| (4) | This entity and its direct and indirect subsidiaries hold our Gracenote businesses. |

| (5) | This entity and its direct and indirect subsidiaries hold certain of our equity method investments, including our investments in CareerBuilder. |

| (6) | This entity and its direct and indirect subsidiaries hold certain of our real estate assets. |

| (7) | Other direct and indirect subsidiaries that hold various broadcasting and other Company assets, including our cost method investments and international businesses. |

Market and Industry Data

Information in this prospectus about the media industry, including our general expectations concerning the industry and our position and share of the various media and entertainment markets in which we operate, are based on estimates prepared using data from various sources and on assumptions made by us. We believe data regarding the media industry and our position and share within the media markets in which we operate are inherently imprecise, but generally indicate our size and position and market share within the industry. Although we believe that the information provided by third parties is generally accurate, we have not independently verified any of that information. While we are not aware of any misstatements regarding any industry data presented in this prospectus, our estimates, in particular as they relate to our general expectations concerning the media industry, involve risks and uncertainties and are subject to change based on various factors, including those discussed under the caption “Risk Factors.”

10

Table of Contents

Trademarks and Service Marks

Tribune Broadcasting, WGN, WPIX, KTLA, Gracenote, Zap2it, and other trademarks or service marks of Tribune Media Company and its subsidiaries appearing in this prospectus are the property of Tribune Media Company or one of its subsidiaries. Solely for convenience, the trademarks, service marks, trade names and copyrights referred to in this prospectus are listed without the ™, ® and © symbols, but such references do not constitute a waiver of any rights that might be associated with the respective trademarks, service marks, trade names and copyrights included or referred to in this prospectus. Trade names, trademarks and service marks of other companies appearing in this prospectus are the property of their respective owners. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply relationships with, or endorsements of us by, these other companies.

11

Table of Contents

The Offering

| Common stock offered by the selling stockholders |

9,240,073 shares of Class A common stock |

| Option to purchase additional shares of common stock |

The underwriters have a 30-day option to purchase up to an additional 1,386,010 shares of Class A common stock from the selling stockholders at the public offering price, less underwriting discounts and commissions. |

| Common stock to be outstanding after this offering |

92,400,734 shares of Class A common stock and 2,391,960 shares of Class B common stock |

| Use of proceeds |

We will not receive any proceeds from the sale of our Class A common stock by the selling stockholders. The selling stockholders will receive all of the net proceeds and bear all commissions and discounts, if any, from the sale of our Class A common stock pursuant to this prospectus. See “Use of Proceeds” and “Principal and Selling Stockholders.” |

| Dividend policy |

We intend to begin payments of regular quarterly cash dividends of $0.25 per share commencing in the second fiscal quarter of 2015. Any payment of dividends will be at the discretion of our Board of Directors and will depend upon various factors then existing. See “Dividend Policy.” |

| NYSE trading symbol |

“TRCO” |

| Risk factors |

See “Risk Factors” and other information included in this prospectus for a discussion of factors that you should consider carefully before deciding to invest in shares of our common stock. |

| Conflicts of interest |

An affiliate of J.P. Morgan Securities LLC is one of the selling stockholders in this offering and will receive net proceeds exceeding 5% of the net proceeds of this offering. As a result it is deemed to have a “conflict of interest” with us within the meaning of Rule 5121 of the Financial Industry Regulatory Authority, or “Rule 5121.” Accordingly, this offering is being made in compliance with the requirements of Rule 5121. Because the common stock to be offered has a bona fide public market, pursuant to Rule 5121, the appointment of a qualified independent underwriter is not necessary. See “Underwriting (Conflicts of Interest).” |

The number of shares of our Class A common stock to be outstanding immediately following this offering is based on the number of shares of our Class A common stock outstanding as of March 27, 2015, and excludes:

| • | 1,371,143 shares of common stock issuable upon exercise of options to purchase shares outstanding as of March 27, 2015 at a weighted average exercise price of $67.20 per share; |

| • | 1,588,318 shares of common stock issuable upon exercise of warrants to purchase shares of our common stock (“Warrants”) outstanding as of March 27, 2015 at an exercise price of $0.001 per share; |

12

Table of Contents

| • | 1,173,957 shares of common stock issuable pursuant to restricted stock units, or “RSUs”, and performance share units, or “PSUs”, as of March 27, 2015; and |

| • | 2,400,048 shares of common stock reserved for future issuance following this offering under our equity plan. |

Shares of common stock issuable upon exercise of options or pursuant to RSUs and available for future issuance under our equity plans do not reflect any adjustment to such options or RSUs, as a result of the special cash dividend of $6.73 per share of common stock, which we paid on April 9, 2015. No adjustment was made to outstanding Warrants in connection with the special dividend, as holders of Warrants received a cash payment equal to the amount of the special cash dividend paid per share of common stock for each Warrant held.

13

Table of Contents

Summary Historical Consolidated Financial Data

The following table sets forth summary historical financial data as of the dates and for the periods indicated. The summary historical financial data as of December 28, 2014, December 29, 2013 and December 31, 2012 and for each of the three years in the period ended December 28, 2014 and for December 31, 2012 have been derived from our audited consolidated financial statements and related notes included elsewhere in this prospectus. The summary historical financial data as of December 30, 2012 have been derived from our consolidated financial statements and related notes not included in this prospectus. The summary historical financial data are qualified in their entirety by, and should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our audited consolidated financial statements and related notes included elsewhere in this prospectus. For a discussion of the distinction between Predecessor and Successor, see Note 3 to our audited consolidated financial statements included elsewhere in this prospectus.

On August 4, 2014, we completed a separation transaction (the “Publishing Spin-off”), resulting in the spin-off of the assets and certain liabilities of the businesses primarily related to our principal publishing operations, other than owned real estate and certain other assets (the “Publishing Business”), through a tax-free, pro rata dividend to our stockholders and warrantholders of 98.5% of the shares of common stock of Tribune Publishing Company (“Tribune Publishing”), and we retained 1.5% of the outstanding common stock of Tribune Publishing. The Publishing Business consisted of newspaper publishing and local news and information gathering functions that operated daily newspapers and related websites, as well as a number of ancillary businesses that leveraged certain of the assets of those businesses. The results of operations for the Publishing Business included in the Publishing Spin-off are presented within discontinued operations in our consolidated statements of operations for all periods presented.

| Successor | Predecessor | |||||||||||||||||

| As of and for the years ended | As of and for the year ended |

|||||||||||||||||

| Dec. 28, 2014 |

Dec. 29, 2013 |

As of and for Dec. 31, 2012(1) |

Dec. 30, 2012 |

|||||||||||||||

| (in thousands, except for per share data) | ||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||

| Operating Revenues |

||||||||||||||||||

| Television and Entertainment |

$ | 1,720,536 | $ | 1,014,424 | $ | — | $ | 1,141,701 | ||||||||||

| Digital and Data |

174,031 | 79,217 | — | 84,512 | ||||||||||||||

| Corporate and Other |

54,792 | 53,599 | — | 6,634 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

| Total operating revenues |

$ | 1,949,359 | $ | 1,147,240 | $ | — | $ | 1,232,847 | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating Profit (Loss) |

||||||||||||||||||

| Television and Entertainment |

$ | 336,921 | $ | 195,940 | $ | — | $ | 366,472 | ||||||||||

| Digital and Data |

3,409 | 16,497 | — | 24,365 | ||||||||||||||

| Corporate and Other |

(39,148 | ) | (13,397 | ) | — | (139,934 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

| Total operating profit |

$ | 301,182 | $ | 199,040 | $ | — | $ | 250,903 | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

| Income from Continuing Operations |

$ | 463,111 | $ | 162,942 | $ | 7,214,125 | $ | 283,635 | ||||||||||

| Earnings Per Share from Continuing Operations Attributable to Common Shareholders(2) |

||||||||||||||||||

| Basic |

$ | 4.63 | $ | 1.63 | ||||||||||||||

| Diluted |

$ | 4.62 | $ | 1.62 | ||||||||||||||

| Balance Sheet Data: |

||||||||||||||||||

| Total Assets |

$ | 11,396,455 | $ | 11,476,009 | $ | 8,673,280 | $ | 6,351,036 | ||||||||||

| Total Non-Current Liabilities |

$ | 5,516,844 | $ | 5,751,611 | $ | 3,308,899 | $ | 716,724 | ||||||||||

| Other Financial Data: |

||||||||||||||||||

| Adjusted EBITDA(3) |

$ | 607,783 | $ | 348,919 | ||||||||||||||

| Television and Entertainment Adjusted EBITDA(3) |

$ | 614,805 | $ | 336,069 | ||||||||||||||

| Digital and Data Adjusted EBITDA(3) |

$ | 38,582 | $ | 28,794 | ||||||||||||||

| Corporate and Other Adjusted EBITDA(3) |

$ | (45,604 | ) | $ | (15,944 | ) | ||||||||||||

14

Table of Contents

| (1) | Operating results for December 31, 2012 include only (i) reorganization adjustments which resulted in a net gain of $4.739 billion before taxes ($4.543 billion after taxes), including a $5 million gain ($9 million loss after taxes) recorded in income from discontinued operations, net of taxes and (ii) fresh-start reporting adjustments which resulted in a net loss of $3.372 billion before taxes ($2.567 billion after taxes, including a loss of $178 million ($95 million after taxes) reflected in income from discontinued operations, net of taxes). See Notes 1, 2 and 4 to our audited consolidated financial statements included elsewhere in this prospectus for further information. |

| (2) | See Note 17 to our audited consolidated financial statements included elsewhere in this prospectus for a description of our computation of basic and diluted earnings per share attributable to the holders of our Class A and Class B common stock. |

| (3) | Adjusted EBITDA is a financial measure that is not recognized under GAAP. Consolidated Adjusted EBITDA is defined as net income before income (loss) from discontinued operations, net of taxes, income taxes, interest income, interest expense, pension expense (credit), equity income and losses, depreciation and amortization, stock-based compensation, certain special items (including severance), non-operating items and reorganization items. Adjusted EBITDA for the Company’s operating segments is calculated as segment operating profit (loss) before depreciation, amortization, pension expense (credit), stock-based compensation and certain special items (including severance). We believe that Adjusted EBITDA is a measure commonly used by investors to evaluate our performance and that of our competitors. We further believe that the disclosure of Adjusted EBITDA is useful to investors, as this non-GAAP measure is used, among other measures, by our management to evaluate our performance. By disclosing Adjusted EBITDA, we believe that we create for investors a greater understanding of, and an enhanced level of transparency into, the means by which our management operates our company. Adjusted EBITDA is not a measure presented in accordance with GAAP, and our use of the term Adjusted EBITDA may vary from that of others in our industry. Adjusted EBITDA has limitations as an analytical tool and should not be considered as an alternative to net income, operating profit, revenues or any other performance measures derived in accordance with GAAP as measures of operating performance. |

| Some of these limitations include: |

| • | Adjusted EBITDA does not reflect interest income or expense; |

| • | Although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and Adjusted EBITDA does not reflect any cash requirements for such replacements; and |

| • | Other companies in our industries may calculate Adjusted EBITDA differently, limiting its usefulness as a comparative measure. |

15

Table of Contents

The following table reconciles Adjusted EBITDA to net income for the periods presented, the most directly comparable GAAP financial measure to Adjusted EBITDA:

| Years ended | ||||||||

| Dec. 28, 2014 | Dec. 29, 2013 | |||||||

| (in thousands) | ||||||||

| Net Income |

$ | 476,663 | $ | 241,555 | ||||

| Income from discontinued operations, net of taxes |

13,552 | 78,613 | ||||||

|

|

|

|

|

|||||

| Income from Continuing Operations |

463,111 | 162,942 | ||||||

| Income tax expense |

278,699 | 95,965 | ||||||

| Reorganization items, net |

7,268 | 16,931 | ||||||

| Other non-operating loss, net |

4,710 | 1,492 | ||||||

| Write-downs of investments |

94 | — | ||||||

| Gain on investment transactions, net |

(372,485 | ) | (150 | ) | ||||

| Loss on extinguishment of debt |

— | 28,380 | ||||||

| Interest expense |

157,866 | 39,134 | ||||||

| Interest and dividend income |

(1,368 | ) | (413 | ) | ||||

| Income on equity investments, net |

(236,713 | ) | (145,241 | ) | ||||

|

|

|

|

|

|||||

| Operating Profit |

301,182 | 199,040 | ||||||

| Depreciation |

70,187 | 41,187 | ||||||

| Amortization |

218,287 | 114,717 | ||||||

| Stock-based compensation |

26,191 | 5,417 | ||||||

| Severance and related charges(1) |

6,609 | 2,556 | ||||||

| Transaction-related costs(2) |

15,684 | 19,774 | ||||||

| Gain on sales of real estate |

(21,691 | ) | (135 | ) | ||||

| Contract termination cost(3) |

15,000 | — | ||||||

| Other |

6,977 | 1,143 | ||||||

| Pension (credit) expense |

(30,643 | ) | (34,780 | ) | ||||

|

|

|

|

|

|||||

| Adjusted EBITDA |

$ | 607,783 | $ | 348,919 | ||||

|

|

|

|

|

|||||

| (1) | Severance and related charges represent charges related to reductions in staffing levels. See Note 6 to our audited consolidated financial statements included elsewhere in this prospectus for further information. |

| (2) | Transaction-related costs primarily include professional fees and integration costs incurred in connection with acquisitions made in the relevant period. |

| (3) | Contract termination cost represents a charge for the early termination of an outside sales force contract in the second quarter of 2014 that will be fully satisfied and paid by our remaining third-party sales force firm. |

16

Table of Contents

The following table reconciles Television and Entertainment Adjusted EBITDA to Television and Entertainment operating profit for the periods presented, the most directly comparable GAAP financial measure to Television and Entertainment Adjusted EBITDA.

| Years ended | ||||||||

| Dec. 28, 2014 | Dec. 29, 2013 | |||||||

| (in thousands of dollars) | ||||||||

| Operating Profit |

$ | 336,921 | $ | 195,940 | ||||

| Depreciation |

50,262 | 29,947 | ||||||

| Amortization |

197,054 | 105,526 | ||||||

| Stock-based compensation |

8,800 | 1,844 | ||||||

| Severance and related charges(1) |

2,098 | 1,641 | ||||||

| Transaction-related costs(2) |

1,894 | 229 | ||||||

| Gains on sales of real estate |

(103 | ) | — | |||||

| Contract termination cost(3) |

15,000 | — | ||||||

| Other |

2,755 | 1,028 | ||||||

| Pension (credit) expense |

124 | (86 | ) | |||||

|

|

|

|

|

|||||

| Adjusted EBITDA |

$ | 614,805 | $ | 336,069 | ||||

|

|

|

|

|

|||||

| (1) | Severance and related charges represent charges related to reductions in staffing levels. See Note 6 to our audited consolidated financial statements included elsewhere in this prospectus for further information. |

| (2) | Transaction-related costs primarily include professional fees and integration costs incurred in connection with acquisitions made in the relevant period. |

| (3) | Contract termination cost represents a charge for the early termination of an outside sales force contract in the second quarter of 2014 that will be fully satisfied and paid by our remaining third-party sales force firm. |

The following table reconciles Digital and Data Adjusted EBITDA to Digital and Data operating profit for the periods presented, the most directly comparable GAAP financial measure to Digital and Data Adjusted EBITDA.

| Years ended | ||||||||

| Dec. 28, 2014 | Dec. 29, 2013 | |||||||

| (in thousands of dollars) | ||||||||

| Operating Profit |

$ | 3,409 | $ | 16,497 | ||||

| Depreciation |

7,744 | 2,576 | ||||||

| Amortization |

21,233 | 9,191 | ||||||

| Stock-based compensation |

1,641 | 17 | ||||||

| Severance and related charges(1) |

3,975 | 279 | ||||||

| Other |

580 | 234 | ||||||

|

|

|

|

|

|||||

| Adjusted EBITDA |

$ | 38,582 | $ | 28,794 | ||||

|

|

|

|

|

|||||

| (1) | Severance and related charges represent charges related to reductions in staffing levels. See Note 6 to our audited consolidated financial statements included elsewhere in this prospectus for further information. |

17

Table of Contents

The following table reconciles Corporate and Other Adjusted EBITDA to Corporate and Other operating loss for the periods presented, the most directly comparable GAAP financial measure to Corporate and Other Adjusted EBITDA.

| Years ended | ||||||||

| Dec. 28, 2014 | Dec. 29, 2013 | |||||||

| (in thousands of dollars) | ||||||||

| Operating Loss |

$ | (39,148 | ) | $ | (13,397 | ) | ||

| Depreciation |

12,181 | 8,664 | ||||||

| Stock-based compensation |

15,750 | 3,556 | ||||||

| Severance and related charges(1) |

536 | 636 | ||||||

| Transaction-related costs(2) |

13,790 | 19,545 | ||||||

| Gains on sales of real estate |

(21,588 | ) | (135 | ) | ||||

| Other |

3,642 | (119 | ) | |||||

| Pension (credit) |

(30,767 | ) | (34,694 | ) | ||||

|

|

|

|

|

|||||

| Adjusted EBITDA |

$ | (45,604 | ) | $ | (15,944 | ) | ||

|

|

|

|

|

|||||

| (1) | Severance and related charges represent charges related to reductions in staffing levels. See Note 6 to our audited consolidated financial statements included elsewhere in this prospectus for further information. |

| (2) | Transaction-related costs primarily include professional fees and integration costs incurred in connection with acquisitions made in the relevant period. |

18

Table of Contents

You should carefully consider each of the following risks, together with all of the other information in this prospectus before making an investment decision. The risks described below are not the only risks that we face. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also affect our business operations. Any of these risks may have a material adverse effect on our business, financial condition, results of operations and cash flows. In such case, the trading price of our common stock may decline, and you may lose all or part of your investment.

Risks Related to Our Business

We expect advertising demand to continue to be impacted by economic conditions and fragmentation of the media landscape.

Advertising revenue is our primary source of revenue, representing approximately 78% of our broadcasting revenue in 2014. Expenditures by advertisers tend to be cyclical, reflecting overall economic conditions, as well as budgeting and buying patterns. National and local economic conditions, particularly in major metropolitan markets, affect the levels of advertising revenue. Changes in gross domestic product, consumer spending, auto sales, housing sales, unemployment rates, job creation, programming content and audience share and rates, as well as federal, state and local election cycles, all impact demand for advertising.

A decline in the economic prospects of advertisers or the economy in general could alter current or prospective advertisers’ spending priorities. Our revenue is sensitive to discretionary spending available to advertisers in the markets we serve, as well as their perceptions of economic trends and uncertainty. Weak economic indicators in various regions across the nation, such as high unemployment rates, weakness in housing and continued uncertainty caused by national and state governments’ inability to resolve fiscal issues in a cost efficient manner to taxpayers may adversely impact advertiser sentiment. These conditions could impair our ability to maintain and grow our advertiser base. In addition, advertising from the automotive, financial, retail and restaurant industries each constitute a large percentage of our advertising revenue. The success of these industries will continue to affect the amount of their advertising spending, which could have an adverse effect on our revenues and results of operations. Furthermore, consolidation across various industries, such as financial institutions and telecommunication companies, impacts demand for advertising. Competition from other media, including other broadcasters, cable systems and networks, satellite television and radio, metropolitan, suburban and national newspapers, websites, magazines, direct marketing and solo and shared mail programs, affects our ability to retain advertising clients and raise rates.

Seasonal variations in consumer spending cause our quarterly advertising revenue to fluctuate. Second and fourth quarter advertising revenue is typically higher than first and third quarter advertising revenue, reflecting the slower economic activity in the winter and summer and the stronger fourth quarter holiday season. In addition, due to demand for political advertising spots, we typically experience fluctuations in our revenues between even and odd-numbered years. During elections for various state and national offices, which are primarily in even-numbered years, advertising revenues tend to increase because of political advertising in our markets. Advertising revenues in odd-numbered years tend to be less than in even-numbered years due to the significantly lower level of political advertising in our markets. Even in even-numbered years, levels of political advertising are affected by campaign finance laws and the ability of political candidates and PACs to raise and spend funds, and our advertising revenues could vary substantially based on these factors.

The proliferation of cable and satellite channels, advances in mobile and wireless technology, the migration of television audiences to the Internet and the viewing public’s increased control over the manner and timing of their media consumption through personal video recording devices, have resulted in greater fragmentation of the television viewing audience and a more difficult advertising sales environment. Demand for our products is also a factor in determining advertising rates. For example, ratings points for our television stations and cable channels are among the factors that are weighed when determining advertising rates.

19

Table of Contents

All of these factors continue to contribute to a difficult advertising sales environment and may further adversely impact our ability to grow or maintain our revenues.

Our business operates in highly competitive markets and our ability to maintain market share and generate operating revenues depends on how effectively we compete with existing and new competition.

Our business operates in highly competitive markets. Our television stations compete for audiences and advertising revenue with other broadcast stations as well as with other media such as the Internet, cable and satellite television, and radio. Some of our current and potential competitors have greater financial and other resources than we do. In addition, cable companies and others have developed national advertising networks in recent years that increase the competition for national advertising. Over the past decade, cable television programming services, other emerging video distribution platforms and the Internet have captured increasing market share, while aggregate viewership of the major broadcast television networks has declined.

Viewer accessibility is also becoming a factor as is the inability to measure new audiences which could impact advertising rates. Advertising rates are set based upon a variety of factors, including a program’s popularity among the advertiser’s target audience, the number of advertisers competing for the available time, the size and demographic make-up of the market served and the availability of alternative advertising avenues in the market. Our ability to maintain market share and competitive advertising rates depends in part on audience acceptance of our network, syndicated and local programming. Changes in market demographics, the entry of competitive stations into our markets, the transition to new methods and technologies for distributing programming and measuring audiences such as Local People Meters, the introduction of competitive local news or other programming by cable, satellite, Internet, telephone or wireless providers, or the adoption of competitive offerings by existing and new providers could result in lower ratings and adversely affect our business, financial condition and results of operations.

Our television stations generate significant percentages of their advertising revenue from a few categories, including automotive, financial institutions, retail, restaurants and political. As a result, even in the absence of a recession or economic downturn, technological, industry, or other changes specifically affecting these advertising sources could reduce advertising revenues and adversely affect our financial condition and results of operations.

Technological changes in product delivery and storage could adversely affect our business.

Our business is subject to rapid technological change, evolving industry standards, and the emergence of new technologies. Advances in technologies or alternative methods of product delivery or storage, or certain changes in consumer behavior driven by these or other technologies and methods of delivery and storage, could have a negative effect on our business.

For example, devices that allow users to view television programs on a time-delayed basis, technologies that enable users to fast-forward or skip advertisements, such as DVRs, and portable digital devices and technology that enable users to store or make portable copies of programming, may cause changes in consumer behavior that could affect the attractiveness of our offerings to advertisers and adversely affect our revenues. In addition, the availability of pay-per-view and further increases in the use of digital devices, including mobile devices, which allow users to view or listen to content of their own choosing, in their own time and remote locations, while avoiding traditional commercial advertisements or subscription payments, could adversely affect our advertising revenues.

Furthermore, in recent years, the national broadcast networks have streamed their programming on the Internet and other distribution platforms in close proximity to network programming broadcast on local television stations, including those that we own. These and other practices by the networks dilute the exclusivity and value of network programming originally broadcast by our local television stations and could adversely affect the business, financial condition and results of operations of our stations.

20

Table of Contents

We may not be able to adequately protect our intellectual property and other proprietary rights that are material to our business, or to defend successfully against intellectual property infringement claims by third parties.

Our business relies on a combination of patented and patent-pending technology, trademarks, trade names, copyrights, and other proprietary rights, as well as contractual arrangements, including licenses, to establish and protect our technology, intellectual property and brand names. We believe our proprietary technology, trademarks and other intellectual property rights are important to our continued success and our competitive position. Any impairment of any such intellectual property or brands could adversely impact the results of our operations or financial condition.

We seek to limit the threat of content piracy; however, policing unauthorized use of our broadcasts, products and services and related intellectual property is often difficult and the steps taken by us may not in every case prevent the infringement by unauthorized third parties. Developments in technology increase the threat of content piracy by making it easier to duplicate and widely distribute pirated material. Our use of contractual provisions, confidentiality procedures and agreements, and trademark, copyright, unfair competition, trade secret and other laws to protect our intellectual property rights and proprietary technology may not be adequate. Litigation may be necessary to enforce our intellectual property rights and protect our proprietary technology, or to defend against claims by third parties that the conduct of our businesses or our use of intellectual property infringes upon such third party’s intellectual property rights. Protection of our intellectual property rights is dependent on the scope and duration of our rights as defined by applicable laws in the U.S. and abroad and the manner in which those laws are construed. If those laws are drafted or interpreted in ways that limit the extent or duration of our rights, or if existing laws are changed, our ability to generate revenue from intellectual property may decrease, or the cost of obtaining and maintaining rights may increase. There can be no assurance that our efforts to enforce our rights and protect our products, services and intellectual property will be successful in preventing content piracy.

Furthermore, any intellectual property litigation or claims brought against us, whether or not meritorious, could result in substantial costs and diversion of our resources, and there can be no assurances that favorable final outcomes will be obtained in all cases. The terms of any settlement or judgment may require us to pay substantial amounts to the other party or cease exercising our rights in such intellectual property. In addition, we may have to seek a license to continue practices found to be in violation of a third party’s rights, which may not be available on reasonable terms, or at all. Our business, financial condition or results of operations may be adversely affected as a result.

The availability and cost of quality network, syndicated and sports programming may impact television ratings.

Most of our stations’ programming is acquired from outside sources, including the networks with which our stations are affiliated. The cost of network and syndicated programming represents a significant portion of television operating expenses. Network programming is dependent on our ability to maintain our existing network affiliations and the continued existence of such networks. Syndicated programming costs are impacted largely by market factors, including demand from other stations within the market, cable channels and other distribution vehicles. Availability of syndicated programming depends on the production of compelling programming and the willingness of studios to offer the programming to unaffiliated buyers. The cost and availability of local sports programming is impacted by competition from regional sports cable networks and other local broadcast stations. Our inability to continue to acquire or produce affordable programming for our stations could adversely affect operating results or our financial condition.

The loss or modification of our network affiliation agreements could have a material and adverse effect on our results of operations.

The non-renewal or termination of our network affiliation agreements would prevent us from being able to carry programming of the relevant network and this loss of programming would require us to obtain replacement programming, which may involve higher costs and which may not be as attractive to our target audiences,

21

Table of Contents

resulting in reduced revenues. Currently, we have 14 stations affiliated with FOX, 13 stations affiliated with CW, 6 stations affiliated with CBS, 3 stations affiliated with ABC and 2 stations affiliated with NBC. We periodically renegotiate our major network affiliation agreements. We cannot predict the outcome of any future negotiations relating to our affiliation agreements or what impact, if any, they may have on our financial condition and results of operations. The non-renewal or termination of any of our network affiliation agreements would prevent us from being able to carry programming of the relevant network. This loss of programming would require us to obtain replacement programming, which may involve higher costs and which may not be as attractive to our target audiences, resulting in reduced revenues. Upon the termination of any of our network affiliation agreements, we would be required to establish a new network affiliation agreement for the affected station with another network or operate as an independent station.

Original programming is generally more expensive than other forms of programming and viewership by the public is difficult to predict, which could lead to fluctuations in revenues and profitability.

The production and distribution of original television series content, such as the content produced or co-produced by Tribune Studios, generally requires a larger up-front investment than other forms of programming and the revenues derived from the airing and distribution of an original television series or other similar content depend primarily upon its acceptance by the public, which is difficult to predict. The commercial success of original content generally depends upon the quality and acceptance of other competing content released into the marketplace at or near the same time, the availability of a growing number of alternative forms of entertainment and leisure time activities, general economic conditions and their effects on consumer spending and other tangible and intangible factors, all of which can change and cannot be predicted with certainty. Audience ratings for a television series are generally a key factor in generating future revenues from other distribution channels, such as domestic and international syndication and video on demand. Further, if our original television programming is unsuccessful, it could impact our ability to renegotiate favorable retransmission consent and carriage fee agreements with cable, satellite and other MVPDs.

We must purchase television programming based on expectations about future revenues. Actual revenues may be lower than our expectations.