Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 31, 2014

or

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________________ to __________________

Commission file number: 000-52917

IHOOKUP SOCIAL, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

|

98-0546715

|

|

|

State or other jurisdiction of

|

(I.R.S. Employer

|

|

|

incorporation or organization

|

Identification No.)

|

125 E Campbell Ave, Campbell CA 95008

(Address of principal executive offices and Zip Code)

|

Registrant’s telephone number, including area code

|

(855) 473-7473

|

Securities registered pursuant to Section 12(b) of the Act

|

Title of each class

|

Name of each exchange on which registered

|

|

|

Common Stock

par value $.0001

|

OTC Pink Sheet

|

Securities registered pursuant to Section 12(g) of the Act

Common Stock, par value $0.0001 per share

(Title of Class)

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Exchange Act from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No o

1

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

o

|

Accelerated filer

|

o

|

|

|

Non-accelerated filer

|

o

|

(Do not check if a smaller reporting company)

|

Smaller reporting company

|

x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes o No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

As of June 30, 2014, the last business day of the registrant’s most recently completed second fiscal quarter the aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant was approximately $1,945,727, based on the closing price (last sale of the day) for the registrant’s common stock on the OTC Bulletin Board on June 30, 2014 of $3.20 ($0.032 pre reverse split) per share.

APPLICABLE ONLY TO CORPORATE REGISTRANTS

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. As of March 31, 2015, there were 25,824,923 shares of the registrant’s common stock issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Not Applicable

2

TABLE OF CONTENTS

PART I

|

ITEM 1.

|

BUSINESS

|

4

|

|

|

ITEM 1A.

|

RISK FACTORS

|

10

|

|

|

ITEM 1B.

|

UNRESOLVED STAFF COMMENTS

|

24

|

|

|

ITEM 2.

|

PROPERTIES

|

24

|

|

|

ITEM 3.

|

LEGAL PROCEEDINGS

|

24

|

|

|

ITEM 4.

|

MINE SAFETY DISCLOSURES

|

24

|

|

|

PART II

|

|||

|

ITEM 5.

|

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

|

24

|

|

|

ITEM 6

|

SELECTED FINANCIAL DATA

|

25

|

|

|

ITEM 7.

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

26

|

|

|

ITEM 7A

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

39

|

|

|

ITEM 8.

|

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

|

40

|

|

|

ITEM 9.

|

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

|

41

|

|

|

ITEM 9A.

|

CONTROLS AND PROCEDURES

|

41

|

|

|

ITEM 9B.

|

OTHER INFORMATION

|

42

|

|

|

PART III

|

|||

|

ITEM 10.

|

DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

|

42

|

|

|

ITEM 11.

|

EXECUTIVE COMPENSATION

|

45

|

|

|

ITEM 12.

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS

|

47

|

|

|

ITEM 13.

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE

|

49

|

|

|

ITEM 14.

|

PRINCIPAL ACCOUNTING FEES AND SERVICES

|

50

|

|

|

PART IV

|

|||

|

ITEM 15.

|

EXHIBITS, FINANCIAL STATEMENT SCHEDULES

|

51

|

|

|

SIGNATURES

|

54

|

||

3

PART I

As used in this report, the terms “we”, “us”, “our”, “our company,” “iHookup” and “the Company” mean iHookup Social Inc. unless the context clearly indicates otherwise.

Cautionary Statement Regarding Forward-looking Information

This annual report on Form 10-K contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. The use of words such as “anticipates,” “estimates,” “expects,” “intends,” “plans” and “believes,” among others, generally identify forward-looking statements. These forward-looking statements include, among others, statements relating to: the Company’s future financial performance, the Company’s business prospects and strategy, anticipated trends and prospects in the industries in which the Company’s businesses operate and other similar matters. These forward-looking statements are based on the Company’s management's expectations and assumptions about future events as of the date of this annual report, which are inherently subject to uncertainties, risks and changes in circumstances that are difficult to predict.

Actual results could differ materially from those contained in these forward-looking statements for a variety of reasons, including, among others, the risk factors set forth below. Other unknown or unpredictable factors that could also adversely affect the Company’s business, financial condition and results of operations may arise from time to time. In light of these risks and uncertainties, the forward-looking statements discussed in this annual report may not prove to be accurate. Accordingly, you should not place undue reliance on these forward-looking statements, which only reflect the views of the Company’s management as of the date of this annual report. The Company does not undertake to update these forward-looking statements

In this annual report on Form 10-K, unless otherwise specified, all dollar amounts are expressed in United States dollars and all references to “common shares” refer to the common shares in our capital stock.

An investment in our common stock involves a number of very significant risks. You should carefully consider the following risks and uncertainties in addition to other information in this annual report on Form 10-K in evaluating our company and our business before purchasing shares of our common stock. Our business, operating results and financial condition could be seriously harmed as a result of the occurrence of any of the following risks. You could lose all or part of your investment due to any of these risks. You should invest in our common stock only if you can afford to lose your entire investment.

ITEM 1. BUSINESS

Who We Are

As of December 31, 2013, Titan Iron Ore. Corp. was a mineral exploration company. Due to our inability to raise capital to further develop mining claims and pursue mineral exploration, we decided to exit the mining business and look for other opportunities. On February 3, 2014, we completed a merger with iHookup Social, Inc., a Delaware corporation (“iHookup”) pursuant to an Agreement and Plan of Merger and Reorganization (the “Merger Agreement”) dated January 31, 2014. Pursuant to the Merger Agreement, we incorporated a new subsidiary called iHookup Operations Corp, a Delaware corporation, which merged with and into iHookup, causing the subsidiary’s separate existence to cease and iHookup to become a wholly-owned subsidiary of the Company. iHookup’s stockholders exchanged all of six thousand (6,000) shares of outstanding common stock for twenty five thousand (25,000) shares of the Company’s newly designated Series A Preferred Stock. Each share of common stock entitles its holder to one vote on each matter submitted to the stockholders. The holders of preferred stock are entitled to cast votes equal to nine (9) times the total number of shares of common stock which are issued and outstanding, voting together with the holders of common stock as a single class. Such Series A Preferred Stock shall also be convertible into the number of shares of common stock which equals nine (9) times the total number of shares of common stock which are issued and outstanding at the time of conversion until the closing of a Qualified Financing (i.e. the sale and issuance of our equity securities that results in gross proceeds in excess of $2,500,000). As a result of the transaction, the former iHookup stockholders received a controlling interest in the Company.

iHookup’s business is development and dissemination of a "proximity based" mobile social media application that facilitates connections between people, utilizing the intelligence of GPS and localized recommendations. We are focusing on this aspect of the business, which is described more fully below.

Corporate Overview

We were incorporated in the State of Nevada on June 5, 2007. Effective June 15, 2011, we completed a merger with our subsidiary, Titan Iron Ore Corp., a Nevada corporation, which was incorporated solely to effect a change in our name to “Titan Iron Ore Corp.”

4

ITEM 1. BUSINESS - continued

Also effective June 15, 2011, we effected a 37 to one forward stock split of our issued and outstanding common and preferred stock. As a result, our authorized capital increased from 100,000,000 shares of common stock with a par value of $0.0001 to 3,700,000,000 shares of common stock with a par value of $0.0001 of which 5,151,000 shares of common stock outstanding increased to 190,587,000 shares of common stock. Subsequently, on June 20, 2011, we issued 2,100,000 common shares pursuant to a private placement unit offering, increasing the number of shares of common stock outstanding to 192,687,000.

Effective June 30, 2011 and in connection with the entry into an agreement (the “Acquisition Agreement”) with J2 Mining Ventures Ltd. (“J2 Mining”) dated June 13, 2011 and attached as Exhibit 10.1 to our Current Report on Form 8-K filed June 16, 2011, we completed the acquisition of a 100% right, title and interest in and to a properties option agreement (the “Option Agreement”) from J2 Mining with respect to iron ore mineral properties located in Albany County, Wyoming, by way of entering an assignment of mineral property option agreement with J2 Mining and Wyomex LLC (the “Assignment Agreement”), whereby our company was assigned 100% of the right, title and interest in and to the Option Agreement from J2 Mining.

In connection with the closing of the Acquisition Agreement, Ohad David, Ruth Navon and Service Merchant Corp. (the “Vendors”), entered into an affiliate stock purchase agreement, whereby, among other things, the Vendors surrendered 142,950,000 common shares for cancellation.

As described above, on February 3, 2014 we completed a merger with iHookup pursuant to the Merger Agreement dated January 31, 2014. Pursuant to the Merger Agreement, we incorporated a new subsidiary called iHookup Operations Corp, a Delaware corporation, which merged with and into iHookup, causing the subsidiary’s separate existence to cease and iHookup to become a wholly-owned subsidiary of the Company. iHookup’s stockholders exchanged all of six thousand (6,000) shares of outstanding common stock for twenty five thousand (25,000) shares of the Company’s newly designated Series A Preferred Stock. Each share of common stock entitles its holder to one vote on each matter submitted to the stockholders. The holders of the Series A Preferred Stock are entitled to cast votes equal to nine (9) times the total number of shares of common stock which are issued and outstanding, voting together with the holders of common stock as a single class. Such Series A Preferred Stock shall also be convertible into the number of shares of common stock which equals nine (9) times the total number of shares of common stock which are issued and outstanding at the time of conversion until the closing of a Qualified Financing (i.e. the sale and issuance of our equity securities that results in gross proceeds in excess of $2,500,000). As a result of the transaction, the former iHookup stockholders received a controlling interest in the Company.

On April 29, 2014, FINRA approved a 20 for 1 reverse stock split whereby 937,459,274 shares of the Company’s common stock then issued and outstanding, were exchanged for 46,872,964 shares of the Company’s common stock.

On March 19, 2015, FINRA approved a 100 for 1 reverse stock split whereby 2,355,489,991, shares of the Company’s common stock then issued and outstanding, were exchanged for 23,554,923 shares of the Company’s common stock.

Mobile Application

Introduction

iHookup Social is seeking to redefine the way people connect with a potential friend or partner. The laws of meeting, socializing and dating have shifted as meeting online or through the use of mobile technology has become a dominant part of today’s mobile-social lifestyle, across various social circles, age groups, races, genders and demographics. iHookup Social’s goal is to facilitate such virtual connections and move them toward real-life interactions, like a matchmaker and concierge in one. As such, the company has begun providing users with locally relevant content, such as popular venues and special merchant discounts, within the user’s vicinity. As this feature continues to be built up, the company believes it will help drive meet ups or “Hookups” to physical locations or events. Ultimately, the company plans to bring together a dynamic opportunity for brands, advertisers and merchants to interact with a network of socially active mobile users on a locally relevant basis, while building customer loyalty, engagement and revenues.

5

ITEM 1. BUSINESS - continued

Products/Services: iHookup application

iHookup is a proximity-based or location-based social platform and discovery application that facilitates communication between two or more users (“iHookup” or “application”). It utilizes the intelligence of GPS and localized recommendations to provide opportunities for making new connections, socializing, dating and expanding existing social circles for individuals, groups and organizations. It is available on the iOS platform and in iTunes stores world-wide, where we offer a free version and a paid version. The free version allows users to browse through the application’s features and user profiles. The paid version which costs $0.99 to download, provides a trial of all subscription based services (which allows users to send message and take advantage of any localized recommendations or offers) for a specified period of time, as determined by the company’s marketing strategy. The application also offers a “virtual currency” component, allowing users to purchase “in application” coin packs that activate virtual gifts and various service-based options (see subscription offers and pricing below – prices are subject to change and often do during this user acquisition phase the company is currently in):

|

Recurring Subscriptions

|

$7.99

|

|

1-Month

|

$17.99

|

|

3-Month

|

$27.99

|

|

6-Month

|

$44.99

|

|

Annual

|

$59.99

|

|

Coin Pack1

|

$2.99

|

|

Coin Pack2

|

$4.99

|

|

Coin Pack 3

|

$9.99

|

In addition, the company has begun providing localized recommendations and merchant discounts to its users and allowing users to share such recommendations and offers with each other. This feature is also linked with each user’s mobile mapping service, allowing for easy routing to the venue or event. As this feature continues to be built up, the company hopes it will help drive encounters or “Hookups” to physical locations or events, become an additional method of retaining its user base and increase the company’s revenue streams in several vertically attractive markets in brands and advertising.

Marketing

We market our application utilizing a variety of online and offline marketing activities. Our offline marketing activities has consisted of traditional marketing and event-based branding in various local markets, such as distributing coasters and flyers at test locations.

Our online marketing activities generally consist of the purchase of mobile-banners and other display advertising and search engine marketing. We run various mobile ad campaigns targeting male, female and Apple / iOS users on Facebook and other regional, US and international sites. In addition, the company produces video ads that may be run on mobile “video” ad networks or be placed based on a variety of alliances with third parties who advertise and promote our services, from time to time. Such video advertising may be expanded and utilized in commercials, on Facebook, YouTube, and various other editorial and public relations efforts.

iHookup is available on in the Apple App Store / iTunes, where our visibility in rank on the free, paid and social networking categories also drives traffic to both versions of the application. The highest ranking achieved by our application in March 2014 on the Apple App Store is as follows:

|

|

·

|

Top Rank Overall Free Apps USA - #532 (June 22, 2014)

|

|

|

·

|

Top Grossing Overall Free Apps USA - #510 (June 17 2014)

|

|

|

·

|

Top Rank Overall Paid Apps USA - #292 (June 22, 2014)

|

|

|

·

|

Top Grossing Overall Paid Apps USA - #651 (June 17 2014)

|

|

|

·

|

Top Grossing Social Networking FREE iPhone / iPod App USA: #28 (July 19, 2014)

|

|

|

·

|

Top Grossing Social Networking PAID iPhone / iPod App USA: #39

|

|

|

·

|

Top Grossing Social Networking FREE iPad App USA: #83

|

|

|

·

|

Top Rank in Social Networking FREE App USA: #49 (June 22, 2014)

|

|

|

·

|

Top Rank Social Networking Paid USA: #6

|

|

|

·

|

Top Rank Social Networking Paid Canada: #13

|

The company plans to announce specific name changes and feature additions to its current application, believed by management to enable the brand to expand its services beyond what currently exists in the marketplace today.

6

ITEM 1. BUSINESS - continued

Revenue

Our revenue is derived primarily from subscription fees for our paid versions and from users purchasing “coins” for added features. Additional revenue opportunities include merchants, brands and advertisers that we are beginning to vertically integrate into our location based offers and discounts.

Competition

The mobile-social business is highly competitive and barriers to entry are minimal. We compete primarily with other social networking, messaging and dating mobile applications (e.g. Tinder), but also category specific websites (e.g. Facebook, Match.com and eHarmony), social apps, dating and matchmaking services, other social media platforms and applications, and other conventional media companies that provide personal services and traditional venues where singles meet (both online and offline). The company hopes to use the dating category as an entry point to a much broader “Social Networking” marketplace, where competitors will include websites and applications offering coupons by merchants and brands (e.g. Living Social, Groupon, What About We).

We believe that our ability to compete successfully will depend primarily upon the following factors:

|

|

•

|

establishing a “Friendly” brand that will be socially shared, acceptable and viral in nature;

|

|

|

•

|

the size and diversity of our registered member and subscriber bases relative to those of our competitors;

|

|

|

•

|

the functionality of our application and the attractiveness of their features and our services and offerings generally to consumers relative to those of our competitors;

|

|

|

•

|

how quickly we can enhance our existing technology and services and/or develop new features and localized opportunities and venue based monetization opportunities in response to:

|

|

•

|

new, emerging and rapidly changing technologies;

|

|

•

|

the introduction of product and service offerings by our competitors;

|

|

•

|

changes in consumer requirements and trends in the single community relative to our competitors; and

|

|

•

|

our ability to engage in cost-effective marketing efforts, including by way of maintaining relationships with third parties with which we have entered into alliances, and the recognition and strength of our various brands relative to those of our competitors.

|

Employees and Key Consultants

Our company has four full time employees and one part time employee.

Intellectual Property

We intend, in due course, subject to legal advice, to apply for trademark, copyright and/or patent protection in the United States and other jurisdictions. We regard our intellectual property, including our software and trademark, as valuable assets and intend to vigorously defend them against infringement.

While there can be no assurance that registered trademarks and copyrights will protect our proprietary information, we intend to file for protection and assert our intellectual property rights against any infringer. Although any assertion of our rights can result in a substantial cost to, and diversion of effort by, our Company, management believes that the protection of our intellectual property rights is an important part of our operating strategy.

Market Opportunity

As a whole, mobile applications create a socially connected experience while allowing users to stay active or on the move, and push forward with personal and professional goals. Mobile dating is one of the fastest growing market segments in mobile communications, continuing to attract new users. A common problem faced across all age and demographic profiles, is the lack of time in each day. Easy, accessible and user driven technologies are replacing traditional avenues of meeting people by providing yet another way to embrace our “Do it all” and “Have it all” mobile - social generation.

Current Market Size

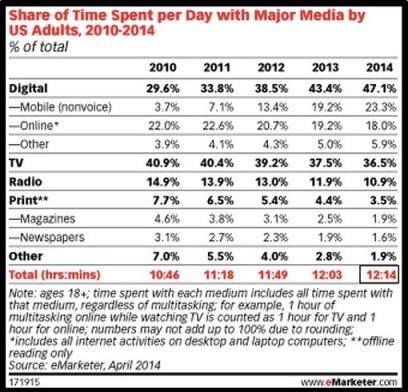

First, the shift from desktop to mobile, whether smartphone or tablet, is happening across a variety of activities, including social networking and online/mobile dating. As the chart below shows, the time spent on mobile usage has steadily overtaken other online activities on desktops or laptops from 2010 to 2014.

7

ITEM 1. BUSINESS - continued

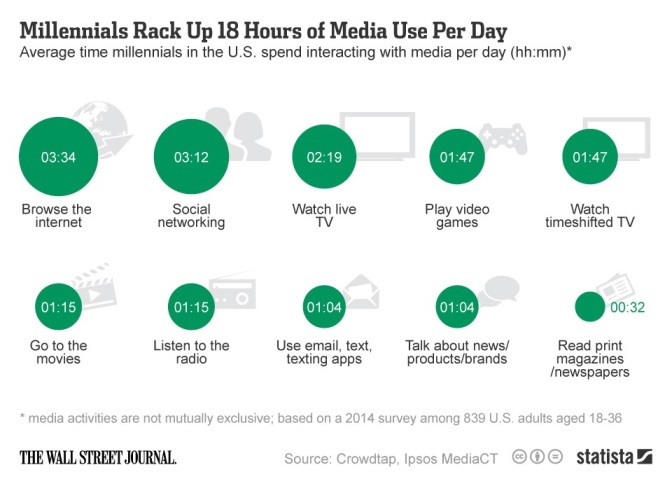

According to the chart below, on average, young US adults aged 18-36, spend over three hours a day on social networking, second only to time spent browsing the internet

8

ITEM 1. BUSINESS - continued

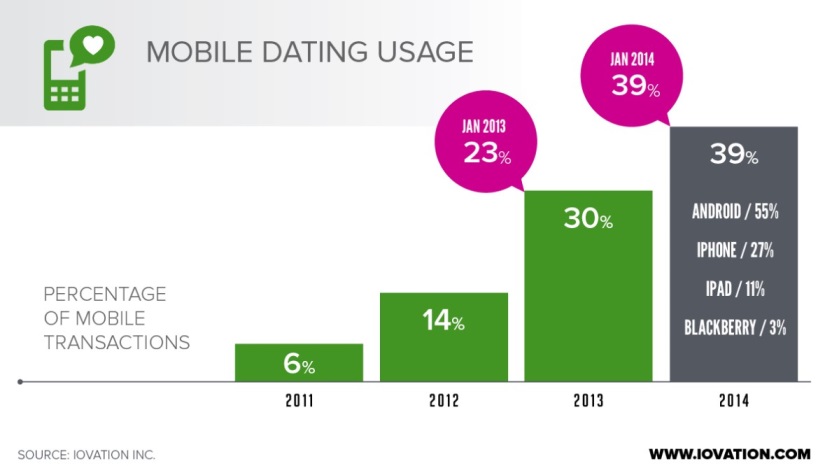

In addition, the study below shows the steady increase of the usage of mobile dating from 6% in 2011 to 39% in 2014. The use of mobile dating applications (which is in the general category of “Social”) has dramatically increased in recent years.

We believe that dating and socializing is inherently local, being better served by mobile applications that provide accessibility wherever users go. Today’s mobile society prefers to not be in front of a computer to view potential connections, or to receive or send messages. Instead, the user’s phone is always by his or her side.

iOS devices are versatile multi-purpose machines that have already significantly impacted the business models of music, games and other Media & Entertainment industry categories. And now, within the nexus of mobile-social-local, mobile connection applications with “hyper-local” features, provide opportunities in a high growth sector.

Growth

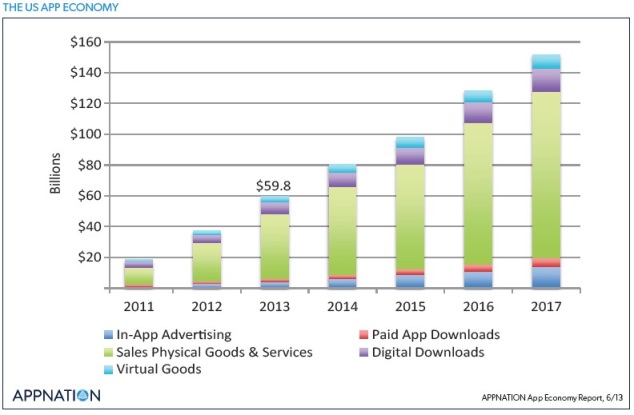

According to the chart below, applications generated a total of $59.8 billion in revenues through in-app advertising, sales of physical goods and services, virtual goods, paid application downloads and digital downloads. As of 2017, this market is projected to grow to over $140 billion.

9

ITEM 1. BUSINESS - continued

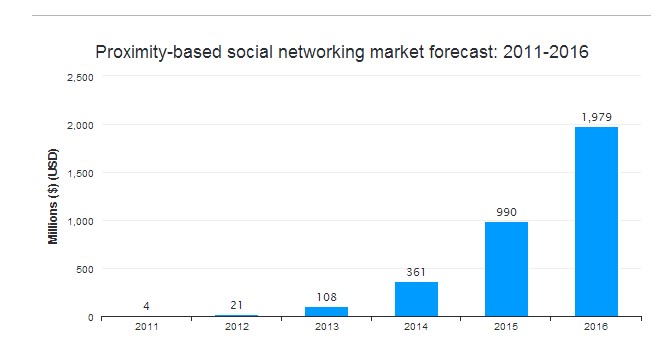

From the chart below, the proximity-based social networking market as of 2014 is valued at $361 million and is projected to grow to $1.979 billion by 2016.

ITEM 1A. RISK FACTORS

RISK FACTORS

The risks and uncertainties below may not be the only ones the Company faces. If any of these risks actually occur, or others not specified below, the business, financial condition, operating results and prospects of the Company could be materially and adversely affected. In that case, the trading price of our common stock could decline.

10

ITEM 1A. RISK FACTORS - continued

General Risks

We may fail to raise sufficient capital.

To the extent that we fail to obtain sufficient operating capital, we may be unable to deal with presently unforeseen contingencies in the future or be able to fund our operations. In addition, we may have more difficulty or find it impossible, to raise third party financing from investors or financial institutions.

Our reserves may be insufficient.

We intend to establish a reserve fund, as determined in the Board’s discretion, for normal working capital contingencies. However, we have been unable to do so. If the reserves are not available to the Company, it may be necessary to attempt to raise additional capital or financing. In the event that such capital or financing is not available on favorable terms, we may be forced to raise additional capital on unfavorable terms. In fact, we have been forced to issue several convertible notes at substantial discounts and interest rates in order to raise the requisite capital for operations.

Risks Related to Our Business and Industry

Our success depends upon the continued growth and acceptance of online/mobile advertising, particularly paid listings, as an effective alternative to traditional, offline advertising and the continued commercial use of the internet.

Many advertisers still have limited experience with mobile advertising and may continue to devote significant portions of their advertising budgets to traditional offline advertising media. Accordingly, we continue to compete with traditional advertising media, including television, radio and print, in addition to a multitude of websites with high levels of traffic and mobile advertising networks, for a share of available advertising expenditures and expect to face continued competition as more emerging media and traditional offline media companies enter the online and mobile advertising markets. We believe that the continued growth and continued acceptance of mobile advertising generally will depend, to a large extent, on its perceived effectiveness and the acceptance of related advertising models (particularly in the case of models that incorporate user targeting and/or utilize mobile devices), the continued growth in commercial use of the internet (particularly abroad) and smart devices, the extent to which web/mobile browsers, software programs and/or mobile applications that limit or prevent advertising from being displayed become commonplace and the extent to which the industry is able to effectively manage click fraud. Any lack of growth in the market for mobile advertising, particularly for paid listings, or any decrease in the effectiveness and value of mobile advertising (whether due to the passage of laws requiring additional disclosure and/or opt-in policies for advertising that incorporates user targeting or other developments) would have an adverse effect on our business, financial condition and results of operations.

We depend, in part, upon arrangements with third parties to drive traffic to our various websites and distribute our products and services.

We engage in a variety of activities, such as search engine optimization and application search optimization, designed to attract traffic to our application and convert visitors into repeat users and customers. How successful we are in these efforts depends, in part, upon our continued ability to enter into arrangements with third parties to drive traffic to our application, as well as the continued introduction of new and enhanced features, products and services that resonate with users and customers generally.

In addition, we have entered into a number of arrangements with third parties to promote and deliver mobile advertising to various social networks or mobile channels. Pursuant to these arrangements, third parties generally promote our application on various mobile applications, their websites or through e-mail campaigns and we either pay on a cost per impression basis (i.e. cost per view) or a fixed fee when visitors to these websites click through to or download our application. These arrangements are generally not exclusive, are short-term in nature and are generally terminable by either party given notice. If existing arrangements with third parties are terminated (or are not renewed upon their expiration) and we fail to replace this traffic and related revenues, or if we are unable to enter into new arrangements with existing and/or new third parties in response to industry trends, our business, financial condition and results of operations could be adversely affected.

Even if we succeed in driving traffic to our application, we may not be able to convert this traffic or otherwise retain users unless we continue to provide quality products and services. We may not be able to adapt quickly and/or in cost-effective manner to frequent changes in user and customer preferences, which can be difficult to predict, or appropriately time the introduction of enhancements and/or new products or services to the market. Our inability to provide quality products and services would adversely affect user and customer experiences, which would result in decreases in users, customers and revenues, which would adversely affect our business, financial condition and results of operations.

11

ITEM 1A. RISK FACTORS - continued

As discussed below, our traffic building and conversion initiatives also involve the expenditure of considerable sums for marketing, as well as for the development and introduction of new products, services and enhancements, infrastructure and other related efforts.

Marketing efforts designed to drive traffic to our various websites may not be successful or cost-effective.

Traffic building and conversion initiatives involve considerable expenditures for online, mobile and offline advertising and marketing. We plan to make significant expenditures for online and mobile display advertising, event-based marketing and traditional offline advertising in connection with these initiatives, which may not be successful or cost-effective. In the case of paid advertising generally, the policies of sellers and publishers of advertising may limit our ability to purchase certain types of advertising or advertise some of our products and services, which could affect our ability to compete effectively and, in turn, adversely affect our business, financial condition and results of operations.

In addition, search engines have increasingly expanded their offerings into other, non-search related categories, and have in certain instances displayed their own integrated or related product and service offerings in a more prominent manner than those of third parties within their search engine results. Continued expansion and competition from search engines could result in a substantial decrease in traffic to our various websites, as well as increased costs if we were to replace free traffic with paid traffic, which would adversely affect our business, financial condition and results of operations.

Lastly, as discussed above, we also have and will enter into various arrangements with third parties in an effort to increase traffic, which arrangements are generally more cost-effective than traditional marketing efforts. If we are unable to renew existing (and enter into new) arrangements of this nature, sales and marketing costs as a percentage of revenue would increase over the long-term.

Any failure to attract and acquire new, and retain existing, traffic, users and customers in a cost-effective manner could adversely affect our business, financial condition and results of operations.

We rely in part on application marketplaces and Internet search engines to drive traffic to our products and services, and if we fail to appear high up in the search results or rankings, traffic to our platform could decline and our business and operating results could be adversely affected.

We rely on application marketplaces, such as Apple’s App Store, to drive downloads of our mobile applications. In the future, Apple or other operators of application marketplaces may make changes to their marketplaces which may make access to our products and services more difficult. Our rankings in Apple’s App Store may also drop based on the following factors:

|

|

•

|

the size and diversity of our registered member and subscriber bases relative to those of our competitors;

|

|

|

•

|

the functionality of our application and the attractiveness of their features and our services and offerings generally to consumers relative to those of our competitors;

|

|

|

•

|

how quickly we can enhance our existing technology and services and/or develop new features and localized opportunities and venue based monetization opportunities in response to:

|

|

•

|

new, emerging and rapidly changing technologies;

|

|

•

|

the introduction of product and service offerings by our competitors;

|

|

•

|

changes in consumer requirements and trends in the single community relative to our competitors; and

|

|

•

|

our ability to engage in cost-effective marketing efforts, including by way of maintaining relationships with third parties with which we have entered into alliances, and the recognition and strength of our various brands relative to those of our competitors.

|

Our estimated income taxes could be materially different from income taxes that we ultimately pay.

We are subject to income taxes in the United States. Significant judgment and estimation is required in determining our provision for income taxes and related matters. In the ordinary course of our business, there are many transactions and calculations where the ultimate tax determinations are uncertain or otherwise subject to interpretation. Our determination of our income tax liability is always subject to review by applicable tax authorities and we are currently subject to audits in a number of jurisdictions. Although we believe our income tax estimates and related determinations are reasonable and appropriate, relevant taxing authorities may disagree. The ultimate outcome of any such audits and reviews could be materially different from estimates and determinations reflected in our historical income tax provisions and accruals. Any adverse outcome of any such audit or review could have an adverse effect on our financial condition and results of operations.

12

ITEM 1A. RISK FACTORS - continued

A variety of new laws, or new interpretations of existing laws, could subject us to claims or otherwise harm our business.

We are subject to a variety of laws in the U.S. and abroad that are costly to comply with, can result in negative publicity and diversion of management time and effort and can subject us to claims or other remedies. Some of these laws, such as income, sales, use, value-added and other tax laws and consumer protection laws, are applicable to businesses generally and others are unique to the various types of businesses in which we are engaged. Many of these laws were adopted prior to the advent of the internet and related technologies and, as a result, do not contemplate or address the unique issues of the internet and related technologies. Laws that do reference the internet are being interpreted by the courts, but their applicability and scope remain uncertain.

For example, through our various businesses we post and link to third party content, including third party advertisements, links and websites, as well as content submitted by users, such as comments, photographs and videos. We could be subject to liability for posting or linking to third party content, and while we generally require third parties to indemnify us for related claims, we may not be able to enforce our indemnification rights. Some laws, including the Communications Decency Act, or CDA, and the Digital Millennium Copyright Act, or DMCA, limit our liability for posting or linking to third party content. For example, the DMCA generally protects online service providers from claims of copyright infringement based on use of third party content, so long as certain statutory requirements are satisfied. However, the scope and applicability of the DMCA are subject to judicial interpretation and, as such, remain uncertain, and the U.S. Congress may enact legislation limiting the protections afforded by the DMCA to online service providers. Moreover, similar protections may not exist in other jurisdictions in which our products are used. As a result, claims could be threatened and filed under both U.S. and foreign laws based upon use of third party content asserting, among other things, defamation, invasion of privacy or right or publicity, copyright infringement or trademark infringement.

Any failure on our part to comply with applicable laws may subject us to additional liabilities, which could adversely affect our business, financial condition and results of operations. In addition, if the laws to which we are currently subject are amended or interpreted adversely to our interests, or if new adverse laws are adopted, our products and services might need to be modified to comply with such laws, which would increase our costs and could result in decreased demand for our products and services to the extent that we pass on such costs to our customers. Specifically, in the case of tax laws, positions that we have taken or will take are subject to interpretation by the relevant taxing authorities. While we believe that the positions we have taken to date comply with applicable law, there can be no assurances that the relevant taxing authorities will not take a contrary position, and if so, that such positions will not adversely affect us. Any events of this nature could adversely affect our business, financial condition and results of operations.

We may fail to adequately protect our intellectual property rights or may be accused of infringing the intellectual property rights of third parties.

We regard our intellectual property rights, including trademarks, domain names, trade secrets, copyrights and other similar intellectual property, as critical to our success. For example, we currently rely heavily on the trademark “iHookup” to market our product and seek to build and maintain brand loyalty and recognition. We intend, in due course, subject to legal advice, to apply for trademark, copyright and/or patent protection in the United States and other jurisdictions. We regard our intellectual property, including our software and trademark, as valuable assets and intend to vigorously defend them against infringement. Effective trademark protection may not be available or may not be sought in every country in which products and services are made available and contractual disputes may affect the use of marks governed by private contract. We have reserved and registered certain domain names, however not every variation of a domain name may be available or be registered, even if available.

While there can be no assurance that registered trademarks and copyrights will protect our proprietary information, we intend to assert our intellectual property rights against any infringer. Although any assertion of our rights can result in a substantial cost to, and diversion of effort by, our Company, management believes that the protection of our intellectual property rights is a key component of our operating strategy.

Our application also relies upon trade secrets and certain copyrightable and patentable proprietary technologies relating to its software and related features, products and services.

We will rely on a combination of laws and contractual restrictions with employees, customers, suppliers, affiliates and others to establish and protect our various intellectual property rights. For example, we plan to apply to register and renew, or secure by contract where appropriate, trademarks and service marks as they are developed and used, and continue to reserve, register and renew domain names as we deem appropriate.

We also plan to apply for copyrights and patents or for other similar statutory protections as we deem appropriate, based on then current facts and circumstances. No assurances can be given that any copyright or patent application we file will result in a copyright or patent being issued, or that any future copyright or patent will afford adequate protection against competitors and similar technologies. In addition, no assurances can be given that third parties will not create new products or methods that achieve similar results without infringing upon copyrights or patents we may own in the future.

13

ITEM 1A. RISK FACTORS - continued

Despite these measures, our intellectual property rights may still not be protected in a meaningful manner, challenges to contractual rights could arise or third parties could copy or otherwise obtain and use our intellectual property without authorization. The occurrence of any of these events could result in the erosion of our brands and limitations on our ability to control marketing on or through the internet using our various domain names, as well as impede our ability to effectively compete against competitors with similar technologies, any of which could adversely affect our business, financial conditions and results of operations.

From time to time, we may be subject to legal proceedings and claims in the ordinary course of business, including claims of alleged infringement of trademarks, copyrights, patents and other intellectual property rights held by third parties. In addition, litigation may be necessary in the future to enforce our intellectual property rights, protect our trade secrets or to determine the validity and scope of proprietary rights claimed by others. Any litigation of this nature, regardless of outcome or merit, could result in substantial costs and diversion of management and technical resources, any of which could adversely affect our business, financial condition and results of operations. Patent litigation tends to be particularly protracted and expensive.

If we fail to grow our user base, or if user engagement or ad engagement on the platform declines, the revenue, business and operating results may be harmed.

The size of the user base and the users’ level of engagement are critical to our success. The financial performance has been and will continue to be significantly determined by success in growing the number of users and increasing their overall level of engagement on the platform as well as the number of ad engagements. We generate a substantial majority of our revenue based upon the number of downloads, migration to subscription accounts and engagement by the users with the ads that we display. If people do not perceive the services to be useful, reliable and trustworthy, we may not be able to attract users or increase the frequency of their engagement with the platform and the ads that we display. There is no guarantee that we will be successful in attracting more users or not suffer erosion of the user base or engagement levels. A number of factors could potentially negatively affect user growth and engagement, including if:

|

|

·

|

users engage with other products, services or activities as an alternative;

|

|

|

·

|

influential users, such as celebrities, athletes, journalists and brands or certain age demographics conclude that an alternative product or service is more relevant;

|

|

|

·

|

we are unable to convince potential new users of the value and usefulness of its products and services;

|

|

|

·

|

there is a decrease in the perceived quality of the content generated by our platform;

|

|

|

·

|

we fail to introduce new and improved products or services or if we introduce new or improved products or services that are not favorably received or that negatively affect user engagement;

|

|

|

·

|

technical or other problems prevent us from delivering our products or services in a rapid and reliable manner or otherwise affect the user experience;

|

|

|

·

|

we are unable to present users with content that is interesting, useful and relevant to them;

|

|

|

·

|

users believe that their experience is diminished as a result of the decisions we make with respect to the frequency, relevance and prominence of ads that we display;

|

|

|

·

|

there are user concerns related to privacy and communication, safety, security or other factors;

|

|

|

·

|

we become subject to hostile or inappropriate usage on our platform;

|

|

|

·

|

there are adverse changes in our products or services that are mandated by, or that we elect to make to address, legislation, regulatory authorities or litigation, including settlements or consent decrees;

|

|

|

·

|

we fail to provide adequate customer service to users; or

|

|

|

·

|

we do not maintain our brand image or its reputation is damaged.

|

14

ITEM 1A. RISK FACTORS - continued

If users do not continue to download and use our application and their engagement is not valuable to other users, we may experience a decline in the number of users accessing the products and services and user engagement, which could result in the loss of advertisers and revenue.

Our success depends on our ability to provide users with valuable content, which in turn depends on the profile descriptions and use of the app by others. We believe that one of our competitive advantages is the quality, quantity and real-time nature of the content on iHookup, and that access to unique or real-time content is one of the main reasons users visit us. We seek to foster a broad and engaged user community, and we encourage celebrities, athletes, and others to use our products and services to meet people and form relationships. If users do not continue to contribute profiles and we are unable to provide users with valuable and timely content or other people to engage with, our user base and user engagement may decline. Additionally, if we are not able to address user concerns regarding the safety and security of our products and services or if we are unable to successfully prevent abusive or other hostile behavior on the platform, the size of the user base and user engagement may decline.

If we are unable to compete effectively for users and advertiser spend, the business and operating results could be harmed.

Competition for users of its products and services is intense. Although we have developed a new platform for public self-expression and meeting people in real time, we face strong competition in this business. We compete against many companies to attract and engage users, including companies which have greater financial resources and substantially larger user bases, such as eHarmony, Match.com and others which offer a variety of Internet and mobile device-based products, services and content. As a result, competitors may acquire and engage users at the expense of the growth or engagement of our user base, which would negatively affect the business.

We believe that our ability to compete effectively for users depends upon many factors both within and beyond our control, including:

|

|

·

|

the popularity, usefulness, ease of use, performance and reliability of our products and services compared to those of our competitors;

|

|

|

·

|

the amount, quality and timeliness of content generated by our users;

|

|

|

·

|

the timing and market acceptance of our products and services;

|

|

|

·

|

the adoption of our products and services internationally;

|

|

|

·

|

its ability, and the ability of our competitors, to develop new products and services and enhancements to existing products and services;

|

|

|

·

|

the frequency and relative prominence of the ads displayed by us or our competitors;

|

|

|

·

|

our ability to establish and maintain relationships with platform partners that integrate with our platform;

|

|

|

·

|

changes mandated by, or that we elect to make to address, legislation, regulatory authorities or litigation, including settlements and consent decrees, some of which may have a disproportionate effect on us;

|

|

|

·

|

government action regulating competition;

|

|

|

·

|

our ability to attract, retain and motivate talented employees, particularly engineers, designers and product managers;

|

|

|

·

|

acquisitions or consolidation within our industry, which may result in more formidable competitors; and

|

|

|

·

|

our reputation and the brand strength relative to our competitors.

|

We also face significant competition for advertiser spend. We compete against online and mobile businesses, including those referenced above, and traditional media outlets, such as television, radio and print, for advertising budgets. In order to grow our revenue and improve our operating results, we must increase our share of spending on advertising relative to our competitors, many of which are larger companies that offer more traditional and widely accepted advertising products. In addition, some of our larger competitors have substantially broader product or service offerings and leverage their relationships based on other products or services to gain additional share of advertising budgets.

We believe that our ability to compete effectively for advertiser spend depends upon many factors both within and beyond our control, including:

|

|

·

|

the size and composition of our user base relative to those of our competitors;

|

|

|

·

|

our ad targeting capabilities, and those of our competitors;

|

|

|

·

|

the timing and market acceptance of our advertising services, and those of our competitors;

|

15

ITEM 1A. RISK FACTORS - continued

|

|

·

|

our marketing and selling efforts, and those of our competitors;

|

|

|

·

|

the pricing for our products relative to the advertising products and services of our competitors;

|

|

|

·

|

the return our advertisers receive from their advertising services, compared to those of our competitors; and

|

|

|

·

|

our reputation and the strength of our brand relative to our competitors.

|

If we are not able to compete effectively for users and advertiser spend our business and operating results would be materially and adversely affected.

User growth and engagement depend upon effective interoperation with operating systems, networks, and devices, that we do not control.

Currently, our application is available only on Apple’s iOS. We are dependent on the interoperability of our products and services with popular devices, and mobile operating systems that we do not control. Any changes in such systems or devices that degrade the functionality of our products and services or give preferential treatment to competitive products or services could adversely affect usage of our products and services. Further, if the number of platforms for which we develop our product expands, it will result in an increase in our operating expenses. In order to deliver high quality products and services, it is important that our products and services work with a range of operating systems and devices that we do not control. In addition, because our users access our products and services through mobile devices, we are particularly dependent on the interoperability of our products and services with mobile devices and operating systems. We may not be successful in developing or maintaining relationships with key participants in the mobile industry or in developing products or services that operate effectively with these operating systems and devices. In the event that it is difficult for our users to access and use our products and services on their mobile devices, our user growth and engagement could be harmed, and our business and operating results could be adversely affected.

We have a limited operating history in a new and unproven market for our platform, which makes it difficult to evaluate our future prospects and may increase the risk that we will not be successful.

We have developed a mobile app for public self-expression and meeting people in real time, and the market for our products and services is relatively new and may not develop as expected, if at all. People who are not our users may not understand the value of our products and services and new users may initially find our products confusing. Convincing potential new users of the value of our products and services is critical to increasing our user base and to the success of our business.

We have a limited operating history, and only began to generate revenue in 2014 which makes it difficult to effectively assess our future prospects or forecast future results. We encounter or may encounter many risks in this developing and rapidly evolving market. These risks and challenges include its ability to, among other things:

|

|

·

|

increase its number of users and user engagement;

|

|

|

·

|

successfully expand our business;

|

|

|

·

|

develop a reliable, scalable, secure, high-performance technology infrastructure that can efficiently handle increased usage;

|

|

|

·

|

convince advertisers of the benefits of our products compared to alternative forms of advertising;

|

|

|

·

|

develop and deploy new features, products and services;

|

|

|

·

|

successfully compete with other companies, some of which have substantially greater resources and market power than us, that are currently in, or may in the future enter, its industry, or duplicate the features of our products and services;

|

|

|

·

|

attract, retain and motivate talented employees, particularly engineers, designers and product managers;

|

|

|

·

|

process, store, protect and use personal data in compliance with governmental regulations, contractual obligations and other obligations related to privacy and security;

|

|

|

·

|

continue to earn and preserve its users’ trust, including with respect to their private personal information; and

|

|

|

·

|

defend ourselves against litigation, regulatory, intellectual property, privacy or other claims.

|

16

ITEM 1A. RISK FACTORS - continued

If we fail to educate potential users and potential advertisers about the value of our products and services, if the market for our platform does not develop as we expect or if we fail to address the needs of this market, our business will be harmed. We may not be able to successfully address these risks and challenges or other unforeseen risks and challenges. Failure to adequately address these risks and challenges could harm our business and cause our operating results to suffer.

Our business depends on the continued and unimpeded access to our products and services on mobile devices by our users and advertisers. If we or our users experience disruptions in service or if mobile service providers are able to block, degrade or charge for access to our products and services, we could incur additional expenses and the loss of users and advertisers.

We depend on the ability of our users and advertisers to access mobile devices. Currently, this access is provided by companies that have significant market power in the broadband and telecommunications access marketplace, including incumbent telephone companies, cable companies, mobile communications companies, government-owned service providers, device manufacturers and operating system providers, any of whom could take actions that degrade, disrupt or increase the cost of user access to our products or services, which would, in turn, negatively impact our business. We also rely on other companies to maintain reliable communications network systems that provide adequate speed, data capacity and security to us and our users. As the number of mobile device users continues to grow, frequency of use and amount of data transmitted, the communications infrastructure that we and our users rely on may be unable to support the demands placed upon it. The failure of the mobile communications infrastructure that we and/or our users rely on, even for a short period of time, could undermine our operations and harm our operating results.

Abusive activities by certain users could diminish the user experience on our platform, which could damage our reputation and deter our current and potential users from using our products and services.

There are a range of abusive activities that are prohibited by the our terms of service and are generally defined as unsolicited, repeated actions that negatively impact other users with the general goal of drawing user attention to a given person, account, site, product or idea. This includes posting large numbers of unsolicited mentions of a user, duplicate outlets, misleading links (e.g., to malware or click-jacking pages) or other false or misleading content, and aggressively following and un-following accounts, adding users to lists, sending invitations to inappropriately attract attention. Our terms of service also prohibit the creation of serial or bulk accounts, both manually or using automation, for disruptive or abusive purposes. Although we continue to invest resources to reduce spam and other abusive behavior, we expect spammers and abusers will continue to seek ways to act inappropriately on our platform. We will continuously combat spam and other abusive behaviors, including by suspending or terminating accounts we believe to be spammers and launching algorithmic changes focused on curbing abusive activities. Combatting spam and other abusive behaviors require the diversion of significant time and focus of our engineering team from improving our products and services. If spam or abusive behavior increase, this could hurt our reputation for delivering relevant content or reduce user growth and user engagement and result in continuing operational cost to us.

If we fail to effectively manage our growth, our business and operating results could be harmed.

If we experience rapid growth in our headcount and operations, it will place significant demands on our management, operational and financial infrastructure. We intend to continue to make substantial investments to expand our operations, research and development, sales and marketing and general and administrative organizations. We face significant competition for employees, particularly engineers, designers and product managers, from other Internet and high-growth companies, which include both publicly-traded and privately-held companies, and we may not be able to hire new employees quickly enough to meet our needs. To attract highly skilled personnel, we will need to continue to offer, highly competitive compensation packages. As we continue to grow, we are subject to the risks of over-hiring, over-compensating our employees and over-expanding our operating infrastructure, and to the challenges of integrating, developing and motivating a rapidly growing employee base. If we fail to effectively manage our hiring needs and successfully integrate new hires, our efficiency and ability to meet our forecasts and our employee morale, productivity and retention could suffer, and our business and operating results could be adversely affected.

Our business and operating results may be harmed by a disruption in our service, or by our failure to timely and effectively scale and adapt our existing technology and infrastructure.

One of the reasons people use our platform is for real-time information and personal contact. We may, in the future, experience service disruptions, outages and other performance problems due to a variety of factors, including infrastructure changes, human or software errors, hardware failure, capacity constraints due to an overwhelming number of people accessing our products and services simultaneously, computer viruses and denial of service or fraud or security attacks. Although we are investing significantly to improve the capacity, capability and reliability of our infrastructure, we are not currently serving traffic equally through the data centers that support our platform. Accordingly, in the event of a significant issue at the data center supporting most of our network traffic, some of our products and services may become inaccessible to the public or the public may experience difficulties accessing our products and services. Any disruption or failure in our infrastructure could hinder our ability to handle existing or increased traffic on our platform, which could significantly harm our business.

17

ITEM 1A. RISK FACTORS - continued

As the number of our users increases and our users generate more content, including photos and videos hosted by us, we may be required to expand and adapt our technology and infrastructure to continue to reliably store, serve and analyze this content. It may become increasingly difficult to maintain and improve the performance of our products and services, especially during peak usage times, as our products and services become more complex and our user traffic increases. This would negatively impact our ability to attract users and advertisers and increase engagement of our users. We expect to continue to make significant investments to maintain and improve the capacity, capability and reliability of our infrastructure. To the extent that we do not effectively address capacity constraints, upgrade our systems as needed and continually develop our technology and infrastructure to accommodate actual and anticipated changes in technology, our business and operating results may be harmed.

If we are unable to maintain and promote our brand, our business and operating results may be harmed.

We believe that maintaining and promoting our brand is critical to expanding our base of users and advertisers. Maintaining and promoting our brand will depend largely on our ability to continue to provide useful, reliable and innovative products and services, which we may not do successfully. We may introduce new features, products, services or terms of service that users, platform partners or advertisers do not like, which may negatively affect our brand. Additionally, the actions of platform partners may affect our brand if users do not have a positive experience using third-party applications. Our brand may also be negatively affected by the actions of users that are hostile or inappropriate to other people, by users impersonating other people, by users identified as spam, by users introducing excessive amounts of spam on its platform or by third parties obtaining control over users’ accounts. Maintaining and enhancing our brand may require iHookup to make substantial investments and these investments may not achieve the desired goals. If we fail to successfully promote and maintain our brand or if we incur excessive expenses in this effort, our business and operating results could be adversely affected.

Negative publicity could adversely affect our business and operating results.

Negative publicity about us, including about our product quality and reliability, changes to our products and services, privacy and security practices, litigation, regulatory activity, the actions of our users or user experience with our products and services, even if inaccurate, could adversely affect our reputation and the confidence in and the use of our products and services. For example, service outages could result in widespread media reports. Such negative publicity could also have an adverse effect on the size, engagement and loyalty of our user base and result in decreased revenue, which could adversely affect our business and operating results.

We focus on product innovation and user engagement rather than short-term operating results.

We encourage employees to quickly develop and help us launch new and innovative features. We focus on improving the user experience for our products and services and on developing new and improved products and services for the advertisers on our platform. We prioritize innovation and the experience for users and advertisers on our platform over short-term operating results. We may make product and service decisions that may reduce our short-term operating results if we believe that the decisions are consistent with its goals to improve the user experience and performance for advertisers, which we believe will improve our operating results over the long term. These decisions may not be consistent with the short-term expectations and may not produce the long-term benefits that we expect, in which case our user growth and user engagement, our relationships with advertisers and our business and operating results could be harmed. In addition, our focus on the user experience may negatively impact our relationships with existing or prospective advertisers. This could result in a loss of advertisers, which could harm our revenue and operating results.

Our products and services may contain undetected software errors, which could harm our business and operating results.

Our products and services incorporate complex software and we encourage our employees to quickly develop and help us launch new and innovative features. Our software may now or in the future contain, errors, bugs or vulnerabilities. Some errors in the software code may only be discovered after the product or service has been released. Any errors, bugs or vulnerabilities discovered in our code after release could result in damage to our reputation, loss of users, loss of platform partners, loss of advertisers or advertising revenue or liability for damages, any of which could adversely affect our business and operating results.

Our business is subject to complex and evolving U.S. laws and regulations. These laws and regulations are subject to change and uncertain interpretation, and could result in claims, changes to its business practices, monetary penalties, increased cost of operations or declines in user growth, user engagement or ad engagement, or otherwise harm our business.

We are subject to a variety of laws and regulations in the United States that involve matters central to our business, including privacy, rights of publicity, data protection, content regulation, intellectual property, competition, protection of minors, consumer protection and taxation. Many of these laws and regulations are still evolving and being tested in courts and could be interpreted or applied in ways that could harm our business, particularly in the new and rapidly evolving industry in which we operate. The introduction of new products or services may subject us to additional laws and regulations. There have been a number of recent legislative proposals in the United States, at both the federal and state level, that would impose new obligations in areas such as privacy. The U.S. government, including the Federal Trade Commission, or the FTC, and the Department of Commerce, has announced that it is reviewing the need for greater regulation for the collection of information concerning user behavior on the Internet and over mobile devices, including regulation aimed at restricting certain tracking and targeted advertising practices.

18

ITEM 1A. RISK FACTORS - continued

Additionally, recent amendments to U.S. patent laws may affect the ability of companies to protect their innovations and defend against claims of patent infringement. Having personal information may subject us to additional regulation. Further, it is difficult to predict how existing laws and regulations will be applied to its business and the new laws and regulations to which we may become subject, and it is possible that they may be interpreted and applied in a manner that is inconsistent with our practices. These existing and proposed laws and regulations can be costly to comply with and can delay or impede the development of new products and services, result in negative publicity, significantly increase our operating costs, require significant time and attention of management and technical personnel and subject us to inquiries or investigations, claims or other remedies, including fines or demands that we modify or cease existing business practices.

Even though our platform is for public self-expression conversation and personal interaction, user trust regarding privacy is important to the growth of users and the increase in user engagement on our platform, and privacy concerns relating to our products and services could damage our reputation and deter current and potential users and advertisers from using our products and services.

From time to time, concerns have been expressed by governments, regulators and others about whether mobile products, services or practices compromise the privacy of users and others. Concerns about, governmental or regulatory actions involving practices with regard to the collection, use, disclosure or security of personal information or other privacy-related matters, even if unfounded, could damage our reputation, cause us to lose users and advertisers and adversely affect our operating results. While we will strive to comply with applicable data protection laws and regulations, as we strive to comply with our own posted privacy policies and other obligations we may have with respect to privacy and data protection, the failure or perceived failure to comply may result, in inquiries and other proceedings or actions against us by governments, regulators or others. These inquiries could result in negative publicity and damage to our reputation and brand, each of which could cause us to lose users and advertisers, which could have an adverse effect on our business.

Any systems failure or compromise of our security that results in the unauthorized access to or release of our users’ or advertisers’ data could significantly limit the adoption of our products and services and cause harm to our reputation and brand and, therefore, our business. We expect to continue to expend significant resources to protect against security breaches. The risk that these types of events could seriously harm our business is likely to increase as we expand the number of products and services we offer, increase the size of our user base and operate in other countries.

If our security measures are breached, or if our products and services are subject to attacks that degrade or deny the ability of users to access our products and services, our products and services may be perceived as not being secure, users and advertisers may curtail or stop using our products and services and our business and operating results could be harmed.

Our products and services involve the storage and transmission of users’ and advertisers’ information, and security breaches expose us to a risk of loss of this information, litigation and potential liability. We may experience cyber-attacks of varying degrees, and as a result, unauthorized parties may obtain, and may in the future obtain, access to its data or its users’ or advertisers’ data. Our security measures may also be breached due to employee error, malfeasance or otherwise. Additionally, outside parties may attempt to fraudulently induce employees, users or advertisers to disclose sensitive information in order to gain access to our data or our users’ or advertisers’ data or accounts, or may otherwise obtain access to such data or accounts. Since our users and advertisers may use their accounts to establish and maintain online identities, unauthorized communications from our accounts that have been compromised may damage their reputations. Any such breach or unauthorized access could result in significant legal and financial exposure, damage to our reputation and a loss of confidence in the security of our products and services that could have an adverse effect on our business and operating results. Because the techniques used to obtain unauthorized access, disable or degrade service or sabotage systems change frequently and often are not recognized until launched against a target, we may be unable to anticipate these techniques or to implement adequate preventative measures. If an actual or perceived breach of security occurs, the market perception of the effectiveness of our security measures could be harmed, we could lose users and advertisers and we may incur significant legal and financial exposure, including legal claims and regulatory fines and penalties. Any of these actions could have a material and adverse effect on our business, reputation and operating results.

We depend on highly skilled personnel to grow and operate our business, and if we are unable to hire, retain and motivate its personnel, we may not be able to grow effectively.