Attached files

| file | filename |

|---|---|

| EX-1.1 - EX-1.1 - Commercial Credit, Inc. | d809455dex11.htm |

| EX-23.1 - EX-23.1 - Commercial Credit, Inc. | d809455dex231.htm |

| EX-10.25 - EX-10.25 - Commercial Credit, Inc. | d809455dex1025.htm |

Table of Contents

As filed with the Securities and Exchange Commission on April 16, 2015

Registration No. 333-202881

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1 to

FORM S-1

REGISTRATION STATEMENT UNDER THE

SECURITIES ACT OF 1933

Commercial Credit, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 6199 | 47-1962209 | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

227 West Trade Street

Suite 1450

Charlotte, North Carolina 28202

(704) 944-2770

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Daniel J. McDonough

227 West Trade Street

Suite 1450

Charlotte, North Carolina 28202

(704) 944-2770

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| David S. Bakst John P. Berkery Mayer Brown LLP 1675 Broadway New York, New York 10022 Telephone: (212) 506-2500 Facsimile: (212) 262-1910 |

Richard D. Truesdell, Jr. Byron B. Rooney Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 Telephone: (212) 450-4000 Facsimile: (212) 701-5800 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ |

Accelerated filer ¨ | Non-accelerated filer þ | Smaller reporting company ¨ |

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of each class of securities to be registered | Proposed maximum aggregate offering price(1)(2) |

Amount of registration fee(3) | ||

| Common Stock, $0.00001 par value per share |

$100,000,000 | $11,620.00 | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes additional shares of common stock that the underwriters have the option to purchase. |

| (3) | This amount was previously paid in connection with the initial filing of this registration statement. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion, dated April 16, 2015

Preliminary prospectus

shares

Commercial Credit, Inc.

Common stock

$ per share

This is the initial public offering of our common stock. We are selling shares of our common stock and the selling stockholders are selling shares of our common stock. We will not receive any proceeds from the sale of shares to be offered by the selling stockholders. We currently expect the initial public offering price to be between $ and $ per share.

We have granted the underwriters an option for a period of 30 days to purchase up to additional shares of our common stock.

Prior to this offering, there has been no public market for our common stock. We have applied for listing of our common stock on the New York Stock Exchange under the symbol “CCR.”

We are an emerging growth company as that term is used in the Jumpstart Our Business Startups Act of 2012 and, as such, will be subject to certain reduced public company reporting requirements for this prospectus and future filings.

Investing in our common stock involves a high degree of risk. See “Risk factors” beginning on page 13.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

| Per share | Total | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions(1) |

$ | $ | ||||||

| Proceeds to us, before expenses |

$ | $ | ||||||

| Proceeds to the selling stockholders, before expenses |

$ | $ | ||||||

| (1) | We have agreed to reimburse the underwriters for certain FINRA-related expenses. See “Underwriting.” |

The underwriters expect to deliver the shares of common stock to purchasers on or about , 2015.

| J.P. Morgan | Keefe, Bruyette & Woods | |

| A Stifel Company | ||

| BMO Capital Markets | SunTrust Robinson Humphrey | Wells Fargo Securities | BB&T Capital Markets |

, 2015

Table of Contents

| ii | ||||

| ii | ||||

| ii | ||||

| 1 | ||||

| 14 | ||||

| 26 | ||||

| 28 | ||||

| 29 | ||||

| 30 | ||||

| 32 | ||||

| 34 | ||||

| Management’s discussion and analysis of financial condition and results of operations |

36 | |||

| 55 | ||||

| 61 | ||||

| 75 | ||||

| 81 | ||||

| 98 | ||||

| 101 | ||||

| 103 | ||||

| 107 | ||||

| Material U.S. federal tax considerations for non-U.S. holders of our common stock |

109 | |||

| 113 | ||||

| 121 | ||||

| 121 | ||||

| 121 | ||||

| 122 | ||||

| Index to condensed consolidated financial statements (Unaudited) |

F-1 | |||

| F-27 | ||||

We have not, the selling stockholders have not and the underwriters have not, authorized anyone to provide you with information that is additional to or different from that contained in this prospectus, any amendment or supplement to this prospectus or any free writing prospectus prepared by us or on our behalf. We, the selling stockholders and the underwriters do not take any responsibility for, and can provide no assurance as to the reliability of, any information other than the information in this prospectus, any

i

Table of Contents

amendment or supplement to this prospectus or any free writing prospectus prepared by us or on our behalf. This document may only be used where it is legal to sell these securities. You should assume that the information contained in this prospectus is accurate only as of the date of this prospectus.

No action is being taken in any jurisdiction outside the United States to permit a public offering of the common stock or possession or distribution of this prospectus, any amendment or supplement to this prospectus or any free writing prospectus in that jurisdiction. Persons who come into possession of this prospectus, any amendment or supplement to this prospectus or any free writing prospectus in jurisdictions outside the United States are required to inform themselves about and to observe any restrictions as to this offering and the distribution of the prospectus applicable to that jurisdiction.

On December 12, 2014, we engaged in a corporate reorganization described under the heading “Prospectus summary—Corporate reorganization,” pursuant to which Commercial Credit Group Inc. became a wholly-owned operating subsidiary of Commercial Credit, Inc., a newly formed holding company, which to date has not conducted any operations and has no material assets or liabilities, including contingent liabilities. Unless otherwise indicated or the context otherwise requires, references in this prospectus to “the company,” “we,” “us” and “our” refer to Commercial Credit, Inc., together with its consolidated subsidiaries, including Commercial Credit Group Inc., and references to “CCG” refer only to Commercial Credit Group Inc., our wholly-owned operating subsidiary. See “Prospectus summary—Corporate reorganization.”

Presentation of financial information

This prospectus contains the historical financial statements and other financial information of Commercial Credit Group Inc., which was recently acquired by and became a wholly-owned subsidiary of Commercial Credit, Inc. Commercial Credit, Inc.’s common shares are being offered hereby. Commercial Credit, Inc. is a newly formed holding company and has engaged to date only in activities incidental to its formation, the corporate reorganization and the initial public offering of our common shares. The consolidated financial statements of Commercial Credit, Inc. for the period ended December 31, 2014 include the financial results of Commercial Credit Group Inc., its wholly-owned subsidiary, as a result of the corporate reorganization that became effective as of December 12, 2014. For periods prior to December 12, 2014, this prospectus only includes consolidated financial statements of Commercial Credit Group Inc. and not Commercial Credit, Inc., as Commercial Credit, Inc. did not have any material assets, liabilities or operations other than nominal organizational expenses until it completed the corporate reorganization. See “Prospectus summary—Corporate reorganization.” We have made rounding adjustments to some of the figures included in this prospectus. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them.

Market and other industry data

This prospectus includes industry data, forecasts and information that we have prepared based, in part, upon data, forecasts and information obtained from independent industry publications and surveys and other information available to us. Some data is also based on our good faith estimates, which are derived from management’s knowledge of the industry and independent sources. Industry publications and surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but we have not independently verified any of the data from third-party sources nor have we ascertained the underlying economic assumptions relied upon therein. Statements as to our market position

ii

Table of Contents

are based on market data currently available to us. While we are not aware of any misstatements regarding the industry data presented herein, our estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under the heading “Risk factors” in this prospectus. Similarly, we believe our internal research is reliable, even though such research has not been verified by any independent sources.

iii

Table of Contents

This summary highlights information appearing elsewhere in this prospectus. This summary does not contain all of the information that you should consider before investing in our common stock. You should read carefully this entire prospectus, including “Risk factors,” the consolidated financial statements and notes thereto and the financial data and related notes contained herein before deciding whether to invest in shares of our common stock.

Our company

We are an independent financial services company engaged in the financing of commercial equipment. We provide secured loans and, to a lesser extent, leases to businesses that operate in the construction, fleet transportation and waste industries in the United States and Canada. Our target customers are primarily middle-market, family-owned businesses, and the equipment they finance with us is, in many cases, vital to their operations. This equipment includes mobile cranes, earth moving and paving equipment, over-the-road trucks and trailers, waste collection trucks and related equipment that are produced primarily by nationally recognized manufacturers.

Our business is relationship and service oriented. The loans and leases we originate enable our customers to acquire equipment and refinance existing obligations. We have a team of more than 50 experienced sales representatives who work directly with our customers, which we believe, given the size of their businesses, are often underserved by larger financial institutions. We complement our interaction with customers by building and maintaining relationships with equipment vendors and manufacturers and educating them about our financing parameters. However, we do not rely on marketing programs with equipment vendors or manufacturers to source new business. We believe that knowledge of our customers, their industries and the equipment they employ enables us to provide superior customer service and customized financing solutions while maintaining strong credit quality.

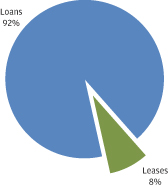

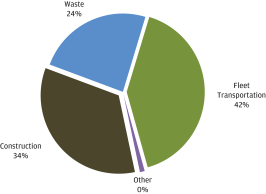

Since our inception in October 2004, our sales force has directly originated $1.9 billion of loans and leases. As of December 31, 2014, we had a finance receivables portfolio of $611.5 million, comprised of over 3,900 loans and leases to more than 1,800 customers. We originate loans and leases that typically range from $50,000 to $2.5 million per transaction. For the nine months ended December 31, 2014, our average new contract was approximately $209,000, had an original term of 46 months and had a yield of 9.8%. We retain all of our originations and hold them to maturity. The composition of our finance receivables portfolio by receivable and industry type as of December 31, 2014 can be seen in the charts below:

| Portfolio by Receivable Type, as of

|

Portfolio by Industry, as of

|

1

Table of Contents

Our finance receivables are secured by a first lien on the specific equipment financed. Additionally, our loans typically have fixed interest rates, are amortizing and include prepayment premium provisions. We also offer lease financing to our customers. As of December 31, 2014, there were $8.9 million of lease residuals retained on our balance sheet representing 1.5% of our finance receivables.

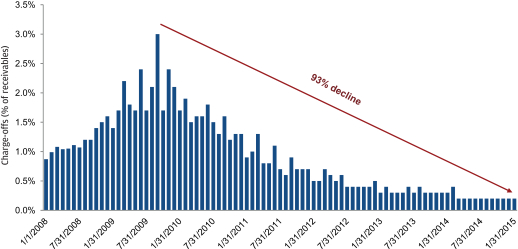

We concentrate on financing equipment that has an economic life longer than the term of the financing provided by us, is unlikely to be subject to rapid technological obsolescence, has applications in a variety of different industries, has a relatively broad resale market and is easily movable. We believe these characteristics of the underlying equipment, coupled with the expertise of our management team in underwriting, structuring and servicing of our finance receivables, have historically enabled us to minimize credit losses. Our annualized net charge-offs as a percentage of average finance receivables were 0.22% for the nine months ended December 31, 2014. For the fiscal year ended March 31, 2014, net charge-offs as a percentage of average finance receivables were 0.31%, and peaked at 0.65% for the fiscal year ended March 31, 2010.

We fund our portfolio through a combination of committed secured bank credit facilities, term and revolving asset-backed securitizations, unsecured subordinated debt and equity. Our funding providers are nationally recognized financial institutions. Our revolving credit facilities are on bilateral terms with staggered debt maturities. As of December 31, 2014, the ratio of our total senior outstanding debt to the sum of our equity plus our outstanding subordinated debt (our “leverage”) was 5.8x or x on a pro forma basis after giving effect to the intended application of net proceeds from this offering. Additionally, our financing strategy seeks to match the duration and interest rate characteristics of our portfolio by utilizing fixed rate term debt and interest rate hedges. As of December 31, 2014, 84% of our debt was either fixed rate debt or floating rate debt that had been swapped to a fixed rate using interest rate swaps.

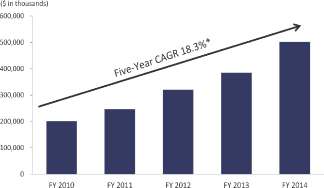

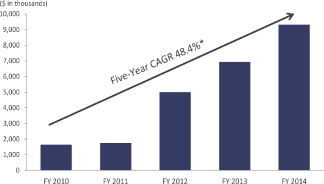

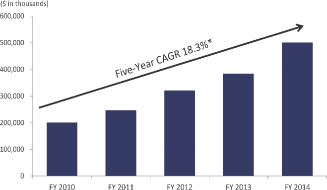

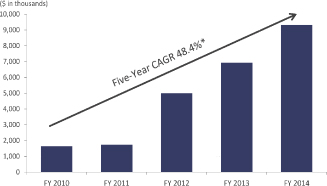

Our primary source of revenue is finance income earned on our finance receivables portfolio. Finance income includes interest, prepayment premiums and other fees less amortization of capitalized origination costs and was $41.1 million for the nine months ended December 31, 2014. Our portfolio yield is calculated as finance income divided by average finance receivables for a given period, stated as a percentage. For the nine months ended December 31, 2014, our annualized portfolio yield was 9.9%. Our net interest margin is the difference between the finance income and our total cost of funds. For the nine months ended December 31, 2014, our net interest margin was 7.0%. We generate profits to the extent that our net interest margin exceeds our provision for credit losses, salaries and operating expenses. For the nine months ended December 31, 2014, we generated net income of $9.0 million and had an annualized return on average shareholders’ equity of 21.1%. Over the last five fiscal years, finance receivables and net income have grown at a compound annual rate of 18.3% and 48.4%, respectively.

2

Table of Contents

5-Year Historical Growth in Finance Receivables

| * | Five-Year CAGR uses the period beginning with the fiscal year ended March 31, 2009. |

5-Year Historical Growth in Net Income

| * | Five-Year CAGR uses the period beginning with the fiscal year ended March 31, 2009. |

Our industry

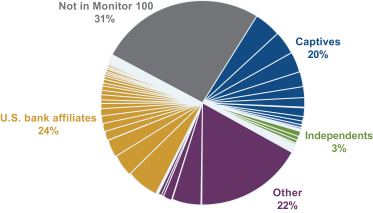

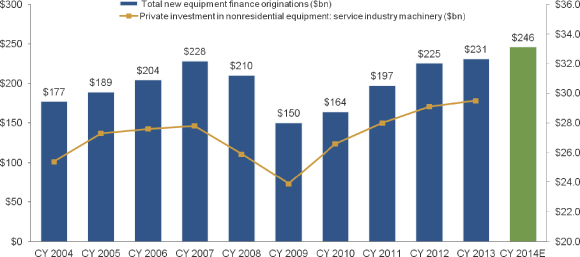

According to the Equipment Leasing and Finance Association (“ELFA”), U.S. equipment finance loans and leases are projected to exceed $900 billion in 2014. According to the 2014 Monitor 100 (“Monitor”), the top 100 equipment finance entities had $569 billion in aggregate net assets as of December 31, 2013 and together originated $231 billion in loans and leases in calendar year 2013. According to ELFA, new business volume across the equipment finance industry grew 9.3% and 16.4% in 2013 and 2012, respectively. Independent finance companies saw volume grow in 2013 at an even faster rate of 17.7%.

We believe that growth in the equipment finance industry is highly correlated to overall economic growth and is driven by investment in new equipment, together with customers’ propensity to utilize financing for existing and new equipment. Since 2010, Gross Private Domestic Investment as a percentage of U.S. GDP has increased by 23%, which we believe indicates a strengthening business appetite for equipment. We believe growth will continue as the equipment replacement cycle drives additional capital expenditures. In calendar year 2013, total public and private sector equipment and software investment grew by 3.2% and equipment finance volume grew by more than 8%.

3

Table of Contents

Industry participants include national and regional banking institutions, independent finance companies, manufacturer-owned finance companies, as well as smaller finance companies. According to Monitor, independent finance companies have represented as much as 10% of the industry’s net assets in 2007 compared to approximately 5% as of December 31, 2013.

Our business and growth strategies

Our business objectives are to grow our portfolio of finance receivables while seeking to maximize long-term earnings growth and generate attractive risk-adjusted returns through economic cycles. We believe the following strategies will help us meet these objectives:

Continue to focus on serving middle-market companies. Historically, small-and medium-sized businesses have been constrained in their ability to access traditional sources of financing. Our focus on middle-market businesses provides us the opportunity to meet what we believe is significant unfulfilled demand for financing among our target customers.

Maintain and grow our existing customer relationships. Our existing customers have historically been and we expect will continue to be a source of new business. Our service-oriented culture, strong customer relationships and focus on being a reliable financing partner have historically resulted in high levels of repeat business. For the nine months ended December 31, 2014, 68% of our originations were generated from existing customers. We believe our direct sales and customer contact model enhances our customer relationships, enabling us to offer customized financing solutions to meet customers’ individual needs. We will seek to continue to build and enhance customer loyalty, allowing us to increase business volume through our existing customer base.

Further penetrate existing markets. We have customers in all 50 states, as well as in Canada where we commenced operations in April 2014. However, we do not currently maintain marketing employees for each of our targeted industries in every state and province. We believe we can generate additional new business by increasing the number of dedicated sales and marketing employees within our current geographic footprint. By strengthening our industry coverage and further penetrating our existing markets, we expect that we can continue to drive significant growth.

Expand our geographic footprint. We plan to place dedicated sales representatives into additional U.S. states and Canadian provinces and expect that additional representatives in such regions will provide substantial incremental origination and portfolio growth. We have increased and intend to increase the number of representatives in key geographic regions that we believe are underserved. We have a proven track record of successfully entering new markets and hiring sales representatives to cover new territories.

Opportunistically pursue portfolio and business acquisitions. We believe that we possess the capacity to manage a larger finance receivables portfolio without substantially increasing our infrastructure costs. This is due to the scalable and efficient nature of our operating platform and the breadth and experience of our management team. As a result, we believe that we are also well positioned to opportunistically pursue portfolio and business acquisitions to complement our organic growth strategy. Currently, we do not have any agreements, arrangements or understandings to make any acquisitions.

4

Table of Contents

Our competitive strengths

We believe that the following competitive strengths enhance our ability to execute our business and growth strategies, creating long-term value for our shareholders:

Relationship-driven lending model.

We originate finance receivables through our team of more than 50 experienced sales representatives, serving over 1,800 unique customers as of December 31, 2014. We focus on direct relationships with end-users, a commitment to superior customer service, maintaining local presence and frequent in-person contact. We believe these attributes promote customer loyalty and present opportunities for repeat business. For the nine months ended December 31, 2014, 68% of our originations were generated from existing customers.

Rigorous risk management culture and collateral expertise leading to strong credit performance.

We maintain a conservative credit culture with strict underwriting standards. We evaluate each loan or lease based on the obligor’s cash flow, ability to pay, character and the collateral value of the equipment. Our underwriting policies and procedures were developed by our senior management team which possesses an average of over 25 years of experience in equipment finance. Substantially all of the loans and leases in our portfolio are subject to cross-collateralization and cross-default provisions. The useful life of the equipment we finance is typically greater than the amortization period of our loans and leases, which minimizes collateral risk and reduces losses. Our annualized net charge-offs as a percentage of average finance receivables were 0.22% for the nine months ended December 31, 2014. For the fiscal year ended March 31, 2014, net charge-offs as a percentage of average finance receivables were 0.31%, and peaked at 0.65% for the fiscal year ended March 31, 2010. Receivables from our small and medium-sized, privately owned customers may entail heightened risks given our customers’ sensitivity to the effects of, among other factors, poor regional and general economic conditions, rising fuel and financing costs, loss of key personnel and increased competition, any of which could negatively effect our customers’ operations and their ability to meet their obligations.

Diversified and high quality portfolio.

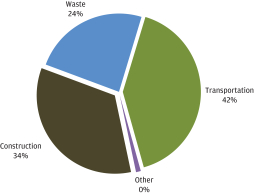

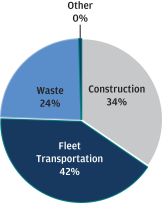

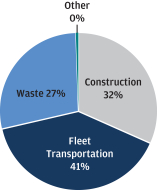

We concentrate on financing equipment that has an economic life longer than the term of the financing provided. Our finance receivables are secured by a first lien on the specific equipment financed. We strive to maintain a diversified portfolio across a number of categories, including customer, industry, equipment type and geography. For example, our largest customer represented 0.82% of our portfolio and our top 10 customers represented 6.5% of our portfolio as of December 31, 2014. Our portfolio is diversified across the fleet transportation (42%), construction (34%) and waste (24%) industries, as of December 31, 2014. We are also geographically diversified with our largest state concentrations in Texas, North Carolina and California constituting 13.0%, 9.7% and 8.8% of our portfolio, respectively, as of December 31, 2014.

Proven organic growth and consistently strong financial performance.

We believe we are well positioned to attract new customers and retain existing customers. Over the five fiscal years ended March 31, 2014, our originations and finance receivables grew at compound annual growth rates of 20.5% and 18.3%, respectively. Our net income has increased in each of our ten full years of operations, including during 2008 and 2009, and our ability to originate new finance receivables and increase our portfolio has helped us continue to grow net finance income and net income. For the five fiscal years ended March 31, 2014, we achieved compound annual growth rates for finance income and net income of 16.1% and 48.4%, respectively. Additionally, for the fiscal year ended March 31, 2014, our net income was $9.3 million, representing a return on average assets of 2.0% and a return on average shareholders’ equity of 19.3%. We

5

Table of Contents

believe that our portfolio size, track record and reputation with our customers, funding providers and employees give us operational scale, diversified and reliable access to funding and reputational advantage over our competitors as we continue to expand our business and attract new talent.

Experienced management team with significant ownership stake.

Members of our management team have worked together for almost two decades dating back to their time together at Financial Federal Corporation, a publicly-traded, independent equipment finance company prior to its acquisition in 2009 by People’s United Financial, Inc., whose portfolio reached a size of $2.0 billion at its peak. Our senior management team averages over 25 years of experience in the equipment finance industry, are major shareholders of the company and will beneficially own % of our common shares after this offering (assuming no exercise of the underwriters’ option to purchase additional shares). We believe this ownership stake aligns their interest with that of our shareholders.

Recent developments

Preliminary results for the year ended March 31, 2015

We are currently in the process of preparing our consolidated financial statements for the year ended March 31, 2015. The following are preliminary estimates of the financial information listed below as of and for the year ended March 31, 2015.

| • | Originations. We expect originations, the aggregate dollar amount of loans and leases booked during a given period, of between approximately $443.0 million to $457.0 million for the year ended March 31, 2015, as compared to $357.3 million for the year ended March 31, 2014. The increase was due to a higher rate of contract originations in this period as a result of the addition of sales and marketing staff in new geographic regions and influenced by a slightly better level of economic activity for our customers. |

| • | Finance receivables. We expect that our finance receivables outstanding at March 31, 2015 will be approximately $641.0 million to $661.0 million, as compared to $501.0 million as of March 31, 2014. The increase was due to the growth in origination volume described above. |

| • | Net income. We expect net income of between approximately $12.0 million to $13.0 million for the year ended March 31, 2015, as compared to $9.3 million for the year ended March 31, 2014. The increase was principally the result of the growth in finance receivables over this period. |

| • | Return on average assets. We expect that our return on average assets for the year ended March 31, 2015 will be between approximately 2.0% and 2.1%, as compared to 2.0% for the year ended March 31, 2014. |

| • | Leverage. We expect our leverage, the ratio of our total senior outstanding debt to the sum of our equity plus our outstanding subordinated debt, will be between approximately 6.0x to 6.1x, as compared to 5.2x as of March 31, 2014. |

| • | Return on average stockholders’ equity. We expect that our return on average stockholders’ equity for the year ended March 31, 2015 will be between approximately 20.6% and 22.2%, as compared to 19.3% for the year ended March 31, 2014. |

The estimates of our consolidated financial information as of and for the year ended March 31, 2015 were prepared by management as described above. These estimates are preliminary and subject to completion of our

6

Table of Contents

financial closing procedures. Our independent registered public accounting firm has not audited, reviewed, compiled or performed any procedures, and does not express an opinion or any other form of assurance, with respect to this preliminary financial information. This summary is not a comprehensive statement of our financial results for this period, and our actual results may differ materially from these estimates due to the completion of our financial closing procedures, final adjustments and other developments, including subsequent events, if any, that may arise between now and the time that the consolidated financial statements for this period are issued. These estimates should not be viewed as a substitute for full annual financial statements prepared in accordance with GAAP. In addition, these estimates for the year ended March 31, 2015 are not necessarily indicative of the results to be achieved for any future period. This summary is qualified by, and should be read together with, “Risk factors,” “Cautionary note regarding forward-looking statements,” “Management’s discussion and analysis of financial condition and results of operations,” the consolidated financial statements and notes thereto and the financial data and related notes contained in this prospectus.

Principal stockholders

The majority of our common stock is held collectively by Lovell Minnick Equity Partners III LP and Lovell Minnick Equity Partners III-A LP, which are investment funds managed by Lovell Minnick Partners LLC. We refer to these stockholders, collectively, as our “Principal Stockholders” or “Lovell Minnick.” Lovell Minnick currently holds 75% of our common shares and will beneficially own % of our common shares after this offering (assuming no exercise of the underwriters’ option to purchase additional shares).

Lovell Minnick Partners is an independent private equity firm, with offices in the Philadelphia and Los Angeles areas, that has raised over $1.1 billion in committed capital since its founding in 1999. The firm specializes in financial services and related business services opportunities and has provided equity capital for management buyouts, succession and ownership transitions, growth investments and recapitalizations for over 30 middle-market companies. See “Risk factors—Following this offering, we will most likely no longer be a controlled company; however, Lovell Minnick and its affiliated funds will continue to own a significant portion of our common stock, and their interests may differ from or conflict with the interests of our other stockholders.”

Risks affecting our business

Participating in this offering involves substantial risk. Our ability to execute our strategy is also subject to certain risks. The risks described under the heading “Risk factors” included elsewhere in this prospectus may cause us not to realize the full benefits of our strengths or may cause us to be unable to successfully execute all or part of our strategy. Some of the most significant challenges and risks include the following:

| • | Macroeconomic conditions could have a material adverse effect on our business, results of operations, financial condition and stock price; |

| • | Changes in market interest rates could have a material adverse effect on our net earnings, funding and liquidity; |

| • | We borrow most of the money we lend to our customers and any constraints on the amount of funds that are available for us to borrow at any given time could have a material adverse effect on our business, results of operations and financial condition; |

| • | Lending to small, privately owned companies exposes us to increased credit risk; |

| • | Our allowance for credit losses may not be adequate to cover actual losses, which may adversely affect our financial condition and results of operations; |

7

Table of Contents

| • | A reduction in the credit ratings of our asset-backed securities could materially increase the cost of our funding from, and restrict our access to, the capital markets; |

| • | Adverse developments in certain industries may have an adverse effect on our business, financial condition and results of operations; and |

| • | Lovell Minnick and its affiliated funds will continue to own a significant portion of our common stock, and their interests may differ from or conflict with the interests of our other stockholders. |

Before you invest in our common stock, you should carefully consider all of the information in this prospectus, including the matters set forth under the heading “Risk factors.”

Company information

We were incorporated in Delaware in 2014 and our wholly-owned, operating subsidiary Commercial Credit Group Inc. was incorporated in Delaware in 2004. Our principal executive offices are located at 227 West Trade Street, Suite 1450, Charlotte, North Carolina 28202 and our telephone number at that address is (704) 944-2770. Our internet address is www.commercialcreditinc.com. The information contained in or accessible from our website is not incorporated by reference into this prospectus, and such information should not be considered to be part of this prospectus.

Corporate reorganization

Commercial Credit, Inc. (“CCI”) is a Delaware corporation that was formed on July 31, 2014 by the board of directors of CCG, a Delaware corporation, for the purpose of creating a holding company corporate structure to optimize our corporate structure as the company’s operations continue to expand. The corporate reorganization was completed as of December 12, 2014 pursuant to which CCI filed an Amended and Restated Certificate of Incorporation (the “Amended Charter”) with the Secretary of State of the State of Delaware, and each stockholder of CCG contributed all of its shares of CCG’s capital stock to CCI in exchange for an equal number of newly issued shares of the corresponding class or series of capital stock of CCI (the “Share Exchange”). Upon the consummation of the Share Exchange, CCG became a direct, wholly owned subsidiary of CCI. Investors in this offering will only acquire, and this prospectus only describes the offering of, common shares of CCI.

We refer to the Share Exchange and the other transactions contemplated thereby as our “corporate reorganization.” The corporate reorganization occurred in several steps that are described below, all of which were completed prior to the consummation of this offering.

Exchange of CCG shares for CCI shares

Prior to the date of the Share Exchange, the capital stock of CCG was divided into Common Stock, par value $0.00001 per share, Series 1 Preferred Stock, par value $0.00001, and Series 2 Preferred Stock, par value $0.00001. On December 12, 2014, CCI filed the Amended Charter with the Secretary of State of the State of Delaware that authorized CCI to issue shares of Common Stock, par value $0.00001 per share, Series 1 Preferred Stock, par value $0.00001, and/or Series 2 Preferred Stock, par value $0.00001. Immediately following the filing of the Amended Charter, each stockholder of CCG entered into a Contribution Agreement, dated as of December 12, 2014, pursuant to which such stockholder contributed its shares of CCG to CCI in exchange for the issuance by CCI to such stockholder of the same number of shares of Common Stock, Series 1 Preferred Stock, and/or Series 2 Preferred Stock, as applicable, of CCI. As a result thereof, CCI became the sole shareholder of CCG.

8

Table of Contents

Concurrently with the Share Exchange, each new stockholder of CCI entered into a Stockholders Agreement and an Investor Rights Agreement with CCI that set forth certain governance and stockholder arrangements that are substantially similar to those that were in effect with respect to CCG prior to the Share Exchange. The Stockholder Agreement and Investor Rights Agreement are further described under the heading “Certain relationships and related party transactions.” Upon the completion of an “Initial Public Offering,” as such term is defined in the Stockholders Agreement to mean the first underwritten registered public offering of the company’s common stock, the Stockholders Agreement will terminate in accordance with its terms. We believe that this offering will satisfy the requirements of an Initial Public Offering as defined in the Stockholders Agreement. In addition, the bylaws of CCI, which were adopted prior to the Share Exchange, replicate the bylaws of CCG that were in effect prior to the Share Exchange.

By virtue of the execution of the Contribution Agreement, each share of Common Stock of CCG that was previously granted pursuant to the Commercial Credit Group Inc. 2012 Equity Incentive Plan (the “2012 Incentive Plan”) as a restricted share was exchanged for one share of Common Stock of CCI. In addition, in connection with corporate reorganization, CCG assigned to CCI, and CCI assumed from CCG, all of CCG’s rights and obligations under the 2012 Incentive Plan and under all restricted share agreements between CCG and each stockholder of CCG party thereto in respect of awards of restricted shares of Common Stock of CCG granted under the 2012 Incentive Plan. As a result thereof, all such restricted share agreements now apply to shares of Common Stock of CCI in the same manner and subject to the same terms and conditions that such restricted share agreements previously applied to shares of Common Stock of CCG prior to the Share Exchange.

Filing of amended charter of CCG

As the final step of our corporate reorganization, CCG filed an Eighth Amended and Restated Certificate of Incorporation with the Secretary of State of the State of Delaware on January 5, 2015. The filing of the Eighth Amended and Restated Certificate of Incorporation of CCG provided for the retirement of the previously authorized Series 1 Preferred Shares and Series 2 Preferred Shares of CCG and implemented a reverse stock split of the previously authorized shares of Common Stock of CCG.

Implications of being an emerging growth company

As a company with less than $1.0 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. As an emerging growth company, we may take advantage of specified reduced reporting requirements and are relieved from certain other significant requirements that are otherwise generally applicable to public companies. We may choose to take advantage of some or all of these provisions for as long as we remain an emerging growth company. We will remain an emerging growth company until the earlier of (1) the last day of the fiscal year (a) following the fifth anniversary of the completion of this offering, (b) in which we have total annual gross revenue of at least $1.0 billion, or (c) in which we are deemed to be a large accelerated filer, which means the market value of our common stock that is held by non-affiliates exceeds $700 million as of the prior September 30th, or (2) the date on which we have issued more than $1.0 billion in non-convertible debt securities during the prior three-year period. See “Risk factors—We are an ‘emerging growth company,’ and any decision on our part to comply only with certain reduced reporting and disclosure requirements applicable to emerging growth companies could make our common stock less attractive to investors.”

The JOBS Act permits an “emerging growth company” like us to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. We are choosing to “opt out” of this provision and, as a result, we will comply with new or revised accounting standards as required when they are adopted. Our decision to opt out of the extended transition period is irrevocable.

9

Table of Contents

The offering

| Common stock offered by us |

shares. |

| Common stock offered by the selling stockholders |

shares. |

| Common stock to be outstanding immediately after the completion of this offering |

shares (assuming no exercise of the underwriters’ option to purchase additional shares). |

| Underwriters’ option to purchase additional shares |

We, along with certain of the selling stockholders, have granted the underwriters a 30-day option to purchase up to an additional shares. If this option is exercised in full, we will issue and sell shares and the selling stockholders will sell shares. |

| Use of proceeds |

We expect to receive net proceeds, after deducting estimated offering expenses and underwriting discounts and commissions payable by us, of approximately $ million (or $ million if the underwriters exercise their option to purchase additional shares in full), based on an assumed offering price of $ per share (the midpoint of the offering price range set forth on the cover page of this prospectus). We intend to use the net proceeds from this offering to retire the outstanding aggregate principal amount of our senior subordinated notes in the amount of $33 million, plus any interest and fees, and for working capital and general corporate purposes. We may also pay down our credit facilities. We will not receive any proceeds from the sale of shares of common stock by the selling stockholders. See “Use of proceeds” and “Principal and selling stockholders.” |

| Dividend policy |

We do not currently pay cash dividends on our common stock and do not anticipate paying any dividends on our common stock in the foreseeable future. Any future determinations relating to our dividend policy will be made at the discretion of our board of directors and will depend on various factors. See “Dividend policy.” |

| Risk factors |

You should read carefully this prospectus, including “Risk factors” for a discussion of factors that you should consider before deciding to invest in shares of our common stock. |

| Proposed trading symbol |

“CCR.” |

10

Table of Contents

Unless otherwise indicated, all information in this prospectus relating to the number of shares of common stock to be outstanding immediately after the completion of this offering:

| • | assumes the conversion, which we expect to take place immediately prior to the completion of this offering, of all outstanding shares of all series of our preferred stock into an aggregate of shares of common stock; |

| • | excludes shares of our common stock reserved as of , 2015 for future grants under our incentive plan, as described under the heading “Executive and director compensation—2015 Stock incentive plan,” which we intend to adopt in connection with this offering; and |

| • | assumes no exercise by the underwriters of their option to purchase up to an additional shares. |

11

Table of Contents

Summary consolidated financial and other data

The following summary of the consolidated financial data of Commercial Credit Group Inc. should be read in conjunction with, and is qualified by reference to, the consolidated financial statements and notes thereto appearing elsewhere in this prospectus, as well as “Selected consolidated financial and other data,” “Management’s discussion and analysis of financial condition and results of operations” and the other financial information included elsewhere in this prospectus. The consolidated statement of income data for the fiscal years ended March 31, 2012, 2013 and 2014 and the summary consolidated balance sheet data at March 31, 2013 and 2014 are derived from, and are qualified by reference to, our audited consolidated financial statements included elsewhere in this prospectus and should be read in conjunction with those consolidated financial statements and notes thereto. The summary consolidated balance sheet data at March 31, 2012 are derived from our consolidated financial statements not included in this prospectus. The consolidated statement of income data for the nine months ended December 31, 2013 and 2014 and the summary consolidated balance sheet data at December 31, 2013 and 2014 are derived from, and are qualified by reference to, our unaudited condensed consolidated financial statements included elsewhere in this prospectus and, in our opinion, reflect all adjustments, consisting of normal accruals, necessary for a fair presentation of the data for those periods. Our results of operations for the nine months ended December 31, 2014 may not be indicative of results that we may achieve for the full fiscal year. See “Index to consolidated financial statements.”

Commercial Credit, Inc. is a newly formed holding company and had only engaged in operations and activities incidental to its formation, the corporate reorganization that became effective as of December 12, 2014 and the initial public offering of our common shares. The consolidated financial statements of Commercial Credit, Inc. for the period ended December 31, 2014 include the financial results of Commercial Credit Group Inc., its wholly-owned subsidiary, as a result of the corporate reorganization. For periods prior to December 12, 2014, this prospectus only includes consolidated financial statements of Commercial Credit Group Inc. and not Commercial Credit, Inc., as Commercial Credit, Inc. did not have any material assets, liabilities or operations other than nominal organizational expenses until it completed the corporate reorganization. Our historical consolidated financial data may not be indicative of future results.

| Year

ended March 31, |

Nine months ended December 31, |

|||||||||||||||||||

| 2012 | 2013 | 2014 | 2013 | 2014 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Statement of Income Data: |

||||||||||||||||||||

| Finance income |

$ | 33,206 | $ | 40,226 | $ | 45,806 | $ | 33,804 | $ | 41,109 | ||||||||||

| Interest expense |

15,353 | 16,546 | 15,586 | 11,622 | 11,850 | |||||||||||||||

|

|

|

|||||||||||||||||||

| Net finance income before provision for credit losses on finance receivables |

17,852 | 23,680 | 30,220 | 22,182 | 29,259 | |||||||||||||||

| Provision for credit losses on finance receivables |

1,975 | 1,825 | 2,348 | 2,098 | 1,700 | |||||||||||||||

|

|

|

|||||||||||||||||||

| Net finance income |

15,877 | 21,855 | 27,872 | 20,084 | 27,559 | |||||||||||||||

| Compensation and benefits |

4,348 | 6,724 | 8,009 | 5,389 | 7,608 | |||||||||||||||

| Other operating expenses |

3,543 | 3,893 | 4,259 | 3,846 | 5,110 | |||||||||||||||

|

|

|

|||||||||||||||||||

| Total operating expenses |

7,891 | 10,617 | 12,268 | 9,235 | 12,718 | |||||||||||||||

| Income before income taxes |

7,986 | 11,238 | 15,605 | 10,850 | 14,841 | |||||||||||||||

| Provision for income taxes |

3,124 | 4,380 | 6,255 | 4,291 | 5,812 | |||||||||||||||

|

|

|

|||||||||||||||||||

| Net income |

$ | 4,861 | $ | 6,857 | $ | 9,349 | $ | 6,559 | $ | 9,029 | ||||||||||

|

|

||||||||||||||||||||

12

Table of Contents

| Year ended March 31, | Nine months ended December 31, |

|||||||||||||||||||

| 2012 | 2013 | 2014 | 2013 | 2014 | ||||||||||||||||

| Earnings per Share Data: |

||||||||||||||||||||

| Earnings per share, basic and diluted(1) |

$ | 1.28 | $(86.74 | ) | $ | 11.93 | $ | — | $ | 13.25 | ||||||||||

| Pro forma earnings per share, basic and diluted(2) |

1.27 | (5.64 | ) | 11.86 | 7.92 | 13.27 | ||||||||||||||

| Weighted average shares used in computing earnings per share, basic and diluted (in thousands) |

245 | 263 | — | — | 2 | |||||||||||||||

| Shares used in computing pro forma earnings per share, basic and diluted(2) (in thousands) |

3,826 | 4,044 | 682 | 669 | 681 | |||||||||||||||

|

|

||||||||||||||||||||

| (1) | On May 10, 2012, pursuant to the Recapitalization, all then-outstanding shares of common stock were converted into Series 1 preferred stock. To show the impact of the Recapitalization on earnings per share for the year, the Company calculated earnings per share separately for the 40-day period prior to Recapitalization, beginning April 1, 2012 to May 10, 2012 (“pre-Recapitalization”) and the 325-day period after Recapitalization beginning May 11, 2012 to March 31, 2013 (“post-Recapitalization). The $(86.74) cited in this table represents the earnings per common share for the pre-Recapitalization period. Although no shares of common stock were outstanding during the post-Recapitalization period ended March 31, 2013, or during the nine month period ended December 31, 2013, the Company had outstanding participating securities in the form of convertible preferred stock and unvested restricted stock in both periods. For additional information regarding the calculation of earnings per share, see Note 11 to the annual consolidated financial statements for the three year period ended March 31, 2014 and Note 10 to the interim unaudited condensed consolidated financial statements for the nine month periods ended December 31, 2013, and 2014. |

| (2) | Pro forma basic and diluted earnings per share have been calculated assuming the conversion of all shares of our preferred stock and unvested restricted stock awards outstanding at each of the relevant period ends into shares of common stock as of the beginning of each of the applicable periods. |

| At March 31, | At December 31, | |||||||||||||||||||

| 2012 | 2013 | 2014 | 2013 | 2014 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Summary Balance Sheet Data: |

||||||||||||||||||||

| Finance receivables, net |

$ | 315,997 | $ | 378,512 | $ | 494,683 | $ | 464,661 | $ | 604,329 | ||||||||||

| Total assets |

345,453 | 404,959 | 541,996 | 504,241 | 649,496 | |||||||||||||||

| Total debt |

300,257 | 350,700 | 479,422 | 443,696 | 577,332 | |||||||||||||||

| Total shareholders’ equity |

36,239 | 44,388 | 52,591 | 49,788 | 61,514 | |||||||||||||||

|

|

||||||||||||||||||||

| Year ended March 31, | Nine months ended December 31, |

|||||||||||||||||||

| 2012 | 2013 | 2014 | 2013 | 2014 | ||||||||||||||||

| ($ in thousands, except for percentages and ratios) | ||||||||||||||||||||

| Operating Data: |

||||||||||||||||||||

|

Originations(1) |

$ | 228,603 | $ | 251,683 | $ | 357,313 | $ | 255,757 | $ | 332,821 | ||||||||||

| Portfolio yield |

11.7% | 11.4% | 10.4% | 10.5% | 9.9% | |||||||||||||||

| Net interest margin |

6.3% | 6.7% | 6.8% | 6.9% | 7.0% | |||||||||||||||

| Net charge-off ratio (annualized)(2) |

0.44% | 0.20% | 0.31% | 0.29% | 0.22% | |||||||||||||||

| Return on average assets |

1.6% | 1.8% | 2.0% | 1.9% | 2.0% | |||||||||||||||

|

Leverage(3) |

4.8x | 4.1x | 5.2x | 5.0x | 5.8x | |||||||||||||||

| Return on average stockholders’ equity |

14.4% | 17.0% | 19.3% | 18.6% | 21.1% | |||||||||||||||

|

|

||||||||||||||||||||

| (1) | Originations are the aggregate dollar amount of loans and leases booked during a given period. |

| (2) | Our net charge-off ratio is the ratio of net charge-offs to the average finance receivables for a given period, stated as a percentage. Net charge-offs is the amount of the reduction in the allowance for credit losses when a finance receivable or a portion thereof is charged off under GAAP. |

| (3) | Our leverage is the ratio of our total senior outstanding debt to the sum of our equity plus our outstanding subordinated debt. The amount payable on our subordinated notes was $22.0 million in the year ended March 31, 2012 and $33.0 million in each of the years ended March 31, 2013 and 2014 and the nine month periods ended December 31, 2013 and 2014. |

13

Table of Contents

An investment in our common stock involves a high degree of risk. You should carefully consider the following risks and the other information contained in this prospectus, including our consolidated financial statements and the related notes, before investing in our common stock. If any of the following risks actually occurs, our business, financial condition, results of operations, cash flows and prospects would likely suffer, possibly materially. In addition, the trading price of our common stock could decline due to any of these risks occurring, and you may lose all or part of your investment in our common stock.

Risks related to our business

Macroeconomic conditions could have a material adverse effect on our business, results of operations, financial condition and stock price.

Key macroeconomic conditions historically have affected our business, results of operations and financial condition and are likely to affect them in the future. Consumer confidence, energy prices, unemployment, infrastructure spending by state and local governments and residential and non-residential construction activity are among the factors that often impact the borrowing behavior of our customers. Poor economic conditions reduce the demand for industrial and commercial equipment and our customers’ ability to repay their obligations to us which, in each case, reduces our finance income and increases our credit losses.

While certain economic conditions in the United States have shown signs of improvement following the recent global economic crisis, economic growth has been slow and uneven as consumers continue to face domestic concerns, as well as economic and political conditions in the global markets. A prolonged period of slow economic growth or a significant deterioration in economic conditions would likely affect our customers’ activity levels and the ability and willingness of customers to finance new purchases or leases or to pay amounts already owed to us, and could have a material adverse effect on our business, results of operations and financial condition.

A deterioration in macroeconomic conditions could also adversely affect our ability to fund in the wholesale market at attractive rates which could increase our cost of capital. For example, in 2009, the economic crisis had a deep impact on the wholesale funding market which significantly affected the terms of our funding in that market, particularly in the aftermath of the bankruptcy of Lehman Brothers Holdings, Inc. A reduction in our financing opportunities or market developments that make wholesale funding unprofitable could negatively impact our business, financial condition and results of operations.

Macroeconomic conditions may also cause our net earnings to fluctuate and diverge from expectations of securities analysts and investors, who may have differing assumptions regarding the impact of these conditions on our business, and this may adversely impact the trading price of our common stock.

Changes in market interest rates could have a material adverse effect on our net earnings, funding and liquidity.

Our profitability depends in large part upon the extent to which our average yield on finance receivables exceeds our average cost of borrowed funds (“net interest spread”). Because our borrowed funds mature or reprice at a faster rate than our finance receivables, a rapid and sustained rise in market interest rates, increasing our total cost of funds, could materially reduce our net interest spread and, therefore, reduce or eliminate our profitability. In addition, increases in market interest rates could materially reduce the volume of originations of new financings and leases because current or prospective customers may refrain from borrowing at higher rates of interest.

14

Table of Contents

We borrow most of the money we lend to our customers and any constraints on the amount of funds that are available for us to borrow at any given time could have a material adverse effect on our business, results of operations and financial condition.

We borrow most of the money we lend to our customers and, as a result, liquidity, or the amount of funds that are available for us to borrow at any given time, is very important to our business. Our inability to access funds, or to access funds on commercially attractive terms, to support our financing activities could have an adverse effect on our business, results of operations and financial condition.

Continuing to meet our cash requirements over the long-term could require substantial liquidity and access to sources of funds, including capital and credit markets. Such markets may not continue to represent a reliable source of financing, particularly if global economic conditions were to deteriorate. In the face of deteriorating global economic conditions, we could face materially higher financing costs, become unable to access adequate funding to operate and grow our business and/or meet our debt service obligations as they mature, and could be required to draw upon contractually committed lending agreements and/or to seek other funding sources. However, under distressed market conditions, such liquidity or funding sources may not be sufficient for our needs or available at all, which would restrict or prohibit our ability to generate new finance receivables and negatively affect our income, results of operations and financial condition.

Lending to small and medium sized, privately owned companies exposes us to increased credit risk.

Inherent in our business is the credit risk associated with our customers. The creditworthiness of each customer and the rate of delinquencies, repossessions and net losses on customer obligations are directly impacted by several factors, including relevant industry and economic conditions, the availability of capital, the experience and expertise of the customer’s management, commodity prices and the sustained value of the underlying collateral. We provide financings primarily to small and medium-sized, privately owned businesses. As compared to larger, publicly owned firms, these companies generally have more limited access to capital and higher funding costs, may be in a weaker financial position and may need more capital to expand or compete. Accordingly, receivables from the type of customers we typically serve may entail heightened risks. These customers are more sensitive to the effects of, among other factors, poor regional and general economic conditions, rising fuel and financing costs, loss of key personnel and increased competition. The effects of any of these factors on our customers’ operations and the ability of our customers to meet their obligations could negatively impact our business, financial condition and results of operations. As of December 31, 2014, no single customer represented more than 0.8% of our finance receivables.

Our allowance for credit losses may not be adequate to cover actual losses, which may adversely affect our financial condition and results of operations.

We maintain an allowance for credit losses to cover management’s estimate of expected future losses as of the balance sheet date resulting from the non-performance of our customers under their contractual obligations. The determination of the allowance involves significant assumptions, complex analysis, and management judgment and requires us to make significant estimates of current credit risks using existing qualitative and quantitative information, any or all of which may change. As a result, our allowance for credit losses may not be adequate to cover our actual losses. In addition, changes in economic conditions affecting our customers, accounting rules and related guidance and other factors, both within and outside of our control, may require changes to the allowance for credit losses. A material increase in our allowance for credit losses or a material difference between our allowance for credit losses and our actual losses may adversely affect our financial condition and results of operations.

15

Table of Contents

A reduction in the credit ratings of our asset-backed securities could materially increase the cost of our funding from, and restrict our access to, the capital markets.

Certain of the asset-backed securities issued by our securitization trusts are rated by Standard & Poor’s Ratings Services (“S&P”) and DBRS, Inc. (“DBRS”). As of December 31, 2014, the company had two term asset securitization borrowings outstanding. Each transaction had three notes outstanding at inception. The Class A-1 Notes were rated A1+(sf) and R-1(h)(sf), the Class A-2 Notes were rated AAA(sf) and AAA(sf) and the Class B Notes were rated A(sf) and A(sf), in each case by S&P and DBRS, respectively. There have been no subsequent changes to these ratings. We have not had any of our current or prior asset-backed securities downgraded by any rating agency, although it is possible that a downgrade of one or more of our asset-backed securities could occur in the future. The ratings of our asset-backed securities are, and will continue to be, based on a number of factors, including the quality of the underlying loans and the credit enhancement structure with respect to each series of asset-backed securities, as well as general performance of the underlying loans. These ratings also reflect the various methodologies and assumptions used by the rating agencies, which are subject to change and could adversely affect our ratings. The rating agencies regularly evaluate the credit ratings of our asset-backed securities. We may be unable to maintain our asset-backed securities’ credit ratings or such credit ratings may be lowered or withdrawn in the future. A downgrade in our asset-backed securities’ credit ratings (or investor concerns that a downgrade may occur) could materially increase the cost of our funding from, and restrict our access to, the capital markets.

If we fail to comply with financial and other covenants under our loan agreements, our business, financial condition and results of operations may be materially and adversely affected.

We enter into loan agreements containing financial and other covenants that require us to maintain certain financial ratios or impose certain restrictions on the disposition of our assets or the conduct of our business. While we are currently in compliance with all financial and other covenants, we may be unable to comply with some or all of these financial and other covenants in the future, particularly in periods of broader economic distress. If we are in breach of one or more financial or other covenants under any of our loan agreements and are not able to obtain waivers from the lenders or prepay such loan, such breach would constitute an event of default under the loan agreement. As a result, repayment of the indebtedness under the relevant loan agreement may be accelerated, which may in turn require us to repay the entire principal amount including interest accrued, if any, of certain of our other existing indebtedness prior to their maturity under cross-default provisions of other loan agreements. If we are required to repay a significant portion or all of our existing indebtedness prior to their maturity, we may lack sufficient financial resources to do so. Furthermore, a breach of those financial and other covenants will also restrict our ability to pay dividends. Any of those events could have a material adverse effect on our business, financial condition and results of operations.

Adverse developments in certain industries may have an adverse effect on our business, financial condition and results of operations.

Our customers are concentrated in the construction, fleet transportation and waste industries, which are sensitive to changes in general levels of activity in related industries, which may include services, manufacturing, mining, distribution and wholesale, forestry, transportation and retail. Adverse developments concerning any of these related industries may also increase the rate of delinquencies and defaults by our customers in the construction, fleet transportation and waste industries. Any resulting delay or reduction in collection of payments on our receivables may negatively impact our business, financial condition and results of operations. Adverse changes in these industries may have a corresponding adverse effect on amounts received upon a foreclosure from the sale or other disposition of financed equipment.

16

Table of Contents

We are in a highly competitive business and may not be able to compete effectively, which could impact our profitability.

Our business is highly competitive. We compete with banks, manufacturer-owned and independent finance and leasing companies, as well as other financial institutions. These competitors may have sources of funds available at a lower cost than those available to us, thereby enabling them to provide financing at rates lower than we may be able to profitably provide. In addition, these competitors may be better positioned than we are to market various services and financing programs to vendors and users of equipment because of their ability to offer additional services and products, and more favorable rates and terms. Many of these competitors offer point-of-sale access to the customer which we cannot. These competitors may have longer operating histories and may possess greater financial and other resources than we do. As a result of competition, we may not be able to attract new customers, retain existing customers or sustain the rate of growth that we have experienced to date, and our ability to maintain or grow our portfolio may decline.

Because our underwriting process relies heavily on information provided by our customers, we are susceptible to customer fraud, which could cause us to suffer losses.

In underwriting new business, we do not utilize credit scoring or actuarial models to evaluate any credit request, but rely on credit packages compiled by our credit analysts, which include, among other things, detailed information provided by the customer. A customer could defraud us by, among other things:

| • | misrepresenting their financial performance or business prospects; |

| • | failing to accurately report their financial position; |

| • | overstating or falsifying records showing their asset values; |

| • | failing to notify us of breaches under agreements with us or other lenders; |

| • | misstating or falsifying required reports; or |

| • | providing inaccurate reporting of other financial information. |

The failure of a customer to accurately report its financial position, compliance with loan covenants or eligibility for additional borrowings could result in our extending credit to a customer that does not meet our underwriting criteria. This may result in an increased likelihood of defaults in payments and increased losses. This risk is heightened for us because most of our customers do not publicly report their financial condition or results of operations.

Technological obsolescence of equipment or regulatory or other changes affecting the equipment we finance may reduce the value of the collateral for our loans.

If technological advances or regulatory changes relating to or affecting the underlying equipment we finance cause such equipment to become obsolete or restrict the use of the equipment or, in either case, render its use uneconomical compared to other available technologies, the value of the underlying equipment will decrease. Such developments, particularly with respect to the types of equipment we finance, would reduce the amount of monies recoverable should the underlying equipment be sold following a customer default on the related receivable and as a result our business, financial condition and results of operations could be negatively affected.

Additionally, most of the underlying equipment we finance uses gasoline or diesel fuel, which is a significant, critical operating expense for our customers. Disruptions in availability or unexpectedly large increases in the price of fuel could impair the ability of our customers to make payments on their contracts, which could negatively impact our business, financial condition and results of operations.

17

Table of Contents

Cyber-attacks or other security breaches could have a material adverse effect on our business.

In the normal course of business, we collect, process and retain sensitive and confidential information regarding our customers. We also have arrangements in place with third parties through which we share and receive information about their customers who are or may become our customers. Although we devote significant resources and management focus to ensuring the integrity of our systems through information security and business continuity programs, our facilities and systems, and those of our third-party service providers, are vulnerable to external or internal security breaches, acts of vandalism, computer viruses, misplaced or lost data, programming or human errors, or other similar events. We and our third-party service providers have experienced all of these events in the past and expect to continue to experience them in the future. These events could interrupt our business or operations, result in significant legal and financial exposure, damage to our reputation or a loss of confidence in the security of our systems, products and services. Although the impact to date from these events has not had a material adverse effect on us, we cannot be sure this will be the case in the future.

Information security risks for financial services companies like us have increased recently in part because of new technologies, the use of the internet and telecommunications technologies (including mobile devices) to conduct financial and other business transactions and the increased sophistication and activities of organized crime, perpetrators of fraud, hackers, terrorists and others. In addition to cyber-attacks or other security breaches involving the theft of sensitive and confidential information, hackers recently have engaged in attacks against large financial institutions that are designed to disrupt key business services, such as consumer-facing web sites. We are not able to anticipate or implement effective preventive measures against all security breaches of these types, especially because the techniques used change frequently and because attacks can originate from a wide variety of sources. We employ detection and response mechanisms designed to contain and mitigate security incidents, but early detection may be thwarted by sophisticated attacks and malware designed to avoid detection.

Geographical concentrations of our customers may affect our business, financial condition and results of operations.

Economic conditions such as unemployment, fuel prices, interest rates, inflation rates and effects of natural catastrophes in a state or province where our customers are located may affect loss experience and payment rates on our receivables. Adverse economic conditions in a state where a large number of our customers are located could have a disproportionately significant effect on the loss experience or payment rates on our receivables. The consequences of a decline in regional economic conditions, including rising unemployment, fluctuating fuel prices, increasing interest rates and a lack of availability of credit, may lead to increased delinquency and default rates by our customers, as well as decreased demand for construction, fleet transportation or waste equipment and declining market value of the related equipment securing our receivables, which could increase the amount of a loss if a customer defaults. As of December 31, 2014, 13.0%, 9.7%, 8.8%, 6.8% and 6.1% of our receivables balance are related to customers located in Texas, North Carolina, California, Georgia and Illinois, respectively. As of December 31, 2014, no other state represented more than 5.0% of our receivables. Adverse economic conditions in one or more of these states may affect demand for construction, fleet transportation and waste equipment and payments on our receivables from our customers located in that state.

The occurrence of a natural disaster in a state may also adversely affect our customers located in that state. In addition, we may be unable to accurately assess the effect of a natural disaster on the economy or on our customers or receivables in an affected state. The effect of natural disasters on the performance of our customers and receivables is unclear, but there may be an adverse effect on general economic conditions, consumer confidence and general market liquidity. Adverse impacts as a result of a further decline in economic

18

Table of Contents

conditions, natural disaster or any similar event may affect our business, financial condition and results of operations.

The loss of one or more of our key personnel, or our failure to attract and retain other highly qualified personnel in the future, could harm our business.

Our success has been and will be largely dependent on Daniel J. McDonough, our Chief Executive Officer, and other key personnel. Competition for qualified personnel in the financial services industry is intense, and we may not be able to retain existing personnel. Although we have entered into employment agreements with Mr. McDonough, Mr. Gebhart, Mr. McGinn, Mr. Pokorny, Mr. Lempko and Mr. Garubo, the agreements have no specific duration and constitute at-will employment. The loss of key personnel, including members of management as well as key marketing and sales personnel, could disrupt our operations and have an adverse effect on our business.

As we continue to grow, we cannot guarantee we will continue to attract the personnel we need to grow our business. If we do not succeed in attracting, hiring, and integrating excellent personnel, or retaining and motivating existing personnel, we may be unable to grow effectively.

If we fail to effectively manage our growth, our results of operations could be adversely affected.