Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - BTCS Inc. | Financial_Report.xls |

| EX-32 - BTCS Inc. | ex32.htm |

| EX-31 - BTCS Inc. | ex31.htm |

| EX-21.1 - BTCS Inc. | ex21-1.htm |

| EX-10.52 - BTCS Inc. | ex10-52.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

[X]

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2014

|

or

|

[ ]

|

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____________ to ______________

|

Commissions file number 000-55141

BITCOIN SHOP, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

|

26-2477977

|

|

|

(State or other jurisdiction of

Incorporation or organization)

|

(I.R.S. Employer

Identification No.)

|

|

1901 North Fort Myer Drive, Suite #1105

Arlington, Virginia

|

22209

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code (202) 430-6576

Securities registered under Section 12(b) of the Exchange Act: None.

Securities registered under Section 12(g) of the Exchange Act:

Common Stock, $0.001 par value

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

Yes [ ] No [X]

Indicate by check mark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers in response to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendments to this From 10-K.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

[ ]

|

Accelerated filer

|

[ ]

|

|

Non-accelerated filer

(Do not check if a smaller reporting company)

|

[ ]

|

Smaller reporting company

|

[X]

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter

As of June 30, 2014, the aggregate market value of voting stock held by non-affiliates of the registrant, based on the closing sales price of Common Stock on June 30, 2014 ($0.17), was approximately $7,632,322. As of April 6, 2015, the registrant had 148,277,563 shares of Common Stock outstanding.

TABLE OF CONTENTS

BITCOIN SHOP, INC.

FORWARD LOOKING STATEMENTS

This Annual Report on Form 10-K and other written and oral statements made from time to time by us may contain forward-looking statements. Forward-looking statements can be identified by the use of words such as “expects,” “plans,” “will,” “forecasts,” “projects,” “intends,” “estimates,” and other words of similar meaning. One can identify them by the fact that they do not relate strictly to historical or current facts. These statements are likely to address our growth strategy, financial results and product and development programs. One must carefully consider any such statement and should understand that many factors could cause actual results to differ from our forward looking statements. These factors may include inaccurate assumptions and a broad variety of other risks and uncertainties, including some that are known and some that are not. No forward-looking statement can be guaranteed and actual future results may vary materially.

These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks in the section entitled “Risk Factors” and the risks set out below, any of which may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. These risks include, by way of example and not in limitation:

|

●

|

The uncertainty of profitability based upon our history of losses;

|

|

●

|

Risks related to failure to obtain adequate financing on a timely basis and on acceptable terms to continue as going concern; and

|

|

●

|

Other risks and uncertainties related to our business plan and business strategy.

|

This list is not an exhaustive list of the factors that may affect any of our forward-looking statements. These and other factors should be considered carefully and readers should not place undue reliance on our forward-looking statements. Forward looking statements are made based on management’s beliefs, estimates and opinions on the date the statements are made and we undertake no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States we do not intend to update any of the forward-looking statements to conform these statements to actual results.

Information regarding market and industry statistics contained in this Annual Report on Form 10-K is included based on information available to us that we believe is accurate. It is generally based on industry and other publications that are not produced for purposes of securities offerings or economic analysis. We have not reviewed or included data from all sources. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and the additional uncertainties accompanying any estimates of future market size, revenue and market acceptance of products and services. As a result, investors should not place undue reliance on these forward-looking statements.

As used in this annual report, the terms “we”, “us”, “our”, “BTCS” and the “Company” mean Bitcoin Shop, Inc. and its subsidiaries, unless otherwise indicated.

PART I

INTRODUCTION

During February 2014 we entered the business of hosting an online ecommerce marketplace where consumers can purchase merchandise using digital currencies, including bitcoin and are building a diversified company with operations in the digital currency ecosystem. In January 2015 we began a rebranding campaign using our BTCS.COM domain (shorthand for Blockchain Technology Consumer Solutions) to better reflect our broadened strategy. We released our new website which included broader information on our strategy, access to our ecommerce site, and launching an invite only beta version of our multi-sig secure storage solution (digital wallet).

We were incorporated in the State of Nevada in 2008 under the name “Hotel Management Systems, Inc.” On February 5, 2014, we entered into an Exchange Agreement with BitcoinShop.us, LLC, a Maryland limited liability company (“Bitcoinshop”), and the holders of the membership interests in BitcoinShop. Upon closing of Share Exchange, Bitcoinshop Members transferred all the outstanding membership interests of Bitcoinshop to the Company in exchange for an aggregate of 100,773,923 shares of the Company’s common stock (the “Reverse Merger”). As a result, Bitcoinshop became a wholly-owned subsidiary of the Company. Immediately following the Share Exchange with Bitcoinshop, the Company discontinued its business as manufacturer of touch screen and touch board products, interactive whiteboard displays and large touch-screens.

OUR BUSINESS

We are an early entrant in the digital currency ecosystem and one of the first U.S. publicly traded companies to be involved with digital currencies. We aim to enable users to engage in the digital currency ecosystem through one point of access — a universal digital currency platform. We plan to design and build this platform under the brand “Blockchain Technology Consumer Solutions,” or “BTCS.” We currently operate a beta ecommerce marketplace which already accepts a variety of digital currencies, have designed a beta secure digital currency storage solution BTCS Wallet, and have been expanding our transaction verification services business, recently adding servers capable of generating bitcoins (i.e. bitcoin mining). In the short term, we believe our transaction verification services business will be a growing source of revenue for us.

Transaction Verification Service Business (bitcoin mining)

We believe that we can establish and expand a low cost transaction verification services business (bitcoin mining) and believe this will provide revenue growth and synergies with our platform development efforts. During January 2015, we entered into a two year lease for an 83,000 square foot facility. Additionally we have the option to purchase the property for $775,000 less the $10,000 security deposit and all lease payments. With minimal improvements, the new facility is anticipated to handle over 10 megawatts (mw) of power and can potentially house up to 40,000 TH/s of mining servers.

Transaction verification entails running ASIC (application-specific integrated circuit) servers which solve a set of prescribed complex mathematical calculations in order to add a block to the Blockchain and thereby confirm bitcoin transactions. When we are successful in adding a block to the Blockchain, we are awarded a fixed number of bitcoins for our effort. Over time it is anticipated that the rewarded value of adding a block to the Blockchain will decrease, and we expect to charge transaction fees to verify transactions.

Given the size and low cost of our facility and electricity, we are also evaluating offering hosted mining services as well as traditional data center services.

In addition to driving growth, our transaction verification services business will generate bitcoins which can be used in our planned universal platform. For example, we are developing a bitcoin-based closed-loop loyalty program for our ecommerce marketplace. We plan to launch the program after completion of our credit card integration initiative. Lastly, to the extent we expand into additional money service businesses in the future, having a steady supply of bitcoins could provide a liquidity pool to support those efforts.

E-commerce Marketplace

We believe our e-commerce marketplace was the first such site to accept bitcoin. Our beta ecommerce marketplace now offers over 250,000 curated products and utilizes our “Intelligent Shopping Engine” to find competitive prices on products from over 250 retailers. In early 2014, we began a complete redesign of our ecommerce marketplace to incorporate our Intelligent Shopping Engine as a value added function to our ecommerce marketplace. During 2014, many new businesses (such as Dell, Microsoft, Overstock, NewEgg and TigerDirect) opted to accept bitcoin as a form of payment. While this poses competition for our marketplace efforts, we believe it strengthens the acceptance of bitcoin and should, in the long run, be beneficial to our planned universal platform.

The online ecommerce marketplace is hosted, maintained, and developed by us. We have developed software that allows us to interface with vendors and search for competitive prices in real time and display up-to-date inventory, and present prices in bitcoin, litecoin or dogecoin according to the exchange rate from USD. The exchange rate is updated frequently and at each stage of the checkout process, when customers reach the checkout page the exchange rate is locked in by our payment processor for 15 minutes and our payment processor assume the currency exchange risk (unless we choose to accept the digital currency). All marketplace customer orders are fulfilled by third party vendors and we are not involved in the logistics chain, however, we oversee the fulfillment process and strive for a smooth shopping experience. Our payment processor allows us to select a ratio of cash versus each respective digital currency we accept. We charge our customers a processing fee on transactions if we are not in the affiliate program with the end retailer selling a particular product. If we are a part of an affiliate program we are paid affiliate fees by the retailer.

Beta Secure Storage Solution (digital wallet)

Our secure bitcoin storage solution (digital wallet), which is currently in invitation only beta, offers a secure way for users to store their bitcoins. Our beta digital wallet is built on Gem’s technology and utilizes a multi-signature solution to secure every transaction with three keys. Every transaction requires valid signatures from at least two of the following three keys: 1. BTCS cosigning key, 2. Primary Key, and 3. Offline Backup Key. Our Company and/or Gem will only be in possession of the BTCS cosigning key and therefore will not be in control of or a custodian of user funds. Our beta digital wallet also utilized two-factor-authentication provided by Authy, a leading security solution firm, to limit unauthorized access. We are currently working to integrate our wallet and ecommerce marketplace to share one user login as well as seeking out a user interface developer to improve the overall continuity of our platform. Additionally we are working on developing a digital wallet Android application.

Digital Currency ATM Initiatives

We currently own two bitcoin ATMs, which we have not yet installed. We anticipate that they will offer an easy way to exchange currency for bitcoin. We are the lead investor in Coin Outlet, a bitcoin ATM manufacturer, which we anticipate will operate our ATMs.

Strategic Partnerships

We have partnered with and invested in four digital currency companies (collectively referred to herein as our “Partner Companies”) to further our efforts to build a universal digital currency platform. We have integrated with GoCoin and Gem. Coin Outlet manufactures and operates AML/KYC compliant bitcoin ATM's with two-way transaction functionality. Coin Outlet provides a means for the general public to buy and sell bitcoins with cash. Gem offers a secure software development toolkit for companies to develop multi-signature storage solutions to store bitcoin. Expresscoin’s service enables consumers a method to access and buy bitcoin and various other altcoins. Expresscoin provides a simple user experience with a central dashboard to keep track of all digital currency balances and activity. GoCoin is an international payment platform enabling online and retail merchants a way to accept bitcoin, litecoin and dogecoin as payment methods.

Blockchain Technologies and Other Growth Initiatives

We are also keenly focused on other blockchain technologies. Since the most prominent use case for blocktain technologies is digital currencies (or more specifically, bitcoin), it remains our core focus. Nonetheless, we anticipate continuing to evaluate other blockchain technology opportunities, as well as technologies that are complementary to our business strategy in an effort to minimize risks and enhance shareholder value. This will include evaluating opportunities that diversify our revenue streams, provide other consumer services and provide on-ramps for new users.

INDUSTRY AND MARKET OVERVIEW (BITCOIN AND BLOCKCHAIN TECHNOLOGIES)

Introduction to Bitcoins and the Bitcoin Network

A bitcoin is one type of a Digital Currency that is issued by, and transmitted through, an open source, math-based protocol platform using cryptographic security that is known as the “Bitcoin Network.” The Bitcoin Network is an online, peer-to-peer user network that hosts the public transaction ledger, known as the “Blockchain,” and the source code that comprises the basis for the cryptography and math-based protocols governing the Bitcoin Network. No single entity owns or operates the Bitcoin Network, the infrastructure of which is collectively maintained by a decentralized user base. Bitcoins can be used to pay for goods and services or can be converted to fiat currencies, such as the US Dollar, at rates determined on Bitcoin Exchanges or in individual end-user-to-end-user transactions under a barter system.

Bitcoins are “stored” or reflected on the digital transaction ledger known as the “Blockchain,” which is a digital file stored in a decentralized manner on the computers of each Bitcoin Network user. The Blockchain records the transaction history of all bitcoins in existence and, through the transparent reporting of transactions, allows the Bitcoin Network to verify the association of each bitcoin with the digital wallet that owns them. The Bitcoin Network and Bitcoin software programs can interpret the Blockchain to determine the exact bitcoin balance, if any, of any digital wallet listed in the Blockchain as having taken part in a transaction on the Bitcoin Network.

The Blockchain is comprised of a digital file, downloaded and stored, in whole or in part, on all bitcoin users’ software programs. The file includes all blocks that have been solved by miners and is updated to include new blocks as they are solved. As each newly solved block refers back to and “connects” with the immediately prior solved block, the addition of a new block adds to the Blockchain in a manner similar to a new link being added to a chain. Each new block records outstanding bitcoin transactions, and outstanding transactions are settled and validated through such recording, the Blockchain represents a complete, transparent and unbroken history of all transactions on the Bitcoin Network.

Each bitcoin transaction is broadcast to the Bitcoin Network and recorded in the Blockchain. “Off-Blockchain transactions” involve the transfer of control over or ownership of a specific digital wallet holding bitcoins or of the reallocation of ownership of certain bitcoins in a pooled-ownership digital wallet, such as a digital wallet owned by a Bitcoin Exchange. Information and data regarding Off-Blockchain transactions is generally not publicly available in contrast to true bitcoin transactions, which are publicly recorded on the Blockchain. Off-Blockchain transactions are not truly bitcoin transactions in that they do not involve the transfer of transaction data on the Bitcoin Network and do not reflect a movement of bitcoins between addresses recorded in the Blockchain. Off-Blockchain transactions are subject to risks as any such transfer of bitcoin ownership is not protected by the protocol behind the Bitcoin Network or recorded in and validated through the Blockchain mechanism.

The Bitcoin Network is decentralized and does not rely on either governmental authorities or financial institutions to create, transmit or determine the value of bitcoins. Rather, bitcoins are created and allocated by the Bitcoin Network protocol through a “mining” process subject to a strict, well-known issuance schedule. The value of bitcoins is determined by the supply of and demand for bitcoins in the Bitcoin Exchange Market (and in private end-user-to-end-user transactions), as well as the number of merchants that accept them. As bitcoin transactions can be broadcast to the Bitcoin Network by any user’s bitcoin software and bitcoins can be transferred without the involvement of intermediaries or third parties, there are little or no transaction costs in direct peer-to-peer transactions on the Bitcoin Network. Third party service providers such as Bitcoin Exchanges and bitcoin third party payment processing services may charge significant fees for processing transactions and for converting, or facilitating the conversion of, bitcoins to or from fiat currency.

The Bitcoin Network was initially contemplated in a white paper that also described bitcoin and the operating software to govern the Bitcoin Network. The white paper was purportedly authored by Satoshi Nakamoto; however, no individual with that name has been reliably identified as bitcoin’s creator, and the general consensus is that the name is a pseudonym for the actual inventor or inventors. The first bitcoins were created in 2009 after Nakamoto released the Bitcoin Network source code (the software and protocol that created and launched the Bitcoin Network). Since its introduction, the Bitcoin Network has been under active, unofficial development by a group of engineers headed by Gavin Andresen, Chief Scientist at the Bitcoin Foundation, and Wladimir J. van der Laan, who was appointed to the role of lead developer by the Bitcoin Foundation in April 2014. As an open source project, bitcoin is not represented by an official organization or authority, although groups including, most prominently, the Bitcoin Foundation work to organize the bitcoin community and to develop and protect the Bitcoin Network’s code.

Overview of the Bitcoin Network’s Operations

In order to own, transfer or use bitcoins, a person generally must have Internet access to connect to the Bitcoin Network. Bitcoin transactions between parties occur very rapidly (within several seconds) and may be made directly between end-users without the need for a third-party intermediary, although there are entities that provide third-party intermediary services. To prevent the possibility of double-spending a single bitcoin, a user must notify the Bitcoin Network of the transaction by broadcasting the transaction data to its network peers. The Bitcoin Network provides confirmation against double-spending by memorializing every transaction in the Blockchain, which is publicly accessible and transparent. This memorialization and verification against double-spending is accomplished through the bitcoin mining process, which adds “blocks” of data, including recent transaction information, to the Blockchain.

Brief Description of Bitcoin Transfers

Prior to engaging in bitcoin transactions, a user generally must first install on its computer or mobile device a bitcoin software program that will allow the user to generate a digital “wallet” (analogous to a bitcoin account). The Bitcoin Network software program and the digital wallet also enable the user to connect to the Bitcoin Network and engage in the transfer of bitcoins with other users. The computer of a user that downloads a Bitcoin Network software program will become a “node” on the Bitcoin Network that assists in validating and relaying transactions from other users. Alternatively, a user may retain a third party to create a digital wallet to be used for the same purpose. There is no limit on the number of digital wallets a user can have, and each such wallet includes one or more unique digital addresses and verification system consisting of a “public key” and a “private key,” which are mathematically related.

In a bitcoin transaction, the bitcoin recipient must provide its digital address, which serves as a routing number to the recipient’s digital wallet on the Blockchain, to the party initiating the transfer. This activity is analogous to a recipient providing a routing address in wire instructions to the payor so that cash may be wired to the recipient’s account. The recipient, however, does not make public or provide to the sender its related private key. The payor, or “spending” party, does reveal its public key in signing and verifying its spending transaction to the Blockchain.

Neither the recipient nor the sender reveal their digital wallet’s private key in a transaction, because the private key authorizes access to, and transfer of, the funds in that digital wallet to other users. Therefore, if a user loses his private key, the user permanently loses access to the bitcoins contained in the associated digital wallet. Likewise, bitcoins are irretrievably lost if the wallet containing them is deleted and no backup of the private key relating to that wallet has been made. In the data packets propagated from a user’s bitcoin software program onto the Bitcoin Network to allow transaction confirmation, the sending party must “sign” its transaction with a data code derived from entering the private key into a “hashing algorithm.” The hashing algorithm converts the private key into a digital signature, which signature serves as validation that the transaction has been authorized by the holder of the digital wallet’s private key. This signature process is typically automated by software that runs the digital wallet and has access to the public and private keys.

Summary of a Bitcoin Transaction

In a bitcoin transaction between two parties, the following circumstances must be in place: (i) the party seeking to send bitcoins must have a digital wallet and the Bitcoin Network must recognize that digital wallet as having sufficient bitcoins for the spending transaction; (ii) the receiving party must have a digital wallet; and (iii) the spending party must have internet access with which to send its spending transaction.

Next, the receiving party must provide the spending party with its wallet’s digital address, an identifying series of 27 to 34 alphanumeric characters that represents the wallet’s routing number on the Bitcoin Network and allow the Blockchain to record the sending of bitcoins to that wallet. The receiving party can provide this address to the spending party in alphanumeric format or an encoded format such as a Quick Response Code (commonly known as a QR Code), which may be scanned by a smartphone or other device to quickly transmit the information.

After the provision of the receiving wallet’s digital address, the spending party must enter the address into its bitcoin software program along with the number of bitcoins to be sent. The number of bitcoins to be sent will typically be agreed upon between the two parties based on a set number of bitcoins or an agreed upon conversion of the value of fiat currency to bitcoins. Most bitcoin software programs also allow, and often suggest, the payment of a transaction fee (also known as a miner’s fee). Transaction fees are not required to be included by many bitcoin software programs, but, when they are included, they are paid by the spending party on top of the specified amount of bitcoins being sent in the transaction. Transaction fees, if any, are typically a fractional number of bitcoins (e.g., 0.005 or 0.0005 bitcoins) and are automatically transferred by the Bitcoin Network to the bitcoin miner that solves and adds the block recording the spending transaction on the Blockchain.

After the entry of the wallet’s digital address, the number of bitcoins to be sent and the transaction fees, if any, to be paid, the spending party will transmit the spending transaction. The transmission of the spending transaction results in the creation of a data packet by the spending party’s bitcoin software program, which data packet includes data showing (i) the destination digital wallet’s address, (ii) the number of bitcoins being sent, (iii) the transaction fees, if any, and (iv) the spending party’s digital signature, verifying the authenticity of the transaction. The data packet also includes references called “inputs” and “outputs,” which are used by the Blockchain to identify the source of the bitcoins being spent and record the flow of bitcoins from one transaction to the next transaction in which the bitcoins are spent. The digital signature exposes the spending party’s digital wallet address and public key to the Bitcoin Network, though, for the receiving party, only its digital wallet address is revealed. The spending party’s bitcoin software will transmit the data packet onto the decentralized Bitcoin Network, resulting in the propagation of the information among the software programs of bitcoin users across the Bitcoin Network for eventual inclusion in the Blockchain. Typically, the data will spread to a vast majority of bitcoin miners within the course of less than a minute.

Bitcoin miners record transactions when they solve for and add blocks of information to the Blockchain. When a miner solves for a block, it creates that block, which includes data relating to (i) the solution to the block, (ii) a reference to the prior block in the Blockchain to which the new block is being added and (iii) all transactions that have occurred but have not yet been added to the Blockchain. The miner becomes aware of outstanding, unrecorded transactions through the data packet transmission and propagation discussed above. Typically, bitcoin transactions will be recorded in the next chronological block if the spending party has an internet connection and at least one minute has passed between the transaction’s data packet transmission and the solution of the next block. If a transaction is not recorded in the next chronological block, it is usually recorded in the next block thereafter.

Bitcoin transactions that are micropayments (typically, less than 0.01 BTC) and that do not include transaction fees to miners are currently deprioritized for recording, meaning that, depending on bitcoin miner policies, these transactions may take longer to record than typical transactions if the transactions do not include a transaction fee. Additionally, transactions initiated by spending wallets with poor connections to the Bitcoin Network (i.e., few or poor quality connections to nodes or “supernodes” that relay transaction data) may be delayed in the propagation of their transaction data and, therefore, transaction recording on the Blockchain. Finally, to the extent that a miner chooses to limit the transactions it includes in a solved block (whether by the payment of transaction fees or otherwise), a transaction not meeting that miner’s criteria will not be included.

To the extent that a transaction has not yet been recorded, there is a greater chance that the spending wallet can double-spend the bitcoins sent in the original transaction. If the next block solved is by an honest miner not involved in the attempt to double-spend bitcoin and if the transaction data for both the original and double-spend transactions have been propagated onto the Bitcoin Network, the transaction that is received with the earlier time stamp will be recorded by the solving miner, regardless of whether the double-spending transaction includes a larger transaction fee. If the double-spend transaction propagates to the solving miner and the original transaction has not, then the double-spending has a greater chance of success. As a result of the high difficulty in successfully initiating a double-spend without the assistance of a coordinated attack, the probability of success for a double-spend transaction attempt is limited.

Upon the addition of a block included in the Blockchain, the bitcoin software program of both the spending party and the receiving party will show confirmation of the transaction on the Blockchain and reflect an adjustment to the bitcoin balance in each party’s digital wallet, completing the bitcoin transaction. Typically, bitcoin software programs will automatically check for and display additional confirmations of six or more blocks in the Blockchain.

Cryptographic Security Used in the Bitcoin Network

Public and Private Keys

The Bitcoin Network uses sophisticated cryptography and a decentralized network to sustain the integrity of bitcoins as an asset and the security of transactions occurring on the Network. The public key cryptography upon which Bitcoin is based requires that every transaction be digitally signed by the software programs used by the spending party in each transaction. This requirement provides assurance that the transaction was, in fact, authorized by the holder of the sending digital wallet’s private key and ensures that bitcoin transactions are secure. The signature appended to a transaction is a number that proves that a signing operation (or validation) took place. It is mathematically generated from a “hash” (the result of a hash algorithm reducing an arbitrarily large amount of data into a fixed length) of the private key for the signing party. By examining the hash, users on the Bitcoin Network can confirm that the user signed the transaction with the appropriate private key, but cannot reverse engineer the private key from the signature.

A public key can be derived from the private key by running a cryptographic algorithm and a digital address can be derived from such public key by running certain other algorithms; however, a public key cannot be reverse engineered from a digital wallet address and, using present technology, a private key is nearly impossible to reverse engineer from a public key. As a result, exposure of a digital wallet’s digital address on the Blockchain (e.g., through a deposit of bitcoins into such wallet) presents a highly remote security risk, if any, to the cryptographic protection of a digital wallet. The exposure of a digital wallet’s public key on the Blockchain (e.g., through a spending transaction from such wallet) marginally increases the security risk to that wallet because a private key may, in theory, be reverse engineered from a public key through the expenditure of large amounts of time and computer power. At present, the time and computational power required to reverse engineer or “key guess” a private key from an exposed public key (also known as a “brute force” attack) is considered to be either implausible or prohibitively expensive on a cost-reward, rational basis due to the elliptic curve cryptography used to create the public-private key pair.

Bitcoin private keys are generated using an Elliptic Curve Digital Signature Algorithm featuring 256-bit private key length. The Elliptic Curve Digital Signature Algorithm is a variant of the US federal government standard encryption signature algorithm using an elliptic curve cryptography. Elliptic curve cryptography expands on early cryptography structures to improve the level of security provided, as compared with prior methods of encryptions such as RSA. The elliptical curve cryptography (including Elliptic Curve Digital Signature Algorithms using 256-bit and 384-bit keys) has been approved for use by the US National Security Trust Agency in its Suite B Cryptography for encryption of state secrets using digital signatures.

Double-Spending and the Bitcoin Network Confirmation System

To ensure the integrity of bitcoin transactions from the recipient’s side (i.e., to prevent double-spending by a spending party), every bitcoin transaction is broadcast to the Bitcoin Network and recorded in the Blockchain through the “mining” process, which time-stamps the transaction and memorializes the change in the ownership of the bitcoin(s) transferred. Adding a block to the Blockchain requires bitcoin miners to exert significant computational effort. Requiring this “proof of work” prevents a malicious actor from either adding fraudulent blocks to generate bitcoins (i.e., counterfeit bitcoins) or overwriting existing valid blocks to reverse its prior transactions.

A transaction in bitcoins between two parties is recorded in the Blockchain in a block only if that block is accepted as valid by a majority of the nodes on the Bitcoin Network. Validation of a block is achieved by confirming the cryptographic hash value included in the block’s solution and by the block’s addition to the longest confirmed Blockchain on the Bitcoin Network. For a transaction, inclusion in a block on the Blockchain constitutes a “confirmation” of the bitcoin transaction. As each block contains a reference to the immediately preceding block, additional blocks appended to and incorporated into the Blockchain constitute additional confirmations of the transactions in such prior blocks, and a transaction included in a block for the first time is confirmed once against double-spending. The layered confirmation process makes changing historical blocks (and reversing transactions) exponentially more difficult the further back one goes in the Blockchain. Bitcoin Exchanges and users can set their own threshold as to how many confirmations are required until funds from the transferor are considered valid.

To undo past transactions in a block recorded on the Blockchain, a malicious actor would have to exert tremendous processing power in re-solving each block in the Blockchain starting with and after the target block and broadcasting all such blocks to the Bitcoin Network. The Bitcoin Network is generally programmed to consider the longest Blockchain containing solved blocks to be the most accurate Blockchain. In order to undo multiple layers of confirmation and alter the Blockchain, a malicious actor must resolve all of the old blocks sought to be regenerated and be able to continuously add new blocks to the Blockchain at a speed that would have to outpace that of all of the other miners on the Bitcoin Network, who would be continuously solving for and adding new blocks to the Blockchain. Given the size and speed of the Bitcoin Network and its decentralization (i.e., worldwide distribution across thousands of users’ computers), it is generally agreed that the cost of amassing such computational power exceeds the profit to be obtained by double-spending or attempting to fabricate prior blocks. As of February 13, 2014, the Bitcoin Network’s estimated hashrate was approximately 318,000,000 gigahashes per second, according to Blockchain.info. As of February 13, 2014, BitcoinCharts.com estimated the computational speed of the combined mining power of the network at approximately 4,047,236 petaFLOPS (petaFLOPS are a standard measure of computer performance); to provide context, the world’s fastest supercomputer reaches a maximum of 33.86 petaFLOPS (or less than a hundredth of a percent of the Bitcoin Network’s collective processing power) and the top 500 supercomputers in the world had a combined processing power of approximately 309 petaFLOPS as of November 2014, according to Top500.org.

If a malicious actor is able to amass 10 percent of the Bitcoin Network’s total hashrate, there is estimated to be a 0.1 percent chance that it would be able to overcome six confirmations. Therefore, given the difficulty in amassing such processing power, six confirmations is an often-cited standard for the validity of transferred funds. We typically recognize a transfer as confirmed upon this industry standard of six confirmations (“Confirmation Protocol”). As one block is added to the Blockchain approximately every six to twelve minutes, a bitcoin transaction will be, on average, confirmed beyond a reasonable doubt in approximately one hour. Merchants selling high-value goods and services, as well as Bitcoin Exchanges and many experienced users, are believed to generally use the six confirmations standard. This confirmation system, however, does not mean that merchants must always wait for multiple confirmations for transactions involving low-value goods and services. As discussed below, the value of a successful double-spending attack involving a low-value transaction may, and perhaps likely will, be significantly less than the cost involved in arranging and executing such double-spending attacks. Furthermore, merchants engaging in low-value transactions may then view the reward of quicker transaction settlements with limited or no Blockchain confirmation as greater than the related risk of not waiting for six confirmations with respect to low-value transactions at points of sale. Conversely, for high-value transactions that are not time sensitive, additional settlement security can be provided by waiting for more than six confirmations.

Transaction Verification (Bitcoin Mining) & Creation of New Bitcoins

Transaction Verification Process (Mining Process)

The process by which bitcoins are “mined” results in new blocks being added to the Blockchain and new bitcoins being issued to the miners. Miners engage in a set of prescribed complex mathematical calculations in order to add a block to the Blockchain and thereby confirm bitcoin transactions included in that block’s data. Miners that are successful in adding a block to the Blockchain are automatically awarded a fixed number of bitcoins for their effort; we also refer to this process of receiving the aforementioned award as transaction verification services. This reward system is the method by which new bitcoins enter into circulation to the public and is accomplished in the added block through the notation of the new bitcoin creation and their allocation to the successful miner’s digital wallet. To begin mining, a user can download and run Bitcoin Network mining software, which, like regular Bitcoin Network software programs, turns the user’s computer into a “node” on the Bitcoin Network that validates blocks.

All bitcoin transactions are recorded in blocks added to the Blockchain. Each block contains the details of some or all of the most recent transactions that are not memorialized in prior blocks, a reference to the most recent prior block, and a record of the award of bitcoins to the miner who added the new block. In order to add blocks to the Blockchain, a miner must map an input data set (i.e., a reference to the immediately preceding block in the Blockchain, plus a block of the most recent Bitcoin Network transactions and an arbitrary number called a “nonce”) to a desired output data set of predetermined length (“hash value”) using the SHA-256 cryptographic hash algorithm. To “solve” or “calculate” a block, a miner must repeat this computation with a different nonce until the miner generates a SHA-256 hash of a block’s header that has a value less than or equal to the current target set by the Bitcoin Network. Each unique block can only be solved and added to the Blockchain by one miner; therefore, all individual miners and mining pools on the Bitcoin Network are engaged in a competitive process and are incentivized to increase their computing power to improve their likelihood of solving for new blocks.

The cryptographic hash function that a miner uses is one-way only and is, in effect, irreversible: hash values are easy to generate from input data (i.e., valid recent network transactions, Blockchain and nonce), but neither a miner nor participant is able to determine the original input data solely from the hash value. As a result, generating a new valid block with a header less than the target prescribed by the Bitcoin Network is initially difficult for a miner, yet other nodes can easily confirm a proposed block by running the hash function just once with the proposed nonce and other input data. A miner’s proposed block is added to the Blockchain once a majority of the nodes on the Bitcoin Network confirms the miner’s work, and the miner that solved such block receives the reward of a fixed number of bitcoins (plus any transaction fees paid by transferors whose transactions are recorded in the block). Therefore, “hashing” is akin to a mathematical lottery, and miners that have devices with greater processing power (i.e., the ability to make more hash calculations per second) are more likely to be successful miners because they can generate more hashes or “entries” into that lottery.

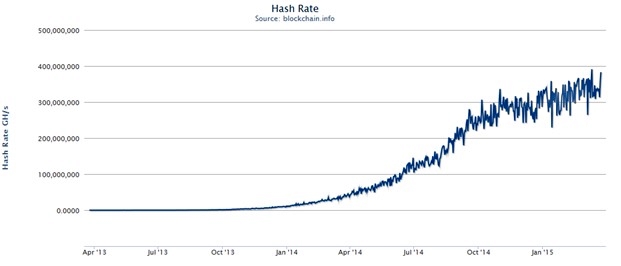

As more miners join the Bitcoin Network and its processing power increases, the Bitcoin Network automatically adjusts the complexity of the block-solving equation in an effort to set distribution such that newly-created blocks will be added to the Blockchain, on average, approximately every ten minutes. Processing power is added to the Bitcoin Network at irregular rates that have grown on a parabolic scale since early 2013, though the rate of additional mining power slowed steadily through 2014, until the computational speed of the network temporarily and marginally declined during December 2014. The following chart, sourced from Blockchain.info, shows the growth of the Bitcoin Network’s total hashrate from April 2013 to February 2015.

The rapid growth of the computational power of Bitcoin Network means that blocks are typically solved faster than the bitcoin protocol’s target of, on average, approximately every 10 minutes. Although the difficulty of the mining process is adjusted on a periodic basis after 2,016 blocks have been added to the Blockchain since the last adjustment, the average solution time for block solution has averaged approximately 7.6 minutes for the 180 days prior to and including December 26, 2014, with a standard deviation of 0.84 minutes.

Incentives for Transaction Verification (Mining)

Miners dedicate substantial resources to mining. Given the increasing difficulty of the target established by the Bitcoin Network, current miners must invest in expensive mining devices with adequate processing power to hash at a competitive rate. The first mining devices were standard home computers; however, mining computers are currently designed solely for mining purposes. Such devices include ASIC machines built by specialized companies like BitFury, KnCMiner, Cointerra, Spondoolies and Butterfly Labs. Miners also incur substantial electricity costs in order to continuously power and cool their devices while solving for a new block. In June 2013, Blockchain.info estimated that the aggregate electricity costs of mining across the Bitcoin Network exceeded $300,000 every 24 hours. Although variables such as the rate and cost of electricity are estimated, as of September 1, 2013, Blockchain.info had revised upward the average 24-hour electricity cost of all mining on the Bitcoin Network to more than $1.5 million. Over the past year and two years, the collective processing power on the Bitcoin Network has increased by more than 30-fold and 13,000 fold, due in part to the development of more energy efficient ASIC mining chips and, during the second half of 2013, the substantial increase in the price of bitcoins. In late 2013, Blockchain.info ceased publishing estimated electric consumption on the Bitcoin Network, in part due to uncertainty in estimating electrical usage as newer, more energy efficient mining hardware became prevalent.

The Bitcoin Network is designed in such a way that the reward for adding new blocks to the Blockchain decreases over time and the production (and reward) of bitcoins will eventually cease. Once such reward ceases, it is expected that miners will demand compensation in the form of transaction fees to ensure that there is adequate incentive for them to continue mining. The amount of transaction fees will be based upon the structural requirements necessary to provide sufficient revenue to incentivize miners, as counterbalanced by the need to retain sufficient bitcoin users (and transactions) to make mining profitable.

Though not free from doubt, bitcoin industry participants have expressed a belief that transaction fees would be enforced through (i) mining operators collectively refusing to record transactions that do not include a payment of a transaction fee or (ii) the updating of bitcoin software to require a minimum transaction fee payment. Under a regime whereby large miners require fees to record transactions, a transaction where the spending party did not include a payment of transaction fees would not be recorded on the Blockchain until a miner who does not require transaction fees solves for a new block (thereby recording all outstanding transaction records for which it has received data). If popular bitcoin software for digital wallets were to require a minimum transaction fee, users of such programs would be required to include such fees; however, because of the open-source nature of the Bitcoin Network, there may be no way to require that all digital wallets include minimum transaction fees for spending transactions. Alternatively, a future Bitcoin Network software update could simply build a small transaction fee payment into all spending transactions (e.g., by deducting a fractional number of bitcoins from all transactions on the Bitcoin Network as transaction fees).

The Bitcoin Network protocol already includes transaction fee rules and the mechanics for awarding transaction fees to the miners that solve for blocks in which the fees are recorded; however, users currently may opt not to pay transaction fees (depending on the bitcoin software they use) and miners may choose not to enforce the transaction fee rules since, at present, the bitcoin rewards are far more substantial than transaction fees. In December 2014, transaction fees accounted for an average of 0.37 percent miners’ total revenue, though the percentage of revenue represented by transaction fees is not static and fluctuates based on the number of transactions for which sending users include transaction fees, the levels of those transaction fees and the number of transactions a miner includes in its solved blocks. Typically, transactions do not have difficulty being recorded if transaction fees are not included.

Mining Pools

The Bitcoin Network’s mining protocol was created in a manner to make it more difficult to solve for new blocks as the processing power dedicated to mining increases (in order to maintain the 10 minute per block solution time average). Therefore, the difficulty of finding a valid hash value has grown exponentially since the first blocks were mined. Currently, the likelihood that an individual acting alone will be able to mine bitcoins is extremely low. As a result, mining “pools” have developed in which multiple miners act cohesively and combine their processing power to solve blocks. When a pool solves a new block, the participating mining pool members split the resulting reward based on the processing power they each contributed to solve for such block. Mining pools provide participants with access to smaller, but steadier and more frequent, bitcoin payouts. According to Blockchain.info, as of December 29, 2014, the largest three mining pools were Discus Fish, AntPool and GHash.io, which, when aggregated, represented approximately 44 percent of the processing power on the Bitcoin Network (as calculated by determining the percentage of blocks mined by each such pool over the prior four days). Also according to Blockchain.info, on such date, the nine largest pools (Discus Fish, AntPool, GHash.io, BTCChina Pool, KnCMiner, BTC Guild, Elgius and Slush) accounted for approximately 70 percent of the mining processing power on the Bitcoin Network. In late May and early June, reports indicated that GHash.io approached and, during a 24- to 48-hour period in early June, may have exceeded one-half of the processing power on the Bitcoin network, as measured by the self-reported processing power of the pool and by measuring the percentage of blocks mined by the pool. It has not been confirmed whether GHash.io exceeded one-half of the processing power on the Bitcoin Network for any period of time, and its percentage of the processing power on the Bitcoin Network has since fallen to approximately ten percent. As of December 26, 2014, Discus Fish was determined to be the largest mining pool, having solved for 22 percent of the block discovered during the prior four days.

Mathematically Controlled Supply

The method for creating new bitcoins is mathematically controlled in a manner so that the supply of bitcoins grows at a limited rate pursuant to a pre-set schedule. The number of bitcoins awarded for solving a new block is automatically halved every 210,000 blocks. Thus, the current fixed reward for solving a new block is 25 bitcoins per block and the reward will decrease by half to become 12.5 bitcoins in or around the start of August 2016 (based on estimates of the rate of block solution calculated by BitcoinClock.com). This deliberately controlled rate of bitcoin creation means that the number of bitcoins in existence will never exceed 21 million and that bitcoins cannot be devalued through excessive production unless the Bitcoin Network’s source code (and the underlying protocol for bitcoin issuance) is altered. As of March 24, 2015, 13,970,000 bitcoins have been mined. It is estimated that more than ninety percent (90 percent) of the 21 million bitcoins will have been produced by 2022.

Modifications to the Bitcoin Protocol

Bitcoin is an open source project (i.e., a product whose source code is freely available to the public and that utilizes crowdsourcing to identify possible issues, problems and defects) and there is no official developer or group of developers that controls the Bitcoin Network. The Bitcoin Network’s development is overseen by a core group of developers, which currently includes Wladimir J. van der Laan, Gavin Andresen, Jeff Garzik, Gregory Maxwell and Pieter Wuille (“Core Developers”). The Core Developers are able to access and can propose alterations to the Bitcoin Network source code hosted on GitHub, an online service and forum used to share and develop open source code. Other programmers have access to and can propose changes to the bitcoin source code on GitHub, but the Core Developers have an elevated level of influence over the process. As a result, the Core Developers are responsible for quasi-official releases of updates and other changes to the Bitcoin Network’s source code. Users and miners must accept any changes made to the Bitcoin Network (including those proposed by the Core Developers) by downloading the proposed modification of the source code.

A modification of the source code is only effective with respect to the bitcoin users and miners that download it. Consequently, as a practical matter, a modification to the source code (e.g., a proposal to increase the 21 million total limit on bitcoins or to reduce the average confirmation time target from 10 minutes per block) only becomes part of the Bitcoin Network if accepted by participants collectively having a substantial majority of the processing power on the Bitcoin Network. If a modification is accepted only by a percentage of users and miners, a division in the Bitcoin Network will occur such that one network will run the pre-modification source code and the other network will run the modified source code; such a division is known as a “fork” in the Bitcoin Network. It should be noted that, although their power to amend the source code is effectively subject to the approval of users and miners, the Core Developers have substantial influence over the development of the Bitcoin Network and the direction of the bitcoin community.

Other Blockchain Technologies

Core Development of the bitcoin source code has increasingly focused on modifications of the bitcoin protocol to allow non-financial and next generation uses (sometimes referred to as Bitcoin 2.0 projects). These uses include smart contracts and distributed registers built into, built atop or pegged alongside the Blockchain. For example, the white paper for Blockstream, a program of which Core Developers Jeff Garzik and Gregory Maxwell are a part, calls for the use of “pegged sidechains” to develop programming environments that are built within block chain ledgers that can interact with and rely on the security of the Bitcoin Network and Blockchain, while remaining independent thereof. We are actively evaluating other Blockhain technologies relate to Bitcoin 2.0 projects. At this time, Bitcoin 2.0 projects remain in early stages and have not been materially integrated into the Blockchain or Bitcoin Network.

Bitcoin Value

Bitcoins are an example of a Digital Currency that is not a fiat currency (i.e., a currency that is backed by a central bank or a national, supra-national or quasi-national organization) and are not backed by hard assets or other credit. As a result, the value of bitcoins is determined by the value that various market participants place on bitcoins through their transactions.

Exchange Valuation

Due to the peer-to-peer framework of the Bitcoin Network and the protocols thereunder, transferors and recipients of bitcoins are able to determine the value of the bitcoins transferred by mutual agreement or barter with respect to their transactions. As a result, the most common means of determining the value of a bitcoin is by surveying one or more Bitcoin Exchanges where bitcoins are publicly bought, sold and traded (i.e., the Bitcoin Exchange Market).

On each Bitcoin Exchange, bitcoins are traded with publicly disclosed valuations for each transaction, measured by one or more fiat currencies such as the US Dollar, the Euro or the Chinese Yuan. Bitcoin Exchanges typically report publicly on their site the valuation of each transaction and bid and ask prices for the purchase or sale of bitcoins. Although each Bitcoin Exchange has its own market price, it is expected that most Bitcoin Exchanges’ market prices should be relatively consistent with the Bitcoin Exchange Market average since market participants can choose the Bitcoin Exchange on which to buy or sell bitcoins ( i.e. , exchange shopping). Arbitrage between the prices on various Bitcoin Exchanges is possible, but the imposition of fees and fiat currency deposit/withdrawal policies appears to have, at times, prevented an active arbitrage mechanism among users on some Bitcoin Exchanges. For example, delayed fiat currency withdrawals imposed by Mt. Gox resulted in Mt. Gox trading at a premium of up to 10 to 20 percent for several months through January 2014. In February 2014, Mt. Gox suspended trading, closed its website and exchange service, and filed for a form of bankruptcy protection from creditors called minji saisei, or civil rehabilitation, to allow courts to seek a buyer. In April 2014, Mt. Gox began liquidation proceedings.

Even in the absence of large trading fees and fiat currency deposit/withdrawal policies, price differentials across Bitcoin Exchanges remain; for example, bitcoins on BTC-e traded at a discount of approximately 0.9 percent relative to the average daily weighted price for bitcoins on BitStamp and Bitfinex during the week ended December 26, 2014. During the prior month, prices on BTC-e typically traded at a discount of between zero and five percent.

Forms of Attack Against the Bitcoin Network

Exploitation of Flaws in the Bitcoin Network’s Source Code

As with any other computer code, the Bitcoin Network source code may contain certain flaws. Several errors and defects have been found and corrected, including those that disabled some functionality for users, exposed users’ information, or allowed users to create multiple views of the Bitcoin Network. Such flaws have been discovered and quickly corrected by the Core Developers or the bitcoin community, thus demonstrating one of the advantages of open source codes that are available to the public: open source codes rely on transparency to promote community-sourced identification and solution of problems within the code.

Reports of flaws in or exploitations of the source code that allow malicious actors to take or create money in contravention of known Bitcoin Network rules have been exceedingly rare. For example, in 2010, a hacker or group of hackers exploited a flaw in the Bitcoin Network source code that allowed them to generate 184 billion bitcoins in a transaction and send them to two digital wallet addresses. However, the bitcoin community and developers identified and reversed the manipulated transactions within approximately five hours, and the flaw was corrected with an updated version of the bitcoin protocol. Another addressed issue with the Bitcoin Network source code, “transaction malleability” was addressed by the Core Developers in a March 2013 software update. The Core Developers, in conjunction with other developers and miners, work continuously to ensure that flaws are quickly fixed or removed.

Greater than Fifty Percent of Network Computational Power

Malicious actors can structure an attack whereby such actor gains control of more than half of the Bitcoin Network’s processing power or “hashrate.” Computer scientists and cryptographers believe that the immense collective processing power of the Bitcoin Network makes it impracticable for an actor to gain control of computers representing a majority of the processing power on the Bitcoin Network. During May and June 2014, mining pool GHash.io’s hashing power approached 50 percent of the processing power on the Bitcoin Network. During a brief period in early June, the mining pool may have controlled in excess of one-half of the Bitcoin Network’s processing power. Although no malicious activity or abnormal transaction recording was observed, the incident establishes that it is possible that a substantial mining pool may accumulate close to or more than a majority of the processing power on the Bitcoin Network. As of December 26, 2014, GHash.io controlled approximately one-tenth of the processing power on the Bitcoin Network, and no single pool controlled more than a quarter of the total processing power.

If a malicious actor acquired sufficient computational power necessary to control the Bitcoin Network (which amount would be well in excess of fifty percent), it would be able to engage in double-spending, or prevent some or all transactions from being confirmed, and prevent some or all other miners from mining any valid new blocks. The malicious actor or group of actors, however, would not be able to reverse other people’s transactions, change the fixed number of bitcoins generated per new block, or transfer previously existing bitcoins that belong to other users.

Cancer Nodes

This form of attack involves a malicious actor propagating “cancer nodes” to isolate certain users from the legitimate Bitcoin Network. A target user functionally surrounded by cancer nodes would be put on a separate “network,” allowing the malicious actor to relay only blocks created by the separate network and thus opening the target user to double-spending attacks. By using cancer nodes, a malicious actor also can disconnect the target user from the bitcoin economy entirely by refusing to relay any blocks or transactions. Bitcoin software programs make these attacks more difficult by limiting the number of outbound connections through which users are connected to the Bitcoin Network.

Manipulating Blockchain Formation

A malicious actor may attempt to double-spend bitcoins by manipulating the formation of the Blockchain rather than through control of the Bitcoin Network. In this type of attack, a miner creates a valid new block containing a double-spend transaction and schedules the release of such attack block so that it is added to the Blockchain before a target user’s legitimate transaction can be included in a block. Variations of this form of attack include the “Finney attack,” “race attack,” and “vector76 attack.” All double-spend attacks require that the miner sequence and execute the steps of its attack with sufficient speed and accuracy. Users and merchants can dramatically reduce the risk of a double-spend attack by waiting for multiple confirmations from the Bitcoin Network before settling a transaction. The Bitcoin Network still may be used to execute instantaneous, low-value transactions without confirmation to the extent the recipient of bitcoins determines that a malicious miner would be unwilling to carry out a double-spend attack for low-value transactions because the reward from mining would be higher than the small profit gained from double-spending. Users and merchants can take additional precautions by adjusting their Bitcoin Network software programs to connect only to other well-connected nodes and to disable incoming connections. These precautions reduce the risk of double-spend attacks involving manipulation of a target’s connectivity to the Bitcoin Network (as is the case with vector76 and race attacks).

Market Participants

Miners

Miners range from bitcoin enthusiasts to professional mining operations that design and build dedicated machines and data centers, but the vast majority of mining is now undertaken by mining pools.

Investment and Speculative Sector

This sector includes the investment and trading activities of both private and professional investors and speculators. These participants range from hedge funds such as Malta-based Exante Ltd. to day-traders who invest in bitcoins by trading on Bitcoin Exchanges such as Slovenia-based BitStamp, US-based Coinbase, and Hong Kong-based Bitfinex.

Historically, larger financial services institutions are publicly reported to have limited involvement in investment and trading in bitcoin. In December 2013, Wedbush Securities and Bank of America Merrill Lynch released preliminary research reports on bitcoin as both a payment tool and investment vehicle. Additionally in December, the Federal Reserve Bank of Chicago released a primer on bitcoin prepared by a senior economist. In early 2014, Fitch Ratings, Goldman Sachs, JPMorgan Chase, PriceWaterhouseCoopers, UBS Securities and Wedbush Securities, among others, released additional research reports analyzing bitcoin on the basis of bitcoin value, technological innovation or payment system mechanics. In December 2014, the Federal Reserve Board’s Divisions of Research & Statistics and Monetary Affairs released an analysis of the Bitcoin Network’s transaction system and the Bitcoin Exchange Market’s economics. Additionally, institutions including Fortress Investment Group, Pantera Capital and our Company made, or proposed to make, direct or indirect investments in bitcoins, the bitcoin ecosystem and Blockchain technologies.

Retail Sector

The retail sector includes users transacting in direct peer-to-peer bitcoin transactions through the direct sending of bitcoins over the Bitcoin Network. The retail sector also includes transactions between consumers paying for goods or services from commercial or service businesses through direct transactions or third-party service providers such as BitPay, Coinbase and GoCoin. Each of BitPay, Coinbase and GoCoin provide a merchant platform for instantaneous transactions whereby the consumer sends bitcoins to BitPay, Coinbase or GoCoin, which then provides either the bitcoins or the cash value thereof to the commercial or service business utilizing the platform. PayPal, Square and Shopify are examples of traditional merchant payment processors or merchant platforms that have also added bitcoin payment options for their merchant customers. Payment processing through bitcoin typically reduces the transaction cost for merchants, relative to the costs paid for credit card transaction processing.

Service Sector

This sector includes companies that provide a variety of services including the buying, selling, payment processing and storing of bitcoins. Bitfinex, BitStamp and BTC-e are three of the largest Bitcoin Exchanges in the world. BTCChina, Huobi and OKCoin are large Bitcoin Exchanges based in China that primarily featuring trading of bitcoins for Chinese Yuan. Coinbase, Circle and Express Coin are each multi-service financial institutions that provide virtual wallets that store bitcoins for users and also serve as a retail gateway whereby users can purchase bitcoins for fiat currency. Coinbase, BitPay, BitPagos and GoCoin are examples of bitcoin payment processors that allow merchants to accept bitcoins as payment. As the Bitcoin Network continues to grow in acceptance, it is anticipated that service providers will expand the currently available range of services and that additional parties will enter the service sector for the Bitcoin Network. For example, bitcoin custodian Xapo was the first bitcoin company to propose and provide a bitcoin debit card service that could permit more simple point-of-sale merchant transactions denominated in bitcoins. Meanwhile, Bitgo Inc., a bitcoin custodian and virtual wallet, has pioneered the use of “multi-signature” storage as an enhanced security feature to retail and enterprise clients. Further, Gem has built and is pioneering a software development toolkit to allow for companies to quickly build “multi-signature” storage solutions; we are the only strategic investor in Gem and recently launched an invite only beta version of it secure storage solution (digital wallet) on Gem’s platform.

Historical Chart of the Price of Bitcoins, 2012-2014

The price of bitcoins is volatile and fluctuations are expected. Movements may be influenced by various factors, including, but not limited to, government regulation, security breaches experienced by service providers, as well as political and economic uncertainties around the world. The below chart reflects the value of a bitcoin as reported by Blockchain.info for the one-year period ending March 24, 2015.

Uses of Bitcoins

Global Bitcoin Market

Global trade in bitcoins consists of individual end-user-to-end-user transactions, together with facilitated exchange-based bitcoin trading. A limited market currently exists for bitcoin-based derivatives. There is currently no reliable data on the total number or demographic composition of users or miners on the Bitcoin Network.

Global Bitcoin Derivatives Markets

Nascent derivatives markets for bitcoins now exist. For example, certain types of options, futures contracts for differences and other derivative instruments are available in certain jurisdictions; however, many of these are not available in the United States and generally are not regulated to the degree that US investors expect derivative instruments to be regulated. The CFTC has approved TeraExchange, LLC as a cash-settled Swap Execution Facility, on which swap contracts may be entered into. On October 9, 2014, TeraExchange announced that it had hosted the first executed bitcoin swap traded on a CFTC-regulated platform. Other parties have acknowledged submitting applications for registration to the CFTC, though no other bitcoin-focused derivatives platform has been approved for registration by the CFTC. Various platforms and Bitcoin Exchanges also offer trading on margin. Currently, the open interest in these bitcoin derivative instruments is quite limited in comparison to the volume of actual bitcoin trades. Additionally, regulation relating to bitcoin derivatives is uncertain and may be subject to further scrutiny, although CFTC commissioners have expressed publicly that derivatives based on Digital Currenciessuch as bitcoins are subject to regulation by the CFTC, including oversight to prevent market manipulation of the price of bitcoins.

End-User-to-End-User

The bitcoin end-user-to-end-user ecosystem operates on a continuous, 24-hour per day basis. This is accomplished through decentralized peer-to-peer transactions between parties on a principal-to-principal basis. All risks and issues of credit are between the parties directly involved in the transaction. Liquidity can change from time to time during the course of a 24-hour trading day. The Bitcoin Network rules that require transaction fees are generally not enforced; therefore transaction costs, if any, are negotiable between the parties and may vary widely, although, where transaction fees are included, they are paid by the sending party in a bitcoin transaction. These transactions occur remotely through the Internet, in-person through forums such as Satoshi Square (an open-air bitcoin trading market held in New York City) or the Bitcoin Center NYC, and physically through bulletin boards. There are currently no official designated market makers for bitcoins and hence no standard transaction sizes, bid-offer spreads or typical known cost per transaction. Marketplaces like LocalBitcoins and ICBIT are intended to bring together counterparties trading in bitcoins but do not provide any clearing or intermediary function.

Bitcoin Exchange Market

Online Bitcoin Exchanges represent the majority of bitcoin buying and selling activity and provide the most data with respect to prevailing valuations of bitcoins. Most Bitcoin Exchanges operate through pooled account systems, whereby the users of the exchange send bitcoins and/or fiat currency to an account of the Bitcoin Exchange, which records user sub-account balances in a ledger entry system. For such pooled account exchanges, trades typically are conducted “off-Blockchain,” meaning that they are settled by reallocating bitcoin and money to and from users on the balanced ledgers of the exchange. Therefore, a trade on a pooled account exchange will not result in a bitcoin transaction being transmitted and subsequently recorded on the Blockchain, or of a money transfer going from one bank account to another. For a pooled-account Bitcoin Exchange, bitcoin transactions and money transfers typically only occur during the withdrawal or deposit of bitcoins or fiat currency by an exchange customer, or if the Bitcoin Exchange needs to shift bitcoins or fiat currency between its pooled accounts for internal purposes. Nevertheless, Bitcoin Exchanges typically publish trade data including last price, bid and ask spread, and trade volume, among other data, on their respective websites and through application programming interfaces.

For most of 2013, Mt. Gox (a Japanese exchange operated at www.mtgox.com by Tibanne Co. Ltd.) was the largest online Bitcoin Exchange in the world. Supporting trading of bitcoins using 16 different fiat currencies, Mt. Gox accounted for nearly three-quarters of all Bitcoin Exchange Market trading during the first half of 2013. For the month of August 2013, Mt. Gox’ market share dropped to just over 50 percent of Bitcoin Exchange Market trading, according to Bitcoinity.org. BitStamp represented approximately one quarter of trading over such period. Together with BTC-e and BTC China, the then-third and fourth largest exchanges by volume, the four largest Bitcoin Exchanges accounted for more than 90 percent of the Bitcoin Exchange Market volume in August 2013.

From September through the beginning of December of 2013, BTC China surpassed US Dollar-denominated Bitcoin Exchanges. This was bolstered by large speculative demand in China which led to the emergence of several large Bitcoin Exchanges and volume on BTC China that was bolstered by a commission-free trading program. Following a December regulatory notice from the People’s Bank of China and five government ministries that limited the ability of Chinese regulated financial and payment institutions to do business with Bitcoin Exchanges, volume on BTC China and similar exchanges such as Huobi and OKCoin dropped below those of Mt. Gox, BitStamp and BTC-e. By the end of 2014, volume on the major Bitcoin Exchanges that do not charge trading commission fees again outpaced the volume on the major US Dollar-denominated exchanges such as BTC-e, Bitfinex and BitStamp.

On February 7, 2014, Mt. Gox suspended the withdrawal of bitcoin, though trading activity continued. Mt. Gox attributed the suspension to problems accounting for “transaction malleability,” which refers to the ability of bitcoin nodes to adjust the “transaction ID” of a bitcoin transaction prior to its inclusion in the Blockchain. A user of an exchange that tracked payments through transaction IDs could then attempt to fool the exchange into believing it had failed to send a withdrawal and sending a second withdrawal in the same amount. Mt. Gox also continued to delay US Dollar withdrawals for a matter of weeks or months from the withdrawal request date. As a result, the price of bitcoins on Mt. Gox fell by more than 60 percent from February 7 to February 18, 2014. BitStamp and BTC-e also temporarily suspended bitcoin withdrawals to review whether their bitcoin withdrawal system was exploitable through transaction malleability, but resumed withdrawals by February 15th. In the March 2014 release of Bitcoin Core version 0.9.0, the Core Developers provided software fixes that limited the ability to adjust the transaction ID of a bitcoin transaction.

On February 25, 2014, Mt. Gox suspended trading on its platform and, three days later, filed for bankruptcy protection in Japanese courts, stating that it had lost approximately 850,000 bitcoins, including approximately 750,000 bitcoins belonging to its customers. Mt. Gox subsequently recovered access to approximately 200,000 of the lost bitcoins. As no full, reliable accounting has been publicly provided, it is difficult to assess whether Mt. Gox’s collapse was due to cyber-attacks (including denial of service and hacking incidents reported in 2011 and 2013), mismanagement or fraud. Following the cessation of trading activity on its platform, Mt. Gox has been in bankruptcy proceedings in Japan and the United States and is in the process of liquidation.

Since the cessation of trading on Mt. Gox, three Bitcoin Exchanges have dominated the US Dollar-denominated trading market (also known as the USD-BTC trading pair): BitStamp, Bitfinex and BTC-e. For the one month period ended December 28, 2014, those three exchanges accounted for just over 79 percent of the market for the USD-BTC trading pair as calculated by both BitcoinCharts.com and Bitcoinity.org (excluding Chinese Bitcoin Exchange OKCoin, which does not impose commissions on trades and is not tracked by BitcoinCharts.com).