Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - VirtualScopics, Inc. | Financial_Report.xls |

| EX-21 - EXHIBIT 21 - VirtualScopics, Inc. | v404973_ex21.htm |

| EX-23.1 - EXHIBIT 23.1 - VirtualScopics, Inc. | v404973_ex23-1.htm |

| EX-31.1 - EXHIBIT 31.1 - VirtualScopics, Inc. | v404973_ex31-1.htm |

| EX-31.2 - EXHIBIT 31.2 - VirtualScopics, Inc. | v404973_ex31-2.htm |

| EX-32.2 - EXHIBIT 32.2 - VirtualScopics, Inc. | v404973_ex32-2.htm |

| EX-32.1 - EXHIBIT 32.1 - VirtualScopics, Inc. | v404973_ex32-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Form 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2014

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the transition period from ____ to____

Commission file number: 000-52018

VIRTUALSCOPICS, INC.

(Exact name of registrant as specified in its charter)

| DELAWARE | 04- 3007151 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 500 Linden Oaks, Rochester, New York | 14625 | ||

| (Address of principal executive offices) | (Zip Code) |

(585) 249-6231

(Registrant's Telephone Number, Including Area Code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE EXCHANGE ACT:

Common Stock, $0.001 par value

NASDAQ Capital Market

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE EXCHANGE ACT:

TITLE OF EACH CLASS:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| ¨ Yes x No |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

| ¨ Yes x No |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers in response to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting” in Rule 12b-2 of the Exchange Act.

| Larger accelerated filer ¨ | Accelerated filer ¨ | |

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ or No x

The aggregate market value of the issuer’s voting and non-voting common equity held by non-affiliates of the issuer as of June 30, 2014 was approximately $10,079,691 (calculated by excluding all shares held by executive officers, directors and holders known to the registrant of five percent or more of the voting power of the registrant's common stock, without conceding that such persons are “affiliates” of the registrant for purposes of the federal securities laws). This amount does not include any value for the issuer’s series A preferred stock, series B preferred stock or series C preferred stock, for which there is no established United States public trading market, or any value for the common stock issuable upon conversion of shares of such preferred stock.

As of March 26, 2015, there were outstanding 2,994,928 shares of the issuer’s common stock, $.001 par value.

Documents Incorporated By Reference: Portions of the Company's Proxy Statement to be delivered to the Company’s stockholders in connection with the Company’s 2015 Annual Meeting of Stockholders, which the Company plans to file with the Securities and Exchange Commission pursuant to Regulation 14A promulgated under the Securities Exchange Act of 1934, on or prior to April 30, 2015, are incorporated by reference in Part III (Items 10, 11, 12, 13 and 14) of this Form 10-K.

TABLE OF CONTENTS

FORWARD-LOOKING STATEMENTS

Some of the statements under the captions of this report on Form 10-K titled “Risk Factors,” “Management's Discussion and Analysis of Financial Condition and Results of Operations” or “Business,” contained or incorporated by reference elsewhere in this report, and in our other reports filed with the Securities Exchange Commission (“SEC”) constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, which involve risks and uncertainties. These statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements include statements that address activities, events or developments that we expect, believe or anticipate may occur in the future, including:

| · | adverse

economic conditions; |

| · | loss

of market share due to competing products and services; |

| · | unexpected costs, lower than expected sales and revenues, and operating defects; |

| · | study cancellations and delays in the startup of trials; |

| · | adverse results of any legal proceedings; |

| · | the volatility of our operating results and financial condition; |

| · | inability

to attract or retain qualified senior management and scientific personnel; |

| · | inability to raise sufficient additional capital to operate our business, if necessary, and; |

| · | changes in government regulations; |

| · | other specific risks that may be referred to in this report. |

All statements, other than statements of historical facts, included in this report regarding our strategy, future operations, financial position, estimated revenue or losses, projected costs, prospects and plans and objectives of management are forward-looking statements. When used in this report, the words “may,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project,” “plan,” “could,” “would” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. All forward-looking statements speak only as of the date of this report. We do not undertake any obligation to update any forward-looking statements or other information contained in this report. Existing stockholders and potential investors should not place undue reliance on these forward-looking statements. Although we believe that our plans, intentions and expectations reflected in or suggested by the forward-looking statements in this report are reasonable, we cannot assure our stockholders or potential investors that these plans, intentions or expectations will be achieved. We disclose important factors that could cause our actual results to differ materially from our expectations under “Risk Factors” and elsewhere in this report. These risk factors qualify all forward-looking statements attributable to us or persons acting on our behalf.

Information regarding market and industry statistics contained in this report is included based on information available to us that we believe is accurate. It is generally based on academic and other publications that are not produced for purposes of securities offerings or economic analysis. We have not reviewed or included data from all sources, and we cannot assure our stockholders or potential investors of the accuracy or completeness of the data included in this report. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and the additional uncertainties accompanying any estimates of future market size, revenue and market acceptance of products and services. We have no obligation to update forward-looking information to reflect actual results or changes in assumptions or other factors that could affect those statements. See “Risk Factors” for a more detailed discussion of uncertainties and risks that may have an impact on future results.

| 3 |

We are a provider of quantitative imaging solutions currently serving the pharmaceutical, biotechnology and medical device industries. We have created a suite of image analysis software tools and applications which are used in detecting and measuring specific anatomical structures and metabolic activity using medical images. Our proprietary software and algorithms provide measurement capabilities designed to improve clinical research and development. We focus on applying our imaging technology to improve the efficiency and effectiveness of the pharmaceutical and medical device research and development processes. We believe our technology can also be used in improving the treatment planning for patients with cancer and other debilitating diseases. We are a Delaware corporation formed in 1988.

Business Overview

Our image-based measurement and visualization tools enable automated, accurate and reproducible measurement of minute changes that occur in anatomic structures in musculoskeletal, oncological, cardiological and neurological diseases. For pharmaceutical, biotechnology and medical device manufacturers, these tools can significantly alleviate or reduce clinical development bottlenecks by increasing the speed, accuracy and reliability of the demonstration of a new compound’s efficacy. Further, these measurements can be used to assess the viability of continuing a drug development project and eliminate as soon as possible further investigation of a drug that is likely to fail. Early termination is critical to the pharmaceutical industry to prevent the expenditure of research and development (“R&D”) funds on a drug that will not perform as expected. We believe that this is especially important today with the large number of compounds that are awaiting evaluation.

We are continuously looking for opportunities to expand the use of our quantitative imaging into new markets. There can be no assurance that we will experience significant demand for any opportunities that are pursued, or that we will have sufficient capital available to successfully commercialize any application.

Benefits to Pharmaceutical, Biotech and Medical Device Companies

The benefits to pharmaceutical companies from using our image analysis tools can include shorter clinical development time and earlier determination of the effectiveness or ineffectiveness of a new drug or compound. Our technology helps to curtail trials that are not likely to be beneficial and to avoid mistaken termination of the investigation of compounds that are likely to prove efficacious, through:

| · | improved precision in the measurement of traditional imaging biomarkers resulting in shorter observation periods, with beneficial cost savings within a clinical trial; |

| · | advanced imaging biomarkers, which are better correlated with disease states, again reducing trial length and therefore costs; and |

| · | reduced processing time for image data analysis through automation. |

In addition, our technology reduces aggregate clinical development costs through:

| · | improved precision of traditional imaging biomarkers, thus requiring smaller patient populations and lower administrative costs; and |

| · | advanced imaging biomarkers that serve as better correlates, leading to better early screening and elimination of weak drug candidates in pre-clinical and early phase trials. |

| 4 |

Our Technology Solution

Oncology Applications

Automated Measurement of Tumor Structure in Oncology

Volumetric imaging modalities such as X-Ray Computed Tomography (CT), Magnetic Resonance Imaging (MRI), and Positron Emission Tomography (PET) can provide a wealth of information about tumor size, structure, and function. However, the standard for clinical assessment of both tumor response to therapy and disease progression, the Response Evaluation Criteria in Solid Tumors (RECIST), focuses on the measurement of a single diameter in the axial plane for each measurable tumor, ignoring much of this additional information. VirtualScopics has developed a system which allows the rapid and efficient assessment of oncology patients per standard RECIST criteria, while also permitting the measurement of more sensitive measures including tumor volume, tumor metabolic rate via FDG-PET, tumor mitotic rate via FLT-PET, or tumor cellular density via diffusion MRI. VirtualScopics’ flexible workflow engine allows us to efficiently handle both large Phase III studies for which RECIST evaluation is the only endpoint, and smaller Phase I and Phase II studies where sponsors may need much more detailed information in order to make go/no-go decisions based on small patient populations.

Innovation in Image-Based Biomarkers

With a multidisciplinary team of medical professionals (including staff radiologists), scientists and software developers, we deliver unparalleled innovation in the analysis of specific biomarkers. Measurements may include specific Food and Drug Administration (“FDA”) acknowledged (e.g. RECIST) biomarkers as well as secondary or exploratory endpoints such as cavitation/necrosis, cellular density, or metabolic rate. By extracting substantially more information from existing imaging modalities such as CT or MRI, we believe we offer a more definite and efficient basis for determining the course of clinical trials.

Measurement of Blood Flow and Metabolic Activity

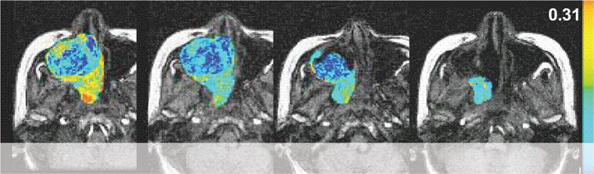

A growing number of anti-cancer drugs both on the market (e.g., Iressa and Avastin) and under development are designed to reduce the blood supply available to tumors, thereby depriving them of the ability to grow and spread. During development, these compounds require the ability to accurately measure blood flow and vascular permeability in vivo, in order to determine dose-response relationships and compound efficacy. In the clinic, this same capability is necessary in order to determine whether a particular patient is responding to treatment. We have developed a method, using dynamic contrast enhanced magnetic resonance imaging (DCE-MRI), to accomplish this. This technique involves repeated imaging, generally every two to six seconds, for a period of several minutes before and after the injection of a gadolinium-based, FDA-approved, contrast agent. Contrast concentration changes over time can then be measured both in normal and cancerous tissues, and based on this information parameters such as blood flow, blood volume and vascular permeability can be derived. These parameters have been shown to relate directly to the activity of anti-angiogenesis and anti-vascular cancer drugs, and to allow the prediction of response or failure after only a few days of treatment, as in the example given above.

With dynamic contrast-enhanced series, changes in signal intensity can be related to tracer concentration in tissues. This information can be used to determine the blood flow to the tumor.

| 5 |

Musculoskeletal Applications

Our image analysis provides a degree of accuracy and reproducibility that cannot be duplicated by manual techniques. Traditional radiologic interpretation of medical images is qualitative and subjective. Using semi-automated, computer-assisted assessment techniques produces quantitative results that are accurate, reproducible and objective. Unlike manual assessment methods, our computer-aided approach allows the user to track the boundary location of each structure in a data set from one scan to another, even if the patient is not positioned in precisely the same way for each scan, or if there have been some anatomical changes between scans. For cartilage volumes and thickness measurements, the Coefficient of Variation (CV) typically falls between 2% and 4% - we can detect minute changes with statistical confidence, allowing our clients to reduce study populations or shorten study durations. For changes in muscle volume, our semi-automated algorithms decrease the variability to below 1%. The reason for this is two-fold: the algorithms that identify the boundaries are both accurate and reproducible, and the time-savings produced by the algorithm reduces reader fatigue – instead of spending six hours reading a case, the reader is able to complete their analysis in about 25% of the time or less.

With our automated analysis, researchers can more confidently make the go/no go decision for a compound early in the evaluation process, allowing scarce resources to be allocated to the most promising candidates. The reason for this is two-fold: the algorithms that identify the boundaries are both accurate and reproducible, and the time-savings produced by the algorithm reduces reader fatigue – instead of spending six hours reading a case, the reader is able to complete their analysis in about 25% of the time or less.

Reproducible medical image analysis is driven by computer image analysis algorithms that enable quantitative measurement of different structural parameters. Guided by the information present in the images, as well as embedded anatomical knowledge, the algorithms enable segmentation of different structures. From an MRI knee scan, for instance, it is possible to produce a three-dimensional reconstruction that graphically distinguishes cartilage from underlying bone, as well as from ligaments, fluid, degenerated menisci or inflamed synovium. This capability provides a valuable assessment tool for clinical research in osteoarthritis - a disease with multiple endpoints - because it allows sensitive and specific measurement of all the components of the knee joint and detects small changes in any of those components over time.

Fatty Liver Disease

Many diseases and safety assessments benefit from the ability to calculate accurate hepatic fat fractions. As an example, non-alcoholic fatty liver disease (NAFLD) has become increasingly prevalent with estimates of 19% of adults in the US (28.8 million). Traditional methods for determining hepatic fat fraction are either extremely invasive (liver biopsy), qualitative (ultrasound), not widespread in clinical practice (magnetic resonance spectroscopy or MRS), or not particularly accurate (in- and out-of-phase dual-echo magnetic resonance imaging or MRI). VirtualScopics worked with a research organization and a sponsor to demonstrate that there is a much more accurate, non-invasive, quantitative technique utilizing MRI that works on most clinical magnets. The results of this study were published in the Journal of Magnetic Resonance Imaging in June of 2013. VirtualScopics has utilized this technique to evaluate the hepatic fat fraction of clinical trial subjects nearly 2,000 times.

Cardiovascular Applications

Cardiovascular disease is one of the leading causes of mortality within most developed countries. Cardiac toxicity is also one of the most common and most dangerous side-effects of a wide range of drugs. Oncology drugs in particular are known to often have adverse effects on cardiac function, and assessment of changes in cardiac function is an important part of the safety evaluation of nearly all oncology drugs. It is therefore very important to have efficient and accurate methods for assessing cardiac function in a clinical trial setting. VirtualScopics has integrated third party software packages, which are FDA-approved medical devices, with our workflow engine and analysis platform. This allows us to provide a wide range of cardiovascular safety and efficacy endpoints to our customers in a reliable and efficient manner, including:

| · | Automatic import of measurement values from ultrasound systems |

| · | Availability of all current 2D Echo-, M-Mode- and Doppler measurements |

| · | Measurement of up to five values for each parameter |

| · | Fast and flexible composition of relevant image data ensured by intuitive user interface |

| · | Side-by-side comparison of current and previous examinations (XA and Echo) |

| · | Comfortable analysis of image sequences using video functions |

| 6 |

| · | Export of image-data to AVI, BMP, JPEG or DICOM format |

The capabilities provided by these software packages, combined with VirtualScopics’ team of cardiologists and radiologists, have allowed VirtualScopics to take on trials which include a wide variety of cardiovascular endpoints including change in left ventricular ejection fraction, change in valve and wall motion, and cardiac strain assessment.

Neurology Applications

Evaluating diseases such as multiple sclerosis (MS), epilepsy, and Alzheimer’s requires the identification and measurement of neurological structures and lesions. Manual tracing, especially of abnormal neurological structures, requires considerable expertise and time. Tracing introduces significant variability even when all measurements are made by one individual, an effect that is compounded with multiple operators. Intra- and inter-operator variability poses a major obstacle for researchers attempting to take advantage of the power of MRI analysis in the study of neurological disease. VirtualScopics eliminates these problems with automated, statistically driven feature analysis. Our algorithms employ the two types of knowledge that expert radiologists use to measure structures within the brain: differentiation of various tissue types and knowledge of structure, size, location, and shape. Our software incorporates a priori model of neurological anatomy that enables the measurement of structures with indistinct boundaries such as the hippocampus. Knowledge of anatomical structures also improves reproducibility, allowing disease progression to be precisely monitored over time.

Many neurological conditions can be detected and evaluated with quantitative measures of structures in MRI studies. While automated measurement tracks lesions in MS clinical trials, it also provides a critical tool in measuring hippocampal volume for diagnosing and monitoring both intractable temporal lobe epilepsy and Alzheimer’s disease. Validation studies prove that our automated approach provides greater speed, precision and accuracy in clinical trials than manual methods do. In MS clinical trials, we provide an FDA-approved metric for quickly determining drug efficacy of MS compounds. A VirtualScopics validation study compared manual tracing using two VirtualScopics software algorithms for automated measurement: geometrically constrained region growth (GEORG) and directed clustering. Our Core Lab utilizes both algorithms to achieve an optimal system for quantification of MS lesions in multi-spectral MRI studies. In the MS validation study, mean processing time was 60 minutes for manual tracing, 10 minutes for GEORG, and 3 minutes for directed clustering. Intra- and inter-operator coefficients of variation were 5.1% and 16.5% for manual tracing, 1.4% and 2.3% for region growth and 1.5% and 5.2% for directed clustering. The study also compared our automated measurement and manual tracing from an expert radiologist against a phantom data set. In all data sets, automated algorithms performed significantly better than manual tracing. Our automated measurements also proved more repeatable than manual methods, an important feature in multi-center clinical trials.

Sales and Marketing

Our sales and business development strategy is centered around the publication and presentation of our technology and services at targeted industry conferences along with an active marketing effort aimed at pharmaceutical, medical device, and biotechnology companies. It is focused on a segmented and targeted approach relative to account type, sales channel, therapeutic area, and study phase. The Sales Plan consists of the positioning of our core imaging services through direct selling efforts and through the PPD Channel in the Oncology, Metabolic, and Cardiology markets and the IXICO strategic alliance in the Alzheimer’s market.

During 2014, we performed services on new and existing contracts with 8 of the 10 leading pharmaceutical, biotechnology and medical device companies. In total, we performed services on 142 projects for 34 customers. We continue to grow our business by leveraging relationships with our current customers and through referrals. As a result, our current customers have been instrumental in introducing us to other therapeutic groups within their organization. Our marketing efforts are instrumental in broadening the awareness of VirtualScopics throughout the industry and educating current customers on the breadth of our services.

| 7 |

Complementing our sales and marketing efforts are our strategic alliances with PPD, Inc. and IXICO, plc. The alliance affords us the opportunity to penetrate an expanded customer base through a combined solution to the market. We are working closely to develop the best in kind solution combining core Clinical Resource Organization (CRO) services with our imaging platform. The alliance also provides for our earlier engagement with potential customers because PPD tends to be engaged earlier in the supplier selection process of the drug development cycle.

In June 2014, we entered into an international commercial alliance with IXICO plc (LON: IXI), a provider of quantitative medical imaging focused on Alzheimer’s, based in London. The alliance will help give us operational capabilities in Europe and a broader range of therapeutic area and modality expertise. By combining our resources, we believe we are enhancing our ability to deliver on the largest trials worldwide and to do so across a more diverse range of therapeutic areas.

Subsequently, we jointly opened an office in New Hope, Pennsylvania, strategically located in the corridor that runs through New Jersey and Pennsylvania, in a location close to many of our pharmaceutical customers.

On December 11, 2014, we entered into an agreement to license IXICO’s TrialTrackerTM proprietary image data and query management platform. The agreement includes the implementation of TrialTrackerTM together with multi-year software license and maintenance support. We were also delighted to announce on December 16, 2014, that the alliance had been awarded its first joint project by a global top 15 pharmaceutical company. This involves the provision of image analysis services for a Phase II oncology clinical trial.

In addition to these initiatives, we actively participate in medical conferences to showcase our technology, services and results, as well as authoring joint publications with sponsors which often results in highly visible research. We have built a strong base of clinical collaborators across varied disease platforms.

Backlog

Backlog represents anticipated service revenue from work not yet completed or performed under signed contracts. Once work commences, revenue is generally recognized over the life of the contract as services are provided. Backlog at December 31, 2014 was approximately $29 million, compared with approximately $24 million at December 31, 2013, an increase of 21%. Subject to the matters addressed in the following paragraph, we believe that approximately $19 million of the backlog will not be recognized as revenue in our fiscal year ending December 31, 2015.

We believe that backlog is a useful measure for management and investors to evaluate our business activity. Nonetheless, there are several factors that can affect whether we will realize the full benefits of projects included in the backlog and the time over which we will realize that revenue. These factors include customers terminating, delaying, or changing the scope of a project for a variety of reasons including, among others, the failure of drugs being tested to satisfy safety requirements, unexpected or undesirable clinical results, client decisions to forego a particular study, and insufficient patient enrollment or investigator recruitment. Furthermore, the contracts may contemplate performance over multiple years. Therefore, revenue may not be realized in the fiscal year in which the contract is signed or the award is made. Recognition of revenue under the contract may also be affected by the timing of patient recruitment and image site identification and training. Additionally, the majority of contracts we have with customers are cancelable for any reason by giving 30 days advance notice. As a result, we cannot assure you amounts included in our backlog will be indicative of future results.

Industry Background and Market Trends

Market in Pharmaceutical and Medical Device Development

| 8 |

Industry Overview

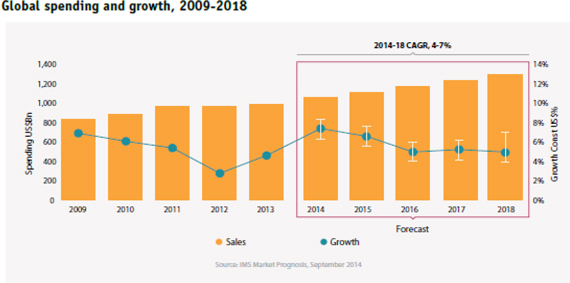

The global pharmaceutical market is expected to reach nearly $1.3 trillion by 2018, an increase of about 30 percent over the 2013 level, driven by population growth, an aging population, and improved access to pharmerging markets. The global compound annual growth rate (CAGR) of the global pharmaceutical market is forecasted to peak in 2014-15 and will be moderate through 2018, due to fewer patent expires, launches of more innovative medicines and price increases with the CAGR expected to stabilize between 4-7 percent through 2018. The U.S. Pharmaceutical market is expected to peak in 2014 with a forecasted growth rate of 11-13 percent and expand by 5-8 percent through 2018. Emerging markets on the other hand are expected to grow collectively at a 8-11 percent rate through 2018. Meanwhile, the five major European markets of Germany, France, Italy, Spain and the UK are expected to grow at only a 1-4 percent pace with Canada expected to grow at a 3-6 percent pace.1

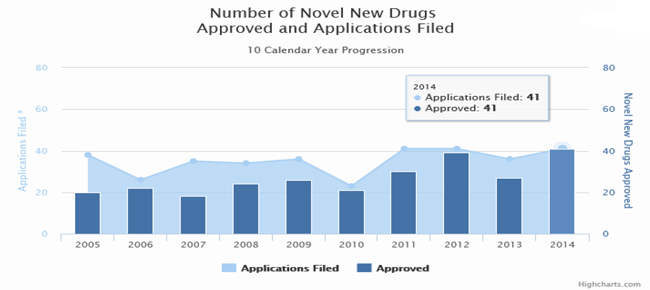

The Center for Drug Evaluation and Research (“CDER”) approved 41 new molecular entities or “NMEs” in 2014, which is more than the average number approved annually during the past decade. For instance from 2005 through 2013, CDER has averaged about 25 NME approvals per year.2

Source: IMS Institute for Healthcare Informatics – The Global Use of Medicines: Outlook through 2018

Source: Food and Drug Administration – 2014 Novel New Drugs Summary

1 IMS Institute for Healthcare Informatics – The Global Use of Medicines: Outlook through 2018

2 Food and Drug Administration – 2014 Novel New Drugs Summary

| 9 |

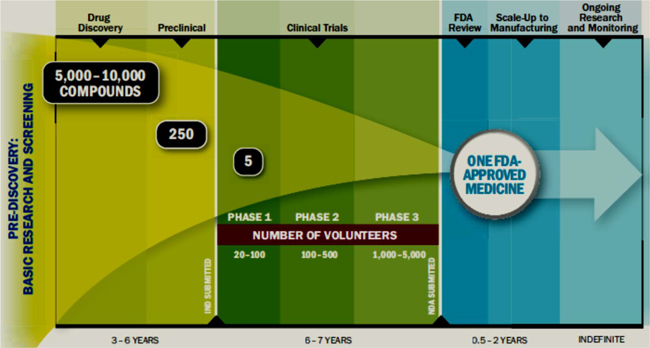

As the growth rate in the demand for prescription drugs decreases, it is getting harder for pharmaceutical companies to maintain the same levels of R&D spending as in the past. Additionally, the cost and complexity of developing new drugs, in part due to the increased scrutiny over product safety and the pressure to demonstrate health outcomes earlier, has increased substantially relative to its potential value. It has been estimated that the average cost to yield a single FDA approved drug is approximately $1.2 billion and the entire research and development and FDA approval process time is between 10 and 15 years. Additionally, for every 5,000 -10,000 compounds that enter at the discovery stage, only one goes on to reach the market. The table below illustrates the complete R&D process from pre discovery to market.

Source: PhRMA – 2013 Profile Pharmaceutical Industry

Drug Development Process

Typically, most functions of the drug and medical device R&D process are managed by clinical research organizations, or CROs. Most biopharma companies are at the end of multi-year patent cliffs and are stepping up investments in their late stage pipelines. The sector is expecting growth with a CAGR of 5-6 percent through 2018. The market is highly concentrated with the top ten players accounting for more than 50% of the CRO Market. The leading CROs by amount of estimated market share are Quintiles (15%), Covance (9%), Parexel (8%), PRA International (7-8%), and PPD (6-7%).3

Although the FDA has reduced the average approval time for new drugs, clinical development time has been increasing over the years, resulting in total development time being fairly flat in recent years. Growing complexities in protocol design leading to longer clinical development times has been the major contributor to the rising costs that sponsors are facing.

The current trend in drug development is for pharmaceutical companies to shift towards a niche market. The 'one size fits all' approach is being replaced by a more targeted, innovative approach to develop treatments for small patient groups with complicated diseases such as cancer, rheumatoid arthritis and immune disorders. Such 'niche buster drugs' are expected to exploit new technologies such as biomarkers and theranostics.

With the U.S. administration implementing health care reform, increased regulatory oversight and pressure on drug companies to reduce prices, we believe there is a need for R&D to become more efficient and reduce costs to prevent an innovation slowdown in the industry. Many leading pharmaceutical companies have restructured their R&D processes by establishing centers of R&D excellence and disease focused centers although historical commercial success rate for new drugs is low, with only 2 out of 10 drugs matching or exceeding average R&D costs.4

3 Results Healthcare – 2013 CRO’s and Other Outsourced Pharmaceutical Support Services

| 10 |

Due to these factors, we believe our quantitative imaging analyses offer solutions to these issues within drug development by providing more precise and reliable information in the assessment of compounds being developed. We believe our increased precision and reproducibility enable our customers to make more confident decisions on the efficacy of their compounds.

Quantitative Image Analysis Services

We have conducted research to determine the size of the market for image analysis services in clinical trials supporting the pharmaceutical, biotech and medical device industries. Based on our research and discussion within the imaging CRO and medical device and drug development industries, we have found that the market is highly competitive and fragmented, with approximately $550 million in total annual revenues projected for 2015. As competition increases, we will look to provide value-added services and undertake marketing and sales programs to differentiate our services based on our technology, expertise, and experience in specific therapeutic areas. Competition has resulted in additional pressure being placed on price, service and quality with the recent consolidations within the industry over the past few years.

We estimate that the annual growth rate for the market is 0% to 10% for the next five years. Our estimates are based on the amount of trials currently conducted within therapeutic areas in which we work and the annual growth rate of the pharmaceutical and CRO markets in which imaging is a component. We believe that some of the largest players, which offer the broadest set of capabilities, are experiencing flat to modest growth relative to their revenues derived by imaging services.

Intellectual Property

We consider our proprietary and patented technology and the technology for which we have applied for patent protection to be of importance to our business plan. We hold eight patents issued by the United States Patent and Trademark Office. These patents begin to expire in 2020 and expire thereafter through 2028. We have also applied for a number of other patents, both domestically and in foreign jurisdictions. To protect our proprietary technology, we rely primarily on a combination of confidentiality procedures and copyright, trademark and patent laws. Our policy is to require employees and consultants to execute confidentiality and invention assignment agreements upon the commencement of their relationship with the Company. These agreements provide that confidential information developed or made known during the course of a relationship with the Company must be kept confidential and not disclosed to third parties except in specific circumstances and for the assignment to VirtualScopics of intellectual property rights developed within the scope of the relationship.

Competition

Our main competitors are imaging clinical research organizations (iCROs) providing clinical trial services to pharmaceutical companies. As of the date of this report, we believe that none of the leading imaging CROs have technology capabilities that are comparable to our technology. iCROs typically provide manual and non-differentiated interpretation of medical images for the pharmaceutical industry. As a result, we believe that currently there is an opportunity for us to establish a technology advantage and a set of differentiated services in the advanced image-based biomarker market.

The main CROs which participate in imaging trials are Perceptive, Icon, and CCBR-Synarc+BioClinica. Additionally, some academic centers have worked on software that has applications for neurological diseases. However, we believe these academic centers lack the required FDA compliance standards and ability to scale their operations to meet customer demand and we believe they offer inferior technology.

4 PhRMA – 2014 Profile Pharmaceutical Industry

| 11 |

Our technology competition is largely comprised of a limited number of university research centers that are developing the next generation of image analysis tools. Aside from university centers, there are a few commercial entities that have a desire to provide these advanced imaging services. However, we believe they are constrained by a lack of technical capabilities.

Government Regulation

Healthcare in the United States is heavily regulated by the federal government, and by state and local governments. The federal laws and regulations affecting healthcare change constantly, thereby increasing the uncertainty and risk associated with any healthcare-related company.

The federal government regulates healthcare through various agencies, including the following:

| · | the Food and Drug Administration, or FDA, which administers the Food, Drug, and Cosmetic Act, or FD&C Act, as well as other relevant laws; |

| · | Centers for Medicare & Medicaid Services, or CMS, which administers the Medicare and Medicaid programs; |

| · | the Office of Inspector General, or OIG, which enforces various laws aimed at curtailing fraudulent or abusive practices, including by way of example, the Anti-Kickback Law, the Anti-Physician Referral Law, commonly referred to as Stark, the Anti-Inducement Law, the Civil Money Penalty Law, and the laws that authorize the OIG to exclude health care providers and others from participating in federal healthcare programs; and |

| · | the Office of Civil Rights which administers the privacy aspects of the Health Insurance Portability and Accountability Act of 1996, or HIPAA. |

All of the aforementioned are agencies within the Department of Health and Human Services, or HHS. Healthcare is also provided or regulated, as the case may be, by the Department of Defense through its TriCare program, the Public Health Service within HHS under the Public Health Service Act, the Department of Justice through the Federal False Claims Act and various criminal statutes, and state governments under the Medicaid program and their internal laws regulating all healthcare activities.

FDA

The FDA regulates medical devices. A “medical device,” or device, is an article, including software and software associated with another medical device, which, among other things, is intended for use in the diagnosis of disease or other conditions, or in the cure, mitigation, treatment or prevention of disease, in man or other animals. Computer software that complements a CT or MRI scan, such as VirtualScopics’, we believe is considered a medical device and is therefore subject to FDA regulation. To date, our sales have been to the pharmaceutical and medical device industries to support their clinical trials. We would need to obtain FDA clearance or approval, as discussed below, before using our technology and services for diagnostic or treatment planning in a clinical setting.

Devices are subject to varying levels of regulatory control, the most comprehensive of which requires that a clinical evaluation be conducted before a device receives approval for commercial distribution. In the United States, we generally are able to obtain permission to distribute a new device in two ways. The first applies to any new device that is substantially equivalent to a device first marketed prior to May 1976. In this case, to obtain FDA permission to distribute the device, we generally must submit a premarket notification application (a section 510(k) submission), and receive an FDA order finding substantial equivalence to a device (first marketed prior to May 1976) and permitting commercial distribution of that device for its intended use. A 510(k) submission must provide information supporting its claim of substantial equivalence to the predicate device.

| 12 |

If clinical data from human experience are required to support the 510(k) submission, these data must be gathered in compliance with investigational device exemption (IDE) regulations for investigations performed in the United States. The FDA review process for premarket notifications submitted pursuant to section 510(k) takes on average about 90 days, but it can take substantially longer if the agency has concerns, and there is no guarantee that the agency will “clear” the device for marketing, in which case the device cannot be used for diagnosis and distributed in the United States. Nor is there any guarantee that the agency will deem the article subject to the 510(k) process, as opposed to the more time-consuming and resource intensive and problematic, premarket approval, or PMA, process described below.

The second, more comprehensive, approval process applies to a new device that is not substantially equivalent to a pre-1976 product. In this case, two steps of FDA approval generally are required before we can market the product in the United States. First, we must comply with IDE regulations in connection with any human clinical investigation of the device. Second, the FDA must review our PMA application, which contains, among other things, clinical information acquired under the IDE. The FDA will approve the PMA application if it finds there is reasonable assurance the device is safe and effective for its intended use.

Certain changes to existing devices that do not significantly affect safety or effectiveness can be made with in vitro testing under reduced regulatory procedures, generally without human clinical trials and by filing a PMA supplement to a prior PMA. Exported devices are subject to the regulatory requirements of each country to which the device is exported, as well as certain FDA export requirements.

After approval or clearance to market is given, the FDA and foreign regulatory agencies, upon the occurrence of certain events, have the power to withdraw the clearance or require changes to a device, its manufacturing process, its labeling or additional proof that regulatory requirements have been met.

A device manufacturer is also required to register with the FDA. As a result, we may be subject to periodic inspection by the FDA for compliance with the FDA’s Quality System Regulation requirements and other regulations. In the European Union, we are required to maintain certain International Organization for Standardization (ISO) certifications in order to sell product and to undergo periodic inspections by notified bodies to obtain and maintain these certifications. These regulations require the Company to manufacture products and maintain documents in a prescribed manner with respect to design, manufacturing, testing and control activities. Further, we are required to comply with various FDA and other agency requirements for labeling and promotion. The Medical Device Reporting regulations require that we provide information to the FDA whenever there is evidence to reasonably suggest that a device may have caused or contributed to a death or serious injury or, if a malfunction of the device were to occur, it could cause or contribute to a death or serious injury. In addition, the FDA prohibits the Company from promoting a medical device for unapproved purposes.

We currently meet the requirements of Good Clinical Practices: Consolidated Guidance, which governs the conduct of clinical trials, and our software complies with the FDA’s Regulation 21 CFR Part 11 (Electronic Records; Signatures) and 21 CFR Part 820.30, which outline the requirements for design controls in medical devices. As mentioned throughout this section, as we develop our approach into personalized medicine, FDA approval would most likely be required for the use of our software in that market.

Privacy Provisions of HIPAA

HIPAA, among other things, protects the privacy and security of individually identifiable health information by limiting its use and disclosure. HIPAA directly regulates “covered entities” (healthcare providers, insurers and clearinghouses) and indirectly regulates “business associates” with respect to the privacy of patients’ medical information. All entities that receive and process protected health information are required to adopt certain procedures to safeguard the security of that information. It is our policy to comply with HIPAA requirements.

| 13 |

Research and Development Costs

We incurred $1,245,264 and $1,510,721 in research and development costs for the years ended December 31, 2014 and 2013, respectively.

Customers

The following table sets forth information as to revenue and percentage of revenue for our largest customers in 2014 and 2013:

| For the Years Ended December 31, | ||||||||||||||||

| 2014 | 2013 | |||||||||||||||

| Customer 1 | $ | 2,699,978 | 26 | % | $ | 4,682,332 | 42 | % | ||||||||

| Customer 2 | $ | 2,158,828 | 21 | % | $ | 1,290,075 | 12 | % | ||||||||

| Customer 3 | $ | 2,083,135 | 20 | % | $ | 1,226,391 | 11 | % | ||||||||

| Customer 4 | $ | 1,082,844 | 10 | % | $ | - | - % | |||||||||

Employees

As of December 31, 2014 we had 95 employees, 85 of which were full-time. We are not party to any collective bargaining agreements and we believe our relationships with our employees are good.

You should carefully consider the following risk factors before making an investment decision. If any of the following risks actually occur, our business, financial condition, or results of operations could be materially adversely affected. In such cases, the trading price of our common stock could decline, and you may lose all or part of your investment.

If our services do not continue to attract interest from new and existing customers, we may not maintain our current level of business or achieve future growth.

If we are unable to continue to attract interest in the industry for our services, we could fail to maintain our current level of business or achieve future growth. This would have a detrimental effect on our business. Our ability to generate revenues is highly dependent on building and maintaining relationships with leading pharmaceutical and biotechnology companies. No assurance can be given that a sufficient number of such companies will maintain or increase their demand for our services, thereby limiting the overall market and not enable us to increase our revenue. In addition, the rate of the growth of MRI and CT image-based biomarkers is difficult to predict. Failure to attract and maintain a significant customer base would have a detrimental effect on our business, operating results and financial condition.

The majority of the contracts we have with customers are cancelable for any reason by giving 30 days advance notice.

Our customers typically engage us to perform services for them on a project-by-project basis and are required by us to enter into a written contractual agreement for the work, labor and services to be performed. Generally, our project contracts are terminable by the customer for any or no reason on 30 days’ advance notice to us. If a number of our customers were to exercise cancellation rights, our business and operating results would be materially and adversely affected.

Our reported amounts of anticipated service revenue to be earned from the backlog may not be indicative of future results.

As of December 31, 2014, the amount of anticipated service revenue remaining to be earned from the backlog was approximately $29 million as compared to approximately $24 million as of December 31, 2013.

| 14 |

Backlog represents anticipated service revenue from work not yet completed or performed under signed contracts. The majority of contracts we have with customers are cancelable for any reason by giving 30 days advance notice. We cannot assure you that this amount will be indicative of future results. Furthermore, the contracts may contemplate performance over multiple years. Therefore, revenue may not be realized in the fiscal year in which the contract is signed or the award is made. There are several factors that can affect whether we will realize the full benefits under a contract or award and the time over which we will realize that revenue including:

| • | Customer cancellation due to performance reasons with their compounds in development; |

| • | Change in the scope of a project; |

| • | Timing of performance, including over multiple years; |

| • | Timing of patient recruitment and image site identification and training. |

Also, if clients delay projects, we will not generate revenue at the rate originally expected. Accordingly, the historical relationship of our reported backlog to revenues may not be indicative of future results.

If we are unable to manage and sustain growth in our business, our operating results would be adversely affected.

We have seen a growing demand for our image analysis services in clinical trials for pharmaceutical companies over the past year. Although there can be no assurance that growth in demand will continue or that customers will complete the clinical trial projects as awarded to us, if it does continue we may be unable to scale our capacity efficiently to meet this demand. If we are unable to do so, we may fail to maintain our operating margins or achieve expected operating margins. This may have a material and adverse effect on our operating results.

Our services may become obsolete if we do not effectively respond to rapid technological change on a timely basis.

Our services depend on the needs of our customers and their desire to utilize image-related services in drug and medical device development. Since the image-based biomarker industry is characterized by evolving technologies, uncertain technology and limited availability of standards, we must respond to new research findings and technological changes affecting our customers. We may not be successful in developing and marketing, on a timely and cost-effective basis, new or modified products and services, which respond to technological changes, evolving customer requirements and competition. If we are unsuccessful in this regard, our business and operating results could be materially and adversely affected.

We have a history of operating losses and uncertain future profitability.

We have incurred losses from operating activities. As we work to grow our business, we may face risks and difficulties in our business including uncertainties of maintaining our current customers, further market penetration, competition, cost increases and delays in achieving business objectives. There can be no assurance that we will succeed in addressing any or all of these risks or that we will achieve future profitability. The failure to do so would have a material adverse effect on our business, financial condition, and operating results.

Although we believe that our services do not and will not infringe upon the patents or violate the proprietary rights of others, it is possible such infringement or violation has occurred or may occur which could have a material adverse effect on our business.

Portions of our business are reliant upon patented and patentable systems and methods used in our image analysis and related intellectual property. In the event that we are deemed to infringe upon the patents or proprietary rights of others, we could be required to modify our products and services or obtain a license for the manufacture and/or sale of such services. In such event, there can be no assurance that we would be able to do so in a timely manner, upon acceptable terms and conditions, or at all, and the failure to do any of the foregoing could have a material adverse effect upon our business. Moreover, there can be no assurance that we will have the financial or other resources necessary to enforce or defend a patent infringement or proprietary rights violation action. In addition, we could be subject to injunctive relief and, under certain circumstances, become liable for damages, which could also have a material adverse effect on our business.

| 15 |

We are subject to pharmaceutical, medical device and healthcare industry regulations, which could adversely affect the nature and extent of the products and services we offer.

Many aspects of the pharmaceutical, medical device and healthcare industry are subject to regulation at the federal level. From time to time, the regulatory entities that have jurisdiction over the industry adopt new or modified regulations or take other actions as a result of their own regulatory processes or as directed by other governmental bodies. This changing regulatory environment could adversely affect the nature and extent of the services we are able to offer.

Our failure to compete effectively in our industry could cause our revenues to decline.

The image analysis industry is highly competitive. We face numerous competitors in our business. If we fail to compete effectively, we will lose clients, which would cause our business to suffer. Our ability to successfully compete is dependent on many factors, including: timely and quality performance; expertise and experience in specific therapeutic areas; the scope of service offerings; strength in various geographic markets; the price of services; our competitors’ service and product offerings; and our ability to upgrade our services in comparison to the service and product offerings of our competitors. If our services are not competitive based on these or other factors, our business, financial condition and results of operations could be materially harmed.

We may in the future experience competition from academic sites, imaging CROs, and other competing technologies.

Competition in the development of imaging solutions may become more widespread as with emerging technologies such as proteomics and genomics which can serve as predictive tools of drug efficacy. Competitors range from university-based research and development projects which would develop advanced tools to development stage companies and major domestic and international companies which would commercialize the tools. Some of these entities have greater financial, technical, marketing, sales, distribution and other resources than ours. There can be no assurance that we can continue to develop our technologies or that present or future competitors will not develop technologies that render our image-based biomarker industry obsolete or less marketable or that we will be able to introduce new products and product enhancements that are competitive with other products marketed by industry participants.

We have experienced significant demand from certain customers, thereby increasing our dependence on these customers until we can further diversify our customer base.

While we continue to serve a broad range of customers, we have experienced strong demand from four of our customers in 2014 as compared to three of our customers in 2013. We depend on these customers to sustain our growth. In 2014 and 2013, these customers accounted for 77% and 65% of our revenue, respectively. We continue to see demand from other customers but not at the same significant pace as these three customers. We continue to invest on our sales and marketing efforts to further diversify our customers and more broadly penetrate the market, in order to minimize reliance on any one customer. As with all of our contracts, these customers may terminate their contractual relationships with us for any or no reason on 30 days’ advance notice. A decision by any of these customers to cancel all of its studies with us could have an adverse impact on the growth of our business.

| 16 |

Consolidation within the pharmaceutical industry and changes within healthcare regulation may have an adverse impact on our business.

Over the past few years, there have been several mergers and acquisitions among pharmaceutical and biotechnology companies. Historically, these transactions have positively impacted our business due to the ability to use our strong relationships within one of the merged entities to better penetrate the combined entity. However, there can be no assurance that consolidation within the industry will continue to be beneficial to us. Additionally, with the recent political landscape and changes within the healthcare industry, there may be an adverse impact on our business if the cost of imaging significantly increases or no longer becomes standard of care for patients. Although, we do not believe imaging will decline in its level of use, if it does we may need to reduce prices or invest in research to advance the education and science of medical imaging.

Consolidation among our competitors could cause us to lose customers or could exert additional pressure on the prices of our services.

There has been a significant amount of consolidation among providers of clinical trial imaging services and other services such as ours. Larger enterprises created through this consolidation may also have greater resources and efficiencies than our company and have other competitive advantages. As a result of this consolidation, competition to provide goods and services to customers has increased. Further consolidation in the industry could exert additional pressure on the prices of our products.

Loss of key personnel, or failure to attract and retain additional personnel, could have a material adverse effect on our business.

Our success will be dependent on our continued ability to attract, retain and motivate highly skilled employees. The Board of Directors appointed director Eric Converse to serve as President and Chief Executive Officer and Jim Groff to serve as Chief Financial Officer during 2014. Leadership transitions can be inherently difficult to manage and may cause disruption to our business or further turnover in our workforce or management team. The loss of services of one or more other members of senior management would likely have a material adverse effect on our business.

Furthermore, our performance also depends on our ability to attract and retain management and qualified scientific and technical operating staff. Competition for these skilled personnel is intense. The loss of services of any key executive, or inability to continue to attract and retain qualified staff could have a material adverse effect on our business, results of operations and financial condition. We do not maintain any key employee insurance on any of our executives.

The trading price of our stock may be adversely affected if we are not able to maintain and grow our business.

We intend to continue to use our cash on hand to broaden our market penetration of our services within the industry. If our plans or assumptions with respect to our business change or prove to be inaccurate, we may be required to use part or all of our cash to fund general operating expenses and/or reduce costs within the organization.

We currently do not plan to raise additional capital. However, if we need to raise additional capital, it may not be available on acceptable terms, or at all. Our failure to obtain required capital, or the acquisition of capital on less favorable terms, would have a material adverse effect on our business. If we issue additional equity securities in the future, there could be a dilution or a reduction in priority of our outstanding securities.

The market price of our common stock may fluctuate significantly.

The market price of our common stock may fluctuate significantly in response to factors, some of which are beyond our control, such as the announcement of new products or product enhancements by us or our competitors; developments concerning intellectual property rights and regulatory approvals; quarterly variations in our competitors’ results of operations; changes in earnings estimates or recommendations by securities analysts; developments in our industry; product liability claims or other litigation; and general market conditions and other factors, including factors unrelated to our own operating performance.

| 17 |

Our common stock may be considered a “penny stock” and may be difficult to sell.

The SEC has adopted regulations which generally define “penny stock” to be an equity security that has a market or exercise price of less than $5.00 per share, subject to specific exemptions. The market price of our common stock is currently below $5.00 per share and therefore may be designated as a “penny stock” according to SEC rules. This designation requires any broker or dealer selling these securities to disclose certain information concerning the transaction, obtain a written agreement from the purchaser and determine that the purchaser is reasonably suitable to purchase the securities. These rules may restrict the ability of brokers or dealers to sell our common stock and may affect the ability of our stockholders to sell their shares.

Our strategic alliance with PPD is an important aspect of our growth, and the market may not value our strategic alliance with PPD as we anticipate.

In 2010, we formed an alliance with PPD to provide a joint solution to provide clients with an integrated and customized clinical development and medical imaging solution for oncology clinical trials. The alliance was expanded in January 2012 to include cardiovascular, central nervous system and medical device studies. If the market does not value this model as we anticipate, our ability to grow our business may be negatively impacted. Additionally, the agreement may be terminated by either party on 90 days’ notice. In the event PPD terminates the agreement, we may also experience a negative impact in our ability to experience the level of growth we have historically achieved.

The inability to maintain our NASDAQ listing may adversely affect the trading market for our common stock.

There can be no assurance that we will be able to maintain compliance with NASDAQ listing requirements, including the $1.00 minimum bid price requirement. If our common stock is delisted from NASDAQ, trading in our common stock could be conducted on the OTC Bulletin Board or in the over-the-counter market in what is commonly referred to as the "pink sheets." If this occurs, a shareholder will find it more difficult to dispose of our common stock or to obtain accurate quotations as to the price of our common stock. Lack of any active trading market would have an adverse effect on a shareholder's ability to liquidate an investment in our common stock easily and quickly at a price acceptable to the shareholder. It might also contribute to volatility in the market price of our common stock and could adversely affect our ability to raise additional equity or debt financing on acceptable terms or at all.

A significant number of the shares of our common stock are eligible for sale, and their sale could negatively affect the market price of our common stock.

Sales of a significant number of shares of our common stock in the public market or the possibility of such sales could harm the market price of our common stock and impede our ability to raise capital through the issuance of equity securities. As of December 31, 2014, we had 2,994,928 shares of common stock outstanding. These shares are eligible for resale in the public market either immediately or subject to applicable limitations of Rule 144. In addition to these outstanding shares of common stock, we also have shares to be issued upon the conversion or exercise of 404,612 outstanding options to purchase common stock, 136,132 warrants to purchase common stock and 478,701 shares of preferred stock that are convertible into common stock. We have registered on Form S-8 the sale of up to 690,000 shares issued or to be issued pursuant to our Amended and Restated 2006 Long-Term Incentive Plan, of which 363,070 are subject to outstanding option awards. Sales of our common stock in the public market may have an adverse effect on the market for the shares of our common stock.

| 18 |

Our principal stockholders have significant voting power and may take actions that may not be in the best interests of other stockholders.

Our officers, directors, principal stockholders (greater than 5%) and their affiliates control approximately 30% of our outstanding voting securities. If these stockholders act together, they will be able to exert significant control over our management and affairs requiring stockholder approval, including approval of significant corporate transactions. This concentration of ownership may have the effect of delaying or preventing a change in control and might adversely affect the market price of our common stock. This concentration of ownership may not be in the best interests of all our stockholders.

We do not anticipate paying dividends on our common stock in the foreseeable future, and the lack of dividends may have a negative effect on the stock price.

We currently intend to retain our future earnings to support operations and to finance expansion and meet dividend obligations on our series C-1 and series B convertible preferred stock. In addition, the terms of our series C-1 and series B preferred stock limit our ability to pay dividends to the holders of our common stock. Therefore, we do not anticipate paying any cash dividends on our common stock in the foreseeable future.

In July 2007 we began leasing approximately 19,500 square feet of office space at our corporate headquarters in Rochester, New York. In June 2012, the Company renewed its lease for five years with a lease commencement date of July 1, 2012. The base annual rent under the lease is $309,075, and increases two percent (2%) per year over the term of the lease.

In May 2014, the Company entered into a lease for approximately 2,190 square feet of office space in New Hope, Pennsylvania. The lease term is for three years with a lease commencement date of June 1, 2014. The base annual rent under the lease is $54,000, and increases three percent (3%) per year over the term of the lease.

None.

ITEM 4: Mine Safety Disclosures

Not applicable.

| 19 |

ITEM 5: Market For Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our shares of common stock are listed for trading on the NASDAQ Capital Market under the trading symbol “VSCP.” The following table sets forth the high and low closing sales prices for our common stock as reported on the NASDAQ Capital Market for the period from January 1, 2013 through December 31, 2014. We affected a 1-for-10 reverse stock split of the Company’s outstanding common stock on August 21, 2013. Corresponding adjustments were made to the number of shares of common stock underlying the Company’s outstanding options, warrants, and preferred stock exercisable for or convertible into common stock and the related long-term incentive plans for such options. All share and related option information presented have been retroactively adjusted to reflect the reduced number of shares and the corresponding increase in stock price resulting from this action. These prices also do not include retail markup, markdown or commission and may not necessarily represent actual transactions. Investors should not rely on historical stock price performance as an indication of future price performance.

| Fiscal Year Ended December 31, 2013 | ||||||||

| High | Low | |||||||

| First Quarter | $ | 7.80 | $ | 6.00 | ||||

| Second Quarter | 6.80 | 3.80 | ||||||

| Third Quarter | 6.70 | 4.20 | ||||||

| Fourth Quarter | 4.82 | 2.93 | ||||||

| Fiscal Year Ended December 31, 2014 | ||||||||

| High | Low | |||||||

| First Quarter | $ | 4.20 | $ | 3.21 | ||||

| Second Quarter | 5.59 | 3.64 | ||||||

| Third Quarter | 5.10 | 3.77 | ||||||

| Fourth Quarter | 4.62 | 3.10 | ||||||

As of March 26, 2015, we had approximately 63 registered holders of record of shares of our common stock.

Dividend Policy

We have never declared a cash dividend on our common stock. We intend to retain any earnings to fund future growth and the operation of our business and, therefore, we do not anticipate paying any cash dividends on our common stock in the foreseeable future. In addition, the terms of our Series B Preferred Stock and Series C-1 Preferred Stock limit our ability to pay dividends to the holders of our common stock. Dividends may be paid on our common stock only if and when declared by our board of directors and paid on an as-converted basis to the holders of our Series A, Series B, and Series C-1 convertible preferred stock.

Equity Compensation Plan Information

The following table summarizes information, as of December 31, 2014, relating to our equity compensation plans:

| 20 |

| Number of Securities to be Issued Upon Exercise of Outstanding Options | Weighted- Average Exercise Price of Outstanding Options | Number of Securities Remaining Available for Future Issuance Under Equity Compensation Plans (Excluding Securities Reflected in Column (a) | ||||||||||

| Plan Category | (a) | (b) | (c) | |||||||||

| Equity compensation plans approved by security holders | 369,612 | (1) | $ | 8.61 | 272,222 | |||||||

| Equity compensation plans not approved by security holders | 35,000 | (2) | $ | 25.00 | - | |||||||

| Total | 404,612 | $ | 10.03 | 272,222 | ||||||||

(1) This amount includes shares options to purchase shares of common stock collectively, under our 2005 and 2006 Long Term Incentive Plans.

(2) In November 2005, our Board of Directors granted to our former Chairman and CEO, Robert Klimasewski, an option to purchase 35,000 shares of our common stock at $25 per share.

Recent Sales of Unregistered Securities

We made no sales of unregistered securities during the quarter ended December 31, 2014.

Issuer Repurchases of Equity Securities

None.

ITEM 7: Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion should be read in conjunction with VirtualScopics’ consolidated balance sheet, and related consolidated statements of operations, changes in stockholders’ equity and cash flows for the years ended December 31, 2014 and 2013, included elsewhere in this report. This discussion contains forward-looking statements, the accuracy of which involves risks and uncertainties. Our actual results could differ materially from those anticipated in the forward-looking statements for many reasons including, but not limited to, those discussed in “Risk Factors” and elsewhere in this report. We disclaim any obligation to update information contained in any forward-looking statements.

Overview

VirtualScopics, Inc. is a leading provider of imaging solutions to accelerate drug and medical device development. We have developed a robust software platform for analysis and modeling of both structural and functional medical images. In combination with our industry-leading experience and expertise in advanced imaging biomarker measurement, this platform provides a uniquely clear window into the biological activity of drugs and devices in clinical trial patients, allowing our customers to make better decisions faster.

Since inception, revenues have been derived primarily from image processing services in connection with pharmaceutical drug trials. For these services, we have been concentrating in the areas of oncology, fatty liver disease, neurology, cardiovascular, and osteoarthritis. We have also derived a small portion of revenue from consulting services. We expect that the concentration of our revenue will continue in these services and in those areas in 2015. Revenues are recognized as the medical images that we process are quantified and delivered to our customers and/or the services are performed.

| 21 |

We are focused on strengthening our core business and increasing the number of contract awards we receive. This effort includes investments in our infrastructure and sales function. We continue to submit proposals and bids for new contracts, however, there can be no assurance that we will secure or maintain contracts from these efforts. Additionally, due to recent consolidation within the industry, our pricing and services may not stay competitive with companies that have a stronger global presence.

There are several factors that can affect whether we will realize the full benefits under any contract and the time over which we will realize that revenue. Customers may not continue our services due to many reasons including lack of demonstrated efficacy with their compounds in development. Furthermore, the contracts may contemplate performance over multiple years. Therefore, revenue may not be realized in the fiscal year in which the contract is signed or awarded. Recognition of revenue under the contract may also be affected by the timing of patient recruitment and image site identification and training.

Results of Operations

Results of Operations for Year Ended December 31, 2014 Compared to Year Ended December 31, 2013

Revenues

We had revenues of $10,452,000 for the year ended December 31, 2014 compared to $11,174,000 for the year ended December 31, 2013, representing a 6% decrease. The decrease in revenues is partially related to the slowdown in the amount of new projects awarded in 2012, the effects of which can carry over multiple years due to the timing in the recognition of revenue for a study can be on average over a three year period. Revenues were also impacted by the timing of the initiation of awarded and contracted projects and the large number of studies that were completed in 2013 and 2014. During the life of a project, quite often there is an expansion in the size of the study. However there are also situations where the sponsor does not recruit the number of subjects or sites as originally budgeted and in those cases there are remaining budget dollars at the end of the study that will not be realized into revenue. Additionally, the decrease in revenues was affected by a six week, retrospective, Phase III breast cancer study which generated over $1 million in revenues during the second quarter of 2013 that did not reoccur in 2014. Excluding this six week nonrecurring study from 2013, revenues would have increased by approximately $278,000 or 3% for the year ended December 31, 2014.

The Company continues to focus on strategies that we believe will lead to increased revenue and profitability. In 2014, the Company finalized an alliance with IXICO, plc located in London, which provides clinical trial solutions focusing on Alzheimer’s disease. The alliance enables the Company to access IXICO’s expertise in this area and provides a European presence. In addition, we believe the integration of the companies’ complementary technologies will help provide more comprehensive and scalable capabilities especially for Phase III studies. The Company also finalized the recruitment of a Scientific Advisory Board which we believe will enhance and deepen our knowledge base in our core competencies and allow for an exchange of ideas and knowledge in each therapeutic area. We continued investments in our sales function by the recent opening of a satellite office in New Hope, Pennsylvania. This office is primarily for sales and project management, allowing our representatives to be closer to our customers in the Pharma corridor.

During 2014, we performed work on 142 different projects in connection with our pharmaceutical drug trials in the fields of oncology, osteoarthritis and various other therapeutic areas. This compares to 138 projects on which we performed work during 2013.

| 22 |

Gross Profit