Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - ENDURANCE SPECIALTY HOLDINGS LTD | d898672d8k.htm |

| EX-99.2 - EX-99.2 - ENDURANCE SPECIALTY HOLDINGS LTD | d898672dex992.htm |

| Exhibit 99.1

|

Endurance: Acquisition of Montpelier Re Investor Presentation

March 31, 2015

|

|

Forward Looking Statements and Regulation G Disclaimer

Cautionary Note Regarding Forward Looking Statements

Some of the statements in this presentation may include, and Endurance may make related oral, forward-looking statements which reflect our current views with respect to future events and financial performance. Such statements may include forward-looking statements both with respect to us in general and the insurance and reinsurance sectors specifically, both as to underwriting and investment matters. These statements may also include assumptions about our proposed acquisition of Montpelier (including its benefits, results, effects and timing). Statements which include the words “should,” “would,” “expect,” “intend,” “plan,” “believe,” “project,” “anticipate,” “seek,” “will,” and similar statements of a future or forward-looking nature identify forward-looking statements in this presentation for purposes of the U.S. federal securities laws or otherwise. We intend these forward-looking statements to be covered by the safe harbor provisions for forward-looking statements in the Private Securities Litigation Reform Act of 1995.

All forward-looking statements address matters that involve risks and uncertainties. Accordingly, there are or may be important factors that could cause actual results to differ materially from those indicated in the forward-looking statements. These factors include, but are not limited to, the effects of competitors’ pricing policies, greater frequency or severity of claims and loss activity, changes in market conditions in the agriculture insurance industry, termination of or changes in the terms of the U.S. multiple peril crop insurance program, a decreased demand for property and casualty insurance or reinsurance, changes in the availability, cost or quality of reinsurance or retrocessional coverage, our inability to renew business previously underwritten or acquired, our inability to maintain our applicable financial strength ratings, our inability to effectively integrate acquired operations, uncertainties in our reserving process, changes to our tax status, changes in insurance regulations, reduced acceptance of our existing or new products and services, a loss of business from and credit risk related to our broker counterparties, assessments for high risk or otherwise uninsured individuals, possible terrorism or the outbreak of war, a loss of key personnel, political conditions, changes in accounting policies, our investment performance, the valuation of our invested assets, a breach of our investment guidelines, the unavailability of capital in the future, developments in the world’s financial and capital markets and our access to such markets, government intervention in the insurance and reinsurance industry, illiquidity in the credit markets, changes in general economic conditions and other factors described in our Annual Report on Form 10-K for the year ended December 31, 2014.

Additionally, the proposed transaction is subject to risks and uncertainties, including: (A) that Endurance and Montpelier may be unable to complete the proposed transaction because, among other reasons, conditions to the closing of the proposed transaction may not be satisfied or waived; (B) uncertainty as to the timing of completion of the proposed transaction; (C) uncertainty as to the actual premium of the Endurance share component of the proposal that will be realized by Montpelier shareholders in connection with the transaction; (D) uncertainty as to the long-term value of Endurance ordinary shares; (E) failure to realize the anticipated benefits and synergies from the proposed transaction, including as a result of failure or delay in integrating Montpelier’s businesses into Endurance; (F) the risk that regulatory or other approvals required for the transaction are not obtained or are obtained subject to conditions that are not anticipated; (G) the inability to retain key personnel; (H) any changes in general economic and/or industry specific conditions; and (I) the outcome of any legal proceedings to the extent initiated against Endurance, Montpelier and others following the announcement of the proposed transaction, as well as Endurance and Montpelier management’s response to any of the aforementioned factors.

The foregoing review of important factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included herein and elsewhere, including the risk factors included in Endurance’s most recent report on Form 10-K and the risk factors included in Montpelier’s most recent report on Form 10-K and other documents of Endurance and

Montpelier on file with the Securities and Exchange Commission (“SEC”). Any forward-looking statements made in this presentation are qualified by these cautionary statements, and there can be no assurance that the actual results or developments anticipated by Endurance will be realized or, even if substantially realized, that they will have the expected consequences to, or effects on, Endurance or its business or operations. Except as required by law, the parties undertake no obligation to update publicly or revise any forward-looking statement, whether as a result of new information, future developments or otherwise.

Additional Information about the Proposed Transaction and Where to Find It

The issuance of Endurance ordinary shares to Montpelier shareholders in the merger will be submitted to shareholders of Endurance for their consideration. The proposed merger will be submitted to shareholders of Montpelier for their consideration. This presentation is not a solicitation of any vote or approval and is not a substitute for the joint proxy statement/prospectus or any other documents which Endurance or Montpelier may send to their respective shareholders in connection with the proposed merger.

This presentation does not constitute an offer to sell or the solicitation of an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of such jurisdiction. No offering of securities shall be made except by means of a proxy statement/prospectus meeting the requirements of the Securities Act of 1933, as amended.

ENDURANCE AND MONTPELIER SHAREHOLDERS ARE URGED TO READ THE JOINT PROXY STATEMENT/PROSPECTUS FOR THE PROPOSED MERGER WHEN IT IS FILED, AND ANY AMENDMENT OR

SUPPLEMENT THERETO THAT MAY BE FILED, WITH THE SEC BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. All such documents, when filed, are available free of charge at the SEC’s website (www.sec.gov) or by directing a request to Endurance at the Investor Relations contact on the next page.

2

|

|

Forward Looking Statements and Regulation G Disclaimer

(cont’d)

Participants in the Solicitation

Endurance and Montpelier and their directors and executive officers are deemed to be participants in any solicitation of Endurance and Montpelier shareholders in connection with the proposed merger. Information about Endurance’s directors and executive officers is available in Endurance’s Definitive Proxy Statement, dated April 9, 2014, for its 2014 Annual General Meeting of shareholders and Form 8-K, dated November 26, 2014. Information about Montpelier’s directors and executive officers is available in Montpelier’s Definitive Proxy Statement, dated March 26, 2014, for its 2014

Annual General Meeting of shareholders and Form 8-K, dated May 15, 2014.

Additional Information

All references in this presentation to “$” refer to United States dollars. The contents of any website referenced in this presentation are not incorporated by reference herein.

Regulation G Disclaimer

In this presentation, management has included and discussed certain non-GAAP measures. Management believes that these non-GAAP measures, which may be defined differently by other companies, better explain the proposed transaction in a manner that allows for a more complete understanding. However, these measures should not be viewed as a substitute for those determined in accordance with GAAP. For a complete description of non-GAAP measures and reconciliations, please review the Investor Financial Supplement on our web site at www.endurance.bm.

The combined ratio is the sum of the loss, acquisition expense and general and administrative expense ratios. Endurance presents the combined ratio as a measure that is commonly recognized as a standard of performance by investors, analysts, rating agencies and other users of its financial information. The combined ratio, excluding prior year net loss reserve development, enables investors, analysts, rating agencies and other users of its financial information to more easily analyze Endurance’s results of underwriting activities in a manner similar to how management analyzes Endurance’s underlying business performance. The combined ratio, excluding prior year net loss reserve development, should not be viewed as a substitute for the combined ratio.

Net premiums written is a non-GAAP internal performance measure used by Endurance in the management of its operations. Net premiums written represents net premiums written and deposit premiums, which are premiums on contracts that are deemed as either transferring only significant timing risk or transferring only significant underwriting risk and thus are required to be accounted for under GAAP as deposits. Endurance believes these amounts are significant to its business and underwriting process and excluding them distorts the analysis of its premium trends. In addition to presenting gross premiums written determined in accordance with GAAP, Endurance believes that net premiums written enables investors, analysts, rating agencies and other users of its financial information to more easily analyze Endurance’s results of underwriting activities in a manner similar to how management analyzes Endurance’s underlying business performance. Net premiums written should not be viewed as a substitute for gross premiums written determined in accordance with GAAP.

Return on Equity (ROE) is comprised using the average common equity calculated as the arithmetic average of the beginning and ending common equity balances for stated periods. The Company presents various measures of Return on Equity that are commonly recognized as a standard of performance by investors, analysts, rating agencies and other users of its financial information.

Contact Information

Endurance Specialty Holdings Ltd. Investor Relations Phone: +1 441 278 0988 Email: investorrelations@endurance.bm

Media Relations

Mark Semer and Thomas Davies Kekst and Company Phone: 212 521 4802/4873

Email: mark-semer@kekst.com and tom-davies@kekst.com

3

|

|

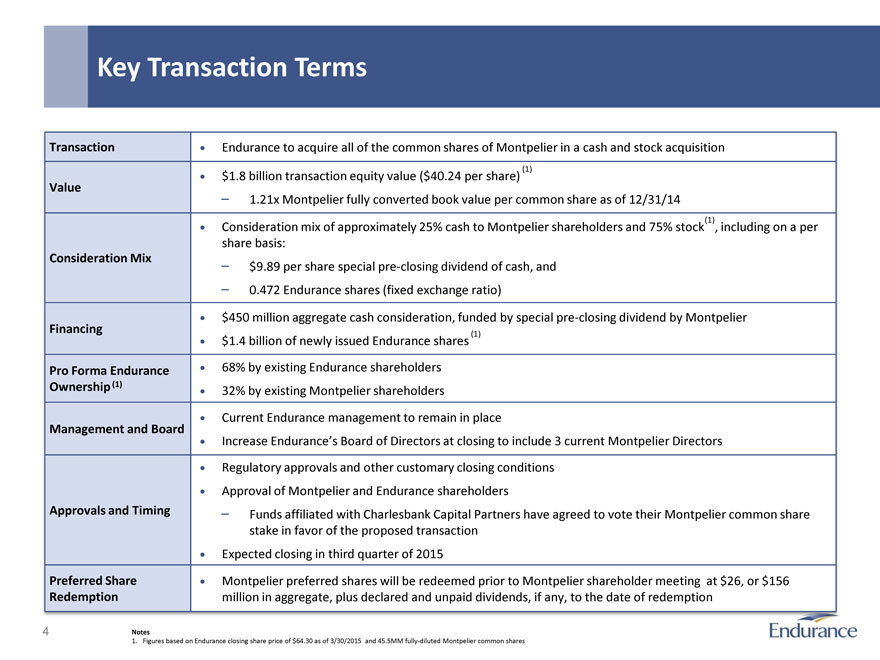

Key Transaction Terms

Transaction • Endurance to acquire all of the common shares of Montpelier in a cash and stock acquisition

• $1.8 billion transaction equity value ($40.24 per share) (1)

Value

1.21x Montpelier fully converted book value per common share as of 12/31/14

• Consideration mix of approximately 25% cash to Montpelier shareholders and 75% stock(1) , including on a per

share basis:

Consideration Mix $9.89 per share special pre-closing dividend of cash, and

0.472 Endurance shares (fixed exchange ratio)

• $450 million aggregate cash consideration, funded by special pre-closing dividend by Montpelier

Financing

• $1.4 billion of newly issued Endurance shares (1)

Pro Forma Endurance • 68% by existing Endurance shareholders

Ownership (1) • 32% by existing Montpelier shareholders

• Current Endurance management to remain in place

Management and Board

• Increase Endurance’s Board of Directors at closing to include 3 current Montpelier Directors

• Regulatory approvals and other customary closing conditions

• Approval of Montpelier and Endurance shareholders

Approvals and Timing Funds affiliated with Charlesbank Capital Partners have agreed to vote their Montpelier common share

stake in favor of the proposed transaction

• Expected closing in third quarter of 2015

Preferred Share • Montpelier preferred shares will be redeemed prior to Montpelier shareholder meeting at $26, or $156

Redemption million in aggregate, plus declared and unpaid dividends, if any, to the date of redemption

Notes

1. Figures based on Endurance closing share price of $64.30 as of 3/30/2015 and 45.5MM fully-diluted Montpelier common shares

4

|

|

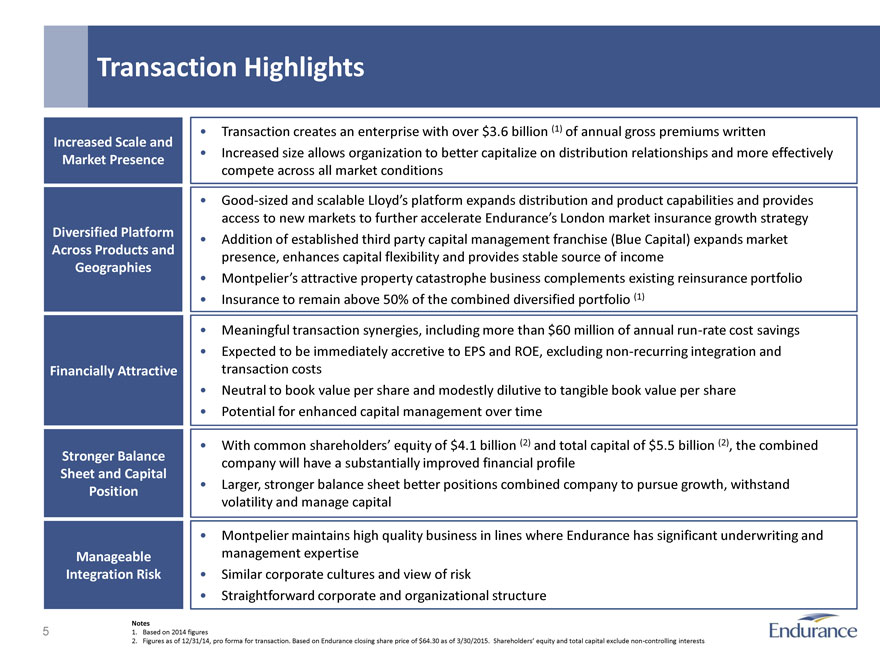

Transaction Highlights

• Transaction creates an enterprise with over $3.6 billion (1) of annual gross premiums written

Increased Scale and

Market Presence • Increased size allows organization to better capitalize on distribution relationships and more effectively

compete across all market conditions

• Good-sized and scalable Lloyd’s platform expands distribution and product capabilities and provides

access to new markets to further accelerate Endurance’s London market insurance growth strategy

Diversified Platform • Addition of established third party capital management franchise (Blue Capital) expands market

Across Products and presence, enhances capital flexibility and provides stable source of income

Geographies

• Montpelier’s attractive property catastrophe business complements existing reinsurance portfolio

• Insurance to remain above 50% of the combined diversified portfolio (1)

• Meaningful transaction synergies, including more than $60 million of annual run-rate cost savings

• Expected to be immediately accretive to EPS and ROE, excluding non-recurring integration and

Financially Attractive transaction costs

• Neutral to book value per share and modestly dilutive to tangible book value per share

• Potential for enhanced capital management over time

• With common shareholders’ equity of $4.1 billion (2) and total capital of $5.5 billion (2), the combined

Stronger Balance company will have a substantially improved financial profile

Sheet and Capital

Position • Larger, stronger balance sheet better positions combined company to pursue growth, withstand

volatility and manage capital

• Montpelier maintains high quality business in lines where Endurance has significant underwriting and

Manageable management expertise

Integration Risk • Similar corporate cultures and view of risk

• Straightforward corporate and organizational structure

Notes

1. Based on 2014 figures

2. Figures as of 12/31/14, pro forma for transaction. Based on Endurance closing share price of $64.30 as of 3/30/2015. Shareholders’ equity and total capital exclude non-controlling interests

5

|

|

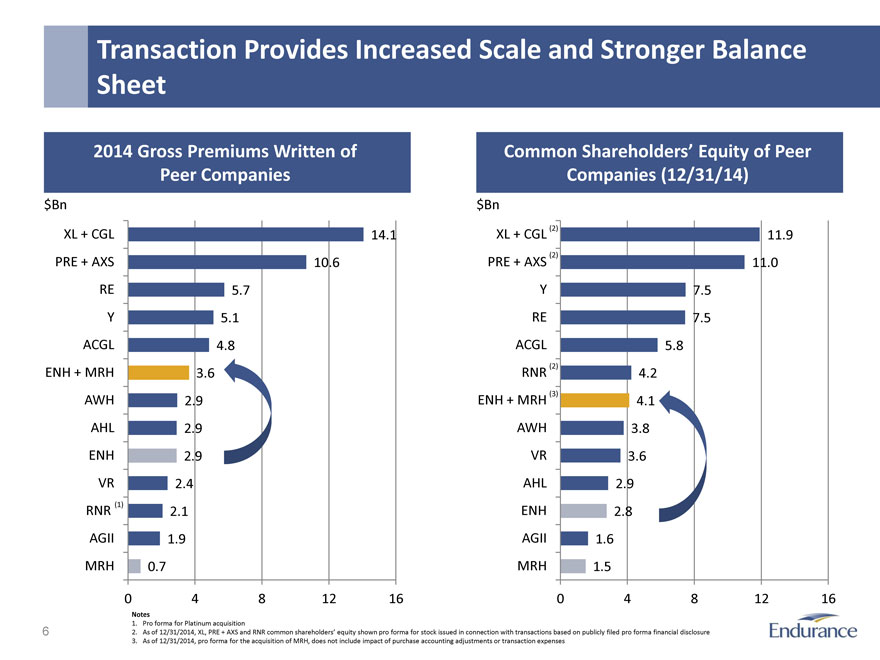

Transaction Provides Increased Scale and Stronger Balance

Sheet

2014 Gross Premiums Written of Common Shareholders’ Equity of Peer

Peer Companies Companies (12/31/14)

$Bn $Bn

XL + CGL 14.1 XL + CGL (2) 11.9

PRE + AXS 10.6 PRE + AXS (2) 11.0

RE 5.7 Y 7.5

Y 5.1 RE 7.5

ACGL 4.8 ACGL 5.8

ENH + MRH 3.6 RNR (2) 4.2

AWH 2.9 ENH + MRH (3) 4.1

AHL 2.9 AWH 3.8

ENH 2.9 VR 3.6

VR 2.4 AHL 2.9

RNR (1) 2.1 ENH 2.8

AGII 1.9 AGII 1.6

MRH 0.7 MRH 1.5

0 4 8 12 16 0 4 8 12 16

Notes

1. Pro forma for Platinum acquisition

2. As of 12/31/2014, XL, PRE + AXS and RNR common shareholders’ equity shown pro forma for stock issued in connection with transactions based on publicly filed pro forma financial disclosure

3. As of 12/31/2014, pro forma for the acquisition of MRH, does not include impact of purchase accounting adjustments or transaction expenses

6

|

|

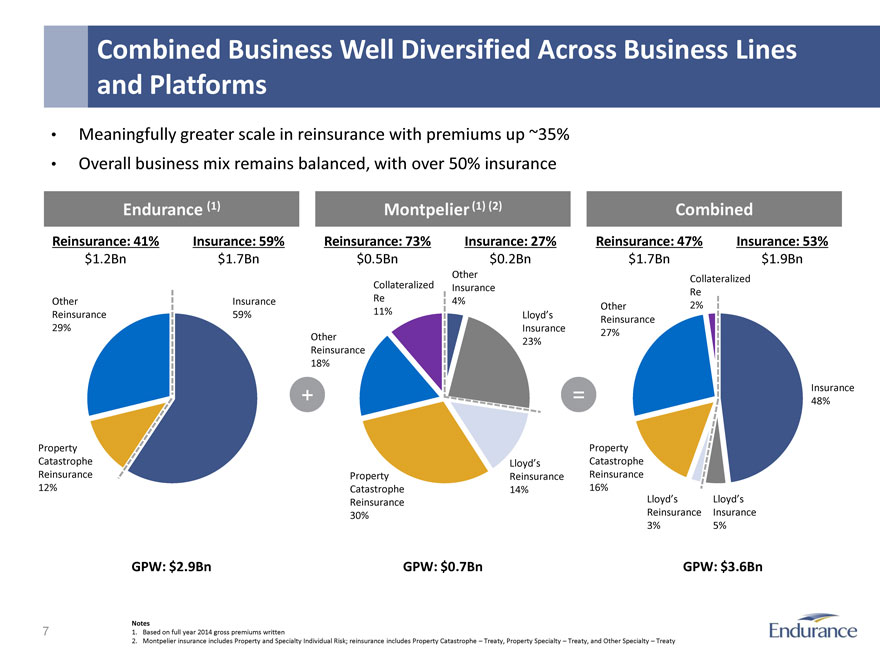

Combined Business Well Diversified Across Business Lines and Platforms

Meaningfully greater scale in reinsurance with premiums up ~35%

Overall business mix remains balanced, with over 50% insurance

Endurance (1) Montpelier (1) (2) Combined

Reinsurance: 41% Insurance: 59% Reinsurance: 73% Insurance: 27% Reinsurance: 47% Insurance: 53%

$1.2Bn $1.7Bn $0.5Bn $0.2Bn $1.7Bn $1.9Bn

Other Collateralized

Collateralized Insurance Re

Other Insurance Re 4% Other 2%

Reinsurance 59% 11% Lloyd’s

Reinsurance

29% Insurance

Other 27%

23%

Reinsurance

18%

+ = Insurance

48%

Property Property

Catastrophe Lloyd’s Catastrophe

Reinsurance Property Reinsurance Reinsurance

12% Catastrophe 14% 16%

Reinsurance Lloyd’s Lloyd’s

30% Reinsurance Insurance

3% 5%

GPW: $2.9Bn GPW: $0.7Bn GPW: $3.6Bn

Notes

1. Based on full year 2014 gross premiums written

2. Montpelier insurance includes Property and Specialty Individual Risk; reinsurance includes Property Catastrophe – Treaty, Property Specialty – Treaty, and Other Specialty – Treaty

7

|

|

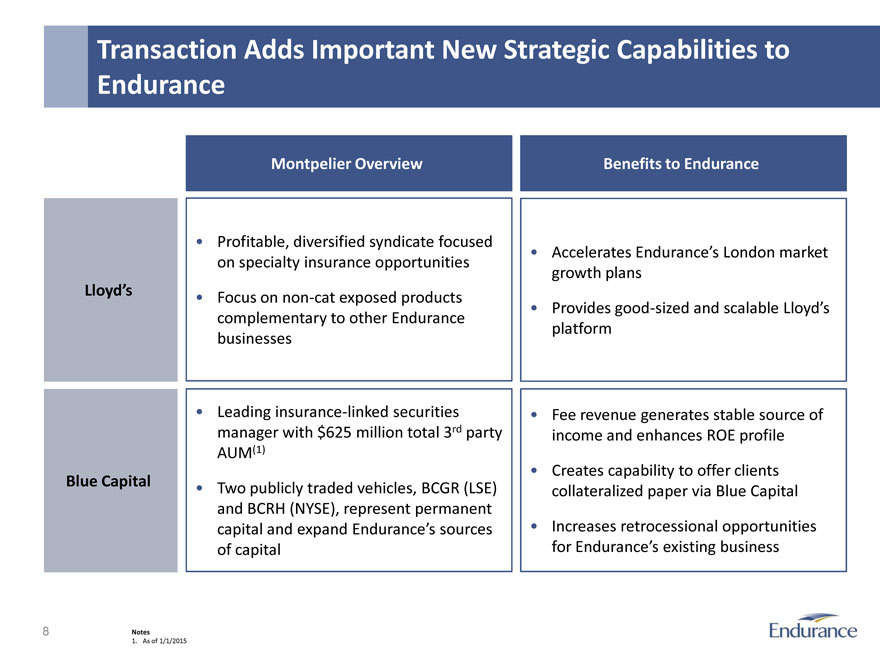

Transaction Adds Important New Strategic Capabilities to

Endurance

Montpelier Overview Benefits to Endurance

• Profitable, diversified syndicate focused

• Accelerates Endurance’s London market

on specialty insurance opportunities

growth plans

Lloyd’s • Focus on non-cat exposed products

• Provides good-sized and scalable Lloyd’s

complementary to other Endurance

platform

businesses

• Leading insurance-linked securities • Fee revenue generates stable source of

manager with $625 million total 3rd party income and enhances ROE profile

AUM(1)

• Creates capability to offer clients

Blue Capital • Two publicly traded vehicles, BCGR (LSE) collateralized paper via Blue Capital

and BCRH (NYSE), represent permanent

capital and expand Endurance’s sources • Increases retrocessional opportunities

of capital for Endurance’s existing business

Notes

1. As of 1/1/2015

8

|

|

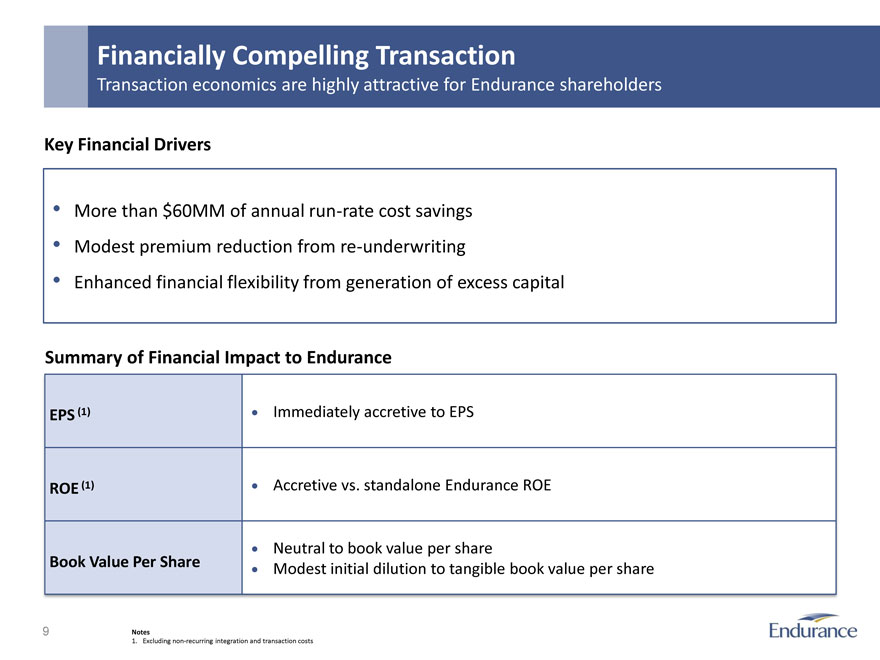

Financially Compelling Transaction

Transaction economics are highly attractive for Endurance shareholders

Key Financial Drivers

• More than $60MM of annual run-rate cost savings

Modest premium reduction from re-underwriting

Enhanced financial flexibility from generation of excess capital

Summary of Financial Impact to Endurance

EPS (1) • Immediately accretive to EPS

ROE (1) • Accretive vs. standalone Endurance ROE

• Neutral to book value per share

Book Value Per Share • Modest initial dilution to tangible book value per share

Notes

1. Excluding non-recurring integration and transaction costs

9

|

|

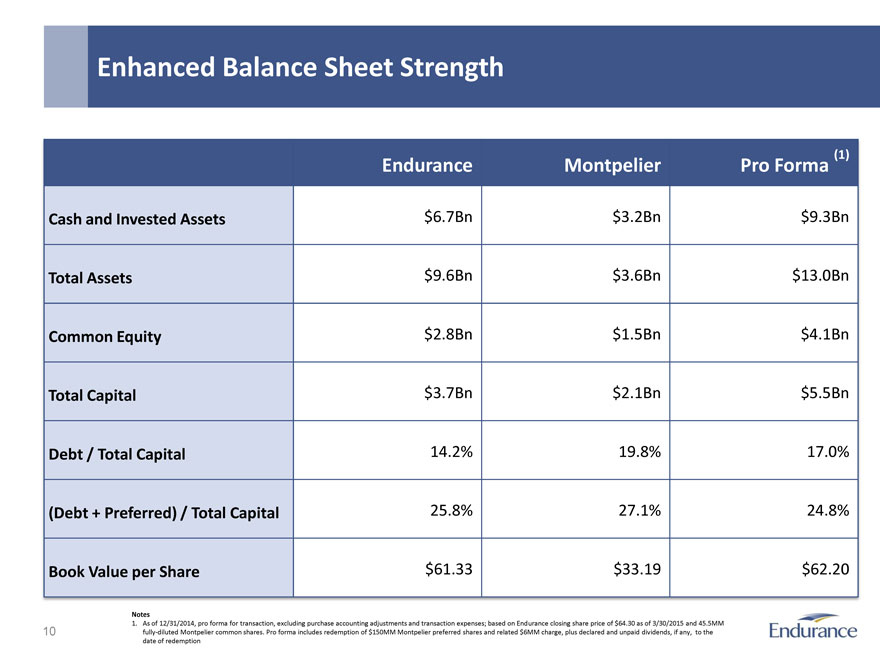

Enhanced Balance Sheet Strength

Endurance Montpelier Pro Forma (1)

Cash and Invested Assets $6.7Bn $3.2Bn $9.3Bn

Total Assets $9.6Bn $3.6Bn $13.0Bn

Common Equity $2.8Bn $1.5Bn $4.1Bn

Total Capital $3.7Bn $2.1Bn $5.5Bn

Debt / Total Capital 14.2% 19.8% 17.0%

(Debt + Preferred) / Total Capital 25.8% 27.1% 24.8%

Book Value per Share $61.33 $33.19 $62.20

Notes

1. As of 12/31/2014, pro forma for transaction, excluding purchase accounting adjustments and transaction expenses; based on Endurance closing share price of $64.30 as of 3/30/2015 and 45.5MM fully-diluted Montpelier common shares. Pro forma includes redemption of $150MM Montpelier preferred shares and related $6MM charge, plus declared and unpaid dividends, if any, to the date of redemption

10

|

|

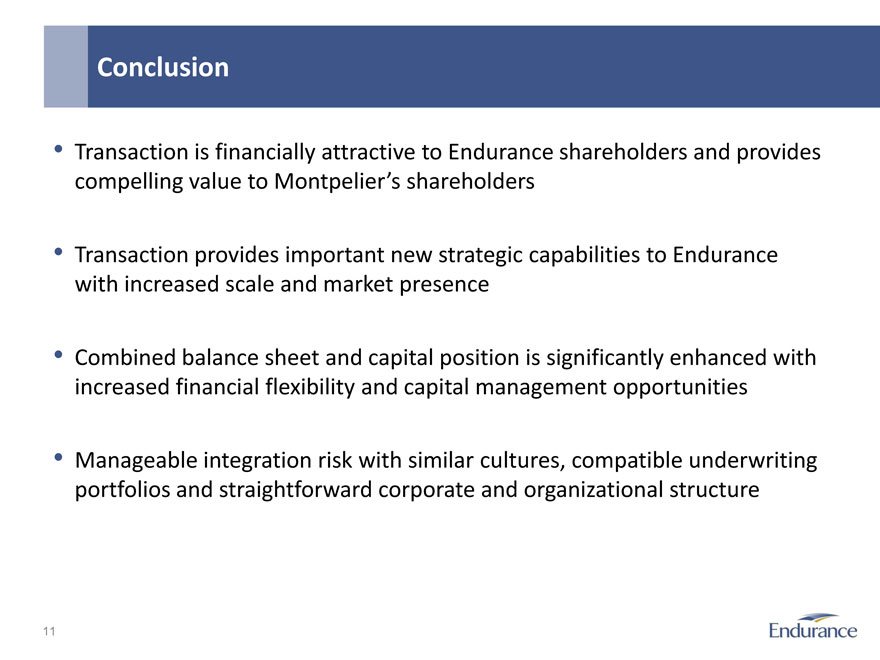

Conclusion

Transaction is financially attractive to Endurance shareholders and provides compelling value to Montpelier’s shareholders

Transaction provides important new strategic capabilities to Endurance with increased scale and market presence

Combined balance sheet and capital position is significantly enhanced with increased financial flexibility and capital management opportunities

Manageable integration risk with similar cultures, compatible underwriting portfolios and straightforward corporate and organizational structure

11