Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - SOCKET MOBILE, INC. | Financial_Report.xls |

| EX-23 - EXHIBIT 23.1 - SOCKET MOBILE, INC. | k10ex23_1.htm |

| EX-31 - EXHIBIT 31.2 - SOCKET MOBILE, INC. | k10ex31_2.htm |

| EX-31 - EXHIBIT 31.1 - SOCKET MOBILE, INC. | k10ex31_1.htm |

| EX-32 - EXHIBIT 32.1 - SOCKET MOBILE, INC. | k10ex32_1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

| (X) | ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

( ) TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from _______ to _______.

Commission file number 1-13810

SOCKET MOBILE, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 94-3155066 | |

(State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

39700 Eureka Drive, Newark, CA 94560

(Address of principal executive offices including zip code)

(510) 933-3000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Exchange Act:

| Title of Each Class | Name of Exchange on Which Registered | |

| Common Stock, $0.001 Par Value per Share | OTCQB |

Securities registered pursuant to Section 12(g) of the Exchange Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES [ ] NO [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES [ ] NO [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES [X] NO [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES [ X ] NO [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer [ ] Accelerated filer [ ] Non-accelerated filer [ ] Smaller reporting company [X]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES [ ] NO [X]

As of June 30, 2014, the aggregate market value of the registrant’s Common Stock ($0.001 par value) held by non-affiliates of the registrant was $8,139,917 based on the closing sale price as reported on the Over the Counter Marketplace system.

Number of shares of Common Stock ($0.001 par value) outstanding as of March 23, 2015: 5,544,230 shares

DOCUMENTS INCORPORATED BY REFERENCE

Items 10, 11, 12, 13, and 14 of Part III are incorporated by reference from the Registrant’s Proxy Statement for the Annual Meeting of Stockholders to be held on June 4, 2015. Such Proxy Statement will be filed within 120 days after the end of the fiscal year covered by this Annual Report on Form 10-K.

This Annual Report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements include statements forecasting our future financial condition and results, our future operating activities, market acceptance of our products, expectations for general market growth of handheld computers and other mobile computing devices, growth in demand for our barcode scanning products, expansion of the markets that we serve, expansion of the distribution channels for our products, adoption of our embedded products by third-party manufacturers of electronic devices, and the timing of the introduction and availability of new products, as well as other forecasts discussed under “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Words such as “may,” “will,” “predicts,” “anticipates,” “expects,” “intends,” “plans,” “believes,” “seeks,” “estimates,” variations of such words, and similar expressions are intended to identify such forward-looking statements. Such forward-looking statements are based on current expectations, estimates, and projections about our industry, management’s beliefs, and assumptions made by management. These forward-looking statements are not guarantees of future performance and are subject to certain risks, uncertainties, and assumptions that are difficult to predict; therefore, actual results and outcomes may differ materially from what is expressed or forecasted in any such forward looking statements. Factors that could cause actual results and outcomes to differ materially include, but are not limited to: continued weakness in the U.S. and world economy generally and in the markets we serve in particular; the risk of delays in the availability of our products due to technological, market or financial factors including the availability of product components and necessary working capital; our ability to successfully develop, introduce and market future products; our ability to effectively manage and contain our operating costs; the availability of announced third-party handheld computer hardware and software that our products are intended to work with; product delays associated with new model introductions and product changeovers by the makers of products that our products are intended to work with; continued growth in demand for handheld computers and barcode scanners; market acceptance of emerging standards such as Bluetooth® and wireless LAN and of our related connection, data collection and mobile handheld computer products; the ability of our strategic relationships to benefit our business as expected; our ability to enter into additional distribution relationships; or other factors described in this Form 10-K including “Item 1A. Risk Factors” and recent Form 8-K and Form 10-Q reports filed with the Securities and Exchange Commission. We assume no obligation to update such forward-looking statements or to update the reasons why actual results could differ materially from those anticipated in such forward-looking statements.

You should read the following discussion in conjunction with the financial statements and notes included elsewhere in this report, and other information contained in other reports and documents filed from time to time with the Securities and Exchange Commission.

The Company

We are a leading producer of mobile cordless barcode scanners for the business mobility markets. Our 2014 barcode scanner revenue grew by 40% over 2013 to $13.7 million, generating 80 percent of our 2014 revenue compared to 62 percent of our revenue in 2013. Our barcode scanner products are designed for a mobile worker using applications running on mobile devices while walking or standing. We offer easy-to-use software developer kits (SDK) to application developers which enable the integration of our barcode scanning software into mobile applications running on smartphones, tablets and mobile computers. These devices use operating systems from Apple® (iOS), Google™ (Android™) and Microsoft® (Windows®/Windows Mobile™). We focus on serving the needs of application developers as our barcode scanner sales are application driven. Once we are built into an application, our products become an ingredient of the application solution and our products are marketed by the application developer or their resellers as part of that solution. Our registered developer program for barcode scanning has grown from 700 developers at the beginning of 2014 to 1,300 developers at the beginning of 2015. Our growth in 2014 was driven by mobile point of sale applications running on Apple tablets. Registered developers are developing applications for other mobile markets including hospitality and commercial services. We offer stand-alone barcode scanning models for both 1D (imager and laser) and 2D barcode scanning in standard cases (in 5 vivid colors) and durable cases. Our 7 Series barcode scanners are designed as handheld while our 8 Series barcode scanners are designed to be attachable to smartphones, but can also be used in handheld mode. All connect cordlessly over Bluetooth with applications running on a smartphone, tablet or mobile computer.

1 |

We also offer a classic handheld mobile computer running Windows Embedded 6.5 operating system from Microsoft. Handheld computer revenue in 2014 was $3.3 million, a decline of 38 percent from revenue of $5.3 million in 2013. Handheld computer revenue has been in decline for several years reflecting the movement of developers away from Windows Embedded devices to smartphones and tablets. Service revenue in 2014 of $0.6 million comprised the balance of our 2014 revenue.

We design our own products, test and assemble product components obtained from third party contract manufacturers. We perform final product assembly, test, package, and distribute our products at and from our Newark, California facility. We offer our products worldwide through two-tier distribution enabling customers to purchase from a large number of on-line resellers around the world including some application developers. We believe growth in mobile applications and the mobile workforce are resulting from technical advances in mobile technologies, cost reductions in mobile devices and the growing adoption by businesses of mobile applications, building a growing demand for our products. Our barcode scanning products address the growing need for speed and accuracy by today’s mobile workers, thereby enhancing their productivity and allowing them to exploit time sensitive opportunities and improve customer satisfaction.

Products

Cordless barcode scanners

We offer a family of cordless barcode scanning products that connect over Bluetooth with smartphones, tablets and mobile computers running operating systems from Apple (iOS), Google (Android), and Microsoft (Windows/Windows Mobile). Our cordless barcode scanners include two dimensional (2D) and linear (1D laser and 1D imager) barcode scanners in both durable and colorful cases. Our series 7 models are lightweight and ergonomically designed as handheld barcode scanners and are widely used with tablet computers. Our series 8 models can be used as handheld or attached to a smartphone to enable one-handed barcode scanning. We also offer wearable cordless ring scanners for hands free barcode scanning. Extended warranty programs are available for all of our barcode scanning products. In 2014, our cordless barcode scanning revenue represented 80 percent of total revenue compared to 62 percent in 2013, and increased 40 percent over 2013.

2 |

Handheld Computers

We offer a family of SoMo® (“Socket® Mobile”) handheld computer products with antimicrobial cases running the Windows Embedded Handheld System 6.5 operating system. Handheld computer accessories include plug-in 1D and 2D barcode scanners, charging cradles, durable cases, and radio frequency identification (RFID) readers with NFC (near field communication). Our handheld computers are designed with wireless LAN (802.11 b/g/n) and Bluetooth connectivity for use with applications that do not require phones. Our newest family of handheld computers, SoMo Model 655, commenced sales in June 2012, replacing the SoMo650 introduced in 2007. In 2014, our handheld computer revenues were $3.3 million or 19 percent of total revenue compared to revenue of $5.3 million or 34 percent of total revenue in 2013.

Service

Our products are warranted for one year and we offer SocketCare extended warranty programs for up to three years including repair or replacement due to accidental breakage. We will also repair or replace products that are beyond their warranty period.

Registered Developers and Developer Support Programs

Barcode Scanning. We offer a barcode scanning software developer kit (SDK) to registered software application developers. Our barcode scanning SDK enables developers to easily integrate Socket’s SocketScan barcode scanning software into their applications. When integrated, the application owns the barcode scanner and controls its behavior. The SocketScan software works with smartphones, tablets and mobile computers using operating systems from Apple (iOS), Google (Android), and Microsoft (Windows and Windows Mobile).

Handheld Computers. Our SDK for the SoMo 655 handheld computer was introduced in the second half of 2012 and enables registered developers to avail themselves of features on our SoMo655 handheld computer that would not otherwise be accessible on the SoMo655 operating system, Windows Embedded 6.5.

Registered developers and developer support. Registered developers consist of third party application providers and developers developing in-house solutions for businesses. As of March 2015 we had more than 1,200 registered developers. Most of the registered developers are registered to use the barcode scanning SDK. The primary segments being addressed by barcode scanning registered developers are mobile point of sale, hospitality and commercial services. We support our registered developers with periodic software updates and assistance and solicit their feedback in considering future product improvements and direction.

General

Total employee headcount on December 31, 2014 was 50. We subcontract the manufacturing of all of our product components to independent third-party contract manufacturers located in the United States, Mexico, Taiwan and Singapore that have the equipment, know-how and capacity to manufacture products to our specifications. We assemble, test and distribute our products from our facilities in Newark, California. Our handheld computers and data collection products are sold through a worldwide network of distributors and on-line resellers, application developers, and value added resellers.

3 |

We were founded in March 1992 as Socket Communications, Inc. and reincorporated in Delaware in 1995 prior to our initial public offering in June 1995. We have financed our operations since inception primarily from the sale of equity capital or convertible debt and a receivables-based revolving line of credit with our bank. We began doing business as Socket Mobile, Inc. in January 2007 to better reflect our market focus on the mobile business market and changed our legal name to Socket Mobile, Inc. in April 2008. Our common stock trades on the OTCQB Market under the symbol “SCKT”. Our principal executive offices are located at 39700 Eureka Drive, Newark, CA 94560, and our phone number is (510) 933-3000. Our Internet home page is located at http://www.socketmobile.com; however, the information on, or that can be accessed through, our home page is not part of this Annual Report. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to such reports are available free of charge on or through our Internet home page, as soon as reasonably practical after we electronically file such material with, or furnish it to, the Securities and Exchange Commission.

Marketing Strategy and Dynamics

Capitalize on Strategic Relationships. We actively promote software application developers to integrate our products into their applications through our registered developer program. We provide easy to use software developer kits (SDK), training and technical support to our registered developers. We support the marketing activities of our registered developers in promoting the applications that include our products. Once our barcode scanning products are integrated into a developer’s application, our products become part of the application solution and are part of the marketing program for that application. We stay current on operating system updates provided by Apple, Google and Microsoft to support new products running the latest versions of their operating systems on smartphones, tablets and mobile computers while providing backward compatibility. We spend extensive engineering time and resources to ensure that our cordless barcode scanning products are compatible with a wide variety of the most popular smartphones, tablets and mobile computers running a variety of operating systems. We adhere to standards of a number of standards setting bodies whose technologies are used in our products including Bluetooth (both handheld computers and cordless barcode scanners) and wireless LAN (handheld computers).

Markets. Our growth in 2014 was driven by sales of barcode scanners integrated into retail mobile point of sale applications for use with Apple tablets. Many developers of mobile point of sale applications have been funded by venture capital enabling their rapid development and growth. Other mobile markets being addressed by registered developers include hospitality and commercial services. We expect all of these markets to increase the availability and use of mobile applications and the demand for mobile barcode scanners. Our SoMo handheld computer is used in health care, hospitality and commercial services applications.

Expand and improve our product offerings. We offer a wide range of products that enable application developers and their customers to design their mobile systems to meet their specific requirements, and we encourage our distributors to support the full range of our products. The goal is for customers to view Socket as a primary source for their mobile barcode scanning needs. Within our family of barcode scanning products, we offer durable and standard cases (the latter in multiple colors), linear imaging and laser barcode scanning, 2D barcode scanning, and two form factors: an ergonomically designed handheld cordless barcode scanner (our model 7 series) and a smartphone attachable barcode scanner (our model 8 series) to enable one-handed barcode scanning. Both series 7 and series 8 products connect cordlessly over Bluetooth and may be used as handheld barcode scanners. We design our products to comply with the regulations of the many worldwide agencies that regulate the safety, performance and use of electronic products. For the SoMo family of handheld computers, we’ve upgraded the operating system and management software, adding many operating system features such as multiple language support, upgraded to later versions of the Windows (Mobile) embedded handheld operating system, and upgraded our Bluetooth and wireless LAN management software.

4 |

Price our products competitively and available worldwide. We have designed our products to be priced competitively although we are subject from time to time to changes in component pricing by our suppliers. We update our products from time to time and work with our vendors to achieve reductions in component pricing. We distribute our products through a worldwide distribution network that places products into geographic regions to shorten purchasing times and provides a credit shield to us. Our largest distributors are Ingram Micro®, ScanSource® and BlueStar, and they support a worldwide network of on-line resellers including Amazon®.com, CDW® and Barcodes, Inc.

Build a Strong Brand Name. We believe that our products make a difference in the daily work life of mobile workers and the people they serve. We are building a brand image focused on business mobility. This image closely associates us with business mobility solutions and to reflect this image, we began doing business as Socket Mobile, Inc. in January 2007 and changed our legal name to Socket Mobile, Inc. in April 2008. We stress with customers the design of our products for the markets they address, emphasizing quality and standards-based connectivity. Mobility requires products that are compact and designed to be handled while mobile, with low power consumption to extend time between charges, and easy to use. We strive to offer high performance products in a wide range of competitive prices. Through our developer support program, we work closely with application developers developing productivity enhancing applications for the mobile workforce. Our overall company brand identity and positioning goal is to be a leading provider of easy-to-deploy business mobility systems to the business mobility market.

Competition and Competitive Risks

The overall market for mobile handheld computing solutions is both complex and competitive. Our barcode scanning hardware products compete with similar hardware products in all of our markets in the United States, Europe and Asia and we differentiate our products with our SocketScan software and software developer kits (SDK). Our longtime focus on creating innovative mobile solutions for the mobile workforce has resulted in good brand name recognition and reputation. We believe that our brand name identifies our products as durable, dependable, small form factor, low power and easy to use, all features designed for a mobile worker while mobile, and the breadth of our product offerings, including the extensive features of our software and software developer kits (SDK), will continue to differentiate us relative to our competitors.

5 |

Cordless Barcode Scanning. We offer a full range of handheld cordless barcode scanners connecting to smartphones, tablets and other computing devices over Bluetooth. Our SocketScan Software Developer Kit (SDK) enables registered third party application developers to integrate the features of our SocketScan software into their applications and helps differentiate our products. We face competition from products similar to our cordless hand scanners from Koamtec, Code Corporation, and Opticon (Japan). Barcodes may also be scanned using the built-in camera in smartphones or tablets with the applications like Scanit or Manatee Works. However, scanning using the built-in camera is typically slower and more awkward especially as the devices get larger. Users may choose a barcode scanner that connects directly to an Apple tablet, iPhone or computer such as offered by Infinite Peripherals and Honeywell. Users also may choose more rugged barcode scanners as an alternative, some of which are integrated into computing devices from manufacturers such as Datalogic, Honeywell®, and Zebra Technologies. Many of these devices are not Apple certified. Many connect to Apple devices over Bluetooth in keyboard emulation mode, and do not offer extensive tools for software developers such as our software developer kit (SDK) to integrate features of our sophisticated barcode scanning software SocketScan into barcode scanning applications.

Handheld Computers. A number of larger, well financed companies manufacture handheld mobile computers. Most of the manufacturers offer only ruggedized systems that are higher priced and larger than our devices but are capable of running the same applications. Many of these systems have built in barcode scanners, are larger, heavier and more expensive, so do not directly compete with our products but are an alternative. These companies include Datalogic, Honeywell®, and Zebra Technologies. Consumer grade products (durable rather than rugged) also provide competitive alternatives to our products. These companies include Bluebird (selling under the brand name Pidion), Unitek and Janam and some of their products include integrated barcode scanners.

Our SoMo655 handheld computer’s operating system is Windows Embedded Handheld 6.5. Microsoft recently announced it would continue to support version 6.5 until 2020 which was designed to assure users of products running this version of a long period of continued support. Microsoft also announced Windows Mobile 8 Embedded, a superset of their phone operating systems for devices having phones and integrated barcode scanners. Windows Mobile 8 Embedded does not apply to our category of handheld computer which has neither a phone nor an integrated barcode scanner as our customers typically operate over wireless LAN and Bluetooth connections within the walls of their organization and do not require a phone. We do not directly compete with devices running Windows Mobile 8 Embedded but they can become competitive alternatives where a phone and an integrated scanner are needed.

Sales of our handheld computer family of products, the SoMo650, introduced in 2007 and replaced in 2012 with the SoMo655, are designed as a close replacement for classic PDAs such as the Hewlett-Packard Series 200 family of handheld computer products that were discontinued by Hewlett-Packard in 2011. We have enhanced our product offerings with a software developer kit (SDK) that enables registered developers to avail themselves of features on our SoMo655 handheld computer that would not otherwise be accessible under the Windows Embedded 6.5 operating system. Sales of handheld mobile computers have been in decline over the past several years as many application developers have been developing mobile applications for smartphones and tablets running Apple (iOS) and Google (Android) operating systems. More than 80,000 SoMo handheld computers have been sold since 2007.

6 |

Proprietary Technology and Intellectual Property

We have been granted 31 U.S. patents and 10 design patents and have other patent applications under review.. We have registered trademarks with the U.S. Patent and Trademark Office for the mark “Socket”, our logo, the terms “Go-WiFi” and “Battery Friendly” and “SoMo”, the mark associated with our mobile handheld computers.

We have developed a number of technological building blocks that enhance our ability to design new hardware and software products, to offer products which run on multiple software and hardware platforms, and to manufacture and package products efficiently.

We own and control the design of our barcode scanners and our SoMo handheld computer, enabling us to modify its features or software to meet specific customer requirements.

Building on our expertise in embedded radio-dependent firmware, within our Bluetooth cordless products are software and firmware that include a wide variety of functions to enable efficient radio control and overall systems functionality. For cordless barcode scanning this includes our patented Error Proof Protocol, which is designed to ensure that scanned data is correctly received by the mobile computing device and allows for real-time validation of data and error notification to the user. We have developed SocketScan barcode scanning software that allows our products to communicate with applications on smartphones and tablets running operating systems from Apple (iOS), Google (Android), and Microsoft (Windows and Windows Mobile).

We have developed a number of software programs that provide unique functions and features for our cordless barcode scanning and handheld computer products. For example, our SocketScan software enables all of our barcode scanning products to scan a variety of barcodes and to route the scanned data to many different types of data files on a number of operating systems used in mobile devices. Our Bluetooth software used in conjunction with our Bluetooth hardware provides a completely functional Bluetooth solution enabling connections and data transfers between Bluetooth-enabled devices. Our wireless local area network software called Enhanced Wi-Fi Companion included with our handheld computers provides an extensive set of features to help the user get and stay connected. This software program used in conjunction with our handheld computers provides a completely functional wireless local area network solution enabling connections and data transfers from and to our mobile computers over wireless local area networks. In addition, our Bluetooth and wireless LAN software programs are aligned to insure optimal performance even when both technologies are being utilized at the same time.

We rely on a combination of patent, copyright, trademark and trade secret laws, and confidentiality procedures to protect our proprietary rights. As part of our confidentiality procedures, we generally enter into non-disclosure agreements with our employees, distributors and strategic partners, and limit access to our software, documentation and other proprietary information. Despite these precautions, it may be possible for a third-party to copy or otherwise obtain and use our products or technology without authorization, or to develop similar technology independently. In addition, we may not be able to effectively protect our intellectual property rights in certain foreign countries. From time to time we receive communications from third parties asserting that our products infringe, or may infringe, their proprietary rights. In connection with any such claims, litigation could be brought against us that could result in significant additional expense or compel us to discontinue or redesign some of our products.

7 |

Personnel

Our future success will depend in significant part upon the continued service of certain of our key technical and senior management personnel, and our continuing ability to attract, assimilate and retain highly qualified technical, managerial and sales and marketing personnel. Our total employee headcount as of December 31, 2014 was 50. Our employees are not represented by a union, and we consider our employee relationships to be good. As of December 31, 2014, we had 15 persons in sales, marketing and customer service, 9 persons in development engineering, 8 persons in finance and administration, and 18 persons in operations.

Our ability to continue as a going concern is dependent upon our ability to maintain ongoing profitable operations and to increase our capital.

Our historical operating losses and declines in our working capital balances are conditions that raise substantial doubt about our ability to continue as a going concern. Our ability to continue as a going concern is dependent upon our ability to maintain ongoing profitable operations and to increase our capital as needed. We have been taking steps intended to improve operating results and achieve future profitability including the introduction of new products, continued close support of our distributors and of our application partners as they establish their mobile applications in key vertical markets, and management of our costs. Our operations in 2014 were profitable and we increased our capital during the year by $895,000. We believe that we will be able to continue to improve our liquidity and secure additional sources of financing by managing our working capital balances, use of our bank lines of credit, and raising additional capital as needed including the exercising of warrants and stock options and the issuance of additional equity securities. Nonetheless, there can be no assurance that we will be successful in achieving any of these steps, and there can be no assurance that additional financing will be available on acceptable terms, if at all, and any such terms may be dilutive to existing stockholders. Our inability to secure and maintain the necessary liquidity would have a material adverse effect on our financial condition and results of operations. Our financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classification of assets and liabilities that may result from our inability to continue as a going concern.

We have a history of operating losses and may not maintain ongoing profitability.

We were profitable in 2014. However, except for fiscal years 2014 and 2004, we incurred significant operating losses in each financial period since our inception. To maintain ongoing profitability, we must accomplish numerous objectives, including continued growth in our business, ongoing support to registered developers whose applications support the use of our barcode scanning products, and the development of successful new products. We cannot foresee with any certainty whether we will be able to achieve these objectives in the future. Accordingly, we may not generate sufficient net revenue or manage our expenses sufficiently to maintain ongoing profitability. If we cannot maintain ongoing profitability, we will not be able to support our operations from positive cash flows, and we would use our existing cash to support operating losses. If we are unable to secure the necessary capital to replace that cash, we may need to suspend some or all of our current operations.

8 |

We may require additional capital in the future, but that capital may not be available on reasonable terms, if at all, or on terms that would not cause substantial dilution to your stock holdings.

We may incur operating losses in future quarters and would need to raise capital to fund such losses. Our forecasts are highly dependent on factors beyond our control, including market acceptance of our products and delays in deployments by businesses of applications that use our

handheld computers and our data collection products. Even if we maintain profitable operating levels, we may need to raise capital to provide sufficient working capital to fund our growth. If capital requirements vary materially from those currently planned, we may require additional capital sooner than expected. There can be no assurance that such capital will be available in sufficient amounts or on terms acceptable to us, if at all.

If application developers are not successful in their efforts to develop, market and sell their applications into which our software and products are incorporated, we may not achieve our sales projections.

We are dependent upon application developers to integrate our scanning and software products into their applications designed for mobile workers using smartphones, tablets and mobile computers, and to successfully market and sell those application products and solutions into the marketplace. We focus on serving the needs of application developers as sales of our barcode scanners are application driven. However, these developers may take considerable time to complete development of their applications, may experience delays in their development timelines, may develop competing applications, may be unsuccessful in marketing and selling their application products and solutions to customers, or may experience delays in customer deployments and implementations, which would adversely affect our ability to achieve our revenue projections.

Global economic conditions may continue to have a negative impact on our business and financial condition in ways that we currently cannot predict, and may further limit our ability to raise additional funds.

Continued tight credit and related strains in the global financial system, particularly in Europe and Asia, may continue to have an impact on our business and our financial condition. We may face significant challenges if economic conditions and conditions in the financial markets do not improve or continue to worsen. In particular, should these conditions cause our revenues to be materially less than forecast, we may find it necessary to initiate further reductions in our expenses and defer product development programs. In addition, our ability to access the capital markets and raise funds required for our operations may be severely restricted at a time when we would like, or need, to do so, which could have an adverse effect on our ability to meet our current and future funding requirements and on our flexibility to react to changing economic and business conditions.

9 |

Our quarterly operating results may fluctuate in future periods, which could cause our stock price to decline.

We expect to experience quarterly fluctuations in operating results in the future. We generally ship orders as received, and as a result we may have little backlog. Quarterly revenues and operating results therefore depend on the volume and timing of orders received during the quarter, which are difficult to forecast. Historically, we have often recognized a substantial portion of our revenue in the last month of the quarter. This subjects us to the risk that even modest delays in orders or in the manufacture of products relating to orders received, may adversely affect our quarterly operating results. Our operating results may also fluctuate due to factors such as:

| • | the demand for our products; |

| • | the size and timing of customer orders; |

| • | unanticipated delays or problems in our introduction of new products and product enhancements; |

| • | the introduction of new products and product enhancements by our competitors; |

| • | the timing of the introduction and deployments of new applications that work with our products; |

| • | changes in the revenues attributable to royalties and engineering development services; |

| • | product mix; |

| • | timing of software enhancements; |

| • | changes in the level of operating expenses; |

| • | competitive conditions in the industry including competitive pressures resulting in lower average selling prices; |

| • | timing of distributors’ shipments to their customers; |

| • | delays in supplies of key components used in the manufacturing of our products, and |

| • | general economic conditions and conditions specific to our customers’ industries. |

Because we base our staffing and other operating expenses on anticipated revenues, unanticipated declines or delays in the receipt of orders can cause significant variations in operating results from quarter to quarter. As a result of any of the foregoing factors, or a combination, our results of operations in any given quarter may be below the expectations of public market analysts or investors, in which case the market price of our common stock would be adversely affected.

In order to maintain the availability of our bank lines of credit we must remain in compliance with the covenants as specified under the terms of the credit agreements and the bank may exercise discretion in making advances to us.

Our credit agreements with our bank requires us to maintain cash and qualified receivables that are at least two times amounts borrowed and outstanding under the credit agreements. The agreements contain customary representations, warranties, covenants and events of default that limit our ability to incur additional liens or indebtedness, make distributions to our stockholders and make investments. The events of default entitle our bank to accelerate our obligations and require repayment of our outstanding indebtedness thereunder. These events of default include a breach of our payment obligations or covenants, a material impairment in our financial condition or ability to repay any indebtedness to our bank and the commencement of dissolution or insolvency proceedings. The agreement may be terminated by us or by our bank at any time. Upon such termination, our bank would no longer make advances under the credit agreement and outstanding advances would be repaid as receivables are collected. All advances are at our bank’s discretion and our bank is not obligated to make advances. Our bank has been granted a first priority security interest in all of our assets, including our intellectual property.

10 |

Goodwill comprises a significant portion of our assets and may be subject to impairment write-downs in future periods which would substantially increase our losses, make it more difficult to achieve profitability, and could cause our stock price to decline.

We review our goodwill for impairment at least annually as of September 30th, and more often if factors suggest potential impairment. Many factors are considered in evaluating goodwill including our market capitalization, comparable companies within our industry, our estimates of our future performance, and discounted cash flow analysis. Many of these factors are highly subjective and may be negatively impacted by our financial results and market conditions in the future. We may incur goodwill impairment charges in the future and any future write-downs of our goodwill would adversely affect our operating results, make it more difficult to maintain profitability, and as a result the market price of our common stock could be adversely affected.

We may be unable to manufacture our products, because we are dependent on a limited number of qualified suppliers for our components.

Several of our component parts, including our barcode scanning modules, and our line of mobile handheld computers, are produced by one or a limited number of suppliers. Shortages or delays could occur in these essential components due to an interruption of supply or increased demand in the industry. Suppliers may choose to restrict credit terms or require advance payment causing delays in the procurement of essential materials. If we are unable to procure certain component parts, we could be required to reduce our operations while we seek alternative sources for these components, which could have a material adverse effect on our financial results. To the extent that we acquire extra inventory stocks to protect against possible shortages, we would be exposed to additional risks associated with holding inventory, such as obsolescence, excess quantities, or loss.

If application developers are not successful in their efforts to develop, market, and sell their applications into which our software and products are incorporated, we may not achieve our sales projections.

We are dependent upon application developers to integrate our scanning software and scanning products into their applications designed for mobile workers using smartphones, tablets and mobile computers, and to successfully market and sell those application products and solutions into the marketplace. We focus on serving the needs of application developers as sales of our barcode scanners are application driven. However, these developers may take considerable time to complete development of their applications, may experience delays in their development timelines, may develop applications that support competitive alternatives to our barcode scanners, may be unsuccessful in marketing and selling their application products and solutions to customers, or may experience delays in customer deployments and implementations, which would adversely affect our ability to achieve our revenue projections.

11 |

If we fail to develop and introduce new products rapidly and successfully, we will not be able to compete effectively, and our ability to generate sufficient revenues will be negatively affected.

The market for our products is prone to rapidly changing technology, evolving industry standards and short product life cycles. If we are unsuccessful at developing and introducing new products and services on a timely basis that include the latest technologies conform to the newest standards and that are appealing to end users, we will not be able to compete effectively, and our ability to generate significant revenues will be seriously harmed.

The development of new products and services can be very difficult and requires high levels of innovation. The development process is also lengthy and costly. Short product life cycles for smartphones and tablets expose our products to the risk of obsolescence and require frequent new product upgrades and introductions. We will be unable to introduce new products and services into the market on a timely basis and compete successfully, if we fail to:

| • | invest significant resources in research and development, sales and marketing, and customer support; |

| • | identify emerging trends, demands and standards in the field of mobile computing products; |

| • | enhance our products by adding additional features; |

| • | maintain superior or competitive performance in our products; and |

| • | anticipate our end users’ needs and technological trends accurately. |

We cannot be sure that we will have sufficient resources to make adequate investments in research and development or that we will be able to identify trends or make the technological advances necessary to be competitive.

A significant portion of our revenue currently comes from a limited number of distributors, and any decrease in revenue from these distributors could harm our business.

A significant portion of our revenue comes from a limited number of distributors. In fiscal years 2014 and 2013, Ingram Micro Inc., ScanSource, Inc., and BlueStar, Inc. together represented approximately 67% and 55%, respectively, of our worldwide revenues. We expect that a significant portion of our revenue will continue to depend on sales to a limited number of distributors. We do not have long-term commitments from our distributors to carry our products, and any of our distributors may from quarter to quarter comprise a significant concentration of our revenues. Any could choose to stop selling some or all of our products at any time, and each of these companies also carries our competitors’ products. If we lose our relationship with any of our significant distributors, we would experience disruption and delays in marketing our products.

We may not be able to collect revenues from customers who experience financial difficulties.

Our accounts receivable are derived primarily from distributors. We perform ongoing credit evaluations of our customers’ financial conditions but generally require no collateral from our customers. Reserves are maintained for potential credit losses, and such losses have historically been within such reserves. However, many of our customers may be thinly capitalized and may be prone to failure in adverse market conditions. Although our collection history has been good, from time to time a customer may not pay us because of financial difficulty, bankruptcy or liquidation. Current global financial conditions may have an impact on our customers’ ability to pay us in a timely manner, and consequently, we may experience increased difficulty in collecting our accounts receivable, and we may have to increase our reserves in anticipation of increased uncollectible accounts.

12 |

We could face increased competition in the future, which would adversely affect our financial performance.

The market for mobile handheld computers in which we operate is very competitive. Our future financial performance is contingent on a number of unpredictable factors, including that:

| • | some of our competitors have greater financial, marketing, and technical resources than we do; |

| • | we periodically face intense price competition, particularly when our competitors have excess inventories and discount their prices to clear their inventories; and |

| • | certain manufacturers of tablets, mobile phones and handheld computers offer products with built-in functions, such as Bluetooth wireless technology, Wi-Fi, or barcode scanning, that compete with our products. |

Increased competition could result in price reductions, fewer customer orders, reduced margins, and loss of market share. Our failure to compete successfully against current or future competitors could harm our business, operating results and financial condition.

If we do not correctly anticipate demand for our products, our operating results will suffer.

The demand for our products depends on many factors and is difficult to forecast. We expect that it will become more difficult to forecast demand given current economic conditions as we introduce and support more products, and as competition in the markets for our products intensifies. If demand is lower than forecasted levels, we could have excess production resulting in higher inventories of finished products and components, which could lead to write-downs or write-offs of some or all of the excess inventories, and reductions in our cash balances. Lower than forecasted demand could also result in excess manufacturing capacity at our third-party manufacturers and in our failure to meet minimum purchase commitments, each of which may lower our operating results.

If demand increases beyond forecasted levels, we would have to rapidly increase production at our third-party manufacturers. We depend on suppliers to provide additional volumes of components, and suppliers might not be able to increase production rapidly enough to meet unexpected demand. Even if we were able to procure enough components, our third-party manufacturers might not be able to produce enough of our devices to meet our customer demand. In addition, rapid increases in production levels to meet unanticipated demand could result in higher costs for manufacturing and supply of components and other expenses. These higher costs could lower our profit margins. Further, if production is increased rapidly, manufacturing yields could decline, which may also lower operating results.

13 |

We rely primarily on distributors, resellers, and vertical industry partners to sell our products, and our sales would suffer if any of these third-parties stops selling our products effectively.

Because we sell our products primarily through distributors, resellers, and vertical industry partners, we are subject to risks associated with channel distribution, such as risks related to their inventory levels and support for our products. Our distribution channels may build up inventories in anticipation of growth in their sales. If such growth in their sales does not occur as anticipated, the inventory build-up could contribute to higher levels of product returns. The lack of sales by any one significant participant in our distribution channels could result in excess inventories and adversely affect our operating results and working capital liquidity.

Our agreements with distributors, resellers, and vertical industry partners are generally nonexclusive and may be terminated on short notice by them without cause. Our distributors, resellers, and vertical industry partners are not within our control, are not obligated to purchase products from us, and may offer competitive lines of products simultaneously. Sales growth is contingent in part on our ability to enter into additional distribution relationships and expand our sales channels. We cannot predict whether we will be successful in establishing new distribution relationships, expanding our sales channels or maintaining our existing relationships. A failure to enter into new distribution relationships or to expand our sales channels could adversely impact our ability to grow our sales.

We allow our distribution channels to return a portion of their inventory to us for full credit against other purchases. In addition, in the event we reduce our prices, we credit our distributors for the difference between the purchase price of products remaining in their inventory and our reduced price for such products. Actual returns and price protection may adversely affect future operating results and working capital liquidity by reducing our accounts receivable and increasing our inventory balances, particularly since we seek to continually introduce new and enhanced products and are likely to face increasing price competition.

We depend on alliances and other business relationships with a small number of third-parties, and a disruption in any one of these relationships would hinder our ability to develop and sell our products.

We depend on strategic alliances and business relationships with leading participants in various segments of the mobile applications and mobile handheld computer markets to help us develop and market our products. Our strategic partners may revoke their commitment to our products or services at any time in the future or may develop their own competitive products or services. Accordingly, our strategic relationships may not result in sustained business alliances, successful product or service offerings, or the generation of significant revenues. Failure of one or more of such alliances could result in delay or termination of product development projects, failure to win new customers, or loss of confidence by current or potential customers.

We have devoted significant research and development resources to design products to work with a number of operating systems used in mobile devices including Windows Mobile, Windows CE, Windows 7/Vista/XP, Windows Embedded Handheld, Apple iOS, Google’s Android and to develop our own family of mobile handheld computers. Such design activities have diverted financial and personnel resources from other development projects. These design activities are not undertaken pursuant to any agreement under which Microsoft, Apple, or Google is obligated to collaborate or to support the products produced from such collaboration. Consequently, these organizations may terminate their collaborations with us for a variety of reasons, including our failure to meet agreed-upon standards or for reasons beyond our control, such as changing market conditions, increased competition, discontinued product lines, and product obsolescence.

14 |

Our intellectual property and proprietary rights may be insufficient to protect our competitive position.

Our business depends on our ability to protect our intellectual property. We rely primarily on patent, copyright, trademark, trade secret laws, and other restrictions on disclosure to protect our proprietary technologies. We cannot be sure that these measures will provide meaningful protection for our proprietary technologies and processes. We cannot be sure that any patent issued to us will be sufficient to protect our technology. The failure of any patents to provide protection to our technology would make it easier for our competitors to offer similar products. In connection with our participation in the development of various industry standards, we may be required to license certain of our patents to other parties, including our competitors that develop products based upon the adopted standards.

We also generally enter into confidentiality agreements with our employees, distributors, and strategic partners, and generally control access to our documentation and other proprietary information. Despite these precautions, it may be possible for a third-party to copy or otherwise obtain and use our products, services, or technology without authorization, develop similar technology independently, or design around our patents.

Effective copyright, trademark, and trade secret protection may be unavailable or limited in certain foreign countries.

We may become subject to claims of intellectual property rights infringement, which could result in substantial liability.

In the course of operating our business, we may receive claims of intellectual property infringement or otherwise become aware of potentially relevant patents or other intellectual property rights held by other parties. Many of our competitors have large intellectual property portfolios, including patents that may cover technologies that are relevant to our business. In addition, many smaller companies, universities, and individuals have obtained or applied for patents in areas of technology that may relate to our business. The industry is moving towards aggressive assertion, licensing, and litigation of patents and other intellectual property rights.

If we are unable to obtain and maintain licenses on favorable terms for intellectual property rights required for the manufacture, sale, and use of our products, particularly those products which must comply with industry standard protocols and specifications to be commercially viable, our results of operations or financial condition could be adversely impacted.

15 |

In addition to disputes relating to the validity or alleged infringement of other parties’ rights, we may become involved in disputes relating to our assertion of our own intellectual property rights. Whether we are defending the assertion of intellectual property rights against us or asserting our intellectual property rights against others, intellectual property litigation can be complex, costly, protracted, and highly disruptive to business operations by diverting the attention and energies of management and key technical personnel. Plaintiffs in intellectual property cases often seek injunctive relief, and the measures of damages in intellectual property litigation are complex and often subjective or uncertain. Thus, any adverse determinations in this type of litigation could subject us to significant liabilities and costs.

New industry standards may require us to redesign our products, which could substantially increase our operating expenses.

Standards for the form and functionality of our products are established by standards committees. These independent committees establish standards, which evolve and change over time, for different categories of our products. We must continue to identify and ensure compliance with evolving industry standards so that our products are interoperable and we remain competitive. Unanticipated changes in industry standards could render our products incompatible with products developed by major hardware manufacturers and software developers. Should any major changes, even if anticipated, occur, we would be required to invest significant time and resources to redesign our products to ensure compliance with relevant standards. If our products are not in compliance with prevailing industry standards for a significant period of time, we would miss opportunities to sell our products for use with new hardware components from mobile computer manufacturers and OEMs, thus affecting our business.

Undetected flaws and defects in our products may disrupt product sales and result in expensive and time-consuming remedial action.

Our hardware and software products may contain undetected flaws, which may not be discovered until customers have used the products. From time to time, we may temporarily suspend or delay shipments or divert development resources from other projects to correct a particular product deficiency. Efforts to identify and correct errors and make design changes may be expensive and time consuming. Failure to discover product deficiencies in the future could delay product introductions or shipments, require us to recall previously shipped products to make design modifications, or cause unfavorable publicity, any of which could adversely affect our business and operating results.

The loss of one or more of our senior personnel could harm our existing business.

A number of our officers and senior managers have been employed for nineteen to twenty-one years by us, including our President, Chief Financial Officer, Vice President of Operations and Vice President of Engineering/Chief Technical Officer. Our future success will depend upon the continued service of key officers and senior managers. Competition for officers and senior managers is intense, and there can be no assurance that we will be able to retain our existing senior personnel. The loss of one or more of our officers or key senior managers could adversely affect our ability to compete.

The expensing of options will continue to reduce our operating results such that we may find it necessary to change our business practices to attract and retain employees.

Historically, we have used stock options as a key component of our employee compensation packages. We believe that stock options provide an incentive to our employees to maximize long-term stockholder value and, through the use of vesting, encourage valued employees to remain with us. The expensing of employee stock options adversely affects our net income and earnings per share, will continue to adversely affect future quarters, and will make profitability harder to achieve. In addition, we may decide in response to the effects of expensing stock options on our operating results to reduce the number of stock options granted to employees or to grant options to fewer employees. This could adversely affect our ability to retain existing employees and attract qualified candidates, and also could increase the cash compensation we would have to pay to them.

16 |

If we are unable to attract and retain highly skilled sales and marketing and product development personnel, our ability to develop and market new products and product enhancements will be adversely affected.

We believe our ability to achieve increased revenues and to develop successful new products and product enhancements will depend in part upon our ability to attract and retain highly skilled sales and marketing and product development personnel. Our products involve a number of new and evolving technologies, and we frequently need to apply these technologies to the unique requirements of mobile products. Our personnel must be familiar with both the technologies we support and the unique requirements of the products to which our products connect. Competition for such personnel is intense, and we may not be able to attract and retain such key personnel. In addition, our ability to hire and retain such key personnel will depend upon our ability to raise capital or achieve increased revenue levels to fund the costs associated with such key personnel. Failure to attract and retain such key personnel will adversely affect our ability to develop and market new products and product enhancements.

Our operating results could be harmed by economic, political, regulatory and other risks associated with export sales.

Export sales (sales to customers outside the United States) accounted for approximately 25% and 30% of our revenue in fiscal years 2014 and 2013, respectively. Accordingly, our operating results are subject to the risks inherent in export sales, including:

| • | longer payment cycles; |

| • | unexpected changes in regulatory requirements, import and export restrictions and tariffs; |

| • | difficulties in managing foreign operations; |

| • | the burdens of complying with a variety of foreign laws; |

| • | greater difficulty or delay in accounts receivable collection; |

| • | potentially adverse tax consequences; and |

| • | political and economic instability. |

Our export sales are primarily denominated in United States dollars and in Euros for our sales to European distributors. Accordingly, an increase in the value of the United States dollar relative to foreign currencies could make our products more expensive and therefore potentially less competitive in foreign markets. Declines in the value of the Euro relative to the United States dollar may result in foreign currency losses relating to collection of Euro denominated receivables if left unhedged. Furthermore, the recent economic instability of the Eurozone could have an adverse effect on our business, including the ability of our distributors to sell our products and our ability the collect the related Euro receivables.

17 |

Our operations are vulnerable to interruption by fire, earthquake, power loss, telecommunications failure, and other events beyond our control.

Our corporate headquarters is located near an earthquake fault. The potential impact of a major earthquake on our facilities, infrastructure, and overall business is unknown. Additionally, we may experience electrical power blackouts or natural disasters that could interrupt our business. Should a disaster be widespread, such as a major earthquake, or result in the loss of key personnel, we may not be able to implement our disaster recovery plan in a timely manner. Any losses or damages incurred by us as a result of these events could have a material adverse effect on our business.

Failure to maintain effective internal controls could have a material adverse effect on our business, operating results and stock price.

We have evaluated and will continue to evaluate our internal control procedures in order to satisfy the requirements of Section 404 of the Sarbanes-Oxley Act, which requires an annual management assessment of the design and effectiveness of our internal control over financial reporting. If we fail to maintain the adequacy of our internal controls, as such standards are modified, supplemented or amended from time to time, we may not be able to ensure that we can conclude on an ongoing basis that we have effective internal control over financial reporting in accordance with Section 404 of the Sarbanes-Oxley Act. Moreover, effective internal controls, particularly those related to revenue recognition, are necessary for us to produce reliable financial reports and are important to helping prevent financial fraud. If we cannot provide reliable financial reports or prevent fraud, our business and operating results could be harmed, investors could lose confidence in our reported financial information, and the trading price of our stock could drop significantly.

The sale of a substantial number of shares of our common stock could cause the market price of our common stock to decline.

Sales of a substantial number of shares of our common stock in the public market could adversely affect the market price for our common stock. The market price of our common stock could also decline if one or more of our significant stockholders decided for any reason to sell substantial amounts of our common stock in the public market.

As of March 23, 2015, we had 5,544,230 shares of common stock outstanding. Substantially all of these shares are freely tradable in the public market, either without restriction or subject, in some cases, only to S-3 prospectus delivery requirements and, in other cases, only to manner of sale, volume, and notice requirements of Rule 144 under the Securities Act.

As of March 23, 2015, we had 2,032,488 shares of common stock subject to outstanding options under our stock option plans, and 195,676 shares of common stock were available for future issuance under the plans. We have registered the shares of common stock subject to outstanding options and reserved for issuance under our stock option plans. Accordingly, the shares of common stock underlying vested options will be eligible for resale in the public market as soon as the options are exercised.

18 |

As of March 23, 2015, we had 169,335 shares of common stock subject to outstanding warrants issued in our 2009 private placement and in connection with a convertible note financing in November 2010. We have registered the resale of all shares of common stock subject to the warrants. Accordingly, the shares of common stock underlying these warrants will be eligible for resale in the public market as soon as the warrants are exercised, subject only to S-3 prospectus delivery requirements.

As of March 23, 2015, we had $752,625 in subordinated convertible notes payable. Up to 977,398 shares of common stock could be issued for conversion of the notes plus all accrued interest thru the maturity date of September 4, 2017.

Volatility in the trading price of our Common Stock could negatively impact the price of our Common Stock.

During the period from January 1, 2014 through March 23, 2015, our common stock price fluctuated between a high of $3.19 and a low of $0.70. On July 30, 2012, our common stock was delisted from the Nasdaq market and began trading on the Over-the-Counter Marketplace due to our equity balances falling below the minimum threshold required for continued Nasdaq listing. We have experienced low trading volumes in our stock, and thus relatively small purchases and sales can have a significant effect on our stock price. The trading price of our common stock could be subject to wide fluctuations in response to many factors, some of which are beyond our control, including general economic conditions and the outlook of securities analysts and investors on our industry. In addition, the stock markets in general, and the markets for high technology stocks in particular, have experienced high volatility that has often been unrelated to the operating performance of particular companies. These broad market fluctuations may adversely affect the trading price of our common stock.

Item 1B. Unresolved Staff Comments

None.

We lease a 37,100 square foot office facility in Newark, California under a lease expiring in June 2022. This facility houses our headquarters and manufacturing operations, and is used by all segments of the Company. We believe that our current facilities are sufficient and adequate to meet our needs for the foreseeable future.

We are currently not a party to any material legal proceedings.

Item 4. Mine Safety Disclosures

Not applicable.

19 |

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Common Stock

The Company’s common stock is traded on the OTCQB Marketplace under the symbol “SCKT.”

The quarterly high and low sales prices of our common stock, as reported on the OTCQB Marketplace through March 23, 2015 and for the last two fiscal years are as shown below:

Common Stock | ||||||||||

Quarter Ended | High | Low | ||||||||

| 2013 | ||||||||||

| March 31, 2013 | $ | 1.89 | $ | 0.70 | ||||||

| June 30, 2013 | $ | 2.20 | $ | 0.92 | ||||||

| September 30, 2013 | $ | 1.98 | $ | 1.12 | ||||||

| December 31, 2013 | $ | 1.45 | $ | 0.70 | ||||||

| 2014 | ||||||||||

| March 31, 2014 | $ | 1.14 | $ | 0.70 | ||||||

| June 30, 2014 | $ | 1.91 | $ | 0.85 | ||||||

| September 30, 2014 | $ | 2.74 | $ | 1.40 | ||||||

| December 31, 2014 | $ | 2.75 | $ | 1.95 | ||||||

| 2015 | ||||||||||

| March 31, 2015 (through March 23, 2015) | $ | 3.19 | $ | 2.00 | ||||||

On March 23, 2015, the closing sales price for our common stock as reported on the OTCQB Marketplace was $2.10. We had approximately 3,400 beneficial stockholders of record as of March 23, 2015. We have not paid dividends on our common stock, and we currrently intend to retain future earnings for use in our business and do not anticipate paying dividends in the foreseeable future.

The information required by this item regarding equity compensation plans is incorporated by reference to the information set forth in Item 12 of this Annual Report on Form 10-K.

20 |

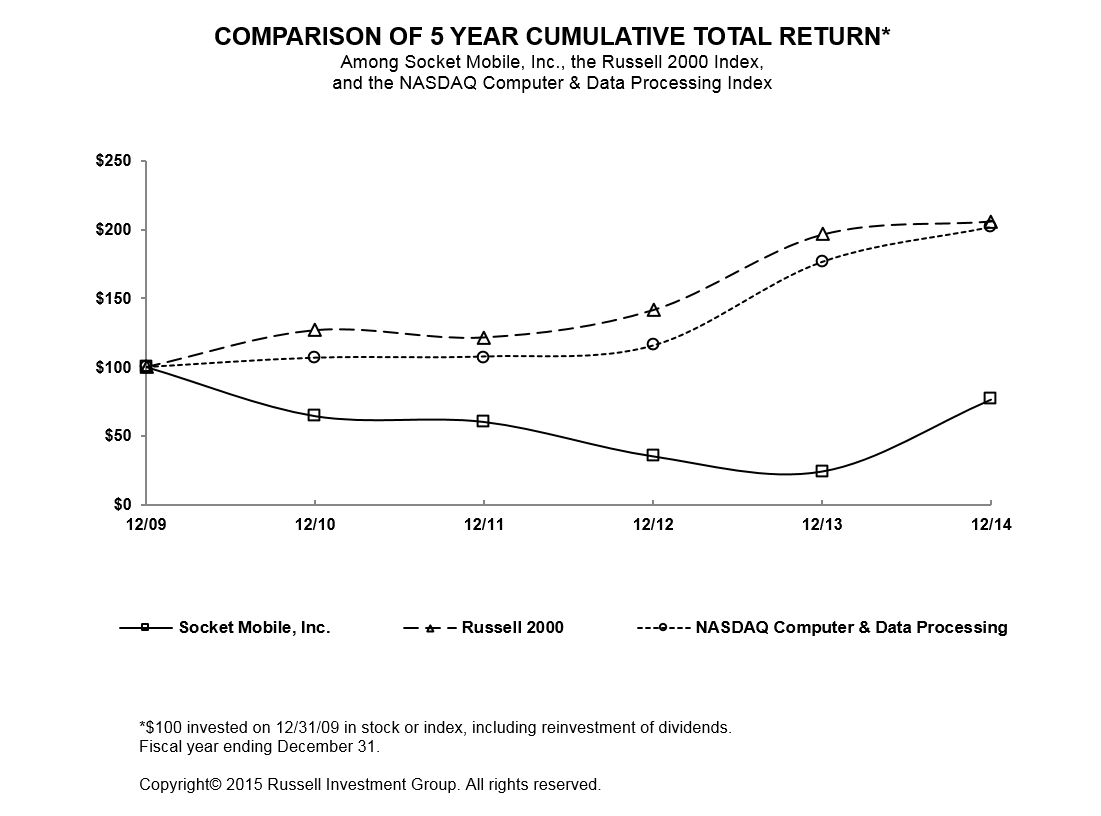

Performance Graph

The performance graph shown below shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended, or otherwise subject to the liabilities under that section, and shall not be deemed to be incorporated by reference into any filing of Socket Mobile, Inc. under the Securities Act of 1933, as amended, or the Exchange Act. The performance graph below shows a five-year comparison of cumulative total stockholder return, calculated on a dividend reinvestment basis and based on a $100 investment, from December 31, 2008 through December 31, 2014 comparing the return on the Company's common stock with the Russell 2000 Index and the NASDAQ Computer & Data Processing Index. No dividends have been declared or paid on the common stock during such period. Historical stock price performance is not necessarily indicative of future stock price performance.

21 |

Item 6. Selected Financial Data

The following selected financial data should be read in conjunction with Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and the financial statements and the notes thereto in Item 8, “Financial Statements and Supplementary Data.”

| Years Ended December 31, | ||||||||||||||||||||

| (Amounts in thousands except per share) | 2010 | (b) | 2011 | (b) | 2012 | 2013 | 2014 | |||||||||||||

| Income Statement Data: | ||||||||||||||||||||

| Revenues | $ | 13,498 | $ | 17,511 | $ | 13,565 | $ | 15,661 | $ | 17,021 | ||||||||||

| Gross profit | $ | 5,401 | $ | 7,250 | $ | 5,047 | $ | 6,303 | $ | 7,413 | ||||||||||

| Operating expenses | $ | 9,116 | $ | 8,524 | $ | 8,056 | $ | 6,426 | $ | 6,482 | ||||||||||

| Net income (loss) | $ | (3,976 | ) | $ | (2,422 | ) | $ | (3,298 | ) | $ | (620 | ) | $ | 432 | ||||||

Net income (loss) per share: Basic | $ | (1.05 | ) | $ | (0.56 | ) | $ | (0.68 | ) | $ | (0.13 | ) | $ | 0.09 | ||||||

| Diluted | $ | (1.05 | ) | $ | (0.56 | ) | $ | (0.68 | ) | $ | (0.13 | ) | $ | 0.08 | ||||||

| Weighted average shares outstanding: | ||||||||||||||||||||

| Basic | 3,796 | 4,360 | 4,854 | 4,865 | 5,006 | |||||||||||||||

| Diluted | 3,796 | 4,360 | 4,854 | 4,865 | 5,251 | |||||||||||||||

| At December 31, | ||||||||||||||||||||

| 2010 | 2011 | 2012 | 2013 | 2014 | ||||||||||||||||

| Balance Sheet Data: | ||||||||||||||||||||

| Cash and cash equivalents | $ | 461 | $ | 957 | $ | 391 | $ | 606 | $ | 633 | ||||||||||

| Restricted cash (a) | $ | 711 | $ | — | $ | — | $ | — | $ | — | ||||||||||

| Total assets | $ | 9,067 | $ | 10,397 | $ | 7,921 | $ | 8,102 | $ | 8,370 | ||||||||||

| Bank line of credit | $ | — | $ | 1,110 | $ | 811 | $ | 764 | $ | 816 | ||||||||||

| Senior convertible note (a) | $ | 330 | $ | — | $ | — | $ | — | $ | — | ||||||||||

| Related party convertible notes payable | $ | — | $ | — | $ | 750 | $ | 812 | $ | 893 | ||||||||||

| Short term notes payable | $ | — | $ | — | $ | 95 | $ | 650 | $ | 600 | ||||||||||

| Capital leases and deferred rent - long term portion | $ | 202 | $ | 184 | $ | 227 | $ | 265 | $ | 276 | ||||||||||

| Total stockholders’ equity | $ | 2,893 | $ | 3,126 | $ | 469 | $ | 133 | $ | 1,029 | ||||||||||

| (a) | Under the terms of the senior convertible note financing closed in November 2010, the Company was required to set aside cash collateral to the extent qualified accounts receivables are less than the note plus interest. At December 31, 2010, the cash collateral requirement was $0.7 million. At December 31, 2010 the amount shown as the Company’s senior convertible note, represents the $1.0 million face value of the note net of debt discount of $0.67 million. The note was subsequently called by the Company in August 2011, and the note holder completed full conversion of the note to common stock by September 2011. |

| (b) | In the years ended December 31, 2010 and 2011, the net loss includes non-cash charges to interest expense of approximately $56,000 and $1,050,000, respectively, related to the Company’s senior convertible note closed in November 2010 (see item (a) discussed immediately above). |

22 |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Liquidity and Going Concern

In 2014, we generated $17.0 million in revenue and $0.4 million in net income. However, except for fiscal years 2014 and 2004, we incurred significant operating losses in each financial period since our inception. As of December 31, 2014, we have an accumulated deficit of $60.7 million. Our cash balance at December 31, 2014 was $0.6 million, including $0.8 million advanced on our bank lines of credit. At December 31, 2014, we had additional unused borrowing capacity of approximately $0.4 million on our bank lines of credit. Our balance sheet at December 31, 2014 has a current ratio (current assets divided by current liabilities) of 0.6 to 1.0, and a working capital deficit of $2.8 million (current assets less current liabilities). These circumstances raise substantial doubt about our ability to continue as a going concern.

We have taken actions to reduce our expenses and to align our cost structure with economic conditions. We have the ability to further reduce expenses if necessary. Steps taken by us to reduce operating losses and achieve profitability included reduction of headcount to manage payroll costs, the introduction of new products, and continued close support of our distributors and registered developers whose applications support the use of our barcode scanning products. We extended the maturity dates on our convertible notes originally issued in 2012 (see NOTE 2 — Related Party Convertible Notes Payable” for more information). We completed additional financing in 2013 (see “NOTE 3 — Related Party and Other Short-Term Notes Payable” for more information). We believe that we will be able to further improve our liquidity and secure additional sources of financing by managing our working capital balances, use of our bank lines of credit, and raising additional capital as needed including the issuance of additional equity securities. However, there can be no assurance that additional capital will be available on acceptable terms, if at all, and any such terms may be dilutive to existing stockholders. Our bank lines of credit may be terminated by the bank or by us at any time (see “NOTE 4 – Bank Financing Arrangements”). If we cannot maintain ongoing profitability, we will not be able to support our operations from positive cash flows, and we would use our existing cash to support operating losses. If we are unable to secure the necessary capital for our business, we may need to suspend some or all of our current operations.

To maintain revenue growth and profitability, we anticipate requirements for cash will include funding of higher receivable and inventory balances, and increased expenses, including an increase of costs relating to new employees to support our growth and increases in salaries, benefits, and related support costs for employees.

Critical Accounting Policies