Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - APX Group Holdings, Inc. | Financial_Report.xls |

| EX-21.1 - EX-21.1 - APX Group Holdings, Inc. | d858687dex211.htm |

| EX-32.2 - EX-32.2 - APX Group Holdings, Inc. | d858687dex322.htm |

| EX-32.1 - EX-32.1 - APX Group Holdings, Inc. | d858687dex321.htm |

| EX-99.1 - EX-99.1 - APX Group Holdings, Inc. | d858687dex991.htm |

| EX-12.1 - EX-12.1 - APX Group Holdings, Inc. | d858687dex121.htm |

| EX-31.1 - EX-31.1 - APX Group Holdings, Inc. | d858687dex311.htm |

| EX-31.2 - EX-31.2 - APX Group Holdings, Inc. | d858687dex312.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2014

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 333-191132-02

APX Group Holdings, Inc.

(Exact name of registrant as specified in its charter)

| DELAWARE | 46-1304852 | |

| State or other jurisdiction of incorporation or organization |

(I.R.S. Employer Identification No.) |

| 4931 North 300 West Provo, UT |

84604 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (801) 377-9111

Securities registered pursuant to Section 12(b) of the Act: NONE

Securities registered pursuant to Section 12(g) of the Act: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ¨ No x

(Note: From January 1, 2014 until the effectiveness of the registrant’s Registration Statement on Form S-4 (File No. 333-193639) on February 4, 2014, the registrant was, and from January 1, 2015, the registrant has been, a voluntary filer not subject to the filing requirements of Section 13 or 15(d) of the Exchange Act; as a voluntary filer the registrant filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant would have been required to file such reports) as if it were subject to such filing requirements.)

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of voting common stock held by non-affiliates of the registrant as of June 30, 2014, the last business day of the registrant’s most recently completed second fiscal quarter, was zero.

As of March 26, 2015, there were 100 shares of the registrant’s common stock par value $0.01 per share, issued and outstanding.

Table of Contents

| Page | ||||||

| PART I | ||||||

| Item 1 |

5 | |||||

| Item 1A |

14 | |||||

| Item 1B |

27 | |||||

| Item 2 |

27 | |||||

| Item 3 |

28 | |||||

| Item 4 |

28 | |||||

| PART II | ||||||

| Item 5 |

28 | |||||

| Item 6 |

28 | |||||

| Item 7 |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

30 | ||||

| Item 7A |

58 | |||||

| Item 8 |

60 | |||||

| Item 9 |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

105 | ||||

| Item 9A |

105 | |||||

| Item 9B |

107 | |||||

| PART III | ||||||

| Item 10 |

108 | |||||

| Item 11 |

111 | |||||

| Item 12 |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

124 | ||||

| Item 13 |

Certain Relationships and Related Transactions, and Director Independence |

126 | ||||

| Item 14 |

131 | |||||

| PART IV | ||||||

| Item 15 |

132 | |||||

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This annual report on Form 10-K includes forward-looking statements regarding, among other things, our plans, strategies and prospects, both business and financial. These statements are based on the beliefs and assumptions of our management. Although we believe that our plans, intentions and expectations reflected in or suggested by these forward-looking statements are reasonable, we cannot assure you that we will achieve or realize these plans, intentions or expectations. Forward-looking statements are inherently subject to risks, uncertainties and assumptions. Generally, statements that are not historical facts, including statements concerning our possible or assumed future actions, business strategies, events or results of operations, are forward-looking statements. These statements may be preceded by, followed by or include the words “believes,” “estimates,” “expects,” “projects,” “forecasts,” “may,” “will,” “should,” “seeks,” “plans,” “scheduled,” “anticipates” or “intends” or similar expressions.

Forward-looking statements are not guarantees of performance. You should not put undue reliance on these statements which speak only as of the date hereof. You should understand that the following important factors, in addition to those discussed in “Risk Factors” and elsewhere in this annual report on Form 10-K, could affect our future results and could cause those results or other outcomes to differ materially from those expressed or implied in our forward-looking statements:

| • | risks of the security and home automation industry, including risks of and publicity surrounding the sales, subscriber origination and retention process; |

| • | the highly competitive nature of the security and home automation industry and product introductions and promotional activity by our competitors; |

| • | litigation, complaints or adverse publicity; |

| • | the impact of changes in consumer spending patterns, consumer preferences, local, regional, and national economic conditions, crime, weather, demographic trends and employee availability; |

| • | adverse publicity and product liability claims; |

| • | increases and/or decreases in utility and other energy costs, increased costs related to utility or governmental requirements; and |

| • | cost increases or shortages in security and home automation technology products or components. |

In addition, the origination and retention of new subscribers will depend on various factors, including, but not limited to, market availability, subscriber interest, the availability of suitable components, the negotiation of acceptable contract terms with subscribers, local permitting, licensing and regulatory compliance, and our ability to manage anticipated expansion and to hire, train and retain personnel, the financial viability of subscribers and general economic conditions.

These and other factors that could cause actual results to differ from those implied by the forward-looking statements in this annual report on Form 10-K are more fully described in the “Risk Factors” section of this annual report on Form 10-K. The risks described in “Risk Factors” are not exhaustive. Other sections of this annual report on Form 10-K describe additional factors that could adversely affect our business, financial condition or results of operations. New risk factors emerge from time to time and it is not possible for us to predict all such risk factors, nor can we assess the impact of all such risk factors on our business or the extent to which any factor or combination of factors may cause actual results to differ materially from those contained in any forward-looking statements. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the foregoing cautionary statements. We undertake no obligations to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise.

BASIS OF PRESENTATION

On November 16, 2012, APX Group, Inc. and two of its historical affiliates, V Solar Holdings, Inc. (“Solar”) and 2GIG Technologies, Inc. (“2GIG”), were acquired by an investor group (collectively, the “Investors”) comprised of certain investment funds affiliated with Blackstone Capital Partners VI L.P. (“Blackstone” or the “Sponsor”), and certain co-investors and management investors. This acquisition was accomplished through certain mergers and related reorganization transactions (collectively, the “Merger”) pursuant to which each of APX Group, Inc., Solar and 2GIG became indirect wholly-owned subsidiaries of 313 Acquisition LLC (“Acquisition LLC”), an entity wholly-owned by the Investors. Upon the consummation of the Merger, APX Group, Inc. and 2GIG became consolidated subsidiaries of APX Group Holdings, Inc.

3

Table of Contents

(“Holdings” or “Parent Guarantor”), which in turn is wholly-owned by APX Parent Holdco, Inc., which in turn is wholly-owned by Acquisition LLC, and Solar became a direct wholly-owned subsidiary of Acquisition LLC. Acquisition LLC, APX Parent Holdco, Inc. and Parent Guarantor have no independent operations and were formed for the purpose of facilitating the Merger.

The Merger, the equity investment by the Investors, entering into our revolving credit facility and $10.0 million of borrowings thereunder, the issuance of $925.0 million aggregate principal amount of 6.375% Senior Secured Notes due 2019 (the “2019 notes”) and $380.0 million aggregate principal amount of 8.75% senior notes due 2020 (the “2020 notes”) and the payment of related fees and expenses are collectively referred to in this annual report on Form 10-K as the “Transactions.” In May 2013, we issued and sold an additional $200.0 million aggregate principal amount of the 2020 notes. That offering is referred to in this annual report on Form 10-K as the “May 2013 Notes Offering.” In December 2013, we issued and sold an additional $250.0 million aggregate principal amount of the 2020 notes. That offering is referred to in this annual report on Form 10-K as the “December 2013 Notes Offering” (and together with the May 2013 Notes Offering, the “2013 Notes Offerings”). In July 2014, we issued and sold an additional $100.0 million aggregate principal amount of the 2020 notes. That offering is referred to in this annual report on Form 10-K as the “July 2014 Notes Offering” (and together with the 2013 Notes Offerings, the “Subsequent Notes Offerings”).

Unless the context suggests otherwise, references in this annual report on Form 10-K to “Vivint®,” the “Company,” “we,” “us” and “our” refer (1) prior to the Merger, to APX Group, Inc. and its subsidiaries and 2GIG and Solar, which were consolidated variable interest entities prior to the Merger and (2) after the Merger, to the Parent Guarantor and its subsidiaries, including 2GIG to the date of the 2GIG Sale (as defined below). References to the “Issuer” refer to APX Group, Inc., exclusive of its subsidiaries. References to “Parent Guarantor” refer to Holdings, exclusive of its subsidiaries.

Our historical and pro forma results of operations prior to the Merger include the results of Solar, which was considered a variable interest entity. As a result of the Merger, while Solar was a variable interest entity of the Company through the date of Solar’s initial public offering in October 2014, we have not been its primary beneficiary since after the date of the Merger. Accordingly, Solar has not been required to be included in the consolidated financial statements of the Company in periods following the Merger. In addition, the historical and pro forma financial information included in this annual report on Form 10-K include the results of operations of 2GIG up through April 1, 2013, which was the date we completed the sale of 2GIG and its subsidiary (the “2GIG Sale”) to Nortek, Inc. (“Nortek”). In connection with the 2GIG Sale, we entered into a five-year supply agreement with 2GIG, pursuant to which they will be the exclusive provider of our control panel requirements, subject to certain exceptions as provided in the supply agreement. Due to our continuing involvement with 2GIG under the supply agreement, it is not considered a discontinued operation. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Basis of Presentation.” Solar and 2GIG do not and will not provide any credit support for any of our indebtedness, including indebtedness incurred under our revolving credit facility, our 2019 notes or our 2020 notes.

The consolidated financial statements for periods preceding the Merger are presented for APX Group, Inc. and its wholly-owned subsidiaries, as well as Solar, 2GIG and their respective subsidiaries (the “Predecessor Period” or “Predecessor” as context requires). The consolidated financial statements for periods succeeding the Merger present the financial position and results of operations of Parent Guarantor and its wholly-owned subsidiaries (“the Successor Period” or “Successor” as context requires). The audited consolidated financial statements for the year ended December 31, 2012 are presented for two periods: the Predecessor Period from January 1, 2012 through November 16, 2012, and the Successor Period from November 17 through December 31, 2012, which relate to the period preceding the Merger and the period succeeding the Merger, respectively. The financial position and results of operations of the Successor are not comparable to the financial position and results of operations of the Predecessor due to the Merger and the application of purchase accounting in accordance with Accounting Standards Codification (“ASC”) 805, Business Combinations.

The unaudited pro forma statement of operations for the year ended December 31, 2012 (“Pro Forma Year”) has been prepared to give pro forma effect to the Transactions as if they had occurred on January 1, 2012. The unaudited pro forma consolidated statement of operations data included in this annual report on Form 10-K does not give effect to the Subsequent Notes Offerings.

The pro forma financial information is for informational purposes only and should not be considered indicative of actual results that would have been achieved had the Transactions actually been consummated on the dates indicated and do not purport to indicate results of operations as of any future date or for any future period. See “Management’s discussion and Analysis of Financial Condition and Results of Operation-Unaudited Pro Forma Financial Information.”

4

Table of Contents

The term “attrition” as used in this annual report on Form 10-K refers to the aggregate number of cancelled security and home automation subscribers during a period divided by the monthly weighted average number of total security and home automation subscribers for such period. Subscribers are considered cancelled when they terminate in accordance with the terms of their contract, are terminated by us or if payment from such subscribers is deemed uncollectible (when at least four monthly billings become past due). Sales of contracts to third parties and certain subscriber residential moves are excluded from the attrition calculation. The term “CAGR”, as used in this annual report on Form 10-K, refers to the compound annual growth rate over the specified period. The term “net subscriber acquisition costs” as used in this annual report on Form 10-K refers to the direct and indirect costs to create a new security and home automation subscriber. These include commissions, equipment, installation, marketing and other allocations (G&A and overhead); less activation fees and up sell revenue. These costs exclude residuals and long-term equity direct-to-home expenses. The term “IRR” means the internal rate of return per subscriber calculated based on our estimates and assumptions related to net subscriber acquisition cost per subscriber, net servicing cost per subscriber, average RMR per new subscriber and attrition. The term “RMR” is the recurring monthly revenue billed to an individual security and home automation subscriber. The term “total RMR” is the aggregate RMR billed to all security and home automation subscribers. The term “total subscribers” is the aggregate number of our active security and home automation subscribers at the end of a given period. The term “average RMR per subscriber” is the total RMR divided by the total subscribers. This is also commonly referred to as Average Revenue per User, or “ARPU.” The term “average RMR per new subscriber” is the aggregate RMR for new subscribers originated during a period divided by the number of new subscribers originated during such period.

Unless specified otherwise, amounts in this annual report on Form 10-K are presented in United States (“U.S.”) dollars. Defined terms in the financial statements have the meanings ascribed to them in the financial statements.

| ITEM 1. | BUSINESS |

Company Overview

We are one of the largest Smart Home companies in North America. In February 2013, we were recognized by Forbes magazine as one of America’s Most Promising Companies. Our fully integrated and remotely accessible residential services platform offers subscribers a suite of products and services that includes interactive security, life-safety, energy management and home automation. We utilize a scalable “direct-to-home” sales model to originate a majority of our new subscribers, which allows us control over our net subscriber acquisition costs. We have built a high-quality subscriber portfolio, with an average credit score of 714, as of December 31, 2014, through our underwriting criteria and compensation structure. Unlike many of our competitors, who generally focus on either subscriber origination or servicing, we originate, install, service and monitor our entire subscriber base, which allows us to control the overall subscriber experience. We seek to deliver a quality subscriber experience with a combination of innovative new products and services and a commitment to customer service, which together with our focus on originating high-quality new subscribers, has enabled us to achieve attrition rates that we believe are historically at or below industry averages. Utilizing this model, we have built a portfolio of approximately 894,000 subscribers, as of December 31, 2014. Approximately 95% and 92% of our revenues during the years ended December 31, 2014 and 2013, respectively, consisted of contractually committed recurring revenues, which have historically resulted in consistent and predictable operating results.

We believe our sales model allows us to originate subscribers at lower net subscriber acquisition cost (as a multiple of RMR) and achieve a higher adoption rate of new service packages compared to many of our competitors. We generate the majority of our new subscribers through our direct-to-home sales channel, which uses teams of trained seasonal sales representatives. For the year ended December 31, 2014, we generated approximately 76% of our new subscribers through our direct-to-home sales channel. In this channel we have historically employed between 2,000 and 2,500 sales representatives and approximately 1,000 installation technicians, who are both largely commission based and deployed in targeted geographical locations. This results in a highly variable cost structure, subscriber density and the ability to complete same-day installations. We diversify our subscriber origination efforts with an “inside sales” channel, which includes our internal-sales call centers, radio, internet and other media advertising, as well as third-party lead generators.

We use underwriting policies that focus on creating a high-quality subscriber portfolio with an attractive return profile with an unlevered IRR in the low to mid 20% range, depending on contractual terms. As of December 31, 2014, based on FICO score at the time of contract origination, approximately 94% of our subscribers had a FICO score of 625 or greater, and the average FICO score of our portfolio was 714. In addition, for the year ended December 31, 2014, over 81% of our new subscribers paid activation fees and, as of December 31, 2014, approximately 88% of our total subscribers are set up on an automatic payment method. We believe that originating high-quality subscribers and our commitment to customer service increases retention which leads to predictable cash flows.

5

Table of Contents

Our business generates positive cash flows from ongoing monitoring and service revenues, which we choose to invest in new subscriber acquisitions and development of additional products and services. During the year ended December 31, 2014 and 2013, respectively, we generated $563.7 million and $500.9 million in total revenue, including $537.7 million and $460.1 million, respectively, in monitoring revenue. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources.”

In fiscal 2013, we completed the 2GIG Sale. Pursuant to the terms of the 2GIG Sale, Nortek acquired all of the outstanding common stock of 2GIG for aggregate cash consideration of approximately $148.9 million. In connection with the 2GIG Sale, we retained sole ownership of the intellectual property and exclusive rights with respect to the next generation of our control panels and certain peripheral equipment. In addition, we entered into a five-year supply agreement with 2GIG, pursuant to which they will be the exclusive provider of our control panel requirements, subject to certain exceptions. The terms of the credit agreement governing our revolving credit facility and the indentures governing the notes permitted us, subject to certain conditions, to distribute all or a portion of the net proceeds from the 2GIG Sale to our stockholders. In May 2013, we distributed $60.0 million of such proceeds to our stockholders in reliance on these provisions. The remaining proceeds have been used to fund our business activities or otherwise used for general corporate purposes, and we do not intend to make future dividends to our stockholders in reliance on these provisions.

The Residential Security and Automation Industry

According to Barnes Associates estimates, the U.S. market for monitoring and related residential electronic security services was over $23 billion in revenue in 2014 and has grown every year for the past 10 years. The penetration rate for this market was estimated at approximately 19%, as of December 31, 2014. This market is characterized by stable revenues from contractually committed recurring monthly payments and has proven to be recession-resistant through the last two economic downturns.

ABI Research estimates the total number of North American subscribers of home automation services will grow from approximately 877,000 in 2011 to over 13.1 million during 2018 and total annual North American revenues from these services to increase from an estimated $3.3 billion in 2011 to $7.5 billion in 2018.

Products and Service Packages

Our products and service packages allow subscribers to remotely control, monitor and manage the security, life-safety, video, lighting, access control and HVAC systems within their homes. Since January 2010, substantially all of the systems we have installed are interactive and Smart Home enabled. In early 2014, we launched Vivint Sky™, an integrated platform consisting of our proprietary SkyControl panel, equipment, cloud software, mobile application and online experience. Each of our service packages has a differentiated set of equipment and functionality, utilizing the Vivint Sky platform. Historically, we have offered contracts to subscribers ranging in length from 36 to 60 months. We offer three service packages: Smart Security, Smart Energy, and Smart Control. In addition, we offer products and services that include wireless internet and cloud based data storage, neither of which was material to our overall business or operating results for the year ended December 31, 2014.

Smart Security

This service package provides subscribers with residential security monitoring, wireless intrusion equipment, and emergency and non-emergency alerts. The current standard price of the Smart Security service package is $53.99 per month and includes the SkyControl panel, which communicates wirelessly with other equipment and features an LCD touchscreen, two-way voice communication, and remote control capabilities, three door or window sensors, a motion detector, a key fob and a yard sign. Subscribers can select additional equipment, such as glass-break detectors, and safety devices, including smoke and carbon monoxide detectors and personal panic pendants, to customize the system for their particular needs. Like all of our home services, subscribers can operate the system remotely through a smart phone application or a web-enabled device. All equipment in the Smart Security service package is connected wirelessly to the SkyControl panel, which then communicates through a wireless infrastructure to our two UL listed redundant central monitoring stations.

Smart Energy

Our Smart Energy service package provides subscribers the ability to monitor, control and conserve energy usage through the SkyControl panel or remotely through a smartphone application or a web-enabled device. The current standard price of the Smart Energy service package is $59.99 per month and includes a smart thermostat and a lamp/small appliance control, in addition to all of the services that are included with our Smart Security package. The SkyControl panel integrates with motion sensors, thermostats and lamps or small appliances to adjust settings based on occupancy. With our smart thermostat, subscribers can also remotely control their home temperature from any web enabled device as well as opt-in to automatically program their thermostat.

6

Table of Contents

Smart Control

Our Smart Control service package is a fully integrated suite of Smart Home products and services that connects various in-home technologies all through a single platform. The current standard price of the Smart Control service package is $69.99 per month and includes all of the services that are included with the Smart Security package along with the following “Smart Home” add-ons: (1) indoor camera, (2) automatic door lock or deadbolt, (3) smart thermostat, and a (4) lamp/small appliance module. With this package subscribers have the ability to remotely manage their home security and lock, unlock and monitor the status of the automatic door locks as well as the ability to remotely monitor activity in their home through video surveillance and text alerts.

For the year ended December 31, 2014, 69% of new subscribers selected additional services beyond our Smart Security package. In order to provide integrated products and services requested by our subscribers, we continually review our product and service packages and pricing, and as a result we expect to modify our product and service packages and pricing in the future.

Existing subscribers may order additional products or upgrade their current services. When they do this, a local field service technician performs the installation at the subscriber’s home, which may result in additional service charges. In addition, the subscriber is typically billed for the cost of the equipment installed and their RMR increases for the additional service offerings.

Operations

Our management team has a proven record of strong growth and operational excellence and, as a result of their leadership, we have successfully grown revenue and total RMR every year since 2006. Our CEO, Todd Pedersen, a visionary leader, encourages a highly entrepreneurial culture that fosters innovation, founded the Company in 1999. Our senior management team averages over 17 years of experience in high growth or large public companies. In connection with the Transactions, senior management and employees invested $155.2 million (a portion of which was used for the Investors’ acquisition of Solar) in the Company.

We are one of a few Smart Home solutions companies in North America that generates substantially all of its revenue organically from a fully integrated model that encompasses all aspects of the subscriber experience, including sales, installation, servicing and monitoring. This approach allows us to deliver a consistent, quality subscriber experience. We believe this contributes to a strong adoption rate for service packages beyond Smart Security and attrition rates at or below industry average. During the year ended December 31, 2014, 69% of new subscribers selected service packages beyond Smart Security. We also enhance the quality of our subscribers’ experience through proven operational performance. During the year ended December 31, 2014, our average response time to alarms was approximately 12 seconds from the time the signal was received at our monitoring stations. We believe the enhanced functionality of our offerings along with the introduction of innovative new service packages, results in increased subscriber usage. An average of 81% of our surveyed subscribers indicated use of their system at least once per week during the year ended December 31, 2014. We believe increased subscriber usage contributes to higher customer satisfaction and may lead to lower attrition.

Our fully integrated subscriber experience allows our sales representatives, customer service representatives and installation technicians to work closely together to provide the subscriber with an integrated process from contact origination to daily use. We believe our field service technicians and customer service representatives deliver a quality customer service experience that enhances our brand and improves customer satisfaction. Customer service representatives generally resolve a majority of maintenance and service related questions over the telephone or through remote-access to the subscriber’s system. We also believe we have higher Net Promoter Scores (a widely used measure of customer satisfaction and loyalty) than our primary competitors and we have been recognized by third-party organizations for providing outstanding customer service.

Field Service

We employ full-time field service technicians (“FSPs”) throughout North America, who reside in their service territories, to provide prompt service to our subscribers. FSPs undergo comprehensive training on our products and service packages. The FSPs typically focus on maintenance and service issues, but also install products and services for a portion of our new subscribers, primarily those originated through inside sales.

7

Table of Contents

We do not maintain costly physical warehouse, retail or office locations for our FSPs. Instead, we provide FSPs with adequate supplies of products and materials and a company-branded service vehicle. Field service inventories are replenished by shipments from our central warehouse.

We utilize software to schedule appointments, route technicians and follow-up with subscribers to ensure that the service was performed to the subscriber’s satisfaction. All of our full-time FSPs receive updates via a smartphone or tablet detailing their next service appointment or installation through our customer relationship management system (“CRM”).

Customer Service and Alarm Monitoring

Our customer service centers are located in Utah. Our two central monitoring facilities are located in Utah and Minnesota and are fully redundant. Both our customer service center and central monitoring facilities are open 24 hours a day, 7 days a week, and 365 days a year. We have received industry awards for our customer service and alarm monitoring operations.

All employees who work in customer service undergo training on billing related issues as well as service package questions. Customer service representatives are required to pass background checks and, depending upon their job function, may require licensing by the state of Utah. All professionals who work in our monitoring facilities undergo comprehensive training and are required to pass background checks and, in certain cases, licensing tests or other checks to obtain the required licensing. Customer service representatives generally resolve a majority of maintenance and service related questions over the telephone or through remote-access to the subscriber’s panel. Issues not resolved by customer service require a service technician to visit the subscriber’s home, which may result in a trip charge to the subscriber.

Billing

Our billing representatives are located in our Utah offices. We cross-train our billing representatives on customer service with the goal of improving the subscriber experience and to increase personnel flexibility. Billing representatives are also required to pass background checks and, depending upon their job function, may also require licensing by the state of Utah. A majority of our subscribers pay electronically either via ACH or credit card. A subscriber who pays electronically is generally placed on a billing cycle based on their contract origination date and, in certain instances, the subscriber may choose their billing date. Our customers billed via direct invoice are either billed on the first day of the month with payment due on the 25th day of the month, or on the 15th day of the month with payment due on the 10th day of the following month. Subscribers are billed in advance for their monthly services based on the subscriber’s billing cycle and not calendar month.

From time to time, for various reasons we may issue a credit to a subscriber for a payment otherwise due, including addressing subscriber concerns or obtaining the renewal of a subscriber contract. Any such credit decreases revenue and cash collected on the relevant subscriber contract in the amount of such credit.

Key Systems

In March 2014, we implemented our new CRM software, which is an integrated customer relationship management and billing system. The CRM is based on well-established enterprise-scale cloud solution. We believe this new CRM will scale with our business, providing the flexibility to accommodate the multiple customer support and billing models resulting from the anticipated expansion in our product and service packages over time. Historically, our internally developed relationship management system (“CMS”) was used by most of our departments for a wide variety of functions, including, but not limited to, new subscriber originations, customer support and inventory tracking in the field. Our new CRM replaced all CMS functionality except for field service inventory tracking, and enables one-call resolution. It also allows for operational efficiency by not requiring the entry of data multiple times and improving data accuracy. Additionally, the data is replicated to both a reporting and a business intelligence server to reduce processing time, as well as to an offsite server used for disaster recovery purposes.

Software Platform

Over 80% of our new subscribers installed in 2014 use our proprietary Vivint Sky platform, consisting of our SkyControl panel, equipment, cloud software, mobile application and online interface. The SkyControl panel is connected to the Internet and mobile devices through the Vivint Sky cloud software. The Vivint Sky platform enables subscribers using SkyControl to access their systems remotely either directly from the web or through our free Vivint Sky app and it facilitates

8

Table of Contents

communications between the panel and our monitoring stations. The Vivint Sky platform allows our subscribers the ability to remotely arm and disarm their SkyControl security systems, receive alerts and notifications regarding activity in their home, control home automation products such as thermostats, door locks, lighting controls and view live and recorded video.

Go!Control was our primary panel installed in new subscribers’ homes prior to the launch of Vivint Sky platform. We license certain communications infrastructure, software and services to support the Go!Control panel from Alarm.com. The Go!Control panel is also connected to the Internet and smart phone and tablet applications through Alarm.com’s hosted platform. Alarm.com also provides the web interface and technology to enable our subscribers using Go!Control panels to access their systems remotely and it facilitates communication between the panel and monitoring stations through third party cellular networks.

Subscriber Contracts – Security and Home Automation

We seek to ensure that our subscribers understand our product and service packages, along with the key terms of their contracts by conducting two live, interactive telephonic surveys with every subscriber. The first survey is conducted prior to the execution of the contract and installation, and the second survey is conducted after the installation is completed. These telephonic surveys are recorded and stored in our CRM, enabling easy access and review.

Term and Termination

Historically, we have offered contracts to subscribers that range in length from 36 to 60 months, subject to automatic monthly renewal after the expiration of the initial term. A majority of subscriber originations since the beginning of 2013 have 60 month contract lengths. Subscribers have a right of rescission period prescribed by applicable law during which such subscriber may cancel the contract without penalty or obligation. These rescission periods range from 3 to 15 days, depending on the jurisdiction in which a subscriber resides. As a company policy we provide new subscribers 70 years of age and older a 30 day right of rescission. Once the applicable rescission period expires, ownership of the equipment transfers to the subscriber and the subscriber is responsible for the monthly services fees under the contract.

Upfront and Monthly Services Fees

Our subscribers typically pay an activation fee (unless waived by us) and the first month’s service at the time of installation. Under the contract, we have the right to pass through to the subscriber any increase in third party costs such as utility or governmental expenses. We have the right to increase the monthly service fees at the time of renewal with prior written notice.

Other Terms

We provide our subscribers with maintenance free of charge for the first 120 days. After 120 days, we will repair or replace defective equipment without charge, but we typically bill the subscriber a trip charge for each service visit. If a utility or governmental agency requires a change to equipment or service after installation of the system, the subscriber must pay for the equipment and labor associated with the required change.

We do not provide insurance or warrant that the system will prevent a burglary, fire, hold-up or any such other event. Our contracts limit our liability to a maximum of $2,000 per event and, where permissible, provide a one-year statute of limitations to file an action against us. We may cease or suspend monitoring and repair service due to, among other things, work stoppages, weather, phone service interruption, government requirements, subscriber bankruptcy or non-payment by subscribers after we have given notice that their service is being cancelled due to such non-payment.

Suppliers

We provide our services through a panel installed at the premises of our subscribers. As of December 31, 2014, approximately 74% of our installed panels were 2GIG Go!Control panels, approximately 19% were SkyControl panels and approximately 7% were Honeywell LYNX and Vista panels. Since early 2014, our primary panel installed for new subscribers is the SkyControl panel. The 2GIG Go!Control panel was our primary panel for subscribers from the beginning of 2010 through early 2014. In fiscal 2013, we completed the 2GIG Sale as described above under “—Company Overview.” Pursuant to the terms of the 2GIG Sale, Nortek acquired all of the outstanding common stock of 2GIG for

9

Table of Contents

aggregate cash consideration of approximately $148.9 million. In connection with the 2GIG Sale, we retained sole ownership of the intellectual property and exclusive rights with respect to the next generation of our control panels and certain peripheral equipment. We expect this proprietary equipment will be a critical component of our future offerings. In addition, we entered into a five-year supply agreement with 2GIG, pursuant to which they will be the exclusive provider of our control panel requirements and certain peripheral equipment, subject to certain exceptions.

Generally, our third-party distributors maintain a safety stock of certain key items to cover any minor supply chain disruptions. Where possible we also utilize dual sourcing methods to minimize the risk of a disruption from a single supplier.

Sales and Marketing

We have two primary sales channels: direct-to-home and inside sales. For the year ended December 31, 2014, we generated approximately 76% of our new subscribers through our direct-to-home sales channel and 24% through inside sales. We believe our approach to managing our sales channels allows us to originate subscribers at a lower net subscriber acquisition cost (as a multiple of RMR) and achieve a higher adoption rate of new service packages compared to our competitors. Our net subscriber acquisition cost in 2014 was in the $1,900 to $1,950 range, a substantial portion of which is variable. Our net subscriber acquisition cost represented approximately 31 times our average RMR per new subscriber added in 2014. We are continually evaluating ways to improve the effectiveness of our subscriber acquisition activities in both our direct-to-home and inside sales channels.

Because we believe attrition is highly correlated with FICO scores and payment type, our compensation structure incentivizes quality subscriber generation by tying compensation to these factors. We have enhanced our underwriting criteria over time, resulting in an average FICO score of our subscriber portfolio of 714, with sub-600 FICO score subscribers representing only approximately 2% of our subscriber portfolio and approximately 94% of our subscribers having FICO scores of 625 or greater, as of December 31, 2014. We plan to maintain our focus on our underwriting standards and expect to continue to structure our sales compensation to incentivize sales representatives based on the creation of high-quality subscribers.

Direct-to-Home Sales

Our direct-to-home sales channel is typically comprised of between 2,000 and 2,500 sales representatives who benefit from our recruiting and training programs designed to promote professionalism and sales productivity. Each year, between April and August, our sales teams travel to approximately 100 pre-selected markets throughout North America to sell our product and service packages. Markets are selected each year based on a number of factors, including demographics, population density and our past experience selling in these markets. Because expenses associated with our direct-to-home sales channel are directly correlated with new subscriber acquisition, we avoid a large fixed cost base and are able to deploy a flexible go-to-market strategy every year. A typical sales team consists of approximately 20 sales representatives and a designated sales manager. Each sales team is supported by approximately 10 trained installation technicians, including a manager for the technicians. There are also regional managers who generally oversee six to eight sales or installation teams.

Inside Sales

Subscribers originated through our inside sales channel have grown as a percentage of our total originations from approximately 10% in 2009 to approximately 24% for the year ended December 31, 2014. Our inside sales channel utilizes both inbound and outbound leads provided by our marketing department to sell to subscribers in the United States and Canada. The marketing department generates leads through multiple sources, both digital and traditional. Leads generated through digital marketing sources include paid, organic and local search and display advertising. Traditional lead sources include radio advertising, shared mail, email remarketing and third-party lead generation affiliates. Upon receiving a lead or an inquiry from a potential subscriber requesting information on our products and service packages, one of our inside sales representatives calls the potential subscriber. Existing subscribers wishing to upgrade equipment or change their service packages are also processed through inside sales.

Sales and Origination Strategy and Compensation

Sales representatives receive compensation based on the number of qualifying sales during the previous week. Criteria for qualifying sales include, but are not limited to, the amount of RMR, the number of points of protection, subscriber FICO score, etc. To motivate sales representatives and help align compensation with subscriber quality, we have

10

Table of Contents

created a point system. The point system provides the sales representative flexibility to tailor the offering to the subscriber’s needs while maintaining control through a direct link to the sales representative’s compensation. In addition, a significant portion of the direct-to-home sales representative’s compensation is not paid until after the completion of the selling season and is paid only on those subscribers who satisfy certain criteria. In order to retain our sales professionals, we pay ongoing residual commissions to sales representatives and sales management for all active subscriber accounts generated by them. Sales management also receives residual commissions for active subscriber accounts generated by sales representatives working for that manager.

Strategy

Strong Platform for Growth

We have established a history of capitalizing on our business model and technology to offer new product and service packages, as evidenced by the launch of Smart Home products and services in 2011 and the Vivint Sky platform and SkyControl panel in early 2014. Our innovative products and service packages have enabled us to increase average RMR per new subscriber from $44.50 in 2009 to $61.89 for the year ended December 31, 2014. Going forward, we intend to capitalize on the low incremental costs inherent in our business model and existing technology to increase market penetration and inside sales. We expanded our business to New Zealand in 2013 and may consider expansion into other markets over time.

Innovation

We strive to bring easy-to-use technology to our subscribers, which allow them to efficiently use our products and services. As evidenced by the launch of our proprietary Vivint Sky platform in early 2014, we have a reputation for developing and deploying products and services for the home that have robust functionality and that are easy to install and use. Both our SkyControl and Go!Control panels provide a platform to introduce new products and service packages to our subscribers. Another example of our emphasis on providing innovative solutions to our subscribers is our acquisition of Space Monkey, Inc. (“Space Monkey”) in August 2014, which provides a data cloud storage technology solution that will integrate with our Vivint Sky platform. By focusing on innovation, and enhancing the functionality of our existing products and service packages, we believe we can increase subscriber usage and customer satisfaction, thereby potentially lowering our attrition.

To enhance the functionality of the products and services included in our systems, we use various third-party manufacturers and service providers in addition to our in-house development and design of certain products and services. We believe that developing, designing and selling our own products and services that are differentiated from those of our competitors will be a critical driver of our future success. Therefore, we expect to continue introducing new, innovative products and services, including panels and peripherals, along with integrated cloud services. We own the design of these new products, and in certain circumstances leverage partnerships with third parties, particularly Original Design Manufacturers for the manufacture of new products (e.g., video cameras, thermostats, door lock hardware, etc.). By vertically integrating the development and design of our products and services with our existing sales and customer service activities, we believe we are able to more quickly respond to market needs, and better understand our subscribers’ interactions and engagement with our products and services. This provides critical data enabling us to improve the power, usability and intelligence of these products and services.

We have invested in a new innovation center in Lehi, Utah to facilitate the research and development of new products and services, both within and beyond our existing service packages. Professionals and engineers at our innovation center have expertise in all aspects of the development process, including hardware development, software development, design and quality assurance.

Competition

The residential electronic security services industry is highly competitive, but fragmented. Our major competitors include The ADT Corporation, Protection One, Inc., Stanley Security Solutions, a subsidiary of Stanley Black and Decker, Monitronics International, Inc., a subsidiary of Ascent Capital Group, Inc., Tyco Integrated Security, a subsidiary of Tyco International Ltd., Comcast Corporation, AT&T Inc. and numerous smaller providers with regional or local coverage. We also face, or may in the future face, competition from other providers of information and communication products and services, a number of which have significantly greater capital and other resources than we do.

Companies in our industry compete primarily on the basis of price in relation to the quality of the products and services they provide. The Company’s brand and reputation, market visibility, service and product capabilities, quality, price, efficient

11

Table of Contents

direct-to-home sales channel and the ability to identify and sell to prospective customers are all factors that contribute to competitive success in the residential electronic services industry. We emphasize the quality of the service we provide, rather than focusing primarily on price competition. We believe we compete effectively against other national, regional and local security alarm monitoring companies by offering our subscribers an attractive value proposition combined with our proven, award-winning customer service.

Although we face additional competition from new competitors such as cable and telecommunications companies, having installed over 1.5 million integrated security systems we believe we are well positioned to compete with them because we benefit from more than 16 years of experience, our efficient direct-to-home sales channel and our award-winning customer service.

Intellectual Property

Patents, trademarks, copyrights, trade secrets, and other proprietary rights are important to our business and we continuously refine our intellectual property strategy to maintain and improve our competitive position. We seek protection on new intellectual property to protect our ongoing technological innovations and strengthen our brand, and we believe we take appropriate action against infringements or misappropriations of our intellectual property rights by others. We review third-party intellectual property rights to help avoid infringement, and to identify strategic opportunities. We typically enter into confidentiality agreements to further protect our intellectual property.

We own a portfolio of issued U.S. patents and pending U.S. and foreign patent applications that relate to a variety of security, home automation and wireless internet technologies utilized in our business. We also own a portfolio of trademarks, including domestic and foreign registrations for Vivint®, and are a licensee of various patents, from our third-party suppliers and technology partners. Due to the importance that customers place on reputation and trust when making a decision on a security provider, our brand is critical to our business. Patents for individual products or technologies extend for varying periods according to the date of patent filing or grant and the legal term of patents in the various countries where patent protection is being sought. Trademark rights may potentially extend for longer periods of time and are dependent upon national laws and use of the marks.

Government Regulations

United States

We are subject to a variety of laws, regulations and licensing requirements of federal, state and local authorities.

We are also required to obtain various licenses and permits from state and local authorities in connection with the operation of our businesses. The majority of states regulate in some manner the sale, installation, servicing, monitoring or maintenance of electronic security systems. In the states that do regulate such activity, security service companies and their employees are typically required to obtain and maintain licenses, certifications or similar permits from the state as a condition to engaging in the security services business.

In addition, a number of local governmental authorities have adopted ordinances regulating the activities of security service companies, typically in an effort to reduce the number of false alarms in their jurisdictions. These ordinances attempt to reduce false alarms by, among other things, requiring permits for individual electronic security systems, imposing fines (on either the subscriber or the company) for false alarms, discontinuing police response to notification of an alarm activation after a subscriber has had a certain number of false alarms, and requiring various types of verification prior to dispatching authorities.

The sales and marketing practices of security service companies are regulated by the federal, state and local agencies. These laws and regulations typically place restrictions on the manner in which electronic security products and services can be advertised and sold, and to provide residential purchasers with certain rescission rights. In certain circumstances, consumer protection laws also require the disclosure of certain information in the contract between the security services company and the subscriber and, in addition, may prohibit the inclusion of certain terms or conditions of sale in such contracts.

12

Table of Contents

Canada

Companies operating in the electronic security service industry in Canada are subject to provincial regulation of their business activities, including the regulation of direct-to-home sales activities and contract terms and the sale, installation and maintenance of electronic security systems. Most provinces in Canada regulate direct-to-home sales activities and contract terms and require that salespeople and the company on whose behalf the salesperson is selling obtain licenses to carry on business in that province. Consumer protection laws in Canada also require that certain terms and conditions be included in the contract between the electronic security services provider and the subscriber.

A number of Canadian municipalities require subscribers to obtain licenses to use electronic security alarms within their jurisdiction. Municipalities also commonly require entities engaged in direct-to-home sales within their municipality to obtain business licenses.

Customers

Our business is not dependent on any single customer or a few customers, the loss of which would have a material adverse effect on the respective market or on us as a whole. No individual customer accounted for more than 10% of our consolidated 2014 revenue.

Seasonality

Our direct-to-home sales are seasonal in nature with a substantial majority of our new subscriber originations occurring during a sales season from April through August. We make investments in the recruitment of our direct-to-home sales force and the inventory prior to each sales season. We experience increases in net subscriber acquisition costs during these time periods.

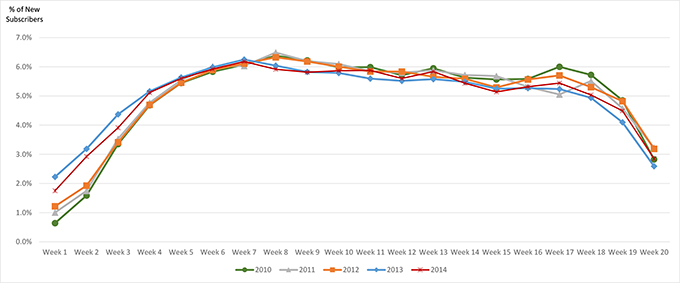

The management of our sales channels has historically resulted in a consistent sales pattern that enables us to more accurately forecast subscriber originations. The chart below depicts the percentage of new subscribers originated each week of the April through August sales season in 2014, 2013, 2012, 2011 and 2010.

Segment Information

Prior to the date of the 2GIG Sale, the Company conducted business through two segments, Vivint and 2GIG. These segments were managed and evaluated separately by management due to the differences in their products and services. We operate primarily in three geographic regions: United States, Canada and New Zealand. The operations in New Zealand are considered immaterial and are reported in conjunction with the United States. See Note 17 in the accompanying consolidated financial statements for more information about our business and geographic segments.

13

Table of Contents

Employees

As of December 31, 2014, we had approximately 3,200 full-time employees, excluding our seasonal direct-to-home installation technicians, sales representatives and certain other support professionals. None of our employees are currently represented by labor unions or trade councils. We believe that we generally have good relationships with our employees. The majority of our employees are located in the Salt Lake City metropolitan area. Employees located outside of the Salt Lake City metropolitan area are primarily comprised of our FSPs, who service our subscribers and are located in all states in the United States except Maine and Vermont and all Canadian provinces except Quebec, and the monitoring professionals located at our monitoring station in South St. Paul, Minnesota.

Corporate Information

APX Group Holdings, Inc. was incorporated under the laws of the state of Delaware on October 26, 2012. Our principal executive offices are located at 4931 North 300 West, Provo, Utah 84604 and our telephone number is (801) 377-9111.

| ITEM 1A. | RISK FACTORS |

You should carefully consider the following risk factors and all other information contained in this annual report on Form 10-K. The risks and uncertainties described below are not the only risks facing us. Additional risks and uncertainties that we are unaware of, or those we currently deem immaterial, also may become important factors that affect us. The following risks could materially and adversely affect our business, financial condition, cash flows or results of operations.

Risks Related To Our Business

Our industry is highly competitive.

We operate in a highly competitive industry. We face competition from several large electronic residential security companies that have or may have greater capital and other resources than us. We also face, and may in the future face, competition from other providers of information and communication products and services, including cable and telecommunications companies, that may have greater capital and resources than us. Competitors that are larger in scale and have greater resources may benefit from greater economies of scale and other lower costs that permit them to offer more favorable terms to consumers (including lower service costs) than we offer, causing such consumers to choose to enter into contracts with such competitors. For instance, cable and telecommunications companies are expanding into the monitored security industry and are bundling their existing offerings with monitored security services. In some instances, it appears that the monitored security services component of such bundled offerings is significantly underpriced and, in effect, subsidized by the rates charged for the other services offered by these companies. These pricing alternatives may influence subscribers’ desire to subscribe to our services at rates and fees we consider appropriate. These competitors may also benefit from greater name recognition and superior advertising, marketing and promotional resources. To the extent that such competitors allocate greater resources to markets where our business is more highly concentrated, the negative impact on our business may increase over time. In addition to potentially reducing the number of new subscribers we are able to originate, increased competition could also result in higher attrition rates that would negatively impact us over time. The benefit offered to larger competitors from economies of scale and other lower costs may be magnified by an economic downturn in which subscribers put a greater emphasis on lower cost products or services. In addition, we face competition from regional competitors that concentrate their capital and other resources in targeting local markets.

We also face potential competition from improvements in do-it-yourself (“DIY”) and self-monitoring systems, which enable consumers to install their own systems and monitor and control their home environment, without third-party involvement or the need for a subscription agreement, through the Internet, text messages, emails or similar communications. Continued pricing pressure or improvements in technology and shifts in consumer preferences towards DIY and self-monitoring could adversely impact our subscriber base or pricing structure and have a material and adverse effect on our business, financial condition, results of operations and cash flows.

We resist competing on price alone because we believe we have competitive advantages such as a reputation for a high level of service and security. However, with cable and telecommunications companies actively targeting the Smart Home market and expanding into the monitored security space, and with large technology companies expanding into the connected home market through the development of their own solutions or the acquisition of other companies with Smart Home solution offerings, this increased competition could result in pricing pressure, a shift in customer preferences

14

Table of Contents

towards the services of these companies and reduce our market share. Continued pricing pressure from these competitors or failure to achieve pricing based on the competitive advantages previously identified above could prevent us from maintaining competitive price points for our products and services resulting in lost customers or in our inability to attract new customers and have an adverse effect on our business, financial condition, results of operations and cash flows.

We rely on long-term retention of subscribers and subscriber attrition can have a material adverse effect on our results.

We incur significant upfront costs to originate new subscribers. Accordingly, our long-term performance is dependent on our subscribers remaining with us for several years after the initial term of their contracts, which is generally between 36 and 60 months. A significant reason for attrition occurs when subscribers relocate and do not reconnect. Subscriber relocations are impacted by changes in the housing market. See “—Our business is subject to macroeconomic and demographic factors that may negatively impact our results of operations.” Some other factors that can increase subscriber attrition include problems experienced with our product or service quality, unfavorable general economic conditions, and the preference for lower pricing of competitors’ products and services over ours. If we fail to keep our customers for a sufficiently long period of time, our profitability, business, financial condition, results of operations and cash flows could be materially and adversely affected. Our inability to retain subscribers for a long term could materially and adversely affect our business, financial condition, cash flows or results of operations.

In addition, we amortize or depreciate our capitalized subscriber acquisition costs based on the estimated life of the subscriber relationships. If attrition rates were to rise significantly, we may be required to accelerate the amortization of expenses or the depreciation of assets related to such subscribers or to impair such assets, which could adversely impact our reported GAAP financial results.

Litigation, complaints or adverse publicity could negatively impact our business, financial condition and results of operations.

From time to time, we engage in the defense of, and may in the future be subject to, certain claims and lawsuits arising in the ordinary course of our business. For example, we have been named as defendants in putative class actions alleging violations of wage and hour laws, the Telephone Consumer Protection Act, common law privacy and consumer protection laws. In addition, we understand that the U.S. Attorney’s office for the District of Utah is engaged in an investigation that we believe relates to certain political contributions made by some of our executive officers and employees. From time to time our subscribers have communicated and may in the future communicate complaints to consumer protection groups and other organizations such as the Better Business Bureau, regulators, law enforcement or the media. Any resulting actions or negative subscriber sentiment or publicity may reduce the volume of our new subscriber originations or increase attrition of existing subscribers. Any of the foregoing may materially and adversely affect our business, financial condition, cash flows or results of operations.

Given our relationship with Vivint Solar and the fact that Vivint Solar uses our registered trademark, “Vivint”, in its name pursuant to a licensing agreement, our subscribers and potential subscribers may associate us with any problems experienced with Vivint Solar or adverse publicity related to their business. Because we have no control over Vivint Solar, we may not be able to take remedial action to cure any issues Vivint Solar has with its customers, and our trademark, brand and reputation may be adversely affected.

We are highly dependent on our ability to attract, train and retain an effective sales force.

Our business is highly dependent on our ability to attract, train and retain an effective sales force, especially for our peak April through August sales season. In addition, because sales representatives become more productive as they gain experience, retaining those individuals is very important for our success. If we are unable to attract, train and retain an effective sales force, our business, financial condition, cash flows or results of operations could be adversely affected.

Our operations depend upon telecommunication services providers to transmit signals to our third-party providers and our monitoring stations.

Our operations depend upon cellular and other telecommunications providers to communicate signals to and from our monitoring stations and subscribers in a timely, cost-efficient and consistent manner. The failure of one or more of these providers to transmit and communicate signals in a timely manner could affect our ability to provide services to our subscribers. There can be no assurance that third-party telecommunications providers and signal-processing centers will continue to transmit and communicate signals to our third-party providers and the monitoring stations without disruption. Any such disruption, particularly one of a prolonged duration, could have a material adverse effect on our business. In addition, failure to renew contracts with existing providers or to contract with other providers on commercially acceptable terms or at all may adversely impact our business.

15

Table of Contents

Certain elements of our operating model have historically relied on our subscribers’ continued selection and use of traditional landline telecommunications to transmit signals to our monitoring stations and to provide services to our subscribers. There is a growing trend for consumers to switch to the exclusive use of cellular, satellite or Internet communication technology in their homes, and telecommunication providers may discontinue their landline services in the future. In addition, many of our subscribers who use cellular communication technology for their systems use products that rely on older 2G technology, and certain telecommunication providers have discontinued 2G services in certain markets, and these and other telecommunication providers may discontinue 2G services in other markets in the future. The discontinuation of landline, 2G and any other services by telecommunications providers in the future would require subscribers to upgrade to alternative, and potentially more expensive, technologies. This could increase our subscriber attrition rates and slow our new subscriber originations. To maintain our subscriber base that uses components that are or could become obsolete, we may be required to upgrade or implement new technologies, including by offering to subsidize the replacement of subscribers’ outdated systems at our expense. Any such upgrades or implementations could require significant capital expenditures and also divert management’s attention and other important resources away from our customer service and new subscriber origination efforts.

Our interactive services are accessed through the Internet and our security monitoring services are increasingly delivered using Internet technologies. Some providers of broadband access may take measures that affect their customers’ ability to use these products and services, such as degrading the quality of the data packets we transmit over their lines, giving those packets low priority, giving other packets higher priority than ours, blocking our packets entirely or attempting to charge their customers more for using our services. In the U.S., there continues to be some uncertainty regarding whether suppliers of broadband Internet access have a legal obligation to allow their customers to access services such as ours without interference. In addition, the Federal Communications Commission (“FCC”) recently adopted net neutrality rules that may impact some aspects of our business. Because these rules are new, we do not yet know the impact the rules may have on our business. Interference with our services or higher charges to customers by broadband service providers for using our products and services could cause us to lose existing subscribers, impair our ability to attract new subscribers and materially and adversely affect our business, financial condition, results of operations and cash flows.

In addition, telecommunication services providers are subject to extensive regulation in the markets where we operate or may expand in the future. Changes in the applicable laws or regulations affecting telecommunication services could require us to change the way we operate, which could increase costs or otherwise disrupt our operations, which in turn could adversely affect our business, financial condition, cash flows or results of operations.

We must successfully upgrade and maintain our information technology systems.

We rely on various information technology systems to manage our operations. We are currently implementing modifications and upgrades to these systems, and have replaced our legacy systems with successor systems with new functionality.

There are inherent costs and risks associated with replacing and changing these systems and implementing new systems, including potential disruption of our internal control structure, substantial capital expenditures, additional administration and operating expenses, retention of sufficiently skilled personnel to implement and operate the new systems, demands on management time and other risks and costs of delays or difficulties in transitioning to new systems or of integrating new systems into our current systems. For example, we encountered issues associated with the implementation of our new integrated CRM system, which resulted in an immaterial error in our financial statements for the quarter ended June 30, 2014. This error was corrected during the quarter ended September 30, 2014. As a result of the issues encountered associated with the CRM implementation, we also issued a significant number of billing-related subscriber credits during the year ended December 31, 2014, which reduced our revenue. While management makes efforts to identify and remediate issues, we can provide no assurance that our remediation efforts will be successful or that we will not encounter additional issues as we complete the implementation of these and other systems. In addition, our information technology system implementations may not result in productivity improvements at a level that outweighs the costs of implementation, or at all. The implementation of new information technology systems may also cause disruptions in our business operations and have an adverse effect on our business, cash flows and operations.

Privacy and data protection laws, privacy or data breaches, or the loss of data could have a material adverse effect on our business.

In the course of our operations, we gather, process, transmit and store subscriber information, including personal, payment, credit and other similar confidential and private information. We use some of this information for operational and marketing purposes and rely on proprietary and commercially available systems, software, tools and monitoring to provide security for such information.

16

Table of Contents

Our collection, retention, transfer and use of this information is regulated by privacy and data protection laws and regulations and industry standards. Our compliance with these laws, regulations and standards increases our operating costs, and additional laws, regulations or standards (and new interpretations of existing laws and regulations) in these areas may further increase our operating costs and adversely affect our ability to effectively market our products and services. Our failure to comply with any of these laws, regulations or standards could result in a loss of subscriber data, fines, sanctions and other liabilities and additional restrictions on our collection, transfer or use of subscriber data. In addition, our failure to comply with any of these laws, regulations or standards could result in a material adverse effect on our reputation, subscriber attrition, new subscriber origination, financial condition, cash flows or results of operations.

Criminals and other nefarious actors are using increasingly sophisticated methods, including cyber-attacks, to capture or alter various types of information relating to subscribers, to engage in illegal activities such as fraud and identity theft, and to expose and exploit potential security and privacy vulnerabilities in corporate systems and web sites. Unauthorized intrusion into the portions of our systems and data storage devices that process and store subscriber information, including but not limited to subscriber transactions and other confidential and private information or the loss of such information, may result in negative consequences. In addition, third parties, including our partners and vendors, could also be a source of security risk to us in the event of a failure of their own security systems and infrastructure. Moreover, we cannot be certain that advances in criminal capabilities, new discoveries in the field of cryptography or other developments will not compromise or breach the technology protecting the networks that access our products and services. Any such compromises or breaches to the systems or loss of data, whether by us, our partners and vendors, or other third parties or as a result of employee error or malfeasance or otherwise, could cause interruptions in operations and damage to our reputation, subject us to costs and liabilities and materially and adversely affect sales, revenues and profits, which in turn could have a material adverse impact on our business, financial condition, cash flows or results of operations.

We are subject to payment related risks.