Attached files

| file | filename |

|---|---|

| EX-10.BBAL - TECH DATA DEFERRED COMPENSATION PLAN TRUST AGREEMENT - TECH DATA CORP | exhibit10-bbal.htm |

| EX-32.A - CERTIFICATION - TECH DATA CORP | exhibit32-afy15.htm |

| EX-31.A - CERTIFICATION - TECH DATA CORP | exhibit31-afy15.htm |

| EX-32.B - CERTIFICATION - TECH DATA CORP | exhibit32-bfy15.htm |

| EX-31.B - CERTIFICATION - TECH DATA CORP | exhibit31-bfy15.htm |

| EX-23.A - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - TECH DATA CORP | exhibit23-afy15.htm |

| EXCEL - IDEA: XBRL DOCUMENT - TECH DATA CORP | Financial_Report.xls |

| EX-21.A - SUBSIDIARIES OF REGISTRANT - TECH DATA CORP | exhibit21-afy15.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended January 31, 2015

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number 0-14625

TECH DATA CORPORATION

(Exact name of Registrant as specified in its charter)

Florida | 59-1578329 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) |

5350 Tech Data Drive Clearwater, Florida | 33760 |

(Address of principal executive offices) | (Zip Code) |

Securities registered pursuant to Section 12(b) of the Act:

Common stock, par value $.0015 per share

Securities registered pursuant to Section 12 (g) of the Act: None

Indicate by a check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by a check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “accelerated filer”, “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated Filer | x | Accelerated Filer | ¨ |

Non-accelerated Filer | ¨ | Smaller Reporting Company Filer | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨No x

Aggregate market value of the voting stock held by non-affiliates was $2,303,476,266 based on the reported last sale price of common stock on July 31, 2014 which is the last business day of the registrant’s most recently completed second fiscal quarter.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

Class | March 11, 2015 |

Common stock, par value $.0015 per share | 36,631,255 |

DOCUMENTS INCORPORATED BY REFERENCE

The registrant’s Proxy Statement for use at the Annual Meeting of Shareholders on June 3, 2015, is incorporated by reference in Part III of this Form 10-K to the extent stated herein.

1

TABLE OF CONTENTS

ITEM 1. | ||

ITEM 1A. | ||

ITEM 1B. | ||

ITEM 2. | ||

ITEM 3. | ||

ITEM 4. | ||

ITEM 5. | ||

ITEM 6. | ||

ITEM 7. | ||

ITEM 7A. | ||

ITEM 8. | ||

ITEM 9. | ||

ITEM 9A. | ||

ITEM 9B. | ||

ITEM 10 | ||

ITEM 11 | ||

ITEM 12 | ||

ITEM 13 | ||

ITEM 14. | ||

ITEM 15. | ||

Exhibits | ||

Certifications | ||

2

PART I

ITEM 1. Business.

Overview

Tech Data Corporation is one of the world’s largest wholesale distributors of technology products. We serve as an indispensable link in the technology supply chain by bringing products from the world’s leading technology vendors to market, as well as providing our customers with advanced logistics capabilities and value-added services. Our customers include approximately 115,000 value-added resellers (“VARs”), direct marketers, retailers and corporate resellers who support the diverse technology needs of end users. We sell to customers in more than 100 countries throughout North America, South America, Europe, the Middle East and Africa. The two primary geographic markets we serve are the Americas and Europe. For a discussion of our geographic reporting segments, see Item 8, "Financial Statements and Supplementary Data.”

The Company’s financial objectives are to grow sales at or above the overall IT market growth rate by gaining share in select product areas, grow earnings in local currency, generate positive cash flow, and earn a return on invested capital above our weighted average cost of capital. To achieve this, we focus on a strategy of excellence in execution, diversification and innovation that we believe differentiates our business in the marketplace.

Execution is fundamental to our business success. We have 26 logistics centers where each day, tens of millions of dollars of technology products are received from vendors, picked and packed and shipped to our customers. Products are generally shipped from regionally located logistics centers the same day the orders are received. In addition, execution is marked by a high level of service provided to our customers through our company’s technical, sales and marketing support, electronic commerce tools, product integration services and financing programs.

Our diversification strategy seeks to continuously remix our product, customer and services portfolios towards higher growth and higher return market segments through organic growth initiatives and acquisitions. We believe that as industry standardization, mobility, cloud computing, the convergence of consumer and professional devices and other potentially disruptive factors transform the way technology is used and delivered, we will leverage our highly efficient infrastructure to capture new market opportunities in specialty areas, such as data center, software, mobility and consumer electronics.

The final tenet of our strategy is innovation. Our IT systems and e-business tools and programs have provided our business with the flexibility to effectively navigate fluctuations in market conditions, structural changes in the technology industry, as well as changes created by products we sell. These IT systems and e-business tools and programs have also worked to strengthen our vendor and customer relationships, while at the same time improving the efficiency of these business partners.

We believe our strategy of execution, diversification and innovation will continue to strengthen our value proposition with vendor partners and reseller customers while positioning us for continued market expansion and profitable growth.

History

Tech Data was incorporated in 1974 to market data processing supplies such as tapes, disk packs, and custom and stock tab forms for mini and mainframe computers directly to end users. With the advent of microcomputer dealers, we made the transition to a wholesale distributor in 1984 by broadening our product line to include hardware products and withdrawing entirely from end-user sales.

From fiscal 1989 through fiscal 2007, we expanded geographically through the acquisitions of several distribution companies in both the Americas and Europe, significantly strengthening our position in certain product and customer segments.

In fiscal 2008, we executed a joint venture agreement with Brightstar Corp. ("Brightstar"), one of the world’s largest wireless products distributors and supply chain solutions providers. Brightstar Europe Limited ("BEL"), our consolidated joint venture with Brightstar, distributed mobile phones and other wireless devices to a variety of customers including mobile operators, dealers, agents, retailers and e-tailers in certain European markets. During the third quarter of fiscal 2013, we acquired Brightstar's fifty percent ownership interest in BEL. The terms of the acquisition agreement included a payment of $165.9 million in cash for Brightstar's equity in BEL and the repayment of all loans advanced by Brightstar to BEL.

In fiscal 2011, we continued to support our diversification strategy by completing five acquisitions in Europe, including the acquisition of Triade Holding B.V. (“Triade”), a privately-held portfolio of leading value-added distributors of consumer electronics and information technology products in the Benelux region, Denmark and Norway. We believe the acquisition of Triade strengthened our presence in these geographies and enabled us to accelerate our diversification strategy into the consumer electronics business in Europe, while leveraging our logistics infrastructure. In a related transaction, BEL acquired Triade’s mobility subsidiaries in Belgium and the Netherlands, significantly extending BEL’s mobility operations in Europe.

3

In fiscal 2012, we made two acquisitions in the European technology distribution marketplace. While the acquisitions did not have a significant impact on our consolidated results of operations, the addition of these businesses expanded our product and customer portfolios and continued to add desired skill sets, while leveraging our logistics infrastructure in Europe. Also in fiscal 2012, expanding upon the success of our mobility distribution joint venture in Europe, we executed an agreement with Brightstar to establish a joint venture in the United States, hereinafter referred to as TDMobility. TDMobility simplifies the selling, delivery and support of mobile services for our reseller customers serving the small and medium business markets. During the fourth quarter of fiscal 2014, we acquired Brightstar's fifty percent ownership interest in TDMobility.

In fiscal 2013, we completed the acquisition of several distribution companies of Specialist Distribution Group (collectively "SDG"), the distribution arm of Specialist Computer Holdings PLC (“SCH”), a privately-held IT services company headquartered in the United Kingdom, for a final purchase price of approximately $358 million. Management believes the acquisition of SDG supports the Company’s diversification strategy by strengthening its European value and broadline offerings in key markets and expanding the Company’s vendor and customer portfolios, while leveraging the Company’s existing pan-European infrastructure.

In the fourth quarter of fiscal 2015, we committed to a plan to sell our business operations in Chile and Peru and in March 2015, the Company entered into an agreement for the sale of these operations. Additionally, in March 2015, we committed to a plan to exit our business operations in Uruguay. The operating results of these entities during fiscal 2015, 2014 and 2013 were insignificant relative to our consolidated financial results.

Industry

The wholesale distribution model has proven to be well suited for both manufacturers and publishers of technology products (also referred to in this document as “vendors”) and resellers of those products. The large number of resellers makes it cost efficient for vendors to rely on wholesale distributors to serve this diverse and highly fragmented customer base.

Resellers in the traditional distribution model are able to build efficiencies and reduce their costs by relying on distributors, such as Tech Data, for a number of services, including multi-vendor solutions, product configuration/integration, marketing support, financing, technical support, and inventory management, which includes direct shipment to end-users and, in some cases, provides end-users with the distributors’ inventory availability.

Due to the large number of vendors and products, resellers often cannot, or choose not to, establish direct purchasing relationships with vendors. As a result, they frequently rely on wholesale distributors, such as Tech Data, who leverage purchasing costs across multiple vendors to satisfy a significant portion of the resellers' product procurement, logistics, financing, marketing and technical support needs.

The technology distribution industry continues to address a broad spectrum of reseller and vendor requirements. While some vendors have elected to sell directly to resellers or end-users for particular customer and product segments, we believe that a vast majority of vendors continue to embrace traditional distributors that have proven capabilities to manage multiple products and resellers, provide access to fragmented markets, and deliver products in a cost-effective and efficient manner.

New products and market opportunities have helped to offset the impact on technology distributors of vendor direct sales. Further, vendors continue to seek the logistics expertise of distributors to penetrate highly fragmented markets such as the small- and medium-sized business (“SMB”) sector, which relies on VARs, our primary customer base, to gain access to and support for new technology. The economies of scale and global reach of large industry-leading and well-capitalized distributors are expected to continue to be significant competitive advantages in this marketplace.

Products and Vendors

We distribute and market hundreds of thousands of products from more than 1,100 of the world’s leading technology hardware suppliers, networking equipment suppliers, software publishers, and other suppliers of technology peripherals, physical security, consumer electronics, digital signage and mobile phone hardware and accessories. These products are typically purchased directly from the vendor on a non-exclusive basis. Conversely, our vendor agreements do not restrict us from selling similar products manufactured by competitors, nor do they require us to sell a specified quantity of product. As a result, we have the flexibility to terminate or curtail sales of one product line in favor of another due to technological change, pricing considerations, product availability, customer demand, or vendor distribution policies. Overall, we believe that our diversified and evolving product portfolio will provide a solid platform for continued growth.

We continually evolve our product line in order to provide our customers with access to the latest technology products. However, from time to time, the demand for certain products that we sell exceeds the supply available from the vendor. In such cases, we generally receive an allocation of the available products. We believe that our ability to compete is not adversely affected by these periodic shortages and the resulting allocations.

4

We believe that our vendor agreements are in the form customarily used by manufacturers and distributors. Agreements typically contain provisions that allow termination by either party upon a short notice period. In most instances, a vendor who elects to terminate a distribution agreement will repurchase the vendor’s products carried in the distributor’s inventory.

Most of our vendor agreements also allow for stock rotation and price protection provisions. Stock rotation rights give us the ability, subject to certain limitations, to return for credit or exchange a portion of those inventory items purchased from the vendor. Price protection situations occur when a vendor credits us for declines in inventory value resulting from the vendor’s price reductions. Along with our inventory management policies and practices, these provisions reduce our risk of loss due to slow-moving inventory, vendor price reductions, product updates or obsolescence.

Sometimes the industry practices discussed above are not embodied in agreements and do not protect us in all cases from declines in inventory value. However, we believe that these practices provide a significant level of protection from such declines, although no assurance can be given that such practices will continue or that they will adequately protect us against declines in inventory value. We sell products in various countries throughout the world, and product categories may vary from region to region. Our consolidated revenue mix may fluctuate between and within our operating segments as well as within our product categories. These fluctuations can be influenced by our diversification strategies, new product offerings and supply and demand fluctuations within our operating regions.

Our consolidated net sales for fiscal 2015, 2014 and 2013 within our strategic focus categories approximated the following:

2015 | 2014 | 2013 | |

Broadline | 47% | 46% | 47% |

Data Center | 22% | 23% | 21% |

Software | 18% | 18% | 19% |

Mobility | 10% | 9% | 8% |

Consumer Electronics | 3% | 4% | 5% |

Our strategic focus categories include the following products:

• | Broadline - We define our broadline category to include, among other products, notebooks, tablets, desktop systems, printers, supplies and components. |

• | Data Center - We define our data center category to include products such as servers, server accessories, networking products, storage hardware and networking support services. |

• | Software - We define our software category as a broad variety of applications containing computer instructions or data that can be stored electronically. We offer a variety of software products, such as virtualization software, security software (firewalls, intrusion, detection and encryption), desktop application software, operating system software, utilities software and software service and support. |

• | Mobility - We define our mobility category to include mobile handsets, navigation devices, aircards, SIM cards and other mobility-related accessories. |

• | Consumer Electronics - We define our consumer electronics category to include car and home audio / visual equipment, blue-ray and DVD players, televisions and related accessories, cameras and related accessories, gaming and home appliances. |

We generated approximately 19%, 21% and 21% of our consolidated net sales in fiscal 2015, 2014 and 2013, respectively, from products purchased from Hewlett-Packard Company. In addition, approximately 15%, 13% and 12% of our consolidated net sales in fiscal 2015, 2014 and 2013 were from products purchased from Apple, Inc. There were no other vendors that accounted for 10% or more of our consolidated net sales in fiscal 2015, 2014 or 2013.

Customers and Services

Our products are purchased directly from vendors in significant quantities and are marketed to an active reseller base of approximately 115,000 VARs, direct marketers, retailers and corporate resellers. While we sell products in various countries throughout the world, and customer channels may vary from region to region, during fiscal 2015, 2014 and 2013 sales within our consolidated customer channels approximated the following:

2015 | 2014 | 2013 | |

VARs | 45% | 51% | 52% |

Direct marketers and retailers | 30% | 28% | 27% |

Corporate resellers | 25% | 21% | 21% |

5

No single customer accounted for more than 10% of our net sales during fiscal 2015, 2014 or 2013.

The market for VARs is attractive because VARs generally rely on distributors as their principal source of technology products and the related financing for the products. This reliance is due to VARs typically not wanting to invest the resources to establish a large number of direct purchasing relationships or stock significant product inventories. Direct marketers, retailers and corporate resellers may establish direct relationships with vendors for their highest volume products, but utilize distributors as the primary source for other product requirements and an alternative source for products acquired directly.

In addition to an extensive product offering from the world's leading technology vendors, we provide resellers a high level of customer service through our training and technical support, suite of electronic commerce tools (including internet order entry and electronic data interchange (“EDI”) services), customized shipping documents, product configuration/integration services and access to flexible financing programs. We also provide services to our vendors by providing them the opportunity to participate in a number of special promotions, and marketing services targeted to the needs of our resellers. While these services are important to our customers, they contribute less than 10% of our consolidated net sales.

We provide our vendors with access to one of the largest bases of resellers throughout the Americas and Europe, delivering products to them from our 26 regionally located logistics centers. We have located our logistics centers near our customers which enables us to deliver products on a timely basis, thereby reducing the customers’ need to invest in inventory (see also Item 2, "Properties" for further discussion of our locations and logistics centers).

Sales and Electronic Commerce

Our sales team consists of field sales and inside telemarketing sales representatives. The sales representatives are provided comprehensive training on our policies and procedures, and the technical specifications of products, and attend product seminars offered by our vendors. Field sales representatives are typically located in major metropolitan areas in their respective geographies and are supported by inside telemarketing sales teams covering a designated territory. Our team concept provides a strong personal relationship between our customers’ representatives and Tech Data. Territories with no field representation are serviced exclusively by inside telemarketing sales teams. Customers typically call our inside sales teams on dedicated telephone numbers or contact us through various electronic methods to place orders. If the product is in stock and the customer has available credit, customer orders are generally shipped the same day from the logistics center nearest the customer or the intended end-user.

Customers often utilize our electronic ordering and information systems. Through our website, customers can gain remote access to our information systems to place orders, or check order status, inventory availability and pricing. Certain of our larger customers have EDI services available whereby orders, order acknowledgments, invoices, inventory status reports, customized pricing information and other industry standard EDI transactions are consummated on-line, which improves efficiency and timeliness for the Company and our customers. In both fiscal 2015 and 2014, approximately 45% of our consolidated net sales originated from orders received electronically.

Competition

We operate in a market characterized by intense competition, based on such factors as product availability, credit terms and availability, price, speed of delivery, effectiveness of information systems and e-commerce tools, ability to tailor solutions to customers' needs, quality and depth of product lines and training, as well as service and support provided by the distributor to the customer. We believe we are well equipped to compete effectively with other distributors in all of these areas.

We compete against several distributors in the Americas market, including broadline product distributors such as Ingram Micro Inc. ("Ingram Micro"), Synnex Corp., and to a lesser extent, more specialized distributors such as Arrow Electronics, Inc. (“Arrow”) and Avnet, Inc. (“Avnet”), along with some regional and local distributors. The competitive environment in Europe is more fragmented, with market share spread among several regional and local competitors such as ALSO/Actebis and Esprinet, as well as international distributors such as Ingram Micro, Westcon Group, Inc., Arrow and Avnet.

The Company also faces competition from companies entering or expanding into the logistics and product fulfillment and e-commerce supply chain services market and certain direct sales relationships between manufacturers, resellers, and end-users continue to introduce change into the competitive landscape of our industry. As we expand our business into new areas, we may face increased competition from other distributors as well as vendors. However, we believe vendors will continue to sell their products through distributors, such as Tech Data, due to our ability to provide them with access to our broad customer base and serve them in a highly cost-effective and efficient manner. Our logistics capabilities, as well as our sales and marketing, credit and product management expertise, allow our vendors to expand their market coverage while lowering their selling, inventory and fulfillment costs.

Employees

On January 31, 2015, we had approximately 8,900 employees (as measured on a full-time equivalent basis). Certain of our employees in various countries outside of the United States are subject to laws providing representation rights to employees on workers' councils.

6

Our success depends on the talent and dedication of our employees and we strive to attract, hire, develop and retain outstanding employees. We believe significant benefits are realized from having a strong and seasoned management team with many years of experience in technology distribution and related industries. We consider relations with our employees to be good.

Foreign and Domestic Operations and Export Sales

We operate predominately in a single industry segment as a distributor of technology products, logistics management, and other value-added services. While we operate primarily in one industry, we manage our business in two geographic segments: the Americas and Europe.

Over the past several years, we have entered new geographic markets, expanded our presence in existing markets and exited certain markets based upon our assessment of, among other factors, our earnings potential and the risk exposure in those markets, including foreign currency exchange, regulatory and political risks. To the extent we decide to close any of our operations, we may incur charges and operating losses related to such closures and recognize a portion of our accumulated other comprehensive income in connection with such a disposition. For information on our net sales, operating income and identifiable assets by geographic region, see Note 14 of Notes to Consolidated Financial Statements.

Asset Management

We manage our inventories in a manner that allows us to maintain sufficient quantities to achieve high order fill rates while attempting to stock only those products in high demand that have a rapid turnover rate. Our business, like that of other distributors, is subject to the risk that the value of inventory will be impacted adversely by suppliers’ price reductions or by technological changes affecting the usefulness or desirability of the products comprising the inventory. Our contracts with most of our vendors provide price protection and stock rotation privileges to reduce the risk of loss due to manufacturer price reductions and slow moving or obsolete inventory. In the event of a vendor price reduction, we generally receive a credit for the impact on products in inventory and we have the right to rotate a certain percentage of purchases, subject to certain limitations. Historically, price protection and stock rotation privileges, as well as our inventory management procedures, have helped reduce the risk of loss of inventory value.

We attempt to control losses on credit sales by closely monitoring customers’ creditworthiness through our IT systems, which contain detailed information on each customer’s payment history and other relevant information. In certain countries, we have obtained credit insurance that insures a percentage of the credit extended by us to certain customers against possible loss. The Company also uses floorplan financing arrangements as an additional approach to mitigate credit risk. Customers who qualify for credit terms are typically granted net 30-day payment terms in the Americas. While credit terms in Europe vary by country, the vast majority of customers are granted credit terms ranging from 30 to 60 days. We also sell products on a prepayment, credit card and cash-on-delivery basis. In addition, certain of the Company’s vendors subsidize floorplan financing arrangements for the benefit of our customers.

Additional Information Available

Our principal Internet address is www.techdata.com. We provide our annual and quarterly reports free of charge on www.techdata.com, as soon as reasonably practicable after they are electronically filed with, or furnished to, the Securities and Exchange Commission (“SEC”). We provide a link to all SEC filings where current reports on Form 8-K and any amendments to previously filed reports may be accessed, free of charge. Information on Tech Data’s website is not incorporated into this Form 10-K or the Company’s other securities filings and is not a part of them.

Executive Officers

The following table sets forth the name, age and title of each of the persons who were serving as executive officers of Tech Data as of March 11, 2015:

7

Name | Age | Title | ||

Robert M. Dutkowsky | 60 | Chief Executive Officer | ||

Jeffery P. Howells | 57 | Executive Vice President and Chief Financial Officer | ||

Néstor Cano | 50 | President, Europe | ||

Joseph H. Quaglia | 50 | President, the Americas | ||

John A. Tonnison | 46 | Executive Vice President and Chief Information Officer | ||

Alain Amsellem | 55 | Senior Vice President and Chief Financial Officer, Europe | ||

Charles V. Dannewitz | 60 | Senior Vice President and Chief Financial Officer, the Americas | ||

Joseph B. Trepani | 54 | Senior Vice President and Corporate Controller | ||

David R. Vetter | 55 | Senior Vice President, General Counsel and Secretary | ||

Robert M. Dutkowsky, Chief Executive Officer, joined Tech Data as Chief Executive Officer and was appointed to the Board of Directors in October 2006. His career began with IBM where, during his 20-year tenure, he served in several senior management positions including Vice President, Distribution - IBM Asia/Pacific. Prior to joining Tech Data, Mr. Dutkowsky served as President, CEO, and Chairman of the Board of Egenera, Inc. (a software and virtualization technology company), from 2004 until 2006, and served as President, CEO, and Chairman of the Board of J.D. Edwards & Co., Inc. (a software company) from 2002 until 2004. He was President, CEO, and Chairman of the Board of GenRad, Inc. from 2000 until 2002. Starting in 1997, Mr. Dutkowsky was Executive Vice President, Markets and Channels, at EMC Corporation before being promoted to President, Data General, in 1999. Mr. Dutkowsky holds a B.S. degree in Industrial and Labor Relations from Cornell University.

Jeffery P. Howells, Executive Vice President and Chief Financial Officer, joined the Company in October 1991 as Vice President of Finance and was promoted to Chief Financial Officer in March 1992. In March 1993, he became Senior Vice President and Chief Financial Officer. In 1997, he was promoted to Executive Vice President and Chief Financial Officer and in 1998 was appointed to the Board of Directors. Prior to joining the Company, Mr. Howells was employed by Price Waterhouse for 11 years. Mr. Howells is a Certified Public Accountant and holds a B.B.A. degree in Accounting from Stetson University.

Néstor Cano, President, Europe, joined Computer 2000 (and the Company via acquisition) in July 1989 as a Software Product Manager and served in various management positions within the Company’s operations in Spain and Portugal from 1990 to 1995, after which time he was promoted to Regional Managing Director. In March 1999, he was appointed Executive Vice President of U.S. Sales and Marketing, and in January 2000 was promoted to President, the Americas. Mr. Cano was promoted to President, Worldwide Operations in August 2000 and was appointed to President, Europe in June 2007. Mr. Cano holds a PDG (similar to an Executive MBA) from IESE Business School in Barcelona and an Engineering Degree from Barcelona University.

Joseph H. Quaglia, President, the Americas, joined the Company in May 2006 as Vice President, East and Government Sales and was promoted to Senior Vice President of U.S. Marketing in November 2007. In February 2012, he was appointed to the additional role of President, TDMobility and he was promoted to President, the Americas in November 2013. Prior to joining the Company, Mr. Quaglia held senior management positions with CA Technologies, StorageNetworks Inc. and network software provider Atabok. Mr. Quaglia holds a B.S. in Computer Science from Indiana State University and an M.B.A. from Butler University.

John A. Tonnison, Executive Vice President and Chief Information Officer, joined the Company in March 2001 as Vice President, Worldwide E-Business and was promoted to Senior Vice President of IT Americas in December 2006. In February 2010, he was appointed to Executive Vice President and Chief Information Officer. Prior to joining the Company, Mr. Tonnison held executive management positions in the U.S., United Kingdom and Germany with Computer 2000, Technology Solutions Network and Mancos Computers. Mr. Tonnison was educated in the United Kingdom and became a U.S. citizen in 2006.

Alain Amsellem, Senior Vice President and Chief Financial Officer, Europe, joined the Company in 1994 through Tech Data’s acquisition of French distributor, Softmart International S.A. and served as France Finance Director until September 1999 when he was promoted to France Managing Director. In August 2004, Mr. Amsellem was promoted to Senior Vice President of Southern Europe, and was appointed Senior Vice President - Europe Finance & Operations in 2007. In February 2014, he was appointed Senior Vice President and Chief Financial Officer, Europe. Mr. Amsellem is a Chartered Accountant and holds a degree in management and chartered accountancy from Paris Dauphine University.

Charles V. Dannewitz, Senior Vice President and Chief Financial Officer, the Americas, joined the Company in February 1995 as Vice President of Taxes. He was promoted to Senior Vice President of Taxes in March 2000, and assumed responsibility for worldwide treasury operations in July 2003. In February 2014, he was appointed Senior Vice President and Chief Financial Officer, the Americas. Prior to joining the Company, Mr. Dannewitz was employed by Price Waterhouse from 1981 to 1995, most recently as a tax partner.

8

Mr. Dannewitz is a Certified Public Accountant and holds a Bachelor of Science Degree in Accounting from Illinois Wesleyan University.

Joseph B. Trepani, Senior Vice President and Corporate Controller, joined the Company in March 1990 as Controller and held the position of Director of Operations from October 1991 through January 1995. In February 1995, he was promoted to Vice President and Worldwide Controller and to Senior Vice President and Corporate Controller in March 1998. Prior to joining the Company, Mr. Trepani was Vice President of Finance for Action Staffing, Inc. from 1989 to 1990. From 1982 to 1989, he was employed by Price Waterhouse. Mr. Trepani is a Certified Public Accountant and holds a Bachelor of Science Degree in Accounting from Florida State University.

David R. Vetter, Senior Vice President, General Counsel and Secretary, joined the Company in June 1993 as Vice President and General Counsel and was promoted to Corporate Vice President and General Counsel in April 2000. In March 2003, he was promoted to his current position of Senior Vice President, and effective July 2003, was appointed Secretary. Prior to joining the Company, Mr. Vetter was employed by the law firm of Robbins, Gaynor & Bronstein, P.A. from 1984 to 1993, most recently as a partner. Mr. Vetter is a member of the Florida Bar Association and holds Bachelor of Arts Degrees in English and Economics from Bucknell University and a Juris Doctorate Degree from the University of Florida.

9

ITEM 1A. Risk Factors.

The following are certain risk factors that could affect our business, financial position and results of operations. These risk factors should be considered in connection with evaluating the forward-looking statements contained in this Annual Report on Form 10-K because these factors could cause the actual results and conditions to differ materially from those projected in the forward-looking statements. Before you buy our common stock or other securities, you should know that making such an investment involves risks, including the risks described below. The risks that have been highlighted below are not the only risks of our business. If any of the risks actually occur, our business, financial condition or results of operations could be negatively affected. In that case, the trading price of our common stock or other securities could decline, and you may lose all or part of your investment. Risk factors that could cause actual results to differ materially from our forward-looking statements are as follows:

Our ability to earn profit is more challenging when sales slow from a down economy as a result of gross profit declining faster than cost reduction efforts taking effect.

High levels of unemployment in the markets we serve, as well as austerity measures that may be implemented by governments in those markets, can constrain economic growth resulting in lower demand for the products and services we sell. When we experience a rapid decline in demand for products we experience more difficulty in achieving the gross profit and operating profit we desire due to the lower sales and increased pricing pressure. The economic environment may also result in changes in vendor terms and conditions, such as rebates, cash discounts and cooperative marketing efforts, which may also result in downward pressure on our gross profit. As a result, there is pressure to reduce the cost of operations in order to maximize operating profits. To the extent we cannot reduce costs to offset such decline in gross profits, our operating margins typically deteriorate. The benefits from cost reductions may also take longer to fully realize and may not fully mitigate the impact of the reduced demand. Should we experience a decline in operating profits, especially in Europe, the valuations we develop for purposes of our goodwill impairment test may be adversely affected, potentially resulting in impairment charges. Deterioration in the financial and credit markets heightens the risk of customer bankruptcies and delays in payment. Future deterioration in the credit markets could result in reduced availability of credit insurance to cover customer accounts. This, in turn, may result in our reducing the credit lines we provide to customers, thereby having a negative impact on our net sales.

Our competitors can take more market share by reducing prices on key vendor products that contribute the most to our profitability.

The Company operates in a highly competitive environment. The technology distribution industry is characterized by intense competition, based primarily on product availability, credit terms and availability, price, effectiveness of information systems and e-commerce tools, speed of delivery, ability to tailor specific solutions to customer needs, quality and depth of product lines and training, service and support. Our customers are not required to purchase any specific volume of products from us and may move business if pricing is reduced by competitors, resulting in lower sales. As a result, we must be extremely flexible in determining when to reduce price to maintain market share and sales volumes and when to allow our sales volumes to decline to maintain the quality of our profitability. The Company competes with a variety of regional, national and international wholesale distributors, some of which may have greater financial resources than the Company.

We are dependent on internal information and telecommunications systems, and any failure of these systems, including system security breaches, data protection breaches, or other cybersecurity attacks, may negatively impact our business and results of operations.

The Company is highly dependent upon its internal information and telecommunications systems to operate its business. Failures of our internal information or telecommunications systems may prevent us from taking customer orders, shipping products and billing customers. Sales may also be impacted if our customers are unable to access our pricing and product availability information. Additionally, if the Company were to experience a security breakdown, disruption or breach that compromised sensitive information, it could harm our relationships with vendors and customers. The occurrence of any of these events could have a negative impact on our business and results of operations.

We may not be able to ship products if our third party shipping companies cease operations temporarily or permanently.

The Company relies on arrangements with independent shipping companies for the delivery of its products from vendors and to customers. The failure or inability of these shipping companies to deliver products, or the unavailability of their shipping services, even temporarily, may have an adverse effect on the Company's business.

10

If our vendors do not continue to provide price protection for inventory we purchase from them our profit from the sale of that inventory may decline.

It is very typical in our industry that the value of inventory will decline as a result of price reductions by vendors or technological obsolescence. It is the policy of most of our vendors to protect distributors from the loss in value of inventory due to technological change or the vendors' price reductions. Some vendors, however, may be unwilling or unable to pay the Company for price protection claims or products returned to them under purchase agreements. Moreover, industry practices are sometimes not embodied in written agreements and do not protect the Company in all cases from declines in inventory value. No assurance can be given that such practices to protect distributors will continue, that unforeseen new product developments will not adversely affect the Company, or that the Company will be able to successfully manage its existing and future inventories.

Failure to obtain adequate product supplies from our largest vendors, or terminations of a supply or services agreement, or a significant change in vendor terms or conditions of sale by our largest vendors may negatively affect our revenue and operating profit.

The Company receives a significant percentage of revenues from products it purchases from certain vendors, such as Hewlett-Packard Company and Apple, Inc. These vendors have significant negotiating power over us and rapid, significant and adverse changes in sales terms and conditions, such as reducing the amount of price protection and return rights as well as reducing the level of purchase discounts and rebates they make available to us, may reduce the profit we can earn on these vendors' products and result in loss of revenue and profitability. The Company's gross profit could be negatively impacted if the Company is unable to pass through the impact of these changes to the Company's customers or cannot develop systems to manage ongoing vendor programs. In addition, the Company's standard vendor distribution agreement permits termination without cause by either party upon 30 days notice. The loss of a relationship with any of the Company's key vendors, a change in their strategy (such as increasing direct sales), the merging of significant vendors, or significant changes in terms on their products may adversely affect the Company's business.

Changes in our credit rating or other market factors may increase our interest expense or other costs of capital or capital may not be available to us on acceptable terms to fund our working capital needs. The inability to obtain such sources of capital could have an adverse effect on the Company's business.

The Company's business requires substantial capital to operate and to finance accounts receivable and product inventory that are not financed by trade creditors. The Company has historically relied upon cash generated from operations, bank credit lines, trade credit from vendors, proceeds from public offerings of its common stock and proceeds from debt offerings to satisfy its capital needs and finance growth. The Company utilizes various financing instruments such as receivables securitization, leases, revolving credit facilities and trade receivable purchase agreements. As the financial markets change and new regulations come into effect, the cost of acquiring financing and the methods of financing may change. Changes in our credit rating or other market factors may increase our interest expense or other costs of capital or capital may not be available to us on acceptable terms to fund our working capital needs. The inability to obtain such sources of capital could have an adverse effect on the Company's business. The Company's credit facilities contain various financial and other covenants that may limit the Company's ability to borrow, or limit the Company's flexibility in responding to business conditions. These financing instruments involve variable rate debt, thus exposing the Company to risk of fluctuations in interest rates. Increases in interest rates would result in an increase in the interest expense on the Company's variable debt, which would reduce the Company's profitability.

We conduct business in countries outside of the United States, which exposes us to fluctuations in foreign currency exchange rates that result in losses in certain periods.

Approximately 68%, 67% and 67% of our revenues in fiscal 2015, 2014 and 2013 were generated in countries outside of the United States, which exposes the Company to fluctuations in foreign currency exchange rates. The Company may enter into short-term forward exchange or option contracts to hedge this risk. Nevertheless, volatile foreign currency exchange rates increase our risk of loss related to products purchased in a currency other than the currency in which those products are sold. While we maintain policies to protect against fluctuation in currency exchange rates, extreme fluctuations have resulted in our incurring losses in some countries. The realization of any or all of these risks could have a significant adverse effect on our financial results. The translation of the financial statements of foreign operations into U.S. dollars is also impacted by fluctuations in foreign currency exchange rates, which may positively or negatively impact our results of operations. In addition, the value of the Company's equity investment in foreign countries may fluctuate based upon changes in foreign currency exchange rates. These fluctuations, which are recorded in a cumulative translation adjustment account, may result in losses in the event a foreign subsidiary is sold or closed at a time when the foreign currency is weaker than when the Company made investments in the country. In addition, our local competitors in certain markets may have different purchasing models that provide them reduced foreign currency exposure compared to the Company. This may result in market pricing that the Company cannot meet without significantly lower profit on sales.

11

We have international operations which expose us to risks associated with conducting business in multiple jurisdictions.

The Company's international operations are subject to other risks such as the imposition of governmental controls, export license requirements, restrictions on the export of certain technology, political instability, trade restrictions, tariff changes, difficulties in staffing and managing international operations, changes in the interpretation and enforcement of laws (in particular related to items such as duty and taxation), difficulties in collecting accounts receivable, longer collection periods and the impact of local economic conditions and practices. There can be no assurance that these and other factors will not have an adverse effect on the Company's business.

In addition, while the Company's labor force in the Americas is currently non-union, employees of certain European subsidiaries are subject to collective bargaining or similar arrangements. The Company does business in certain foreign countries where labor disruption is more common than is experienced in the United States and some of the freight carriers used by the Company are unionized. A labor strike by a group of the Company's employees, one of the Company's freight carriers, one of its vendors, a general strike by civil service employees, or a governmental shutdown could have an adverse effect on the Company's business. Many of the products the Company sells are manufactured in countries other than the countries in which the Company's logistics centers are located. The inability to receive products into the logistics centers because of government action or labor disputes at critical ports of entry may have an adverse effect on the Company's business.

We cannot predict what losses we might incur in litigation matters, regulatory enforcement actions and contingencies that we may be involved with from time to time, including in connection with the restatement of prior financial statements.

The SEC has requested information from the Company with respect to the restatement of certain of our consolidated financial statements and other financial information from fiscal 2009 to fiscal 2013, and the Company is cooperating with the SEC request. See Item 3, “Legal Proceedings.” This pending SEC request for information and other potential proceedings could result in fines and other penalties. The Company has not reserved any amount in respect of these matters in its consolidated financial statements.

The Company cannot predict whether monetary losses, if any, it experiences in any proceedings related to the restatement will be covered by insurance or whether insurance proceeds recovered will be sufficient to offset such losses. Potential civil or regulatory proceedings may also divert the efforts and attention of the Company’s management from business operations.

The Company cannot predict what losses we might incur from other litigation matters, regulatory enforcement actions and contingencies that we may be involved with from time to time. There are various other claims, lawsuits and pending actions against us. We do not expect that the ultimate resolution of these other matters will have a material adverse effect on our consolidated financial position. However, the resolution of certain of these matters could be material to our operating results for any particular period, depending on the level of income for such period. We can make no assurances that we will ultimately be successful in our defense of any of these other matters.

ITEM 1B. Unresolved Staff Comments.

Not applicable.

ITEM 2. Properties.

Our executive offices are located in Clearwater, Florida. As of January 31, 2015, we operated a total of 26 logistics centers to provide our customers timely delivery of products. Fourteen of these logistics centers are located in the Americas and twelve are located in Europe.

As of January 31, 2015, we leased or owned approximately 7.7 million square feet of space. The majority of our office facilities and logistics centers are leased. Our facilities are well maintained and are adequate to conduct our current business. We do not anticipate significant difficulty in renewing our leases as they expire or securing replacement facilities.

ITEM 3. Legal Proceedings.

Prior to fiscal 2004, one of the Company’s subsidiaries, located in Spain, was audited in relation to various value added tax (“VAT”) matters. As a result of those audits, the Spanish subsidiary received notices of assessment from the Regional Inspection Unit of Spain’s taxing authority that allege the subsidiary did not properly collect and remit VAT. The Spanish subsidiary appealed these assessments to the Madrid Central Economic Administrative Courts beginning in March 2010. Following the administrative court proceedings the matter was appealed to the Spanish National Appellate Court. During the fourth quarter of fiscal year 2014, the Spanish National Appellate Court issued an opinion upholding the assessment for several of the assessed years. The Spanish National Appellate Court opinion represented a subsequent event that occurred prior to the issuance of the fiscal 2013 financial statements in relation to a loss contingency that existed as of January 31, 2013. The Company increased its accrual for costs associated with this matter by recording a charge of $41.0 million in the fiscal 2013 Consolidated Statement of Income, including $29.5 million recorded in "value added tax assessment" to cover the assessment and various penalties and $11.5 million recorded in "interest expense" for interest that could be assessed. During the second quarter of fiscal year 2015, the Madrid Economic Administrative Court issued a decision revoking the penalties for certain of the assessed years. As a result of this decision, during the fiscal year ended January 31, 2015 the Company decreased its accrual for costs associated with this matter by $6.2 million, which is recorded in "value added tax assessment" in the Consolidated Statement of Income. The Company believes that the Spanish subsidiary's defense to the remaining assessments has solid legal grounds and is continuing to vigorously defend its position by appealing to the Spanish Supreme Court. The Company estimates the total exposure for these assessments, including various penalties and interest, was approximately $43.7 million and $56.4 million at January 31, 2015 and 2014, respectively, which is included in "accrued expenses and other liabilities" in the Consolidated Balance Sheet.

In December 2010, in a non-unanimous decision, a Brazilian appellate court overturned a 2003 trial court which had previously ruled in favor of the Company’s Brazilian subsidiary related to the imposition of certain taxes on payments abroad related to the licensing of commercial software products, commonly referred to as “CIDE tax.” The Company estimates the total exposure where the CIDE tax, including interest, may be considered due to be approximately $24.6 million and $25.3 million at January 31, 2015 and 2014, respectively. The Brazilian subsidiary has appealed the unfavorable ruling to the Supreme Court and Superior Court, Brazil's two highest appellate courts. Based on the legal opinion of outside counsel, the Company believes that the chances of success on appeal of this matter are favorable and the Brazilian subsidiary intends to vigorously defend its position that the CIDE tax is not due. However, due to the lack of predictability of the Brazilian court system, the Company has concluded that it is reasonably possible that the Brazilian subsidiary may incur a loss up to the total exposure described above. The Company believes the resolution of this litigation will not be material to the Company’s consolidated net assets or liquidity. In addition to the discussion regarding the CIDE tax above, the Company’s Brazilian subsidiary has been undergoing several examinations of non-income related taxes. Given the complexity and lack of predictability of the Brazilian tax system, the Company believes that it is reasonably possible that a loss may have been incurred. However, due to the early stages of the examination, the complex nature of the Brazilian tax system and the absence of communication from the local tax authorities regarding these examinations, the Company is currently unable to determine the likelihood of these examinations resulting in assessments nor estimate the amount of loss, if any, that may be reasonably possible if such assessment were to be made.

The SEC has requested information from the Company with respect to the restatement of certain of our consolidated financial statements and other financial information from fiscal 2009 to 2013. The Company is cooperating with the SEC’s request for information.

12

The Company is subject to various other legal proceedings and claims arising in the ordinary course of business. The Company’s management does not expect that the outcome in any of these other legal proceedings, individually or collectively, will have a material adverse effect on the Company’s financial condition, results of operations, or cash flows.

ITEM 4. Mine Safety Disclosures.

Not applicable.

13

PART II

ITEM 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our common stock is traded on the NASDAQ Stock Market, Inc. (“NASDAQ”) under the symbol “TECD.” We have not paid cash dividends since fiscal 1983 and the Board of Directors has no current plans to institute a cash dividend payment policy in the foreseeable future. The table below presents the quarterly high and low sale prices for our common stock as reported by the NASDAQ. As of March 11, 2015, there were 231 holders of record and we believe that there were 15,001 beneficial holders.

Sales Price | |||

High | Low | ||

Fiscal year 2015 | |||

Fourth quarter | $64.18 | $55.83 | |

Third quarter | $71.31 | $52.22 | |

Second quarter | $65.56 | $58.15 | |

First quarter | $65.98 | $50.21 | |

Sales Price | |||

High | Low | ||

Fiscal year 2014 | |||

Fourth quarter | $55.36 | $48.35 | |

Third quarter | $54.07 | $48.71 | |

Second quarter | $51.89 | $45.63 | |

First quarter | $54.60 | $43.02 | |

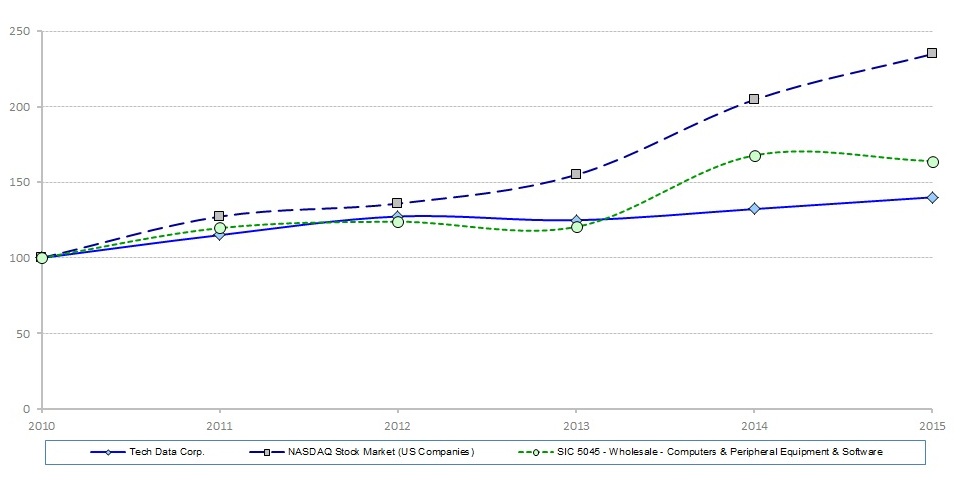

Stock Performance Chart

The five-year stock performance chart below assumes an initial investment of $100 on February 1, 2010 and compares the cumulative total return for Tech Data, the NASDAQ Stock Market (U.S.) Index, and the Standard Industrial Classification, or SIC, Code 5045 – Computer and Peripheral Equipment and Software. The comparisons in the table are provided in accordance with SEC requirements and are not intended to forecast or be indicative of possible future performance of our common stock.

14

Comparison of Cumulative Total Return

Assumes Initial Investment of $100 on February 1, 2010

Among Tech Data Corporation,

NASDAQ Stock Market (U.S.) Index and SIC Code 5045

2010 | 2011 | 2012 | 2013 | 2014 | 2015 | ||||||

Tech Data Corporation | 100 | 115 | 127 | 125 | 132 | 140 | |||||

NASDAQ Stock Market (U.S.) Index | 100 | 127 | 136 | 155 | 205 | 235 | |||||

SIC Code 5045 – Computer and Peripheral Equipment and Software | 100 | 120 | 124 | 121 | 168 | 164 | |||||

Securities Authorized for Issuance under Equity Compensation Plans

Information regarding the Securities Authorized for Issuance under Equity Compensation Plans can be found under Item 12 of this Report.

Unregistered Sales of Equity Securities

None.

Issuer Purchases of Equity Securities

On December 4, 2014, the Company's Board of Directors authorized a share repurchase program of up to $100.0 million of the Company's common stock. In conjunction with the Company's share repurchase program, we executed a 10b5-1 plan that instructs the broker selected by the Company to repurchase shares on behalf of the Company. The amount of common stock repurchased in accordance with the 10b5-1 plan on any given trading day is determined by a formula in the plan, which is based on the market price of our common stock. Shares repurchased by the Company are held in treasury for general corporate purposes, including issuances under equity incentive and benefit plans.

During fiscal 2015, the Company repurchased 896,718 shares at an average price of $59.10 per share, for a total cost, including expenses, of approximately $53.0 million under this program.

15

The following table presents information with respect to purchases of common stock by the Company under the share repurchase program during the quarter ended January 31, 2015:

Issuer Purchases of Equity Securities | ||||||||||||||

Maximum dollar | ||||||||||||||

Total number of shares | value of shares | |||||||||||||

purchased as part | that may yet | |||||||||||||

Total number of | Average price paid | of a publicly announced | be purchased under | |||||||||||

Period | shares purchased | per share | plan or programs | the plan or programs | ||||||||||

November 1 - November 30, 2014 | 0 | $ | 0 | 0 | $ | 100,000,000 | ||||||||

December 1 - December 31, 2014 | 268,009 | $ | 61.50 | 268,009 | $ | 83,518,673 | ||||||||

January 1 - January 31, 2015 | 628,709 | $ | 58.08 | 628,709 | $ | 47,002,593 | ||||||||

Total | 896,718 | $ | 59.10 | 896,718 | ||||||||||

16

ITEM 6. Selected Financial Data.

The following table sets forth certain selected consolidated financial data. This information should be read in conjunction with Management’s Discussion and Analysis of Financial Condition and Results of Operations and our consolidated financial statements and notes thereto appearing elsewhere in this Annual Report.

FIVE-YEAR FINANCIAL SUMMARY

(In thousands, except per share data)

Year ended January 31, | |||||||||||||||||||

2015 | 2014 | 2013 | 2012 | 2011 | |||||||||||||||

Income statement data: (1) | |||||||||||||||||||

Net sales | $ | 27,670,632 | $ | 26,821,904 | $ | 25,358,329 | $ | 25,647,313 | $ | 23,619,938 | |||||||||

Gross profit | 1,393,954 | 1,362,346 | 1,303,054 | 1,377,441 | 1,278,253 | ||||||||||||||

Operating income (2) (3) (4) (5) (6) (7) | 267,635 | 227,513 | 263,720 | 304,546 | 321,408 | ||||||||||||||

Consolidated net income (6) (8) (9) (10) (11) | 175,172 | 179,932 | 183,040 | 201,202 | 212,992 | ||||||||||||||

Net income attributable to noncontrolling interest (12) | 0 | 0 | (6,785 | ) | (10,452 | ) | (4,620 | ) | |||||||||||

Net income attributable to shareholders of Tech Data Corporation | $ | 175,172 | $ | 179,932 | $ | 176,255 | $ | 190,750 | $ | 208,372 | |||||||||

Net income per share attributable to shareholders of Tech Data Corporation—basic | $ | 4.59 | $ | 4.73 | $ | 4.53 | $ | 4.36 | $ | 4.29 | |||||||||

Net income per share attributable to shareholders of Tech Data Corporation—diluted | $ | 4.57 | $ | 4.71 | $ | 4.50 | $ | 4.30 | $ | 4.25 | |||||||||

Dividends per common share | 0 | 0 | 0 | 0 | 0 | ||||||||||||||

Balance sheet data: (1) | |||||||||||||||||||

Working capital (13) | $ | 1,834,997 | $ | 1,851,447 | $ | 1,700,485 | $ | 1,720,564 | $ | 1,899,124 | |||||||||

Total assets | 6,138,246 | 7,169,666 | 6,830,960 | 5,796,268 | 6,524,639 | ||||||||||||||

Revolving credit loans and current maturities of long-term debt, net | 13,303 | 43,481 | 167,522 | 48,490 | 434,435 | ||||||||||||||

Long-term debt, less current maturities | 353,097 | 354,121 | 354,458 | 57,253 | 60,076 | ||||||||||||||

Equity attributable to shareholders of Tech Data Corporation | 1,960,143 | 2,098,611 | 1,918,369 | 1,953,804 | 2,108,451 | ||||||||||||||

(1) | See further discussion in Note 5 of Notes to Consolidated Financial Statements of the Company’s acquisition of SDG in fiscal 2013. |

(2) | During fiscal 2015, the Company incurred $22.0 million of restatement and remediation related expenses and recorded a gain of $5.1 million associated with legal settlements with certain manufacturers of LCD flat panel displays (see further discussion in Note 1 of Notes to Consolidated Financial Statements). |

(3) | During fiscal 2015, the Company decreased its accrual for various value added tax matters related to its Spanish subsidiary by $6.2 million (see further discussion in Note 13 of Notes to Consolidated Financial Statements). |

(4) | During fiscal 2015, the Company incurred a $1.3 million loss on disposal of subsidiaries related to the plan to sell certain of the Company’s operations in Latin America (see further discussion in Note 6 of Notes to Consolidated Financial Statements). |

(5) | During fiscal 2014, the Company incurred $53.8 million of restatement and remediation related expenses and recorded a gain of $35.5 million associated with legal settlements with certain manufacturers of LCD flat panel displays (see further discussion in Note 1 of Notes to Consolidated Financial Statements). |

(6) | During fiscal 2013, the Company increased its accrual for various value added tax matters related to its Spanish subsidiary by $41.0 million, including operating expenses of $29.5 million in relation to the assessment and penalties and $11.5 million for associated interest expense (see further discussion in Note 13 of Notes to Consolidated Financial Statements). |

(7) | During fiscal 2012, the Company incurred a $28.3 million loss on disposal of subsidiaries related to the closure of certain of the Company’s operations in Latin America. |

(8) | During fiscal 2015, the Company recorded income tax benefits of $19.2 million primarily related to the reversal of deferred tax valuation allowances in certain jurisdictions in Europe, partially offset by income tax expenses of $5.6 million related to undistributed earnings on assets held for sale in certain Latin American jurisdictions (see further discussion in Note 8 of Notes to Consolidated Financial Statements). |

(9) | During fiscal 2014, the Company recorded income tax benefits of $45.3 million for the reversal of deferred tax valuation allowances primarily related to certain jurisdictions in Europe (see further discussion in Note 8 of Notes to Consolidated Financial Statements). |

(10) | During fiscal 2013, the Company recorded a $25.1 million reversal of deferred tax valuation allowances related to a specific jurisdiction in Europe (see further discussion in Note 8 of Notes to Consolidated Financial Statements). |

(11) | During fiscal 2012, the Company recorded a $13.6 million reversal of deferred tax valuation allowances which was substantially offset by the write-off of deferred income tax assets associated with the closure of Brazil’s commercial operations. |

(12) | During fiscal 2013, the Company completed the acquisition of Brightstar Corp.’s fifty percent ownership interest in Brightstar Europe Limited, which was a consolidated joint venture between Tech Data and Brightstar Corp (see further discussion in Note 5 of Notes to Consolidated Financial Statements). |

(13) | Working capital represents total current assets less total current liabilities in the Consolidated Balance Sheet. |

17

ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Forward-Looking Statements

This Annual Report on Form 10-K, including this Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”), contains forward-looking statements, as described in the “safe harbor” provision of the Private Securities Litigation Reform Act of 1995. These statements involve a number of risks and uncertainties and actual results could differ materially from those projected. These forward-looking statements regarding future events and the future results of Tech Data Corporation (“Tech Data”, “we”, “our”, “us” or the “Company”) are based on current expectations, estimates, forecasts, and projections about the industries in which we operate and the beliefs and assumptions of our management. Words such as “expects,” “anticipates,” “targets,” “goals,” “projects,” “intends,” “plans,” “believes,” “seeks,” “estimates,” variations of such words, and similar expressions are intended to identify such forward-looking statements. In addition, any statements that refer to projections of our future financial performance, our anticipated growth and trends in our businesses, and other characterizations of future events or circumstances, are forward-looking statements. Readers are cautioned that these forward-looking statements are only predictions and are subject to risks, uncertainties, and assumptions. Therefore, actual results may differ materially and adversely from those expressed in any forward-looking statements. Readers are referred to the cautionary statements and important factors discussed in Item 1A, "Risk Factors" in this Annual Report on Form 10-K for the year ended January 31, 2015 for further information. We undertake no obligation to revise or update publicly any forward-looking statements for any reason.

Overview

Tech Data is one of the world’s largest wholesale distributors of technology products. We serve as an indispensable link in the technology supply chain by bringing products from the world’s leading technology vendors to market, as well as providing our customers with advanced logistics capabilities and value-added services. Our customers include value-added resellers (“VARs”) direct marketers, retailers and corporate resellers who support the diverse technology needs of end users. We manage our business in two geographic segments: the Americas and Europe.

Our financial objectives are to grow sales at or above the overall IT market growth rate by gaining share in select product areas, grow earnings in local currency, generate positive cash flow, and earn a return on invested capital above our weighted average cost of capital. To achieve this, we are focused on a strategy of execution, diversification and innovation that we believe differentiates our business in the marketplace.

The fundamental element of our strategy is execution. Our execution strategy is supported by our highly efficient infrastructure, combined with our multiple service offerings, to generate demand, develop markets and provide supply chain services for our vendors and customers. The technology distribution industry in which we operate is characterized by narrow gross profit as a percentage of sales (“gross margin”) and narrow income from operations as a percentage of sales (“operating margin”). Historically, our gross and operating margins have been impacted by intense price competition and declining average selling prices per unit, as well as changes in terms and conditions with our vendors, including those terms related to rebates, price protection, product returns and other incentives. We expect these conditions to continue in the foreseeable future and, therefore, we will continue to proactively evaluate our pricing policies and inventory management practices in response to potential changes in our vendor terms and conditions and the general market environment. More than 90% of the Company's net sales are on one common IT platform, which we believe will give Tech Data significant competitive advantages in providing greater supply chain opportunities by expanding our value-added services to our customers, on-boarding new vendors and products faster and improving our ability to rapidly respond to changes in the market.

In addition to execution, our strategy includes ongoing diversification and realignment of our customer and product portfolios to improve long-term profitability throughout our operations. Our broadline distribution business, characterized as high volume, more commoditized offerings, and comprised primarily of personal computer systems, tablets, peripherals, supplies and other similar products, remains a core part of our business and represents a significant percentage of our revenue, albeit not a majority. However, as technology advances, we have continued to evolve our business model, product mix, and value-added offerings in order to provide our vendors with the most efficient distribution channel for their products, and our customers with a broad array of innovative solutions to sell.

18

On November 1, 2012, we completed the acquisition of several distribution companies of Specialist Distribution Group (collectively "SDG"), the distribution arm of Specialist Computer Holdings PLC, a privately-held IT services company headquartered in the United Kingdom, for a final purchase price of approximately $358 million. We believe the acquisition of SDG supported our diversification strategy by strengthening our European value and broadline offerings in key markets and expanding our vendor and customer portfolios, while leveraging our existing pan-European infrastructure.

Another strategic area of investment is our integrated supply chain services designed to provide innovative third party logistics and other offerings to our business partners. We have seen these offerings grow within our European mobility and broadline businesses in both geographies. Our evolving mix of products, services, customers and geographies are important factors in achieving our strategic financial goals. As we execute our diversification strategy we continuously monitor the extension of credit and other terms and conditions offered to our customers to prudently balance risk, profitability and return on invested capital.

The final tenet of our strategy is innovation. Our IT systems and e-business tools and programs have provided our business with the flexibility to effectively navigate fluctuations in market conditions, structural changes in the technology industry, as well as changes created by the products we sell. An example of our investment in innovation and one that we believe is providing us with the flexibility to meet the demands of the ever-evolving technology market, is our continued deployment of internal IT systems across both our Americas and European regions, including the integration of SDG, which was completed in the first quarter of fiscal 2015. We believe our global IT systems provide us with a competitive advantage allowing us to drive efficiencies throughout our business while delivering innovative solutions for our business partners.

We believe our strategy of execution, diversification and innovation differentiates us in the markets we serve and we believe we have opportunities for further gains in market share as our customer satisfaction ratings continue to improve. We continually evaluate the current and potential profitability and return on our investments in all geographies and consider changes in current and future investments based on risks, opportunities and current and anticipated market conditions. In connection with these evaluations, we may incur additional costs to the extent we decide to increase or decrease our investments in certain geographies. For example, during the fourth quarter of fiscal 2015, we committed to a plan to sell our business operations in Chile and Peru and in March 2015, the Company entered into an agreement for the sale of these operations. Additionally, in March 2015 we committed to a plan to exit our business operations in Uruguay. The operating results of these entities during fiscal 2015, 2014, and 2013 were insignificant relative to our consolidated financial results. We will also continue to evaluate targeted strategic investments across our operations and new business opportunities and invest in those markets and product segments we believe provide us with the greatest opportunities for profitable growth. Finally, from a balance sheet perspective, we require working capital primarily to finance accounts receivable and inventory. We have historically relied upon debt, trade credit from our vendors, and accounts receivable financing programs for our working capital needs. At January 31, 2015, we had a debt to total capital ratio (calculated as total debt divided by the aggregate of total debt and total equity) of 16%.

Critical Accounting Policies and Estimates

The information included within MD&A is based upon our consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States ("GAAP"). The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses, and related disclosures. On an ongoing basis, we evaluate these estimates, including those related to bad debts, inventory, vendor incentives, goodwill and intangible assets, deferred taxes, and contingencies. Our estimates and judgments are based on currently available information, historical results, and other assumptions we believe are reasonable. Actual results could differ materially from these estimates. We believe the critical accounting policies discussed below affect the more significant judgments and estimates used in the preparation of our consolidated financial statements.

Accounts Receivable