Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - NN INC | d896736d8k.htm |

Exhibit 99.1

|

|

Exhibit 99.1

Investor Presentation

March 23, 2015

|

|

Forward-Looking Statement & Disclaimer

Forward Looking Statement: With the exception of the historical information contained in this presentation, the matters described

herein contain forward-looking statements that are made pursuant to the safe harbor provisions of the Private Securities Litigation

Reform Act of 1995. Forward-looking statements involve a number of risks and uncertainties that may cause actual results to be

materially different from such forward-looking statements. Such factors include, among others, general economic conditions and

economic conditions in the industrial sector, competitive influences, risks that current customers will commence or increase captive

production, risks of capacity underutilization, quality issues, availability of raw materials, currency and other risks associated with

international trade, the Company’s dependence on certain major customers, and other risk factors and cautionary statements listed

from time to time in the Company’s periodic reports filed with the Securities and Exchange Commission, including, but not limited to,

the Company’s Annual Report on 10 -K for the fiscal year ended December 31, 2013 .

Disclaimer: NN disclaims any obligation to update any such factors or to publicly announce the result of any revisions to any of the

forward-looking statements included herein or therein to reflect future events or developments.

This presentation includes certain non-GAAP measures as defined by SEC rules. A reconciliation of those measures to the most

directly comparable GAAP equivalent is provided at the end of this presentation.

2

|

|

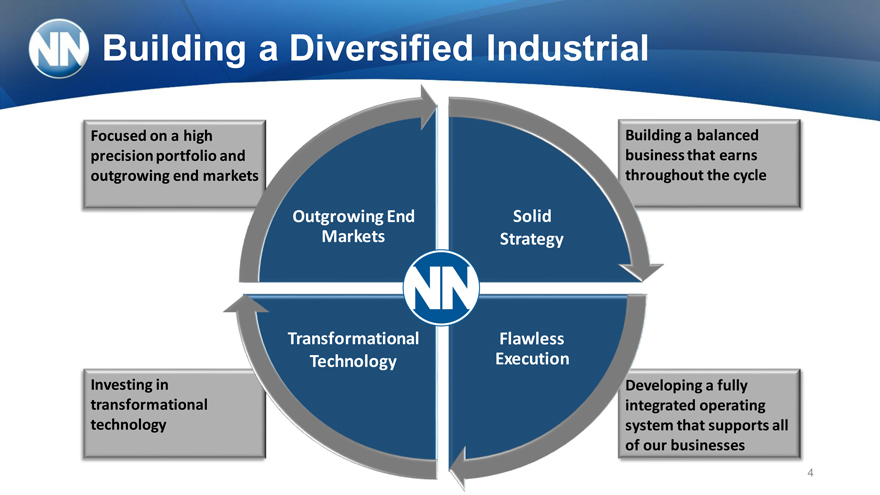

Building a Diversified Industrial

3

|

|

Building a Diversified Industrial

Focused on a high precision portfolio and outgrowing end markets

Building a balanced business that earns throughout the cycle

Investing in transformational technology

Developing a fully integrated operating system that supports all of our businesses

Outgrowing End Markets

Solid

Strategy

Transformational technology

Flawless execution

4

|

|

Building a Diversified Industrial

We have made significant progress against other DIs…

Rank among comparable S/Mid-Cap DIs

Metric Ä Rank

2012—13 2013—14

Sales Growth 8 1 +7

Adjusted Operating

8 5 +3

Margin

Return on Equity 8 5 +3

Total Return 10 1 +9

P/E Ratio 5 6 -1

…but we remain undervalued to our peers

Compared to 9 S/Mid Cap companies outlined on page 10 5

Analysis was done on year over year, TTM, and 2 year TTM period or using 2014 estimates

Source: Bloomberg Analytics

|

|

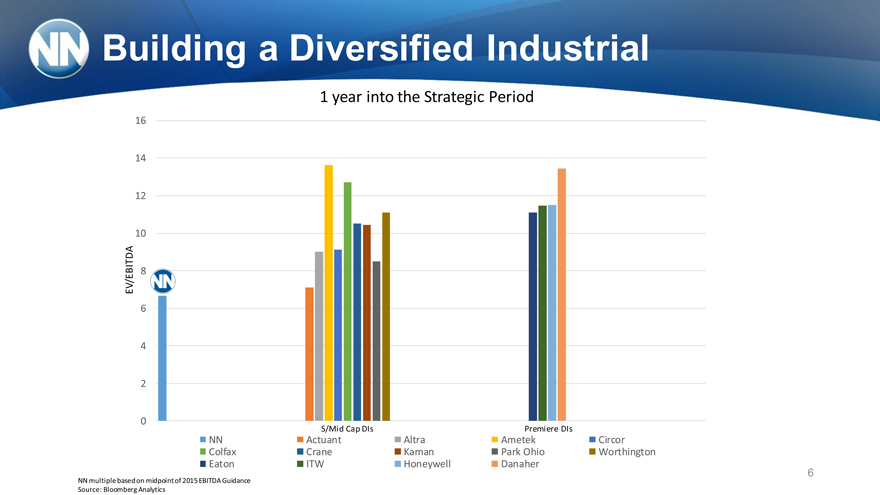

Building a Diversified Industrial

1 year into the Strategic Period

16

14

12

10

EV/EBITDA 8

6

4

2

0

S/Mid Cap DIs Premiere DIs

NN Actuant Altra Ametek Circor

Colfax Crane Kaman Park Ohio Worthington

Eaton ITW Honeywell Danaher

6

NN multiple based on midpoint of 2015 EBITDA Guidance

Source: Bloomberg Analytics

|

|

Company Overview

7

|

|

History & Today

2015 revenue guidance revised to $670M—$690M – solely due to FX translation

Global reach, local depth

Top 3 globally in both bearing components, and precision metal components

25 manufacturing facilities with operations in 10 countries

4,200 employees

Three R&D Centers around the globe

Supplying to diversified end markets in over 30 countries

1980Metal Bearing 1999Components 2000 2001 2003 2005 2006 2014…

Industrial Veenendaal SNR Ball Whirlaway V-S Chelsea

NN founded Molding Euroball Delta Rubber RFK Autocam

in Erwin, TN Assets Corporation Industries Grinding

Corporation Company

8

|

|

Foundation for Growth

Five new Board appointments since 2012

New President & CEO in 2013, key management retained

Developed Treasury, FP&A, Supply Chain, Shared Services and

IT group infrastructure

Design of the NN Operating System

Enhanced management bandwidth with acquisitions

The fundaments of our plan have not changed. We will continue to deliver on our commitments. 9

|

|

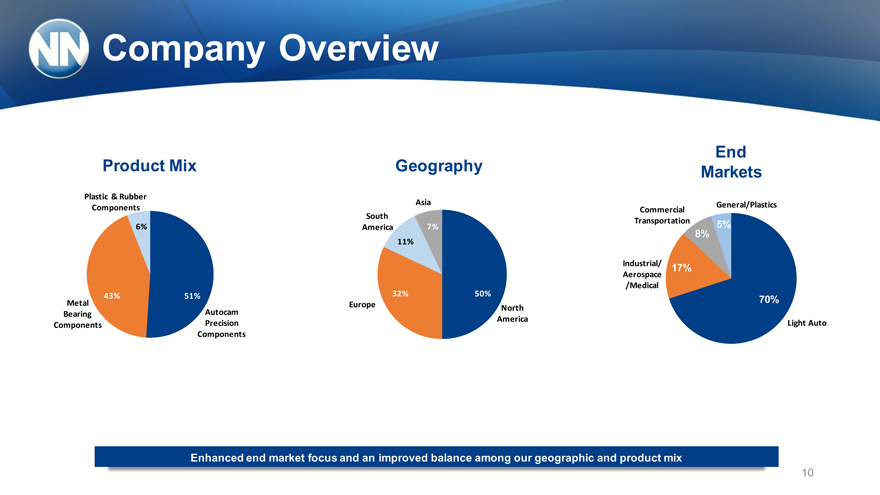

Company Overview

Product Mix

Plastic & Rubber

Components

6%

43% 51%

Metal

Bearing Autocam

Components Precision

Components

Geography

Asia

South

America 7%

11%

7%

32% 50%

Europe North

America

End

Markets

Commercial General/Plastics

Transportation 5%

8%

Industrial/ 17%

Aerospace

/Medical

70%

Light Auto

Enhanced end market focus and an improved balance among our geographic and product mix

10

|

|

Customer Profile

11

|

|

Value Proposition

Ability to manufacture precision products with ultra tight tolerances in high volume

Total product life cycle

Established global footprint

Highly specialized skill and engineering in bearing components and precision machining

Significant proprietary knowledge and trade secrets

Leading manufacturer of high precision components 12

|

|

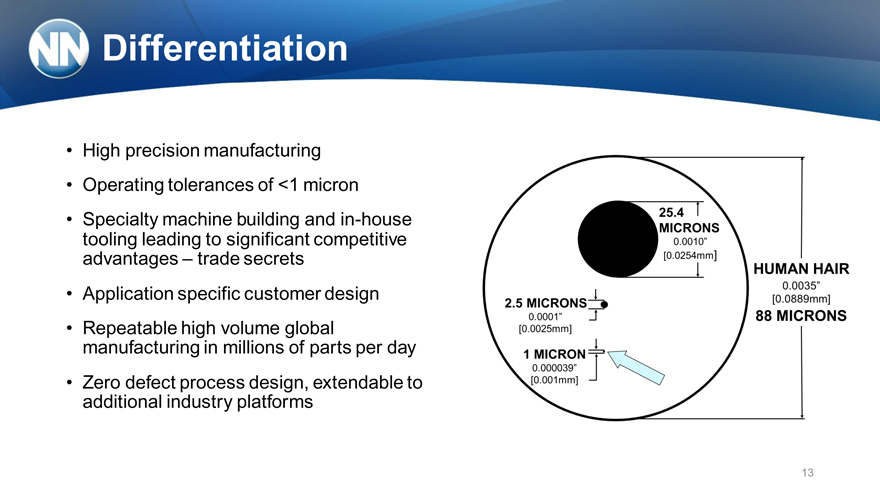

Differentiation

High precision manufacturing

Operating tolerances of <1 micron

Specialty machine building and in-house tooling leading to significant competitive advantages – trade secrets

Application specific customer design

Repeatable high volume global manufacturing in millions of parts per day

Zero defect process design, extendable to additional industry platforms

13

|

|

Global Footprint

—Metal Bearing Components

—Autocam Precision Components

—Plastic & Rubber Components

—Corporate Headquarters

25 high precision manufacturing facilities on 4 continents

14

|

|

Moving Forward

15

|

|

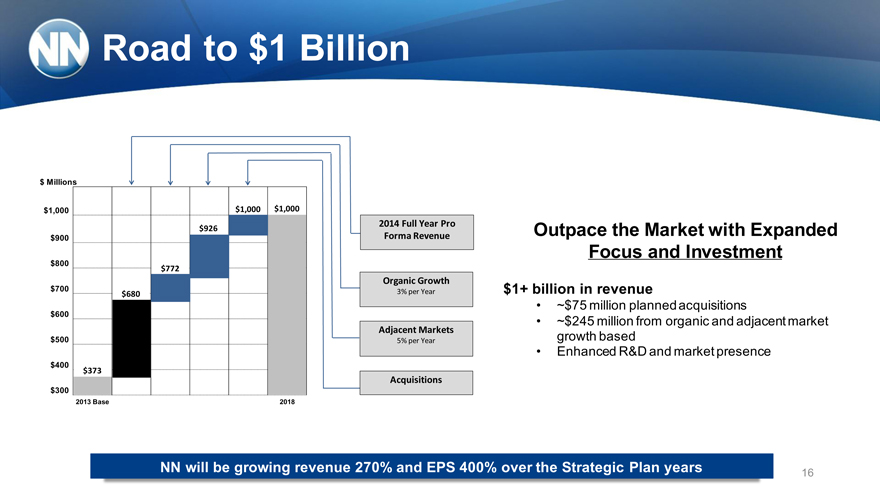

Road to $1 Billion

$ Millions

$1,000 $1,000 $1,000

2014 Full Year Pro $926 Forma Revenue

$900

$800 $772

Organic Growth

$700 3% per Year $680

$600

Adjacent Markets

$500 5% per Year

$400 $373

Acquisitions

$300 $200 2013 Base 2018

Outpace the Market with Expanded Focus and Investment

$1+ billion in revenue

~$75 million planned acquisitions

~$245 million from organic and adjacent market growth based

Enhanced R&D and market presence

NN will be growing revenue 270% and EPS 400% over the Strategic Plan years 16

|

|

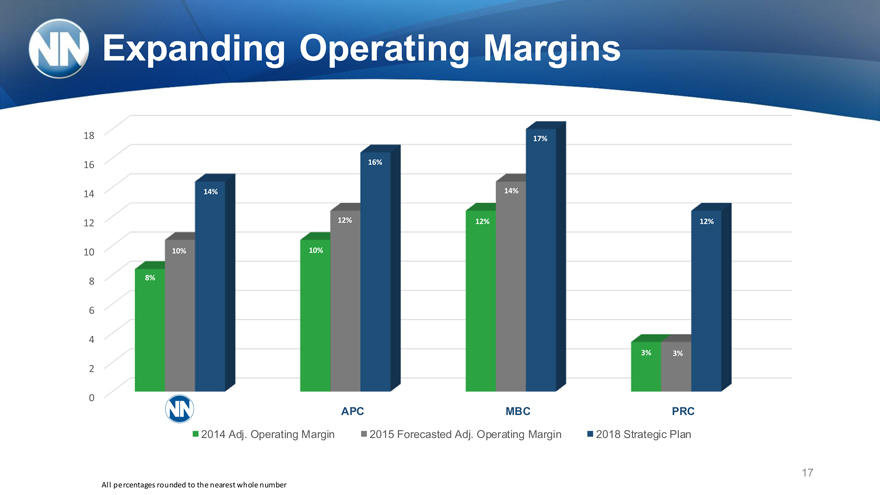

Expanding Operating Margins

18 17%

16 16%

14 14% 14%

12 12% 12% 12%

10 10% 10%

8 8%

6

4

3% 3%

2

0

APC MBC PRC

2014 Adj. Operating Margin 2015 Forecasted Adj. Operating Margin 2018 Strategic Plan

17

All percentages rounded to the nearest whole number

|

|

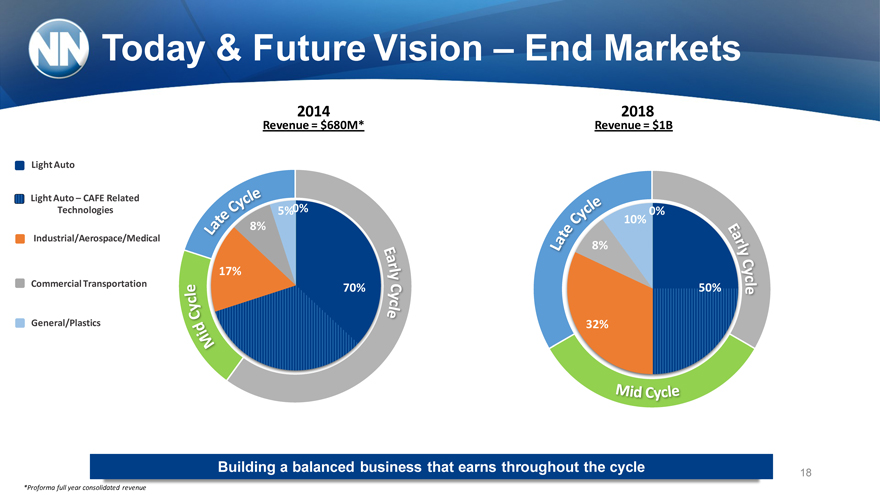

Today & Future Vision – End Markets

Light Auto

Light Auto – CAFE Related

Technologies

Industrial/Aerospace/Medical

Commercial Transportation

General/Plastics

2014 2018

Revenue = $680M* Revenue = $1B

5%

8%

17%

70%

10%

8%

50%

32%

Building a balanced business that earns throughout the cycle 18

*Proforma full year consolidated revenue

|

|

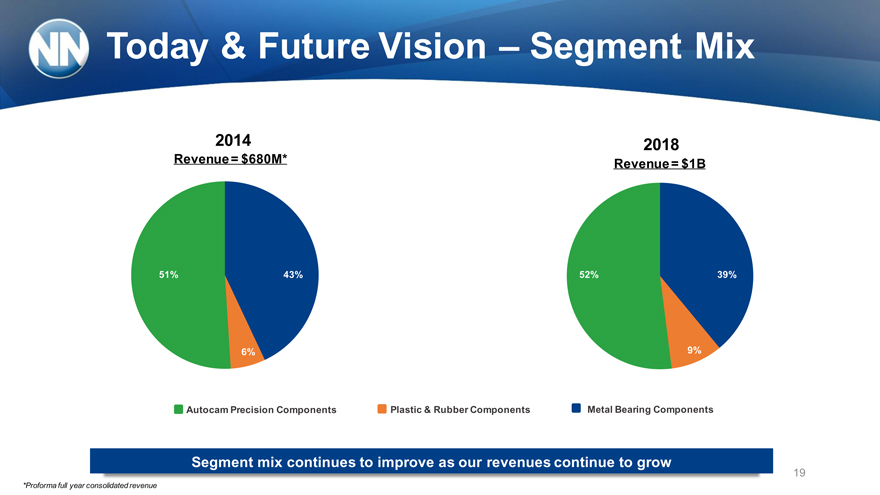

Today & Future Vision – Segment Mix

2014 2018

Revenue = $680M* Revenue = $1B

51 43% %

51% 43% 43 52% 39% %

6% 9% 6%

31 43% 50 51

% % % Autocam Precision 60 Components Plastic & Rubber Components Metal Bearing Components % 25 %

Segment mix continues to improve as our revenues continue to grow 19

*Proforma full year consolidated revenue

|

|

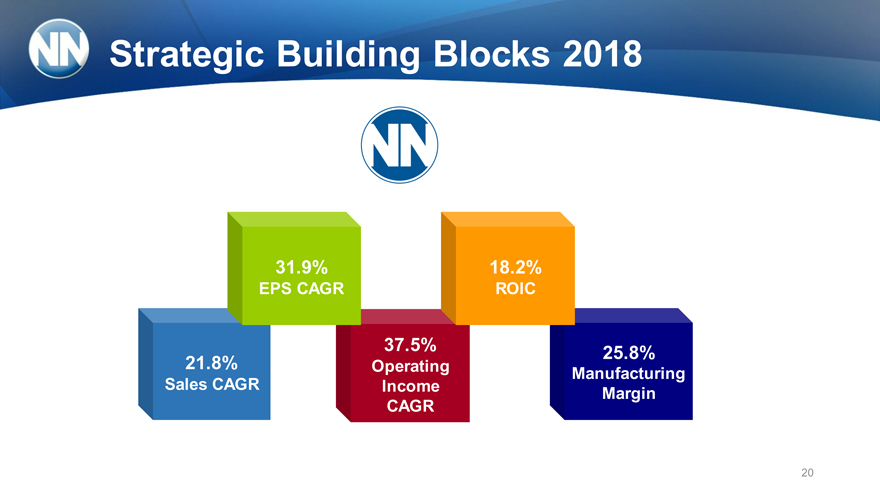

Strategic Building Blocks 2018

31.9% 18.2%

EPS CAGR ROIC

37.5% 8% 25.

21.8% Operating

Manufacturing Sales CAGR Income Margin CAGR

20

|

|

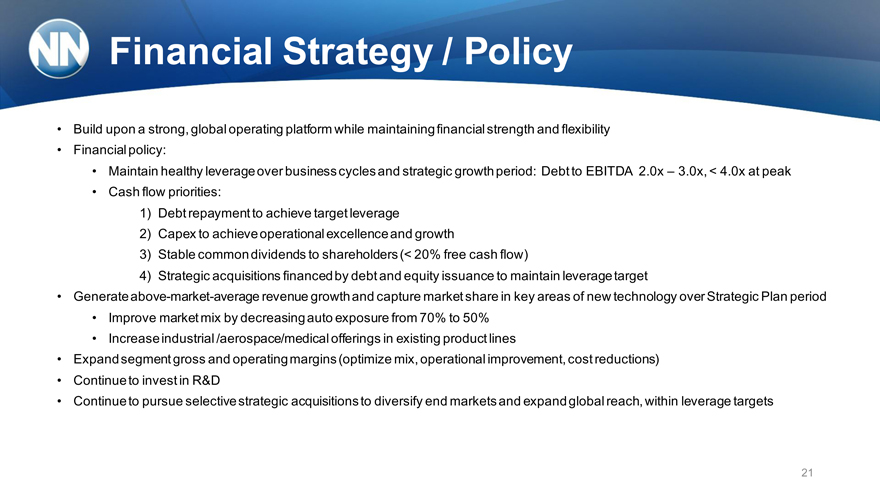

Financial Strategy / Policy

Build upon a strong, global operating platform while maintaining financial strength and flexibility

Financial policy:

Maintain healthy leverage over business cycles and strategic growth period: Debt to EBITDA 2.0x – 3.0x, < 4.0x at peak

Cash flow priorities:

1) Debt repayment to achieve target leverage

2) Capex to achieve operational excellence and growth

3) Stable common dividends to shareholders (< 20% free cash flow)

4) Strategic acquisitions financed by debt and equity issuance to maintain leverage target

Generate above-market-average revenue growth and capture market share in key areas of new technology over Strategic Plan period

Improve market mix by decreasing auto exposure from 70% to 50%

Increase industrial /aerospace/medical offerings in existing product lines

Expand segment gross and operating margins (optimize mix, operational improvement, cost reductions)

Continue to invest in R&D

Continue to pursue selective strategic acquisitions to diversify end markets and expand global reach, within leverage targets

21

|

|

22

|

|

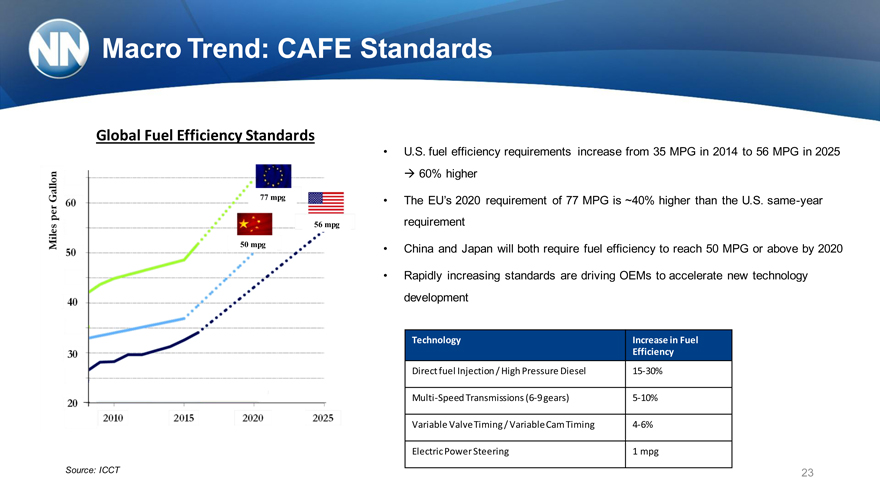

Macro Trend: CAFE Standards

Global Fuel Efficiency Standards

77 mpg

56 mpg

50 mpg

Source: ICCT

U.S. fuel efficiency requirements increase from 35 MPG in 2014 to 56 MPG in 2025

? 60% higher

The EU’s 2020 requirement of 77 MPG is ~40% higher than the U.S. same-year

requirement

China and Japan will both require fuel efficiency to reach 50 MPG or above by 2020

Rapidly increasing standards are driving OEMs to accelerate new technology

development

Technology Increase in Fuel

Efficiency

Direct fuel Injection / High Pressure Diesel 15-30%

Multi-Speed Transmissions (6-9 gears) 5-10%

Variable Valve Timing / Variable Cam Timing 4-6%

Electric Power Steering 1 mpg

23

|

|

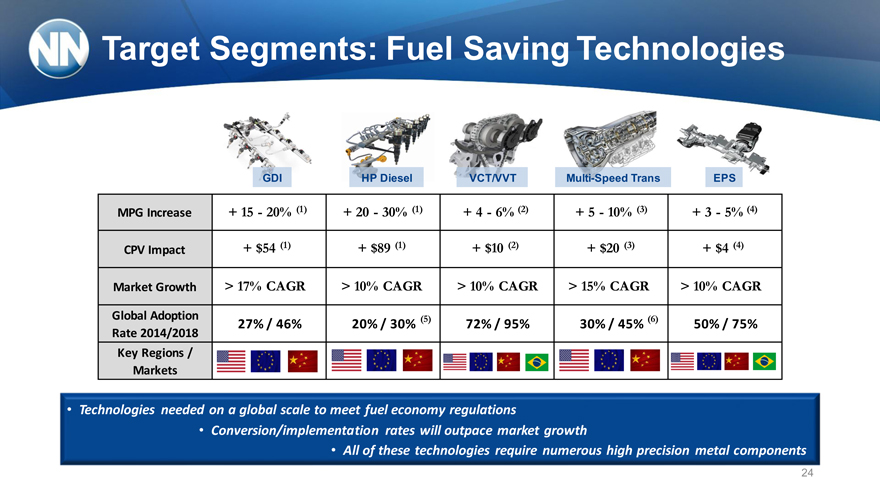

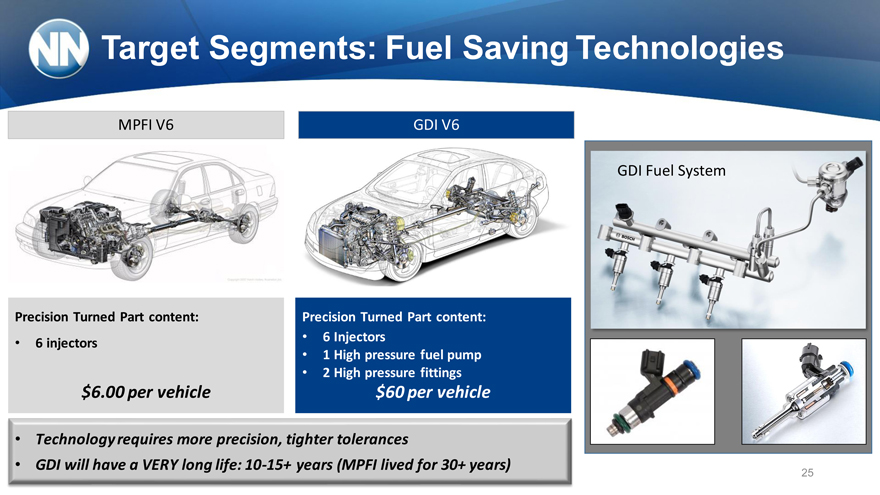

Target Segments: Fuel Saving Technologies

GDI HP Diesel VCT/VVT Multi-Speed Trans EPS

MPG Increase + 15—20% (1) + 20—30% (1) + 4—6% (2) + 5—10% (3) + 3—5% (4)

CPV Impact + $54 (1) + $89 (1) + $10 (2) + $20 (3) + $4 (4)

Market Growth > 17% CAGR > 10% CAGR > 10% CAGR > 15% CAGR > 10% CAGR

Global Adoption (5) (6)

27% / 46% 20% / 30% 72% / 95% 30% / 45% 50% / 75%

Rate 2014/2018

Key Regions /

Markets

Technologies needed on a global scale to meet fuel economy regulations

Conversion/implementation rates will outpace market growth

• All of these technologies require numerous high precision metal components

24

|

|

Target Segments: Fuel Saving Technologies

MPFI V6 GDI V6

GDI Fuel System

Precision Turned Part content: Precision Turned Part content:

6 injectors 6 Injectors

• 1 High pressure fuel pump

• 2 High pressure fittings

$6.00 per vehicle $60 per vehicle

Technology requires more precision, tighter tolerances

GDI will have a VERY long life: 10-15+ years (MPFI lived for 30+ years) 25

|

|

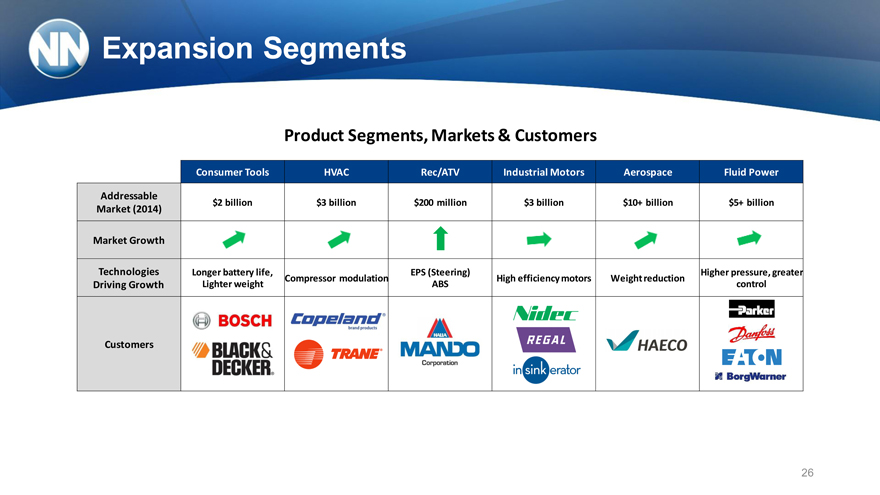

Expansion Segments

Product Segments, Markets & Customers

Consumer Tools HVAC Rec/ATV Industrial Motors Aerospace Fluid Power

Addressable $2 billion $3 billion $200 million $3 billion $10+ billion $5+ billion

Market (2014)

Market Growth

Technologies Longer battery life, EPS (Steering) Higher pressure, greater Compressor modulation High efficiency motors Weight reduction Driving Growth Lighter weight ABS control

Customers

26

|

|

27

|

|

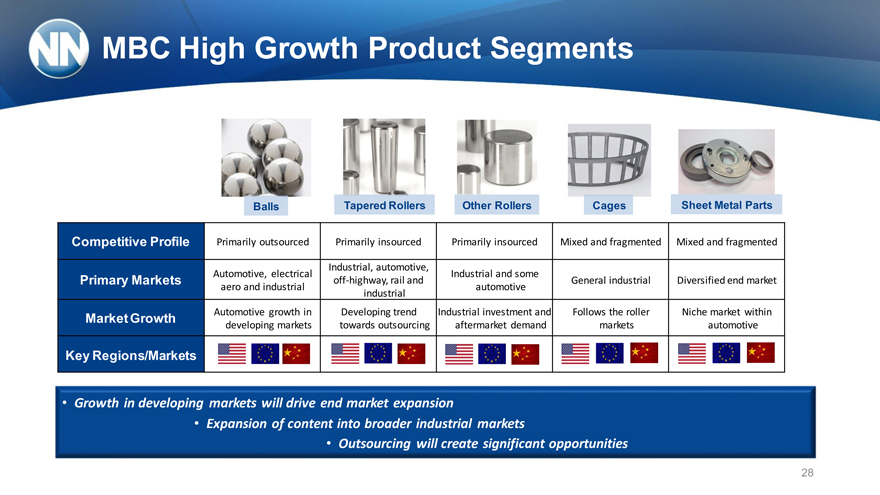

MBC High Growth Product Segments

Balls Tapered Rollers Other Rollers Cages Sheet Metal Parts

Competitive Profile Primarily outsourced Primarily insourced Primarily insourced Mixed and fragmented Mixed and fragmented

Industrial, automotive,

Automotive, electrical Industrial and some

Primary Markets off-highway, rail and General industrial Diversified end market

aero and industrial automotive

industrial

Market Growth Automotive growth in Developing trend Industrial investment and Follows the roller Niche market within

developing markets towards outsourcing aftermarket demand markets automotive

Key Regions/Markets

Growth in developing markets will drive end market expansion

Expansion of content into broader industrial markets

• Outsourcing will create significant opportunities

28

|

|

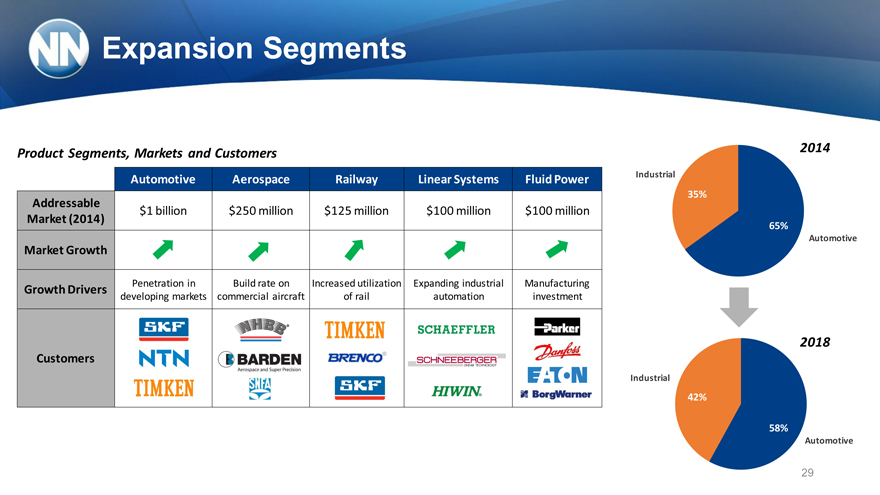

Expansion Segments

Product Segments, Markets and Customers 2014

Automotive Aerospace Railway Linear Systems Fluid Power Industrial

35%

Addressable

$1 billion $250 million $125 million $100 million $100 million

Market (2014)

65%

Automotive

Market Growth

Growth Drivers Penetration in Build rate on Increased utilization Expanding industrial Manufacturing

developing markets commercial aircraft of rail automation investment

2018

Customers

Industrial

42%

58%

Automotive

29

|

|

2014 Results

30

|

|

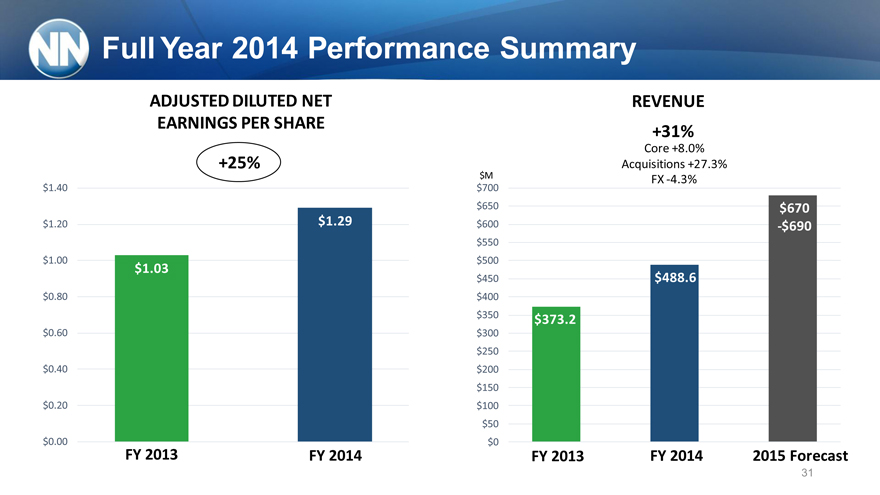

Full Year 2014 Performance Summary

ADJUSTED DILUTED NET

EARNINGS PER SHARE

+25%

$1.40

$1.20 $1.29

$1.00

$1.03

$0.80

$0.60

$0.40

$0.20

$0.00

FY 2013 FY 2014

REVENUE

+31%

Core +8.0%

Acquisitions +27.3%

$M FX -4.3%

$700

$650 $670

$600 -$690

$550

$500

$450 $488.6

$400

$350 $373.2

$300

$250

$200

$150

$100

$50

$0

FY 2013 FY 2014 2015 Forecast

31

|

|

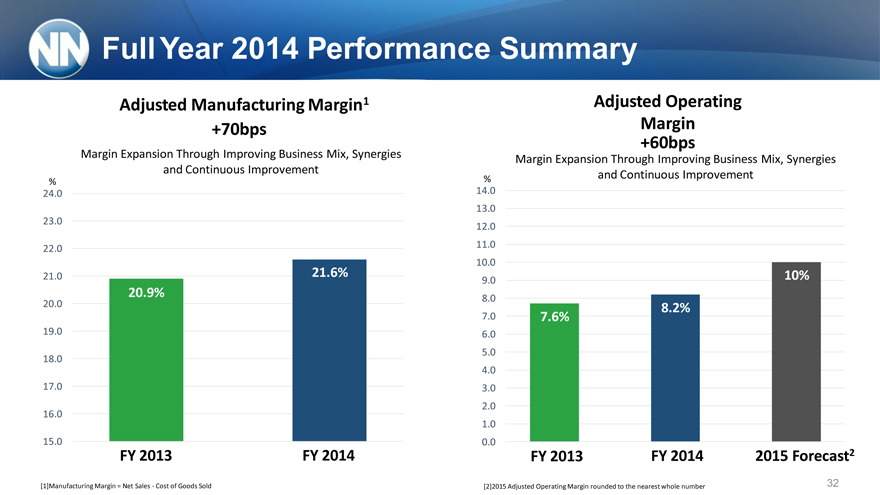

Adjusted Operating Margin +60bps

Margin Expansion Through Improving Business Mix, Synergies % and Continuous Improvement

Full Year 2014 Performance Summary

Adjusted Manufacturing Margin1 +70bps

Margin Expansion Through Improving Business Mix, Synergies and Continuous Improvement

%

24.0

23.0

22.0

21.0 21.6% 20.9%

20.0 19.0 18.0 17.0 16.0

15.0

FY 2013 FY 2014

14.0 13.0 12.0 11.0 10.0

9.0 10%

8.0 8.2%

7.0 7.6%

6.0

5.0

4.0

3.0

2.0

1.0

0.0

FY 2013 FY 2014 2015 Forecast2

[1]Manufacturing Margin = Net Sales—Cost of Goods Sold

[2]2015 Adjusted Operating Margin rounded to the nearest whole number

32

|

|

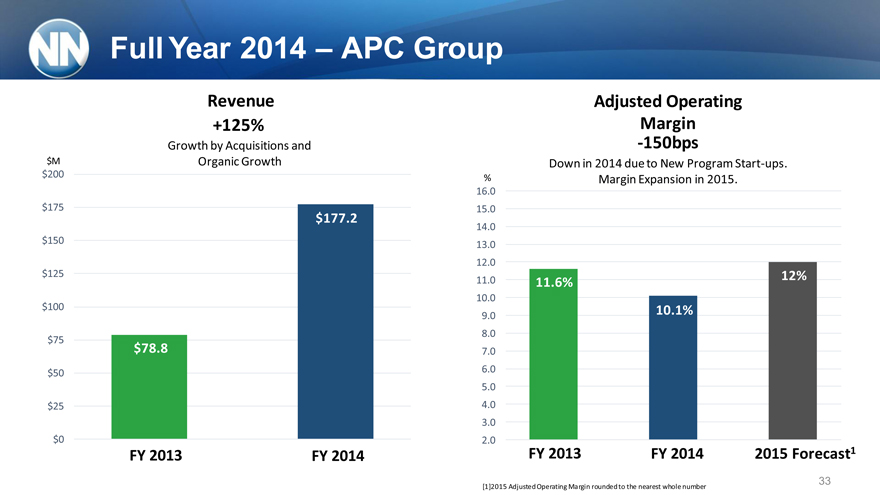

Full Year 2014 – APC Group

Revenue +125%

Growth by Acquisitions and $M Organic Growth

$200

$175

$177.2

$150

$125

$100

20.9%

$75

$78.8

$50

$25

$0

FY 2013 FY 2014

Adjusted Operating

Margin

-150bps

Down in 2014 due to New Program Start-ups.

% Margin Expansion in 2015.

16.0

15.0

14.0

13.0

12.0

11.0 12%

11.6%

10.0

10.1%

9.0

8.0

7.0

6.0

5.0

4.0

3.0

2.0

FY 2013 FY 2014 2015 Forecast1

33

[1]2015 Adjusted Operating Margin rounded to the nearest whole number

|

|

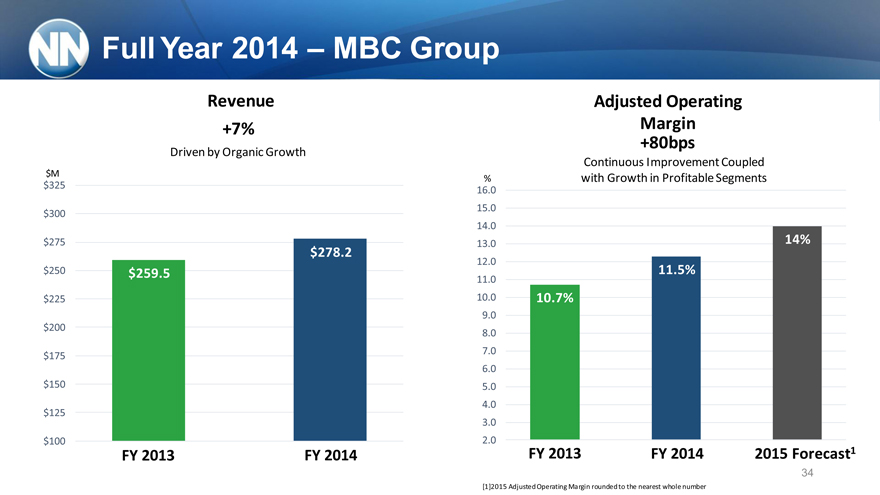

Full Year 2014 – MBC Group

Revenue

+7%

Driven by Organic Growth

$M

$325

$300

$275 $278.2

$250 $259.5

$225

$200

$175

$150

$125

$100

FY 2013 FY 2014

Adjusted Operating

Margin

+80bps

Continuous Improvement Coupled

% with Growth in Profitable Segments

16.0

15.0

14.0

13.0 14%

12.0

11.5%

11.0

10.0 10.7% 8.2

9.0 6%

8.0

7.0

6.0

5.0

4.0

3.0

2.0

FY 2013 FY 2014 2015 Forecast1

34

[1]2015 Adjusted Operating Margin rounded to the nearest whole number

|

|

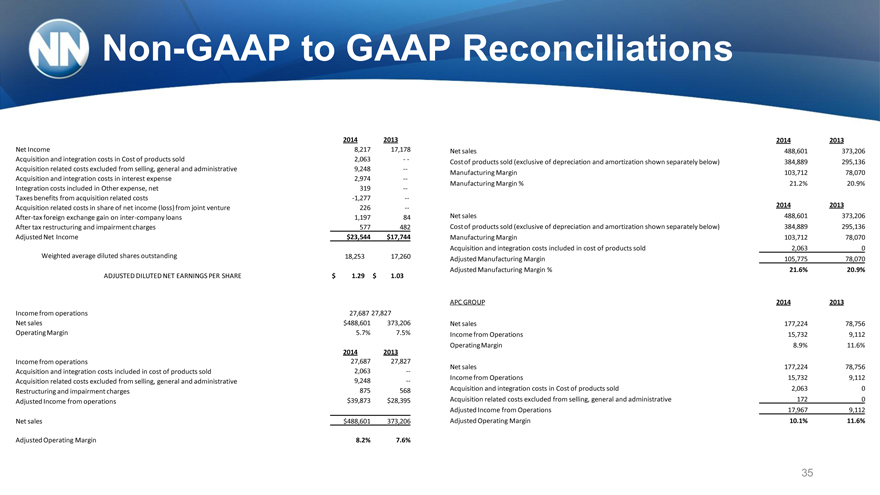

Non-GAAP to GAAP Reconciliations

2014 2013 2014 2013

Net Income 8,217 17,178 Net sales 488,601 373,206 Acquisition and integration costs in Cost of products sold 2,063 — Cost of products sold (exclusive of depreciation and amortization shown separately below) 384,889 295,136 Acquisition related costs excluded from selling, general and administrative 9,248 — Manufacturing Margin 103,712 78,070 Acquisition and integration costs in interest expense 2,974 — Manufacturing Margin % 21.2% 20.9% Integration costs included in Other expense, net 319 — Taxes benefits from acquisition related costs -1,277 — 2014 2013

Acquisition related costs in share of net income (loss) from joint venture 226 —

After-tax foreign exchange gain on inter-company loans 1,197 84 Net sales 488,601 373,206 After tax restructuring and impairment charges 577 482 Cost of products sold (exclusive of depreciation and amortization shown separately below) 384,889 295,136 Adjusted Net Income $23,544 $17,744 Manufacturing Margin 103,712 78,070 Acquisition and integration costs included in cost of products sold 2,063 0 Weighted average diluted shares outstanding 18,253 17,260 Adjusted Manufacturing Margin 105,775 78,070 Adjusted Manufacturing Margin % 21.6% 20.9% ADJUSTED DILUTED NET EARNINGS PER SHARE $ 1.29 $ 1.03

APC GROUP 2014 2013

Income from operations 27,687 27,827

Net sales $488,601 373,206 Net sales 177,224 78,756 Operating Margin 5.7% 7.5% Income from Operations 15,732 9,112 Operating Margin 8.9% 11.6%

2014 2013

Income from operations 27,687 27,827

Net sales 177,224 78,756 Acquisition and integration costs included in cost of products sold 2,063 —Income from Operations 15,732 9,112 Acquisition related costs excluded from selling, general and administrative 9,248 —875 568 Acquisition and integration costs in Cost of products sold 2,063 0 Restructuring and impairment charges Adjusted Income from operations $39,873 $28,395 Acquisition related costs excluded from selling, general and administrative 172 0 Adjusted Income from Operations 17,967 9,112 Net sales $488,601 373,206 Adjusted Operating Margin 10.1% 11.6%

Adjusted Operating Margin 8.2% 7.6%

35

|

|

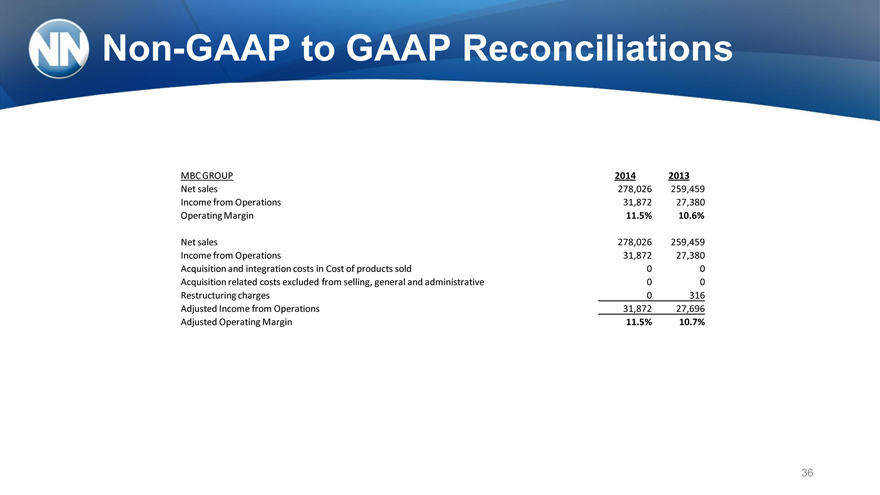

Non-GAAP to GAAP Reconciliations

MBC GROUP 2014 2013 Net sales 278,026 259,459 Income from Operations 31,872 27,380 Operating Margin 11.5% 10.6%

Net sales 278,026 259,459 Income from Operations 31,872 27,380 Acquisition and integration costs in Cost of products sold 0 0 Acquisition related costs excluded from selling, general and administrative 0 0 Restructuring charges 0 316 Adjusted Income from Operations 31,872 27,696 Adjusted Operating Margin 11.5% 10.7%

36

|

|

Investor Presentation

March 23, 2015