Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - NATIONAL FUEL GAS CO | d893922d8k.htm |

National Fuel Gas

Company Investor Presentation

Scotia Howard Weil 43

rd

Annual

Energy Conference -

March 2015

1

Exhibit

99 |

Corporate

This

presentation

may

contain

“forward-looking

statements”

as

defined

by

the

Private

Securities

Litigation

Reform

Act

of

1995,

including

statements

regarding

future

prospects,

plans,

objectives,

goals,

projections,

estimates

of

oil

and

gas

quantities,

strategies,

future

events

or

performance

and

underlying

assumptions,

capital

structure,

anticipated

capital

expenditures,

completion

of

construction

projects,

projections

for

pension

and

other

post-retirement

benefit

obligations,

impacts

of

the

adoption

of

new

accounting

rules,

and

possible

outcomes

of

litigation

or

regulatory

proceedings,

as

well

as

statements

that

are

identified

by

the

use

of

the

words

“anticipates,”

“estimates,”

“expects,”

“forecasts,”

“intends,”

“plans,”

“predicts,”

“projects,”

“believes,”

“seeks,”

“will,”

“may,”

and

similar

expressions.

Forward-looking

statements

involve

risks

and

uncertainties

which

could

cause

actual

results

or

outcomes

to

differ

materially

from

those

expressed

in

the

forward-looking

statements.

The

Company’s

expectations,

beliefs

and

projections

are

expressed

in

good

faith

and

are

believed

by

the

Company

to

have

a

reasonable

basis,

but

there

can

be

no

assurance

that

management’s

expectations,

beliefs

or

projections

will

result

or

be

achieved

or

accomplished.

In

addition

to

other

factors,

the

following

are

important

factors

that,

in

the

view

of

the

Company,

could

cause

actual

results

to

differ

materially

from

those

discussed

in

the

forward-looking

statements:

factors

affecting

the

Company’s

ability

to

successfully

identify,

drill

for

and

produce

economically

viable

natural

gas

and

oil

reserves,

including

among

others

geology,

lease

availability,

title

disputes,

weather

conditions,

shortages,

delays

or

unavailability

of

equipment

and

services

required

in

drilling

operations,

insufficient

gathering,

processing

and

transportation

capacity,

the

need

to

obtain

governmental

approvals

and

permits,

and

compliance

with

environmental

laws

and

regulations;

the

cost

and

effects

of

legal

and

administrative

claims

against

the

Company

or

activist

shareholder

campaigns

to

effect

changes

at

the

Company;

changes

in

laws,

regulations

or

judicial

interpretations

to

which

the

Company

is

subject,

including

those

involving

derivatives,

taxes,

safety,

employment,

climate

change,

other

environmental

matters,

real

property,

and

exploration

and

production

activities

such

as

hydraulic

fracturing;

governmental/regulatory

actions,

initiatives

and

proceedings,

including

those

involving

rate

cases

(which

address,

among

other

things,

target

rates

of

return,

rate

design

and

retained

natural

gas),

environmental/safety

requirements,

affiliate

relationships,

industry

structure,

and

franchise

renewal;

changes

in

the

price

of

natural

gas

or

oil;

changes

in

price

differentials

between

similar

quantities

of

natural

gas

or

oil

sold

at

different

geographic

locations,

and

the

effect

of

such

changes

on

commodity

production,

revenues

and

demand

for

pipeline

transportation

capacity

to

or

from

such

locations;

other

changes

in

price

differentials

between

similar

quantities

of

natural

gas

or

oil

having

different

quality,

heating

value,

hydrocarbon

mix

or

delivery

date;

impairments

under

the

SEC’s

full

cost

ceiling

test

for

natural

gas

and

oil

reserves;

uncertainty

of

oil

and

gas

reserve

estimates;

significant

differences

between

the

Company’s

projected

and

actual

production

levels

for

natural

gas

or

oil;

delays

or

changes

in

costs

or

plans

with

respect

to

Company

projects

or

related

projects

of

other

companies,

including

difficulties

or

delays

in

obtaining

necessary

governmental

approvals,

permits

or

orders

or

in

obtaining

the

cooperation

of

interconnecting

facility

operators;

changes

in

demographic

patterns

and

weather

conditions;

changes

in

the

availability,

price

or

accounting

treatment

of

derivative

financial

instruments;

financial

and

economic

conditions,

including

the

availability

of

credit,

and

occurrences

affecting

the

Company’s

ability

to

obtain

financing

on

acceptable

terms

for

working

capital,

capital

expenditures

and

other

investments,

including

any

downgrades

in

the

Company’s

credit

ratings

and

changes

in

interest

rates

and

other

capital

market

conditions;

changes

in

economic

conditions,

including

global,

national

or

regional

recessions,

and

their

effect

on

the

demand

for,

and

customers’

ability

to

pay

for,

the

Company’s

products

and

services;

the

creditworthiness

or

performance

of

the

Company’s

key

suppliers,

customers

and

counterparties;

economic

disruptions

or

uninsured

losses

resulting

from

major

accidents,

fires,

severe

weather,

natural

disasters,

terrorist

activities,

acts

of

war,

cyber

attacks

or

pest

infestation;

significant

differences

between

the

Company’s

projected

and

actual

capital

expenditures

and

operating

expenses;

changes

in

laws,

actuarial

assumptions,

the

interest

rate

environment

and

the

return

on

plan/trust

assets

related

to

the

Company’s

pension

and

other

post-retirement

benefits,

which

can

affect

future

funding

obligations

and

costs

and

plan

liabilities;

increasing

health

care

costs

and

the

resulting

effect

on

health

insurance

premiums

and

on

the

obligation

to

provide

other

post-retirement

benefits;

or

increasing

costs

of

insurance,

changes

in

coverage

and

the

ability

to

obtain

insurance.

Forward-looking

statements

include

estimates

of

oil

and

gas

quantities.

Proved

oil

and

gas

reserves

are

those

quantities

of

oil

and

gas

which,

by

analysis

of

geoscience

and

engineering data, can be estimated with reasonable certainty to be economically producible under

existing economic conditions, operating methods and government regulations.

Other

estimates

of

oil

and

gas

quantities,

including

estimates

of

probable

reserves,

possible

reserves,

and

resource

potential,

are

by

their

nature

more

speculative

than

estimates

of

proved

reserves.

Accordingly,

estimates

other

than

proved

reserves

are

subject

to

substantially

greater

risk

of

being

actually

realized.

Investors

are

urged

to

consider

closely

the

disclosure

in

our

Form

10-K

available

at

www.nationalfuelgas.com.

You

can

also

obtain

this

form

on

the

SEC’s

website

at

www.sec.gov.

For

a

discussion

of

the

risks

set

forth

above

and

other

factors

that

could

cause

actual

results

to

differ

materially

from

results

referred

to

in

the

forward-looking

statements,

see

“Risk

Factors”

in

the

Company’s

Form

10-K

for

the

fiscal

year

ended

September

30,

2014

and

the

Form

10-Q

for

the

quarter

ended

December

31,

2014.

The

Company

disclaims

any

obligation

to

update

any

forward-looking

statements

to

reflect

events

or

circumstances

after

the

date

thereof

or

to

reflect

the

occurrence

of

unanticipated

events.

Safe Harbor For Forward Looking Statements

2 |

Corporate

3 Million BBls of Crude Oil Production

$260 Million of Midstream Adjusted EBITDA

800,000 Net Acres in Pennsylvania

1.914 Tcfe of Proved Reserves

Quality Assets, Exceptional Location, Unique Integration

3 |

Corporate

Unique Integrated Business Model Provides Competitive Advantage

The National Fuel Value Proposition

4

800,000

net

acres

in

Pennsylvania

–

2

nd

largest

acreage

position

in

Marcellus

Shale

(1)

WDA mineral ownership = no royalty or drilling commitments

Stacked pay potential in Marcellus, Utica and Geneseo shales

Coordinated midstream infrastructure build-out

Opportunity for further pipeline expansion to accommodate Appalachian supply growth

Creating sustainable value for shareholders remains our #1 priority

Considerable Upstream and Midstream Growth Opportunities in Appalachia

Integration significantly reduces operational and financing costs

Diversified cash flows provide stability in challenging commodity price environment

Strong Balance Sheet and History of Disciplined Financial Management

Investment grade credit rating and liquidity to support Appalachian growth strategy

Disciplined capital investment focused on economic returns

112-year commitment to the dividend

(1) Per NGI’s Shale Daily

(January 5, 2015). 780,000 acres prospective in Marcellus Shale.

|

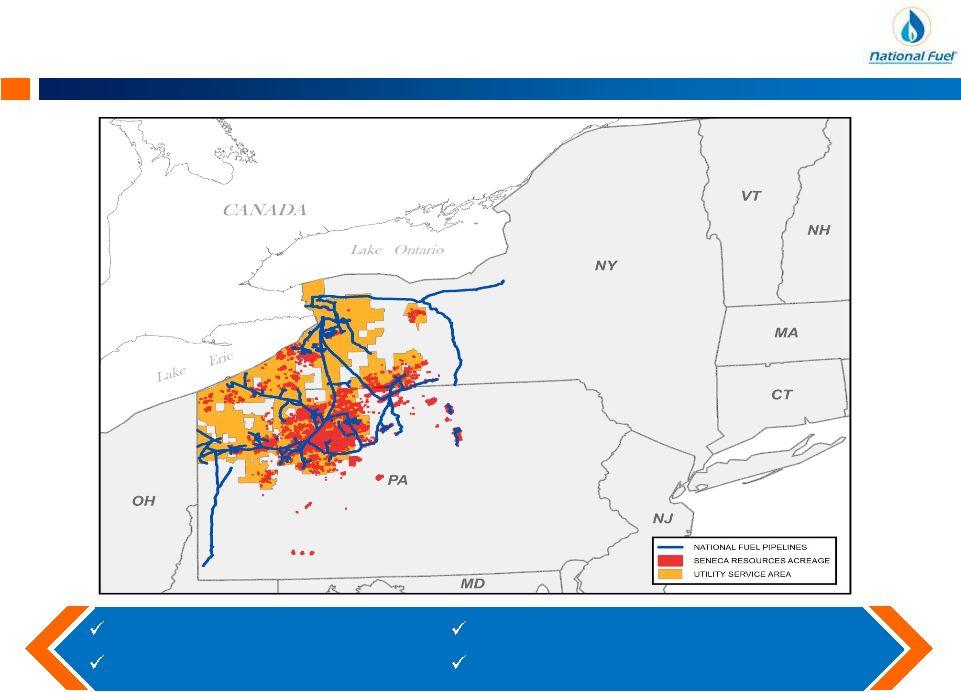

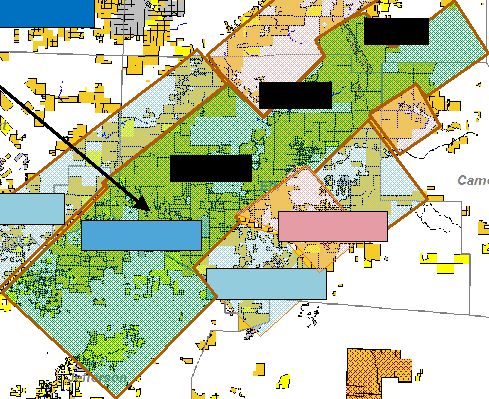

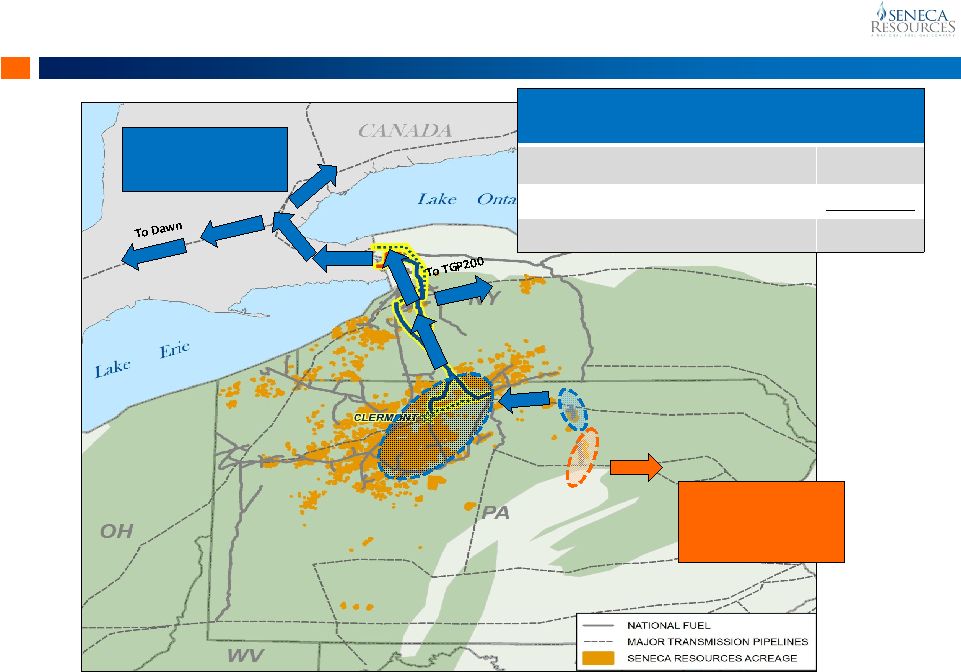

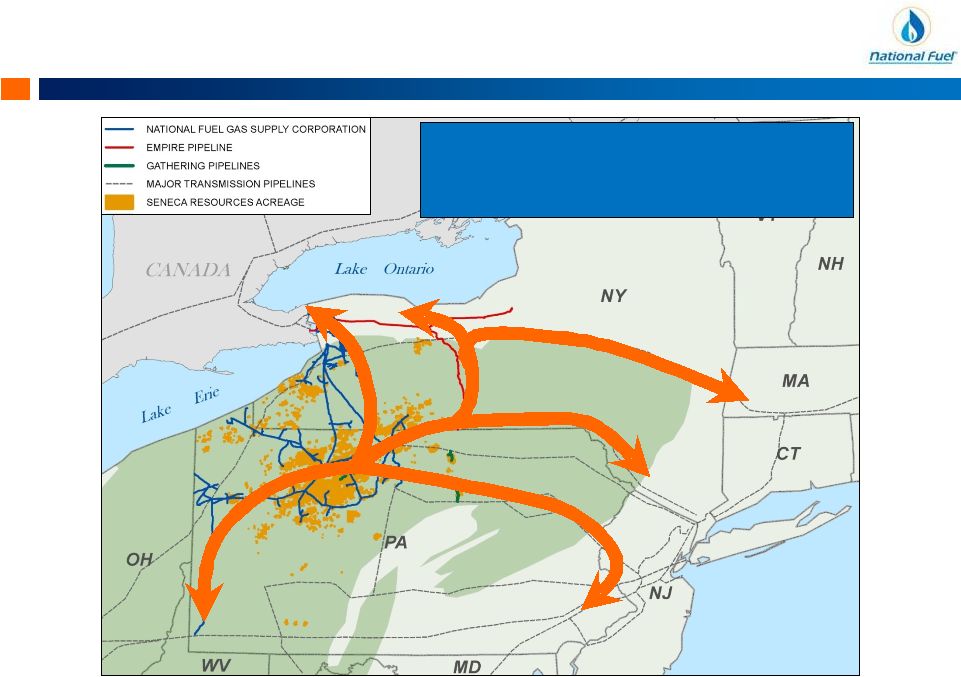

Corporate

Upstream & Midstream –

Common Vision For Growth

5

Western Development Area

Tier I Acreage: 200,000 Acres

Clermont Gathering System

NFG Supply & Other Interconnects

High quality

Marcellus acreage

Connected to our

interstate pipeline

network

Pipeline capacity to premium

and alternate markets

Northern Access Projects

490 MMcf/d to Canada by 2016 |

Corporate

EBITDA Growth by Segment

6

Note: A reconciliation of Adjusted EBITDA to Net Income as presented on the Consolidated

Statement of Income and Earnings Reinvested in the Business is included at the end of this presentation. |

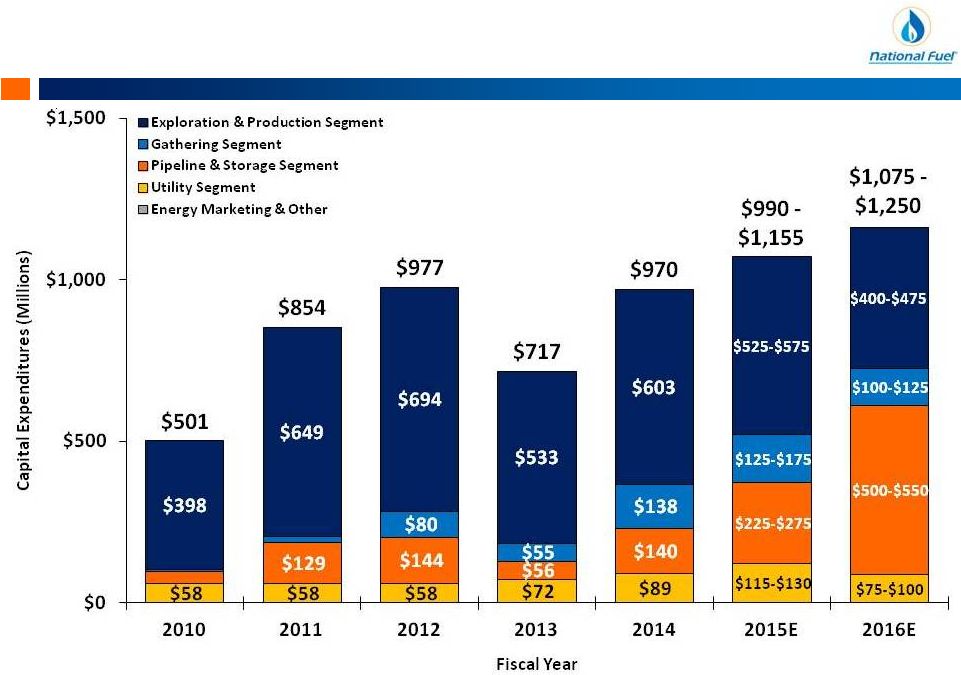

Corporate

Adjusting Capex to Capitalize on Opportunities

7

Note: A reconciliation to Capital Expenditures as presented on the Consolidated Statement of

Cash Flows is included at the end of this presentation. |

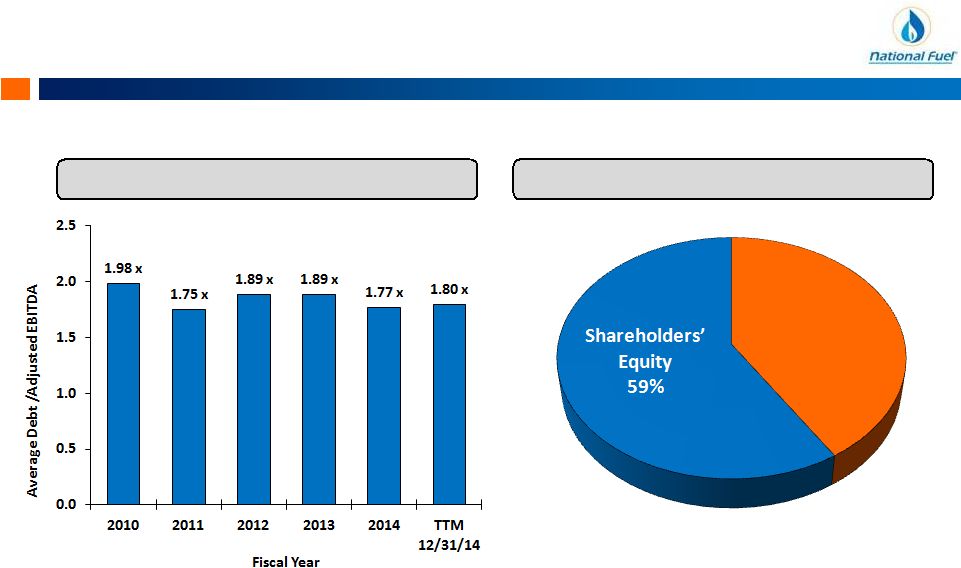

Corporate

Maintaining a Strong Balance Sheet

8

Note: A reconciliation of Adjusted EBITDA to Net Income is included at the end of this

presentation. (1)

Long-term debt of $1.649 billion and short-term debt of $172.9 million.

Total Debt

(1)

41%

$4.4 Billion

As of December 31, 2014

Debt/Adjusted EBITDA

Capitalization |

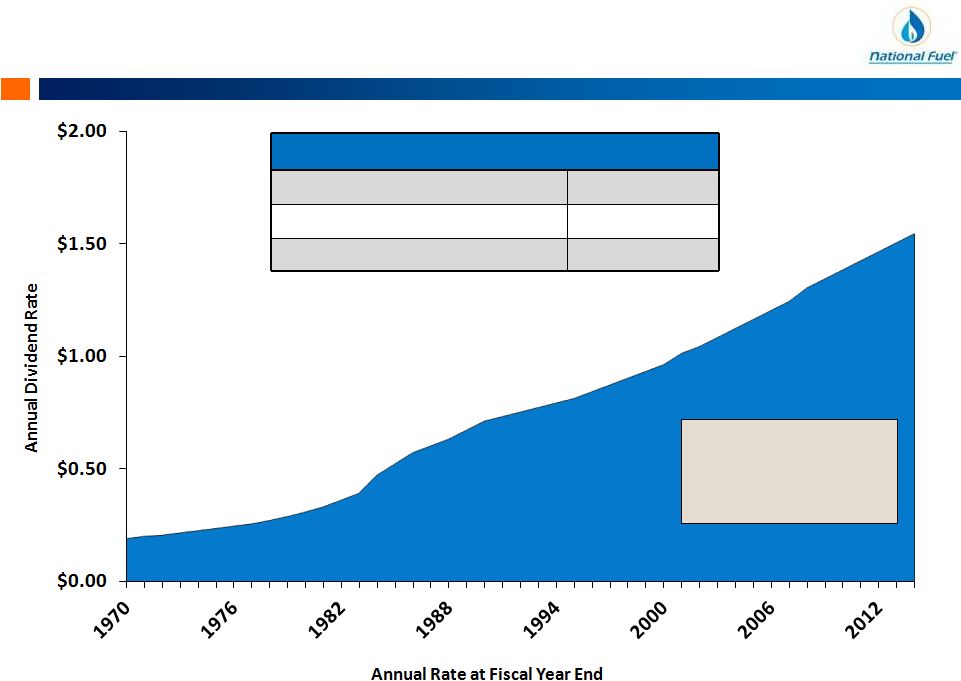

Corporate

Dividend Track Record

9

(1) As of March 18, 2015.

Current

Dividend Yield

(1)

2.5%

Dividend Consistency

Consecutive Dividend Payments

112 Years

Consecutive Dividend Increases

44 Years

Current Annualized Dividend Rate

$1.54 per Share |

Upstream

Overview Exploration & Production

10 |

Upstream

Proven Record of Reserve Growth

11

(1) Represents a three-year average U.S. finding and development cost.

Fiscal

Years

3-Year

F&D Cost

(1)

($/Mcfe)

2007-2009

$5.35

2008-2010

$2.37

2009-2011

$2.09

2010-2012

$1.87

2011-2013

$1.67

2012-2014

$1.38

•

2014 F&D Cost = $1.15

•

Marcellus F&D: $1.00

•

327% Reserve

Replacement Rate

•

73% Proved Developed |

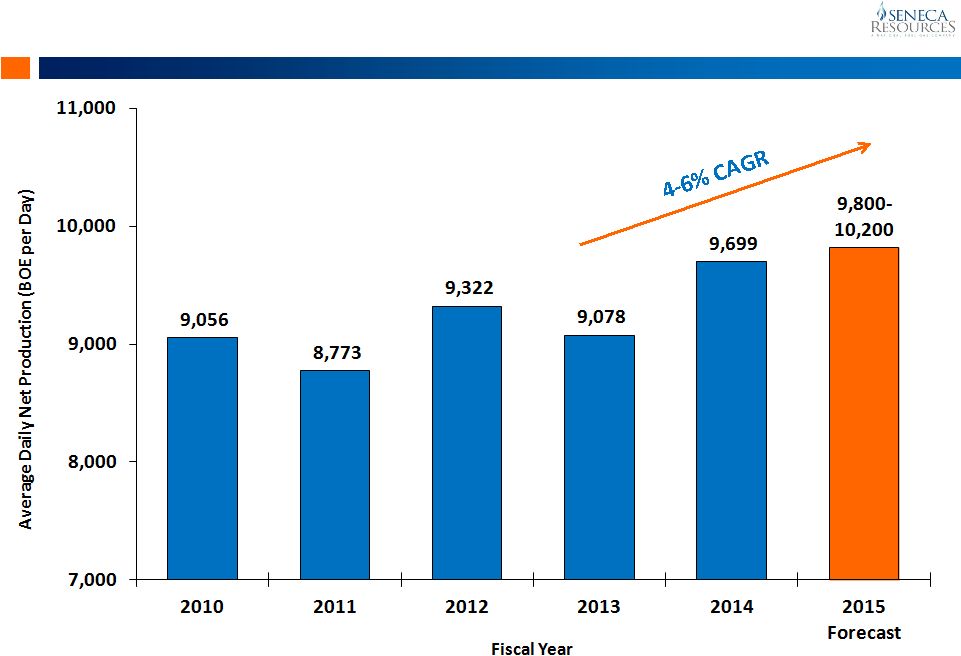

Upstream

Delivering Tremendous Production Growth

12 |

Upstream

Disciplined Capital Spending

13 |

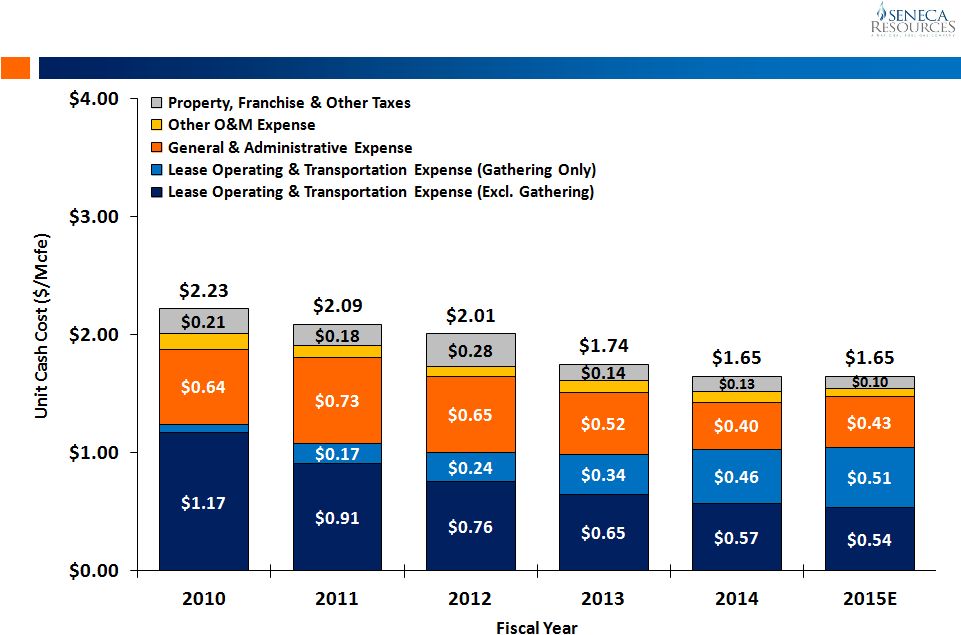

Upstream

Highly Competitive Cost Structure

14

(1)

Represents the midpoint of current General & Administrative Expense guidance of $0.40 to

$0.45 per Mcfe for fiscal 2015. (2)

The total of the two LOE components represents the midpoint of current LOE guidance of $1.00

to $1.10 per Mcfe for fiscal 2015. (3)

The cost of firm transportation is reflected in price realizations (a deduction to gross

revenues). As such, it is not included in LOE. (1)

(2)

(2)

(3) |

Upstream

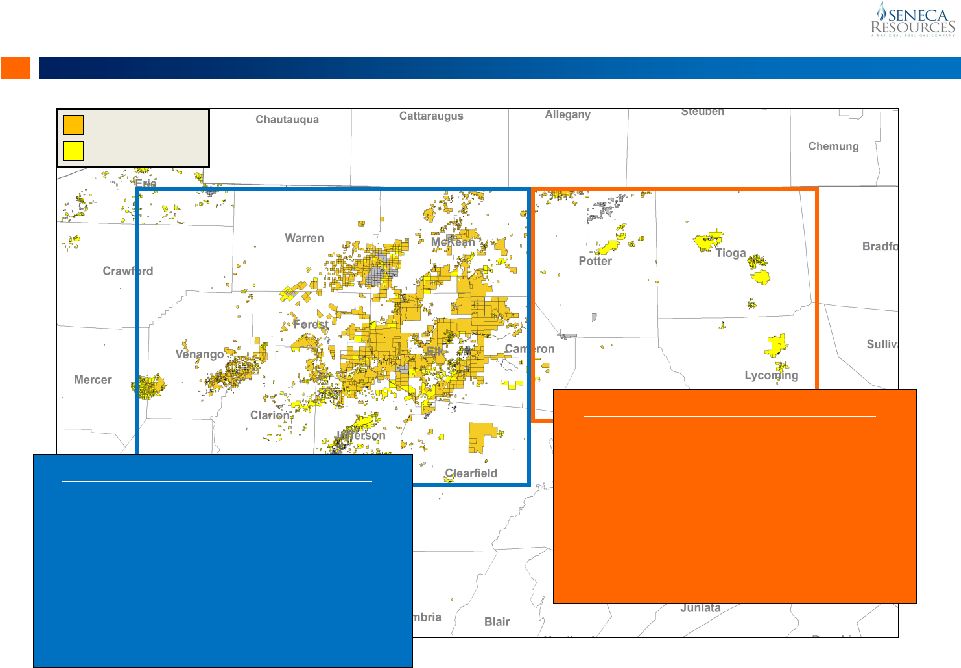

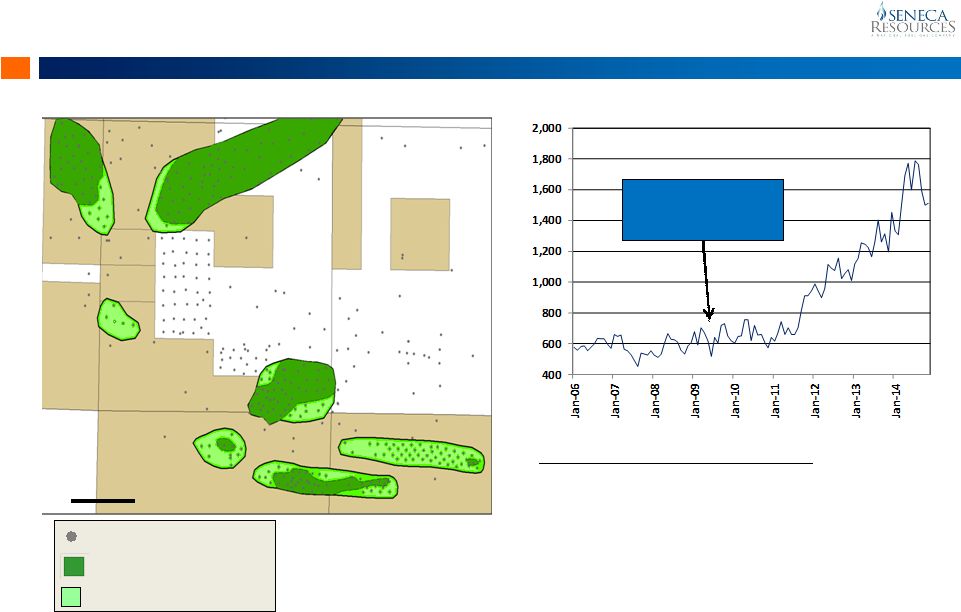

Marcellus Shale: Prolific Pennsylvania Acreage

15

Eastern Development Area (EDA)

•

Mostly leased (16-18% royalty)

•

No near-term lease expiration

•

Limited development drilling until firm

transportation capacity on Atlantic

Sunrise becomes available in late 2017

o

Drilling activity will HBP key acreage

Western Development Area (WDA)

•

Average

net

revenue

interest

(NRI):

98%

o

No

lease

expiration

o

No

royalty

on

most

acreage

•

Highly

contiguous

o

Significant

economies

of

scale

•

1,700

to

2,000

locations

de-risked

Seneca Lease

Seneca Fee

720,000 Acres

60,000 Acres |

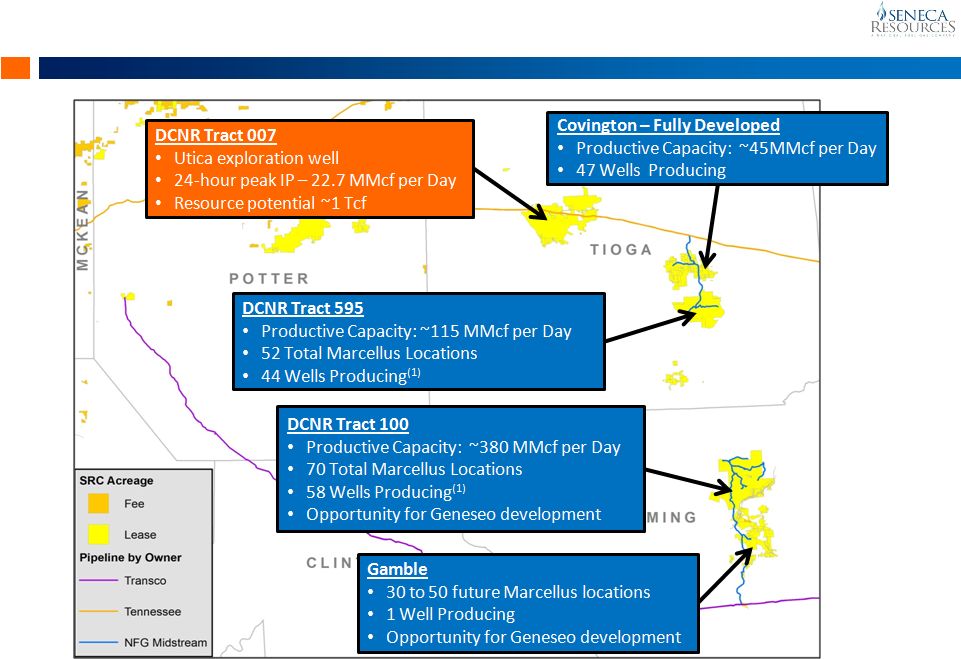

Upstream

Marcellus Well Results

16

(1)

Does

not

include

a

well

drilled

into

and

producing

from

the

Geneseo

Shale.

Area

Producing Well

Count

Peak 24-Hour

Rate (MMcfd)

Average

7-Day (MMcf/d)

Average Treatable

Lateral Length (ft)

Clermont / Rich Valley

(CRV)

Elk, Cameron &

McKean counties

19

8.1

7.2

5,710’

WDA Development Wells:

EDA Development Wells:

Area

Producing Well

Count

Peak 24-Hour

Rate (MMcfd)

Average

7-Day (MMcf/d)

Average Treatable

Lateral Length (ft)

Covington

Tioga

County

47

5.2

4.7

4,023’

Tract 595

Tioga

County

43

(1)

7.4

6.1

4,765’

Tract 100

Lycoming

County

57

(1)

16.8

14.8

5,270’ |

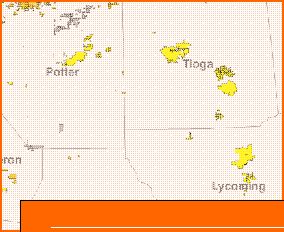

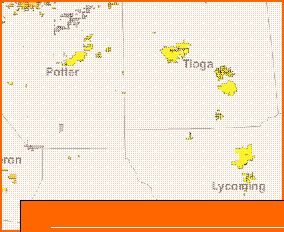

Upstream

EDA Delivering Significant Growth

17

(1)

One

well

included

in

this

total

is

drilled

into

and

producing

from

the

Geneseo

Shale. |

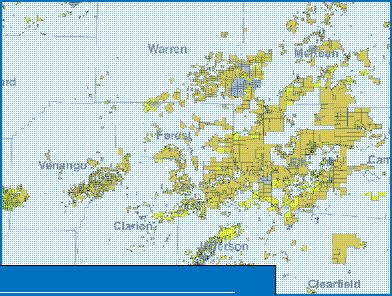

Upstream

Focusing on WDA Development

18

Note:

Assumes

6,000’

treated

lateral

length.

4 -

6 BCF/well

4 -

6 BCF/well

6 -

8 BCF/well

2-4 BCF/well

SRC Lease Acreage

SRC Fee Acreage

EOG Earned JV Acreage

Seneca’s Tier I Acreage:

•

200,000 Acres

•

6-8 Bcfe EUR Wells

•

Economic at $2.60 to $4.00/MMbtu

CRV

Hemlock

Ridgeway

2-4 BCF/well |

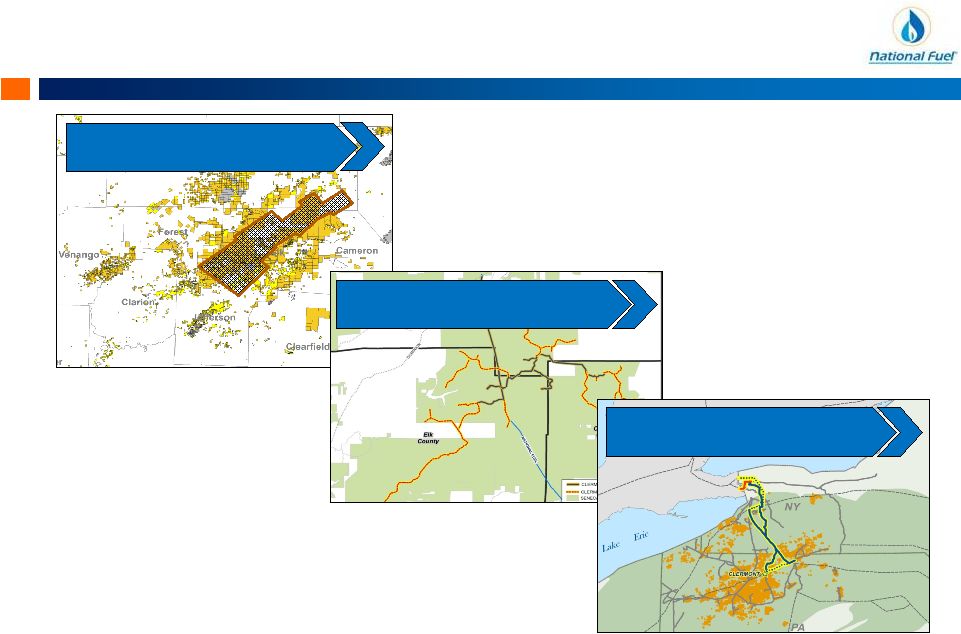

Upstream

Clermont/Rich Valley (CRV) Area

19 |

Upstream

~2,000 Economic WDA Locations Below $4/MMBtu

20

(1)

Internal

Rate

of

Return

(IRR)

includes

estimated

well

costs

under

current

cost

structure,

LOE,

and

Gathering

tariffs

anticipated

for

each

prospect.

Prospect

Product

Locations

Remaining to

Be Drilled

Completed

Lateral Length

(ft)

EUR

Assumption

(MMcf)

BTU

$4.50

Dawn/Nymex

(% IRR)

$4.00

Dawn/Nymex

(% IRR)

15% IRR

Realized Price

DCNR 100

Dry Gas

13

5,582

13,540

1030

>100%

74%

$1.84

Gamble

Dry Gas

28

4,605

11,240

1030

72%

50%

$2.08

DCNR 595

Dry Gas

8

4,475

6,890

1030

46%

33%

$2.28

Clermont - Rich Valley

Dry Gas

148

7,000

7,817

1050

42%

28%

$2.60

Hemlock

Dry Gas

157

7,000

7,000

1050

35%

24%

$2.78

Ridgway

Dry Gas

564

7,000

6,300

1111

31%

21%

$2.90

Remaining Tier 1

Dry Gas

1,020

7,000

6,000

1030 - 1100

$3.00 -

$4.00

Future Resource

Dry & Wet

Gas

1,620

7,000

6,000

1030 - 1350

>$4.00

Additional Delineation Required

(1) |

Upstream

WDA Mineral Interests Significantly Enhance Returns

21

(1)

Internal

Rate

of

Return

(IRR)

includes

estimated

well

costs

under

current

cost

structure,

LOE,

and

Gathering

tariffs

anticipated

for

each

prospect.

($/Mcf)

The Seneca

Advantage

0% Royalty

Realized Price

$ 2.60

Less: Royalty Payment

(0.00)

Less: Cash Operating Expenses

(0.65)

Cash Margin

$ 1.95

Before Tax IRR

(1)

15%

A producer burdened by a 15% royalty would

require a $0.46 higher realized price to achieve

same level of economics as Seneca Resources

Producer

Paying

15% Royalty

$ 2.60

(0.39)

(0.65)

$ 1.56

8%

Clermont/Rich Valley Example |

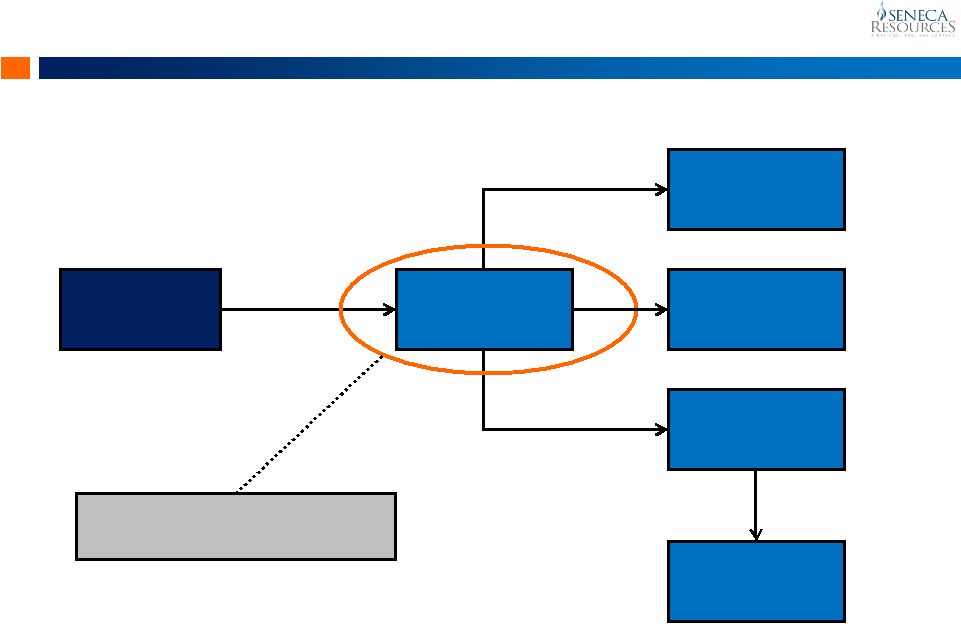

Upstream

How Does Seneca Sell its Production?

22

Well Head

Interconnection

with Interstate

Pipeline Network

Gathering

System

3rd Party

Marketer

(or spot market)

Firm Transport

Demand Center

(firm sales or

spot market)

Contracted Basis

Differential

FT Rate

Spot Market

Breakeven economics based on a

realized price after gathering |

Upstream

Adding Long-Term Firm Transport to the Portfolio

23

(1) A large majority of the executed firm sales agreements continue for the

remainder of the firm transportation contract term. Project

(Counterparty)

In-

Service

Date

Contract

Term

Delivery

Market

FT Capacity (Dth/day)

Matched Firm

Sales Contracts

Fiscal

2015

Fiscal

2016

Fiscal

2017

Fiscal

2018

Northeast Supply

Diversification

Project (TGP)

Nov.

2012

15 years

Canada

50,000

50,000

50,000

50,000

Executed Contracts

50,000 Dth/d

for 10 years

Niagara

Expansion/

TETCO

(TGP

&

NFG)

Nov.

2015

15 years

Canada

---

158,000

158,000

158,000

Executed Contracts

140,000 Dth/d

for 15 years

TETCO

---

12,000

12,000

12,000

Northern Access

2016 (NFG/

TransCanada/

Union)

Nov.

2016

15 years

Canada

---

---

350,000

350,000

Evaluating

marketing

opportunities

TGP 200

(NY)

---

---

140,000

140,000

Atlantic Sunrise

(Transco)

Nov.

2017

15 years

Mid-

Atlantic/

Southeast

---

---

---

189,405

Executed Contracts

189,405 Dth/d

for first 5 years

(1)

Total Firm Transportation Capacity

50,000

220,000

710,000

899,405 |

Upstream

Significant Base of Long-Term Firm Contracts

24

(1) Includes base firm sales contracts not tied to firm transportation capacity.

Atlantic Sunrise

Williams Co. (Transco)

189,405 Dth/d

Northern Access 2016

NFG & TransCanada

490,000 Dth/d

Niagara Expansion

TGP & NFG

170,000 Dth/d

Current Firm Sales & FT

(1)

914,405 Dth per day

(1)

Total Firm Contracts by FY 2018 |

Upstream

Reaching High Value Markets

25

Seneca FT Capacity by Fiscal 2018

(Dth per day)

Canadian Markets

558,000

Mid-Atlantic, Southeast & Other

+ 341,405

Total Firm Transport Capacity

899,405

To Mid-Atlantic

& Southeast

Markets

To Canadian

Markets |

Upstream

Firm Sales Provide Market for Appalachian Production

26

(1)

EDA

and

WDA

carry

an

average

net

revenue

interest

(NRI)

of

82%

-

84%

and

98%,

respectively.

Values

shown

represent

the

price

or

differential

to

a

reference

price

(netback

price)

at

the

first

non-affiliated

interstate

pipeline,

including

the

cost

of

all

related

downstream

transportation

EDA

(1)

320,098 Dth/d

280,036 Dth/d

280,036 Dth/d

WDA

(1)

61,427 Dth/d

60,000 Dth/d

60,000 Dth/d

50,000

Fixed $3.77

50,000

Fixed $3.77

50,000

Fixed $3.77

Dominion

95,327

Less: $0.42

Dominion

85,000

Less: $0.47

Dominion

85,000

Less: $0.47

NYMEX

236,198

Less: $0.51

NYMEX

205,036

Less: $0.59

NYMEX

205,036

Less: $0.59

381,525

340,036

340,036 |

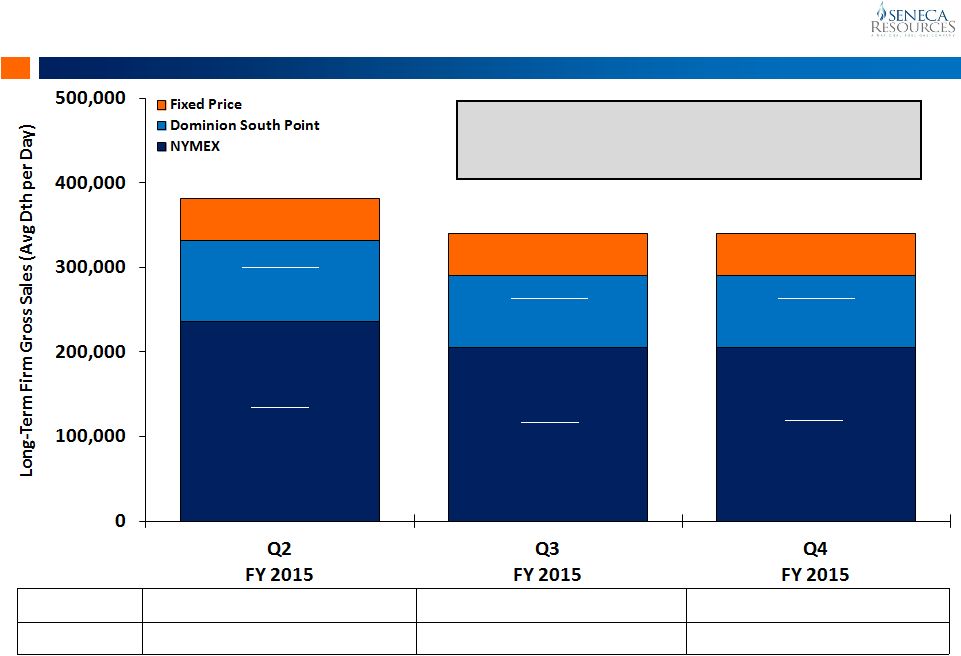

Upstream

Current Natural Gas Hedge Positions

27

(1) For the remaining nine months of fiscal 2015. |

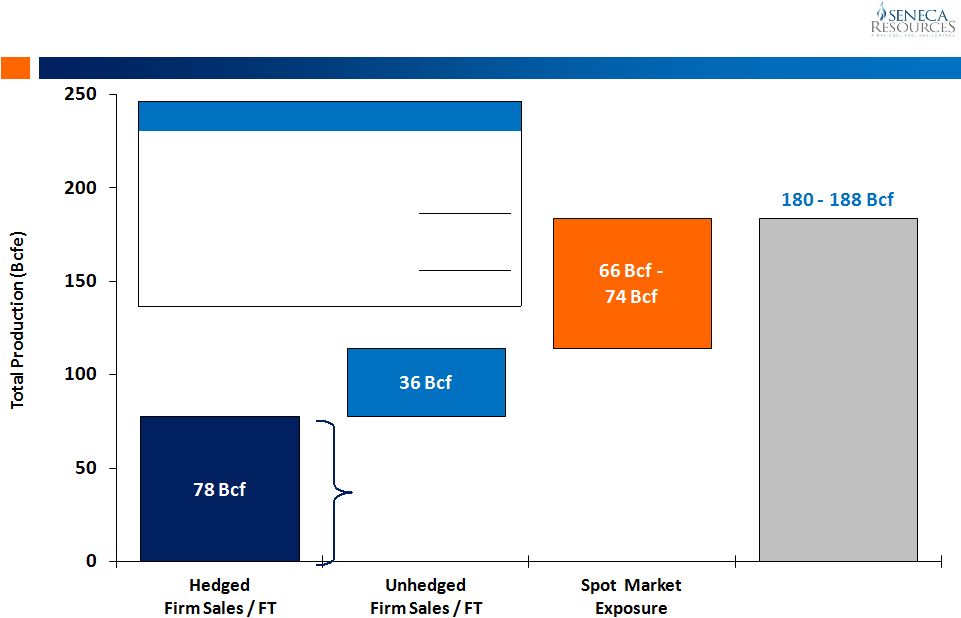

Upstream

FY 2015 Production –

Firm Sales & Spot Exposure

28

(1)

Spot price assumptions reflected in fiscal 2015 earnings guidance range.

(2)

Indicates firm sales not backed by financial hedges. Non-hedged DOM firm sales include 5.6

Bcf of non-operated production volumes. Firm Sales with Price Certainty

76.5 Bcf at ~$3.70/Mcf

Spot Price Exposure

27 Bcf at $2.00-$2.25/Mcf

(1)

2.7 Bcf

(2)

7.3 Bcf

(2) |

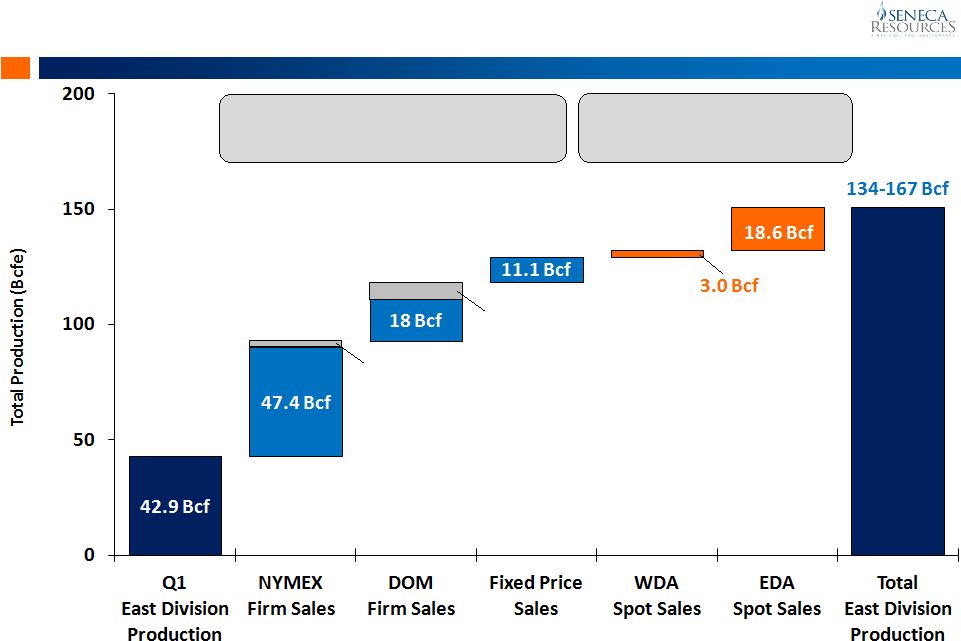

Upstream

FY

2016

Productive

Capacity

(1)

29

(1)

Productive capacity reflects firm sales commitments and assumes no price-related

curtailments on projected production exposed to local Appalachian spot pricing. Productive capacity is not

intended to reflect production guidance for fiscal 2016.

(2)

Unhedged firm sales includes non-operated production volumes.

FY 2016 Productive Capacity Summary

Hedged Firm Sales / FT

78 Bcf

Unhedged Firm Sales / FT

(2)

36 Bcf

Productive Capacity Exposed to Spot

66 -

74 Bcf

Total East Div. Productive Capacity

180 -

188 Bcf

West Division (California)

20 -

22 Bcfe

Total SRC Productive Capacity

200 -

210 Bcfe

Total

East Division

Productive Capacity

Price Certainty

at ~$3.75 /Mcf

(2) |

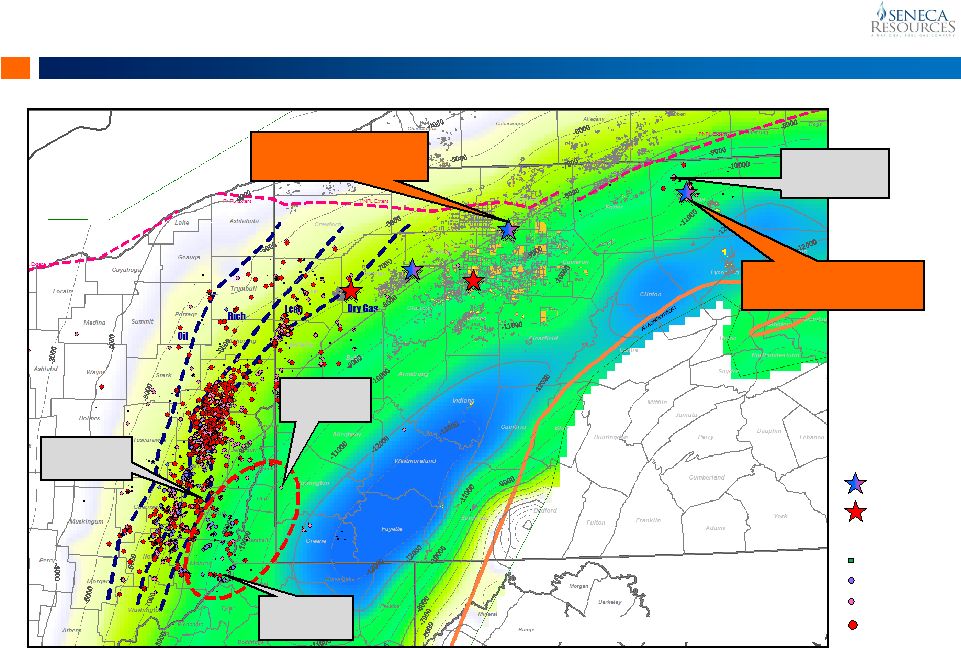

Upstream

Utica/Point Pleasant: Industry Activity

30

Range

59 Mmcf/d

Rice

42

Mmcf/d

Shell

26.5

Mmcf/d

PGE

PGE

Permitted

Permitted

Drilling

Drilling

Completed

Completed

Production

Production

Seneca Vert.

Seneca Vert.

Seneca Horiz.

Seneca Horiz.

MHR

46 Mmcf/d

Color-filled contours are Trenton TVDSS; CI = 1000’

Seneca -

DCNR 007

IP: 22.7 MMcfd

Seneca –

Mt. Jewett

IP: 8.9 MMcfd |

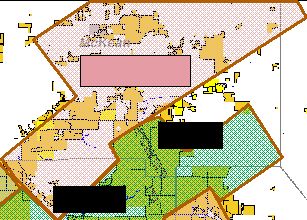

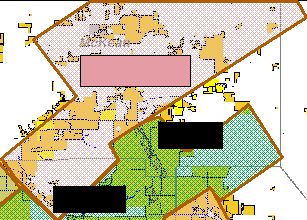

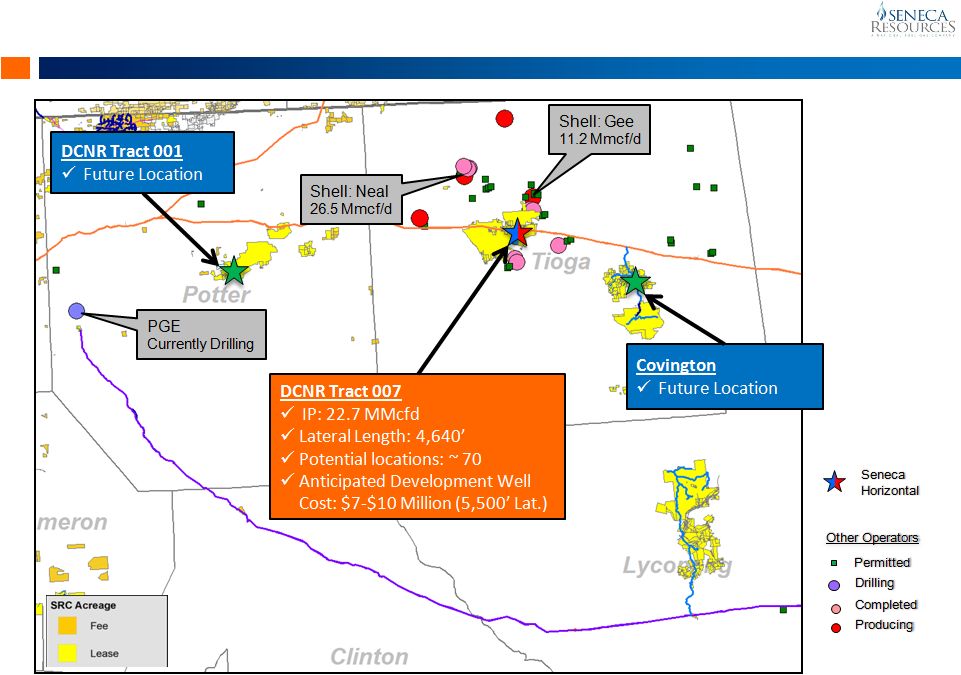

Upstream

Utica/Point

Pleasant Shale: EDA Opportunities

31 |

Upstream

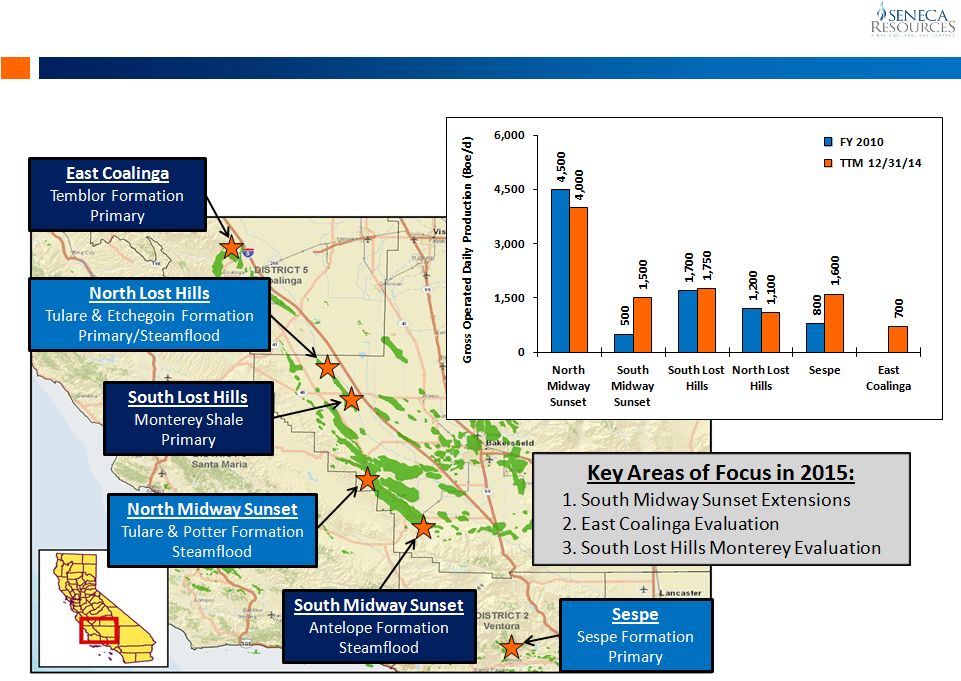

California: Stable Production; Modest Growth

32 |

Upstream

South Midway Sunset Development

33

252 Pool

97X Pool

SE Pool

251 Pool

B Pool

A Pool

Extended Pool Boundary

Original Pool Boundary

Existing Wells

1000’

16X Pool

Seneca Acquired

in June 2009

Highlights Since Acquisition

•

Significantly increased daily production

•

Drilled 114 new producers

•

Added 3.3 MMBO of proven reserves

•

Increased steam capacity by 420%

•

Identified opportunities for additional

pool development |

Upstream

California: East Coalinga Summary

34

•

Production has increased from 214 BOPD to

750 BOPD

•

Drilled 31 new producers and 1 water disposal

well in 2014

•

Plan to drill 5 wells in 2015

•

Evaluating potential of undeveloped Upper

Temblor heavy oil reservoir in Section 28

Seneca Acquired

in January 2013 |

Upstream

Focused on High Return Opportunities

35

CALIFORNIA

Field

Average

Well Cost

Average

EUR

(MBO)

Estimated

IRR

@$55/Bbl

Fiscal 2015

Locations

South Midway Sunset

$250,000

39

57%

36

North Midway Sunset

$300,000

30

25%

15

East Coalinga

$420,000

29

15%

5 |

Upstream

California: Modest Growth Anticipated in 2015

36 |

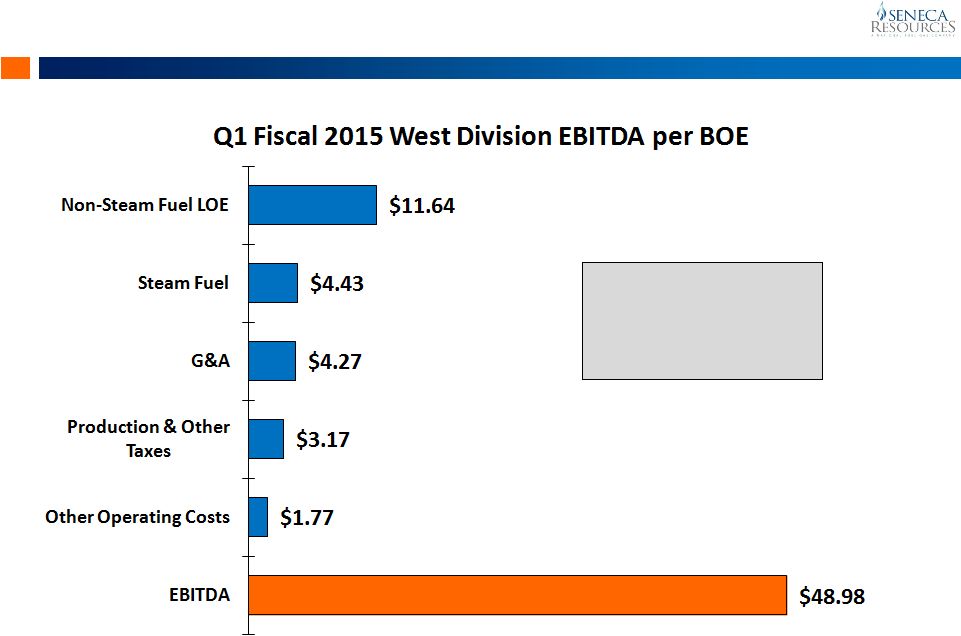

Upstream

Strong Margins Support Significant Free Cash Flow

37

Average Revenue

for Q1 FY2015

(1)

$74.26 per BOE

(1)

Includes impact of hedging. |

Midstream

Overview Pipeline & Storage

Gathering

38 |

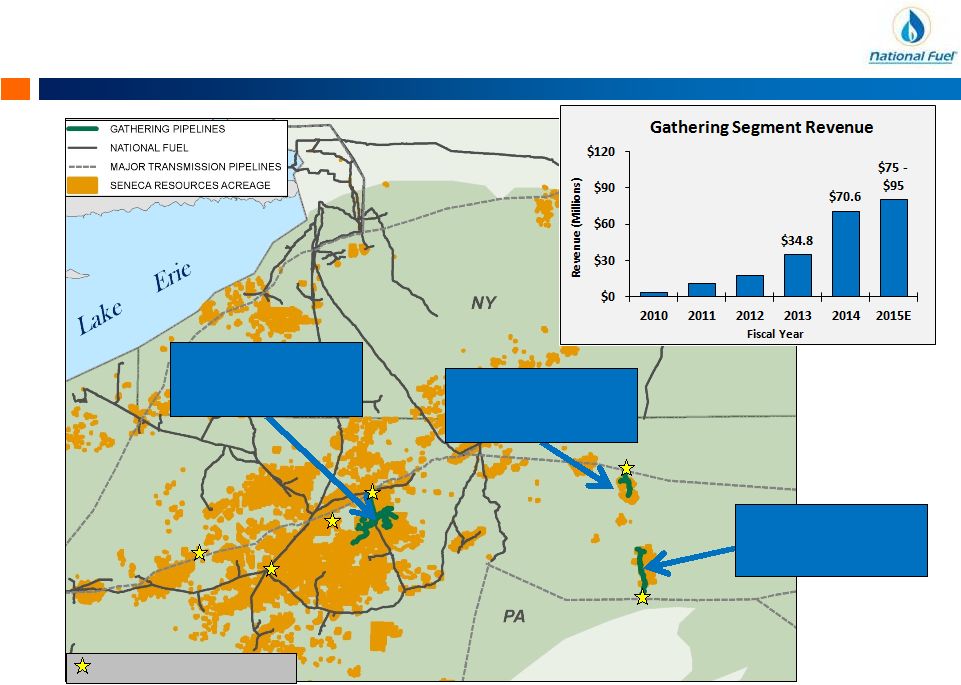

Midstream

Gathering is the First Step to Reaching a Market

39

(1)

Fiscal

2015

estimated

revenue

reflects

projected

throughput

based

on

the

range

of

Seneca’s

Fiscal

2015

production

guidance

(155-190

Bcfe).

TGP 300

Transco

TGP 200

Covington

Gathering System

(In-Service)

Gathering Interconnects

Clermont

Gathering System

(In-Service)

Trout Run

Gathering System

(In-Service)

(1) |

Midstream

Gathering Supporting Seneca’s EDA Production

40

(1) Fiscal 2015 estimated throughput reflects the midpoint of Seneca’s Fiscal

2015 production guidance range (155-190 Bcfe). •

In-Service Date: November 2009

•

Capacity: 220,000 Dth per day

•

Interconnect: TGP 300

•

Capital Expenditures (to date): $32 Million

Interconnects

(1)

•

In-Service Date: May 2012

•

Capacity: 466,000 to 585,000 Dth per day

•

Interconnect: Transco –

Leidy Lateral

•

Capital Expenditures (to date): $162 Million

Covington Gathering System

Trout Run Gathering System |

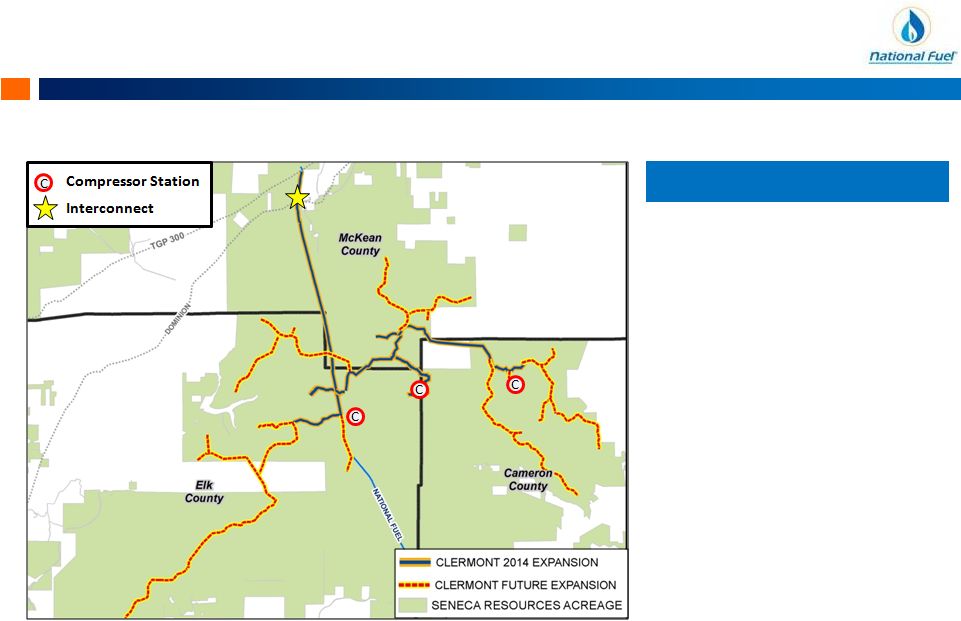

Midstream

•

In-Service: July 2014

•

Ultimate Trunkline Capacity:

1+ Bcf per day

•

Interconnects

o

TGP 300 (current)

o

NFG Supply Corporation

(Northern Access 2016)

•

Capital Expenditures:

o

To date: $115 Million

o

2015

(1)

: $95 -

$135 Million

Clermont Gathering System has Large Expandability

41

(1) For the remaining nine months of fiscal 2015.

Clermont Gathering System |

Midstream

Positioned to Serve Growing Production in Appalachia

42

NFG is focused on expanding our pipeline

systems to support the growing needs of

Appalachian producers and shippers |

Midstream

Major Expansion Designed for Canadian Deliveries

43

•

Customer: Seneca Resources

•

In-Service: November 2015

•

System: NFG Supply Corp.

•

Capacity: 140,000 Dth per day

o

Lease to TGP as part of their

Niagara Expansion project

•

Interconnect

o

Niagara (TransCanada)

•

Total Cost: $66 Million

•

Major Facilities

o

23,000 HP Compression

Northern Access 2015 |

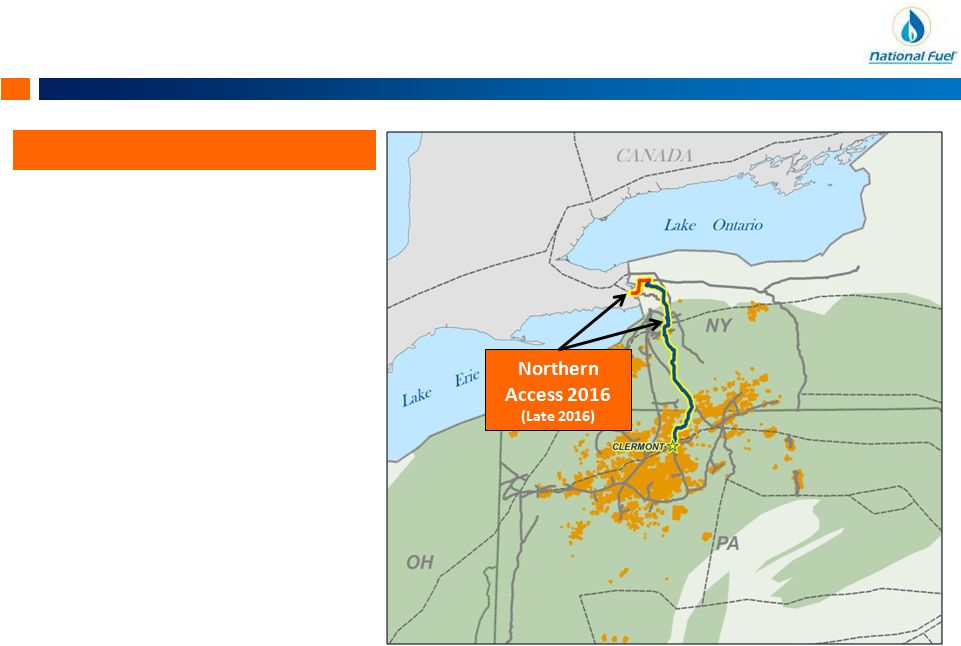

Midstream

Northern Access 2016 Provides Access to Canada

44

•

Customer: Seneca Resources

•

In-Service: November 2016 target

•

Capacity: 490,000 Dth/d

•

Interconnects:

o

TransCanada –

Chippawa

(350,000 Dth/d)

o

TGP 200 –

East Aurora

(140,000 Dth/d)

•

Total Cost: ~$451 Million

•

FERC Timing

o

Pre-filing: July 2014

o

Certificate filing: March 2015

Northern Access 2016 |

Midstream

Recent

3

rd

Party

Expansions

Highly

Successful

45

Completed Expansions

Capacity (Dth/day)

Northern Access 2012

320,000

Tioga County Ext. & Lamont

440,000

Line N & Mercer Expansion

458,000

Total New Capacity

1,218,000

Capital Cost ($Millions)

Northern Access 2012

$72

Tioga County Ext. & Lamont

$72

Line N & Mercer Expansion

$138

Total Capital Expenditures

$282

Northern

Access 2012

Tioga County

Extension

Line N Projects

Annual Revenues ($Millions)

Northern Access 2012

$16.1

Tioga County Ext. & Lamont

$33.4

Line N & Mercer Expansion

$23.1

Total Reservation Charges

$72.6 |

Midstream

Mercer

(TGP Station 219)

Pairing Line N Expansions with System Modernization

46

•

In-Service: November 2015

•

System: NFG Supply Corp.

•

Capacity: 175,000 Dth per day

o

Range Resources (145,000 Dth/d)

o

Seneca Resources (30,000 Dth/d)

•

Interconnect

o

Mercer (TGP Station 219)

o

Holbrook (TETCO)

•

Total Cost: $86 Million

o

Expansion: $45 Million

o

Modernization: $41 Million

•

Major Facilities

o

3,550 HP Compressor

o

23.3 miles –

24”

Replacement Pipe

Westside Expansion &

Modernization

Holbrook (TETCO)

Westside

Expansion &

Modernization |

Midstream

Developing Unique Solutions for Shippers

47

•

In-Service: November 2015

•

System: NFG Supply & Empire Pipeline

•

New No-Notice Services

o

Precedent agreements executed with

RG&E, NYSEG & NFG Utility

o

Preserving 172,500 Dth per day (RG&E)

o

Preserving 20,000 Dth per day (NYSEG)

o

Retained Storage: 3.3 Bcf

o

New incremental transportation

capacity of 49,000 Dth per day

•

Interconnect

o

Tuscarora (NFG/Supply)

•

Total Cost: $58.5 Million

•

Major Facilities

o

1,384 HP Compressor

o

17 miles –

12”/16”

Pipeline

Tuscarora Lateral

Tuscarora

Lateral |

Midstream

Recent Capacity

Additions

1,218,000 Dth/day

Significant Expansions Are Driving Growth

48

Completed Projects (Since 2009)

Total Expansion (2009-2016+)

Capacity

Additions

2,072,000 Dth/day

In-Service 2015

364,000 Dth/day

In-Service 2016+

490,000 Dth/day

Planned Projects (2015+)

Precedent Agreements Executed |

Downstream

Overview Utility

Energy Marketing

49 |

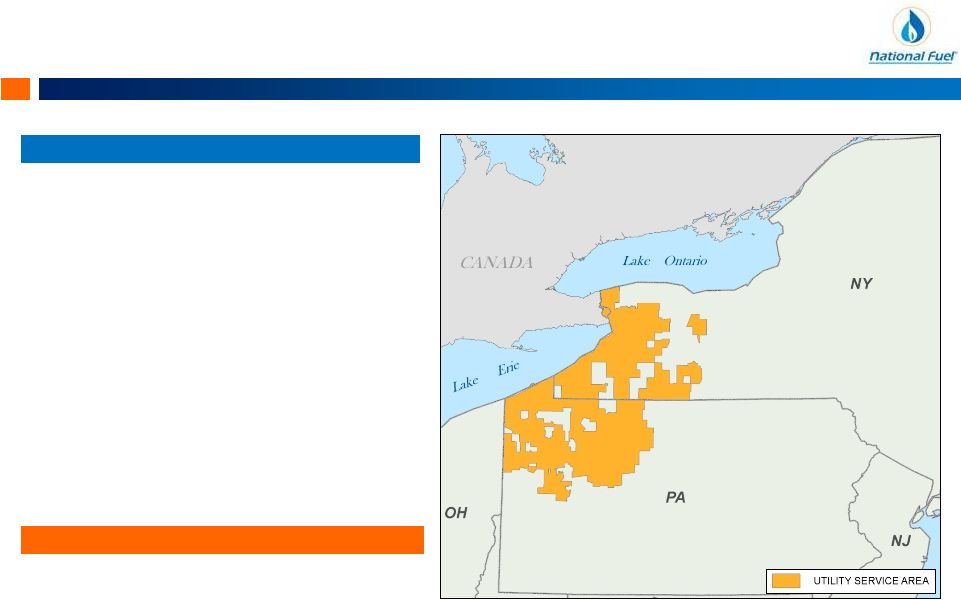

Downstream

New York & Pennsylvania Service Territories

50

Total

Customers:

524,300

Rate Mechanisms:

o

Revenue Decoupling

o

Weather Normalization

o

Low Income Rates

o

Merchant Function Charge (Uncollectibles Adj.)

o

90/10 Sharing (Large Customers)

NY PSC Rate Case Settlement, May 2014

o

Rates Unchanged

o

9.1% ROE Confirmed

o

2-Tier Earnings Sharing Mechanism

o

9.5% to 10.5% -

Share 50%

o

10.5% > -

Share 80%

o

$8.2 MM CapEx -

system replacement

o

$8.0 MM incremental O&M (post-retirement benefits)

Total

Customers:

213,500

Rate Mechanisms:

o

Low Income Rates

o

Merchant Function Charge

ROE:

Black

Box

Settlement

(2007)

New York

Pennsylvania |

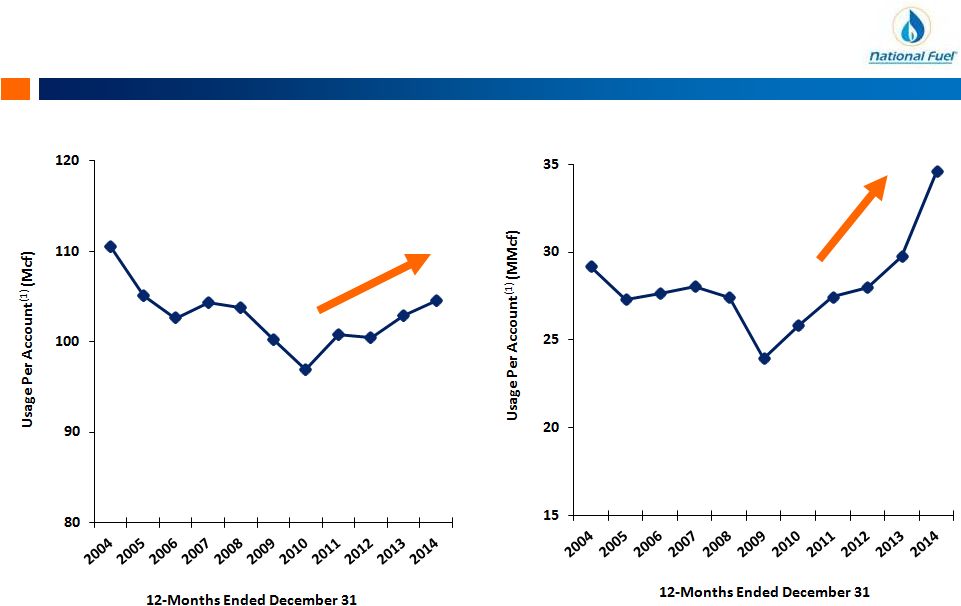

Downstream

Utility: Shifting Trends in Customer Usage

51

(1) Weighted Average of New York and Pennsylvania service territories (assumes normal

weather). Residential Usage

Industrial Usage |

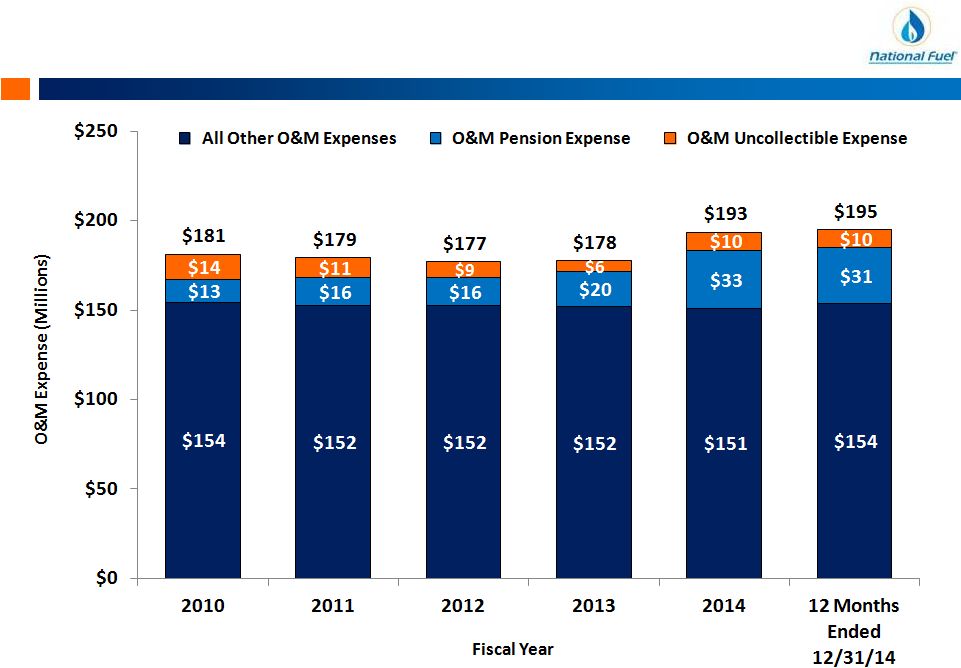

Downstream

A Proven History of Controlling Costs

52 |

Downstream

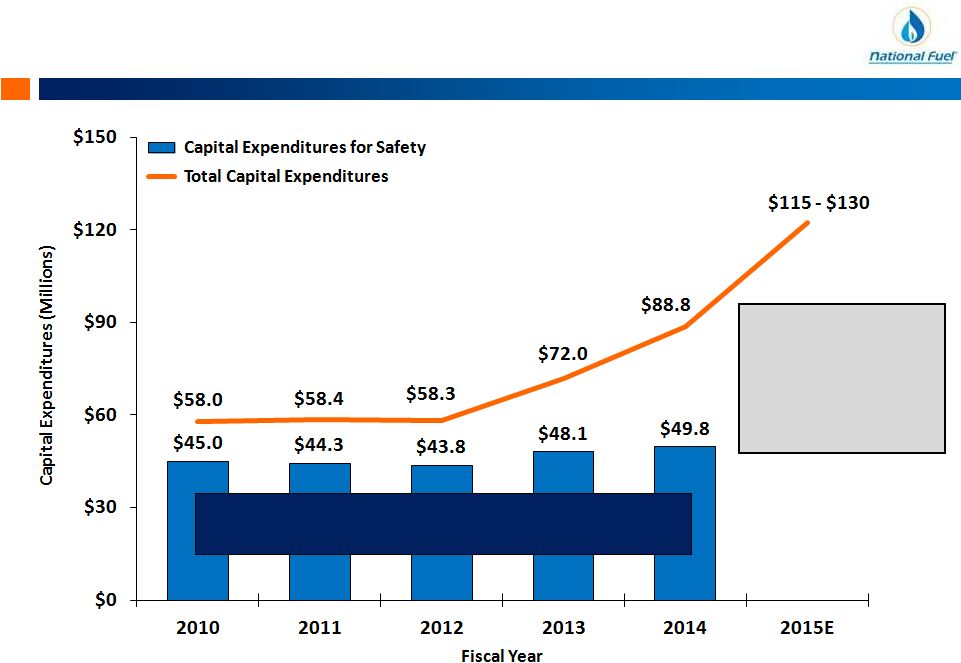

Utility: Strong Commitment to Safety

53

The Utility remains focused on maintaining the

ongoing safety and reliability of its system

Near-term increase due

to ~$60MM upgrade of

the Utility’s Customer

Information System and

~$25MM NRG Dunkirk

power plant project |

Appendix

54 |

Appendix

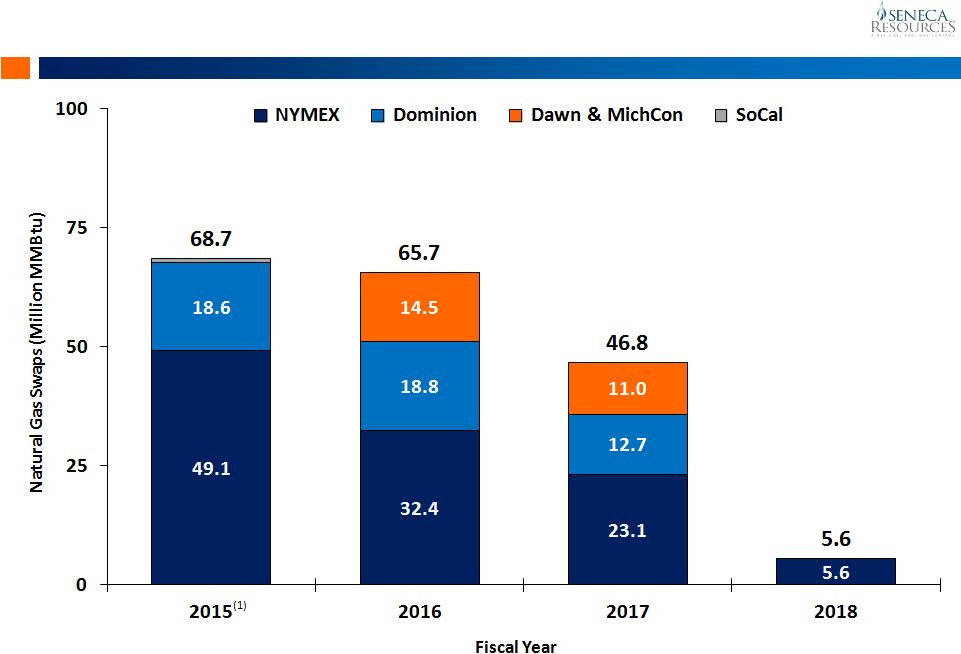

Natural Gas Hedge Positions

55

(1) For the remaining nine months of fiscal 2015.

(Volumes in thousands Mmbtu; Prices in $/Mmbtu)

Fiscal 2015

(1)

Fiscal 2016

Fiscal 2017

Fiscal 2018

Volume

Avg.

Price

Volume

Avg.

Price

Volume

Avg.

Price

Volume

Avg.

Price

NYMEX Swaps

49,130

$4.18

32,350

$4.24

23,130

$4.50

5,550

$4.59

Dominion

Swaps

18,630

$3.74

18,840

$3.78

12,720

$3.87

-

-

SoCal Swaps

900

$4.35

-

-

-

-

-

-

MichCon

Swaps

-

-

9,000

$4.10

3,000

$4.10

-

-

Dawn Swaps

-

-

5,490

$4.36

7,950

$4.14

-

-

Fixed Price

Physical Sales

13,650

$3.77

18,300

$3.77

18,250

$3.77

1,550

$3.77

Total

82,310

$4.01

83,980

$4.03

65,050

$4.11

7,100

$4.41 |

Appendix

Crude Oil Hedge Positions

56

(1) For the remaining nine months of fiscal 2015.

Fiscal 2015

(1)

Fiscal 2016

Fiscal 2017

Fiscal 2018

Volume

Avg.

Price

Volume

Avg.

Price

Volume

Avg.

Price

Volume

Avg.

Price

Midway

Sunset

(MWSS)

Swaps

108,000

$92.10

36,000

$92.10

-

-

-

-

Brent

Swaps

765,000

$98.32

933,000

$95.18

384,000

$92.30

75,000

$91.00

NYMEX

Swaps

297,000

$90.14

300,000

$86.09

-

-

-

-

Total

1,170,000

$95.67

1,269,000

$92.95

384,000

$92.30

75,000

$91.00

(Volumes & Prices in Bbl) |

Appendix

WDA Delineation Well Results

57

Area

Producing

Well Count

Peak 24-Hour

Rate (MMcfd)

Average

7-Day (MMcf/d)

Average Treatable

Lateral Length (ft)

Ridgway

Elk County

1

7.1

6.4

5,537’

Church Run

Elk & Jefferson

counties

2

4.8

4.5

4,690’

Hemlock

Elk County

2

5.4

5.2

7,067’

Owl’s Nest

Elk & Forest counties

1

6.1

5.8

6,137’

Sulger Farms

Jefferson County

1

6.1

5.6

5,778’ |

Appendix

Comparable GAAP Financial Measure Slides & Reconciliations

58

This

presentation

contains

certain

non-GAAP

financial

measures.

For

pages

that

contain

non-GAAP

financial

measures,

pages

containing

the

most

directly

comparable

GAAP

financial

measures

and

reconciliations

are

provided

in

the

slides

that

follow.

The

Company

believes

that

its

non-GAAP

financial

measures

are

useful

to

investors

because

they

provide

an

alternative

method

for

assessing

the

Company’s

ongoing

operating

results,

for

measuring

the

Company’s

cash

flow

and

liquidity,

and

for

comparing

the

Company’s

financial

performance

to

other

companies.

The

Company’s

management

uses

these

non-GAAP

financial

measures

for

the

same

purpose,

and

for

planning

and

forecasting

purposes.

The

presentation

of

non-GAAP

financial

measures

is

not

meant

to

be

a

substitute

for

financial

measures

prepared

in

accordance

with

GAAP.

The

Company

defines

Adjusted

EBITDA

as

reported

GAAP

earnings

before

the

following

items:

interest

expense,

depreciation,

depletion

and

amortization,

interest

and

other

income,

impairments,

items

impacting

comparability

and

income

taxes. |

Appendix

National Fuel Gas Company

59

Reconciliation of Adjusted EBITDA to Consolidated Net Income

($ Thousands)

FY 2010

FY 2011

FY 2012

Exploration & Production - West Division Adjusted EBITDA

187,838

$

187,603

$

226,897

$

215,042

$

217,150

$

206,875

$

Exploration & Production - All Other Divisions Adjusted EBITDA

139,624

189,854

170,232

277,341

322,322

332,332

Total Exploration & Production Adjusted EBITDA

327,462

$

377,457

$

397,129

$

492,383

$

539,472

$

539,207

$

Total Adjusted EBITDA

Exploration & Production Adjusted EBITDA

327,462

$

377,457

$

397,129

$

492,383

$

539,472

$

539,207

$

Pipeline & Storage Adjusted EBITDA

120,858

111,474

136,914

161,226

186,022

186,799

Gathering Adjusted EBITDA

2,021

9,386

14,814

29,777

64,060

73,437

Utility Adjusted EBITDA

167,328

168,540

159,986

171,669

164,643

162,779

Energy Marketing Adjusted EBITDA

13,573

13,178

5,945

6,963

10,335

12,359

Corporate & All Other Adjusted EBITDA

408

(12,346)

(10,674)

(9,920)

(11,078)

(11,515)

Total Adjusted EBITDA

631,650

$

667,689

$

704,114

$

852,098

$

953,454

$

963,066

$

Total Adjusted EBITDA

631,650

$

667,689

$

704,114

$

852,098

$

953,454

$

963,066

$

Minus: Net Interest Expense

(90,217)

(75,205)

(82,551)

(89,776)

(90,107)

(88,818)

Plus: Other Income

6,126

5,947

5,133

4,697

9,461

10,416

Minus: Income Tax Expense

(137,227)

(164,381)

(150,554)

(172,758)

(189,614)

(189,349)

Minus: Depreciation, Depletion & Amortization

(191,199)

(226,527)

(271,530)

(326,760)

(383,781)

(393,414)

Plus/Minus: Income/(Loss) from Discontinued Operations, Net of Tax (Corp. & All Other)

6,780

-

-

-

-

-

Plus: Gain on Sale of Unconsolidated Subsidiaries (Corp. & All

Other) -

50,879

-

-

-

-

Plus: Elimination of Other Post-Retirement Regulatory Liability

(P&S) -

-

21,672

-

-

-

Minus: Pennsylvania Impact Fee Related to Prior Fiscal Years (E&P)

-

-

(6,206)

-

-

-

Minus: New York Regulatory Adjustment (Utility)

-

-

-

(7,500)

-

-

Rounding

-

-

(1)

-

-

-

Consolidated Net Income

225,913

$

258,402

$

220,077

$

260,001

$

299,413

$

301,901

$

Consolidated Debt to Total Adjusted EBITDA

Long-Term Debt, Net of Current Portion (End of Period)

1,049,000

$

899,000

$

1,149,000

$

1,649,000

$

1,649,000

$

1,649,000

$

Current Portion of Long-Term Debt (End of Period)

200,000

150,000

250,000

-

-

-

Notes Payable to Banks and Commercial Paper (End of Period)

-

40,000

171,000

-

85,600

172,900

Total Debt (End of Period)

1,249,000

$

1,089,000

$

1,570,000

$

1,649,000

$

1,734,600

$

1,821,900

$

Long-Term Debt, Net of Current Portion (Start of Period)

1,249,000

1,049,000

899,000

1,149,000

1,649,000

1,649,000

Current Portion of Long-Term Debt (Start of Period)

-

200,000

150,000

250,000

-

-

Notes Payable to Banks and Commercial Paper (Start of Period)

-

-

40,000

171,000

-

-

Total Debt (Start of Period)

1,249,000

$

1,249,000

$

1,089,000

$

1,570,000

$

1,649,000

$

1,649,000

$

Average Total Debt

1,249,000

$

1,169,000

$

1,329,500

$

1,609,500

$

1,691,800

$

1,735,450

$

Average Total Debt to Total Adjusted EBITDA

1.98 x

1.75 x

1.89 x

1.89 x

1.77 x

1.80 x

FY 2013

12-Months

Ended 12/31/14

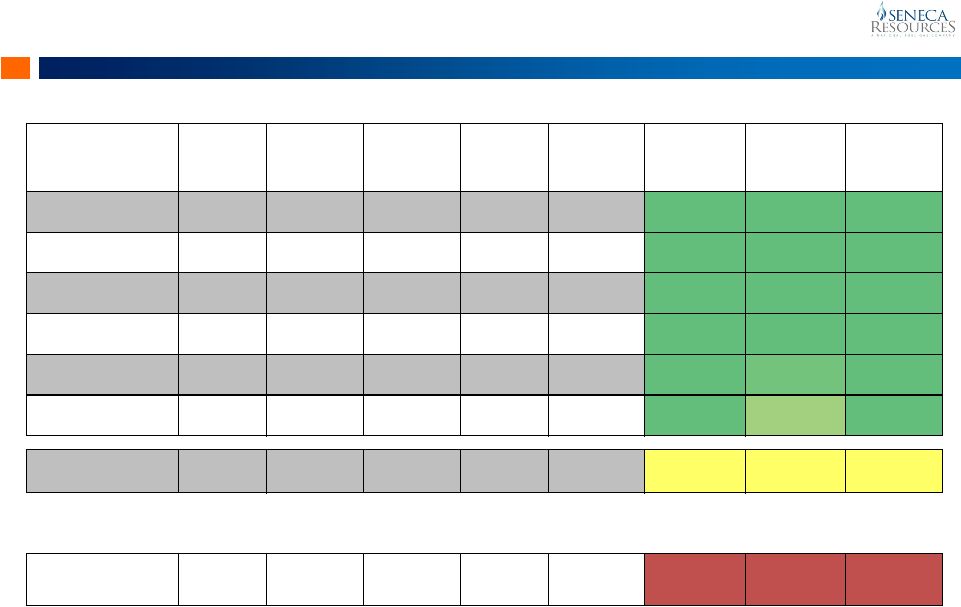

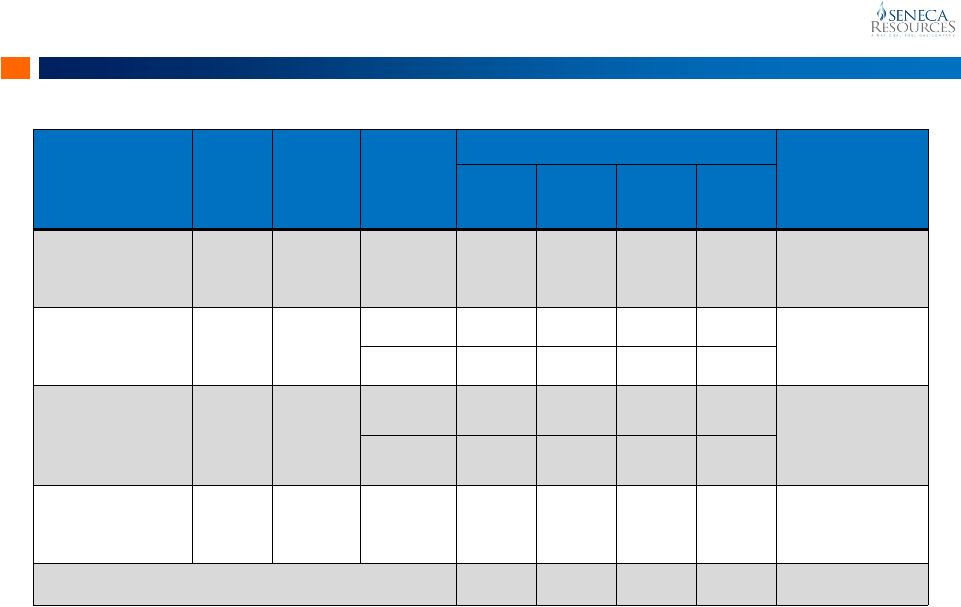

FY 2014 |

Appendix

National Fuel Gas Company

Reconciliation of Segment Capital Expenditures to

Consolidated Capital Expenditures

($ Thousands)

FY 2015

FY 2010

FY 2011

FY 2012

FY 2013

FY 2014

Forecast

Capital Expenditures from Continuing Operations

Exploration & Production Capital Expenditures

398,174

$

648,815

$

693,810

$

533,129

$

602,705

$

$525,000-575,000

Pipeline & Storage Capital Expenditures

37,894

129,206

144,167

56,144

$

139,821

$

$225,000-275,000

Gathering Segment Capital Expenditures

6,538

17,021

80,012

54,792

$

137,799

$

$125,000-175,000

Utility Capital Expenditures

57,973

58,398

58,284

71,970

$

88,810

$

$115,000-130,000

Energy Marketing, Corporate & All Other Capital Expenditures

773

746

1,121

1,062

$

772

$

-

Total

Capital Expenditures from Continuing Operations 501,352

$

854,186

$

977,394

$

717,097

$

969,907

$

$990,000-1,155,000

Capital Expenditures from Discountinued Operations

All Other Capital Expenditures

150

$

-

$

-

$

-

$

-

$

-

$

Plus (Minus)

Accrued Capital Expenditures Exploration & Production FY 2014 Accrued Capital

Expenditures -

$

-

$

-

$

-

$

(80,108)

$

Exploration & Production FY 2013 Accrued Capital Expenditures

-

-

-

(58,478)

58,478

-

Exploration & Production FY 2012 Accrued Capital Expenditures

-

-

(38,861)

38,861

-

-

Exploration & Production FY 2011 Accrued Capital Expenditures

-

(103,287)

103,287

-

-

-

Exploration & Production FY 2010 Accrued Capital Expenditures

(78,633)

78,633

-

-

-

-

Exploration & Production FY 2009 Accrued Capital Expenditures

19,517

-

-

-

-

-

Pipeline & Storage FY 2014 Accrued Capital Expenditures

-

-

-

-

(28,122)

Pipeline & Storage FY 2013 Accrued Capital Expenditures

-

-

-

(5,633)

5,633

-

Pipeline & Storage FY 2012 Accrued Capital Expenditures

-

-

(12,699)

12,699

-

-

Pipeline & Storage FY 2011 Accrued Capital Expenditures

-

(16,431)

16,431

-

-

-

Pipeline & Storage FY 2010 Accrued Capital Expenditures

-

3,681

-

-

-

-

Pipeline & Storage FY 2008 Accrued Capital Expenditures

-

-

-

-

-

-

Gathering FY 2014 Accrued Capital Expenditures

-

-

-

-

(20,084)

Gathering FY 2013 Accrued Capital Expenditures

-

-

-

(6,700)

6,700

-

Gathering FY 2012 Accrued Capital Expenditures

-

-

(12,690)

12,690

-

-

Gathering FY 2011 Accrued Capital Expenditures

-

(3,079)

3,079

-

-

-

Gathering FY 2009 Accrued Capital Expenditures

715

-

-

-

-

-

Utility FY 2014 Accrued Capital Expenditures

-

-

-

-

(8,315)

Utility FY 2013 Accrued Capital Expenditures

-

-

-

(10,328)

10,328

-

Utility FY 2012 Accrued Capital Expenditures

-

-

(3,253)

3,253

-

-

Utility FY 2011 Accrued Capital Expenditures

-

(2,319)

2,319

-

-

-

Utility FY 2010 Accrued Capital Expenditures

-

2,894

-

-

-

-

Total

Accrued Capital Expenditures (58,401)

$

(39,908)

$

57,613

$

(13,636)

$

(55,490)

$

-

$

Eliminations

-

$

-

$

-

$

-

$

-

$

-

$

Total

Capital Expenditures per Statement of Cash Flows 443,101

$

814,278

$

1,035,007

$

703,461

$

914,417

$

$990,000-1,155,000

60 |