Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Greenbacker Renewable Energy Co LLC | Financial_Report.xls |

| EX-3.2 - EXHIBIT 3.2 - Greenbacker Renewable Energy Co LLC | s100851_ex3-2.htm |

| EX-31.1 - EXHIBIT 31.1 - Greenbacker Renewable Energy Co LLC | s100851_ex31-1.htm |

| EX-32.2 - EXHIBIT 32.2 - Greenbacker Renewable Energy Co LLC | s100851_ex32-2.htm |

| EX-31.2 - EXHIBIT 31.2 - Greenbacker Renewable Energy Co LLC | s100851_ex31-2.htm |

| EX-32.1 - EXHIBIT 32.1 - Greenbacker Renewable Energy Co LLC | s100851_ex32-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 333-178786-01

GREENBACKER RENEWABLE ENERGY COMPANY LLC

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 80-0872648 | |

| (State or Other Jurisdiction of | (I.R.S. Employer | |

| Incorporation or Organization) | Identification No.) |

369 Lexington Avenue, Suite 312

New York, NY 10017

Tel (646) 237-7884

(Address, including zip code and telephone number, including area code, of registrants Principal Executive Office)

Charles Wheeler

c/o Greenbacker Capital Management LLC

369 Lexington Avenue, Suite 312

New York, NY 10017

Tel (646) 237-7884

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act of 1933. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of March 4, 2015, the registrant had 1,613,502 shares of common stock, $0.001 par value, outstanding.

TABLE OF CONTENTS

In this annual report on Form 10-K, except as otherwise indicated, the terms:

| • | The term "LLC" refers to Greenbacker Renewable Energy Company LLC; |

| • | “we,” “us,” “our” and the “company” refers, collectively, to Greenbacker Renewable Energy Company LLC and Greenbacker Renewable Energy Corporation; |

| • | The “advisor” and “GCM” refer to Greenbacker Capital Management LLC, our advisor; |

| • | The term “Special Unitholder” refers to GREC Advisors, LLC, a Delaware limited liability company, which is a subsidiary of our advisor; |

| • | The term “special unit” refers to the special unit of limited liability company interest in the LLC entitling the Special Unitholder to an incentive allocation and distribution; |

| • | The term “SC Distributors” and “dealer manager” refer to SC Distributors, LLC, a Delaware limited liability company, the LLC’s dealer manager; |

| • | “GREC” refers to Greenbacker Renewable Energy Corporation, a Maryland corporation; |

| • | “Greenbacker Administration” and “Administrator” refers to Greenbacker Administration, LLC, our Administrator; and |

| • | “Greenbacker Group LLC” refers to a sponsor of the company and the parent of GCM. |

FORMATION OF OUR COMPANY

Greenbacker Renewable Energy Company LLC, a Delaware limited liability company is an externally managed energy company that intends to acquire and manage income-generating renewable energy and energy efficiency projects, and other energy-related businesses, as well as finance the construction and/or operation of these and sustainable development projects and businesses. The LLC plans to conduct substantially all of its operations through its wholly-owned subsidiary, Greenbacker Renewable Energy Corporation (“GREC”). GREC is a Maryland corporation formed in November 2011 and the LLC currently holds all of the outstanding shares of capital stock of GREC. The LLC and GREC (collectively “we”, “us”, “ours”, and the “company”) will be externally managed and advised by Greenbacker Capital Management LLC (the “advisor” or “GCM”), a renewable energy, energy efficiency and sustainability related project acquisition, consulting and development company. The LLC’s fiscal year end is December 31.

The company is offering up to $1,500,000,000 in shares of limited liability company interests, or the shares, including up to $250,000,000 pursuant to the distribution reinvestment plan, on a “best efforts” basis through SC Distributors, LLC, the dealer manager, meaning it is not required to sell any specific number or dollar amount of shares. The dealer manager coordinates the distribution of our shares, manages our relationships with participating broker-dealers and provides assistance in connection with compliance matters relating to the marketing of our offering. The dealer manager provides only the foregoing distribution-related services to us, and does so pursuant to the dealer manager agreement in place. The dealer manager exercises no control or influence over our investment, asset management or accounting functions or any other aspect of our management or operations. For the avoidance of doubt, the dealer manager owns no equity interests in our advisor.

The company is publicly offering three classes of shares: Class A shares, Class C shares and Class I shares in any combination with a dollar value up to the maximum offering amount. The share classes have different selling commissions, dealer manager fees and there is an ongoing distribution fee with respect to Class C shares. The company has adopted a distribution reinvestment plan pursuant to which a shareholder may elect to have the full amount of cash distributions reinvested in additional shares. The company reserves the right to reallocate the shares offered between Class A, Class C and Class I shares and between this offering and the distribution reinvestment plan.

| 1 |

On March 28, 2014, the company met the initial offering requirement of $2,000,000, and on April 25, 2014 held the initial closing. As of December 31, 2014, the company is selling shares on a continuous basis at a price of $10.00 per Class A share, $9.576 per Class C share and $9.186 per Class I share. Management considers the breaking of escrow to be the beginning of the company’s operations. Accordingly, the Statements of Operations and Cash Flows are presented for the period April 25, 2014 (commencement of operations) through December 31, 2014. Commencing on June 30, 2014 and each quarter thereafter, our advisor, utilizing the services of an independent valuation firm when necessary, reviews and approves the net asset value for each class of shares, subject to the oversight of the board of directors. The company expects such determination will ordinarily be made within 30 days after each such completed fiscal quarter. To the extent that the net asset value per share on the most recent valuation date increases above or decreases below the net proceeds per share, the company will adjust the offering prices of all classes of shares. The adjustments to the per share offering prices, which will become effective five business days after such determination is published, will ensure that after the effective date of the new offering prices, the offering prices per share, after deduction of selling commissions, dealer manager fees and organization and offering expenses, are not above or below net asset value per share as of the most recent valuation date. The purchase price per share to be paid by each investor will be equal to the price that is in effect on the date such investor submits his or her completed subscription agreement to the dealer manager. The shares are offered in the primary offering at a price based on the most recent valuation, plus related selling commissions, dealer manager fees and organization and offering expenses. Five days after the completion of each quarter end valuation, shares will be offered pursuant to the distribution reinvestment plan at a price equal to the current offering price per each class of shares, less the sales selling commissions and dealer manager fees associated with that class of shares in the primary offering.

OVERVIEW OF OUR BUSINESS

Our business objective is to generate attractive risk-adjusted returns for our members, consisting of both current income and long-term capital appreciation, by acquiring, and financing the construction and/or operation of income-generating renewable energy, energy efficiency and sustainable development projects, primarily within but also outside of North America. We expect the size of our investments to generally range between approximately $1 million and $100 million. We will seek to maximize our risk-adjusted returns by: (1) capitalizing on market opportunities; (2) focusing on hard assets that produce dependable cash flows; (3) efficiently utilizing government incentives where available; (4) employing creative deal structuring to optimize capital, and ownership structures; (5) partnering with experienced financial, legal, engineering and other professional firms; (6) employing sound due diligence and risk mitigation processes; and (7) monitoring and managing our portfolio of assets on an ongoing basis.

Our goal is to assemble a diversified portfolio of renewable energy, energy efficiency and other sustainability related projects and businesses. Renewable energy projects generally earn revenue through the sale of generated electricity as well as frequently through the sale of other commodities such as renewable energy certificates (“RECs”) and energy efficiency certificates (“EECs”), which are generated by the projects and the sale of by-products such as organic compost materials. We expect initially to focus on solar energy and wind energy projects as well as energy efficiency projects. We believe solar energy projects generally offer more predictable power generation characteristics, due to the relative predictability of sunlight over the course of time compared to other renewable energy classes and therefore we expect they will provide more stable income streams. However, technological advances in wind turbines and other energy generation technologies, as well as government incentives make wind energy and other types of projects attractive as well. Solar energy projects provide maximum energy production during the middle of the day and in the summer months when days are longer and nights shorter. Generally, the demand for power in the United States tends to be higher at those times due to the use of air conditioning and as a result energy prices tend to be higher. Solar energy projects tend to have minimal environmental impact enabling such projects to be developed close to areas of dense population where electricity demand is highest. Solar technology is scalable and well-established and it will be a relatively simple process to integrate new acquisitions and projects into our portfolio. Over time, we expect to broaden our strategy to include other types of renewable energy projects and energy efficiency projects and businesses, which may include wind farms, hydropower assets, geothermal plants, biomass and biofuel assets, combined heat and power technology assets, fuel cell assets and other energy efficiency assets, among others, and to the extent we deem the opportunity attractive, other energy and sustainability related assets and businesses.

| 2 |

Our preferred investment strategy is to acquire controlling equity stakes in our target assets and to oversee and supervise their operations. We define controlling equity stakes as companies in which we own 25% or more of the voting securities of such company or have greater than 50% representation on such company’s board. However, we will also provide financing to projects owned by others, including through the provision of secured loans which may or may not include some form of equity participation. We may also provide projects with senior unsecured debt, subordinated secured debt, subordinated unsecured debt, mezzanine debt, convertible debt, convertible preferred equity, and preferred equity, and make minority equity investments. We may also participate in projects by acquiring contractual payment rights or rights to receive a proportional interest in the operating cash flow or net income of a project. We may also make equity investments in or loans to parties financing the supply of renewable energy and energy efficiency to residential and commercial customers or the adoption of strategies to reduce the consumption of energy by those customers. Our strategy will be tailored to balance long-term cash flow certainty, which we can achieve through long-term agreements for our products, with shorter term arrangements that allow us to potentially generate higher risk-adjusted returns.

Our renewable energy projects will generate revenue primarily by selling (1) generated electric power to local utilities and other high quality, utility, municipal and corporate counterparties, and (2) in some cases, RECs, EECs, and other commodities associated with the generation or savings of power. We will therefore seek to acquire or finance projects that contain transmission infrastructures and access to power grids or networks that will enable the generated power to be sold. We generally expect our projects will have power purchase agreements with one or more counterparties, including local utilities or other high credit quality counterparties, who agree to purchase the electricity generated from the project. We refer to these power purchase agreements as “must-take contracts,” and we refer to these other counterparties as “off-takers.” These must-take contracts guarantee that all electricity generated by each project will be purchased. Although we intend to work primarily with high credit quality counterparties, in the event that an off-taker cannot fulfill its contractual obligation to purchase the power, we generally can sell the power to the local utility or other suitable counterparty, which would potentially ensure revenue is generated for all solar electricity generation. We will also generate revenue from the receipt of interest, fees, capital gains and distributions from investments in our target assets.

These power purchase agreements, when structured with utilities and other large commercial users of electricity, are generally long-term in nature with all electricity generated by the project purchased at a rate established pursuant to a formula set by contract. The formula is often dependent upon the type of subsidies, if any, offered by the local and state governments for project development. Although we expect to focus on projects with long-term contracts that ensure price certainty, we will also look for projects with shorter term arrangements that will allow us, through these projects, to participate in market rate changes which we expect may lead to higher current income.

We expect certain of the power purchase agreements for our projects will be structured as “behind the meter” agreements with residential, commercial or government entities, which provide that all electricity generated by a project will be purchased by the off taker at an agreed upon rate that may be set at a slight discount to the retail electric rate for the off-taker. These agreements also typically provide for annual rate increases over the term of the agreement although that is not a necessary requirement. The behind the meter agreement is generally long-term in nature and further typically provides that, should the off taker fail to fulfill its contractual obligation, any electricity that is not purchased by the off-taker may be sold to the local utility, usually at the wholesale spot electric rate.

We may also acquire residential solar assets and subsequently lease them to a residential owner on a long term basis. In these arrangements with residential owners, the residential owner directly receives the benefit of the electricity generated by the solar asset. We may also structure our investments in residential solar with a similar commercial arrangement to that of the power purchase agreements with utilities and other large commercial users of electricity for our energy projects, as described above.

We may also finance energy efficiency projects, which seek to enable residential customers, businesses and governmental organizations to consume less energy while at the same time providing the same or greater level of amenity. Financing for energy efficiency projects is generally used to pay for energy efficiency retrofits of buildings, homes, businesses, and replacement of other inefficient energy consuming assets with more modern technologies. These projects can be structured to provide predictable long-term cash flows by receiving a portion of the energy savings and the sale of associated RECs and EECs generated by such installations. In each of our renewable energy and energy efficiency investments, we also intend, where appropriate, to maximize the benefits of renewable portfolio standards (“RPS”) as well as other U. S. federal, state and local government support and incentives for the renewable energy industry.

| 3 |

The LLC will conduct a significant portion of its operations through GREC, of which it is the sole shareholder, holding both shares of common stock and the special preferred stock. We intend to operate our business in a manner that will permit us to maintain our exemption from registration under the Investment Company Act of 1940, as amended (the “Investment Company Act”).

Pursuant to the offering, which commenced on August 5, 2013, we are offering on a continuous basis up to $1,500,000,000 in shares of our limited liability company interests, consisting of up to $1,250,000,000 of shares in the primary offering and up to $250,000,000 of shares pursuant to the distribution reinvestment plan. SC Distributors, LLC is the dealer manager for the offering. The company’s offering period, which is currently scheduled to terminate two years after the initial offering date, or August 8, 2015, is expected to be extended as allowed under current securities law. After the finalization of the December 31, 2014 net asset value, the current offering price of the Class A shares is $10.000 per share, the current offering price of the Class C shares is $9.576 per share and the current offering price of the Class I shares is $9.186 per share.

On March 28, 2014, we satisfied the minimum offering requirement of $2,000,000 and commenced operations as of April 25, 2014. As of December 31, 2014, our advisor had purchased 20,100 Class A shares for aggregate gross proceeds of $201,000 and an affiliate of our advisor had purchased 170,000 shares for aggregate gross proceeds of $1,700,000. Through participation in the distribution reinvestment program, the advisor and affiliate as of December 31, 2014 owned 20,550 and 173,809 shares, respectively. As of December 31, 2014, we had received subscriptions for and issued 1,236,345 of our shares (including shares issued under the distribution reinvestment plan) for gross proceeds of $12,438,700 (before dealer-manager fees of $694,159 and selling commissions of $208,215 for net proceeds of $11,536,326).

OUR ADVISOR

GCM, a private firm that intends to register as an investment adviser under the Investment Advisers Act of 1940, as amended (the “Advisers Act”), no later than it is required to do so pursuant to the Advisers Act, serves as our advisor. Under the direction of our board of directors, GCM manages our day-to-day operations and provides advisory and management services to us.

Led by its Chief Executive Officer, David Sher, who has six years of experience in the energy infrastructure and project finance sector and 24 years of experience in the financial services sector, its President and Chief Investment Officer, Charles Wheeler (Mr. Wheeler also serves as our President and board of directors’ member, as well as President, CEO and as a director of GREC), who has 24 years of experience in the energy infrastructure and project finance sector and 26 years of experience in the financial services sector, its Chief Financial Officer, Richard Butt, who has six years of experience in the energy infrastructure and project finance sector and over 30 years of experience in the financial services sector and Managing Director Robert Sher, who has five years of experience in the energy infrastructure and project finance sector (Robert Sher is the brother of David Sher), GCM’s management team has in excess of 50 years of experience in the energy, infrastructure, and project finance sectors and over 75 years of experience in the financial services sector. Over this time, they have developed significant commercial relationships across multiple industries that we believe will benefit us as we implement our business plan. GCM maintains comprehensive renewable energy, project finance, and capital markets databases and has developed proprietary analytical tools and due diligence processes that will enable GCM to identify prospective projects and to structure transactions quickly and effectively on our behalf. Neither GCM, Greenbacker Group LLC nor our senior management team have previously sponsored any other programs, either public or non-public, or any other programs with similar investment objectives as us.

| 4 |

We seek to capitalize on the significant investing experience of our advisor’s management team, including the 24 years of investment banking and renewable energy expertise of Charles Wheeler, our Chief Executive Officer and President, and the Chief Investment Officer and a Senior Managing Director of GCM. Mr. Wheeler has held various senior positions with Macquarie Group, including Head of Financial Products for North America and Head of Renewables for North America. While serving as Head of Renewables for North America, Mr. Wheeler’s experience included evaluating wind project developers, solar asset acquisitions, assisting in the development of wind and solar greenfield projects, and assisting in the preparation of investment analyses for a biomass facility. Before moving to the United States to serve as Head of Financial Products for Macquarie Group in North America, Mr. Wheeler was a Director of the Financial Products Group in Australia with responsibility for the development, distribution and ongoing management of a wide variety of retail financial products, including Real Estate Investment Trusts (“REITs”), infrastructure bonds, international investment trusts and diversified domestic investment trusts. Mr. Wheeler brings his extensive background in renewable energy and project and structured finance to help us effectively execute our strategy.

GCM’s CEO, David Sher has extensive experience in the financial services and capital markets industries as well as significant successful entrepreneurial experience. Mr. Sher was previously a senior adviser at Prospect Capital Corporation, a mezzanine debt and private equity firm that manages a publicly traded, closed-end, dividend-focused business development company. Prior to joining Prospect, Mr. Sher was a serial entrepreneur, founding a number of ventures in the financial services and brokerage industry. Mr. Sher was a founder and Managing Director of ESP Technologies, a leading provider of financial software and services to institutional asset managers and hedge funds. Prior to ESP, Mr. Sher was a founder and CEO of an online brokerage company, ElephantX dot com Inc. He was also co-founder of Lafayette Capital Management LLC, a statistical arbitrage hedge fund, and spent six years at The Bear Stearns and Company, Inc. where he developed trading ideas and strategies for institutional and brokerage correspondent clearing customers.

Together with Charles Wheeler and David Sher, Richard Butt is an integral part of GCM’s management team with significant experience in the investment management industry. Over the course of his 35+ year career, Mr. Butt has held a variety of senior management positions for global investment and financial institutions. Most recently, from July 2012 to August 2013, he served as President and Chief Executive Officer of P3 Global Management LLC, a firm focused on investing in municipal infrastructure assets. From August 2006 to January 2011, he served as President of Macquarie Capital Investment Management LLC., with offices in New York and Sydney, Australia, responsible for administration, operations, finance, compliance, treasury, marketing, business operations and FX/cash management for portfolios domiciled in North America, Australia, Asia, Europe and the Caribbean. In addition, Mr. Butt served as Chief Financial and Accounting Officer for Macquarie Global Infrastructure Fund, a New York Stock Exchange listed closed end fund (NYSE: MGU). Prior to joining Macquarie, Mr. Butt served as President of Refco Alternative Investments LLC and Refco Fund Holdings LLC, the commodity pool businesses associated with Refco, Inc., from January 2003 to August 2006. In this capacity, Mr. Butt was responsible for the initial development and ongoing operations of numerous public and private commodity pools. During the period from1990 through 2003, he served in various operational and financial capacities with multiple mutual / hedge fund third party administration firms. Earlier in his career, he served as Vice President at Fidelity Investments, where he was responsible for fund accounting and financial reporting for all equity and global mutual funds. Mr. Butt is a Certified Public Accountant previously working at major accounting firms such as PricewaterhouseCoopers LLP, from July 1978 to July 1984, where he was an Audit Manager, and KPMG from December 1994 to October 1996, where he was a Director in their financial services consulting practice. Mr. Butt holds a Bachelor in Management Science from Duke University.

Robert Sher, who is responsible for identification of potential alternative energy investments, has extensive experience in the financial services, capital markets and energy industries. Mr. Sher most recently consulted for an Irish based renewable energy fund focused on the acquisition of wind and solar properties in Spain and Ireland. Prior to such time, Mr. Sher co-founded three diverse entrepreneurial ventures including a statistical arbitrage hedge fund, ESP Technologies, at which he served as managing director, an innovative institutional brokerage company and a financial technology company which was sold to a consortium of institutional investors in 2007. Prior to co-founding ESP, Mr. Sher was a founder, President and Head of Operations of ElephantX dot com Inc. Prior to the establishment of ElephantX dot com Inc., Mr. Sher co-founded and ran operations for Lafayette Capital Management LLC. Mr. Sher started his career at Citibank NA where he managed emerging markets customer service and accounting teams, servicing their institutional client base.

| 5 |

A GLOBAL ENERGY PARTNER

In its role as strategic partner to our advisor, GGIC, LTD (“GGIC”) will assist our advisor in identifying and evaluating investment opportunities and monitoring those investments over time. This unique relationship allows our advisor to leverage the relationships, expertise, origination capabilities, and proven investment and monitoring processes used by GGIC.

GGIC is managed by Franklin Park Holdings (“FPH”), a firm that focuses on investments in the global power and utilities sector and has developed, invested in and managed power and utility projects in the United States, Asia and Latin America. Between 2007 and 2012, FPH was responsible for developing, implementing and managing the businesses of GGIC. FPH owns an interest in the operating assets of GGIC, including an indirect investment in our advisor, GCM. In addition to their experience with GGIC, FPH’s management team, Thomas Tribone, Sonny Lulla and Robert Venerus, are former Senior Executives of The AES Corporation, a Fortune 200 power company. Thomas Tribone and Sonny Lulla serve on GCM’s investment committee.

INVESTMENT COMMITTEE OF OUR ADVISOR

Our advisor utilizes an internal investment committee to oversee the implementation of our investment strategy and to govern multiple aspects of our portfolio. The investment committee, among other things:

| • | determines the composition of our portfolio, the nature and timing of the changes to our portfolio and the manner of implementing such changes; |

| • | identifies, evaluates and negotiates the structure of the investments we make (including performing due diligence on our prospective projects); |

| • | closes and monitors the investments we make; and |

| • | assists in the preparation of requests to members. |

The investment committee is comprised of Charles Wheeler, who also serves as President of the company, and is Senior Managing Director and Chief Investment Officer of our advisor and a member of our board of directors, David Sher, who serves as Chief Executive Officer of our advisor and is a member of our board of directors, and two representatives of GGIC— Sonny Lulla and Thomas Tribone. No member of the investment committee has ever served as an officer or director of RCS Capital Corporation (“RCS”) (the parent of the dealer manager), or any of their affiliates.

OVERVIEW OF SIGNIFICANT GOVERNMENT INCENTIVES

The renewable energy and energy efficiency sector attracts significant U.S. federal, state and local government support and incentives to address technical barriers to the deployment of renewable energy and energy efficiency technologies and to promote the use of renewable energy and energy saving strategies. These U.S. federal, state and local government incentives have historically functioned to increase (1) the revenue generated by, and (2) the equity returns available from, renewable energy projects. Energy efficiency projects are also eligible to receive government incentives at the U.S. federal, state and local levels that can be applied to offset project development costs. Governments in other jurisdictions also provide various types of incentives.

Corporate entities are eligible to receive benefits through tax credits, such as production tax credits (“PTCs”), investment tax credits (“ITCs”), tax deductions, accelerated depreciation and U.S. federal grants and loan guarantees (from the U.S. Department of Energy, for instance), as described below.

In addition, we intend to take advantage of net metering rules in certain jurisdictions that provide a method of crediting customers who produce electricity on-site for generation in excess of their own electricity consumption or via community energy products. The excess energy produced is generally returned to the grid.

The following is a description of certain U.S. federal and state government incentives, which we may utilize in executing our business strategy.

| 6 |

U.S. Federal Incentives

Corporate Depreciation: Modified Accelerated Cost Recovery System (“MACRS”). Under MACRS, owners of renewable energy and some energy efficiency projects can recover capital invested through accelerated depreciation, which reduces the payment of corporate tax.

Production Tax Credits. PTCs are provided to owners of certain renewable energy projects that produce electricity for sale to unrelated persons. This credit is applicable for a 10-year period from the time a project is placed into service and benefits owners with tax liabilities against which to claim the tax credit. PTCs for wind energy, hydro, geothermal and bio energy projects expires for projects the construction of which begins after December 31, 2014.

Investment Tax Credits. ITCs provide that eligible systems, such as solar systems and fuel cell systems, receive a credit of 30% of the eligible cost-basis with no maximum limit. This credit is currently structured as a tax credit, whereby the owners of a qualifying renewable energy or energy efficient project can elect to receive the tax credit once the project is placed into service. The placed-in-service deadline for solar energy projects to produce electricity can be as late as December 31, 2016.

State Incentives

Renewable Portfolio Standards. RPSs, while varying based on jurisdiction, specify that a portion of the power utilized by local utilities must be derived from renewable energy sources. Currently, according to the Annual Energy Outlook, more than 30 state governments have enacted RPS programs, set mandates, or set goals that require utilities to include or obtain a minimum percentage of their energy from specific renewable energy sources. Under the RPS programs, utilities can (1) build or own renewable energy generation facilities, (2) purchase energy or RECs generated from renewable energy generation facilities, or (3) pay a penalty for any shortfalls in meeting the RPS.

Renewable Energy Certificates. RECs (or EECs) are used in an RPS program as tradable certificates that represent a certain number of kilowatt hours of energy that have been generated by a renewable source or that has been saved by an energy efficiency project, which provide further support to renewable energy initiatives. RECs are a separate commodity from the underlying power and can be traded or sold to utilities or third parties who need credits to meet RPS requirements or to brokers and other market makers for investment purposes. Many states have energy specific REC programs.

Feed-In Tariffs. Certain U.S. states and provinces of Canada have implemented feed-in tariffs (“FITs”) that entitle the renewable energy producer to enter into long-term contracts pursuant to which payment is based on the cost of generation for the different types of renewable energy projects. In addition to differences in FITs based on the type of project, FITs vary based on projects in different locations, such as rooftops or ground-mounted for solar PV projects, different sizes, and different geographic regions. FITs are available to anyone including homeowners, business owners, farmers, as well as private investors. The tariffs are typically designed to ratchet downward over time to both track and encourage technological change.

ENVIRONMENTAL REGULATION

Various U.S. federal, state and local permits are required to construct renewable energy and energy efficiency projects. The projects in which we invest must conform to all applicable environmental regulations and codes, including those relating to the discharge of materials into the air, water and ground, which will vary from place to place and time to time, as well as based on the type of renewable energy asset involved in the project.

We seek to purchase, finance or otherwise invest in projects that are at least “shovel ready,” meaning that all, or substantially all, planning, engineering and permitting, including all major permits and approvals from local and state regulatory agencies, are in place and construction can begin immediately or upon receipt of certain final permits that must be obtained immediately prior to construction. However, the projects in which we invest may incur significant costs in the ordinary course of business related to the maintenance and continued compliance with these laws, regulations and permit requirements.

| 7 |

Failure to comply with these laws, regulations and permit requirements may result in administrative, civil and criminal penalties, imposition of investigatory, cleanup and site restoration costs and liens, denial or revocation of permits or other authorizations and issuance of injunctions to limit or cease operations. In addition, claims for damages to persons or property have been brought and may in the future result from environmental and other impacts of the activities of our projects.

COMPETITION

Though we believe there is currently a capital shortage in the renewable energy sector, we will still compete for projects with other energy corporations, investment funds (including private equity funds and mezzanine funds), traditional financial services companies such as commercial banks and other sources of funding, as well as utilities and other producers of electricity. Moreover, alternative investment vehicles, such as hedge funds, also make investments in renewable energy projects. Our competitors may be substantially larger and have considerably greater financial, technical and marketing resources than we do.

STAFFING

We will not have any employees. Our day-to-day investment operations are managed by GCM. In addition, pursuant to an administration agreement with Greenbacker Administration LLC (Greenbacker Administration), it provides us with administrative services. As of the date hereof, Greenbacker Administration has delegated certain of its administrative functions to US Bancorp Financial Services LLC as well as an accounting for our investments to an independent firm which provides outsourced bookkeeping and accounting services. Greenbacker Administration may enter into similar arrangements with other third party administrators, including with respect to cash management and accounting services. While Greenbacker Administration may perform certain asset management and oversight services, as well as asset accounting and administration services, for the company, it is anticipated that Greenbacker Administration will delegate the majority of such administrative functions to third parties in order to recognize certain operational efficiencies for the benefit of the company.

ADVISORY AGREEMENT

Advisory Services

GCM, a private firm that intends to register as an investment adviser under the Advisers Act no later than it is required to do so pursuant to the Advisers Act, serves as our advisor. Under the direction of our board of directors, GCM manages our day-to-day operations and provides advisory and management services to us. Under the terms of our advisory agreement, GCM will, among other things:

| • | determine the composition of our portfolio, the nature and timing of the changes to our portfolio and the manner of implementing such changes; |

| • | identify, evaluate and negotiate the structure of the investments we make (including performing due diligence on our prospective projects); |

| • | close and monitor the investments we make; and |

| • | assist in the preparation of requests to members. |

We currently expect our advisor and its officers and employees to spend substantially all of their time and resources on us. Pursuant to our advisory agreement, officers and personnel of the advisor who provide services to us must comply with our code of business conduct and ethics, including the conflicts of interest policy included in the code of business conduct and ethics. However, GCM’s services under the advisory agreement are not exclusive, and it, and its members and affiliates, are free to furnish similar services to other entities so long as its services to us are not impaired.

The advisory agreement was previously approved by our board of directors and became effective on April 25, 2014, the date we met our minimum offering requirement and commenced operations. Unless earlier terminated as described below, the advisory agreement will remain in effect for a period of one year from the date it became effective and will remain in effect from year-to-year thereafter if approved annually by a majority of our independent directors.

| 8 |

We may terminate the advisory agreement, without penalty, upon 60 days’ written notice. The decision to terminate the agreement may be made by a majority of our independent directors. In addition, GCM may terminate the advisory agreement with us upon 120 days’ written notice. If the advisory agreement is terminated or not renewed, we will pay our advisor accrued and unpaid fees and expense reimbursements, including any payment of subordinated fees, earned prior to termination or non-renewal of the advisory agreement. Furthermore, if the advisory agreement is terminated or not renewed, GCM will have no further obligation to limit expenses charged to us per the expense reimbursement agreement as well as incur offering expenses on behalf of the company and we will not have any further obligation to reimburse GCM for operating or offering expenses not reimbursed as of the date of the termination.

Pursuant to the advisory agreement, which has been approved by our board of directors, GCM is authorized to retain one or more subadvisors with expertise in our target assets to assist GCM in fulfilling its responsibilities under the advisory agreement. However, GCM will be required to monitor any subadvisor to ensure that material information discussed by management of any subadvisor is communicated to our board of directors, as appropriate. As of December 31, 2014, no subadvisors have been retained by GCM.

If GCM retains any subadvisor to assist it in fulfilling its responsibilities under the advisory agreement, our advisor will pay such subadvisor a portion of the fees that it receives from us. We will not pay any additional fees to a subadvisor. While our advisor will oversee the performance of any subadvisor, our advisor will remain primarily liable to us to perform all of its duties under the advisory agreement, including those delegated to any subadvisor.

Management Fee and Incentive Allocation and Distribution

Pursuant to an advisory agreement, we pay GCM a base management fee for advisory and management services. The base management fee is calculated at a monthly rate of 0.167% (2.00% annually) of our gross assets (including amounts borrowed). For services rendered under the advisory agreement, the base management fee is payable monthly in arrears. The base management fee is calculated based on the average of the values of our gross assets for each day of the prior month. Base management fees for any partial period are appropriately pro-rated.

GCM may elect to defer or waive all or a portion of the fees that would otherwise be paid to it in its sole discretion. Any portion of a deferred fee not taken as to any period will be deferred without interest and may be taken in any other period prior to the occurrence of a liquidity event as GCM may determine in its sole discretion.

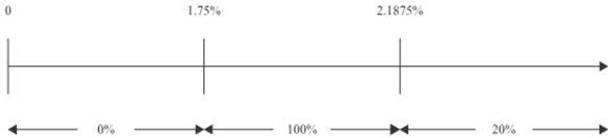

In addition, the Special Unitholder, an entity affiliated with our advisor, holds the special unit in our company entitling it to an incentive allocation and distribution. Pursuant to the company’s amended and restated limited liability company agreement (“LLC Agreement”), the incentive allocation and distribution, or incentive distribution, is comprised of three parts as follows: The first part, the income incentive distribution, is calculated and payable quarterly in arrears based on our pre-incentive distribution net investment income for the immediately preceding fiscal quarter. For this purpose, pre-incentive distribution net investment income means (1) interest income, (2) dividend, project and distribution income from equity investments (but excluding that portion of distributions that are treated as a return of capital) and (3) any other income (including any other fees, such as commitment, origination, structuring, diligence and consulting fees or other fees that we receive, but excluding any fees for providing managerial assistance) accrued during the fiscal quarter, minus our operating expenses for the fiscal quarter (including the base management fee, expenses payable under the administration agreement with our Administrator, and any interest expense and distributions paid on any issued and outstanding indebtedness and preferred units of limited liability company interest, but excluding the incentive distribution). Pre-incentive distribution net investment income includes, in the case of investments with a deferred interest feature (such as original issue discount, debt instruments with pay in kind interest and zero coupon securities), accrued income that we have not yet received in cash. If interest income is accrued but never paid, our board of directors would decide to write off the accrual in the fiscal quarter when the accrual is determined to be uncollectible. The write off would cause a decrease in interest income for the fiscal quarter equal to the amount of the prior accrual. GCM is not under any obligation to reimburse us for any part of the incentive distribution it received that was based on accrued income that we never receive as a result of a default by an entity on the obligation that resulted in the accrual of such income. Pre-incentive distribution net investment income does not include any realized capital gains, realized capital losses, unrealized capital appreciation or depreciation or any accrued income taxes and other taxes including, but not limited to, franchise, property, and sales taxes. Pre-incentive distribution net investment income, expressed as a rate of return on the value of our average adjusted capital at the end of the fiscal quarter will be compared to a “hurdle rate” of 1.75% per fiscal quarter (7.00% annualized). Our net investment income used to calculate this part of the incentive distribution is also included in the amount of our gross assets used to calculate the 2.00% annualized base management fee.

| 9 |

Adjusted capital shall mean: cumulative gross proceeds generated from sales of our shares and preferred units of limited liability company interests (including our distribution reinvestment plan) reduced for distributions to members of proceeds from non-liquidation dispositions of our assets and amounts paid for share repurchases pursuant to our share repurchase program. Average adjusted capital shall mean: the average value of the adjusted capital for the two most recently completed fiscal quarters.

The Special Unitholder shall receive an incentive distribution with respect to our pre-incentive distribution net investment income in each fiscal quarter as follows:

| • | no incentive distribution in any fiscal quarter in which our pre-incentive distribution net investment income does not exceed the “hurdle rate” of 1.75%; |

| • | 100% of our pre-incentive distribution net investment income with respect to that portion of such pre-incentive distribution net investment income, if any, that exceeds the hurdle but is less than 2.1875% in any fiscal quarter (8.75% annualized with a 7% annualized hurdle rate). We refer to this portion of our pre-incentive distribution net investment income (which exceeds the hurdle but is less than 2.1875%) as the “catch-up.” The “catch-up” is meant to provide the Special Unitholder with 20% of our pre-incentive distribution net investment income as if a hurdle did not apply if this net investment income exceeds 2.1875% in any fiscal quarter; and |

| • | 20% of the amount of our pre-incentive distribution net investment income, if any, that exceeds 2.1875% in any fiscal quarter (8.75% annualized with a 7% annualized hurdle rate) is distributed to the Special Unitholder (once the hurdle is reached and the catch-up is achieved, 20% of all pre-incentive distribution investment income thereafter is allocated to the Special Unitholder). |

The following is a graphical representation of the calculation of the income-related portion of the incentive distribution:

Quarterly Incentive Distribution Based on Net Investment Income

Pre-incentive distribution net investment income

(expressed as a percentage of the value of average adjusted capital)

Percentage of pre-incentive distribution net investment income

allocated to the Special Unitholder

These calculations are appropriately prorated for any period of less than three months and adjusted for any share issuances or repurchases during the relevant quarter. You should be aware that a rise in the general level of interest rates can be expected to lead to higher interest rates applicable to our debt investments. Accordingly, an increase in interest rates would make it easier for us to meet or exceed the incentive distribution hurdle rate and may result in an increase of the amount of incentive distributions payable to the Special Unitholder with respect to pre-incentive distribution net investment income.

| 10 |

The second part of the incentive distribution, the capital gains incentive distribution, will be determined and payable in arrears as of the end of each fiscal quarter (or upon termination of the advisory agreement, as of the termination date) and will equal 20.0% of our realized capital gains, if any, on a cumulative basis from inception through the end of each fiscal quarter, computed net of all realized capital losses and unrealized capital depreciation on a cumulative basis, less the aggregate amount of any previously paid capital gains incentive distributions. For purposes of calculating the foregoing: (1) the calculation of the incentive distribution shall include any capital gains that result from cash distributions that are treated as a return of capital, (2) any such return of capital will be treated as a decrease in our cost basis of an investment, and (3) all quarterly valuations will be determined by us in accordance with our valuation procedures. In determining the capital gains incentive distribution to which the Special Unitholder may be entitled, we will calculate the aggregate realized capital gains, aggregate realized capital losses and aggregate unrealized capital depreciation, as applicable, with respect to each of our assets. For this purpose, aggregate realized capital gains, if any, will equal the sum of the differences between the net sales price of each investment, when sold or otherwise disposed, and the aggregate cost basis of such investment reduced by cash distributions that are treated as returns of capital. Aggregate realized capital losses will equal the sum of the amounts by which the net sales price of each investment, when sold or otherwise disposed, is less than the aggregate cost basis of such investment reduced by cash distributions that are treated as returns of capital. Aggregate unrealized capital depreciation will equal the sum of the difference, if negative, between the valuation of each investment as of the applicable date and the aggregate cost basis of such investment reduced by cash distributions that are treated as returns of capital. At the end of the applicable period, the amount of capital gains that serves as the basis for our calculation of the capital gains incentive distribution will equal the aggregate realized capital gains, excluding any accrued income taxes and other taxes including, but not limited to, franchise, property, and sales taxes associated with the sale or disposal of the asset, less aggregate realized capital losses and less aggregate unrealized capital depreciation with respect to our assets. If this number is positive at the end of such period, then the capital gains incentive distribution for such period will be equal to 20% of such amount, less the aggregate amount of any capital gains incentive distributions paid in all prior periods.

Because of the structure of the incentive distribution, it is possible that the Special Unitholder may be entitled to receive an incentive distribution in a fiscal quarter where we incur a loss. For example, if we receive pre-incentive distribution net investment income in excess of the hurdle rate for a fiscal quarter, we will make the applicable income incentive distribution even if we have incurred a loss in that fiscal quarter due to realized or unrealized losses on our investments.

The third part of the incentive distribution, which we refer to as the liquidation incentive distribution, will equal 20.0% of the net proceeds from a liquidation of our company in excess of adjusted capital, as calculated immediately prior to liquidation. In the event of any liquidity event that involves a listing of our shares, or a transaction in which our members receive shares of a company that is listed, on a national securities exchange, if that liquidity event produces a listing premium (which we define as the amount, if any, by which our listing value following such liquidity event exceeds the adjusted capital, as calculated immediately prior to such listing), the liquidation incentive distribution, which will equal 20% of any listing premium, will be determined and payable in arrears 30 days after the commencement of trading following such liquidity event. For the purpose of calculating this distribution, our “listing value” will be the product of: (i) the number of listed shares and (ii) average closing price per share over the 30 trading-day period following such liquidity event. For the purpose of calculating the listing premium, any cash consideration received by members in connection with any such liquidity event will be included in (as an addition to) our listing value. In the event that the members receive non-listed securities as full or partial consideration with respect to any listing, no value will be attributed to such non-listed securities.

The liquidation incentive distribution is payable in cash or shares, or in any combination thereof.

Upon the occurrence of (1) non-renewal of the advisory agreement upon the expiration of its then current term; (2) termination of the advisory agreement for any reason under circumstances where an affiliate of Greenbacker Group LLC does not serve as the advisor under any replacement advisory agreement; or (3) resignation of GCM under the advisory agreement, which we refer to as a “trigger event”, we will have the right, but not the obligation, to repurchase the special unit or the special preferred stock, as applicable, at the fair market value of the special unit or the special preferred stock on the date of termination, as determined by an independent appraiser. In such event, the purchase price will be paid in cash or shares of limited liability company interests, at the option of the Special Unitholder. We must purchase any such interests within 120 days after giving the Special Unitholder written notice of our desire to repurchase the special unit or the special preferred stock. If the advisory agreement is terminated or not renewed, we will pay our advisor accrued and unpaid fees and expense reimbursements, including any payment of subordinated fees, earned prior to termination or non-renewal of the advisory agreement.

| 11 |

Examples of Quarterly Incentive Distribution Calculation

Example 1: Income Related Portion of Incentive Distribution:

Alternative 1

Assumptions

Investment income (including interest, distributions, fees, etc.) = 1.25%

Hurdle rate (1) = 1.75%

Management fee (2) = 0.500%

Other operating expenses (i.e. legal, accounting, custodian, transfer agent, etc.) = 0.20%

Pre-incentive distribution net investment income

(investment income – (management fee + other operating expenses)) = 0.55%

Pre-incentive net investment income does not exceed hurdle rate, therefore there is no incentive distribution.

Alternative 2

Assumptions

Investment income (including interest, distributions, fees, etc.) = 2.70%

Hurdle rate (1) = 1.75%

Management fee (2) = 0.50%

Other operating expenses (i.e. legal, accounting, custodian, transfer agent, etc.) = 0.20%

Pre-incentive distribution net investment income

(investment income – (management fee + other operating expenses)) = 2.00%

Pre-incentive net investment income exceeds hurdle rate, therefore there is an income incentive distribution payable by us to GCM.

Incentive distribution = 100% × pre-incentive distribution net investment income, subject to the “catch-up” (3)

= 100% × (2.00% – 1.75%)

= 0.25%

Alternative 3

Assumptions

Investment income (including interest, distributions, fees, etc.) = 3.00%

Hurdle rate (1) = 1.75%

Management fee (2) = 0.50%

Other operating expenses (i.e. legal, accounting, custodian, transfer agent, etc.) = 0.20%

Pre-incentive distribution net investment income

(investment income – (management fee + other operating expenses)) = 2.30%

Pre-incentive net investment income exceeds hurdle rate, therefore there is an income incentive distribution made to the

Special Unitholder.

Incentive distribution = 20% × pre-incentive distribution net investment income, subject to “catch-up” (3)

Incentive distribution = 100% × “catch-up” + (20% × (pre-incentive distribution net investment income – 2.1875%))

Catch-up = 2.1875% – 1.75%

= 0.4375%

Incentive distribution = (100% × 0.4375%) + (20% × (2.3% – 2.1875%))

= 0.4375% + (20% × 0.1125%)

= 0.4375% + 0.0225%

= 0.46%

| 12 |

| (1) | Represents 7.00% annualized hurdle rate. |

| (2) | Represents 2.00% annualized management fee. |

| (3) | The “catch-up” provision is intended to provide the Special Unitholder with an incentive distribution of 20% on all of our pre-incentive distribution net investment income as if a hurdle rate did not apply when our net investment income exceeds 2.1875% in any fiscal quarter. |

Example 2: Capital Gains Portion of Incentive Distribution:

Alternative 1

Assumptions

| • | Year 1: $20 million investment made in company A (“Investment A”), and $30 million investment made in company B (“Investment B”) |

| • | Year 2: Investment A sold for $50 million and fair market value (“FMV”) of Investment B determined to be $32 million |

| • | Year 3: FMV of Investment B determined to be $25 million |

| • | Year 4: Investment B sold for $31 million |

The capital gains portion of the incentive distribution would be:

| • | Year 1: None |

| • | Year 2: Capital gains incentive distribution of $6 million ($30 million realized capital gains on sale of Investment A multiplied by 20%) |

| • | Year 3: None |

| • | Year 4: Capital gains incentive distribution of $200,000 |

$6.2 million ($31 million cumulative realized capital gains multiplied by 20%) less $6 million (capital gains fee taken in Year 2)

Alternative 2

Assumptions

| • | Year 1: $20 million investment made in company A (“Investment A”), $30 million investment made in company B (“Investment B”) and $25 million investment made in company C (“Investment C”) |

| • | Year 2: Investment A sold for $50 million, FMV of Investment B determined to be $25 million and FMV of Investment C determined to be $25 million |

| • | Year 3: FMV of Investment B determined to be $27 million and Investment C sold for $30 million |

| • | Year 4: FMV of Investment B determined to be $35 million |

| • | Year 5: Investment B sold for $20 million |

The capital gains incentive distribution, if any, would be:

| • | Year 1: None |

| • | Year 2: $5 million capital gains incentive distribution |

| • | 20% multiplied by $25 million ($30 million realized capital gains on Investment A less $5 million unrealized capital depreciation on Investment B) |

| • | Year 3: $1.4 million capital gains incentive distribution(1) |

| 13 |

$6.4 million (20% multiplied by $32 million ($35 million cumulative realized capital gains less $3 million unrealized capital depreciation)) less $5 million capital gains fee received in Year 2

| • | Year 4: None |

| • | Year 5: None |

$5 million (20% multiplied by $25 million (cumulative realized capital gains of $35 million less realized capital losses of $10 million)) less $6.4 million cumulative capital gains fee paid in Year 2 and Year 3

| (1) | As illustrated in Year 3 of Alternative 1 above, if we were to be wound up on a date other than December 31st of any year, we may have paid aggregate capital gains incentive distributions that are more than the amount of such fees that would be payable if we had been wound up on December 31 of such year. |

Example 3: Liquidation Incentive Distribution:

Alternative 1

Assumptions

| • | Year 1: Gross offering proceeds total $85 million. $20 million investment made in company A (“Investment A”), $30 million investment made in company B (“Investment B”) and $25 million investment made in company C (“Investment C”). |

| • | Year 2: Investment A sold for $25 million and all proceeds, net of any capital gains incentive distributions payable, are returned to members. FMV of Investment B determined to be $30 million and FMV of Investment C determined to be $27 million. |

| • | Year 3: FMV of Investment B determined to be $31 million. FMV of Investment C Determined to be $20 million. |

| • | Year 4: FMV of Investment B determined to be $35 million. FMV of Investment C determined to be $25 million. |

| • | Year 5: Investments B and C sold in an orderly liquidation for total proceeds of $55 million. All proceeds, net of any capital gains incentive distributions payable, are returned to members. |

The capital gains incentive distribution, if any, would be:

| • | Year 1: None |

| • | Year 2: Incentive distribution on capital gains during operations of $1 million ($5 million realized capital gains on sale of Investment A multiplied by 20.0%). Adjusted capital now equals $61 million ($85 million gross proceeds less $24 million returned to members from the sale of portfolio investments). |

| • | Year 3: None |

| • | Year 4: None |

| • | Year 5: No liquidation incentive distribution due—Liquidation proceeds of $55 million are less than adjusted capital immediately prior to liquidation ($61 million). |

Alternative 2

Assumptions

| • | Year 1: Gross offering proceeds total $85 million. $20 million investment made in company A (“Investment A”), $30 million investment made in company B (“Investment B”) and $25 million investment made in company C (“Investment C”). |

| 14 |

| • | Year 2: Investment A sold for $25 million and all proceeds, net of any capital gains incentive distributions payable, are returned to members. FMV of Investment B determined to be $30 million and FMV of Investment C determined to be $27 million. |

| • | Year 3: FMV of Investment B determined to be $31 million. FMV of Investment C determined to be $20 million. |

| • | Year 4: FMV of Investment B determined to be $35 million. FMV of Investment C determined to be $25 million. |

| • | Year 5: Investments B and C sold in an orderly liquidation for total proceeds of $80 million. All proceeds, net of any capital gains incentive distributions payable, are returned to members. |

The capital gains incentive distribution, if any, would be:

| • | Year 1: None |

| • | Year 2: Incentive distribution on capital gains during operations of $1 million ($5 million realized capital gains on sale of Investment A multiplied by 20.0%). Adjusted capital now equals $61 million ($85 million gross proceeds less $24 million returned to members from the sale of portfolio investments). |

| • | Year 3: None |

| • | Year 4: None |

| • | Year 5: $3.8 million liquidation incentive distribution—20.0% multiplied by liquidation proceeds ($80 million) in excess of adjusted capital immediately prior to liquidation ($61 million), or $19 million. |

Alternative 3 (If the liquidity event is a listing)

Assumptions

| • | Year 1: Gross offering proceeds total $85 million. $20 million investment made in company A (“Investment A”), $30 million investment made in company B (“Investment B”) and $25 million investment made in company C (“Investment C”). |

| • | Year 2: Investment A sold for $25 million and all proceeds, net of any capital gains incentive distributions payable, are returned to members. |

Incentive distribution on capital gains paid to GCM of $1 million ($5 million realized capital gains on sale of Investment A multiplied by 20.0%). Adjusted capital now equals $61 million ($85 million gross proceeds less $24 million returned to members from the sale of portfolio investments).

| • | Year 3: No change in adjusted capital. |

| • | Year 4: No change in adjusted capital. |

| • | Year 5: All shares of the company are listed on a national securities exchange. The listing value is $85 million. |

The liquidation incentive distribution in this example would be:

Year 5: $4.8 million liquidation incentive distribution (20% multiplied by $24 million listing premium ($85 million listing value in excess of $61 million of adjusted capital immediately prior to listing)).

The returns shown are for illustrative purposes only. There is no guarantee that positive returns will be realized and actual returns may vary from those shown in the examples above.

Payment of Our Expenses

Our primary operating expenses are the payment of advisory fees and other expenses under the advisory agreement and other expenses necessary for our operations. Our advisory fee compensates GCM for its work in identifying, evaluating, negotiating, executing, monitoring and servicing our investments. We may also pay fees and expenses on a direct cost basis to Greenbacker Administration or others engaged by the Greenbacker Administration for the administrative services they provide directly or indirectly under the administration agreement.

| 15 |

We will bear all other expenses of our operations and transactions, including (without limitation) fees and expenses relating to:

| • | corporate and organizational expenses relating to offerings of our shares, subject to limitations included in the advisory agreement; | |

| • | the cost of effecting sales and repurchase of shares and other securities; | |

| • | investment advisory fees; | |

| • | fees payable to third parties relating to, or associated with, making investments and valuing investments, including fees and expenses associated with performing due diligence reviews of prospective investments; | |

| • | transfer agent and custodial fees; | |

| • | fees and expenses associated with marketing efforts; | |

| • | federal and state registration fees; | |

| • | federal, state and local taxes; | |

| • | independent directors’ fees and expenses; | |

| • | costs of proxy statements, members’ reports and notices; | |

| • | fidelity bond, directors and officers/errors and omissions liability insurance and other insurance premiums; | |

| • | direct costs such as printing, mailing, long distance telephone, and staff; | |

| • | fees and expenses associated with independent audits and outside legal costs, including compliance with the Sarbanes-Oxley Act of 2002; | |

| • | costs associated with our reporting and compliance obligations under applicable federal and state securities laws; | |

| • | brokerage commissions, origination fees and any investment banking fees related to our investments; | |

| • | all other expenses incurred by GCM, in performing its obligations subject to the limitations included in the advisory agreement; and | |

| • | all other expenses incurred by either the Administrator, its’ delegates or us in connection with administering our business, including payments for the administrative services the Administrator provides under the administration agreement that will be based upon our allocable portion (subject to the review and approval of our board of directors) of the Administrator’s overhead and other expenses. |

Pursuant to the expense reimbursement agreement, between the company and advisor (i) for the period beginning January 30, 2014 and ending December 31, 2014, our advisor reimbursed operating expenses for the company in an amount sufficient to keep total annual operating expenses (exclusive of interest, taxes, dividend expense, borrowing costs, organizational and extraordinary expenses) of the company (“Expenses”) at percentages of average net assets of such class for any calculation period no higher than 6.0% for Class A, Class C, and Class I shares (the “Maximum Rates”), and (ii) the company shall reimburse our advisor, within 30 days of delivery of a request in proper form, for such Expenses, provided that such repayments do not cause the total Expenses attributable to a share class during the year of repayment to exceed the Maximum Rates. No repayments by the company to advisor shall be permitted after the earlier of (i) the company’s offering has expired or is terminated or (ii) December 31, 2016. The expense reimbursement agreement was amended in December 2014 to continue until the earlier of December 31, 2015 or the end of the offering. Furthermore, if the advisory agreement is terminated or not renewed, our advisor will have no further obligation to limit expenses per the expense reimbursement agreement as well as incur offering expenses on behalf of the company and the company will not have any further obligation to reimburse our advisor for operating and offering expenses not reimbursed as of the date of the termination.

| 16 |

Organization and Offering Expenses

We will reimburse our advisor and its affiliates for organization and offering expenses it may incur on our behalf but only to the extent that the reimbursement would not cause the selling commissions, the dealer manager fee and the other organization and offering expenses borne by us to exceed 15.0% of gross offering proceeds as of the date of the reimbursement. If we raise the maximum offering amount in the primary offering and under the distribution reinvestment plan, we expect organization and offering expenses (other than selling commissions and the dealer manager fee) to be 1.5% of gross offering proceeds. These organization and offering expenses include all expenses (other than selling commissions and the dealer manager fee) to be paid by us in connection with the offering, including but not limited to:

| • | Our legal, accounting, printing, mailing and filing fees; | |

| • | Charges of our escrow holder and transfer agent, charges of our advisor for administrative services related to the issuance of shares in the offering; | |

| • | Reimbursement of bona fide due diligence expenses of broker-dealers; | |

| • | Reimbursement of our advisor for costs in connection with preparing sales materials, the cost of bona fide training and education meetings held by us (primarily the travel, meal and lodging costs of registered representatives of broker-dealers), attendance and sponsorship fees and cost reimbursement for employees of our affiliates to attend retail seminars conducted by broker-dealers; and | |

| • | Reimbursement to participating broker-dealers for technology costs associated with the offering, costs and expenses related to such technology costs and costs and expenses associated with the facilitation of the marketing of shares and the ownership of shares by such broker-dealers’ customers, which will be included in underwriting compensation. |

Other Operating Expenses

We will reimburse the expenses incurred by GCM or its affiliates in connection with its provision of services to us, including the investigation and monitoring of our investments and costs incurred in connection with GCM’s valuation methodologies or the effecting of sales and repurchases of our shares and other securities. We will not reimburse our advisor or its affiliates for (i) rent or depreciation, utilities, capital equipment and other administrative items; (ii) salaries, fringe benefits and other similar items incurred or allocated to any controlling person of GCM; (iii) the salaries and benefits paid to any executive officer or board member of GCM; or (iv) any services for which GCM receives a separate fee.

Indemnification

The advisory agreement provides that, absent willful misfeasance, bad faith or negligence in the performance of its duties or by reason of the reckless disregard of its duties and obligations, GCM and its officers, managers, partners, agents, employees, controlling persons, members and any other person or entity affiliated with it are entitled to indemnification from us for any damages, liabilities, costs and expenses (including reasonable attorneys’ fees and amounts reasonably paid in settlement) arising from the rendering of GCM’s services under the advisory agreement or otherwise as advisor of Greenbacker Renewable Energy Company LLC. Notwithstanding the above, our LLC Agreement provides that we shall not hold harmless our advisor or any of its affiliates for any loss or liability suffered by us unless all of the following conditions are met:

| • | the party seeking exculpation or indemnification has determined in good faith that the course of action leading to the loss or liability was in our best interests; | |

| • | the party seeking exculpation or indemnification was acting on our behalf or providing services to us; | |

| • | the loss or liability was not the result of negligence or misconduct; and |

| 17 |

| • | the indemnification is recoverable only out of net assets and not from our members. |

Organization of GCM

GCM is a Delaware limited liability company. The principal executive offices of GCM are located at 369 Lexington Avenue, Suite 312, New York, NY 10017.

VALUATION PROCESS AND DETERMINATION OF NET ASSET VALUE

Relevance of Our Net Asset Value

Our net asset value per share has been calculated and published on a quarterly basis since our first full quarter ending June 30, 2014. For most of our investments, market quotations are not available and are valued at fair value as determined in good faith by our advisor and/or an independent valuation firm, subject to the review and approval of the board of directors.

Our net asset value will:

| • | be disclosed in our quarterly and annual financial statements; | |

| • | determine the price per share that is paid to shareholder participants in our share repurchase program, and the price per share paid by participants in our distribution reinvestment plan after the conclusion of this offering; | |

| • | be an input in the computation of fees earned by our advisor and the Special Unitholder whose fees and distributions are linked, directly or indirectly, in whole or part to the value of our gross assets; and | |

| • | be evaluated alongside the net proceeds per share to us from this offering to ensure the net offering price per share is not above or below our net asset value per share. |

Determination of Our Net Asset Value

We calculate our net asset value per share by subtracting all liabilities from the total carrying amount of our assets, which includes the fair value of our investments, and dividing the result by the total number of outstanding shares on the date of valuation.

We have adopted Accounting Standards Codification Topic 820, Fair Value Measurements and Disclosures (formerly Statement of Financial Accounting Standards No. 157, Fair Value Measurements), or ASC Topic 820, which defines fair value, establishes a framework for measuring fair value in accordance with generally accepted accounting principles and expands disclosures about fair value measurements.

ASC Topic 820 defines fair value as “the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date”, other than a forced sale or liquidation. The transaction to sell the asset or transfer the liability is a hypothetical transaction at the measurement date, considered from the perspective of a market participant that holds the asset or owes the liability. ASC Topic 820 provides a consistent definition of fair value which focuses on exit price and prioritizes, within a measurement of fair value, the use of market-based inputs over entity-specific inputs. In addition, ASC Topic 820 provides a framework for measuring fair value and establishes a three-level hierarchy for fair value measurements based upon the transparency of inputs to the valuation of an asset or liability as of the measurement date. The three levels of valuation hierarchy established by ASC Topic 820 are defined as follows:

Level 1: Quoted prices in active markets for identical assets or liabilities, accessible by the company at the measurement date.

Level 2: Quoted prices for similar assets or liabilities in active markets, or quoted prices for identical or similar assets or liabilities in markets that are not active, or other observable inputs other than quoted prices.

Level 3: Unobservable inputs for the asset or liability.

| 18 |

In all cases, the level in the fair value hierarchy within which the fair value measurement in its entirety falls will be determined based on the lowest level of input that is significant to the fair value measurement. Our assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment and considers factors specific to each investment.