Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

(Mark One)

|

|||

|

☒

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2014

|

||

|

☐

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____ to ____

|

|

Commission File Number 001-14785

|

|

GSE Systems, Inc.

|

|

(Exact name of registrant as specified in its charter)

|

|

Delaware

|

52-1868008

|

|

|

(State of incorporation)

|

(I.R.S. Employer Identification Number)

|

|

|

1332 Londontown Blvd., Suite 200, Sykesville MD

|

21784

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

|

Registrant's telephone number, including area code: (410) 970-7800

|

|

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

|

|

Title of each class

|

Name of each exchange on which registered

|

|

|

Common Stock, $.01 par value

|

NYSE MKT

|

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of "large accelerated filer", "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer ☐

|

Accelerated filer ☐

|

Non-accelerated filer ☐

|

Smaller reporting company ☒

|

|

(Do not check if a smaller reporting company)

|

Indicate by check mark whether the registrant is a shell company (as defined in rule 12(b)-2 of the Exchange Act). Yes o No ☒

The aggregate market value of Common Stock held by non-affiliates of the Registrant was $28,901,284 on June 30, 2014, the last business day of the Registrant's most recently completed second fiscal quarter, based on the closing price of such stock on that date of $1.66.

The number of shares outstanding of the registrant's Common Stock as of March 18, 2015 was 17,887,859 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's Proxy Statement for the 2015 Annual Meeting of Stockholders to be filed pursuant to Regulation 14A under the Securities Exchange Act of 1934, as amended, are incorporated by reference into Part III.

1

TABLE OF CONTENTS

|

PART I

|

Page

|

|

|

Item 1.

|

4

|

|

|

Item 1A.

|

13

|

|

|

Item 1B.

|

20

|

|

|

Item 2.

|

20

|

|

|

Item 3.

|

20

|

|

|

Item 4.

|

20

|

|

|

PART II

|

||

|

Item 5.

|

21

|

|

|

Item 6.

|

24

|

|

|

Item 7.

|

25

|

|

|

Item 7A.

|

43

|

|

|

Item 8.

|

44

|

|

|

Item 9.

|

45

|

|

|

Item 9A.

|

45

|

|

|

Item 9B.

|

45

|

|

|

PART III

|

||

|

Item 10.

|

46

|

|

|

Item 11.

|

46

|

|

|

Item 12.

|

46

|

|

|

Item 13.

|

46

|

|

|

Item 14.

|

47

|

|

|

PART IV

|

||

|

Item 15.

|

47

|

|

|

48

|

||

|

49

|

| * | to be incorporated by reference from the Proxy Statement for the registrant's 2015 Annual Meeting of Shareholders. |

2

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS.

This report and the documents incorporated by reference herein contain "forward-looking" statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act") that are based on management's assumptions, expectations and projections about us, and the industry within which we operate, that have been made pursuant to the Private Securities Litigation Reform Act of 1995 which reflect our expectations regarding our future growth, results of operations, performance and business prospects and opportunities. Wherever possible, words such as "anticipate", "believe", "continue", "estimate", "intend", "may", "plan", "potential", "predict", "expect", "should", "will" and similar expressions, or the negative of these terms or other comparable terminology, have been used to identify these forward-looking statements. These forward-looking statements may also use different phrases. These statements regarding our expectations reflect our current beliefs and are based on information currently available to us. Accordingly, these statements by their nature are subject to risks and uncertainties, including those listed under Item 1A Risk Factors, which could cause our actual growth, results, performance and business prospects and opportunities to differ from those expressed in, or implied by, these statements. We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements and you should not place undue reliance on our forward-looking statements. Actual results or events could differ materially from the plans, intentions and expectations disclosed in the forward-looking statements we make. Except as otherwise required by federal securities law, we are not obligated to update or revise these forward looking statements to reflect new events or circumstances. We caution you that a variety of factors, including but not limited to the factors described below under Item 1A Risk Factors and the following, could cause our business conditions and results to differ materially from what is contained in forward-looking statements:

| - | changes in the rate of economic growth in the United States and other major |

international economies;

| - | changes in investment by the nuclear and fossil electric utility industry, the chemical and petrochemical industries and the U.S. military; |

| - | changes in the financial condition of our customers; |

| - | changes in regulatory environment; |

| - | changes in project design or schedules; |

| - | contract cancellations; |

| - | changes in our estimates of costs to complete projects; |

| - | changes in trade, monetary and fiscal policies worldwide; |

| - | currency fluctuations; |

| - | war and/or terrorist attacks on facilities either owned or where equipment or services are or may be provided; |

| - | outcomes of future litigation; |

| - | protection and validity of our trademarks and other intellectual property rights; |

| - | increasing competition by foreign and domestic companies; |

| - | compliance with our debt covenants; |

| - | recoverability of claims against our customers and others; and |

| - | changes in estimates used in our critical accounting policies. |

Other factors and assumptions not identified above were also involved in the formation of these forward-looking statements and the failure of such other assumptions to be realized, as well as other factors, may also cause actual results to differ materially from those projected. Most of these factors are difficult to predict accurately and are generally beyond our control. You should consider the areas of risk described above in connection with any forward-looking statements that may be made by us. You should not place undue reliance on any forward-looking statements. New factors emerge from time to time, and it is not possible for us to predict which factors will arise.

We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise. You are advised, however, to consult any additional disclosures we make in proxy statements, quarterly reports on Form 10-Q and current reports on Form 8-K filed with the SEC.

Company Information Available on the Internet

Our Internet address is www.gses.com. We make available free of charge through our Internet site our annual reports on Form 10-K; quarterly reports on Form 10-Q; current reports on Form 8-K; and any amendment to those reports filed or furnished pursuant to the Exchange Act as soon as reasonably practicable after such material is electronically filed with, or furnished to, the SEC.

3

PART I

GSE Systems, Inc. ("GSE Systems", "GSE", the "Company", "we", "us" or "our"), a NYSE MKT company trading under symbol GVP, is a team of dedicated people that help customers meet their performance improvement goals and reduce their risk. We do this by combining expertise in simulation, visualization, engineering, equipment operations, and training to improve both plant and human performance.

We execute projects globally with over 330 employees operating from offices in the U.S., China, India, Sweden and the United Kingdom. While the majority of revenue comes from the nuclear and fossil power generation markets, we also serve the oil and gas, refining, chemicals, petrochemicals, industrial gas, manufacturing, transportation and plant utilities markets.

GSE Systems was formed on March 30, 1994 to consolidate the simulation and related businesses of S3 Technologies, General Physics International Engineering & Simulation and EuroSim, each separately owned and operated by ManTech International Corporation, GP Strategies Corporation and Vattenfall AB, respectively.

On April 26, 2010, we completed the acquisition of TAS Holdings Ltd ("TAS") and subsequently merged TAS into our UK subsidiary, GSE Systems Ltd. Our UK operations, located in Stockton-On-Tees, England provides engineering consulting, specifically in electrical system design, instrumentation and controls engineering and automation engineering. The majority of our UK customers are in the petroleum refining, oil and gas, chemical and petrochemical industries.

On January 4, 2011, we acquired EnVision Systems, Inc. ("EnVision"). The EnVision product line consists of interactive computer-based tutorials and related simulation models primarily for the petrochemical and oil & gas refining industries. The EnVision products provide a foundation in process fundamentals and plant operations and interaction. We have more than 750 installations of EnVision product in over 28 countries, and our approximately 130 clients include Shell Oil Company, BP Products North America ("BP"), Total and Chevron.

On November 14, 2014, we acquired Hyperspring, LLC, an Alabama limited liability company. Hyperspring is a staff augmentation company that hires personnel to fulfill staff positions on a short-term basis for energy industry customers, primarily nuclear power customers. Hyperspring personnel provide training, operations and maintenance support including: generic fundamentals exams (GFES), accreditation training visit (ATV) preparation, senior reactor operator (SRO) certification, procedure development, work management, tagging/labeling, outage execution, planning/scheduling, corrective action, self-assessments and equipment reliability. Customers include TVA, Entergy, PSEG Nuclear LLC and NRG Energy Inc.

In conjunction with the Hyperspring acquisition, the Company acquired a 50% ownership stake in IntelliQlik, LLC, a Delaware limited liability company. IntelliQlik is developing a software platform for online learning and learning management for the energy market. A former Member of Hyperspring also has a 50% ownership stake in IntelliQlik.

On December 31, 2014 the Company merged EnVision with GSE Power Systems, Inc. and changed the name of GSE Power Systems, Inc. to GSE Performance Solutions, Inc. The change reflects our growing focus on providing solutions to improve Human and Plant Performance Lifecycles.

For years we have described ourselves as a simulation company, providing mainly simulation solutions to improve designs, de-risk projects and train operators. Our acquisition of Hyperspring, LLC and investment in IntelliQlik, LLC in November 2014 are helping to accelerate our transformation into a Performance Improvement Company. We improve plant performance with a combination of simulation, engineering and plant services that help clients improve their plant's profitability, productivity and safety, and assist in decommissioning the plants at the end of their life cycle. We improve human performance by providing technologies and services that systematically help clients in recruiting and selecting the right person for the job and training that individual throughout their career from entry-level to expert.

As of December 31, 2014, GSE Systems was the parent company of:

| ¨ | GSE Performance Solutions, Inc. (formerly GSE Power Systems, Inc.), a Delaware corporation |

| ¨ | GSE Power Systems, AB, a Swedish corporation; |

| ¨ | GSE Engineering Systems (Beijing) Co. Ltd., a Chinese limited liability company; |

| ¨ | GSE Systems, Ltd., a Scottish limited liability company; |

| ¨ | EnVision Systems (India) Pvt. Ltd., an Indian limited liability company; and |

| ¨ | Hyperspring, LLC, an Alabama limited liability company. |

The Company has a 50% interest in IntelliQlik, LLC, a Delaware limited liability company and a 50% interest in General Simulation Engineering RUS LLC, a Russian closed joint-stock company.

4

Operating Segments

With the acquisition of Hyperspring, we now operate through two reportable business segments. We are organized by operating groups primarily based upon the services performed by each group. Each operating group consists of business units which are focused on providing specific products and services to certain classes of customers or within targeted markets. Marketing and communications, accounting, finance, legal, human resources, information systems and other administrative services are organized at the corporate level. Business development and sales resources are aligned with operating groups to support existing customer accounts and new customer development. Our two business segments are:

|

·

|

Performance Improvement Solutions

|

As evidenced through the change in the company name of our U.S. operating company to GSE Performance Solutions, Inc., our Performance Improvement Solutions business segment encompasses all of the solution-oriented technologies and services traditionally associated with GSE which focus on both our client's people and their plants and operations. This segment includes various simulation, training and engineering products and services delivered across the breadth of industries we serve. Our simulation solutions include platforms ranging from (1) the non-specific plant systems of our EnVision product line used to teach fundamental processes to newly hired employees, to (2) custom plant-specific simulators used to train plant operators, to (3) engineering-grade simulation solutions used to help clients verify and validate control systems prior to new plant construction or modification of existing plants, to (4) engineering-grade simulation solutions used for human factors engineering. Training applications include turnkey and custom training services and 3D visualization training products to make training more effective. Our engineering services include plant design, automation and control systems design, functional safety and compliance analysis, and engineering consultations.

|

·

|

Staff Augmentation

|

Staff Augmentation services provide specialized workforce solutions primarily to the nuclear industry. These employees work at our clients' facilities under client direction. Examples of staff augmentation positions include instructors, procedure writers, work management specialists, planners, outage execution specialists, corrective action and self-assessment specialists, and training material developers. This business is managed through our Hyperspring LLC subsidiary. The business model, management focus, margins and other factors clearly separate this business line from the rest of the GSE product and service portfolio. Hyperspring has been providing these services since 2005.

Financial information about our business segments and geographic operations and revenue are provided in Note 16 of the accompanying Consolidated Financial Statements.

Products, Services, Strategy

We believe the most serious future challenge facing the industries we serve is not their access to technology, their access to markets, nor their access to operating capital. Instead the challenge will be their access to a trained and efficient workforce. This challenge manifests itself due to both the knowledge that will be lost as a large percentage of the experienced workforce reaches retirement age in the next ten years and the replacement of these experienced workers by a new generation who have different learning styles and work expectations.

This belief is supported by the following trends as reported in the U.S. Department of Energy's National Energy Technology Laboratory 2013 report entitled Emerging Workforce Trends in the U.S. Energy and Mining Industries: A Call to Action.

|

·

|

About 1/3 of the U.S. energy industry workforce is comprised of "baby boomers" (those born between 1946 and 1964), and they are poised to retire in great numbers by the end of this decade,

|

|

·

|

There are too few younger workers in the pipeline to replace them, and many of the younger workers lack the necessary science, technology, engineering and math skills needed for many energy jobs,

|

|

·

|

There is a critical need to capture the knowledge of experienced employees before they leave.

|

Exacerbating this workforce trend is the continuing domestic and global population increases which will continue to increase the overall demand for energy. As the U.S.' current educational system is not able to provide the needed trained workers in adequate numbers, the onus is on the energy industry itself to address its training needs at both entry levels and more senior levels. A complete lifecycle of training, from a worker's entry into the energy industry through to the achievement of expert knowledge and skills, is now required for the energy industry more than ever.

Business leaders are recognizing the problem and the challenge ahead. A study published in Harvard Business Review (May 28, 2013) revealed that Boards of Directors identified Talent Management as their number one concern. Those same executives rated their companies very poorly on key elements of talent management including attracting, hiring, assessing and developing top talent.

As companies are always under pressure to improve productivity, reduce costs and improve operating margins, energy industry companies have been working to create leaner, more competent organizations that can rapidly respond to a changing environment. Increasing pressures to improve profitability have resulted in flatter organizational structures within companies with less middle management to exercise control. According to the International Atomic Energy Agency (IAEA) article, A Systematic Approach to Human Performance Improvement in Nuclear Power Plants: Training Solutions, companies understand and value the potential contribution that every employee can make to their overall success. As a result, companies have been emphasizing the quality of their human performance processes and the building of excellent educational processes for their employees.

5

Entry2Expert Performance Cycle

To assist our clients in creating world-class internal training and performance improvement programs, we are building the E2E (Entry2Expert) Performance Solution, a set of integrated and scalable products and services which provide a structured program from employee selection and onboarding through continuous skills improvement for experienced employees. GSE can now provide the right training solution for the right step in each employee's career.

The major elements of the E2E Performance Solution include:

|

·

|

Employee Screening and Selection: Leveraging the use of simulation and providing experts in employee assessments, we help clients ensure their candidates for employment possess both technical aptitude as well as personality traits suited for the specific job functions.

|

|

·

|

Training Needs Assessments: We help clients define their specific training needs by analyzing the job functions and processes specific to their plant. This is the first step in creating a structured training program that will provide consistent and predictable results.

|

|

·

|

Training Program Development: Following the ADDIE (Analyze, Design, Develop, Implement, and Evaluate) model for training program management, we can structure the entire training program for the client, including training media and modes, such as self-paced e-Learning, instructor-led classroom, in-depth simulation, and serious gaming.

|

|

·

|

Self-Paced Training Tutorials: We have a full complement of e-Learning material. The products include basic equipment and component fundamentals that are applicable across a variety of industries, as well as comprehensive training for the oil and gas and refining markets. Using a blended learning approach, students learn the overall purpose of plant systems, the major equipment, how the equipment is operated and controlled. This methodology ensures the students know the basics before entering a plant-specific training program. We have delivered over 500 such tutorial programs in multiple languages worldwide.

|

|

·

|

Instructor-Led Training: We provide classroom and simulator instructors as adjunct staff or to teach turnkey training programs using training materials that either we or the client have developed. Turnkey courses include ANSI Fundamentals (math and sciences), Generic Fundamentals (nuclear plant components, systems, and reactor theory), Senior Reactor Operator (SRO) Certification, and Engineering Systems Program courses.

|

6

|

·

|

Universal Training Simulators: These products complement the Self-Paced Training Tutorials by reinforcing what the student learned in the tutorial by putting it into practice on the Universal Simulator. The simulation models are high fidelity and engineering correct, but represent a typical plant or typical process, versus the exact replication of a client's plant. We have delivered over 250 such simulation models to clients consisting of major oil companies and educational institutions.

|

|

·

|

Part-Task Training Simulators: Like the Universal Simulators, we provide other unique training solutions such as a generic nuclear plant simulator, VPanel displays which replicate control room hardware and simulator solutions specific to industry need, such as Severe Accident models to train on and aid in the understanding of events such as the Fukushima Daiichi accident.

|

|

·

|

3D Visualization: Being able to visualize complex processes, or detailed maintenance tasks significantly improves understanding and retention while reducing the learning process. We provide 3D visualization solutions to help customers "see" and understand the internal workings complex systems such as nuclear reactors, or how to maintain complicated pieces of equipment. Blending the learning strategy of incorporating 3D visualization with high-fidelity, real-time simulation models enables us to provide the energy industry with better, faster, and less costly training in an immersive environment that is ideally suited for the next generation workforce.

|

|

·

|

Plant-Specific Operator Training Simulators: These simulators provide an exact replication of the plant control room and plant operations. They provide the highest level of realism and training and allow users to practice their own plant-specific procedures. Clients can safely practice startup, shutdown, normal operations, as well as response to abnormal events we all hope they never have to experience in real life. We have delivered nearly 450 plant-specific simulators to clients in the nuclear power, fossil power and process industries worldwide.

|

The goal of our E2E performance lifecycle offering is to ensure superior human achievement in the dimensions of:

|

·

|

Recruiting, screening, and selecting the right workforce

|

|

·

|

Shortening the learning process

|

|

·

|

Reduce human errors

|

|

·

|

Mitigate effects of retirement and turnover

|

|

·

|

Improve workforce agility

|

|

·

|

Achieve and maintain certifications and compliance

|

|

·

|

All of which improve our customers' bottom lines

|

The dramatic increase in energy demand world-wide over the next 30 years will require significant amounts of training for new employees and also require new plants using energy of all sources. Obviously, these new plants will need to be engineered and designed prior to construction, and due to their high-fidelity our modeling tools are being increasingly used to verify and validate control system and overall plant designs.

7

Design2Decom Performance Cycle

Just like the Entry2Expert (E2E) process helps improve the performance of our customers' people, Design2Decom (D2D) encompasses a range of services and technologies aimed at improving plant performance. From getting a client's system on-line faster, to operating safety, and support from experienced staff throughout the lifecycle, services include:

|

·

|

Engineering Consultancy, Project Execution and Project Management: Whether in the feasibility, concept or detail design stages of a plant or for plant modifications, we help clients design and implement engineering projects across several disciplines:

|

|

o

|

Instrumentation Engineering

|

|

o

|

Control Systems Engineering

|

|

o

|

Automation Design Engineering

|

|

o

|

Electrical Design Engineering

|

|

·

|

Virtual commissioning of plants. Our high-fidelity, simulation-based engineering solutions test design assumptions and provide feedback throughout the design process for:

|

|

o

|

Integrated systems design validation

|

|

o

|

Control strategy design validation

|

|

o

|

Human factors engineering support

|

|

o

|

Operating procedure validation

|

|

o

|

Control system validation

|

|

·

|

Safety and Compliance: Our engineering expert de-risk operations through engineering assessments and remediation services to ensure safety and legislative compliance in the following areas:

|

|

o

|

Functional Safety

|

|

o

|

Electrical Safety

|

|

o

|

Hazardous Areas Safety

|

|

o

|

Arc Flash Safety

|

|

o

|

Alarm Management

|

8

|

·

|

Specialized Plant Support: As our customers' experienced staffs retire, access to experts that can help with specialized plant projects is critical. Through the acquisition of Hyperspring, we also provide expert support either through staff augmentation or turnkey projects for the following:

|

|

o

|

Procedure Development

|

|

o

|

Training Material Upgrade and Development

|

|

o

|

Work Management

|

|

o

|

Outage Execution

|

|

o

|

Planning and Scheduling

|

|

o

|

Corrective Actions

|

|

o

|

Self-Assessments

|

|

o

|

Equipment Reliability

|

|

·

|

Decommissioning: As plants reach the end of their useful life, decommissioning and deconstruction is a critical service, particularly in the nuclear industry where contaminated material must be handled in safe and precise manners. Our engineering, simulation and visualization capabilities enable clients to plan for, train for, and execute decommissioning while minimizing exposure to hazardous materials and saving money.

|

The goal of Design2Decom (D2D) is to help clients optimize plant performance and compliance in terms of the following:

|

·

|

Finding design errors during engineering rather than construction allowing plant startup to occur sooner saving countless man-hours and dollars while simultaneously allowing revenue generation sooner.

|

|

·

|

Ensuring plants are safely operated within the regulatory requirements.

|

|

·

|

Providing expert support for specialized projects and to augment an aging workforce.

|

|

·

|

Limiting cost and hazards exposure through intelligent decommissioning solutions.

|

Our two overarching solution sets, Entry2Expert (E2E) and Design2Decom (D2D) bring together the collection of skills GSE has amassed over more than 40 years from its traditional roots in custom simulation to the acquisition of the specialized engineering capabilities of TAS Holding, entry and intermediate level training solutions via our EnVision acquisition, and now extensive training and plant support capabilities by acquiring Hyperspring.

9

Customers and Locations

For more than 40 years, we have been developing next-generation, custom training simulation technologies. Since we built the first commercial full-scope nuclear power plant simulator in 1971, we have completed more than 1,100 installations in 50 countries and have built more full-scope power plant simulators than all of our competitors combined.

In 2014, approximately 52% of our revenue was generated from end-users outside the United States. A small representative list of our customers include: ABB Inc., Comisión Federal de Electricidad (Mexico), EDF Energy (United Kingdom), Emerson Process Management, Kärnkraftsäkerhet och Utbildning AB (Sweden), Kraftwerks–Simulator-Gesellschaft GmbH (Germany), PSEG Nuclear, Inc., Shangdong Nuclear Power Co. Ltd. (China), Siemens AG, Slovenské elektrárne, a.s. (Slovakia), State Nuclear Power Automation System Engineering Company (China), and Westinghouse Electric Co.

Hydrocarbon and chemical process customers include numerous large oil refineries and chemical plants such as BP (worldwide), Statoil ASA (Norway), Chevron (USA), Emerson Process Management, Saudi Basic Industries Corporation (Saudi Arabia), Shell Oil Company (worldwide), Savannah River Nuclear Solutions, LLC (USA), Total (Belgium), and Bechtel Hanford National Laboratory (USA).

The following Power Simulation customer has provided more than 10% of the Company's consolidated revenue for the indicated periods:

|

Years ended December 31,

|

|||

|

2014

|

2013

|

||

|

Slovenské elektrárne, a.s.

|

2.3%

|

24.4%

|

|

Marketing and Sales

We market our products and services through a network of direct sales staff, agents and representatives, and strategic alliance partners. Market-oriented business and customer account teams define and implement specific campaigns to pursue opportunities.

We also launched a proactive public relations program, issuing more non-financial press releases aimed at product development and delivery, as well as our role in numerous industry trade shows and technical conferences. We are active across numerous social media platforms to build a stronger presence across all media our clients use to find information about the company.

The Company's ability to support its multi-facility, international and/or multinational clients is facilitated by its network of offices and strategic partners in the U.S. and overseas. In addition to the offices located overseas, the Company's ability to conduct international business is enhanced by its multilingual and multicultural workforce. GSE has strategic relationships with system integrators and agents representing its interests in the Czech Republic, Bulgaria, Japan, Mexico, South Korea, Taiwan, Ukraine and various locations in the Gulf Coast Countries of the Middle East.

Competition

The Power Simulation business encounters intense competition. In the nuclear simulation market, GSE competes directly with firms primarily from Canada, France and Russia, such as L-3 MAPPS Inc., a subsidiary of L-3 Communications (Canada), CORYS T.E.S.S (France) and Western Services Corporation (significant presence in Russia). In the fossil simulation market, the Company competes with smaller companies in the U.S. and overseas. In the process industries the main competition comes from large DCS/Automation companies such as Honeywell and Schneider. Competition for generalized engineering services, particularly those served from our office in the U.K., tend to be very locally oriented.

Hyperspring services include training related products and services as well as staff augmentation solutions. The competition for training related services includes: GP Strategies, The Westwind Group, Professional Training Technologies, and Western Technical Services. The competition for staff augmentation includes: Absolute Consulting, CB&I, Planet Forward, and The Westwind Group.

10

Competitive Advantages

While there is competition in various industry niches, there are few companies in our space that can combine the engineering, simulation and training expertise we now have through the execution of our acquisition strategy. None of our traditional competitors serve the broader performance improvement market.

|

·

|

Unique Combination of Talent. Nobody in our market space brings together the sophistication of simulation technology with the engineering expertise, training expertise and visualization expertise to provide the holistic people and plant performance improvement solutions.

|

|

·

|

Reputation for Customer Satisfaction. As part of its ISO-9000 Quality Program Certification, GSE measures customer satisfaction across numerous factors such as On-Time Delivery, Problem Solving, and Customer Communication. In each category measured we routinely exceed customer expectations.

|

|

·

|

Industry Expertise. GSE is a leading innovator and developer of real-time software with more than 40 years of experience producing high-fidelity, real-time simulators. As a result, the Company has acquired substantial applications expertise in the energy and industrial process industries. The Company employs a highly educated and experienced multinational workforce of over 300 employees, including approximately 180 engineers and scientists. Of the almost 180 engineers, approximately 49% of these engineers and scientists have advanced science and technical degrees in fields such as chemical, mechanical and electrical engineering, applied mathematics and computer sciences, while an additional 33% have master degrees, and another 12% have doctorate degrees in the aforementioned fields.

|

|

·

|

Proprietary Software Tools. GSE has developed a library of proprietary software tools including auto-code generators and system models that substantially facilitate and expedite the design, production and integration, testing and modification of software and systems. These tools are used to automatically generate the computer code and systems models required for specific functions commonly used in simulation applications, thereby enabling it or its customers to develop high-fidelity, real-time software quickly, accurately and at lower costs. The Company has a substantial library of Process-Specific Simulation models and eLearning Modules aimed at the oil and gas, refining and specialty chemicals market.

|

|

·

|

Training Curricula. The Company has developed hundreds of detailed courses and simulator exercise material or specific industrial applications including oil and gas refining, gas-oil production, nuclear and combined cycle gas turbine power plant and desalination.

|

|

·

|

In the area of training and training related products, Hyperspring can now include: state of the art 3D graphics and simulation to enhance our offerings and differentiate us from our competitors. The area of staff augmentation is mostly focused on training and operations support. The senior management of Hyperspring has strong active ties to the industries we serve which allows us to interface with our customers directly in the course of doing business versus having to periodically call on customers. Our proximity allows us a significant competitive advantage in that we can immediately offer solutions and therefore bypass lengthy bid processes.

|

11

Intellectual Property.

The Company depends upon its intellectual property rights in its proprietary technology and information. GSE maintains a portfolio of trademarks (both registered and unregistered), copyrights (both registered and unregistered), and licenses. While such trademarks, copyrights and licenses as a group are of material importance to the Company, it does not consider any one trademark, copyright, or license to be of such importance that the loss or expiration thereof would materially affect the Company. The Company relies upon a combination of trade secrets, copyright, and trademark law, contractual arrangements and technical means to protect its intellectual property rights. GSE distributes its software products under software license agreements that grant customers nonexclusive licenses for the use of its products, which are nontransferable. Use of the licensed software is restricted to designated computers at specified sites, unless the customer obtains a site license of its use of the software. Software and hardware security measures are also employed to prevent unauthorized use of the Company's software, and the licensed software is subject to terms and conditions prohibiting unauthorized reproduction of the software.

The Company does not own any patents. The Company believes that all of the Company's trademarks (especially those that use the phrase "GSE Systems") are valid and will have an unlimited duration as long as they are adequately protected and sufficiently used. The Company's licenses are perpetual in nature and will have an unlimited duration as long as they are adequately protected and the parties adhere to the material terms and conditions.

GSE has six registered U.S. trademarks: GSE Systems®, JTOPMERET®, RELAP5-HD®, D/3®, SABL® and SimExec®. Some of these trademarks have also been registered in foreign countries. The Company also claims trademark rights to BRUS™, ESmart™, GAARDS™, GCONTROL+™, GFLOW+™, GLOGIC+™, GPower+™, Enterprise Data Management, Java Application and Development Environment (JADE)™, OpenSim™, PEGASUS Plant Surveillance and Diagnosis System™, PSA-HD™, RACS™, Sens Base™, SIMON™, SimSuite Power™, SimSuite Pro™, SmartTutor™, THOR™, VPanel ™, Vista PIN™, and Xtreme I/S™.

In addition, the Company maintains federal statutory copyright protection with respect to its software programs and products, has registered copyrights for some of the documentation and manuals related to these programs, and maintains trade secret protection on its software products.

Despite these protections, the Company cannot be sure that it has protected or will be able to protect its intellectual property adequately, that the unauthorized disclosure or use of its intellectual property will be prevented, that others have not or will not develop similar technology independently, or, to the extent it owns any patents in the future, that others have not or will not be able to design around those patents. Furthermore, the laws of certain countries in which the Company's products are sold do not protect its products and intellectual property rights to the same extent as the laws of the United States.

Industries Served.

The following chart illustrates the approximate percentage of the Company's 2014 and 2013 consolidated revenue by industries served:

|

Years ended December 31,

|

|||

|

2014

|

2013

|

||

|

Nuclear power industry

|

57%

|

65%

|

|

|

Fossil fuel power industry

|

22%

|

16%

|

|

|

Process industry

|

14%

|

16%

|

|

|

Training and education industry

|

1%

|

3%

|

|

|

Other

|

6%

|

0%

|

|

|

Total

|

100%

|

100%

|

|

Contract Backlog.

The Company does not reflect an order in backlog until it has received a contract that specifies the terms and milestone delivery dates or other payment terms. As of December 31, 2014, the Company's aggregate contract backlog totaled approximately $48.4 million of which approximately $31.6 million or 65.3% is expected to be converted to revenue by December 31, 2015. As of December 31, 2013, the Company's aggregate contract backlog totaled approximately $38.0 million.

Employees.

As of December 31, 2014, the Company had 335 employees as compared to 235 employees at December 31, 2013.

12

The following are some of the factors that we believe could cause our actual results to differ materially from historical results and from the results contemplated by the forward-looking statements contained in this report and other public statements made by us. Additional risks and uncertainties not presently known to us, or that we currently see as immaterial, may also harm our business. Most of these risks are generally beyond our control. If any of the risks or uncertainties described below, or any such additional risks and uncertainties actually occurs, our business, results of operations and financial condition could be materially and adversely affected. The following information should be read in conjunction with Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operations and the consolidated financial statements and related notes under Item 8 - Financial Statements and Supplementary Data.

Our business is largely dependent on sales to the nuclear power industry. Any disruption in this industry would have a material adverse effect upon our revenue.

In 2014, 57% of our revenue was from customers in the nuclear power industry (65% in 2013). We expect to derive a significant portion of our revenue from customers in the nuclear power industry for the foreseeable future. Our ability to supply nuclear power plant simulators and related products and services is dependent on the continued operation of nuclear power plants and, to a lesser extent, on the construction of new nuclear power plants. A wide range of factors affect the continued operation and construction of nuclear power plants, including the political and regulatory environment, the availability and cost of alternative means of power generation, the occurrence of future nuclear incidents, such as the one which occurred at the Fukushima Daiichi nuclear plant in 2011, and general economic conditions.

Our sales to foreign customers expose us to risks associated with operating internationally.

Sales of products and services to end users outside the United States accounted for approximately 52% of the Company's consolidated revenue in 2014 and 67% of consolidated revenue in 2013. Consequently, our businesses are subject to a variety of risks that are specific to international operations, including the following:

| ¨ | export regulations that could erode profit margins or restrict exports; |

| ¨ | compliance with the U.S. Foreign Corrupt Practices Act and similar non-U.S. regulations; |

| ¨ | the burden and cost of compliance with foreign laws, treaties and technical standards and changes in those regulations; |

| ¨ | contract award and funding delays; |

| ¨ | potential restrictions on transfers of funds; |

| ¨ | potential difficulties in accounts receivable collection; |

| ¨ | currency fluctuations; |

| ¨ | import and export duties and value added taxes; |

| ¨ | transportation delays and interruptions; |

| ¨ | difficulties involving strategic alliances and managing foreign sales agents or representatives; |

| ¨ | uncertainties arising from foreign local business practices and cultural considerations; and |

| ¨ | potential military conflicts and political risks. |

While we have and will continue to adopt measures to reduce the potential impact of losses resulting from the risks of our foreign business, we cannot ensure that such measures will be adequate. The following foreign countries have provided more than 10% of our consolidated revenue for the indicated period:

|

Year Ended December 31,

|

|||

|

2014

|

2013

|

||

|

United Kingdom

|

12%

|

14%

|

|

|

People's Republic of China

|

11%

|

10%

|

|

|

Slovak Republic

|

2%

|

24%

|

|

13

Hyperspring's revenue, results of operations, and cash flows may suffer upon the loss of a significant customer.

We completed the acquisition of Hyperspring, LLC on November 14, 2014. See Note 3 to our Consolidated Financial Statements. For the years ended December 31, 2014 and 2013, the following customers accounted for in excess of 10% of Hyperspring's revenues:

|

Year Ended December 31,

|

|||

|

2014

|

2013

|

||

|

Tennessee Valley Authority

|

62%

|

72%

|

|

|

PSEG Nuclear LLC

|

17%

|

7%

|

|

|

Entergy Corporation

|

11%

|

13%

|

|

Hyperspring's contract for staff augmentation services with Tennessee Valley Authority expires on May 9, 2015 and such contract is expected to be rebid. Hyperspring also has a contract with PSEG Nuclear to provide training support which expires in December 2021. Hyperspring may lose a significant customer if any existing contract with such customer expires without being extended, renewed, renegotiated or is terminated by the customer prior to expiration, to the extent such early termination is permitted by the contract. A number of Hyperspring's other contracts with significant customers are typically subject to expiration during each year and they may lose any of these contracts if we are unable to extend, renew or renegotiate the contracts. The loss of any significant customer would adversely affect Hyperspring's revenue, results of operations, and cash flows.

Our expense levels are based upon our expectations as to future revenue, so we may be unable to adjust spending to compensate for a revenue shortfall. Accordingly, any revenue shortfall would likely have a disproportionate effect on our operating results.

Our revenue was $37.9 million and $47.6 million for the years ended December 31, 2014 and 2013, respectively. Our operating loss was $6.9 million and $10.7 million, for the years ended December 31, 2014 and 2013, respectively. Our operating results have fluctuated in the past and may fluctuate significantly in the future as a result of a variety of factors, including purchasing patterns, timing of new products and enhancements by us and our competitors, and fluctuating global economic conditions. Since our expense levels are based in part on our expectations as to future revenue and includes certain fixed costs, we may be unable to adjust spending in a timely manner to compensate for any revenue shortfall and such revenue shortfalls would likely have a disproportionate adverse effect on our operating results.

14

Our backlog is subject to reduction and cancellation.

Backlog represents products or services that our customers have committed by contract to purchase from us. Our backlog as of December 31, 2014 and 2013 was $48.4 million and $38.0 million, respectively. Our backlog is subject to fluctuations and is not necessarily indicative of future backlog or sales. Moreover, cancellations of purchase orders or reductions of the services requested in existing contracts could substantially and materially reduce our backlog and, consequently, future revenues. Our failure to replace canceled or reduced backlog would have an adverse effect on our operating results.

We are a party to fixed price contracts and will enter into similar contracts in the future, which could result in reduced profits or losses if we are not able to accurately estimate or control costs.

A significant portion of our revenue is attributable to contracts entered into on a fixed price basis, which allows us to benefit from cost savings, but we carry the burden of cost overruns. If our initial estimates are incorrect, or if unanticipated circumstances arise, we could experience cost overruns which would result in reduced profits or even result in losses on these contracts. Our financial condition is dependent upon our ability to maximize our earnings from our contracts. Lower earnings or losses caused by cost overruns could have a negative impact on our financial results.

Under time and materials contracts, we are paid for labor at negotiated hourly billing rates and for certain expenses. Under cost-reimbursable contracts, which are subject to a contract ceiling amount, we are reimbursed for allowable costs and paid a fee, which may be fixed or performance based. However, if costs exceed the contract ceiling or are not allowable under the provisions of the contract or applicable regulations, we may not be able to obtain reimbursement for all such costs.

Our inability to successfully estimate and manage costs on each of these contract types may materially and adversely affect our financial condition.

Our Simulation business is dependent on product innovation and research and development, which costs are incurred prior to revenue for new products and improvements.

We believe that our success will depend in large part on our ability to maintain and enhance our current product line, develop new products, maintain technological competitiveness and meet an expanding range of customer needs. Our product development activities are aimed at the development and expansion of our library of software modeling tools, the improvement of our display systems and workstation technologies, and the advancement and upgrading of our simulation technology. The life cycles for software modeling tools, graphical user interfaces, and simulation technology are variable and largely determined by competitive pressures. Consequently, we will need to continue to make significant investments in research and development to enhance and expand our capabilities in these areas and to maintain our competitive advantage.

We use derivative instruments in the normal course of our business which could result in financial losses that negatively impact our net income.

We periodically enter into forward foreign exchange contracts to manage market risks associated with the fluctuations in foreign currency exchange rates on foreign-denominated trade receivables. We could recognize financial losses as a result of volatility in the market values of these contracts or if a counterparty fails to perform. We attempt to minimize credit exposure by limiting counterparties to internationally recognized financial institutions.

15

We issue performance, advance payment, and bid bonds in the normal course of our business which could result in financial losses that negatively impact our net income.

We are often required to issue performance bonds to our customers as a normal part of our business activities. Our customers may have the ability to draw upon these performance bonds in the event we fail to cure a material breach of the contract within 30 days of receiving notice from the customer regarding the nature of the breach. As of December 31, 2014, we had issued advance payment and performance bonds on eleven contracts totaling $4.2 million, all of which have been cash collateralized except one bond totaling $48,000; the largest of these performance bonds was for $1.6 million. Although we expect no material breaches to occur on these contracts, if such a breach were to occur and we failed to cure such breach, we could incur a loss of up to $4.2 million.

We rely upon our intellectual property rights for the success of our business; however, the steps we have taken to protect our intellectual property may be inadequate.

Although we believe that factors such as the technological and creative skills of our personnel, new product developments, frequent product enhancements and reliable product maintenance are important to establishing and maintaining a technological leadership position, our business depends, in part, on our intellectual property rights in our proprietary technology and information. We rely upon a combination of trade secret, copyright, and trademark law, contractual arrangements and technical means to protect our intellectual property rights. We enter into confidentiality agreements with our employees, consultants, joint venture and alliance partners, customers and other third parties that are granted access to our proprietary information, and limit access to and distribution of our proprietary information. There can be no assurance, however, that we have protected or will be able to protect our proprietary technology and information adequately, that the unauthorized disclosure or use of our proprietary information will be prevented, that others have not or will not develop similar technology or information independently, or, to the extent we own any patents in the future, that others have not or will not be able to design around those future patents. Furthermore, the laws of certain countries in which our products are sold do not protect our products and intellectual property rights to the same extent as the laws of the United States.

The industries in which we operate are highly competitive. This competition may prevent us from raising prices at the same pace at which our costs increase.

Our businesses operate in highly competitive environments with both domestic and foreign competitors, many of whom have substantially greater financial, marketing and other resources than we do. The principal factors affecting competition include price, technological proficiency, ease of system configuration, product reliability, applications expertise, engineering support, local presence and financial stability. We believe competition in the simulation fields may further intensify in the future as a result of advances in technology, consolidations and/or strategic alliances among competitors, increased costs required to develop new technology and the increasing importance of software content in systems and products. As our business has a significant international component, changes in the value of the dollar could adversely affect our ability to compete internationally.

16

We may encounter difficulties in effectively integrating acquired businesses.

As part of our business strategy, we have acquired companies with compatible or related products. These and any future acquisitions we make will be accompanied by the risks commonly encountered in acquisitions of companies, which include, among other things:

| ¨ | potential exposure to unknown liabilities of the acquired companies; |

| ¨ | higher than anticipated acquisition costs and expenses; |

| ¨ | difficulty and expense of assimilating the operations and personnel of the companies, especially if the acquired operations are geographically distant; |

| ¨ | potential disruption of our ongoing business and diversion of management time and attention; |

| ¨ | failure to maximize our financial and strategic position by the successful incorporation of acquired technology; |

| ¨ | difficulties in adopting and maintaining uniform standards, controls, procedures and policies; |

| ¨ | loss of key employees and customers as a result of changes in management; and |

| ¨ | possible dilution to our shareholders. |

We may not be successful in overcoming these risks or any other problems encountered in connection with any of our acquisitions.

A failure to attract and retain technical personnel could reduce our revenue and our operational effectiveness.

There is a continuing demand for qualified technical personnel. We believe that our future growth and success will depend upon our ability to attract, train and retain such personnel. Our design and development efforts depend on hiring and retaining qualified technical personnel. An inability to attract or maintain a sufficient number of technical personnel could have a material adverse effect on our contract performance or on our ability to capitalize on market opportunities.

The nuclear power industry, our largest customer group, is associated with a number of hazards which could create significant liabilities.

Our business could expose us to third party claims with respect to product, environmental and other similar liabilities. Although we have sought protection from these potential liabilities through a variety of legal and contractual provisions as well as through liability insurance, the effectiveness of such protections has not been fully tested. Certain of our products and services are used by the nuclear power industry primarily in operator training. Although our contracts for such products and services typically contain provisions designed to protect us from potential liabilities associated with such use, there can be no assurance that we would not be materially adversely affected by claims or actions which may potentially arise.

17

Cyber security incidents could disrupt business operations, result in the loss of critical and confidential information, and adversely impact our reputation and results of operations.

Global cyber security threats can range from uncoordinated individual attempts to gain unauthorized access to our information technology (IT) systems to sophisticated and targeted measures known as advanced persistent threats. While we employ comprehensive measures to prevent, detect, address and mitigate these threats (including access controls, data encryption, vulnerability assessments, continuous monitoring of our IT networks and systems and maintenance of backup and protective systems), cyber security incidents, depending on their nature and scope, could potentially result in the misappropriation, destruction, corruption or unavailability of critical data and confidential or proprietary information (our own or that of third parties) and the disruption of business operations. The potential consequences of a material cyber security incident include reputational damage, litigation with third parties, diminution in the value of our investment in research, development and engineering, and increased cyber security protection and remediation costs, which in turn could adversely affect our competitiveness and results of operations.

Third-party claims that we allegedly infringe the intellectual property rights of others may be costly to defend or settle and could damage our business.

We cannot be certain that our software and services do not infringe issued patents, copyrights, trademarks or other intellectual property rights of third parties. We may be subject to legal proceedings and claims from time to time, including claims of alleged infringement of intellectual property rights of third parties by us or our licensees concerning their use of our software products and integration technologies and services. Third parties may bring claims of infringement against us. Because our software is integrated with our customers' networks and business processes, as well as other software applications, third parties may bring claims of infringement against us, as well as our customers and other software suppliers, if the cause of the alleged infringement cannot easily be determined.

Claims of alleged infringement may have a material adverse effect on our business and may discourage potential customers from doing business with us on acceptable terms, if at all. Defending against claims of infringement may be time-consuming and may result in substantial costs and diversion of resources, including our management's attention to our business. Furthermore, a party making an infringement claim could secure a judgment that requires us to pay substantial damages. A judgment could also include an injunction or other court order that could prevent us from selling our software or require that we re-engineer some or all of our products. Claims of intellectual property infringement also might require us to enter costly royalty or license agreements. We may be unable to obtain royalty or license agreements on terms acceptable to us or at all. Our business, operating results and financial condition could be harmed significantly if any of these events occurred, and the price of our common stock could be adversely affected. In addition, we have agreed, and may agree in the future, to indemnify certain of our customers against claims that our software infringes upon the intellectual property rights of others. Although we carry general liability insurance, our current insurance coverage may not apply to, and likely would not protect us from, liability that may be imposed under any of the types of claims described above.

We are subject to a wide variety of laws and regulations.

Our businesses are subject to regulation by U.S. federal and state laws and foreign laws, regulations and policies. Changes to laws or regulations may require us to modify our business objectives if existing practices become more restricted, subject to escalating costs or prohibited outright. Particular risks include regulatory risks arising from federal laws, such as laws regarding export of sensitive technologies or technical information. Our business and the industries in which we operate are also at times being reviewed or investigated by regulators, which could lead to enforcement actions, fines and penalties or the assertion of private litigation claims and damages.

18

Our stockholder protection rights agreement and classified Board of Directors could deter acquisition proposals and make it difficult for a third party to acquire control of the Company, which could have a negative effect on the price of our Common Stock.

We have a stockholder protection rights agreement and a classified Board of Directors, which could discourage potential acquisition proposals and could delay or prevent a change in control. This deterrent could adversely affect the price of our Common Stock and make it difficult to affect a change in the composition of the Board of Directors or a change in management.

The price of our common stock is highly volatile and could decline regardless of our operating performance.

The market price of our common stock could fluctuate in response to, among other things:

| ¨ | changes in economic and general market conditions; |

| ¨ | changes in the outlook and financial condition of certain of our significant customers and industries in which we have a concentration of business; |

| ¨ | changes in financial estimates, treatment of our tax assets or liabilities or investment recommendations by securities analysts following our business; |

| ¨ | changes in accounting standards, policies, guidance or interpretations or principles; |

| ¨ | sales of common stock by our directors, officers and significant stockholders; |

| ¨ | our failure to achieve operating results consistent with securities analysts' projections; and |

| ¨ | the operating and stock price performance of competitors. |

These factors might adversely affect the trading price of our common stock and prevent you from selling your common stock at or above the price at which you purchased it. In addition, in recent periods, the stock market has experienced significant price and volume fluctuations. This volatility has had a significant impact on the market price of securities issued by many companies, including ours and others in our industry. These changes can occur without regard to the operating performance of the affected companies. As a result, the price of our common stock could fluctuate based upon factors that have little or nothing to do with our company, and these fluctuations could materially reduce our share price.

A sustained decline in the price of our common stock or weaker than forecasted operating results could result in write-downs of goodwill and capitalized software.

In conjunction with business acquisitions, we record goodwill at fair value and review its fair value for impairment annually as of November 30, or on an interim basis if impairment indicators are present, such as a significant reduction in our market capitalization, significant declines in operating performance or disruptions to the business that could reduce our future cash flow. On November 14, 2014, we recorded $5.6 million of goodwill related to our acquisition of Hyperspring, LLC. We can provide no assurance that we will not have an impairment charge in future periods as the result of changing conditions. In 2013, the Company incurred a goodwill impairment of $4.5 million. See Note 4 to our Consolidated Financial Statements for information regarding our goodwill.

Certain computer software development costs are capitalized in the accompanying consolidated balance sheets. Capitalization of computer software development costs begins upon the establishment of technological feasibility. Capitalization ceases and amortization of capitalized costs begins when the software product is commercially available for general release to customers. Amortization of capitalized computer software development costs is included in cost of revenue and is determined using the straight-line method over the remaining estimated economic life of the product, typically three years. On an annual basis, and more frequently as conditions indicate, we assess the recoverability of the unamortized software development costs by estimating the net undiscounted cash flows expected to be generated by the sale of the product. If the undiscounted cash flows are not sufficient to recover the unamortized software costs we will write-down the investment to its estimated fair value based on the future undiscounted cash flows. The excess of any unamortized computer software costs over the related net realizable value is written down and charged to operations.

Based upon indicators of impairment in the second quarter of 2013, which included a substantial decrease in the Company's market capitalization, we performed an interim goodwill impairment test as of June 30, 2013. In conjunction with the goodwill impairment test, we analyzed the net realizable value of our capitalized software development costs and, based upon the results of this analysis, took a $2.2 million charge to earnings for a write-down of the capitalized software development costs. After the write-down, we had $769,000 of capitalized software remaining on the balance sheet at June 30, 2013. As of December 31, 2014 we have $1.4 million of capitalized software development costs recorded on the balance sheet. See Note 8 to our Consolidated Financial Statements for information regarding our capitalized software development costs.

19

None.

The Company is headquartered in a facility in Sykesville, Maryland (approximately 43,000 square feet). The lease for this facility expires on June 30, 2023. The Company has subleased approximately 1,000 square feet of the facility.

In addition, the Company leases office space domestically in St. Marys, Georgia, Huntsville, Alabama, Madison, New Jersey, Cary, North Carolina and Tarrytown, New York and internationally in Beijing, China, Chennai, India, Nyköping, Sweden and Stockton-On-Tees, England. The Company leases these facilities for terms ending between 2015 and 2023.

The Company and its subsidiaries are from time to time involved in ordinary routine litigation incidental to the conduct of its business. The Company and its subsidiaries are not a party to, and its property is not the subject of, any material pending legal proceedings that, in the opinion of management, are likely to have a material adverse effect on the Company's business, financial condition or results of operations.

Not applicable.

20

PART II

| ITEM 5. | MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES. |

The Company's common stock is listed on the NYSE MKT Stock Exchange, where it trades under the symbol "GVP". The following table sets forth, for the periods indicated, the high and low sale prices for the Company's common stock reported by the NYSE MKT Stock Exchange for each full quarterly period within the two most recent fiscal years:

|

2014

|

||||||||

|

Quarter

|

High

|

Low

|

||||||

|

First

|

$

|

1.90

|

$

|

1.62

|

||||

|

Second

|

$

|

1.81

|

$

|

1.65

|

||||

|

Third

|

$

|

1.78

|

$

|

1.54

|

||||

|

Fourth

|

$

|

1.65

|

$

|

1.20

|

||||

|

2013

|

||||||||

|

Quarter

|

High

|

Low

|

||||||

|

First

|

$

|

2.55

|

$

|

1.97

|

||||

|

Second

|

$

|

2.00

|

$

|

1.49

|

||||

|

Third

|

$

|

1.85

|

$

|

1.40

|

||||

|

Fourth

|

$

|

1.73

|

$

|

1.54

|

||||

21

The following table sets forth the equity compensation plan information for the year ended December 31, 2014:

|

Plan category

|

Number of Securities to

be Issued Upon Exercise of

Outstanding Options,

Warrants and Rights

(a)

|

Weighted Average Exercise Price of

Outstanding Options, Warrants and Rights

(b)

|

Number of Securities Remaining

Available for Future Issuance Under Equity Compensation Plans

(Excluding Securities Reflected in Column (a))

(c)

|

|||||||||

|

Equity compensation plans approved by security holders

|

2,708,273

|

$

|

3.12

|

1,147,967

|

||||||||

|

Equity compensation plans not approved by security holders

|

--

|

$

|

--

|

--

|

||||||||

|

Total

|

2,708,273

|

$

|

3.12

|

1,147,967

|

||||||||

There were approximately 910 holders of record of the common stock as of December 31, 2014. The Company has never declared or paid a cash dividend on its common stock. The Company currently intends to retain future earnings to finance the growth and development of its business and, therefore, does not anticipate paying any cash dividends in the foreseeable future on its common stock.

The Company believes factors such as quarterly fluctuations in results of operations and announcements of new products by the Company or by its competitors may cause the market price of the common stock to fluctuate, perhaps significantly. In addition, in recent years the stock market in general, and the shares of technology companies in particular, have experienced extreme price fluctuations. The Company's common stock has also experienced a relatively low trading volume, making it further susceptible to extreme price fluctuations. These factors may adversely affect the market price of the Company's common stock.

Issuer Purchases of Equity Securities

On March 21, 2011, the Board of Directors authorized the purchase of up to $3.0 million of the Company's common stock in accordance with the safe harbor provisions of Rule 10b-18 of the Securities Exchange Act of 1934. During the year ended December 31, 2013, the Company repurchased 494,424 shares at an aggregate cost of $0.8 million. The Company completed the share repurchase program in October 2013 and thus did not repurchase shares during 2014.

22

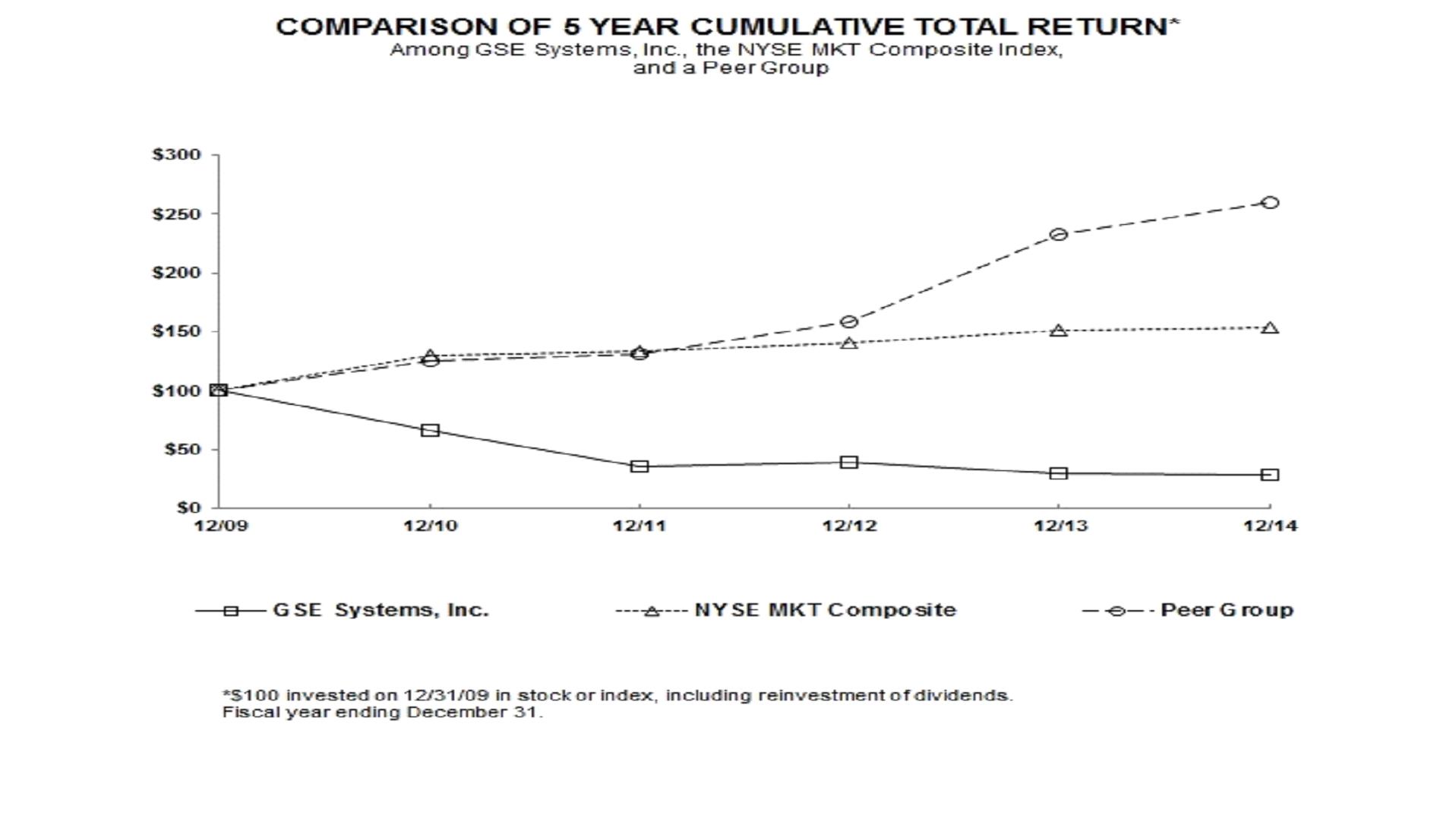

Performance Graph

The following graph compares the Company's cumulative total shareholder return since December 31, 2009 through December 31, 2014 with that of the NYSE MKT Composite Index and a peer group index. The Peer Group consists of companies selected on a line-of-business basis and includes Aspen Technology, Inc., L-3 Communications Holdings and Honeywell International. The graph assumes an initial investment of $100 on December 31, 2009 in the Company's common stock and each index. There were no dividends declared or paid by the Company during the five year period. The Company has never paid a dividend on its common stock. The indices are re-weighted daily, using the market capitalization on the previous tracking day. The comparisons shown in the graph below are based upon historical data. The stock price performance shown in the graph below is not necessarily indicative of, or intended to forecast, the potential future performance of the Company's common stock. The graph was prepared for the Company by Research Data Group, Inc.

|

Year ended December 31,

|

|||||||||||

|

2009

|

2010

|

2011

|

2012

|

2013

|

2014

|

||||||

|

GSE Systems, Inc.

|

100.00

|

66.06

|

35.58

|

39.42

|

29.20

|

29.01

|

|||||

|

NYSE MKT Composite

|

100.00

|

129.56

|

133.75

|

140.87

|

150.79

|

153.24

|

|||||

|

Peer Group

|

100.00

|

125.21

|

130.64

|

158.84

|

233.06

|

259.37

|

|||||

23

Historical consolidated results of operations and balance sheet data presented below have been derived from the historical financial statements of the Company. This information should be read in connection with the Company's consolidated financial statements.

|

(in thousands, except per share data)

|

Years ended December 31,

|

|||||||||||||||||||

|

2014 (1)

|

2013

|

2012

|

2011 (2)

|

2010 (3)

|

||||||||||||||||

|

Consolidated Statements of Operations:

|

||||||||||||||||||||

|

Contract revenue

|

$

|

37,930

|

$

|

47,562

|

$

|

52,246

|

$

|

51,126

|

$

|

47,213

|

||||||||||

|

Cost of revenue

|

26,551

|

34,981

|

34,509

|

34,781

|

36,081

|

|||||||||||||||

|

Write-down of capitalized software development costs (4)

|

-

|

2,174

|

-

|

-

|

-

|

|||||||||||||||

|

Gross profit

|

11,379

|

10,407