Attached files

| file | filename |

|---|---|

| EX-31.1 - EX-31.1 - InfraREIT, Inc. | d889218dex311.htm |

| EX-31.2 - EX-31.2 - InfraREIT, Inc. | d889218dex312.htm |

| EX-10.9 - EX-10.9 - InfraREIT, Inc. | d889218dex109.htm |

| EX-32.1 - EX-32.1 - InfraREIT, Inc. | d889218dex321.htm |

| EX-99.1 - EX-99.1 - InfraREIT, Inc. | d889218dex991.htm |

| EX-21.1 - EX-21.1 - InfraREIT, Inc. | d889218dex211.htm |

| EX-32.2 - EX-32.2 - InfraREIT, Inc. | d889218dex322.htm |

| EX-10.7 - EX-10.7 - InfraREIT, Inc. | d889218dex107.htm |

| EX-10.49 - EX-10.49 - InfraREIT, Inc. | d889218dex1049.htm |

| EX-10.15 - EX-10.15 - InfraREIT, Inc. | d889218dex1015.htm |

| EX-10.13 - EX-10.13 - InfraREIT, Inc. | d889218dex1013.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-36822

InfraREIT, Inc.

(Exact name of Registrant as specified in its charter)

| Maryland | 75-2952822 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification Number) | |

| 1807 Ross Avenue, 4th Floor, Dallas, Texas |

75201 | |

| (Address of Principal Executive Offices) | (Zip Code) | |

(214) 855-6700

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Class |

Name of Each Exchange on Which Registered | |

| Common Stock, $0.01 par value per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ¨ No x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large Accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The registrant completed the initial public offering of its common stock on February 4, 2015. Accordingly, there was no public market for the registrant’s common stock as of June 30, 2014, the last business day of the registrant’s most recently completed second fiscal quarter. The aggregate market value of the common stock owned by non-affiliates on March 12, 2015 was $611,647,888, calculated by reference to the closing price of $26.42 per share for the registrant’s common stock on the New York Stock Exchange on such date. For purposes of calculating this amount only, all directors, executive officers and beneficial owners of 5% or more of the outstanding common stock on March 12, 2015 have been deemed to be affiliates.

As of March 12, 2015, 43,565,495 shares of common stock were issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE: None

Table of Contents

InfraREIT, Inc.

| Page | ||||||

| PART I | ||||||

| Glossary of Terms | 3 | |||||

| Forward-Looking Statements | 5 | |||||

| Explanatory Note | 6 | |||||

| Item 1. |

6 | |||||

| Item 1A. |

27 | |||||

| Item 1B. |

52 | |||||

| Item 2. |

52 | |||||

| Item 3. |

52 | |||||

| Item 4. |

52 | |||||

| Item 5. |

53 | |||||

| Item 6. |

55 | |||||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

58 | ||||

| Item 7A. |

74 | |||||

| Item 8. |

74 | |||||

| Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

74 | ||||

| Item 9A. |

75 | |||||

| Item 9B. |

75 | |||||

| Item 10. |

75 | |||||

| Item 11. |

83 | |||||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters |

88 | ||||

| Item 13. |

Certain Relationships and Related Transactions and Director Independence |

90 | ||||

| Item 14. |

97 | |||||

| Item 15. |

99 | |||||

| 105 | ||||||

2

Table of Contents

This glossary highlights some of the industry terms that we use in this Annual Report on Form 10-K and is not a complete list of all of the defined terms used herein.

| Abbreviation |

Term | |

| AFUDC |

allowance for funds used during construction | |

| CREZ |

competitive renewable energy zones, as defined by a 2005 Texas law establishing the Texas renewable energy program | |

| CWIP |

construction work in progress | |

| DC Tie |

high-voltage direct current interconnection necessary to provide for electricity flow between asynchronous electric grids in North America | |

| DCRF filing |

a distribution cost recovery factor filing with the Public Utility Commission of Texas that a distribution service provider is permitted to make to update its distribution tariffs to reflect recent capital expenditures, among other matters | |

| Distribution |

that portion of a power delivery network consisting of an interconnected group of electric distribution lines, towers, poles, substations, transformers and associated assets over which electric power is distributed from points within the transmission network to end use consumers | |

| DSP |

a distribution service provider, i.e., a utility operating within the Electric Reliability Council of Texas territory that owns and operates electric distribution facilities, or other participants in the Electric Reliability Council of Texas territory that collect and remit payments on behalf of a distribution service provider | |

| electric utilities |

DSPs, transmission service providers, transmission and distribution service providers, municipalities, cooperatives and others defined as Electric Utilities by the Public Utility Commission of Texas | |

| ERCOT |

Electric Reliability Council of Texas | |

| ERCOT 4CP |

the average of ERCOT coincident peak demand for the months of June, July, August and September, excluding the portion of coincident peak demand attributable to wholesale storage load (during 2013, ERCOT 4CP was approximately 65 gigawatts) | |

| FERC |

Federal Energy Regulatory Commission | |

| Footprint Projects |

transmission or distribution projects primarily situated within our distribution service territory, or that physically hang from its existing transmission assets, such as the addition of another circuit to our existing transmission lines, or that are physically located within one of our substations; Footprint Projects do not include the addition of a new substation on our existing transmission lines or generation interconnects to our existing transmission lines, unless the addition or interconnection occurred within our distribution service territory | |

| kV |

kilovolt | |

| kW |

kilowatt | |

| kWh |

kilowatt-hour | |

3

Table of Contents

| Abbreviation |

Term | |

| MW | megawatts | |

| PUCT | Public Utility Commission of Texas | |

| rate base | calculated as our gross electric plant in service under generally accepted accounting principles, which is the aggregate amount of our total cash expenditures used to construct such assets plus AFUDC, less accumulated depreciation, and adjusted for accumulated deferred income taxes | |

| REP | retail electric provider, which are the companies that sell electricity to Texas customers | |

| revenue requirement | a transmission and distribution service provider’s revenue requirement is equal to its targeted total costs, including operating and maintenance costs, return on rate base and taxes | |

| ROFO Projects | identified projects that are being developed by Hunt Consolidated, Inc. and its affiliates with respect to which we have a right of first offer | |

| service territory | a designated area in which a utility is required or has the right to supply electric service to ultimate customers under a regulated utility structure | |

| TCOS filing | an interim transmission cost of service filing with the PUCT that a transmission service provider is permitted to make up to twice per year to update its transmission cost of service, and therefore its transmission tariff, to reflect recent capital expenditures, among other matters. An interim TCOS filing establishes transmission cost of service until the next rate case or interim TCOS filing | |

| T&D | electric transmission and distribution | |

| T&D assets | rate-regulated electric transmission and distribution assets such as power lines, substations, transmission towers, distribution poles, transformers and related property and assets | |

| TDSP | transmission and distribution service provider, i.e. a utility operating within the ERCOT territory that owns and operates both electric transmission facilities and electric distribution facilities | |

| transmission | that portion of a power delivery network consisting of an interconnected group of electric transmission lines, towers, poles, switchyards, substations, transformers and associated assets over which electric power is transmitted between points of supply or generation and distribution | |

| TSP | a transmission service provider, i.e., a utility operating within the ERCOT territory that owns and operates electric transmission facilities | |

4

Table of Contents

Some of the information in this Annual Report on Form 10-K may contain forward-looking statements. Forward-looking statements give InfraREIT, Inc.’s (“we” or the “Company”) current expectations, contain projections of results of operations or financial condition or forecasts of future events. Words such as “could,” “will,” “may,” “assume,” “forecast,” “position,” “predict,” “strategy,” “expect,” “intend,” “plan,” “estimate,” “anticipate,” “believe,” “project,” “budget,” “potential” or “continue” and similar expressions are used to identify forward-looking statements. Without limiting the generality of the foregoing, forward-looking statements contained in this document include our expectations regarding our strategies, objectives, growth and anticipated financial and operational performance, including guidance regarding our capital expenditures and rate base, expected lease payments, infrastructure programs, estimated cash flow projections, estimated distributions to our stockholders and tax position. Forward-looking statements can be affected by assumptions used or by known or unknown risks or uncertainties. Consequently, no forward-looking statements can be guaranteed.

A forward-looking statement may include a statement of the assumptions or bases underlying the forward-looking statement. We believe that we have chosen these assumptions or bases in good faith and that they are reasonable. However, when considering these forward-looking statements, you should keep in mind the risk factors and other cautionary statements in this document. Actual results may vary materially. You are cautioned not to place undue reliance on any forward-looking statements. You should also understand that it is not possible to predict or identify all such factors and should not consider the following list to be a complete statement of all potential risks and uncertainties. Factors that could cause our actual results to differ materially from the results contemplated by such forward-looking statements include:

| • | risks that the Footprint Projects we expect will not materialize for a variety of reasons, including as a result of reductions in oil and gas drilling and related activity in the Permian Basin due to lower oil and gas prices relative to our current expectations; |

| • | our ability to acquire ROFO Projects or other T&D assets from Hunt Consolidated, Inc. and its subsidiaries on terms that are accretive to our stockholders; |

| • | our current reliance on our tenant for all of our revenues and, as a result, our dependency on our tenant’s solvency and financial and operating performance; |

| • | defaults on or non-renewal or early termination of leases by our tenant; |

| • | risks related to future lease negotiations; |

| • | changes in the regulated rates the tenants of our assets may charge their customers; |

| • | the completion of our capital expenditure projects on time and on budget; |

| • | competitive conditions for the development and acquisition of T&D assets; |

| • | insufficient cash available to meet distribution requirements; |

| • | the price and availability of debt and equity financing; |

| • | increased interest rates; |

| • | changes in the availability and cost of capital; |

| • | our level of indebtedness or debt service obligations; |

| • | changes in governmental policies or regulations with respect to our permitted capital structure, acquisitions and dispositions of assets, recovery of investments and our authorized rate of return; |

| • | weather conditions and other natural phenomena; |

| • | the effects of existing and future tax and other laws and governmental regulations; |

| • | our failure to qualify or maintain our status as a real estate investment trust (REIT); |

| • | availability of qualified personnel; |

| • | the termination of our management agreement or development agreement or the loss of the services of Hunt Utility Services, LLC or the loss of access to the development function of Hunt Transmission Services, L.L.C.; |

| • | the effects of future litigation; |

| • | changes in the tax laws applicable to REITs; |

| • | adverse economic developments in the electric power industry; |

5

Table of Contents

| • | changes in general business and economic conditions, particularly in Texas; and |

| • | certain factors discussed elsewhere in this Form 10-K. |

Forward-looking statements speak only as of the date on which they are made. While we may update these statements from time to time, we are not required to do so other than pursuant to applicable laws. For a further discussion of these and other factors that could impact our future results and performance, see Item 1A., Risk Factors.

The registrant is a Maryland corporation named InfraREIT, Inc. Before our initial public offering (IPO), which closed on February 4, 2015, substantially all of our business and assets were owned, directly or indirectly, by InfraREIT, L.L.C., a Delaware limited liability company. On February 4, 2015, immediately following the consummation of our IPO, InfraREIT, L.L.C. was merged with and into InfraREIT, Inc. (Merger), with InfraREIT, Inc. as the surviving company. As used in this Annual Report on Form 10-K, unless the context requires otherwise or except as otherwise noted, the words “Company,” “we,” “our” and “us” refer to InfraREIT, L.L.C. or InfraREIT, Inc. after giving effect to the Merger, as the context requires, together with its subsidiaries, including InfraREIT Partners, LP (Operating Partnership), a Delaware limited partnership. “InfraREIT” when used in a historical context refers to InfraREIT, L.L.C. and when used in the present tense or prospectively refers to InfraREIT, Inc. References to our “pre-IPO investors” refer to the investors in InfraREIT, L.L.C. and/or our Operating Partnership, as the context requires, prior to the consummation of our IPO and Merger. Hunt Consolidated, Inc. (HCI) and its subsidiaries (collectively, Hunt), includes Hunt Utility Services, LLC (Hunt Manager), Hunt-InfraREIT, L.L.C. (Hunt-InfraREIT) and Hunt Transmission Services, L.L.C. (Hunt Developer). References to the InfraREIT, L.L.C. board of directors refer to the board of directors of InfraREIT, L.L.C. prior to the Merger, which included five voting members appointed by Hunt and each of the founding investors (as defined below) and four non-voting members. References to “pre-IPO board of directors” and similar terms refer to our board of directors prior to the close of business on January 29, 2015, at which time our board of directors was comprised of W. Kirk Baker, David A. Campbell and Hunter L. Hunt, each of whom is a member of our current board of directors. All other references to our “board of directors,” our “board” or our “directors” refer to the current board of directors of InfraREIT, Inc., the composition of which is described in Item 10, Directors, Executive Officers and Corporate Governance in this Annual Report on Form 10-K. Our tenant is Sharyland Utilities, L.P. (Sharyland). Unless otherwise indicated or the context requires, all information in this Annual Report on Form 10-K gives effect to a 1 for 0.938550 reverse split of the shares of InfraREIT, L.L.C. and a concurrent 1 for 0.938550 reverse split of the units representing limited partnership interests in our Operating Partnership, which we effected on January 29, 2015.

| Item 1. | Business |

Company Overview

We are an externally managed REIT that owns T&D assets in Texas. We believe we are well positioned to take advantage of favorable trends in the T&D sector, including the replacement of aging assets and the construction of new assets to address growing energy demand. We believe our attractive REIT structure and focus on Texas and the southwestern United States, where we can leverage a proven track record of identifying, developing, constructing and acquiring critical infrastructure assets, provide us with a significant competitive advantage to execute our growth strategy.

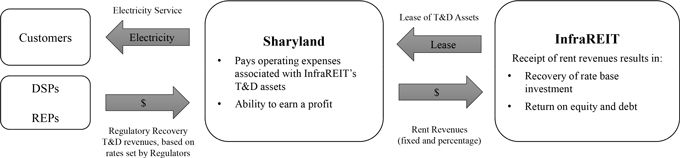

We lease our T&D assets to Sharyland, a Texas based regulated electric utility, pursuant to leases that require Sharyland to make lease payments to us when our assets are placed in service. To support these lease payments, Sharyland delivers electric service and collects revenues directly from REPs and DSPs, which pay rates approved by the PUCT.

We have grown rapidly over the last several years, with our rate base increasing from approximately $60 million as of December 31, 2009 to approximately $1.1 billion as of December 31, 2014. We expect to grow our rate base in the future through organic growth, as well as through acquisitions of T&D assets, including ROFO Projects, from Hunt and Sharyland, who originated and founded our business, and from third parties.

Our business originated in the late 1990s when members of the Hunt family founded Sharyland, the first investor owned utility created in the United States since the 1960s. In 2007, we obtained a private letter ruling from the Internal Revenue Service (IRS) confirming that our T&D assets could constitute real estate assets under applicable REIT rules. In 2008, the PUCT approved a restructuring that allowed us to utilize our REIT structure. In 2010, InfraREIT was formed as a REIT and, as part of that transaction, Hunt contributed assets into InfraREIT and obtained equity commitments from the following institutional investors (collectively, founding investors): Marubeni Corporation, John Hancock Life Insurance Company (U.S.A.), OpTrust Infrastructure N.A. Inc. and Teachers Insurance and Annuity Association of America. InfraREIT, Inc. was formed as a Delaware corporation in 2001, converted into a Maryland corporation on September 29, 2014 and acquired the general partner interest in our Operating Partnership upon the closing of the Merger on February 4, 2015.

6

Table of Contents

We intend to distribute substantially all of our cash available for distribution, less prudent reserves, through regular quarterly cash dividends. Our initial quarterly dividend rate is $0.225 per share, or $0.90 per share on an annualized basis. On March 6, 2015, our board of directors declared a dividend of $0.14 per share of common stock, which represents a pro-rated quarterly dividend of $0.225 per share, calculated from the closing date of our IPO on February 4, 2015 through March 31, 2015. We believe that as we grow our rate base we will also be able to increase our cash available for distribution and, as a result, increase our distribution per share. Our ability to grow our rate base, cash available for distribution and distributions per share is subject to a number of factors and other risks described under Item 1A., Risk Factors.

Our principal executive offices are located at 1807 Ross Avenue, 4th Floor, Dallas, Texas 75201, and our telephone number is (214) 855-6700. We maintain a website at www.infrareitinc.com. The information contained on our website or that can be accessed through our website does not constitute part of this Annual Report on Form 10-K. A print copy of this Annual Report on Form 10-K will be provided without charge upon written request to Investor Relations at our address above. A direct link to our filings with the Securities and Exchange Commission (SEC) is available on our website under the Investor Relations tab. Also available on our website are copies of our Corporate Governance Guidelines; Audit Committee Charter; Compensation, Nominating and Corporate Governance Committee Charter; Conflicts Committee Charter; and Code of Business Conduct and Ethics, all of which will be provided without charge upon written request to Investor Relations at the above address. Our Code of Business Conduct and Ethics applies to all of our officers and directors, including our principal executive officer, principal financial officer and principal accounting officer as well as employees of Hunt Manager. Our common stock is traded on the New York Stock Exchange under the trading symbol “HIFR.”

Our T&D Assets

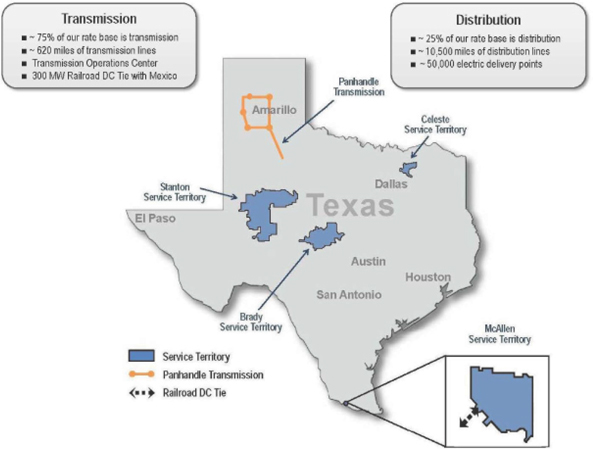

Our T&D assets are located throughout Texas, including the Texas Panhandle near Amarillo, the Permian Basin in and around Stanton, Central Texas around Brady, Northeast Texas in and around Celeste and South Texas near McAllen. Our T&D assets consist of over 50,000 electricity delivery points, approximately 620 miles of transmission lines, approximately 10,500 miles of distribution lines, 35 substations and a 300 MW high-voltage DC Tie between Texas and Mexico, which we refer to as the Railroad DC Tie. The following map shows the location and breakdown of our T&D assets:

7

Table of Contents

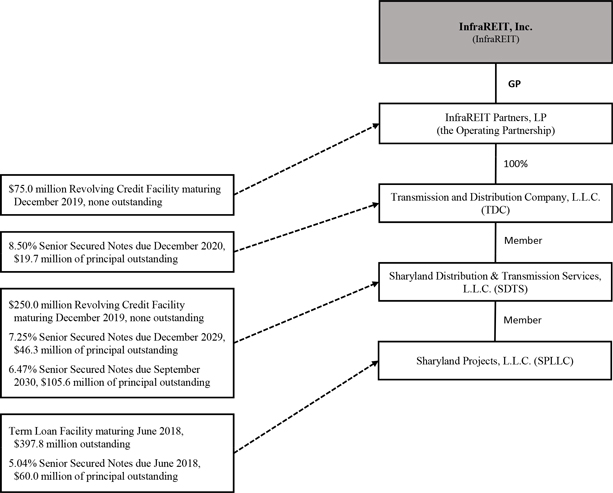

Our T&D assets are owned by our subsidiary Sharyland Distribution and Transmission Services, L.L.C. (SDTS) and its wholly-owned subsidiaries, Sharyland Projects, L.L.C. (SPLLC) and SDTS FERC, L.L.C. (SDTS FERC). Substantially all of our T&D assets are security under our SDTS revolving credit facility and SDTS senior secured notes. Our Panhandle transmission assets constructed pursuant to the CREZ project are security under a separate CREZ project finance loan we have with a consortium of banks. For more information on our revolving credit facility, senior secured notes and CREZ project finance loan, see the caption Credit Arrangements under Liquidity and Capital Resources in Item 7., Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following table is a summary description of our T&D assets as of December 31, 2014:

| Asset Name |

Owner/Landlord |

Location of Assets |

Description of Assets | |||

| Panhandle Assets |

SPLLC | Texas Panhandle | Approximately 300 miles of 345 kV transmission lines and 4 designated collection stations | |||

| Stanton/Brady/Celeste Assets |

SDTS | In and around Stanton, Brady and Celeste, Texas | Approximately 9,500 miles of overhead distribution lines and underground distribution lines; transmission lines and substations | |||

| McAllen Assets |

SDTS | Primarily South Texas | DC Tie; transmission operations center; approximately 15 miles of 138 kV transmission lines; distribution lines and 3 substations | |||

| Stanton Transmission Loop Assets |

SDTS FERC | Near Stanton, Texas | Approximately 305 miles of 138 kV transmission lines and connected substations | |||

| ERCOT Transmission Assets |

SDTS | Texas Panhandle | A substation in the Panhandle; additional ERCOT transmission assets may be added in the future | |||

Business Strategy

Focus on T&D assets. We intend to focus on owning T&D assets with long lives, low operating risks and stable cash flows consistent with the characteristics of our current portfolio. We believe that by focusing on this asset class and leveraging our industry knowledge we will maximize our strategic opportunities and overall financial performance.

Pursue sustainable dividend per share growth. We believe our platform will enable us to grow our rate base and, as a result, increase the amount of distributions we make to our stockholders. To achieve this growth, we will pursue the following:

| • | Grow rate base by investing in Footprint Projects. We expect to make significant capital expenditures in Footprint Projects, driven primarily by investments to improve reliability, meet customer requirements and support oil and gas activities in our Stanton territory in the Permian Basin and interconnections to our Panhandle transmission assets. |

| • | Acquire ROFO Projects and other T&D projects from Hunt. Hunt Developer has agreed to offer ROFO Projects to us prior to their completion. See the description of our development agreement with Hunt Developer, and a description of the ROFO Projects, below under the caption Our Relationship with Hunt. We are not obligated to purchase, and Hunt is not obligated to sell, these projects if we do not agree upon the price and other terms of the purchase. Hunt has informed us that it intends for us to be the primary owner of Hunt’s T&D development projects as those projects are completed and placed in service. |

| • | Acquire other T&D assets from third parties. We intend to leverage relationships that we, Sharyland and Hunt maintain in the energy industry to source acquisition opportunities. We have a track record of acquiring T&D assets from third parties as a result of relationships maintained by Hunt and Sharyland’s business development teams. We believe that our structure, which relies on an ongoing relationship with operating lessees, combined with Sharyland’s operating track record and Hunt’s reputation as an innovative and credible developer of energy assets, will competitively position us to acquire other T&D assets. |

8

Table of Contents

Focus on Texas and southwestern United States initially. We are primarily focused on two main markets, Texas and the southwestern United States, where we believe the electric transmission sector will continue to grow significantly. This also allows us to leverage our existing relationships and a proven track record of identifying, developing, constructing and acquiring critical infrastructure assets. Substantially all of the ROFO Projects are located in Texas or the southwestern United States. Over time, we may expand our focus to other jurisdictions with favorable regulatory and growth characteristics.

Maintain a strong financial profile. We intend to maintain a balanced capital structure that enables us to increase our dividend over time and serve the long-term interests of our stockholders. Our financing policies will seek an optimal capital structure through various capital formation alternatives to minimize interest rate and refinancing risks and position us to pay stable and growing long-term dividends and maximize value.

Competitive Strengths

Our assets generate stable cash flows. We generate revenue by leasing T&D assets to Sharyland. Sharyland’s lease payments to us are largely comprised of fixed base rent, with the remaining lease payments to us derived from a percentage of Sharyland’s gross revenue in excess of a specified threshold. Sharyland receives revenues from DSPs and REPs, which pay Sharyland PUCT approved rates. The PUCT approved rates are designed to allow the applicable utility to recover costs associated with maintaining and operating the assets and earn a return on invested capital. Through our leases, which include mechanisms for rent increases as we grow our rate base, we expect to benefit from the stability of Sharyland’s rate-regulated revenue stream. See the caption Our Leases under Our Tenant below.

Our T&D assets are located in high growth areas. Our Stanton territory assets serve a region atop the Permian Basin, which has experienced a rapid expansion in oil and gas investment. Our transmission assets in the Texas Panhandle are located in one of the most attractive wind corridors in the world and, we believe, will benefit from expanding wind power generation investment. Our McAllen territory is located in one of the most rapidly growing population areas of Texas and benefits from its border with Mexico, where we recently expanded power interconnection facilities through a long standing relationship with Comisión Federal de Electricidad (CFE), which operates the Mexican national electric grid.

The ability to update transmission rates through interim TCOS filings, combined with Sharyland’s current distribution customer and load growth, reduces the necessity of filing frequent rate cases. The majority of Sharyland’s expected 2015-2017 capital expenditures are for transmission assets. Like other utilities in Texas, Sharyland is able to minimize regulatory lag through interim TCOS filings. See the caption Our Revenue Model below. With respect to capital expenditures for distribution assets, Sharyland’s revenues, and its lease payments to us, will grow as capital expenditures are made to support new customers and/or existing customers increase their electricity usage. We believe this growth will enable us to invest in our Footprint Projects and receive increased lease payments from Sharyland, without the need for Sharyland to frequently file rate cases to request increases in rates to cover such costs.

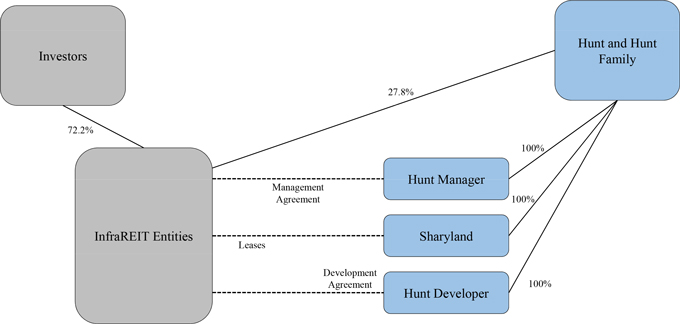

We benefit from our strong ties to and our alignment with Hunt. Hunt, and members of the Hunt family, own and control Hunt Manager, Sharyland and Hunt Developer. As of March 12, 2015, Hunt owns 3,176,878 shares of our common stock and 13,663,095 units in our Operating Partnership (OP Units), which are subject to long-term lock-ups with us. This ownership constitutes 27.8% of our outstanding equity if all outstanding OP Units were exchanged for shares of our common stock. In addition, the incentive payment under our management agreement with Hunt Manager is linked to our financial performance, requiring payment only if our quarterly distributions exceed $0.27 per share per quarter.

Sharyland has a proven development, construction and operating history and a strong reputation in Texas. Since Sharyland began operations in 1999, it has successfully developed, constructed and operated several T&D projects, including the CREZ project and the Railroad DC Tie, and successfully integrated and improved the operations of Cap Rock Holding Corporation (Cap Rock) following our acquisition of it in 2010. Sharyland completed the CREZ project in November 2013, within the original timeframe outlined by the PUCT and under budget. Sharyland’s expertise and reputation helps Sharyland maintain positive customer and regulatory relationships, which we believe increases our ability to generate the returns we expect on our T&D assets.

We have rights to Hunt’s T&D projects. Our development agreement with Hunt Developer requires Hunt to offer all ROFO Projects to us prior to their completion. Hunt and Sharyland are responsible for Sharyland’s growth from a start-up operation to a utility that operates approximately $1.1 billion in rate base as of December 31, 2014.

9

Table of Contents

Hunt originated, and Hunt Manager and Hunt have expertise in applying, the REIT structure to regulated T&D assets. Over the last nine years, Hunt and Sharyland gained significant experience applying the REIT structure to a high-growth, regulated T&D business. Furthermore, in 2010, Hunt and Sharyland successfully acquired and integrated the Cap Rock T&D assets and operation directly into our REIT structure. Hunt’s team also successfully sourced, structured and negotiated on our behalf debt and equity financing arrangements to fund our organic growth, construction projects and Cap Rock acquisition. We believe Hunt and Hunt Manager’s knowledge and experience gives us a competitive advantage in analyzing the complexities associated with our expected rate base growth, executing on development and acquisition opportunities within a REIT structure, obtaining regulatory approvals and structuring lease agreements with tenants.

Our REIT structure and balance sheet provide us with long-term cash distribution advantages. We believe our REIT structure positions us well to make enhanced cash distributions to our stockholders over the long term as compared with utilities and power-oriented yield vehicles. Additionally, with the completion of our IPO, we expect to fund estimated capital expenditures from Footprint Projects through the end of 2017 without raising proceeds from additional equity offerings. See Liquidity and Capital Resources in Item 7., Management’s Discussion and Analysis of Financial Condition and Results of Operations for a description of our liquidity and target credit metrics.

Our Relationship with Hunt

Ownership

As of March 12, 2015, Hunt owns 3,176,878 shares of our common stock and 13,663,095 OP Units, which are subject to long-term lock-ups with us. This ownership constitutes 27.8% of our outstanding equity if all OP Units were exchanged for shares of our common stock. While Hunt has entered into a lock-up agreement related to these shares and OP Units, it also has informed us that it intends to continue to hold a substantial portion of this equity for the foreseeable future.

We have various agreements with Hunt, Hunt Developer, Hunt Manager and Sharyland. The following chart illustrates our relationships and alignment with each of these entities as of March 12, 2015.

Hunt’s Development Projects

Our development agreement with Hunt Developer and Sharyland provides us with a right of first offer to acquire the ROFO Projects, which consist solely of T&D projects that Hunt is developing or constructing. Although Hunt may develop other T&D projects that do not currently constitute ROFO Projects under the development agreement, Hunt has informed us that it intends for us to be the primary owner of all of Hunt’s T&D development projects as those projects are completed and placed in service. Under the terms of the development agreement, Hunt has the obligation to offer the ROFO Projects to us at least 90 days prior to the date on which such assets are expected to be placed in service. We expect the purchase price for the

10

Table of Contents

ROFO Projects or any other T&D projects Hunt develops will be negotiated by Hunt and the Conflicts Committee of our board of directors, which is comprised of six independent members of our board of directors, and will be based on a number of factors, such as the cash flow and rate base for the assets, market conditions, potential for incremental Footprint Projects, whether the assets are subject to a lease with Sharyland or another tenant, the terms of any such lease and the regulatory return we expect the assets will earn. Sharyland and Hunt Developer are each parties to our development agreement. However, the agreement, by its terms, applies to activities by all Hunt affiliates. As such, when discussing the development agreement, we use the term “Hunt” to refer to Hunt Developer, Sharyland and other affiliates of HCI.

Development Team

Our development agreement with Hunt Developer provides us with continued access to the Hunt Developer and Sharyland development teams and the development projects they source. Hunt Developer’s active and experienced T&D project development team members have, on average, 15 years of industry experience. The Hunt Developer team has experience with ERCOT, the Southwest Power Pool, the California ISO, Western Electric Coordinating Council and CFE, which enables them to identify and pursue T&D opportunities across the southwestern United States. This team has an extensive track record of successfully pursuing a variety of projects, including greenfield development, acquisitions, partnering with municipalities and cooperatives and cross border activity. Our access to Hunt Developer and Sharyland development pipelines position us to capitalize on growth opportunities beyond our existing footprint and potentially add to our current list of ROFO Projects offered by Hunt.

ROFO Projects

Our development agreement with Hunt Developer and Sharyland provides us with a right of first offer to acquire ROFO Projects that Hunt is currently developing or constructing, including the following:

| ROFO Project |

Description |

Status | ||

| Cross Valley transmission line |

Approximately 50 mile transmission line in South Texas near the Mexican border. Total estimated construction cost (including financing costs) of $160 million to $185 million, of which $34.2 million has been spent though December 31, 2014. | Under construction; expected completion in 2016 | ||

| Golden Spread Electric Coop (GSEC) interconnection |

Approximately 55 mile transmission line connecting one of GSEC’s gas-fired generation facilities to our Panhandle transmission line. Total estimated construction cost (including financing costs) of $100 million to $120 million, of which $7.0 million has been spent through December 31, 2014. | Under construction; expected completion in 2016 | ||

| Southline Transmission Project |

Approximately 240 miles of new transmission lines and upgrades of approximately 120 miles of existing transmission lines in southern New Mexico and southern Arizona. Initially estimated construction cost (excluding financing costs) of $700 million to $800 million. | In active development; draft environmental impact statement published | ||

| Verde Transmission Project |

Approximately 30 mile transmission line in northern New Mexico. Initially estimated construction cost (excluding financing costs) of $60 million to $80 million. | In development | ||

We have provided information about the Cross Valley and GSEC interconnection projects because of their size, their prominence in our core Texas markets and our belief that these ROFO Projects are the most likely ROFO Projects to be completed and offered to us. Although they are in the early stages of development and budgets for such projects, as well as potential arrangements that might result in developing the projects with partners, have not been finalized, we have also provided information about the Southline Transmission Project and Verde Transmission Project because they are the most prominent and advanced of Hunt’s non-Texas ROFO Projects. However, there can be no assurances that any of the ROFO Projects will be completed and offered to us or, if completed and offered to us, that the price and other terms of the acquisition of such projects can be negotiated on terms acceptable to us.

11

Table of Contents

Other ROFO and Development Projects

In addition to the construction and development activity related to the projects above, Hunt and Sharyland are also evaluating and developing various projects in ERCOT and other regions of the United States. Such ROFO Projects include proposals to (i) reinforce the existing transmission grid in the Panhandle and South Plains region as new wind generators connect to the transmission grid, (ii) develop additional high-voltage DC ties along the Texas and desert Southwest border with Mexico, (iii) increase electric transmission between the PJM and MISO grids through projects in the Midwest and (iv) provide import capacity from New Mexico and Arizona into California.

Hunt and Sharyland are also developing a number of projects that are not included in the ROFO Projects list. A typical example involves initiatives in South Texas to develop new transmission lines to enhance grid reliability and enable generation interconnections. For any non-ROFO projects, Hunt has informed us that it intends for us to be the primary owner of Hunt’s T&D development projects as those projects are completed and placed in service. However, there can be no assurances that any of the non-ROFO Projects will be completed and offered to us or, if completed and offered to us, that the price and other terms of the acquisition of such projects can be negotiated on terms acceptable to us.

Transfer of ROFO Project Assets

Effective January 15, 2015, we transferred the assets related to the Cross Valley transmission line and GSEC interconnection projects, which are designated as ROFO Projects under our development agreement, to Hunt or one of its affiliates. Hunt Developer will continue to construct these projects and will offer such projects to us prior to completion pursuant to the terms of the development agreement. In exchange for these assets, we received $41.2 million, which equaled the rate base of the transferred assets plus reimbursement of out of pocket expenses associated with the formation of related special purpose entities and the Cross Valley project financing.

Our Revenue Model

We lease our T&D assets to Sharyland, which makes lease payments to us consisting of base rent and percentage rent. To support its lease payments to us, Sharyland delivers electric service and collects revenues directly from DSPs and REPs, which pay PUCT approved rates. Under the terms of our leases, Sharyland is responsible for the operation of our assets, payment of all property related expenses associated with our assets, including repairs, maintenance, insurance and taxes (other than income taxes) and construction of Footprint Projects. As our rate base increases through Footprint Projects, ROFO Projects or other acquisitions, we generally expect our lease revenue to increase.

Rent Revenue

Rental Rates

All of our current revenue is comprised of rental payments from Sharyland under lease supplements that were negotiated at various times between 2010 and 2015. Lease supplements are exhibits to our leases that include the economics of the lease obligations that Sharyland owes us. Historically, we and Sharyland have negotiated rent payments intended to provide us with approximately 97% of the projected regulated return on rate base investment attributable to our assets that we and Sharyland would receive if we were a fully-integrated utility. See the caption Regulatory Recovery under Factors Expected to Affect Our Operating Results and Financial Condition included in Item 7., Management’s Discussion and Analysis of Financial Condition and Results of Operations. We and Sharyland have negotiated these rental rates based on the premise that we, as the owner of regulated T&D assets, should receive most of the regulated return on our invested capital, while leaving Sharyland with a portion of the return that gives it the opportunity to operate prudently and remain financially stable. Our leases require us to continue to negotiate rent payments in the future in a manner similar to this historical negotiation.

12

Table of Contents

Sharyland makes lease payments to us that consist of base rent and percentage rent (based on an agreed percentage of Sharyland’s gross revenues, as defined in our leases, in excess of a specified threshold). Because our existing rate base will decrease over time as our T&D assets are depreciated, revenue under our leases will decrease over time unless we add to our existing rate base by making additional capital expenditures to offset the decreases in the rent resulting from depreciation. The weighted average annual depreciation rate of our assets as of December 31, 2014 was 2.68%. We negotiated our current leases to provide for base rent to comprise approximately 80-90% of the total expected rent (with the exception of the lease related to our Stanton transmission loop assets, which does not provide for percentage rent).

Lease Renewals

We expect to renew our leases with Sharyland prior to expiration. Our leases provide that we and Sharyland negotiate lease terms based on our historical negotiations and the return that utilities in Texas are allowed to earn at the time of the negotiation. We generally expect that renewal terms will be at least five years. If either we or Sharyland do not wish to renew a lease, or we cannot agree to new lease terms, we expect that our rent negotiations with a new third-party tenant would be based on the rate base of the assets subject to the expired lease and the rate of return expected at the time a new lease is negotiated, among other factors. The lease of our T&D assets located mainly in and around the cities of Stanton, Brady and Celeste, Texas (S/B/C lease), which relates to approximately 30% of our existing assets as of December 31, 2014, expires on December 31, 2015, and leases relating to our remaining assets expire at various times between December 31, 2019 and December 31, 2022. Our conflict of interest policy requires that the Conflict Committee of our board of directors approve any lease renewal.

Lease Supplements

Our leases provide that as the completion of Footprint Projects increases our rate base, we and Sharyland will negotiate lease supplements so that Sharyland makes additional rent payments to us on this incremental rate base. Various factors could cause Sharyland’s expected lease payments on incremental rate base to be different than its lease payments to us on our existing rate base. For instance, if a rate case was finalized since the last lease or lease supplement, the new lease supplement would use regulatory assumptions from the most recent rate case. Also, our leases provide that either party can negotiate for economics that differ from our existing leases based on appropriate factors that our leases do not specifically list. However, the negotiation of lease supplements relates only to the revenue we expect to be generated from the incremental rate base subject to the negotiation, and in no circumstance will the negotiation change the rent payments negotiated with respect to prior leases and lease supplements.

Rate Base Growth

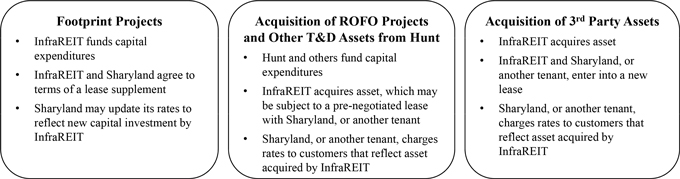

We will add to our rate base through capital expenditures for Footprint Projects, acquisitions of ROFO Projects or acquisitions of other T&D assets from Hunt or third parties.

For Footprint Projects, we generally fund all of the capital expenditures during the development or construction phase of a project, and these expenditures increase our rate base when they are placed in service. In advance of the time assets are placed in service, we will work with Sharyland to negotiate a supplement to our leases. Sharyland also may make a regulatory filing to update its rates to reflect the additional rate base.

When we acquire ROFO Projects or other T&D assets from Hunt, we would expect to assume any lease that is already negotiated with Sharyland or another tenant with respect to those T&D assets, and we will work with Sharyland or another tenant to update existing rates, as appropriate, for the addition to our rate base.

Prior to closing an acquisition from a third-party, we will work with Sharyland, or another tenant, to pursue the addition of new leases and updating of existing rates, as appropriate, for the addition to our rate base.

13

Table of Contents

Described below are the key steps by which placing new assets into service increases our rate base and/or our expected lease payments, although the order and timing of each step will vary by asset:

Our Tenant

Overview

Our tenant, Sharyland, has been a regulated utility since 1999 and currently serves over 50,000 electricity delivery points in 29 counties throughout Texas. Sharyland is responsible for construction management, operation and maintenance of our T&D assets and regulatory oversight and compliance. See Our Leases below and Financial Information Related to Our Tenant under Item 7., Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Our Relationship with Sharyland

The objective of a REIT structure is to provide for efficient access to capital markets to fund infrastructure additions while positioning a qualified utility to operate and control the infrastructure assets. We believe the REIT structure we established with Sharyland meets this objective.

A REIT is required to lease its assets to third-party tenants and to generate a substantial portion of its income from lease payments from these tenants. As a result, we have structured ownership of our T&D assets through a lessor/lessee structure, with Sharyland acting as the tenant under each of our leases. Sharyland, as lessee, has control of, and is responsible for operating and maintaining, our T&D assets. We are a passive owner of our T&D assets, with no operational control over those assets. We have memorialized Sharyland’s operational control primarily through the leases. However, the PUCT order approving our structure also requires that Sharyland maintain operational control of SDTS as the managing member. Under the PUCT order and the SDTS company agreement, we are not able to remove Sharyland as managing member without prior PUCT permission. We have negative control rights over SDTS that passive owners would expect such as the right to approve renewals of the leases or any new leases, sales or dispositions of assets, debt issuances and annual budgets, subject to some exceptions. To the extent that day-to-day operations of SDTS involve matters primarily related to passive ownership of the assets, such as capital sourcing, financing, cash management and investor relations, Sharyland has delegated those responsibilities and authorities to us pursuant to a delegation agreement.

The leases assume that Sharyland, as lessee, should earn a regulated return to compensate it for the capital it has invested and for the risks that it is taking as the tenant under the lease. Sharyland bears the risks that most utilities face, such as, changes in regulatory policy, changes in regulated rates, change in usage and demand, credit risk of counterparties, damage to properties, increases in operating expenses and increases in taxes. Many of these risks may ultimately lead to lower revenue, or increased costs, which would affect Sharyland’s ability to fulfill its lease obligations or its willingness to enter into new leases or renewals of existing leases under similar economic terms. We believe that Sharyland is incentivized to operate the assets in accordance with good utility practice to ensure that it is able to continue to lease the assets and be a utility in good standing with the PUCT. As a public utility, Sharyland’s practices, cost structure and its investments are subject to review by the PUCT, and Sharyland understands that we expect a regulated return on the investments we make in our T&D assets. Therefore, Sharyland is incentivized to only incur costs and investments that are reasonable and necessary, while also honoring obligations to customers.

14

Table of Contents

The leases also assume that, as lessor and owner of the T&D assets, we should receive a regulated return on the capital we invested in our T&D assets. The combined return that we and Sharyland receive should be comparable to the return that other integrated T&D utilities receive. As part of our negative control rights in the SDTS company agreement, we have the right to approve the annual financial plan of SDTS and any leases between Sharyland and SDTS. We intend to negotiate the leases to ensure that we receive our expected regulated return, keeping in mind that Sharyland has to be willing to enter into the lease. Thus, both parties will negotiate the leases keeping in mind the current and expected economic, regulatory and capital market environments. It is in each party’s best interest to negotiate leases that are expected to result in beneficial economic outcomes. To the extent that conditions change, both parties are incentivized to negotiate long-term solutions.

Separation of Utility Functions

Pursuant to our leases, the SDTS company agreement and the delegation agreement, we have separated, between Sharyland and us, the functionality that is typically combined under one commonly owned group in an integrated utility. Through Hunt Manager, we are generally responsible for debt and equity financing, capital markets planning, investor relations, tax administration and accounting for the substantial portion of the combined utility’s assets and liabilities. Sharyland is responsible for operating, repairing and maintaining the T&D assets, planning new T&D projects, handling customer complaints, managing regulatory matters and relationships with various regulatory bodies, handling community relations matters, accounting for substantially all of the combined utility’s operations and maintenance costs, ensuring that the T&D assets and the combined utility’s operations comply with applicable environmental, safety and other laws applicable to operations, working with us to forecast the combined utility’s capital needs, construction management and all other matters related to the operation of the combined utility. Since we separated these functions in 2010, Hunt Manager and Sharyland have developed expertise in ensuring that the relationship functions properly and that electricity is effectively and efficiently provided in a safe and reliable manner to Sharyland’s customers.

Our Leases

We lease all of our T&D assets to Sharyland under the following five separate leases:

McAllen Lease. SDTS and Sharyland are party to a lease pursuant to which Sharyland leases our assets located in South Texas, including our Railroad DC Tie and our transmission operation centers in Amarillo, Texas. We refer to this lease as the McAllen Lease. This lease currently expires on December 31, 2019.

S/B/C Lease. SDTS and Sharyland are party to a lease pursuant to which Sharyland leases our T&D assets located in and around Stanton, Brady and Celeste, Texas, other than our 138 kV transmission loop, which is described below. We refer to this lease as the S/B/C Lease. This lease currently expires on December 31, 2015.

CREZ Lease. SPLLC and Sharyland are party to a lease pursuant to which Sharyland leases substantially all of our Panhandle transmission assets. We refer to this lease as the CREZ Lease. This lease currently expires on December 31, 2020.

Stanton Transmission Loop Lease. SDTS FERC, a wholly-owned subsidiary of SDTS, and SU FERC, L.L.C., which is a wholly-owned subsidiary of Sharyland, are party to a lease pursuant to which Sharyland leases our 138 kV transmission line that loops around our Stanton, Texas territory in the Permian Basin. This transmission line formerly was subject to FERC regulation prior to January 1, 2014 before being transitioned to ERCOT. We refer to this lease as the Stanton Transmission Loop Lease. This lease currently expires on December 31, 2021.

ERCOT Transmission Lease. SDTS and Sharyland are party to a lease pursuant to which Sharyland leases a small portion of our Panhandle transmission assets, which we refer to as the ERCOT Transmission Lease, and which currently expires on December 31, 2022.

Net Lease

Each of our lease agreements is a net lease that grants Sharyland exclusive rights to and responsibility for the maintenance and operation of our T&D assets, requires Sharyland to maintain appropriate insurance with respect to our T&D assets, requires Sharyland to pay any property, franchise, sales and other taxes related to the T&D assets and gives Sharyland responsibility for regulatory compliance and reporting requirements related to our T&D assets. See the caption Insurance below for disclosure regarding the waivers we have provided to Sharyland regarding the insurance requirements in our leases.

15

Table of Contents

Operation of Our T&D Assets

The leases require that Sharyland operate the T&D assets in a reasonable and prudent manner in accordance with PUCT guidelines and applicable law. Sharyland must obtain and maintain any licenses, permits or other approvals required by applicable law to operate the T&D assets under the leases.

Expenditures

The following chart demonstrates how the leases define and assign responsibility for various expenditures related to our T&D assets:

| Type of Expenditure |

Definition |

Sharyland’s Responsibilities |

Our Responsibilities | |||

| Footprint Projects | Expenditures for T&D projects primarily situated within our distribution service territory or that are added to an existing transmission substation or physically hang from our existing transmission assets and that are characterized as capital expenditures under generally accepted accounting principles in the United States (U.S. GAAP) that are used to acquire real property assets | Send us three-year capital expenditure budgets, request that we fund these Footprint Projects as prudent, construct T&D assets with the capital we provide and pay us rent with respect to these capital expenditures, typically commencing when the related assets are placed in service | Fund capital expenditures requested by Sharyland | |||

| Repairs | Expenditures related to our T&D assets that are expensed, and not capitalized under U.S. GAAP | Make and fund all repairs | None | |||

Whether a particular expenditure is characterized as a Footprint Project, which we are required to fund, or a repair, which Sharyland is required to fund, depends on its characterization under U.S. GAAP. Expenditures relating to Footprint Projects are capitalized under U.S. GAAP, and expenditures relating to repairs to our existing T&D assets are expensed under U.S. GAAP. As a result of this construct, capital expenditures that we fund related to Footprint Projects increase our net electric plant.

Sharyland is required to provide a capital expenditure budget on a rolling three year basis that sets forth anticipated capital expenditures related to Footprint Projects, which the leases require us to fund. Because Sharyland is obligated to pay us rent with respect to our capital expenditures, and because of our strong working relationship with Sharyland and its history as a prudent and responsible operating utility, we do not expect that Sharyland will require us to fund capital expenditures unless Sharyland believes those expenditures are prudent and will be included in our rate base.

Rent

We have negotiated the rental rates under our lease supplements with Sharyland at various times between 2010 and 2015. Historically, we and Sharyland have negotiated rent payments intended to provide us with approximately 97% of the projected regulated return on rate base investment attributable to our assets that we and Sharyland would receive if we were a fully integrated utility. We and Sharyland have negotiated these rental rates based on the premise that we, as the owner of regulated T&D assets, should receive most of the regulated return on our invested capital, while leaving Sharyland with a portion of the return that gives them the opportunity to operate prudently and remain financially stable.

Actual revenue and expenses incurred by Sharyland will be different from those expected at the time we negotiate rental rates with Sharyland. As a result, we and Sharyland may earn more or less than originally projected. Our leases prohibit both parties from adjusting for the effect of differences between Sharyland’s actual and projected results.

Sharyland makes scheduled base rent and percentage rent payments under each of our leases with the exception of the Stanton Transmission Loop Lease, which does not provide for percentage rent. The percentage rent is based upon a percentage of Sharyland’s annual gross revenue in excess of specified threshold amounts, which are at least equal to base rent under each of our leases. Our leases define gross revenue to mean all revenue that Sharyland generates from the leasehold T&D assets, subject to the following definitional provisions. First, the definition of gross revenue specifically excludes pass through items. For instance, Sharyland’s tariff includes rate riders, including a rider allowing Sharyland to recover costs related to its move to

16

Table of Contents

competition. Revenue that Sharyland collects pursuant to this rider is excluded from the definition of gross revenue under our leases. Second, we also subtract from revenue an amount necessary to provide Sharyland with a return on any capital expenditures that Sharyland has made related to the leasehold assets. For instance, Sharyland has made capital expenditure investments in rolling stock such as service trucks. We did not fund these capital expenditures because the related assets do not constitute real property under applicable law. Sharyland is entitled to make a return on those investments, just as we are entitled to make a return in investments on our T&D assets. Our leases provide Sharyland with this return by subtracting the related return amount from gross revenue, allowing Sharyland to retain 100% of this revenue. Third, we allocate total transmission revenue based on net plant in service for each lease for purposes of calculating the amount of gross revenue Sharyland has generated under each lease. We make this allocation because Sharyland’s transmission revenue, which is paid by all DSPs in ERCOT, cannot be tracked to a particular lease, which distinguishes it from distribution revenue. We have ERCOT transmission assets in all five of our leases.

Supplements

We negotiated our S/B/C Lease and McAllen Lease payments with Sharyland assuming that we would fund a certain amount of base capital expenditures annually. If capital expenditures are expected to exceed these base capital expenditures, we negotiate rent supplements with Sharyland. No base capital expenditure level is assumed in our CREZ Lease or ERCOT Transmission Lease, so all expected capital expenditures related to these leases result in a related negotiated rent supplement with Sharyland. None of the capital expenditures we make are allocated to the Stanton Transmission Loop Lease. For purposes of determining whether there are capital expenditures that require rent supplements, we measure capital expenditures based on the date the assets funded by those capital expenditures are placed in service, rather than the date of funding the capital expenditures. Placed in service, in this context, means the related T&D project has been completed and is used and useful to ratepayers. Likewise, Sharyland will not begin collecting revenue on those assets until after the time they are placed in service, not the time when they are funded.

As our rate base increases, Sharyland is required to agree to lease supplements to increase its rent payments to us. The amount of the rent increase is subject to negotiation each time a supplement is agreed to, but our existing leases provide that our historical agreements with Sharyland on target rate of return will serve as the basis for the rental rate increase, subject to limited factors that can affect the negotiation. For example, the negotiated target rate of return on the incremental rate base may be different from the negotiated target rate of return on the prior rate base due to a variety of factors, including the rate of return that utilities in Texas are generally earning at the time of the relevant negotiation. The leases do not explicitly define which factors would be appropriate or the effect that any appropriate factor should have on the negotiation. However, the negotiation of lease supplements relates only to the revenue we expect to be generated from the incremental rate base subject to the negotiation, and in no circumstance will the negotiation change the rent payments negotiated with respect to prior leases and lease supplements or result in any true up with respect thereto.

Additionally, the lease supplement process allows us to address and update a number of other matters under our leases, such as updating the amount of revenue attributable to Sharyland’s capital expenditures and related matters. Because we frequently prepare supplements based on the expectations we and Sharyland have regarding various matters, including expected capital expenditures, we have a mechanism, which we refer to as a validation, that we use to amend previously negotiated supplements in order to reflect the difference between the capital expenditures we expected and the capital expenditures that were actually placed in service and related matters such as the actual placed in service date of T&D assets funded by our capital expenditures. For instance, in March 2015, we executed amended lease supplements with Sharyland in connection with a validation of the amount of the 2014 placed in service capital expenditures. In no event will we use the validation process to account for differences between the expected and actual return on capital expenditures. If we and Sharyland are unable to agree on a rent supplement or a validation, the leases obligate us to submit the dispute to binding arbitration.

Generally, we expect to enter into lease supplements related to capital expenditures in advance of the year in which the related assets are placed in service. For instance, in late 2014, we entered into revised lease supplements that memorialized Sharyland’s obligation to pay us rent on the capital expenditures we expect for 2015. As 2015 progresses, if the amount of expected placed in service capital expenditures, or the related placed in service dates, differ from expectations, either Sharyland or we may request a rent validation in order to adjust rent obligations to reflect the difference between actual and expected capital expenditure amounts and placed in service dates. Our leases do not require that we follow this exact timeline and process; therefore, we may determine, with Sharyland, that an alternate process is more efficient.

17

Table of Contents

Events of Default

Under our leases, a default will be deemed to occur upon certain events, including (1) the failure of Sharyland to pay rent, after applicable cure periods, (2) certain events of bankruptcy or insolvency with respect to Sharyland, (3) Sharyland’s breach of a representation or warranty in a lease in a material manner, (4) Sharyland’s breach of a covenant in a lease in a material manner or (5) a final judgment for the payment of cash in excess of $1,000,000 is rendered against Sharyland and is not bonded, stayed pending appeal or discharged within 60 days.

Remedies Upon a Default

Upon a default under a lease, we may, at our option, exercise the following remedies: (1) subject to PUCT approval, terminate the applicable lease agreement upon notice to Sharyland and recover any damages to which we are entitled under applicable law, (2) subject to PUCT approval, terminate Sharyland’s right to use our T&D assets and recover any damages to which we are entitled under applicable law and (3) take reasonable action to cure Sharyland’s default at Sharyland’s expense.

Renewal

Our leases provide that, if both we and Sharyland desire to renew a lease, we and Sharyland will negotiate rent applicable to the renewal term based on our historical negotiations and the return that utilities in Texas are generally earning at the time of the negotiation. Generally, we expect to begin the process of renegotiating a lease within the six month period prior to its expiration and that renewal terms will be at least five years, although the leases do not require this length of a renewal term, and we may agree with Sharyland that a shorter or longer renewal term will apply.

Financial Covenants

Under our leases, Sharyland is prohibited from incurring indebtedness other than:

| • | Secured indebtedness, which may be senior to or pari passu with Sharyland’s lease obligations to us, in an amount equal to the greater of: |

| • | $5 million; or |

| • | 1% of the sum of, without duplication: |

| • | the consolidated net plant (as defined in our leases) of Sharyland; |

| • | the consolidated net plant of any guarantor under a lease of our T&D assets to Sharyland; and |

| • | the portion of the consolidated net plant of SDTS that is the subject of the applicable lease. |

| • | Additional indebtedness, which must be subordinated to the lease obligations that Sharyland owes to us, in an amount equal to the greater of: |

| • | $10 million; or |

| • | 1.5% of the sum of, without duplication: |

| • | the consolidated net plant of Sharyland; |

| • | the consolidated net plant of any guarantor under a lease of our T&D assets to Sharyland; and |

| • | the portion of the consolidated net plant of SDTS that is the subject of the applicable lease. |

| • | An additional $5 million of loans from us to Sharyland to fund Sharyland’s capital expenditures. |

18

Table of Contents

| • | With respect to indebtedness of Sharyland’s subsidiaries that is nonrecourse to Sharyland, an additional amount equal to the product of: |

| • | the lesser of: |

| • | the regulatory approved debt ratio (expressed as a percentage) plus 5%; or |

| • | 65%; and |

| • | Sharyland’s consolidated net plant. |

In determining Sharyland’s net plant, the effect of failed sale-leaseback treatment will be reversed in a manner determined by Sharyland in good faith. See Financial Information Related to Our Tenant under Item 7., Management’s Discussion and Analysis of Financial Condition and Results of Operations for a description of the manner in which Sharyland’s reverses the effect of failed sale-leaseback accounting. In addition, under our leases, Sharyland has agreed to comply with certain of our covenants relating to Sharyland under our debt arrangements.

Assignment and Subletting

Sharyland may not assign or otherwise transfer or sublet any of our T&D assets under the leases without our prior written consent and the approval of the PUCT or other applicable governmental authority.

Indemnification

Sharyland is required to defend, indemnify and hold us harmless from and against any and all claims, obligations, liabilities, damages and costs and expenses arising from any act or omission of Sharyland with respect to (1) the operation of the T&D assets, (2) damage to the T&D assets, (3) physical injuries or death (including in connection with the operation of the T&D assets), (4) any breach of any representation or warranty or covenant or (5) any negligence, recklessness or intentional misconduct of Sharyland.

Lease Expiration

The S/B/C Lease, which relates to approximately 30% of our existing assets at December 31, 2014, expires on December 31, 2015 and leases relating to our remaining assets expire at various times between December 31, 2019 and December 31, 2022. Our conflict of interest policy requires that the Conflicts Committee of our board of directors approve any lease renewal. If either we or Sharyland do not wish to renew a lease, we expect that our rent negotiations with a new third-party tenant would be based on the rate base of the assets subject to the expired lease and the rate of return expected at the time a new lease is negotiated, among other factors. In any event, because our T&D assets are rate-regulated and necessary for the transmission and distribution of electricity, we expect that they will continue to generate tariff revenue. As a result, we believe we will be able to identify a qualified tenant to operate our T&D assets who will be able to make lease payments to us based on the tariff revenue our assets generate. Before we can lease our T&D assets subject to the expiring lease to a new tenant, we and Sharyland must obtain PUCT approval for the transfer of the related operating licenses. Sharyland is required under the leases to use commercially reasonable efforts to obtain these approvals as soon as is reasonably practicable. Until we obtain those approvals, Sharyland will continue to operate our T&D assets and pay us rent. If it takes longer than 12 months to obtain these approvals, rent payments will be adjusted to 80% of the amounts otherwise due, if the failure to obtain the approval is a result of our failure to reasonably pursue the approval, and will be 105% of the amounts otherwise due, if the failure to obtain the approval is the result of Sharyland’s failure to reasonably pursue the approvals. We also have the right to buy, from Sharyland, any equipment or property that Sharyland uses in connection with the lease, with the price equal to the greater of 110% of book value or fair market value, as mutually agreed by Sharyland and us.

Significant Agreements

Management Agreement

We are parties to a management agreement with Hunt Manager pursuant to which Hunt Manager manages our day-to-day business, subject to oversight from our board of directors.

19

Table of Contents

Compensation

The following table summarizes the fees and expense reimbursements that we pay to Hunt Manager pursuant to the management agreement:

| Compensation |

Description | |

| Base Fee | We will pay an annual base fee, or management fee, of $10.0 million through April 1, 2015. Effective April 1, 2015, the annual base fee will increase from $10.0 million annually to $13.1 million annually through April 1, 2016. The base fee for each twelve month period on April 1 thereafter will equal 1.5% of our total equity (including non-controlling interest) as of December 31 of the immediately preceding year, subject to a $30.0 million cap, unless a greater amount is approved by a majority of our independent directors (or a committee comprised solely of independent directors). | |

| Incentive Payment | We will pay Hunt Manager an incentive payment, payable quarterly, equal to 20% of quarterly per OP Unit distributions (inclusive of the incentive payment) in excess of $0.27 per OP Unit per quarter, which is 120% of our initial projected annualized per OP Unit distribution for the year ended December 31, 2015, divided by four; provided, however, that any distributions in excess of our cash available for distribution (as defined in the management agreement as an amount equal to (A) net income before noncontrolling interest, plus (B) depreciation, plus (C) amortization of deferred financing costs, if any, minus (D) AFUDC equity, minus (E) capital expenditures to maintain net assets (which equals depreciation expense), subject to adjustments to eliminate the impact of certain other non-cash items) will not be considered distributions for purposes of calculating the incentive fee. | |

| Reimbursement of Expenses | We will reimburse Hunt Manager for all third-party expenses incurred on our behalf or otherwise in connection with the operation of our business, other than: compensation expenses related to Hunt Manager’s personnel (including our officers), occupancy costs incurred by Hunt Manager related to its place of business, time or project-based billing for work done by Hunt affiliates, travel and expenses for Hunt Manager’s employees and fees or costs associated with professional service organizations, publications, periodicals, professional development or related matters for Hunt Manager employees, all of which will be the exclusive responsibility of Hunt Manager. | |

| Termination Fee | If we exercise our right not to renew the management agreement at the end of the then-current term, we will be required to pay Hunt Manager a termination fee, in cash or equity, at our election, in an amount equal to three times the most recent annualized base management fee and incentive payment amount. If we elect to pay the termination fee in equity, the fee will be paid in OP Units, which will be issued five days after the effective date of termination, with the number of OP Units based on the volume weighted average price of our common stock during the 10 trading day period that precedes such effective date of termination. | |

Term