Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - GLOBAL BRASS & COPPER HOLDINGS, INC. | d849722dex231.htm |

| EX-12.1 - EX-12.1 - GLOBAL BRASS & COPPER HOLDINGS, INC. | d849722dex121.htm |

| EX-10.7 - EX-10.7 - GLOBAL BRASS & COPPER HOLDINGS, INC. | d849722dex107.htm |

| EX-10.9 - EX-10.9 - GLOBAL BRASS & COPPER HOLDINGS, INC. | d849722dex109.htm |

| EX-21.1 - EX-21.1 - GLOBAL BRASS & COPPER HOLDINGS, INC. | d849722dex211.htm |

| EX-10.8 - EX-10.8 - GLOBAL BRASS & COPPER HOLDINGS, INC. | d849722dex108.htm |

| EX-31.1 - EX-31.1 - GLOBAL BRASS & COPPER HOLDINGS, INC. | d849722dex311.htm |

| EXCEL - IDEA: XBRL DOCUMENT - GLOBAL BRASS & COPPER HOLDINGS, INC. | Financial_Report.xls |

| EX-31.2 - EX-31.2 - GLOBAL BRASS & COPPER HOLDINGS, INC. | d849722dex312.htm |

| EX-32.1 - EX-32.1 - GLOBAL BRASS & COPPER HOLDINGS, INC. | d849722dex321.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No. 001-35938

GLOBAL BRASS AND COPPER HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 06-1826563 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification Number) | |

| 475 N. Martingale Road Suite 1050 Schaumburg, IL |

60173 | |

| (Address of principal executive offices) | (Zip Code) | |

(847) 240-4700

(Registrant’s telephone number, including area code)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant on June 30, 2014, the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $356.7 million (based upon the closing price per share of the registrant’s common stock on the New York Stock Exchange on that date).

On February 24, 2015, there were 21,478,746 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of this Form 10-K incorporate by reference certain information from the Registrant’s definitive Proxy Statement for its Annual Meeting of Shareholders to be held on May 21, 2015.

Table of Contents

| PART I | ||||||

| Item 1. | 1 | |||||

| Item 1A. | 16 | |||||

| Item 1B. | 42 | |||||

| Item 2. | 42 | |||||

| Item 3. | 43 | |||||

| Item 4. | 43 | |||||

| PART II | ||||||

| Item 5. | 44 | |||||

| Item 6. | 46 | |||||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

47 | ||||

| Item 7A. | 80 | |||||

| Item 8. | 82 | |||||

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

136 | ||||

| Item 9A. | 136 | |||||

| Item 9B. | 137 | |||||

| PART III | ||||||

| Item 10. | 138 | |||||

| Item 11. | 138 | |||||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

138 | ||||

| Item 13. | Certain Relationships and Related Transactions, and Director Independence |

139 | ||||

| Item 14. | 139 | |||||

| PART IV | ||||||

| Item 15. | 139 | |||||

| SIGNATURES | 143 | |||||

i

Table of Contents

Our Company

Global Brass and Copper Holdings, Inc. (“Holdings,” the “Company,” “we,” “us,” or “our”) was incorporated in Delaware on October 10, 2007. Holdings, through its wholly-owned principal operating subsidiary, Global Brass and Copper, Inc. (“GBC”), commenced commercial operations on November 19, 2007 following the acquisition of the worldwide metals business from Olin Corporation. The majority of our operations and sales activities are focused in North America under the Olin Brass, Chase Brass and A.J. Oster brand names.

We are a leading, value-added converter, fabricator, processor and distributor of specialized copper and brass products, including a wide range of sheet, strip, foil, rod, tube and fabricated metal component products. While we primarily process copper and copper-alloys, we also reroll and form certain other metals such as stainless steel, carbon steel and aluminum. Using processed scrap, copper cathode and other refined metals, we engage in metal melting and casting, rolling, drawing, extruding, welding and stamping to fabricate finished and semi-finished alloy products.

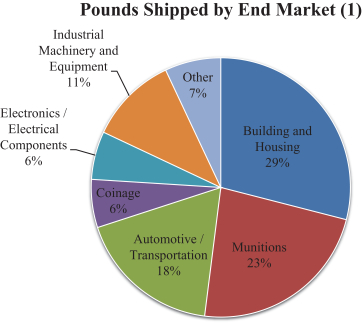

Our products are used in a variety of applications across diversified end markets, including the building and housing, munitions, automotive, transportation, coinage, electronics/electrical components, industrial machinery and equipment and general consumer end markets. We access these end markets through direct mill sales, our captive distribution network and third-party distributors. We hold the exclusive production and distribution rights in North America for a free machining, lead-free brass rod product, which we sell under the Green Dot™ and Eco Brass® brand names. The vertical integration of the manufacturing capabilities of Olin Brass and the distribution capabilities of A.J. Oster allows us to access a wide variety of customers with both high and low volume demand for our products.

We service nearly 1,700 customers in 29 countries across five continents. We employ approximately 1,900 people and operate 11 manufacturing facilities and distribution centers across the United States (“U.S.”), Puerto Rico and Mexico to service our North American customers.

We have an 80% ownership interest in a value-added service center in Guangzhou, China (“Olin Luotong Metals”) and the other 20% is owned by Chinalco Luoyang Copper Co. Ltd. (“Chinalco”). We participate in Dowa-Olin Metal Corporation (“Dowa Joint Venture”), a 50% owned marketing and sales joint venture with DOWA Metaltech Co. Ltd. (“Dowa Co.”) located in Hamamatsu, Japan. Through Olin Luotong Metals and the Dowa Joint Venture, together with our sales offices in China and Singapore, we supply our products in China and throughout Asia. We service our European customers through distribution arrangements in the United Kingdom and Germany.

Unlike traditional metals companies, including those that engage in mining, smelting and refining activities, we are purely a metal converter, fabricator, processor and distributor and do not attempt to generate profits from fluctuations in metal prices. Our financial performance is primarily driven by metal conversion economics, not by the underlying movements in the price of copper and the other metals we use. Through our “balanced book” approach (as further described under “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Factors Affecting Our Results of Operations—Balanced Book”), we strive to match the timing, quantity and price of our metal sales with the timing, quantity and price of our replacement metal purchases. This practice substantially reduces the financial impact of metal price movements on our earnings and operating margins.

Recent Transactions

On February 3, 2014 the Company completed an additional follow-on public offering (“Additional Follow-on Public Offering”) of 7,310,000 shares of its common stock, including 910,000 shares of common stock sold in

1

Table of Contents

connection with the full exercise of the option to purchase additional shares granted to the underwriters. Halkos Holdings, LLC, (“Halkos”), a 34.4% stockholder of the Company prior to the Additional Follow-on Public Offering sold all of the shares in the Additional Follow-on Public Offering and received all of the net proceeds from the offering. After giving effect to the Additional Follow-on Public Offering, Halkos no longer owns any shares of our common stock.

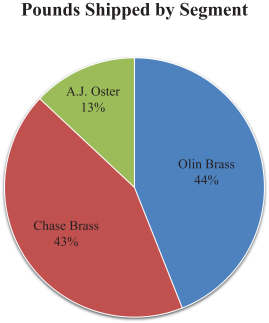

Shipment Overview

The following charts show our pounds shipped to external customers by our three operating segments and key end markets for the year ended December 31, 2014.

2

Table of Contents

| (1) | Pounds shipped by end markets in the above chart reflects management’s allocation among end markets of pounds shipped by Chase Brass to distributors, job shops and forging shops. See Item 1, “Business—Chase Brass.” |

Financial information for the last three years concerning our business segments and the geographic areas of our operations is incorporated herein by reference from “Note 18, Segment Information.”

Segments Overview

We have three operating segments: Olin Brass, Chase Brass and A.J. Oster.

|

|

| ||||

| Description | • Leading manufacturer, fabricator and converter of specialized copper and brass sheet, strip, foil, tube and fabricated products |

• Leading manufacturer and supplier of brass rod |

• Leading processor and distributor of copper and brass products | |||

| Key End Markets | • Munitions, Automotive, Coinage, Building and Housing, Electronics/ Electrical Components |

• Building and Housing, Transportation, Electronics/Electrical Components and Industrial Machinery and Equipment |

• Building and Housing, Automotive, Electronics/ Electrical Components |

Olin Brass

Olin Brass is a leading manufacturer and converter of specialized copper and brass sheet, strip and fabricated products. The Olin Brass segment also rerolls and forms other alloys such as stainless steel, carbon steel and aluminum. Key attributes of sheet and strip are conductivity, corrosion resistance, strength, malleability, cosmetic appearance and bactericidal properties. Sheet and strip is generally manufactured from copper and copper-alloy scrap.

Olin Brass manufactures its products through four sites in North America, employs 1,287 people as of December 31, 2014 and produces a wide variety of products. During the year ended December 31, 2014, it produced 51 alloys, including 16 high performance alloys (“HPAs”). Olin Brass is working to expand its market portfolio further by capitalizing on certain trends, including applications that utilize the bactericidal properties of copper and possible transition to the dollar coin in the U.S.

Olin Brass’ integrated brass mill in East Alton, Illinois is our main operating facility, which produces strip products that are either sold directly to external customers, sold to its affiliate, A.J. Oster, or shipped to Olin Brass’ downstream operations for further value-added processing. Olin Brass’ downstream operations include:

| • | a stamping operation located in East Alton; |

| • | a rolling mill in Waterbury, Connecticut with rolling, annealing, leveling, plating and slitting capabilities for various products (“Somers Thin Strip”); |

| • | a manufacturing facility in Bryan, Ohio specializing in products sold in the automotive and electronics/electrical components end markets; and |

| • | a manufacturing facility in Cuba, Missouri that produces high frequency welded copper-alloy tube for heat transfer, utility, decorative, automotive and plumbing applications. |

3

Table of Contents

Olin Brass’ products are sold to original equipment manufacturers (“OEMs”), external customers, distributors/rerollers or to its affiliate, A.J. Oster. In the year ended December 31, 2014, approximately 17% of Olin Brass’ products were shipped to supply chain customers, of which management estimates that approximately 60% were directly associated with the building and housing or automotive sectors. For the year ended December 31, 2014, Olin Brass sold approximately 15% of its domestic copper-based products to A.J. Oster.

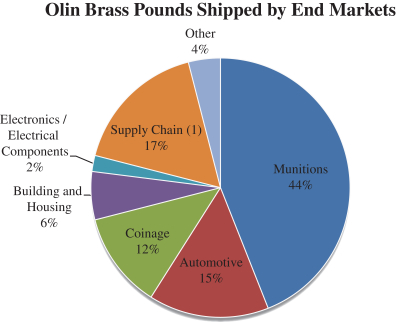

The following chart shows the primary end markets for Olin Brass’ products and the percentage of shipments for each during the year ended December 31, 2014.

| (1) | Approximately 60% of supply chain customer shipments are directly associated with the building and housing and automotive end markets according to management estimates. Shipments to A.J. Oster are reflected in the supply chain end market and are eliminated in consolidation. |

Munitions End Market

Olin Brass manufactures products utilized in both the military and commercial munitions markets, such as strip and cups, including for uses in shot shells, bullet jackets, centerfire, rimfire and small caliber military munitions.

Customers in this end market include major munitions producers in the U.S., as well as government facilities producing small caliber ammunition. Demand within this market is affected by the U.S. government’s security policies, as well as consumer demand for firearms and munitions. While munitions demand is predominantly domestic, occasional opportunities arise to supply U.S. alliance partners with these products.

Automotive End Market

Olin Brass manufactures both strip and fabricated products used as electronic and electrical connectors for use in automobiles. These products are made with HPAs, suitable for applications requiring high reliability, high temperature and low insertion force. For example, these electrical connectors, along with lead frames

4

Table of Contents

manufactured by us, are used in junction boxes, wiring harnesses, ignition systems, lighting and automotive entertainment systems.

Customers in this end market include primary automotive connector suppliers in the U.S. Although historically the business in this end market remained largely regional in the U.S., Olin Brass and A.J. Oster are collectively working to capitalize on the migration of automotive production to Mexico, where an A.J. Oster service center is located. Demand within this end market is affected by the level of consumer spending on automobiles, which is significantly dependent on overall economic conditions.

Coinage End Market

Olin Brass supplies coinage strip for use in the production of dollar coins, quarters, dimes and nickels. Customers in this end market include the United States Mint, for which we are a supplier contracted through 2017. Olin Brass has been a supplier to the United States Mint for over 30 years and expects to continue to renew its contract periodically with the United States Mint for the foreseeable future.

The demand within this end market is affected by the level of activities in retail transactions.

Building and Housing End Market

Olin Brass manufactures a variety of strip, welded tube and stamped parts used in commercial and residential buildings, such as faucets, locksets, decorative door hardware and hinges, which require workability, corrosion resistance and attractive appearance. Olin Brass also manufactures strip used in products that require electrical conductivity such as plug outlets, switches, lamp shells, other wiring devices, industrial controls, circuit breakers and switchgears. These products are generally manufactured with copper and copper-alloy sheet and strip, both HPAs and standard alloys, as well as copper-alloy welded tube.

Customers in this end market are OEMs producing building and housing products. These products are supplied either directly to customers or to A.J. Oster. Olin Brass also supplies building and housing products in China through Olin Luotong Metals.

While demand within this end market is affected by new residential housing, existing home sales and commercial construction, all of which are significantly dependent on overall economic conditions, the correlation between housing statistics and our sales is not entirely direct. Our key products are typically installed near the completion of construction, meaning there is an inherent lag time compared to housing starts, and sales of our building and housing products can be affected by factors such as housing mix (unit size, unit price point and the mix of multi-family versus single-family construction). Sales of our products can also be impacted by changes in the composition of materials and fixtures used in construction as well as import and export dynamics.

Electronics/Electrical Components End Market

Olin Brass manufactures strip used in integrated circuit sockets for circuit boards, electrical connectors for laptop computers, consumer electronics and appliances, and foils for flexible circuit applications. The strip manufactured in this end market is high in HPA content and is sold directly to end-use customers and distributors.

Customers in this end market are primarily electronics manufacturers that operate globally. A portion of these customers is serviced through A.J. Oster, and the remainder is supplied directly by Olin Brass, with our Somers Thin Strip facility providing the foil products on a global scale.

Demand within this end market is affected by consumer spending on electronics, which may fluctuate significantly as a result of economic conditions.

5

Table of Contents

International

Asia

Olin Brass’ operations in Asia primarily consist of Olin Luotong Metals; GBC Metals Asia Pacific PTE, a 100% owned subsidiary in Singapore; and the Dowa Joint Venture.

Established in 2002, Olin Luotong Metals is a service center that distributes HPAs, which are manufactured by Olin Brass in the U.S., into the Chinese market and other standard alloys, which are manufactured by Chinalco. Olin Luotong Metals performs value-added slitting and winding operations to these alloys prior to distribution. Its primary customers include major multinational manufacturers of components used in automotive, electronic and electrical applications. Almost all of Olin Luotong Metals’ sales are settled in U.S. dollars. During the year ended December 31, 2014, Olin Luotong Metals generated $38.4 million of net sales, which represented 5% of Olin Brass’ net sales (excluding sales to other Olin Brass affiliates). During the year ended December 31, 2014, 3% of Olin Brass’ product was shipped from Olin Luotong Metals.

Established in 1987, the main function of the Dowa Joint Venture is to market and sell HPAs licensed from Olin Brass and manufactured at Dowa Co.’s strip mills to key customers in Japan and southeast Asia. The primary markets served include electronic lead frames and electrical connectors. During the year ended December 31, 2014, the Dowa Joint Venture generated $72.2 million of net sales. As the Dowa Joint Venture is accounted for as a non-consolidated entity, these sales are not included in our total net sales or the net sales of Olin Brass.

GBC Metals Asia Pacific PTE markets and sells HPAs supplied primarily by Olin Brass and the Dowa Joint Venture into key electronics markets in Asia, including Singapore, Malaysia, South Korea, Taiwan and China. During the year ended December 31, 2014, GBC Metals Asia Pacific PTE generated $12.3 million of net sales, which represented 2% of Olin Brass’ net sales (excluding sales to other Olin Brass affiliates). During the year ended December 31, 2014, less than 1% of Olin Brass’ product was shipped from GBC Metals Asia Pacific PTE.

Sales volume of Olin Brass in Asia (excluding the Dowa Joint Venture), which includes pounds shipped from Olin Luotong Metals, GBC Metals Asia Pacific PTE and exports to Asia from our domestic Olin Brass locations, was 10.8 million pounds during the year ended December 31, 2014 (4% of total pounds shipped by Olin Brass) and primarily served the automotive, electronics/electrical components and building and housing end markets.

Europe

Olin Brass’ business in Europe is conducted through distribution arrangements with Aurubis U.K. in the United Kingdom and Türkis GmbH in Germany.

Sales volume of Olin Brass in the European region was 0.8 million pounds during the year ended December 31, 2014 (less than 1% of total pounds shipped by Olin Brass) and primarily served the munitions end market.

Others

Sales volume from Olin Brass’ international business in regions other than Asia and Europe, including sales shipments in Mexico and Canada, was 11.6 million pounds during the year ended December 31, 2014 (4% of total pounds shipped by Olin Brass) and primarily served the automotive and electronics/electrical components end markets.

Chase Brass

Chase Brass primarily manufactures brass rod, including round, hexagonal and other shapes, ranging from 1/4 inch to 4.5 inches in diameter. Its customers machine or otherwise process the rod for applications used in

6

Table of Contents

various end markets. Brass rod is primarily used for forging and machining products, such as valves and fittings. Key attributes of brass rod include its machinability, corrosion resistance and moderate strength. Brass rod is generally manufactured from copper or copper-alloy scrap.

All of Chase Brass’ rod is manufactured at its Montpelier, Ohio facility. In January 2008, Chase Brass acquired the order book, customer list and certain other assets of the North American operations of Bolton Metals Product Company (“Bolton”). This acquisition boosted Chase Brass’ capabilities and customer base.

Chase Brass has been able to capitalize on opportunities arising from regulation limiting lead content in potable water plumbing fixtures. We believe this legislation will continue to increase the need for low-lead and lead-free materials, including Eco Brass®.

Chase Brass’ products are sold directly to OEMs or to supply chain customers, including distributors, job shops and forging shops. During the year ended December 31, 2014, approximately 32% of Chase Brass’ products were sold to distributors, job shops and forging shops, which were allocated by management to Chase Brass’ end markets based on information gathered by management from these customers.

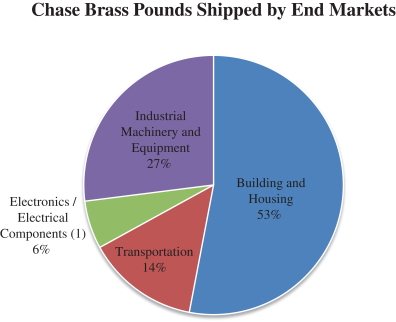

The following chart shows the primary end markets for Chase Brass’ products and the percentage of shipments for each during the year ended December 31, 2014. Note, during the year ended December 31, 2014, Chase Brass shipped a total of 221.3 million pounds, including 70.0 million pounds shipped to distributors, job shops and forging shops, which were allocated by management to Chase Brass’ end markets based on information gathered by management from such distributors, job shops and forging shops to calculate the pounds shipped to the various end markets presented below.

| (1) | Substantially all of Chase Brass’ electronics/electrical components shipments are directly associated with the building and housing and transportation end markets. |

Building and Housing End Market

Chase Brass manufactures brass rod for use in faucets, valves and fittings used in residential and commercial construction.

7

Table of Contents

Chase Brass produces a number of low-lead and lead-free products, or “green portfolio” products, which comply with state laws in California and Vermont as well as Federal standards (patterned after legislation enacted in California and Vermont) that became effective in January 2014. This legislation defines the allowed level of lead content in products used in plumbing and drinking water applications. Chase Brass’ Green Dot rod (Eco Brass®) and Eco Brass® ingot products are part of the green portfolio, and Chase Brass is the exclusive licensee of the intellectual property rights for their production, sale and distribution in North America. Chase Brass also manufactures other non-patented green portfolio products. Our green portfolio products accounted for approximately 15% of pounds shipped by Chase Brass during the year ended December 31, 2014. Customers in this end market include major faucet, valve and fitting manufacturers who are producing multiple products using green portfolio materials.

While demand within this end market is affected by new residential housing, existing home sales and commercial construction, all of which are significantly dependent on overall economic conditions, the correlation between housing statistics and our sales is not entirely direct. Our key products are typically installed near the completion of construction, meaning there is an inherent lag time compared to housing starts, and sales of our building and housing products can be affected by factors such as housing mix (unit size, unit price point and the mix of multi-family versus single-family construction). Sales of our products can also be impacted by changes in the composition of materials and fixtures used in construction, as well as import and export dynamics.

Transportation End Market

Chase Brass manufactures brass rod for uses in automobiles and heavy trucks. Specific applications include heavy truck braking systems, tire valves, temperature sensors and various truck and automotive fittings. Demand within this end market is affected by levels of transportation activity, levels of maintenance capital spending by transportation companies and the level of commercial truck fleet replacement activity, all of which are affected significantly by overall economic conditions. Customers in this end market include major OEMs in the transport industry and customers who support domestic automotive production.

Electronics/Electrical Components End Market

Chase Brass manufactures brass rod used for telecommunication applications, including products such as coaxial connectors and traps and filters for cable television, as well as larger connectors supporting the cell tower industry. Demand within this end market is affected by consumer spending along with new home construction.

Customers within these end markets include major manufacturers of specialty products for use in home and commercial construction, both of which are very dependent on overall economic conditions. Management believes that substantially all of the shipments in this market segment are directly associated with the building and housing market and transportation end markets.

Industrial Machinery and Equipment End Market

Chase Brass manufactures brass rod used in industrial valves and fittings. Demand within this end market is affected by capital spending levels, U.S. GDP growth and industrial production growth in the U.S.

Customers in this end market include various major diversified manufacturers and a variety of screw machine companies supporting OEMs.

International

Chase Brass primarily supplies products within North America. Sales volume to Canada and Mexico was 19.4 million pounds (9% of total pounds shipped by Chase Brass) during the year ended December 31, 2014.

8

Table of Contents

A.J. Oster

A.J. Oster is a processor and distributor of primarily copper and copper-alloy sheet, strip and foil, operating six strategically-located service centers in the U.S., Puerto Rico and Mexico. Key A.J. Oster competitive advantages are short lead-times with high reliability, small-quantity deliveries and a wide range of high-quality, copper-based products.

For the year ended December 31, 2014, Olin Brass provided A.J. Oster with 54% of its copper-based products. Aurubis is A.J. Oster’s second largest supplier after Olin Brass, supplying approximately 30% of A.J. Oster’s copper-based products in the year ended December 31, 2014. Many of the coils purchased from Olin Brass and Aurubis are full-width and require slitting.

Each A.J. Oster service center reliably provides a broad range of high-quality products at quick lead-times in small quantities. These capabilities, combined with A.J. Oster’s operations of precision slitting, hot tinning, traverse winding, cutting, edging and special packaging, provide value to a broad customer base.

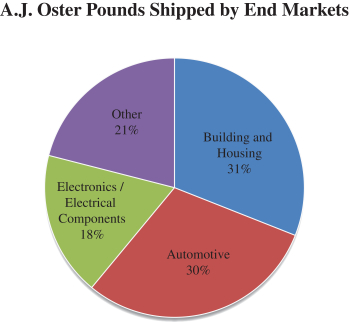

The following chart shows the primary end markets for A.J. Oster’s products and the percentage of shipments for each during the year ended December 31, 2014.

Building and Housing End Market

A.J. Oster slits and distributes copper-alloy strip and aluminum foil used for products in commercial and residential buildings. The two primary applications are electrical and hardware.

Electrical products are primarily for wiring devices. Other applications include switchgears, switches, controls and circuit breakers. Several of our customers for these products are in Puerto Rico or Mexico. These customers require short lead-times, small quantities and numerous specifications. A.J. Oster’s capabilities are well-suited for these geographic locations and the stringent service requirements of the electrical end market because A.J. Oster is able to provide customers with high-quality metals, in less-than-truckload quantities, and can deliver products shortly after receiving orders.

9

Table of Contents

Hardware products include products such as faucets, window trim, locksets, hinges and kick plates.

While demand in the building and housing end market is affected by new residential housing existing home sales and commercial construction, all of which are significantly dependent on overall economic conditions, the correlation between housing statistics and our sales is not entirely direct. Our key products are typically installed late in the housing construction cycle, meaning there is an inherent lag in volumes, and sales of our building and housing products can be affected by factors such as housing mix (unit size, unit price point and the mix of multi-family versus single-family construction). Sales of our products can also be impacted by the actual timing of housing starts and completions as well as to changes in the materials and fixtures used in construction that may contain fewer copper products or materials and fixtures than were used in the past as well as import and export dynamics.

Automotive End Market

A.J. Oster slits, traverse winds, hot tin dips, coats and distributes copper-alloy strip and aluminum foil used in automobile production. Primary customer products are electrical connectors, automotive trim and heat exchangers.

A.J Oster has excellent geographic coverage to service this market. Our A.J. Oster subsidiary in Queretaro, Mexico is well-positioned to take advantage of the growing number of second-tier automobile component suppliers that are growing in Mexico.

Demand within this end market is affected by the level of consumer spending on automobiles, which is significantly dependent on overall economic conditions.

Electronics/Electrical Components End Market

A.J. Oster slits, traverse winds, hot tin dips, coats and distributes copper-alloy strip used for electrical connectors in computers, consumer electronics and automobiles. The markets served by A.J. Oster are service intensive and therefore require A.J. Oster capabilities.

The demand within this end market is affected by consumer spending on electronics, which may fluctuate significantly as a result of economic conditions.

International

A.J. Oster’s North American operations include a service center in central Mexico. The facility is located in Queretaro in the center of Mexico’s industrial triangle marked by Mexico City, Monterey and Guadalajara and is easily accessible by highway connections to the United States.

Automakers in Mexico produce approximately three million automobiles per year. Automotive sub-suppliers that consume copper-alloy strip are now locating facilities in central Mexico in order to support primary automotive manufacturing.

A.J. Oster is well positioned to capture growth in the Mexican market for copper-alloy strip because of its ability to provide Mexican customers with high-quality metals, in less-than-truckload quantities and to deliver the products shortly after receiving orders. Our customers located in Mexico will require first-class service and quality levels traditionally demanded by the electrical, electronics and automotive industries. Meeting these demands is a core competency of A.J. Oster.

Net sales from A.J. Oster Mexico were $46.9 million during the year ended December 31, 2014 (15% of A.J. Oster net sales). During the year ended December 31, 2014, 14% of A.J. Oster’s product was shipped from Mexico.

10

Table of Contents

Raw Materials and Supply

We manufacture our products from scrap metal (both internally generated and externally sourced) or virgin raw materials. During the year ended December 31, 2014, 88% of our metal came from scrap metal, and the remainder came from virgin raw materials. Olin Brass utilizes both scrap and virgin raw materials, while Chase Brass primarily uses scrap.

Virgin raw materials, including copper cathode, are purchased at a premium on the London Metal Exchange (“LME”) or Commodities Exchange (“COMEX”) or directly from key dealers that support producers around the world. Although virgin raw materials are more expensive compared to scrap, we use them to produce HPAs and other products that require exact specifications.

Customers

Our customer base is broadly diversified, spanning various North American end markets, including building and housing, munitions, automotive, transportation, coinage, electronics/electrical components, industrial machinery and equipment and general consumer end markets. In the year ended December 31, 2014, we sold over 15,000 different stock keeping units (“SKUs”) to nearly 1,700 customers.

In the year ended December 31, 2014, net sales from our foreign entities were $97.6 million. We have long-term relationships with our customers, many of which are secured through short-term contracts. Our relationships with many of our significant customers have lasted more than 30 years.

Each of our three operating segments has at least 10% of their net sales concentrated in a large customer during the year ended December 31, 2014. Olin Brass generated 21% of its total net sales from one customer and 19% of its total net sales from another customer. A.J. Oster generated 13% of its total net sales from one customer. Chase Brass generated 14% of its total net sales from one customer. On a consolidated basis, we did not generate more than 10% of our total net sales from any one customer for the year ended December 31, 2014.

Competition

We compete with other companies on price, service, quality, breadth, and availability of product both domestically and internationally. We believe we have been able to compete effectively because of our high levels of service, breadth of product offering, knowledgeable and trained sales force, modern equipment, numerous locations, geographic dispersion, economies of scale, and sales volume.

The North American market for brass and copper strip and sheet and brass rod consists of a few large participants and a few smaller competitors for Olin Brass and Chase Brass. A.J. Oster’s competition consists of a number of smaller competitors. Our international competitors are based principally in Europe and Asia.

Our largest competitors in each of the markets in which we operate are the following:

| • | Aurubis and PMX Industries, Inc.: manufacturers of copper and copper-alloys in the form of strip, sheet and plate (Olin Brass); |

| • | ThyssenKrupp Materials NA, Copper and Brass Sales Division: processor and distributor of copper, brass, stainless and aluminum products; Wieland Metals, Inc.: re-roll mill and service center for copper and copper-alloy strip (A.J. Oster); |

| • | Mueller Industries, Inc.: manufacturer of brass rod (Chase Brass). |

We use data published by Copper Development Association Inc. (“CDA”), Copper and Brass Servicenter Association, Inc. (both independent industry associations) and management estimates to determine our market share. Using this information, for the year ending December 31, 2014:

| • | Olin Brass accounted for 33% of North American shipments (including shipments to A.J. Oster) of copper and brass alloys in the form of sheet, strip and plate; |

11

Table of Contents

| • | A.J. Oster accounted for 32% of North American shipments of copper and brass, sheet and strip products from distribution centers and rerolling facilities; and |

| • | Chase Brass accounted for 48% of North American shipments of brass rod, not including imports. |

Government Regulation and Environmental Matters

Bactericidal Products

Through its membership in the CDA, Olin Brass has completed the required Federal Environmental Protection Agency (“EPA”) and applicable state registration processes that allow it to market its CuVerro™ products with certain approved bactericidal claims. Laboratory testing has shown that bactericidal copper touch surfaces made with CuVerro™ kill more than 99.9% of bacteria within two hours. We believe that Olin Brass’ copper-based CuVerro™ materials are in compliance, in all material respects, with EPA standards for products recognized by the EPA as having bactericidal properties.

In connection with these EPA registrations, the CDA is required to implement a “stewardship” plan that is designed to ensure that bactericidal copper alloys are properly used and marketed. The stewardship requirement reflects the EPA’s concern that the improper marketing of bactericidal copper alloys could lead users to mistakenly believe that the use of these products is a simple solution to fight infections. The stewardship efforts are intended to emphasize that all marketing statements are consistent with the approved EPA product label, including the need to state clearly that the alloys are intended as a supplement to, but are not a substitute for, standard cleaning and sanitization procedures. These standards also apply to marketing by our customers who use CuVerro™ in their products.

Even though the marketing of copper products as bactericidal started in 2008, the manufacturers of such products are still in the process of determining what specific bactericidal claims may be made in compliance with the EPA’s and Federal Insecticide, Fungicide and Rodenticide Act’s (“FIFRA”) requirements. Therefore, there remains some uncertainty when determining whether a particular marketing approach is consistent with the EPA registration requirements. Accordingly, it is possible that we or other manufacturers may be found to be non-compliant by the EPA for current, past or future marketing claims and activities, despite efforts to comply. The EPA can impose administrative or judicial sanctions and penalties against those violating federal regulations, including corrective disclosures, civil administrative penalties, stop sale orders, cancellations of registrations, seizures, injunctions and criminal sanctions. Any failure by us or our customers who use CuVerro™ in their products to comply with FIFRA’s requirements with respect to CuVerro™ could therefore expose us to various enforcement actions or other claims or adverse impacts to our reputation. The stewardship program required under the EPA registration is an industry-wide activity, and the actions of other CDA members could jeopardize the marketing of all bactericidal copper products registered through the CDA (including CuVerro™). If the EPA were to determine that the stewardship program is not being implemented effectively, the EPA may initiate a variety of corrective actions, which could adversely affect us and other CDA members, including cancelling all CDA registrations. If the EPA were to initiate an enforcement action that affects us or our customers, it may have a material adverse effect on our ability to market CuVerro™ as an bactericidal product.

Lead-free and Low-lead Plumbing Products

New regulations designed to reduce lead content in drinking water plumbing devices provide an opportunity for future growth. Chase Brass is a premier provider of specialized lead-free products and low-lead alloys. Federal legislation in the United States (the Reduction of Lead in Drinking Water Act, which was patterned after legislation enacted in California and Vermont) required the reduction of lead content in all drinking water plumbing devices beginning in January 2014. This legislation presents a significant growth opportunity for Chase Brass. Our Eco Brass® products meet Federal, California and Vermont standards and can be used to produce cast, machined and forged faucet parts. We currently supply major faucet, valve and fitting manufacturers who produce multiple products using machined Eco Brass® parts.

12

Table of Contents

Environmental

Our operations are subject to a number of Federal, state and local laws and regulations relating to the protection of the environment and to workplace health and safety. In particular, our operations are subject to extensive Federal, state and local laws and regulations governing the creation, transportation, use, release and disposal of wastes, air and water emissions, the storage and handling of hazardous substances, environmental protection, remediation, workplace exposure and other matters. Hazardous materials used in our operations include general commercial lubricants, cleaning solvents and cutting oils. Among the regulated activities that occur at some of our facilities are: the accumulation of scrap metal, which is sold for recycling; and the generation of hazardous waste, solid wastes and wastewaters, such as water from burning tables operated at some of our facilities. The generation, storage, and disposal of these wastes is done in accordance with the Federal Water Pollution Control Act, the Comprehensive Environmental Response, Compensation, and Liability Act (“CERCLA”) and the Resource Conservation and Recovery Act, and we use third-party commercial disposal services as permitted by these laws for the removal and disposal of these wastes. The storage, handling and use of lubricating and cutting oils and small quantities of maintenance-related products and chemicals are also regulated under environmental laws, and the health hazards of these materials are communicated to employees pursuant to the Occupational Safety and Health Act.

In general, our facilities’ operations do not involve the types of emissions of air pollutants, discharges of pollutants to land or surface water, or treatment, storage or disposal of hazardous waste which would ordinarily require Federal or state environmental permits. Some of our facilities possess authorizations under the Clean Air Act for air emissions from paints and coatings. At some locations, we also possess hazardous materials storage permits under local fire codes or ordinances for the storage of combustible materials such as oils or paints. At some facilities we possess state or local permits for on-site septic systems. Our cost of obtaining and complying with such permits has not been, and is not anticipated to be, material.

We believe that we are in substantial compliance with all applicable environmental and workplace health and safety laws and do not currently anticipate that we will be required to expend any substantial amounts in the foreseeable future in order to meet such requirements. Nevertheless, some of the properties we own or lease are located in areas with a history of heavy industrial use, and are near sites listed on the CERCLA National Priority List, CERCLIS and comparable state listings. CERCLA establishes responsibility for clean-up without regard to fault for persons who have released or arranged for disposal of hazardous substances at sites that have become contaminated and for persons who own or operate contaminated facilities. In many cases, courts have imposed joint and severable liability on parties at CERCLA clean-up sites. We have a number of properties located in or near industrial or light industrial use areas; accordingly, these properties may have been contaminated by pollutants which may have migrated from neighboring facilities or have been released by prior occupants. Some of our properties have been affected by releases of cutting oils and similar materials and we are investigating and remediating such known contamination pursuant to applicable environmental laws. The costs of these clean-ups have not been material in the past. We are not currently subject to any material claims or notices with respect to clean-up or remediation under CERCLA or similar laws for contamination at our leased or owned properties or at any off-site location. However, we could be notified of such claims in the future. It is also possible that we could be identified by the EPA, a state agency, or one or more third parties as a potentially responsible party under CERCLA or under analogous state laws.

Pursuant to the agreement, dated November 19, 2007, by which we purchased our current operating locations from Olin Corporation, Olin Corporation agreed to retain responsibility for a wide range of liabilities under environmental laws arising out of existing contamination on our properties, and agreed to indemnify us without limitation with respect to these liabilities. Specifically, Olin Corporation retained responsibility for:

| • | compliance with all obligations to perform investigations and remedial action required under the Connecticut Real Property Transfer Act at properties in Connecticut; |

| • | pending corrective action/compliance obligations under the Federal Resource Conservation and Recovery Act for certain areas of concern at our East Alton, Illinois facility; and |

13

Table of Contents

| • | all obligations under environmental laws arising out of 24 additional specifically identified areas of concern on various of our properties. |

Olin Corporation also retained complete responsibility for all liabilities arising out of then pending governmental inquiries relating to environmental matters; for “any liability or obligation in connection with a facility of the Business to the extent related to pre-Closing human exposure to Hazardous Materials, including asbestos-containing materials”; and for “any liability or obligation in connection with the off-site transportation or disposal of Hazardous Materials arising out of any pre-Closing operations of the Business”.

Since 2007, Olin Corporation has continued to perform environmental remedial actions on our properties, including the East Alton, Illinois and Waterbury, Connecticut properties, and continues to work closely with us to address matters covered by the indemnity. Because of the Olin Corporation indemnity, we have not been required to engage in any significant environmental cleanup activity on our properties and do not currently have any material reserves established to address environmental remedial requirements.

Employees

The following table shows the composition of our workforce by operating segment and Corporate as of December 31, 2014.

| Employees | % of Total | |||||||

| Olin Brass |

1,287 | 68 | % | |||||

| A.J. Oster |

276 | 15 | % | |||||

| Chase Brass |

310 | 16 | % | |||||

| Corporate |

23 | 1 | % | |||||

|

|

|

|

|

|||||

| Total |

1,896 | 100 | % | |||||

|

|

|

|

|

|||||

As of December 31, 2014, 1,182, or approximately 62%, of our employees at various sites were members of unions. We have generally maintained good relationships with all unions and employees, which has been an important aspect of our ability to be competitive in our industry. Generally, our various agreements with unions in the United States have contractual terms which range from 1 to 4 years.

Since our acquisition of the worldwide metals business of Olin Corporation in November 2007, we have not experienced any work stoppages at any of our facilities. We believe we will continue to be able to renew the outstanding collective bargaining agreements upon acceptable terms. Historically, we have succeeded in negotiating new collective bargaining agreements without a strike.

Research and Development

As of December 31, 2014, we employed six scientists in metallurgy and electrochemistry. We intend to continue to invest in research and development to develop new products and to expand our value-added services to meet our customers’ needs.

Our research and development expenditures for the year ended December 31, 2014 were $1.6 million (less than 1% of total net sales).

Risk Management and Insurance

The primary risks in our operations are personal injury, property damage, transportation, criminal acts, risks associated with international operations, directors’ and officers’ liability and general commercial liabilities. We are insured against general commercial liabilities, automobile accidents (including injury to employees and physical damage of goods and property and employer liabilities), directors’ and officers’ liability, crime, foreign

14

Table of Contents

risks, environmental liability, aircraft products liability, ocean cargo liability and flood through insurance policies provided by various insurance companies up to amounts we consider sufficient to protect against losses due to claims associated with these risks.

We also maintain bonds with certain Federal, state and international authorities to insure against risks relating to, among other things, delays due to customs clearances, compliance with certain laws and regulations and import and export of goods.

Safety

Consistent with other strategic initiatives, management is pursuing a ‘Best in Class’ performance status for employee safety. Our management has committed itself to achieving a formal ‘Star’ certification within the Occupational Safety and Health Administration (“OSHA”) sponsored Voluntary Protection Program, or VPP. A formal VPP Star certification is OSHA’s official recognition for outstanding efforts between employers and employees for achieving exemplary occupational safety and health. The Safety Excellence / VPP initiative shifts the safety paradigm to an aggressive proactive approach that stresses strong employee participation and collaboration, management accountability, employee training and hazard elimination as core foundational elements.

Patents, Trademarks and Other Intellectual Property Rights

Chase Brass has an exclusive intellectual property license, valid through the expiration of the U.S. patents in 2027, to produce and sell Eco Brass® rod and ingot in North America, granted by Mitsubishi Shindoh Company, Ltd., the Japanese company that owns the relevant intellectual property rights. We have sublicensed our rights to three sublicensees, none of which is currently a competitor of any of our subsidiaries or segments. These sublicensing arrangements are valid until the expiration of the relevant patents in North America. In addition, we have alloy licensing arrangements with companies in Germany, Japan and China.

As of December 31, 2014, we owned 182 patents, of which 49 were U.S. patents. We also own various trademarks relating to our products. As of December 31, 2014, we owned 26 trademarks, of which 12 are U.S. trademarks. Most of these are owned by GBC Metals, LLC, a wholly owned subsidiary of ours. We license the marks OLIN BRASS and OLIN METALS for metal products from Olin Corporation. These licenses continue unless we breach the license agreement. We also license stylized versions of these marks from Olin Corporation and the license to the stylized version includes an annual termination option.

We license the intellectual property rights related to certain proprietary alloy systems to other major brass mills around the world, including Dowa Co. As of December 31, 2014, there were nine such licenses.

Government Contract

The United States Mint is a significant customer of Olin Brass, which has been an authorized supplier to the United States Mint since 1969 and currently has a contractual arrangement to supply nickel and brass coinage strip to multiple United States Mint facilities through 2017. The United States Mint can terminate our contract in whole or in part when it is in the best interest of the United States Mint to do so and any damages payable to us by the United States Mint for such termination would not include lost profits.

Seasonality and Backlog

There is a slight decrease in our net sales in the fourth quarter as a result of the decrease in demand due to customer shutdowns for the holidays and year-end maintenance of plants and inventory by customers. We also typically experience slight working capital increases in the first fiscal quarter.

15

Table of Contents

Available Information

Our website address is http://www.gbcholdings.com. We make available on our website, free of charge, the periodic reports that we file with or furnish to the Securities and Exchange Commission (“SEC”), as well as all amendments to these reports, as soon as reasonably practicable after such reports are filed with or furnished to the SEC. We also make available on our website or in printed form upon request, free of charge, our Corporate Governance Guidelines, Code of Business Conduct and Ethics, charters for the standing committees of our Board of Directors and other information related to the Company. We are not including the information contained on our website as a part of, or incorporating it by reference into, this report.

The public may read and copy any materials that we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington D.C. 20549. The public may obtain information about the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an internet site (http://www.sec.gov) that contains reports, proxy and information statements and other information related to issuers that file electronically with the SEC.

We are exposed to various risks as we operate our businesses. To provide a framework to understand our operating environment of the Company, we are providing a brief explanation of the more significant risks associated with our businesses. Although we have tried to identify and discuss key risk factors, others could emerge in the future.

Risks Related to Our Business

Our business, financial condition and results of operations or cash flows could be negatively affected by downturns in economic cycles in general or cyclicality in our end markets, both inside and outside of the U.S. Our future growth also depends, to a significant extent, on improvements in general economic conditions and in conditions in our end markets.

Many of our products are used in industries that are, to varying degrees, cyclical and have historically experienced periodic downturns due to factors such as economic conditions, energy prices, the availability of credit, consumer sentiment, demand and other factors beyond our control. These economic and industry downturns have resulted in diminished product demand and excess capacity for our products. The significant deterioration in economic conditions that occurred during the second half of 2008 and continued into 2009 resulted in disruptions in a number of our end markets. Any future economic disruptions may negatively impact our end markets or the consumers served by those end markets, which would adversely affect our operating results.

Future disruptions in the commercial credit markets may impact liquidity in the global credit market, and we are not able to predict the impact any such worsening conditions would have on our customers in general, and our results of operations specifically. Businesses in one or more of the end markets that we serve, or consumers in one or more of the end markets that our customers serve, may postpone or choose not to make purchases in response to economic uncertainty, tighter credit, negative financial news, unemployment, interest rates, adverse consumer sentiment and declines in housing prices or other asset values.

In particular, the historically cyclical and volatile building and housing sector in the U.S. has not yet fully recovered from the downturn that began in 2007. If the housing, remodeling and residential and commercial construction markets stagnate or deteriorate, demand from such markets for our products, especially our brass rod products, is likely to be adversely affected. Any recovery in such markets will not necessarily directly correlate with increased sales or profitability. Our key products are typically installed late in the housing construction cycle, meaning there is an inherent lag in volumes, and sales of our building and housing products

16

Table of Contents

can be affected by factors such as housing mix (unit size, unit price point and the mix of multi-family versus single-family construction). Sales of our products can also be impacted by the actual timing of housing starts and completions as well as to changes in the materials and fixtures used in construction that may contain fewer copper products or materials and fixtures than were used in the past. In addition, competition from imports and other sources may also dampen the effects of any such recovery on our results of operations.

Similarly, the automotive end market has in the past experienced significant downturns in connection with, or in anticipation of, declines in general economic conditions. Demand for vehicles depends largely on the strength of the economy, employment levels, consumer confidence levels, the availability and cost of credit and the cost of fuel. Negative economic developments could reduce demand for new vehicles, causing our customers to reduce their vehicle and automotive component part production in North America.

The coinage and general consumer end markets are also affected by economic cycles. Demand for coinage-related products generally increases with the number of cash transactions that occur, and the number of cash transactions generally increases during periods of economic growth. Demand for consumer goods is also very sensitive to economic conditions and drives demand in our electronics/ electrical components end market.

As a result, cyclicality in economic conditions and in the end markets that we serve could have a material adverse effect on our business, financial condition, results of operations and cash flows. Our growth prospects also depend, to a significant extent, on the degree by which general economic conditions and conditions in the end markets that we serve continue to improve.

Failure to maintain our balanced book approach would cause increased volatility in our profitability and our operating results and may result in significant losses.

Copper scrap and cathode are subject to significant cyclical price fluctuations. The availability and price of copper scrap and cathode depend on a number of factors outside our control, including general economic conditions, international demand for metal and internal recycling activities by primary copper producers and other consumers of copper. The cost of copper scrap and cathode represents the largest component of our cost of sales.

We use our balanced book approach to substantially reduce the impact of metal price movements on operating margins from our non-toll sales, which are sales for which we assume responsibility for metal procurement and then recover the metal replacement cost from the customer. Non-toll sales represented approximately 75% of our unit sales volume during the year ended December 31, 2014. Under our balanced book approach, we seek to match the timing, quantity and price of the metal component of net sales with the timing, quantity and price of replacement metal purchases on all of our non-toll sales. We use a combination of matching price date of shipment terms, firm price terms and derivatives transactions to achieve our balanced book. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Factors Affecting Our Results of Operations—Balanced Book”.

We may not be able to maintain our balanced book if our customers become unwilling to bear metal price risk through the matching of price date of shipment terms. We may also not be able to find counterparties for the derivatives transactions entered into in connection with firm price terms, and the cost of those derivatives transactions may increase such that entering into such transactions is no longer cost-effective to us. Those risks may increase during periods of very high copper prices or increased volatility in those prices.

If we fail to effectively maintain our balanced book, our profitability will be significantly affected by fluctuations in metal costs and our ability to recoup metal costs through product pricing. As a result, the volatility of our results of operations would increase dramatically. Furthermore, if we are unable to maintain our balanced book approach, we will potentially replace metal at a different price than the price recovered from the customer, generating a loss in circumstances where the replacement price is higher than the price recovered from the customer.

17

Table of Contents

Although we maintain our balanced book approach, metal costs still affect our profitability through “shrinkage” and inventory valuation adjustments.

Shrinkage loss, which is primarily the loss of raw metal that occurs in the melting and casting operations, is an inherent part of a metal fabrication and conversion business. Despite our use of our balanced book approach to mitigate the impact of metal price fluctuations, we must bear the cost of any shrinkage during production, which may increase the volatility of our results of operations. Because we process a large amount of metal in our operations, a small increase in our shrinkage rates can have a significant effect on our margins and profitability. In addition, if metal prices increase, the same amount of shrinkage will have a greater effect on our manufacturing costs and have a more significant negative impact on our margins and profitability.

The market price of metals and related scrap used in production is subject to significant volatility. During periods when open-market prices decline below net book value, we may need to record a provision to reduce the carrying value of our inventory and increase cost of sales. Additionally, the cost of our inventories is primarily determined using the last-in, first-out (“LIFO”) method. Under the LIFO inventory valuation method, changes in the cost of raw materials and production activities are recognized in cost of sales in the current period. In a period of rising raw material prices, cost of sales expense recognized under LIFO is generally higher than the cash costs incurred to acquire the inventory sold. Conversely, in a period of declining raw material prices, cost of sales recognized under LIFO is generally lower than cash costs incurred to acquire the inventory sold. The impact of LIFO accounting on our financial results may be significant with respect to period-to-period comparisons. During 2013, certain domestic metal inventory quantities were reduced, resulting in a liquidation of LIFO inventory layers carried at lower costs prevailing in prior years as compared with metal prices prevailing in the market at the time of the inventory depletion and the effect of this reduction of inventory decreased cost of sales by $2.0 million. During 2014, certain domestic metal inventory quantities were reduced, resulting in a liquidation of LIFO inventory layers carried at higher costs prevailing in prior years as compared with metal prices prevailing in the market at the time of the inventory depletion and the effect of this reduction of inventory increased cost of sales by $0.6 million. See “Management’s Discussion and Analysis of Operating Results and Financial Condition—Key Factors Affecting Our Results of Operations—Metal Cost”.

Because our balanced book approach does not reduce the effects of fluctuations in metal prices on our working capital requirements, higher metal prices could have a negative effect on our liquidity.

Our balanced book approach does not reduce the impact of the volatility in metal prices on our working capital requirements. Metal prices impact our investment in working capital because our collection terms with our customers are longer than our payment terms to our suppliers. As a result, when metal prices are rising, even if the number of pounds of metal we process does not change, we tend to use more cash or draw more on our asset-based revolving loan facility (“ABL Facility”) to cover the cash flow delay from material replacement purchase to cash collection. Thus, when metal prices increase, our working capital may be negatively affected as we are required to draw more on our cash or available financing sources to pay for raw materials. As a result, our liquidity may be negatively affected by increasing metal prices. Metal price volatility may also require us to draw on working capital sources more quickly and unpredictably, and therefore at higher cost. See “Management’s Discussion and Analysis of Operating Results and Financial Condition—Key Factors Affecting Our Results of Operations—Metal Cost”.

Limited access to raw materials, infrastructure or fuel could negatively affect our business, financial condition or results of operations or cash flows.

Our ability to fulfill our customer orders in a timely and cost-effective manner depends on our ability to secure a sufficient and constant supply of raw materials and fuel and access to infrastructure adequate to fulfill our business needs. Although we often seek to source our copper from scrap, including internally generated scrap and repurchases of our customers’ scrap, where scrap is either not available or is not appropriate for use, we use virgin raw materials such as copper cathode, which are generally more expensive than scrap. We depend on natural gas for our manufacturing operations and source natural gas through open-market purchases.

18

Table of Contents

We depend on scrap for our operations and acquire our scrap inventory from numerous sources. These suppliers generally are not bound by long-term contracts and have no obligation to sell scrap metals to us. In periods of low metal prices, suppliers may elect to hold scrap waiting for higher prices. The supply of scrap metal available to us could be adversely impacted at any time due to slowdowns in industrial production or consumer consumption. If an adequate supply of scrap metal is not available to us, we would be unable to use scrap as a source of supply at desired volumes, forcing us to use a larger amount of more expensive virgin raw materials and our results of operations and financial condition would be materially and adversely affected. Furthermore, with the growth of the economy of China, the demand for certain raw materials has increased significantly while the supply of such raw materials may not have increased correspondingly. In addition, the SEC has recently issued an order amending a rule to allow shares of a physically backed copper exchange traded fund (“ETF”) to be listed and publicly traded. Such fund, and other copper ETFs like it, hold copper cathode as collateral against their shares. The acquisition of copper cathode by copper ETFs and other similar entities may materially decrease or interrupt the availability of copper for immediate delivery in the United States, which could materially increase our cost of copper and copper scrap, result in potential supply shortages, and increase price volatility for copper and copper scrap. All of the above factors may affect our ability to secure the necessary raw materials in a cost-effective manner for production of our products.

We may experience disruptions in the supply of natural gas as a result of delivery curtailments to industrial customers due to extremely cold weather. We may also experience disruptions or increases in cost with respect to our access to water, electrical power, transport and wastewater treatment services and other infrastructure (including those subject to our transition services agreement with the parent of our predecessor). We may also experience other delays or shortages in the supply of raw materials. If we are unable to obtain adequate, cost efficient or timely deliveries of required raw materials and fuel or adequate and cost-effective access to infrastructure, we may be unable to manufacture sufficient quantities of products on a timely basis. This could cause us to lose sales, incur additional costs, delay new product introductions or harm our reputation in the end markets that we serve. An inability to find an adequate and timely supply of raw materials or adequate and cost-effective access to infrastructure could have a material adverse effect on our profit margin, and in turn on our business, financial condition, results of operations or cash flows.

Increases in the cost of energy could cause our cost of sales to increase, thereby reducing operating results and limiting our operating flexibility.

In 2014, the cost of energy and utilities represented approximately 7% of our non-metal cost of sales. The prices of natural gas and electricity can be particularly volatile. As a result, our natural gas and electricity costs may fluctuate dramatically, and we may not be able to mitigate the effect of higher natural gas and electricity costs on our cost of sales. A substantial increase in energy costs could cause our operating costs to increase and our business, financial condition, results of operations and cash flows may be materially and adversely affected. Although we attempt to mitigate short-term volatility in natural gas and electricity costs through the use of derivatives contracts, we may not be able to eliminate the long-term effects of such cost volatility. Furthermore, in an effort to offset the effect of increasing costs, we may have also limited our potential benefit from declining costs.

Our substantial leverage and debt service obligations may adversely affect our financial condition and restrict our operating flexibility, including our ability to raise additional capital to fund our operations, limit our ability to react to changes in the economy or our industry and prevent us from meeting our obligations under our indebtedness.

We are highly leveraged. As of December 31, 2014, our total indebtedness was $380.8 million. We also had an additional $199.5 million available for borrowing under the ABL Facility as of that date. Based on the amount of indebtedness outstanding and applicable interest rates at December 31, 2014, our annualized cash interest expense would be $36.1 million, which includes $0.5 million of interest expense related to our capital lease obligations. Additionally, we may potentially borrow under the ABL Facility, which is a floating-rate obligation, and thus, the related interest expense is subject to increase in the event interest rates were to rise.

19

Table of Contents

Our substantial indebtedness and debt service obligations could have important consequences for investors, including:

| • | they may impose, along with the financial and other restrictive covenants under our credit agreements, significant operating and financial restrictions, including our ability to borrow money, dispose of assets or raise equity for our working capital, capital expenditures, dividend payments, debt service requirements, strategic initiatives or other purposes; |

| • | they may limit our flexibility in planning for, or reacting to, changes in our operations or business; |

| • | we may be more highly leveraged than some of our competitors, which may place us at a competitive disadvantage; and |

| • | they may make us more vulnerable to downturns in our business or the economy. |

Any of these consequences could have a material adverse effect on our business, financial condition, results of operations, prospects and ability to satisfy our obligations under our indebtedness. In addition, there would be a material adverse effect on our business, financial condition, results of operations and cash flows if we were unable to service our indebtedness or obtain additional financing, as needed.

Covenants under our debt agreements impose operating and financial restrictions. Failure to comply with these covenants could have a material adverse effect on our business, financial condition, results of operations or cash flows.

The agreement governing the ABL Facility and the indenture governing the 9.50% Senior Secured Notes due 2019 (“Senior Secured Notes”) contain various covenants that limit or prohibit our ability, among other things, to:

| • | incur or guarantee additional indebtedness; |

| • | pay dividends on our capital stock or redeem, repurchase, retire or make distributions in respect of our capital stock or subordinated indebtedness or make certain other restricted payments; |

| • | make certain loans, acquisitions, capital expenditures or investments; |

| • | sell certain assets, including stock of our subsidiaries; |

| • | enter into certain sale and leaseback transactions; |

| • | create or incur certain liens; |

| • | consolidate, merge, sell, transfer or otherwise dispose of all or substantially all of our assets; |

| • | enter into certain transactions with our affiliates; and |

| • | engage in certain business activities. |

The agreement governing the ABL Facility also contains a financial covenant that requires us to maintain a fixed charge coverage ratio that is tested whenever excess availability, as defined in such agreement, falls below a certain level. The fixed charge coverage ratio, as defined in the agreement, requires us to maintain a minimum ratio of “EBITDA” (as defined in the agreement governing the ABL Facility) to the amount of our fixed charges for the twelve consecutive months prior to the date on which the ratio is tested. The agreement governing the ABL Facility also requires excess availability to remain above a certain level to avoid default. For more information regarding these covenants, please see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Covenant Compliance” and “Outstanding Indebtedness”.

As of December 31, 2014, we were in compliance with all of the covenants contained in our debt agreements. A violation of covenants may result in default or an event of default under our debt agreements.

20

Table of Contents

Upon the occurrence of an event of default under the agreement governing the ABL Facility or the indenture governing the Senior Secured Notes, the requisite lenders under the ABL Facility or the requisite noteholders under the indenture could elect to declare all amounts of such indebtedness outstanding to be immediately due and payable and, in the case of the ABL Facility, terminate any commitments to extend further credit. If we are unable to repay those amounts, the lenders under such facilities may proceed against the collateral granted to them to secure such indebtedness. Substantially all of our assets are pledged as collateral under the ABL Facility and to secure the Senior Secured Notes. If the lenders or noteholders, as applicable, accelerate the repayment of borrowings, such acceleration would have a material adverse effect on our business, financial condition, results of operations or cash flows. Furthermore, cross-default provisions in the ABL Facility provide that any default under the indenture governing the Senior Secured Notes or other significant debt agreements could trigger a cross-default under the ABL Facility. If we are unable to repay the amounts outstanding under these agreements or obtain replacement financing on acceptable terms, which ability will depend in part upon the impact of economic conditions on the liquidity of credit markets, our creditors may exercise their rights and remedies against us and the assets that serve as collateral for the debt, including initiating a bankruptcy proceeding.

Although the terms of the credit agreement governing the ABL Facility and the indenture governing the Senior Secured Notes contain restrictions on our ability to incur additional indebtedness, these restrictions are subject to a number of important qualifications and exceptions, which would allow us to borrow additional indebtedness. Additional leverage could have a material adverse effect on our business, financial condition and results of operations and could increase other risks harmful to our financial condition and results of operations.

For a more detailed description on the limitations on our ability to incur additional indebtedness and our compliance with financial covenants, please see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Covenant Compliance” and “Outstanding Indebtedness”.