Attached files

| file | filename |

|---|---|

| EX-10.(H) - EX-10.(H) - AMPCO PITTSBURGH CORP | d836471dex10h.htm |

| EX-21 - EX-21 - AMPCO PITTSBURGH CORP | d836471dex21.htm |

| EX-32.2 - EX-32.2 - AMPCO PITTSBURGH CORP | d836471dex322.htm |

| EX-31.2 - EX-31.2 - AMPCO PITTSBURGH CORP | d836471dex312.htm |

| EX-31.1 - EX-31.1 - AMPCO PITTSBURGH CORP | d836471dex311.htm |

| EX-23.1 - EX-23.1 - AMPCO PITTSBURGH CORP | d836471dex231.htm |

| EX-32.1 - EX-32.1 - AMPCO PITTSBURGH CORP | d836471dex321.htm |

| EX-10.(G) - EX-10.(G) - AMPCO PITTSBURGH CORP | d836471dex10g.htm |

| EX-10.(I) - EX-10.(I) - AMPCO PITTSBURGH CORP | d836471dex10i.htm |

| EXCEL - IDEA: XBRL DOCUMENT - AMPCO PITTSBURGH CORP | Financial_Report.xls |

| EX-23.2 - EX-23.2 - AMPCO PITTSBURGH CORP | d836471dex232.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR- 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2014

Commission File Number 1-898

AMPCO-PITTSBURGH CORPORATION

| Pennsylvania | 25-1117717 | |

| (State of Incorporation) | I.R.S. Employer ID No. | |

|

600 Grant Street, Suite 4600 |

||

| Pittsburgh, PA 15219 | (412) 456-4400 | |

| (Address of principal executive offices) | (Registrant’s telephone number) | |

| Securities registered pursuant to Section 12(b) of the Act: | ||

| Title of each class | Name of each exchange on which registered | |

| Common stock, $1 par value | New York Stock Exchange | |

| Securities registered pursuant to Section 12(g) of the Act: | None | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes No ü

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No ü

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ü No

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T(§232.405 of this chapter) during the preceding 12 months (or such shorter period that the registrant was required to submit and post such files). Yes ü No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ü]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer Accelerated Filer ü Non-accelerated Filer Smaller reporting company

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes No ü

The aggregate market value of the voting stock of Ampco-Pittsburgh Corporation held by non-affiliates on June 30, 2014 (based upon the closing price of the Registrant’s Common Stock on the New York Stock Exchange on that date) was approximately $191.6 million.

As of March 12, 2015, 10,425,664 common shares were outstanding.

Documents Incorporated by Reference: Part III of this report incorporates by reference certain information from the Proxy Statement for the 2015 Annual Meeting of Shareholders.

Table of Contents

i

Table of Contents

FORWARD-LOOKING STATEMENTS

The Private Securities Litigation Reform Act of 1995 (the “Act”) provides a safe harbor for forward-looking statements made by or on our behalf. Management’s Discussion and Analysis of Financial Condition and Results of Operation and other sections of the Annual Report on Form 10-K as well as the consolidated financial statements and notes thereto may contain forward-looking statements that reflect our current views with respect to future events and financial performance.

All statements in this document other than statements of historical fact are statements that are, or could be, deemed “forward-looking statements” within the meaning of the Act. In this document, statements regarding future financial position, sales, costs, earnings, cash flows, other measures of results of operations, capital expenditures or debt levels and plans, objectives, outlook, targets, guidance or goals are forward-looking statements. Words such as “may,” “intend,” “believe,” “expect,” “anticipate,” “estimate,” “project,” “forecast” and other terms of similar meaning that indicate future events and trends are also generally intended to identify forward looking statements. Forward-looking statements speak only as of the date on which such statements are made, are not guarantees of future performance or expectations, and involve risks and uncertainties. For us, these risks and uncertainties include, but are not limited to, those described under Item 1A. Risk Factors of this Annual Report on Form 10-K. In addition, there may be events in the future that we are not able to predict accurately or control which may cause actual results to differ materially from expectations expressed or implied by forward-looking statements. Except as required by applicable law, we assume no obligation, and disclaim any obligation, to update forward-looking statements whether as a result of new information, events or otherwise.

GENERAL DEVELOPMENT OF BUSINESS

Ampco-Pittsburgh Corporation (the “Corporation”) was incorporated in Pennsylvania in 1929. The Corporation, individually or together with its consolidated subsidiaries, is also referred to herein as the “Registrant”.

In 2013, the Forged and Cast Rolls segment recognized a need to diversify its product offerings and started producing non-roll products - primarily ingot and open die forged products which are used in the gas and oil industry and the aluminum and plastic extrusion industries. As the demand for the non-roll product has grown, we determined that Forged and Cast Engineered Products is a more appropriate segment name and have reflected that change throughout this Annual Report on Form 10-K.

The Corporation classifies its businesses in two segments: Forged and Cast Engineered Products and Air and Liquid Processing.

FINANCIAL INFORMATION ABOUT SEGMENTS

The sales and operating profit of the Corporation’s two segments and the identifiable assets attributable to both segments for the three years ended December 31, 2014 are set forth in Note 19 (Business Segments) on page 53 of this Annual Report on Form 10-K.

NARRATIVE DESCRIPTION OF BUSINESS

Forged and Cast Engineered Products Segment

Union Electric Steel Corporation produces ingot and forged products that service a wide variety of industries globally. It specializes in the production of forged hardened steel rolls used in cold rolling by producers of steel, aluminum and other metals throughout the world. In addition, it produces ingot and open die forged products which are used in the gas and oil industry and the aluminum and plastic extrusion industries. Although currently representing a minor portion of the segment’s business activity, sales of ingot and open die forged products are expected to grow and become a more significant portion of our segment’s business activity. It is headquartered in Carnegie, Pennsylvania with three manufacturing facilities in Pennsylvania and one in Indiana. Union Electric Steel Corporation is one of the largest producers of forged hardened steel rolls in the world. In addition to a few domestic competitors, several major European, South American and Asian manufacturers also compete in both the domestic and foreign markets. In 2007, a subsidiary became a 49% partner in a joint venture in China to manufacture large forged backup rolls, principally in weights and sizes larger than those which can be made in the subsidiary’s facilities in the United States.

1

Table of Contents

Union Electric Steel UK Limited produces cast rolls for hot and cold strip mills, medium/heavy section mills and plate mills in a variety of iron and steel qualities. It is located in Gateshead, England and is a major supplier of cast rolls to the metalworking industry worldwide. It primarily competes with European, Asian and North and South American companies in both the domestic and foreign markets. Union Electric Steel UK Limited is a 25% partner in a Chinese joint venture which produces cast rolls.

Air and Liquid Processing Segment

Aerofin Division of Air & Liquid Systems Corporation produces custom-engineered finned tube heat exchange coils and related heat transfer products for a variety of industries including fossil fuel and nuclear power generation, automotive, industrial process and HVAC, and is located in Lynchburg, Virginia.

Buffalo Air Handling Division of Air & Liquid Systems Corporation produces large custom air handling systems used in commercial, institutional and industrial buildings and is located in Amherst, Virginia.

Buffalo Pumps Division of Air & Liquid Systems Corporation manufactures a line of centrifugal pumps for the refrigeration, power generation and marine defense industries and is located in North Tonawanda, New York.

All three of the divisions in this segment are principally represented by a common independent sales organization and have several major competitors.

In both segments, the products are dependent on engineering, principally custom designed, and are sold to sophisticated commercial and industrial users located throughout the world.

The Forged and Cast Engineered Products segment has two international customers which constituted approximately 29% of its sales in 2014. The loss of both of these customers could have a material adverse effect on the segment.

For additional information on the products produced and financial information about each segment, see Note 19 (Business Segments) on page 53 of this Annual Report on Form 10-K.

Raw Materials

Raw materials used in both segments are generally available from many sources and the Corporation is not dependent upon any single supplier for any raw material. Substantial volumes of raw materials used by the Corporation are subject to significant variations in price. The Corporation generally does not purchase or commit for the purchase of a major portion of raw materials significantly in advance of the time it requires such materials but does make forward commitments for the supply of natural gas.

Patents

While the Corporation holds some patents, trademarks and licenses, in the opinion of management they are not material to either segment of the Corporation’s business, other than in protecting the goodwill associated with the names under which products are sold.

Backlog

The backlog of orders at December 31, 2014 was approximately $168 million compared to a backlog of $197 million at year-end 2013. Approximately 15% of the backlog is expected to be released after 2015.

Competition

The Corporation faces considerable competition from a large number of companies in both segments. The Corporation believes, however, that it is a significant factor in each of the niche markets which it serves. Competition in both segments is based on quality, service, price and delivery. For additional information, see “Narrative Description of Business” on page 1 of this Annual Report on Form 10-K.

Research and Development

As part of an overall strategy to develop new markets and maintain leadership in each of the industry niches served, the Corporation’s businesses in both segments incur expenditures for research and development. The activities that are undertaken are designed to

2

Table of Contents

develop new products, improve existing products and processes, enhance product quality, adapt products to meet customer specifications and reduce manufacturing costs. In the aggregate, these expenditures approximated $1.33 million in 2014, $1.41 million in 2013 and $1.48 million in 2012.

Environmental Protection Compliance Costs

Expenditures for environmental control matters were not material to either segment in 2014 and such expenditures are not expected to be material in 2015.

Employees

On December 31, 2014, the Corporation had 1,076 active employees.

FINANCIAL INFORMATION ABOUT GEOGRAPHIC AREAS

The Forged and Cast Engineered Products segment has a manufacturing operation in England and a small European sales and engineering support group in Belgium. For financial information relating to foreign and domestic operations see Note 19 (Business Segments) on page 53 of this Annual Report on Form 10-K.

AVAILABLE INFORMATION

The Corporation files annual, quarterly and current reports, amendments to those reports, proxy statements and other information with the Securities and Exchange Commission (“SEC”). You may access and read the Corporation’s filings without charge through the SEC’s website at www.sec.gov. You may also read and copy any document the Corporation files at the SEC’s Public Reference Room located at 100 F. Street, N.E., Room 1580, Washington, DC 20549. Please call the SEC at 1-800-SEC-0330 for further information on the Public Reference Room.

The Corporation’s Internet address is www.ampcopittsburgh.com. The Corporation makes available, free of charge on its Internet website, access to these reports as soon as reasonably practicable after such material is filed with, or furnished to, the SEC. The information on the Corporation’s website is not part of this Annual Report on Form 10-K.

EXECUTIVE OFFICERS

The name, age, position with the Corporation(1) and business experience for the past five years of the Executive Officers of the Corporation are as follows:

John S. Stanik (age 61). Mr. Stanik has served as the Corporation’s Chief Executive Officer since January 2015. He previously worked at Calgon Carbon Corporation, an international company specializing in purification products, technologies and services, from 1991 through 2012 when he retired for personal reasons. Mr. Stanik served as President and Chief Executive Officer of Calgon Carbon from 2003 to 2012 and became its Chairman of the Board in 2007.

Rose Hoover (age 59). Ms. Hoover has been employed by the Corporation for more than thirty-five years. She has served as Executive Vice President and Chief Administrative Officer of the Corporation since May 2011; Senior Vice President of the Corporation since April 2009 and prior to that served as Vice President Administration of the Corporation since 2006. She has also served as Secretary of the Corporation for more than five years.

Marliss D. Johnson (age 50). Ms. Johnson has been Chief Financial Officer and Treasurer of the Corporation since May 2013. Prior to that, she was Vice President, Controller and Treasurer of the Corporation for more than ten years. Ms. Johnson is a Certified Public Accountant with fourteen years of experience with a major accounting firm prior to joining the Corporation.

Robert G. Carothers (age 65). Mr. Carothers has been employed by Union Electric Steel, a subsidiary of the Corporation, for more than forty years. He has served as Chairman, Chief Executive Officer, and President of the Corporation’s Forged and Cast Engineered Products Segment since April 2009 and prior to that served as President of Union Electric Steel since 1998.

3

Table of Contents

Terrence W. Kenny (age 55). Mr. Kenny has been employed by the Corporation for almost thirty years. He has served as President of the Air and Liquid Processing Group since April 2009 and prior to that served as Group Vice President of the Corporation for more than five years.

| (1) | Officers serve at the discretion of the Board of Directors and none of the listed individuals serves as a director of a public company, except that Mr. Stanik is a director of the Corporation. |

From time to time, important factors may cause actual results to differ materially from any future expected results based on performance expressed or implied by any forward-looking statements made by us, including known and unknown risks, uncertainties and other factors, many of which are not possible to predict or control. Several of these factors are described from time to time in our filings with the Securities and Exchange Commission, but the factors described in filings are not the only risks that are faced.

Cyclical Demand for Products/Economic Downturns

A significant portion of our sales consists of rolling mill rolls to customers in the global steel industry which can be periodically impacted by economic or cyclical downturns. Such downturns, the timing and length of which are difficult to predict, may reduce the demand for, and sales of, our forged and cast steel rolls both in the United States and the rest of the world. Lower demand for rolls may also adversely impact profitability as other competing roll producers lower selling prices in the market place in order to fill their manufacturing capacity. Cancellation of orders or deferral of delivery of rolls may occur and produce an adverse impact on financial results. In addition, sales of non-roll product, consisting of open die forged product primarily for the gas and oil industries, are impacted by fluctuations in global energy prices.

Steel Industry Consolidation

Globally, the steel industry has undergone structural change by way of consolidation and mergers. In certain markets, the resultant reduction in the number of steel plants and the increased buying power of the enlarged steel producing companies may put pressure on the selling prices and profit margins of rolls.

Export Sales

Exports are a significant proportion of our sales. Historically, changes in foreign exchange rates, particularly in respect of the U.S. dollar and the euro, have impacted the export of our products and may do so again in the future. Other factors which may adversely impact export sales and operating results include political and economic instability, export controls, changes in tax laws and tariffs and new indigenous producers in overseas markets. A reduction in the level of export sales may have an adverse impact on our financial results. In addition, exchange rate changes may allow foreign roll suppliers to compete in our home markets.

Foreign Currency Exchange Rates

Certain of our subsidiaries operate in foreign jurisdictions and, accordingly, earn revenues, pay expenses, own assets and incur liabilities in countries using currencies other than the U.S. dollar. Since our consolidated financial statements are presented in U.S. dollars, we must translate revenues and expenses into U.S. dollars at the average exchange rate during each reporting period, and assets and liabilities into U.S. dollars at the exchange rate in effect at the end of each reporting period. Therefore, increases or decreases in the value of the U.S. dollar against other major currencies will affect the translated value for revenue, expenses and balance sheet items denominated in foreign currencies and could materially affect our financial results expressed in U.S. dollars.

Capital Spending

Each of our businesses is susceptible to the general level of economic activity, particularly as it impacts industrial and construction capital spending. A downturn in capital spending in the United States and elsewhere may reduce demand for and sales of our air handling, power generation and refrigeration equipment, and rolling mill rolls. Lower demand may also reduce profit margins due to our competitors and us striving to maximize manufacturing capacity by lowering prices.

4

Table of Contents

Prices and Availability of Commodities

We use certain commodities in the manufacture of our products. These include steel scrap, ferroalloys and energy. Any sudden price increase may cause a reduction in profit margins or losses where fixed-priced contracts have been accepted or increases cannot be obtained in future selling prices. In addition, there may be curtailment in electricity or gas supply which would adversely impact production. Shortage of critical materials while driving up costs may be of such severity as to disrupt production, all of which may impact sales and profitability.

Labor Agreements

We have several key operations which are subject to multi-year collective bargaining agreements with our hourly work force. While we believe we have good relations with our unions, there is the risk of industrial action or work stoppage at the expiration of an agreement if contract negotiations break down, which may disrupt manufacturing and impact results of operations.

Dependence on Certain Equipment

Our principal business relies on certain unique equipment such as an electric arc furnace and a spin cast work roll machine. Although a comprehensive critical spare inventory of key components for this equipment is maintained, if any such unique equipment is out of operation for an extended period, it may result in a significant reduction in our sales and earnings.

Asbestos Litigation

Our subsidiaries, and in some cases, we, are defendants in numerous claims alleging personal injury from exposure to asbestos-containing components historically used in certain products of our subsidiaries. Through year-end 2014, our insurance has covered a substantial majority of our settlement and defense costs. We believe that the estimated costs net of anticipated insurance recoveries of our pending and future asbestos legal proceedings for the next ten years will not have a material adverse effect on our consolidated financial condition or liquidity. However, there can be no assurance that our subsidiaries or we will not be subject to significant additional claims in the future or that our subsidiaries’ ultimate liability with respect to asbestos claims will not present significantly greater and longer lasting financial exposure than provided for in our consolidated financial statements. Similarly, although the Corporation believes that the assumptions employed in valuing its insurance coverage were reasonable, there are other assumptions that could have been employed that would have resulted in materially lower insurance recovery projections. The ultimate net liability with respect to such pending and any unasserted claims is subject to various uncertainties, including the following:

| • | the number of claims that are brought in the future; |

| • | the costs of defending and settling these claims; |

| • | insolvencies among our insurance carriers and the risk of future insolvencies; |

| • | the possibility that adverse jury verdicts could require damage payments in amounts greater than the amounts for which we have historically settled claims; |

| • | possible changes in the litigation environment or federal and state law governing the compensation of asbestos claimants; |

| • | the risk that the bankruptcies of other asbestos defendants may increase our costs; and |

| • | the risk that our insurance will not cover as much of our asbestos liabilities as anticipated. |

Because of the uncertainties related to such claims, it is possible that the ultimate liability could have a material adverse effect on our consolidated financial condition or liquidity in the future.

Environmental Matters

We are subject to various domestic and international environmental laws and regulations that govern the discharge of pollutants and disposal of wastes and which may require that we investigate and remediate the effects of the release or disposal of materials at sites associated with past and present operations. We could incur substantial cleanup costs, fines and civil or criminal sanctions, third party property damage or personal injury claims as a result of violations or liabilities under these laws or non-compliance with environmental permits required at our facilities.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

The Corporation has no unresolved staff comments.

5

Table of Contents

The location and general character of the principal locations in each segment, all of which are owned unless otherwise noted, are as follows:

| Company and Location | Principal Use | Approximate Square Footage |

Type of Construction | |||

| FORGED AND CAST ENGINEERED PRODUCTS SEGMENT | ||||||

| Union Electric Steel Corporation |

||||||

| Route 18 Burgettstown, PA 15021 |

Manufacturing facilities | 296,800 on 55 acres | Metal and steel | |||

| 726 Bell Avenue Carnegie, PA 15106 |

Manufacturing facilities and offices | 165,900 on 8.7 acres | Metal and steel | |||

| U.S. Highway 30 Valparaiso, IN 46383 |

Manufacturing facilities | 88,000 on 20 acres | Metal and steel | |||

| 1712 Greengarden Road Erie, PA 16501 |

Manufacturing facilities | 40,000* | Metal and steel | |||

| Bosstraat 54 3560 Lummen Belgium |

Sales and engineering | 4,500* | Cement block | |||

| Union Electric Steel UK Limited |

||||||

| Coulthards Lane Gateshead, England |

Manufacturing facilities and offices | 274,000 on 10 acres | Steel framed, metal and brick | |||

|

AIR AND LIQUID PROCESSING SEGMENT |

||||||

| Air & Liquid Systems Corporation | ||||||

|

Aerofin Division 4621 Murray Place Lynchburg, VA 24506 |

Manufacturing facilities and offices |

146,000 on 15.3 acres |

Brick, concrete and steel | |||

| Buffalo Air Handling Division |

||||||

| Zane Snead Drive Amherst, VA 24531 |

Manufacturing facilities and offices | 89,000 on 19.5 acres | Metal and steel | |||

| Buffalo Pump Division | ||||||

| 874 Oliver Street N. Tonawanda, NY 14120 |

Manufacturing facilities and offices | 94,000 on 9 acres | Metal, brick and cement block | |||

| * | Facility is leased. |

The Corporation’s office space and the Air & Liquid Systems’ headquarters office space are leased. All of the owned facilities are adequate and suitable for their respective purposes.

The Forged and Cast Engineered Products segment’s facilities were operated within 65% to 75% of their normal capacity during 2014. The facilities of the Air and Liquid Processing segment were operated within 60% to 70% of their normal capacity. Normal capacity is defined as capacity under approximately normal conditions with allowances made for unavoidable interruptions, such as lost time for repairs, maintenance, breakdowns, set-up, failure, supply delays, labor shortages and absences, Sundays, holidays, vacation, inventory taking, etc. The number of work shifts is also taken into consideration.

6

Table of Contents

LITIGATION

The Corporation and its subsidiaries are involved in various claims and lawsuits incidental to their businesses. In addition, it is also subject to asbestos litigation as described below.

Asbestos Litigation

Claims have been asserted alleging personal injury from exposure to asbestos-containing components historically used in some products of predecessors of the Corporation’s Air & Liquid Systems Corporation subsidiary (“Asbestos Liability”) and of an inactive subsidiary in dissolution. During 2013, all pending claims against the inactive subsidiary in dissolution were settled, dismissed or barred, and the dissolution court issued a final order thereby concluding the dissolution proceedings. Those subsidiaries, and in some cases the Corporation, are defendants (among a number of defendants, often in excess of 50) in cases filed in various state and federal courts.

Asbestos Claims

The following table reflects approximate information about the claims for Asbestos Liability against the subsidiaries and the Corporation for the two years ended December 31, 2014 and 2013. 2013 includes asbestos claims asserted against the inactive subsidiary in dissolution.

| 2014 | 2013 | |||||||

| Total claims pending at the beginning of the period |

8,319 | 8,007 | ||||||

| New claims served |

1,466 | 1,432 | ||||||

| Claims dismissed |

(1,094 | ) | (803 | ) | ||||

| Claims settled |

(234 | ) | (317 | ) | ||||

| Total claims pending at the end of the period (1) |

8,457 | 8,319 | ||||||

| Gross settlement and defense costs (in 000’s) |

$ | 20,801 | $ | 22,618 | ||||

| Average gross settlement and defense costs per claim resolved (in 000’s) |

$ | 15.66 | $ | 20.19 | ||||

| (1) | Included as “open claims” are approximately 1,647 and 1,636 claims in 2014 and 2013, respectively, classified in various jurisdictions as “inactive” or transferred to a state or federal judicial panel on multi-district litigation, commonly referred to as the MDL. |

A substantial majority of the settlement and defense costs reflected in the above table was reported and paid by insurers. Because claims are often filed and can be settled or dismissed in large groups, the amount and timing of settlements, as well as the number of open claims, can fluctuate significantly from period to period.

Asbestos Insurance

The Corporation and its Air & Liquid Systems Corporation (“Air & Liquid”) subsidiary are parties to a series of settlement agreements (“Settlement Agreements”) with insurers that have coverage obligations for Asbestos Liability (the “Settling Insurers”). Under the Settlement Agreements, the Settling Insurers accept financial responsibility, subject to the terms and conditions of the respective agreements, including overall coverage limits, for pending and future claims for Asbestos Liability. The Settlement Agreements encompass the substantial majority of insurance policies that provide coverage for claims for Asbestos Liability.

The Settlement Agreements include acknowledgements that Howden North America, Inc. (“Howden”) is entitled to coverage under policies covering Asbestos Liability for claims arising out of the historical products manufactured or distributed by Buffalo Forge, a former subsidiary of the Corporation (the “Products”). The Settlement Agreements do not provide for any prioritization on access to the applicable policies or any sublimits of liability as to Howden or the Corporation and Air & Liquid, and, accordingly, Howden may access the coverage afforded by the Settling Insurers for any covered claim arising out of a Product. In general, access by Howden to the coverage afforded by the Settling Insurers for the Products will erode coverage under the Settlement Agreements available to the Corporation and Air & Liquid for Asbestos Liability.

7

Table of Contents

On February 24, 2011, the Corporation and Air & Liquid filed a lawsuit in the United States District Court for the Western District of Pennsylvania against thirteen domestic insurance companies, certain underwriters at Lloyd’s, London and certain London market insurance companies, and Howden. The lawsuit seeks a declaratory judgment regarding the respective rights and obligations of the parties under excess insurance policies that were issued to the Corporation from 1981 through 1984 as respects claims against the Corporation and its subsidiary for Asbestos Liability and as respects asbestos bodily-injury claims against Howden arising from the Products. The Corporation and Air & Liquid have reached Settlement Agreements with all but two of the defendant insurers in the coverage action. Those Settlement Agreements specify the terms and conditions upon which the insurer parties are to contribute to defense and indemnity costs for claims for Asbestos Liability. One of the Settlement Agreements entered into by the Corporation and Air & Liquid also provided for the dismissal of claims, without prejudice, regarding two upper-level excess policies issued by one of the insurers. The Court has entered Orders dismissing all claims in the action filed against each other by the Corporation and Air & Liquid, on the one hand, and by the settling insurers, on the other. Howden also reached an agreement with eight domestic insurers addressing asbestos-related bodily injury claims arising from the Products, and claims as to those insurers and Howden have been dismissed. Various counterclaims, cross claims and third party claims have been filed in the litigation and remain pending although only two domestic insurers and Howden remain in the litigation as to the Corporation and Air & Liquid. On September 27, 2013, the Court issued a memorandum opinion and order granting in part and denying in part cross motions for summary judgment filed by the Corporation and Air & Liquid, Howden, and the insurer parties still in the litigation. At a hearing on January 13, 2015, the Court ruled that final judgment in accordance with the Court’s prior rulings will be entered in the case. Upon entry of final judgment, the Corporation, Air & Liquid, certain insurers, and Howden may appeal to the United States Court of Appeals for the Third Circuit.

Asbestos Valuations

In 2006, the Corporation retained Hamilton, Rabinovitz & Associates, Inc. (“HR&A”), a nationally recognized expert in the valuation of asbestos liabilities, to assist the Corporation in estimating the potential liability for pending and unasserted future claims for Asbestos Liability. HR&A was not requested to estimate asbestos claims against the inactive subsidiary in dissolution, which the Corporation believes are immaterial. Based on this analysis, the Corporation recorded a reserve for Asbestos Liability claims pending or projected to be asserted through 2013 as of December 31, 2006. HR&A’s analysis has been periodically updated since that time. Most recently, the HR&A analysis was updated in 2014, and additional reserves were established by the Corporation as of December 31, 2014 for Asbestos Liability claims pending or projected to be asserted through 2024. The methodology used by HR&A in its projection in 2014 of the operating subsidiaries’ liability for pending and unasserted potential future claims for Asbestos Liability, which is substantially the same as the methodology employed by HR&A in prior estimates, relied upon and included the following factors:

| • | HR&A’s interpretation of a widely accepted forecast of the population likely to have been exposed to asbestos; |

| • | epidemiological studies estimating the number of people likely to develop asbestos-related diseases; |

| • | HR&A’s analysis of the number of people likely to file an asbestos-related injury claim against the subsidiaries and the Corporation based on such epidemiological data and relevant claims history from January 1, 2012 to December 8, 2014; |

| • | an analysis of pending cases, by type of injury claimed and jurisdiction where the claim is filed; |

| • | an analysis of claims resolution history from January 1, 2012 to December 8, 2014 to determine the average settlement value of claims, by type of injury claimed and jurisdiction of filing; and |

| • | an adjustment for inflation in the future average settlement value of claims, at an annual inflation rate based on the Congressional Budget Office’s ten year forecast of inflation. |

Using this information, HR&A estimated in 2014 the number of future claims for Asbestos Liability that would be filed through the year 2024, as well as the settlement or indemnity costs that would be incurred to resolve both pending and future unasserted claims through 2024. This methodology has been accepted by numerous courts.

In conjunction with developing the aggregate liability estimate referenced above, the Corporation also developed an estimate of probable insurance recoveries for its Asbestos Liabilities. In developing the estimate, the Corporation considered HR&A’s projection for settlement or indemnity costs for Asbestos Liability and management’s projection of associated defense costs (based on the current defense to indemnity cost ratio), as well as a number of additional factors. These additional factors included the Settlement Agreements then in effect, policy exclusions, policy limits, policy provisions regarding coverage for defense costs, attachment points, prior impairment of policies and gaps in the coverage, policy exhaustions, insolvencies among certain of the insurance carriers, and

8

Table of Contents

the nature of the underlying claims for Asbestos Liability asserted against the subsidiaries and the Corporation as reflected in the Corporation’s asbestos claims database, as well as estimated erosion of insurance limits on account of claims against Howden arising out of the Products. In addition to consulting with the Corporation’s outside legal counsel on these insurance matters, the Corporation consulted with a nationally-recognized insurance consulting firm it retained to assist the Corporation with certain policy allocation matters that also are among the several factors considered by the Corporation when analyzing potential recoveries from relevant historical insurance for Asbestos Liabilities. Based upon all of the factors considered by the Corporation, and taking into account the Corporation’s analysis of publicly available information regarding the credit-worthiness of various insurers, the Corporation estimated the probable insurance recoveries for Asbestos Liability and defense costs through 2024. Although the Corporation believes that the assumptions employed in the insurance valuation were reasonable and previously consulted with its outside legal counsel and insurance consultant regarding those assumptions, there are other assumptions that could have been employed that would have resulted in materially lower insurance recovery projections.

Based on the analyses described above, the Corporation’s reserve at December 31, 2014 for the total costs, including defense costs, for Asbestos Liability claims pending or projected to be asserted through 2024 was $189 million, of which approximately 64% was attributable to settlement costs for unasserted claims projected to be filed through 2024 and future defense costs. While it is reasonably possible that the Corporation will incur additional charges for Asbestos Liability and defense costs in excess of the amounts currently reserved, the Corporation believes that there is too much uncertainty to provide for reasonable estimation of the number of future claims, the nature of such claims and the cost to resolve them beyond 2024. Accordingly, no reserve has been recorded for any costs that may be incurred after 2024.

The Corporation’s receivable at December 31, 2014 for insurance recoveries attributable to the claims for which the Corporation’s Asbestos Liability reserve has been established, including the portion of incurred defense costs covered by the Settlement Agreements in effect through December 31, 2014, and the probable payments and reimbursements relating to the estimated indemnity and defense costs for pending and unasserted future Asbestos Liability claims, was $141 million.

The following table summarizes activity relating to insurance recoveries for each of the years ended December 31, 2014 and 2013.

| 2014 | 2013 | |||||||

| Insurance receivable – asbestos, beginning of the year |

$ | 110,741 | $ | 118,115 | ||||

| Settlement and defense costs paid by insurance carriers |

(17,159 | ) | (23,714 | ) | ||||

| Changes in estimated coverage |

47,069 | 16,340 | ||||||

| Insurance receivable – asbestos, end of the year |

$ | 140,651 | $ | 110,741 | ||||

The insurance receivable recorded by the Corporation does not assume any recovery from insolvent carriers and a substantial majority of the insurance recoveries deemed probable was from insurance companies rated A – (excellent) or better by A.M. Best Corporation. There can be no assurance, however, that there will not be further insolvencies among the relevant insurance carriers, or that the assumed percentage recoveries for certain carriers will prove correct. The difference between insurance recoveries and projected costs is not due to exhaustion of all insurance coverage for Asbestos Liability. The Corporation and the subsidiaries have substantial additional insurance coverage which the Corporation expects to be available for Asbestos Liability claims and defense costs that the subsidiaries and it may incur after 2024. However, this insurance coverage also can be expected to have gaps creating significant shortfalls of insurance recoveries as against claims expense, which could be material in future years.

The amounts recorded by the Corporation for Asbestos Liabilities and insurance receivables rely on assumptions that are based on currently known facts and strategy. The Corporation’s actual expenses or insurance recoveries could be significantly higher or lower than those recorded if assumptions used in the Corporation’s or HR&A’s calculations vary significantly from actual results. Key variables in these assumptions are identified above and include the number and type of new claims to be filed each year, the average cost of disposing of each such new claim, average annual defense costs, compliance by relevant parties with the terms of the Settlement Agreements, the resolution of remaining coverage issues with insurance carriers, and the solvency risk with respect to the relevant insurance carriers. Other factors that may affect the Corporation’s Asbestos Liability and ability to recover under its insurance policies include uncertainties surrounding the litigation process from jurisdiction to jurisdiction and from case to case, reforms that may be made by state and federal courts, and the passage of state or federal tort reform legislation.

The Corporation intends to evaluate its estimated Asbestos Liability and related insurance receivables as well as the underlying assumptions on a regular basis to determine whether any adjustments to the estimates are required. Due to the uncertainties

9

Table of Contents

surrounding asbestos litigation and insurance, these regular reviews may result in the Corporation incurring future charges; however, the Corporation is currently unable to estimate such future charges. Adjustments, if any, to the Corporation’s estimate of its recorded Asbestos Liability and/or insurance receivables could be material to operating results for the periods in which the adjustments to the liability or receivable are recorded, and to the Corporation’s liquidity and consolidated financial position.

ENVIRONMENTAL

The Corporation is currently performing certain remedial actions in connection with the sale of real estate previously owned and appropriate reserves have been established.

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

The shares of common stock of Ampco-Pittsburgh Corporation are traded on the New York Stock Exchange (symbol AP). Cash dividends have been paid on common shares in every year since 1965.

| 2014 Per Share | 2013 Per Share | |||||||||||||||||||||||||||

| Common Stock Price |

Common Stock Price |

|||||||||||||||||||||||||||

| Quarter | High | Low | Dividends Declared |

High | Low | Dividends Declared |

||||||||||||||||||||||

| First |

$ | 20.91 | $ | 16.45 | $ | 0.18 | $ | 21.00 | $ | 17.55 | $ | 0.18 | ||||||||||||||||

| Second |

23.73 | 18.71 | 0.18 | 19.31 | 16.99 | 0.18 | ||||||||||||||||||||||

| Third |

24.90 | 19.62 | 0.18 | 20.69 | 16.24 | 0.18 | ||||||||||||||||||||||

| Fourth |

22.28 | 16.75 | 0.18 | 19.70 | 17.10 | 0.18 | ||||||||||||||||||||||

| Year |

24.90 | 16.45 | 0.72 | 21.00 | 16.24 | 0.72 | ||||||||||||||||||||||

The number of registered shareholders at December 31, 2014 and 2013 equaled 400 and 423, respectively.

10

Table of Contents

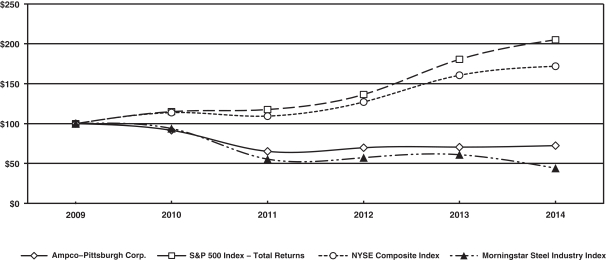

STOCK PERFORMANCE GRAPH

Comparison of Five Year Cumulative Total Return

Standard & Poors 500, NYSE Composite and Morningstar’s Steel Industry

(Performance results through December 31, 2014)

COMPARISON OF CUMULATIVE TOTAL RETURN*

Assumes $100 invested at the close of trading on the last trading day preceding January 1, 2009 in Ampco-Pittsburgh Corporation common stock, Standard & Poors 500 Index, NYSE Composite Index and Morningstar’s Steel Industry group.

*Cumulative total return assumes reinvestment of dividends.

In the above graph, the Corporation has used Morningstar’s Steel Industry group for its peer comparison. The diversity of products produced by subsidiaries of the Corporation makes it difficult to match to any one product-based peer group. Although not totally comparable, the Steel Industry group was chosen because the largest percentage of the Corporation’s sales is to the global steel industry.

Historical stock price performance shown on the above graph is not necessarily indicative of future price performance.

11

Table of Contents

ITEM 6. SELECTED FINANCIAL DATA

| Year Ended December 31, | ||||||||||||||||||||

| (dollars, except per share amounts, and shares outstanding in thousands) |

2014 | 2013 | 2012 | 2011 | 2010 | |||||||||||||||

| Net sales |

$ 272,858 | $ 281,050 | $ 292,905 | $ 344,816 | $ 326,886 | |||||||||||||||

| Net (loss) income(1) |

(1,187 | ) | 12,437 | 8,355 | 21,309 | 15,456 | ||||||||||||||

| Total assets |

536,409 | 502,673 | 533,179 | 531,632 | 526,963 | |||||||||||||||

| Shareholders’ equity |

205,148 | 234,995 | 192,093 | 192,872 | 196,777 | |||||||||||||||

| Net (loss) income per common share: |

||||||||||||||||||||

|

Basic(1) |

(0.11 | ) | 1.20 | 0.81 | 2.07 | 1.51 | ||||||||||||||

| Diluted |

(0.11 | ) | 1.20 | 0.80 | 2.05 | 1.50 | ||||||||||||||

| Per common share: |

||||||||||||||||||||

| Cash dividends declared |

0.72 | 0.72 | 0.72 | 0.72 | 0.72 | |||||||||||||||

| Shareholders’ equity |

19.68 | 22.65 | 18.57 | 18.68 | 19.10 | |||||||||||||||

| Market price at year end |

19.25 | 19.45 | 19.98 | 19.34 | 28.05 | |||||||||||||||

| Weighted average common shares outstanding |

10,405 | 10,358 | 10,338 | 10,319 | 10,254 | |||||||||||||||

| Number of registered shareholders |

400 | 423 | 454 | 487 | 507 | |||||||||||||||

| Number of employees |

1,076 | 1,109 | 1,178 | 1,240 | 1,264 | |||||||||||||||

| (1) | Net (loss) income includes: |

2014 – An after-tax charge of $2,916 or $0.28 per common share for estimated costs of asbestos-related litigation through 2024 net of estimated insurance recoveries (see Note 17 to Consolidated Financial Statements).

2013 – An after-tax credit of $10,621 or $1.03 per common share for estimated additional insurance recoveries expected to be available to satisfy asbestos liabilities through 2022 resulting from settlement agreements reached with various insurance carriers (see Note 17 to Consolidated Financial Statements) offset by an after-tax charge of $4,165 or $0.40 per common share to recognize an other-than-temporary impairment of our investment in a forged roll joint venture company (see Note 2 to Consolidated Financial Statements) for a net increase to net income of $6,456 or $0.63 per common share.

2010 – An after-tax charge of $12,931 or $1.26 per common share for estimated costs of asbestos-related litigation through 2020 net of estimated insurance recoveries (see Note 17 to Consolidated Financial Statements).

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION

(in thousands, except per share amounts)

EXECUTIVE OVERVIEW

Ampco-Pittsburgh Corporation operates in two business segments – the Forged and Cast Engineered Products segment and the Air and Liquid Processing segment. The Forged and Cast Engineered Products segment consists of Union Electric Steel Corporation (“Union Electric Steel” or “UES”) and Union Electric Steel UK Limited (“UES-UK”). Union Electric Steel produces ingot and forged products that service a wide variety of industries globally. It specializes in the production of forged hardened steel rolls used in cold rolling by producers of steel, aluminum and other metals throughout the world. In addition, it produces ingot and open die forged products (‘non-roll products”) which are used in the gas and oil industry and the aluminum and plastic extrusion industries. Headquartered in Carnegie, Pennsylvania with three manufacturing facilities in Pennsylvania and one in Indiana, UES is one of the largest producers of forged hardened steel rolls in the world. In addition to a few domestic competitors, several major European, South American and Asian manufacturers also compete in both the domestic and foreign markets. UES-UK produces cast rolls for hot

12

Table of Contents

and cold strip mills, medium/heavy section mills and plate mills in a variety of iron and steel qualities. It is located in Gateshead, England and is a major supplier of cast rolls to the metalworking industry worldwide. It primarily competes with European, Asian and North and South American companies in both the domestic and foreign markets.

The Air and Liquid Processing segment includes Aerofin, Buffalo Air Handling and Buffalo Pumps, all divisions of Air & Liquid Systems Corporation (“Air and Liquid”), a wholly-owned subsidiary of the Corporation. Aerofin produces custom-engineered finned tube heat exchange coils and related heat transfer products for a variety of industries including fossil fuel and nuclear power generation, automotive, industrial process and HVAC. Buffalo Air Handling produces large custom-designed air handling systems for commercial, institutional and industrial building markets. Buffalo Pumps manufactures centrifugal pumps for the marine defense, refrigeration and power generation industries. The segment has operations in Virginia and New York with headquarters in Pennsylvania. The segment distributes a significant portion of its products through a common independent group of sales offices located throughout the United States and Canada.

The Forged and Cast Engineered Products segment has been operating at levels below capacity due to the worldwide reduction in demand for roll product. Market conditions in the United States and the EU28 countries continue to be difficult. Business opportunities in Asia (particularly China), India and other world regions remain infrequent as a result of indigenous supply enabling purchases to be made domestically at lower pricing than offered by traditional western suppliers. With the global steelmaking industry also operating below capacity and the resulting supply demand imbalance in the market place, pricing has suffered and profit margins have decreased. Asian and Indian roll producers have been offering aggressive pricing to gain market share in Western and Middle Eastern markets. Additionally, cost reduction requirements at most steel and aluminum producers throughout our customer base have led them to mandate severe discounts from suppliers. For 2015, we expect demand for rolls to be weak and pricing pressures to remain. Ongoing efforts to diversify our customer base have resulted in expansion of our non-roll products. Although currently representing a minor portion of the segment’s business activity, sales of our non-roll products have outperformed expectations, offsetting some of the effects of constraints currently affecting the roll market, and utilized available production capacity. For 2015, we expect sales of our non-roll products to grow and become a more significant portion of our segment’s business activity.

Union Electric Steel MG Roll Co., Ltd (“UES-MG”), the Chinese joint venture company in which a subsidiary of UES holds a 49% interest, principally manufactures and sells forged backup rolling mill rolls of a size and weight currently not able to be produced by UES. The joint venture has been adversely impacted by the global economy, with significantly depressed pricing, reduced demand and excess roll inventories of its potential customer base in China – all hindering profitability. Losses have been incurred since 2009, in which we have recognized our share (49%) in our consolidated statements of operations, and are expected to continue in 2015. Additionally, the overall financial strength of the joint venture continues to deteriorate with a greater reliance on the 51% partner or entities controlled by the 51% partner to provide financing and working capital. In the fourth quarter of 2013, we, with the help of outside consultants and appraisers, concluded that the estimated fair value of our investment in UES-MG was less than our carrying amount and that the decline was “other than temporary”. Accordingly, we recognized an impairment charge reducing the carrying amount of our investment to its estimated fair value. We will continue to monitor the carrying value of this investment ($2,574 at December 31, 2014) to determine if future charges are necessary.

For the Air and Liquid Processing segment, increases in spending in the industrial replacement market positively impacted our heat exchange coil business and strength in spending in the fossil-fueled power generation market benefited our centrifugal pump business. These improvements, however, were offset by the continuing slowness of new construction for institutional markets which impacted our custom air handling and heat exchange coil businesses. The focus for this segment is to continue to develop new product lines and to strengthen the sales distribution networks.

13

Table of Contents

CONSOLIDATED RESULTS OF OPERATIONS OVERVIEW

The Corporation

| 2014 | 2013 | 2012 | ||||||||||||||||||||||

| Net Sales: |

||||||||||||||||||||||||

| Forged and Cast Engineered Products |

$ | 179,388 | 66% | $ | 187,286 | 67% | $ | 189,470 | 65% | |||||||||||||||

| Air and Liquid Processing |

93,470 | 34% | 93,764 | 33% | 103,435 | 35% | ||||||||||||||||||

| Consolidated |

$ | 272,858 | 100% | $ | 281,050 | 100% | $ | 292,905 | 100% | |||||||||||||||

| Income (Loss) from Operations: |

||||||||||||||||||||||||

| Forged and Cast Engineered Products |

$ | 4,380 | $ | 13,936 | $ | 18,415 | ||||||||||||||||||

| Air and Liquid Processing(1) |

4,222 | 24,945 | 7,267 | |||||||||||||||||||||

| Corporate costs |

(8,522 | ) | (9,914 | ) | (9,390 | ) | ||||||||||||||||||

| Consolidated |

$ | 80 | $ | 28,967 | $ | 16,292 | ||||||||||||||||||

| Backlog: |

||||||||||||||||||||||||

| Forged and Cast Engineered Products |

$ | 131,118 | 78% | $ | 159,344 | 81% | $ | 154,527 | 79% | |||||||||||||||

| Air and Liquid Processing |

36,830 | 22% | 38,117 | 19% | 41,277 | 21% | ||||||||||||||||||

| Consolidated |

$ | 167,948 | 100% | $ | 197,461 | 100% | $ | 195,804 | 100% | |||||||||||||||

| (1) | Income (loss) from operations for the Air and Liquid Processing segment for 2014 includes a pre-tax charge of $4,487 for estimated costs of asbestos-related litigation through 2024 net of estimated insurance recoveries whereas 2013 includes a pre-tax credit of $16,340 for estimated additional insurance recoveries expected to be available to satisfy asbestos liabilities through 2022 resulting from settlement agreements reached with various insurance carriers and 2012 includes a pre-tax credit of $540 for estimated costs of asbestos-related litigation through 2022 net of estimated insurance recoveries (see Note 17 to Consolidated Financial Statements). |

Consolidated net sales for 2014 decreased when compared to 2013 primarily due to a lower volume of shipments and weaker pricing for our Forged and Cast Engineered Products group. Consolidated net sales for 2013 decreased when compared to 2012 principally due to a decline in new construction spending by institutional markets for the Air and Liquid Processing group. A discussion of sales and backlog for the Corporation’s two segments is included below.

Operating income for 2014 includes a pre-tax charge of $4,487 for estimated additional costs of asbestos-related litigation through 2024 net of estimated insurance recoveries whereas 2013 includes a pre-tax credit of $16,340 for estimated additional insurance recoveries expected to be available to satisfy asbestos liabilities through 2022. Operating income for the current year was further impacted by weak demand and ongoing pricing pressures but benefitted from lower pension and other postretirement costs. For 2013, the improvement to operating income from the $16,340 pre-tax credit for estimated additional insurance recoveries expected to be available to satisfy asbestos liabilities through 2022 was offset primarily by lower margins for our Forged and Cast Engineered Products segment. Corporate expenses are less in the current year due to lower employee-related expenses including pension and other postretirement benefit costs whereas in 2013 such costs were higher than in 2012.

Gross margin, excluding depreciation, as a percentage of net sales, was 19.9%, 22.7% and 22.9% for 2014, 2013 and 2012, respectively. The decrease from earlier years is primarily attributable to our Forged and Cast Engineered Products segment and a lower volume of shipments and level of production and ongoing price discounting to remain competitive. The expected impact to gross margin is somewhat offset by lower pension and other postretirement benefit costs of approximately $3,927.

Selling and administrative expenses totaled $37,380 (13.7% of net sales), $39,682 (14.1% of net sales) and $40,530 (13.8% of net sales) for 2014, 2013 and 2012, respectively. The decrease in 2014 from 2013 is principally related to lower pension and other postretirement costs of $1,216 and commissions of $878. The decrease in 2013 from 2012 is primarily attributable to lower uninsured legal and case management costs and valuation expenses associated with asbestos litigation of $1,088.

The charge for asbestos litigation in 2014 represents an extension of the estimated costs of pending and future asbestos claims, net of additional insurance recoveries, from 2022 to the end of 2024. The credit for asbestos litigation in 2013 represents the estimated

14

Table of Contents

additional insurance recoveries expected to be available to satisfy asbestos liabilities through 2022 resulting from settlement agreements reached with various insurance carriers in 2013. The credit for asbestos litigation in 2012 represents an extension of the estimated costs of pending and future asbestos claims, net of additional insurance recoveries, from 2020 to the end of 2022. The claims result from alleged personal injury from exposure to asbestos-containing components historically used in some products manufactured by certain companies which now operate as divisions of the Air and Liquid Processing segment. See Note 17 to Consolidated Financial Statements.

Other income (expense) fluctuated primarily as a result of changes in foreign exchange gains and losses and charges related to operations discontinued years ago. (Losses) gains on foreign exchange transactions approximated $(488), $(227) and $107 for 2014, 2013 and 2012, respectively, and charges related to operations discontinued years ago equaled $(443), $(1,412) and $(1,054), respectively.

Our statutory income tax rate equals 35% which compares to an effective income tax rate of 85.9%, 21.4% and 34.4% for 2014, 2013 and 2012, respectively. The effective income tax rate for 2014 is greater than the prior year rates due to a reduction in current year earnings, which caused permanent adjustments to have a greater impact on the overall effective income tax rate, and certain favorable permanent differences including our share of losses from our investment in a forged roll joint venture company offset by the revaluation of deferred income tax assets associated with decreases in the statutory income tax rates for New York and Indiana. The effective income tax rate for 2013 was lower than our statutory income tax rate due to beneficial permanent differences for our domestic operations and tax benefit related to the impairment charge recognized on our investment in a forged roll joint venture company.

Equity losses in the Chinese joint venture represent Union Electric Steel’s share (49%) of the losses of UES-MG and the impairment charge we recognized in 2013 on our investment in the joint venture company (see Note 2 to Consolidated Financial Statements).

As a result of the above, for 2014, we lost $1,187 or $0.11 per common share which includes an after-tax charge of $2,916 or $0.28 per common share for estimated costs of asbestos-related litigation through 2024 net of estimated insurance recoveries (see Note 17 to Consolidated Financial Statements). For 2013, we earned $12,437 or $1.20 per common share which includes an after-tax credit of $10,621 or $1.03 per common share for estimated additional insurance recoveries expected to be available to satisfy asbestos liabilities through 2022 resulting from settlement agreements reached with various insurance carriers (see Note 17 to Consolidated Financial Statements) offset by an after-tax charge of $4,165 or $0.40 per common share to recognize an other-than-temporary impairment of our investment in a forged roll joint venture company (see Note 2 to Consolidated Financial Statements) for a net increase to net income of $6,456 or $0.63 per common share. For 2012, we earned $8,355 or $0.81 per common share.

Forged and Cast Engineered Products

| 2014 | 2013 | 2012 | ||||||||||

| Net sales |

$ | 179,388 | $ | 187,286 | $ | 189,470 | ||||||

| Operating income |

$ | 4,380 | $ | 13,936 | $ | 18,415 | ||||||

| Backlog |

$ | 131,118 | $ | 159,344 | $ | 154,527 | ||||||

For 2014, net sales and operating income for the segment were lower in comparison to a year ago principally due to a worldwide reduction in demand for roll product. Net sales for our cast rolls business in England benefited from a higher level of shipments and sales of our non-roll products have outperformed expectations; however, lower net sales for our forged roll operations in the United States more than offset the expected contribution provided by each of them. The lower volume of shipments negatively impacted earnings by approximately $3,000. Pricing and profit margins also decreased from a year ago due to the supply demand imbalance in the roll industry which further affected operating results by approximately $4,500. While freight and commission costs declined in the current year by approximately $1,850 on lower sales, the prior year included $1,500 of insurance proceeds for lost margin on rolls damaged in 2012.

Net sales for 2013 decreased slightly when compared to 2012 due to a decline in selling prices offset by a higher level of shipments. The lower selling prices adversely impacted operating income by approximately $12,500; however, the additional volume improved operating income by approximately $4,500. Operating income for 2013 also benefited from receipt of $1,500 of insurance proceeds for lost margin on rolls damaged in 2012 and improved quality resulting in a reduction of warranty-related provisions.

15

Table of Contents

Improvement in the weighted-average exchange rates used to translate sales of UES-UK from the British pound to the U.S. dollar increased sales for 2014 when compared to 2013 and 2012 by approximately $2,900 and $2,200, respectively. The impact to operating income was not significant.

Backlog at the end of 2014 decreased from 2013 and 2012 due to a combination of larger customers placing orders quarter by quarter versus annually and the falloff in demand as roll customers operate below capacity. As of December 31, 2014, approximately $23,284 of the backlog is expected to be released after 2015.

Air and Liquid Processing

| 2014 | 2013 | 2012 | ||||||||||

| Net sales |

$ | 93,470 | $ | 93,764 | $ | 103,435 | ||||||

| Operating income |

$ | 4,222 | $ | 24,945 | $ | 7,267 | ||||||

| Backlog |

$ | 36,830 | $ | 38,117 | $ | 41,277 | ||||||

For 2014, sales for the segment were flat. Net sales of pumps grew slightly, at approximately 2%, in 2014 from 2013 with the higher volume of shipments of commercial pumps helping to offset the decline to U.S. Navy shipbuilders and in pump replacement parts. Additionally, revenue for air handlers improved from a year ago due to an increase in the volume of shipments principally to the pharmaceutical market. Net sales of heat exchange coils, however, fell from a year ago, by approximately 8%, primarily due to a lower volume of shipments for the fossil fuel and nuclear power generation market which is being impacted by reduced demand and increased competition. For 2013, sales for the segment decreased when compared to 2012 principally as a result of reduced demand for custom air handling equipment combined with excess capacity in the industry. Additionally, 2012 benefited from completion of a large order for a customer in medical research.

Operating income for 2014 includes a pre-tax charge of $4,487 for estimated costs of asbestos-related litigation through 2024 net of estimated insurance recoveries. By comparison, operating income for 2013 includes a pre-tax credit of $16,340 for the estimated additional insurance recoveries expected to be available to satisfy asbestos liabilities through 2022 resulting from settlement agreements reached with various insurance carriers during the year and 2012 includes a pre-tax credit of $540 representing an adjustment to previously-provided charges for asbestos-related litigation net of estimated insurance recoveries. See Note 17 to Consolidated Financial Statements for further information. Uninsured legal and case management and valuation costs associated with asbestos litigation for each of the years approximated $340, $649 and $1,737, respectively.

The decline in backlog at December 31, 2014 from 2013 and 2012 is primarily attributable to fewer pumps orders from U.S. Navy shipbuilders and a decrease in orders for air handling units offset by a large order for the fossil fuel power generation market. The majority of the year-end backlog is scheduled to ship in 2015.

LIQUIDITY AND CAPITAL RESOURCES

Net cash flows provided by operating activities for 2014 equaled $19,975 compared to $37,774 and $25,444 for 2013 and 2012, respectively. While the charge (credit) for asbestos litigation recorded in each of the years impacted earnings, it did not affect cash flows by the same amount. Instead, the asbestos liability, net of insurance recoveries, will be paid over a number of years and will generate tax benefits. Net asbestos-related payments, including reimbursement of past costs, equaled $3,642, $(985) and $7,932 in 2014, 2013 and 2012, respectively, and are expected to approximate $4,000 in 2015. Contributions to our pension and other postretirement plans approximated $2,500 in 2014, $7,400 in 2013 (of which $5,000 were voluntary contributions) and $2,500 in 2012. As a result of voluntary contributions and relief provided by Moving Ahead for Progress in the 21st Century (“MAP-21”) and subsequently the Highway and Transportation Funding Act of 2014 (“HAFTA”), which reduces funding requirements for single-employer defined benefit plans, no minimum contributions are required for 2015. Additional voluntary contributions may be made however. Net cash flows provided by operating activities for 2014 were affected by higher accounts receivable attributable to mix, slower payments by customers and longer payment terms granted to customers. By comparison, net cash flows provided by operating activities for 2013 benefited from a reduction in inventory when compared to 2012.

16

Table of Contents

Net cash flows used in investing activities were $13,219, $11,926 and $9,369 in 2014, 2013 and 2012, respectively, the majority of which represents capital expenditures for our Forged and Cast Engineered Products group. In 2010, UES-UK was awarded a government grant with a portion of the proceeds received in 2012. As of December 31, 2014, anticipated future capital expenditures approximate $6,288, the majority of which will be spent in 2015.

Net cash outflows from financing activities represent primarily the payment of dividends of $0.72 per common share. Additionally, stock options were exercised resulting in proceeds from the issuance of common stock and excess tax benefits.

The effect of exchange rate changes on cash and cash equivalents is primarily attributable to the fluctuation of the British pound against the U.S. dollar.

As a result of the above, cash and cash equivalents decreased by $812 in 2014 and ended the year at $97,098 (of which $9,479 is held by foreign operations) in comparison to $97,910 and $78,889 at December 31, 2013 and 2012, respectively. Repatriation of foreign funds may result in the Corporation accruing and paying additional income tax; however, the majority of foreign funds is currently deemed to be permanently reinvested and no additional provision for income tax has been made. Funds on hand and funds generated from future operations are expected to be sufficient to finance our operational and capital expenditure requirements. We also maintain short-term lines of credit in excess of the cash needs of our businesses. The total available at December 31, 2014 was approximately $9,200 (including £3,000 in the United Kingdom and €400 in Belgium).

We had the following contractual obligations outstanding as of December 31, 2014:

| Payments Due by Period | ||||||||||||||||||||||||

| Total | <1 year | 1–3 years | 3–5 years | >5 years | Other | |||||||||||||||||||

| Industrial Revenue Bonds(1) |

$ | 13,311 | $ | 0 | $ | 0 | $ | 0 | $ | 13,311 | $ | 0 | ||||||||||||

| Operating Lease Obligations |

1,400 | 823 | 471 | 106 | 0 | 0 | ||||||||||||||||||

| Capital Expenditures |

6,288 | 6,288 | 0 | 0 | 0 | 0 | ||||||||||||||||||

| Pension and Other Postretirement Benefit Obligations(2) |

49,673 | 2,619 | 7,686 | 20,046 | 19,322 | 0 | ||||||||||||||||||

| Purchase Obligations(3) |

4,375 | 2,828 | 1,547 | 0 | 0 | 0 | ||||||||||||||||||

| Unrecognized Tax Benefits(4) |

52 | 0 | 0 | 0 | 0 | 52 | ||||||||||||||||||

| Total |

$ | 75,099 | $ | 12,558 | $ | 9,704 | $ | 20,152 | $ | 32,633 | $ | 52 | ||||||||||||

| (1) | Represents principal only. Interest is not included since it is variable; interest rates averaged less than 1% in the current year. The Industrial Revenue Bonds begin to mature in 2020; however, if the bonds are unable to be remarketed they will be refinanced under a separate facility. See Note 6 to Consolidated Financial Statements. |

| (2) | Represents estimated contributions to our pension and other postretirement plans. Actual required contributions are contingent on a number of variables including future investment performance of the plans’ assets and may differ from these estimates. See Note 7 to Consolidated Financial Statements. Contributions to the U.S. defined benefit plan are based on the projected funded status of the plan including anticipated normal costs, amortization of unfunded liabilities and an 8% expected return on plan assets. With respect to the U.K. defined benefit plan, the Trustees and UES-UK have agreed to a recovery plan that estimates the amount of employer contributions, based on U.K. regulations, necessary to eliminate the funding deficit of the plan over an agreed period. |

| (3) | Represents primarily commitments by one of our Forged and Cast Engineered Products subsidiaries for the purchase of natural gas through 2017 covering approximately 32% of anticipated needs. See Note 11 to Consolidated Financial Statements. |

| (4) | Represents uncertain tax positions. Amount included as “Other” represents portion for which the period of cash settlement cannot be reasonably estimated. See Note 13 to Consolidated Financial Statements. |

With respect to environmental matters, we are currently performing certain remedial actions in connection with the sale of real estate previously owned. Environmental exposures are difficult to assess and estimate for numerous reasons including lack of reliable data, the multiplicity of possible solutions, the years of remedial and monitoring activity required and the identification of new sites. However, we believe the potential liability for all environmental proceedings of approximately $325 accrued at December 31, 2014 is considered adequate based on information known to date (see Note 18 to Consolidated Financial Statements).

The nature and scope of our business brings us into regular contact with a variety of persons, businesses and government agencies in the ordinary course of business. Consequently, we and certain of our subsidiaries from time to time are named in various legal actions.

17

Table of Contents

Generally, we do not anticipate that our financial condition or liquidity will be materially affected by the costs of known, pending or threatened litigation. However, claims have been asserted alleging personal injury from exposure to asbestos-containing components historically used in some products and there can be no assurance that future claims will not present significantly greater and longer lasting financial exposure than presently contemplated (see Note 17 to Consolidated Financial Statements).

OFF-BALANCE SHEET ARRANGEMENTS

Our off-balance sheet arrangements include operating leases, capital expenditures and purchase obligations disclosed in the contractual obligations table and the letters of credit unrelated to the Industrial Revenue Bonds as discussed in Note 8 to the Consolidated Financial Statements.

EFFECTS OF INFLATION

While inflationary and market pressures on costs are likely to be experienced, it is anticipated that ongoing improvements in manufacturing efficiencies and cost savings efforts will mitigate the effects of inflation on 2015 operating results. The ability to pass on increases in the price of commodities to the customer is contingent upon current market conditions with us potentially having to absorb some portion of the increase. Product pricing for the Forged and Cast Engineered Products segment is reflective of current costs with a majority of orders subject to a variable-index surcharge program which helps to protect the segment and its customers against the volatility in the cost of certain raw materials. Additionally, long-term labor agreements exist at each of the key locations. Although certain of these agreements expire in 2015, we, as is consistent with past practice, will negotiate with the intent to secure mutually beneficial arrangements covering multiple years (see Note 8 to Consolidated Financial Statements). Finally, commitments have been executed for natural gas usage and certain commodities (copper and aluminum) to cover a portion of orders in the backlog (see Note 11 to Consolidated Financial Statements).

APPLICATION OF CRITICAL ACCOUNTING POLICIES

We have identified critical accounting policies that are important to the presentation of our financial condition, changes in financial condition and results of operations and involve the most complex or subjective assessments. Critical accounting policies relate to accounting for pension and other postretirement benefits, assessing recoverability of long-lived assets, litigation, income taxes and stock-based compensation.

Accounting for pension and other postretirement benefits involves estimating the cost of benefits to be provided well into the future and attributing that cost over the time period each employee works. To accomplish this, input from our actuary is evaluated and extensive use is made of assumptions about inflation, long-term rate of return on plan assets, longevity, rates of increases in compensation, employee turnover and discount rates.

The expected long-term rate of return on plan assets is an estimate of average rates of earnings expected to be earned on funds invested or to be invested to provide for the benefits included in the projected benefit obligation. Since these benefits will be paid over many years, the expected long-term rate of return is reflective of current investment returns and investment returns over a longer period. Also, consideration is given to target and actual asset allocations, inflation and real risk-free return. We believe the expected long-term rate of return of 8% for our domestic plan and 5.40% for our foreign plan to be reasonable. Actual returns on plan assets for 2014 and 2013, respectively, approximated 6.93% and 19.22% for our domestic plan and 12.40% and 12.42% for our foreign plan.

The discount rates used in determining future pension obligations and other postretirement benefits for each of our plans are based on rates of return on high-quality fixed-income investments currently available and expected to be available during the period to maturity of pension and other postretirement benefits. High-quality fixed-income investments are defined as those investments which have received one of the two highest ratings given by a recognized rating agency with maturities of 10+ years. We believe the assumed discount rates of 4.10% for our domestic plan, 4.00% for our other postretirement benefits plan and 3.50% for our foreign plan as of December 31, 2014 to be reasonable.