Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Glori Energy Inc. | Financial_Report.xls |

| EX-32.1 - EXHIBIT 32.1 - Glori Energy Inc. | gloriexhibit3211.htm |

| EX-31.1 - EXHIBIT 31.1 - Glori Energy Inc. | gloriexhibit3111.htm |

| EX-32.2 - EXHIBIT 32.2 - Glori Energy Inc. | gloriexhibit3221.htm |

| EX-31.2 - EXHIBIT 31.2 - Glori Energy Inc. | gloriexhibit3121.htm |

| EX-14.1 - EXHIBIT 14.1 - Glori Energy Inc. | a141codeofethics.htm |

| EX-99.2 - EXHIBIT 99.2 - Glori Energy Inc. | a992cobbreport01-01x15.htm |

| EX-23.2 - EXHIBIT 23.2 - Glori Energy Inc. | gloriholdingsconsentletter.htm |

| EX-23.1 - EXHIBIT 23.1 - Glori Energy Inc. | a231fy2014gloriauditconsent.htm |

| 10-K - 10-K - Glori Energy Inc. | glri1231201410-k.htm |

| EX-23.3 - EXHIBIT 23.3 - Glori Energy Inc. | a233consentofcobb.htm |

| ||||

Forecast of Production and Reserves | ||||

in and related to | ||||

Shuck Field, Etzold Unit | ||||

located in Seward County, Kansas | ||||

for | ||||

Glori Holdings Inc. | ||||

January 1, 2015 | ||||

Collarini Associates | ||||

Collarini Associates

3100 Wilcrest Drive, Suite 140

Houston, Texas 77042

Tel. (832) 251-0160

www.collarini.com

February 9, 2015

Mr. Victor Perez

Glori Holdings Inc.

4315 South Drive

Houston, Texas 77053

Dear Mr. Perez:

In accordance with your request, Collarini Associates (Collarini) has estimated the proved reserves and future revenue, as of January 1, 2015, to the interest of Glori Holdings Inc. (Glori) in and related to the Shuck Field, Etzold Unit, located in Seward County, Kansas. This report is based on SEC guideline pricing and unescalated costs as set forth herein. The estimate of proved reserves and the future revenue therefrom conform to all standards and definitions promulgated in Section 210.4-10 of Regulation S - X issued by the Securities and Exchange Commission in November 1988 and amended in December 2008. Estimates of probable and possible reserves and the future revenue therefrom are optional by Regulation S - X, and are not included herein at your request. It is estimated these volumes represent 100% of Glori’s total proved reserves.

As presented in the accompanying detailed projections by reservoir and by reserve category, we estimate the net reserves and future net income to Glori's interest, as of January 1, 2015, to be:

Net Remaining Reserves | Future Net Income (M$) | ||||||

Reserve Category | Oil (MBO) | Gas (MMCF) | Undiscounted | Present Worth at 10% | |||

Proved | |||||||

Producing | 15 | 0 | 401 | 337 | |||

Total Proved | 15 | 0 | 401 | 337 | |||

Oil volumes are generally expressed in thousands of stock tank barrels (MBO), where one barrel is equivalent to 42 United States gallons.

The reserves and future income shown in this report are related to reservoirs which were identified by Glori Holdings Inc. The estimates do not include any value which might be attributable to additional reservoirs or untested acreage in which Glori Holdings Inc. may also hold an interest.

Net sales, as defined in this report, are before deducting production taxes. Net income is after deducting these taxes, and after deducting future capital costs and operating expenses, but before consideration of federal income taxes. The future net income has also been shown discounted at ten

Glori Holdings Inc.

February 9, 2015

Page Two

percent to determine its present worth. This present worth is included to indicate a time value of money. This should not be construed as representing the market value of the property. Our estimates of future cash flows do not include abandonment costs, but do include estimates of all costs required to recover reserves including drilling and recompletions.

Reserves in this report were estimated using all applicable engineering and geological data available such as, but not limited to, historic production volumes, initial flow test information, flowing tubing pressures, shut-in tubing pressures, bottom hole pressures, repeat formation test data, pressure- volume-temperature fluid analysis, geological well logs, sidewall core analysis, and whole core analysis at the time the report was conducted.

The reserve volumes and their respective classifications and categorizations were estimated by performance methods, volumetric methods, analogy, or combination of methods. Performance methods generally included decline curve analysis and material balance analysis where representative data was available. Volumetric estimated generally included a combination of geological and engineering interpretations, while analogy methods included reserve estimates from historical performance of similar wells and reservoirs in the field or nearby fields.

Proved reserve classifications were determined based on the “reasonable certainty” of recovering the estimated volumes or more. The proved reserve categorizations were based on the stage of maturity and development of the respective proved reserves.

Based on gross oil equivalent barrels, approximately 100 percent of Glori’s proved reserves are located in the Shuck Field, Seward County, Kansas, USA. Glori’s reserves are 100 percent developed.

Glori’s proved reserves are 100% proved producing. All of the proved producing reserves were estimated by performance methods. These estimates are based on gross oil equivalent barrels that Glori holds an interest in.

For the proved producing reserves, each well’s current production was compared to historical production and a decline curve was established.

Hydrocarbon prices used in this report are based on SEC price parameters using the average prices received on the first of each month during the 12-month period prior to the ending date of the period covered in this report, determined as an unweighted arithmetic average of the first-day-of-the-month price for each month within such period. The product prices used to determine future gross revenue for each field were determined by applying benchmark pricing as described above then adjusted by “differentials” only to the extent provided by SEC guidelines. These “differentials” generally adjust the benchmark prices on a field by field basis to account for product quality, transportation, and marketing. The “differentials” were calculated by Glori. Collarini accepted the “differentials” as factual data and did not confirm the accuracy of these adjustments.

Pricing used in this report represent an SEC guideline price of $94.99 for WTI at Cushing, Oklahoma. These prices were then adjusted for oil gravity and transportation differentials of minus $6.22.

Glori Holdings Inc.

February 9, 2015

Page Three

Operating costs were provided by Glori Holdings Inc. Collarini could not audit or confirm the accuracy of these expenses. These current expenses are held constant through the life of the property. These costs include processing fees where applicable.

Collarini Associates utilized all data, appropriate methods and procedures deemed necessary to conduct and finalize this report to conform to all standards and definitions promulgated in Section 210.4-

10 of Regulation S – X issued by the Securities and Exchange Commission in November 1988 and amended in December 2008.

The reserves presented in this report are estimates only and should not be construed as being exact quantities. They may or may not be recovered, and if recovered, the revenues, costs, and expenses therefrom may be more or less than the estimated amounts. Because of governmental policies, uncertainties of supply and demand, and international politics, the actual sales rates and the prices actually received for the reserves, as well as the costs of recovery, may vary from those assumptions included in this report. Also, estimates of reserves may increase or decrease as a result of future operational decisions, mechanical problems, and the price of oil and gas.

All reserve estimates have been performed in accordance with sound engineering principles and generally accepted industry practice. As in all aspects of oil and gas evaluation, there are uncertainties inherent in the interpretation of engineering data, and all conclusions represent only informed professional judgments.

A visual inspection of the properties themselves was not considered necessary for the purpose of this report. No assessment of compliance with environmental regulations or future liability for site remediation was made. We are independent consultants; we do not own any interest in this property and are not employed contingent upon the value of this property. All engineering calculations and basic data used in the analysis are maintained on file in our office and are available for review.

Mr. Mitchell C. Reece was the technical person primarily responsible for overseeing the reserves audit. Mr. Reece attended Texas A&M University, and graduated in 1979 with a Bachelor of Science Degree in Petroleum Engineering. He is a Registered Professional Engineer in the State of Texas, United States of America, and has in excess of 30 years' experience in petroleum engineering studies and evaluations.

Very truly yours,

COLLARINI ASSOCIATES

Mitch Reece, P.E. President

MCR/tlp

Collarini Engineering Inc.

Texas Board of Professional Engineers Registration F-5660

RESERVE DEFINITIONS

SEC PARAMETERS1

RESERVES

Reserves are estimated remaining quantities of oil and gas and related substances anticipated to be economically producible, as of a given date, by application of development projects to known accumulations. In addition, there must exist, or there must be a reasonable expectation that there will exist, the legal right to produce or a revenue interest in the production, installed means of delivering oil and gas or related substances to market, and all permits and financing required to implement the project.

Note to paragraph above: Reserves should not be assigned to adjacent reservoirs isolated by major, potentially sealing, faults until those reservoirs are penetrated and evaluated as economically producible. Reserves should not be assigned to areas that are clearly separated from a known accumulation by a non-productive reservoir (i.e., absence of reservoir, structurally low reservoir, or negative test results). Such areas may contain prospective resources (i.e., potentially recoverable resources from undiscovered accumulations).

DEVELOPED OIL AND GAS RESERVES are reserves of any category that can be expected to be recovered:

(i) Through existing wells with existing equipment and operating methods or in which the cost of the required equipment is relatively minor compared to the cost of a new well; and

(ii) Through installed extraction equipment and infrastructure operational at the time of the reserves estimate if the extraction is by means not involving a well.

UNDEVELOPED OIL AND GAS RESERVES are reserves of any category that are expected to be recovered from new wells on undrilled acreage, or from existing wells where a relatively major expenditure is required for recompletion.

(i) Reserves on undrilled acreage shall be limited to those directly offsetting development spacing areas that are reasonably certain of production when drilled, unless evidence using reliable technology exists that establishes reasonable certainty of economic producibility at greater distances.

(ii) Undrilled locations can be classified as having undeveloped reserves only if a development plan has been adopted indicating that they are scheduled to be drilled within five years, unless the specific circumstances, justify a longer time.

(iii) Under no circumstances shall estimates for undeveloped reserves be attributable to any acreage for which an application of fluid injection or other improved recovery technique is contemplated, unless such techniques have been proved effective by actual projects in the same reservoir or an analogous reservoir, as defined in Analogus Reservoirs below, or by other evidence using reliable technology establishing reasonable certainty.

_________________________

1 As per Section 210.4-10 of SEC Regulation S-X dated November 1988 and as amended December 29, 2008.

RESERVE DEFINITIONS

SEC PARAMETERS (Cont.)1

PROVED OIL AND GAS RESERVES

Proved Reserves are those quantities of oil and gas, which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible—from a given date forward, from known reservoirs, and under existing economic conditions, operating methods, and government regulations—prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether deterministic or probabilistic methods are used for the estimation. The project to extract the hydrocarbons must have commenced or the operator must be reasonably certain that it will commence the project within a reasonable time.

(i) The area of the reservoir considered as proved includes:

(a) The area identified by drilling and limited by fluid contacts, if any, and

(b) Adjacent undrilled portions of the reservoir that can, with reasonable certainty, be judged to be continuous with it and to contain economically producible oil or gas on the basis of available geoscience and engineering data.

(ii) In the absence of data on fluid contacts, proved quantities in a reservoir are limited by the lowest known hydrocarbons (LKH) as seen in a well penetration unless geoscience, engineering, or performance data and reliable technology establishes a lower contact with reasonable certainty.

(iii) Where direct observation from well penetrations has defined a highest-known oil (HKO) elevation and the potential exists for an associated gas cap, proved oil reserves may be assigned in the structurally higher portions of the reservoir only if geoscience, engineering, or performance data and reliable technology establish the higher contact with reasonable certainty.

(iv) Reserves which can be produced economically through application of improved recovery techniques (including, but not limited to, fluid injection) are included in the proved classification when:

(a) Successful testing by a pilot project in an area of the reservoir with properties no more favorable than in the reservoir as a whole, the operation of an installed program in the reservoir or an analogous reservoir, or other evidence using reliable technology establishes the reasonable certainty of the engineering analysis on which the project or program was based; and

(b) The project has been approved for development by all necessary parties and entities, including governmental entities.

(v) Existing economic conditions include prices and costs at which economic producibility from a reservoir is to be determined. The price shall be the average price during the 12- month period prior to the ending date of the period covered by the report, determined as an unweighted arithmetic average of the first-day-of-the-month price for each month within such period, unless prices are defined by contractual arrangements, excluding escalations based upon future conditions.

_________________________

1 As per Section 210.4-10 of SEC Regulation S-X dated November 1988 and as amended December 29, 2008.

RESERVE DEFINITIONS

SEC PARAMETERS (Cont.)1

Reasonable certainty If deterministic methods are used, reasonable certainty means a high degree of confidence that the quantities will be recovered. If probabilistic methods are used, there should be at least a 90% probability that the quantities actually recovered will equal or exceed the estimate. A high degree of confidence exists if the quantity is much more likely to be achieved than not, and, as changes due to increased availability of geoscience (geological, geophysical, and geochemical), engineering, and economic data are made to estimated ultimate recovery (EUR) with time, reasonably certain EUR is much more likely to increase or remain constant than to decrease.

Reliable technology Reliable technology is a grouping of one or more technologies (including computational methods) that have been field tested and have been demonstrated to provide reasonably certain results with consistency and repeatability in the formation being evaluated or in an analogous formation.

Deterministic estimate The method of estimating reserves or resources is called deterministic when a single value for each parameter (from the geoscience, engineering, or economic data) in the reserves calculation is used in the reserves estimation procedure.

Probabilistic estimate The method of estimation of reserves or resources is called probabilistic when the full range of values that could reasonably occur for each unknown parameter (from the geoscience and engineering data) is used to generate a full range of possible outcomes and their associated probabilities of occurrence.

Analogous Reservoir Analogous reservoirs, as used in resources assessments, have similar rock and fluid properties, reservoir conditions (depth, temperature, and pressure) and drive mechanisms, but are typically at a more advanced stage of development than the reservoir of interest and thus may provide concepts to assist in the interpretation of more limited data and estimation of recovery. When used to support proved reserves, an “analogous reservoir” refers to a reservoir that shares the following characteristics with the reservoir of interest:

(i) Same geological formation (but not necessarily in pressure communication with the reservoir of interest);

(ii) Same environment of deposition;

(iii) Similar geological structure; and

(iv) Same drive mechanism.

Instruction to Analogous reservoir: Reservoir properties must, in the aggregate, be no more favorable in the analog than in the reservoir of interest.

Proved Producing Reserves are those reserves which are expected to be recovered from existing completion intervals open at the time of the estimate and producing in existing wells.

Proved Nonproducing Shut-In Reserves are those reserves which are expected to be recovered from existing completion intervals open at the time of the estimate, but which had not started producing, or were shut in for market conditions or minor pipeline connection.

Proved Nonproducing Behind Pipe Reserves are those reserves which are expected to be recovered from zones behind casing in existing wells, which will require additional completion work or a future recompletion prior to the start of production.

________________________

1 As per Section 210.4-10 of SEC Regulation S-X dated November 1988 and as amended December 29, 2008.

SHUCK FIELD, ETZOLD UNIT

Seward County, Kansas

BACKGROUND

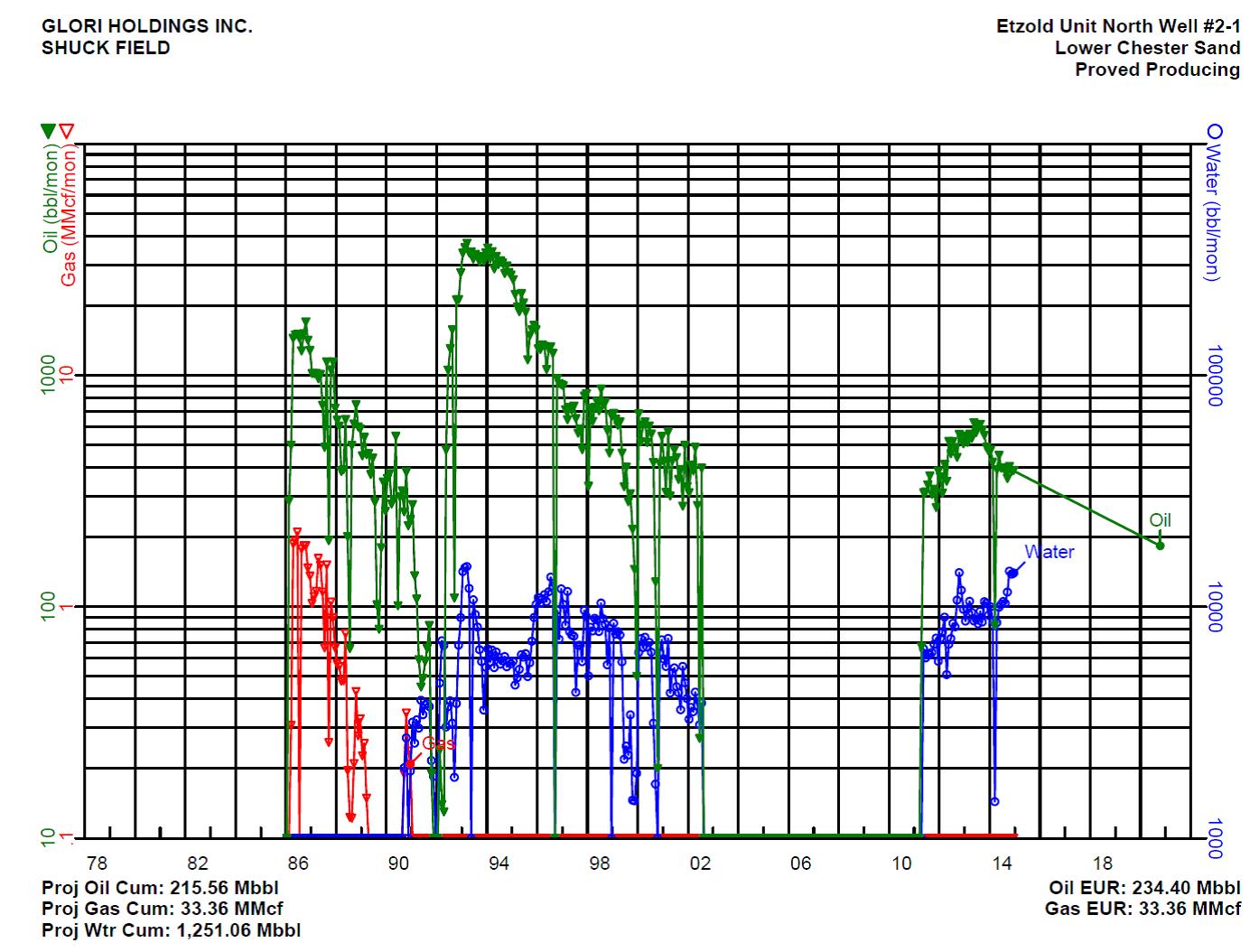

The Shuck Field, Etzold Unit, is located in the southwest portion of Kansas in Seward County. Anadarko originally developed the field and initiated a waterflood from 1989 to 2002. Merit was assigned the field in 2005. Merit then offered Glori Holdings Inc. the opportunity to acquire Merit's interest in the northern portion of the field in return for assuming field liability and a 7.5% royalty interest. Surface equipment has been replaced due to deterioration or prior removal. There are currently two wells producing and six active injection wells. In December, oil production was 420 BOPM and 13,975 BWPM. Glori Holdings Inc. has a 100% gross working interest and 80.0%

net revenue interest in the unit, including the royalty reduction. The reservoir has recovered over

2 MMBO under primary and secondary recovery. In 2012, Glori Holdings Inc. purchased the south portion of the Etzold Unit and is evaluating future plans.

GEOSCIENCE

The Shuck Field, Etzold Unit, consists of the Lower Chester Sand and several stray sands. The Lower Chester Sand is of Mississippian Age and equivalent to the Morrow formation. The field is located on a north-south channel axis. Several large fields are also along this axis. Permeability varies vertically, indicating that there could be significant by-passed reserves.

ENGINEERING

Gross proved reserves of 19 MBO are estimated to remain as of January 1, 2015. All are in the producing category. These reserves were determined by performance. The wells are being carefully monitored due to unknown water levels and the dispersion of the water across the reservoir.

Operating expenses are $11,970 per well per month. These expenses were provided by Glori Holdings Inc. These operating expenses include the operating costs of the facilities and injection wells. The oil price differential was based on 2013 and 2014 actuals and was decreased by $6.22 per barrel. Transportation costs are also included in this differential. Abandonment costs were assumed to be equal to salvage value.

Effective January 1, 2014

GLORI HOLDINGS INC.

SHUCK FIELD

Total Reserves

Ranked by 1/1/15 Reserve Category and NPW at 10 %

Well | Reservoir | Res. Cat. | Production | Net Sales M$ | Prod. Tax M$ | Oper. Exp. M$ | Exp & Cap Invest M$ | Net Income M$ | NPW at 10% (M$) | Cum NPW (M$) | ||||

8/8ths (Mbbl) | 8/8ths (MMcf) | Net (Mbbl) | Net (MMcf) | |||||||||||

1 | Etzold Unit North Well #2-1 | Lower Chester Sand | PDP | 19 | 0 | 15 | 0 | 1,338 | 107 | 831 | 0 | 401 | 337 | 337 |

2 | Etzold Unit North Well #3-5 | Lower Chester Sand | PDP | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 337 |

Total Proved Producing | 19 | 0 | 15 | 0 | 1,338 | 107 | 831 | 0 | 401 | 337 | ||||

1 | Etzold Unit North Well #1-1 | Lower Chester Sand | PDSI | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 337 |

Total Proved Shut-In | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||||

Total Proved | 19 | 0 | 15 | 0 | 1,338 | 107 | 831 | 0 | 401 | 337 | ||||

Coll_Eco1Line2_100208.rpt | Collarini Associates | 2/9/2015 |

Etzold Unit Production Plots 1-1-15.xlsx | Collarini Associates | 2/9/2015 |

GLORI HOLDINGS INC. SHUCK FIELD, ETZOLD UNIT Reserve Summary | |||||||||||

Reservoir | Well # | Reserve Category | Gross Reserves Remaining 1/1/15 | Net Reserves Remaining 1/1/15 | * | Comments | |||||

MBO | MMCF | MBO | MMCF | ||||||||

Lower Chester Sand | Etzold Unit North Well #2-1 | PDP | 19 | 0 | 15 | 0 | P | Decline-curve | |||

Lower Chester Sand | Etzold Unit North Well #3-5 | PDP | 0 | 0 | 0 | 0 | P | Noncommercial | |||

Total Proved Producing | 19 | 0 | 15 | 0 | |||||||

Lower Chester Sand | Etzold Unit North Well #1-1 | PDSI | 0 | 0 | 0 | 0 | P | Noncommercial | |||

Total Proved Shut-In | 0 | 0 | 0 | 0 | |||||||

TOTAL PROVED RESERVES | 19 | 0 | 15 | 0 | |||||||

* Reserves Methodology: | |||||||||||

V = Volumetrics | P = Performance | ||||||||||

Etzold Unit ResSum 1-1-15.xlsx | Collarini Associates | Page 1 of 1 2/9/2015 |

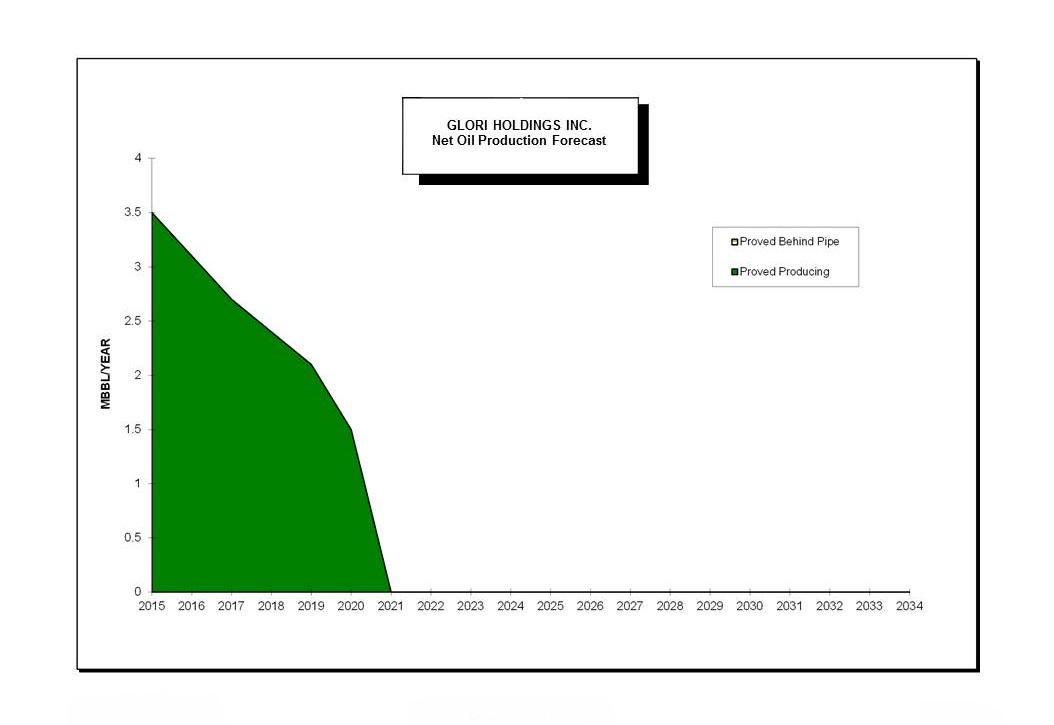

PROJECTION OF ESTIMATED PRODUCTION AND REVENUE GLORI HOLDINGS INC. AS OF JANUARY 01, 2015 | ||||||||||||

SEC Pricing 12-31-14 | ||||||||||||

Present Worth Profile | ||||||||||||

SHUCK FIELD | ––Mid-Year Discounting–– | |||||||||||

Total | 8.00 | % | 348.4 | 25.00 | % | 268.7 | ||||||

10.00 | % | 337.1 | 30.00 | % | 251.0 | |||||||

Proved | 12.00 | % | 326.4 | 35.00 | % | 235.3 | ||||||

15.00 | % | 311.3 | 40.00 | % | 221.2 | |||||||

20.00 | % | 288.7 | 50.00 | % | 197.3 | |||||||

Year Ending 12-31 | Gross Wells | GROSS PRODUCTION | NET PRODUCTION | Oil Price ($/bbl) | Gas Price ($/Mcf) | NGL Price ($/gal) | ||||||

Oil, (Mbbl) | Gas, (MMcf) | NGL, (Mgal) | OIl, (Mbbl) | Gas, (MMcf) | NGL, (Mgal) | |||||||

2015 | 2 | 4.3 | 0.0 | 0.0 | 3.5 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||

2016 | 1 | 3.8 | 0.0 | 0.0 | 3.1 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||

2017 | 1 | 3.3 | 0.0 | 0.0 | 2.7 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||

2018 | 1 | 2.9 | 0.0 | 0.0 | 2.4 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||

2019 | 1 | 2.6 | 0.0 | 0.0 | 2.1 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||

2020 | 1 | 1.8 | 0.0 | 0.0 | 1.5 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||

After | 0.0 | 0.0 | 0.00 | 0.0 | 0.0 | 0.00 | 0.00 | 0.00 | 0.00 | |||

Remaining | 18.8 | 0.0 | 0.00 | 15.1 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | |||

Cumulative | 868.4 | 62.9 | 0.0 | |||||||||

Ultimate | 887.3 | 62.9 | 0.0 | |||||||||

Year Ending 12-31 | Net Sales | Other Revenue | Production Taxes | Operating Expense | Exp/Cap Invest | Net Income | Cumulative Net Income | Pres. Worth @ 10.00% | ||||||||||||||||

--(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | |||||||||||||||||

2015 | 306.9 | 0.0 | 24.5 | 143.6 | 0.0 | 138.7 | 138.7 | 132.2 | ||||||||||||||||

2016 | 270.8 | 0.0 | 21.7 | 143.6 | 0.0 | 105.5 | 244.1 | 223.3 | ||||||||||||||||

2017 | 237.6 | 0.0 | 19.0 | 143.6 | 0.0 | 74.9 | 319.1 | 281.9 | ||||||||||||||||

2018 | 209.1 | 0.0 | 16.7 | 143.6 | 0.0 | 48.7 | 367.8 | 316.4 | ||||||||||||||||

2019 | 184.0 | 0.0 | 14.7 | 143.6 | 0.0 | 25.7 | 393.5 | 332.9 | ||||||||||||||||

2020 | 129.9 | 0.0 | 10.4 | 112.4 | 0.0 | 7.1 | 400.6 | 337.1 | ||||||||||||||||

After | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||||||||||||

Total | 1,338.3 | 0.0 | 107.1 | 830.6 | 0.0 | 400.6 | 400.6 | 337.1 | ||||||||||||||||

2/9/15 | This forecast accompanies the COLLARINI ASSOCIATES report and is subject to its specific conditions. | |||||||||||||||||||||||

PROJECTION OF ESTIMATED PRODUCTION AND REVENUE GLORI HOLDINGS INC. AS OF JANUARY 01, 2015 | ||||||||||||

SEC Pricing 12-31-14 | ||||||||||||

Present Worth Profile | ||||||||||||

SHUCK FIELD | ––Mid-Year Discounting–– | |||||||||||

Total | 8.00 | % | 348.4 | 25.00 | % | 268.7 | ||||||

Proved Producing | 10.00 | % | 337.1 | 30.00 | % | 251.0 | ||||||

12.00 | % | 326.4 | 35.00 | % | 235.3 | |||||||

15.00 | % | 311.3 | 40.00 | % | 221.2 | |||||||

20.00 | % | 288.7 | 50.00 | % | 197.3 | |||||||

Year Ending 12-31 | Gross Wells | GROSS PRODUCTION | NET PRODUCTION | Oil Price ($/bbl) | Gas Price ($/Mcf) | NGL Price ($/gal) | ||||||

Oil, (Mbbl) | Gas, (MMcf) | NGL, (Mgal) | OIl, (Mbbl) | Gas, (MMcf) | NGL, (Mgal) | |||||||

2015 | 1 | 4.3 | 0.0 | 0.0 | 3.5 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||

2016 | 1 | 3.8 | 0.0 | 0.0 | 3.1 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||

2017 | 1 | 3.3 | 0.0 | 0.0 | 2.7 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||

2018 | 1 | 2.9 | 0.0 | 0.0 | 2.4 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||

2019 | 1 | 2.6 | 0.0 | 0.0 | 2.1 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||

2020 | 1 | 1.8 | 0.0 | 0.0 | 1.5 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||

After | 0.0 | 0.0 | 0.00 | 0.0 | 0.0 | 0.00 | 0.00 | 0.00 | 0.00 | |||

Remaining | 18.8 | 0.0 | 0.00 | 15.1 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | |||

Cumulative | 408.7 | 48.2 | 0.0 | |||||||||

Ultimate | 427.5 | 48.2 | 0.0 | |||||||||

Year Ending 12-31 | Net Sales | Other Revenue | Production Taxes | Operating Expense | Exp/Cap Invest | Net Income | Cumulative Net Income | Pres. Worth @ 10.00% | ||||||||||||||||

--(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | |||||||||||||||||

2015 | 306.9 | 0.0 | 24.5 | 143.6 | 0.0 | 138.7 | 138.7 | 132.2 | ||||||||||||||||

2016 | 270.8 | 0.0 | 21.7 | 143.6 | 0.0 | 105.5 | 244.1 | 223.3 | ||||||||||||||||

2017 | 237.6 | 0.0 | 19.0 | 143.6 | 0.0 | 74.9 | 319.1 | 281.9 | ||||||||||||||||

2018 | 209.1 | 0.0 | 16.7 | 143.6 | 0.0 | 48.7 | 367.8 | 316.4 | ||||||||||||||||

2019 | 184.0 | 0.0 | 14.7 | 143.6 | 0.0 | 25.7 | 393.5 | 332.9 | ||||||||||||||||

2020 | 129.9 | 0.0 | 10.4 | 112.4 | 0.0 | 7.1 | 400.6 | 337.1 | ||||||||||||||||

After | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||||||||||||

Total | 1,338.3 | 0.0 | 107.1 | 830.6 | 0.0 | 400.6 | 400.6 | 337.1 | ||||||||||||||||

2/9/15 | This forecast accompanies the COLLARINI ASSOCIATES report and is subject to its specific conditions. | |||||||||||||||||||||||

PROJECTION OF ESTIMATED PRODUCTION AND REVENUE SHUCK FIELD GLORI HOLDINGS INC. AS OF JANUARY 01, 2015 | ||||||||||||||

Etzold Unit North Well #2-1 | ||||||||||||||

Proved Producing | ||||||||||||||

Lower Chester Sand | Present Worth Profile | |||||||||||||

––Mid-Year Discounting–– | ||||||||||||||

SEC Pricing 12-31-14 | 8.00 | % | 348.4 | 25.00 | % | 268.7 | ||||||||

Initial | Final | 10.00 | % | 337.1 | 30.00 | % | 251.0 | |||||||

Gross Working Interest | 1.000000 | 1.000000 | 12.00 | % | 326.4 | 35.00 | % | 235.3 | ||||||

Net Revenue Interest | 0.800000 | 0.800000 | 15.00 | % | 311.3 | 40.00 | % | 221.2 | ||||||

20.00 | % | 288.7 | 50.00 | % | 197.3 | |||||||||

Year Ending 12-31 | Gross Wells | GROSS PRODUCTION | NET PRODUCTION | Oil Price ($/bbl) | Gas Price ($/Mcf) | NGL Price ($/gal) | ||||||||

Oil, (Mbbl) | Gas, (MMcf) | NGL, (Mgal) | OIl, (Mbbl) | Gas, (MMcf) | NGL, (Mgal) | |||||||||

2015 | 1 | 4.3 | 0.0 | 0.00 | 3.5 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||||

2016 | 1 | 3.8 | 0.0 | 0.00 | 3.1 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||||

2017 | 1 | 3.3 | 0.0 | 0.00 | 2.7 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||||

2018 | 1 | 2.9 | 0.0 | 0.00 | 2.4 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||||

2019 | 1 | 2.6 | 0.0 | 0.00 | 2.1 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||||

2020 | 1 | 1.8 | 0.0 | 0.00 | 1.5 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | ||||

After | 0.0 | 0.0 | 0.00 | 0.0 | 0.0 | 0.00 | 0.00 | 0.00 | 0.00 | |||||

Remaining | 18.8 | 0.0 | 0.00 | 15.1 | 0.0 | 0.00 | 88.77 | 0.00 | 0.00 | |||||

Cumulative | 215.6 | 33.4 | 0.0 | |||||||||||

Ultimate | 234.4 | 33.4 | 0.0 | |||||||||||

Year Ending 12-31 | Net Sales | Other Revenue | Production Taxes | Operating Expense | Exp/Cap Invest | Net Income | Cumulative Net Income | Pres. Worth @ 10.00% | ||||||||||||||||

--(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | |||||||||||||||||

2015 | 306.9 | 0.0 | 24.5 | 143.6 | 0.0 | 138.7 | 138.7 | 132.2 | ||||||||||||||||

2016 | 270.8 | 0.0 | 21.7 | 143.6 | 0.0 | 105.5 | 244.1 | 223.3 | ||||||||||||||||

2017 | 237.6 | 0.0 | 19.0 | 143.6 | 0.0 | 74.9 | 319.1 | 281.9 | ||||||||||||||||

2018 | 209.1 | 0.0 | 16.7 | 143.6 | 0.0 | 48.7 | 367.8 | 316.4 | ||||||||||||||||

2019 | 184.0 | 0.0 | 14.7 | 143.6 | 0.0 | 25.7 | 393.5 | 332.9 | ||||||||||||||||

2020 | 129.9 | 0.0 | 10.4 | 112.4 | 0.0 | 7.1 | 400.6 | 337.1 | ||||||||||||||||

After | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||||||||||||

Total | 1,338.3 | 0.0 | 107.1 | 830.6 | 0.0 | 400.6 | 400.6 | 337.1 | ||||||||||||||||

2/9/15 | This forecast accompanies the COLLARINI ASSOCIATES report and is subject to its specific conditions. | |||||||||||||||||||||||

PROJECTION OF ESTIMATED PRODUCTION AND REVENUE SHUCK FIELD GLORI HOLDINGS INC. AS OF JANUARY 01, 2015 | ||||||||||||||

Etzold Unit North Well #3-5 | ||||||||||||||

Proved Producing | ||||||||||||||

Lower Chester Sand | Present Worth Profile | |||||||||||||

––Mid-Year Discounting–– | ||||||||||||||

SEC Pricing 12-31-14 | 8.00 | % | 0.0 | 25.00 | % | 0.0 | ||||||||

Initial | Final | 10.00 | % | 0.0 | 30.00 | % | 0.0 | |||||||

Gross Working Interest | 1.000000 | 0.000000 | 12.00 | % | 0.0 | 35.00 | % | 0.0 | ||||||

Net Revenue Interest | 0.800000 | 0.000000 | 15.00 | % | 0.0 | 40.00 | % | 0.0 | ||||||

20.00 | % | 0.0 | 50.00 | % | 0.0 | |||||||||

Year Ending 12-31 | Gross Wells | GROSS PRODUCTION | NET PRODUCTION | Oil Price ($/bbl) | Gas Price ($/Mcf) | NGL Price ($/gal) | ||||||||

Oil, (Mbbl) | Gas, (MMcf) | NGL, (Mgal) | OIl, (Mbbl) | Gas, (MMcf) | NGL, (Mgal) | |||||||||

2015 | 0 | 0.0 | 0.0 | 0.00 | 0.0 | 0.0 | 0.00 | 0.00 | 0.00 | 0.00 | ||||

After | 0.0 | 0.0 | 0.00 | 0.0 | 0.0 | 0.00 | 0.00 | 0.00 | 0.00 | |||||

Remaining | 0.0 | 0.0 | 0.00 | 0.0 | 0.0 | 0.00 | 0.00 | 0.00 | 0.00 | |||||

Cumulative | 193.1 | 14.8 | 0.0 | |||||||||||

Ultimate | 193.1 | 14.8 | 0.0 | |||||||||||

Year Ending 12-31 | Net Sales | Other Revenue | Production Taxes | Operating Expense | Exp/Cap Invest | Net Income | Cumulative Net Income | Pres. Worth @ 10.00% | ||||||||||||||||

--(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | |||||||||||||||||

2015 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||||||||||||

After | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||||||||||||

Total | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||||||||||||

2/9/15 | This forecast accompanies the COLLARINI ASSOCIATES report and is subject to its specific conditions. | |||||||||||||||||||||||

PROJECTION OF ESTIMATED PRODUCTION AND REVENUE GLORI HOLDINGS INC. AS OF JANUARY 01, 2015 | ||||||||||||

SEC Pricing 12-31-14 | ||||||||||||

SHUCK FIELD | Present Worth Profile | |||||||||||

Total | ––Mid-Year Discounting–– | |||||||||||

Proved Shut-In | 8.00 | % | 0.0 | 25.00 | % | 0.0 | ||||||

10.00 | % | 0.0 | 30.00 | % | 0.0 | |||||||

12.00 | % | 0.0 | 35.00 | % | 0.0 | |||||||

15.00 | % | 0.0 | 40.00 | % | 0.0 | |||||||

20.00 | % | 0.0 | 50.00 | % | 0.0 | |||||||

Year Ending 12-31 | Gross Wells | GROSS PRODUCTION | NET PRODUCTION | Oil Price ($/bbl) | Gas Price ($/Mcf) | NGL Price ($/gal) | ||||||

Oil, (Mbbl) | Gas, (MMcf) | NGL, (Mgal) | OIl, (Mbbl) | Gas, (MMcf) | NGL, (Mgal) | |||||||

2015 | 1 | 0.0 | 0.0 | 0.00 | 0.0 | 0.0 | 0.00 | 0.00 | 0.00 | 0.00 | ||

After | 0.0 | 0.0 | 0.00 | 0.0 | 0.0 | 0.00 | 0.00 | 0.00 | 0.00 | |||

Remaining | 0.0 | 0.0 | 0.00 | 0.0 | 0.0 | 0.00 | 0.00 | 0.00 | 0.00 | |||

Cumulative | 459.8 | 14.8 | 0.0 | |||||||||

Ultimate | 459.8 | 14.8 | 0.0 | |||||||||

Year Ending 12-31 | Net Sales | Other Revenue | Production Taxes | Operating Expense | Exp/Cap Invest | Net Income | Cumulative Net Income | Pres. Worth @ 10.00% | ||||||||||||||||

--(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | |||||||||||||||||

2015 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||||||||||||

After | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||||||||||||

Total | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||||||||||||

2/9/15 | This forecast accompanies the COLLARINI ASSOCIATES report and is subject to its specific conditions. | |||||||||||||||||||||||

PROJECTION OF ESTIMATED PRODUCTION AND REVENUE SHUCK FIELD GLORI HOLDINGS INC. AS OF JANUARY 01, 2015 | ||||||||||||||

Etzold Unit North Well #1-1 | ||||||||||||||

Proved Shut-In | ||||||||||||||

Lower Chester Sand | Present Worth Profile | |||||||||||||

––Mid-Year Discounting–– | ||||||||||||||

SEC Pricing 12-31-14 | 8.00 | % | 0.0 | 25.00 | % | 0.0 | ||||||||

Initial | Final | 10.00 | % | 0.0 | 30.00 | % | 0.0 | |||||||

Gross Working Interest | 1.000000 | 1.000000 | 12.00 | % | 0.0 | 35.00 | % | 0.0 | ||||||

Net Revenue Interest | 0.800000 | 0.800000 | 15.00 | % | 0.0 | 40.00 | % | 0.0 | ||||||

20.00 | % | 0.0 | 50.00 | % | 0.0 | |||||||||

Year Ending 12-31 | Gross Wells | GROSS PRODUCTION | NET PRODUCTION | Oil Price ($/bbl) | Gas Price ($/Mcf) | NGL Price ($/gal) | ||||||||

Oil, (Mbbl) | Gas, (MMcf) | NGL, (Mgal) | OIl, (Mbbl) | Gas, (MMcf) | NGL, (Mgal) | |||||||||

2015 | 1 | 0.0 | 0.0 | 0.00 | 0.0 | 0.0 | 0.00 | 0.00 | 0.00 | 0.00 | ||||

After | 0.0 | 0.0 | 0.00 | 0.0 | 0.0 | 0.00 | 0.00 | 0.00 | 0.00 | |||||

Remaining | 0.0 | 0.0 | 0.00 | 0.0 | 0.0 | 0.00 | 0.00 | 0.00 | 0.00 | |||||

Cumulative | 459.8 | 14.8 | 0.0 | |||||||||||

Ultimate | 459.8 | 14.8 | 0.0 | |||||||||||

Year Ending 12-31 | Net Sales | Other Revenue | Production Taxes | Operating Expense | Exp/Cap Invest | Net Income | Cumulative Net Income | Pres. Worth @ 10.00% | ||||||||||||||||

--(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | --(M$)-- | |||||||||||||||||

2015 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||||||||||||

After | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||||||||||||

Total | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||||||||||||

2/9/15 | This forecast accompanies the COLLARINI ASSOCIATES report and is subject to its specific conditions. | |||||||||||||||||||||||