Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Fuel Systems Solutions, Inc. | Financial_Report.xls |

| EX-31.2 - EX-31.2 - Fuel Systems Solutions, Inc. | fsys-ex312_201412316.htm |

| EX-32.2 - EX-32.2 - Fuel Systems Solutions, Inc. | fsys-ex322_201412317.htm |

| EX-23.1 - EX-23.1 - Fuel Systems Solutions, Inc. | fsys-ex231_201412318.htm |

| EX-31.1 - EX-31.1 - Fuel Systems Solutions, Inc. | fsys-ex311_2014123110.htm |

| EX-32.1 - EX-32.1 - Fuel Systems Solutions, Inc. | fsys-ex321_2014123111.htm |

| EX-21.1 - EX-21.1 - Fuel Systems Solutions, Inc. | fsys-ex211_201412319.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

or

|

¨ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File No.: 001-32999

FUEL SYSTEMS SOLUTIONS, INC.

(Exact Name of Registrant as Specified in Its Charter)

|

Delaware |

|

20-3960974 |

|

(State or Other Jurisdiction Of Incorporation or Organization) |

|

(I.R.S. Employer Identification No.) |

780 Third Avenue, 25th Floor, New York, New York 10017

(Address of Principal Executive Offices, Including Zip Code)

(646) 502-7170

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, $0.001 par value per share (including attached Stock Purchase Rights)

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer x Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the common stock held by non-affiliates of the registrant as of June 30, 2014, was approximately $205.5 million based upon the closing sale price of the registrant’s common stock of $11.14 on June 30, 2014, as reported on the Nasdaq Stock Market.

As of February 13, 2015, the registrant had 19,331,413 shares of common stock, $0.001 par value per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement which will be filed with the SEC in connection with the 2015 Annual Meeting of Shareholders are incorporated by reference into Part III of this Form 10-K.

FUEL SYSTEMS SOLUTIONS, INC.

TABLE OF CONTENTS

|

|

|

|

Page |

|

|

|

PART I

|

|

|

Item 1. |

|

4 |

|

|

Item 1A. |

|

10 |

|

|

Item 1B. |

|

17 |

|

|

Item 2. |

|

17 |

|

|

Item 3. |

|

17 |

|

|

Item 4. |

|

17 |

|

|

|

|

PART II

|

|

|

Item 5. |

|

18 |

|

|

Item 6. |

|

19 |

|

|

Item 7. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

21 |

|

Item 7A. |

|

38 |

|

|

Item 8. |

|

38 |

|

|

Item 9. |

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

38 |

|

Item 9A. |

|

38 |

|

|

Item 9B. |

|

39 |

|

|

|

|

PART III

|

|

|

Item 10. |

|

40 |

|

|

Item 11. |

|

40 |

|

|

Item 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

40 |

|

Item 13. |

|

Certain Relationships and Related Transactions and Director Independence |

40 |

|

Item 14. |

|

41 |

|

|

|

|

PART IV

|

|

|

Item 15. |

|

42 |

|

|

|

|

45 |

|

|

|

|

F-1 |

2

FORWARD-LOOKING STATEMENTS

This Form 10-K contains certain forward-looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995. These statements may be found throughout this Form 10-K. These statements are not historical facts, but instead involve known and unknown risks, uncertainties and other factors that may cause our or our company’s actual results, levels of activity, performance or achievements to be materially different from the information expressed or implied by these forward looking statements. Statements in this Form 10-K that are not historical facts are hereby identified as “forward-looking statements” for the purpose of the safe harbor provided by Section 21E of the Securities Exchange Act of 1934, as amended, and Section 27A of the Securities Act of 1933, as amended. Words such as: “may,” “will,” “would,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” “continue,” “seeks,” “on-going” or the negative of these terms or other comparable terminology often identify forward-looking statements, although not all forward-looking statements contain these words. You should consider statements that contain these words carefully because they describe our expectations, plans, strategies and goals and beliefs concerning future business conditions, our results of operations, financial position and our business outlook, or state other “forward-looking” information based on currently available information. There are a number of important factors that could cause actual results to differ materially from the results anticipated by these forward-looking statements. These risks and uncertainties and certain other factors which may impact our continuing business financial condition or results of operations, or which may cause actual results to differ from such forward-looking statements, include, but are not limited to, the unpredictable nature of the developing alternative fuel U.S. automotive market, customer dissatisfaction with our products or services, the inability to deliver our products on schedule, a further slowing of economic activity, our ability to maintain customer program relationships, potential changes in tax policies and government incentives and their effect on the economic benefits of our products to consumers, the continued weakness in financial and credit markets, the growth of non-gaseous alternative fuel products and other new technologies, the price differential between alternative gaseous fuels and gasoline, and the repeal or implementation of government regulations relating to reducing vehicle emissions, economic uncertainties caused by political instability in certain of the markets we do business in, the impact of the Argentinean debt crisis on our business, our ability to realign costs with current market conditions, as well as the risks and uncertainties included in Item 1A “Risk Factors” of this Form 10-K. These forward-looking statements are not guarantees of future performance. We cannot assure you that the forward-looking statements in this Form 10-K will prove to be accurate. Furthermore, if our forward-looking statements prove to be inaccurate, the inaccuracy may be material. In light of the significant uncertainties in these forward-looking statements, you should not place undue reliance on these forward looking statements. The forward-looking statements made in this Form 10-K relate to events and state our beliefs, intent and our view of future events only as of the date of the filing of this Form 10-K. We undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events.

3

PART I

PART I

Overview

Fuel Systems Solutions is a leader in providing alternative fuel systems for transportation, industrial, and refueling applications worldwide as well as idle reduction technologies for the heavy duty truck and rail markets. By combining the expertise of industry leading BRC and IMPCO Technologies, Inc. in 2005, as well as further strategic and focused acquisitions, Fuel Systems Solutions represents over 50 years of experience in the industry. We have a global presence and operate in geographies and markets that are underpenetrated and growing, driven by compelling economics, government support, and local demand. Our dedicated and bi-fuel technologies offer our customers a broad range of cost-effective products and applications that we tailor to local specifications. Our technologies enable our customers to:

|

· |

benefit from significantly lower retail fuel prices, capturing the differential between traditional fuels and compressed natural gas (CNG), liquid propane gas (LPG), and other gaseous fuels; |

|

· |

contribute to cleaner air and environment as carbon emissions of natural gas are in general lower than gasoline and diesel; and |

|

· |

help displace oil and exploit natural gas reserves so as to increase energy independence. |

Our components and systems control the pressure and flow of gaseous alternative fuels, such as propane and natural gas used in internal combustion engines. Our products improve efficiency, enhance power output and reduce emissions by electronically sensing and regulating the proper proportion of fuel and air required by the internal combustion engine. We also provide engineering and systems integration services to address our individual customer requirements for product performance, durability and physical configuration. We supply our products and systems to the marketplace through a global distribution network of distributors and dealers in more than 60 countries and through numerous original equipment manufacturers, or OEMs.

We offer an array of components, systems and fully integrated solutions for our customers, including:

|

· |

fuel delivery—pressure regulators, fuel injectors, flow control valves and other components designed to control the pressure, flow and/or metering of gaseous fuels; |

|

· |

electronic controls—solid-state components and proprietary software that monitor and optimize fuel pressure and flow to meet manufacturers’ engine requirements; |

|

· |

gaseous fueled internal combustion engines—engines manufactured by OEMs that are integrated with our fuel delivery and electronic controls; |

|

· |

systems integration—systems integration support to integrate the gaseous fuel storage, fuel delivery and /or electronic control components and sub-systems to meet OEM and aftermarket requirements; |

|

· |

auxiliary power systems—fully integrated auxiliary power systems for truck and diesel locomotives; and |

|

· |

natural gas compressors—natural gas compressors and refueling systems for light and heavy duty refueling applications. |

Automobile manufacturers, taxi companies, transit and shuttle bus companies and delivery fleets are among the most active customers for our transportation products. Our largest markets for transportation products are currently, and have historically been, outside the United States. To capture demand in the now emerging United States market for alternative gaseous fuel-powered vehicles and equipment, we have a full suite of automotive capabilities, including U.S. Environmental Protection Agency (“EPA”) certified product lines, a California Air Resources Board (“CARB”) certified product line and in-house OEM systems engineering platform, enhancing our ability to leverage our existing relationship with fleet customers and other manufacturers as they roll out CNG and LPG versions of key fleet vehicles in North America.

Manufacturers of industrial mobile and power generation equipment, stationary engines, and heavy duty trucks and buses are among the most active customers for our industrial products. Our broad product range allows us to provide turnkey EPA and CARB-certified and non-certified engine systems, customer specified fuel systems modules and/or components, as well as auxiliary power units (APUs). The wide availability of gaseous fuels in world markets combined with their lower emissions and cost compared to gasoline and diesel fuels is driving growth in the global alternative fuel industry.

4

Unless the context otherwise requires, the terms “we,” “us,” “our”, “Fuel Systems” and “the Company” refer to Fuel Systems Solutions, Inc., or Fuel Systems and its subsidiaries. We were incorporated in Delaware in 1985 after having provided automotive and alternative fuel solutions in a variety of organizational structures since 1958. In 2006, we reorganized our business and corporate structure creating Fuel Systems Solutions, Inc. as a holding company. Beginning with the second quarter of 2012, in an effort to more properly align structure and business activities, management reorganized operations into two new operating segments, FSS Industrial and FSS Automotive. Our FSS Industrial operations consist of our industrial mobile and stationary, APU, and the heavy duty commercial transportation operations. Our FSS Automotive operations consist of the company’s passenger and light duty commercial transportation (OEM), automotive aftermarket, and transportation infrastructure operations.

The predecessor to Fuel Systems was IMPCO Technologies, Inc., and all of our filings with the Securities and Exchange Commission (“SEC”) prior to our reorganization are filed under the name of IMPCO Technologies, Inc. Our periodic and current reports, and any amendments to those reports, are available, free of charge, as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC on our website: www.fuelsystemssolutions.com. The information on our website is not incorporated by reference into this report. You may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street NE, Washington, D.C. 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains an Internet site that contains reports, proxy and information statements, and other information regarding us at http://www.sec.gov.

Our Industry

Our business is primarily focused on the alternative fuel industry. We believe three independent market factors—economics, energy independence and environmental concerns—are driving the growth of the market for alternative fuel technology. We believe the historic price differential between propane or natural gas and gasoline and diesel results in an economic benefit to end users of alternative fuel technology. In transportation markets, the price of alternative fuels such as natural gas or propane is typically substantially less than the price of gasoline. By converting a liquid fueled internal combustion engine to run on propane or natural gas, customers can capitalize on this fuel price differential. End-users may recoup the cost of the conversion within six to eighteen months, depending on the fuel cost disparity prevailing at the time and fuel usage. In addition to economic benefits of alternative fuels to end-users, some governments have sought to create a demand for alternative fuels in order to reduce their dependence on imported oil and reduce their unfavorable balance of payments by relying on their natural gas reserves. Alternative fuel vehicles that operate on natural gas or propane can lessen the demand for crude oil.

We are directly involved in two markets: automotive and industrial. These markets have seen growth in the use of clean-burning gaseous fuels due to the less harmful emissions effects of gaseous fuels and the cost advantage available in many markets of gaseous fuels over gasoline and diesel fuels.

Automotive

According to the most recent statistics from the World LP Gas Association and International Association for Natural Gas Vehicles, there are over 23 million propane, or LPG, vehicles and approximately 16.7 million natural gas vehicles in use worldwide, either for personal mobility, fleet conveyance, or public transportation. As the world’s vehicle population increases, it is expected that the passenger vehicle fleet growth will occur in developing countries within Asia, North Africa and areas of the Middle East. These regions currently have the lowest ratio of vehicles per one thousand people and are slated to grow rapidly over the next ten years as economic improvements stimulate personal vehicle ownership. In Europe, Asia and Latin America, alternative fuel vehicles operating on propane and natural gas are widely available through OEM and aftermarket distribution channels and have gained important penetration of total vehicles in circulation in many countries.

In the United States the transportation market for LPG, CNG and other gaseous fuel vehicles has been limited, but recently a market for dedicated and bi-fuel natural gas vehicles has emerged and we believe we are well positioned to take advantage of opportunities as they develop. See Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Overview”.

Industrial

Engines in equipment such as forklifts, aerial platforms, sweepers, turf equipment, power generators and other industrial equipment have long been workhorses of developed countries and comprise a significant portion of our global business. With developed countries such as the United States, and the countries in Asia and Europe seeking a broader consensus on regulation of emission sources in an attempt to further reduce air pollution, many countries have legislated, and we believe will continue to legislate, emission standards for this type of equipment.

5

Our industrial brands focus on serving the market with fuel systems, services and emission certified engine packages. With the imposition of new emissions regulations, OEMs will require advanced technologies that permit the use of gaseous fuels in order to satisfy not only new regulations but also their customers’ requirements for durability, performance and reliability. We have developed and are currently supplying a series of advanced technology alternative fuel systems to the industrial OEM market under the brand name Spectrum®.

Competitive Advantages

We believe we have developed a technological leadership position in the alternative fuel industry based on our experience in designing, manufacturing and commercializing alternative fuel delivery products and components; our relationships with leading companies in transportation; our knowledge of the power generation and industrial markets; our financial commitment to research and product development; and our proven ability to develop and commercialize new products. We believe our competitive strengths include:

|

· |

strong technological base; |

|

· |

strong global distribution and OEM customer relationships; |

|

· |

extensive manufacturing experience; |

|

· |

established systems integration expertise; and |

|

· |

participating in end-markets with growth and served by a global footprint. |

Customers and Strategic Relationships

Our customers include some of the world’s largest engine, vehicle and industrial equipment OEMs.

We are working with a number of our customers to address their future product and application requirements as they integrate more advanced, certified gaseous fuel systems into their business strategies. Additionally, we continually survey and evaluate the benefits of joint ventures, acquisitions and strategic alliances with our customers and other participants in the alternative fuel industry to strengthen our global business position.

In 2014, 2013, and 2012, no customers represented more than 10.0% of our consolidated sales. During 2014, 2013, and 2012, sales to our top ten customers accounted for 26.3%, 34.1%, and 28.7% of our consolidated sales, respectively. If our largest customer or several of these key customers were to reduce their orders substantially, we would suffer a decline in sales and profits, and those declines could be substantial.

Products and Services

Our products include gaseous fuel regulators, fuel shut-off valves, fuel metering and delivery systems, complete engine systems, auxiliary power systems and electronic controls for use in internal combustion engines for the transportation, mobile and power generation markets. In addition to these core products, which we manufacture, we also design, assemble and market ancillary components required for complete systems operating on alternative fuels, as well as a complete range of compressors for natural gas refueling applications.

6

All of our products are designed, tested and validated in accordance with our own internal requirements, as well as tested and certified with major regulatory and safety agencies throughout the world, including Underwriters Laboratories in North America, TÜV in Europe, and the Environmental Protection Agency and CARB in the United States. The following table describes the features of our products:

|

Products |

|

|

Features |

|

Fuel Metering |

|

· |

Full range of injectors designed to operate on propane, natural gas or biogas fuels |

|

|

|

|

|

|

|

|

· |

Electronic control overlays allow integration with modern emissions monitoring systems for full emissions compliance capability |

|

|

|

|

|

|

|

|

· |

Designed for high resistance to poor fuel quality |

|

|

|

|

|

|

Fuel Regulation |

|

· |

Reduces pressure of gaseous and liquid fuels |

|

|

|

|

|

|

|

|

· |

Vaporizes liquid fuels |

|

|

|

|

|

|

|

|

· |

Handles a wide range of inlet pressures |

|

|

|

|

|

|

Fuel Shut-Off |

|

· |

Mechanically or electronically shuts off fuel supply to the regulator and engine |

|

|

|

|

|

|

|

|

· |

Available for high-pressure vapor natural gas and low-pressure liquid propane |

|

|

|

|

|

|

|

|

· |

Designs also incorporate standard fuel filtration to ensure system reliability |

|

|

|

|

|

|

Electronics & Controls |

|

· |

Provides closed loop fuel control allowing integration with existing sensors to ensure low emissions |

|

|

|

|

|

|

|

|

· |

Integrates gaseous fuel systems with existing engine management functions |

|

|

|

|

|

|

Engine-Fuel Delivery Systems |

|

· |

Turnkey kits for a variety of engine sizes and applications |

|

|

|

|

|

|

|

|

· |

Customized applications interface based on customer requirements |

|

|

|

|

|

|

Fuel Systems |

|

· |

Complete vehicle and equipment systems for aftermarket and post-production OEM conversion |

|

|

|

|

|

|

|

|

· |

Complete engine and vehicle management systems for heavy on-highway vehicles |

|

|

|

|

|

|

|

|

· |

Complete engine and vehicle management systems for off-highway and industrial engines used for material handling, power generation and industrial applications |

|

|

|

|

|

|

Compressors |

|

· |

Complete range of compressors for natural gas refueling applications and turnkey refueling stations |

|

|

|

|

|

|

Auxiliary Power Systems |

|

· |

Range of auxiliary power systems products for truck and rail applications |

7

We have developed capabilities that we use to develop a broad range of products to satisfy our customers’ needs and applications. These capabilities/applications fall into the following categories:

|

Capabilities |

|

|

Applications |

|

Design and Systems Integration |

|

· |

Strong team of applications engineers for component, system and engine level exercises providing support to customers in the application of our gaseous fuel products |

|

|

|

|

|

|

|

|

· |

Applications engineering services for whole vehicle/machine integration outside of our products |

|

|

|

|

|

|

|

|

· |

Full three dimensional design modeling and component rapid prototyping services |

|

|

|

|

|

|

Certification |

|

· |

Certification of component products and systems in line with the requirements of California Air Resources Board and Environmental Protection Agency for off- highway engines as well as European ECE-ONU certifications |

|

|

|

|

|

|

|

|

· |

Provide customers with the required tools to manage in-field traceability and other requirements beyond initial emission compliance |

|

|

|

|

|

|

Testing and Validation |

|

· |

Component endurance testing |

|

|

|

|

|

|

|

|

· |

Component thermal and flow performance cycling |

|

|

|

|

|

|

|

|

· |

Engine and vehicle testing and evaluation for performance and emissions |

|

|

|

|

|

|

Sub-System Assembly |

|

· |

Pre-assembled modules for direct delivery to customers’ production lines |

|

|

|

|

|

|

|

|

· |

Sourcing and integrating second and third tier supplier components |

|

|

|

|

|

|

Final Assembly & Test |

|

· |

Full vehicle final up-fit assembly and test operating as an extension of the OEM production line/process |

|

|

|

|

|

|

Training and Technical Service |

|

· |

Complete technical service support, including technical literature, web-based information, direct telephone interface (in all major countries) and on-site support |

|

|

|

|

|

|

|

|

· |

Training services through sponsored programs at approved colleges, at our facilities worldwide and on-site at customer facilities |

|

|

|

|

|

|

Service Parts and Warranty Support |

|

· |

Access to service parts network, along with direct support in development of customers’ own internal service parts programs and procedures |

|

|

|

|

|

Sales and Distribution

We sell products through a worldwide network encompassing distributors and dealers in more than 60 countries and through a sales force that develops sales with distributors, OEMs and large end-users. Our operations focus on OEM and aftermarket distributors in the transportation, mobile and power generation markets. Of these markets, we believe that the greatest potential for growth is in the Asia, North and South America and Middle East regions in sales to transportation OEMs and aftermarket distributors and installers and in North America in sales to industrial OEMs and the related aftermarket.

During the years 2014, 2013, and 2012, sales to distributors accounted for 77.5%, 71.6%, and 68.7%, respectively, of our revenue, and sales to OEM customers accounted for 22.5%, 28.4%, and 31.3%, respectively, of our revenue.

Distributors generally service the aftermarket business for the conversion of liquid fueled engines to gaseous fuels. Many distributors have been our customers for more than 20 years.

Information regarding revenue, income and assets of each of our two business segments, FSS Industrial operations and FSS Automotive operations, and our revenue and assets by geographic area is included in Note 19 to the consolidated financial statements included elsewhere in this Annual Report on Form 10-K as well as in Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations”.

8

Manufacturing

We manufacture and assemble a majority of our products at our facilities in Santa Ana, California, Union City, Indiana, Kitchener, Canada, Beccar, Argentina and Cherasco, Italy and to a lesser extent at some of our other international facilities. Current manufacturing operations consist primarily of mechanical component assembly and testing, forging and light machining, electronic PCB assembly and testing and system up-fitting. We rely on outside suppliers for parts and components and obtain components for products from a variety of domestic and foreign automotive and electronics suppliers, die casters, stamping operations, specialized diaphragm manufacturers and machine shops.

Machined die cast aluminum parts and supplier engineered parts represent the major components of our cost of sales. Coordination with suppliers for quality control and timely shipments is a high priority to maximize inventory management. We use a computerized material requirement planning system to schedule material flow and balance the competing demands of timely shipments, productivity and inventory management. Our manufacturing facilities in California, Canada, and Argentina are ISO-9001 certified, while the facilities in Italy are ISO/TS-16949 and ISO-9001 certified.

Research and Development

Our research and development programs provide the technical capabilities that are required for the development of systems and products that support the use of gaseous fuels in internal combustion engines. Our research and development is focused on fuel delivery and electronic control systems and products for motor vehicles, engines, forklifts, stationary engines and small industrial engines. Over the past few years, we expanded our research and development facility in Italy and in the U.S. to continue to serve our customers with new products and capabilities. Our research and development expenditures were approximately $26.2 million, $27.5 million, and $28.3 million, in 2014, 2013, and 2012, respectively.

Competition

Our key competitors in gaseous fuel delivery products, accessory components and engine conversions markets include Westport Innovations Inc. located in Canada; Enovation Controls LLC and Woodward, Inc. located in North America; Landi Group and O.M.T. Tartarini, S.r.L. located in Italy; and Nikki Company Ltd. located in Japan. These companies, together with us, account for a majority of the world market for alternative fuel products and services. In the future, we may face competition from traditional automotive component suppliers, such as the Bosch Group, Delphi Corporation, Siemens VDO Automotive AG, and Visteon Corporation, and from motor vehicle OEMs that develop fuel systems internally. Industry participants compete on price, product performance and customer support.

Product Certification

We must obtain emission compliance certification from the Environmental Protection Agency to sell certain of our products in the United States, receive certification from CARB to sell certain products in California and other states, and meet European standards for emission regulations in Europe. Each car, truck, van or engine sold in each of these markets must be certified before it can be introduced into commerce, and its products must meet component, subsystem and system level durability, emission, refueling and various idle tests. We have also obtained international emissions compliance certification in Europe, Thailand and India. We strive to meet stringent industry standards set by various regulatory bodies. Approvals enhance the acceptability of our products in the worldwide marketplace. Many foreign countries also accept these agency approvals as satisfying the “approval for sale” requirements in their markets.

Employees

As of December 31, 2014, we employed approximately 1,500 persons. Of these employees, approximately 300 were employed in our FSS Industrial operations, of which approximately 170 are non-US employees, and approximately 1,200 were employed in our FSS Automotive operations, of which approximately 1,100 are foreign employees. Employees in Italy, the Netherlands and Argentina are represented by a collective bargaining agreement. Personnel employed by our foreign subsidiaries are often subject to national labor contracts. We consider our relations with our current employees and unions to be good.

Intellectual Property

We currently rely primarily on patent and trade secret laws to protect our intellectual property. We currently have numerous patents registered in countries located in North America, Europe, and Asia. We do not expect the expiration of our patents to have a material effect on our revenue.

9

We also rely on a combination of trademark, trade secret and other intellectual property laws and various contract rights to protect our proprietary rights. We believe that our intellectual property protected by copyright and trademark protection is less significant than our intellectual property protected by patents.

An expansion of OEM offering of gaseous fuel vehicles employing internally developed OEM technology would likely result in a decrease in our revenue and profit margins.

We derive a substantial portion of our revenue from the sale of gaseous fuel systems and components to automobile OEMs. An expansion in the offering of OEM gaseous fuel vehicles employing internally developed OEM technology could reduce demand for our systems and components and would likely have a negative impact on our revenue and profits.

We currently face, and will continue to face, significant competition, which could materially and adversely affect us.

We currently compete with companies that manufacture products to convert liquid-fueled internal combustion engines to gaseous fuels. Our competitors in the future may have greater name recognition, larger customer bases, broader global reach and a wider array of product lines, as well as greater financial resources and access to capital than we have. We are also subject to competition from other alternative fuels and alternative fuel technologies, including ethanol, electric and hybrid electric and fuel cells, and we cannot assure you that such technologies will not be favored over gaseous fuel technologies in the future. We also cannot assure you that our competitors will not create new and improved innovative gaseous fuel technologies. Increases in the market for alternative fuel vehicles may cause automobile or engine manufacturers to develop and produce their own fuel conversion or fuel management equipment rather than purchasing the equipment from suppliers such as us or to employ competing technologies. Further, greater acceptance of alternative fuel engines may result in new competitors. Should any of these events occur, either alone or in combination, the total potential demand for, and pricing of, our products could be negatively affected and cause us to lose business, which could materially and adversely affect us.

We maintain a significant investment in inventory and have made significant investments in the expansion of our operations to meet demand for our product without long-term contracts with customers. A decline in our customers’ purchases would lead to a decline in our revenue and could result in a decrease in our operating results and cash flows.

We do not have long-term contracts with our customers. Generally, our product sales are made on a purchase order basis, which allows our customers to reduce or discontinue their purchases from us. Accordingly, we cannot predict the timing, frequency or size of our future customer orders. Our ability to accurately forecast our sales is further complicated by the continuing global economic and financial uncertainty. Our total inventory at December 31, 2014 was $80.0 million, a decrease of $15.1 million compared to our total inventory at December 31, 2013. If we fail to anticipate the changing needs of our customers and accurately forecast our customer demands, our existing and potential customers may not place orders with us, which would decrease our revenue, and we may accumulate significant inventories of products that we will be unable to sell which may result in a significant decline in the value of our inventory. As a result, our revenue, gross profit and other operating results and cash flows may be materially and adversely affected.

We may continue to make significant investments in our business without any guarantees or long-term commitments from our customers that they will continue to purchase our components and systems with the same timing, frequency and size as we expect. As a result, if there is insufficient demand for our components and systems, we may not recover the costs of any increased investment in our operations, which could have a material, adverse effect on our financial position, liquidity and results of operations.

Reduced consumer or corporate spending due to weakness in the financial markets and uncertainties in the economy, domestically and internationally, may materially and adversely affect our revenue, operating results and cash flows.

We depend on demand from the consumer, OEM, contract manufacturing, industrial, automotive and other markets we serve for the end market applications that use our products and services. All of these markets have been, and may continue to be, affected by the instability in global financial markets. Reductions in consumer or corporate demand for our products and services as a result of uncertain conditions in the macroeconomic environment, such as volatile energy prices, inflation, fluctuations in interest rates, difficulty securing credit, extreme volatility in security prices, diminished liquidity, or other economic factors, may materially and adversely affect our revenue, operating results and cash flows.

Weak economic conditions, such as those being experienced in Europe, may materially impact our customers and suppliers with which we do business. Currently, the demand in Europe for new automobiles remains weak. Economic and financial market conditions that adversely affect our customers may cause them to terminate existing purchase orders, reduce the volume of products

10

they purchase from us in the future or seek price concessions. In connection with the sale of products, we normally do not require collateral as security for customer receivables and do not purchase credit insurance. We may have significant balances owing from customers who operate in cyclical industries or who may not be able to secure sufficient credit in order to honor their obligations to us. Failure to collect a significant portion of amounts due on those receivables could have a material adverse effect on our results of operations, liquidity and financial condition.

Adverse economic and financial market conditions may also cause our suppliers to be unable to provide materials and components to us or may cause suppliers to make changes in the credit terms they extend to us, such as shortening the required payment period for our amounts owing them or reducing the maximum amount of trade credit available to us. While we have not yet experienced changes of this type, they could have a material adverse effect on our results of operations, liquidity and financial condition. If we are unable to successfully anticipate changing economic and financial markets conditions, we may be unable to effectively plan for, and respond to, those changes, and we could be materially and adversely affected.

Currency exchange rate fluctuations may adversely affect our operating results and cash flows and may have a material adverse effect on our revenue and overall financial results.

Because of our significant operations outside of the United States, we engage in business relationships and transactions that involve many different currencies. Exchange rates between the U.S. dollar and the local currencies in these foreign locations where we do business can vary unpredictably. These variations may have an effect on the prices we pay for key materials and services from overseas vendors in our functional currencies under agreements that are priced in local currencies. If the rate of the U.S. dollar depreciates against local currencies, our effective costs for such materials and services would increase, adversely affecting our operating results and cash flows.

For the year ended December 31, 2014, non-U.S. operations accounted for approximately 81.0% of our revenue. Most revenues and expenses of our non-U.S. operations are in local currency. Our financial statements are presented in U.S. dollars, therefore, gains and losses on the conversion of foreign currency denominated expenses into U.S. dollars could cause fluctuations in our operating results, and fluctuating exchange rates could cause significantly reduced revenue and gross margins from non-U.S. dollar-denominated revenue, which could materially and adversely affect our overall financial results.

Also, for the year ended December 31, 2014, Euro denominated revenue accounted for approximately 55.9% of our total revenue; therefore a substantial appreciation in the rate of exchange of the U.S. dollar against the Euro could have a significant adverse effect on our financial results.

We currently do not engage in financial hedging against these risks and may not be able to hedge against these risks in the future.

Fluctuation in oil or natural gas prices (including LPG) may result in a decline in the demand for our products and services, which would materially and adversely affect our revenue, operating results and cash flows.

We believe that our sales are favorably impacted by changes in consumer demand prompted by rising oil prices and concern over potential increases in oil prices. Conversely, when oil prices decrease and remain low or continue to decrease, it may result in a decline of the demand for our products and services. In addition, volatility in the price of natural gas may have an equal though opposite impact on the demand for our products and services. The potential decline in the demand for our products and services caused by these price fluctuations could materially and adversely affect our revenue, operating results and cash flows.

We engage in related party transactions, which result in a conflict of interest involving our management.

We have engaged in the past, and continue to engage, in a significant number of related party transactions, specifically between the Company’s foreign subsidiaries and members of the family of Mariano Costamagna, our Chief Executive Officer, Director and one of our largest stockholders, his brother Pier Antonio Costamagna (one of our former executive officers who retired, effective February 5, 2014, as General Manager of MTM, S.r.L. (“MTM”), a wholly owned subsidiary of the Company), and companies in which our Chief Executive Officer’s family has controlling or other ownership interests. Our Board of Directors (“Board”), its Audit Committee and its Nominating and Corporate Governance Committee seek to review on an ongoing basis related party transactions as well as identify and evaluate new potential related party transactions to properly account for, disclose and maintain control over these transactions. We cannot assure you that the terms of the transactions with these various related parties are on terms as favorable to us as those that could have been obtained in arm’s-length transactions with third parties, or that the existing policies and procedures are sufficient to identify and completely address all related party transactions and conflicts of interest that may arise. Related party transactions could result in related parties receiving more favorable treatment than an unaffiliated third party would receive, although these parties may provide goods or services that are not readily available elsewhere in some situations. In addition, related party

11

transactions present difficult conflicts of interest, could result in significant and minor disadvantages to our company and may impair investor confidence, which could materially and adversely affect us. Related party transactions could also cause us to become materially dependent on related parties in the ongoing conduct of our business, and related parties may be motivated by personal interests to pursue courses of action that are not necessarily in the best interests of our company and our stockholders.

We face risks associated with marketing, distributing, and servicing our products internationally and could be adversely affected if we are unable to grow our business in developing and emerging markets or as a result of political and economic instability or civil unrest in these markets.

In addition to our operations in the United States, we currently operate in Canada, Italy, the Netherlands, Japan, Brazil, Argentina and Venezuela, and market our products and technologies in other international markets, including both industrialized and developing countries. During the years ended December 31, 2014, 2013, and 2012 approximately 27.2%, 29.7%, and 25.0% of our revenue, respectively, was derived from sales to customers located within the United States and Canada. During the years ended December 31, 2014, 2013, and 2012 approximately 72.8%, 70.3%, and 75.0% of our revenue, respectively, was derived from sales to customers located in Asia-Pacific, Europe, and Latin America. Additionally, at December 31, 2014, approximately 84.0% of our employees and 65.2% of our distributors and dealers worldwide were located outside the United States. Political and economic instability or civil unrest in the markets where we operate, including Venezuela, could have a material adverse impact on our sales.

Our combined international operations are subject to various risks common to international activities, such as the following:

|

· |

our ability to maintain good relations with our overseas employees, suppliers, distributors and customers to collect amounts owed from our overseas customers; |

|

· |

the possibility that our distributors and agents will continue to sell products into countries subject to United States sanctions notwithstanding our policies prohibiting such sales; |

|

· |

expenses and administrative difficulties associated with maintaining a significant labor force outside the United States, including, without limitation, the need to comply with employment and tax laws and to adhere to the terms of real property leases and other financing arrangements in foreign nations; |

|

· |

exposure to currency fluctuations; |

|

· |

potential difficulties in enforcing contractual obligations and intellectual property rights; |

|

· |

complying with a wide variety of laws and regulations, including product certification, environmental, and import and export laws; |

|

· |

the challenges of operating in disparate geographies and cultures; |

|

· |

political and economic instability; |

|

· |

adverse tax consequences, including, without limitation, restrictions on our ability to repatriate dividends from our subsidiaries; and |

|

· |

Government authorities in some countries that may from time to time use fuel price as an instrument of fiscal policy and taxation that may vary for different types of fuels, including gaseous fuels. |

From time to time, we restructure our manufacturing capacity, and we may have difficulty managing these changes.

From time to time, we engage in a number of manufacturing expansion and contraction projects, based on the then-current and forecasted needs of our business. In addition, from time to time, we engage in international restructuring efforts in order to better align our business functions with our international operations and transition to other lower cost locations in continuation of our cost reduction efforts. These efforts can require significant investment by us, and have in the past and could continue to result in increased expenses, inefficiencies and reduced gross margins.

Our management team may have difficulty managing our manufacturing capacity and transition projects or otherwise managing any growth or downsizing in our business that we may experience. Risks associated with right-sizing our manufacturing capacity may include those related to:

|

· |

managing multiple, concurrent capacity expansion or reduction projects; |

|

· |

managing the reduction of employee headcount for facilities where we reduce or cease our activities; |

12

|

· |

accurately predicting any increases or decreases in demand for our products and managing our manufacturing capacity appropriately; |

|

· |

under-utilized capacity, particularly during the start-up phase of a new manufacturing facility and the effects on our gross margin of under-utilization; |

|

· |

managing increased employment costs and scrap rates often associated with periods of growth or contraction; |

|

· |

implementing, integrating and improving operational and financial systems, procedures and controls, including our computer systems; |

|

· |

construction delays, equipment delays or shortages, labor shortages and disputes and production start-up problems; and |

|

· |

cost overruns and charges related to our expansion or contraction of activities. |

Our management team may not be effective in restructuring our manufacturing facilities, and our systems, procedures and controls may not be adequate to support such changes in manufacturing capacity. Any inability to manage changes in our manufacturing capacity may harm our profitability and growth.

New technologies may render our existing products obsolete, which could materially and adversely affect us.

New developments in technology may negatively affect the development or sale of some or all of our products or make our products obsolete. Our inability to enhance existing products in a timely manner or to develop and introduce new products that incorporate new technologies, conform to increasingly stringent emission standards and performance requirements, and achieve market acceptance in a timely manner could negatively impact our competitive position and may materially and adversely affect us. New product development or modification is costly, involves significant research, development, time and expense and may not necessarily result in the successful commercialization of any new products.

The development of our business is dependent on the availability of gaseous fueling infrastructure

Many countries, including the United States, currently have limited or no infrastructure to deliver natural gas and propane to vehicle based consumers. Currently in the United States, alternative fuels such as natural gas cannot be readily obtained by consumers for motor vehicle use and only a small percentage of motor vehicles manufactured for the United States are equipped to use alternative fuels. Users of gaseous fuel vehicles may not be able to obtain fuel conveniently and affordably, which may adversely affect the demand for our products and services. We cannot assure you that the United States or global market for gaseous fuel engines will expand broadly or, if it does, that it will result in increased sales of our fuel system products.

The unpredictable nature of the developing alternative fuel U.S. automotive business may materially and adversely affect our revenue, operating results and cash flows.

Although we believe that we are positioned to compete in the dedicated and bi-fuel natural gas vehicle (NGV) OEM market emerging in the U.S. and our vehicle modification and systems integration capabilities for a variety of alternative fuel applications (including CNG and propane) present us with a unique advantage, the unpredictable nature of the developing alternative fuel U.S. automotive business may materially and adversely affect our revenue, operating results and cash flows as well as the recoverability of our initial investments. Our U.S. automotive business, through acquisitions and additional investments, has the capabilities necessary to be a leader in the U.S. market but we cannot assure you that this market will continue to develop, at what rate it will develop or whether our investments in this market will result in increased sales for us or be profitable.

We could be adversely affected by violations of the U.S. Foreign Corrupt Practices Act and similar foreign anti-bribery laws.

The U.S. Foreign Corrupt Practices Act (“FCPA”) and similar anti-bribery laws in other jurisdictions prohibit companies and their intermediaries and agents from making improper payments to foreign officials, including employees of government owned businesses, as well as private organizations, for the purpose of obtaining or retaining business. During the last few years, the United States Department of Justice and the SEC have brought an increasing number of FCPA enforcement cases, many resulting in very large fines and deferred criminal prosecutions. We operate in many countries which are viewed as high risk for FCPA compliance. Our Code of Conduct mandates compliance with the FCPA and other similar anti-bribery laws and we have recently instituted training programs for our employees around the world. Despite our training programs and compliance policies, there can be no assurance that all employees and third-party intermediaries (including our distributors and agents) will comply with anti-corruption laws. Any such violation could have a material adverse effect on our business. As part of our anti-bribery policies, in the event that we have reason to believe that our employees, agents, distributors or other third parties that transact the Company’s business have or may have violated applicable anti-corruption laws, including the FCPA, we may investigate or have outside counsel or agents investigate the relevant

13

facts and circumstances. We have incurred and in the future may incur additional compliance costs associated with the implementation of our FCPA compliance policies and training programs, which could have a material impact on our business.

In any acquisition or joint venture that we engage in, we expose ourselves to the possibility that the employees and agents of such businesses may not have conducted themselves in compliance with the anti-corruption laws of the FCPA. In response to increasing FCPA enforcement actions in the United States, we have sought and continue to seek to impose contractual provisions and undertake cost appropriate due diligence. We cannot provide assurance that we will always be protected from the consequences of acts which may have violated the FCPA.

Violations of the FCPA may result in significant civil and criminal fines, as well as criminal convictions. Violations of the FCPA and other foreign anti-bribery laws, or allegations of such violations, could disrupt our business and cause us to suffer civil and criminal financial penalties and other sanctions, which are likely to have a material adverse impact on our business, financial condition, and results of operations.

We are subject to governmental certification requirements and other regulations, and more stringent regulations in the future may impair our ability to market our products.

We must obtain product certification from governmental agencies, such as the Environmental Protection Agency and the California Air Resources Board, to sell certain of our products in the United States and must obtain other product certification requirements in Europe and other regions. A significant portion of our future revenue will depend upon sales of fuel management products that are certified to meet existing and future air quality and energy standards. We cannot assure you that our products will meet these standards in the future. We incur significant research and developments costs to ensure that our products comply with emissions standards and meet certification requirements in the countries where our products are sold. Our failure to comply with certification requirements could result in the recall of our products as well as civil and/or criminal penalties.

Any new government regulation that affects our alternative fuel technologies, whether at the foreign, federal, state, or local level, including any regulations relating to installation and service of these systems, may increase our costs and the price of our systems and adversely affect the effectiveness of the related technologies. As a result, these regulations could materially and adversely affect us.

Our business is directly and significantly affected by regulations relating to reducing vehicle emissions. If current regulations are repealed or if the implementation of current regulations is suspended or delayed, our revenue, operating results and cash flows may decrease significantly.

If regulations relating to vehicle emissions are amended in a manner that may allow for more lenient standards, or if the implementation of such currently existing standards is delayed or suspended, the demand for our products and services could diminish, and our revenue, operating results and cash flows could decrease significantly. In addition, demand for our products and services may be adversely affected by the perception that emission regulations will be suspended or delayed. Accordingly, we rely on stricter emissions regulations, the adoption of which are out of our control and cannot be assured, to stimulate our growth.

Regulations related to “conflict minerals” may force us to incur additional expenses, may make our supply chain more complex and may result in damage to our reputation with customers.

On August 22, 2012, under the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, the SEC adopted requirements for companies that use certain minerals and metals, known as conflict minerals, in their products, whether or not these products are manufactured by third parties. These requirements require companies to perform due diligence, disclose and report whether or not such minerals originate from the Democratic Republic of Congo and adjoining countries. The implementation of these requirements could adversely affect the sourcing, availability and pricing of minerals used in the manufacture of our products. In addition, we may incur additional costs to comply with the disclosure requirements, including costs related to determining the source of any of the relevant minerals and metals used in our products. Since our supply chain is complex, we may not be able to sufficiently verify the origins for these minerals and metals used in our products through the due diligence procedures that we implement, which may harm our reputation. In addition, we may incur additional costs as a result of changes to product, processes or sources of supply as a consequence of these new requirements.

The “conflict mineral” disclosure obligations are complex. Our first report was filed with the SEC on June 2, 2014 and covers our activities during 2013. These reports are dependent upon our implemented systems and processes as well as information provided by our suppliers of products that contain, or potentially contain, conflict minerals. To the extent that the information that we receive from our suppliers is inaccurate or inadequate, or if our implemented systems and processes to obtain that information does not fulfill the SEC’s requirements, we could face both reputational and SEC enforcement risks.

14

Some of our foreign subsidiaries have done business in countries subject to U.S. sanctions and embargoes.

Some of our foreign subsidiaries in the past have sold fuel delivery systems, related parts and accessories to customers in countries currently subject to sanctions and embargoes imposed by the U.S. government, the E.U., the United Nations, and other countries when we did not believe such sales violated these sanctions or embargoes. We may sell products into countries currently subject to sanctions or embargoes if we believe those sales would not violate the sanctions or embargos and the changing embargo regimes with respect to such countries do not present inappropriate business risks. However, the sanctions are complex and are constantly changing. Changing embargo and sanction regimes can make unlawful activities which were previously lawful. We may decide not to sell into countries because of the risk of changing regimes. We believe we have procedures in place to conduct U.S. and foreign operations without violating U.S., EU, or other sanctions. However, if we fail to comply with U.S. sanctions, EU sanctions or other sanctions, we could be subject to material fines and penalties and incur damage to our reputation, which may lead to a reduction in the market price of our common stock.

In addition, our foreign subsidiaries’ sales into such countries, even if they did not violate the sanctions and embargos, could reduce demand for our common stock among certain of our investors.

We have goodwill and intangible assets that may become impaired, which could impact our results of operations.

Approximately $7.0 million, or 2.1%, of our total assets at December 31, 2014 were net intangible assets, including technology, customer relationships and trade name, and approximately $7.4 million, or 2.3%, of our total assets at December 31, 2014 were goodwill that relates to our acquisitions. We amortize the intangible assets, with the exception of goodwill, based on our estimate of their remaining useful lives and their values at the time of acquisition. We are required to test goodwill for impairment at least on an annual basis, or earlier if we determine it may be impaired due to change in circumstances. We are required to test the other intangible assets with definite useful lives for impairment whenever events or changes in circumstances indicate that the carrying amounts of the intangible assets may not be recoverable. If impairment exists in any of these assets, we are required to write-down the related asset to its estimated recoverable value as of the measurement date. Such impairment write-downs may significantly impact our results of operations and financial position. For the year ended December 31, 2014, we recognized an impairment charge of approximately $39.9 million representing the write-off of goodwill associated with three of our reporting units, and an impairment charge of approximately $1.7 million representing write off of intangible assets associated with two of our reporting units. For the year ended December 31, 2012, we recognized an impairment charge of approximately $9.9 million representing the write-off of goodwill and an impairment charge of approximately $9.9 million representing write off of intangible assets associated with two of our reporting units.

We may not be able to successfully integrate our previously acquired businesses or any future acquired businesses into our existing worldwide business without substantial expenses, delays or other operational or financial problems.

As a part of our business strategy, we may seek to acquire additional businesses, technologies or products in the future. We cannot assure you that any prior acquisition or any future transaction we complete will result in long-term benefits to us or our stockholders or that our management will be able to integrate or manage the acquired business effectively, efficiently and in a timely manner. We could also incur unanticipated expenses or losses in connection with any acquisition, including as a result of disputes associated with an earn-out right, or future transaction.

Acquisitions entail numerous risks, including difficulties associated with the integration of operations, technologies, products and personnel that, if realized, could harm our operating results. Risks related to potential acquisitions include, but are not limited to:

|

· |

difficulties in combining previously separate businesses into a single unit; |

|

· |

inability to overcome differences in foreign business practices, accounting practices, customs and importation regulations, language and other barriers in connection with the acquisition of foreign companies; |

|

· |

substantial diversion of management’s time and attention from day-to-day business when evaluating and negotiating such transactions and then integrating an acquired business; |

|

· |

discovery, after completion of the acquisition, of liabilities assumed from the acquired business or of assets acquired; |

|

· |

costs and delays in implementing, and the potential difficulty in maintaining, uniform standards, controls, procedures and policies, including the integration of different information systems; |

|

· |

the presence or absence of adequate internal controls and/or significant fraud in the financial systems of acquired companies; and |

|

· |

failure to achieve anticipated benefits, such as cost savings and revenue enhancements. |

15

The protection of our intellectual property may be costly and ineffective. If we are not able to adequately secure or enforce protection of our intellectual property, then we may not be able to compete effectively and we may not be profitable.

Our future success depends in part on our ability to protect our intellectual property. We rely primarily on patent and trade secret laws to protect our intellectual property. We currently have numerous patents registered in countries located in North America, Europe, and Asia. We also rely on a combination of trademark, trade secret and other intellectual property laws and various contract rights to protect our proprietary rights. However, we cannot be sure that these intellectual property rights provide sufficient protection from competition. Third parties may claim that our products and systems infringe their patents or other intellectual property rights. Third party infringement claims, regardless of their outcome, would not only consume our financial resources, but also would divert the time and effort of our management and could result in our customers or potential customers deferring or limiting their purchase or use of the affected products or services until resolution of the litigation. If a competitor were to challenge our patents, or assert that our products or processes infringe its patent or other intellectual property rights, we could incur substantial litigation costs, be forced to design around their patents, pay substantial damages or even be forced to cease our operations, any of which could be expensive and have an adverse effect on our operating results.

We depend on a limited number of third party suppliers for key materials and components for our products.

We have established relationships with third party suppliers that provide materials and components for our products. A supplier’s failure to supply materials or components in a timely manner or to supply materials and components that meet our quality, quantity or cost requirements, combined with a delay in our ability to obtain substitute sources for these materials and components in a timely manner or on terms acceptable to us, would harm our ability to manufacture our products effectively, or would significantly increase our production costs, either of which could materially and adversely affect us. In addition, we rely on a limited number of suppliers for certain proprietary die cast parts, electronics, software, catalysts and engines for use in our end products. Approximately 23.0%, 26.7%, and 24.4% of our purchases of raw materials and services during the years ended December 31, 2014, 2013, and 2012, respectively, were supplied by ten entities. During 2014, 2013, and 2012, no suppliers represented more than 10.0% of our purchases of raw materials and services.

Class action litigation due to stock price volatility or other factors could cause us to incur substantial costs and divert our management’s time and attention.

From January 1, 2014 through December 31, 2014, our stock price fluctuated from a low of $8.04 to a high of $14.02. From January 1, 2013 through December 31, 2013, our stock price fluctuated from a low of $12.39 to a high of $20.69. From January 1, 2012 through December 31, 2012, our stock price fluctuated from a low of $13.52 to a high of $28.89. In the past, securities class action litigation often has been brought against a company following periods of volatility in the market price of its securities. Any securities litigation could result in substantial costs and could divert the time and attention of our management.

Our actual operating results may differ materially from our guidance.

From time to time, we release guidance in our quarterly earnings releases, quarterly earnings conference calls or otherwise, regarding our future performance that represent our management’s estimates as of the date of release. This guidance, which includes forward-looking statements, is based on projections prepared by our management. These projections are not prepared with a view toward compliance with published guidelines of the American Institute of Certified Public Accountants, and neither our registered public accountants nor any other independent expert or outside party compiles or examines the projections and, accordingly, no such person expresses any opinion or any other form of assurance with respect thereto.

Projections are based upon a number of assumptions and estimates that, while presented with numerical specificity, are inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond our control and are based upon specific assumptions with respect to future business decisions, some of which will change. The principal reason that we release guidance is to provide a basis for our management to discuss our business outlook with analysts and investors. We do not accept any responsibility for any projections or reports published by any such persons.

Guidance is necessarily speculative in nature, and it can be expected that some or all of the assumptions and estimates inherent in the guidance furnished by us will not materialize or will vary significantly from actual results. Accordingly, our guidance is only an estimate of what management believes is realizable as of the date of release. Actual results will vary from our guidance and the variations may be material. In light of the foregoing, investors are urged not to rely upon, or otherwise consider, our guidance in making an investment decision in respect of our common stock.

16

We may have security breaches of our information technology infrastructure and systems

Our information technology infrastructure and systems may be vulnerable to cyber-terrorism, computer viruses, system failures and other intentional or unintentional interference, negligence, fraud and other unauthorized attempts to access or interfere with these systems and proprietary information. Although we believe we have implemented and maintain reasonable security controls over proprietary information as well as information of our customers, stockholders and employees, a breach of these security controls may have a material adverse effect on our business, financial condition and results of operations and could subject us to significant regulatory actions and fines, litigation, loss, third-party damages and other liabilities.

None.

Facilities

Our executive offices are located in New York, New York. We currently lease additional manufacturing, research and development and general office facilities, under leases expiring through 2020, in the following locations set forth below:

|

Location |

|

Principal Uses |

|

Square Footage |

|

|

|

FSS Industrial Operations: |

|

|

|

|

|

|

|

Ontario, Canada |

|

Sales, marketing application, development and assembly, manufacturing |

|

|

110,000 |

|

|

Santa Ana, California |

|

Sales, manufacturing, design, and development |

|

|

108,000 |

|

|

Delfgauw, Holland |

|

Sales, marketing application, development and assembly |

|

|

20,000 |

|

|

Calgary, Canada |

|

Sales, marketing application, development and assembly |

|

|

11,000 |

|

|

Fukuoka, Japan |

|

Sales, marketing application and assembly |

|

|

8,000 |

|

|

FSS Automotive Operations: |

|

|

|

|

|

|

|

Cherasco, Italy |

|

Sales, marketing application, development and assembly, manufacturing |

|

|

678,000 |

|

|

Beccar, Argentina |

|

Sales, marketing and assembly, manufacturing |

|

|

129,000 |

|

|

Sterling Heights, Michigan |

|

Sales, marketing application, development and assembly |

|

|

83,000 |

|

|

Union City, Indiana |

|

Sales, marketing application and assembly |

|

|

75,000 |

|

|

Changodar (Ahmedabad), India |

|

Sales and assembly |

|

|

91,000 |

|

|

Cesena, Italy |

|

Sales, marketing application, development and assembly |

|

|

11,000 |

|

|

Badia, Italy |

|

Sales and assembly |

|

|

15,000 |

|

|

Valencia, Venezuela |

|

Sales and assembly |

|

|

12,000 |

|

|

San Paulo, Brazil |

|

Sales and marketing |

|

|

5,000 |

|

|

Total |

|

|

|

|

1,356,000 |

|

We also lease nominal amounts of office space in various countries. We believe our facilities are presently adequate for our current core product manufacturing operations and OEM development programs and production.

From time to time, we may be involved in litigation relating to claims arising out of the ordinary course of our business including, but not limited to, product liability, employment matters, patents and trademark, and customer accounts collections. We are not a party to, and to our knowledge there are not threatened, any claims or actions against us, the ultimate disposition of which would have a material adverse effect on us.

Not applicable.

17

PART II

|

Item 5. |

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

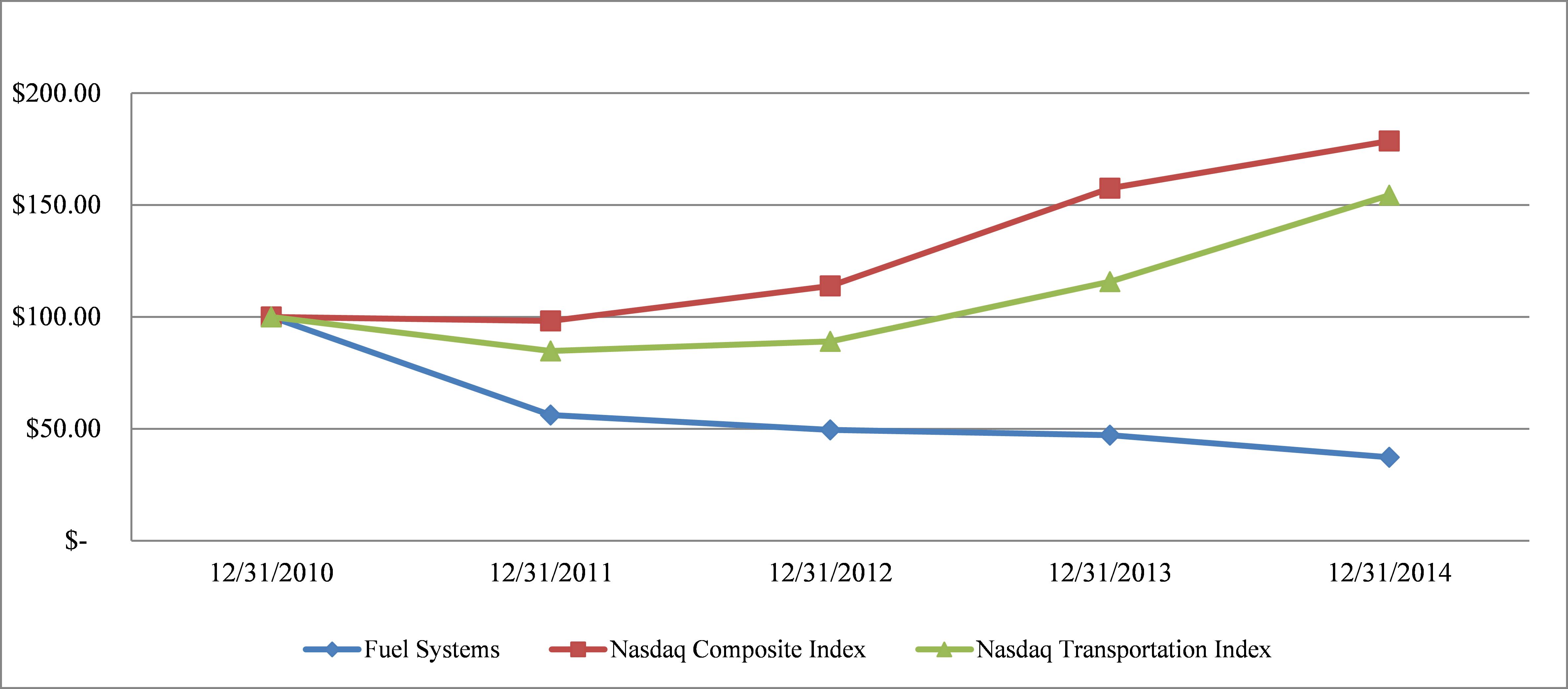

Our common stock is traded on the NASDAQ Stock Market under the symbol “FSYS.” As of February 13, 2015, there were approximately 241 holders of record of our common stock. The high and low per share prices of our common stock as reported on the Nasdaq Stock Market were as follows:

|

|

High |

|

|

Low |

|

||

|

Year Ended December 31, 2014 |

|

|

|

|

|

|

|

|

First Quarter |

$ |

14.02 |

|

|

$ |

10.30 |

|

|

Second Quarter |

$ |

11.41 |

|

|

$ |

9.42 |

|

|

Third Quarter |

$ |

11.28 |

|

|

$ |

8.89 |

|

|

Fourth Quarter |

$ |

11.73 |

|

|

$ |

8.04 |

|

|

Year Ended December 31, 2013 |

|

|

|

|

|