Attached files

| file | filename |

|---|---|

| EX-21 - EX-21 - CENTURY BANCORP INC | d831292dex21.htm |

| EX-31.2 - EX-31.2 - CENTURY BANCORP INC | d831292dex312.htm |

| EX-32.2 - EX-32.2 - CENTURY BANCORP INC | d831292dex322.htm |

| EX-32.1 - EX-32.1 - CENTURY BANCORP INC | d831292dex321.htm |

| EX-31.1 - EX-31.1 - CENTURY BANCORP INC | d831292dex311.htm |

| EXCEL - IDEA: XBRL DOCUMENT - CENTURY BANCORP INC | Financial_Report.xls |

| EX-23.1 - EX-23.1 - CENTURY BANCORP INC | d831292dex231.htm |

Table of Contents

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| (Mark One) | ||

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the fiscal year ended December 31, 2014 | ||

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the transition period from to |

Commission file number 0-15752

CENTURY BANCORP, INC.

(Exact name of registrant as specified in its charter)

| COMMONWEALTH OF MASSACHUSETTS | 04-2498617 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification number) | |

| 400 MYSTIC AVENUE, MEDFORD, MA | 02155 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number including area code:

(781) 391-4000

Securities registered pursuant to Section 12(b) of the Act:

| Class A Common Stock, $1.00 par value | Nasdaq Global Market | |

| (Title of class) | (Name of Exchange) |

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark whether the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulations S-T (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ |

Accelerated filer þ | Non-accelerated filer ¨ | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þ

State the aggregate market value of the registrant’s voting and nonvoting stock held by nonaffiliates, computed using the closing price as reported on Nasdaq as of June 30, 2014 was $126,730,689.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock as of February 28, 2015:

Class A Common Stock, $1.00 par value 3,600,729 Shares

Class B Common Stock, $1.00 par value 1,967,180 Shares

DOCUMENTS INCORPORATED BY REFERENCE

List hereunder the following documents if incorporated by reference and the Part of the Form 10-K (e.g., Part I, Part II, etc.) into which the document is incorporated: (1) Any annual report to security holders; (2) Any proxy or information statement; and (3) Any prospectus filed pursuant to Rule 424(b) or (c) under the Securities Act of 1933. The listed documents should be clearly described for identification purposes (e.g., annual report to security holders for fiscal year ended December 24, 1980).

| (1) | Portions of the Registrant’s Annual Report to Stockholders for the fiscal year ended December 31, 2014 are incorporated into Part II, Items 5-8 of this Form 10-K. |

Table of Contents

CENTURY BANCORP INC.

FORM 10-K

| Page | ||||||

| ITEM 1 | 1-5 | |||||

| ITEM 1A | 5-6 | |||||

| ITEM 1B | 6 | |||||

| ITEM 2 | 6 | |||||

| ITEM 3 | 6 | |||||

| ITEM 4 | 6 | |||||

| ITEM 5 | 7-8 | |||||

| ITEM 6 | 8 | |||||

| ITEM 7 | MANAGEMENT’S DISCUSSION AND ANALYSIS OF RESULTS OF OPERATIONS AND FINANCIAL CONDITION |

8 | ||||

| ITEM 7A | 8 | |||||

| ITEM 8 | 8 | |||||

| ITEM 9 | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

8 | ||||

| ITEM 9A | 8-9 | |||||

| ITEM 9B | 9 | |||||

| ITEM 10 | 91-95 | |||||

| ITEM 11 | 96-105 | |||||

| ITEM 12 | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS |

106-107 | ||||

| ITEM 13 | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

107 | ||||

| ITEM 14 | 108 | |||||

| ITEM 15 | 108-110 | |||||

| SIGNATURES | 111 | |||||

i

Table of Contents

| ITEM 1. BUSINESS |

The Company

Century Bancorp, Inc. (together with its bank subsidiary, unless the context otherwise requires, the “Company”) is a Massachusetts state-chartered bank holding company headquartered in Medford, Massachusetts. The Company is a Massachusetts corporation formed in 1972 and has one banking subsidiary (the “Bank”): Century Bank and Trust Company formed in 1969. At December 31, 2014, the Company had total assets of $3.6 billion. Currently, the Company operates 26 banking offices in 20 cities and towns in Massachusetts, ranging from Braintree in the south to Andover in the north. The Bank’s customers consist primarily of small and medium-sized businesses and retail customers in these communities and surrounding areas, as well as local governments and institutions throughout Massachusetts.

The Company’s results of operations are largely dependent on net interest income, which is the difference between the interest earned on loans and securities and interest paid on deposits and borrowings. The results of operations are also affected by the level of income and fees from loans, deposits, as well as operating expenses, the provision for loan losses, the impact of federal and state income taxes and the relative levels of interest rates and economic activity.

The Company offers a wide range of services to commercial enterprises, state and local governments and agencies, non-profit organizations and individuals. It emphasizes service to small and medium-sized businesses and retail customers in its market area. The Company makes commercial loans, real estate and construction loans and consumer loans, and accepts savings, time, and demand deposits. In addition, the Company offers to its corporate and institutional customers automated lock box collection services, cash management services and account reconciliation services, and actively promotes the marketing of these services to the municipal market. Also, the Company provides full service securities brokerage services through a program called Investment Services at Century Bank, which is supported by LPL Financial, a third party full-service securities brokerage business.

The Company provides financial services, including cash management, lockbox processing and short-term and long-term financing, to municipalities in Massachusetts, New Hampshire and Rhode Island. The Company has client engagements with approximately 235 government entities throughout the region.

Availability of Company Filings

Under the Securities Exchange Act of 1934, Sections 13 and 15(d), periodic and current reports must be filed with the Securities and Exchange Commission (the “SEC”). The public may read and copy any materials filed with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0030. The Company electronically files with the SEC its periodic and current reports, as well as other filings it makes with the SEC from time to time. The SEC maintains an Internet site that contains reports and other information regarding issuers, including the Company, that file electronically with the SEC, at www.sec.gov, in which all forms filed electronically may be accessed. Additionally, our annual report on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K and additional shareholder information are available free of charge on the Company’s website: www.centurybank.com.

Employees

As of December 31, 2014, the Company had 361 full-time and 79 part-time employees. The Company’s employees are not represented by any collective bargaining unit. The Company believes that its employee relations are good.

Financial Services Modernization

On November 12, 1999, President Clinton signed into law The Gramm-Leach-Bliley Act (“Gramm-Leach”) which significantly altered banking laws in the United States. Gramm-Leach enables combinations among banks,

1

Table of Contents

securities firms and insurance companies beginning March 11, 2000. As a result of Gramm Leach, many of the depression-era laws that restricted these affiliations and other activities that may be engaged in by banks and bank holding companies were repealed. Under Gramm-Leach, bank holding companies are permitted to offer their customers virtually any type of financial service that is financial in nature or incidental thereto, including banking, securities underwriting, insurance (both underwriting and agency) and merchant banking.

In order to engage in these financial activities, a bank holding company must qualify and register with the Federal Reserve Board as a “financial holding company” by demonstrating that each of its bank subsidiaries is “well capitalized,” “well managed,” and has at least a “satisfactory” rating under the Community Reinvestment Act of 1977 (the “CRA”). The Company has not elected to become a financial holding company under Gramm-Leach.

These financial activities authorized by Gramm-Leach may also be engaged in by a “financial subsidiary” of a national or state bank, except for insurance or annuity underwriting, insurance company portfolio investments, real estate investment and development and merchant banking, which must be conducted in a financial holding company. In order for the new financial activities to be engaged in by a financial subsidiary of a national or state bank, Gramm-Leach requires each of the parent bank (and any bank affiliates) to be “well capitalized” and “well managed;” the aggregate consolidated assets of all of that bank’s financial subsidiaries may not exceed the lesser of 45% of its consolidated total assets or $50 billion; the bank must have at least a satisfactory CRA rating; and, if the bank is one of the 100 largest banks, it must meet certain financial rating or other comparable requirements. The Company does not currently conduct activities through a financial subsidiary.

Gramm-Leach establishes a system of functional regulation, under which the federal banking agencies will regulate the banking activities of financial holding companies and banks’ financial subsidiaries, the SEC will regulate their securities activities, and state insurance regulators will regulate their insurance activities. Gramm-Leach also provides new protections against the transfer and use by financial institutions of consumers’ nonpublic, personal information.

Holding Company Regulation

The Company is a bank holding company as defined by the Bank Holding Company Act of 1956, as amended (the “Holding Company Act”), and is registered as such with the Board of Governors of the Federal Reserve Bank (the “FRB”), which is responsible for administration of the Holding Company Act. Although the Company may meet the qualifications for electing to become a financial holding company under Gramm-Leach, the Company has elected to retain its pre-Gramm-Leach status for the present time under the Holding Company Act. As required by the Holding Company Act, the Company files with the FRB an annual report regarding its financial condition and operations, management and intercompany relationships of the Company and the Bank. It is also subject to examination by the FRB and must obtain FRB approval before (i) acquiring direct or indirect ownership or control of more than 5% of the voting stock of any bank, unless it already owns or controls a majority of the voting stock of that bank, (ii) acquiring all or substantially all of the assets of a bank, except through a subsidiary which is a bank, or (iii) merging or consolidating with any other bank holding company. A bank holding company must also give the FRB prior written notice before purchasing or redeeming its equity securities, if the gross consideration for the purchase or redemption, when aggregated with the net consideration paid by the company for all such purchases or redemptions during the preceding 12 months, is equal to 10% or more of the company’s consolidated net worth.

The Holding Company Act prohibits a bank holding company, with certain exceptions, from (i) acquiring direct or indirect ownership or control of more than 5% of any class of voting shares of any company which is not a bank or a bank holding company, or (ii) engaging in any activity other than managing or controlling banks, or furnishing services to or performing services for its subsidiaries. A bank holding company may own, however, shares of a company engaged in activities which the FRB has determined are so closely related to banking or managing or controlling banks as to be a proper incident thereto.

The Company and its subsidiaries are examined by federal and state regulators. The FRB has regulatory authority over holding company activities and performed a review of the Company and its subsidiaries as of June 2014.

2

Table of Contents

USA PATRIOT Act

Under Title III of the USA PATRIOT Act, also known as the “International Money Laundering Abatement and Anti-Terrorism Act of 2001”, all financial institutions are required in general to identify their customers, adopt formal and comprehensive anti-money laundering programs, scrutinize or prohibit altogether certain transactions of special concern, and be prepared to respond to inquiries from U.S. law enforcement agencies concerning their customers and their transactions. Additional information-sharing among financial institutions, regulators, and law enforcement authorities is encouraged by the presence of an exemption from the privacy provisions of the Gramm-Leach Act for financial institutions that comply with this provision and the authorization of the Secretary of the Treasury to adopt rules to further encourage cooperation and information-sharing. The effectiveness of a financial institution in combating money laundering activities is a factor to be considered in any application submitted by the financial institution under the Holding Company Act or Bank Merger Act.

Sarbanes-Oxley Act

The Sarbanes-Oxley Act, signed into law July 30, 2002, addresses, among other issues, corporate governance, auditor independence and accounting standards, executive compensation, insider loans, whistleblower protection and enhanced and timely disclosure of corporate information. The SEC has adopted a substantial number of implementing rules and the Financial Industry Regulatory Authority (FINRA) has adopted corporate governance rules that have been approved by the SEC and are applicable to the Company. The changes are intended to allow stockholders to monitor more effectively the performance of companies and management. As directed by Section 302(a) of the Sarbanes-Oxley Act, the Company’s Chief Executive Officer and Chief Financial Officer are each required to certify that the Company’s quarterly and annual reports do not contain any untrue statement of a material fact. This requirement has several parts, including certification that these officers are responsible for establishing, maintaining and regularly evaluating the effectiveness of the Company’s disclosure controls and procedures and internal controls over financial reporting; that they have made certain disclosures to the Company’s auditors and the Board of Directors about the Company’s disclosure controls and procedures and internal control over financial reporting, and that they have included information in the Company’s quarterly and annual reports about their evaluation of the Company’s disclosure controls and procedures and internal control over financial reporting, and whether there have been significant changes in the Company’s internal disclosure controls and procedures or in other factors that could significantly affect such controls and procedures subsequent to the evaluation and whether there have been any significant changes in the Company’s internal control over financial reporting that have materially affected or reasonably likely to materially affect the Company’s internal control over financial reporting, and compliance with certain other disclosure objectives. Section 906 of the Sarbanes-Oxley Act requires an additional certification that each periodic report containing financial statements fully complies with the requirements of Section 13(a) and 15(d) of the Securities Exchange Act of 1934 and that the information in the report fairly presents, in all material respects, the financial conditions and results of operations of the Company.

Dodd-Frank Wall Street Reform and Consumer Protection Act

On July 21, 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act became law. The Act was intended to address many issues arising in the recent financial crisis and is exceedingly broad in scope affecting many aspects of bank and financial market regulation. The Act requires, or permits by implementing regulation, enhanced prudential standards for banks and bank holding companies inclusive of capital, leverage, liquidity, concentration and exposure measures. In addition, traditional bank regulatory principles such as restrictions on transactions with affiliates and insiders were enhanced. The Act also contains reforms of consumer mortgage lending practices and creates a Bureau of Consumer Financial Protection which is granted broad authority over consumer financial practices of banks and others. It is expected as the specific new or incremental requirements applicable to the company become effective that the costs and difficulties of remaining compliant with all such requirements will increase. The Act broadens the base for FDIC assessments to average consolidated assets less tangible equity of financial institutions and also permanently raises the current standard maximum FDIC deposit insurance amount to $250,000. The Act extended unlimited deposit insurance on non-interest bearing transaction accounts through December 31, 2012. In addition, the Act added a new Section 13 to

3

Table of Contents

the Holding Company Act, the so-called “Volcker Rule,” (the “Rule”) which generally restricts certain banking entities such as the Company and its subsidiaries or affiliates, from engaging in proprietary trading activities and owning equity in or sponsoring any private equity or hedge fund. The Rule became effective July 21, 2012. The final implementing regulations for the Rule were issued by various regulatory agencies in December, 2013, and under an extended conformance regulation, compliance must be achieved by July 21, 2015 and with the covered funds restrictions by July 21, 2017. Under the Rule, the Company may be restricted from engaging in proprietary trading, investing in third party hedge or private equity funds or sponsoring new funds unless it qualifies for an exemption from the rule. The Company has little involvement in prohibited proprietary trading or investment activities in covered funds and the Company does not expect that complying with the requirements of the Rule will have any material effect on the Company’s financial condition or results of operation.

Deposit Insurance Premiums

The Bank’s deposits have the benefit of FDIC insurance up to applicable limits. The FDIC’s Deposit Insurance Fund is funded by assessments on insured depository institutions, which depend on the risk category of an institution and the amount of assets that it holds. The FDIC may increase or decrease the assessment rate schedule on a semi-annual basis.

On September 29, 2009, the FDIC adopted a Notice of Proposed Rulemaking (NPR) that would require insured institutions to prepay their estimated quarterly risk-based assessments for the fourth quarter of 2009 and for all of 2010, 2011 and 2012. The FDIC Board voted to adopt a uniform three-basis point increase in assessment rates effective on January 1, 2011, and extend the restoration period from seven to eight years. This rule was finalized on November 2, 2009. The Company’s quarterly risk-based deposit insurance assessments were paid from this amount until June 30, 2013. The Company received a refund of $2.4 million of prepaid FDIC assessments in June 2013.

In February 2011, the FDIC approved a rule to change the assessment base from adjusted domestic deposits to average consolidated total assets minus average tangible equity. The rule has kept the overall amount collected from the industry very close to the amount collected prior to the new calculation.

Risk-Based Capital Guidelines

Federal banking regulators have issued risk-based capital guidelines, which assign risk factors to asset categories and off-balance-sheet items. Also, the Basel Committee has issued capital standards entitled “Basel III: A global regulatory framework for more resilient banks and banking systems” (“Basel III”). The Federal Reserve Board has finalized its rule implementing the Basel III regulatory capital framework. The rule, that came into effect in January 2015, sets the Basel III minimum regulatory capital requirements for all organizations. It includes a new common equity Tier I ratio of 4.5 percent of risk-weighted assets, raises the minimum Tier I capital ratio from 4 percent to 6 percent of risk-weighted assets and would set a new conservation buffer of 2.5 percent of risk-weighted assets. The Company has analyzed the final rules; the implementation of the framework will not have a material impact on the Company’s financial condition or results of operations.

Competition

The Company experiences substantial competition in attracting deposits and making loans from commercial banks, thrift institutions and other enterprises such as insurance companies and mutual funds. These competitors include several major commercial banks whose greater resources may afford them a competitive advantage by enabling them to maintain numerous branch offices and mount extensive advertising campaigns. A number of these competitors are not subject to the regulatory oversight that the Company is subject to, which increases these competitors’ flexibility.

Forward-Looking Statements

Certain statements contained herein are not based on historical facts and are “forward-looking statements” within the meaning of Section 21A of the Securities Exchange Act of 1934. Forward-looking statements, which are based on various assumptions (some of which are beyond the Company’s control), may be identified by reference to a future period or periods, or by the use of forward-looking terminology, such as “may,” “will,”

4

Table of Contents

“believe,” “expect,” “estimate,” “anticipate,” “continue” or similar terms or variations on those terms, or the negative of these terms. Actual results could differ materially from those set forth in forward-looking statements due to a variety of factors, including, but not limited to, those related to the economic environment, particularly in the market areas in which the Company operates, competitive products and pricing, fiscal and monetary policies of the U.S. Government, changes in government regulations affecting financial institutions, including regulatory fees and capital requirements, changes in prevailing interest rates, acquisitions and the integration of acquired businesses, credit risk management, asset/liability management, the financial and securities markets, and the availability of and costs associated with sources of liquidity.

The Company does not undertake, and specifically disclaims any obligation, to publicly release the result of any revisions which may be made to any forward-looking statements to reflect the occurrence of anticipated or unanticipated events or circumstances after the date of such statements.

| ITEM 1A. | RISK FACTORS |

The risk factors that may affect the Company’s performance and results of operations include the following:

(i) the Company’s business is dependent upon general economic conditions in Massachusetts, New Hampshire and Rhode Island. The national and local economies may adversely affect the Company’s performance and results of operations;

(ii) the Company’s earnings depend, to a great extent, upon the level of net interest income generated by the Company, and therefore the Company’s results of operations may be adversely affected by increases or decreases in interest rates or by the shape of the yield curve;

(iii) the banking business is highly competitive and the profitability of the Company depends upon the Company’s ability to attract loans and deposits in Massachusetts, New Hampshire, and Rhode Island, where the Company competes with a variety of traditional banking companies, some of which have vastly greater resources, and nontraditional institutions such as credit unions and finance companies;

(iv) at December 31, 2014, approximately 63.5% of the Company’s loan portfolio was comprised of commercial and commercial real estate loans, exposing the Company to the risks inherent in financings based upon analyses of credit risk, the value of underlying collateral, including real estate, and other more intangible factors, which are considered in making commercial loans;

(v) at December 31, 2014, approximately 30.7% of the Company’s loan portfolio was comprised of residential real estate and home equity loans, exposing the Company to the risks inherent in financings based upon analyses of credit risk and the value of underlying collateral. Accordingly, the Company’s profitability may be negatively impacted by errors in risk analyses, by loan defaults and the ability of certain borrowers to repay such loans may be adversely affected by any downturn in general economic conditions;

(vi) economic conditions and interest rate risk could adversely impact the fair value and the ultimate collectibility of the Company’s investments. Should an investment be deemed “other than temporarily impaired”, the Company would be required to writedown the carrying value of the investment through earnings. Such writedown(s) may have a material adverse effect on the Company’s financial condition and results of operations;

(vii) writedown of goodwill and other identifiable intangible assets would negatively impact our financial condition and results of operations. At December 31, 2014, our goodwill and other identifiable intangible assets were approximately $2.7 million;

(viii) acts or threats of terrorism and actions taken by the United States or other governments as a result of such acts or threats, including possible military action, could further adversely affect business and economic conditions in the United States of America generally and in the Company’s markets, which could adversely affect the Company’s financial performance and that of the Company’s borrowers and on the financial markets and the price of the Company’s Class A common stock;

(ix) changes in the extensive laws, regulations and policies governing bank holding companies and their subsidiaries could alter the Company’s business environment or affect the Company’s operations;

5

Table of Contents

(x) the potential need to adapt to industry changes in information technology systems, on which the Company is highly dependent to secure bank and customer financial information, could present operational issues, require significant capital spending or impact the Company’s reputation; and

These factors, as well as general economic and market conditions in the United States of America, may materially and adversely affect the Company’s performance, results of operations and the market price of shares of the Company’s Class A common stock.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

No written comments received by the Company from the SEC regarding the Company’s periodic or current reports remain unresolved.

| ITEM 2. | PROPERTIES |

The Company owns its main banking office, headquarters, and operations center in Medford, Massachusetts, which were expanded in 2004, and 11 of the 25 other facilities in which its branch offices are located. The remaining offices are occupied under leases expiring on various dates from 2015 to 2026. The Company believes that its banking offices are in good condition.

During July 2012, the Company received state regulatory approval to close a branch at Chestnut Hill in Newton, Massachusetts. The branch closed on September 21, 2012 and the accounts were temporarily moved to the Brookline, Massachusetts branch. During July 2012, the Company entered into a lease agreement and received regulatory approval to open a branch at a new location at Chestnut Hill in Newton, Massachusetts. The branch opened on November 7, 2013 and the majority of the accounts that were temporarily moved to the Brookline, Massachusetts branch were moved to the new branch at Chestnut Hill in Newton, Massachusetts.

During December 2013, the Company entered into a lease agreement to open a branch located in Woburn, Massachusetts. The branch opened on November 3, 2014.

During March 2014, the Company entered into a lease agreement to open a branch located on Boylston Street in Boston, Massachusetts. This property is leased from an entity affiliated with Marshall M. Sloane, Chairman of the Board of the Company. This agreement was approved by the Board of Directors in the absence of the Chairman of the Board. The branch is scheduled to open during the first quarter of 2015. The deposits from the Kenmore Square, Boston Massachusetts branch, which closed on September 30, 2014, will be moved to the new Boylston Street branch.

| ITEM 3. | LEGAL PROCEEDINGS |

The Company and its subsidiaries are parties to various claims and lawsuits arising in the course of their normal business activities. Although the ultimate outcome of these suits cannot be ascertained at this time, it is the opinion of management that none of these matters, even if it resolved adversely to the Company, will have a material adverse effect on the Company’s consolidated financial position.

| ITEM 4. | MINE SAFETY DISCLOSURES |

Not applicable.

6

Table of Contents

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

(a) The Class A Common Stock of the Company is traded on the NASDAQ National Global Market under the symbol “CNBKA.” The price range of the Company’s Class A common stock since January 1, 2013 is shown on page 12. The Company’s Class B Common Stock is not traded on any national securities exchange or other public trading market.

The shares of Class A Common Stock are generally not entitled to vote on any matter, including in the election of Company Directors, but, in limited circumstances, may be entitled to vote as a class on certain extraordinary transactions, including any merger or consolidation (other than one in which the Company is the surviving corporation or one which by law may be approved by the directors without any stockholder vote) or the sale, lease, or exchange of all or substantially all of the property and assets of the Company. Since the vote of a majority of the shares of the Company’s Class B Common Stock, voting as a separate class, is required to approve certain extraordinary corporate transactions, the holders of Class B Common Stock have the power to prevent any takeover of the Company not approved by them.

(b) Approximate number of equity security holders as of December 31, 2014:

| Title of Class |

Approximate Number of Record Holders |

|||

| Class A Common Stock |

1,067 | |||

| Class B Common Stock |

39 | |||

(c) Under the Company’s Articles of Organization, the holders of Class A Common Stock are entitled to receive dividends per share equal to at least 200% of dividends paid, if any, from time to time, on each share of Class B Common Stock.

The following table shows the dividends paid by the Company on the Class A and Class B Common Stock for the periods indicated.

| Dividends per Share |

||||||||

| Class A | Class B | |||||||

| 2013 |

||||||||

| First quarter |

$ | .12 | $ | .06 | ||||

| Second quarter |

.12 | .06 | ||||||

| Third quarter |

.12 | .06 | ||||||

| Fourth quarter |

.12 | .06 | ||||||

| 2014 |

||||||||

| First quarter |

$ | .12 | $ | .06 | ||||

| Second quarter |

.12 | .06 | ||||||

| Third quarter |

.12 | .06 | ||||||

| Fourth quarter |

.12 | .06 | ||||||

The Company’s ability to pay dividends on its shares depends generally on dividends it receives from the Bank. Both Massachusetts and federal law limit the payment of dividends by the Bank to the Company. Under FDIC regulations and applicable Massachusetts law, the dollar amount of dividends and any other capital distributions that the Bank may make depends upon its capital position and recent net income. Generally, so long as the Bank remains adequately capitalized, it may potentially make capital distributions during any calendar year equal to up to 100% of net income for the year to date plus retained net income for the two preceding years. However, if the Bank’s capital becomes impaired or the FDIC or Commissioner otherwise determines that the Bank should conserve capital, the Bank may be prohibited or otherwise limited from paying any dividends or making any other capital distributions.

7

Table of Contents

The Federal Reserve Board also has authority to prohibit dividends by bank holding companies such as the Company, if their actions constitute unsafe or unsound practices. Prior to the recent financial crisis, the Federal Reserve Board issued a policy statement and supervisory guidance on the payment of cash dividends by bank holding companies, which expresses the Federal Reserve Board’s view that a bank holding company should pay cash dividends only to the extent that, (1) the company’s net income for the past year is sufficient to cover the cash dividends, (2) the rate of earnings retention is consistent with the company’s capital needs, asset quality, and overall financial condition, and (3) the minimum regulatory capital adequacy ratios are met. It is also the Federal Reserve Board’s policy that bank holding companies should not maintain dividend levels that undermine their ability to serve as a source of strength to their banking subsidiaries. It is expected that the Federal Reserve Board will be more rather than less restrictive for the foreseeable future about dividend practices.

(d) The following schedule provides information with respect to the Company’s equity compensation plans under which shares of Class A Common Stock are authorized for issuance as of December 31, 2014:

| Equity Compensation Plan Information | ||||||||||||

| Plan Category |

Number of Shares to be Issued Upon Exercise of Outstanding Options (a) |

Weighted-Average Exercise Price of Outstanding Options (b) |

Number of Shares Remaining Available for Future Issuance Under Equity Compensation Plans (Excluding Shares Reflected in Column (a)) (c) |

|||||||||

| Equity compensation plans approved by security holders |

— | $ | — | 233,934 | ||||||||

| Equity compensation plans not approved by security holders |

— | — | — | |||||||||

|

|

|

|

|

|

|

|||||||

| Total |

— | $ | — | 233,934 | ||||||||

(e) The performance graph information required herein is shown on page 12.

| ITEM 6. | SELECTED FINANCIAL DATA |

The information required herein is shown on pages 11 and 12.

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF RESULTS OF OPERATIONS AND FINANCIAL CONDITION |

The information required herein is shown on pages 13 through 36.

| ITEM 7A. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

The information required herein is shown on pages 32 and 33.

| ITEM 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA |

The information required herein is shown on pages 37 through 87.

| ITEM 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

None.

| ITEM 9A. | CONTROLS AND PROCEDURES |

The Company’s principal executive officer and principal financial officer have evaluated the Company’s disclosure controls and procedures as of December 31, 2014. Based on this evaluation, the principal executive officer and principal financial officer have concluded that the Company’s disclosure controls and procedures are effective. The Company’s disclosure controls and procedures also effectively ensure that information required to be disclosed in the Company’s filings and submissions with the Securities and Exchange Commission under the Securities Exchange Act of 1934 is accumulated and reported to Company management (including the principal

8

Table of Contents

executive officer and principal financial officer) and is recorded, processed, summarized and reported within the time periods specified by the Securities and Exchange Commission. In addition, the Company has reviewed its internal control over financial reporting and there have been no changes that occurred during the fourth fiscal quarter that have materially affected, or are reasonably likely to materially affect its internal control over financial reporting or in other factors that could significantly affect its internal control over financial reporting.

On May 14, 2013, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) released an updated version of its Internal Control — Integrated Framework (2013) (2013 Framework). The 2013 Framework’s internal control components (i.e., control environment, risk assessment, control activities, information and communication, and monitoring activities) remain predominantly the same as those in the 1992 Framework. However, the 2013 Framework was expanded to include 17 principles which must be present and functioning in order to have an effective system of internal controls. The Company implemented the 2013 Framework effective December 31, 2014.

Management’s report on internal control over financial reporting is shown on page 90. The audit report of the registered public accounting firm is shown on page 89.

| ITEM 9B. | OTHER INFORMATION |

None.

9

Table of Contents

10

Table of Contents

| 2014 | 2013 | 2012 | 2011 | 2010 | ||||||||||||||||

| (dollars in thousands, except share data) | ||||||||||||||||||||

| FOR THE YEAR |

||||||||||||||||||||

| Interest income |

$ | 85,371 | $ | 79,765 | $ | 81,494 | $ | 78,065 | $ | 76,583 | ||||||||||

| Interest expense |

19,136 | 18,805 | 19,540 | 22,766 | 24,817 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income |

66,235 | 60,960 | 61,954 | 55,299 | 51,766 | |||||||||||||||

| Provision for loan losses |

2,050 | 2,710 | 4,150 | 4,550 | 5,575 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income after provision for loan losses |

64,185 | 58,250 | 57,804 | 50,749 | 46,191 | |||||||||||||||

| Other operating income |

15,271 | 18,615 | 15,865 | 16,240 | 15,999 | |||||||||||||||

| Operating expenses |

56,730 | 55,812 | 53,238 | 48,742 | 47,372 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income before income taxes |

22,726 | 21,053 | 20,431 | 18,247 | 14,818 | |||||||||||||||

| Provision for income taxes |

866 | 1,007 | 1,392 | 1,554 | 1,244 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

$ | 21,860 | $ | 20,046 | $ | 19,039 | $ | 16,693 | $ | 13,574 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Average shares outstanding Class A, basic |

3,591,732 | 3,575,683 | 3,557,693 | 3,543,233 | 3,521,179 | |||||||||||||||

| Average shares outstanding Class B, basic |

1,969,030 | 1,980,855 | 1,990,474 | 1,997,411 | 2,012,327 | |||||||||||||||

| Average shares outstanding Class A, diluted |

5,562,209 | 5,557,693 | 5,549,191 | 5,541,794 | 5,535,742 | |||||||||||||||

| Average shares outstanding Class B, diluted |

1,969,030 | 1,980,855 | 1,990,474 | 1,997,411 | 2,012,327 | |||||||||||||||

| Total shares outstanding at year-end |

5,567,909 | 5,556,584 | 5,554,959 | 5,542,697 | 5,540,247 | |||||||||||||||

| Earnings per share: |

||||||||||||||||||||

| Basic, Class A |

$ | 4.78 | $ | 4.39 | $ | 4.18 | $ | 3.68 | $ | 3.00 | ||||||||||

| Basic, Class B |

$ | 2.39 | $ | 2.19 | $ | 2.09 | $ | 1.84 | $ | 1.50 | ||||||||||

| Diluted, Class A |

$ | 3.93 | $ | 3.61 | $ | 3.43 | $ | 3.01 | $ | 2.45 | ||||||||||

| Diluted, Class B |

$ | 2.39 | $ | 2.19 | $ | 2.09 | $ | 1.84 | $ | 1.50 | ||||||||||

| Dividend payout ratio |

10.1 | % | 10.9 | % | 11.5 | % | 13.1 | % | 16.0 | % | ||||||||||

| AT YEAR-END |

||||||||||||||||||||

| Assets |

$ | 3,624,036 | $ | 3,431,154 | $ | 3,086,209 | $ | 2,743,225 | $ | 2,441,684 | ||||||||||

| Loans |

1,331,366 | 1,264,763 | 1,111,788 | 984,492 | 906,164 | |||||||||||||||

| Deposits |

2,737,591 | 2,715,839 | 2,445,073 | 2,124,584 | 1,902,023 | |||||||||||||||

| Stockholders’ equity |

192,500 | 176,472 | 179,990 | 160,649 | 145,025 | |||||||||||||||

| Book value per share |

$ | 34.57 | $ | 31.76 | $ | 32.40 | $ | 28.98 | $ | 26.18 | ||||||||||

| SELECTED FINANCIAL PERCENTAGES |

||||||||||||||||||||

| Return on average assets |

0.61 | % | 0.60 | % | 0.65 | % | 0.63 | % | 0.56 | % | ||||||||||

| Return on average stockholders’ equity |

11.57 | % | 11.58 | % | 11.06 | % | 10.72 | % | 9.52 | % | ||||||||||

| Net interest margin, taxable equivalent |

2.22 | % | 2.21 | % | 2.51 | % | 2.48 | % | 2.52 | % | ||||||||||

| Net charge-offs as a percent of average loans |

0.05 | % | 0.08 | % | 0.15 | % | 0.21 | % | 0.44 | % | ||||||||||

| Average stockholders’ equity to average assets |

5.27 | % | 5.22 | % | 5.85 | % | 5.88 | % | 5.93 | % | ||||||||||

| Efficiency ratio |

62.0 | % | 63.0 | % | 62.1 | % | 62.2 | % | 65.0 | % | ||||||||||

11

Table of Contents

Financial Highlights — (Continued)

| Per Share Data 2014, Quarter Ended |

December 31, | September 30, | June 30, | March 31, | ||||||||||||

| Market price range (Class A) |

||||||||||||||||

| High |

$ | 40.50 | $ | 38.88 | $ | 37.68 | $ | 37.00 | ||||||||

| Low |

34.26 | 34.10 | 33.05 | 32.95 | ||||||||||||

| Dividends Class A |

0.12 | 0.12 | 0.12 | 0.12 | ||||||||||||

| Dividends Class B |

0.06 | 0.06 | 0.06 | 0.06 | ||||||||||||

| 2013, Quarter Ended |

December 31, | September 30, | June 30, | March 31, | ||||||||||||

| Market price range (Class A) |

||||||||||||||||

| High |

$ | 35.98 | $ | 37.80 | $ | 35.75 | $ | 35.40 | ||||||||

| Low |

29.67 | 31.22 | 31.11 | 30.41 | ||||||||||||

| Dividends Class A |

0.12 | 0.12 | 0.12 | 0.12 | ||||||||||||

| Dividends Class B |

0.06 | 0.06 | 0.06 | 0.06 | ||||||||||||

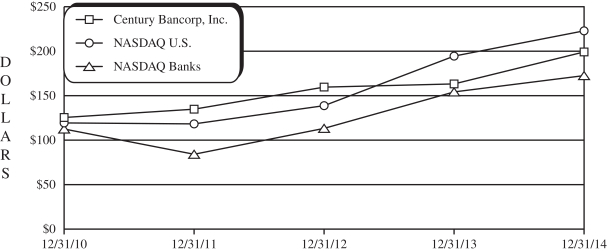

The stock performance graph below compares the cumulative total shareholder return of the Company’s Class A Common Stock from December 31, 2009 to December 31, 2014 with the cumulative total return of the NASDAQ Market Index (U.S. Companies) and the NASDAQ Bank Stock Index. The lines in the graph represent monthly index levels derived from compounded daily returns that include all dividends. If the monthly interval, based on the fiscal year-end, was not a trading day, the preceding trading day was used.

Comparison of Five-Year

Cumulative Total Return*

| Value of $100 Invested on December 31, 2009 at: | 2010 | 2011 | 2012 | 2013 | 2014 | |||||||||||||||

| Century Bancorp, Inc. |

$ | 124.20 | $ | 133.36 | $ | 158.08 | $ | 161.79 | $ | 197.55 | ||||||||||

| NASDAQ Banks |

111.35 | 83.04 | 111.88 | 152.85 | 170.93 | |||||||||||||||

| NASDAQ U.S. |

118.02 | 117.04 | 137.47 | 192.62 | 221.02 | |||||||||||||||

| * | Assumes that the value of the investment in the Company’s Common Stock and each index was $100 on December 31, 2009 and that all dividends were reinvested. |

12

Table of Contents

Management’s Discussion and Analysis of Results of Operations and Financial Condition

FORWARD-LOOKING STATEMENTS

Certain statements contained herein are not based on historical facts and are “forward-looking statements” within the meaning of Section 21A of the Securities Exchange Act of 1934. Forward-looking statements, which are based on various assumptions (some of which are beyond the Company’s control), may be identified by reference to a future period or periods, or by the use of forward-looking terminology, such as “may,” “will,” “believe,” “expect,” “estimate,” “anticipate,” “continue” or similar terms or variations on those terms, or the negative of these terms. Actual results could differ materially from those set forth in forward-looking statements due to a variety of factors, including, but not limited to, those related to the economic environment, particularly in the market areas in which the Company operates, competitive products and pricing, fiscal and monetary policies of the U.S. Government, changes in government regulations affecting financial institutions, including regulatory fees and capital requirements, changes in prevailing interest rates, acquisitions and the integration of acquired businesses, credit risk management, asset/liability management, the financial and securities markets, and the availability of and costs associated with sources of liquidity.

The Company does not undertake, and specifically disclaims any obligation, to publicly release the result of any revisions which may be made to any forward-looking statements to reflect the occurrence of anticipated or unanticipated events or circumstances after the date of such statements.

RECENT MARKET DEVELOPMENTS

The financial services industry continues to face challenges in the aftermath of the recent national and global economic crisis. Since June 2009, the U.S. economy has been recovering from the most severe recession and financial crisis since the Great Depression. There have been some improvements in private sector employment, industrial production and U.S. exports; nevertheless, the pace of economic recovery has been slow. Financial markets have improved since the depths of the crisis but are still unsettled and volatile. There is continued concern about the U.S. economic outlook.

On July 21, 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Act”) became law. The Act was intended to address many issues arising in the recent financial crisis and is exceedingly broad in scope, affecting many aspects of bank and financial market regulation. The Act requires, or permits by implementing regulation, enhanced prudential standards for banks and bank holding companies inclusive of capital, leverage, liquidity, concentration and exposure measures. In addition, traditional bank regulatory principles such as restrictions on transactions with affiliates and insiders were enhanced. The Act also contains reforms of consumer mortgage lending practices and creates a Bureau of Consumer Financial Protection, which is granted broad authority over consumer financial practices of banks and others. It is expected that as the specific new or incremental requirements applicable to the Company become effective, the costs and difficulties of remaining compliant with all such requirements will increase. The Act broadens the base for FDIC assessments to average consolidated assets less tangible equity of financial institutions and also permanently raises the current standard maximum FDIC deposit insurance amount to $250,000. The Act extended unlimited deposit insurance on non-interest bearing transaction accounts through December 31, 2012. In addition, the Act added a new Section 13 to the Bank Holding Company Act, the so-called “Volcker Rule,” (the “Rule”) which generally restricts certain banking entities such as the Company and its subsidiaries or affiliates, from engaging in proprietary trading activities and owning equity in or sponsoring any private equity or hedge fund. The Rule became effective July 21, 2012. The final implementing regulations for the Rule were issued by various regulatory agencies in December, 2013 and under an extended conformance regulation compliance, must be achieved by July 21, 2015 and with the covered funds restrictions by July 21, 2017. Under the Rule, the Company may be restricted from engaging in proprietary trading, investing in third party hedge or private equity funds or sponsoring new funds unless it qualifies for an exemption from the rule. The Company has little involvement in prohibited proprietary trading or investment activities in covered funds and the Company does not expect that complying with the requirements of the Rule will have any material effect on the Company’s financial condition or results of operation.

13

Table of Contents

Management’s Discussion and Analysis of Results of Operations and Financial Condition — (Continued)

On September 29, 2009, the FDIC adopted a Notice of Proposed Rulemaking (NPR) that would require insured institutions to prepay their estimated quarterly risk-based assessments for the fourth quarter of 2009 and for all of 2010, 2011 and 2012. The FDIC Board voted to adopt a uniform three-basis point increase in assessment rates effective on January 1, 2011, and extend the restoration period from seven to eight years. This rule was finalized on November 2, 2009. The Company’s quarterly risk-based deposit insurance assessments were paid from this amount until June 30, 2013. The Company received a refund of $2.4 million of prepaid FDIC assessments in June 2013.

Federal banking regulators have issued risk-based capital guidelines, which assign risk factors to asset categories and off-balance-sheet items. Also, the Basel Committee has issued capital standards entitled “Basel III: A global regulatory framework for more resilient banks and banking systems” (“Basel III”). The Federal Reserve Board has finalized its rule implementing the Basel III regulatory capital framework. The rule, that came into effect in January 2015, sets the Basel III minimum regulatory capital requirements for all organizations. It includes a new common equity Tier I ratio of 4.5 percent of risk-weighted assets, raises the minimum Tier I capital ratio from 4 percent to 6 percent of risk-weighted assets and would set a new conservation buffer of 2.5 percent of risk-weighted assets. The Company has analyzed the final rules; the implementation of the framework will not have a material impact on the Company’s financial condition or results of operations.

OVERVIEW

Century Bancorp, Inc. (together with its bank subsidiary, unless the context otherwise requires, the “Company”) is a Massachusetts state-chartered bank holding company headquartered in Medford, Massachusetts. The Company is a Massachusetts corporation formed in 1972 and has one banking subsidiary (the “Bank”): Century Bank and Trust Company formed in 1969. At December 31, 2014, the Company had total assets of $3.6 billion. Currently, the Company operates 26 banking offices in 20 cities and towns in Massachusetts, ranging from Braintree in the south to Andover in the north. The Bank’s customers consist primarily of small and medium-sized businesses and retail customers in these communities and surrounding areas, as well as local governments and institutions throughout Massachusetts.

The Company’s results of operations are largely dependent on net interest income, which is the difference between the interest earned on loans and securities and interest paid on deposits and borrowings. The results of operations are also affected by the level of income and fees from loans, deposits, as well as operating expenses, the provision for loan losses, the impact of federal and state income taxes and the relative levels of interest rates and economic activity.

The Company offers a wide range of services to commercial enterprises, state and local governments and agencies, non-profit organizations and individuals. It emphasizes service to small and medium sized businesses and retail customers in its market area. The Company makes commercial loans, real estate and construction loans and consumer loans, and accepts savings, time, and demand deposits. In addition, the Company offers to its corporate and institutional customers automated lock box collection services, cash management services and account reconciliation services, and actively promotes the marketing of these services to the municipal market. Also, the Company provides full service securities brokerage services through a program called Investment Services at Century Bank, which is supported by LPL Financial, a third party full-service securities brokerage business.

The Company has client engagements in Massachusetts, New Hampshire and Rhode Island with approximately 235 government entities throughout the region.

The Company had net income of $21,860,000 for the year ended December 31, 2014, compared with net income of $20,046,000 for the year ended December 31, 2013, and net income of $19,039,000 for the year ended December 31, 2012. Class A diluted earnings per share were $3.93 in 2014, compared to $3.61 in 2013 and $3.43 in 2012.

14

Table of Contents

Management’s Discussion and Analysis of Results of Operations and Financial Condition — (Continued)

Earnings per share (EPS) for each class of stock and for each year ended December 31, is as follows:

| 2014 | 2013 | 2012 | ||||||||||

| Basic EPS – Class A common |

$ | 4.78 | $ | 4.39 | $ | 4.18 | ||||||

| Basic EPS – Class B common |

$ | 2.39 | $ | 2.19 | $ | 2.09 | ||||||

| Diluted EPS – Class A common |

$ | 3.93 | $ | 3.61 | $ | 3.43 | ||||||

| Diluted EPS – Class B common |

$ | 2.39 | $ | 2.19 | $ | 2.09 | ||||||

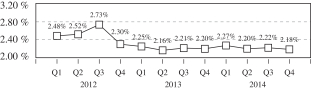

The trends in the net interest margin are illustrated in the graph below:

Net Interest Margin

From the beginning of 2012 through the third quarter of 2012, management stabilized the net interest margin by continuing to lower the cost of funds, and by deploying excess liquidity through expansion of the investment portfolio. Also, the Company collected approximately $3,253,000 of prepayment penalties during 2012. The primary factor accounting for the decrease in the net interest margin for the fourth quarter of 2012 and through the fourth quarter of 2013 was an additional large influx of deposits. Management invested the funds in shorter term securities. The net interest margin has declined slightly throughout 2014.

While management will continue its efforts to improve the net interest margin, there can be no assurance that certain factors beyond its control, such as the prepayment of loans and changes in market interest rates, will continue to positively impact the net interest margin.

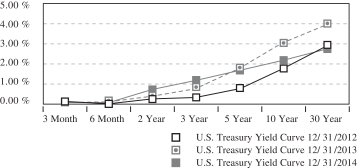

Historical U.S. Treasury Yield Curve

A yield curve is a line that typically plots the interest rates of U.S. Treasury Debt, which have different maturity dates but the same credit quality, at a specific point in time. The three main types of yield curve shapes are normal, inverted and flat. Over the past three years, the U.S. economy has experienced low short-term rates. During 2013, longer-term rates increased resulting in a steepening of the yield curve. During 2014, longer-term rates decreased resulting in a flattening of the yield curve.

During 2014, the Company’s earnings were positively impacted primarily by an increase in net interest income. This increase was primarily due to an increase in earning assets. During 2013, the Company’s earnings were positively impacted primarily by an increase in other operating income and a decrease in provision for loan

15

Table of Contents

Management’s Discussion and Analysis of Results of Operations and Financial Condition — (Continued)

losses. This increase in other operating income was primarily due to an increase in net gains on sales of loans and net gains on sales of securities. The decrease in the provision for loan losses was primarily attributable to a lower level of charge-off activity and changes in portfolio composition. During 2014, 2013 and 2012, the U.S. economy experienced a lower short-term rate environment. The lower short-term rates negatively impacted the net interest margin as the rate at which short-term deposits could be invested declined more than the rates offered on those deposits. The net interest margin was positively impacted in 2012 as a result of prepayment penalties that were collected during the year.

Total assets were $3,624,036,000 at December 31, 2014, an increase of 5.6% from total assets of $3,431,154,000 at December 31, 2013.

On December 31, 2014, stockholders’ equity totaled $192,500,000, compared with $176,472,000 on December 31, 2013. Book value per share increased to $34.57 at December 31, 2014, from $31.76 on December 31, 2013.

During July 2012, the Company received state regulatory approval to close a branch at Chestnut Hill in Newton, Massachusetts. The branch closed on September 21, 2012 and the accounts were temporarily moved to the Brookline, Massachusetts branch. During July 2012, the Company entered into a lease agreement and received regulatory approval to open a branch at a new location at Chestnut Hill in Newton, Massachusetts. The branch opened on November 7, 2013 and the majority of the accounts that were temporarily moved to the Brookline, Massachusetts branch were moved to the new branch at Chestnut Hill in Newton, Massachusetts.

During December 2013, the Company entered into a lease agreement to open a branch located in Woburn, Massachusetts. The branch opened on November 3, 2014.

During March 2014, the Company entered into a lease agreement to open a branch located on Boylston Street in Boston, Massachusetts. This property is leased from an entity affiliated with Marshall M. Sloane, Chairman of the Board of the Company. This agreement was approved by the Board of Directors in the absence of the Chairman of the Board. The branch is scheduled to open during the first quarter of 2015. The deposits from the Kenmore Square, Boston Massachusetts branch, which closed on September 30, 2014, will be moved to the new Boylston Street branch.

CRITICAL ACCOUNTING POLICIES

Accounting policies involving significant judgments and assumptions by management, which have, or could have, a material impact on the carrying value of certain assets and impact income, are considered critical accounting policies.

The Company considers impairment of investment securities and allowance for loan losses to be its critical accounting policies. There have been no significant changes in the methods or assumptions used in the accounting policies that require material estimates and assumptions.

Impaired Investment Securities

If a decline in fair value below the amortized cost basis of an investment security is judged to be “other-than-temporary,” the cost basis of the investment is written down to fair value. The amount of the writedown is included as a charge to earnings. The amount of the impairment charge is recognized in earnings with an offset for the noncredit component which is recognized through other comprehensive income. Some factors considered for other-than-temporary impairment related to a debt security include an analysis of yield which results in a decrease in expected cash flows, whether an unrealized loss is issuer specific, whether the issuer has defaulted on scheduled interest and principal payments, whether the issuer’s current financial condition hinders its ability to make future scheduled interest and principal payments on a timely basis or whether there was a downgrade in ratings by rating agencies.

16

Table of Contents

Management’s Discussion and Analysis of Results of Operations and Financial Condition — (Continued)

The Company does not intend to sell any of its debt securities with an unrealized loss, and it is not more likely than not that it will be required to sell the debt securities before the anticipated recovery of their remaining amortized cost, which may be maturity.

Allowance for Loan Losses

Arriving at an appropriate level of allowance for loan losses necessarily involves a high degree of judgment. Management maintains an allowance for loan losses to absorb losses inherent in the loan portfolio. The allowance is based on assessments of the probable estimated losses inherent in the loan portfolio. Management’s methodology for assessing the appropriateness of the allowance consists of several key elements, which include the formula allowance and specific allowances for identified problem loans.

The formula allowance evaluates groups of loans to determine the allocation appropriate within each portfolio segment. Specific allowances for loan losses entail the assignment of allowance amounts to individual loans on the basis of loan impairment. The formula allowance and specific allowances also include management’s evaluation of various factors, including business and economic conditions, delinquency trends, charge-off experience and other qualitative factors. Further information regarding the Company’s methodology for assessing the appropriateness of the allowance is contained within Note 1 of the “Notes to Consolidated Financial Statements.”

Management believes that the allowance for loan losses is adequate. In addition, various regulatory agencies, as part of the examination process, periodically review the Company’s allowance for loan losses. Such agencies may require the Company to recognize additions to the allowance based on their judgments about information available to them at the time of their examination.

FINANCIAL CONDITION

Investment Securities

The Company’s securities portfolio consists of securities available-for-sale (“AFS”) and securities held-to-maturity (“HTM”).

Securities available-for-sale consist of certain U.S. Treasury and U.S. Government Sponsored Enterprise mortgage-backed securities; state, county and municipal securities; privately issued mortgage-backed securities; other debt securities; and other marketable equities.

These securities are carried at fair value, and unrealized gains and losses, net of applicable income taxes, are recognized as a separate component of stockholders’ equity. The fair value of securities available-for-sale at December 31, 2014 totaled $448,390,000 and included gross unrealized gains of $1,630,000 and gross unrealized losses of $1,450,000. A year earlier, the fair value of securities available-for-sale was $464,245,000 including gross unrealized gains of $821,000 and gross unrealized losses of $2,519,000. In 2014, the Company recognized gains of $450,000 on the sale of available-for-sale securities. In 2013 and 2012, the Company recognized gains of $3,019,000 and $1,843,000, respectively.

Securities classified as held-to-maturity consist of U.S. Government Sponsored Enterprises and mortgage-backed securities. Securities held-to-maturity as of December 31, 2014 are carried at their amortized cost of $1,406,792,000. A year earlier, securities held-to-maturity totaled $1,487,884,000.

During the third quarter of 2013, $987,037,000 of securities available-for-sale with unrealized losses of $25,333,000 were transferred to securities held-to-maturity. This was done in response to rising interest rates and an assessment of liquidity needs.

17

Table of Contents

Management’s Discussion and Analysis of Results of Operations and Financial Condition — (Continued)

The following table sets forth the fair value and percentage distribution of securities available-for-sale at the dates indicated.

Fair Value of Securities Available-for-Sale

| 2014 | 2013 | 2012 | ||||||||||||||||||||||

| At December 31, |

Amount | Percent | Amount | Percent | Amount | Percent | ||||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||||||

| U.S. Treasury |

$ | 2,000 | 0.4 | % | $ | 1,998 | 0.4 | % | $ | 2,004 | 0.1 | % | ||||||||||||

| U.S. Government Sponsored Enterprises |

— | 0.0 | % | 10,004 | 2.2 | % | 130,340 | 9.1 | % | |||||||||||||||

| SBA Backed Securities |

6,717 | 1.5 | % | 7,302 | 1.6 | % | 8,156 | 0.6 | % | |||||||||||||||

| U.S. Government Agency and Sponsored Enterprises Mortgage-Backed Securities |

337,093 | 75.2 | % | 403,189 | 86.8 | % | 1,233,357 | 86.0 | % | |||||||||||||||

| Privately Issued Residential Mortgage-Backed Securities |

1,874 | 0.4 | % | 2,277 | 0.5 | % | 2,947 | 0.2 | % | |||||||||||||||

| Obligations Issued by States and Political Subdivisions |

96,784 | 21.6 | % | 36,723 | 7.9 | % | 55,174 | 3.8 | % | |||||||||||||||

| Other Debt Securities |

3,524 | 0.8 | % | 2,176 | 0.5 | % | 2,253 | 0.2 | % | |||||||||||||||

| Equity Securities |

398 | 0.1 | % | 576 | 0.1 | % | 570 | 0.0 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total |

$ | 448,390 | 100.0 | % | $ | 464,245 | 100.0 | % | $ | 1,434,801 | 100.0 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

The majority of the Company’s securities AFS are classified as Level 2, as defined in Note 1 of the “Notes to Consolidated Financial Statements.” The fair values of these securities are obtained from a pricing service, which provides the Company with a description of the inputs generally utilized for each type of security. These inputs include benchmark yields, reported trades, broker/dealer quotes, issuer spreads, two-sided markets, benchmark securities, bids, offers and reference data. Management’s understanding of a pricing service’s pricing methodologies includes obtaining an understanding of the valuation risks, assessing its qualification, verification of sources of information and processes used to develop prices and identifying, documenting, and testing controls. Management’s validation of a vendor’s pricing methodology includes establishing internal controls to determine that the pricing information received by a pricing service and used by management in the valuation process is relevant and reliable. Market indicators and industry and economic events are also monitored. The decline in fair value from amortized cost for individual available-for-sale securities that are temporarily impaired is not attributable to changes in credit quality. Because the Company does not intend to sell any of its debt securities and it is not more likely than not that it will be required to sell the debt securities before the anticipated recovery of their remaining amortized cost, the Company does not consider these investments to be other-than-temporarily impaired at December 31, 2014.

Securities available-for-sale totaling $96,886,000, or 2.67% of assets, are classified as Level 3, as defined in Note 1 of the “Notes to Consolidated Financial Statements.” These securities are generally equity investments or municipal securities with no readily determinable fair value. The securities are carried at fair value with periodic review of underlying financial statements and credit ratings to assess the appropriateness of these valuations.

Debt securities of Government Sponsored Enterprises refer primarily to debt securities of Fannie Mae and Freddie Mac.

18

Table of Contents

Management’s Discussion and Analysis of Results of Operations and Financial Condition — (Continued)

The following table sets forth the amortized cost and percentage distribution of securities held-to-maturity at the dates indicated.

Amortized Cost of Securities Held-to-Maturity

| 2014 | 2013 | 2012 | ||||||||||||||||||||||

| At December 31, |

Amount | Percent | Amount | Percent | Amount | Percent | ||||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||||||

| U.S. Government Sponsored Enterprises |

$ | 251,617 | 17.9 | % | $ | 291,779 | 19.6 | % | $ | 17,747 | 6.4 | % | ||||||||||||

| U.S. Government Sponsored Enterprise Mortgage-Backed Securities |

1,155,175 | 82.1 | % | 1,196,105 | 80.4 | % | 257,760 | 93.6 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total |

$ | 1,406,792 | 100.0 | % | $ | 1,487,884 | 100.0 | % | $ | 275,507 | 100.0 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

The following two tables set forth contractual maturities of the Bank’s securities portfolio at December 31, 2014. Actual maturities will differ from contractual maturities because borrowers may have the right to call or prepay obligations with or without call or prepayment penalties.

Fair Value of Securities Available-for-Sale Amounts Maturing

| Within One Year |

% of Total |

Weighted Average Yield |

One Year to Five Years |

% of Total |

Weighted Average Yield |

Five Years to Ten Years |

% of Total |

Weighted Average Yield |

Over Ten Years |

% of Total |

Weighted Average Yield |

|||||||||||||||||||||||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. Treasury |

$ | 2,000 | 0.4 | % | 0.23 | % | $ | — | 0.0 | % | 0.00 | % | $ | — | 0.0 | % | 0.00 | % | $ | — | 0.0 | % | 0.00 | % | ||||||||||||||||||||||||

| SBA Backed Securities |

— | 0.0 | % | 0.00 | % | — | 0.0 | % | 0.00 | % | 4,560 | 1.0 | % | 0.84 | % | 2,157 | 0.5 | % | 0.93 | % | ||||||||||||||||||||||||||||

| U.S. Government Agency and Sponsored Enterprise Mortgage-Backed Securities |

344 | 0.1 | % | 3.74 | % | 205,354 | 45.8 | % | 0.60 | % | 131,173 | 29.3 | % | 0.55 | % | 222 | 0.1 | % | 2.21 | % | ||||||||||||||||||||||||||||

| Privately Issued Residential Mortgage-Backed Securities |

1,874 | 0.4 | % | 1.54 | % | — | 0.0 | % | 0.00 | % | — | 0.0 | % | 0.00 | % | — | 0.0 | % | 0.00 | % | ||||||||||||||||||||||||||||

| Obligations of States and Political Subdivisions |

90,700 | 20.2 | % | 0.68 | % | 2,264 | 0.5 | % | 2.73 | % | — | 0.0 | % | 0.00 | % | 3,820 | 0.8 | % | 0.59 | % | ||||||||||||||||||||||||||||

| Other Debt Securities |

200 | 0.1 | % | 0.98 | % | 900 | 0.2 | % | 1.11 | % | — | 0.0 | % | 0.00 | % | 1,025 | 0.2 | % | 6.00 | % | ||||||||||||||||||||||||||||

| Equity Securities |

— | 0.0 | % | 0.00 | % | — | 0.0 | % | 0.00 | % | — | 0.0 | % | 0.00 | % | — | 0.0 | % | 0.00 | % | ||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Total |

$ | 95,118 | 21.2 | % | 0.70 | % | $ | 208,518 | 46.5 | % | 0.63 | % | $ | 135,733 | 30.3 | % | 0.56 | % | $ | 7,224 | 1.6 | % | 1.51 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Non- Maturing |

% of Total |

Weighted Average Yield |

Total | % of Total |

Weighted Average Yield |

|||||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||||||

| U.S. Treasury |

$ | — | 0.0 | % | 0.00 | % | $ | 2,000 | 0.4 | % | 0.23 | % | ||||||||||||

| SBA Backed Securities |

— | 0.0 | % | 0.00 | % | 6,717 | 1.5 | % | 0.87 | % | ||||||||||||||

| U.S. Government Agency and Sponsored |

||||||||||||||||||||||||

| Enterprise Mortgage-Backed Securities |

— | 0.0 | % | 0.00 | % | 337,093 | 75.2 | % | 0.59 | % | ||||||||||||||

| Privately Issued Residential Mortgage-Backed Securities |

— | 0.0 | % | 0.00 | % | 1,874 | 0.4 | % | 1.54 | % | ||||||||||||||

| Obligations of States and Political Subdivisions |

— | 0.0 | % | 0.00 | % | 96,784 | 21.6 | % | 0.72 | % | ||||||||||||||

| Other Debt Securities |

1,399 | 0.3 | % | 3.24 | % | 3,524 | 0.8 | % | 2.08 | % | ||||||||||||||

| Equity Securities |

398 | 0.1 | % | 3.09 | % | 398 | 0.1 | % | 3.09 | % | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total |

$ | 1,797 | 0.4 | % | 3.21 | % | $ | 448,390 | 100.0 | % | 0.64 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

19

Table of Contents

Management’s Discussion and Analysis of Results of Operations and Financial Condition — (Continued)

Amortized Cost of Securities Held-to-Maturity Amounts Maturing

| Within One Year |

% of Total |

Weighted Average Yield |

One Year to Five Years |

% of Total |

Weighted Average Yield |

Five Years to Ten Years |

% of Total |

Weighted Average Yield |

Over Ten Years |

% of Total |

Weighted Average Yield |

Total | % of Total |

Weighted Average Yield |

||||||||||||||||||||||||||||||||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. Government Sponsored Enterprises |

$ | — | 0.0 | % | 0.00 | % | $ | 103,044 | 7.3 | % | 1.19 | % | $ | 148,573 | 10.6 | % | 1.85 | % | $ | — | 0.0 | % | 0.00 | % | $ | 251,617 | 17.9 | % | 1.58 | % | ||||||||||||||||||||||||||||||

| U.S. Government Sponsored Enterprise Mortgage-Backed Securities |

3,837 | 0.3 | % | 3.16 | % | 992,434 | 70.5 | % | 2.34 | % | 157,117 | 11.2 | % | 2.31 | % | 1,787 | 0.1 | % | 3.36 | % | 1,155,175 | 82.1 | % | 2.34 | % | |||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

| Total |

$ | 3,837 | 0.3 | % | 3.16 | % | $ | 1,095,478 | 77.8 | % | 2.23 | % | $ | 305,690 | 21.8 | % | 2.09 | % | $ | 1,787 | 0.1 | % | 3.36 | % | $ | 1,406,792 | 100.0 | % | 2.20 | % | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

At December 31, 2014 and 2013, the Bank had no investments in obligations of individual states, counties, municipalities or nongovernment corporate entities which exceeded 10% of stockholders’ equity. In 2014, sales of securities totaling $40,285,000 in gross proceeds resulted in a net realized gain of $450,000. There were no sales of state, county or municipal securities during 2014 and 2013. In 2013, sales of securities totaling $224,045,000 in gross proceeds resulted in net realized gains of $3,019,000. In 2012, sales of securities totaling $294,881,000 in gross proceeds resulted in net realized gains of $1,843,000.

Management reviews the investment portfolio for other-than-temporary impairment of individual securities on a regular basis. The results of such analysis are dependent upon general market conditions and specific conditions related to the issuers of our securities.

Loans