Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - ZIX CORP | Financial_Report.xls |

| EX-31.2 - EX-31.2 - ZIX CORP | d851543dex312.htm |

| EX-23.1 - EX-23.1 - ZIX CORP | d851543dex231.htm |

| EX-32.1 - EX-32.1 - ZIX CORP | d851543dex321.htm |

| EX-31.1 - EX-31.1 - ZIX CORP | d851543dex311.htm |

Table of Contents

United States

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 0-17995

Zix Corporation

(Exact Name of Registrant as Specified in its Charter)

| Texas | 75-2216818 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification Number) |

2711 N. Haskell Avenue, Suite 2200, LB 36, Dallas, Texas 75204-2960

(Address of Principal Executive Offices)

(214) 370-2000

(Registrant’s Telephone Number, Including Area Code)

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of each class of stock |

Name of each exchange on which registered | |

| Common Stock $0.01 Par Value |

NASDAQ |

Securities Registered Pursuant to Section 12(b) of the Act: None

Indicate by check mark whether the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark whether the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such reports) Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of March 9, 2015, there were 56,984,827 shares of Zix Corporation $0.01 par value common stock outstanding. As of June 30, 2014, the aggregate market value of the shares of Zix Corporation common stock held by non-affiliates was $199,220,616.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s 2015 Proxy Statement are incorporated by reference into Part III of this Form 10-K.

Table of Contents

| Item 1. | 3 | |||||

| Item 1A. | 8 | |||||

| Item 1B. | 14 | |||||

| Item 2. | 14 | |||||

| Item 3. | 14 | |||||

| Item 4. | 14 | |||||

| Item 5. | 15 | |||||

| Item 6. | 16 | |||||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

17 | ||||

| Item 7A. | 27 | |||||

| Item 8. | 27 | |||||

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

27 | ||||

| Item 9A. | 27 | |||||

| Item 9B. | 30 | |||||

| Item 10. | 31 | |||||

| Item 11. | 31 | |||||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

31 | ||||

| Item 13. | Certain Relationships and Related Transactions, and Director Independence |

31 | ||||

| Item 14. | 31 | |||||

| Item 15. | 31 |

2

Table of Contents

Zix Corporation (“ZixCorp®,” the “Company,” “we,” “our,” or “us”) offers email encryption, data loss prevention and Bring-Your-Own-Device (“BYOD”) security to meet business data protection and compliance needs. We primarily serve organizations in the healthcare, financial services, insurance and government sectors, including significant federal financial regulators - such as the Federal Financial Institutions Examination Council (“FFIEC”), divisions of the U.S. Treasury, the U.S. Securities and Exchange Commission (SEC), one in every four U.S. banks, more than 30 Blue Cross Blue Shield organizations and one in every five U.S. hospitals.

Zix ® Email Encryption enables the secure exchange of emails that include sensitive information through a comprehensive secure messaging service, which allows an enterprise to use policy-driven rules to determine which email messages should be sent securely to comply with regulations or company-defined policies. Zix Email Encryption is a Software-as-a-Service (“SaaS”) solution, for which customers pay an annual service subscription fee.

The main differentiator for Zix Email Encryption in the marketplace is its exceptional ease of use. The best example of this is its ability to provide transparent delivery of secure, encrypted email. Most email encryption solutions are focused on the sender. They typically introduce an added burden on receivers, often requiring additional user authentication with the creation of a new user identity and password. We designed our solution to alleviate the receiver’s burden by enabling the delivery of encrypted email automatically and transparently. ZixCorp enables transparent delivery through (1) ZixDirectory®, the world’s largest email encryption community which is designed to share identities of our tens of millions of members (growing by approximately 110,000 members per week), (2) ZixCorp’s patented Best Method of Delivery®, which is designed to deliver email according to the sender’s encryption policy, and (3) ZixGateway®, which is an enterprise gateway that automatically decrypts the message. The result is the industry’s only transparent encrypted email, such that secure email can be exchanged without extra steps or passwords for both senders and receivers. ZixCorp delivers more than 1,100,000 encrypted messages on a typical business day. Of those messages, 75% are exchanged transparently between senders and receivers.

ZixCorp launched ZixDLP®, an email-specific data loss prevention (“DLP”) solution in early 2013. By focusing strictly on email, ZixDLP addresses business’s greatest source of data loss – corporate email. The straightforward DLP approach decreases the complexity and cost often associated with other DLP solutions. ZixDLP is also designed to reduce deployment time from months to hours and minimize impact on customer resources and workflow. In addition, ZixDLP offers a convenient experience for both employees interacting with the solution and administrators managing the system.

Leveraging the company’s leadership and expertise in email encryption, ZixDLP uses ZixCorp’s proven policy and content scanning capabilities with new quarantine functionality. The quarantine system and its intuitive interface allow administrators to (1) easily define policies and create custom lexicons for quarantining email messages, (2) conveniently manage quarantined messages using flexible searching and filtering options, (3) release or delete individual or multiple quarantined messages with one click, (4) review reports that monitor quarantine activities and trends and (5) automate custom notifications informing employees of quarantined messages.

ZixDLP is available as an add-on for existing ZixCorp customers or as a bundle with Zix Email Encryption for new customers. ZixDLP is also available as a standalone solution that can easily integrate with most email systems and email encryption solutions.

In late 2013, ZixCorp launched ZixOne®, a unique mobile email app that solves the key IT challenge created by the BYOD trend in the workplace. BYOD describes the increasing trend of employees using their personal devices to conduct work. ZixOne provides access to corporate email while never allowing that data to be persistently stored on the device where it is vulnerable to loss or theft. If the device is lost or stolen, an administrator can simply disable access to corporate email from that device through ZixOne.

Unlike other BYOD solutions, ZixOne meets employee demands of convenience, control and privacy while giving companies the ability to secure corporate data and meet compliance needs. With seamless access to work email in a secure, simple-to-use environment, employees can stay productive while preserving device independence. A BYOD solution that is acceptable to employees and yet provides strong data protection for corporate data solves one of today’s greatest IT management challenges.

3

Table of Contents

Our business operations and service offerings are supported by the ZixData CenterTM, a SysTrust/SOC3 certified, SOC2 accredited, PCI DSS V2.0 certified facility. The operations of the ZixData Center are independently audited annually to maintain AICPA SysTrust/SOC3 certification in the areas of security, confidentiality, integrity and availability. Auditors also produce a SOC2 (formerly SAS70 Type II) report on the effectiveness of operational controls used over the audit period. The ZixData Center is staffed 24 hours a day with a track record that exceeds 99.99% availability.

Our company was incorporated in Texas in 1988. Originally named Amtech Corporation, we changed our name to ZixIt® Corporation in 1999 when we entered the encrypted email market. In 2002, we became Zix Corporation. Our executive offices are located at 2711 North Haskell Avenue, Suite 2200, LB 36, Dallas, Texas 75204-2960, (214) 370-2000.

Overview

Email is a mission-critical means of communication for enterprises. However, if email leaves a secure network environment in clear text, it can be intercepted along the path between a sender and a recipient, which permits theft, redirection, manipulation or exposure to unauthorized parties. Failure to control and manage such risks can result in enforcement penalties for noncompliance under numerous regulations, in addition to damaged reputation, competitive disadvantage, a loss of intellectual property or other corporate assets, exposure to negligence or liability claims, and diversion of resources to repair such damage. For example, healthcare organizations, business associates and sub-contractors are subject to the Privacy, Security, and Enforcement Rules of the Health Information Portability Accountability Act (“HIPAA”) as amended by the Health Information Technology for Economic and Clinical Health Act (“HITECH Act”). Financial institutions are subject to data privacy laws including the Gramm-Leach-Bliley Act (“GLBA”). These federal laws help drive the use of encrypted email. In addition, individual states such as Massachusetts and Nevada have enacted privacy laws requiring encryption of certain email messages, and almost all states encourage email encryption by allowing exemptions from data breach notification laws.

Corporations require easy to use, cost-effective email protection that can be used on an enterprise-wide basis. They need it to be quickly deployed and regularly updated to evolve with innovative technology practices and meet changing regulatory standards. To satisfy these needs, our Email Encryption Service provides a comprehensive solution that analyzes and encrypts email communications.

Our Email Encryption Service allows a user to send encrypted email to any email user, anywhere and on any Internet-enabled device. Encrypted email is delivered through the patented Best Method of Delivery protocol which automatically determines the most direct and appropriate means of delivery, based on the sender’s and recipient’s communications environment and preferences. The protocol supports a number of encrypted email delivery mechanisms, including S/MIME, TLS, OpenPGP, “push” delivery and secure portal “pull” delivery. These last two mechanisms enable users to send messages securely to anyone with an email address, including those who do not have an encryption tool. Our Best Method of Delivery makes the technology simple for end users and provides flexibility and ease of implementation for information technology professionals. We believe the ability to send messages through different modes of delivery is one of many differentiators that makes our Email Encryption Service superior to competitive offerings.

The deployment of our Email Encryption Service at the periphery of the customer’s network means our Email Encryption Service encrypts outbound email for an enterprise without the need to create, deploy or manage end user encryption keys or deploy desktop software. Our technology solutions are easy to use, easy to deploy, and can be made operational quickly.

Our service has an integrated policy management capability. This policy engine can inspect the contents of emails and apply policies matching specific industry criteria such as HIPAA, the HITECH Act and GLBA. Customers can also build their own custom policies. This policy driven email encryption for regulatory compliance means customers can reduce the training required of their staff and significantly reduce the risk of inadvertently sending sensitive content by controlling the method of delivery through preset policies.

4

Table of Contents

Competition

The most significant differentiator for ZixCorp’s Email Encryption Service as compared with our competition is ease of use. The best example of our unequalled ease of use is transparent delivery of encrypted email messages. We are able to deliver transparent email encryption as a result of our SaaS architecture, ZixDirectory, Best Method of Delivery and ZixGateway. The most critical and highly differentiated component of our solution is the ZixDirectory which provides the ability to share user identities for encryption, which in turn provides frictionless interoperability between users in a community of interest such as healthcare, finance or government.

In addition, our service differs from the products and services of most of our competitors because we offer a SaaS architecture, while most of our competitors offer primarily a product-based approach that the customer builds and runs themselves. Some of our competitors have substantial information technology security and email protection products; however, our competitors’ customers tend to build and operate their own systems, and the directory of user identities each competitor creates is not shared. This practice is less desirable as different companies’ encrypted email systems are not easily made interoperable.

Our capability to offer interoperability is particularly important when it is necessary to communicate with external networks, as is the case with the healthcare and financial services markets. Our customers become part of the ZixDirectory, a global “white pages” enabling transparent secure communications with other ZixGateway customers using our centralized key management system and overall unique approach to implementing secure e-mail. We enable secure communications with other users via TLS, Open PGP, “push” delivery and secure portal “pull” delivery mechanisms. However, we believe our unique transparent delivery is the more preferred delivery model.

Zix Email Encryption and Zix DLP focus on the secure (i.e., encrypted) delivery and data loss prevention sub-segments of the e-mail security market. We view our primary competitors as Proofpoint Inc., Microsoft, Barracuda Networks, Sophos Inc., and McAfee, Inc. Technically, while these companies offer “send-to-anyone” encrypted email, we believe they are unable to offer the benefits that come from access to the ZixDirectory, use of our Best Method of Delivery protocol, and the industry’s only transparent email encryption. Nevertheless, some of these competitors are large enterprises with substantial financial and technical resources that exceed those we possess.

As discussed above, with the introduction of ZixOne the Company entered the BYOD mobile device security market. In the BYOD market, we view our primary competitors as companies that provide enterprise mobility management (“EMM”), which includes but is not limited to mobile device management (“MDM”), containerization and app wrapping technology. EMM is premised on storing business data on an employee’s personally owned device. In order to secure business data on personal devices, EMM requires individual users to permit their employer access to and control over personally owned smartphones and tablet computers and therefore can create user concerns about loss of control and privacy of their devices. In contrast, ZixOne enables Android® or IOS® mobile devices to view remotely stored corporate email, calendar and contacts, and to interact with that data. ZixOne more effectively protects business email data by never allowing it to be stored on the device, where it might be subjected to exposure from theft or loss of the device. Moreover, ZixOne does not require employees to relinquish device control or personal privacy to their employer. We believe these differentiators to make ZixOne an attractive BYOD solution. Nevertheless, ZixCorp is new to the BYOD and mobile security space, whereas competitors have an established brand in the market with substantial financial and technical resources that exceed those we possess. We view our primary competitors as AirWatch/VMware, Citrix (with XenMobile), Good Technology, IBM/Fiberlink (with MaaS360), Microsoft (with ActiveSync), and MobileIron.

Regulatory Drivers

We have been successful in securing additional market penetration for Zix Email Encryption in our target vertical markets of healthcare, finance services and government due to regulations that address the need for email privacy and security.

The demand for email encryption in the healthcare sector, including business associates of healthcare providers, results principally from regulatory requirements under HIPPA and HITECH Act. The Privacy and Security rules under those acts provide severe penalties for violations, include strict breach notification requirements, and allow

5

Table of Contents

states to pursue HIPAA violations. In the financial services industry, financial institutions and their service providers are subject to the GLBA, which is enforced by the U.S. Federal Trade Commission (“FTC”). The FTC has issued guidance saying that businesses that transmit sensitive data by email should be sure to encrypt the data.

In choosing an email security provider, companies are influenced by the solutions chosen by their regulators. Our customers include all of the federal regulators who comprise the FFIEC as well as the state banking regulators in more than twenty states. Our service is also a recommended solution of the Conference of State Bank Supervisors, whose memebers regulate the more than 6,000 state-chartered banks in the U.S.

Additionally, state data breach laws and privacy regulations, along with highly publicized breaches, have enhanced security awareness in vertical markets outside of healthcare and financial services and have prompted affected organizations to consider adopting systems that ensure data security and privacy. Even where there are no specific regulations, businesses may require email protection to adhere to evolving industry best practices for protecting sensitive information.

Sales and Marketing

We sell our Zix Email Encryption, Zix DLP and ZixOne Services through a direct sales force that focuses on larger businesses and a telesales force that focuses on small to medium-sized accounts. We also use a network of resellers and other distribution partners, including other service providers seeking an email encryption offering in an original equipment manufacturing (“OEM”)-like relationship. New first year orders (“NFYOs”), defined as the twelve month value of orders received from new customers), derived from our value-added resellers, OEM and third party distribution channels for 2014 were 58% of the total new first year orders compared to 59% in 2013. Google, Inc. continues to be our largest third party reseller representing approximately 4% of NFYOs in 2014. We now have more than 200 value-added resellers and over 100 managed security service providers across the U.S.

Employees

We had 198 employees as of December 31, 2014. The majority of our employees are located in Dallas, Texas; we also have a sales office in Burlington, Massachusetts; and a smaller office located in Ottawa, Ontario, Canada.

Research and Development — Patents and Trademarks

We incurred research and development expenses of $9.1 million, $9.6 million, and $7.4 million for the twelve-month periods ended December 31, 2014, 2013, and 2012, respectively.

Over the course of 2014 we continued to make investments toward strengthening and expanding our service portfolio. In addition to delivery of more than 20 new features for ZixOne and major enhancements to ZixDLP quarantine management, notification and workflows, we upgraded our core encryption strength and multi-language capabilities in the ZixPort hosted environment. A new hosted infrastructure was designed and deployed to efficiently deliver a “cloud version” of our ZixGateway service to the small-medium business segment and content filtering options and complex policy configurations were added to the ZixGateway feature set. We also made significant advancements in online ordering and provisioning capabilities to better serve the needs of our OEM and Managed Service Provider customers.

The following are registered trademarks of ours and certain of our subsidiaries: “ZixCorp,” “ZixGateway,” “ZixDirectory,” ZixIt, “ZixPort,” and “PocketScript”.

Compliance with Environmental Regulations

We have not incurred, and do not expect to incur, any material expenditures or obligations related to environmental compliance issues.

6

Table of Contents

Governmental Contracts

We have contracts with many local, state and federal agencies and regulators, which in aggregate contribute approximately six percent of our annual revenue.

Significant Customers

In each of 2014, 2013, and 2012, no single customer accounted for 10% or more of our total revenues. Our accounts receivable balance at December 31, 2012, included receivables from one customer comprising 12% of the net total. These receivables were paid to the Company in the first quarter 2013.

Backlog

Our backlog is comprised of contractual commitments that we expect to recognize as revenue in the future. Our backlog was $69.3 million at December 31, 2014, compared to $65.7 million at December 31, 2013.

As of December 31, 2014, our backlog is comprised of the following elements: $22.5 million of deferred revenue that has been billed and paid, $6.5 million billed but unpaid, and approximately $40.3 million of unbilled contracts.

The backlog is recognized into revenue ratably as the services are performed. Approximately 57% of our total backlog at December 31, 2014, is expected to be recognized as revenue during 2015.

Seasonality

Our business is not materially impacted by seasonality.

Geographic Information

Our operations are primarily based in the U.S., with approximately 5% of our employees located in Canada. Except for a United Kingdom based data center, we do not operate in, or have dependencies on, any other foreign countries. Our revenues and orders to-date are almost entirely sourced in the U.S. and all significant corporate assets at December 31, 2014, were located in the U.S.

Available Information

Our Internet address is www.zixcorp.com. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), are available on our website, without charge, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The information found on our website shall not be considered to be part of this or any other report filed with or furnished to the SEC.

In addition to our website, you may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 450 Fifth Street, N.W., Washington, D.C. 20549. You may obtain information on the operation of the SEC’s Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains a website that contains reports, proxy and other information statements, and other information regarding issuers, including us, that file electronically with the SEC. The address of the website is www.sec.gov.

NOTE ON FORWARD-LOOKING STATEMENTS AND RISK FACTORS

This document contains “forward-looking statements” (including the discussion appearing under the caption “Liquidity Summary” in “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations,”) within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Act”) and Section 21E of the Exchange Act. All statements other than statements of historical fact are “forward-looking statements” for purposes of federal and state securities laws, including: any projections of future business, market share, earnings, revenues, recognition of revenues from backlog, cash receipts, or other financial items; any statements of the plans, strategies, and objectives of management for future operations; any statements concerning proposed new products, services, or developments; any statements regarding future economic conditions or performance; any

7

Table of Contents

statements of belief; and any statements of assumptions underlying any of the foregoing. Forward-looking statements may include the words “may,” “will,” “predict,” “project,” “forecast,” “plan,” “should,” “could,” “goal,” “estimate,” “intend,” “continue,” “believe,” “expect,” “outlook,” “anticipate,” “hope,” and other similar expressions. Any forward-looking statements involve risks and uncertainties that could cause actual events or results to differ materially from the events or results described in the forward-looking statements, including, but not limited to, the risks and uncertainties described in the “Item 1A Risk Factors” section.

Although we believe that expectations reflected in any of our forward-looking statements are reasonable, actual results could differ materially from those projected or assumed in any of our forward-looking statements. Our future financial condition and results of operations, as well as any forward-looking statements, are subject to change and to inherent risks and uncertainties, such as those disclosed in this document. We do not intend, and undertake no obligation, to update any forward-looking statement.

The following is a cautionary discussion of risks, uncertainties and assumptions that we believe are significant to our business, financial condition and financial results. In addition to the factors discussed elsewhere in this Annual Report on Form 10-K, the following are some of the important factors that, individually or in the aggregate, we believe could make our results differ materially from those described in any forward-looking statements. It is impossible to predict or identify all such factors and, as a result, you should not consider the following factors to be a complete discussion of risks, uncertainties and assumptions.

Our business depends upon customers using email to exchange confidential information, and a significant shift of those messages to other communication channels could impair our growth prospects and negatively affect our business, financial condition and financial results.

Our customers deploy and use our products and services to easily, securely and confidentially send and receive email messages. Our business and revenue substantially depend on our current and potential customers using email to exchange sensitive information electronically. New technologies, products, or business models that could support secure communications could be disruptive to our business. If prospective or current customers were to send and receive sensitive information using technology or communication channels other than email, our growth prospects and our business, financial condition and financial results could be materially adversely affected.

Our business relies on securing new customer subscriptions and subscription renewals from existing customers.

A large portion of our revenue is derived from customer subscriptions, and in many cases existing customers have no contractual obligations to purchase beyond the initial subscription or contract period. We may not maintain historical subscription rates, and we may be unable to accurately predict our customer renewal rates. Our customers’ renewal rates may decline or fluctuate as a result of a number of factors, including the level of their satisfaction with our products and technical support services, customer budgets and the pricing of our products compared with those offered by our competitors. If new subscriptions or subscription renewals decline, our revenue or revenue growth may decline, and our business may suffer.

Public key cryptography technology used in our businesses is subject to technology integrity risks that could reduce demand for our products and services and could negatively affect our business, financial condition and financial results.

Our business employs public key cryptography technology and other encryption technologies to encrypt and decrypt messages. The security afforded by encryption depends on the integrity of the private key, which is predicated on the assumption that it is very difficult to mathematically derive the private key from the related public key. Successful decryption of intercepted encrypted email, or public reports of successful decryption, whether or not true, could reduce demand for our products and services. If new methods or technologies, such as quantum computing, make it easier to derive the private key from the related public key, the security of encryption services using public key cryptography technology could be impaired and our products and services could become

8

Table of Contents

unmarketable. That could require us to make significant changes to our services, which could increase our costs, damage our reputation, or otherwise harm our business. Any of these events could reduce our revenues, increase our expenses and materially adversely affect our business, financial condition and financial results.

The growth of our business may require significant investment in systems and infrastructure and these investments may achieve delayed, or lower than expected benefits, which could impair our profitability and negatively affect our business, financial condition and financial results.

As our operations grow in size and scope, we continually need to improve and upgrade our technology offerings, systems and infrastructure to offer an increasing number of customers enhanced products, services, features and functionality, while maintaining the reliability and integrity of our systems and infrastructure and pursuing reduced costs per transaction. Expanding our technology offerings, systems and infrastructure may require us to commit substantial financial, operational and technical resources, with no assurance that the volume of our business will increase, which could reduce our net income, deplete our cash, and materially adversely affect our business, financial condition and financial results.

We face strong competition, which could negatively affect our business, financial condition and financial results.

The markets in which we compete are characterized by rapid change and converging technologies and are very competitive. With rising demand for private and secure email communications, there is strong competition for email encryption products and services. Our Email Encryption and data loss prevention business competes with products and services offered by companies such as Microsoft, Barracuda Networks, Inc., McAfee, Inc., Proofpoint, and Sophos Inc. Our ZixOne business completes with products and services offered by companies such as AirWatch/VMWare, Citrix (with XenMobile), Good Technology, IBM/Fiberlink (with MaaS360), Microsoft (with ActiveSync), and MobileIron. Strong competition requires us to develop new technology solutions and service offerings to expand the functionality and value that we offer to our customers. Some of our competitors bundle their competing products and services with products and services that we do not offer, which could make our offering less attractive by comparison. As a result of the bundling by these competitors, it can be difficult for our customers to compare the cost of our offerings with competing offerings. In some instances, competing products and services may seem to be offered by our competitors at little to no additional cost to the customer. In addition, our competitors may develop products and services that are perceived by customers as equivalent to, or having advantages over, our products and services. Competitors could capture a significant share in our markets, causing our sales and revenue to decline or grow more slowly. Barriers to entry are relatively low, and new ventures are often formed that create products competitive with our products. Competitive pressures could lead to price discounting or to increases in expenses such as advertising and marketing costs. Increased competition could also decrease demand for our products and services. Competition could reduce our revenues and net income and materially adversely affect our business, financial condition and financial results.

Industry consolidation may lead to increased competition and may harm our operating results.

There has been a trend toward industry consolidation in our industry for several years. We expect this trend to continue as companies attempt to strengthen or hold their market positions in an evolving industry and as companies are acquired or are unable to continue operations. For example, some of our current and potential competitors have made acquisitions, or announced new strategic alliances. Companies that are strategic alliance partners in some areas of our business may acquire or form alliances with our competitors, thereby reducing their business with us. We believe that industry consolidation may result in stronger competitors that are better able to compete as sole-source vendors for customers. This could have a material adverse effect on our business, financial condition and financial results.

9

Table of Contents

Some competitors have advantages that may allow them to compete more effectively than us, which could negatively affect our business, financial condition and financial results.

Some of our competitors have longer operating histories, more extensive operations, greater name recognition, larger technical staffs, bigger product development and acquisition budgets, established relationships with more distributors and hardware vendors, and greater financial and marketing resources than we do. These advantages might enable them (independently or through alliances) to develop and expand functionality of products and services faster than we can, to spend more money to market and distribute products and services than we can, or to offer their products and services at prices lower than ours. These advantages could reduce our revenues and net income and materially adversely affect our business, financial condition and financial results.

We increasingly rely on third party distributors to help us market our products and services, and our failure to succeed in those relationships could negatively affect our business, financial condition and financial results.

We distribute an increasing percentage of our products and services by entering into alliances with third parties who can offer our products and services along with their own or our competitors’ products and services. Increased reliance on third parties to market and distribute our products and services exposes us to a variety of risks. For example, we have limited control over the sales cycles of third party distributors, which could increase the length of our sales cycle, cause our revenue to fluctuate unpredictably and make it difficult to accurately forecast our revenue. In addition, we may not succeed in developing or maintaining marketing alliances. Companies with which we have marketing alliances may in the future discontinue their relationships with us, form marketing alliances with our competitors, or develop and market their own products and services that compete with ours. If a significant distributor were to discontinue its relationship with us, we could experience an interruption in the distribution of our products and services and our revenues could decline. Our failure to develop, maintain and expand strategic distribution relationships could reduce our revenues and net income and materially adversely affect our business, financial condition and financial results.

Our business depends on market acceptance of our products and services, and our failure to achieve and maintain influential customers could negatively affect our business, financial condition and financial results.

In order to continue to operate profitably and grow, we must achieve and maintain broad market acceptance of our products and services at a price that provides us with an acceptable rate of return relative to our costs. We have been successful in selling our Email Encryption products and services to high-profile customers in the healthcare, financial services and government segments of the market. The acceptance and use of our products and services by those significant customers facilitates our sales to potential customers, and an expanding base of users in the Zix Directory aids in our market penetration and expansion. The loss of an influential customer of our existing products and services, or the failure to achieve sufficient market adoption of new products including ZixDLP and ZixOne, could impair our ability to expand the market penetration of our products and services, or cause us to reduce or increase prices, which could reduce our revenues and net income and materially adversely affect our business, financial condition and financial results.

Unfavorable economic environments could negatively affect our business, financial condition and financial results.

Challenging economic conditions worldwide have from time to time contributed, and may continue to contribute, to slowdowns in technology and networking industries at large, as well as in the specific markets in which we operate. If economic growth in those markets is slow, or credit is unavailable at a reasonable cost, current and potential customers may delay or reduce technology purchases, including the deployment or expansion of our products and services. This could result in reduced sales of our products and services, longer sales cycles, slower adoption of new technologies and increased price competition. In addition, adverse economic conditions could negatively affect the cash flow of our customers and distributors, which might result in failures or delays in payments to us. This could increase our credit risk exposure and delay our recognition of revenue. Specific economic trends, such as declines in the demand for cloud computing services and computing devices, or softness in corporate information technology spending, could have a more direct impact on our business. If these conditions persist, spread or deteriorate further, our business, financial condition and financial results could be materially adversely affected.

10

Table of Contents

Our failure to keep pace with rapid technology changes could have a negative impact on our business, financial condition and financial results.

The markets for our products and services are characterized by rapid technological developments and frequent changes in customer requirements. We must continually improve the performance, features and reliability of our products and services, particularly in response to competitive offerings, to keep pace with these developments. We must ensure that our products and services address evolving operating environments, devices, industry trends, certifications and standards. For example, we have been required to expand our offerings for virtual computer environments and mobile environments to support a broader range of mobile devices. We also may need to develop products that are compatible with new operating systems while remaining compatible with existing, popular operating systems. Our business could be harmed by our competitors announcing or introducing new products and services that could be perceived by customers as superior to ours. We spend considerable resources on technology research and development, but our research and development resources are more limited than many of our competitors. Our failure to introduce new or enhanced products on a timely basis, to keep pace with rapid industry, technological or market changes or to gain customer acceptance for our new and existing products and services, such as mobile device data protection, could have a material adverse effect on our business, financial condition and financial results.

If our products do not work properly, our business, financial condition and financial results could be negatively affected and we could experience negative publicity, declining sales and legal liability.

We produce complex products that incorporate leading-edge technology, including both hardware and software, that must operate in a wide variety of technology environments. Software may contain defects or “bugs” that can interfere with expected operations. There can be no assurance that our testing programs will be adequate to detect all defects prior to the product being introduced, which might decrease customer satisfaction with our products and services. The product reengineering cost to remedy a product defect could be material to our operating results. Our inability to cure a product defect could result in the temporary or permanent withdrawal of a product or service, negative publicity, damage to our reputation, failure to achieve market acceptance, lost revenue and increased expense, any of which could have a material adverse effect on our business, financial condition and financial results.

The infrastructure supporting our business may suffer capacity constraints and business interruptions that could cause us to lose customers, increase our operating costs and could negatively affect our business, financial condition and financial results.

Our business depends on our providing our customers reliable, real-time access to our data centers and networks. Customers will not tolerate a service hampered by slow delivery times, unreliable service levels, service outages, or insufficient capacity. System capacity limits or constraints arising from unexpected increases in our volume of business or network traffic could cause interruptions, outages or delays in our services, or deterioration in their performance, or could impair our ability to process transactions. We may not be able to accurately project the rate of increase in usage of our systems or to timely increase capacity to accommodate increased traffic on our systems. System delays or interruptions may prevent us from efficiently providing services to our customers or other third parties, which could result in our losing customers and revenues, or incurring liabilities that could have a material adverse effect on our business, financial condition and financial results.

Our business depends substantially on our data center facilities, and their unreliability or unavailability for a significant period could cause us to lose customers and could negatively affect our business, financial condition and financial results.

Much of the computer and communications hardware upon which our businesses depend is located in our data center facilities in Dallas and Austin, Texas and in the United Kingdom. Our data centers might be damaged or interrupted by fire, flood, power loss, telecommunications failure, break-ins, cyber-attacks, earthquakes, terrorist

11

Table of Contents

attacks, hostilities or war or other events. Computer viruses, equipment failure, denial of service attacks, and similar disruptions affecting the internet or our systems might cause service interruptions, delays and loss of critical data, and could prevent us from providing our services. Problems affecting our data center operations or the networks on which we rely could result in loss of revenues, increased expenses, failure to achieve market acceptance, diversion of resources, injury to our reputation, liability and increased costs. We do not carry sufficient insurance to compensate us for all losses that may occur as a result of any of these events. The occurrence of any of these events could materially adversely affect our business, financial condition and financial results.

Outages or problems with systems and infrastructure supplied by third parties could negatively affect our business, financial condition and financial results.

Our business relies on third-party suppliers of the telecommunications infrastructure. We use various communications service suppliers and the global internet to provide network access between our data centers, our customers and end-users of our services. If those suppliers do not enable us to provide our customers with reliable, real-time access to our systems, we may be unable to gain or retain customers. These suppliers periodically experience outages or other operational problems as a result of internal system failures or external third party actions. Though our products generally tolerate isolated supplier failures, multiple supplier outages or problems could materially adversely affect our business, financial condition and financial results.

The security of our networks and data centers is critical to our business and an actual or perceived breach of security through a cyber-attack or otherwise could cause us to lose customers and could negatively affect our business, financial condition and financial results.

We are dependent on our networks and data centers to provide our products and services. Due to the nature of the products and services we provide and the sensitive nature of the information we collect, process, store, use and transmit, we may face cyber-attacks that attempt to penetrate our networks and data centers. Our business depends on customers having and maintaining confidence that we provide effective network and security protection. To reduce the risk of a successful cyber-attack, we have implemented significant physical and logical security measures to detect, identify and mitigate threats as well as to monitor for and respond to potential breaches and incidents. Despite these security measures, our networks and data centers may remain vulnerable to cyber-attack. If a cyber-attack or other breach of security occurs, or is perceived to have occurred, in our internal systems or at our data centers and networks, it could cause negative publicity, interruption of our services, damage to our reputation, unauthorized disclosure of our customers’ confidential or proprietary information (including personally identifiable information), disclosure of our intellectual property, disclosure, modification or removal of our confidential or sensitive information, loss of customers, lost revenue and increased expense (including potentially indemnification or warranty costs), any of which could have a material adverse effect on our business, financial condition and financial results.

Our usage of personal information, and inadvertent exposure of confidential or personal information, could cause us to violate data privacy laws or lose customers and could negatively affect our business, financial condition and financial results.

We transmit large amounts of encrypted personally identifiable information about individuals, such as personal healthcare or financial information. Our processing and storage of these types of data incident to transmission is subject to confidentiality agreements with our clients and handling of this data is increasingly subject to regulation around the world. These regulations may result in conflicting requirements and may change over time. Changes in requirements under these regulations may be inconsistent with our existing data management practices. If so, we could be required to fundamentally change our business activities and practices or modify our software, which could have an adverse effect on our business. Any inability to adequately address privacy concerns, even if unfounded, or to comply with applicable privacy or data protection laws, regulations and policies, could result in additional cost an liability to us, damage our reputation, inhibit sales and harm our business. Furthermore, any unauthorized disclosure of personal or other confidential information (including due to a cyber-attack) or other failure by us to comply with data privacy requirements could subject us to significant penalties, damages, remediation and other expenses, and damage to our reputation, any of which could have a material adverse effect on our business, financial condition and financial results

12

Table of Contents

Problems with enforcing our intellectual property rights or using third party intellectual property could negatively affect our business, financial condition and financial results.

We rely on a combination of contractual rights, trademarks, trade secrets, patents and copyrights to establish and protect intellectual property rights and other proprietary rights in our products and services. These intellectual property rights or other proprietary rights might be challenged, invalidated or circumvented. The steps we have taken to protect our proprietary information may not prevent its misuse, theft or misappropriation. Competitors may independently develop technologies or products that are substantially equivalent or superior to our products or that inappropriately incorporate our intellectual property rights or other proprietary technology into their products. Competitors may hire our former employees who may misappropriate our intellectual property rights or other proprietary technology. Some jurisdictions may not provide adequate legal protection of our intellectual property rights or other proprietary technology.

We may have to defend our rights in intellectual property that we use in our services, and we could be found to infringe the intellectual property rights of others, which could be disruptive and expensive to our business.

We may have to defend against claims that we or our customers are infringing the rights of third parties in patents, copyrights, trademarks and other intellectual property. If we acquire technology to include in our products from third parties, our exposure to infringement actions may increase because we must rely upon these third parties to verify the origin and ownership of such technology. Intellectual property litigation and controversies are disruptive and expensive. Even unmeritorious claims brought against us or our customers may harm our reputation and customer relationships, may cause us to incur significant legal and other fees to defend, and may have to be settled for significant amounts. Infringement claims could require us to develop non-infringing services or enter into expensive royalty or licensing arrangements. Our business, financial condition and financial results could be materially adversely affected if we are not able to develop non-infringing technology or license technology on commercially reasonable terms.

We may face risks from using “open source” software that could negatively affect our business, financial condition and financial results.

Like many other software companies, we use “open source” software in order to take advantage of common industry building blocks and to add functionality to our products quickly and inexpensively. Open source software license terms could adversely affect our intellectual property rights in our products that include open source software. Depending upon how the open source software is deployed, we could be required to offer products that use the open source software for no cost, or make available the source code for modifications or derivative works. Any of these obligations could have an adverse impact on our intellectual property rights and revenue from products incorporating the open source software. Using open source code could also cause us to inadvertently infringe third-party intellectual property rights or require us to publicly disclose proprietary information. We have processes and controls in place that are designed to address these risks and concerns, but we cannot be sure that all open source software is submitted for approval prior to use in our products nor that our process or controls will be sufficient to mitigate all risk in this regard.

We may fail to recruit and retain key personnel, which could impair our ability to meet key objectives.

Our success depends on our ability to attract and retain highly-skilled technical, managerial, sales, and marketing personnel. Changes in key personnel may be disruptive to our business. It could be difficult, time consuming and expensive to replace key personnel. Integrating new key personnel may be difficult and costly. Volatility, lack of positive performance in our stock price or changes to our overall compensation program including our stock incentive program may adversely affect our ability to retain key employees, many of whom are compensated, in part, based on the performance of our stock price. The loss of services of any of our key personnel, the inability to retain and attract qualified personnel in the future or delays in hiring required personnel could make it difficult to meet key objectives. Any of these impairments related to our key personnel could negatively affect our business, financial condition and financial results.

13

Table of Contents

Governmental restrictions on the sale of our products and services in non-U.S. markets could negatively affect our business, financial condition and financial results.

Exports of software solutions and services using encryption technology such as ours are generally restricted by the U.S. government. Although we have obtained U.S. government approval to export our service to almost all countries, the list of countries to which we (and our distributors) cannot export our products and services could be expanded in the future. In addition, some countries impose restrictions on the importation and use of encryption solutions and services such as ours. The cost of compliance with U.S. and other export laws, or our failure to obtain governmental approvals to offer our products and services in non-U.S. markets, could affect our ability to sell our products and services and could impair our international expansion. We face a variety of other legal and compliance risks. If we or our distributors fail to comply with applicable law and regulations, we may become subject to penalties, fines or restrictions that could materially adversely affect our business, financial condition and financial results.

Exercises of options for our common stock would dilute the ownership interests of existing shareholders and could negatively affect the value of our securities.

We have a significant number of outstanding options held by our employees. The exercise of options, and the resulting issuance of additional shares of our common stock, would substantially dilute the ownership interests and voting rights of our current shareholders. Issuance or sales of those additional shares could cause our securities to decline in value.

Item 1B. Unresolved Staff Comments

None.

We leased properties during 2014 that are considered significant to the operations of the business in the following locations: Burlington, Massachusetts; Ottawa, Ontario, Canada; the United Kingdom; and Dallas and Austin, Texas. Our Burlington employees perform sales and marketing activities. Our Ottawa employees perform both client services and sales support activities. The United Kingdom facility provides data center support for our European customers. The Dallas office is our headquarters, which includes research and development, marketing, sales and all general administrative services, and the ZixData Center. Our Austin location is used primarily for fail-over and business continuity services and is used to some extent to support normal ongoing operations. Our facilities are suitable for our current needs and are considered adequate to support expected near term growth.

We are subject to legal proceedings, claims, and litigation against our business. While the outcome of these matters is currently not determinable, and the costs and expenses of defending these matters may be significant, we currently do not expect that the ultimate costs to resolve these matters will have a material adverse effect on our consolidated financial statements.

Item 4. Mine Safety Disclosures

Not applicable.

14

Table of Contents

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our common stock trades on The Nasdaq Stock Market under the symbol ZIXI. The table below shows the high and low sales prices by quarter for fiscal 2014 and 2013.

| 2014 | 2013 | |||||||||||||||

| Quarter Ended |

High | Low | High | Low | ||||||||||||

| March 31 |

$ | 4.94 | $ | 3.88 | $ | 3.90 | $ | 2.84 | ||||||||

| June 30 |

$ | 4.27 | $ | 3.10 | $ | 4.32 | $ | 3.37 | ||||||||

| September 30 |

$ | 4.08 | $ | 2.90 | $ | 5.03 | $ | 4.09 | ||||||||

| December 31 |

$ | 3.83 | $ | 3.03 | $ | 4.97 | $ | 3.90 | ||||||||

At March 9, 2015, there were 56,984,827 shares of common stock outstanding held by 418 stockholders of record. On that date, the last reported sales price of the common stock was $4.06.

We have not paid any cash dividends on our common stock and do not anticipate doing so in the foreseeable future.

For information regarding options and stock-based compensation awards outstanding and available for future grants, see “Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.”

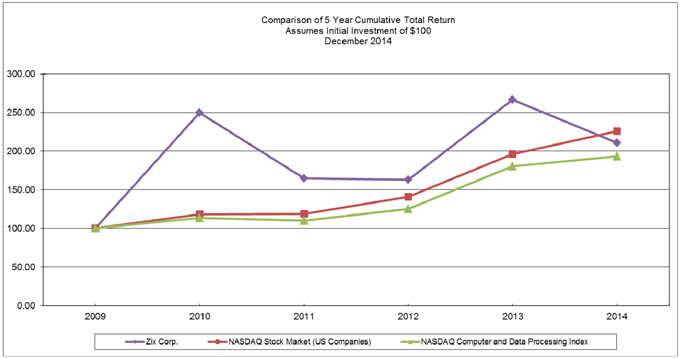

Performance Graph

The following graph compares the cumulative total return of an investment in our common stock over the five-year period ended December 31, 2014, as compared with the cumulative total return of an investment in (i) the Center for Research in Securities Prices (“CRSP”) Total Return Index for Nasdaq Stock Market (U.S. companies) and (ii) the CRSP Total Return Index for Nasdaq Computer and Data Processing Stocks. The comparison assumes $100 was invested on December 31, 2009, in our common stock and in each of the two indices and assumes reinvestment of dividends, if any. The stock price performance on the following graph is not necessarily indicative of future stock performance. A listing of the companies comprising each of the CRSP- NASDAQ indices used in the following graph is available, without charge, upon written request.

15

Table of Contents

Sale of Unregistered Securities

None.

Purchases of Equity Securities by the Issuer

None.

Item 6. Selected Financial Data

The following selected financial data should be read in conjunction with “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations,” the consolidated financial statements and notes thereto. No cash dividends were declared in any of the five years shown below:

| Year Ended December 31, | ||||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | 2010 | ||||||||||||||||

| (In thousands, except per share data) | ||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||

| Revenues |

$ | 50,347 | $ | 48,138 | $ | 43,356 | $ | 38,145 | $ | 33,066 | ||||||||||

| Cost of revenue |

8,324 | 7,614 | 7,609 | 7,211 | 6,468 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross margin |

42,023 | 40,524 | 35,747 | 30,934 | 26,598 | |||||||||||||||

| Research and development expenses |

9,051 | 9,563 | 7,419 | 5,229 | 5,089 | |||||||||||||||

| Selling, general and administrative expenses |

26,222 | 21,646 | 19,385 | 15,128 | 16,363 | |||||||||||||||

| Income tax expense (benefit) to continuing operations(1) |

2,830 | (1,006 | ) | (1,949 | ) | (11,889 | ) | (35,500 | ) | |||||||||||

| Income from continuing operations |

4,103 | 10,453 | 11,003 | 22,554 | 40,720 | |||||||||||||||

| Basic income per common share from continuing operations |

$ | 0.07 | $ | 0.17 | $ | 0.18 | $ | 0.34 | $ | 0.63 | ||||||||||

| Diluted income per common share from continuing operations |

$ | 0.07 | $ | 0.17 | $ | 0.17 | $ | 0.34 | $ | 0.61 | ||||||||||

| Shares used in computing basic income per common share |

57,949 | 61,139 | 62,211 | 65,439 | 64,401 | |||||||||||||||

| Shares used in computing diluted income per common share |

58,967 | 62,527 | 62,875 | 67,262 | 66,742 | |||||||||||||||

| Statements of Cash Flows Data: |

||||||||||||||||||||

| Net cash flows provided by (used for): |

||||||||||||||||||||

| Operating activities |

$ | 13,317 | $ | 13,298 | $ | 12,533 | $ | 13,219 | $ | 7,190 | ||||||||||

| Investing activities |

(3,402 | ) | (1,593 | ) | (1,533 | ) | (1,471 | ) | (1,467 | ) | ||||||||||

| Financing activities |

(15,748 | ) | (7,175 | ) | (8,692 | ) | (15,687 | ) | 5,609 | |||||||||||

| Balance Sheet Data: |

||||||||||||||||||||

| Cash, Cash Equivalents and Marketable Securities |

$ | 21,685 | $ | 27,518 | $ | 22,988 | $ | 20,680 | $ | 24,619 | ||||||||||

| Working capital(2) |

2,249 | 12,127 | 6,626 | 5,497 | 9,822 | |||||||||||||||

| Total assets |

83,724 | 90,702 | 82,849 | 77,552 | 66,852 | |||||||||||||||

| Debt obligations |

— | — | — | — | 186 | |||||||||||||||

| Stockholders’ equity |

56,270 | 66,234 | 61,245 | 57,757 | 46,887 | |||||||||||||||

Operations Data in the preceding table excludes all activity of the discontinued operations.

| (1) | The $1.0 million, $1.9 million, $11.9 million and $35.5 million tax benefits in 2013, 2012, 2011 and 2010 resulted from the release of a portion of our deferred tax asset valuation allowance. Based on analysis of both projected and current earnings excluding discontinued operations, we have estimated these tax assets as likely to be utilized prior to expiration. See “Income Taxes” in “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.” |

| (2) | Working capital includes deferred revenue totaling $21.6 million, $19.1 million, $17.5 million, $16.6 million, and $15.3 million as of December 31, 2014, 2013, 2012, 2011 and 2010 respectively. |

16

Table of Contents

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward-Looking Statements

The following discussion and analysis contains forward-looking statements about trends, uncertainties and our plans and expectations of what may happen in the future. Forward-looking statements involve risks and uncertainties that could cause actual events or results to differ materially from the events or results described in the forward-looking statements, including risks and uncertainties described above in “Item 1A. Risk Factors.” Readers are cautioned not to place undue reliance on forward-looking statements. The forward-looking statements are based upon information available to us on the date of this report. We undertake no obligation to publicly update or revise any forward-looking statements.

Overview

We are a leader in providing secure email encryption in a SaaS model. We provide email encryption, DLP and BYOD solutions to meet the data protection and compliance needs of organizations primarily in the healthcare, finance, and government sectors. A core competency is our ability to deliver this complex service offering with a high level of availability, reliability, integrity and security.

Our 2014 results included record revenues and the continued introduction of two new service offerings, ZixDLP and ZixOne. We attribute our success to on going efforts to build a solid and predictable business based on our successful recurring revenue subscription business model. For 2014 we continued to benefit from growing concerns for data security and integrity issues which continue to make headline news as well as the growing acceptance of cloud-based offerings along with the growing need for regulatory compliance.

For 2014, we reported revenue of $50.3 million, an increase of $2.2 million over the prior year, driven principally by continued growth in our Email Encryption business. The Company’s operating income for 2014 was $6.8 million, a decrease of $2.6 million over the prior year, resulting from increases in selling and marketing expenses.

For the year ended December 31, 2014, our gross profit of $42.0 million increased 4% compared to 2013. This increase was primarily driven by increased revenue. Our 2014 operating income of $6.8 million decreased $2.6 million over the prior year, as the gross profit increase was offset by increased selling and marketing investments.

17

Table of Contents

Our $4.1 million net income in 2014 reflected an increase in tax expense of $3.8 million compared to 2013. Our $10.5 million net income in 2013 reflected a decrease to our valuation allowance of $4.1 million, of which $2.7 million was due to operations and offset current tax expense. The remaining $1.4 million was due to a partial reversal of the remaining valuation allowance and recorded as a tax benefit.

Other Financial Highlights

| • | Backlog was $69.3 million at the end of 2014, compared with $65.7 million at the end of 2013 |

| • | Total orders for 2014 were $55.4 million, a decrease of 2% from the 2013 total orders of $56.6 million |

| • | Our deferred revenue at the end of 2014 was $22.5 million, compared with $20.4 million at the end of 2013 |

| • | We generated cash flows from operations of $13.3 million during fiscal 2014. Our cash and cash equivalents were $21.7 million at the end of 2014, compared with $27.5 million at the end of 2013. |

| • | Our shared, cloud-based ZixDirectory now has approximately 45 million members including some of the most respected institutions in the country. |

Our services are sold on a subscription basis with contract terms generally ranging from one to five years. We provide a financial incentive to our customers and sales force to contract for three to five years. Historically, most of our customers contract for three year terms, except for our large partner (i.e., “OEM”) orders which are one year terms. At the end of the contract term we attempt to renew the subscription, again attempting to secure a three to five year term. Our customers pay us annually at the start of the subscription term and each succeeding year on the anniversary of the commencement of the service. We recognize revenue ratably on a monthly basis over the term of the subscription once service commences.

We attempt to grow the business by signing new customers to subscription services and/or selling new or higher volume services to existing customers (i.e., “upsell”) while retaining existing customers through renewal of their services.

Our total orders consist of orders from new customers, upsell to existing customers, plus renewal orders. Total orders may vary from quarter to quarter due to the timing of renewal orders which will fluctuate in amount due to timing and length of expiring subscription terms. Similarly, total new orders and upsell orders will fluctuate in amount due to term length.

To better understand new orders, management tracks the first year value of new orders as well as the total order value for the subscription term because total order value will exceed the first year value on multi-year orders. By segregating the first year value of new orders, we eliminate the fluctuation in total order amount caused by the dollar impact of multi-year contracts. We refer to this metric as New First Year Orders (“NFYOs”).

Our backlog consists of the total order value of contracted business that has not yet been recognized into revenue. Backlog is calculated by adding to the existing contracted order value the total value of all orders booked in the period (e.g., quarterly) less the value of revenue recognized for that period. Although orders are non-cancellable, occasionally we adjust backlog for customer bankruptcy or change of term, but these instances are rare and do not materially impact the backlog amount. The backlog will grow if the value of total orders added in a period exceeds the value of revenue recognized in that period. Conversely, the backlog amount will decline if revenue recognized exceeds the total order value added for the period. Although rare, a decline in backlog may result from fluctuations in total orders caused by timing of renewal orders described above.

We retain approximately 90% of our recurring revenue on an annual basis. We calculate this percentage by comparing the annual recurring revenue to the annual recurring revenue plus annual revenue lost from cancelled subscriptions. Deferred revenue is the value of contracted business that has been paid but has not been recognized as revenue. See description of the components of the backlog following in Item 7 of this Form 10-K under the heading, “Backlog and Orders.”

18

Table of Contents

Our revenue growth is dependent on our ability to sell subscription services to new customers, upsell new services or increase volume with existing customers and retain existing customers by renewing their subscription services. Generally, if annual NFYOs exceed the annual value of cancelled subscriptions, revenue should grow. However, revenue growth may fluctuate due to timing of deployment of new services and subscription cancellations. For example, a new order reported in NFYOs in one quarter may not be deployed to the customer until the following quarter and therefore delay commencement of revenue recognition. Similarly, a cancellation of a contract with an expiration in the first month of a quarter will have a higher negative impact on revenue in the quarter than a contract of the same amount with an expiration in the last month of a quarter. The impact of these quarter to quarter fluctuations tends to diminish over annual periods making year over year quarterly revenue comparisons more indicative of revenue growth than sequential quarterly revenue comparisons.

Our operations and future prospects are further discussed throughout this “Management’s Discussion and Analysis of Financial Condition and Results of Operations” (“MD&A”).

There are no assurances we will be successful in our efforts to achieve continued growth. Our continued growth depends on the timely development and market acceptance of our products and services. See “Item 1A. Risk Factors” for more information on the risks relative to our operations and future prospects.

Revenue

Revenue increased by 5% in 2014 compared with 2013. Our revenue growth was driven by our successful subscription model that continues to yield steady additions to the subscriber base coupled with a high rate of renewing existing customers. Revenue growth in 2014 was slowed due to lower orders from our largest OEM partner, Google. Google email encryption orders were interrupted during their transition from Google Message Encryption to a new platform, Google Apps Message Encryption which began in 2013 and was not completed until October of 2014. Due to our subscription model, where we defer and spread revenue ratably over the term on of the contract (OEM contracts are 1-year terms), most of the negative revenue impact from the order interruption was felt in 2014. With the completion of the transition in October of 2014, we expect to see Google order volume begin to increase in 2015 and related revenue begin to improve in the second half of 2015 and into 2016.

Critical Accounting Policies and Estimates

In preparing our consolidated financial statements, we make estimates, assumptions and judgments that can have a significant impact on revenue, income from operations and net income, as well as the value of certain assets and liabilities on our consolidated balance sheet. The application of our critical accounting policies requires an evaluation of a number of complex criteria and significant accounting judgments by us. Management bases its estimates on historical experience and on various other assumptions that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities. We evaluate our estimates on a regular basis and make changes accordingly. Senior management has discussed the development, selection and disclosure of these estimates with the Audit Committee of our Board of Directors. Actual results may materially differ from these estimates under different assumptions or conditions. If actual results were to differ from these estimates materially, the resulting changes could have a material adverse effect on our consolidated financial statements.

We consider accounting policies to be critical when they require us to make assumptions about matters that are highly uncertain at the time the accounting estimate is made and when different estimates that our management reasonably has used have a material effect on the presentation of our financial condition, changes in financial condition or results of operations. Management believes the following critical accounting policies reflect our more significant estimates and assumptions used in the preparation of the consolidated financial statements.

Our critical accounting policies included the following:

| • | Revenue recognition |

| • | Income taxes |

| • | Valuation of goodwill and other intangible assets |

| • | Stock-based compensation costs |

19

Table of Contents

For additional discussion of the Company’s significant accounting policies, refer to Note 2 to our consolidated financial statements.

Revenue Recognition

We develop, market, and support applications that connect, protect and deliver information in a secure manner. Our services can be placed into several key revenue categories where each category has similar revenue recognition traits: Email Encryption, DLP, and BYOD email subscription-based services, various transaction fees and related professional services. The majority of our revenues are generated through a combination of direct sales and a network of resellers and other distribution partners.

Under all product categories and distribution models, we recognize revenue after all of the following occur:

| • | persuasive evidence of an arrangement exists, |

| • | delivery has occurred or services have been rendered, |

| • | the price is fixed and determinable, and |

| • | collectability is reasonably assured. |

Discounts provided to customers are recorded as reductions in revenue.

Our Email Encryption, DLP, and BYOD email services are subscription-based. Providing these services includes delivering subscribed-for software and providing secure electronic communications and customer support throughout the subscription period. Our subscribers generally execute multiple-year contracts that are irrevocable and non-refundable in nature and require annual, up-front payments. Subscription fees received from customers are initially recorded as deferred revenue and then recognized as revenue ratably over the subscription period. We do not offer stand alone services. Further, any hardware provided as an incidental part of our services primarily includes manufacturer provided warranty provisions. We recorded no warranty expense in any of the presented periods.

Income Taxes