Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - TRANS WORLD CORP | Financial_Report.xls |

| EX-23.1 - EX-23.1 - TRANS WORLD CORP | a15-1787_1ex23d1.htm |

| EX-23.2 - EX-23.2 - TRANS WORLD CORP | a15-1787_1ex23d2.htm |

| EX-21.0 - EX-21.0 - TRANS WORLD CORP | a15-1787_1ex21d0.htm |

| EX-32.0 - EX-32.0 - TRANS WORLD CORP | a15-1787_1ex32d0.htm |

| EX-31.0 - EX-31.0 - TRANS WORLD CORP | a15-1787_1ex31d0.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2014

or

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to .

Commission File No.: 000-25244

TRANS WORLD CORPORATION

(Exact name of Registrant as specified in its charter)

|

Nevada |

|

13-3738518 |

|

|

|

|

|

545 Fifth Avenue, Suite 940 |

|

|

Registrant’s telephone number, including area code: (212) 983-3355

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.001 par value

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES o NO x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. YES o NO x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO o

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). YES x NO o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-X is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule12b-2 of the Exchange Act.

|

Large accelerated filer o |

Accelerated filer o |

Non-accelerated filer (Do not check if a smaller reporting company) o |

|

Smaller reporting company x |

|

|

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). YES o NO x

The aggregate market value of the Common Stock of the Registrant held by non-affiliates as of June 27, 2014, based upon the average bid and asked price of $3.30 as reported on the OTC Bulletin Board on that date, was $29,071,136.00. As of March 10, 2015, there were 8,821,205 shares of Common Stock of the Registrant deemed outstanding.

APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PRECEDING FIVE YEARS:

Indicate by check mark whether the Registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. YES o NO o

Documents incorporated by reference: None.

TRANS WORLD CORPORATION

FORM 1O-K

|

|

|

|

Page |

|

PART I. |

|

|

|

|

|

1 | ||

|

|

|

1 | |

|

|

|

2 | |

|

|

|

2 | |

|

|

|

2 | |

|

|

|

3 | |

|

|

|

3 | |

|

|

|

3 | |

|

|

|

3 | |

|

|

|

4 | |

|

|

|

4 | |

|

|

|

4 | |

|

|

|

5 | |

|

|

|

5 | |

|

|

|

6 | |

|

|

|

6 | |

|

|

|

7 | |

|

|

7 | ||

|

|

12 | ||

|

|

13 | ||

|

|

|

14 | |

|

|

|

14 | |

|

|

|

14 | |

|

|

14 |

TABLE OF CONTENTS

|

|

|

|

Page |

|

|

|

| |

|

|

14 | ||

|

|

15 | ||

|

|

|

15 | |

|

|

|

16 | |

|

|

|

16 | |

|

|

|

17 | |

|

|

|

Sales of Unregistered Equity Securities — Use of Proceeds from Registered Securities |

17 |

|

|

18 | ||

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

18 | |

|

|

|

18 | |

|

|

|

19 | |

|

|

|

19 | |

|

|

|

20 | |

|

|

|

21 | |

|

|

|

23 | |

|

|

|

24 | |

|

|

|

25 | |

|

|

25 | ||

|

|

27 | ||

|

|

Changes In and Disagreements with Accountants on Accounting and Financial Disclosure |

54 | |

|

|

54 | ||

|

|

55 |

TABLE OF CONTENTS

|

|

|

|

Page |

|

|

|

| |

|

|

55 | ||

|

|

|

57 | |

|

|

|

57 | |

|

|

|

57 | |

|

|

|

59 | |

|

|

|

60 | |

|

|

60 | ||

|

|

|

60 | |

|

|

|

63 | |

|

|

|

63 | |

|

|

|

64 | |

|

|

|

65 | |

|

|

|

66 | |

|

|

|

66 | |

|

|

|

66 | |

|

|

|

67 | |

|

|

|

67 | |

|

|

|

Potential Payments upon Termination of Employment or a Change in Control |

68 |

|

|

|

69 | |

|

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

70 | |

|

|

Certain Relationships and Related Transactions, and Director Independence |

71 | |

|

|

72 |

|

|

|

|

Page |

|

|

|

| |

|

|

73 | ||

|

|

| ||

|

73 | |||

|

77 | |||

|

27 | |||

The following discussion should be read in conjunction with the consolidated financial statements and notes thereto included elsewhere in this Annual Report on Form 10-K. This Annual Report on Form 10-K contains certain forward-looking statements including expectations of market conditions, challenges and plans, within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and is subject to the Safe Harbor provisions created by that statute. Reference is made to Part I, Item 1A “Risk Factors” and to Part II, Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Forward Looking Statements” for a discussion of the Registrant’s qualifications with respect to certain information presented in this Annual Report on Form 10-K.

All references to “$” or “USD” means U.S. dollars, “€” or “EUR” means euros and “CZK” means Czech korunas. Unless noted otherwise, all USD equivalents of foreign currency amounts are converted at the year-end exchange rates, of December 31, 2014.

General Development of Business

Trans World Corporation (hereinafter referred to as “we,” “us,” “Company,” or “TWC” or terms of similar import) was organized as a Nevada corporation in October 1993 for the acquisition, development and management of gaming establishments, to the extent permitted by applicable local laws, featuring live and mechanized gaming, including video gaming devices such as video poker machines, primarily in Louisiana. In 1998, we amended our operating strategy by shifting our focus to the casino market in Europe. Furthermore, as a means of diversification of our business, we have also expanded our growth strategy to develop and/or acquire small-to-mid-size four-star hotels of 80-400 rooms located in or near key metropolitan and resort areas of Europe, which may also include gaming operations.

Today, we operate three full-service casinos, one of which is attached to a complementary full-service hotel, the Hotel Savannah and Spa, referred to jointly herein as the “Route 59 Complex.” The three casinos are in the Czech Republic, located in Ceska Kubice (“Ceska”), Hate (“Route 59”), and Dolni Dvoriste (“Route 55”). The Czech casinos, which conduct business under our registered brand name, American Chance Casinos (“ACC”), are situated at border locations and draw the majority of their customers from Germany and Austria. Each of the casinos has a distinctive theme, portraying recognizable American design: Frank Lloyd-Wright-inspired “Organic Modern” in the 1930’s for Ceska; New Orleans in the 1920’s for Route 59; and Miami Beach “Streamline Moderne” in the early 1950’s for Route 55. ACC’s operating strategy centers on differentiating its products and service offerings from its direct competitors, the very formal German and Austrian casinos in our market areas, and as a result, management has strived to create gaming environments with casual and exciting atmospheres, emphasizing entertainment and state-of-the-art equipment. Further, as part of the ACC operating formula, our management endeavors to uphold the integrity and professionalism of our operations as a means to dispel any concerns that customers and governments might have about gambling.

In addition to the above gaming operations, the Route 59 Complex includes a 77-room, four-star deluxe hotel, the Hotel Savannah, which is physically connected to our Route 59 casino in Hate, and a full-service spa, the Spa at Savannah (the “Spa”), which is operated by an independent contractor and is attached to the hotel. The hotel features eight banquet halls for meetings and special events as well as a full-service restaurant and bar.

Effective November 28, 2013, in order to reflect the Company’s industry diversification, we changed the name of our primary Czech operating subsidiary, American Chance Casinos a.s., to “Trans World Hotels & Entertainment, a.s.” (“TWH&E”), while still operating our casinos under the ACC brand, without interruption. Effective January 1, 2014, in the final stage of consolidation, Trans World Hotels k.s., which owned the Hotel Savannah and the Spa, was merged into TWH&E.

On September 10, 2014, TWC, through its Czech subsidiary, TWH&E, acquired all of the partnership interests of a private family partnership that owned the Hotel Columbus, a four-star, 117-room hotel (the “Hotel Columbus”) located in Seligenstadt, near Frankfurt, Germany, for approximately $6.9 million, excluding transfer taxes and closing costs. Although the transaction closed, and TWH&E acquired the Hotel Columbus on September 10, 2014, the signing parties agreed to set the acquisition date retroactive to September 1, 2014, which had no impact on the purchase price. The Hotel Columbus features five meeting rooms, a restaurant and separate breakfast room, each with its own kitchen, two bars, a 32-space parking garage and 27 surface lot parking places, including a

satellite parking area located across the street from the Hotel. See also Note 13 - “Acquisition and Purchase Price Allocation” of the Notes to the Consolidated Financial Statements, included in this Annual Report in Part II, Item 8.

Following the Hotel Columbus acquisition, we determined that the Company had two reportable segments: a casino segment and a hotel segment. We have reflected such change in our financial reporting for the year ended December 31, 2014.

Although our principal executive offices are located in New York City, we have no operating presence in the United States. Information about our reporting units and geographic areas of operation is incorporated by reference from Note 1 of the Notes to Consolidated Financial Statements included in this Annual Report in Part II, Item 8.

Our corporate offices are located at 545 Fifth Avenue, Suite 940, New York, New York 10017, our telephone number is (212) 983-3355, our website is www.transwc.com and the ACC website is www.acc.cz. Neither website is a part of this Form 10-K.

TWC is engaged in the acquisition, development and management of niche casino operations in Europe, which feature gaming tables and mechanized gaming devices, such as video slot machines, as well as the acquisition, development and management of small-to-mid-size four-star hotels, which may include casino facilities. Our expansion into the hotel industry is founded on management’s belief that hotels in the small-to-mid-size class are complementary to our casino brand, that opportunities in one of these two industries often lead to, or are tied to, opportunities in the other industry, and that a more diversified portfolio of assets gives us greater stability and makes TWC more attractive to potential investors. Further, several of our top management executives have extensive experience in the hotel industry.

Market Overview and Competition

Historically, casinos in Germany and Austria have been characterized by formal atmospheres and an air of exclusivity, while our casinos offer a relaxed but exciting ambiance, which has become a desirable alternative for many of our patrons. Further, we have established ACC as a reputable casino company in the Czech Republic through our more than fifteen years of consistent high customer service standards, professionalism, and strict adherence to all local gaming regulations.

As of December 31, 2014, six casinos operate in direct competition with our Ceska casino. Each of our Route 59 and Route 55 casinos currently has two direct competitors. Some of these competitors are larger and have financial and/or other resources that are greater than ours.

While we do not consider our gaming business to be seasonal, it is occasionally impacted by extreme weather conditions and major sporting events, such as the Football (i.e., soccer) World Cup and the (Football) Euro Cup, that keep potential customers from visiting our casinos. See also Item 1A “Risk Factors — Climate Impact.”

We compete for guests based primarily on brand name recognition and reputation, location, customer satisfaction, quality of service, amenities, quality of the gaming experience, quality of our accommodations, room rates, security and the ability to earn and redeem loyalty program points. We believe that increased gaming in other locations in or near the markets areas in which we operate, and the increase in popularity of internet gaming, could create additional competition for us and could adversely affect our operations and development plans. Further, the gaming industry in Eastern Europe faces competition from a variety of sources for discretionary consumer spending, including spectator sports and other entertainment and gaming options. Competitive gaming activities include traditional casinos, video lottery terminals, state-sponsored lotteries and other forms of legalized gaming. Additionally, internet gaming and wagering is growing rapidly and affecting competition in our industry. We anticipate competition in this area will become more intense as new web-based ventures enter the industry.

Costs and Effects of Environmental Compliance

We incurred no material costs or effects of environmental compliance for the year ended December 31, 2014. See also Part I, Item 1A “Risks Factors — Climate Impact.”

The Company does not engage in research and development other than internal market research for general business development, and does not account for research expenditures separately under generally accepted accounting principles and did not incur any separate research and development expense for 2014 or 2013.

Available Information - Internet Access

We are a “smaller reporting company” under the rules of the Securities and Exchange Commission (“SEC”). Copies of our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 (the “Exchange Act”) are available free of charge on or through our website (www.transwc.com) as soon as reasonably practicable after we electronically file the material with the Securities and Exchange Commission. In addition, the public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an Internet site (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers (including the Company) that file electronically with the SEC.

As a complement to our gaming operations, in January 2009, we built and opened Hotel Savannah, a 77-room, European four-star deluxe hotel, the first constructed hotel for the Company. In conjunction with opening the hotel, we also launched a full-service spa, the Spa, which is attached to the hotel. The Spa features a large indoor pool and Ayurvedic massage therapy, which is sub-contracted to a local operator. Hotel Savannah, which features eight banquet halls for meetings and conventions, is connected to our Route 59 casino with the hotel restaurant linking the two buildings. The combined operation of the hotel and spa is intended to and has proven to benefit Route 59 by attracting additional business to the casino, contributing incremental cash, and enhancing the Company’s overall results.

Our free-standing casinos each offer free parking, a restaurant, lounge areas and multiple bars. We own the land and buildings that comprise our casino and hotel assets. Each of our casinos is within an hour’s drive from a major city in either Germany (i.e., Regensburg) or Austria (i.e., Vienna and Linz).

On November 23, 2011, TWC purchased the Ceska casino building, associated land and an adjacent outbuilding and related plot from the town of Ceska Kubice, from which TWC had been renting the facilities. The combined price was 11.6 million CZK, or at that time, $612,000. In conjunction with this purchase, TWC was granted by the township of Ceska Kubice a three-year municipal loan of CZK 9.0 million, or $395,000. The loan, which was due to mature on November 23, 2014, was paid in full on January 16, 2014. The acquisition allowed us to undertake much needed capital improvements to the building, as competition in the Ceska area has increased dramatically in recent years. By the end of 2014, we had invested in total approximately CZK 48.6 million, or $2.1 million, into our expansion and renovation program for the Ceska Casino. The first phase expanded the Ceska facility by connecting the existing casino with an annex building, in which five private, luxurious guest-sleeping rooms, equipped with full amenities, used primarily as courtesy accommodations for our VIP clients; administrative offices; and storage areas are now located. Additionally, the expansion phase encompassed the enlargement of the restaurant and the entertainment facility and construction of a new, expansive reception area. The project was planned in such a way so as to avoid any disruption to the casino’s operations. As a result of the completion of the first phase of the project, the casino increased its real estate footprint by nearly 60%, to 13,644 square feet of space, or 1,268 square meters, not including an expanded outdoor parking lot. Ceska has now surpassed Route 55 as the largest casino property we own. The casino held a gala re-launch on June 29, 2013. The second phase, consisting mainly of renovation of older parts of the casino, with a budget of CZK 4.6 million, or approximately $202,000, was completed at the end of the first quarter of 2014. It encompassed additional renovation and reconfiguration of the existing slot areas. The remodeled slot room permitted the addition of 20 video slot machines, which were added on

September 1, 2013. The total cost of the casino purchase, facility expansion and renovation has been funded by excess cash flow from the Company’s operations.

Our newly-expanded and renovated Ceska casino now has a Frank Lloyd-Wright-inspired “Organic Modern” theme of the 1930’s. As of February 28, 2015, Ceska had 15 gaming tables, including six card tables, seven roulette tables, and a 10-position, Slingshot, multi-win roulette table. The casino also features 100 video slot machines. The property also features a dedicated stage area, for shows and live performances, with a separate dining facility and five private, luxurious guest-sleeping rooms, equipped with full amenities. The address of our Ceska casino is Ceska Kubice 64, Ceska Kubice 345 32, Czech Republic.

As of February 28, 2015, our Route 59 casino, which has a New Orleans in the 1920’s theme, operated 21 gaming tables, consisting of ten card tables, ten roulette tables, and a 16-position, Slingshot multi-win roulette table, as well as 126 video slot machines. In March 2009, a reception area in the corridor between the casino and adjacent Hotel Savannah was opened to permit easier access between the two operations. Route 59 is located at 199 American Way, Hate-Chvalovice, Znojmo 669 02.

Our Route 55 casino features a Miami Beach “Streamline Moderne” style, reminiscent of Miami Beach in the early 1950’s. As of February 28, 2015, the two-story casino offered 23 tables, including 12 card tables, 10 roulette tables, a 16-position, Slingshot multi-win roulette table, as well as 138 video slot machines. On the mezzanine level, the casino offers an Italian restaurant, an open buffet area, a VIP lounge, a VIP gaming room, and three private, luxurious guest-sleeping rooms, equipped with full amenities. Similar to the five guest rooms at Ceska, these rooms, when not used as courtesy accommodations for our valuable players and guests, can be rented out. Route 55 is located at Grenzubergang Wullowitz, Dolni Dvoriste 382 72, Czech Republic.

On September 1, 2014, we acquired the Hotel Columbus, a four-star 117-room hotel, located in Seligenstadt, approximately 25 minutes equidistant from Frankfurt city center, Germany and the Frankfurt international airport. The Hotel Columbus features five meeting rooms, a restaurant and separate breakfast room, each with its own kitchen, two bars, a 32-space parking garage and 27 surface lot parking places, including a satellite parking area located across the street from the Hotel.

In the highly competitive gaming and hospitality industries in which we operate, our trade names and logos are important to the success of our business. All of our casinos operate under the trade name “American Chance Casinos” and feature the radiating crown logo, which we believe has become synonymous in our markets with our reputation for excellence in service, casual fun and state-of-the-art equipment. In addition, the Savannah Deluxe Hotel flowering tree logo has come to represent luxury and convenience for our overnight guests at our Route 59 casino while the TWC crowned globe logo reflects the Company’s growing international presence. The Company also maintains separate websites for our casinos and two hotels that provide the user with updated information, and for the hotels, the ability to book online.

Our current operations are predominantly in the gaming industry and located primarily in the Czech Republic. In an effort to diversify the Company’s operations, our senior corporate management, composed of several individuals who have extensive experience in the hotel industry, continues to explore ways to expand the Company’s operations through the acquisition and/or development of new, complementary gaming and non-gaming business units, while continuing to maximize the potential of the Company’s existing operations. In line with this growth and diversification strategy, we are seeking to enhance our operations through the addition of casinos as well as other integrated operations, as was done for Route 59 with the addition of Hotel Savannah and the Spa, or stand-alone operations, such our recently acquired Hotel Columbus.

During the year ended December 31, 2014, we maintained and enhanced our marketing and promotional programs for our casinos, focusing primarily on internal and customer-oriented loyalty reward programs. In 2014, we strove to offer higher-value amenities, more giveaways and to provide live entertainment, in an ongoing effort to secure and enhance our competitive position in the markets that we serve. The casinos’ event calendars

concentrated on key, player-tested, popular events and holidays, while simultaneously focusing on higher player-incentive games to retain existing players. In addition, we continued our sponsorships of several regional athletic teams and were a benefactor in a number of community and social projects during the year as a way to further promote our image and positive contribution to the communities in which we operate. We also continued our popular, cultural-themed and holiday-related parties, which feature live entertainment, raffles and complimentary grand buffets. Further, we aggressively targeted key cities in our media campaigns, most notably Vienna, Linz and Regensburg and the areas surrounding these cities. With respect to Hotel Columbus, our new hotel operation in Seligenstadt, Germany, we focused our sales efforts to draw corporate business from Frankfurt, which is the nearest metropolitan area to our hotel and worked to cultivate the existing and new local business relationships.

We are subject to numerous foreign federal and local government laws and regulations, including those relating to the operation of a casino business, the operation of our hotel segment, the preparation and sale of food and beverages, building and zoning requirements, data privacy and general business license and permit requirements, in the various jurisdictions in which we manage and own properties. Our ability to acquire and/or develop new casino and/or hotel properties and to remodel, refurbish or add to existing properties is also dependent on obtaining permits from local authorities. We are also subject to laws governing our relationships with employees, including minimum wage requirements, overtime, working conditions, hiring and firing, non-discrimination for disabilities and other individual characteristics, work permits and benefit offerings. Compliance with these various laws and regulations can affect the revenues and profits of the properties we own and could adversely affect our operations. We believe that our businesses are conducted in compliance with applicable laws and regulations.

Our casino operations are also subject to extensive regulation under the laws, rules and regulations of the jurisdiction where each is located. These laws, rules and regulations generally concern the responsibility, financial stability and character of the owners, managers, and persons with financial interests in the gaming operations. Violations of laws in one jurisdiction could result in disciplinary action in other jurisdictions. The Company must also pay gaming and income taxes and conduct its operations so as to maintain its gaming licenses and to maintain its good relations with our regulators that will help us renew our gaming licenses at the appropriate times. Gaming licenses and approvals, once obtained, can be suspended or revoked for a variety of reasons. We cannot assure you that we can obtain all required licenses and approvals on a timely basis or at all, or that, once obtained, the findings of suitability, licenses and approvals will not be suspended, conditioned, limited or revoked. If we ever are prohibited from operating our casinos or any other property we may own and operate in the future, we would, to the extent permitted by law, seek to recover our investment by selling the property affected, but there are no assurances that we would be able to recover its full value, nor can we assure you that legislative initiatives will not adversely affect our operations. In 1998, the Czech Republic House of Deputies passed an amendment to the gaming law, which restricted foreign ownership of casino licenses. In response, we restructured our Czech subsidiaries and legal entities to comply with the amendment and were subsequently granted 10-year gaming licenses or permits, which have since been renewed by the government of the Czech Republic for another 10-year term, expiring in 2018. These licenses cover all of the casinos we own in the Czech Republic. The permits are amended each time we add a new operating branch or unit. The no-cost permits are renewable by application and must be granted as long as the corporate casino operator meets the following conditions: (i) maintenance of the required basic capital, which, in our case, includes a gaming bond of CZK 22 million or approximately $1.0 million, for our primary operating subsidiary; (ii) be designated as a public or private stock company (using the Czech abbreviation “a.s.”); (iii) have executive board members of the Czech stock company who do not have criminal records; and (iv) have no overdue taxes. We have been and are currently in full compliance with all such conditions.

There can be no assurance that such licenses, approvals or findings of suitability will be obtained or will not be revoked, suspended or conditioned, or that we will be able to obtain the necessary approvals for our future activities.

Application of Future or Additional Regulatory Requirements

In the future, we may seek the necessary licenses, approvals and findings of suitability in other jurisdictions where the Company may conduct business. There is pending legislation before the Czech Parliament that may have significant impact on our operations, depending on the final outcome of that bill. See also, Part I, Item 1A. “Risk Factors — Potential changes in legislation and regulation of our operations.”

In August 2009, the Republic of Hungary awarded a Hungarian company, KC Bidding Kft. (“KCB”), in which we hold a 25% equity interest, the right to open a “Class I” casino in the administrative area of the Central-Transdanubian Region of Hungary, west of Budapest. A “Class I” casino is defined as a casino that operates a minimum of 100 gaming tables and 1,000 slot machines. With the award in hand, KCB, which is 75% owned by Vigotop Limited, a Cyprus-based company (“Vigotop”), then executed a concession contract with the Republic of Hungary on October 9, 2009. Subsequently, KCB founded a license concession company, SDI Europe Kft. (“SDI”), which is a wholly-owned subsidiary of KCB, for the purpose of operating the Class I casino. According to the terms of the award and once all regulatory requirements were met, the casino license was to have been granted for 20 years from the date of opening, which was to have occurred on or before January 1, 2014, with one, 10-year extension option. During this time, no additional casino licenses would have been granted by the Hungarian government in this region.

Since January 12, 2011, the date KCB received written notice of the cancellation by the Ministry for the National Economy of Hungary (the “MOE”), there have been several lawsuits and countersuits initiated by the MOE and KCB, contesting the cancellation of the concession contract, which was signed on October 9, 2009, and alleged breaches of its terms. KCB’s suit against the government was ultimately dismissed by the court on procedural grounds, which left the MOE’s lawsuits against KCB for: (i) KCB’s alleged violation of the MOE’s periodic reporting requirements; and (ii) KCB’s alleged obligation to pay a termination penalty in conjunction with the MOE’s cancelation of KCB’s concession contract as the only remaining active court cases. Upon final resolution of the reporting violation case, the court will proceed with the MOE’s lawsuit against KCB regarding the concession contract cancelation fee, which was suspended pending the outcome of the reporting violation case.

In light of an existing agreement between TWC and Vigotop regarding the costs associated with the venture to obtain the casino license, the Company would not be liable for the cost of potentially adverse outcomes in the court cases that KCB is a party to. Consequently, TWC’s management believes that a negative outcome of the court cases would not materially affect the Company’s consolidated financial statements and/or results of operations.

Pursuant to Section 13(r) of the Exchange Act, if during 2014, TWC or any of its affiliates have engaged in certain transactions with Iran or with persons or entities designated under certain executive orders, we would be required to disclose information regarding such transactions in our Annual Report as required under Section 219 of the Iran Threat Reduction and Syria Human Rights Act of 2012, or ITRA. During 2014 and 2013, the Company did not engage in any of the law’s enumerated transactions with Iran or with persons or entities related to Iran.

Value Added Taxes

In conformity with the European Union (“EU”) taxation legislation, the Czech Republic’s value added tax (“VAT”) has gradually increased from 5%, when that country joined the EU in 2004, to 21%, the effective rate since 2013. Unlike in other industries, VATs are not recoverable for gaming operations. The recoverable VAT under the Hotel Savannah and Hotel Columbus operations was not material for the years ended December 31, 2014 and 2013, respectively.

Gaming Taxes

In December 2011, the Czech parliament passed sweeping gaming tax legislation, which was then signed by the Czech president into law. The new gaming tax (“New Gaming Tax”) law took effect beginning January 1, 2012. The changes in the gaming tax law are summarized below:

|

|

|

Gaming Tax Law (Effective January 1, 2012) |

|

Live Games |

|

20% Gaming Tax from revenue earned from live games (70% of tax paid to the federal government; 30% paid to the local municipality). |

|

|

|

|

|

Slots |

|

20% Gaming Tax from revenue earned from slot games (20% of tax paid to the federal government; 80% paid to the local municipality); CZK 55 (or approximately $3.00) Gaming Tax per Slot Machine, per Day (paid to the federal government). |

|

|

|

|

|

Net Income |

|

19% corporate income tax on adjusted net income earned in the Czech Republic, net of exemptions (paid to the federal government). |

The New Gaming Tax is payable by the 25th day following the end of each calendar quarter, while corporate income tax obligation is paid by June 30th of the subsequent year. The Company is also required to make estimated quarterly income tax payments since the third quarter of 2013. TWC is current on all of its Czech tax payments at December 31, 2014 and through the date of this report.

TWC’s gaming-related taxes and fees for the years ended December 31, 2014 and 2013 are summarized in the following table:

|

|

|

For the Year Ended |

| ||||

|

(amounts in thousands) |

|

2014 |

|

2013 |

| ||

|

|

|

|

|

|

| ||

|

Gaming revenues (excl. ancillary revenues) |

|

$ |

34,024 |

|

$ |

33,203 |

|

|

|

|

|

|

|

| ||

|

Gaming taxes |

|

$ |

7,160 |

|

$ |

6,975 |

|

|

Gaming taxes as % of gaming revenues (above) |

|

21.0 |

% |

21.0 |

% | ||

Corporate Income Taxes

Effective January 1, 2012, in conjunction with the changes to gaming taxes, the Czech government instituted an effective corporate income tax, currently 19.0%, on all income, including gaming income, which prior to the law changes were subject only to gaming taxes. For the year ended December 31, 2014, the Company incurred an estimated income tax expense of $1,308,000, inclusive of a past year income tax credit of $10,000 and a deferred income tax expense of $161,000 related to adjustments for foreign book tax differences on fixed assets. The prior year income tax expense of $1,056,000 included a past year income tax credit of $7,000.

As of December 31, 2014, we had a total of 502 employees. As of year-end 2014, we had 100 full-time employees in our casino in Ceska Kubice, 151 at Route 59, 148 at Route 55, 47 at Hotel Savannah and the Spa, 34 at Hotel Columbus, 17 in our shared services offices located above the Ceska casino, and five in the Company’s headquarters in New York. None of our employees are represented by a union nor are we a party to any labor contract. We believe that our employee relations are excellent.

We have described below what we currently believe to be the material risks and uncertainties in our business.

Before making an investment decision with respect to our Common Stock, you should carefully consider the risks and uncertainties described below, together with all of the other information included or incorporated by reference in this Annual Report on Form 10-K. We also face other risks and uncertainties beyond what is described below. Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial may also adversely affect our business. Further, past financial performance may not be a reliable indication of future performance and historical trends should not be used to anticipate results or trends in future periods. This Annual Report on Form 10-K is qualified in its entirety by these risk factors. If any of the following risks actually occur, our business, financial condition, results of operations and prospects could be materially and adversely affected. If this were to happen, the value of our Common Stock could decline significantly. You could lose all or part of your investment.

General economic trends are unfavorable

The recent worldwide economic downturn in 2009 and the anemic economic growth that followed since, as well as the current debt crisis in the EU, had, has and may, in the future, continue to have a negative impact on our financial performance. Lingering adverse conditions in local, regional, national and global markets could negatively impact our operations in the future. During periods of economic contraction like that recently experienced, certain costs can remain fixed or even increase, while revenues decline. The gaming services we provide are similar to other leisure activities in that they depend on personal discretionary expenditures, which are likely to decline during economic downturns. Continued adverse developments affecting economies throughout the world, and particularly in Europe, including a general tightening of the availability of credit, unemployment, increasing energy costs, deflation, political or economic turmoil, government debt crises, acts of war or terrorism, natural disasters, declining consumer confidence or significant declines in world stock markets could lead to a further reduction in discretionary spending on entertainment and leisure activities, which could adversely affect our business, financial condition,

results of operations and prospects. In some cases, even the perception of an impending economic downturn or the continuation of a recessionary climate can be enough to discourage consumers from spending on leisure activities. We cannot predict at this time what the full effect and extent of the global recession will be and the subsequent extended period of slow-growth in Europe on our business, financial condition, or results of operations.

We face significant competition

We operate in a highly competitive industry with a large number of participants, many of which have financial and other resources that are greater than ours. The gaming industry faces competition from a variety of sources for discretionary consumer spending including spectator sports and other entertainment and gaming options, as well as home entertainment alternatives. Competitive gaming activities include traditional casinos, video lottery terminals, internet gaming, state-sponsored lotteries and other forms of legalized gaming in the Czech Republic, Germany, Austria and in other jurisdictions.

Legalized gaming is currently permitted in various forms in the Czech Republic, Austria and Germany. Moreover, established gaming jurisdictions could award additional gaming licenses or permit the expansion of existing gaming operations. If additional gaming opportunities become available near our operations, such gaming opportunities could have a material, adverse impact on our business, financial condition, results of operations and prospects.

Additionally, internet gaming and wagering is growing rapidly and may be affecting competition in our industry. Web-based businesses may offer consumers a wide variety of events to wager on, including other games, racetracks and sporting events. Unlike most web-based gaming companies, we pay taxes in the jurisdictions in which we operate and our operations require ongoing capital expenditures for both their continued smooth operations, maintenance, renovation and growth. We could also face significantly greater costs in operating our business compared to these “virtual” internet gaming companies. We cannot offer the same number of gaming options as internet-based gaming companies. Many internet-based gaming companies are located off-shore and avoid regulation under applicable Czech laws. These companies may divert wagering dollars from live wagering venues, such as our casinos. The continued growth and success of these on-line ventures could have a material, adverse impact on our business, financial condition, results of operations and prospects.

Our principal competitors are other operators of full service and select service properties, including other major hospitality chains with well-established and recognized brands. We also compete against smaller hotel chains and independent and local hotel owners and operators. If we are unable to compete successfully, our revenues or profits may decline or our ability to maintain or increase our market share may be diminished. We compete for guests based primarily on location, customer satisfaction, room rates, quality of service, amenities, and quality of accommodations. Most of our competitors are larger than we are based on the number of properties they manage, franchise or own or based on the number of rooms or geographic locations where they operate. Many of our competitors also have recognizable brands, participate with online travel merchants and have a large number of members participating in their guest loyalty programs which may enable them to attract more customers and more effectively retain such guests. Our competitors generally also have greater financial and marketing resources than we do, which could allow them to improve their properties and expand and improve their marketing efforts in ways that could affect our ability to compete for guests effectively.

We are subject to the business, financial and operating risks inherent to the hospitality industry

Our hotel segment is subject to a number of business, financial and operating risks inherent to the hospitality industry, including:

· changes in taxes and governmental regulations that influence or set wages, prices, interest rates or construction and maintenance procedures and costs;

· the costs and administrative burdens associated with complying with applicable laws and regulations;

· the costs or desirability of complying with local practices and customs;

· the availability and cost of capital necessary for us to fund acquisitions, investments, capital expenditures and service debt obligations;

· delays in or cancellations of planned or future acquisition or development projects;

· foreign exchange rate fluctuations;

· changes in operating costs, including, but not limited to, energy, food, workers’ compensation, benefits, insurance and unanticipated costs resulting from statutory requirements and/or force majeure events;

· increases in cost for healthcare coverage for employees and potential government regulation in respect of health coverage;

· shortages of labor or labor disruptions;

· shortages of desirable locations for acquisition or development;

· unrealistic purchase prices set by sellers; and,

· the ability of third-party internet travel intermediaries to attract customers for our properties.

Any of these factors could limit or reduce the prices we charge for our hospitality products or services, including the rates our properties charge for rooms. These factors can also increase our costs or affect our ability to develop or acquire new properties or maintain and operate our existing properties. As a result, any of these factors can reduce our profits and limit our opportunities for growth.

Fluctuations in currency exchange rates could adversely affect our business

Our facilities in the Czech Republic represent a significant portion of our business, and the revenue generated is generally denominated in euros and the expenses incurred by these facilities are largely denominated in CZK. The potential depreciation in the value of either of these currencies against the USD would adversely impact the revenue and operating profit from our operations when translated into USD, which would have a commensurate effect on our consolidated results of operations. (See also “Item 7A. Quantitative and Qualitative Disclosure about Market Risk — Foreign Currency Exchange Rate Risk”). We do not currently hedge our exposure to fluctuations of these foreign currencies, and there is no guarantee that we will be able to successfully hedge any future foreign currency exposure, if we subsequently choose to do so in the future.

Need to diversify

At this time, our operations are primarily located in the Czech Republic. Therefore, any future adverse legislation in the Czech Republic may have an adverse impact on our operations, financial results, financial condition and prospects. To counteract this risk, we acquired the Hotel Columbus in Seligenstadt, Germany, in September 2014 and are currently seeking to develop and/or acquire additional interests in gaming operations and/or hotels in other European countries. However, there can be no assurance that we will be able to develop or acquire such new operations in the future.

Need for additional financing

Although we have achieved net income for the twelfth consecutive year, pursuant to our growth strategies, we may require additional debt and/or equity financing for the acquisition and development of new businesses or business units. We may also need to access the capital markets or otherwise obtain additional funds to finance acquisitions, the continuing maintenance, renovation, or re-theming of currently owned facilities or the development of new operations (such as Hotel Savannah). There is no guarantee that we will be able to obtain such financing or funds in the future on favorable terms to us, or at all.

Licensing and regulation

Our gaming operations are subject to regulation by each federal and local jurisdiction in which we operate. Each of our officers may be subject to strict scrutiny and approval from the gaming commission or other regulatory body of each jurisdiction in which we conduct gaming operations. Furthermore, the operations of our casinos are contingent upon maintaining all necessary regulatory licenses, permits, approvals, registrations, findings of suitability, orders and authorizations. The laws, regulations and ordinances requiring these licenses, permits and other approvals generally relate to the operations of the casinos, the payment of taxes, the responsibility, financial stability and character of the owners and managers of gaming operations, as well as persons financially interested or involved in gaming operations. All of our casinos are duly licensed by the Ministry of Finance of the Czech Republic, and we are subject to ongoing regulation to maintain these operations.

Czech regulatory authorities have broad powers to request detailed financial and other information, to limit, condition, suspend or revoke a registration, gaming license or related approval and to approve changes in our

operations. The suspension or revocation of any license which may be granted to us could significantly harm our business, financial condition, results of operations and prospects. Any change in the laws, regulations or licenses applicable to our business or a violation of any current or future laws or regulations applicable to our business or gaming licenses could require us to make substantial expenditures or could otherwise negatively affect our gaming operations.

Potential changes in legislation and regulation of our operations

Laws and regulations governing the conduct of gaming activities and the obligations of gaming companies in any jurisdiction in which we have or in the future may have gaming operations are subject to change and could impose additional operating, financial or other burdens on the way we conduct our business.

Moreover, legislation to prohibit, limit, or add burdens to our business may be introduced in the future in the Czech Republic or elsewhere where gaming has been legalized. In addition, from time to time, legislators and special interest groups (which may include our competitors) have proposed legislation that would expand, restrict or prevent gaming operations or which may otherwise adversely impact our operations in the jurisdictions in which we operate. Any expansion of gaming or restriction on or prohibition of our gaming operations, increase in gaming taxes, or enactment of other adverse regulatory changes could have a material adverse effect on our business, financial condition, operating results and prospects.

Gaming legislation is introduced in the Czech Parliament from time to time. In October 2014, the Czech Ministry of Finance (“MOF”), the national governmental authority that regulates gambling in the Czech Republic, introduced proposed legislation that would, if approved, among other things, limit the number of gambling establishments, limit the number of slot machines, shorten license periods, require security bonds for each casino operation by location, limit betting amounts and the amount of losses per hour and per month for players, limit the duration of each individual’s playtime and the pace of certain live games, prohibit the serving of complimentary food, beverage or cigarettes, link slot machines to an MOF database, create an online database of gamblers that is linked to the MOF, and give localities more power over gaming establishments. The MOF has also stated publicly that it is contemplating the introduction of a new tax law that could increase gaming taxes. The draft law is now subject to comment by interested parties, review by other government agencies, parliamentary procedure that could include amendments that could materially change the proposal, and amendment and/or ratification in the Czech Senate, all of which is not expected to occur until the end of 2015. Because the parameters and effects of this current proposed legislation are still speculative at this point in time, the Company cannot predict what the ultimate statute will contain, whether it will be passed in the Czech Parliament, or whether it will be signed by the Czech President. Therefore, we cannot, as of the date of this report, specifically predict the proposed legislation and its effect on the results of operations or financial condition of the Company. However, if it is adopted in its current form, it would have a material adverse effect on our results of operation and business prospects.

Taxation of gaming operations

Gaming operators are typically subject to significant taxes, which may increase at any time. Any material increase in these taxes or fees would adversely affect our business, results of operations, financial condition and prospects. The Czech Republic currently has a number of laws related to various taxes imposed by governmental authorities. Applicable taxes include VAT, gaming tax, corporate income tax, and payroll (social) taxes. In December 2011, the Czech government passed sweeping gaming tax legislation that became effective in 2012. In this new tax law, the government eliminated the “charity contribution tax” scheme and, in lieu of it, changed the existing revenue-based, tiered rate gaming tax structure to a flat 20% gaming tax on all gaming revenues, plus an applicable corporate income tax (19%) on adjusted net income (derived from any revenue sources, including gaming). These tax law changes have negatively and materially impacted, and will continue to negatively impact, our results of operations since 2012. These tax law changes, together with other legal compliance areas (for example, customs and currency control matters) are subject to review and investigation by a number of different Czech governmental authorities, which are authorized by law to impose fines, penalties and interest charges. These reviews may create additional tax risks that, if applied to TWC, could have a material adverse effect on our business, results of operations, financial condition and prospects.

Dependence upon key personnel

Our ability to successfully implement our strategy of expansion, manage the existing casinos, and maintain a competitive position will continue to depend, in large part, on the ability of Mr. Rami S. Ramadan, the Company’s President, Chief Executive Officer (“CEO”), and Chief Financial Officer (“CFO”). The Company is also dependent upon other key employees, casino managers, and consultants, whom we retain from time to time.

International activities

Our operations are completely outside of the United States. Operating internationally involves additional risks including, but not limited to currency exchange rates, different legal or regulatory environments, political and economic risks relating to the stability or predictability of foreign governments, differences in the manner in which different cultures do business, difficulties in staffing and managing foreign operations, differences in financial reporting, operating difficulties, different types of criminal threats and other factors. The occurrence of any of these risks, if severe enough, could have a material adverse effect on our financial condition or results of operations.

Climate impact

The operations of our facilities are subject to disruptions or reduced patronage as a result of severe weather conditions, natural disasters and other casualty events, including loss of service due to casualty, forces of nature, mechanical or electrical or telecommunications failure, traffic and road conditions, extended or extraordinary maintenance, flood, wind, snow, ice or other severe weather conditions. As the majority of our clientele travel from German and Austrian border regions by automobile, we are highly dependent on the volume and frequency of these players’ visitations, which impact our operating revenues. Inclement weather conditions on the roads to our casinos can serve to drastically reduce the number of visitations, which did in fact occur in the first and second quarter of 2013. On the other hand, warm and favorable outdoor weather can also divert players to alternative activities, such as family outings. The frequency and strength of any of these aforementioned climate conditions could have a material adverse effect on our business, results of operations, and prospects.

Liability insurance

We may not have sufficient insurance coverage in the event of a catastrophic property or casualty loss. We may also suffer disruption of our business in the event of a terrorist attack (at our premises or elsewhere), or other catastrophic property, or casualty loss, or be subject to claims by third parties injured or harmed while visiting our locations. While we currently carry adequate general liability insurance and business interruption insurance, such insurance may not be sufficient to cover all losses in such event.

No dividends

We have not paid any dividends to date on our Common Stock. Currently, our plan is to retain future earnings, if and when generated, for investment in our current operations and for future project developments. Any future determination to pay dividends will be at the discretion of our board of directors and will depend on our financial condition, capital requirements, restrictions contained in current or future financing instruments and such other factors as our board of directors deems relevant. See the “Dividend” section of Item 5. “Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities — Share Repurchase.”

Dilutive effect of options, warrants, restricted stock and deferred compensation stock

As of February 28, 2015, there were options outstanding to purchase 585,125 shares of our Common Stock, plus 305,482 shares issuable under the Company’s Deferred Compensation Plan and 75,000 shares of performance-tied restricted stock, which, if all were vested and exercised, would represent 9.9% of the 9,786,812 fully-diluted shares. The issuance of such securities would have a dilutive effect on any earnings per share that we may generate when the earnings per share are evaluated on a fully diluted basis.

Possible adverse effect of issuance of preferred stock

Our Articles of Incorporation authorize the issuance of four million shares of “blank check” preferred stock, with designations, rights and preferences to be determined from time to time by our Board of Directors. Accordingly, our Board of Directors is empowered, without further stockholder approval, to issue preferred stock with dividend, liquidation, conversion, voting or other rights that could adversely affect the dividend rights and/or voting power or other rights of the holders of the Common Stock. In the event of issuance, the preferred stock could be used, under certain circumstances, as a method of discouraging, delaying or preventing a change in control of the Company. Our Board of Directors has no current plans to issue any shares of preferred stock. However, there can be no assurance that preferred stock will not be issued at some time in the future.

Failure to maintain the security of personally identifiable and other information, non-compliance with our contractual or other legal obligations regarding such information, or a violation of the Company’s privacy and security policies with respect to such information

In connection with our business, we collect and retain large volumes of certain types of personally identifiable and other information pertaining to our customers, stockholders and employees. Such information includes, but is not limited to, large volumes of customer identity and credit and payment card information. The legal, regulatory and contractual environment surrounding information security and privacy is constantly evolving and under increasing attack by cyber-criminals in the U.S. and Europe. A significant actual or potential theft, loss, fraudulent use or misuse of customer, employee or our corporate data by cybercrime or otherwise, non-compliance with our contractual or other legal obligations regarding such data, or a violation of our privacy and security policies with respect to such data could adversely impact our reputation, business integrity, and ultimately, our business prospects, and could result in fines, litigation or regulatory action against us.

Item 1B. Unresolved Staff Comments.

None.

A summary of our properties as of February 28, 2015 is presented below in square feet and in square meters:

|

Property Name |

|

City/Town |

|

Country |

|

Owned/Leased |

|

Square Feet |

|

Square Meters |

|

|

TWC Corporate Offices |

|

New York |

|

United States |

|

Leased |

|

1,915 |

|

178 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ceska (1) |

|

Ceska Kubice |

|

Czech Republic |

|

|

|

|

|

|

|

|

· Total Plot #1 - Casino & Land |

|

|

|

|

|

Owned |

|

40,264 |

|

3,742 |

|

|

· Casino Building (footprint) |

|

|

|

|

|

|

|

25,469 |

|

2,367 |

|

|

· Parking & Landscape |

|

|

|

|

|

|

|

6,596 |

|

613 |

|

|

· Vacant Land |

|

|

|

|

|

|

|

8,199 |

|

762 |

|

|

· Parking & Landscape |

|

|

|

|

|

Leased |

|

64,366 |

|

5,982 |

|

|

· Staff Housing |

|

|

|

|

|

Leased |

|

15,871 |

|

1,475 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Folmova Vacant Land (1) |

|

Folmova |

|

Czech Republic |

|

Owned |

|

210,175 |

|

19,533 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Route 55 (1) |

|

Dolni Dvoriste |

|

Czech Republic |

|

|

|

|

|

|

|

|

· Total Plot #1 - Casino & Land |

|

|

|

|

|

Owned |

|

365,410 |

|

33,960 |

|

|

· Casino Building (footprint) |

|

|

|

|

|

|

|

20,315 |

|

1,888 |

|

|

· Total Plot #2 - Vacant Land (total 14,497 m(2)) |

|

|

|

|

|

50% Owned |

|

77,999 |

|

7,249 |

|

|

· 50% owned by Czech State |

|

|

|

|

|

|

|

|

|

|

|

|

· Total Plot #3 - Vacant Land |

|

|

|

|

|

Owned |

|

352,153 |

|

32,728 |

|

|

· Parking & Landscape |

|

|

|

|

|

Owned |

|

176,604 |

|

16,413 |

|

|

· Staff Housing I |

|

|

|

|

|

Leased |

|

4,756 |

|

442 |

|

|

· Staff Housing II |

|

|

|

|

|

Leased |

|

6,155 |

|

572 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Route 59 Complex (1) |

|

Hate/Znojmo |

|

Czech Republic |

|

|

|

|

|

|

|

|

· Total Plot #1 - Casino & Land |

|

|

|

|

|

Owned |

|

475,173 |

|

44,161 |

|

|

· Casino Building (footprint) |

|

|

|

|

|

|

|

23,769 |

|

2,209 |

|

|

· Parking & Landscape |

|

|

|

|

|

|

|

53,628 |

|

4,984 |

|

|

· Vacant Land |

|

|

|

|

|

|

|

397,776 |

|

36,968 |

|

|

· Total Plot #2 - Hotel Savannah |

|

|

|

|

|

Owned |

|

91,917 |

|

8,543 |

|

|

· Hotel Building (footprint) |

|

|

|

|

|

|

|

32,463 |

|

3,017 |

|

|

· Parking & Landscape |

|

|

|

|

|

|

|

48,694 |

|

4,526 |

|

|

· The Spa at the Hotel Savannah (footprint) |

|

|

|

|

|

|

|

10,760 |

|

1,000 |

|

|

· Staff Housing |

|

|

|

|

|

Leased |

|

17,151 |

|

1,594 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Hotel Columbus (2) (3) |

|

Seligenstadt |

|

Germany |

|

|

|

|

|

|

|

|

· Total Plot #1 - Hotel & Land |

|

|

|

|

|

Owned |

|

37,639 |

|

3,498 |

|

|

· Hotel Building (footprint) |

|

|

|

|

|

|

|

18,306 |

|

1,701 |

|

|

· Parking & Landscape |

|

|

|

|

|

|

|

7,694 |

|

715 |

|

|

· Vacant Land |

|

|

|

|

|

|

|

11,639 |

|

1,082 |

|

|

· Total Plot #2 - Columbus Parking |

|

|

|

|

|

Owned |

|

11,298 |

|

1,050 |

|

|

· Parking & Landscape |

|

|

|

|

|

|

|

7,532 |

|

700 |

|

|

· Vacant Land |

|

|

|

|

|

|

|

3,766 |

|

350 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Square Feet/Meters Owned: |

|

1,838,632 |

|

170,877 |

| ||||

(1) Casino segment.

(2) Hotel segment.

(3) This property is subject to a mortgage from Bank Sparkasse Langen-Seligenstadt. See Note 4 of the Notes to the Consolidated Financial Statements, included in this Annual Report in Part II, Item 8.

Our corporate offices are located at 545 Fifth Avenue, Suite 940, New York, New York, occupying 1,915 square feet of office space pursuant to a renewal in 2010 of our five-year lease, expiring in March 2015. We intend to renew our lease for another five years, provided the renewal terms are economically reasonable to us.

We believe that our existing office and other operating properties are in good condition and are sufficient and suitable for the conduct of our business. In the event we need to expand our operations, we believe that suitable space will be available on commercially reasonable terms.

On November 23, 2011, we acquired the Ceska casino building and associated land and an adjacent outbuilding and related parcel of land from the town of Ceska Kubice, from which we had been renting the facilities. We built out the casino by constructing an annex building to it, making it the largest casino we own to date. See Part I, Item 1, “Our Facilities” above for more details.

We also own a parcel of raw land in the town of Folmova, Czech Republic, near the German border, approximately a quarter mile away from our Ceska casino.

In Hate, we own the casino building and a parcel of land upon a portion of which the casino building sits. On another portion of this land, we constructed and opened Hotel Savannah and the Spa, which are connected to the Route 59 casino, jointly referred to as the “Route 59 Complex.” We opened the hotel on January 14, 2009, and on April 16th of the same year, we held the official launch of Hotel Savannah and the Spa. The combined facilities have effectively become a thriving entertainment complex that has attracted visitors and regular guests and players from the surrounding region.

In April 2002, we acquired a parcel of land in Dolni Dvoriste, Czech Republic. On this parcel, we constructed what was at the time, our largest casino, Route 55, which was completed and opened in December 2004.

On an annual basis, we also lease accommodations for staff in Ceska Kubice, Hate (Route 59) and in Dolni Dvoriste (Route 55).

In September 2014, we acquired a four-star 117-room hotel, Hotel Columbus, located in the suburbs of Seligenstadt, Germany, about a 20-minute, equidistant drive from Frankfurt city center and the Frankfurt International Airport. Hotel Columbus was constructed in 2001 and was operated profitably at the time of purchase by a private family primarily as a business hotel. Hotel Columbus currently has 99 single rooms and 18 double rooms. It also features six meeting rooms, a spacious restaurant and separate breakfast room, each with its own kitchen, two bars, a 37-place parking garage and 22 surface lot parking places. TWC believes that the addition of this hotel will further contribute the Company’s profitability and diversification goals. Hotel Columbus is located at Am Reitpfad 4, 63500 Seligenstadt, Germany.

We may be, from time to time, a party to various legal proceedings and administrative actions, all arising from the ordinary course of business. We are not currently involved in any material legal proceeding nor were we involved in any material litigation during the year ended December 31, 2014 and through the date of our filing.

Item 4. Mine Safety Disclosures

Not applicable.

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our Common Stock is quoted on the Over-The-Counter Markets Group (“OTCQB”) under the symbol “TWOC.”

The stock performance graph and related information presented below is not deemed to be “soliciting material” or to be “filed” with the Securities and Exchange Commission or subject to Regulation 14A or 14C under the Securities Exchange Act of 1934 or to the liabilities of Section 18 of the Securities Exchange Act of 1934, and will not be deemed to be incorporated by reference into any filing under the Securities Act of 1933 or the Securities Exchange Act of 1934, except to the extent we specifically incorporate it by reference into such a filing.

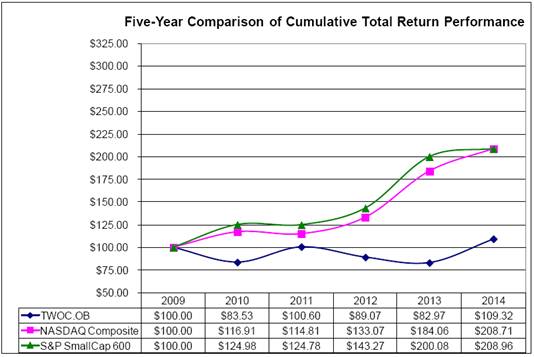

The following graph illustrates a five-year comparison of cumulative total return performance of our Common Stock from December 31, 2009 through December 31, 2014, and compares it to the cumulative total return of the “NASDAQ Composite” and the “S&P SmallCap 600” indices. The comparison assumes a $100 investment on December 31, 2009, in our Common Stock and in each of the foregoing indices, and assumes reinvestment of dividends, if any. We paid no dividends during this period.

The above table is not intended to forecast future performance of our Common Stock.

As of February 28, 2015, our stock price was $3.10. The following table sets forth the high and low prices of the Company’s Common Stock for fiscal years 2013 and 2014 as quoted on OTCQB. All such quotations reflect inter-dealer prices, without retail mark up, mark down or commission, and may not represent actual transactions. There is minimal market liquidity for our Common Stock, as 88.5% of the stock is held by institutional investors. Thus, there is infrequent and minor trades that can occur, which precipitates wide spreads in the “bid” and “ask” quotes of our Common Stock, on any given day.

|

Common Stock |

|

High |

|

Low |

| ||

|

2013 |

|

|

|

|

| ||

|

First Quarter |

|

$ |

2.70 |

|

$ |

2.25 |

|

|

Second Quarter |

|

$ |

2.75 |

|

$ |

2.15 |

|

|

Third Quarter |

|

$ |

2.65 |

|

$ |

2.22 |

|

|

Fourth Quarter |

|

$ |

3.25 |

|

$ |

2.34 |

|

|

2014 |

|

|

|

|

| ||

|

First Quarter |

|

$ |

3.10 |

|

$ |

2.46 |

|

|

Second Quarter |

|

$ |

3.60 |

|

$ |

3.00 |

|

|

Third Quarter |

|

$ |

3.35 |

|

$ |

3.00 |

|

|

Fourth Quarter |

|

$ |

3.28 |

|

$ |

2.80 |

|

As of February 28, 2015, there were 8,821,205 outstanding shares of Common Stock held of record by approximately 400 shareholders and outstanding options to purchase an aggregate of 585,125 shares of Common Stock, of which 435,125 are exercisable. At such date, there were also 75,000 shares of restricted stock, none of which have vested. In addition, there are 305,482 shares of Common Stock issuable under the Company’s Deferred Compensation Plan at February 28, 2015.

We have not paid any dividends to date on our Common Stock. Currently, our plan is to retain future earnings, if and when generated, for investment in our current operations and for future project developments. Any future determination to pay dividends will be at the discretion of our board of directors and will depend on our financial condition, capital requirements, restrictions contained in current or future financing instruments and such other factors as our board of directors deems relevant.

On November 12, 2012, TWC’s board of directors approved a renewable stock repurchase program, in accordance with the retirement method, authorizing the repurchase of up to 500,000 shares of the Company’s Common Stock, over a 12-month period. The program did not obligate the Company to acquire any particular amount of Common Stock, and it could be modified, extended, suspended or discontinued at any time. The program was allowed to expire on November 12, 2014, its second anniversary. The repurchase history is listed in the table below:

ISSUER PURCHASES OF EQUITY SECURITIES

|

Date |

|

Total |

|

Average |

|

Cumulative Total of |

|

Maximum Number |

| |

|

11/19/2012 |

|

4,900 |

|

$ |

2.50 |

|

4,900 |

|

495,100 |

|

|

12/20/2012 |

|

30,000 |

|

$ |

2.65 |

|

34,900 |

|

465,100 |

|

|

01/16/2013 |

|

5,000 |

|

$ |

2.50 |

|

39,900 |

|

460,100 |

|

|

01/18/2013 |

|

900 |

|

$ |

2.50 |

|

40,800 |

|

459,200 |

|

|

01/25/2013 |

|

4,500 |

|

$ |

2.50 |

|

45,300 |

|

454,700 |

|

|

03/08/2013 |

|

100 |

|

$ |

2.54 |

|

45,400 |

|

454,600 |

|

|

03/25/2013 |

|

200 |

|

$ |

2.50 |

|

45,600 |

|

454,400 |

|

|

03/26/2013 |

|

200 |

|

$ |

2.65 |

|

45,800 |

|

454,200 |

|

|

04/04/2013 |

|

250 |

|

$ |

2.65 |

|

46,050 |

|

453,950 |

|

|

04/09/2013 |

|

250 |

|

$ |

2.40 |

|

46,300 |

|

453,700 |

|

|

11/21/2013 |

|

15,200 |

|

$ |

3.20 |

|

61,500 |

|

438,500 |

|

|

01/09/2014 |

|

100 |

|

$ |

2.55 |

|

61,600 |

|

438,400 |

|

|

03/07/2014 |

|

300 |

|

$ |

3.01 |

|

61,900 |

|

438,100 |

|

|

03/12/2014 |

|

300 |

|

$ |

3.03 |

|

62,200 |

|

437,800 |

|

|

10/02/2014 |

|

2,500 |

|

$ |

3.00 |

|

64,700 |

|

435,300 |

|

Sales of Unregistered Equity Securities — Use of Proceeds from Registered Securities

We issued, on August 15, 2014, to each of Mr. Heurtematte and Mr. Baker (the “Former Directors”) 6,985 (or a total of 13,970) authorized but unregistered shares of the Common Stock, plus each a check for approximately $38 representing the cumulative residual balance of their quarterly deferments. These stock and cash issuances were in full satisfaction of TWC’s obligation (which amounted to an aggregate of approximately $46,600) to them under the Company’s Deferred Compensation Plan.