Attached files

| file | filename |

|---|---|

| 8-K - 8-K - TEXAS CAPITAL BANCSHARES INC/TX | d884958d8k.htm |

| EX-99.1 - EX-99.1 - TEXAS CAPITAL BANCSHARES INC/TX | d884958dex991.htm |

| EX-99.3 - EX-99.3 - TEXAS CAPITAL BANCSHARES INC/TX | d884958dex993.htm |

January 21, 2015

TCBI Q4 2014

Earnings

Exhibit 99.2 |

Certain matters discussed on this call may contain “forward-looking

statements” as defined in federal securities laws, which

are subject to risks and uncertainties and are based on Texas Capital’s

current estimates or expectations of future events or future results.

These statements are not historical in nature and can generally be identified by such words as “believe,”

“expect,”

“estimate,”

“anticipate,”

“plan,”

“may,”

“will,”

“intend”

and similar expressions. A number of factors, many of which

are beyond Texas Capital’s control, could cause actual results to differ

materially from future results expressed or implied by

our

forward-looking

statements.

These

risks

and

uncertainties

include

the

risk

of

adverse

impacts

from

general

economic conditions, the effects of recent declines in oil and gas prices on our

customers, competition, changes in interest rates

and

exposure

to

regulatory

and

legislative

changes.

These

and

other

factors

that

could

cause

results

to

differ

materially from those described in the forward-looking statements, as well as

a discussion of the risks and uncertainties that may affect Texas

Capital’s business, can be found in our Annual Report on Form 10-K and other filings made by Texas

Capital with the Securities and Exchange Commission. Forward-looking

statements speak only as of the date of this call. Texas Capital is under

no obligation, and expressly disclaims any obligation, to update, alter or revise its forward-looking

statements, whether as a result of new information, future events or

otherwise. 2 |

Opening Remarks & Financial Highlights

3

Core

Earnings

Power

Strong

Balanced

Growth

Credit

Quality

•

Exceptional growth in traditional LHI balances despite highly competitive

C&I market, with increase in Q4-2014 average balances of $498

million compared to Q3-2014 •

Growth in mortgage finance loans (MFLs) with little evidence of seasonality in

Q4-2014 •

Continued strong growth in demand and total deposits

•

Asset sensitivity position increased with extended duration of low-cost

funding •

Growth in total loans continues to produce strong net revenue

•

Operating leverage improved with rate of growth in net revenue greater than NIE

for full year

•

Business

model

focused

on

organic

growth

demonstrates

ability

to

produce

high

returns on invested capital

•

Credit metrics remain strong with nominal increase in NPAs

•

NCOs at 5 bps in Q4-2014 and 7 bps YTD

•

High allowance coverage ratios

•

Provision primarily related to growth in core LHI |

4

Energy Commentary

•

TCBI has deep experience in energy lending

•

Executives, lenders, credit policy and engineers, on average, have more than 3

decades of experience •

Since our inception there have been five corrections in energy commodity prices,

with no significant consequences

•

Cumulative energy losses < $300,000 in 15 years

•

Outstanding loans in energy portfolio 6% of total loans

•

Price

decks

are

dynamic,

but

our

underwriting

standards

have

not

changed

since

our

inception

•

Average credit line is approximately 60% funded

•

Agreements generally provide unilateral discretion to reduce borrowing bases as

necessary •

Over 90% of oil-weighted outstandings are hedged

•

Hedged price much higher than lifting costs, providing significant cash flow to

reduce debt •

Collateral comprised of long-lived reserves providing capacity to absorb

price swings •

In-house engineering reviews all credits and reports to Credit Policy

•

Anticipate some downgrades; currently nothing that would drive significant

allocation of loan loss reserves

•

Exposure to oil service

•

Less than 1% of total loans

•

Exposure generally limited to production, not the higher risk drilling and

completion |

Revenue & Expense

5

•

High returns maintained with effective

deployment of additional capital

•

Improvement in operating leverage and

Efficiency Ratio for full year

•

Strong

capacity

for

Net

Revenue

growth

•

Total loans spread at 3.91%

•

Net Revenue increased 2% from Q3-2014

•

Reduction in NIM driven by growth, liquidity

build and debt issuance in Q1

•

Continued focus on managing growth in NIE

•

Effective utilization of professional resources

and reduction in legal expense

•

Linked quarter net decrease in incentive expense

linked to performance and change in stock price

•

Provision expense related to growth

represents net interest income contribution of

loan growth for 3+ months

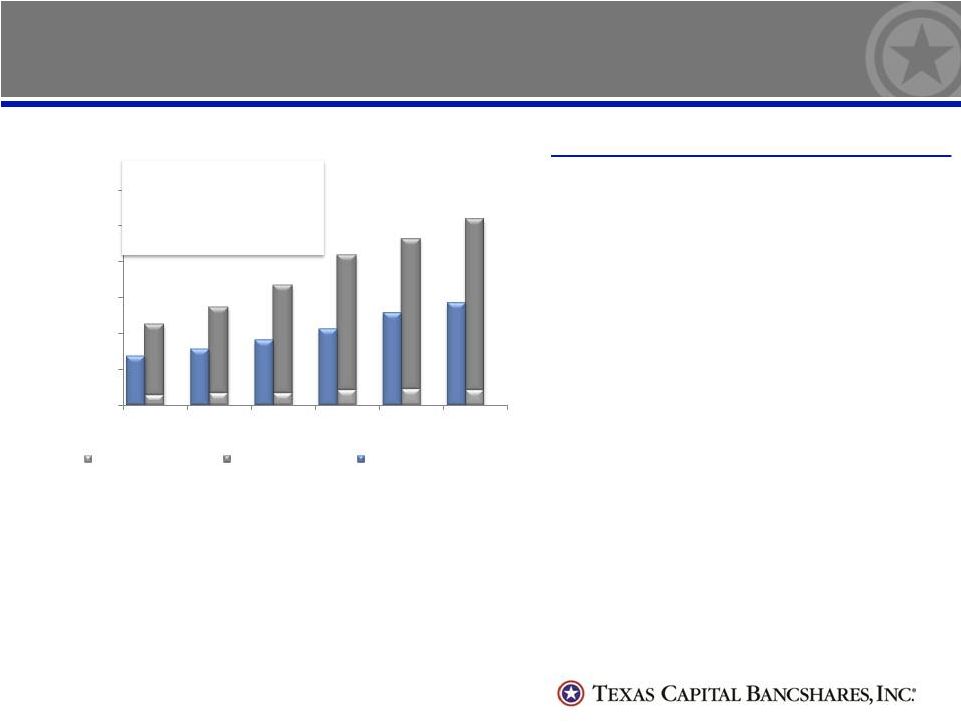

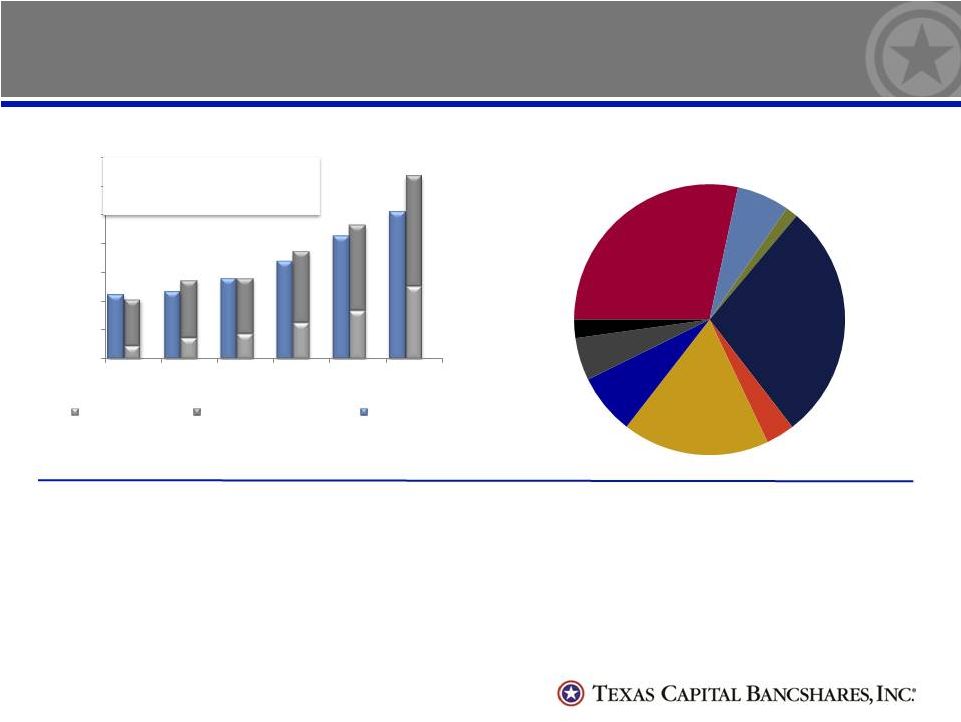

Revenue & Expense Trends

Revenue & Expense Highlights

Operating Revenue CAGR: 18%

Net Interest

Income CAGR:

19%

Non-interest Income CAGR: 8%

Non-interest Expense CAGR: 14%

Net Income CAGR: 41%

0

100,000

200,000

300,000

400,000

500,000

600,000

2009

2010

2011

2012

2013

2014

Non-interest Income

Net Interest Income

Non-interest Expense |

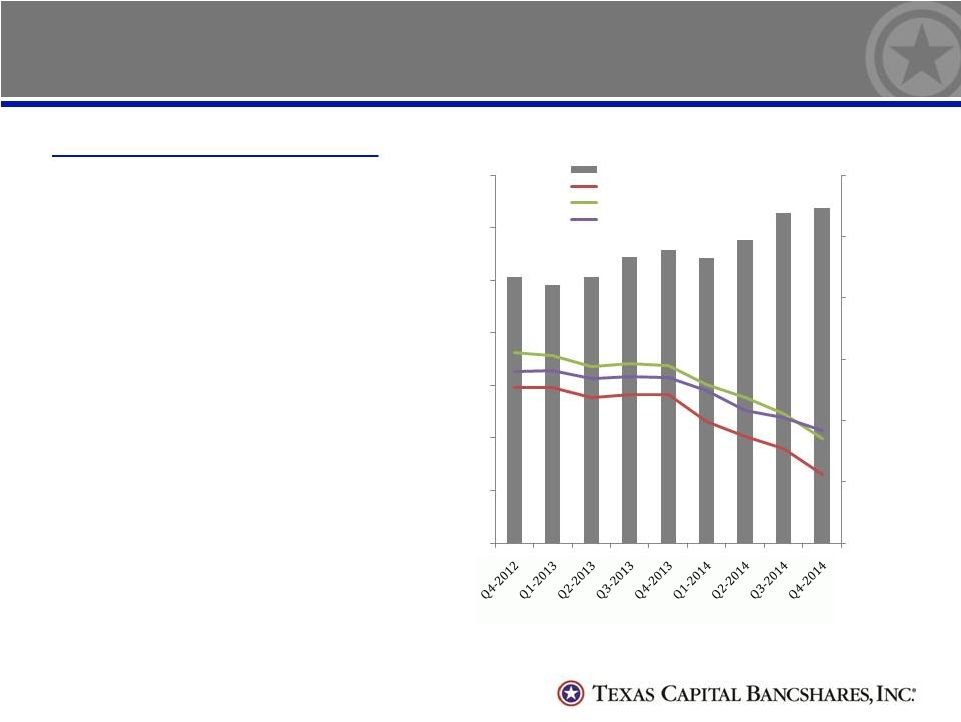

Net Interest Income & Margin

6

•

Net interest income growth of 2%

from Q3-2014 and 14% from Q4-

2013

•

Yields on traditional LHI down

modestly with 5% growth in average

balances from Q3-2014

•

MFL growth benefits NII

•

Yield reduction based on profile of

customers

•

Favorable deposit position

•

High risk-adjusted returns despite

impact on NIM

•

Core

funding

costs

–

deposits

and

borrowed

funds

–

flat

at

17

bps

•

Deposit growth consistent with plan

to increase liquidity

•

Minor benefit to NII

•

Impact on NIM consistent with

objectives

•

Significant increase in asset

sensitivity and duration of low-cost

funding

Net Interest Income & Margin Trends

NIM Highlights

3.00%

3.50%

4.00%

4.50%

5.00%

5.50%

6.00%

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

Net Interest income ($MM)

Net Interest Margin (%)

Earning Asset Yield (%)

Total Loan Spread (%) |

Analysis of Net Interest Income & Expenses

7

NII ($MM)

NIM (%)

125.7

Q3 2014

3.77%

.1

Increase in liquidity

(.12)

(3.0)

Decrease in LHI loan yields

(.08)

(.6)

Decrease in MF loan yields

(.02)

1.5

Mix shift of MF loans/total loans

.01

3.8

Impact of increase in earning

assets

-

.1

Other

-

$127.6

Q4 2014

3.56%

Non-interest expense ($MM)

Linked quarter

increases/

(decreases)

Q3 2014

$71.9

Salaries

and

employee

benefits

–

related

to stock price changes

(.8)

Salaries and employee benefits –

performance based incentives, LTI and

annual incentive pool

.1

Legal

&

other

professional

–

effective

use of professional services; legal

reduced and varies by quarter

(1.1)

Salaries and employee benefits –

continued build out

2.1

All other –

includes occupancy,

technology and marketing, all with some

one-time and seasonal expenses

1.9

Q4 2014

$74.1 |

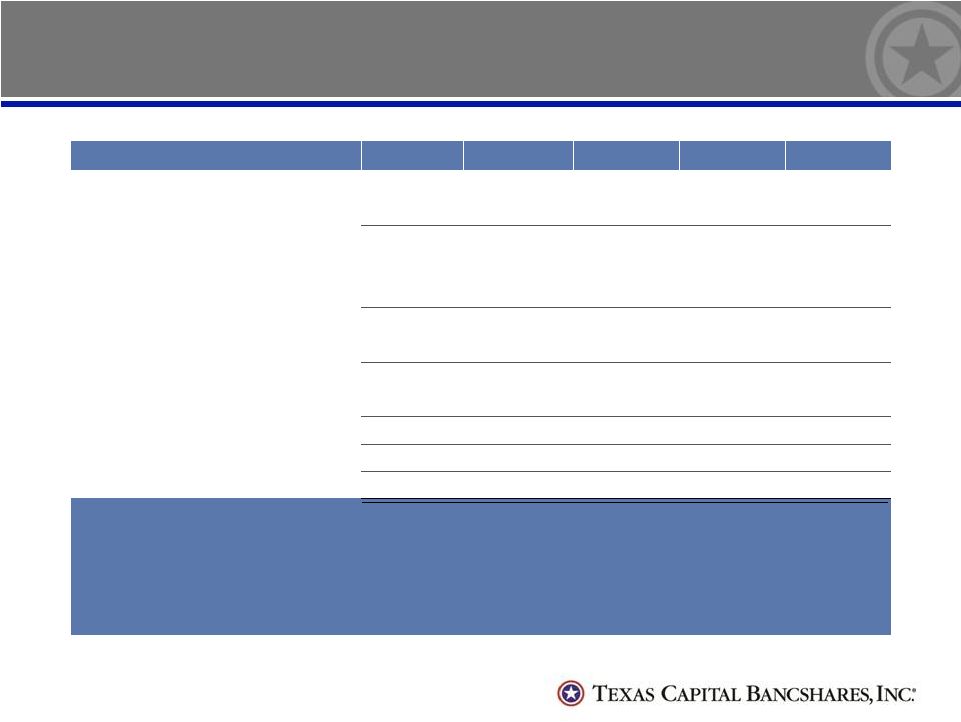

Performance Summary -

Quarterly

8

(in thousands)

Q4 2014

Q3 2014

Q2 2014

Q1 2014

Q4 2013

Net interest income

$ 127,582

$ 125,661

$ 115,407

$ 108,315

$ 111,475

Non-interest income

11,226

10,396

10,533

10,356

11,184

Net revenue

138,808

136,057

125,940

118,671

122,659

Provision for credit losses

6,500

6,500

4,000

5,000

5,000

OREO valuation and write-down expense

-

-

-

-

466

Total provision and OREO valuation

6,500

6,500

4,000

5,000

5,466

Non-interest expense

74,117

71,915

69,765

69,317

69,822

Income before income taxes

58,191

57,642

52,175

44,354

47,371

Income tax expense

20,357

20,810

18,754

16,089

17,012

Net income

37,834

36,832

33,421

28,265

30,359

Preferred stock dividends

2,437

2,438

2,437

2,438

2,438

Net income available to common shareholders

$ 35,397

$ 34,394

$ 30,984

$ 25,827

$ 27,921

Diluted EPS

$ .78

$ .78

$ .71

$ .60

$ .67

Net interest margin

3.56%

3.77%

3.87%

3.99%

4.21%

ROA

1.03%

1.07%

1.08%

1.01%

1.10%

ROE

11.41%

12.11%

11.38%

10.20%

11.94%

Efficiency

(1)

53.4%

52.9%

55.4%

58.4%

56.9%

(1) Excludes OREO valuation charge |

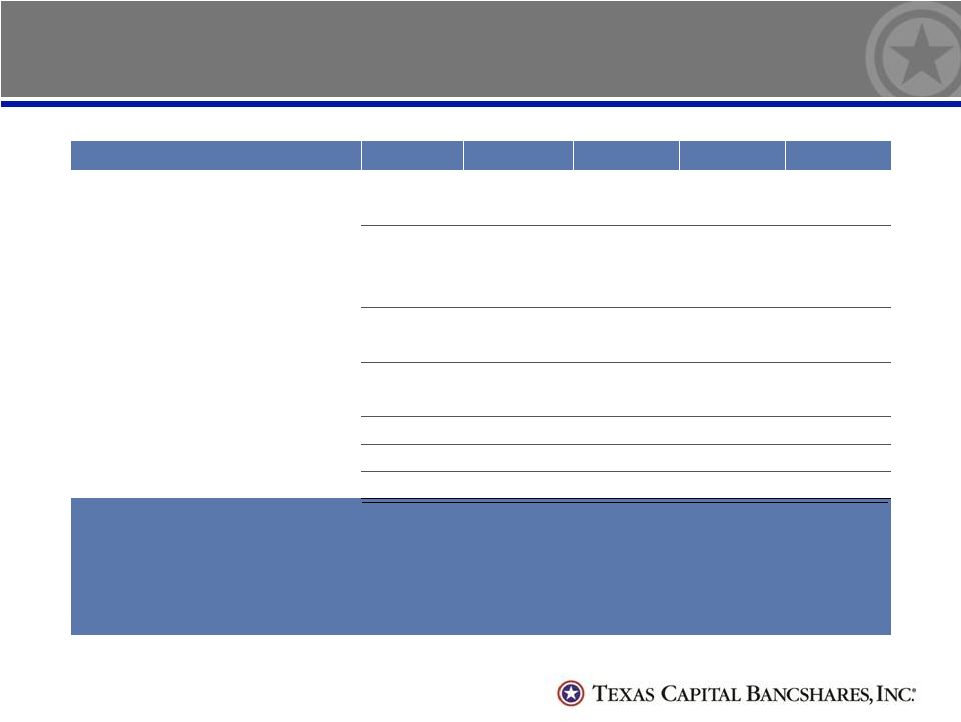

9

Performance Summary -

Annual

9

(in thousands)

2014

2013

2012

2011

2010

Net interest income

$ 476,965

$ 419,513

$ 376,879

$ 302,937

$ 241,674

Non-interest income

42,511

44,024

43,040

32,232

32,263

Net revenue

519,476

463,537

419,919

335,169

273,937

Provision for credit losses

22,000

19,000

11,500

28,500

53,500

OREO valuation and write-down expense

-

920

6,883

6,798

8,504

Total provision and OREO valuation

22,000

19,920

18,383

35,298

62,004

Non-interest expense

285,114

255,809

212,998

181,529

155,120

Income before income taxes

212,362

187,808

188,538

118,342

56,813

Income tax expense

76,010

66,757

67,866

42,366

19,626

Net income

136,352

121,051

120,672

75,976

37,187

Preferred stock dividends

9,750

7,394

-

-

-

Net income available to common shareholders

$ 126,602

$ 113,657

$ 120,672

$ 75,976

$ 31,187

Diluted EPS

$ 2.88

$ 2.72

$ 3.01

$ 1.99

$ 1.00

Net interest margin

3.78%

4.22%

4.41%

4.68%

4.28%

ROA

1.05%

1.17%

1.35%

1.12%

.63%

ROE

11.31%

12.82%

16.93%

13.39%

7.23%

Efficiency

(1)

54.9%

55.2%

49.8%

54.1%

56.6%

(1) Excludes OREO valuation charge |

2015 Outlook

10

Business Driver

2015 Outlook v. 2014 Results

Average LHI

Low teens percent growth

Average

LHI

–

Mortgage

Finance

Flat to single digit percent growth

Average Deposits

Mid to high teens percent growth

Net Interest Income

Low double-digit percent growth, with continued low interest rates

and impact of days in Q1

Net Interest Margin

3.40% to 3.50%, continued compression with growth and liquidity

build

Net Charge-Offs

Less than 0.25%

NIE

Low to mid-teens percent growth

Efficiency Ratio

Mid –fifties, includes continued development of product extension and

regulatory

compliance

costs,

with

improvement

expected

in

2

half

of

2015

Diluted shares

2015 will include full effect of 2014 common equity offerings

nd |

Loan & Deposit Growth

11

•

Broad-based

growth

in

average

traditional

LHI

–

Growth

of

$498.1

million

(5%)

from

Q3-2014

and

$1.8

billion

(22%) from Q4-2013

•

Period-end balance $233.6 million higher than Q4-2014 average balance and

20% above Q4-2013 period-end balance

•

MF performance exceeded industry trends with increase in averages of 1% from

Q3-2014 and 55% from Q4- 2013

•

Average DDA increased 8% from Q3-2014 and 53% from Q4-2013

•

Total average deposits increased 8% from Q3-2014 and 36% from

Q4-2013 Growth Highlights

Balance Trends

Total Loan Composition

($14.3 Billion at 12/31/14)

Demand Deposit CAGR: 42%

Total Deposit CAGR: 25%

Loans Held for Investment CAGR: 18%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2009

2010

2011

2012

2013

2014

Demand Deposits

Interest Bearing Deposits

Loans HFI

Business

Assets

28%

Energy

6%

Highly

Liquid

Assets

2%

Mortgage

Finance

29%

Other Assets

3%

Comml R/E

Mkt. Risk

18%

Residential

R/E Mkt.

Risk

7%

Owner

Occupied

R/E

5%

Unsecured

2% |

Asset Quality

12

•

Total credit cost of $6.5 million for Q4-2014, compared

to $6.5 million in Q3-2014 and $5.5 million in Q4-2013

•

NCOs $1.1 million, or 5 bps, in Q4-2014 compared to 3

bps in Q3-2014 and 6 bps in Q4-2013

•

No OREO valuation charge in Q4-2014 or Q3-2014

compared to $466,000 in Q4-2013

•

Modest increase in non-accruals and OREO now less

than $1 million

Asset Quality Highlights

Non-accrual loans

Q4-2014

Commercial

$ 33,122

Construction

–

Real estate

9,947

Consumer

62

Equipment leases

173

Total non-accrual loans

43,304

Non-accrual loans as % of loans

excluding MF

.43%

Non-accrual loans as % of total

loans

.30%

OREO

568

Total Non-accruals + OREO

$ 43,872

Non-accrual loans + OREO as %

of loans excluding MF + OREO

.43%

Reserve to non-accrual loans

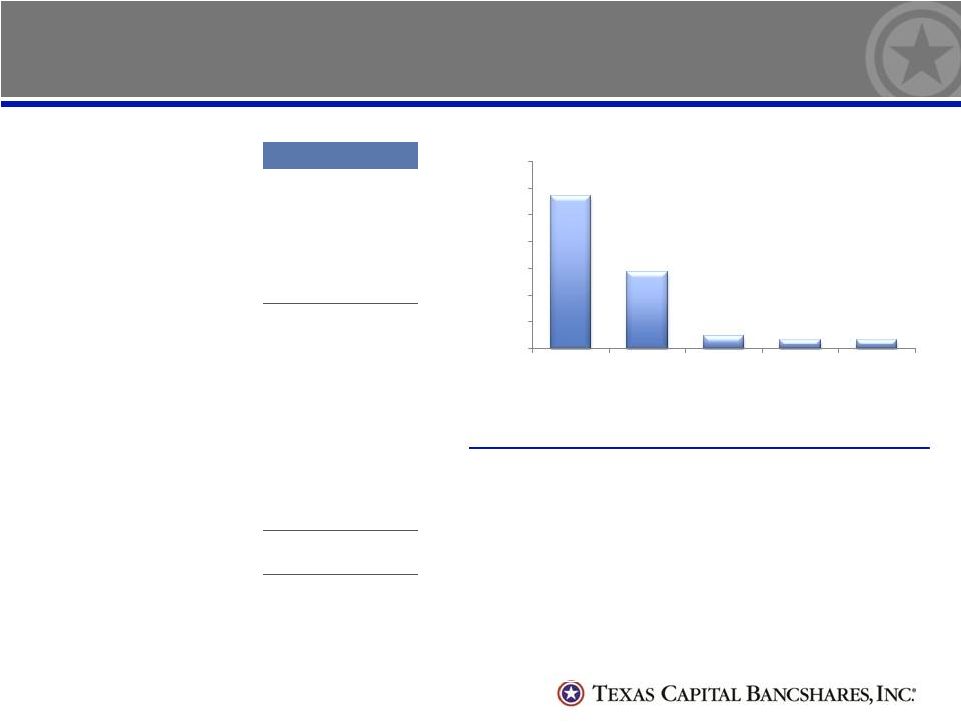

2.3x

NCO / Average Traditional LHI

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

2010

2011

2012

2013

2014

1.14%

0.58%

0.10%

0.07%

0.07% |

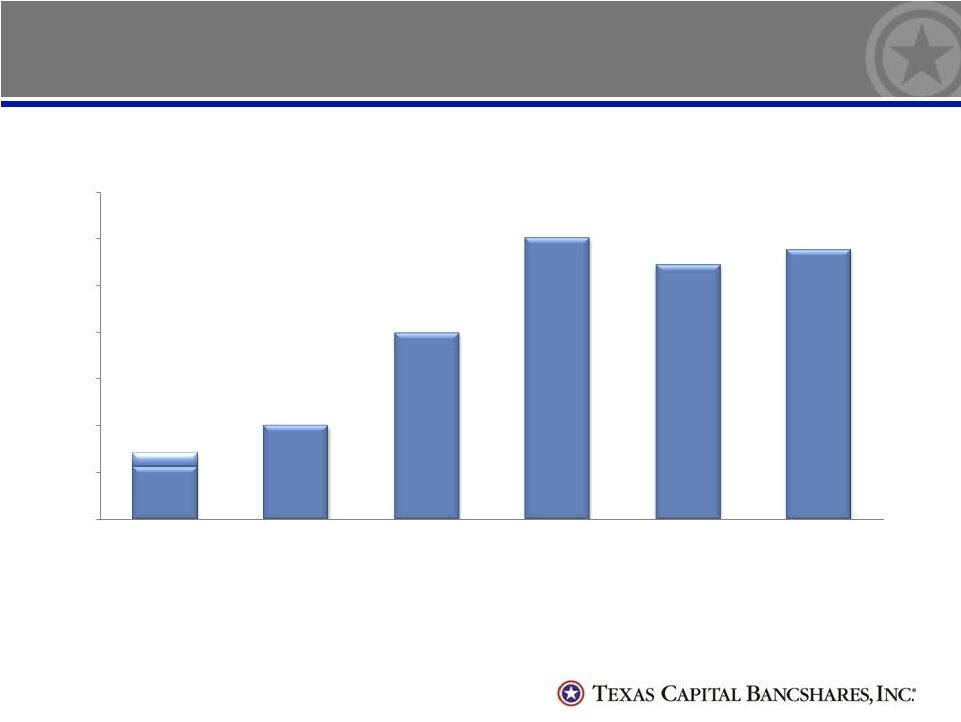

EPS Growth

13

2009^

2010

2011

2012

2013

2014

^Excludes $.15 effect of preferred TARP dividend during

2009. Reported EPS was

$0.56. EPS

Growth (5-yr CAGR of 39%)

$0.71

$1.00

$1.99

$3.01

$2.72

$2.88

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50 |

Closing Comments

•

Proven

organic

growth

business

model

continues

to

produce

in

key

lines

of

business

with improvements in operating leverage

•

Solid

core

earnings

power

and

strong

asset

growth

experienced

in

2014;

2015

expected

to be challenging year for asset growth

•

Despite drop in energy prices, remain confident about underwriting standards and

performance of energy portfolio

•

Continue to have critical focus on maintaining excellent credit quality which

could limit C&I growth

•

Continued success in building liquidity which will continue in 2015

•

Remain highly asset sensitive based on how we run our business; now better

positioned to take advantage of increases in short-term rates

•

Successful track record of talent acquisition and being opportunistic with

hires •

No real seasonality experienced in Q4-2014 as Mortgage Finance continues to

exceed industry trends with improved market position

•

Strong

build

out

in

2014

and

the

first

half

of

2015

positions

us

for

improving

earnings

trajectory in 2016

14 |

Q&A

15 |

Appendix

16 |

Average Balances, Yields & Rates -

Quarterly

17

(in thousands)

Q4 2014

Q3 2014

Q4 2013

Avg. Bal.

Yield Rate

Avg. Bal.

Yield Rate

Avg. Bal.

Yield Rate

Assets

Securities

$ 42,515

3.80%

$ 46,413

3.86%

$ 65,067

4.25%

Fed funds sold & liquidity investments

882,001

.25%

388,855

.25%

158,594

.21%

Loans held for investment, mortgage finance

3,471,737

3.06%

3,452,782

3.13%

2,238,730

3.59%

Loans held for investment

9,921,323

4.40%

9,423,259

4.52%

8,142,569

4.73%

Total loans, net of reserve

13,296,921

4.08%

12,784,614

4.18%

10,297,290

4.52%

Total earning assets

14,221,437

3.85%

13,219,882

4.06%

10,520,951

4.45%

Total assets

$14,631,072

$13,629,609

$10,899,266

Liabilities and Stockholders’

Equity

Total interest bearing deposits

$ 7,405,436

.28%

$ 6,856,542

.27%

$ 5,887,252

.26%

Other borrowings

251,449

.19%

309,868

.20%

314,018

.20%

Subordinated notes

286,000

5.88%

286,000

5.88%

111,000

6.58%

Long-term debt

113,406

2.19%

113,406

2.19%

113,406

2.21%

Total interest bearing liabilities

8,056,291

.50%

7,565,816

.50%

6,425,676

.40%

Demand deposits

5,047,876

4,669,772

3,289,307

Stockholders’

equity

1,380,646

1,276,603

1,077,822

Total liabilities and stockholders’

equity

$14,631,072

.28%

$13,629,609

.28%

$10,899,266

.24%

Net interest margin

3.56%

3.77%

4.21%

Total deposits and borrowed funds

$12,704,761

.17%

$11,836,182

.16%

$ 9,490,577

.17%

Loan spread

3.91%

4.02%

4.35% |

18

Average Balances, Yields & Rates -

Annual

18

(in thousands)

2014

2013

Avg. Bal.

Yield Rate

Avg. Bal.

Yield Rate

Assets

Securities

$ 49,200

3.98%

$ 77,178

4.39%

Fed funds sold & liquidity investments

444,673

.25%

144,050

.21%

Loans held for investment, mortgage finance

2,948,938

3.19%

2,342,149

3.75%

Loans held for investment

9,265,435

4.51%

7,471,676

4.73%

Total loans, net of reserve

12,123,010

4.22%

9,735,543

4.53%

Total earning assets

12,616,883

4.08%

9,956,771

4.47%

Total assets

$13,016,611

$10,348,404

Liabilities and Stockholders’

Equity

Total interest bearing deposits

$ 6,677,371

.27%

$ 5,407,810

.26%

Other borrowings

379,877

.20%

653,318

.19%

Subordinated notes

271,617

5.97%

111,000

6.60%

Long-term debt

113,406

2.19%

113,406

2.24%

Total interest bearing liabilities

7,442,271

.50%

6,285,534

.40%

Demand deposits

4,188,173

2,967,063

Stockholders’

equity

1,269,601

1,001,215

Total liabilities and stockholders’

equity

$13,016,611

.29%

$10,348,404

.24%

Net interest margin

3.78%

4.22%

Total deposits and borrowed funds

$11,245,421

.17%

$ 9,028,191

.17%

Loan spread

4.05%

4.36% |

Average Balance Sheet -

Quarterly

19

(in thousands)

QTD Average

Q4/Q3 %

Change

YOY %

Change

Q4 2014

Q3 2014

Q4 2013

Total assets

$14,631,072

$13,629,609

$10,899,266

7%

34%

Loans held for investment

9,921,323

9,423,259

8,142,569

5%

22%

Loans held for investment, mortgage

finance

3,471,737

3,452,782

2,238,730

1%

55%

Total loans

13,393,060

12,876,041

10,381,299

4%

29%

Securities

42,515

46,413

65,067

(8)%

(35)%

Demand deposits

5,047,876

4,669,772

3,289,307

8%

53%

Total deposits

12,453,312

11,526,314

9,176,559

8%

36%

Stockholders’

equity

1,380,646

1,276,603

1,077,822

8%

28% |

20

Average Balance Sheet -

Annual

20

(in thousands)

YTD Average

YOY % Change

2014

2013

Total assets

$13,016,611

$10,348,404

26%

Loans held for investment

9,265,435

7,471,676

24%

Loans held for investment, mortgage finance

2,948,938

2,342,149

26%

Total loans

12,214,373

9,813,825

24%

Securities

49,200

77,178

(36)%

Demand deposits

4,188,173

2,967,063

41%

Total deposits

10,865,544

8,374,873

30%

Stockholders’

equity

1,269,601

1,001,215

27% |

Period End Balance Sheet

21

(in thousands)

Period End

Q4/Q3 %

Change

YOY %

Change

Q4 2014

Q3 2014

Q4 2013

Total assets

$15,899,946

$14,266,503

$11,720,064

11%

36%

Loans held for investment

10,154,887

9,686,422

8,486,603

5%

20%

Loans held for investment, mortgage

finance

4,102,125

3,774,467

2,784,265

9%

47%

Total loans

14,257,012

13,460,889

11,270,868

6%

26%

Securities

41,719

43,938

63,214

(5)%

(34)%

Demand deposits

5,011,619

4,722,479

3,347,567

6%

50%

Total deposits

12,673,300

11,715,808

9,257,379

8%

37%

Stockholders’

equity

1,484,190

1,297,922

1,096,350

14%

35% |