Attached files

| file | filename |

|---|---|

| EX-32.1 - CERTIFICATION - Nxt-ID, Inc. | f10k2014ex32i_nxtid.htm |

| EX-31.1 - CERTIFICATION - Nxt-ID, Inc. | f10k2014ex31i_nxtid.htm |

| EX-31.2 - CERTIFICATION - Nxt-ID, Inc. | f10k2014ex31ii_nxtid.htm |

| EX-32.2 - CERTIFICATION - Nxt-ID, Inc. | f10k2014ex32ii_nxtid.htm |

| EXCEL - IDEA: XBRL DOCUMENT - Nxt-ID, Inc. | Financial_Report.xls |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2014

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________ to ___________

Commission file number: 000-54960

Nxt-ID, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 46-0678374 | |

(State

or other jurisdiction of |

(I.R.S.

Employer Identification No.) |

288 Christian Street

Oxford, CT 06478

(Address of principal executive offices)(Zip Code)

Registrant’s telephone number, including area code: (203) 266-2103

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: | Name of each exchange on which registered: | |

Common Stock, par value $0.0001 Warrants to purchase Common Stock (expiring September 15, 2019) |

The Nasdaq Stock Market LLC The Nasdaq Stock Market LLC

|

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter periods that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III or this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer ☐ | Smaller reporting company ☒ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

On June 30, 2014, the last business day of the second fiscal quarter, our common stock traded on OTCBB under the symbol NXTD. The aggregate market value of the common stock held by non-affiliates of the registrant, as of June 30, 2014, the last business day of the second fiscal quarter, was approximately $12,862,944 based on a total number of shares of our common stock outstanding that day of 22,028,285 and a closing price of $3.91. Shares of common stock held by each director, each officer and each person who owns 10% or more of the outstanding common stock have been excluded from this calculation in that such persons may be deemed to be affiliates. The determination of affiliate status is not necessarily conclusive.

The registrant had 24,858,874 shares of its common stock outstanding as of February 27, 2015.

DOCUMENTS INCORPORATED BY REFERENCE

None.

TABLE OF CONTENTS

| Page | ||

| PART I | ||

| Item 1. | Business | 1 |

| Item 1A. | Risk Factors | 8 |

| Item 1B. | Unresolved Staff Comments | 18 |

| Item 2. | Properties | 18 |

| Item 3. | Legal Proceedings | 18 |

| Item 4. | Mine Safety Disclosures | 18 |

| PART II | ||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 19 |

| Item 6. | Selected Financial Data | 20 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 20 |

| Item 7A. | Quantitative and Qualitative Disclosures about Market Risk | 27 |

| Item 8. | Financial Statements and Supplementary Data | 27 |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 27 |

| Item 9A. | Controls and Procedures | 27 |

| Item 9B. | Other Information | 28 |

| PART III | ||

| Item 10. | Directors, Executive Officers and Corporate Governance | 29 |

| Item 11. | Executive Compensation | 33 |

| Item 12. | Security Ownership Of Certain Beneficial Owners And Management and Related Stockholder Matters | 35 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 37 |

| Item 14. | Principal Accounting Fees and Services | 37 |

| PART IV | ||

| Item 15. | Exhibits, Financial Statement Schedules | 39 |

| SIGNATURES | 41 | |

| INDEX TO EXHIBITS | 42 | |

| i |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (this “Report”) contains “forward-looking statements” within the meaning of the Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements discuss matters that are not historical facts. Because they discuss future events or conditions, forward-looking statements may include words such as “anticipate,” “believe,” “estimate,” “intend,” “could,” “should,” “would,” “may,” “seek,” “plan,” “might,” “will,” “expect,” “predict,” “project,” “forecast,” “potential,” “continue” negatives thereof or similar expressions. These forward-looking statements are found at various places throughout this Report and include information concerning possible or assumed future results of our operations; business strategies; future cash flows; financing plans; plans and objectives of management; any other statements regarding future operations, future cash needs, business plans and future financial results, and any other statements that are not historical facts.

From time to time, forward-looking statements also are included in our other periodic reports on Forms 10-Q and 8-K, in our press releases, in our presentations, on our website and in other materials released to the public. Any or all of the forward-looking statements included in this Report and in any other reports or public statements made by us are not guarantees of future performance and may turn out to be inaccurate. These forward-looking statements represent our intentions, plans, expectations, assumptions and beliefs about future events and are subject to risks, uncertainties and other factors. Many of those factors are outside of our control and could cause actual results to differ materially from the results expressed or implied by those forward-looking statements. In light of these risks, uncertainties and assumptions, the events described in the forward-looking statements might not occur or might occur to a different extent or at a different time than we have described. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this Report. All subsequent written and oral forward-looking statements concerning other matters addressed in this Report and attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this Report.

Except to the extent required by law, we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events, a change in events, conditions, circumstances or assumptions underlying such statements, or otherwise.

For discussion of factors that we believe could cause our actual results to differ materially from expected and historical results see “Item 1A - Risk Factors” below.

| ii |

PART I

| Item 1. | Business |

Our Company

We are an early stage technology company that is focused on products, solutions, and services that have a need for biometric secure access control. We have three distinct lines of business that we are currently pursuing: mobile commerce (“m-commerce”); law enforcement and biometric access control applications; and law enforcement. Our initial efforts have primarily focused on the development of our secure products for the growing m- commerce market, most immediately, a secure mobile electronic smart wallet. Wocket™ is a smart wallet, the next evolution in smart devices following the smart phone and smart watch, designed to protect your identity and replace all the cards in your wallet, with no smart phone required. Wocket™ works anywhere credit cards are accepted and only works with your biometric stamp of approval. Credit, debit, ATM, loyalty, gift, ID, membership, insurance, ticket, emergency, medical, business, contacts, coupon, and virtually any card can be protected on Wocket™. More than 10,000 cards, records, coupons, etc. and 100 voice commands can also be stored on Wocket™.

Our plan also anticipates that we will use our core biometric facial and voice recognition algorithms to develop security applications (both cloud based and locally hosted) that can be used for corporations (industrial uses, such as enterprise computer networks) as well as individuals (consumer uses, such as smart phones, tablets or personal computers). Finally, our plan calls for a suite of high level security products and facial recognition applications that can be utilized by law enforcement, the defense industry, and the U.S. Department of Homeland Security.

We believe that our MobileBioTM products, together with our biometric security solutions, will provide distinct advantages within these markets by improving mobile security. Currently most mobile devices continue to be protected simply by PIN numbers. This security methodology is easily duplicated on another device, and can be easily spoofed or hacked. Our biometric security paradigm is Dynamic Pairing Codes (DPC). DPC is a new, proprietary method to secure users, devices, accounts, locations and servers over any communication media by sharing key identifiers, including biometric-enabled identifiers, between end-points by passing dynamic pairing codes (random numbers) between end-points to establish sessions and/or transactions without exposing identifiers or keys. The recent high-level breaches of personal credit card data raises serious concerns among consumers about the safety of their money. These consumers are also resistant to letting technology companies learn even more about their personal purchasing habits.

We also plan to service the access control and law enforcement facial recognition markets with our existing 3D facial recognition technology products beginning with U.S. federal and state governmental agencies. These products, whose underlying technologies have been licensed by us, provide customers with the capability to enroll subjects in a 3D database and use that database for verification of identities. During 2012, we acquired 100% of the membership interests in an entity affiliated with its founders as a means toward advancing our business plan.

The Company is an early stage entity and has incurred net losses since its inception. In order to execute the Company’s long-term strategic plan to develop and commercialize its core products, the Company will need to raise additional funds, through public or private equity offerings, debt financings, or other means. The Company can give no assurance that the cash raised subsequent to December 31, 2014 or any additional funds raised will be sufficient to execute its business plan. These conditions raise substantial doubt about the Company’s ability to continue as a going concern. The Company can give no assurance that additional funds will be available on reasonable terms, or available at all, or that it will generate sufficient revenue to alleviate these conditions.

The Company’s ability to execute its business plan is dependent upon its ability to raise additional equity, secure debt financing, and/or generate revenue. Should the Company not be successful in obtaining the necessary financing, or generate sufficient revenue to fund its operations, the Company would need to curtail certain of its operational activities. The accompanying financial statements do not include any adjustments that might be necessary should the Company be unable to continue as a going concern.

Our independent registered public accounting firm’s report contains an explanatory paragraph that expresses substantial doubt about our ability to continue as a going concern.

Wocket™

We believe that many credit card holders will be reluctant to use their smartphone for mobile payments and completely abandon their wallets. We have developed a separate physical electronic smart wallet that is intended to hold information from credit cards, debit cards, loyalty cards, identification cards, and virtually any magnetic stripe card to allow the owner of the card to configure a single, dynamic, electronic card to replicate any of the copied cards and thereby reduce the number of physical cards carried in a wallet. As designed, users will simply scan in each card, slide through each of the scanned “soft-cards” via a touch screen display and select the card the user wishes to program. The resultant electronic card can then be swiped just like a regular credit, debit, or virtually any other card. The system consists of 2 devices: an electronic smart wallet “wocket” and a dynamic smart card. The electronic smart wallet will be secured by biometric identification and will also have a range of accessories that allow the user to carry a driver’s license and cash in the same device, replacing the wallet altogether. We have completed the design and prototype stages of the Wocket and units are currently being fabricated for production testing and sale. Our current plans call for us to commence shipping Wockets in the second quarter of 2015.

We intend to initially market the Wocket to technology minded consumers through direct sales via our website, social media and digital marketing to websites and forums that the consumer may frequent. Thereafter we will expand our reach through distinct channel partners with widespread retail distribution. At the same time we are also seeking partnerships with corporations and financial institutions that have an interest in fraud prevention. We intend to leverage our encryption capabilities to these potential partners as well.

| 1 |

Wocket™ prototype

MobileBio VoiceMatch®

Voicematch® is a new method of recognizing both speakers and specific words providing innovative multi-factor recognition. Voice authentication is a more natural biometric method of authentication than fingerprint that allows an individual access to multiple devices. Voicematch is efficient enough to run on low-power devices and runs or will run on mobile platforms such as Android and iOS, as well as laptops and desktops. The product helps to address the growing BYOD (Bring your own device) problem for corporations by positively identifying the individual using the mobile device. Voicematch® is a potential original equipment manufacturer (“OEM”) product for smartphone manufacturers. The product will also be sold as a standard development kit (“SDK”) to provide corporations the opportunity to add a further layer of biometric protection to their websites and smartphone applications for their customers.

We expect commercial versions of the product to be available later in 2015; although we cannot provide any assurances of this.

FaceMatch®

FaceMatch® is intended to serve as a modular facial recognition system for smartphones, tablets, laptop and desktop computers. FaceMatch®, depending on the number of cameras available and level of security desired, will use 2D, partial 3D or 3D facial recognition algorithms to allow the user access to their device. The software is intended to be hosted on the device or through a cloud computing solution. The software will also be designed to be available as an “app” on the iPhone and Android platforms, although there are presently no definitive agreements in place with either of the sponsors of those platforms. The FaceMatch® app will not retain any personal information on the user. The FaceMatch® app is near the completion of its development for desktop and laptop use. The development work for the FaceMatch® app for tablet and smartphone use has not yet begun but will use the same basic technology. Our current plans assume that sales from this product will commence later in 2015, although we cannot provide any assurances.

Through the acquisition of 3D-ID LLC, the Company acquired 3D FaceMatch® and 3D SketchArtist™ facial recognition products which are available for sale. These products are primarily designed for access control, law enforcement and travel and immigration in contrast to the MobileBio™ products which are designed for individual security on mobile devices.

3D FaceMatch® Biometric Identity Systems

The ActiveID Biometric Identity System is a completely modular and field proven identity management platform providing fusion of 3D facial recognition, 2D facial recognition and optional fingerprint biometrics. Available as a standalone solution or readily integrated into national scale systems for travel and immigration, access control and law enforcement, ActiveID products feature patented FaceMatch® 3D facial recognition.

A complete ActiveID solution includes: 1) one or more Enrollment Systems including integrated lighting for high-quality mug shot or passport imagery; 2) databases containing enrolled 3D facial templates, 2D images, application-tailored personal data, and optional fingerprints; and 3) one or more Verifier and/or Identifier stations to determine identities. Duplicate ID/imposter searches can be performed at any step.

Except for the Biometric Camera hardware, all products consist of software running on industry-standard encrypted networks, databases, and computers. All software is easily customized to support specific process needs, and several pre-configured solutions are available including prisoner management, facility access control, and fused face/fingerprint verification.

3D SketchArtist™

3D SketchArtist™ is a 3D software face composite sketch tool that makes sketching a face simple, fast, and realistic. Using patented 3D morphing technology, law enforcement professionals can now sketch an accurate composite with 3D life-like features. 3D SketchArtist™ transforms ordinary sketches into rapidly evolving mock-ups that can be modified with a simple click of the mouse. Facial features, poses, expressions, and even lighting can be modified to reflect a witness description in mere seconds. 3D SketchArtist™ is user-friendly so that anyone can use it to render accurate composites of a suspect, quickly and easily. What once could only be performed by professional sketch artists can now be performed with minimal training.

Our Industry

The January 2015 issue of the Nilson Report shows that on a planet-wide basis, transactions at merchants on the leading payment cards rose to $187.3 billion in 2013, of which 43.7% were generated in the United States.

In addition, it is estimated that there are approximately 180 million cardholders in the U.S. alone with each cardholder owning in excess of three payment cards. Some experts believe that in the foreseeable future most people will have embraced and fully adopted the use of smart-device swiping for purchases they make, nearly eliminating the need for cash or credit cards. These experts feel that the explosive growth in the use of smartphones and other mobile devices, combined with the convenience, security, and other affordances of mobile payments systems, makes these systems an obvious choice to replace established modes of payment in day-to-day commerce.

| 2 |

Others who do not agree with this scenario say cash and credit cards will remain the dominant method of carrying out transactions in advanced countries because the security implications raise too many concerns among consumers about the safety of their money. These consumers are also resistant to letting technology companies learn even more about their personal purchasing habits.

We believe that credit and debit card fraud will continue to be of concern to holders, even if the number of credit card holders/users continues to grow and with it the number of credit card transactions. We believe there is a significant segment of this market that will be reluctant to use their smartphone for mobile payments due to a variety of reasons including: limited battery life; dependency on wireless network coverage; and well publicized security threats.

Rather than depend solely on a smart phone, our business plan is to develop a next generation electronic smart wallet. We believe that this constitutes unique technology because it takes a very different approach relative to the current offerings: instead of replacing the wallet, our aim is to improve it. We believe that our Wocket™ wallet will reduce the number of cards to be carried in a consumer’s wallet while capable of supporting most payment methods currently available at Point-of-Sale (POS) retailers around the world including magnetic stripe, bar codes and QR codes and in the near future, Near Field Communications (NFC) all within a secure biometric vault. We believe that we can encourage individuals who are reluctant to use a smartphone for mobile payments to utilize an electronic wallet based on the security offerings that we have embedded in this product.

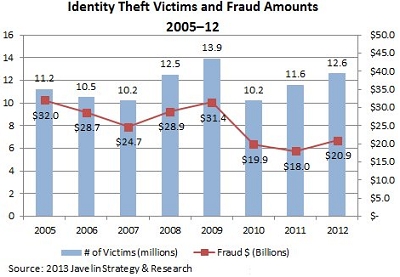

Each year approximately 12 million people in the United States are victims of identity theft and 44% of known causes of identity theft can be traced to a lost or stolen wallet or purse.

We believe that Wocket™ can significantly reduce the incidence of identity theft by concealing the card holder’s personal information on a tamper proof secure chip on the Wocket that can only be accessed by a voice biometric or PIN. Furthermore, the Wocket Card does not retain any information after the card has been swiped so, unlike the loss or theft of a wallet, the loss or theft of a Wocket or Wocket Card does not lead to a breach of personal information.

According to International Data Corporation (“IDC”), the mobile phone market on a worldwide basis approximated 1.8 billion units in 2013. Of that amount smart phones represent a large and growing segment of the market. Smart phones also typically serve as portable media players and camera phones with high-resolution touchscreen displays and web browsers that can access and properly display standard web pages, GPS navigation, Wi-Fi and mobile broadband access.

We believe that our MobileBio™ cell phone facial and voice recognition opportunity, once developed, will address a worldwide market of smart phones sales, which we believe is continuing to grow. We anticipate partnering with application providers on smartphones that have an interest in additional security for their particular application by using 3D or near 3D facial and/or voice recognition on their smartphone to gain access to a particular application; for example, touchless payment applications, banking applications and securities trading applications.

Other Uses for Facial Recognition Technology

Biometric identifiers have long been used by governments and commercial enterprises to verify a person’s identity. Signatures are an example of a behavioral biometric that has been used for centuries. With the advent of the photograph, the first paper-based physiological biometric technique was developed to verify a person’s identity. Photographs on passports and drivers licenses are obvious examples of early biometric features added to government-issued identity documents.

On the other hand, law enforcement agencies have routinely used fingerprints to positively identify suspects of a crime. In the 1990s, the use of fingerprints for criminal systems entered the digital age when the FBI awarded a contract to a team of Martin Marietta, Sagem Morpho, and Calspan (later known as the Lockheed Martin team) to build an electronic storage and search system that incorporated fingerprint files (or Integrated Automated Fingerprint Identification System - IAFIS), replacing the paper files. By capturing biometric information electronically and storing the files within a secure network for over 10 years, the U.S. government has been creating the foundation for greater use of biometrics in government and commercial activities.

| 3 |

However, terrorists and other criminals are now more capable of subverting traditional paper-based security measures through improved forgery and information-sharing technology and techniques. Furthermore, the evolution of the internet and the subsequent deviation from paper-based data storage and processes to electronic-based systems has opened the door to increased identity theft and other fraudulent activities within the commercial world.

In order to address deficiencies in current security systems used, we intend to market products that can be used by both government and commercial consumers as a viable, more powerful alternative to security measures currently being used by them. We believe that its products will contain the necessary security solutions to cover both consumer preferences with MobileBio FaceMatch® and the Wocket™ and government and commercial needs with its 3D facial recognition access control products.

Our Competition

The markets for our products are extremely competitive and are characterized by rapid technological change as a result of technical developments exploited by our competitors, changing technical needs of customers, and frequent introductions of new features. We expect competition to increase as other companies introduce products that are competitively priced, that may have increased performance or functionality, or that incorporate technological advances not yet developed or implemented by us. Some of our present and potential competitors may have financial, marketing, and research resources substantially greater than ours.

Competitors in the digital wallet marketplace include:

Google Wallet - A mobile payment system developed by Google that allows its users to store debit cards, credit cards, loyalty cards, and gift cards among other things, as well as redeeming sales promotions on their mobile phone.

Apple Pay – A mobile payment service that lets certain Apple mobile devices make payments at the time of retail and online checkout.

Paypal - A mobile service that can send money between other PayPal users and friends, track your balances, check in to pay from ones phone, and order ahead at restaurants.

LoopPay – A mobile payment system that uses Magnetic Secure Transmission to broadcast a signal to a point of sale payment terminal. This company was acquired by Samsung Electronics Co. in February 2015.

All of the above products rely on the use of a smartphone. The fundamental competitive advantage of the Wocket is that it is not smartphone dependent and is as simple to use as the swipe of a credit card. It will work in situations where there is no cell phone signal or internet connectivity. In addition the Wocket features biometric and other security features not available on a smartphone.

Other Biometric Markets

There are a number of suppliers of biometric products that deliver to the market place presently. One of the largest suppliers is L1 Identity Solutions (“L1”), which has primarily concentrated its prior efforts in the government and corporate sectors. L1 is a vertically integrated biometric solutions provider with a large established base of business and it has well developed government marketing channels. L1 was sold to Safran in 2010. Another established supplier is Cognitec, a German facial recognition company, with worldwide distribution.

Google and Apple are developing facial recognition applications for smartphones. The Google app can currently be deceived by using a photograph of the user. Apple is using a 2D to 3D conversion model which holds better promise but this is already a heavily patented area.

Rather than competing directly against these well-established entities, we plan to develop and foster market niches that would serve affordable lower priced retail consumer, small business biometric applications and end users not necessarily involved in large enterprise activities. We believe that our MobileBio™ technology that we are developing is the key to differentiating our solutions to the end user by providing what we maintain is a true end-to-end security offering using our patent-pending dynamic pairing codes that dynamically utilize identifiers that uniquely identify the user, device, manufacturer, account, location, and session or transaction, the combination of which changes periodically in real-time among all points along the communication path so that communication and data is protected 100% of the time. The biosensors that we are developing are intended to integrate with multiple devices, apps, users, operating systems, firmware, remote services and virtually any “entities” so that intercommunications with all entities, local or remote, are protected. One of the major areas of concern with facial recognition is user privacy with most companies utilizing private data for other marketing purposes. Our apps will not sell or share any personal information on the user.

We plan to offer what we believe to be unique features that will include cloud-based identity and authentication MobileBio™ management services that secure biometric authentication across mobile devices, as well as a new, innovative Facial Recognition technology and a physical alternative to current e-wallets that are embedded in smartphones.

| 4 |

The value proposition that we plan to offer customers with our versatile, simple MobileBio™ technology is complete interoperability of sensors with mobile applications and cloud-based services, which will secure the mobile money/m-commerce market by filling a versatility and flexibility gap in lacking with current solutions.

In order to compete effectively in this environment, our plan is to continually develop and market new and enhanced products at competitive prices, and have the resources to invest in significant research and development activities. There is a risk that we may not be able to make the technological advances necessary to compete successfully. Existing and new competitors may enter or expand their efforts in our markets, or develop new products to compete against ours. Our competitors may develop new technologies or enhancements to existing products or introduce new products that will offer superior price or performance features. New products or technologies may render our products obsolete. Many of our primary competitors are well-established companies that have substantially greater financial, managerial, technical, marketing, personnel and other resources than we do.

Our Business Strategy

Against the backdrop of challenges with identification of individuals, more and more mobile phones are being used as a source of payment for goods and services. We believe that worldwide mobile payment volume will continue to grow rapidly in the upcoming years.

We intend to initially market the Wocket to technology minded consumers through direct sales via our website, social media and digital marketing to websites and forums that the consumer may frequent. Thereafter we will expand our reach through distinct channel partners with widespread retail distribution. At the same time we are also seeking partnerships with corporations and financial institutions that have an interest in fraud prevention. We intend to leverage our encryption capabilities to these potential partners as well.

Worldwide, government agencies, financial, corporate and industrial entities are investing a considerable amount of resources into improving security systems as a result of ongoing security breaches which accompany acts of terrorism, financial and resource thefts that dangerously expose flaws and weaknesses in today’s safety mechanisms. Badge or password-based authentication procedures are too easy to hack. Biometrics represents a viable and robust alternative but also has potential for drawbacks as well; for example, iris scanning, while very reliable is considered too intrusive; fingerprints are socially accepted, but not applicable to non-consenting individuals and have proven to be fooled. Alternatively, facial recognition represents a good compromise between what’s socially acceptable and what’s reliable, even when operating under controlled conditions. We believe that facial recognition has emerged as one of the fastest growing technologies among the biometric technologies accepted worldwide. Facial recognition is applicable to both verification and identification. In addition, it is the only biometric system that can routinely be used in a covert manner for surveillance of uncooperative individuals as a person’s face is easily captured at a distance by video technology with or without consent.

Based on our anecdotal analysis of certain macro trends, we believe that the world-wide facial recognition market for all applications of the technology grow for the foreseeable future as consumers come to understand and adapt biometric technologies as a preferred manner for security, particularly mobile security. We believe that 3D facial recognition technology will gain traction for access control and is already being used by organizations with a high traffic volume to quickly, easily and securely authenticate users. Currently, 2D facial recognition is used primarily by law enforcement officials to identify someone by comparing their 2D image against a large database of pictures, whereas 3D facial recognition is designed primarily for verification - to confirm that someone is exactly whom they say they are. 3D face readers can also be used with PINs, access control cards and other biometric factors for multifactor authentication. 3D face recognition is as fast and accurate as fingerprint technology and is ideal in situations where workers’ hands are full or dirty, or where employees wear gloves or other applications where fingerprints would be inconvenient or difficult to obtain.

Our plans call for the positioning of its products to have applications in markets as diverse as Military and Homeland Defense, Law Enforcement, Commercial and Consumer.

For sales to the Department of Defense, we partnered with established Prime Contractors that have or are bidding for Contact vehicles through which sales may be made. Our current Partners include Battelle Memorial Institute and Verizon Federal Systems.

We currently plan for our sales to Law Enforcement Agencies to be made through distributors. Our management has several key relationships from past engagements that it is pursuing.

We intend to market the MobileBio VoiceMatch and FaceMatch® product to application providers on iPhone and Android devices that have a need to increased security because of the nature of the application. To make potential buyers aware of the product the Company will use social networks, such as Twitter, Facebook and YouTube as well as traditional PR.

Our Intellectual Property

Our ability to compete effectively depends to a significant extent on our ability to protect our proprietary information. We currently rely and will continue to rely primarily on patents and trade secret laws and confidentiality procedures to protect our intellectual property rights. We have filed two patents based on the Wocket™ and Dynamic Pairing Codes (DPC) a proprietary method used by the Company to secure users, devices, accounts, locations and servers over any communication media by sharing key identifiers, including biometric-enabled identifiers, between end-points by passing dynamic pairing codes (random numbers) between end-points to establish sessions and/or transactions without exposing identifiers or keys. We are currently in the process of applying for our third patent on multi-factor voice authentication.

| 5 |

Subsequent to the acquisition of 3D-ID, we licensed sixteen (16) U.S. patents. We enter into confidentiality agreements with our consultants and key employees, and maintain control over access to and distribution of our technology, software and other proprietary information. The steps we have taken to protect our technology may be inadequate to prevent others from using what we regard as our technology to compete with us.

We do not generally conduct exhaustive patent searches to determine whether the technology used in our products infringes patents held by third parties. In addition, product development is inherently uncertain in a rapidly evolving technological environment in which there may be numerous patent applications pending, many of which are confidential when filed, with regard to similar technologies.

We may face claims by third parties that our products or technology infringe their patents or other intellectual property rights in the future. Any claim of infringement could cause us to incur substantial costs defending against the claim, even if the claim is invalid, and could distract the attention of our management. If any of our products are found to violate third-party proprietary rights, we may be required to pay substantial damages. In addition, we may be required to re-engineer our products or seek to obtain licenses from third parties to continue to offer our products. Any efforts to re-engineer our products or obtain licenses on commercially reasonable terms may not be successful, which would prevent us from selling our products, and in any case, could substantially increase our costs and have a material adverse effect on our business, financial condition and results of operations.

Licensed Patents

| Patent Title | Serial/Patent/ Registration Number |

| Method

and Apparatus for High Resolution Three Dimensional Display |

6,064,423 |

| Omni-Directional Cameras | D436,612 |

| High

Speed Three Dimensional Imaging Method |

6,028,672 |

| Method

and System for Three-Dimensional Imaging Using Light Pattern Having Multiple Sub-Patterns |

6,700,669 |

| Method

And Apparatus for Omnidirectional Three Dimensional Imaging |

6,744,569 |

| Face Recognition System and Method | 7,221,809 |

| A System and a Method for Three-Dimensional Imaging Systems | 7,349,104 |

| Method

and Apparatus for an Interactive Volumetric Three Dimensional Display |

7,098,872 |

| Face Recognition System and Method | 7,876,931 |

| Method

and Apparatus for Omni-Directional Video Surveillance System |

7,940,299 |

| A

System and a Method for a Smart Surveillance System |

7,358,498 |

| A

High Speed Three Dimensional Imaging Method |

6,147,760 |

| Method

And Apparatus for Modeling Via a Three-Dimensional Image Mosaic System |

6,819,318 |

| Method

and System for a Three Dimensional Facial Recognition System |

7,804,997 |

| Method

and Apparatus for Omni-Directional Three-Dimensional Imaging |

6,304,285 |

| Method and Apparatus for Generating Structural Pattern Illumination | 6,937,348 |

Corporate Information

History

We were incorporated in the state of Delaware on February 8, 2012. We are a technology company with particular core competencies in biometrics that is targeting the growing m-commerce market with our innovative MobileBio™ suite of biometric solutions that are intended to secure mobile platforms. Our MobileBio™ solutions are intended to provide distinct advantages within these markets by filling a gap left by traditional biometric solutions that either are physically integrated and thus, not flexible or versatile, or provide poor interoperability between different mobile devices and insecure remote services. The Company also plans to serve the access control and law enforcement facial recognition markets.

| 6 |

Effective June 25, 2012, the Company acquired 100% of the membership interests in 3D-ID, LLC (“3D-ID”), a limited liability company formed in Florida in February 2011 and owned by the Company’s founders. Since this was a transaction between entities under common control, in accordance with Accounting Standards Codification (“ASC”) 805, “Business Combinations”, Nxt-ID recognized the net assets of 3D-ID at their carrying amounts in the accounts of Nxt-ID on the date that 3D-ID was organized, February 14, 2011.

Gino M. Pereira and David Tunnell, the founders of Nxt-ID, were an integral part of the senior management teams at Technest Holdings, an OTC Bulletin Board public company, and its subsidiary Genex Technologies. Genex Technologies was founded in 1995 to develop and commercialize the unique Rainbow® method of capturing 3D data. Since its founding Genex has developed into one of the market leaders in advanced imaging, including 3D and 360-degree technologies.

Genex has developed innovative technologies and products for all aspects of imaging, including capture, processing, display, and enhancement. Genex’s products range from 3D cameras to surveillance algorithms to integrated facial recognition systems.

Genex and Technest have won awards from the Department of Defense, National Institutes of Health (“NIH”), National Institute of Standards and Technology (“NIST”) and National Science Foundation (“NSF”) amounting to over $30 million in support of this technology.

Nxt-ID has licensed all the Technest/Genex technology (exclusively in Federal, State and Municipal applications) through the acquisition of 3D-ID to provide a product portfolio and a strong technical foundation for its further development efforts.

In addition, Nxt-ID has also licensed on a non-exclusive basis, distribution, manufacturing rights and know-how from Geometrix, a leading 3D imaging company using a different technical approach to Technest. This technology performed very favorably at the Face Recognition Vendor Test conducted by NIST. In addition, the Company has also licensed on a non-exclusive basis, distribution, manufacturing rights and technical know-how from Animetrics, an innovative facial biometric and forensics company.

Nxt-ID also has key scientific and engineering personnel that have had key roles in the development of these technologies and have an important intellectual knowledge base that the Company intends to leverage.

Other

Our principal executive offices are located at 288 Christian Street, Oxford, CT 06478, and our telephone number is (203) 266-2103. Our website address is www.nxt-id.com. The information contained therein or connected thereto shall not be deemed to be incorporated into this Report. The information on our website is not part of this Report.

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or JOBS Act. We will remain an emerging growth company for up to five years, or until the earliest of (i) the last day of the first fiscal year in which our annual gross revenue exceed $1 billion, (ii) the date that we become a ‘‘large accelerated filer’’ as defined in Rule 12b-2 under the Exchange Act, which would occur if the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter or (iii) the date on which we have issued more than $1 billion in non-convertible debt during the preceding three-year period. Pursuant to Section 102 of the JOBS Act, we have provided reduced executive compensation disclosure and have omitted a compensation discussion and analysis from this Report. Pursuant to Section 107 of the JOBS Act, we have elected to utilize the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards.

Employees

As of December 31, 2014, we had a total of 16 full-time employees, 9 in product engineering, 3 in finance and administration and 4 in customer service and product fulfillment. None of our employees is represented by a collective bargaining agreement, nor have we experienced any work stoppage. We consider our relations with our employees to be good. Our future success depends on our continuing ability to attract and retain highly qualified engineers, graphic designers, computer scientists, sales and marketing and senior management personnel. In addition, we have independent contractors whose services we are using on an as-needed basis to assist with the engineering and design of our products.

| 7 |

| Item 1A. | Risk Factors |

Our business, financial condition and operating results are subject to a number of risk factors, both those that are known to us and identified below and others that may arise from time to time. These risk factors could cause our actual results to differ materially from those suggested by forward-looking statements in this report and elsewhere, and may adversely affect our business, financial condition or operating results. If any of those risk factors should occur, moreover, the trading price of our securities could decline, and investors in our securities could lose all or part of their investment in our securities. These risk factors should be carefully considered in evaluating our prospects.

Risks Relating to our Business

We are uncertain of our ability to continue as a going concern, indicating the possibility that we may not be able to operate in the future.

To date, we have completed only the initial stages of our business plan and we can provide no assurance that we will be able to generate a sufficient amount of revenue, if at all, from our business in order to achieve profitability. It is not possible for us to predict at this time the potential success of our business. The revenue and income potential of our proposed business and operations are currently unknown. If we cannot continue as a viable entity, you may lose some or all of your investment in our Company.

The Company is an early stage entity and has incurred net losses of $7,076,609 for the year ended December 31, 2014. As of December 31, 2014, the Company had cash and stockholders’ equity of $2,201,287 and $2,735,344, respectively. At December 31, 2014, the Company had working capital of $2,579,121. Our ability to continue as a going concern is contingent upon, among other factors, our ability to raise additional cash from equity financings, secure debt financing, and/or generate revenue from the sales of our products. We cannot provide any assurance that we will be able to raise additional capital. If we are unable to secure additional capital, we may be required to curtail our research and development initiatives and take additional measures to reduce costs in order to conserve our cash in amounts sufficient to sustain operations and meet our obligations.

Our independent registered public accounting firm’s report contains an explanatory paragraph that expresses substantial doubt about our ability to continue as a going concern.

Because we are an early stage company, we expect to incur significant additional operating losses.

The Company is an early stage entity. The amount of future losses and when, if ever, we will achieve profitability are uncertain. Our current products have not generated significant commercial revenue for our Company and there can be no guarantee that we can generate sufficient revenues from the commercial sale of our products in the near future to fund our ongoing capital needs.

We have a limited operating history upon which you can gauge our ability to obtain profitability.

We have a limited operating history and our business and prospects must be considered in light of the risks and uncertainties to which early stage companies are exposed. We cannot provide assurances that our business strategy will be successful or that we will successfully address those risks and the risks described herein. Most important, if we are unable to secure future capital, we may be unable to continue our operations. We may incur losses on a quarterly or annual basis for a number of reasons, some of which may be outside our control.

If we cannot obtain additional capital required to finance our research and development efforts, our business may suffer and you may lose the value of your investment.

We may require additional funds to further execute our business plan and expand our business. If we are unable to obtain additional capital when needed, we may have to restructure our business or delay or abandon our development and expansion plans. If this occurs, you may lose part or all of your investment. We will have ongoing capital needs as we expand our business. If we raise additional funds through the sale of equity or convertible securities, your ownership percentage of our common stock will be reduced. In addition, these transactions may dilute the value of our common stock. We may have to issue securities that have rights, preferences and privileges senior to our common stock. The terms of any additional indebtedness may include restrictive financial and operating covenants that would limit our ability to compete and expand. There can be no assurance that we will be able to obtain the additional financing we may need to fund our business, or that such financing will be available on terms acceptable to us.

| 8 |

We face intense competition in our market, especially from larger, well-established companies, and we may lack sufficient financial or other resources to maintain or improve our competitive position.

A number of other companies engage in the business of developing applications for facial recognition for access control. The market for biometric security products is intensely competitive, and we expect competition to increase in the future from established competitors and new market entrants. Our current competitors include both emerging or developmental stage companies such as ourselves as well as larger companies. Many of our existing competitors have, and some of our potential competitors could have, substantial competitive advantages such as:

| ● | Greater name recognition and longer operating histories; | |

| ● | Larger sales and marketing budgets and resources; | |

| ● | Broader distribution and established relationships with distribution partners and end-customers; | |

| ● | Greater customer support resources; | |

| ● | Greater resources to make acquisitions; | |

| ● | Larger and more mature intellectual property portfolios; and | |

| ● | Substantially greater financial, technical, and other resources. |

In addition, some of our larger competitors have substantially broader product offerings and leverage their relationships based on other products or incorporate functionality into existing products to gain business in a manner that discourages users from purchasing our products, including through selling at zero or negative margins, product bundling, or closed technology platforms. Conditions in our market could change rapidly and significantly as a result of technological advancements, partnering by our competitors or continuing market consolidation. New start-up companies that innovate and large competitors that are making significant investments in research and development may invent similar or superior products and technologies that compete with our products and technology. Our current and potential competitors may also establish cooperative relationships among themselves or with third parties that may further enhance their resources.

Our markets are subject to technological change and our success depends on our ability to develop and introduce new products.

Each of the governmental and commercial markets for our products is characterized by:

| ● | Changing technologies; | |

| ● | Changing customer needs; | |

| ● | Frequent new product introductions and enhancements; | |

| ● | Increased integration with other functions; and | |

| ● | Product obsolescence. |

Our success will be dependent in part on the design and development of new products. To develop new products and designs for our target markets, we must develop, gain access to and use leading technologies in a cost-effective and timely manner and continue to expand our technical and design expertise. The product development process is time-consuming and costly, and there can be no assurance that product development will be successfully completed, that necessary regulatory clearances or approvals will be granted on a timely basis, or at all, or that the potential products will achieve market acceptance. Our failure to develop, obtain necessary regulatory clearances or approvals for, or successfully market potential new products could have a material adverse effect on our business, financial condition and results of operations.

Claims by others that we infringe their intellectual property rights could increase our expenses and delay the development of our business. As a result, our business and financial condition could be harmed.

Our industries are characterized by the existence of a large number of patents as well as frequent claims and related litigation regarding patent and other intellectual property rights. We cannot be certain that our products do not and will not infringe issued patents, patents that may be issued in the future, or other intellectual property rights of others.

We do not have the resources to conduct exhaustive patent searches to determine whether the technology used in our products infringes patents held by third parties. In addition, product development is inherently uncertain in a rapidly evolving technological environment in which there may be numerous patent applications pending, many of which are confidential when filed, with regard to similar technologies.

We may face claims by third parties that our products or technology infringe their patents or other intellectual property rights. Any claim of infringement could cause us to incur substantial costs defending against the claim, even if the claim is invalid, and could distract the attention of our management. If any of our products are found to violate third-party proprietary rights, we may be required to pay substantial damages. In addition, we may be required to re-engineer our products or obtain licenses from third parties to continue to offer our products. Any efforts to re-engineer our products or obtain licenses on commercially reasonable terms may not be successful, which would prevent us from selling our products, and, in any case, could substantially increase our costs and have a material adverse effect on our business, financial condition and results of operations.

| 9 |

We may not be able to protect our intellectual property rights adequately.

Our ability to compete for government contracts is affected, in part, by our ability to protect our intellectual property rights. We rely on a combination of patents, trademarks, copyrights, trade secrets, confidentiality procedures and non-disclosure and licensing arrangements to protect our intellectual property rights. Despite these efforts, we cannot be certain that the steps we take to protect our proprietary information will be adequate to prevent misappropriation of our technology or protect that proprietary information. The validity and breadth of claims in technology patents involve complex legal and factual questions and, therefore, may be highly uncertain. Nor can we assure you that, if challenged, our patents will be found to be valid or enforceable, or that the patents of others will not have an adverse effect on our ability to do business. In addition, the enforcement of laws protecting intellectual property may be inadequate to protect our technology and proprietary information.

We may not have the resources to assert or protect our rights to our patents and other intellectual property. Any litigation or proceedings relating to our intellectual property, whether or not meritorious, will be costly and may divert the efforts and attention of our management and technical personnel.

We also rely on other unpatented proprietary technology, trade secrets and know-how and no assurance can be given that others will not independently develop substantially equivalent proprietary technology, techniques or processes, that such technology or know-how will not be disclosed or that we can meaningfully protect our rights to such unpatented proprietary technology, trade secrets, or know-how. Although intend to enter into non-disclosure agreements with our employees and consultants, there can be no assurance that such non-disclosure agreements will provide adequate protection for our trade secrets or other proprietary know-how.

Our success will depend, in part, on our ability to obtain new patents.

To date, we have licensed sixteen (16) United States patents and our success will depend, in part, on our ability to obtain patent and trade secret protection for proprietary technology that we currently possess or that we may develop in the future. No assurance can be given that any pending or future patent applications will issue as patents, that the scope of any patent protection obtained will be sufficient to exclude competitors or provide competitive advantages to us, that any of our patents will be held valid if subsequently challenged or that others will not claim rights in or ownership of the patents and other proprietary rights held by us.

Furthermore, there can be no assurance that our competitors have not or will not independently develop technology, processes or products that are substantially similar or superior to ours, or that they will not duplicate any of our products or design around any patents issued or that may be issued in the future to us. In addition, whether or not patents are issued to us, others may hold or receive patents which contain claims having a scope that covers products or processes developed by us.

We may not have the resources to adequately defend any patent infringement litigation or proceedings. Any such litigation or proceedings, whether or not determined in our favor or settled by us, is costly and may divert the efforts and attention of our management and technical personnel. In addition, we may be required to obtain licenses to patents or proprietary rights from third parties. There can be no assurance that such licenses will be available on acceptable terms if at all. If we do not obtain required licenses, we could encounter delays in product development or find that the development, manufacture or sale of products requiring such licenses could be foreclosed. Accordingly, challenges to our intellectual property, whether or not ultimately successful, could have a material adverse effect on our business and results of operations.

We rely on a third party for licenses relating to a critical component of our technology. The failure of such licensor would materially and adversely affect our business and product offerings.

We currently license technology for a critical component of our current product offerings from a third party. The third party’s independent registered public accounting firm included an explanatory paragraph in its audit report as it relates to the third party’s ability to continue as a going concern in its recent financial statement. In the event that our licensor were to fail, it could impact our license arrangement and impede our ability to further commercialize our technology. In the event we were to lose our license or our license were to be renegotiated as a result of our licensor’s failure, our ability to manage our business would suffer and it would significantly harm our business, operating results and financial condition.

Our future success depends on the continued service of management, engineering and sales personnel and our ability to identify, hire and retain additional personnel.

Our success depends, to a significant extent, upon the efforts and abilities of members of senior management. We have entered into an employment agreement with our Chief Executive Officer, but have not entered into an employment agreement with our Chief Financial officer or Chief Technology Officer and we have no current plans to use employment agreements as a tool to attract and retain new hires that we may make of key personnel in the future. The loss of the services of one or more of our senior management or other key employees could adversely affect our business. We currently maintain a key person life insurance policy on our Chief Executive Officer only.

There is intense competition for qualified employees in our industry, particularly for highly skilled design, applications, engineering and sales people. We may not be able to continue to attract and retain developers, managers, or other qualified personnel necessary for the development of our business or to replace qualified individuals who may leave us at any time in the future. Our anticipated growth is expected to place increased demands on our resources, and will likely require the addition of new management and engineering staff as well as the development of additional expertise by existing management employees. If we lose the services of or fail to recruit engineers or other technical and management personnel, our business could be harmed.

| 10 |

The requirements of being a public company may strain our resources and divert management’s attention.

As a public company, we are subject to the reporting requirements of the Securities Exchange Act of 1934, as amended (“Exchange Act”), the Sarbanes-Oxley Act of 2002, the Dodd-Frank Act and other applicable securities rules and regulations. Compliance with these rules and regulations will increase our legal and financial compliance costs, make some activities more difficult, time-consuming, or costly, and increase demand on our systems and resources. The Exchange Act requires, among other things, that we file annual and current reports with respect to our business and operating results.

As a result of disclosure of information in this prospectus and in filings required of a public company, our business and financial condition is more visible, which we believe may result in threatened or actual litigation, including by competitors and other third parties. If such claims are successful, our business and operating results could be harmed, and even if the claims do not result in litigation or are resolved in our favor, these claims, and the time and resources necessary to resolve them, could divert resources of our management and harm our business and operating results.

Periods of rapid growth and expansion could place a significant strain on our resources, including our employee base, which could negatively impact our operating results.

We may experience periods of rapid growth and expansion, which may place significant strain and demands on our management, our operational and financial resources, customer operations, research and development, marketing and sales, administrative, and other resources. To manage our possible future growth effectively, we will be required to continue to improve our management, operational and financial systems. Future growth would also require us to successfully hire, train, motivate and manage our employees. In addition, our continued growth and the evolution of our business plan will require significant additional management, technical and administrative resources. If we are unable to manage our growth successfully we may not be able to effectively manage the growth and evolution of our current business and our operating results could suffer.

We depend on contract manufacturers, and our production and products could be harmed if it is unable to meet our volume and quality requirements and alternative sources are not available.

We rely on contract manufacturers to provide manufacturing services for our products. If these services become unavailable, we would be required to identify and enter into an agreement with a new contract manufacturer or take the manufacturing in-house. The loss of our contract manufacturers could significantly disrupt production as well as increase the cost of production, thereby increasing the prices of our products. These changes could have a material adverse effect on our business and results of operations.

Our insiders and affiliated parties beneficially own a significant portion of our stock.

As of the date of hereof, our executive officers, directors, and affiliated parties beneficially own approximately 72.3% of our common stock. As a result, our executive officers, directors and affiliated parties will have significant influence to:

| ● | Elect or defeat the election of our directors; | |

| ● | Amend or prevent amendment of our certificate of incorporation or bylaws; | |

| ● | Effect or prevent a merger, sale of assets or other corporate transaction; and | |

| ● | Affect the outcome of any other matter submitted to the stockholders for vote. |

In addition, any sale of a significant amount of our common stock held by our directors and executive officers, or the possibility of such sales, could adversely affect the market price of our common stock. Management’s stock ownership may discourage a potential acquirer from making a tender offer or otherwise attempting to obtain control of us, which in turn could reduce our stock price or prevent our stockholders from realizing any gains from our common stock.

We are presently a small company with limited resources and personnel to establish a comprehensive system of internal controls. If we fail to maintain an effective system of internal controls, we would not be able to accurately report our financial results or prevent fraud. As a result, current and potential stockholders could lose confidence in our financial reporting, which would harm our business and the trading price of our stock.

Effective internal controls are necessary for us to provide reliable financial reports and effectively prevent fraud. If we cannot provide reliable financial reports or prevent fraud, our brand and operating results would be harmed. We may in the future discover areas of our internal controls that need improvement. For example, because of size and limited resources, our external auditors may determine that we lack the personnel and infrastructure necessary to properly carry out an independent audit function. Although we believe that we have adequate internal controls for a company with our size and resources, we are not certain that the measures that we have in place will ensure that we implement and maintain adequate controls over our financial processes and reporting in the future. Any failure to implement required new or improved controls, or difficulties encountered in their implementation, would harm our operating results or cause us to fail to meet our reporting obligations. Inferior internal controls would also cause investors to lose confidence in our reported financial information, which would have a negative effect on our company and, if a public market develops for our securities, the trading price of our stock.

Our management is responsible for establishing and maintaining adequate internal control over financial reporting. Internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements in accordance with U.S. generally accepted accounting principles. A material weakness is a deficiency, or a combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of annual or interim financial statements will not be prevented or detected on a timely basis.

| 11 |

If we do not effectively manage changes in our business, these changes could place a significant strain on our management and operations.

Our ability to grow successfully requires an effective planning and management process. The expansion and growth of our business could place a significant strain on our management systems, infrastructure and other resources. To manage our growth successfully, we must continue to improve and expand our systems and infrastructure in a timely and efficient manner. Our controls, systems, procedures and resources may not be adequate to support a changing and growing company. If our management fails to respond effectively to changes and growth in our business, including acquisitions, this could have a material adverse effect on the Company’s business, financial condition, results of operations and future prospects.

We are an emerging growth company within the meaning of the Securities Act, and if we decide to take advantage of certain exemptions from various reporting requirements applicable to emerging growth companies, our common stock could be less attractive to investors.

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act, or the JOBS Act. For as long as we continue to be an emerging growth company, we may take advantage of exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies, including not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We could be an emerging growth company for up to five years, although we could lose that status sooner if our revenues exceed $1 billion, if we issue more than $1 billion in non-convertible debt in a three year period, or if the market value of our common stock held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, in which case we would no longer be an emerging growth company as of the following December 31. We cannot predict if investors will find our common stock less attractive because we may rely on these exemptions. If some investors find our common stock less attractive as a result, there may be a less active trading market for our common stock and our stock price may be more volatile.

Under the JOBS Act, emerging growth companies may also delay adopting new or revised accounting standards until such time as those standards apply to private companies. We have irrevocably elected not to avail ourselves of this exemption from new or revised accounting standards and, therefore, will be subject to the same new or revised accounting standards as other public companies that are not emerging growth companies.

We may not be able to access the equity or credit markets.

We face the risk that we may not be able to access various capital sources including investors, lenders, or suppliers. Failure to access the equity or credit markets from any of these sources could have a material adverse effect on the Company’s business, financial condition, results of operations, and future prospects.

Persistent global economic trends could adversely affect our business, liquidity and financial results.

Although improving, persistent global economic conditions, particularly the scarcity of capital available to smaller businesses, could adversely affect us, primarily through limiting our access to capital and disrupting our clients’ businesses. In addition, continuation or worsening of general market conditions in economies important to our businesses may adversely affect our clients’ level of spending and ability to obtain financing, leading to us being unable to generate the levels of sales that we require. Current and continued disruption of financial markets could have a material adverse effect on the Company’s business, financial condition, results of operations and future prospects.

We may seek or need to raise additional funds. Our ability to obtain financing for general corporate and commercial purposes or acquisitions depends on operating and financial performance, and is also subject to prevailing economic conditions and to financial, business and other factors beyond our control. The global credit markets and the financial services industry have been experiencing a period of unprecedented turmoil characterized by the bankruptcy, failure or sale of various financial institutions. An unprecedented level of intervention from the U.S. and other governments has been seen. As a result of such disruption, our ability to raise capital may be severely restricted and the cost of raising capital through such markets or privately may increase significantly at a time when we would like, or need, to do so. Either of these events could have an impact on our flexibility to fund our business operations, make capital expenditures, pursue additional expansion or acquisition opportunities, or make another discretionary use of cash and could adversely impact our financial results.

| 12 |

Although recent trends point to continuing improvements, there is still lingering volatility and uncertainty. A change or disruption in the global financial markets for any reason may cause consumers, businesses and governments to defer purchases in response to tighter credit, decreased cash availability and declining consumer confidence. Accordingly, demand for our products could decrease and differ materially from their current expectations. Further, some of our customers may require substantial financing in order to fund their operations and make purchases from us. The inability of these customers to obtain sufficient credit to finance purchases of our products and meet their payment obligations to us or possible insolvencies of our customers could result in decreased customer demand, an impaired ability for us to collect on outstanding accounts receivable, significant delays in accounts receivable payments, and significant write-offs of accounts receivable, each of which could adversely impact our financial results.

Risks Related to Our Biometric Recognition Applications and Related Products

Our biometric products and technologies may not be accepted by the intended commercial consumers of our products, which could harm our future financial performance.

There can be no assurance that our biometric systems will achieve wide acceptance by commercial consumers of such security-based products, and market acceptance generally. The degree of market acceptance for products and services based on our technology will also depend upon a number of factors, including the receipt and timing of regulatory approvals, if any, and the establishment and demonstration of the ability of our proposed device to provide the level of security in an efficient manner and at a reasonable cost. Our failure to develop a commercial product to compete successfully with existing security technologies could delay, limit or prevent market acceptance. Moreover, the market for new biometric-based security systems is largely undeveloped, and we believe that the overall demand for mobile biometric-based security systems technology will depend significantly upon public perception of the need for such a level of security. There can be no assurance that the public will believe that our level of security is necessary or that private-industry will actively pursue our technology as a means to solve their security issues. Long-term market acceptance of our products and services will depend, in part, on the capabilities, operating features and price of our products and technologies as compared to those of other available products and services. As a result, there can be no assurance that currently available products, or products under development for commercialization, will be able to achieve market penetration, revenue growth or profitability.

| 13 |

Our biometric applications may become obsolete if we do not effectively respond to rapid technological change on a timely basis.

The biometric identification and personal identification industries are characterized by rapid technological change, frequent new product innovations, changes in customer requirements and expectations and evolving industry standards. If we are unable to keep pace with these changes, our business may be harmed. Products using new technologies, or emerging industry standards, could make our technologies less attractive. If addition, we may face unforeseen problems when developing our products, which could harm our business. Furthermore, our competitors may have access to technologies not available to us, which may enable them to produce products of greater interest to consumers or at a more competitive cost.