Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - INNERWORKINGS INC | v402076_ex31-1.htm |

| EX-21.1 - EXHIBIT 21.1 - INNERWORKINGS INC | v402076_ex21-1.htm |

| EX-23.1 - EXHIBIT 23.1 - INNERWORKINGS INC | v402076_ex23-1.htm |

| EXCEL - IDEA: XBRL DOCUMENT - INNERWORKINGS INC | Financial_Report.xls |

| EX-32.1 - EXHIBIT 32.1 - INNERWORKINGS INC | v402076_ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - INNERWORKINGS INC | v402076_ex31-2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2014

Commission file number: 000-52170

INNERWORKINGS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 20-5997364 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 600 West Chicago Avenue, Suite 850 , Chicago, IL 60654 | (312) 642-3700 | |

| (Address of principal executive offices) (Zip Code) | (Registrants’ telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Stock, $0.0001 par value | Nasdaq Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨

No x

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨

No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ¨ | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

The aggregate market value of the common equity held by non-affiliates of the registrant as of June 30, 2014, the last business day of the registrant’s most recent completed second quarter, was $316,956,806 (based on the closing sale price of the registrant’s common stock on that date as reported on the Nasdaq Global Market).

As of February 25, 2014, the registrant had 53,946,282 shares of common stock, par value $0.0001 per share, outstanding which includes 1,072,005 shares of unvested restricted stock awards that have voting rights and are held by members of the Board of Directors and the Company’s employees.

DOCUMENTS INCORPORATED BY REFERENCE

The registrant intends to file with the Securities and Exchange Commission a proxy statement pursuant to Regulation 14A within 120 days of the end of the fiscal year ended December 31, 2014. Portions of such proxy statement are incorporated by reference into Part III of this Annual Report on Form 10-K.

TABLE OF CONTENTS

| 2 |

Unless otherwise indicated or the context otherwise requires, references in this Annual Report on Form 10-K to “InnerWorkings, Inc.,” “InnerWorkings,” the “Company,” “we,” “us” or “our” are to InnerWorkings, Inc., a Delaware corporation, and its subsidiaries.

Forward-Looking Statements

Certain statements in this Annual Report on Form 10-K are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These statements involve a number of risks, uncertainties and other factors that could cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by these forward-looking statements. Factors which could materially affect such forward-looking statements can be found in Part I, Item 1A entitled “Risk Factors” and Part II, Item 7 entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this Annual Report on Form 10-K. Investors are urged to consider these factors carefully in evaluating the forward-looking statements and are cautioned not to place undue reliance on such forward-looking statements. The forward-looking statements made herein are only made as of the date hereof and we undertake no obligation to publicly update such forward-looking statements to reflect subsequent events or circumstances.

| Item 1. | Business |

Our Company

We are a leading global marketing execution firm for Fortune 500 brands across a wide range of industries. As a comprehensive outsourced enterprise solution, we leverage proprietary technology, an extensive supplier network and deep domain expertise to streamline the creation, production and distribution of marketing and promotional materials, signage and displays, retail experiences, events and promotions, and product packaging across every major market worldwide. The items we source are generally procured through the marketing supply chain, and we refer to these items collectively as marketing materials. Our technology and databases of product and supplier information are designed to capitalize on excess manufacturing capacity and other inefficiencies in the traditional marketing materials supply chain to obtain favorable pricing while delivering high-quality products and services for our clients.

Our proprietary software applications and databases create a fully-integrated solution that stores, analyzes and tracks the production capabilities of our supplier network, as well as detailed pricing data. As a result, we have one of the largest independent repositories of supplier capabilities and pricing data for suppliers of marketing materials around the world. We leverage our supplier capabilities and pricing data to match our orders with suppliers that are optimally suited to meet the client’s needs at a highly competitive price.

Through our network of more than 10,000 global suppliers, we offer a full range of print, fulfillment and logistics services that allow us to procure marketing materials of virtually any kind. The breadth of our product offerings and services and the depth of our supplier network enable us to fulfill the marketing materials procurement needs of our clients. By leveraging our technology and data, our clients are able to reduce overhead costs, redeploy internal resources and obtain favorable pricing and service terms. In addition, our ability to track individual transactions and provide customized reports detailing procurement activity on an enterprise-wide basis provides our clients with greater visibility and control of their marketing materials expenditures.

We generate revenue by procuring and purchasing marketing materials from our suppliers and selling those products to our clients. We procure products for clients across a wide range of industries, such as retail, financial services, hospitality, consumer packaged goods, non-profits, healthcare, food and beverage, broadcasting and cable, and transportation. Our clients fall into two categories, enterprise and middle market. We enter into contracts with our enterprise clients to provide some, or substantially all, of their marketing materials, typically on a recurring basis. We provide marketing materials to our middle market clients on an order-by-order basis.

We were formed in 2001, commenced operations in 2002 and converted from a limited liability company to a Delaware corporation in January 2006. Our corporate headquarters are located in Chicago, Illinois. For the year ended December 31, 2014, we served more than 7,000 clients. We have increased our annual revenue from $5.0 million in 2002 to $1.0 billion in 2014, representing a compound annual growth rate of 55.5%.

As of December 31, 2014, we operated in 71 global office locations. We organize our operations into three segments based on geographic regions: North America, Latin America and EMEA. The North America segment includes operations in the United States and Canada; the Latin America segment includes operations in Mexico, South America and Central America; and the EMEA segment includes operations in the United Kingdom, continental Europe, the Middle East, Africa and Asia. We believe the opportunity exists to expand our business into new geographic markets. Our objective is to continue to increase our sales in the major markets in the United States and internationally. We intend to hire or acquire more account executives within close proximity to these large markets.

| 3 |

Industry Overview

Our business of providing marketing execution solutions primarily includes the procurement of marketing materials, branded merchandise and retail displays. Based on external sources, including Pira International, we estimate the market for marketing materials, branded merchandise and retail displays, in aggregate, to exceed $200 billion annually in the United States. With 31% of our 2014 revenues generated from our international segments, there is also significant opportunity for our marketing execution solutions outside the United States.

Procurement of marketing materials is often dispersed across several areas of a business, including sales, marketing, communications and finance. The traditional process of procuring, designing and producing an order often requires extensive collaboration by manufacturers, designers, agencies, brokers, fulfillment and other middlemen, which is highly inefficient for the customer, who typically pays a mark-up at each intermediate stage of the supply chain. Consolidating marketing activities across the organization represents an opportunity to reduce total expenditure and decrease the number of vendors in the marketing supply chain.

To become more competitive, many businesses seek to focus on their core competencies and outsource non-core business functions, which typically include marketing execution. According to a recent report issued by HfS Research Ltd, the global business process outsourcing market is expected to reach $380 billion by 2017, representing 25% growth over 2012.

We seek to capitalize on the trends impacting the marketing supply chain and the movement towards outsourcing of non-core business functions by leveraging our propriety technology, expansive database, extensive supplier network and purchasing power.

Our Solution

Utilizing our proprietary technology and data, we provide our clients a global solution to procure and deliver marketing materials at favorable prices. Our network of more than 10,000 global suppliers offers a wide variety of products and a full range of print, fulfillment and logistics services.

Our procurement software and database seeks to capitalize on excess manufacturing capacity and other inefficiencies in the traditional supply chain for marketing materials. We believe that the most competitive prices we obtain from our suppliers are offered by the suppliers with the most unused capacity. We utilize our technology to:

| • | greatly increase the number of suppliers that our clients can access efficiently; |

| • | obtain favorable pricing and deliver high quality products and services for our clients; and |

| • | aggregate our purchasing power. |

Our proprietary technology and data streamline the procurement process for our clients by eliminating inefficiencies within the traditional marketing or print supply chain and expediting production. However, our technology cannot manage all of the variables associated with procuring marketing materials, which often involves extensive collaboration among numerous parties. Effective management of the procurement process requires that dedicated and experienced personnel work closely with both clients and suppliers. Our account executives and production managers perform that critical function.

Account executives act as the primary sales staff to our clients. Production managers manage the entire procurement process for our clients to ensure timely and accurate delivery of the finished product. For each order we receive, a production manager uses our technology to gather specifications, solicit bids from the optimal suppliers, establish pricing with the client, manage production and purchase and coordinate the delivery of the finished product.

Each client is assigned an account executive and one or more production managers, who develop contacts with client personnel responsible for authorizing and making purchases. Our largest clients often are assigned multiple production managers. In certain cases, our production managers function on-site at the client. Whether on-site or off-site, a production manager functions as a virtual employee of the client. As of December 31, 2014, we had over 650 production managers, including over 300 production managers working on-site at our clients. Although our clients fall into two categories, enterprise and middle market, the production process for each client category is substantially similar.

Our Proprietary Technology

Our proprietary technology is a fully-integrated solution that stores equipment profiles for our supplier network and price data for orders we quote and execute. Our technology allows us to match orders with the suppliers in our network that are optimally suited to produce an order at a highly competitive price. Our technology also allows us to efficiently manage the critical aspects of the procurement process, including gathering order specifications, identifying suppliers, establishing pricing, managing production and coordinating purchase and delivery of the finished product.

| 4 |

Our database stores the production capabilities of our supplier network, as well as price and quote data for bids we receive and transactions we execute. As a result, we maintain one of the largest independent repositories of equipment profiles and price data for suppliers of marketing materials. Our production managers use this data to discover excess manufacturing capacity, select optimal suppliers, negotiate favorable pricing and efficiently procure high-quality products and services for our clients. We rate our suppliers based on product quality, customer service and overall satisfaction. This data is stored in our database and used by our production managers during the supplier selection process.

We believe our proprietary technology allows us to procure marketing materials more efficiently than traditional manual or semi-automated systems used by many printers and print brokers in the marketplace. Our technology includes the following features:

| • | Customized order management. Our solution automatically generates customized data entry screens based on product type and guides the production manager to enter the required job specifications. For example, if a production manager selects “envelope” in the product field, the screen will automatically prompt the production manager to specify the size, paper type, window size and placement and display style. |

| • | Cost management. Our solution reconciles supplier invoices to executed orders to ensure the supplier adhered to the pricing and other terms contained in the order. In addition, it includes checks and balances that allow us to monitor important financial indicators relating to an order, such as projected gross margin and significant job alterations. |

| • | Standardized reporting. Our solution generates transaction reports that contain quote, supplier capability, price and customer service information regarding the orders the client has completed with us. These reports can be customized, sorted and searched based on a specified time period or the type of product, price or supplier. In addition, the reports give our clients insight into their spend for each individual job and on an enterprise-wide basis, which allows the client to track the amounts it spends on job components such as paper, production and logistics. |

| • | Task-tracking. Our solution creates a work order checklist that sends e-mail reminders to our production managers regarding the time elapsed between certain milestones and the completion of specified deliverables. These automated notifications enable our production managers to focus on more critical aspects of the process and eliminate delays. |

| • | Historical price baseline. Some of our larger clients provide us with pricing data for orders they completed before they began to use our solution. For these clients, our solution automatically compares our current price for a job to the price obtained by the client for a comparable historical job, which enables us to demonstrate on an ongoing basis the cost savings we provide. |

We have created customized e-commerce stores on our client and third party platforms to order pre-selected products, such as personalized stationery, marketing brochures, and promotional products. Automated order processes can send requests to our vendors for fulfillment or printing of variable print on demand products.

Our Clients

We procure marketing materials for corporate clients across a wide range of industries, such as retail, financial services, hospitality, consumer packaged goods, non-profits, healthcare, food and beverage, broadcasting and cable, and transportation. Our clients also include printers that outsource jobs to us because they do not have the requisite capabilities or capacity to complete an order. For the year ended December 31, 2014, we served more than 7,000 clients through approximately 6,000 suppliers. For the years ended December 31, 2012, 2013 and 2014, our largest customer accounted for 8%, 5% and 6% of our revenue, respectively. Revenue from our top ten clients accounted for 32%, 30% and 28% of our revenue in 2012, 2013 and 2014, respectively.

We generate revenue by procuring and purchasing marketing materials from our suppliers and selling those products to our clients. Our clients fall into two categories, enterprise and middle market. We enter into contracts with our enterprise clients to provide some or substantially all of their marketing materials, typically on a recurring basis. Our contracts with our enterprise clients are generally for a three to five year term with a termination right upon advance notice ranging from 90 days to twelve months. For the years ended December 31, 2012, 2013 and 2014, enterprise clients accounted for 75%, 77% and 79% of our revenue, respectively. We provide marketing materials to our middle market clients on an order-by-order basis. For the years ended December 31, 2012, 2013 and 2014, middle market clients accounted for 25%, 23% and 21% of our revenue, respectively.

Our Products and Services

We offer a full range of solutions to support the marketing execution needs of our clients. Our outsourced print management solution encompasses the design, sourcing, and delivery of printed marketing materials such as direct mail, in-store signage, and marketing collateral. We provide a similar outsourced solution for the design, sourcing, and delivery of other categories in the marketing supply chain, such as branded merchandise and product packaging. We also assist clients with the management of events and promotions spending and related procurement needs. Our retail environments solution involves the design, sourcing, and installation of point of sale displays, permanent retail fixtures, and overall store design. We also offer on-site outsourced creative studio services, as well as on-demand creative services.

We offer comprehensive fulfillment and logistics services, such as kitting and assembly, inventory management and pre-sorting postage. These services are often essential to the completion of the finished product. For example, we assemble multi-level direct mailings, insurance benefits packages and coupons and promotional incentives that are included with credit card and bank statements. We also provide creative services, including copywriting, graphics and website design, identity work and marketing collateral development, and pre-media services, such as image and print-ready page processing and proofing capabilities. Our e-commerce and online collaboration technology empowers our clients with branded self-service ecommerce websites that prompt quick and easy online ordering, fulfillment, tracking and reporting.

| 5 |

We agree to provide our clients with products that conform to the industry standard of a “commercially reasonable quality” and our suppliers in turn agree to provide us with products of the same quality. The quotes we execute with our clients typically include customary provisions that limit the amount of our liability for product defects. To date, we have not experienced significant claims or liabilities relating to defective products.

Our Supplier Network

Our network of more than 10,000 global suppliers includes printers, graphic designers, paper mills and merchants, digital imaging companies, specialty binders, finishing and engraving firms, fulfillment and distribution centers and manufacturers of displays and promotional items.

These suppliers have been selected from among thousands of potential suppliers worldwide on the basis of price, quality and customer service. We direct requests for quotations to potential suppliers based on historical pricing data, quality control rankings and geographic proximity to a client or other criteria specified by our clients. In 2014, our top ten suppliers accounted for approximately 10% of our cost of goods sold, and no supplier accounted for more than 2% of our cost of goods sold.

We have established a quality control program that is designed to ensure that we deliver high-quality products and services to our clients through the suppliers in our network.

Sales and Marketing

Our account executives sell our marketing execution solutions to corporate clients. As of December 31, 2014, we had approximately 400 account executives. Our agreements with our account executives require them to market and sell our solutions on an exclusive basis and contain non-competition and non-solicitation provisions that apply during and for a specified period after the term of their service.

We expect to continue our growth by recruiting and retaining highly qualified account executives and providing them with the tools to be successful in the marketplace. There are a large number of experienced sales representatives globally and we believe that we will be able to identify additional qualified account executives from this pool of individuals. We also expect to augment our sales force through selective acquisitions of other businesses that offer marketing execution services, including print brokers that employ experienced sales personnel with established client relationships.

We believe that we offer account executives an attractive opportunity because they can utilize our vast supplier network, proprietary pricing data and customized order management solution to sell to their clients virtually any type of marketing materials at a highly competitive price. In addition, the diverse production and service capabilities of the suppliers in our network provide our account executives the opportunity to deliver a more complete product and service offering to their clients. We believe we can better attract and retain experienced account executives than our competitors because of the breadth of products offered by our supplier network.

To date, we have been successful in attracting and retaining qualified account executives. The integration process consists of training with our sales management, as well as access to a variety of sales and educational resources that are available on our intranet.

Competition

Our marketing execution solutions compete with companies in the print industry and several print-related industries, including graphics art and digital imaging and fulfillment and logistics. As a result, we compete on some level with virtually every company that is involved in printing, from printers to graphic designers, pre-press firms and fulfillment companies.

Our primary competitors are printers that employ traditional methods of marketing and selling their printed materials. The printers with which we compete generally own and operate their own printing equipment and typically serve clients only within the specific product categories and print types that their equipment produces.

We also compete with print management firms and brokers. These competitors generally do not own or operate printing equipment, and typically work with a limited number of suppliers and have minimal financial investment in the quality of the products produced for their clients. Our industry experience indicates that several of these competitors, such as Williams Lea, LogicSource and HH Global, offer print procurement services or enterprise software applications for the print industry.

The principal elements of competition in marketing materials procurement are price, product quality, customer service and reliability. Although we believe our business delivers products and services on competitive terms, our business and the marketing execution industry are relatively new and are evolving rapidly. The individuals responsible for purchasing marketing materials at our prospective clients may prefer to utilize the traditional services offered by the printers with whom we compete. Alternatively, some of these printers may elect to compete with us directly by offering procurement services or enterprise software applications, and their well-established client relationships, industry knowledge, brand recognition, financial and marketing capabilities, technical resources and pricing flexibility may provide them with a competitive advantage over us.

| 6 |

Intellectual Property

We rely primarily on a combination of copyright, trademark and trade secret laws to protect our intellectual property rights. We also protect our proprietary technology through confidentiality and non-disclosure agreements with our employees and independent contractors.

Our IT infrastructure provides a high level of security for our proprietary database. The storage system for our proprietary data is designed to ensure that power and hardware failures do not result in the loss of critical data. The proprietary data is protected from unauthorized access through a combination of physical and logical security measures, including firewalls, antivirus software, intrusion detection software, password encryption and physical security, with access limited to authorized IT personnel. In addition to our security infrastructure, our system data is backed up and stored in a redundant facility on a daily basis to prevent the loss of our proprietary data due to catastrophic failures or natural disasters. We test our overall IT recovery ability and co-location facility semi-annually and test our back-up processes quarterly to verify that we can recover our business critical systems in a timely fashion.

Employees

As of December 31, 2014, we had approximately 1,600 employees and independent contractors in more than 30 countries. We consider our employee relations to be strong.

Our Website

Our website is http://www.inwk.com. We make available, free of charge through our website, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, and Current Reports on Form 8-K, including exhibits and any amendments to those reports, filed with or furnished to the SEC. We make these reports available through our website as soon as reasonably practicable after our electronic filing of such materials with, or the furnishing of them to, the SEC. The information contained on our website is not a part of this Annual Report on Form 10-K and shall not be deemed incorporated by reference into this Annual Report on Form 10-K or any other public filing made by us with the SEC.

| 7 |

| Item 1A. | Risk Factors |

Set forth below are certain risk factors that could harm our business, results of operations and financial condition. You should carefully read the following risk factors, together with the financial statements, related notes and other information contained in this Annual Report on Form 10-K. Our business, financial condition and operating results may suffer if any of the following risks are realized. If any of these risks or uncertainties occur, the trading price of our common stock could decline and you might lose all or part of your investment. This Annual Report on Form 10-K contains forward-looking statements that contain risks and uncertainties. Please refer to the discussion of “forward-looking statements” on page one of this Annual Report on Form 10-K in connection with your consideration of the risk factors and other important factors that may affect future results described below.

Risks Related to Our Business

Competition could substantially impair our business and our operating results.

We compete with companies in the print industry and several print-related industries, including graphics art and digital imaging, and fulfillment and logistics. Competition in these industries is intense. Our primary competitors are printers that employ traditional methods of marketing and selling their printed materials. Many of these printers, such as Quad/Graphics and R.R. Donnelley, have larger client bases and significantly more resources than we do. Print buyers may prefer to utilize the traditional services offered by the printers with whom we compete. Alternatively, some of these printers may elect to offer outsourced print procurement services or enterprise software applications, and their well-established client relationships, industry knowledge, brand recognition, financial and marketing capabilities, technical resources and pricing flexibility may provide them with a competitive advantage over us.

We also compete with a number of print management firms and brokers. Several of these competitors, such as Williams Lea, LogicSource and HH Global, offer outsourced print procurement services or enterprise software applications for the print industry. These competitors, or new competitors that enter the market, may also offer print procurement services similar to and competitive with, or superior to, our current or proposed offerings and may achieve greater market acceptance. In addition, a software solution and database similar to our proprietary technology could be created over time by a competitor with sufficient financial resources and comparable experience in the print industry. If our competitors are able to offer comparable services, we could lose clients, and our market share could decline.

Our competitors may also establish cooperative relationships to increase their ability to address client needs. Increased competition may lead to revenue reductions, reduced gross margins or a loss of market share, any one of which could harm our business and our operating results.

If our services do not achieve widespread commercial acceptance, our business will suffer.

Most companies currently coordinate the procurement and management of their print orders with their own employees using a combination of telephone, facsimile, e-mail, their own technology platforms and the Internet. Growth in the demand for our services depends on the adoption of our outsourcing model for print procurement services. We may not be able to persuade prospective clients to change their traditional print management processes. Our business could suffer if our services are not accepted or are not perceived by the marketplace to be effective or valuable.

If our suppliers do not meet our needs or expectations, or those of our clients, our business would suffer.

The success of our business depends to a large extent on our relationships with our clients and our reputation for high quality marketing materials and marketing execution services. We do not own printing presses or other manufacturing equipment. Instead, we rely on third-party suppliers to deliver the products and services that we provide to our clients. As a result, we do not directly control the products manufactured or the services provided by our suppliers. If our suppliers do not meet our needs or expectations, or those of our clients, our professional reputation may be damaged, our business would be harmed and we could be subject to legal liability.

A significant portion of our revenue is derived from a relatively limited number of large clients and any loss of, or decrease in sales to, these clients could harm our results of operations.

A significant portion of our revenue is derived from a relatively limited number of large clients. Revenue from our top ten clients accounted for 32%, 30% and 28% of our revenue during the years ended December 31, 2012, 2013 and 2014, respectively. Our largest client accounted for 8%, 5% and 6% of our revenue in 2012, 2013 and 2014, respectively. We are likely to continue to experience ongoing client concentration, particularly if we are successful in attracting large enterprise clients. Moreover, there may be a loss or reduction in business from one or more of our large clients. It is also possible that revenue from these clients, either individually or as a group, may not reach or exceed historical levels in any future period. The loss or significant reduction of business from our major clients would adversely affect our results of operations.

| 8 |

A significant or prolonged economic downturn, or a dramatic decline in the demand for marketing materials, could adversely affect our revenue and results of operations.

Our results of operations are affected directly by the level of business activity of our clients, which in turn is affected by the level of economic activity and cyclicality in the industries and markets that they serve. Certain of our products are sold to industries, including the advertising, retail, consumer products, housing, financial and pharmaceutical industries, that experience significant fluctuations in demand based on general economic conditions, cyclicality and other factors beyond our control. Continued economic uncertainty or an economic downturn could result in a reduction of the marketing budgets of our clients or a decrease in the number of marketing materials that our clients order from us. Reduced demand from one of these industries or markets could adversely affect our revenues, operating income and profitability.

A decrease in the number of our suppliers could adversely affect our business.

Our suppliers are not contractually required to continue to accept orders from us. If production capacity at a significant number of our suppliers becomes unavailable, we will be required to use fewer suppliers, which could significantly limit our ability to serve our clients on competitive terms. In addition, we rely on price bids provided by our suppliers to populate our database. If the number of our suppliers decreases significantly, we may not be able to obtain sufficient pricing information for our database, which could adversely affect our ability to obtain favorable pricing for our clients and adversely affect our operating income and profitability.

We may face difficulties as we expand our operations into countries in which we have limited operating experience.

Aggregate revenue from our Latin America and EMEA segments (collectively referred to as the International segment in prior years) represented 18%, 26% and 31% of total revenue for the years ended December 31, 2012, 2013 and 2014, respectively. We intend to expand our global footprint, which may involve expanding into countries other than those in which we currently operate or increasing our operations in countries where we currently have limited operations and resources. Our business outside of the United States is subject to various risks, including:

| • | changes in economic and political conditions; |

| • | changes in and compliance with international and domestic laws and regulations, including anti-corruption laws such as the U.S. Foreign Corrupt Practices Act and the U.K. Anti-Bribery Act; |

| • | wars, civil unrest, acts of terrorism and other conflicts; |

| • | natural disasters; |

| • | compliance with and changes in tariffs, trade restrictions, trade agreements and taxations; |

| • | difficulties in managing or overseeing foreign operations; |

| • | limitations on the repatriation of funds because of foreign exchange controls; |

| • | political and economic corruption; |

| • | less developed and less predictable legal systems than those in the United States; and |

| • | intellectual property laws of countries which do not protect our intellectual property rights to the same extent as the laws of the United States. |

The occurrence or consequences of any of these factors may lead to significant legal or compliance expenses and may restrict our ability to operate in the affected region or result in the loss of clients in the affected region or other regions, which could adversely affect our revenue, operating income and profitability.

As we expand our business in foreign countries, we will become exposed to increased risk of loss from foreign currency fluctuations and exchange controls, particularly the strengthening of the U.S. dollar against major currencies, as well as longer accounts receivable payment cycles. We have limited control over these risks, and if we do not correctly anticipate changes in international economic and political conditions, we may not alter our business practices in time to avoid adverse effects.

The European economy continues to experience overall weakness as a result of lingering high unemployment, sovereign debt issues and tightening of government budgets. Continued weak economic conditions in Europe could adversely affect our results of operations in the European countries in which we conduct business. Additionally, concerns persist regarding the debt burden of certain of the countries that have adopted the euro currency (the “euro zone”) and their ability to meet future financial obligations, as well as concerns regarding the overall stability of the euro to function as a single currency among the diverse economic, social and political circumstances within the euro zone. We conduct a portion of our business in euro. Although it remains uncertain whether significant changes in utilization of the euro will occur or what the potential impact of such changes in the euro zone or globally might be, a material shift in circulation of the euro could result in disruptions to our business and negatively impact our results of operations.

If we are unable to expand the number of our account executives, or if a significant number of our account executives leave InnerWorkings, our ability to increase our revenues could be negatively impacted.

Our ability to expand our business will depend largely on our ability to attract additional account executives with established client relationships. Competition for qualified account executives can be intense and we may be unable to hire such individuals. Any difficulties we experience in expanding the number of our account executives could have a negative impact on our ability to expand our client base, increase our revenue and continue our growth.

In addition, we must retain our current account executives and properly incentivize them to obtain new clients and maintain existing client relationships. If a significant number of our account executives leave InnerWorkings and take their clients with them, our revenue could be negatively impacted. Although we have entered into non-competition agreements with our account executives, we may need to litigate to enforce our rights under these agreements, which could be time-consuming, expensive and ineffective. A significant increase in the turnover rate among our current account executives could also increase our recruiting costs and decrease our operating efficiency and productivity, which could lead to a decline in the demand for our services.

| 9 |

If we are unable to expand our enterprise client base, our revenue growth rate may be negatively impacted.

As part of our growth strategy, we seek to attract new enterprise clients and expand relationships with existing enterprise and middle market clients. If we are unable to attract new enterprise clients or expand our relationships with our existing enterprise and middle market clients, our ability to grow our business will be hindered.

Most of our clients may terminate their relationships with us on short notice and with no penalties or limited penalties.

Our middle market clients, which accounted for approximately 25%, 26% and 21% of our revenue for the years ended December 31, 2012, 2013 and 2014, respectively, typically use our services on an order-by-order basis rather than under long-term contracts. These clients have no obligation to continue using our services and may stop purchasing from us at any time. We have entered into contracts with our enterprise clients, which accounted for approximately 75%, 77% and 79% of our revenue for the years ended December 31, 2012, 2013 and 2014, respectively, that are generally for three to five year terms. Most of these contracts, however, permit the clients to terminate our engagements upon prior notice ranging from 90 days to 12 months with limited or no penalties.

The volume and type of services we provide our clients may vary from year to year and could be reduced if a client were to change its outsourcing or print procurement strategy. If a significant number of our middle market or enterprise clients elect to terminate or not to renew their engagements with us, or if the volume of their print orders decreases, our business, operating results and financial condition could suffer.

We may not be able to develop or implement new systems, procedures and controls that are required to support the anticipated growth in our operations.

Our revenue increased from $5.0 million in 2002 to $1.0 billion in 2014, representing a compound annual growth rate of 55.5%. Between January 1, 2002 and December 31, 2014, the number of our employees and independent contractors increased from 21 to approximately 1,600. Continued growth could place a significant strain on our ability to:

| • | recruit, motivate and retain qualified account executives, production managers and management personnel; |

| • | preserve our culture, values and entrepreneurial environment; |

| • | develop and improve our internal administrative infrastructure and execution standards; and |

| • | maintain high levels of client satisfaction. |

To manage our growth, we must implement and maintain proper operational and financial controls and systems. Further, we will need to manage our relationships with various clients and suppliers. We cannot give any assurance that we will be able to develop and implement, on a timely basis, the systems, procedures and controls required to support the growth in our operations or effectively manage our relationships with various clients and suppliers. If we are unable to manage our growth, our business, operating results and financial condition could be adversely affected.

Our business and stock price may be adversely affected if our internal control over financial reporting is not effective.

Section 404 of the Sarbanes-Oxley Act of 2002 requires companies to conduct a comprehensive evaluation of their internal control over financial reporting. To comply with this statute, each year we are required to document and test our internal control over financial reporting; our management is required to assess and issue a report concerning our internal control over financial reporting; and our independent registered public accounting firm is required to report on the effectiveness of our internal control over financial reporting.

In this Annual Report on Form 10-K, we reported that our internal control over financial reporting were effective as of December 31, 2014. See “Item 9A. Controls and Procedures.”

However, we cannot assure that we will not discover other material weaknesses in the future. The existence of one or more material weaknesses could result in errors in our financial statements, and substantial costs and resources may be required to rectify these or other internal control deficiencies, and may subject us to risk of litigation, for which we may incur substantial costs regardless of its outcome. If we cannot produce reliable financial reports, investors could lose confidence in our reported financial information, the market price of our common stock could decline significantly, we may be unable to obtain additional financing to operate and expand our business, and our business and financial condition could be harmed.

| 10 |

The global integration of our technology platform may result in business interruptions.

We are currently implementing a common technology platform across our global operations. The implementation of and such changes to our technology platform and related software carry risks such as cost overruns, project delays and business interruptions and delays. If we experience a material business interruption as a result of this process, it could have a material adverse effect on our business, financial position and results of operations.

Security and privacy breaches may damage client relations and inhibit our growth.

The secure and uninterrupted operation of our information technology systems is critical to our business. These systems host our own confidential information as well as third-party data, which may be targeted by sophisticated cyber attacks or other attempted intrusions. If we are the victim of a significant data security breach, or if our clients perceive that we are unable to protect the security of their confidential information, we could suffer harm to our reputation with clients, be exposed to liability, and incur significant remediation costs, which could have a material adverse effect on our business, financial position, and results of operations.

A decrease in levels of excess capacity in the commercial print industry could have an adverse impact on our business.

We believe that for the past several years the U.S. commercial print industry has experienced significant levels of excess capacity. Our business seeks to capitalize on imbalances between supply and demand in the print industry by obtaining favorable pricing terms from suppliers in our network with excess capacity. Reduced excess capacity in the print industry generally, and in our supplier network specifically, could have an adverse impact on our ability to execute our business strategy and on our business results and growth prospects.

Our inability to protect our intellectual property rights may impair our competitive position.

If we fail to protect our intellectual property rights adequately, our competitors could replicate our proprietary technology and processes and offer similar services, which would harm our competitive position. We rely primarily on a combination of trademark and trade secret laws and confidentiality and nondisclosure agreements to protect our proprietary technology. We cannot be certain that the steps we have taken to protect our intellectual property rights will be adequate or that third parties will not infringe or misappropriate our rights or imitate or duplicate our services or methodologies. We may need to litigate to enforce our intellectual property rights or determine the validity and scope of the rights of others. Any such litigation could be time-consuming and costly.

If we are unable to maintain our proprietary technology, demand for our services, and, therefore our revenue could decrease.

We rely heavily on our proprietary technology to procure marketing materials for our clients. To keep pace with changing technologies and client demands, we must correctly interpret and address market trends and enhance the features and functionality of our technology in response to these trends, which may lead to significant research and development costs. We may be unable to accurately determine the needs of print buyers or the trends in the marketing materials industry or to design and implement the appropriate features and functionality of our technology in a timely and cost-effective manner, which could result in decreased demand for our services and a corresponding decrease in our revenue.

In addition, we must protect our systems against physical damage from fire, earthquakes, power loss, telecommunications failures, computer viruses, hacker attacks, physical break-ins and similar events. Any software or hardware damage or failure that causes interruption or an increase in response time of our proprietary technology could reduce client satisfaction and decrease usage of our services.

If the key members of our management team do not remain with us in the future, our business, operating results and financial condition could be adversely affected.

Our future success will depend to a significant extent on the continued services of Eric Belcher, our Chief Executive Officer, Ryan Spohn, our Controller and interim Chief Financial Officer, John Eisel, our Chief Operating Officer, and Ron Provenzano, our General Counsel. The loss of the services of these individuals could adversely affect our business, operating results and financial condition and could divert other senior management time in searching for their replacements.

We may not be able to identify suitable acquisition candidates, effectively integrate newly acquired businesses or achieve expected profitability from acquisitions.

Part of our growth strategy is to increase our revenue and the markets that we serve through the acquisition of additional businesses. We are actively considering certain acquisitions and will likely consider others in the future. There can be no assurance that suitable candidates for acquisitions can be identified or, if suitable candidates are identified, that acquisitions can be completed on acceptable terms, if at all. Even if suitable candidates are identified, any future acquisitions may entail a number of risks that could adversely affect our business and the market price of our common stock, including the integration of the acquired operations, diversion of management’s attention, risks of entering markets in which we have limited experience, adverse short-term effects on our reported operating results, the potential loss of key employees of acquired businesses and risks associated with unanticipated liabilities.

We have used, and expect to continue to use, shares of our common stock to pay for all or a portion of our acquisitions. If the owners of potential acquisition candidates are not willing to receive our common stock in exchange for their businesses, our acquisition prospects could be limited. Future acquisitions could also result in accounting charges, potentially dilutive issuances of equity securities and increased debt and contingent liabilities, including liabilities related to unknown or undisclosed circumstances, any of which could have a material adverse effect on our business and the market price of our common stock.

| 11 |

Our business is subject to seasonal sales fluctuations, which could result in volatility or have an adverse effect on the market price of our common stock.

Our business is subject to some degree of sales seasonality. Historically, the percentage of our annual revenue earned during the third and fourth fiscal quarters has been higher due, in part, to a greater number of orders for marketing materials in anticipation of the year-end holiday season. If our business continues to experience seasonality, we may incur significant additional expenses during our third and fourth quarters, including additional staffing expenses. Consequently, if we were to experience lower than expected revenue during any future third or fourth quarter, whether from a general decline in economic conditions or other factors beyond our control, our expenses may not be offset, which would have a disproportionate impact on our operating results and financial condition for that year. Such fluctuations in our operating results could result in volatility or have an adverse effect on the market price of our common stock.

Price fluctuations in raw materials costs could adversely affect the margins on our orders.

The print industry relies on a constant supply of various raw materials, including paper and ink. Prices within the print industry are directly affected by the cost of paper, which is purchased in a price sensitive market that has historically exhibited price and demand cyclicality. Prices are also affected by the cost of ink. Our profit margin and profitability are largely a function of the rates that our suppliers charge us compared to the rates that we charge our clients. If our suppliers increase the price of our print orders, and we are not able to find suitable or alternative suppliers, our profit margin may decline.

If any of our products cause damages or injuries, we may experience product liability claims.

Clients and third parties who claim to suffer damages or an injury caused by our products may bring lawsuits against us. Defending lawsuits arising out of any of the products we provide to our clients could be costly and absorb substantial amounts of management attention, which could adversely affect our financial performance. A significant product liability judgment against us could harm our reputation and business.

If any of our key clients fails to pay for our services, our profitability would be negatively impacted.

We take full title and risk of loss for the printed products we procure from our suppliers. Our obligation to pay our suppliers is not contingent upon receipt of payment from our clients. In 2012, 2013 and 2014, our revenue was $789.6 million, $891.0 million and $1,000.1 million, respectively, and our top ten clients accounted for 32%, 30% and 28%, respectively, of such revenue. If any of our key clients fails to pay for our services, our profitability would be negatively impacted.

Our ability to raise capital in the future may be limited, and our failure to raise capital when needed could prevent us from growing.

We may in the future be required to raise capital through public or private financing or other arrangements. Such financing may not be available on acceptable terms, or at all, and our failure to raise capital when needed could harm our business. Additional equity financing may be dilutive to the holders of our common stock, and debt financing, if available, may involve restrictive covenants and could reduce our profitability. If we cannot raise funds on acceptable terms, we may not be able to grow our business or respond to competitive pressures.

Risks Related to Ownership of Our Common Stock

The trading price of our common stock has been and may continue to be volatile.

The trading prices of many small, mid-cap companies are highly volatile. Since our initial public offering in August 2006 through December 31, 2014, the closing sale price of our common stock as reported by the Nasdaq Global Market has ranged from a low of $1.92 on March 2, 2009 to a high of $18.69 on October 9, 2007.

Certain factors may continue to cause the market price of our common stock to fluctuate, including:

| • | fluctuations in our quarterly financial results or the quarterly financial results of companies perceived to be similar to us; |

| • | changes in market valuations of similar companies; |

| • | changes in economic and political conditions in the United States or abroad; |

| • | success of competitive products or services; |

| • | changes in our capital structure, such as future issuances of debt or equity securities; |

| • | announcements by us, our competitors, our clients or our suppliers of significant products or services, contracts, acquisitions or strategic alliances; |

| • | regulatory developments in the United States or foreign countries; |

| • | litigation involving our company, our general industry or both; |

| • | additions or departures of key personnel; |

| • | investors’ general perception of us; and |

| • | changes in general industry and market conditions. |

In addition, if the stock market in general experiences a loss of investor confidence, the trading price of our common stock could decline for reasons unrelated to our business, financial condition or results of operations. If any of the foregoing occurs, it could cause our stock price to fall and may expose us to class action lawsuits that, even if unsuccessful, could be costly to defend and a distraction to management. As a result, you could lose all of part of your investment.

| 12 |

Our quarterly results are difficult to predict and may vary from quarter to quarter, which may result in our failure to meet the expectations of investors and increased volatility of our stock price.

The continued use of our services by our clients depends, in part, on the business activity of our clients and our ability to meet their cost saving needs, as well as their own changing business conditions. The time between our payment to the supplier and our receipt of payment from our clients varies with each job and client. In addition, a significant percentage of our revenue is subject to the discretion of our enterprise and middle market clients, who may stop using our services at any time, subject, in the case of most of our enterprise clients, to advance notice requirements. Therefore, the number, size and profitability of jobs may vary significantly from quarter to quarter. As a result, our quarterly operating results are difficult to predict and may fall below the expectations of current or potential investors in some future quarters, which could lead to a significant decline in the market price of our stock. This may lead to volatility in our stock price. The factors that are likely to cause these variations include:

| • | the demand for our marketing execution solutions; |

| • | the use of outsourced enterprise solutions; |

| • | clients’ business decisions regarding the quantities of marketing materials they purchase; |

| • | the number, timing and profitability of our jobs, unanticipated contract terminations and job postponements; |

| • | new product introductions and enhancements by our competitors; |

| • | changes in our pricing policies; |

| • | our ability to manage costs, including personnel costs; and |

| • | costs related to possible acquisitions of other businesses. |

Concentration of ownership of our common stock among our executive officers, directors and principal stockholders may prevent investors from influencing significant corporate decisions.

As of December 31, 2014, our executive officers, directors and stockholders of more than 10% of our common stock beneficially owned or controlled approximately 37% of our common stock. If these stockholders choose to act together, they may be able to exercise significant influence over all matters requiring stockholder approval, including the election of directors, any amendments to our certificate of incorporation and significant corporate transactions. Without the consent of these stockholders, we could be delayed or prevented from entering into transactions (including the acquisition of our company by third parties) that may be viewed as beneficial to us or our other stockholders. In addition, this significant concentration of stock ownership may adversely affect the trading price of our common stock if investors perceive disadvantages in owning stock in a company with controlling stockholders.

We do not currently intend to pay dividends, which may limit the return on your investment in us.

We have not declared or paid any cash dividends on our common stock. We currently intend to retain all available funds and any future earnings for use in the operation and expansion of our business and do not anticipate paying any cash dividends in the foreseeable future.

If our board of directors authorizes the issuance of preferred stock, holders of our common stock could be diluted and harmed.

Our board of directors has the authority to issue up to 5,000,000 shares of preferred stock in one or more series and to establish the preferred stock’s voting powers, preferences and other rights and qualifications without any further vote or action by the stockholders. The issuance of preferred stock could adversely affect the voting power and dividend liquidation rights of the holders of common stock. In addition, the issuance of preferred stock could have the effect of making it more difficult for a third party to acquire, or discouraging a third party from acquiring, a majority of our outstanding voting stock or otherwise adversely affect the market price of our common stock. It is possible that we may need to raise capital through the sale of preferred stock in the future.

| Item 1B. | Unresolved Staff Comments |

None.

| 13 |

| Item 2. | Properties |

Properties

Our principal executive offices are located in Chicago, Illinois. We have 24 other office locations in the United States and 46 office locations in 36 other countries around the world. These other offices are located in Canada, Chile, Brazil, Peru, Mexico, Argentina, the United Kingdom, France, Switzerland, Denmark, Czech Republic, Germany, Ireland, Russia, China, Hong Kong, Australia and various other countries, and are principally used for sales, operations, finance, administration and warehousing. We believe that our facilities are generally suitable to meet our needs for the foreseeable future; however, we will continue to seek additional space as needed to satisfy our growth. All of the properties where we conduct our business are leased. The terms of the leases vary and have expiration dates ranging from December 31, 2014 to November 21, 2021.

| Item 3. | Legal Proceedings |

For information on our legal proceedings, see Note 10 to the Consolidated Financial Statements included in this Annual Report on Form 10-K.

| Item 4. | Mine Safety Disclosures |

Not applicable.

| 14 |

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Market Information

Our common stock is listed and traded on the Nasdaq Global Select Market under the symbol “INWK”. The following table sets forth the high and low sales prices for our common stock as reported by the Nasdaq Global Select Market for each of the periods listed.

| High | Low | |||||||

| 2013 | ||||||||

| First Quarter | $ | 15.80 | $ | 12.00 | ||||

| Second Quarter | $ | 15.16 | $ | 9.35 | ||||

| Third Quarter | $ | 12.29 | $ | 9.75 | ||||

| Fourth Quarter | $ | 10.46 | $ | 5.54 | ||||

| 2014 | ||||||||

| First Quarter | $ | 8.62 | $ | 6.79 | ||||

| Second Quarter | $ | 8.86 | $ | 6.90 | ||||

| Third Quarter | $ | 8.96 | $ | 7.80 | ||||

| Fourth Quarter | $ | 9.44 | $ | 6.56 | ||||

Holders

As of March 6, 2015, there were 50 holders of record of our common stock. The holders of our common stock are entitled to one vote per share.

Dividends

We currently do not intend to pay any dividends on our common stock. We intend to retain all available funds and any future earnings for use in the operation and expansion of our business. Any determination in the future to pay dividends will depend upon our financial condition, capital requirements, operating results and other factors deemed relevant by our board of directors, including any contractual or statutory restrictions on our ability to pay dividends.

Recent Sales of Unregistered Securities

On September 4, 2014, we issued 214,579 unregistered shares of our common stock to the sellers of Eyelevel, Inc., an Oregon corporation, and 452,092 unregistered shares of our common stock to the sellers of EYELEVEL s.r.o., a Czech Republic limited liability company, EYELEVEL Solutions Ltd., a United Kingdom limited company, EYELEVEL, LLC, a Russian limited liability company, EYELEVEL RETAIL SOLUTIONS CONSULTORIA LTDA, a Brazilian limited liability company, Taizhou EYELEVEL Store Fixtures Co., Ltd., a Chinese limited liability company, EYELEVEL Solution Pty Ltd CAN 158 690 432, an Australian proprietary limited company, and EYELEVEL Limited, a Hong Kong company. The shares were issued as partial consideration in connection with the acquisition of these companies. All such shares of common stock were issued in reliance upon the exemption from registration provided by Section 4(a)(2) of the Securities Act, as the shares were issued to the owners of a business acquired in a privately negotiated transaction not involving a public offering or solicitation.

Issuer Purchases of Equity Securities

The following table provides information relating to our purchase of shares of our common stock in fourth quarter of 2014. All these purchases reflect shares withheld upon vesting of restricted stock for minimum tax withholding obligations.

| Period | Number of Shares Purchased(1) | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs | ||||||||||||

| 10/1/14-10/31/14 | 33 | $ | 8.82 | - | - | |||||||||||

| 11/1/14-11/30/14 | 9,277 | 8.14 | - | - | ||||||||||||

| 12/1/14-12/31/14 | - | - | - | - | ||||||||||||

| Total | 9,310 | $ | 8.14 | - | - | |||||||||||

| (1) | Total number of shares delivered to us by employees to satisfy the mandatory tax withholding requirement upon vesting of restricted stock. |

On February 12, 2015, we announced that our Board of Directors approved a share repurchase program providing us authorization to repurchase up to an aggregate of $20 million of our common stock through open market and privately negotiated transactions over a two-year period. The timing and amount of any share repurchases will be determined based on market conditions, share price and other factors, and the program may be discontinued or suspended at any time. Repurchases will be made in compliance with SEC rules and other legal requirements.

| 15 |

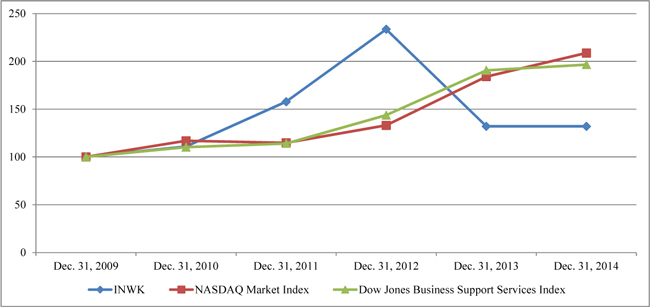

Stock Performance Graph

The information contained in the following chart is not considered to be “soliciting material,” or “filed,” or incorporated by reference in any past or future filing by the Company under the Securities Act or Exchange Act unless, and only to the extent that, the Company specifically incorporates it by reference.

The following graph assumes $100 was invested on December 31, 2009 in the common stock of the Company, and each of the following indices and assumes reinvestment of any dividends. The stock price performance on the graph below is not necessarily indicative of future stock price performance.

| Dec. 31, 2009 | Dec. 31, 2010 | Dec. 31, 2011 | Dec. 31, 2012 | Dec. 31, 2013 | Dec. 31, 2014 | |||||||||||||||||||

| INWK | $ | 100 | $ | 111 | $ | 158 | $ | 234 | $ | 132 | $ | 132 | ||||||||||||

| NASDAQ Market Index | $ | 100 | $ | 117 | $ | 115 | $ | 133 | $ | 184 | $ | 209 | ||||||||||||

| Dow Jones Business Support Services Index | $ | 100 | $ | 110 | $ | 114 | $ | 144 | $ | 191 | $ | 197 | ||||||||||||

| 16 |

| Item 6. | Selected Financial Data |

The following table presents selected consolidated financial and other data as of and for the periods indicated. You should read the following information together with the more detailed information contained in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the accompanying notes.

| Year ended December 31, | ||||||||||||||||||||

| 2010 | 2011 | 2012 | 2013 | 2014 | ||||||||||||||||

| (in thousands, except per share amounts) | ||||||||||||||||||||

| Consolidated statements of operations data: | ||||||||||||||||||||

| Revenue | $ | 482,212 | $ | 632,314 | $ | 789,585 | $ | 890,960 | $ | 1,000,133 | ||||||||||

| Cost of goods sold | 366,200 | 484,932 | 612,026 | 688,934 | 770,674 | |||||||||||||||

| Gross profit | 116,012 | 147,382 | 177,559 | 202,026 | 229,459 | |||||||||||||||

| Selling, general and administrative expenses | 91,796 | 115,818 | 146,124 | 183,443 | 195,006 | |||||||||||||||

| Depreciation and amortization | 9,009 | 10,172 | 10,790 | 13,664 | 17,723 | |||||||||||||||

| Change in fair value of contingent consideration | - | (1,702 | ) | (27,689 | ) | (31,331 | ) | (37,873 | ) | |||||||||||

| Preference claim settlement charge | - | 950 | 1,099 | - | - | |||||||||||||||

| VAT settlement charge | - | - | 1,485 | - | - | |||||||||||||||

| Goodwill impairment charge | - | - | - | 37,908 | - | |||||||||||||||

| Intangible asset impairment charges | - | - | - | - | 2,710 | |||||||||||||||

| Restructuring and other charges | - | - | - | 4,322 | - | |||||||||||||||

| Income (loss) from operations | 15,207 | 22,144 | 45,750 | (5,980 | ) | 51,893 | ||||||||||||||

| Gain on sale of investments | 3,578 | 3,948 | 1,196 | - | - | |||||||||||||||

| Interest income | 151 | 182 | 66 | 76 | 57 | |||||||||||||||

| Interest expense | (1,928 | ) | (2,251 | ) | (2,438 | ) | (2,954 | ) | (4,428 | ) | ||||||||||

| Other, net | (49 | ) | - | 94 | (357 | ) | (747 | ) | ||||||||||||

| Total other income (expense) | 1,752 | 1,879 | (1,082 | ) | (3,235 | ) | (5,118 | ) | ||||||||||||

| Income (loss) before income taxes | 16,959 | 24,023 | 44,668 | (9,215 | ) | 46,775 | ||||||||||||||

| Income tax expense (benefit) | 5,749 | 7,407 | 5,874 | (556 | ) | 2,313 | ||||||||||||||

| Net income (loss) | $ | 11,210 | $ | 16,616 | $ | 38,794 | $ | (8,659 | ) | $ | 44,462 | |||||||||

| Net income (loss) per share of common stock: | ||||||||||||||||||||

| Basic | $ | 0.25 | $ | 0.36 | $ | 0.79 | $ | (0.17 | ) | $ | 0.85 | |||||||||

| Diluted | $ | 0.24 | $ | 0.34 | $ | 0.76 | $ | (0.17 | ) | $ | 0.84 | |||||||||

| Shares used in per share calculations: | ||||||||||||||||||||

| Basic | 45,704 | 46,428 | 48,811 | 50,875 | 52,095 | |||||||||||||||

| Diluted | 47,582 | 48,818 | 51,240 | 50,875 | 53,104 | |||||||||||||||

| As of December 31, | ||||||||||||||||||||

| 2010 | 2011 | 2012 | 2013 | 2014 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Consolidated balance sheet data: | ||||||||||||||||||||

| Cash and cash equivalents | $ | 5,259 | $ | 13,219 | $ | 17,219 | $ | 18,606 | $ | 22,578 | ||||||||||

| Working capital(1) | 64,982 | 65,815 | 84,489 | 57,766 | 95,160 | |||||||||||||||

| Total assets | 279,925 | 457,653 | 514,780 | 614,667 | 631,250 | |||||||||||||||

| Revolving credit facility(2) | 47,400 | 60,000 | 65,000 | 69,000 | 104,539 | |||||||||||||||

| Capital leases | 28 | 65 | - | - | - | |||||||||||||||

| Total stockholders’ equity | 160,184 | 181,725 | 242,952 | 245,442 | 296,147 | |||||||||||||||

| (1) | Working capital represents accounts receivable, unbilled revenue, inventories, prepaid expenses and other current assets, offset by accounts payable, accrued expenses and other current liabilities. |

| (2) | The Company entered into a Credit Agreement, dated as of August 2, 2010, subsequently amended most recently as of September 25, 2014 to fund acquisitions and for general working capital purposes. |

| 17 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The following discussion should be read in conjunction with the consolidated financial statements and accompanying notes, which appear elsewhere in this Annual Report on Form 10-K. It contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of various factors, including those discussed below and elsewhere in this Annual Report on Form 10-K, particularly in Part I, Item 1A “Risk Factors.”

Overview

We are a leading global marketing execution firm for Fortune 500 brands across a wide range of industries. As a comprehensive outsourced enterprise solution, we leverage proprietary technology, an extensive supplier network and deep domain expertise to streamline the creation, production and distribution of marketing and promotional materials, signage and displays, retail experiences, events and promotions, and product packaging across every major market worldwide. The items we source are generally procured through the marketing supply chain, and we refer to these items collectively as marketing materials. Our technology and databases of product and supplier information are designed to capitalize on excess manufacturing capacity and other inefficiencies in the traditional marketing materials supply chain to obtain favorable pricing while delivering high-quality products and services for our clients. Since 2002, we have expanded from a regional focus to a national and now global focus.

Our proprietary software applications and databases create a fully-integrated solution that stores, analyzes and tracks the production capabilities of our supplier network, as well as detailed pricing data. As a result, we have one of the largest independent repositories of supplier capabilities and pricing data for suppliers of marketing materials around the world. We leverage our supplier capabilities and pricing data to match our orders with suppliers that are optimally suited to meet the client’s needs at a highly competitive price.

Through our network of more than 10,000 global suppliers, we offer a full range of print, fulfillment and logistics services that allow us to procure marketing materials of virtually any kind. The breadth of our product offerings and services and the depth of our supplier network enable us to fulfill the marketing materials procurement needs of our clients. By leveraging our technology and data, our clients are able to reduce overhead costs, redeploy internal resources and obtain favorable pricing and service terms. In addition, our ability to track individual transactions and provide customized reports detailing procurement activity on an enterprise-wide basis provides our clients with greater visibility and control of their marketing materials expenditures.

We generate revenue by procuring and purchasing products from our suppliers and selling those products to our clients. We procure products for clients across a wide range of industries, such as retail, financial services, hospitality, consumer packaged goods, non-profits, healthcare, food and beverage, broadcasting and cable, and transportation. Our clients fall into two categories, enterprise and middle market. We enter into contracts with our enterprise clients to provide some, or substantially all, of their marketing materials, typically on a recurring basis. We provide marketing materials to our middle market clients on an order-by-order basis.

We were formed in 2001, commenced operations in 2002 and converted from a limited liability company to a Delaware corporation in January 2006. Our corporate headquarters are located in Chicago, Illinois. As of December 31, 2014, we had approximately 1,600 employees and independent contractors in more than 30 countries. We organize our operations into three segments based on geographic regions: North America, Latin America and EMEA. In 2014, we generated global revenue from third parties of $688.9 million in the North America segment, $99.7 million in the Latin America segment and $211.5 million in the EMEA segment. We believe the opportunity exists to expand our business into new geographic markets. Our objective is to continue to increase our sales in the major print markets in the United States and internationally. We intend to hire or acquire more account executives within close proximity to these large markets.

Revenue