Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - China Biologic Products Holdings, Inc. | v400524_ex32-2.htm |

| EX-23.1 - EXHIBIT 23.1 - China Biologic Products Holdings, Inc. | v400524_ex23-1.htm |

| EX-31.2 - EXHIBIT 31.2 - China Biologic Products Holdings, Inc. | v400524_ex31-2.htm |

| EXCEL - IDEA: XBRL DOCUMENT - China Biologic Products Holdings, Inc. | Financial_Report.xls |

| EX-31.1 - EXHIBIT 31.1 - China Biologic Products Holdings, Inc. | v400524_ex31-1.htm |

| EX-32.1 - EXHIBIT 32.1 - China Biologic Products Holdings, Inc. | v400524_ex32-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 31, 2014

¨

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to _____________

Commission File No. 001-34566

CHINA BIOLOGIC PRODUCTS, INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

75-2308816 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

18th Floor, Jialong International Building,

19 Chaoyang Park Road

Chaoyang District, Beijing 100125

People’s Republic of China

(Address of principal executive offices)

(+86) 10-6598-3111

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

|

Common Stock, par value $0.0001 per share Preferred Share Purchase Rights |

NASDAQ Global Select Market NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Exchange Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files) Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large Accelerated Filer ¨ |

Accelerated Filer x |

| Non-Accelerated Filer ¨ (Do not check if a smaller reporting company) |

Smaller reporting company ¨ |

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of common stock held by non-affiliates of the registrant, based upon the closing sale price on June 30, 2014 as reported on the NASDAQ Global Select Market, was approximately $358 million.

There were a total of 24,811,792 shares of the registrant’s common stock outstanding as of March 4, 2015.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Proxy Statement for its 2015 Annual Meeting of Stockholders to be filed with the Commission within 120 days after the close of the Registrant’s fiscal year are incorporated by reference into Part III of this Annual Report on Form 10-K.

| Annual Report on Form 10-K |

| Year Ended December 31, 2014 |

TABLE OF CONTENTS

Special Note Regarding Forward Looking Statements

In addition to historical information, this report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. We use words such as “believe,” “expect,” “anticipate,” “project,” “target,” “plan,” “optimistic,” “intend,” “aim,” “will” or similar expressions which are intended to identify forward-looking statements. Such statements include, among others, those concerning market and industry segment growth and demand and acceptance of new and existing products; expectations regarding governmental approvals of our new products; any projections of sales, earnings, revenue, margins or other financial items; any statements of the plans, strategies and objectives of management for future operations; any statements regarding future economic conditions or performance; as well as all assumptions, expectations, predictions, intentions or beliefs about future events. You are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, as well as assumptions, which, if they were to ever materialize or prove incorrect, could cause the results of the Company to differ materially from those expressed or implied by such forward-looking statements. Risks and uncertainties that could cause actual results to differ materially from those anticipated include risks related to, among others, our ability to overcome competition from local and international pharmaceutical enterprises; decrease in the availability, or increase in the cost, of plasma; failure to renew plasma collection permits for plasma stations; failure to meet the GMP standard or other mandatory requirements for any of our facilities; failure to obtain PRC governmental approval to increase retail prices of certain of our biopharmaceutical products; loss of key members of our senior management; and unexpected changes in the PRC government’s regulation of the biopharmaceutical industry in China, or changes in China’s economic situation and legal environment. Additional disclosures regarding factors that could cause our results and performance to differ from results or performance anticipated by this report are discussed in Item 1A “Risk Factors.”

Readers are urged to carefully review and consider the various disclosures made by us in this report and our other filings with the SEC. These reports attempt to advise interested parties of the risks and factors that may affect our business, prospects, financial condition and results of operations. The forward-looking statements made in this report speak only as of the date hereof and we disclaim any obligation, except as required by law, to provide updates, revisions or amendments to any forward-looking statements to reflect changes in our expectations or future events.

Use of Terms

Except as otherwise indicated by the context and for the purposes of this report only, references in this report to:

| · | “China Biologic,” “we,” “us,” the “Company,” or “our” are to the combined business of China Biologic Products, Inc., a Delaware corporation, and its direct and indirect subsidiaries; |

| · | “China” or “PRC” are to the People’s Republic of China, excluding, for the purposes of this report only, Taiwan and the special administrative regions of Hong Kong and Macau; |

| · | “CFDA” are to China Food and Drug Administration; |

| · | “Exchange Act” are to the Securities Exchange Act of 1934, as amended; |

| · | “GMP” are to good manufacturing practice; |

| · | “Guizhou Taibang” are to our majority owned subsidiary Guizhou Taibang Biological Products Co., Ltd., a PRC company, formerly known as Guiyang Qianfeng Biological Products Co., Ltd.; |

| · | “Huitian” are to Xi’an Huitian Blood Products Co., Ltd., a PRC company in which we hold a minority equity interest; |

| · | “NDRC” are to the PRC National Development and Reform Commission; |

| 1 |

| · | “New GMP Standard” are to the Drug Good Manufacturing Practice Regulations enacted by China’s Ministry of Health on February 12, 2001 and the Good Manufacturing Practice Implementation Guidelines published by CFDA on February 24, 2011; |

| · | “RMB” are to the legal currency of China; |

| · | “SEC” are to the Securities and Exchange Commission; |

| · | “Securities Act” are to the Securities Act of 1933, as amended; |

| · | “Shandong Taibang” are to our majority owned subsidiary Shandong Taibang Biological Products Co. Ltd., a PRC company; |

| · | “Taibang Biological” are to Taibang Biological Ltd., a British Virgin Islands company, formerly known as Logic Express, Ltd.; |

| · | “Taibang Holdings” are to Taibang Holdings (Hong Kong) Limited, a Hong Kong company, formerly known as Logic Holdings (Hong Kong) Limited; and |

| · | “U.S. dollars” or “$” are to the legal currency of the United States. |

| 2 |

OVERVIEW

We are a biopharmaceutical company principally engaged in the research, development, manufacturing and sales of human plasma-based biopharmaceutical products in China. We are the largest non-state-owned producer of plasma products and the second largest producer in China in terms of 2014 sales, based on our industry knowledge. We operate our business through two majority owned subsidiaries, Shandong Taibang, a company based in Tai’an, Shandong Province and Guizhou Taibang, a company based in Guiyang, Guizhou Province. We also hold a minority equity interest in Huitian, a plasma products company based in Xi’an, Shaanxi Province.

We have a strong product portfolio with over 20 different dosage forms of plasma products. Our principal products are human albumin and immunoglobulin for intravenous injection, or IVIG. Albumin has been used for almost 50 years to treat critically ill patients by assisting the maintenance of adequate blood volume and pressure. IVIG is used for certain disease prevention and treatment by enhancing specific immunity. These products use human plasma as their principal raw material. Sales of human albumin products represented approximately 39.3%, 44.1% and 44.6% of our total sales for 2014, 2013 and 2012, respectively. Sales of IVIG products represented approximately 40.4%, 38.0% and 39.0% of our total sales for 2014, 2013 and 2012, respectively. All of our products are prescription medicines administered in the form of injections.

Our sales model focuses on direct sales to hospitals and inoculation centers and is complemented by distributor sales. In 2014, we generated sales of $243.3 million, an increase of 19.6% from 2013, and recorded net income attributable to the Company of $70.9 million, an increase of 29.9% from 2013. In 2013, we generated sales of $203.4 million, an increase of 10.0% from 2012, and recorded net income attributable to the Company of $54.6 million, an increase of 20.7% from 2012.

We operate and manage our business as one single segment. We do not account for the results of our operations on a geographic or other basis.

Corporate History and Structure

China Biologic Products, Inc. was originally incorporated on December 20, 1989 under the laws of the State of Texas as Shepherd Food Equipment, Inc. On November 20, 2000, Shepherd Food Equipment, Inc. changed its corporate name to Shepherd Food Equipment, Inc. Acquisition Corp., or Shepherd. Shepherd is the survivor of a May 28, 2003 merger between Shepherd and GRC Holdings, Inc., or GRC, a Texas corporation. In the merger, the surviving corporation adopted the articles of incorporation and bylaws of GRC and changed its corporate name to GRC Holdings, Inc. On January 10, 2007, a plan of conversion became effective pursuant to which GRC was converted into a Delaware corporation and changed its name to China Biologic Products, Inc. On July 19, 2006, we completed a reverse acquisition with Logic Express Ltd., or Logic Express, a British Virgin Islands company, as a result of which Logic Express became our wholly owned subsidiary, the former shareholders of Logic Express became our then controlling stockholders, and Logic Express’s majority owned PRC subsidiary, Shandong Taibang, became our majority owned indirect subsidiary. Logic Express changed its corporate name to Taibang Biological Limited in 2006.

Our common stock was initially quoted on the over-the-counter market maintained by Pink Sheets LLC. On February 29, 2008, our common stock was approved for quotation on the Over-The-Counter Bulletin Board under the trading symbol “CBPO.OB.” On November 25, 2009, our common stock was approved for listing on the NASDAQ Global Market under the symbol “CBPO” and subsequently approved for listing on the NASDAQ Global Select Market on December 7, 2010.

| 3 |

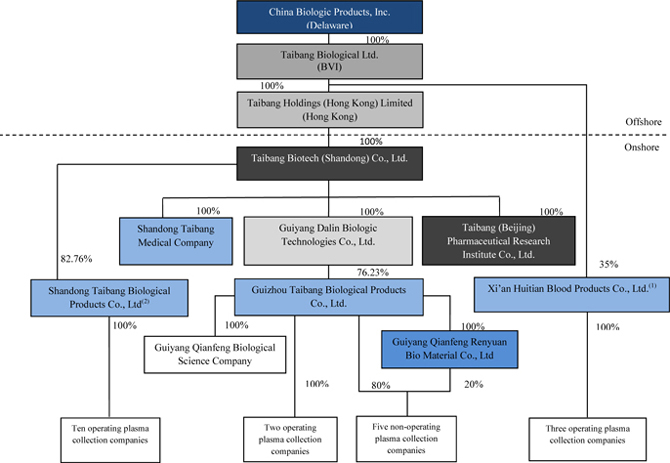

The following chart reflects our current corporate structure as of the date of this prospectus supplement:

| (1) | Pursuant to an investment entrustment agreement dated September 12, 2008, Shandong Taibang holds the 35% equity interest in Huitian as a nominee for the benefit of Taibang Biological. For further details on the investment entrustment agreement, see our Current Report on Form 8-K filed with the SEC on October 16, 2008. |

| (2) | In February 2015, Taibang Holdings transferred its 82.76% equity interest in Shandong Taibang to Taibang Biotech (Shandong) Co., Ltd. |

INDUSTRY

Overview

We operate in the plasma industry in China. We derive certain industry related data from a China-specific report prepared by The Marketing Research Bureau, Inc., or MRB, for 2012, which was published in December 2013, and a commissioned report prepared by MRB in June 2014. MRB is an independent research firm focused on blood and plasma industry data on a global level.

| 4 |

China is the second largest plasma products market in the world, after the United States. According to MRB, China’s plasma products market (excluding recombinant products) grew from $0.43 billion in 2006 to $1.66 billion in 2012 in terms of sales revenue, representing a compound annual growth rate, or CAGR, of 25.5%. Based on our industry knowledge, human albumin products dominated China’s plasma products market with a market share of 69.1% in terms of sales revenue in 2014 while IVIG and hyper immunoglobulin products accounted for 22.4% and 5.9%, respectively, of the market. Other plasma products, including coagulation factors, accounted for the remaining 2.6% of the market in 2014. Compared to the more developed countries, China has a lower per capita usage level of plasma products, and China’s plasma products market is significantly different in terms of product composition and range. In more developed countries such as the United States, IVIG products account for a majority of plasma product sales. This difference is mainly due to the maturity levels of the plasma industries in these countries. For instance, plasma fractionation came into existence in the 1940s in the United States, whereas in China, plasma processing appeared in the 1960s or 1970s, according to MRB. Until the early 1970s, the U.S. plasma products market was dominated by albumin products, as is the case in the Chinese market presently. The current low per-capita consumption of IVIG products in China is primarily attributable to a lack of awareness of the benefits of IVIG therapy, especially in medical conditions such as primary immune deficiency or chronic inflammatory demyelinating polyneuropathy, and lower per capita healthcare spending conditions in China. China’s plasma products market is expected to be increasingly driven by IVIG products in the future as IVIG therapy becomes more widespread as a result of the combined efforts of physician education and product promotion, among other factors.

Based on our industry knowledge, China National Biotec Group, or CNBG, a state-owned enterprise, was China’s largest plasma products manufacturer with a market share of 10.7% in terms of sales revenue of plasma products in 2014. China Biologic was the second largest plasma products manufacturer and the largest non-state-owned manufacturer, with a market share of 8.2% in terms of sales revenue of plasma products in 2014.

Overall Plasma Products Market Trends

According to MRB, China’s plasma products market has grown from $0.80 billion in 2009 to $1.66 billion in 2012 in terms of sales revenue, representing a CAGR of 27.5%. Key market characteristics and trends of China’s plasma products market include the following:

Stringent regulation and high entry barriers. China’s plasma products market is stringently regulated. Because of the public health crises of contaminated plasma products experienced by China over the past decade, China has and is expected to continue to maintain stringent regulations for the plasma products industry in the foreseeable future. The PRC State Council ceased issuing new plasma fractionation licenses since 2001, and there are approximately 30 licensed producers of plasma products in China, of which only no more than 25 are currently in operation. Nearly all of these producers make albumin and IVIG products, and only four of them, including China Biologic, make factor VIII products. Furthermore, foreign investment in domestic producers of plasma products is restricted and subject to a stringent approval process. As a result, existing China-based producers with large production capacities face limited competition and are uniquely positioned.

Demand outstripping supply. Due to stringent regulations on the collection of raw plasma from human beings and a lack of plasma donation, there has been a shortage of plasma products in China since the 1980s. Plasma product manufacturers sell their products at or near the maximum retail reimbursement price and generally do not engage in export sales. In the case of factor VIII products, the supply shortage is demonstrated by the growth of recombinant products which are sold at three times the price as plasma-derived factor VIII products. In 2010, the PRC Ministry of Health estimated that China’s market demand for plasma products was 8,000 tonnes per annum while domestic supply only met approximately half of such demand. The gap between demand and supply enhances pricing power for market leading producers, and it is expected that such gap will likely to continue in the foreseeable future.

| 5 |

Ban on imports. As a measure to prevent a range of viral risks, China strictly prohibits the importation of plasma products, except for human albumin and recombinant factor VIII products. In those market segments, such as IVIG, where importation is prohibited, domestic producers are shielded from competition from their multinational peers, and the demand for such products in China has been supplied entirely by domestically-sourced plasma.

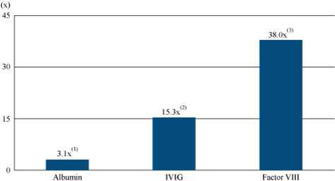

Low consumption level and huge growth potential. While China’s plasma products market has experienced rapid growth in recent years, China’s per capita consumption of plasma products lags substantially behind more developed countries. The following chart sets forth the comparison of per capita consumptions of selected plasma products in China and the United States in 2012:

Source: MRB

| (1) | Based on 2012 per capita consumption (kilogram per million inhabitants) in the Unites States divided by 2012 per capita consumption in China. |

| (2) | Based on 2012 per capita consumption (kilogram per million inhabitants) in the Unites States divided by 2012 per capita consumption in China. |

| (3) | Based on 2012 per capita consumption (International Units per inhabitant) in the Unites States divided by 2012 per capita consumption in China. |

As a result of growing number of patients desiring treatment of plasma products, increasing awareness of health benefits of plasma products and rising affordability of plasma products since the commencement of China’s healthcare reform, it is projected that China’s plasma products market will continue to have substantial growth potential.

Increasing market concentration of top players. China’s current landscape of plasma products producers is relatively fragmented. However, factors such as stringent regulations, tightened quality control and heavy capital expenditure requirements have contributed to increasing industry consolidation in recent years. For instance, CFDA recently issued new GMP requirements to re-certify all the fractionation plants by the end of 2013, which has resulted in the shutdown of smaller fractionation plants that were unable to upgrade their production lines by the deadline. Market leaders with stable plasma supplies complemented by further collection expansion potentials, strong product portfolios and robust research and development capabilities are expected to be able to continue to solidify their positions and further gain development advantages.

Albumin Market Trends

According to MRB, human albumin products accounted for a majority of China’s plasma products market in 2012, which was approximately 40% larger than the albumin products market in the United States. According to MRB, China’s albumin products market grew from $406.5 million in terms of sales revenue in 2009 to $945.2 million in 2012, representing a CAGR of 32.5%.

| 6 |

The demand for albumin products in China was high and continued to grow as a result of the high incidence of hypoalbumiemia from liver cirrhosis and hepatitis B. Unlike many other plasma products, albumin products may be imported from other countries, and as a result many multinational plasma product manufacturers are expected to increasingly divert a large portion of their albumin products to China’s market in the future so long as the price in China remains competitive. Based on our industry knowledge, the largest four multinational plasma product manufacturers accounted for approximately 56% of China’s albumin products market in 2014, with CSL Behring as the market leader with a market share of 24.5% in terms of sales volume. CNBG, Shanghai RAAS Blood Products Co., Ltd., and China Biologic were the largest three domestic albumin product manufacturers with a market share of 8.0%, 5.4% and 5.3%, respectively, in terms of sales volume in 2014. Based on our industry knowledge, the combined local and imported albumin supplies did not fully meet the demand in China in 2014.

IVIG Market Trends

According to MRB, China’s IVIG products market grew from $296.8 million in terms of sales revenue in 2009 to $469.5 million in 2012, representing a CAGR of 16.5%. Based on our industry knowledge, CNBG was the market leader with a market share of 19.8% in terms of sales volume in 2014, and China Biologic ranked second with a market share of 15.4%.

In more developed countries, the major applications of IVIG therapy are for chronic diseases such as primary immune deficiency and chronic inflammatory demyelinating polyneuropathy, which require treatment for a number of years or even lifetime. In contrast, in China, IVIG therapy is only used to treat acute diseases and infections. The substantial growth in China’s IVIG products market in recent years was mainly due to the IVIG therapy for Hand, Foot and Mouth Disease, which is rare and less known in more developed countries. Compared with the markets in these countries, China’s IVIG products market is far from mature. In 2012, for instance, the per-capita consumption of IVIG products in China was 11 grams per 1,000 inhabitants, as compared to 168 grams per 1,000 inhabitants in the United States, according to MRB, and therefore there is tremendous growth potential as China’s IVIG consumption draws closer to that of the United States. Developing this market requires significant efforts from IVIG manufacturers to educate physicians, the public and the health authorities on the benefits of IVIG therapy for a number of medical conditions. In countries with higher per-capita consumption of IVIG products, the efficacy of IVIG therapy in a number of medical conditions was promoted by the following means over the years: clinical trials, anecdotal reports, scientific articles, educational activities for physicians and medical students, medical conferences and seminars, and promotional campaigns such as advertisements in medical journals. The role of a specialized sales force was also instrumental in the rapid acceptance of IVIG therapy in North America and Europe. In addition, patient organizations, which are largely supported by IVIG manufacturers, have also become increasingly important in recent years, as they are able to draw physicians’ attention to antibody deficiency tests. All of these factors may be replicated in China as a result of IVIG manufacturers’ educational and promotional efforts as well as economic development and healthcare spending growth in China.

Factor VIII Market Trends

According to MRB, China’s market size for plasma-derived factor VIII was $19.2 million in terms of sales revenue in 2012, as compared to $10.6 million in 2009, representing a CAGR of 21.9%.

Based on our industry knowledge, only four domestic plasma product manufacturers offered plasma-derived factor VIII in 2014. Hualan Biological Engineering Inc. was the market leader with a market share of 42.0% in terms of sales volume (excluding recombinant factor VIII products) in 2014.

| 7 |

There were over 10,000 registered patients of hemophilia in China as of December 31, 2014, according to China Hemophilia Association, which underpins a significant market demand for factor VIII products. Due to an acute shortage of plasma-derived coagulation factor concentrates available in China as a result of limited coagulation factor manufacturers, recombinant factor VIII products have taken a growing role in hemophilia care in China. However, since recombinant products are approximately three times more expensive than plasma-derived factor VIII products and not covered by national health insurance for full reimbursement in China, they are used only in the absence of suitable plasma-derived products. As an increasing number of China-based manufacturers, including China Biologic, commercially launched factor VIII products, the supply is expected to increase and lead to overall market growth. It is unlikely, however, that plasma-derived factor VIII will be able to fully meet the market demand if hemophilia care continues to improve in China. China’s market for factor VIII products is expected to experience a continued shortage of plasma-derived factor VIII products in the foreseeable future.

BUSINESS

Our Competitive Strengths

We believe that the following competitive strengths enable us to compete effectively in and capitalize on the growth of the plasma products market:

Leading producer of plasma products in China with strong market position

We are the largest non-state-owned producer of plasma products and the second largest producer in China in terms of 2014 sales based on our industry knowledge. In the albumin segment, which accounts for a majority of the market in China, we are the third largest domestic producer with a market share of 5.3% in terms of 2014 sales based on our industry knowledge. In the IVIG segment, which is the second largest segment of the plasma products market in China, we are the second largest producer overall in China with a market share of 15.4% in terms of 2014 sales based on our industry knowledge.

We have a strong product portfolio with over 20 different dosage forms of plasma products crossing nine categories. Since different types of plasma products utilize different protein components of plasma, different types of plasma products can be produced from the same raw plasma supply with minimal incremental increase in raw material cost. Our broad product portfolio therefore provides us with the benefit of higher comprehensive plasma utilization, which in turn contributes to higher profit margins.

We believe product safety and supply stability are the most critical considerations for hospitals and inoculation centers in making purchase decisions on plasma products. We have not historically experienced any issue of failing to receive pre-sale approval or had a recall with respect to any of our plasma products. As a leading producer of plasma products, we have been able to maintain a steady plasma supply volume and sales volume over the years. Our safety record and the stability of our supply, we believe, have strengthened our business relationship with existing customers and enhanced our ability to acquire new customers.

Stable supply of plasma with strategically located collection stations

Our ability to secure and expand our supply of plasma, a critical raw material for our operations, is one of our key strengths. Our plasma collection network consists of 12 captive plasma stations. In 2014, we were the second largest plasma collector in China in terms of collection volume with approximately 14% of the total national supply, based on our industry knowledge.

| 8 |

We operate eight plasma collection stations in Shandong Province, two in Guangxi Province and two in Guizhou Province, covering 31 cities and counties with an aggregate population of approximately 38.4 million. Shandong Province has one of the largest population and Guangxi Province and Guizhou Province are among the least economically developed regions in China — both favorable characteristics underpinning a strong and stable plasma supply.

We continue to seek innovative ways to identify and attract potential donors. Our messages focus on the life-saving and other social contribution aspects of plasma donation. To this end, we regularly organize a variety of community events, while also regularly reviewing our donor compensation to ensure that it remains competitive. In addition, we actively seek to expand the geographic territories of our existing collection stations to gain access to additional donor populations. As a result of our activities, our plasma collection volume increased 12% from 2013 to 2014.

Unique and effective sales model targeting hospitals

Our sales model focuses on direct sales to hospitals and inoculation centers and is complemented by distributor sales, which we believe is unique in the industry. Under this sales model, our products reach all of the 31 provinces, municipalities and autonomous regions in China.

In 2014, 65.4% of sales of our plasma products were generated from direct sales, and in 2014, our direct sales network covered approximately 641 hospitals and inoculation centers. Our sales and marketing team, consisting of 131 employees in 2014, is responsible for the sales and marketing efforts to our end customers and provide product educational programs and other sales support directly to doctors and nurses. These efforts are designed to ensure effective and seamless communications with our end-customers and provide us with first hand intelligence on latest industry trends and market demands. For example, our sales and marketing team actively promotes new IVIG indications that are widely accepted in more developed countries but less known among Chinese physicians. These efforts contributed significantly to the growth of our IVIG sales, which increased by $21.1 million from $77.3 million in 2013 to $98.4 million in 2014.

Our direct sales network is complemented by sales through distributors, which accounted for 34.6% of our plasma sales in 2014. We select our distributors through a rigorous process, which focuses on market leadership in the covered region, the degree of control we have over to which hospitals our products are sold (i.e. larger and higher tiered hospitals are preferred), and the level of access we have to our customers (i.e. greater access enables us to better track the sales of our products).

We believe that our unique sales model of focusing on direct sales is cost-effective and has helped us to achieve strong financial performance. Our selling expenses as a percentage of sales in 2014, 2013 and 2012 were 4.4%, 5.2% and 7.8%, respectively; and our operating margin was 45.7%, 42.7% and 40.3%, respectively.

Robust near-term product pipeline to capture full plasma value chain backed by strong research and development capabilities

We currently have five new products under development, with one of them in registration stage and expected to be commercially launched by the end of 2015 and one in clinical trial stage and expected to be commercially launched by 2016. We expect our expanding product portfolio to further increase our comprehensive plasma utilization, which will in turn lead to higher profit margins. With our current and pipeline products, we believe that by 2016, our product offerings will be able to capture substantially all of the value along the plasma products value chain.

| 9 |

Our ability to bring new products to market reflects a research and development process that is designed to be demand-driven and highly responsive to physician feedback and the latest trends in medicine. To complement our research and development efforts, we also work closely with a number of leading research institutes in China specializing in plasma products. As of December 31, 2014, we held 43 patents for plasma products.

Experienced and committed management team

We have an experienced, dedicated and visionary management team with an in-depth understanding of the pharmaceutical industry in China. Our Chairman and Chief Executive Officer, Mr. David (Xiaoying) Gao, with more than 12 years of experience in the pharmaceutical industry, was instrumental in the development and implementation of our business strategy. Before joining the Company, Mr. Gao was the chief executive officer of BMP Sunstone Corporation before being acquired by Sanofi. Our Chief Financial Officer, Ming Yang, has more than 17 years of financial management and accounting experience. Mr. Guangli Pang and Mr. Gang Yang, the general manager of Shandong Taibang and Guizhou Taibang, respectively, have more than 30 and 20 years of experience, respectively, in the plasma products industry in China. Since our current senior management team was put in place in 2012, we have been committed to improving corporate governance and enhancing shareholder value. We believe our management team, with their extensive industry background and strong management talent, provides a strong foundation for the execution of our growth strategy and achievement of our goals.

Our Business Strategy

Our mission is to become a first-class biopharmaceutical enterprise in China. To achieve this objective, we have implemented a business strategy with the following key components:

Market development and network expansion

Leveraging on the high quality and steady supply of our products, we intend to expand our geographic coverage in China to include markets where we envision significant growth potential. In particular, we plan to further strengthen our direct sales by growing our sales and marketing team and expanding our coverage among hospitals and inoculation centers. We also plan to strengthen our relationships with major distributors in tier-one cities to deepen our penetration in those markets.

Securing the supply of plasma

Due to the shortage of plasma, we plan to build new plasma collection stations throughout China as well as to expand collection territories of existing plasma stations in order to secure our plasma supply. We currently have a total of 12 plasma stations in operation, of which eight are in Shandong Province, two in Guangxi Province and two in Guizhou Province. In October 2014, Shandong Taibang, one of our majority owned subsidiaries, received the approval from the Hebei Provincial Health and Family Planning Commission to build two new plasma collection stations in Hebei Province. Meanwhile, we are carrying out various promotional activities to stabilize and expand our donor base for our existing plasma stations. A majority of our plasma stations recorded increases in plasma collection volume in 2014 as compared to 2013.

Acquisition of competitors and/or other biologic related companies

In addition to organic growth, acquisition is an important part of our expansion strategy. Although there are about approximately 30 approved plasma-based biopharmaceutical manufacturers in the market, we believe that there are no more than 25 manufacturers currently in operation in China, only about half of which are competitive. We estimate that the top five manufacturers in China accounted for more than 50% market share (excluding imports) in 2014. Furthermore, we believe that the regulatory authorities are considering further industry reform and those smaller, less competitive manufacturers will face possible revocation of their manufacturing permits by the regulators due to the cost of compliance, making them potential targets for acquisition. If we are presented with appropriate opportunities, we may acquire additional companies, products or technologies in the biologic related sectors (including but not limited to medical, pharmaceutical and biopharmaceutical) to complement our current business operations.

| 10 |

Further strengthening of research and development capability

We believe that, unlike other more developed countries such as the United States, China’s plasma products are at an early stage of development. There are many other plasma products that are being used in the United States, which are not currently being manufactured or used widely in China. We intend to strengthen our research and development capabilities through in-house development and partnership with leading international players so as to expand our product line to include plasma products that have higher margins and are technologically more advanced. We believe that our increased focus on research and development will give us a competitive advantage in China over our competitors.

Our Products

Our principal products are our approved human albumin and IVIG products. Human albumin is principally used to treat critically ill patients by replacing lost fluid and maintaining adequate blood volume and pressure. IVIG products are primarily used to enhance specific immunity, a defense mechanism by which the human body generates certain immunoglobulin, or antibodies, against invasion by potentially dangerous substances. In a situation where the human body cannot effectively react with these foreign substances, injection of our products will provide sufficient antibodies to neutralize such substances. We are currently approved to produce over 20 different dosage forms of plasma products.

| Approved Products(1)(2) | Treatment/Use | |

| Human albumin – 20%/10ml, 20%/25ml, 20%/50ml, 10%/100ml, 10%/20ml, 10%/50ml, 25%/50ml and 20%/50ml (10g, from factor IV) | Shock caused by blood loss trauma or burn; raised intracranial pressure caused by hydrocephalus or trauma; oedema or ascites caused by hepatocirrhosis and nephropathy; prevention and treatment of low-density-lipoproteinemia; and neonatal hyperbilirubinemia. | |

| Human immunoglobulin – 10%/3ml and 10%/1.5ml | Original immunoglobulin deficiency, such as X chain low immunoglobulin, familiar variable immune deficiency, immunoglobulin G secondary deficiency; secondary immunoglobulin deficiency, such as severe infection, newborn sepsis; and auto-immune deficiency diseases, such as original thrombocytopenia purpura or kawasaki disease. | |

| IVIG – 5%/25ml, 5%/50ml, 5%/100ml and 5%/200ml | Same as above. | |

| Thymopolypeptides injection – 20mg/2ml and 5mg/2ml | Treatment for various original and secondary T-cell deficiency syndromes, some auto-immune deficiency diseases and various cell immunity deficiency diseases, and assists in the treatment for tumors. | |

| Human hepatitis B immunoglobulin – 100 IU(3),200IU and 400IU | Prevention of measles and contagious hepatitis. When applied together with antibiotics, its curative effect on certain severe bacteria or virus infection may be improved. | |

| Human rabies immunoglobulin – 100IU, 200IU and 500IU | Mainly for passive immunity from bites or claws by rabies or other infected animals. All patients suspected of being exposed to rabies are treated with a combined dose of rabies vaccine and human rabies immunoglobulin. | |

| Human tetanus immunoglobulin – 250IU | Mainly used for the prevention and therapy of tetanus. Particularly applied to patients who have allergic reactions to tetanus antitoxin. |

| Placenta polypeptide – 4ml/vial | Treatment for cell immunity deficiency diseases, viral infection and leucopenia caused by various reasons, and assist in postoperative healing. | |

| Factor VIII – 200IU and 300IU | Treatment for coagulopathies such as hemophilia A and increased concentration of coagulation factor VIII. | |

| Human prothrombin complex concentrate (or PCC) – 300IU | Treatment for congenital and acquired clotting factor II, VII, IX, X deficiency, such as Hemophilia B, excessive anticoagulant, and vitamin K deficiency, etc. |

| 11 |

|

(1) |

“%” represents the degree of dosage concentration for the product and each product has its own dosage requirement. For example, human albumin 20%/10ml means 2g of human albumin is contained in each 10ml packaging and human immunoglobulin 10%/3ml means 300mg of human immunoglobulin is contained in each 3ml packaging. Under PRC law, each variation in the packaging, dosage and concentration of medical products requires separate registration and approval by CFDA before it may be commercially available for sale. For example, among our human albumin products, only human albumin 20%/10ml, 20%/25ml, 20%/50ml, 10%/100ml, 10%/20ml, 10%/50ml, 25%/50ml and 20%/50ml (10g, from factor IV) products are currently approved and are commercially available.

|

| (2) |

“IU” means International Units. IU is a unit used to measure the activity of many vitamins, hormones, enzymes, and drugs. An IU is the amount of a substance that has a certain biological effect. For each substance there is an international agreement on the biological effect that is expected for 1 IU. In the case of immunoglobulin, it means the number of effective units of antibodies in each package.

|

| (3) | Tetanus antitoxin is a cheaper injection treatment for tetanus. However it is not widely used because most people are allergic to it. |

Our approved human albumin, immunoglobulin (including IVIG), factor VIII and PCC products all use human plasma as the primary raw material. All of our approved products are prescription medicines administered in the form of injections.

We have two product liability insurance policies covering Shandong Taibang’s and Guizhou Taibang’s products in the amount of RMB20 million (approximately $3.2 million) each. Since our establishment in 2002, we have been subject to three lawsuits filed by patients who were treated with our products and received blood and/or plasma transfusions. See “Risk Factors — Risks Related to Our Business — Product liability claims or product recalls involving our products could have a material and adverse effect on our business” for further details. We do not believe these three claims to have a material and adverse impact on the Company.

Raw Materials

Plasma

Plasma is the principal raw material for our biopharmaceutical products. We currently operate 10 plasma stations through Shandong Taibang and two plasma stations through Guizhou Taibang. We believe that our plasma stations give us a stable source of plasma supply and control over product quality. Also, we believe that we have enjoyed benefits of economies of scale, including sharing certain administration and management expenses across our several plasma stations. We currently maintain sufficient plasma supply for approximately six months of production.

Other Raw Materials and Packaging Materials

Other raw materials used in the production of our biopharmaceutical products include reagents and consumables such as filters and alcohol. The principal packaging materials we use include glass bottles for our injection products as well as external packaging and printed instructions for our biopharmaceutical products. We acquire our raw materials and packaging materials from our approved suppliers in China and overseas. We select our suppliers based on quality, consistency, price and delivery of the raw materials which they supply.

| 12 |

Our five largest suppliers in the aggregate accounted for approximately 30.2%, 39.3% and 38.0% of our total procurement for the years ended December 31, 2014, 2013 and 2012, respectively. We have not experienced any shortage of supply or significant quality issue with respect to any raw materials and packaging materials.

Plasma Collection

All of our plasma is collected through plasma stations of Shandong Taibang and Guizhou Taibang. These stations purchase, collect, examine and deepfreeze plasma on behalf of Shandong Taibang and Guizhou Taibang and are subject to provincial health bureau’s rules, regulations and specifications for quality, packaging and storage. Each station is only allowed to collect plasma from healthy donors within its respective districts and in accordance with a time table set by its respective parent company, Shandong Taibang or Guizhou Taibang. The plasma must be tested negative for HBsAb, HCV and HIV antibodies and the RPR test, contain ALT 25 units (ALT) and plasma protein 55g/l, and contain no virus pollution or visible erythrolysis, lipemia, macroscopic red blood cell or any other irregular finding. The plasma is packaged in 25 to 30 separate 600g bags in each box and then stored at a temperature of -20°C or lower within limited time after collection to ensure that it will congeal within six hours. Each bag is labeled with a computer-generated tracking code. Shandong Taibang and Guizhou Taibang are responsible for the overall technical and quality supervision of the plasma collection, packaging and storage at each plasma station.

Sales, Marketing and Distribution

Because all of our products are prescription drugs, we can only sell to hospitals and inoculation centers directly or through approved distributors. For 2014, 2013 and 2012, direct sales to hospitals and inoculation centers represented approximately 65.4%, 66.8% and 66.4%, respectively, of our total plasma sales. Our five largest customers in the aggregate accounted for approximately 14.6%, 11.0% and 10.8% of our total sales for 2014, 2013 and 2012, respectively. Our largest customer accounted for approximately 4.2%, 2.7% and 3.6% of our total sales for 2014, 2013 and 2012, respectively.

We select our distributors through a rigorous process, which focuses on market leadership in the covered region, the degree of control we have over to which hospitals our products are sold (i.e. larger and higher tiered hospitals are preferred), and the level of access we have to our customers (i.e. greater access enables us to better track the sales of our products). As part of our effort to ensure the quality of our distributors, we also conduct due diligence to verify whether potential distributors have obtained necessary permits and licenses and facilities (such as cold storage) for the distribution of our biopharmaceutical products and assess their financial condition. Certain of our regional distributors are appointed on an exclusive basis within a specified geographic territory. Our supply contracts set out the quantity and price of products to be supplied by us. For distributors, our contracts also contain guidelines for the sale and distribution of our products, including restrictions on the geographical territory in which the products may be sold. We provide our distributors with training in relation to our products and on sales techniques. We generally require our distributors to pay in advance before we deliver products, with a few exceptions for a credit period of no longer than 60 days to major distributors in tier-one cities. For hospitals and clinics, we generally grant a credit period of no longer than 90 days, with exceptions to certain high credit-worthy customers of up to six months. For 2014, 2013 and 2012, we had not incurred any significant bad debts from our customers.

| 13 |

Our largest geographic market is Shandong Province, representing approximately 23.9%, 27.3% and 24.1% of our total sales for 2014, 2013 and 2012, respectively. Hebei Province is our second largest geographic market, representing 10.4%, 6.3% and 5.5% of our total sales for 2014, 2013 and 2012, respectively. In addition to Shandong Province and Guizhou Province, we also have sales presence in 29 other provinces, municipalities and autonomous regions.

As of December 31, 2014, our marketing and after-sales services department consisted of 131 employees.

We believe that due to the nature of our products, the key factors of our competitiveness centers on product safety, steady supply, brand recognition, timely availability and pricing. As all of our products are prescription medicines, we are not allowed to advertise our products in the mass media. For 2014, 2013 and 2012, total sales and marketing expenses amounted to approximately $10.7 million, $10.6 million and $14.4 million, respectively, representing approximately 4.4%, 5.2% and 7.8%, respectively, of our total sales.

Our Research and Development Efforts

Each of Shandong Taibang and Guizhou Taibang has its own research and development department, or collectively, our R&D Departments. All of our research and development researchers hold degrees in medicine, pharmacy, biology, biochemistry or other relevant field. Our R&D Departments are responsible for the development and registration of our products. We also cooperate with a number of leading institutions in China specializing in plasma products to strengthen our research and development capacity.

We employ a market driven approach to initiate research and development projects, including both product and production technique development. We believe that the key to our industry’s developments is the safety of products and maximizing the yield per unit volume of plasma. Our research and development efforts are focused on the following areas:

| • | broaden the breadth and depth of our portfolio of plasma products; | |

| • | enhance the yield per unit volume of plasma through new collection techniques; | |

| • | maximize manufacturing efficiency and safety; | |

| • | promote product safety through implementation of new technologies; and | |

| • | refine production technology for existing products. |

All the products we currently manufacture have been developed in-house. The following table outlines our research and development work in progress:

| Products Currently in Development | Treatment/Use | Status of Product Development | Stage* | |||

| Human hepatitis B immunoglobulin (pH4) for intravenous injection | Prevention of measles and contagious hepatitis. When applied together with antibiotics, its curative effect on certain severe bacteria or virus infection may be improved. | Application made to CFDA for official production permit and product certification. Commercial production expected in 2015. | 4 | |||

| Human fibrinogen | Treatment for lack of fibrinogen and increase human fibrinogen concentration. | Clinical trial is undergoing. Commercial production expected in 2016. | 3 | |||

| Immune Globulin Intravenous (Human), Caprylate/Chromatography Purified and 20 nm virus filtration | Treatment for original immunoglobulin deficiency; secondary immunoglobulin deficiency and auto-immune deficiency diseases. | Application in progress for clinical trial. Approval of clinical trials expected in 2015. | 2 | |||

| Human Antithrombin III (concentration) | Treatment for (i) hereditary antithrombin III deficiency in connection with surgical or obstetrical procedures and (ii) thromboembolism. | Application for clinical trial submitted to CFDA. Approval of clinical trials expected in 2015. | 2 | |||

| Human Cytomegalovirus Immunoglobulin | Prophylaxis and treatment of CMV infection, especially for the prevention of active virus replication for patients in immunosuppression, such as organ transplantation patients. | Develop the manufacturing process for the new medicine on an expanded basis in the workshop. Application for clinical trial expected in 2015. | 1 |

| 14 |

* |

These stages refer to the stages in the regulatory approval process for our products described in “— Regulation.” |

For 2014, 2013 and 2012, total research and development expenses amounted to approximately $4.2 million, $4.2 million and $3.0 million, respectively, representing approximately 1.7%, 2.1% and 1.6%, respectively, of our total sales.

Competition

We are subject to intense competition. There are both local and overseas pharmaceutical enterprises that are engaged in the manufacture and sale of potential substitute or similar biopharmaceutical products as our products in China. These competitors may have more capital, better research and development resources, more manufacturing and marketing capability and experience than we do. In our industry, we compete based upon product quality, product cost, ability to produce a diverse range of products and logistical capabilities.

Our profitability may be adversely affected if (i) competition intensifies; (ii) competitors reduce prices; (iii) PRC government requires us to reduce the prices of our products; or (iv) competitors develop new products or product substitutes with comparable medicinal applications or therapeutic effects which are more effective or less costly than ours.

There are approximately 30 approved manufacturers of plasma products in China of which no more than 25 are currently in operation. Many of these manufacturers are essentially producing the same type of products that we produce: human albumin and various types of immunoglobulin. However, due to regulations of the PRC Ministry of Health, we believe that it is difficult for new manufacturers to enter into the industry. We believe that our major competitors in China include China National Biotec Group, Hua Lan Biological Engineering, Shanghai RAAS Blood Products Co., Ltd., Shanxi Kangbao Biological Product Co., Ltd., Sichuan Yuanda Shuyang Pharmaceutical Co and Jiangxi Boya Bio pharmaceutical Co., Ltd.

In addition, we also face competition from imported products where importation is allowed. China became a member of the World Trade Organization in December 2001 and as a result imported biopharmaceutical products enjoy lower tariffs. Since 2009, China has experienced a substantial increase in volume of imported human albumin. If importation of human albumin continues to increase, we may face more fierce competition in domestic human albumin market.

Based on our industry knowledge, we are the second largest plasma products manufacturer and the largest non-state-owned manufacturer in China, with a market share of 8.2% in terms of 2014 sales. To solidify our market position, we have also expanded our product portfolio to include factor VIII in 2012. We received the manufacturing approval certificate and the GMP certification for production facility from CFDA for factor VIII in 2012. We also have obtained the manufacturing approval certificate for human prothrombin complex concentrate, or PCC, in July 2013, and obtained the GMP certification for the production facility of PCC in March 2014.

| 15 |

We will continue to meet challenges and secure our market position by enhancing our existing products, introducing new products to meet customer demand, delivering quality products to our customers in a timely manner and maintaining our established industry reputation.

Our Intellectual Property

We held 48 issued patents and 11 pending patent applications in China for certain manufacturing processes and packing designs as of December 31, 2014. We also had nine registered trademarks in China as of December 31, 2014.

In addition, we had registered three domain names as of December 31, 2014, namely, www.chinabiologic.com, www.ctbb.com.cn and www.taibanggz.com.

Regulation

Set forth below is a summary of the major PRC regulations relating to our business.

Due to the nature of our products, we are supervised by various levels of the PRC Ministry of Health and/or CFDA. Such supervision includes the safety standards regulating our raw material supplies (mainly plasma), our manufacturing process and our finished products.

We are also subject to other PRC regulations, including those relating to taxation, foreign currency exchange and dividend distributions.

Plasma collection

Substantially all plasma donations for commercialized plasma products are done through plasma stations. Plasma donation means donors give only selected blood components — platelets, plasma, red cells, infection-fighting white cells, or a combination of these, depending on donors blood type and the needs of the community. Plasma stations in China are commonly used to collect plasma. In China, current regulations only allow an individual donor to donate blood in 14-day intervals, with a maximum quantity of 580ml (or about 600 gram) per donation.

The following are the general regulatory requirements to establish a plasma station in China:

| • | meet the overall plan in terms of the total number, distribution, and operational scale of plasma stations; | |

| • | have the required professional health care technicians to operate a station; | |

| • | have the facility and a hygienic environment to operate a station; | |

| • | have an identification system to identify donors; | |

| • | have the equipment to operate a station; and | |

| • | have the equipment and quality control technicians to ensure the quality of the plasma collected. |

| 16 |

Plasma stations were historically owned and managed by the PRC health authorities. In March 2006, the PRC Ministry of Health and other eight central governmental departments of the PRC State Council promulgated the Measures for the Reform of Blood Collection Stations whereby the ownership and management of the plasma stations are required to be transferred to plasma-based biopharmaceutical companies while the regulatory supervision and administrative control remain with the government. As a result, all plasma stations are now having direct supply relationship with their parent fractionation facilities.

Set out below are some of the safety features at China’s plasma stations:

| • | Plasma stations can only source plasma from donors within the assigned district approved by the provincial health authorities; |

| • | Plasma stations must perform a health check on the donor. Once the donor passes the health check, a “donor permit” is issued to the donor. The standards of the health check are established by the health authorities at the PRC State Council level; |

| • | The designing and printing of the “donor permit” is administrated by the provincial health authorities, autonomous region or municipality government, as the case maybe. The “donor permit” cannot be altered, copied or assigned; |

| • | Before donors can donate plasma, the station must verify their identities and the validity of their “donor permits.” The donors must pass the verification procedures before they are given a health check and blood test. For those donors who have passed the verification, health check and blood test and whose plasma were donated according to prescribed procedures, the station will set up a record; |

| • | Collected plasma which passes quality testing cannot be used to produce plasma products until its donor donates again after a 90-day quarantine period and the subsequently donated plasma passes quality testing as well; |

| • | All plasma stations are subject to the regulations on the prevention of communicable diseases. They must strictly adhere to the sanitary requirements and reporting procedures in the event of an epidemic situation. |

The operation of plasma collection stations is subject to stringent regulations by the PRC government. We estimate that there were approximately 190 plasma stations in operation in China as of December 31, 2014.

Importation of blood products

According to current PRC regulations, except for human albumin and recombinant factor VIII products, all the plasma products are banned from importation into China.

Production of plasma products

The manufacture and sale of plasma products are subject to stringent regulations by the PRC government. Under PRC law, each variation in the packaging, dosage and concentration of medical products requires separate registration and approval by CFDA before it may be commercially available for sale. For example, among our human albumin products, only human albumin 20%/10ml, 20%/25ml, 20%/50ml, 10%/100ml, 10%/20ml, 10%/50ml, 25%/50ml and 20%/50ml (10g, from factor IV) products have been approved and are commercially available.

| 17 |

The table below illustrates the PRC approval process for the manufacture and sale of new medicines:

| Stage | Activities | ||

| 1 | Pre-clinical | The pre-clinical research stage mainly involves the following steps: | |

| Research | l Initiate the research project, study the project feasibility and develop a plan for testing and producing the new medicine; | ||

| l Develop the scope and the techniques for testing the new medicine in the laboratory; | |||

| l Develop laboratory-scale manufacturing process for the new medicine; | |||

| l Develop the manufacturing process for the new medicine on an expanded basis in the workshop; and | |||

| l Develop the virus inactivation process/techniques, engage qualified institution to assess the virus inactivation process/techniques, and report the related documents to the related government authority for re-assessment. | |||

| 2 | Clinical trial | The clinical trial application stage mainly involves the following steps: | |

| application | l Submit required sample products and documents to the PRC Provincial Food and Drug Administration, or PFDA. PFDA will perform an on-site examination on the documents and equipment, and then transfer all the required materials to CFDA, who will further review the documents and test the sample products; | ||

| l Submit a draft clinical trial program to CFDA for the application of the clinical trial; and | |||

| l Approval of the clinical trial. | |||

| 3 | Clinical trials | Clinical trials range from Phase I to IV: | |

| l Phase I: preliminary trial of clinical pharmacology and human safety evaluation studies. The primary objective is to observe the pharmacokinetics and the tolerance level of the human body to the new medicine as a basis for ascertaining the appropriate delivery methods or dosage. | |||

| l Phase II: preliminary exploration on the therapeutic efficacy. The purpose is to assess preliminarily the efficacy and safety of the new medicine on patients and to provide the basis for designing dosage tests in phase III. | |||

| l Phase III: confirm the therapeutic efficacy. The objective is to further verify the efficacy and safety of the new medicine on patients, to evaluate the benefits and risks and finally to provide sufficient experimental evidence to support the registration application of the new medicine. | |||

| l Phase VI: application research conducted after the launch of a new medicine. The objective is to observe the efficacy and adverse reaction of the new medicine under extensive use, to perform an evaluation of the benefits and risks of the application among ordinary or special group of patients, and to ascertain and optimize the appropriate dosage and formula for application. | |||

| 4 | Registration | The registration stage mainly involves the following steps: | |

| l Submit documents related to pre-clinical and clinical trials to PFDA, which will perform on-site inspection on the clinical trials and then transfer the related documents to CFDA for further review; | |||

| l On-site inspection by CFDA on three consecutive sample productions at the production facilities; | |||

| l Grant of the manufacturing approval certificate following the public notification period; and | |||

| l Grant of GMP certificate following the public notification period. |

| 18 |

| 5 | Production and | The production and approval for sale stage mainly involves the following steps: | |

| approval for sale | l Produce the approved products in qualified facilities with requisite GMP certificates; | ||

| l Submit documentation and samples of mass production products to CFDA for inspection; and | |||

| l Grant of qualification certificate to mass production products for sale on a batch-by-batch basis. |

New GMP Standard

All of our production facilities are required to obtain GMP certificates for their pharmaceutical production activities. In February 2011, CFDA enacted the New GMP Standard, which has significantly increased standards for quality control, documentation, and overall manufacturing processes of blood products, vaccines, injections and other sterile pharmaceutical products. The New GMP Standard requires us to, among others, maintain and operate a comprehensive and effective product quality control system throughout the production process. In addition, it imposes higher standards for our production facilities. The New GMP Standard became applicable to all of our production facilities at the end of 2013. After respective upgrades on their production facilities, Shandong Taibang and Guizhou Taibang obtained the renewed GMP certificate in June 2013 and March 2014, respectively. Huitian has suspended the production at its production facilities for technical upgrade and will apply for a new GMP certificate upon the completion of the upgrade. Huitian may not be able to obtain the certificate, which would prevent it from carrying on its business at these facilities and harm our profitability. See “Risk Factors — Risk Related to Our Business — We may not be able to carry on our business if we lose any of the required permits and licenses. Moreover, Huitian has suspended the production at its production facilities for technical upgrade and will apply for a new GMP certificate upon the completion of the upgrade; however, it may not be able to obtain the certificate, which would prevent it from carrying on its business at these facilities and harm our profitability” for details.

Pricing

Retail prices of certain pharmaceutical products are subject to various regulations. According to the “Regulations on Controlling Blood Products” promulgated by the PRC State Council in 1996, regional offices of the Pricing Bureau and the PRC Ministry of Health have the authority to regulate retail prices for controlled plasma products. In addition, retail prices of pharmaceutical products fully or partially covered under the national insurance system are also subject to the price ceilings set out in the National (Medical) Insurance Catalog, or the NIC, which may be adjusted by NDRC from time to time. The hospitals as participants of the national insurance program cannot sell the products to patients at prices exceeding such retail price ceilings. The provincial governments in turn often establish a tender price ceiling for product tender offer made to hospitals based on, amongst other things, the regional living standards, cost of production of the manufacturers and the corresponding retail price ceiling. The ex-factory prices and the distributor’s wholesale prices cannot exceed the tender price ceiling. Five of our principal products, human albumin, IVIG, human rabies immunoglobulin, human tetanus immunoglobulin and factor VIII, are included in the NIC and are subject to tender price ceilings. Two of our principal products, placenta polypeptide and human hepatitis B immunoglobulin, although not included in the NIC, are also subject to tender price ceilings in certain provinces. Our profit margin for any price-controlled product is effectively controlled by the tender price ceiling. When a tender price ceiling puts significant pressure on the profit margin of a given product, we may appeal to the provincial governments for lifting of such tender price ceiling.

| 19 |

In an announcement published in September 2012, or the 2012 Adjustment, NDRC adjusted retail price ceilings for 95 oncology, immunology and hematology drugs, which became effective on October 8, 2012. Two of our approved products, IVIG and factor VIII were affected by the 2012 Adjustment. The new retail price ceilings for IVIG products were lower than the current prevailing market retail prices in some of our regional markets while those for factor VIII were close to the then prevailing market retail prices. As a result, some local governments revised tender price ceilings for IVIG products. In January 2013, NDRC further adjusted retail price ceilings for certain drug products, which became effective on February 1, 2013, or the 2013 Adjustment. Three of our approved products, human albumin, human rabies immunoglobulin and human tetanus immunoglobulin are affected by the 2013 Adjustments. The 2013 Adjustment slightly increased retail price ceilings for both human albumin and human tetanus immunoglobulin products and subject human rabies immunoglobulin products to a retail price ceiling for the first time. The retail price ceiling imposed on human rabies immunoglobulin products by the 2013 Adjustment is close to the prevailing market retail price.

Taxation

On March 16, 2007, the National People’s Congress of China passed the Enterprise Income Tax Law, or the EIT Law, and on November 28, 2007, the PRC State Council passed its implementation rules, which became effective on January 1, 2008. Before the implementation of the EIT Law, foreign invested enterprises, or FIEs, established in China, unless granted preferential tax treatments by the PRC government, were generally subject to an enterprise income tax, or EIT, rate of 33.0%, which included a 30.0% state income tax and a 3.0% local income tax. The EIT Law and its implementation rules impose a unified EIT of 25.0% on all domestic-invested enterprises and FIEs, unless they qualify under certain limited exceptions. In addition, the EIT Law terminated the “two-year exemption and three-year half reduction” and “five-year exemption and five-year half-reduction” tax preferential policy enjoyable by FIEs under the old EIT laws. The PRC State Administration of Taxation, or SAT, then promulgated a series of regulations to implement the EIT Law, under which FIEs established before March 16, 2007, or Old FIEs, were given a five-year grandfather period during which they can continue to enjoy their existing preferential tax treatments. During this five-year grandfather period, Old FIEs that enjoyed tax rates lower than 25% under the old EIT Law could gradually increase their EIT rate by 2% per year until their tax rate reached 25%.

In addition to the changes to the tax structure, under the EIT Law, an enterprise established outside of China with “de facto management bodies” within China is considered a resident enterprise and will normally be subject to an EIT of 25% on its global income. The implementation rules define the term “de facto management bodies” as “an establishment that exercises, in substance, overall management and control over, among others, the production, business, recruitment and accounting aspects of a Chinese enterprise.” If the PRC tax authorities subsequently determine that we should be classified as a resident enterprise, then our global income will be subject to PRC income tax of 25%. For detailed discussion of PRC tax issues related to resident enterprise status, see “Risk Factors — Risks Related to Doing Business in China — Under the Enterprise Income Tax Law, we may be classified as a “resident enterprise” of China. Such classification will likely result in unfavorable tax consequences to us and our non-PRC stockholders.”

The EIT Law confirmed that qualified high and new technology enterprises may enjoy a preferential income tax rate of 15%, instead of the uniform enterprise income tax rate of 25%. The PRC Ministry of Science and Technology, the PRC Ministry of Finance and SAT jointly promulgated the Measures for Determination of High and New Technology Enterprise on August 14, 2008 to provide the detailed rules for the examination of qualifications and approval of certificates for high and new technology enterprises. Each certificate of high and new technology enterprise is valid for three years. Shandong Taibang was recognized by Shandong provincial government as a high and new technology enterprise in 2008 and renewed the certificate in 2011, as a result of which Shandong Taibang is entitled to enjoy a preferential income tax rate of 15% until the end of 2013. In October 2014, Shandong Taibang obtained a notice from the Shandong provincial government that granted it the high and new technology enterprise certificate. This certificate entitled Shandong Taibang to enjoy a preferential income tax rate of 15% for a period of three years from 2014 to 2016. Shandong Taibang may apply for a renewal for an additional three years from 2017 to 2019 upon its expiration.

| 20 |

According to Notice on Issues Concerning Relevant Tax Policies in Deepening the Implantation of the Western Development Strategy jointly promulgated by the PRC Ministry of Finance, the PRC General Administration of Customs and SAT on July 27, 2011, enterprises located in the western region of China which have at least 70% of their income from the businesses falling with in the Category of Encouraged Industries in Western Region of China may enjoy a preferential income tax of 15% within the period from January 1, 2011 to December 31, 2020. Guizhou Taibang, being a qualified enterprise located in the western region of China, enjoys a preferential income tax rate of 15% effective from January 1, 2011 to December 31, 2020.

Foreign currency exchange

The principal regulation governing foreign currency exchange in China is the Foreign Currency Administration Rules (1996), as amended (2008). Under these rules, RMB is freely convertible for current account items, such as trade and service-related foreign exchange transactions, but not for capital account items, such as direct investment, loan or investment in securities outside China unless the prior approval of, and/or registration with, SAFE or its local counterparts (as the case may be) is obtained.

Pursuant to the Foreign Currency Administration Rules, FIEs in China may purchase foreign currency without the approval of SAFE for trade and service-related foreign exchange transactions by providing commercial documents evidencing these transactions. They may also retain foreign exchange (subject to a cap approved by SAFE) to satisfy foreign exchange liabilities or to pay dividends. In addition, if a foreign company acquires a company in China, the acquired company will also become an FIE. However, the relevant PRC government authorities may limit or eliminate the ability of FIEs to purchase and retain foreign currencies in the future. In addition, foreign exchange transactions for direct investment, loan and investment in securities outside China are still subject to limitations and require approvals from, and/or registration with, SAFE.

Dividend distributions

Under applicable PRC regulations, FIEs in China may pay dividends only out of their accumulated profits, if any, determined in accordance with PRC accounting standards and regulations. In addition, an FIE in China is required to set aside at least 10% of its after-tax profit based on PRC accounting standards each year to its general reserves until the accumulative amount of such reserves reach 50% of its registered capital. These reserves are not distributable as cash dividends. The board of directors of a FIE also has the discretion to allocate a portion of its after-tax profits to staff welfare and bonus funds, which may not be distributed to equity owners except in the event of liquidation.

In addition, under the EIT law, the Notice of the State Administration of Taxation on Negotiated Reduction of Dividends and Interest Rates, promulgated on January 29, 2008, the Arrangement between the PRC and the Hong Kong Special Administrative Region on the Avoidance of Double Taxation and Prevention of Fiscal Evasion, or the Double Taxation Treaty, which became effective on December 8, 2006, and the Notice of the State Administration of Taxation Regarding Interpretation and Recognition of Beneficial Owners under Tax Treaties, which became effective on October 27, 2009, dividends from our PRC subsidiary, Taibang Biotech (Shandong) Co., Ltd., paid to us through our Hong Kong subsidiary, Taibang Holdings, may be subject to a withholding tax at a rate of 10%, or at a rate of 5% if Taibang Holdings is considered a “beneficial owner” that is generally engaged in substantial business activities in Hong Kong and entitled to treaty benefits under the Double Taxation Treaty.

| 21 |

Our Employees

As of December 31, 2014, we employed 1,684 full-time employees, of which 63 were seconded to us by the Shandong Institute.

We believe we are in material compliance with all applicable labor and safety laws and regulations in China. We participate in various employee benefit plans that are organized by municipal and provincial governments, including retirement, medical, unemployment, work injury and maternity benefit plans for our managerial and key employees. In addition, we provide short term insurance plans for all our employees while on duty to cover work related accidents. We believe that we maintain a satisfactory working relationship with our employees and we have not experienced any significant labor disputes or any difficulties in recruiting staff for our operations.

Corporate Information