UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

OR

| ¨ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-34004

SCRIPPS NETWORKS INTERACTIVE, INC.

(Exact name of registrant as specified in its charter)

|

|

|

| Ohio |

|

61-1551890 |

| (State or other jurisdiction of |

|

(IRS Employer |

| incorporation or organization) |

|

Identification Number) |

|

|

| 9721 Sherrill Boulevard |

|

|

| Knoxville, Tennessee |

|

37932 |

| (Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number, including area code: (865) 694-2700

|

|

|

| Title of each class |

|

Name of each exchange on which registered |

| Securities registered pursuant to Section 12(b) of the Act: |

|

New York Stock Exchange |

| Class A Common shares, $.01 par value |

|

|

Securities registered pursuant to Section 12(g) of the Act:

Not applicable

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to

Section 13 of Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by

check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this

chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such

files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in

definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, non-accelerated filer, or a smaller reporting company

(as defined in Rule 12b-2 of the Exchange Act).

|

|

|

|

|

|

|

| Large accelerated filer |

|

x |

|

Accelerated filer |

|

¨ |

|

|

|

|

| Non-accelerated filer |

|

¨ |

|

Smaller reporting company |

|

¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the

Act). Yes ¨ No x

The aggregate market value of Class A Common shares of the registrant held by non-affiliates of the registrant on June 30, 2014, was approximately $6,720,000,000. All Class A Common shares

beneficially held by executives and directors of the registrant and signatories to the Scripps Family Agreement have been deemed, solely for the purpose of the foregoing calculation, to be held by affiliates of the registrant. There is no active

market for our Common Voting shares.

As of January 31, 2015, there were 97,345,917 of the registrant’s Class A Common shares,

$.01 par value per share, outstanding and 34,317,171 of the registrant’s Common Voting shares, $.01 par value per share, outstanding.

Certain information required for Part III of this report is incorporated herein by reference to the proxy statement for the 2015 annual meeting of

shareholders.

INDEX TO SCRIPPS NETWORKS INTERACTIVE, INC. ANNUAL REPORT ON FORM 10-K FOR THE YEAR ENDED

DECEMBER 31, 2014

2

As used in this Annual Report on Form 10-K, the terms “SNI,” “the Company,”

“we,” “our” or “us” may, depending on the context, refer to Scripps Networks Interactive, Inc. (“SNI”), to one or more of its consolidated subsidiary companies, or to all of them taken as a whole.

AVAILABLE INFORMATION

Our Company website is www.scrippsnetworksinteractive.com. Copies of all of our filings with the U. S. Securities and Exchange Commission (the

“SEC”) are available free of charge on our website as soon as reasonably practicable after such material is filed with, or furnished to, the SEC. Our website also includes copies of the charters for our Compensation,

Nominating & Governance and Audit Committees, our Corporate Governance Principles, our Insider Trading Policy, our Ethics Policy and our Code of Business Conduct and Ethics for the Chief Executive Officer and Senior Financial Officers.

All of these documents are also available to shareholders in print upon request.

FORWARD-LOOKING STATEMENTS

Our Annual Report on Form 10-K contains certain forward-looking statements related to our businesses that are

based on our current expectations. Forward-looking statements are subject to certain risks, trends and uncertainties that could cause actual results to differ materially from the expectations expressed in the forward-looking statements. Such risks,

trends and uncertainties, which, in most instances, are beyond our control, include changes in advertising demand and other economic conditions; consumers’ tastes; program costs; labor relations; technological developments; competitive

pressures; interest rates; regulatory rulings; and reliance on third-party vendors for various products and services. The words “believe,” “expect,” “anticipate,” “estimate,” “intend” and similar

expressions identify forward-looking statements. All forward-looking statements, which are as of the date of this filing, should be evaluated with the understanding of their inherent uncertainty. We undertake no obligation to publicly update any

forward-looking statements to reflect events or circumstances after the date the statement is made.

3

PART I

ITEM 1. BUSINESS

BUSINESS OVERVIEW

SNI is one of the leading developers of lifestyle-oriented content for linear

and interactive video platforms including television and the internet, with respected, high-profile brands. Our businesses engage audiences and efficiently serve advertisers by delivering entertaining and highly useful content that focuses on

specifically defined topics of interest.

We manage our operations through our reportable segment, lifestyle media.

Lifestyle media includes our six national television networks, HGTV, Food Network, Travel Channel, DIY Network, Cooking Channel and Great American Country. Lifestyle media also includes websites that are associated with the aforementioned television

brands and other internet-based businesses serving home, food and travel related categories.

We also have established lifestyle media brands internationally. Our lifestyle-oriented channels are available in the United Kingdom (“UK”), other European markets, the Middle East and Africa

(“EMEA”), Asia-Pacific (“APAC”) and Latin America. The results for our international businesses are not separately identified as a reportable segment and are included within our corporate and other segment caption.

Our businesses earn revenue from advertising sales, affiliate fees and ancillary sales, including the sale and licensing of content and

consumer products. Programming expenses, employee costs and sales and marketing expenses are our primary operating costs.

We seek to engage audiences that are highly desirable to advertisers with entertaining and informative lifestyle content that is

produced for television, the internet and any other media platforms consumers choose. We intend to expand and enhance our lifestyle brands through creating popular new programming and content, distributing on various platforms, such as mobile

phones, tablets and video-on-demand, licensing of content and branded consumer products and increasing our international footprint.

BUSINESS SEGMENTS

Lifestyle Media

Our lifestyle media segment includes our six national television networks

and our portfolio of related interactive lifestyle brands. The segment generates revenue principally from the sale of advertising time on national television networks and interactive media platforms and from affiliate fees paid by service providers

that distribute our programming content. In 2014, revenues from advertising sales and affiliate fees approximated 69 percent and 29 percent, respectively, of total revenue for the lifestyle media segment. Our lifestyle media segment also earns

revenue from the licensing of content to third parties and brands for consumer products, such as videos, books, kitchenware and tools.

Advertising revenue generated by our national television networks depends on viewership ratings, as determined by Nielsen Media Research and other third-party research companies, and advertising rates

paid by advertisers for delivery of advertisements to certain viewer demographics. Revenue from advertising is subject to seasonality, market-based variations and general economic conditions. Advertising revenue is typically highest in the second

and fourth quarters and can fluctuate relative to the popularity of specific programs, blocks of programming during defined periods of the day and seasonal demand of advertisers. Revenues from affiliates are negotiated with individual multichannel

service providers. The negotiations typically result in multi-year carriage agreements that contain scheduled rate increases. The affiliate fees we receive are determined by the number of subscribers with access to the programming of our various

networks.

Programming expenses, employee costs and sales and marketing expenses are the primary operating costs of our

lifestyle media segment. Program amortization represented 46 percent of lifestyle media expenses in 2014, reflecting our continued investment in the improved quality and variety of programming on our networks. We incur sales and marketing expenses

to support brand-building initiatives at all of our television networks.

4

Our lifestyle-oriented interactive businesses are focused on the internal development and

acquisition of interactive media that is intended to diversify sources of revenue and enhance our competitive advantage as a leading provider of home, food, travel and lifestyle content. Revenue generated by our lifestyle interactive businesses is

derived primarily from the sale of display, banner and video advertising.

The lifestyle-oriented interactive businesses

consist of multiple websites, including, but not limited to, our six network-branded websites, HGTV.com, Foodnetwork.com, Travelchannel.com, DIYNetwork.com, Cookingchanneltv.com and GACTV.com. In addition to serving as home websites for the

television programming networks, the websites provide informational and instructional content on specific topics within their respective lifestyle content categories. The Company also operates uLive.com, a digital platform launched in 2013 that

distributes video programming and expands our lifestyle content into new categories, such as parenting, beauty and wellness. uLive.com presents both original video, as well as content aggregated from numerous partners, and generates revenue by

delivering advertising to users of the site. All of the interactive businesses benefit from archived television network programming, of which approximately 94 percent on a dollar basis, is owned by us. Our ownership of programming enables us to

efficiently and economically repurpose it for use on the internet and other interactive distribution channels, including video-on-demand and streaming services.

The lifestyle websites accounted for about 5 percent of the lifestyle media segment’s total revenue in 2014. The

strategic focus of the lifestyle interactive businesses is to grow advertising revenues by increasing views and video plays and attracting more unique visitors to our websites through site enhancements and additional video. Our strategy also

includes attracting a broader audience through placing our video programming on national video streaming sites, developing new sources of revenue that capitalize on traffic growth at our websites and capitalizing on the movement of advertising

dollars to mobile platforms.

We also have 50 percent ownership interests in HGTV Magazine JV and Food Network Magazine JV

and a 7.25 percent ownership interest in Fox-BRV

Southern Sports Holdings LLC, which comprises the Sports South and Fox Sports Net South regional television networks.

HGTV

HGTV reaches approximately 96 million domestic television households and is

simulcast in high definition (“HD”). HGTV programming content commands an audience interested specifically in home-related topics. HGTV is television’s only network dedicated solely to such topics as decorating, interior design, home

remodeling, landscape design and real estate. HGTV strives to engage audiences by creating original programming that is entertaining, instructional and informative. HGTV appeals more strongly to female viewers with higher incomes in the 18 to 49 age

range and 25 to 54 age range.

Programming on HGTV includes House Hunters, House Hunters International, Rehab

Addict, Fixer Upper, The Property Brothers and Flip or Flop. The network also has developed successful programming events, including the HGTV Dream Home Giveaway, HGTV Smart Home Giveaway, HGTV Urban Oasis Giveaway

and annual live coverage of the Tournament of Roses Parade. Many of the programs on HGTV feature, or are hosted by, high-profile television personalities such as Drew and Jonathan Scott; Nicole Curtis; Chip and Joanna Gaines; Tarek

and Christina El Moussa and cousins Anthony Carrino and John Colaneri.

Food Network

Food Network is available in approximately 97 million U.S. television households and is simulcast in HD. We currently own approximately 69 percent of

the Food Network, and we are the managing partner. The Tribune Media Company (“Tribune”) has a noncontrolling interest of approximately 31 percent in Food Network.

Food Network programming content attracts audiences interested in food-related topics such as food preparation, dining out,

entertaining, food manufacturing, nutrition and healthy eating. Food Network engages audiences by creating original programming that is entertaining, instructional and informative. Food Network appeals more strongly to female viewers with higher

incomes in the 18 to 49 age range and 25 to 54 age range.

5

Programming on Food Network includes primetime series Beat Bobby Flay, Chopped,

Cutthroat Kitchen, Diners, Drive-ins and Dives, Food Network Star; Guy’s Grocery Games and Restaurant Impossible, as well as daytime series Giada at Home, The Kitchen, Pioneer Woman and

Trisha’s Southern Kitchen. Food Network hosts include high-profile television personalities such as Anne Burrell, Alex Guarnaschelli, Alton Brown, Bobby Flay, Giada De Laurentiis, Guy Fieri, Rachael Ray, Ree Drummond, Robert Irvine and

Trisha Yearwood.

Travel Channel

Travel Channel is available in about 92 million domestic television households and is simulcast in HD. We currently own 65 percent of the Travel Channel. Cox Communications, Inc. has a noncontrolling

interest of 35 percent in Travel Channel.

Travel Channel programming content attracts travel enthusiasts and is a

leading travel multi-media brand offering quality television, video and mobile entertainment and information. Travel Channel programming appeals to viewers who are more affluent than the average cable viewer and skews slightly toward adult men in

the 18 to 49 age range.

Programming on Travel Channel includes Hotel Impossible, Mysteries at the

Museum, Bizarre Foods, Trip Flip, Booze Traveler, Expedition Unknown and Ghost Adventures. Many of the programs on Travel Channel feature, or are hosted by, high-profile television personalities such

as Andrew Zimmern, Samantha Brown, Don Wildman, Anthony Melchiorri, Bert Kreischer, Jack Maxwell, Josh Gates and Zak Bagans.

DIY Network

DIY Network is available in approximately 58 million U.S. television households and is simulcast in HD. DIY Network programming

provides entertaining and informational content across a broad range of do-it-yourself categories including home building, home improvement, crafts, gardening and landscaping. DIY Network appeals more strongly to male viewers with higher incomes in

the 18 to 49 age range and 25 to 54 age range.

Programming on DIY Networks includes Vanilla Ice Project,

Vanilla Ice Goes Amish,

Sledgehammer and the Crashers series. Many of the programs on DIY Network feature, or are hosted by, television personalities such as Jason Cameron, Alison Victoria,

Matt Muenster and Chris Lambton.

Cooking Channel

Cooking Channel is available in about 62 million domestic households and is simulcast in HD. We currently own approximately 69 percent of this network, which represents a controlling interest.

Tribune has a noncontrolling interest of approximately 31 percent in Cooking Channel.

Cooking Channel programming caters to

avid food lovers by focusing on food information and instructional cooking and delivers content focused on baking, ethnic cuisine, wine and spirits, healthy and vegetarian cooking and kids’ foods. The Cooking Channel appeals more strongly to

female viewers with higher incomes in the 18 to 49 age range and 25 to 54 age range.

Programming on Cooking Channel

includes Brunch @ Bobby’s, Emeril’s Florida, Extra Virgin, Man Fire Food, My Grandmother’s Ravioli and Rev Run’s Sunday Suppers. Cooking Channel hosts include notable television personalities such as

Debi Mazar and Gabriele Corcos, Emeril Lagasse, Haylie Duff, Mo Rocca, Rev Run and Justine Simmons.

Great American Country

Great American Country reaches about 60 million U.S. television households and is simulcast in HD. Great American Country provides its viewers with

programming that celebrates the country lifestyle and includes the country music experience, music performance specials, live concerts and country music videos.

Content on Great American Country includes Farm Kings, Kimberly’s Simply Southern, Celebrity Motor Homes and the Top 20 Country Countdown.

International

As a producer of

lifestyle content throughout the world, SNI is gaining scale through a concerted international growth strategy. As of December 31, 2014, the Company distributed six lifestyle brands via 20 unique distribution feeds, including HGTV,

6

DIY Network, Food Network, Asian Food Channel (“AFC”), Fine Living, and Travel Channel, reaching over 130 million subscribers. Content is distributed in 29 languages with channel

feeds customized according to language in more than 160 countries and territories across Europe, Middle East, Africa, Asia Pacific, Latin America and the Caribbean.

Internationally, we also have joint-venture partnerships with BBC Worldwide for UKTV and its suite of 10 general entertainment and lifestyle networks in the UK, and Shaw Media for HGTV, DIY Network and

Food Network in Canada. Programming content is made available through licensing and distribution to more than 220 countries and territories around the world.

In 2009, the Company launched its first international pay television channel through Food Network in the UK. The channel first launched on pay television, then expanded its distribution in 2011 to

free-to-air on Freeview, initially in primetime and then as a full 24-hour broadcast channel in 2012. Currently, Food Network is the top lifestyle channel and the third most viewed non-scripted factual channel in the UK. Food Network is also

available across EMEA, APAC and Latin America, where it most recently launched in Brazil.

In 2013, the Company acquired

AFC, a complementary channel brand to Food Network, in Asia. AFC, which is based in Singapore, broadcasts 24 hours a day, seven days a week and reaches about 8 million subscribers in 11 markets.

Travel Channel International Ltd. (“TCI”) was acquired in 2012 along with its base of operations in London. TCI is broadcast

in 21 languages across a wide network of affiliates throughout EMEA and APAC. In 2013, TCI also became available on Freeview in primetime in the UK.

In early 2014, we launched the Fine Living Network in Italy on the digital terrestrial television. Since its launch, over 40 percent of Italy’s television population has tuned into the channel. In

late 2014, we launched HGTV in Singapore, which is the first channel dedicated to the home and lifestyle category across Asia Pacific.

Our international businesses earn revenues from advertising sales, affiliate fees and the licensing of

programming to third parties. Satellite transmission fees, programming expenses, employee costs and sales and marketing expenses are the primary operating costs of our international

businesses.

Competition

Cable, satellite and telecommunications network programming is a highly competitive business in the U.S. and worldwide. Our television networks and websites generally compete for advertising revenue with

other cable and broadcast television networks, online and mobile outlets, radio programming and print media. Our television networks and websites also compete for their target audiences with all forms of programming and other media provided to

viewers, including broadcast networks, local over-the-air television stations, competitors’ pay and basic cable television networks, pay-per-view and video-on-demand services, streaming services, online activities and other forms of news,

information and entertainment. Additionally, our networks compete with other television networks for affiliate fees derived from distribution agreements with cable television and satellite operators, telecommunication service providers and other

distributors.

Intellectual Property

Our intellectual property (“IP”) assets include copyrights in television content, trademarks in brands, names and logos, websites, and licenses from third parties. To defend these assets, we

rely upon a combination of common law, statutory and contractual legal protections. There can be no assurance, however, of the degree to which these measures will be successful. Moreover, effective IP protection may be either unavailable or limited

in certain foreign territories. Policing unauthorized use of our products and services and related IP is difficult and costly. Third parties may challenge the validity or scope of our IP from time to time, and the success of any such challenges

could result in the limitation or loss of IP rights. Irrespective of their validity, such claims may result in substantial costs and diversion of resources which could have an adverse effect on our operations. In addition, piracy, which encompasses

the theft of our signal and unauthorized use of our content in the digital environment, continues to present a threat to revenues.

7

Regulatory Matters

The Company is subject to and affected by laws and regulations of U.S. federal, state and local governmental authorities as well as to the laws and regulations of international countries and bodies,

such as the European Union (the “EU”). These laws and regulations are subject to change. Additionally, the Federal Communications Commission (the “FCC”) regulates cable television and satellite operators and telecommunication

providers, which could affect our networks indirectly.

Closed Captioning

All of our cable networks must provide closed-captioning programming for the hearing impaired. The 21st Century Communications and Video Accessibility Act of 2010 also

requires us to provide closed captioning on certain video programming that we offer on the internet.

CALM Act

FCC rules require multichannel video programming distributors to ensure that all commercials comply with specified volume standards. Our affiliation

agreements generally require us to certify compliance with such standards.

“Must-Carry” Requirements

The FCC’s implementation of the statutory “must-carry” obligations requires cable operators and multichannel video programming distributors

to give broadcasters preferential access to channel space. In contrast, programming television networks, such as ours, have no guaranteed right of carriage on these systems. This may reduce the amount of channel space that is available for carriage

of our television networks by these systems.

Regulation of the Internet and Mobile Applications

We operate numerous websites and make available mobile applications (“apps”) which we use to distribute information about our programs and to

engage more deeply with our viewers. The operation of these websites and distribution of these apps are subject to a range of federal, state and local laws, such as privacy and consumer protection regulations.

Employees

As of December 31, 2014, we had approximately 2,100 full-time equivalent employees.

Executive Officers of the Company

Our

executive officers as of February 27, 2015 were as follows:

|

|

|

|

|

| Name |

|

Age |

|

Position |

| Kenneth W. Lowe |

|

64 |

|

Chairman, President and Chief Executive Officer (since July 2008); President, Chief Executive Officer and Director, The E. W. Scripps Company (2000 to 2008) |

|

|

|

| Joseph G. NeCastro |

|

58 |

|

Chief Development Officer (since February 2015); Chief Financial & Administrative Officer (2010 to 2015); Executive Vice President and Chief Financial Officer (2008 to 2010);

Executive Vice President and Chief Financial Officer, The E. W. Scripps Company (2006 to 2008) |

|

|

|

| Burton Jablin |

|

54 |

|

President, Scripps Networks (since October 2013); President, Home Category (2010 to 2013), President, HGTV (2008 to 2010); President HGTV, The E. W. Scripps Company (2001 to

2008) |

|

|

|

| Cynthia L. Gibson |

|

50 |

|

Executive Vice President, Chief Legal Officer and Corporate Secretary (since December 2012); Executive Vice President, Legal Affairs (2009 to

2012) |

8

|

|

|

|

|

| Name |

|

Age |

|

Position |

|

|

|

| Mark S. Hale |

|

56 |

|

Executive Vice President, Global Operations and Chief Technology Officer (since February 2010); Senior Vice President, Technology Operations and Chief Technology Officer (2008 to

2010); Senior Vice President/Technology Operations, The E. W. Scripps Company (2006 to 2008) |

|

|

|

| Lori A. Hickok |

|

51 |

|

Executive Vice President, Chief Financial Officer (since February 2015); Executive Vice President, Finance (2010 to 2015); Senior Vice

President, Finance (2008 to 2010); Vice President and Controller, The E. W. Scripps Company (2002 to 2008) |

|

|

|

| Nello-John Pesci Jr. |

|

52 |

|

Executive Vice President, Chief Human Resources Officer (since February 2015); Executive Vice President, Human Resources (2014 to 2015); Senior Vice President, Human Resources (2010

to 2014); Global Human Resources Leader, Procter & Gamble Company (1991 to 2010) |

ITEM 1A. RISK FACTORS

A number of significant risk factors could materially affect our specific business operations and cause our performance to differ materially from any future results projected or implied by our prior

statements. Based on the information currently known to us, we believe that the following information identifies the most significant risk factors affecting our company. The risks and uncertainties our Company faces, however, are not limited to

those set forth in the risk factors described below. Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial may also adversely affect our business.

In addition, past financial performance may not be a reliable indicator of future performance, and historical trends should not be used

to anticipate results or trends in future periods.

If any of the following risks or uncertainties develops into actual events, these events

could have a material effect on our business, financial condition or results of operations. In such case, the trading price of our common shares could decline.

Changes in public and consumer tastes and preferences could reduce demand for our services and reduce profitability of our businesses.

Each of our networks provides content and services whose success is primarily dependent upon acceptance by the public. We must consistently create and

distribute offerings that appeal to the prevailing consumer tastes at any point in time. Audience preferences change frequently, and it is a challenge to anticipate what content will be successful at any point. Other factors, including the

availability of alternative forms of entertainment and leisure time activities, general economic conditions and the growing competition for consumer discretionary spending may also affect the audience for our content and services. If our networks do

not achieve sufficient consumer acceptance, revenues may decline and adversely affect our profitability.

If we are unable to maintain

distribution agreements with cable and satellite distributors and telecommunications service providers (“Distributors”) at acceptable rates and terms, our revenues and profitability could be negatively affected.

We enter into multi-year contracts for our national television networks with Distributors. Our long-term distribution arrangements enable us to reach a

large percentage of cable households across the United States. As these contracts expire, we must renew or renegotiate them. If we are unable to renew them on acceptable terms or at rates similar to those in other affiliate contracts, we may lose

distribution rights and/or affiliate fee revenues.

These distribution agreements may also include “most favored

nation” (“MFN”) clauses. Such clauses typically provide that, in the event we enter into an agreement with another Distributor on more favorable terms, those terms must be offered to the Distributor holding the MFN right, subject to

certain exceptions and conditions. The MFN clauses within our distribution agreements are generally complex. Parties may interpret them differently and reach a

9

conflicting view of compliance of that held by the Company, which, if proven correct, could have an adverse effect on our financial condition or results of operations.

The loss of a significant affiliate arrangement on basic programming tiers could reduce distribution of our networks, thereby adversely

affecting affiliate fee revenue, subjecting certain of our intangible assets to possible impairments and potentially impacting our ability to sell advertising or the rates we charge for such advertising.

Three of our networks that are carried on digital tiers are dependent upon the willingness of consumers to pay for such tiers, as well

as our ability to negotiate favorable carriage agreements on widely accepted digital tiers.

Further consolidation among

cable and satellite distributors and telecommunications service providers could adversely affect our revenues, profitability and financial condition of our businesses. Consolidation among Distributors has given the largest cable and satellite

television systems considerable leverage in their relationship with programmers. The two largest cable television system operators provide service to approximately 35 percent of households receiving cable or satellite television service today, while

the two largest satellite television operators provide service to an additional 34 percent of such households.

Continued

consolidation within the industry could reduce the number of Distributors available to carry our programming, subject our affiliate fee revenue to greater volume discounts and further increase the negotiating leverage of the cable and satellite

television system operators, which could have an adverse effect on our financial condition or results of operations.

Our networks face

significant competitive pressures related to attracting consumers and advertisers. Failure by us to maintain our competitive advantage may affect the profitability of our networks.

We face substantial competition from alternative providers of similar services. Our national television networks compete for viewers with other broadcast and national television networks and with home

video products and internet usage, as well as with other programming providers for carriage of programming. Additionally, our national television networks compete for advertising revenues with a

variety of other media alternatives, including other broadcast and national television networks, the internet, newspapers, radio stations and print media. Our websites compete for visitors and advertising dollars with other forms of media aimed at

attracting similar audiences and, therefore, must provide popular content in order to maintain and increase site traffic. Competition may divert consumers from our services, which could reduce the profitability of our networks.

Changes in consumer behavior resulting from new technologies and distribution platforms may impact the performance of our networks.

We must adapt to advances in technologies and distribution platforms related to content transfer to ensure that our content remains

desirable and widely available to our audiences. The ability to anticipate and take advantage of new and future sources of revenue from technological developments will affect our ability to continue to increase our revenue and expand our business.

Additionally, we must adapt to the changing consumer behavior driven by advances in technology, such as video-on-demand, and devices, such as tablets and mobile, providing consumers the ability to view content from remote locations and enabling

general preferences for user-generated and interactive content. Changes of these types may impact our traditional distribution methods for our content. If we cannot ensure that our distribution methods and content allow us to reach our target

audiences, there could be a negative effect on our business.

Our lifestyle media business is subject to risks of adverse changes in

laws and regulations, which could result in reduced distribution of certain of our national television networks.

Our programming

services and the distributors of our programming, including cable and satellite operators, telecommunication providers and internet companies, are regulated by U.S. federal laws and regulations issued and administered by various federal

agencies, including the FCC, as well as by state and local governments. The U.S. Congress and the FCC currently have under consideration, and may in the

10

future adopt, new laws, regulations and policies regarding a wide variety of matters that could, directly or indirectly, affect our operations. For example, legislators and regulators continue to

consider rules that would effectively require cable television operators to offer all programming on an à la carte basis, which would allow viewers to subscribe to individual networks rather than a package of channels, and/or require

programmers to sell channels to Distributors on an à la carte basis. Certain cable television operators and other Distributors have already introduced tiers, or more targeted channel packages, to their customers that may or may not include

some or all of our networks. The unbundling of programming could reduce distribution of certain of our networks, thereby leading to reduced viewership and increased marketing expenses and affect our ability to compete for or attract the same level

of advertising dollars or distribution fees.

Changes in economic conditions in the United States, the regional economies in which we

operate or in specific industry sectors could adversely affect the profitability of our businesses.

Approximately 70 percent of

our consolidated revenues in 2014 were derived from marketing and advertising spending by businesses operating in the United States. Advertising and marketing spending is sensitive to economic conditions and tends to decline in recessionary periods.

An economic decline could reduce advertising prices and volume, resulting in a decrease in our advertising revenues.

The loss of key

talent could disrupt our business and adversely affect the profitability of our businesses.

Our business depends upon the continued

efforts, abilities and expertise of our corporate and divisional executive teams and entertainment personalities. We employ or contract with entertainment personalities who may have loyal audiences. These individuals are important to audience

endorsement of our programs and other content. There can be no assurance that these individuals will remain with us or retain their current audiences. If we fail to retain key individuals or if our entertainment personalities lose their current

audience base, our operations could be adversely affected.

The financial performance of our equity method investments could adversely impact our results of

operations.

We have investments in businesses that we account for under the equity method of accounting. We do not control the day to

day operations of our equity method investments, and thus the management of these businesses by our partners could impact their performance. Additionally, these businesses are subject to laws, regulations or market conditions, or have risks inherent

in their operations, similar to the businesses we operate. Any of these factors could adversely impact our results of operations and the value of our investment.

We are subject to risks related to our international operations.

We have operations

and investments in a number of foreign jurisdictions. The inherent economic risks of doing business in international markets include, among other things, changes in the economic environment, exchange controls, tariffs and other trade barriers,

foreign taxation, corruption and, in some markets, increased risk of political instability. Additionally, the local currencies in which our international operations conduct their business could change in value relative to the U.S. dollar, exposing

our results to exchange rate fluctuations.

We may not be able to protect IP rights upon which our business relies. If we lose IP

protection, we may lose valuable assets.

Our business depends on our IP. We attempt to protect these IP rights through a combination

of copyright, trade secret, patent and trademark law and contractual restrictions, such as confidentiality agreements. We also depend on our trade names and domain names. We file applications for patents, trademarks and other IP registrations, but

we may not be granted such IP protections. In addition, even if such registrations are issued, they may not fully protect all important aspects of our business, and there is no guarantee that our business does not, or will not, infringe upon IP

rights of others. Furthermore, IP laws vary from country to country, and it may be more difficult to protect and enforce our IP rights in some foreign jurisdictions. In the future, we may need to litigate in the United States or elsewhere to enforce

our IP rights or determine the

11

validity and scope of the proprietary rights of others. This litigation could potentially be expensive and possibly divert the attention of our management. Despite our efforts to protect our

proprietary rights, unauthorized parties may attempt to copy or otherwise obtain and use our service, technology and other IP, and we cannot be certain that the steps we have taken will prevent any misappropriation or confusion among consumers and

merchants or unauthorized use of these rights. If we are unable to protect and enforce our IP rights, then we may not realize the full value of these assets, and our business may suffer.

We face cybersecurity and similar risks, which could result in the disclosure of confidential information, disruption of our programming services, damage to our brands and reputation, legal exposure

and financial losses

Our online, mobile and app offerings, as well as our internal systems, involve the storage and transmission of

our and our users’ proprietary information, and we and our partners rely on various technology systems in connection with the production and distribution of our programming. Although we monitor our security measures regularly, they may be

breached due to employee error, computer malware, viruses, hacking and phishing attacks or otherwise. Additionally, outside parties may attempt to fraudulently induce employees or users to disclose sensitive or confidential information in order to

gain access to our data or our users’ data. Because the techniques used to obtain unauthorized access, disable or degrade service or sabotage systems change frequently and often are not recognized until launched against a target, we may be

unable to anticipate these techniques or to implement adequate preventative measures. Any such breach or unauthorized access could result in a loss of our or our users’ proprietary information, a disruption of our services or a reduction of the

revenues we are able to generate from such services, damage to our brands and reputation, a loss of confidence in the security of our offerings and services and significant legal and financial exposure, each of which could potentially have an

adverse effect on our business.

We may be subject to claims of infringement of third-party IP rights, which could harm our business.

From time to time, third parties may assert against us or our customers alleged patent, copyright, trademark or other IP rights to

technologies that are important to our business. We may be subject to IP infringement claims from certain individuals and companies who have acquired patent portfolios for the sole purpose of asserting such claims against other companies. Any claims

that our products or processes infringe the IP rights of others, regardless of the merit or resolution of such claims, could cause us to incur significant costs in responding to, defending and resolving such claims, and may divert the efforts and

attention of our management and technical personnel away from our business for a period of time. In addition, if we are unable to continue use of certain IP rights, our revenue could be negatively impacted.

If we are unable to successfully integrate key acquisitions our business results could be negatively impacted.

We may grow through acquisitions in certain markets. Acquisitions involve risks, including difficulties in integrating acquired operations, diversions of

management resources, debt incurred in financing such acquisitions and other unanticipated problems and liabilities. If we are unable to mitigate these risks, the integration and operations of an acquired business could be adversely impacted.

Similarly, declines in business performance and the related effect on the fair values of goodwill and other intangible assets could trigger impairment charges, which could materially affect our reported net earnings.

Financial market conditions may impede access to or increase the cost of financing our operations and investments.

The ongoing changes in U.S. and global credit and equity markets may make it more difficult for many businesses to obtain financing on acceptable terms.

In addition, our borrowing costs can be affected by short and long-term debt ratings assigned by independent rating agencies which are based, in significant part, on our performance as measured by credit metrics such as interest coverage and

leverage

12

ratios. A decrease in these ratings could increase our cost of borrowing or make it more difficult for us to obtain future financing.

The concentrated ownership of our Common Voting Shares limits the ability of the holders of our Class A Common Shares to influence corporate matters.

We have two classes of shares: Common Voting Shares and Class A Common Shares. Holders of Class A Common Shares are entitled to elect one-third

of the Board of Directors (the “Board”), but are not permitted to vote on any other matters except as required by Ohio law. Holders of Common Voting Shares are entitled to elect the remainder of the Board and to vote on all other matters.

Approximately 92 percent of the Common Voting Shares are subject to the Scripps Family Agreement. The provisions of the Scripps Family Agreement fully govern the transfer and voting of Common Voting Shares subject to the agreement. As a result, the

holders of the Common Voting Shares subject to the Scripps Family agreement have the ability to elect two-thirds of the Board and to direct the outcome of any matter that does not require a vote of the Class A Common Shares. This concentrated

control limits the ability of our Class A Common shareholders to influence corporate matters and could potentially enable the Company to take actions that these shareholders would not view as beneficial. As a result, the market price of our

Class A Common Shares could be adversely affected.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2.

PROPERTIES

We operate primarily from an owned office facility in Knoxville, TN, and leased facilities in New York,

NY, Washington, DC., Miami, FL, London and Singapore. Additionally, we lease other facilities that employ a smaller portion of our workforce.

Management believes its properties are adequate to support the business efficiently and that the properties and equipment have been

well maintained.

ITEM 3. LEGAL PROCEEDINGS

From time to time, the Company receives notices from third parties claiming that it infringes their IP rights. Claims of IP infringement could require us to enter into royalty or licensing agreements on

unfavorable terms, incur substantial monetary liability or be enjoined preliminarily or permanently from further use of the IP in question. In addition, certain agreements entered into by the Company may require the Company to indemnify the other

party for certain third-party IP infringement claims, which could increase the Company’s damages and its costs of defending against such claims. Even if the claims are without merit, defending against the claims can be time-consuming and

costly.

The costs and other effects of pending or future litigation, governmental investigations, legal and administrative

cases and proceedings (whether civil or criminal), settlements, judgments and investigations, claims and changes in those matters (including those matters described above) and developments or assertions by or against the Company relating to IP

rights and IP licenses, could have a material effect on the Company’s business, financial condition and operating results. No current legal matters are expected to result in any material loss.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

13

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER

MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our Class A Common Shares are traded on the New York Stock Exchange (“NYSE”)

under the ticker symbol SNI. As of December 31, 2014, there were approximately 51,000 owners of our Class A Common Shares based on security position listings, and 69 owners of our Common Voting Shares, which do not have a public market.

The following table reflects the range of high and low selling prices of our common stock

by quarterly period.

|

|

|

|

|

|

|

|

|

| |

|

High |

|

|

Low |

|

| 2014 |

|

|

|

|

|

|

|

|

| First quarter |

|

$ |

86.62 |

|

|

$ |

71.33 |

|

| Second quarter |

|

$ |

82.37 |

|

|

$ |

72.13 |

|

| Third quarter |

|

$ |

86.48 |

|

|

$ |

76.13 |

|

| Fourth quarter |

|

$ |

82.78 |

|

|

$ |

71.06 |

|

| 2013 |

|

|

|

|

|

|

|

|

| First quarter |

|

$ |

65.81 |

|

|

$ |

57.32 |

|

| Second quarter |

|

$ |

71.05 |

|

|

$ |

63.53 |

|

| Third quarter |

|

$ |

79.13 |

|

|

$ |

66.83 |

|

| Fourth quarter |

|

$ |

86.41 |

|

|

$ |

72.30 |

|

The following table

provides information about the Company purchases of equity securities that are registered by the Company pursuant to section 12 of the Exchange Act during the quarter ended December 31, 2014:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Period |

|

Total Number of

Shares Purchased |

|

|

Average Price Paid per

Share |

|

|

Total Number of

Shares Purchased as

Part of Publicly

Announced Plans

or

Programs |

|

|

Maximum Dollar Value

of Shares that May Yet

Be Purchased Under

the Plans or

Programs |

|

| 10/1/14 — 10/31/14 |

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

845,855,310 |

|

| 11/1/14 — 11/30/14 |

|

|

463,232 |

|

|

$ |

77.69 |

|

|

|

463,232 |

|

|

|

809,858,138 |

|

| 12/1/14 — 12/31/14 |

|

|

4,681,717 |

|

|

|

77.50 |

|

|

|

4,681,717 |

|

|

|

447,501,680 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total |

|

|

5,144,949 |

|

|

$ |

77.52 |

|

|

|

5,144,949 |

|

|

$ |

447,501,680 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Under a share repurchase program (the “repurchase program”) authorized by the

Board, the Company is permitted to acquire $2 billion of Class A Common Shares.

On February 19, 2015, the Board

authorized an additional $1 billion for the repurchase program. Following the February 19, 2015 authorization, $1.4 billion remains available for repurchase under the repurchase program. There is no expiration date for the repurchase program,

and we are under no commitment or obligation to repurchase any particular amount of Class A Common Shares under this repurchase program.

There were no sales of unregistered equity securities during the quarter for which this

report is filed.

Dividends — The Company paid a quarterly cash dividend of 20 cents per share and 15 cents per share in

2014 and 2013, respectively. The declaration and payment of dividends is evaluated by the Company’s Board. Future dividends are subject to our earnings, financial condition and capital requirements.

14

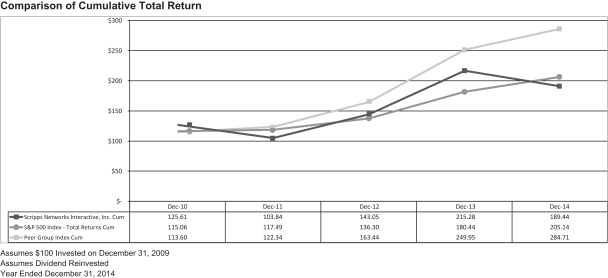

Performance Graph — The following graph compares the cumulative total stockholder return

on our Class A Common Shares with the comparable cumulative return of the S&P 500 index and an index based on a peer group of media companies for the five years ended December 31, 2014. The performance graph assumes that

the value of the investment in our common shares, the S&P 500 index and peer group of media companies was $100 on December 31, 2009, and that all dividends were reinvested.

The companies that comprise our peer group include AMC Networks, Inc., Discovery Communications, Inc., The Walt Disney

Company, Time Warner, Inc., Twenty-First Century Fox, Inc. and Viacom, Inc.

The peer group index is weighted based on market

capitalization.

ITEM 6. SELECTED FINANCIAL DATA

The Selected Financial Data required by this item is filed as part of this Form 10-K. See Index to Consolidated Financial Statement Information at page

F-1 of this Form 10-K.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

Management’s Discussion and Analysis of Financial Condition and Results of Operations required by this item is filed as part

of this Form 10-K. See Index to Consolidated Financial Statement Information at page F-1 of this Form 10-K.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

The market risk information required by this item is filed as part of this Form 10-K. See Index to Consolidated Financial Statement Information at page

F-1 of this Form 10-K.

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

The Financial Statements and Supplementary Data required by this item are filed as part of this Form 10-K. See

Index to Consolidated Financial Statement Information at page F-1 of this Form 10-K.

ITEM 9. CHANGES IN AND

DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

None.

ITEM 9A. CONTROLS AND PROCEDURES

The Controls and Procedures

required by this item are filed as part of this Form 10-K. See Index to Consolidated Financial Statement Information at page F-1 of this Form 10-K.

ITEM 9B. OTHER INFORMATION

None.

15

PART III

ITEM 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

Information regarding executive officers is included in Part I of this Form 10-K as permitted by General Instruction G(3).

Information required by Item 10 of Form 10-K relating to directors is incorporated by reference to the material captioned

“Election of Directors” in our definitive proxy statement for the Annual Meeting of Shareholders (“Proxy Statement”). Information regarding Section 16(a) compliance is incorporated by reference to the material captioned

“Section 16(a) Beneficial Ownership Compliance” in the Proxy Statement.

We have adopted a code of ethics that

applies to all employees, officers and directors of SNI. We also have a code of ethics for the CEO and Senior Financial Officers. This code of ethics meets the requirements defined by Item 406 of Regulation S-K and the requirement of a code of

business conduct and ethics under NYSE listing standards. Copies of our codes of ethics are posted on our website at www.scrippsnetworksinteractive.com.

Information regarding our audit committee financial expert is incorporated by reference to the material captioned “Corporate Governance” in the Proxy Statement.

The Proxy Statement will be filed with the SEC in connection with our 2015 Annual Meeting of Stockholders.

ITEM 11. EXECUTIVE COMPENSATION

The information required by Item 11 of Form 10-K is incorporated by reference to the materials captioned “Compensation Discussion and

Analysis” and “Executive Compensation Tables” in the Proxy Statement.

ITEM 12. SECURITY

OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS

The information required by Item 12 of Form 10-K is

incorporated by reference to the materials captioned “Report on the Security Ownership of Certain Beneficial Owners” and “Equity Compensation Plan Information” in the Proxy Statement.

ITEM 13. CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE

The information required by Item 13 of Form 10-K is incorporated by reference to the materials captioned “Corporate Governance” and

“Report on Related Party Transactions” in the Proxy Statement.

ITEM 14. PRINCIPAL ACCOUNTING FEES

AND SERVICES

The information required by Item 14 of Form 10-K is incorporated by reference to the material captioned “Independent

Auditors” in the Proxy Statement.

16

PART IV

ITEM 15. EXHIBITS AND FINANCIAL STATEMENT SCHEDULE

Financial Statements and Supplemental

Schedule

(a) The consolidated financial statements of SNI are filed as part of this Form 10-K. See Index to Consolidated

Financial Statement Information at page F-1.

The reports of Deloitte & Touche LLP, an Independent Registered

Public Accounting Firm, dated February 27, 2015, are filed as part of this Form 10-K. See Index to Consolidated Financial Statement Information at page F-1.

(b) The Company’s consolidated supplemental schedule is filed as part of this Form 10-K. See Index to Consolidated Financial

Statement Schedules at page S-1.

Exhibits

The information required by this item appears at page E-1 of this Form 10-K.

17

SIGNATURES

Pursuant to the requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly

authorized.

|

|

|

|

|

|

|

|

|

|

|

SCRIPPS NETWORKS INTERACTIVE, INC. |

|

|

|

|

| Dated: February 27, 2015 |

|

|

|

By: |

|

/s/ Kenneth W. Lowe |

| Kenneth W. Lowe |

|

|

|

|

|

|

| Chairman, President and Chief Executive Officer |

|

|

|

|

|

|

Pursuant to the requirements of the Securities Exchange Act of 1934, this report has been signed below by the following

persons on behalf of the registrant in the capacities indicated, on February 27, 2015.

|

|

|

|

|

| Signature |

|

|

|

Title |

|

|

|

| /s/ Kenneth W. Lowe Kenneth W. Lowe |

|

|

|

Chairman, President and Chief Executive Officer (Principal Executive Officer) |

|

|

|

| /s/ Lori A. Hickok Lori A. Hickok |

|

|

|

Executive Vice President, Chief Financial Officer (Principal Financial and Accounting Officer) |

|

|

|

| /s/ Gina L. Bianchini Gina L. Bianchini |

|

|

|

Director |

|

|

|

| /s/ Michael R. Costa Michael R. Costa |

|

|

|

Director |

|

|

|

| /s/ David A. Galloway David A. Galloway |

|

|

|

Director |

|

|

|

| /s/ Jarl Mohn Jarl Mohn |

|

|

|

Director |

|

|

|

| /s/ Richelle P. Parham Richelle P. Parham |

|

|

|

Director |

|

|

|

| /s/ Nicholas B. Paumgarten Nicholas B. Paumgarten |

|

|

|

Director |

|

|

|

| /s/ Mary Peirce Mary Peirce |

|

|

|

Director |

|

|

|

| /s/ Jeffrey Sagansky Jeffrey Sagansky |

|

|

|

Director |

|

|

|

| /s/ Nackey E. Scagliotti Nackey E. Scagliotti |

|

|

|

Director |

|

|

|

| /s/ Wesley W. Scripps Wesley W. Scripps |

|

|

|

Director |

|

|

|

| /s/ Ronald W. Tysoe Ronald W. Tysoe |

|

|

|

Director |

18

SCRIPPS NETWORKS INTERACTIVE, INC. INDEX TO CONSOLIDATED FINANCIAL STATEMENT INFORMATION

F-1

Selected Financial Data

Five-Year Financial Highlights

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (in millions, except per share data) |

|

2014 |

|

|

2013 |

|

|

2012 |

|

|

2011 |

|

|

2010 |

|

| Summary of Operations |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Operating revenues (1)(3): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Lifestyle media |

|

$ |

2,575 |

|

|

$ |

2,456 |

|

|

$ |

2,253 |

|

|

$ |

2,041 |

|

|

$ |

1,864 |

|

| Corporate and other |

|

|

90 |

|

|

|

76 |

|

|

|

54 |

|

|

|

31 |

|

|

|

19 |

|

| Intersegment eliminations |

|

|

|

|

|

|

(1 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total operating revenues |

|

$ |

2,665 |

|

|

$ |

2,531 |

|

|

$ |

2,307 |

|

|

$ |

2,072 |

|

|

$ |

1,883 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Segment profit (loss) (1)(2)(3): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Lifestyle media |

|

$ |

1,255 |

|

|

$ |

1,202 |

|

|

$ |

1,124 |

|

|

$ |

1,046 |

|

|

$ |

901 |

|

| Corporate and other |

|

|

(134 |

) |

|

|

(100 |

) |

|

|

(83 |

) |

|

|

(69 |

) |

|

|

(66 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total segment profit |

|

$ |

1,122 |

|

|

$ |

1,102 |

|

|

$ |

1,041 |

|

|

$ |

977 |

|

|

$ |

835 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income from continuing operations attributable to SNI common shareholders (4) |

|

$ |

545 |

|

|

$ |

505 |

|

|

$ |

681 |

|

|

$ |

473 |

|

|

$ |

398 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Per Share Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income from continuing operations attributable to SNI common shareholders per basic share of common stock (4) |

|

$ |

3.86 |

|

|

$ |

3.43 |

|

|

$ |

4.48 |

|

|

$ |

2.87 |

|

|

$ |

2.39 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income from continuing operations attributable to SNI common shareholders per diluted share of common stock (4) |

|

$ |

3.83 |

|

|

$ |

3.40 |

|

|

$ |

4.44 |

|

|

$ |

2.86 |

|

|

$ |

2.37 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash dividends declared |

|

|

.80 |

|

|

|

.60 |

|

|

|

.48 |

|

|

|

.38 |

|

|

|

.30 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Balance Sheet Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total assets |

|

$ |

4,668 |

|

|

$ |

4,438 |

|

|

$ |

4,139 |

|

|

$ |

3,962 |

|

|

$ |

3,388 |

|

| Debt (5)(6)(7) |

|

$ |

2,379 |

|

|

$ |

1,384 |

|

|

$ |

1,384 |

|

|

$ |

1,384 |

|

|

$ |

884 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Certain amounts may not foot since each is rounded independently.

Notes to Selected Financial Data

| (1) |

Operating revenues and segment profit (loss) represent the measures used to evaluate the operating performance of our business segments in accordance with financial

accounting standards for disclosures about segments of an enterprise and related information. See page F-8. |

| (2) |

Segment profit is a supplemental non-GAAP financial measure. “GAAP” is defined as generally accepted accounting principles in the United States. Our chief

operating decision maker evaluates the operating performance of our business segments and makes decisions about the allocation of resources to our reportable segments using a measure we call segment profit. Segment profit excludes interest, income

taxes, depreciation and amortization, divested operating units, investment results and certain other items that are included in net income determined in accordance with GAAP. For a reconciliation of this financial measure to operating income see the

table on page F-9. |

| (3) |

In 2014, we made changes to our management reporting structure related to operating results from our uLive business and our businesses located in the Caribbean. In

conjunction with these changes in our reporting structure, we now report the results of uLive within the lifestyle media segment, rather than the corporate and other caption. The results of the Caribbean businesses are now reported within

international operations, included within the corporate and other caption for segment reporting purposes, rather than the lifestyle media segment. For comparability purposes, prior year segment results have also been reclassified to reflect the

impact of these management reporting changes. These reclassifications only affect our segment reporting and do not change our consolidated operating revenues, operating income or net income. |

F-2

| (4) |

Our income tax provision in 2012 reflects an income tax benefit of $213 million arising from the reversal of valuation allowances on deferred tax assets related to

capital loss carry forwards. Previously, the Company had estimated that it would be unable to use any of the capital loss carry forwards generated from the sale of our Shopzilla and uSwitch businesses. As a consequence of a restructuring that was

completed to achieve a more efficient tax structure, the Company recognized a $574 million capital gain that utilized substantially all of its capital loss carry forwards. This income tax benefit was partially offset by $23.1 million of state income

tax expenses recognized on the capital gain that utilized these capital loss carry forwards. |

| (5) |

On December 15, 2009, we acquired a 65 percent controlling interest in the Travel Channel. In connection with this acquisition, a majority-owned subsidiary of SNI

completed a private placement of $885 million aggregate principal Senior Notes that mature in 2015 |

| (6) |

In 2011, we completed the sale of $500 million aggregate principal Senior Notes that mature in 2016. |

| (7) |

In 2014, we completed the sale of $500 million aggregate principal Senior Notes that mature in 2019 and $500 million aggregate principal Senior Notes that mature in

2024. |

F-3

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

This discussion and analysis of financial condition and results of operations is based upon the consolidated financial statements

and the notes thereto. You should read this discussion in conjunction with those financial statements.

Forward-Looking Statements

This discussion and the information contained in the notes to the consolidated financial statements contain certain forward-looking statements that are based on our

current expectations. Forward-looking statements are subject to certain risks, trends and uncertainties that could cause actual results to differ materially from the expectations expressed in the forward-looking statements. Such risks, trends and

uncertainties, which, in most instances, are beyond our control, include changes in advertising demand and other economic conditions; consumers’ tastes; program costs; labor relations; technological developments; competitive pressures; interest

rates; regulatory rulings; and reliance on third-party vendors for various products and services. The words “believe,” “expect,” “anticipate,” “estimate,” “intend” and similar expressions identify

forward-looking statements. All forward-looking statements, which are as of the date of this filing, should be evaluated with the understanding of their inherent uncertainty. We undertake no obligation to publicly update any forward-looking

statement to reflect events or circumstances after the date the statement is made.

Overview

SNI is one of the leading developers of lifestyle-oriented content for linear and interactive video platforms including television and the internet, with

respected, high-profile brands. We seek to engage audiences that are highly desirable to advertisers with entertaining and informative lifestyle content that is produced for television, the internet and any other media platforms consumers choose. We

intend to expand and enhance our lifestyle brands through creating popular new programming and content, distributing on various platforms, such as mobile phones, tablets and video-on-demand, licensing of content and branded consumer products and

increasing our international footprint.

We manage our operations through our reportable segment, lifestyle media. Lifestyle media

includes our national television networks, HGTV, Food Network, Travel Channel, DIY Network, Cooking Channel and Great American Country. Lifestyle media also includes websites that are associated with the aforementioned television brands and other internet-based businesses serving home, food and travel related categories.

Lifestyle media

generated revenues of approximately $2.6 billion during 2014, which represented 97 percent of our consolidated revenues, compared with $2.5 billion and 97 percent in 2013 and $2.3 billion and 98 percent in 2012. Lifestyle media generates revenue

principally from the sale of advertising time on national television networks and interactive media platforms and from affiliate fees paid by cable and television systems, telecommunication service providers and other distributors that carry our

network programming. Advertising revenues for lifestyle media may be affected by the strength of advertising markets and general economic conditions and may also fluctuate depending on the success of our programming, as measured by viewership at any

given time, and by seasonality. In 2014, lifestyle media revenues from advertising sales and affiliate fees were approximately 69 percent and 29 percent, respectively, of total revenue for the segment. Lifestyle media also earns revenue from the

licensing of content to third parties and brands for consumer products, such as videos, books, kitchenware and tools.

Programming expenses, employee costs and sales and marketing expenses are the primary operating costs of our lifestyle media. Program

amortization represented 46 percent of lifestyle media expenses in 2014, reflecting our continued investment in the improved quality and variety of programming on our networks. We incur sales and marketing expenses to support brand-building

initiatives at all of our television networks.

We also have established lifestyle media brands internationally. We currently

broadcast 20 channels reaching approximately 130 million subscribers under the HGTV, DIY, Food Network, AFC, Fine Living and Travel Channel brands. Our broadcast channels are distributed in 29 languages with channel feeds customized according

to language in more than 160 countries and territories across Europe, Middle

F-4

East, Africa, Asia Pacific, Latin America and the Caribbean. In addition to the broadcast networks, we also license a portion of our programming to other broadcasters that can be seen in over 220

countries and territories. Operating results for our international businesses are reported within our corporate and other segment caption.

Our international businesses generated revenues of approximately $90.2 million during 2014, which represented 3 percent of our consolidated revenues compared with $75.7 million and 3 percent in 2013 and

$54.5 million and 2 percent in 2012. These businesses earn revenues from advertising sales, affiliate fees and the licensing of programming to third parties. In 2014, revenues from advertising sales, affiliate fees and program licensing were

approximately 32 percent, 48 percent and 20 percent, respectively, of total revenue for our international businesses. Satellite transmission fees, programming expenses, employee costs and sales and marketing expenses are the primary operating costs

for our international businesses.

The growth of our international business, both organically and through acquisitions and

joint ventures, has been, and continues to be, a strategic priority of the Company. In the fourth quarter of 2014, we launched HGTV in Singapore, which is the first channel dedicated to the home and lifestyle category across Asia Pacific. In the

third quarter of 2014, we announced the launch of Food Network in Brazil. In the first quarter of 2014, we launched the Fine Living Network in Italy on digital terrestrial television. Since its launch, over 40 percent of Italy’s television

population has tuned into the channel. In the second quarter of 2013, we completed our acquisition of AFC. AFC, which is based in Singapore, reaches about 8 million subscribers in 11 markets. In the second quarter of 2012, we completed our

acquisition of TCI. TCI is broadcast in 21 languages across a wide network of affiliates throughout EMEA and APAC.

Results

of Operations

The competitive landscape in our business is affected by multiple media platforms competing for consumers and advertising

dollars. We strive to create popular programming that resonates with viewers across a variety of demographic groups, develop brands and create new media platforms through which we can capitalize on the audiences we aggregate.

Consolidated Results of Operations — Results of operations were as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (in thousands) |

|

For the years ended December 31, |