Attached files

| file | filename |

|---|---|

| EX-23 - EX-23 - TREX CO INC | d828432dex23.htm |

| EX-21 - EX-21 - TREX CO INC | d828432dex21.htm |

| EX-32 - EX-32 - TREX CO INC | d828432dex32.htm |

| EX-31.1 - EX-31.1 - TREX CO INC | d828432dex311.htm |

| EX-10.3 - EX-10.3 - TREX CO INC | d828432dex103.htm |

| EX-31.2 - EX-31.2 - TREX CO INC | d828432dex312.htm |

| EX-10.1 - EX-10.1 - TREX CO INC | d828432dex101.htm |

| EXCEL - IDEA: XBRL DOCUMENT - TREX CO INC | Financial_Report.xls |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-14649

Trex Company, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 54-1910453 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 160 Exeter Drive, Winchester, Virginia | 22603-8605 | |

| (Address of principal executive offices) | (Zip Code) | |

(540) 542-6300

Registrant’s telephone number, including area code:

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: |

Name of each exchange on which registered: | |

| Common Stock, par value $0.01 per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posed pursuant to Rule 405 of Regulation S-T during the preceding 12 months. Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting Company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting Company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer þ | Accelerated filer ¨ | |||

| Non-accelerated filer ¨ (Do not check if a smaller reporting Company) | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell Company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate market value of the registrant’s common equity held by non-affiliates of the registrant at June 30, 2014, which was the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $908.9 million based on the closing price of the common stock as reported on the New York Stock Exchange on such date and assuming, for purposes of this computation only, that the registrant’s directors, executive officers and beneficial owners of 10% or more of the registrant’s common stock are affiliates.

The number of shares of the registrant’s common stock outstanding on February 10, 2015 was 32,020,203.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the following documents are incorporated by reference in this Form 10-K as indicated herein:

| Document |

Part of 10-K into which incorporated | |

| Proxy Statement relating to Registrant’s 2015 Annual Meeting of Stockholders |

Part III |

Table of Contents

| Page | ||||||

| PART I | ||||||

| Item 1. |

1 | |||||

| Item 1A. |

9 | |||||

| Item 1B. |

13 | |||||

| Item 2. |

13 | |||||

| Item 3. |

14 | |||||

| Item 4. |

14 | |||||

| PART II | ||||||

| Item 5. |

15 | |||||

| Item 6. |

17 | |||||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

19 | ||||

| Item 7A. |

31 | |||||

| Item 8. |

32 | |||||

| Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

32 | ||||

| Item 9A. |

32 | |||||

| Item 9B. |

35 | |||||

| PART III | ||||||

| Item 10. |

36 | |||||

| Item 11. |

36 | |||||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

36 | ||||

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

36 | ||||

| Item 14. |

36 | |||||

| PART IV | ||||||

| Item 15. |

37 | |||||

| F-1 | ||||||

i

Table of Contents

NOTE ON FORWARD-LOOKING STATEMENTS

This report, including the information it incorporates by reference, contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. We intend our forward-looking statements to be covered by the safe harbor provisions for forward-looking statements in these sections. All statements regarding our expected financial position and operating results, our business strategy, our financing plans, forecasted demographic and economic trends relating to our industry and similar matters are forward-looking statements. These statements can sometimes be identified by our use of forward-looking words such as “believe,” “may,” “will,” “anticipate,” “estimate,” “expect” or “intend.” We cannot promise you that our expectations in such forward-looking statements will turn out to be correct. Our actual results could be materially different from our expectations because of various factors, including the factors discussed under “Risk Factors” in this report.

ii

Table of Contents

Some of the information contained in this report concerning the markets and industry in which we operate is derived from publicly available information and from industry sources. Although we believe that this publicly available information and the information provided by these industry sources are reliable, we have not independently verified the accuracy of any of this information.

| Item 1. | Business |

General

Trex Company, Inc. (the “Company”), founded as a Delaware corporation in 1998, is the world’s largest manufacturer of wood-alternative decking and railing products, which are marketed under the brand name Trex®. Our principal executive offices are located at 160 Exeter Drive, Winchester, Virginia 22603, and our telephone number at that address is (540) 542-6300. We operate in one business segment.

Products

We offer a comprehensive set of aesthetically durable, low maintenance product offerings in the decking, railing, porch, fencing, trim, steel deck framing and outdoor lighting categories. We believe that the range and variety of our product offerings allow consumers to design much of their outdoor living space using Trex brand products. A majority of our products are made in a proprietary process that combines waste wood fibers and scrap polyethylene. Our products are provided in a wide selection of popular sizes and lengths and are available with several finishes and numerous colors.

Decking. We market our decking products under a number of brand names. Our principal brand names for decking are: Trex Transcend®, Trex Enhance® and Trex Select®, which each feature a protective shell for enhanced protection against fading, staining, mold and scratching. We also offer Trex Hideaway®, a hidden fastening system for specially grooved boards.

Railing. Our railing products are Trex Transcend Railing, Trex Designer Series Railing®, Trex Select Railing, and Trex Reveal® aluminum railing. Trex Transcend Railing is available in the colors of Trex Transcend decking and finishes that make it appropriate for use with Trex decking products as well as other decking materials, which we believe enhances the sales prospects of our railing products. Our Designer Series Railing system consists of a decorative top and bottom rail, refined balusters, our Trex RailPost™, and post caps and skirts. Trex Select Railing, which is white, is for consumers who desire a simple clean finished look for their deck. Trex Reveal aluminum railing, which is available in three colors, is for consumers who want a sleek, contemporary aesthetic look.

Porch. Our Trex Transcend Porch Flooring and Railing System is an integrated system of porch components and accessories.

Fencing. We offer our Trex Seclusions® fencing product through two specialty distributors. This product consists of structural posts, bottom rail, pickets, top rail and decorative post caps.

Trim. Our TrexTrim™ product is a low maintenance cellular PVC residential exterior trim product that offers exceptional workability, durability, visual appeal and a low level of required maintenance.

Steel Deck Framing. We offer a triple-coated steel deck framing system called Trex Elevations®.

Outdoor Lighting. Our outdoor lighting systems are Trex DeckLighting™ and Trex Landscape Lighting™. Trex DeckLighting is a line of energy-efficient LED dimmable deck lighting, which is designed for use on posts, floors and steps. The line includes a post cap light, deck rail light, riser light and a recessed deck light. Trex Landscape Lighting line includes an energy-efficient well light, path light, multifunction light and spotlight.

1

Table of Contents

We are a licensor in a number of licensing agreements with third parties to manufacture and sell products under the Trex trademark. Our licensed products are:

| • | Trex Outdoor Furniture™, which is a line of outdoor furniture products manufactured and sold by Poly-Wood, Inc.; |

| • | Trex RainEscape®, which is an above joist deck drainage system manufactured and sold by Dri-Deck Enterprises, LLC; |

| • | Trex CustomCurve®, which is an on-site system that allows contractors to heat and bend Trex products manufactured and sold by CurveIt, LLC; |

| • | Trex Pergolas, which are pergolas made from TrexTrim™, our low maintenance cellular PVC trim product, marketed by Home and Leisure, Inc. dba Backyard America; |

| • | Diablo® Trex Blade, which is a specialty saw blade for wood-plastic composite decking manufactured and sold by Freud America, Inc.; |

| • | Trex SpiralStairs™ and Structural Steel Posts (for use with the Elevations system), manufactured and sold by M. Cohen and Sons, Inc. dba The Iron Shop; and |

| • | Trex Outdoor Cabinets, which are outdoor storage cabinets manufactured and sold by NatureKast Products LLC. |

Trex products offer a number of significant aesthetic advantages over wood while eliminating many of wood’s major functional disadvantages, which include warping, splitting and other damage from moisture. Our products require no staining, are resistant to moisture damage, provide a splinter-free surface and need no chemical treatment against rot or insect infestation. These features eliminate most of the on-going maintenance requirements for a wood deck and make Trex products less costly than wood over the life of the deck. Like wood, Trex products are slip-resistant (even when wet) but are less vulnerable to damage from ultraviolet rays. Special characteristics (including resistance to splitting, the ability to bend, and ease and consistency of machining and finishing) facilitate deck, railing, fencing and trim installation, reduce contractor call-backs and afford customers a wide range of design options. Trex decking products do not have the tensile strength of wood and, as a result, are not used as primary structural members in posts, beams or columns used in a deck’s substructure. However, Trex does offer the Trex Elevations steel deck framing system.

We have received product building code listings from the major U.S. and Canadian building code listing agencies for both our decking and railing systems. Our listings facilitate the acquisition of building permits by deck builders and promote consumer and industry acceptance of our products as an alternative to wood in decking. In addition, Trex Seclusions privacy fencing has passed the Miami/Dade County wind load testing, a widely regarded standard for assessing a fencing product’s performance under extreme environmental conditions.

During the second half of 2014, we began manufacturing and selling polyethylene pellets made from recycled plastic into the plastic bag, film and sheet markets and other commercial business applications. Our entry into this adjacent industry enables us to leverage our core recycling and extrusion capabilities, adding significant value to our polyethylene sales. As of December 31, 2014, one polyethylene pellet manufacturing line was operational, and an additional three lines are expected to be built during the first half of 2015.

Growth Strategies

Our long-term goal is to perpetuate our position as the leading producer of branded superior wood-alternative outdoor living products by increasing our market share and expanding into new product categories and geographic markets. To attain this goal, we intend to employ the following long-term strategies:

| • | Innovation: Bring to the market new products that address unmet consumer and trade professional needs. Provide a compelling value proposition through ease of installation, low maintenance, long-term durability and superior aesthetics. |

2

Table of Contents

| • | Brand: Expand preference and commitment for the Trex brand with both the consumer and trade professional. Deliver on the brand’s promise of superior quality, functionality, aesthetics and overall performance in the outdoor living space. Leverage online efforts to build a bigger Trex brand presence digitally, extending our footprint nationally and globally. |

| • | Channels: Achieve comprehensive market segment and geographic coverage for Trex products by increasing the number of stocking dealers and retailers and expanding our international presence, thereby making our products available wherever our customers choose to purchase their decking, railing, porch, trim, steel deck framing and outdoor lighting products. |

| • | Quality: Continuously advance the quality of all operational and business processes, with the goal of achieving superior product quality and service levels, thereby giving us a sustainable competitive advantage. |

| • | Cost: Through capital investments and process engineering, continuously seek to lower the cost to manufacture Trex products. Investments in plastic recycling capabilities will allow us to add significant value to our polyethylene sales and expand our ability to use a wider breadth of waste streams thereby lowering our raw material costs. We plan to concentrate on improving the productivity of our production process, from raw materials preparation through extrusion into finishing and packaging. |

Customers and Distribution

We distribute our products as follows:

Wholesale Distributors/Retail Lumber Dealers. We generate most of our sales through our wholesale distribution network by selling Trex products to wholesale distributors, who in turn, sell our products to retail lumber outlets. These retail dealers market to both homeowners and contractors, but they emphasize sales to professional contractors, remodelers and homebuilders. Contractor-installed decks generally are larger installations with professional craftsmanship. Our retail dealers generally provide sales personnel trained in Trex products, contractor training, inventory commitment and point-of-sale display support.

We believe that attracting wholesale distributors, who are committed to our products and marketing approach and can effectively sell higher value products to contractor-oriented lumber yards and other retail outlets, is important to our future growth. Our distributors are able to provide value-added service in marketing our products because they sell premium wood decking products and other innovative building materials that typically require product training and personal selling efforts. We typically appoint two distributors on a non-exclusive basis to distribute Trex products within a specified area. The distributor generally purchases our products at prices in effect at the time we ship the product to the distributor. Based on our 2014 net sales, sales to one of our distributors, Boise Cascade, exceeded 10% of our net sales.

Home Depot and Lowe’s. We sell our products through Home Depot and Lowe’s stores. Home Depot and Lowe’s purchase products directly from us for stocking on their shelves. They also purchase product through our wholesale distributors for special orders placed by consumers. Although Home Depot and Lowe’s serve the contractor market, the largest part of their sales are to “do-it-yourself” homeowner customers that shop for their materials at Home Depot and Lowe’s stores rather than at retail lumber dealers. We believe that brand exposure through Home Depot and Lowe’s distribution promotes consumer acceptance of our products.

Manufacturing Process

We operate manufacturing facilities located in Winchester, Virginia and Fernley, Nevada.

Trex products are primarily manufactured from waste wood fiber and scrap polyethylene. Our primary manufacturing process involves mixing wood particles with plastic, heating and finally extruding, or forcing, the highly viscous and abrasive material through a profile die. We have many proprietary and skill-based advantages in this process.

3

Table of Contents

Production of a wood-alternative decking such as ours requires significant capital investment, special process expertise and time to develop. We have continuously invested the capital necessary to expand our manufacturing throughput and improve our manufacturing processes. We have also broadened the range of raw materials that we can use to produce a consistent and high-quality finished product. We maintain research and development operations in the Trex Technical Center adjacent to our Winchester, Virginia manufacturing facilities. In connection with our building code listings, we maintain a quality control testing program that is monitored by an independent inspection agency.

We utilize Six Sigma practices and Standard Lean Manufacturing methodology within our plant operations. We also incorporate the use of these tools throughout our Company in the planning and execution of those projects that are the most important to our success.

Research and Development

Our research and development efforts focus on innovation and developing new products, lowering the cost of manufacturing our existing products and redesigning existing product lines to increase efficiency and enhance performance. For the years ended December 31, 2014, 2013 and 2012, research and development costs were $2.3 million, $2.9 million and $2.9 million, respectively, and have been included in “Selling, general and administrative expenses” in the accompanying consolidated statements of comprehensive income.

Suppliers

The production of most of our products requires the supply of waste wood fiber and scrap polyethylene.

We fulfill requirements for raw materials under both purchase orders and supply contracts. In the year ended December 31, 2014, we purchased substantially all of our waste wood fiber requirements under purchase orders, which do not involve long-term supply commitments. Substantially all of our polyethylene purchases are under short-term supply contracts that average approximately two years for which pricing is negotiated as needed.

Waste Wood Fiber. Woodworking plants or mills are our preferred suppliers of waste wood fiber because the waste wood fiber produced by these operations contains little contamination and is low in moisture. These facilities generate waste wood fiber as a byproduct of their manufacturing operations.

If the waste wood fiber meets our specifications, our waste wood fiber supply agreements generally require us to purchase at least a specified minimum and at most a specified maximum amount of waste wood fiber each year. Depending on our needs, the amount of waste wood fiber that we actually purchase within the specified range under any supply agreement may vary significantly from year to year.

Scrap Polyethylene. The polyethylene we consumed in 2014 was primarily composed of scrap plastic film and plastic bags. Approximately two billion pounds of polyethylene resin are used in the manufacture of stretch film and plastic bags in the United States each year. We will continue to seek to meet our future needs for scrap polyethylene from the expansion of our existing supply sources and the development of new sources. We believe our use of multiple sources provides us with a cost advantage and facilitates an environmentally responsible approach to our procurement of polyethylene.

Our ability to source and use a wide variety of polyethylene is important to our cost strategy. We maintain this ability through the continued expansion of our plastic reprocessing operations in combination with the advancement of our proprietary material preparation and extrusion processes.

Third-Party Manufacturing. We outsource the production of certain products to third-party manufacturers under supply contracts that commit us to purchase minimum levels for each year extending through 2015. We have purchase commitments under the third-party manufacturing contracts of $1.9 million for the year ending December 31, 2015.

4

Table of Contents

Competition

Our primary competition consists of wood products, which constitutes a substantial majority of decking and railing sales, as measured by linear feet of lumber. Many of the conventional lumber suppliers with which we compete have established ties to the building and construction industry and have well-accepted products. A majority of the lumber used in wood decks is pressure-treated lumber. Southern yellow pine and fir have a porosity that readily allows the chemicals used in the pressure treating process to be absorbed. The same porosity makes southern yellow pine susceptible to absorbing moisture, which causes the lumber to warp, crack, splinter and expel fasteners. In addition to pine and fir, other segments of wood material for decking include redwood, cedar and tropical hardwoods, such as ipe, teak and mahogany. These products are often significantly more expensive than pressure-treated lumber, but do not eliminate many of the disadvantages of other wood products.

In addition to wood, we also compete with other manufacturers of wood-alternative products. Industry studies indicate that we have the leading market share of the wood-alternative segment of the decking and railing market. Our principal competitors include Advanced Environmental Recycling Technologies, Inc., CPG International and Fiber Composites, LLC.

Our ability to compete depends, in part, on a number of factors outside our control, including the ability of our competitors to develop new wood-alternative decking and railing products that are competitive with our products. We believe that the principal competitive factors in the decking and railing market include product quality, price, aesthetics, maintenance cost, distribution and brand strength. We believe we compete favorably with respect to these factors. We believe that our products offer aesthetic and cost advantages over the life of a deck when compared to other types of decking and railing materials. Although a contractor-installed deck built with Trex products using a pressure-treated wood substructure generally costs more than a deck made entirely from pressure-treated wood, Trex products eliminate many of the on-going maintenance required for a pressure-treated deck and are, therefore, less costly over the life of the deck. We believe that our manufacturing process and utilization of relatively low-cost raw material sources provide us with a competitive cost advantage relative to other manufacturers of wood-alternative decking and railing products. The scale of our operations also confers cost efficiencies in manufacturing, sales and marketing.

Seasonality

Our net sales, gross profit and income from operations have historically varied from quarter to quarter. Such variations are often attributable to seasonal trends in the demand for our products. We have historically experienced lower net sales during the fourth quarter because holidays and adverse weather conditions in certain regions reduce the level of home improvement and construction activity.

Government Regulation

We are subject to federal, state and local environmental regulation. The emissions of particulates and other substances from our manufacturing facilities must meet federal and state air quality standards implemented through air permits issued to us by the Department of Environmental Quality of the Commonwealth of Virginia, the Division of Environmental Protection of Nevada’s Department of Conservation and Natural Resources and the Mississippi Department of Environmental Quality. Our facilities are regulated by federal and state laws governing the disposal of solid waste and by state and local permits and requirements with respect to wastewater and storm water discharge. Compliance with environmental laws and regulations has not had a material adverse effect on our business, operating results or financial condition.

Our operations also are subject to work place safety regulation by the U.S. Occupational Safety and Health Administration, the Commonwealth of Virginia, the State of Nevada and the State of Mississippi. Our compliance efforts include safety awareness and training programs for our production and maintenance employees.

5

Table of Contents

Intellectual Property

Our success depends, in part, upon our intellectual property rights relating to our products, production processes and other operations. We rely upon a combination of trade secret, nondisclosure and other contractual arrangements, and patent, copyright and trademark laws, to protect our proprietary rights. We have made substantial investments in manufacturing process improvements that have enabled us to increase manufacturing line production rates, facilitate our development of new products, and produce improvements in our existing products’ dimensional consistency, surface texture and color uniformity.

Intellectual property rights may be challenged by third parties and may not exclude competitors from using the same or similar technologies, brands or works. We seek to secure effective rights for our intellectual property, but cannot provide assurance that third parties will not successfully challenge, or avoid infringing, our intellectual property rights.

We have obtained two patents for complementary methods of preparing the raw materials for the manufacturing phase of production, one patent on an apparatus for implementing one of the methods, and one patent on a tool for use with the installation of the decking board. We intend to maintain our existing patents in effect until they expire, beginning in 2015, as well as to seek additional patents as we consider appropriate.

We consider our trademarks to be of material importance to our business plans. The U.S. Patent and Trademark Office has granted us federal registrations for many of our trademarks. Federal registration of trademarks is effective for as long as we continue to use the trademarks and renew their registrations. We do not generally register any of our copyrights with the U.S. Copyright Office, but rely on the protection afforded to such copyrights by the U.S. Copyright Act. This law provides protection to authors of original works, whether published or unpublished, and whether registered or unregistered. We enter into confidentiality agreements with our employees and limit access to and distribution of our proprietary information. If it is necessary to disclose proprietary information to third parties for business reasons, we require that such third parties sign a confidentiality agreement prior to any disclosure.

Employees

At December 31, 2014, we had approximately 630 full-time employees, approximately 470 of whom were employed in our manufacturing operations. Our employees are not covered by collective bargaining agreements. We believe that our relationships with our employees are favorable.

Web Sites and Additional Information

The SEC maintains an Internet web site at www.sec.gov that contains reports, proxy statements, and other information regarding our Company. In addition, we maintain an Internet corporate web site at www.trex.com. We make available through our web site our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports, as soon as reasonably practicable after we electronically file or furnish such material with or to the SEC. We do not charge any fees to view, print or access these reports on our web site. The contents of our web site are not a part of this report.

6

Table of Contents

Executive Officers and Directors

The table below sets forth information concerning our executive officers and directors as of February 16, 2015.

| Name |

Age | Positions with Company | ||

| Ronald W. Kaplan |

63 | Chairman, President and Chief Executive Officer; Director | ||

| James E. Cline |

63 | Senior Vice President and Chief Financial Officer | ||

| William R. Gupp |

55 | Senior Vice President, General Counsel and Secretary | ||

| F. Timothy Reese |

62 | Senior Vice President, Operations | ||

| Christopher P. Gerhard |

42 | Vice President, Sales | ||

| Adam D. Zambanini |

38 | Vice President, Marketing | ||

| Michael F. Golden |

60 | Director | ||

| Jay M. Gratz |

62 | Director | ||

| Frank H. Merlotti, Jr. |

64 | Director, Lead Independent Director | ||

| Richard E. Posey |

68 | Director | ||

| Patricia B. Robinson |

62 | Director | ||

| Gerald Volas |

60 | Director |

Ronald W. Kaplan has served as Chairman, President and Chief Executive Officer of the Company since May 2010. From January 2008 to May 2010, Mr. Kaplan served as a director and President and Chief Executive Officer of the Company. From February 2006 through December 2007, Mr. Kaplan served as Chief Executive Officer of Continental Global Group, Inc., a manufacturer of bulk material handling systems. For 26 years prior to this, Mr. Kaplan was employed by Harsco Corporation, an international industrial services and products company, at which he served in a number of capacities, including as Senior Vice President-Operations, and, from 1994 through 2005, as President of Harsco’s Gas Technologies Group, which manufactures containment and control equipment for the global gas industry. Mr. Kaplan received a B.A. degree in economics from Alfred University and a M.B.A. degree from the Wharton School of Business, University of Pennsylvania.

James E. Cline has served as Senior Vice President and Chief Financial Officer of the Company since August 2013 and as Vice President and Chief Financial Officer between March 2008 and July 2013. Mr. Cline served from July 2005 through December 2007 as the President of Harsco GasServ, a subsidiary of Harsco Corporation and a manufacturer of containment and control equipment for the global gas industry. From January 2008 through February 2008, in connection with the purchase of Harsco GasServ by Taylor-Wharton International LLC, which is owned by Windpoint Partners Company, Mr. Cline served as a consultant to the buyers by providing transition management and financial services. From April 1994 through June 2005, Mr. Cline served as the Vice President and Controller of Harsco GasServ. Mr. Cline served in various capacities with Huffy Corporation from June 1976 to February 1994, including as the Director of Finance of its True Temper Hardware subsidiary, a manufacturer of lawn care and construction products with nine manufacturing locations in the United States, Canada and Ireland. Mr. Cline received a B.S.B.A. degree in accounting from Bowling Green State University.

William R. Gupp has served as Senior Vice President, General Counsel and Secretary of the Company since August 2014. From October 2009 to August 2014, Mr. Gupp served as Chief Administrative Officer, General Counsel and Secretary, and from May 2001 to October 2009, Mr. Gupp served as Vice President and General Counsel. From March 1993 to May 2001, Mr. Gupp was employed by Harsco Corporation, an international industrial services and products company, most recently as Senior Counsel and Director-Corporate Development. From August 1985 to March 1993, Mr. Gupp was employed by the law firm of Harter, Secrest & Emery. Mr. Gupp received a B.S. degree in accounting from Syracuse University and a J.D. from the University of Pennsylvania Law School.

F. Timothy Reese has served as Senior Vice President, Operations of the Company since August 2013 and as Vice President, Operations between February 2008 and July 2013. From March 2007 through January 2008,

7

Table of Contents

Mr. Reese served as Operations Director for the Americas Region of DuPont Teijin Films, a DuPont Teijin Films U.S. Limited Partnership and producer of polyester films. From 1979 to March 2007, Mr. Reese served in various positions with DuPont, including Global Director, Business and Integrated Operations, DuPont High Performance Films, from November 1995 through November 1998; Director/Plant Manager, Global Operations, Cyrel® Packaging Graphics Products, from December 1998 through May 2000; Director, Global Operations and Six Sigma Champion, Cyrel® Packaging Graphics Products, from June 2000 through February 2001; and Director/Plant Manager in multiple assignments from March 2001 through February 2007, including in Corporate Operations, Human Resources and DuPont Chemical Solutions Enterprise. Mr. Reese served in the U.S. Navy and received a B.S. in ocean engineering with an emphasis on mechanical engineering from the U.S. Naval Academy.

Christopher P. Gerhard has served as Vice President, Sales of the Company since June 2012. From May 2006 through June 2012, Mr. Gerhard served in a number of capacities at the Company, most recently as Director, Field Sales. From 2002 to May 2006, Mr. Gerhard served in various capacities with Kraft Foods North America, a manufacturer of food and beverages, most recently as Southeast Region Customer Category Manager. Mr. Gerhard received a B.A. in English from the University of North Carolina—Greensboro, and a Masters in Science from Ohio University.

Adam D. Zambanini has served as Vice President, Marketing of the Company since January 2011. From September 2005 through December 2010, Mr. Zambanini served in a number of capacities at the Company, most recently as Director, Marketing. From January 2000 through September 2005, Mr. Zambanini was employed by Rubbermaid Commercial Products, most recently as Product Manager. Mr. Zambanini received a B.S. in mechanical engineering from Penn State University, and a M.B.A. degree from Averett University.

Michael F. Golden has served as a director of the Company since February 2013. Mr. Golden is retired. Mr. Golden served as President and Chief Executive Officer of Smith and Wesson Holding Corporation, a manufacturer of firearms and firearms-related products and accessories, from December 2004 until his retirement in September 2011, and currently serves as a director of such company. Mr. Golden was employed in various executive positions with the Kohler Company, which manufactures kitchen and bath plumbing fixtures, furniture, tile, engines, and generators, and operates resorts, from February 2002 until December 2004, with his most recent position being the President of its Cabinetry Division. Mr. Golden was the President of Sales for the Industrial/Construction Group of the Stanley Works Company, which manufactures tools and hardware, from 1999 until 2002; Vice President of Sales for Kohler’s North American Plumbing Group from 1996 until 1998; and Vice President, Sales and Marketing for a division of The Black & Decker Corporation, which manufactures tools and hardware, where he was employed from 1981 until 1996. Mr. Golden also serves on the Board of Directors of Quest Resources Holding Company. Mr. Golden received a B.S. degree in Marketing from Pennsylvania State University and a M.B.A. degree from Emory University.

Jay M. Gratz has served as a director of the Company since February 2007. Mr. Gratz has served as the Chief Financial Officer of VisTracks, Inc., an application enabling platform service provider, since March 2010, and a director of such company since April 2010. Mr. Gratz was a partner in Tatum LLC, a national executive services and consulting firm that focuses on the needs of the Office of the CFO between February 2010 and March 2010. From October 2007 through February 2010, Mr. Gratz was an independent consultant. From 1999 through October 2007, Mr. Gratz served as Executive Vice President and Chief Financial Officer of Ryerson Inc., a metals processor and distributor, and as President of Ryerson Coil Processing Division from November 2001 until October 2007. Mr. Gratz served as Vice President and Chief Financial Officer of Inland Steel Industries, a steel company, from 1994 through 1998, and served in various other positions, including Vice President of Finance, within that company since 1975. Mr. Gratz is a Certified Public Accountant. He received a B.A. degree in economics from State University of New York in Buffalo and a M.B.A. degree from Northwestern University Kellogg Graduate School of Management.

Frank H. Merlotti, Jr. has served as a director of the Company since February 2006 and as Lead Independent Director since April 2014. Mr. Merlotti is retired. Mr. Merlotti served as President of the Coalesse

8

Table of Contents

business unit of Steelcase, Inc., a manufacturer of office furniture and furniture systems, from October 2006 until his retirement in September 2013, and as President of Steelcase North America from September 2002 through September 2006. Mr. Merlotti served as President and Chief Executive Officer of G&T Industries, a manufacturer and distributor of fabricated foam and soft-surface materials for the marine, office furniture and commercial building industries, from August 1999 to September 2002. From 1991 through 1999, Mr. Merlotti served as President and Chief Executive Officer of Metropolitan Furniture Company, a Steelcase Design Partnership company. From 1985 through 1999, Mr. Merlotti served as General Manager of the Business Furniture Division of G&T Industries.

Richard E. Posey has served as a director of the company since May 2009. Mr. Posey is retired. He served as President and Chief Executive Officer of Moen Incorporated, a manufacturer of faucets, from January 2002 until his retirement in September 2007. Prior to joining Moen, Mr. Posey was President and Chief Executive Officer of Hamilton Beach / Proctor Silex, Inc., a manufacturer of small kitchen appliances, for five years. Mr. Posey began his career at S.C. Johnson & Son, a supplier of cleaning and other household products, where for 22 years he served in a series of increasingly responsible management positions, both overseas and in the U.S., culminating with Executive Vice President, Consumer Products, North America. Mr. Posey is a Founding Trustee, Virginia Commonwealth University School of Engineering Foundation. He received a B.A. degree in English from The University of Southern California and a M.B.A. degree from The University of Michigan.

Patricia B. Robinson has served as a director of the Company since November 2000. Ms. Robinson has been an independent consultant since 1999. From 1977 to 1998, Ms. Robinson served in a variety of positions with Mead Corporation, a forest products company, including President of Mead School and Office Products, Vice President of Corporate Strategy and Planning, President of Gilbert Paper, Plant Manager of a specialty machinery facility and Product Manager for new packaging product introductions. Ms. Robinson received a B.A. degree in economics from Duke University and a M.B.A. degree from the Darden School at the University of Virginia.

Gerald Volas has served as a director of the Company since March 2014. Mr. Volas has been employed by Masco Corporation, one of the world’s leading manufacturers of brand-name products for the home improvement and new home construction industries, in various positions of increasing responsibility since 1982. Since February 2005, he has served as a Group Executive responsible for almost all of Masco’s operating companies at one time or another. He currently is responsible for a number of Masco operating companies accounting for approximately 50% of Masco’s revenues in 2012. From April 2001 to February 2005, he served as President of Liberty Hardware, a Masco operating company, from January 1996 to April 2001, he served as a Group Controller supporting a variety of Masco operating companies, and from May 1982 to January 1996, he served in progressive financial roles including Vice President/Controller at BrassCraft Manufacturing Company, a Masco operating company. Mr. Volas is a Certified Public Accountant. He received a Bachelor of Business Administration degree from the University of Michigan.

| Item 1A. | Risk Factors |

Our business is subject to a number of risks, including the following:

We may not be able to grow unless we increase market acceptance of our products, compete effectively and develop new products and applications.

Our primary competition consists of wood products, which constitute a substantial majority of decking, railing, porches, fencing, trim and deck framing sales. Since wood-alternative products were introduced to the market in the early 1990’s, their market acceptance has increased, but during the past few years, the rate of conversion from purchasing wood products to purchasing wood-alternative products slowed. Our ability to grow will depend, in part, on our success in continuing to convert demand for wood products into a demand for wood-alternative Trex products. To increase our market share, we must overcome:

| • | the consumer lack of awareness of the enhanced value of wood-alternative decking, railing, porches, fencing, trim and deck framing products in general and Trex brand products in particular; |

9

Table of Contents

| • | the resistance of many consumers and contractors to change from well-established wood products; |

| • | the consumer lack of awareness that the greater initial expense of Trex products compared to wood is a one-time cost that is reduced over time as Trex products have a longer life span than wood; |

| • | the established relationships existing between suppliers of wood products and contractors and homebuilders; |

| • | actual and perceived quality issues with first generation wood-alternative products; and |

| • | the competition from other wood-alternative manufacturers. |

We must also compete with a number of companies in the wood-alternative segment of the decking, railing, fencing and trim markets and with wood producers that currently have more production capacity than is required to meet the demand for such products. Our failure to compete successfully in such markets could have a material adverse effect on our ability to replace wood or increase the market share of wood-alternatives compared to wood. Many of the conventional lumber suppliers with which we compete have established ties to the building and construction industry and have well-accepted products. Our ability to compete depends, in part, upon a number of factors outside our control, including the ability of competitors to develop new non-wood alternatives that are more competitive with Trex products.

In addition to the above, substantially all of our revenues are derived from sales of our proprietary wood/plastic composite material. Although we have developed, and continue to develop, new products made from other materials, if we should experience significant problems, real or perceived, with product quality or acceptance of the Trex wood/polyethylene composite material, our lack of product diversification could have a significant adverse impact on our net sales levels.

Our prospects for sales growth and profitability may be adversely affected if we fail to maintain product quality and product performance at an acceptable cost.

We will be able to expand our net sales and to sustain and enhance profitable operations only if we succeed in maintaining the quality and performance of our products. If we should not be able to produce high-quality products at standard manufacturing rates and yields, unit costs may be higher. A lack of product performance would negatively affect our profitability by impeding acceptance of our products in the marketplace and by leading to higher product replacement and consumer relations expenses. In recent periods, we have experienced significant warranty expenses related to material produced at our Nevada facility prior to 2007 that exhibits surface flaking. We have limited our financial exposure by agreeing to settle a nationwide class action lawsuit which fixes our obligation in each claim to provide replacement product and provide a partial labor reimbursement. However, because the establishment of reserves is an inherently uncertain process involving estimates of the number of future claims and the average cost of claims, our ultimate losses may differ from our warranty reserve. Increases we have made to the warranty reserve and payments for related claims in recent years have had a material adverse effect on our profitability and cash flows. Future increases to the warranty reserve could have a material adverse effect on our profitability and cash flows should we make such increases and pay such claims.

In addition, our products are used outdoors and are sometimes subject to heavy use and harsh exposure to the environment. Although our Limited Warranty excludes any conditions attributable to “any act of God (such as flooding, hurricane, earthquake, lightning, etc., ), environmental condition (such as air pollution, mold, mildew, etc.), staining from foreign substances (such as dirt, grease, oil, etc.), or normal weathering (defined as exposure to sunlight, weather and atmosphere which may cause any colored surface to gradually fade, chalk, or accumulate dirt or stains”), to the extent that our products are affected in any way, this may lead to an increased risk of product liability claims or litigation.

A number of class action lawsuits based upon mold growth, color fading and color variation on our products have been brought against us, all of which have been settled. (See Part I, Item 3, Legal Proceedings, for a

10

Table of Contents

discussion of these lawsuits.) In the event future lawsuits are brought against us relating to alleged product quality issues, such lawsuits are a potential financial exposure to us and could cause adverse publicity, which in turn could result in a loss of consumer confidence in our products and also reduce our sales. Product quality claims could increase our expenses and have a material adverse effect on demand for our products and, consequently, reduce our net sales, net income and liquidity.

Our business is subject to risks in obtaining the raw materials we use at acceptable prices.

The production of our product requires substantial amounts of wood fiber and polyethylene. Our business strategy is to create a substantial cost advantage over our competitors by using waste wood fibers and scrap polyethylene. Our business could suffer from the termination of significant sources of raw materials, the payment of higher prices for raw materials or from the failure to obtain sufficient additional raw materials to meet planned increases in production. Our ability to obtain adequate supplies of scrap polyethylene depends on our success in developing new sources that meet our quality requirements, maintaining favorable relationships with suppliers and managing the collection of supplies from geographically dispersed locations.

We sell to certain customers that account for a significant portion of our sales, and the loss of one or more of these customers could have an adverse effect on our business.

A limited number of customers account for a significant percentage of our sales. Specifically, sales through our 15 largest customers each year accounted for approximately 86% of gross sales during fiscal year 2014, 89% during fiscal year 2013 and 90% during fiscal year 2012.

We expect that a significant portion of our sales will continue to be sold through a small number of customers, and certain customers will continue to account for a significant portion of our sales. The loss of a significant customer could have a negative impact on our business, financial condition and results of operations.

We have limited ability to control or project inventory build-ups in our distribution channel that can negatively affect our sales in subsequent periods.

The dynamic nature of our industry can result in substantial fluctuations in inventory levels of Trex products carried in our two-step distribution channel. We have limited ability to control or precisely project inventory build-ups, which can adversely affect our net sales levels in subsequent periods. We make the substantial majority of our sales to wholesale distributors, who, in turn, sell our products to local lumber yards. Because of the seasonal nature of the demand for decking, railing, deck framing, fencing and trim, our distribution channel partners must forecast demand for our products, place orders for the products, and maintain Trex product inventories in advance of the prime deck-building season, which generally occurs in our late first through third fiscal quarters. Accordingly, our results for the second and third fiscal quarters are difficult to predict and past performance will not necessarily indicate future performance. Inventory levels respond to a number of changing conditions in our industry, including product price increases resulting from escalating raw materials costs, increases in the number of competitive producers and in the production capacity of those competitors, the rapid pace of product introduction and innovation, changes in the levels of home-building and remodeling expenditures, and the cost and availability of credit.

The demand for our products is affected by adverse weather conditions.

Our products are generally purchased shortly before installation and used in outdoor environments. As a result, there is a correlation between the amount of product we sell and the weather conditions around the time they are to be installed. Weather conditions, such as very high or low temperatures, intense and prolonged precipitation, hurricanes, floods, and regional fires in the regions we sell our products interfere with ordinary construction, delay projects and can even lead to cessation of certain construction involving our products.

11

Table of Contents

Since weather conditions and seasonal cycles cannot be accurately predicted, adverse weather conditions may shift our sales to subsequent reporting periods, or may also reduce overall sales given the limited decking season in many locations. Prolonged adverse weather conditions could have a negative impact on our financial statements.

We depend on third parties for transportation services and the lack of availability of transportation and/or increases in cost could materially adversely affect our business and operations.

Our business depends on the transportation of both finished goods to our distributors and the transportation of raw materials to us. We rely on third parties for transportation of these items. In particular, a significant portion of our finished goods are transported by flatbed trucks, which are occasionally in high demand (especially at the end of calendar quarters) and/or subject to price fluctuations based on market conditions and the price of fuel.

If the required supply of transportation services is unavailable when needed, we may be unable to sell our products at full value, or at all. Similarly, if any of these providers were unavailable to deliver raw materials to us in a timely manner, we may be unable to manufacture our products in response to customer demand. This could harm our reputation, negatively impact our customer relationships and have a material adverse effect on our financial condition and results of operation. In addition, a material increase in transportation rates or fuel surcharges could materially adversely affect our profitability.

The demand for our products is influenced by general economic conditions and could be adversely affected by economic downturns.

The demand for our products is correlated to changes in the health of the economy in general, and the level of activity in home improvements and, to a much lesser extent, new home construction. These levels of activity, in turn, are affected by such factors as home equity values, credit availability, consumer confidence and spending habits, employment, interest rates, inflation and general economic conditions. Market conditions in the housing industry slowed significantly in recent years, particularly in new home construction. Home equity values in many markets that decreased significantly during those time periods have only begun to recover. This devaluation in home equity values has adversely affected the availability of home equity withdrawals, which have resulted in decreased home improvement spending. We cannot predict when the economy, the home remodeling and new home construction environments will fully recover or if the current recovery will continue. Any continued economic downturn could reduce consumer income or equity capital available for spending on discretionary items such as decking, railing, porches, fencing and trim, which could adversely affect the demand for our products.

We have significant capital invested in property, plant and equipment that may become obsolete or impaired and result in a charge to our earnings.

At December 31, 2014, we had $98.7 million of net property, plant and equipment, $6.8 million of which relates to assets located at our Olive Branch, Mississippi manufacturing facility that was shut down in September 2007. In addition, each year we make significant capital investments to improve or expand our manufacturing capabilities. These improvements sometimes involve the implementation of new technology and replacement of existing equipment at our manufacturing facilities, which may result in charges to our earnings if the existing equipment is not fully depreciated. Significant replacement of equipment or changes in the expected cash flows related to our assets could result in reduced earnings in future periods.

Our level of indebtedness, and ability to continue to obtain financing on favorable terms, could adversely affect our financial health and ability to compete.

As of December 31, 2014, we had no outstanding indebtedness. At certain periods during the year, we borrowed significant amounts on our senior secured credit facility for working capital purposes, and it is

12

Table of Contents

foreseeable that we will need to borrow on the facility in 2015 for similar purposes. In addition, we may borrow money in the event we elect to pursue an acquisition or other transactions. Accordingly, our future level of indebtedness could have important consequences. For example, it may:

| • | increase our vulnerability to general adverse economic and industry conditions, including interest rate fluctuations; |

| • | require us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures and other general corporate purposes; |

| • | limit our ability to borrow additional funds to alleviate liquidity constraints, as a result of financial and other restrictive covenants in our indebtedness; |

| • | limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

| • | place us at a competitive disadvantage relative to companies that have less indebtedness; and |

| • | limit our ability to refinance our principal secured indebtedness. |

In addition, our senior secured credit facility imposes operating and financial restrictions that may limit our discretion on some business matters, which could make it more difficult for us to expand, finance our operations and engage in other business activities that may be in our interest. These restrictions may limit our ability to:

| • | incur additional indebtedness and additional liens on our assets; |

| • | engage in mergers or acquisitions or dispose of assets; |

| • | enter into sale-leaseback transactions; |

| • | pay dividends or make other distributions; |

| • | voluntarily prepay other indebtedness; |

| • | enter into transactions with affiliated persons; |

| • | make investments; and |

| • | change the nature of our business. |

We may incur indebtedness in addition to our current indebtedness. Any additional indebtedness we may incur in the future could subject us to similar or even more restrictive conditions.

Our ability to make future principal and interest payments, borrow and repay amounts under our revolving credit facility and continue to comply with our loan covenants will depend primarily on our ability to generate sufficient cash flow from operations. Our failure to comply with our loan covenants might cause our lenders to accelerate our repayment obligations under our credit facility, which may be declared payable immediately based on a default. To remain in compliance with our credit facility, we must maintain specified financial ratios based on our levels of debt, fixed charges, and earnings (excluding extraordinary gains and extraordinary non-cash losses) before interest, taxes, depreciation and amortization, all of which are subject to the risks of our business.

| Item 1B. | Unresolved Staff Comments |

None.

| Item 2. | Properties |

We lease our corporate headquarters in Winchester, Virginia, which consists of approximately 32,000 square feet of office space, under a lease that expires in March 2020. In 2005, in anticipation of relocating our

13

Table of Contents

corporate headquarters, we entered into an agreement to lease 55,047 square feet of office space in Dulles, Virginia. The lease expires in mid-2019. Subsequently, we reconsidered our decision to relocate our corporate headquarters and decided not to move. We have executed subleases for 24,732 square feet of the leased space and are currently marketing the remaining portion of the space to find a suitable tenant. For a description of our financial reporting in connection with the Dulles lease agreement, see Note 12 to our consolidated financial statements appearing elsewhere in this report.

We own approximately 66 contiguous acres of land in Winchester, Virginia and the buildings on this land. The site includes our research and development technical facility and manufacturing facilities, which contain approximately 465,000 square feet of space. We own approximately 37 acres of land in Fernley, Nevada and the buildings on this land. The site includes our manufacturing facility, which contains approximately 240,000 square feet of space, and outside open storage. We own approximately 102 acres of land in Olive Branch, Mississippi and the buildings on this land. The site contains four buildings with approximately 200,000 square feet for manufacturing and raw material handling operations. In September 2007, we suspended operations at our Olive Branch facility and consolidated all of our manufacturing operations into our Winchester and Fernley sites. Our facilities provide adequate capacity for current and anticipated future consumer demand.

We lease a total of approximately one million square feet of warehouse space under leases with expiration dates ranging from 2015 to 2025. For information about these leases, see Note 9 to our consolidated financial statements appearing elsewhere in this report.

The equipment and machinery we use in our operations consist principally of plastic and wood conveying and processing equipment. We own all of our manufacturing equipment. We lease forklift equipment at our facilities under operating leases.

We regularly evaluate our various facilities and equipment and make capital investments where necessary. In 2014, we spent a total of $13.0 million on capital expenditures, primarily related to new poly processing lines and upgrades to our existing production lines to support the manufacture of our high-performance products. We estimate that our capital expenditures in 2015 will be in approximately $20 million. We expect to use these expenditures principally to support cost reduction initiatives, new product launches in current and adjacent categories and general business support.

| Item 3. | Legal Proceedings |

On December 16, 2013, the United States District Court, Northern District of California Court granted final approval of the settlement with the law firm of Hagens Berman Sobol Shapiro LLP, relating to the previously reported class action lawsuit brought on behalf of Dean Mahan, and other named and similarly situated plaintiffs generally which alleged certain defects in the Company’s products relating to mold growth, color fading and color variation. As of the date of this report, the Company has distributed all cash payments and rebate certificates under the settlement. Claimants who were denied relief could appeal Trex’s decision, and the deadline for appeals has now passed. The Company believes that payments to consumers for all relief under the settlement will not exceed approximately $1.0 million. In addition to such amount, the Company previously paid $1.8 million related to this litigation, representing payment of attorneys’ fees to class counsel and named plaintiff awards in the nationwide settlement and the settlement of corollary cases brought in Indiana, Kentucky, New Jersey and Michigan, all as previously disclosed.

The Company has other lawsuits, as well as other claims, pending against it which are ordinary routine litigation and claims incidental to the business. Management has evaluated the merits of these other lawsuits and claims, and believes that their ultimate resolution will not have a material effect on the Company’s consolidated financial condition, results of operations, liquidity or competitive position.

| Item 4. | Mine Safety Disclosures |

Not applicable.

14

Table of Contents

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Market for Common Stock

Our common stock has been listed on the New York Stock Exchange, or NYSE, since April 8, 1999. Between April 8, 1999 and November 22, 2009, it was listed under the symbol “TWP”. Effective November 23, 2009, the symbol changed to “TREX”. The table below shows the reported high and low sale prices of our common stock for each quarter during 2014 and 2013 as reported by the New York Stock Exchange. All common stock share and per share data in the table below are presented on a post-split basis to reflect the two-for-one stock split of our common stock distributed on May 7, 2014 to stockholders of record at the close of business on April 7, 2014.

| 2014 |

High | Low | ||||||

| First Quarter |

$ | 43.43 | $ | 31.05 | ||||

| Second Quarter |

40.51 | 28.26 | ||||||

| Third Quarter |

39.49 | 25.14 | ||||||

| Fourth Quarter |

44.82 | 31.08 | ||||||

| 2013 |

High | Low | ||||||

| First Quarter |

$ | 25.75 | $ | 19.05 | ||||

| Second Quarter |

29.02 | 22.62 | ||||||

| Third Quarter |

26.06 | 20.63 | ||||||

| Fourth Quarter |

41.52 | 23.13 | ||||||

Dividend Policy

We have never paid cash dividends on our common stock and our credit agreement places limitations on our ability to pay cash dividends. We intend to retain future earnings to finance the development and expansion of our business and, therefore, have no current intention to pay cash dividends. However, we reconsider our dividend policy on a regular basis and may determine to pay dividends in the future.

15

Table of Contents

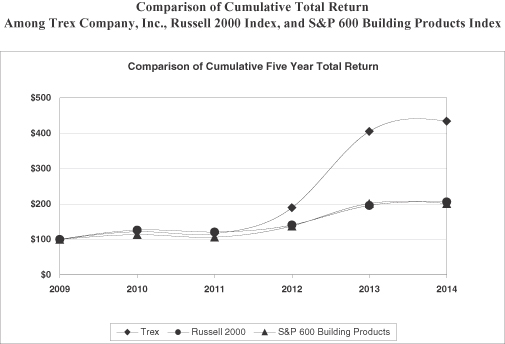

Stockholder Return Performance Graph

The following graph and table show the cumulative total stockholder return on Trex Company’s common stock for the last five fiscal years compared to the Russell 2000 Index and the Standard and Poor’s 600 Building Products Index. The graph assumes $100 was invested on December 31, 2009 in (1) Trex Company common stock, (2) the Russell 2000 Index and (3) the S&P 600 Building Products Index, and assumes reinvestment of dividends and market capitalization weighting as of December 31, 2010, 2011, 2012, 2013 and 2014.

| December 31, 2009 |

December 31, 2010 |

December 31, 2011 |

December 31, 2012 |

December 31, 2013 |

December 31, 2014 |

|||||||||||||||||||

| Trex Company |

$ | 100.00 | $ | 122.24 | $ | 116.84 | $ | 189.90 | $ | 405.71 | $ | 434.49 | ||||||||||||

| Russell 2000 |

$ | 100.00 | $ | 126.85 | $ | 121.55 | $ | 141.42 | $ | 196.32 | $ | 205.92 | ||||||||||||

| S&P 600 BPI |

$ | 100.00 | $ | 113.57 | $ | 106.72 | $ | 138.59 | $ | 202.05 | $ | 201.56 | ||||||||||||

Other Stockholder Matters

As of February 10, 2015, there were approximately 186 holders of record of our common stock.

In 2014, we submitted to the NYSE in a timely manner the annual certification that our Chief Executive Officer was not aware of any violation by us of the NYSE corporate governance listing standards.

16

Table of Contents

| Item 6. | Selected Financial Data |

The following table presents selected financial data as of December 31, 2014, 2013, 2012, 2011 and 2010 and for each of the years in the five-year period ended December 31, 2014.

The selected financial data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes thereto appearing elsewhere in this report.

| Year Ended December 31, (1) | ||||||||||||||||||||

| 2014 | 2013 (2) | 2012 (3) | 2011 (4) | 2010 (5) | ||||||||||||||||

| (In thousands, except share and per share data) | ||||||||||||||||||||

| Statement of Comprehensive Income Data: |

||||||||||||||||||||

| Net sales |

$ | 391,660 | $ | 342,511 | $ | 307,354 | $ | 266,789 | $ | 317,690 | ||||||||||

| Cost of sales |

251,464 | 243,893 | 222,772 | 203,998 | 244,875 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross profit |

140,196 | 98,618 | 84,582 | 62,791 | 72,815 | |||||||||||||||

| Selling, general and administrative expenses |

72,370 | 73,967 | 71,907 | 60,620 | 67,764 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income from operations |

67,826 | 24,651 | 12,675 | 2,171 | 5,051 | |||||||||||||||

| Interest expense, net |

878 | 602 | 8,946 | 16,364 | 15,288 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) before income taxes |

66,948 | 24,049 | 3,729 | (14,193 | ) | (10,237 | ) | |||||||||||||

| Provision (benefit) for income taxes |

25,427 | (10,549 | ) | 1,009 | (2,605 | ) | (171 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

$ | 41,521 | $ | 34,598 | $ | 2,720 | $ | (11,588 | ) | $ | (10,066 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Basic earnings (loss) per share |

$ | 1.28 | $ | 1.03 | $ | 0.08 | $ | (0.38 | ) | $ | (0.33 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Basic weighted average shares outstanding |

32,319,649 | 33,589,682 | 32,247,184 | 30,776,912 | 30,374,056 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Diluted earnings (loss) per share |

$ | 1.27 | $ | 1.01 | $ | 0.08 | $ | (0.38 | ) | $ | (0.33 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Diluted weighted average shares outstanding |

32,751,074 | 34,273,502 | 34,129,712 | 30,776,912 | 30,374,056 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Cash Flow Data: |

||||||||||||||||||||

| Cash provided by operating activities |

$ | 58,642 | $ | 45,208 | $ | 60,443 | $ | 33,847 | $ | 18,994 | ||||||||||

| Cash used in investing activities |

(12,873 | ) | (12,697 | ) | (7,484 | ) | (9,367 | ) | (9,773 | ) | ||||||||||

| Cash used in financing activities |

(39,997 | ) | (30,898 | ) | (55,326 | ) | (47,224 | ) | (1,465 | ) | ||||||||||

| Other Data (unaudited): |

||||||||||||||||||||

| EBITDA (6) |

$ | 82,653 | $ | 40,597 | $ | 29,149 | $ | 20,589 | $ | 24,666 | ||||||||||

| Balance Sheet Data: |

||||||||||||||||||||

| Cash and cash equivalents and restricted cash |

$ | 9,544 | $ | 3,772 | $ | 2,159 | $ | 41,526 | $ | 27,270 | ||||||||||

| Working capital |

35,787 | 28,994 | 10,158 | (18,574 | ) | 66,057 | ||||||||||||||

| Total assets |

195,824 | 188,157 | 168,615 | 228,090 | 247,815 | |||||||||||||||

| Total debt (including derivatives) |

— | — | 5,000 | 86,425 | 85,095 | |||||||||||||||

| Total stockholder’s equity |

$ | 113,385 | $ | 106,616 | $ | 93,986 | $ | 92,499 | $ | 102,922 | ||||||||||

| (1) | All common stock share and per share data in the above table are presented on a post-split basis to reflect the two-for-one stock split of our common stock distributed on May 7, 2014 to stockholders of record at the close of business on April 7, 2014. |

| (2) | Year ended December 31, 2013 was materially affected by a pre-tax increase of $20.0 million to the warranty reserve and a $19.9 million income tax benefit resulting from a significant reversal of our valuation allowance, $10.9 million of which was a direct result of the Company’s decision to exit a full valuation allowance. |

17

Table of Contents

| (3) | Year ended December 31, 2012 was materially affected by a pre-tax increase of $21.5 million to the warranty reserve. |

| (4) | Year ended December 31, 2011 was materially affected by a pre-tax increase of $10.0 million to the warranty reserve and a $2.6 million income tax benefit as a result of the settlement of uncertain tax positions. |

| (5) | Year ended December 31, 2010 was materially affected by a pre-tax increase of $15.0 million to the warranty reserve and $3.9 million for minimum purchase penalties. |

| (6) | EBITDA represents net income before interest, income taxes, depreciation and amortization. EBITDA is not a measurement of financial performance under accounting principles generally accepted in the United States, or GAAP. The Company has included data with respect to EBITDA because management evaluates and projects the performance of the Company’s business using several measures, including EBITDA. Management considers EBITDA to be an important supplemental indicator of the Company’s operating performance, particularly as compared to the operating performance of the Company’s competitors, because this measure eliminates many differences among companies in capitalization and tax structures, capital investment cycles and ages of related assets, as well as some recurring non-cash and non-operating charges to net income or loss. For these reasons, management believes that EBITDA provides important supplemental information to investors regarding the operating performance of the Company and facilitates comparisons by investors between the operating performance of the Company and the operating performance of its competitors. Management believes that consideration of EBITDA should be supplemental, because EBITDA has limitations as an analytical financial measure. These limitations include the following: |

| • | EBITDA does not reflect the Company’s cash expenditures, or future requirements for capital expenditures, or contractual commitments; |

| • | EBITDA does not reflect the interest expense, or the cash requirements necessary to service interest or principal payments, on the Company’s indebtedness; |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and EBITDA does not reflect any cash requirements for such replacements; |

| • | EBITDA does not reflect the effect of earnings or charges resulting from matters the Company considers not to be indicative of its ongoing operations; and |

| • | not all of the companies in the Company’s industry may calculate EBITDA in the same manner in which the Company calculates EBITDA, which limits its usefulness as a comparative measure. |

The Company compensates for these limitations by relying primarily on its GAAP results to evaluate its operating performance and by considering independently the economic effects of the foregoing items that are not reflected in EBITDA. As a result of these limitations, EBITDA should not be considered as an alternative to net income (loss), as calculated in accordance with GAAP, as a measure of operating performance, nor should it be considered as an alternative to cash flows as a measure of liquidity. The following table sets forth, for the years indicated, a reconciliation of EBITDA to net income (loss):

| Year Ended December 31, | ||||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | 2010 | ||||||||||||||||

| (In thousands) | ||||||||||||||||||||

| Net income (loss) |

$ | 41,521 | $ | 34,598 | $ | 2,720 | $ | (11,588 | ) | $ | (10,066 | ) | ||||||||

| Plus interest expense, net |

878 | 602 | 8,946 | 16,364 | 15,288 | |||||||||||||||

| Plus income tax provision (benefit) |

25,427 | (10,549 | ) | 1,009 | (2,605 | ) | (171 | ) | ||||||||||||

| Plus depreciation and amortization |

14,827 | 15,946 | 16,474 | 18,418 | 19,615 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| EBITDA |

$ | 82,653 | $ | 40,597 | $ | 29,149 | $ | 20,589 | $ | 24,666 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

18

Table of Contents

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

This management’s discussion and analysis contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All statements regarding our expected financial position and operating results, our business strategy, our financing plans, forecasted demographic and economic trends relating to our industry and similar matters are forward-looking statements. These statements can sometimes be identified by our use of forward-looking words such as “may,” “will,” “anticipate,” “estimate,” “expect,” “intend” or similar expressions. We cannot promise you that our expectations in such forward-looking statements will turn out to be correct. Our actual results could be materially different from our expectations because of various factors, including the factors discussed under “Item 1A. Risk Factors.” These statements are also subject to risks and uncertainties that could cause the Company’s actual operating results to differ materially. Such risks and uncertainties include the extent of market acceptance of the Company’s products; the costs associated with the development and launch of new products and the market acceptance of such new products; the sensitivity of the Company’s business to general economic conditions; the impact of seasonal and weather-related demand fluctuations on inventory levels in the distribution channel and sales of the Company’s products; the availability and cost of third-party transportation services for our products and raw materials; the Company’s ability to obtain raw materials at acceptable prices; the Company’s ability to maintain product quality and product performance at an acceptable cost; the level of expenses associated with product replacement and consumer relations expenses related to product quality; and the highly competitive markets in which the Company operates.

OVERVIEW