Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - COOPER TIRE & RUBBER CO | Financial_Report.xls |

| EX-32 - EX-32 - COOPER TIRE & RUBBER CO | d846103dex32.htm |

| EX-23 - EX-23 - COOPER TIRE & RUBBER CO | d846103dex23.htm |

| EX-21 - EX-21 - COOPER TIRE & RUBBER CO | d846103dex21.htm |

| EX-24 - EX-24 - COOPER TIRE & RUBBER CO | d846103dex24.htm |

| EX-31.1 - EX-31.1 - COOPER TIRE & RUBBER CO | d846103dex311.htm |

| EX-31.2 - EX-31.2 - COOPER TIRE & RUBBER CO | d846103dex312.htm |

| EX-10.(XXXIV) - EX-10.(XXXIV) - COOPER TIRE & RUBBER CO | d846103dex10xxxiv.htm |

| EX-10.(XVIII) - EX-10.(XVIII) - COOPER TIRE & RUBBER CO | d846103dex10xviii.htm |

| EX-10.(XXXIII) - EX-10.(XXXIII) - COOPER TIRE & RUBBER CO | d846103dex10xxxiii.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

For Annual and Transition Reports Pursuant to Sections 13 or 15(d) of the Securities Exchange Act of 1934

(Mark One)

| x | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

for the fiscal year ended December 31, 2014

or

| ¨ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

for the transition period from to

Commission File Number 001-04329

COOPER TIRE & RUBBER COMPANY

(Exact name of registrant as specified in its charter)

| DELAWARE | 34-4297750 | |

| (State of incorporation) | (I.R.S. employer identification no.) | |

| 701 Lima Avenue, Findlay, Ohio | 45840 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (419) 423-1321

Securities registered pursuant to Section 12(b) of the Act:

| (Title of each class) |

(Name of each exchange on which registered) | |

| Common Stock, $1 par value per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | x | Accelerated filer | ¨ | |||

| Non-Accelerated Filer | ¨ (Do not check if a small reporting company) | Smaller Reporting Company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting common stock held by non-affiliates of the registrant at June 30, 2014 was $1,829,259,610.

The number of shares outstanding of the registrant’s common stock as of February 19, 2015 was 57,389,702.

DOCUMENTS INCORPORATED BY REFERENCE

Certain information from the registrant’s definitive proxy statement for its 2015 Annual Meeting of Stockholders will be herein incorporated by reference into Part III, Items 10 – 14, of this report.

Table of Contents

COOPER TIRE & RUBBER COMPANY – FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2014

| Page | ||||

| Cover |

1 | |||

| 2 | ||||

| 2-5 | ||||

| 5-11 | ||||

| 11 | ||||

| 12 | ||||

| 12-13 | ||||

| 13 | ||||

| 15-17 | ||||

| 18 | ||||

| Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations |

19-32 | |||

| Item 7A – Quantitative and Qualitative Disclosures About Market Risk |

32 | |||

| 33-75 | ||||

| Item 9 – Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

76 | |||

| 76-77 | ||||

| 77 | ||||

| 78 | ||||

| 78 | ||||

| 78 | ||||

| Item 13 – Certain Relationships and Related Transactions, and Director Independence |

79 | |||

| 79 | ||||

| 79 | ||||

| 80 | ||||

| 81-83 | ||||

| Item 1. | BUSINESS |

Cooper Tire & Rubber Company with its subsidiaries (“Cooper” or the “Company”) is a leading manufacturer and marketer of replacement tires. It is the fourth largest tire manufacturer in North America and, according to a recognized trade source, the Cooper family of companies is the twelfth largest tire company in the world based on sales. Cooper specializes in the design, manufacture, marketing and sales of passenger car and light truck tires. Cooper and its subsidiaries also sell medium truck, motorcycle and racing tires.

The Company is organized into two separate, reportable business segments: Americas Tire Operations and International Tire Operations. Each segment is managed separately. Additional information on the Company’s segments, including their financial results, total assets, products, markets and presence in particular geographic areas, appears in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the “Business Segments” note to the consolidated financial statements.

Cooper Tire & Rubber Company was incorporated in the state of Delaware in 1930 as the successor to a business originally founded in 1914. Based in Findlay, Ohio, Cooper and its family of companies currently operate 8 manufacturing facilities and 21 distribution centers in 11 countries. As of December 31, 2014, it employed 8,881 persons worldwide.

- 2 -

Table of Contents

Business Segments

Americas Tire Operations Segment

The Americas Tire Operations segment manufactures and markets passenger car and light truck tires, primarily for sale in the United States (“U.S.”) replacement market. The segment also distributes tires for racing, medium truck and motorcycles. The racing and motorcycle tires are manufactured in the Company’s International Tire Operations segment and by others. The medium truck tires are sourced through an off-take agreement subsequent to the Company’s sale of its ownership interest in its former Cooper Chengshan (Shandong) Tire Company Ltd., joint venture, which is now known as Prinx Chengshan Tire (“CCT”). Major distribution channels and customers include independent tire dealers, wholesale distributors, regional and national retail tire chains, and large retail chains that sell tires as well as other automotive products. The segment does not sell its products directly to end users, except through three Company-owned retail stores. The segment sells a limited number of tires to original equipment manufacturers (“OEMS”).

The segment operates in a highly competitive industry, which includes Bridgestone Corporation, Goodyear Tire & Rubber Company and Groupe Michelin. These competitors are substantially larger than the Company and serve OEMs as well as the replacement tire market. The segment also faces competition from low-cost producers in Asia, Mexico, South America and Central Europe. Some of those producers are foreign affiliates of the segment’s competitors in North America. The segment had a market share in 2014 of approximately 12 percent of all light vehicle replacement tire sales in the U.S. The segment also participates in the U.S. medium truck replacement market. In addition to manufacturing tires in the U.S., the segment has a joint venture manufacturing operation in Mexico, Corporacion de Occidente SA de CV (“COOCSA”). A portion of the products manufactured by the segment are exported throughout the world.

Success in competing for the sale of replacement tires is dependent upon many factors, the most important of which are price, quality, performance, line coverage, availability through appropriate distribution channels and relationships with dealers and retailers. Other factors include warranty, credit terms and other value-added programs. The segment has built close working relationships through the years with independent dealers. It believes those relationships have enabled it to obtain a competitive advantage in that channel of the market. As a steadily increasing percentage of replacement tires are sold by large regional and national tire retailers, the segment has increased its penetration of those distribution channels, while maintaining a focus on its traditionally strong network of independent dealers.

The segment’s replacement tire business has a broad customer base that includes purchasers of proprietary brand tires that are marketed and distributed by the Company and private label tires which are manufactured by the Company but marketed and distributed by the Company’s customers. The segment is a leading supplier of private label tires in the U.S.

Customers generally place orders on a month-to-month basis and the segment adjusts production and inventory to meet those orders which results in varying backlogs of orders at different times of the year. Tire sales are subject to a seasonal demand pattern. This usually results in the sales volumes being strongest in the third and fourth quarters and weaker in the first and second quarters.

International Tire Operations Segment

The International Tire Operations segment has manufacturing operations in the United Kingdom (“U.K.”), the Republic of Serbia (“Serbia”) and the People’s Republic of China (“PRC”). The U.K. entity manufactures and markets passenger car, light truck, motorcycle and racing tires and tire retread material for the global market. On January 17, 2012, the segment acquired certain assets of a light vehicle tire manufacturing facility in Serbia. This entity manufactures light vehicle tires for the European markets. The segment’s Cooper Kunshan entity in the PRC currently manufactures light vehicle tires. Under an agreement with the government of the PRC, all of the tires produced at this facility through 2012 had been exported. Beginning in 2013, tires produced at this facility have also been sold in the domestic market. The segment also had a joint venture in the PRC, CCT, which manufactured and marketed radial and bias medium truck tires as well as passenger and light truck tires for the global market. The Company sold its ownership interest in this joint venture in November 2014 and signed off-take agreements under which CCT will continue to produce Cooper-branded products, including medium truck tires, through mid-2018. A small percentage of the tires manufactured by the segment are sold to OEMs.

The segment has also established sales, marketing, distribution and research and development capabilities to support the Company’s objectives.

As in the Americas, the segment operates in a highly competitive industry, which includes Bridgestone Corporation, Goodyear Tire & Rubber Company and Groupe Michelin. These competitors are substantially larger than the Company and serve OEMs as well as the replacement tire market. The segment also faces competition from low-cost producers in certain markets.

- 3 -

Table of Contents

Raw Materials

The Company’s principal raw materials include natural rubber, synthetic rubber, carbon black, chemicals and steel reinforcement components. The Company acquires its raw materials from various sources around the world to assure continuing supplies for its manufacturing operations and mitigate the risk of potential supply disruptions.

During 2014, the Company experienced lower raw material costs compared with 2013. The pricing volatility of natural rubber and certain other raw materials contributes to the difficulty in accurately predicting and managing these costs.

The Company has a purchasing office in Singapore to acquire natural rubber directly from producers in Southeast Asia. This purchasing operation enables the Company to work directly with producers to continually improve consistency and quality while reducing the costs of materials, transportation and transactions.

The Company’s contractual relationships with its raw material suppliers are generally based on long-term agreements and/or purchase order arrangements. For natural rubber and natural gas, procurement is managed through a combination of buying forward production requirements and utilizing the spot market. For other principal materials, procurement arrangements include supply agreements that may contain formula-based pricing based on commodity indices, multi-year agreements or spot purchases. These arrangements only cover quantities needed to satisfy normal manufacturing demands.

Working Capital

The Company’s working capital consists mainly of inventory, accounts receivable and accounts payable. These working capital accounts are closely managed by the Company. Inventory balances are primarily valued at a last-in, first-out (“LIFO”) basis in the Americas Tire Operations segment and under the first-in, first-out (“FIFO”) or average cost method for entities in the International Tire Operations segment. Inventories turn regularly, but balances typically increase during the first half of the year before declining as a result of increased sales in the second half. The Company’s inventory levels are kept within the targeted range to meet projected demand. The mix of inventory is critical to inventory turnover and meeting customer demand. Accounts receivable and accounts payable are also affected by this business cycle, typically requiring the Company to have greater working capital needs during the second and third quarters. The Company engages in a rigorous credit analysis of its customers and monitors their financial positions. The Company offers incentives to certain customers to encourage the payment of account balances prior to their scheduled due dates.

At December 31, 2014, the Company held cash and cash equivalents of $552 million.

Research, Development and Product Improvement

The Company directs its research activities toward product development, performance and operating efficiency. The Company conducts extensive testing of current tire lines, as well as new concepts in tire design, construction and materials. During 2014, approximately 101 million miles of tests were performed on indoor test wheels and in monitored road tests. The Company has a tire and vehicle test track in Texas that assists with the Company’s testing activities. Uniformity equipment is used to physically monitor manufactured tires for high standards of ride quality. The Company continues to design and develop specialized equipment to fit the precise needs of its manufacturing and quality control requirements. Research and development expenditures were $50.8 million, $51.1 million and $56.8 million during 2012, 2013 and 2014, respectively.

Patents, Intellectual Property and Trademarks

The Company owns and/or has licenses to use patents and intellectual property covering various aspects in the design and manufacture of its products and processes and equipment for the manufacture of its products. While the Company believes these assets as a group are of material importance, it does not consider any one asset or group of these assets to be of such importance that the loss or expiration thereof would materially affect its business.

The Company owns and uses tradenames and trademarks worldwide. While the Company believes such tradenames and trademarks as a group are of material importance, the trademarks the Company considers most significant to its business are those using the words “Cooper,” “Mastercraft” and “Avon.” The Company believes all of these significant trademarks are valid and will have unlimited duration as long as they are adequately protected and appropriately used. Certain other tradenames and trademarks are being amortized over the next four to fourteen years.

- 4 -

Table of Contents

Seasonal Trends

There is year-round demand for passenger and truck replacement tires, but passenger replacement tire sales are generally strongest during the third and fourth quarters of the year. Winter tires are sold principally during the months of June through November.

Environmental Matters

The Company recognizes the importance of compliance in environmental matters and has an organizational structure to supervise environmental activities, planning and programs. The Company also participates in activities concerning general industry environmental matters. The Company’s operations have been recognized with several awards for efforts to improve energy efficiency.

The Company’s manufacturing facilities, like those of the industry generally, are subject to numerous laws and regulations designed to protect the environment. In general, the Company has not experienced difficulty in complying with these requirements and believes they have not had a material adverse effect on its financial condition or the results of its operations. The Company expects additional requirements with respect to environmental matters will be imposed in the future. The Company’s 2014 expense and capital expenditures for environmental matters at its facilities were not material, nor is it expected that expenditures in 2015 for such uses will be material.

Foreign Operations

The Company has a manufacturing facility, a technical center, a distribution center and its European headquarters office located in the U.K. There are seven distribution centers and six sales offices in Europe. The Company has a manufacturing facility in Serbia. The Company has a manufacturing facility, two distribution centers, a technical center, a sales office and an administrative office in the PRC. The Company also has a purchasing office in Singapore. In Mexico, the Company has a joint venture manufacturing facility, a sales office and a distribution center.

Additional information on the Company’s foreign operations can be found in the “Business Segments” note to the consolidated financial statements.

Available Information

The Company makes available free of charge, on or through its website, its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after it electronically files such material with, or furnishes it to, the U.S. Securities and Exchange Commission (“SEC”). The Company’s internet address is http://www.coopertire.com. The Company has adopted charters for each of its Audit, Compensation and Nominating and Governance Committees, corporate governance guidelines and a code of business ethics and conduct, which are available on the Company’s website and will be available to any stockholder who requests them from the Company’s Director of Investor Relations. The information contained on the Company’s website is not incorporated by reference in this annual report on Form 10-K and should not be considered a part of this report.

| Item 1A. | RISK FACTORS |

Some of the more significant risk factors related to the Company and its subsidiaries follow:

Pricing volatility for raw materials or commodities or an inadequate supply of key raw materials could result in increased costs and may significantly affect the Company’s profitability.

The pricing volatility for natural rubber, petroleum-based materials and other raw materials contributes to the difficulty in managing the costs of raw materials. Costs for certain raw materials used in the Company’s operations, including natural rubber, chemicals, carbon black, steel reinforcements and synthetic rubber remain highly volatile. Increasing costs for raw material supplies will increase the Company’s production costs and affect its margins if the Company is unable to pass the higher production costs on to its customers in the form of price increases. Decreasing costs for raw materials could also affect margins if the Company is unable to maintain its pricing structure by offering price reductions to remain competitive. Further, if the Company is unable to obtain adequate supplies of raw materials in a timely manner for any reason, its operations could be interrupted or otherwise adversely affected.

- 5 -

Table of Contents

The Company is facing heightened risks due to the current business environment.

Current global economic conditions may affect demand for the Company’s products, create volatility in raw material costs and affect the availability and cost of credit. These conditions also affect the Company’s customers and suppliers as well as the ultimate consumer.

Deterioration in the global macroeconomic environment or in specific regions could impact the Company and, depending upon the severity and duration of these factors, the Company’s profitability and liquidity position could be negatively impacted.

The Company’s competitors may also change their actions as a result of changes to the business environment, which could result in increased price competition and discounts, resulting in lower margins for the business.

The Company’s results could be impacted by changes in tariffs imposed by the U.S. or other governments on imported tires.

The Company’s ability to competitively source and sell tires can be significantly impacted by changes in tariffs imposed by various governments. Other effects, including impacts on the price of tires, responsive actions from other governments and the opportunity for competitors to establish a presence in markets where the Company participates, could also have significant impacts on the Company’s results.

Antidumping and countervailing duty investigations into certain passenger car and light truck tires imported from the PRC into the United States were initiated on July 14, 2014. The preliminary determinations announced in both investigations were affirmative and resulted in the imposition of additional duties from each. It is too early to determine the ultimate outcome of these investigations and what impact they will have on the Company. Final determinations in these investigations are expected during the third quarter of 2015.

The Company is facing supply risks related to certain tires it purchases from CCT.

In 2014, the Company sold its ownership interest in CCT and entered into off-take agreements with CCT to provide the continuous supply of certain CCT-produced tires for the Company. If there are any disruptions in or quality issues with the supply of Cooper-branded products, it could have a material negative impact on the Company’s business. In addition, the Company could be required to find an alternative source for CCT-produced tires and there can be no assurance that the Company will be able to do so in a timely manner. CCT is currently the sole supplier of medium truck tires for the Company

The Company may fail to successfully develop or implement information technologies or related systems, resulting in a significant competitive disadvantage.

Successfully competing in the highly competitive tire industry can be impacted by the successful development of information technology. If the Company fails to successfully implement information technology systems, it may be at a disadvantage to its competitors resulting in lost sales and negative impacts on the Company’s earnings.

The Company has implemented an Enterprise Resource Planning (“ERP”) system in the United States and is continuing to implement the system globally, which will require significant amounts of capital and human resources to deploy. These requirements may exceed the Company’s projections. If for any reason this implementation is not successful, the Company could be required to expense rather than capitalize related amounts. Throughout implementation of the system there are also risks created to the Company’s ability to successfully and efficiently operate.

The Company’s industry is highly competitive, and the Company may not be able to compete effectively with lower-cost producers and larger competitors.

The replacement tire industry is a highly competitive, global industry. Some of the Company’s competitors are larger companies with greater financial resources. Most of the Company’s competitors have operations in lower-cost countries. Intense competitive activity in the replacement tire industry has caused, and will continue to cause, pressures on the Company’s business. The Company’s ability to compete successfully will depend in part on its ability to balance capacity with demand, leverage global purchasing of raw materials, make required investments to improve productivity, eliminate redundancies and increase production at low-cost, high-quality supply sources. If the Company is unable to offset continued pressures with improved operating efficiencies, its sales, margins, operating results and market share would decline and the impact could become material on the Company’s earnings.

- 6 -

Table of Contents

The Company may be adversely affected by legal actions, including products liability claims which, if successful, could have a negative impact on its financial position, cash flows and results of operations.

The Company’s operations expose it to legal actions, including potential liability for personal injury or death as an alleged result of the failure of or conditions in the products that it designs, manufactures and sells. Specifically, the Company is a party to a number of products liability cases in which individuals involved in motor vehicle accidents seek damages resulting from allegedly defective tires that it manufactured. Products liability claims and lawsuits, including possible class action, may result in material losses in the future and cause the Company to incur significant litigation defense costs. The Company is largely self-insured against these claims. These claims could have a negative effect on the Company’s financial position, cash flows and results of operations.

From time to time, the Company is also subject to litigation or other commercial disputes and other legal proceedings relating to its business, including purported class action lawsuits, derivative lawsuits and other litigation related to the now terminated merger agreement with the Apollo entities. Due to the inherent uncertainties of any litigation, commercial disputes or other legal proceedings, the Company cannot accurately predict their ultimate outcome, including the outcome of any related appeals. An unfavorable outcome could materially adversely impact the Company’s financial condition, cash flows and results of operations.

The Company’s expenditures for pension and other postretirement obligations could be materially higher than it has predicted if its underlying assumptions prove to be incorrect.

The Company provides defined benefit and hybrid pension plan coverage to union and non-union U.S. employees and a contributory defined benefit plan in the U.K. The Company’s pension expense and its required contributions to its pension plans are directly affected by the value of plan assets, the projected and actual rates of return on plan assets and the actuarial assumptions the Company uses to measure its defined benefit pension plan obligations, including the discount rate at which future projected and accumulated pension obligations are discounted to a present value and the inflation rate. The Company could experience increased pension expense due to a combination of factors, including the decreased investment performance of its pension plan assets, decreases in the discount rate, changes in its assumptions relating to the expected return on plan assets and updates to mortality tables. The Company could also experience increased other postretirement expense due to decreases in the discount rate, increases in the health care trend rate and changes in the health care environment.

In the event of declines in the market value of the Company’s pension assets or lower discount rates to measure the present value of pension and other postretirement benefit obligations, the Company could experience changes to its Consolidated Balance Sheet or significant cash requirements.

Compliance with regulatory initiatives could increase the cost of operating the Company’s business.

The Company is subject to federal, state, local and foreign laws and regulations. Compliance with those laws now in effect, or that may be enacted, could require significant capital expenditures, increase the Company’s production costs and affect its earnings and results of operations.

Several countries have or may implement labeling requirements for tires. This legislation could cause the Company’s products to be at a disadvantage in the marketplace resulting in a loss of market share or could otherwise impact the Company’s ability to distribute and sell its tires.

In addition, while the Company believes that its tires are free from design and manufacturing defects, it is possible that a recall of the Company’s tires could occur in the future. A recall could harm the Company’s reputation, operating results and financial position.

The Company is also subject to legislation governing labor occupational safety and health both in the U.S. and other countries. The related legislation can change over time making it more expensive for the Company to produce its products. The Company could also, despite its best efforts to comply with these laws, be found liable and be subject to additional costs because of this legislation.

The Company has a risk due to volatility of the capital and financial markets.

The Company periodically requires access to the capital and financial markets as a significant source of liquidity for maturing debt payments or working capital needs that it cannot satisfy by cash on hand or operating cash flows. Substantial volatility in world capital markets and the banking industry may make it difficult for the Company to access credit markets and to obtain financing or refinancing, as the case may be, on satisfactory terms or at all. In addition, various additional factors, including a deterioration of the Company’s credit ratings or its business or financial condition, could further impair its access to the capital markets. Additionally, any inability to access the capital markets, including the ability to refinance existing debt when due, could require the Company to defer critical capital expenditures, reduce or not pay dividends, reduce spending in areas of strategic importance, sell important assets or, in extreme cases, seek protection from creditors. See also related comments under “There are risks associated with the Company’s global strategy which includes using joint ventures and partially-owned subsidiaries.”

- 7 -

Table of Contents

The Company’s operations in the PRC have been financed in part using multiple loans from several lenders to finance facility construction, expansions and working capital needs. These loans are generally for terms of three years or less. Therefore, debt maturities occur frequently and access to the capital markets is crucial to their ability to maintain sufficient liquidity to support their operations.

The Company conducts its manufacturing, sales and distribution operations on a worldwide basis and is subject to risks associated with doing business outside the U.S.

The Company has affiliate, subsidiary and joint venture operations worldwide, including in the U.S., the U.K., Europe, Mexico and the PRC. The Company has one manufacturing entity, Cooper Kunshan, in the PRC. The Company also is the majority owner of COOCSA, a manufacturing entity in Mexico, and has established an operation in Serbia. In 2014, the Company sold its ownership interest in CCT and entered into off-take agreements with CCT to continue supplying tires to the Company. CCT is currently the sole supplier of medium truck tires for the Company. There are a number of risks in doing business abroad, including political and economic uncertainty, social unrest, sudden changes in laws and regulations, shortages of trained labor and the uncertainties associated with entering into joint ventures or similar arrangements in foreign countries. These risks may impact the Company’s ability to expand its operations in different regions and otherwise achieve its objectives relating to its foreign operations, including utilizing these locations as suppliers to other markets. In addition, compliance with multiple and potentially conflicting foreign laws and regulations, import and export limitations and exchange controls is burdensome and expensive. The Company’s foreign operations also subject it to the risks of international terrorism and hostilities and to foreign currency risks, including exchange rate fluctuations and limits on the repatriation of funds.

If the Company fails to develop technologies, processes or products needed to support consumer demand it may lose significant market share or be unable to recover associated costs.

The Company’s ability to sell tires may be significantly impacted if it does not develop or have available technologies, processes, or products that competitors may be developing and consumers demanding. This includes but is not limited to changes in the design of and materials used to manufacture tires.

Technologies may also be developed by competitors that better distribute tires to consumers, which could affect the Company’s customers.

Additionally, developing new products and technologies requires significant investment and capital expenditures, is technologically challenging and requires extensive testing and accurate anticipation of technological and market trends. If the Company fails to develop new products that are appealing to its customers, or fails to develop products on time and within budgeted amounts, the Company may be unable to recover its product development and testing costs. If the Company cannot successfully use new production or equipment methodologies it invests in, it may also not be able to recover those costs.

A disruption in, or failure of, the Company’s information technology systems, including those related to cybersecurity, could adversely affect the Company’s business operations and financial performance.

The Company relies on the accuracy, capacity and security of its information technology systems across all of its major business functions, including its research and development, manufacturing, sales, financial and administrative functions. Despite the security measures that the Company has implemented, including those related to cybersecurity, its systems could be breached or damaged by computer viruses, natural or man-made incidents or disasters or unauthorized physical or electronic access. A system failure, accident or security breach could result in business disruption, theft of its intellectual property, trade secrets or customer information and unauthorized access to personnel information. To the extent that any system failure, accident or security breach results in disruptions to its operations or the theft, loss or disclosure of, or damage to, its data or confidential information, the Company’s reputation, business, results of operations, cash flows and financial condition could be materially adversely affected. In addition, the Company may be required to incur significant costs to protect against and, if required, remediate the damage caused by such disruptions or system failures in the future.

Any interruption in the Company’s skilled workforce, or that of its suppliers or customers, including labor disruptions, could impair its operations and harm its earnings and results of operations.

The Company’s operations depend on maintaining a skilled workforce and any interruption of its workforce due to shortages of skilled technical, production or professional workers, work disruptions, or other events could interrupt the Company’s operations and affect its operating results. Further, a significant number of the Company’s employees are currently represented by unions. If the Company is unable to resolve any labor disputes or if there are work stoppages or other work disruptions at the Company or any of its suppliers or customers, the Company’s business and operating results could suffer. See also related comments under “The Company is facing supply risks related to certain tires it purchases from CCT.”

- 8 -

Table of Contents

If the Company is unable to attract and retain key personnel, its business could be materially adversely affected.

The Company’s business depends on the continued service of key members of its management. The loss of the services of a significant number of members of its management team could have a material adverse effect on its business. The Company’s future success will also depend on its ability to attract, retain and develop highly skilled personnel, such as engineering, marketing and senior management professionals. Competition for these employees is intense, especially in the PRC, and the Company could experience difficulty from time to time in hiring and retaining the personnel necessary to support its business. If the Company does not succeed in retaining its current employees and attracting new high-quality employees, its business could be materially adversely affected.

If assumptions used in developing the Company’s strategic plan are inaccurate or the Company is unable to execute its strategic plan effectively, its profitability and financial position could be negatively impacted.

The Company faces both general industry and company-specific challenges. These include volatile raw material costs, increasing product complexity and pressure from competitors with greater resources or manufacturing in lower-cost regions. To address these challenges and position the Company for future success, the Company continues to execute towards strategic imperatives outlined in its Strategic Plan. The three strategic imperatives are building a sustainable cost competitive position, driving top-line profitable growth and building organizational capabilities and enablers to support strategic goals.

The Company continually reviews and updates its business plans to achieve these imperatives. If the assumptions used in developing the Company’s business plans vary significantly from actual conditions, the Company’s sales, margins and profitability could be harmed. If the Company is unsuccessful in implementing the tactics necessary to execute its business plans it may not be able to achieve or sustain future profitability, which could impair its ability to meet debt and other obligations and could otherwise negatively affect its operating results, financial condition and liquidity.

The Company may not be successful in executing and integrating acquisitions into its operations, which could harm its results of operations and financial condition.

The Company routinely evaluates potential acquisitions and may pursue acquisition opportunities, some of which could be material to its business. The Company cannot provide assurance whether it will be successful in pursuing any acquisition opportunities or what the consequences of any acquisition would be. The Company may encounter various risks in any acquisitions, including:

| • | the possible inability to integrate an acquired business into its operations; |

| • | diversion of management’s attention; |

| • | loss of key management personnel; |

| • | unanticipated problems or liabilities; and |

| • | increased labor and regulatory compliance costs of acquired businesses. |

Some or all of those risks could impair the Company’s results of operations and impact its financial condition. The Company may finance any future acquisitions from internally generated funds, bank borrowings, public offerings or private placements of equity or debt securities, or a combination of the foregoing. Acquisitions may involve the expenditure of significant funds and management time.

Acquisitions may also require the Company to increase its borrowings under its bank credit facilities or other debt instruments, or to seek new sources of liquidity. Increased borrowings would correspondingly increase the Company’s financial leverage, and could result in lower credit ratings and increased future borrowing costs. These risks could also reduce the Company’s flexibility to respond to changes in its industry or in general economic conditions.

In addition, the Company’s business plans call for growth, particularly in Asia. If the Company is unable to identify or execute on appropriate opportunities for acquisition, investment or growth, its business could be materially adversely affected.

There are risks associated with the Company’s global strategy which includes using joint ventures and partially-owned subsidiaries.

The Company’s strategy includes the use of joint ventures and other partially-owned subsidiaries. These entities operate in countries outside of the U.S., are generally less well capitalized than the Company and bear risks similar to the risks of the Company. In addition, there are specific risks applicable to these subsidiaries and these risks, in turn, add potential risks to the Company. Such risks include greater risk of joint venture partners or other investors failing to meet their obligations under related shareholders’ agreements; conflicts with joint venture partners; the possibility of a joint venture partner taking valuable knowledge from the Company; and risk of being denied access to the capital markets, which could lead to resource demands on the Company in order to maintain or advance its strategy. The Company’s outstanding notes and primary credit facility contain cross default provisions in the event of certain defaults by the Company under other agreements with third parties. For further discussion of access to the capital markets, see also related comments under “The Company has a risk due to volatility of the capital and financial markets.”

- 9 -

Table of Contents

If the price of energy sources increases, the Company’s operating expenses could increase significantly or the demand for the Company’s products could be affected.

The Company’s manufacturing facilities rely principally on natural gas, as well as electrical power and other energy sources. High demand and limited availability of natural gas and other energy sources can result in significant increases in energy costs increasing the Company’s operating expenses and transportation costs. Higher energy costs would increase the Company’s production costs and adversely affect its margins and results of operations. If the Company is unable to obtain adequate sources of energy, its operations could be interrupted.

In addition, if the price of gasoline increases significantly for consumers, it can affect driving and purchasing habits and impact demand for tires.

The Company is required to comply with environmental laws and regulations that could cause it to incur significant costs.

The Company’s manufacturing facilities are subject to numerous federal, state, local and foreign laws and regulations designed to protect the environment, and the Company expects that additional requirements with respect to environmental matters will be imposed on it in the future. In addition, the Company has contractual indemnification obligations for environmental remediation costs and liabilities that may arise relating to certain divested operations. Material future expenditures may be necessary if compliance standards change, if material unknown conditions that require remediation are discovered, or if required remediation of known conditions becomes more extensive than expected. If the Company fails to comply with present and future environmental laws and regulations, it could be subject to future liabilities or the suspension of production, which could harm its business or results of operations. Environmental laws could also restrict the Company’s ability to expand its facilities or could require it to acquire costly equipment or to incur other significant expenses in connection with its manufacturing processes.

The Company has been and may continue to be impacted by currency fluctuations, which may reduce reported results for our international operations and otherwise adversely affect our business.

Because the Company conducts transactions in various non-U.S. currencies, including the Euro, Canadian dollar, British pound sterling, Swiss franc, Swedish kronar, Mexican peso and Chinese yuan, fluctuations in foreign currency exchange rates may impact the Company’s financial condition, results of operations and cash flows. Our operating results are subject to the effects of fluctuations in the value of these currencies and fluctuations in the related currency exchange rates. As a result, the Company’s sales have historically been affected by, and may continue to be affected by, these fluctuations. Exchange rate movements between currencies in which the Company sells its products have been affected by and may continue to result in exchange losses that could materially affect results. During times of strength of the U.S. dollar, the reported revenues of the Company’s international operations will be reduced because local currencies will translate into fewer dollars. In addition, a strong U.S. dollar may increase the competitiveness of competitors based outside of the United States. As a result, continued strengthening of the U.S. dollar may have a material adverse effect on the Company’s financial condition, results of operations and cash flows.

The Company may not be able to protect its intellectual property rights adequately.

The Company’s success depends in part upon its ability to use and protect its proprietary technology and other intellectual property, which generally covers various aspects in the design and manufacture of its products and processes. The Company owns and uses tradenames and trademarks worldwide. The Company relies upon a combination of trade secrets, confidentiality policies, nondisclosure and other contractual arrangements and patent, copyright and trademark laws to protect its intellectual property rights. The steps the Company takes in this regard may not be adequate to prevent or deter challenges, reverse engineering or infringement or other violations of its intellectual property, and the Company may not be able to detect unauthorized use or take appropriate and timely steps to enforce its intellectual property rights. In addition, the laws of some countries may not protect and enforce the Company’s intellectual property rights to the same extent as the laws of the U.S. Further, while the Company believes it has rights to use all intellectual property in the Company’s use, if the Company is found to infringe on the rights of others it could be adversely impacted.

The Company is facing risks relating to enactment of healthcare legislation.

The Company is facing risks emanating from the enactment of legislation by the U.S. government including the Patient Protection and Affordable Care Act and the related Healthcare and Education Reconciliation Act, which are collectively referred to as healthcare legislation. This major legislation is being implemented over a period of several years and the ultimate cost and the potentially adverse impact to the Company and its employees cannot be quantified at this time.

- 10 -

Table of Contents

The impact of proposed new accounting standards may have a negative impact on the Company’s financial statements.

The Financial Accounting Standards Board is considering several projects which may result in the modification of accounting standards affecting the Company, including standards relating to revenue recognition, financial instruments, leasing, and others. Any such changes could have a negative impact on the Company’s financial statements.

The realizability of deferred tax assets may affect the Company’s profitability and cash flows.

The Company has significant net deferred tax assets recorded on the balance sheet and determines at each reporting period whether or not a valuation allowance is necessary based upon the expected realizability of such deferred tax assets. In the U.S., the Company has recorded deferred tax assets, the largest of which relate to products liability, pension and other postretirement benefit obligations, partially offset by deferred tax liabilities, the most significant of which relates to accelerated depreciation. The Company’s non-U.S. deferred tax assets relate to pension, accrued expenses and net operating losses, and are partially offset by deferred tax liabilities related to accelerated depreciation. Based upon the Company’s assessment of the realizability of its net deferred tax assets, the Company maintains a small valuation allowance for the portion of its U.S. deferred tax assets primarily associated with a capital loss carryforward. In addition, the Company has recorded valuation allowances for deferred tax assets primarily associated with non-U.S. net operating losses. The Company’s assessment of the realizability of deferred tax assets is based on certain assumptions regarding future profitability, and potentially adverse business conditions that could have a negative impact on the realizability and therefore impact the Company’s operating results or financial position.

| Item 1B. | UNRESOLVED STAFF COMMENTS |

None.

- 11 -

Table of Contents

| Item 2. | PROPERTIES |

As shown in the following table, at December 31, 2014, the Company maintained 51 manufacturing, distribution, retail stores and office facilities worldwide. The Company owns a majority of the manufacturing facilities while some manufacturing, distribution and office facilities are leased.

| Americas Tire Operations | International Tire Operations | |||||||||||||||||||

| Type of Facility |

United States | Mexico | Europe | Asia | Total | |||||||||||||||

| Manufacturing |

4 | 1 | * | 2 | 1 | 8 | ||||||||||||||

| Distribution |

10 | 1 | 8 | 2 | 21 | |||||||||||||||

| Retail Stores |

3 | — | — | — | 3 | |||||||||||||||

| Technical centers and offices |

6 | 1 | 8 | 4 | 19 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total |

23 | 3 | 18 | 7 | 51 | |||||||||||||||

| * | This includes a manufacturing facility that is a joint venture. |

The Company believes its properties have been adequately maintained, generally are in good condition and are suitable and adequate to meet the demands of each segment’s business.

| Item 3. | LEGAL PROCEEDINGS |

The Company is a defendant in various judicial proceedings arising in the ordinary course of business. A significant portion of these proceedings are products liability cases in which individuals involved in vehicle accidents seek damages resulting from allegedly defective tires manufactured by the Company. After reviewing all of these proceedings, and taking into account all relevant factors concerning them, the Company does not believe that any liabilities resulting from these proceedings are reasonably likely to have a material adverse effect on its liquidity, financial condition or results of operations in excess of amounts recorded at December 31, 2014. In the future, such costs could have a materially greater impact on the consolidated results of operations and financial position of the Company than in the past.

Certain Litigation Related to the Apollo Merger

Following the announcement of the proposed acquisition of the Company by wholly owned subsidiaries of Apollo Tyres Ltd. (the “Apollo entities”) in June 2013, alleged stockholders of the Company filed putative class action lawsuits in state courts in Delaware and Ohio. These lawsuits, captioned In re Cooper Tire & Rubber Co. Stockholders Litigation, No. 9658 VCL and Auld v. Cooper Tire & Rubber Co., et al., No. 2013 CV 293, alleged that the directors of the Company breached their fiduciary duties to the Company’s stockholders by agreeing to enter into the proposed transaction for an allegedly unfair price and as the result of an allegedly unfair process. The lawsuits sought, among other things, declaratory and injunctive relief. On December 30, 2013, the Company terminated the merger agreement with the Apollo entities. Following the termination of the merger agreement, the plaintiffs voluntarily dismissed the Delaware and Ohio lawsuits in April 2014.

On October 4, 2013, the Company filed a complaint in the Court of Chancery of the State of Delaware, captioned Cooper Tire Co. v. Apollo (Mauritius) Holdings Pvt. Ltd., et al., No. 8980- VCG, asking that the Apollo entities be required to use their reasonable efforts to close the then pending merger transaction as expeditiously as possible and also seeking, among other things, declaratory relief and damages. On October 14, 2013, the Apollo entities filed counterclaims against the Company seeking declaratory and injunctive relief.

On October 31, 2014, the court granted Apollo’s motion for declaratory judgment that the conditions to closing the then pending transaction were not satisfied before the November 2013 trial. On November 26, 2014, the Company appealed the Chancery Court’s decision to the Delaware Supreme Court. On December 3, 2014, the parties reached an agreement to dismiss the appeal and the underlying action, acknowledge the termination of the Merger Agreement, and to release all claims relating to the Merger Agreement, subject to the dismissal of the action. On December 17, 2014, the Company dismissed the appeal and the parties filed a stipulation of dismissal of the underlying action.

- 12 -

Table of Contents

Federal Securities Litigation

On January 17, 2014, alleged stockholders of the Company filed a putative class-action lawsuit against the Company and certain of its officers in the United States District Court for the District of Delaware relating to the terminated Apollo transaction. That lawsuit, captioned OFI Risk Arbitrages, et al. v. Cooper Tire & Rubber Co., et al., No. 1:14-cv-00068-LPS, generally alleges that the Company and certain officers violated the federal securities laws by issuing allegedly misleading disclosures in connection with the terminated transaction and seeks, among other things, damages. The Company and its officers believe that the allegations against them lack merit and intend to defend the lawsuit vigorously.

The Company regularly reviews the probable outcome of such legal proceedings, the expenses expected to be incurred, the availability and limits of the insurance coverage, and accrues for these proceedings at the time a loss is probable and the amount of the loss can be estimated.

The outcome of these pending proceedings cannot be predicted with certainty and an estimate of any such loss cannot be made at this time. The Company believes that based upon information currently available, any liabilities that may result from these proceedings are not reasonably likely to have a material adverse effect on the Company’s liquidity, financial condition or results of operations.

Stockholder Derivative Litigation

On February 24, March 6, and April 17, 2014, purported stockholders of the Company filed derivative actions on behalf of the Company in the U.S. District Court for the Northern District of Ohio and the U.S. District Court for the District of Delaware against certain current officers and employees and the then current members of the Company’s board of directors. The lawsuits have been transferred to the U.S. District Court for the District of Delaware and consolidated under the caption Fitzgerald v. Armes, et al., No. 1:14-cv-479 (D. Del.). The Company is named as a nominal defendant in the lawsuits, and the lawsuits seek recovery for the benefit of the Company. The plaintiffs allege that the defendants breached their fiduciary duties to the Company by issuing allegedly misleading disclosures in connection with the terminated merger transaction and that the defendants violated Section 14(a) of the Securities Exchange Act of 1934 by means of the same allegedly misleading disclosures. The plaintiffs also assert claims for waste of corporate assets, unjust enrichment, “gross mismanagement” and “abuse of control.” The complaints seek, among other things, unspecified money damages from the defendants, injunctive relief and an award of attorney’s fees. A purported shareholder of the Company has also submitted a demand to the Company’s board of directors that it cause the Company to bring claims against certain of the Company’s officers and directors for the matters alleged in the shareholder derivative lawsuits.

The Company regularly reviews the probable outcome of such legal proceedings, the expenses expected to be incurred, the availability and limits of the insurance coverage, and accrues for such legal proceedings at the time a loss is probable and the amount of the loss can be estimated.

These cases do not assert claims against the Company. The outcome of these pending proceedings cannot be predicted with certainty and an estimate of any loss cannot be made at this time. The Company believes that based upon information currently available, any liabilities that may result from these proceedings are not reasonably likely to have a material adverse effect on the Company’s liquidity, financial condition or results of operations.

| Item 4. | RESERVED |

- 13 -

Table of Contents

EXECUTIVE OFFICERS OF THE REGISTRANT

The names, ages and all positions and offices held by all executive officers of the Company are as follows:

| Name |

Age | Executive Office Held |

Business Experience | |||

| Roy V. Armes |

62 | Chairman of the Board, Chief Executive Officer, President and Director | Chairman of the Board since December 2007, Chief Executive Officer, President and Director since January 2007. | |||

| Brenda S. Harmon |

63 | Senior Vice President and Chief Human Resources Officer | Senior Vice President, Chief Human Resources Officer since December 2009. Previously Owner of Harmon Consulting Services since November 2008. | |||

| Bradley E. Hughes |

53 | Senior Vice President and Chief Operating Officer | Senior Vice President and Chief Operating Officer since January 2015. Senior Vice President and President-International Tire Operations from July 2014 to January 2015. Senior Vice President and Chief Financial Officer from September 2014 to December 2014. Senior Vice President, Chief Financial Officer and Treasurer from July 2014 to September 2014. Vice President, Chief Financial Officer and Treasurer from November 2013 to July 2014. Vice President and Chief Financial Officer from November 2009 to November 2013. | |||

| Ginger M. Jones |

50 | Vice President and Chief Financial Officer | Vice President and Chief Financial Officer since December 2014. Previously Senior Vice President and Chief Financial Officer of Plexus Corporation, an electronics manufacturing services company, from 2011 to May 2014; Vice President and Chief Finance Officer from 2007 to 2011. | |||

| Stephen Zamansky |

44 | Senior Vice President, General Counsel and Secretary | Senior Vice President, General Counsel and Secretary since July 2014. Vice President, General Counsel and Secretary from April 2011 to July 2014. Previously Senior Vice President, General Counsel & Secretary of Trinity Coal Corporation, a privately held mining company, from 2008 to March 2011. Trinity was acquired by the Essar Group in 2010 and commenced bankruptcy proceedings in March 2013. | |||

- 14 -

Table of Contents

| Item 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

| (a) | Market information |

Cooper Tire & Rubber Company common stock is traded on the New York Stock Exchange under the symbol CTB. The following table sets forth, for the periods indicated, the high and low sales prices of the common stock as reported in the consolidated reporting system for the New York Stock Exchange Composite Transactions:

| Year Ended December 31, 2013 | High | Low | ||||||

| First Quarter |

$ | 28.24 | $ | 24.09 | ||||

| Second Quarter |

34.79 | 23.04 | ||||||

| Third Quarter |

33.26 | 28.61 | ||||||

| Fourth Quarter |

31.49 | 20.55 | ||||||

| Year Ended December 31, 2014 | High | Low | ||||||

| First Quarter |

$ | 26.74 | $ | 21.95 | ||||

| Second Quarter |

30.10 | 23.40 | ||||||

| Third Quarter |

31.34 | 27.50 | ||||||

| Fourth Quarter |

35.31 | 27.24 | ||||||

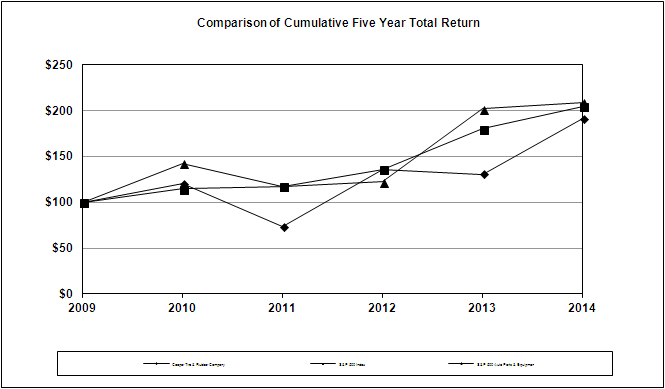

Five-Year Stockholder Return Comparison

The SEC requires that the Company include in its annual report to stockholders a line graph presentation comparing cumulative five-year stockholder returns on an indexed basis with the Standard & Poor’s (“S&P”) Stock Index and either a published industry or line-of-business index or an index of peer companies selected by the Company. The Company in 1993 chose what is now the S&P 500 Auto Parts & Equipment Index as the most appropriate of the nationally recognized industry standards and has used that index for its stockholder return comparisons in all of its annual reports since that time.

The following chart assumes three hypothetical $100 investments on December 31, 2009, and shows the cumulative values at the end of each succeeding year resulting from appreciation or depreciation in the stock market price, assuming dividend reinvestment.

- 15 -

Table of Contents

Total Return To Shareholders

(Includes reinvestment of dividends)

| ANNUAL RETURN PERCENTAGE | ||||||||||||||||||||

| Years Ending | ||||||||||||||||||||

| Company / Index |

Dec 10 | Dec 11 | Dec 12 | Dec 13 | Dec 14 | |||||||||||||||

| Cooper Tire & Rubber Company |

20.34 | -39.09 | 85.24 | -3.70 | 46.24 | |||||||||||||||

| S&P 500 Index |

15.06 | 2.11 | 16.00 | 32.39 | 13.69 | |||||||||||||||

| S&P 500 Auto Parts & Equipment |

42.78 | -17.74 | 4.45 | 64.76 | 3.68 | |||||||||||||||

| Base Period Dec 09 |

INDEXED RETURNS Years Ending |

|||||||||||||||||||||||

| Company / Index |

Dec 10 | Dec 11 | Dec 12 | Dec 13 | Dec 14 | |||||||||||||||||||

| Cooper Tire & Rubber Company |

100 | 120.34 | 73.30 | 135.77 | 130.76 | 191.22 | ||||||||||||||||||

| S&P 500 Index |

100 | 115.06 | 117.49 | 136.30 | 180.44 | 205.14 | ||||||||||||||||||

| S&P 500 Auto Parts & Equipment |

100 | 142.78 | 117.46 | 122.68 | 202.13 | 209.56 | ||||||||||||||||||

- 16 -

Table of Contents

| (b) | Holders |

The number of holders of record at December 31, 2014 was 2,004.

| (c) | Dividends |

The Company has paid consecutive quarterly dividends on its common stock since 1973. Future dividends will depend upon the Company’s earnings, financial condition and other factors. Additional information on the Company’s liquidity and capital resources can be found in “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” The Company’s retained earnings are available for the payment of cash dividends and the purchases of the Company’s shares. Quarterly dividends per common share for the most recent two years were as follows:

| 2013 | 2014 | |||||||||

| March 29 |

$ | 0.105 | March 28 |

$ | 0.105 | |||||

| June 28 |

0.105 | June 27 |

0.105 | |||||||

| September 30 |

0.105 | September 26 |

0.105 | |||||||

| December 31 |

0.105 | December 30 |

0.105 | |||||||

|

|

|

|

|

|||||||

| Total: |

$ | 0.420 | Total: |

$ | 0.420 | |||||

|

|

|

|

|

|||||||

| (d) | Issuer purchases of equity securities |

The following table sets forth a summary of the Company’s purchases during the quarter ended December 31, 2014 of equity securities registered by the Company pursuant to Section 12 of the Securities Exchange Act of 1934, as amended:

| Period |

Total Number of Shares Purchased |

Average Price Paid per Share |

Total Number of Shares Purchased as Part of Public Announced Plans or Programs (1) |

Maximum Dollar Value of Shares that May Yet Be Purchased Under the Plans or Programs (1)(2) |

||||||||||||

| October 1, 2014 through October 31, 2014 |

— | $ | — | — | $ | 40,000,000 | ||||||||||

| November 1, 2014 through November 30, 2014 |

— | $ | — | — | $ | 40,000,000 | ||||||||||

| December 1, 2014 through December 31, 2014 |

— | $ | — | — | $ | 40,000,000 | ||||||||||

|

|

|

|

|

|||||||||||||

| Total |

— | — | ||||||||||||||

| (1) | Refer to Note 14 of Notes to Condensed Consolidated Financial Statements for information regarding the Accelerated Share Repurchase program (“the ASR program”). |

| (2) | On August 6, 2014, the Board of Directors authorized the repurchase of up to $200 million of the Company’s outstanding common stock pursuant to an accelerated share repurchase program. In August 2014, the Company paid $200 million under the ASR program and received an initial delivery of 5,567,154 shares of its common stock, representing approximately 80 percent of the shares expected to be repurchased in connection with the transaction. On February 13, 2015, the Company completed its ASR program. The Company received 784,694 shares of its common stock from the ASR counterparty upon completion of the program. Shares purchased pursuant to the ASR program are presented in the above table in the periods in which they were received. The original $200 million was reduced by $160 million representing the approximately 80 percent of the shares to be repurchased that have been delivered to the Company as of December 31, 2014. |

- 17 -

Table of Contents

| Item 6. | SELECTED FINANCIAL DATA |

| (Dollar amounts in thousands except for per share amounts) | ||||||||||||||||||||||||

| Net Sales |

Operating Profit |

Income from Continuing Operations Before Income taxes |

Net Income from Continuing Operations available to Cooper Tire & Rubber Company common stockholders |

Earnings Per Share from Continuing Operations available to Cooper Tire & Rubber Company common stockholders |

||||||||||||||||||||

| Basic | Diluted | |||||||||||||||||||||||

| 2010 (a) |

3,342,708 | 188,374 | 159,826 | 116,331 | 1.90 | 1.86 | ||||||||||||||||||

| 2011 (b) |

3,907,820 | 163,301 | 134,146 | 253,503 | 4.08 | 4.02 | ||||||||||||||||||

| 2012 |

4,200,836 | 396,962 | 368,450 | 220,371 | 3.52 | 3.49 | ||||||||||||||||||

| 2013 |

3,439,233 | 240,714 | 212,971 | 111,013 | 1.75 | 1.73 | ||||||||||||||||||

| 2014 (c) |

3,424,809 | 300,458 | 348,519 | 213,578 | 3.48 | 3.42 | ||||||||||||||||||

| Stockholders’ Equity |

Redeemable Noncontrolling Shareholders’ Interests |

Long-term Debt |

Total Assets |

Net Property, Plant & Equipment |

||||||||||||||||

| 2010 |

523,050 | 71,442 | 320,724 | 2,305,537 | 824,735 | |||||||||||||||

| 2011 (b) |

697,890 | — | 329,496 | 2,509,918 | 899,044 | |||||||||||||||

| 2012 |

908,416 | — | 336,142 | 2,801,160 | 929,255 | |||||||||||||||

| 2013 |

1,157,625 | — | 320,959 | 2,738,147 | 974,269 | |||||||||||||||

| 2014 (c) |

884,261 | — | 298,931 | 2,489,931 | 740,203 | |||||||||||||||

| Capital Expenditures |

Depreciation and Amortization |

Dividends Per Share |

Average Common Shares (000s) |

Number of Employees |

||||||||||||||||

| 2010 |

119,738 | 123,721 | 0.42 | 61,299 | 12,898 | |||||||||||||||

| 2011 |

155,406 | 122,899 | 0.42 | 62,150 | 12,890 | |||||||||||||||

| 2012 |

187,336 | 128,916 | 0.42 | 62,561 | 13,550 | |||||||||||||||

| 2013 |

180,448 | 134,751 | 0.42 | 63,327 | 13,280 | |||||||||||||||

| 2014 (c) |

145,041 | 139,166 | 0.42 | 61,402 | 8,881 | |||||||||||||||

| (a) | The Company’s continuing operations recorded $20,649 of restructuring charges in 2010, associated with the closures of its Albany, Georgia manufacturing facility and other initiatives. |

| (b) | The Company’s continuing operations recorded the partial release of a valuation allowance on deferred tax assets of $167,224 during 2011. The Redeemable noncontrolling shareholders’ interests were moved to Noncontrolling shareholders’ interests in consolidated subsidiaries within Equity at December 31, 2011 when the put option held by the Company’s joint venture partner in CCT expired unexercised. |

| (c) | Reflects the sale of the Company’s ownership interest in CCT during the fourth quarter of 2014. |

- 18 -

Table of Contents

| Item 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Business of the Company

The Company specializes in the design, manufacture, marketing and sales of passenger car and light truck tires. It and its subsidiaries also sell medium truck, motorcycle and racing tires. The Company’s products are sold globally, primarily in the replacement tire market to independent tire dealers, wholesale distributors, regional and national retail tire chains and large retail chains that sell tires as well as other automotive products.

The Company faces both general industry and company-specific challenges. These include volatile raw material costs, increasing product complexity and pressure from competitors with manufacturing in lower-cost regions. To address these challenges and position the Company for future success, the Company continues to execute towards strategic imperatives outlined in its Strategic Plan. The three strategic imperatives are building a sustainable cost competitive position, driving top-line profitable growth and building organizational capabilities and enablers to support strategic goals.

In recent years, the Company expanded operations in what are considered lower-cost countries. These initiatives include the Cooper Kunshan Tire manufacturing operation in the PRC, the former CCT joint venture in the PRC (in which the Company sold its ownership interest in November 2014), a joint venture manufacturing operation in Mexico and a manufacturing facility in Serbia. Products from these operations provide a lower-cost source of tires for existing markets and have been used to expand the Company’s market share in Mexico, Eastern Europe and the PRC. Through a variety of other projects, the Company also has improved the competitiveness of its manufacturing operations in the United States.

On June 12, 2013, the Company and the Apollo entities announced the execution of the Agreement and Plan of Merger under which a wholly-owned subsidiary of the Apollo entities was to acquire the Company in an all-cash transaction valued at approximately $2.5 billion. On December 30, 2013, the Company terminated the Agreement and Plan of Merger.

On July 13, 2013, workers at CCT began a temporary work stoppage related to concerns regarding the then-pending merger between the Apollo entities and the Company. On August 17, 2013, those workers returned to work on a limited basis to manufacture only non-Cooper-branded products, but took other disruptive actions, including denying access to certain representatives of the Company and withholding certain business and financial information. Subsequent to the merger agreement termination, representatives of the Company regained access to the CCT facilities, including business and financial information and the operation resumed production of Cooper-branded products. On January 29, 2014, the Company entered into an agreement with Chengshan Group Company Ltd. (“Chengshan”) and The Union of Cooper Chengshan (Shandong) Tire Company Co., Ltd. regarding CCT that, among other matters, provided Chengshan, with certain conditions and exceptions, a limited contractual right to either (i) purchase the Company’s 65 percent equity interest in CCT or (ii) sell its 35 percent equity interest in CCT to the Company. In October 2014, the Company received the required documentation from Chengshan indicating its intent to exercise its call option under the CCT Agreement. On November 26, 2014, the Chinese State Administration for Industry & Commerce issued a new business license for CCT and on November 30, 2014, the Company completed the sale of its 65 percent ownership interest in CCT to Prairie Investment Limited, a wholly owned subsidiary of Chengshan. The Company signed off-take agreements under which CCT will continue to produce Cooper-branded products, including medium truck tires, through mid-2018.

The following discussion of financial condition and results of operations should be read together with “Selected Financial Data,” the Company’s consolidated financial statements and the notes to those statements and other financial information included elsewhere in this report.

This Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) presents information related to the consolidated results of the operations of the Company, a discussion of past results for both of the Company’s segments, future outlook for the Company and information concerning the liquidity, capital resources and critical accounting policies of the Company. The Company’s future results may differ materially from those indicated in the forward-looking statements. See Risk Factors in Item 1A for information regarding forward-looking statements.

- 19 -

Table of Contents

Consolidated Results of Operations

| (Dollar amounts in millions except per share amounts) | % | % | ||||||||||||||||||

| 2012 | Change | 2013 | Change | 2014 | ||||||||||||||||

| Revenues: |

||||||||||||||||||||

| Americas Tire |

$ | 3,095.6 | -19.7 | % | $ | 2,486.6 | 4.0 | % | $ | 2,585.5 | ||||||||||

| International Tire |

1,576.0 | -21.2 | % | 1,241.5 | -8.1 | % | 1,140.8 | |||||||||||||

| Eliminations |

(470.8 | ) | -38.6 | % | (288.9 | ) | 4.4 | % | (301.5 | ) | ||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Net sales |

$ | 4,200.8 | -18.1 | % | $ | 3,439.2 | -0.4 | % | $ | 3,424.8 | ||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Operating profit (loss): |

||||||||||||||||||||

| Americas Tire |

$ | 295.9 | -31.0 | % | $ | 204.2 | 34.6 | % | $ | 274.8 | ||||||||||

| International Tire |

143.6 | -41.5 | % | 84.0 | -11.2 | % | 74.6 | |||||||||||||

| Eliminations |

(5.7 | ) | -159.6 | % | 3.4 | -100.0 | % | — | ||||||||||||

| Unallocated corporate charges |

(36.8 | ) | 38.3 | % | (50.9 | ) | -3.7 | % | (49.0 | ) | ||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Operating profit |

397.0 | -39.4 | % | 240.7 | 24.8 | % | 300.4 | |||||||||||||

| Interest expense |

(29.5 | ) | -5.4 | % | (27.9 | ) | 0.7 | % | (28.1 | ) | ||||||||||

| Interest income |

2.5 | -68.0 | % | 0.8 | 87.5 | % | 1.5 | |||||||||||||

| Gain on sale of interest in subsidiary |

— | n/m | — | n/m | 77.5 | |||||||||||||||

| Other - net |

(1.5 | ) | -60.0 | % | (0.6 | ) | 366.7 | % | (2.8 | ) | ||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Income before income taxes |

368.5 | -42.2 | % | 213.0 | 63.6 | % | 348.5 | |||||||||||||

| Provision for income taxes |

116.0 | n/m | 79.4 | 40.7 | % | 111.7 | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Net income |

252.5 | -47.1 | % | 133.6 | 77.2 | % | 236.8 | |||||||||||||

| Noncontrolling shareholders’ interests |

(32.1 | ) | -29.6 | % | (22.6 | ) | 2.7 | % | (23.2 | ) | ||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Net income attributable to Cooper Tire & Rubber Company |

$ | 220.4 | -49.6 | % | $ | 111.0 | 92.4 | % | $ | 213.6 | ||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Basic earnings per share |

$ | 3.52 | -50.3 | % | $ | 1.75 | 98.9 | % | $ | 3.48 | ||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Diluted earnings per share |

$ | 3.49 | -50.4 | % | $ | 1.73 | 97.7 | % | $ | 3.42 | ||||||||||

|

|

|

|

|

|

|

|||||||||||||||

- 20 -

Table of Contents

2014 versus 2013

Consolidated net sales for 2014 were $3,425 million, a decrease of $14 million from 2013. The decrease in net sales was the result of less favorable pricing and mix ($260 million), offset by increased unit volumes ($288 million), which includes the recovery of $132 million in unit volumes across both segments associated with the 2013 labor issues at CCT. This volume recovery was partially offset by the reduction in unit volumes resulting from the sale of CCT in the fourth quarter of 2014 ($61 million). The International Tire Operations segment experienced favorable exchange rates in 2014 ($19 million).