Attached files

| file | filename |

|---|---|

| EX-10.6 - EXHIBIT 10.6 - PHILLIPS 66 PARTNERS LP | mlp-20141231_10xkxexhibit1.htm |

| EX-12 - EXHIBIT 12 - PHILLIPS 66 PARTNERS LP | mlp-20141231_10xkxexhibit12.htm |

| EX-23 - EXHIBIT 23 - PHILLIPS 66 PARTNERS LP | mlp-20141231_10xkxexhibit23.htm |

| EX-21 - EXHIBIT 21 - PHILLIPS 66 PARTNERS LP | mlp-20141231_10xkxexhibit21.htm |

| EX-32 - EXHIBIT 32 - PHILLIPS 66 PARTNERS LP | mlp-20141231_10xkxexhibit32.htm |

| EX-31.1 - EXHIBIT 31.1 - PHILLIPS 66 PARTNERS LP | mlp-20141231_10xkxexhibit311.htm |

| EX-31.2 - EXHIBIT 31.2 - PHILLIPS 66 PARTNERS LP | mlp-20141231_10xkxexhibit312.htm |

| EXCEL - IDEA: XBRL DOCUMENT - PHILLIPS 66 PARTNERS LP | Financial_Report.xls |

| XML - IDEA: XBRL DOCUMENT - PHILLIPS 66 PARTNERS LP | R9999.htm |

2014 | ||||

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended | December 31, 2014 |

OR

[ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from | to | ||

Commission file number: 001-36011

Phillips 66 Partners LP

(Exact name of registrant as specified in its charter)

Delaware | 38-3899432 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

3010 Briarpark Drive, Houston, Texas 77042

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (855) 283-9237

Securities registered pursuant to Section 12(b) of the Act: | ||

Title of each class | Name of each exchange on which registered | |

Common Units, Representing Limited Partnership Interests | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None | ||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | [X] Yes [ ] No | |||

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. | [ ] Yes [X] No | |||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | [X] Yes [ ] No | |||

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). | [X] Yes [ ] No | |||

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. | [X] | |||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. | ||||

Large accelerated filer [X] | Accelerated filer [ ] | Non-accelerated filer [ ] | Smaller reporting company [ ] | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). | [ ] Yes [X] No | |||

The aggregate market value of the registrant’s common units held by non-affiliates of the registrant on June 30, 2014, the last business day of the registrant’s most recently completed second fiscal quarter, based on the closing price on that date of $75.56, was $1,408 million. This figure excludes common units beneficially owned by the directors and executive officers of Phillips 66 Partners GP LLC, our General Partner, and Phillips 66 Company.

Documents incorporated by reference:

None

PHILLIPS 66 PARTNERS LP

TABLE OF CONTENTS | |

Item | Page |

Unless the context otherwise indicates, all references to “Phillips 66 Partners LP,” “the Partnership,” “us,” “our,” “we,” or similar expressions refer to Phillips 66 Partners LP, including its consolidated subsidiaries. This Annual Report on Form 10-K contains forward-looking statements including, without limitation, statements relating to our plans, strategies, objectives, expectations and intentions. The words “anticipate,” “estimate,” “believe,” “budget,” “continue,” “could,” “intend,” “may,” “plan,” “potential,” “predict,” “seek,” “should,” “will,” “would,” “expect,” “objective,” “projection,” “forecast,” “goal,” “guidance,” “outlook,” “effort,” “target” and similar expressions identify forward-looking statements. The Partnership does not undertake to update, revise or correct any forward-looking information unless required to do so under the federal securities laws. Readers are cautioned that such forward-looking statements should be read in conjunction with the Partnership’s disclosures under the heading “CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS,” beginning on page 63.

PART I

Items 1 and 2. BUSINESS AND PROPERTIES

ORGANIZATIONAL STRUCTURE

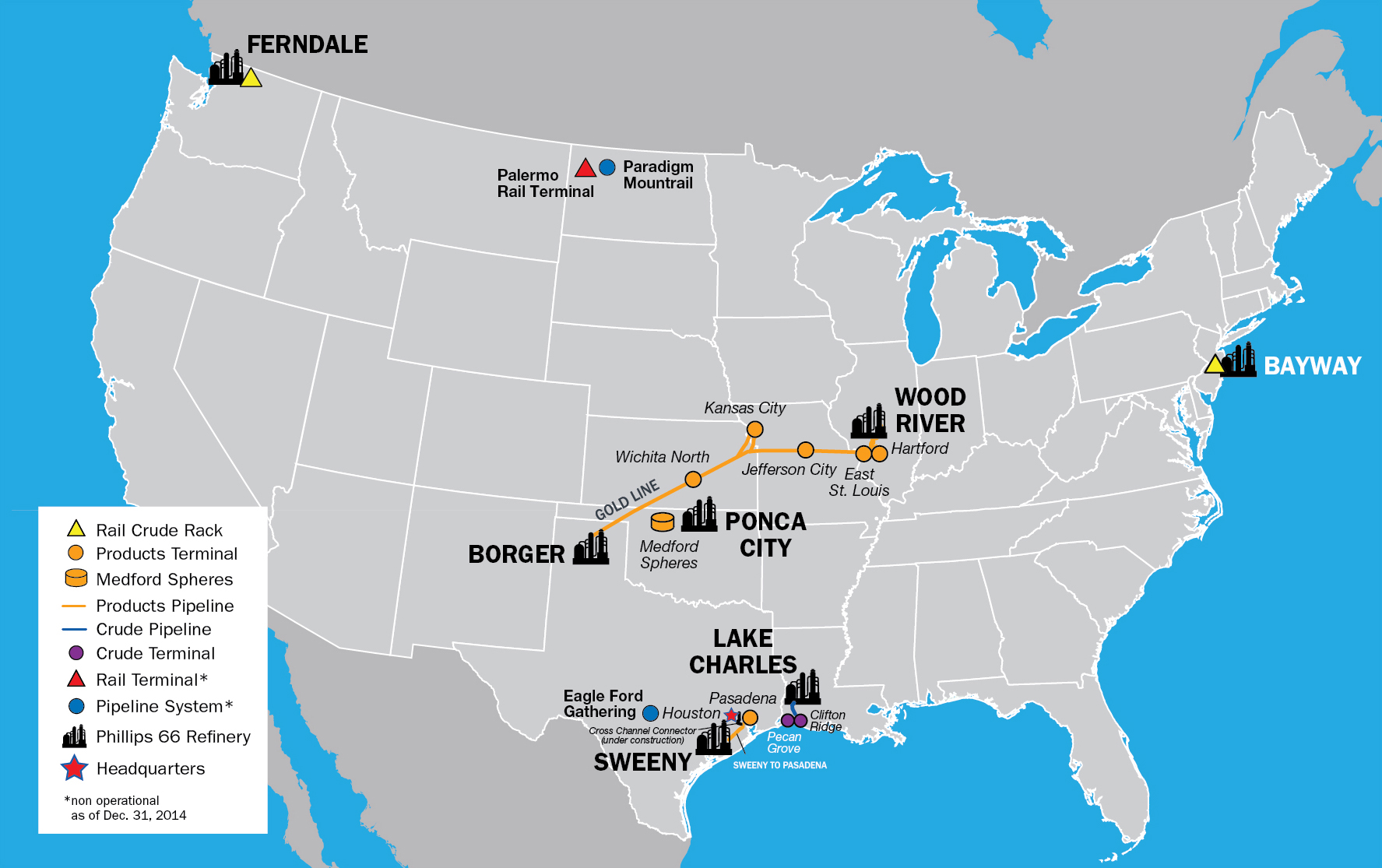

Phillips 66 Partners LP, headquartered in Houston, Texas, is a Delaware limited partnership formed in 2013 by Phillips 66 Company and Phillips 66 Partners GP LLC (our General Partner), both wholly owned subsidiaries of Phillips 66. On July 26, 2013, we completed our initial public offering (the Offering), and our common units trade on the New York Stock Exchange (NYSE) under the symbol “PSXP.” As of December 31, 2014, Phillips 66, through Phillips 66 Company, owned 20,938,498 common units and 35,217,112 subordinated units, representing an aggregate 73.3 percent limited partner interest, as well as a 100 percent interest in our General Partner, who owned 1,531,518 general partner units, representing a 2 percent general partner interest.

We are a growth-oriented master limited partnership formed by Phillips 66 to own, operate, develop and acquire primarily fee-based crude oil, refined petroleum product and natural gas liquids (NGL) pipelines, terminals and other transportation and midstream assets. Our assets consist of crude oil and refined petroleum product pipeline, terminal, rail rack and storage systems in the Central, Gulf Coast, Atlantic Basin and Western regions of the United States that are integral to the Phillips 66 refining and marketing operations they support. We generate revenue primarily by charging tariffs and fees for transporting crude oil and refined petroleum products through our pipelines and terminaling and storing crude oil and refined petroleum products at our terminals, rail racks and storage facilities. We do not take ownership of the crude oil or refined petroleum products that we transport, terminal and store, and we do not engage in the trading of any commodities. We have multiple commercial agreements with Phillips 66 that currently are the source of substantially all of our revenue. These agreements are long-term, fee-based agreements with minimum volume commitments and inflation escalators. We believe these agreements promote stable and predictable cash flows. Our operations consist of one reportable segment and are all conducted in the United States. See Item 8. Financial Statements and Supplementary Data, for financial information on our operations and assets.

2014 Developments

Gold Line/Medford Acquisition

In February 2014, we entered into a Contribution, Conveyance and Assumption Agreement with subsidiaries of Phillips 66 to acquire the Gold Line Products System and the Medford Spheres (collectively, the Gold Line/Medford Assets) from certain of those subsidiaries (the Gold Line/Medford Acquisition). The transaction closed on February 28, 2014, with an effective date of March 1, 2014.

Bayway/Ferndale/Cross-Channel Acquisition

In October 2014, we entered into a Contribution, Conveyance and Assumption Agreement with subsidiaries of Phillips 66 to acquire the Bayway and Ferndale rail racks and the Cross-Channel Connector assets (collectively, the Bayway/Ferndale/Cross-Channel Assets) from certain of those subsidiaries (the Bayway/Ferndale/Cross-Channel Acquisition). In addition, we entered into a separate Purchase and Sale Agreement (PSA) with a subsidiary of Phillips 66 to acquire assets under construction associated with the Cross-Channel Connector organic growth project. The transactions closed on December 1, 2014.

1

Palermo Rail Terminal Project Acquisition

In December 2014, we entered into a PSA and a Contribution Agreement with certain subsidiaries of Phillips 66 to acquire real property, assets under construction, lease agreements and permits associated with a rail terminal project (the Palermo Acquisition). The transactions closed on December 5, 2014, and December 10, 2014.

Eagle Ford Gathering System Project Acquisition

In December 2014, we entered into a PSA with a subsidiary of Phillips 66 to acquire real property and assets under construction associated with a gathering system project (the Eagle Ford Acquisition). The transaction closed on December 31, 2014.

Joint Ventures

In November 2014, we entered into agreements with Paradigm Energy Partners, LLC (Paradigm) to form Phillips 66 Partners Terminal LLC and Paradigm Pipeline LLC, two joint ventures established to develop the Palermo Rail Terminal, a central delivery facility and the Sacagawea Pipeline in North Dakota. The joint venture transactions closed on January 16, 2015.

For ease of reference, we refer to the Gold Line/Medford Assets, Bayway/Ferndale/Cross-Channel Assets and the assets associated with the Palermo Acquisition and Eagle Ford Acquisition collectively as “the Acquired Assets,” and the Gold Line/Medford Acquisition, Bayway/Ferndale/Cross-Channel Acquisition, Palermo Acquisition and Eagle Ford Acquisition collectively as “the Acquisitions.”

SUMMARY OF ASSETS AND OPERATIONS

At December 31, 2014, our assets consisted of the following systems:

• | Clifton Ridge Crude System. A crude oil pipeline, terminal and storage system located in Sulphur, Louisiana, that is the primary source for delivery of crude oil to Phillips 66’s Lake Charles Refinery. |

• | Sweeny to Pasadena Products System. A refined petroleum product pipeline, terminal and storage system extending from Phillips 66’s Sweeny Refinery in Old Ocean, Texas, to our refined petroleum product terminal in Pasadena, Texas, and ultimately connecting to the Explorer and Colonial refined petroleum product pipeline systems and other third-party pipeline and terminal systems. This system is the primary distribution outlet for diesel and gasoline produced at Phillips 66’s Sweeny Refinery. |

• | Hartford Connector Products System. A refined petroleum product pipeline, terminal and storage system located in Hartford, Illinois, that distributes diesel and gasoline produced at Phillips 66’s jointly owned and operated Wood River Refinery to third-party pipeline and terminal systems, including the Explorer pipeline system. |

• | Gold Line Products System. A refined petroleum product pipeline system that runs from the Phillips 66 jointly owned and operated refinery in Borger, Texas, to Cahokia, Illinois, with access to Phillips 66’s Ponca City Refinery, as well as two parallel lateral lines that run from Paola, Kansas, to Kansas City, Kansas. The system includes four terminals located at Wichita, Kansas; Kansas City, Kansas; Jefferson City, Missouri; and Cahokia, Illinois. |

• | Medford Spheres. Two refinery-grade propylene storage spheres located in Medford, Oklahoma, that commenced operations in March 2014. The Medford Spheres provide an outlet for delivery of refinery-grade propylene from Phillips 66’s Ponca City Refinery, through interconnections with third-party pipelines, to Mont Belvieu, Texas. |

• | Bayway Rail Rack. A four-track, 120-rail-car crude oil receiving facility located in Linden, New Jersey, within Phillips 66’s Bayway Refinery, which commenced operations in August 2014. The rail rack unloads crude oil and delivers it to storage tanks within the Bayway Refinery. |

2

• | Ferndale Rail Rack. A two-track, 54-rail-car crude oil receiving facility located in Ferndale, Washington, adjacent to Phillips 66’s Ferndale Refinery, which commenced operations in November 2014. The rail rack unloads crude oil and delivers it to storage tanks at the adjacent Ferndale Refinery. |

• | Cross-Channel Connector Project. A refined petroleum product pipeline originating at our Pasadena terminal in Pasadena, Texas, running to terminal facilities located at Kinder Morgan’s Pasadena terminal and its Galena Park Station in Galena Park, Texas, and terminating at the Holland Avenue Junction in Galena Park, Texas. We have undertaken an organic growth project to provide shippers with a connection from our Pasadena terminal to third-party systems with water access on the Houston Ship Channel. The entire products system is anticipated to be completed and commence operations in the second quarter of 2015. |

• | Palermo Rail Terminal Project. A project to construct a crude oil rail-loading facility in Palermo, North Dakota. The facility is designed to have an initial capacity of 100,000 barrels per day, with the flexibility to be expanded to 200,000 barrels per day. In December 2014, we purchased real property, assets under construction, lease agreements and permits associated with the rail terminal from Phillips 66. The terminal will have direct access to the Sacagawea Pipeline and provide east and west coast railway access for third-party shippers. The terminal is anticipated to be completed and in service in the fourth quarter of 2015. |

• | Eagle Ford Gathering System Project. A project to construct a crude oil gathering system that will consist of two pipelines and a storage facility near Helena and Tilden, Texas. The gathering system is designed to connect Eagle Ford production to third party pipelines. In December 2014, we purchased real property and assets under construction associated with the gathering system project from Phillips 66. The entire gathering system is anticipated to be completed and commence operations in the third quarter of 2015. |

3

Pipeline Assets

The following table sets forth certain information regarding our pipeline assets as of December 31, 2014. Except for the Cross-Channel Connector Pipeline, each asset listed below currently has an associated commercial agreement with Phillips 66:

System Name | Diameter | Length (Miles) | Active Throughput Capacity (Thousands of Barrels Daily) | Commodity Handled | Associated Phillips 66 Refinery | Significant Third-Party Pipeline System Connections | ||||||||

Clifton Ridge Crude System | ||||||||||||||

Clifton Ridge to Lake Charles Refinery | 20” | 10 | 260 | Crude Oil | Lake Charles | Shell Houston-to-Houma | ||||||||

Pecan Grove to Clifton Ridge | 12” | 0.6 | 56 | Crude Oil | Lake Charles | N/A | ||||||||

Shell to Clifton Ridge | 20” | 0.6 | 312 | Crude Oil | Lake Charles | Shell Houston-to-Houma | ||||||||

Sweeny to Pasadena Products System | ||||||||||||||

Sweeny Refinery to Pasadena, Texas | 12” | 60 | 125 | Refined Petroleum Products | Sweeny | Explorer; Colonial | ||||||||

Sweeny Refinery to Pasadena, Texas | 18” | 60 | 138 | Refined Petroleum Products | Sweeny | Colonial | ||||||||

Hartford Connector Products System | ||||||||||||||

Wood River Refinery to Hartford, Illinois | 12” | 3 | 80 | Refined Petroleum Products | Wood River | Explorer | ||||||||

Hartford, Illinois to Explorer Pipeline | 24” | 1 | 430 | Refined Petroleum Products | Wood River | Explorer | ||||||||

Gold Line Products System | ||||||||||||||

Borger Refinery to Wichita, Kansas | 16” | 273 | 120 | Refined Petroleum Products | Borger | NuStar | ||||||||

Wichita, Kansas to Paola, Kansas | 16” | 143 | 132 | Refined Petroleum Products | Borger/ Ponca City | NuStar | ||||||||

Paola, Kansas to East St. Louis, Illinois | 8”-12” | 265 | 53 | Refined Petroleum Products | Borger/ Ponca City | Explorer; Buckeye | ||||||||

Paola, Kansas to Kansas City, Kansas | 8” | 53 | 24 | Refined Petroleum Products | Borger/ Ponca City | Magellan | ||||||||

Paola, Kansas to Kansas City, Kansas | 10” | 53 | 72 | Refined Petroleum Products | Borger/ Ponca City | Magellan | ||||||||

Cross-Channel Connector Pipeline | 20” | 2.5 | 120 | Refined Petroleum Products | Sweeny | Kinder Morgan | ||||||||

4

Terminal, Rail Rack and Storage Assets

The following table sets forth certain information regarding our terminal, rail rack and storage assets as of December 31, 2014, each of which currently has an associated commercial agreement with Phillips 66:

System Name | Tank Shell Storage Capacity (Thousands of Barrels) | Active Terminaling Capacity* (Thousands of Barrels Daily) | Commodity Handled | Associated Phillips 66 Refinery | Significant Third-Party Pipeline System Connections | |||||||

Clifton Ridge Crude System | ||||||||||||

Clifton Ridge Terminal | 3,410 | 12 | Crude Oil | Lake Charles | Shell Houston-to-Houma | |||||||

Pecan Grove Storage | 142 | N/A | Crude Oil | Lake Charles | N/A | |||||||

Sweeny to Pasadena Products System | ||||||||||||

Pasadena Terminal | 3,210 | 65 | Refined Petroleum Products | Sweeny | Explorer; Colonial | |||||||

Hartford Connector Products System | ||||||||||||

Hartford Terminal | 1,075 | 25 | Refined Petroleum Products | Wood River | Explorer | |||||||

Gold Line Products System | ||||||||||||

East St. Louis Terminal | 2,245 | 78 | Refined Petroleum Products | Borger/ Ponca City | Explorer; Buckeye | |||||||

Jefferson City Terminal | 110 | 16 | Refined Petroleum Products | Borger/ Ponca City | N/A | |||||||

Kansas City Terminal | 1,294 | 66 | Refined Petroleum Products | Borger/ Ponca City | Magellan | |||||||

Wichita North Terminal | 679 | 19 | Refined Petroleum Products | Borger/ Ponca City | NuStar | |||||||

Medford Spheres | 70 | N/A | Refined Petroleum Products | Ponca City | Sterling | |||||||

Bayway Rail Rack | N/A | 75 | Crude Oil | Bayway | N/A | |||||||

Ferndale Rail Rack | N/A | 30 | Crude Oil | Ferndale | N/A | |||||||

Marine Assets

The following table sets forth certain information regarding our marine assets as of December 31, 2014, each of which currently has an associated commercial agreement with Phillips 66:

System Name | Dock Throughput Capacity (Thousands of Barrels Hourly) | Commodity Handled | Associated Phillips 66 Refinery | |||

Clifton Ridge Crude System | ||||||

Clifton Ridge Ship Dock | 48 | Crude Oil | Lake Charles | |||

Pecan Grove Barge Dock | 6 | Crude Oil; Lubricant Base Stocks | Lake Charles | |||

Hartford Connector Products System | ||||||

Hartford Barge Dock | 3 | Dyed Diesel; Naphtha; Lubricant Base Stocks | Wood River | |||

5

The following table sets forth the percentage of the referenced Phillips 66 refinery’s supply/production volumes that were delivered by or distributed on our systems for each of the periods set forth below:

Percentage of Volumes Transported

Year Ended December 31 | |||||||

2014 | 2013 | 2012 | |||||

Lake Charles Refinery | |||||||

Clifton Ridge crude pipelines | 97 | % | 93 | 90 | |||

Sweeny Refinery | |||||||

Sweeny to Pasadena products pipelines | 100 | % | 98 | 100 | |||

Wood River Refinery | |||||||

Hartford Connector products pipelines | 20 | % | 18 | 17 | |||

Borger Refinery | |||||||

Gold Line products pipelines | 41 | % | 47 | 40 | |||

Ponca City Refinery | |||||||

Gold Line products pipelines | 20 | % | 13 | 17 | |||

6

ASSET PORTFOLIO

Clifton Ridge Crude System

Our Clifton Ridge Crude System is strategically positioned to support flexible crude oil supply options for Phillips 66’s Lake Charles Refinery in Westlake, Louisiana. Our Clifton Ridge Crude System consists of the following pipelines and terminals:

• | Clifton Ridge terminal. Our Clifton Ridge terminal is located on the Calcasieu River approximately ten miles from the Lake Charles Refinery. The facility consists of a single-berth ship dock with an average ship delivery of 512,000 barrels at a flow rate of 48,000 barrels per hour, 12 above-ground storage tanks with approximately 3.4 million barrels of total storage capacity and a truck offloading facility. The Clifton Ridge terminal receives crude oil by pipeline, barge, tanker, and truck; stores crude oil in its storage tanks; and delivers crude oil to the Lake Charles Refinery through our Clifton Ridge to Lake Charles refinery pipeline. |

• | Pecan Grove terminal. Our Pecan Grove terminal is located on the Calcasieu River adjacent to our Clifton Ridge terminal. The facility consists of a single-berth barge dock with an average barge delivery of 33,000 barrels at a flow rate of 3,500 to 6,000 barrels per hour and three above-ground storage tanks with 142,000 barrels of total storage capacity. The Pecan Grove terminal receives crude oil and lubricant base stocks delivered to the terminal by barge, and delivers crude oil to the Lake Charles Refinery through our Clifton Ridge terminal and lubricant base stocks to Phillips 66’s lubricant blending facility located adjacent to the terminal. |

• | Clifton Ridge to Lake Charles refinery pipeline. Our Clifton Ridge to Lake Charles refinery crude oil pipeline consists of approximately 10 miles of 20-inch pipeline that delivers crude oil from the Clifton Ridge terminal to the Lake Charles Refinery. The pipeline has a total capacity of 260,000 barrels per day. |

• | Pecan Grove to Clifton Ridge pipeline. Our Pecan Grove to Clifton Ridge crude oil pipeline consists of approximately 0.6 miles of 12-inch pipeline that delivers crude oil bi-directionally between the Pecan Grove terminal and the Clifton Ridge terminal. The pipeline has a total capacity of 56,000 barrels per day. |

• | Shell to Clifton Ridge pipeline. Our Shell to Clifton Ridge crude oil pipeline consists of approximately 0.6 miles of 20-inch pipeline that delivers crude oil from the Shell Houston-to-Houma crude oil pipeline to the Clifton Ridge terminal. The Shell to Clifton Ridge crude oil pipeline has a total capacity of 312,000 barrels per day. |

Sweeny to Pasadena Products System

Our Sweeny to Pasadena Products System is strategically positioned to transport refined petroleum products from Phillips 66’s Sweeny Refinery in Old Ocean, Texas, to major third-party interstate pipeline systems, including the Explorer and Colonial refined petroleum product pipeline systems. The Explorer and Colonial pipeline systems are two major interstate pipeline systems that transport refined petroleum products from the Gulf Coast to marketing terminals throughout the Midwestern, Southeastern and Northeastern regions of the United States.

Our Sweeny to Pasadena Products System consists of the following pipelines and terminal:

• | Sweeny to Pasadena pipelines. Our Sweeny to Pasadena pipelines consist of approximately 60 miles of 12-inch pipeline that delivers gasoline and approximately 60 miles of 18-inch pipeline that delivers diesel from the Sweeny Refinery to our Pasadena terminal, as well as a pump station located at the Sweeny Refinery. The active capacity of the 12-inch pipeline and the 18-inch pipeline is 125,000 barrels per day and 138,000 barrels per day, respectively. |

• | Pasadena terminal. Our Pasadena terminal is located in Pasadena, Texas, and consists of a five-bay truck rack with 65,000 barrels per day of active terminaling capacity, 22 above-ground storage tanks with approximately 3.2 million barrels of total storage capacity and a vapor combustion unit. The terminal delivers refined petroleum products, including distillate and gasoline, to third-party pipeline systems, including the Explorer, Colonial, Enterprise, Chevron, Magellan Midstream and Kinder Morgan refined petroleum product pipeline systems, as well as local terminals. |

7

Hartford Connector Products System

Our Hartford Connector Products System is strategically positioned to transport refined petroleum products that are produced at the Wood River Refinery (a refinery jointly owned by Phillips 66 and Cenovus Energy Inc.) in Roxana, Illinois, to major third-party interstate pipeline systems, including the Explorer refined petroleum product pipeline system. We also receive refined petroleum products into our Hartford Connector Products System for delivery to marketing outlets through third-party pipeline systems.

Our Hartford Connector Products System consists of the following pipelines and terminal:

• | Wood River to Hartford pipeline. Our Wood River to Hartford pipeline consists of approximately three miles of 12-inch pipeline that delivers diesel and gasoline produced at the Wood River Refinery to our Hartford terminal. The 12-inch pipeline has a total capacity of 80,000 barrels per day. |

• | Hartford terminal. Our Hartford terminal is located in Hartford, Illinois, approximately three miles from the Wood River Refinery. The facility consists of a three-bay diesel truck rack with an active capacity of 25,000 barrels per day and 13 above-ground storage tanks with a total storage capacity of approximately 1.1 million barrels. The Hartford terminal delivers diesel, gasoline and jet fuel to the Explorer refined petroleum product pipeline system through a direct pipeline connection to Explorer pipeline and delivers diesel, gasoline and naphtha to, and receives lubricant base stocks from, barges through our interconnecting pipelines to our Hartford barge dock. |

• | Hartford to Explorer pipeline. Our Hartford to Explorer pipeline consists of approximately one mile of 24-inch pipeline that delivers refined petroleum products from the Hartford terminal to the Explorer refined petroleum product pipeline system. The pipeline has a total capacity of 430,000 barrels per day. |

• | Hartford barge dock. Our Hartford barge dock is located on the Mississippi River approximately one mile from our Hartford terminal. Our Hartford barge dock consists of a single-berth barge loading facility with an average barge loading of 13,000 barrels at an average flow rate of 3,000 barrels per hour, approximately 0.8 miles of 8-inch pipeline that transports lubricant base stocks and diesel, and approximately 0.8 miles of 14-inch pipeline that delivers diesel and naphtha from our Hartford terminal to the Hartford barge dock for delivery to third-party vessels. |

Gold Line Products System

Our Gold Line Products System is strategically positioned to transport refined petroleum products that are produced at the Borger Refinery (a refinery jointly owned by Phillips 66 and Cenovus Energy Inc.) in Borger, Texas, to major third-party interstate pipeline systems, including the Explorer refined petroleum product pipeline system, and also to four terminals located in Wichita, Kansas, Kansas City, Kansas, Jefferson City, Missouri, and Cahokia, Illinois, with access to Phillips 66’s Ponca City Refinery.

Our Gold Line Products System consists of the following pipelines and terminals:

• | Borger Refinery to Wichita pipeline. Our Borger to Wichita pipeline consists of approximately 273 miles of 16-inch pipeline that delivers diesel and gasoline produced at the Borger Refinery to our Wichita North terminal. The 16-inch pipeline has a total capacity of 120,000 barrels per day. |

• | Wichita to Paola pipeline. Our Wichita to Paola pipeline consists of approximately 143 miles of 16-inch pipeline with a connection to receive refined petroleum products from the Ponca City Refinery via the Phillips 66-owned Standish pipeline. The 16-inch pipeline has a total capacity of 132,000 barrels per day. |

• | Paola to East St. Louis pipeline. Our Paola to East St. Louis pipeline consists of approximately 265 miles of 8- to 12-inch pipeline that delivers diesel and gasoline to our Jefferson City and East St. Louis terminals. The pipeline has a total capacity of 53,000 barrels per day. |

• | Paola to Kansas City pipelines. Our Paola to Kansas City pipelines consist of two parallel 53-mile lateral lines that run from Paola, Kansas, to Kansas City, Kansas. These 8-inch and 10-inch pipelines have a total aggregate capacity of 96,000 barrels per day. |

8

• | East St. Louis terminal. Our East St. Louis terminal is located in Cahokia, Illinois, approximately 681 miles from the Borger Refinery. The facility consists of a six-bay truck rack with an active capacity of 78,000 barrels per day and 19 above-ground storage tanks with a total storage capacity of approximately 2.2 million barrels. The East St. Louis terminal delivers diesel, gasoline and jet fuel to the Explorer and Buckeye refined petroleum product pipeline systems through a direct pipeline connection. |

• | Jefferson City terminal. Our Jefferson City terminal is located in Jefferson City, Missouri. The facility consists of a two-bay truck rack with an active capacity of 16,000 barrels per day and 8 above-ground storage tanks with a total storage capacity of approximately 110,000 barrels. |

• | Kansas City terminal. Our Kansas City terminal is located in Kansas City, Kansas, approximately 469 miles from the Borger Refinery. The facility consists of a five-bay truck rack with an active capacity of 66,000 barrels per day and 17 above-ground storage tanks with a total storage capacity of approximately 1.3 million barrels. The Kansas City terminal delivers diesel, gasoline and jet fuel to the Magellan refined petroleum product pipeline system through a direct pipeline connection. |

• | Wichita North terminal. Our Wichita North terminal is located in Wichita, Kansas, approximately 273 miles from the Borger Refinery. The facility also receives refined petroleum products from the Ponca City Refinery via the Phillips 66-owned Standish pipeline. The facility consists of a two-bay truck rack with an active capacity of 19,000 barrels per day and 19 above-ground storage tanks with a total storage capacity of approximately 679,000 barrels. The Wichita North terminal delivers diesel, gasoline and jet fuel to the NuStar refined petroleum product pipeline system through a direct pipeline connection. |

Medford Spheres

Our Medford Spheres provide an outlet for delivery of refinery-grade propylene from the Ponca City Refinery, through interconnections with third-party pipelines, to Mont Belvieu, Texas. The two refinery-grade propylene storage spheres are located in Medford, Oklahoma, and have a total aggregate working capacity of 70,000 barrels. Medford Spheres commenced operations in March 2014.

Bayway Rail Rack

Our Bayway Rail Rack is located in Linden, New Jersey, within the Bayway Refinery. The rail rack consists of a four-track crude oil receiving facility with a rail unloading capacity of 75,000 barrels per day. The facility commenced commercial operations in August 2014 and is capable of unloading 120 railcars simultaneously.

Ferndale Rail Rack

Our Ferndale Rail Rack is located in Ferndale, Washington, adjacent to the Ferndale Refinery. The rail rack consists of a two-track crude oil receiving facility with a rail unloading capacity of 30,000 barrels per day. The facility commenced commercial operations in November 2014 and is capable of unloading 54 railcars simultaneously.

Cross-Channel Connector Project

Our Cross-Channel Connector project is a 20-inch refined products pipeline originating at our Pasadena terminal, running to terminal facilities located at Kinder Morgan’s Pasadena terminal and its Galena Park station in Galena Park, Texas, and terminating at the Holland Avenue Junction in Galena Park, Texas. We have undertaken an organic growth project to provide shippers with a connection from the Pasadena terminal to third-party systems with water access on the Houston Ship Channel. The pipeline system will have an initial capacity of up to 180,000 barrels per day and is anticipated to be completed and commence operations in the second quarter of 2015.

9

Bakken Joint Ventures

In January 2015, we closed on our joint venture transactions with Paradigm to develop and operate midstream logistics infrastructure in the Bakken region of North Dakota:

• | Phillips 66 Partners Terminal LLC. We contributed the Palermo Rail Terminal project to the terminal joint venture, Phillips 66 Partners Terminal LLC, in exchange for a 70 percent interest, with Paradigm owning the remaining 30 percent interest. The Palermo Rail Terminal is a crude oil rail-loading facility currently under construction on a 710-acre site near Palermo, North Dakota. The terminal will have an initial capacity of 100,000 barrels per day, with the flexibility to be expanded to 200,000 barrels per day. It is located on a railway main line with two mainline switches, allowing east- and west-bound rail traffic. The terminal is anticipated to include a pipeline delivery and receipt connection to the Sacagawea Pipeline, allowing the terminal to receive crude oil from areas in Dunn and McKenzie County, North Dakota, and deliver it to terminals and pipelines located in Stanley, North Dakota. The terminal will also include adequate space for up to 12 truck unloading facilities and approximately 300,000 barrels of operational storage, with permits allowing total storage capacity of up to 2.4 million barrels. We are constructing and will operate the terminal. The terminal is anticipated to be completed and in service in the fourth quarter of 2015. |

• | Paradigm Pipeline LLC. We and Paradigm each own a 50 percent interest in the pipeline joint venture, Paradigm Pipeline LLC. The pipeline joint venture will own an 88 percent interest in Sacagawea Pipeline Company, LLC, the owner of the Sacagawea Pipeline, with the remaining 12 percent interest owned by Grey Wolf Midstream, LLC. The pipeline joint venture will also construct and own a crude oil storage terminal and a central delivery facility for various crude gathering systems located in Keene, North Dakota (the Paradigm CDP). The Sacagawea Pipeline project is a 76-mile pipeline being developed to deliver crude oil from various points in and around Johnson’s Corner and the Paradigm CDP, located in McKenzie County, North Dakota, to destinations with take away options for both rail and pipeline in Palermo and Stanley, North Dakota. Paradigm is constructing the pipeline and we will be the operator. The pipeline is anticipated to commence operations in the fourth quarter of 2015. |

Eagle Ford Gathering System Project

Our Eagle Ford Gathering System is a crude oil gathering system, currently under construction, that will consist of two pipelines and a storage facility near Helena and Tilden, Texas. The gathering system is designed to connect Eagle Ford production to third-party pipelines. The pipelines will include a 6-inch, 6-mile crude oil pipeline near Helena and a 10-inch, 17-mile crude oil pipeline near Tilden with 7 origination/injection points. The storage facility, located in Tilden, will have a capacity of 90,000 barrels with an injection point into a third-party pump station. The Helena portion of the gathering system began operations in January 2015, and the entire gathering system is anticipated to be completed and in service in the third quarter of 2015, upon commencement of operations at the Tilden section of the gathering system. In January 2015, we entered into a throughput and deficiency agreement with Phillips 66, which provides minimum volume commitments on the gathering system when each portion of the system is completed and in service.

10

COMMERCIAL AND OTHER AGREEMENTS WITH PHILLIPS 66

Our assets are physically connected to, and integral to the operation of, Phillips 66’s wholly owned Lake Charles, Sweeny, Ponca City, Bayway and Ferndale refineries and its jointly owned Wood River and Borger refineries. In connection with the Offering and the Acquisitions, we entered into multiple commercial agreements with Phillips 66, and amended an existing commercial agreement with Phillips 66, which include minimum volume commitments and inflation escalators. Currently, those agreements are the source of a significant portion of our revenue. Under these long-term, fee-based agreements, we provide transportation, terminaling and storage services to Phillips 66, and Phillips 66 commits to provide us with minimum quarterly volumes of crude oil and refined petroleum products.

The following table sets forth minimum commitment information regarding our commercial agreements with Phillips 66 as of December 31, 2014.

Agreement | Phillips 66 Minimum Volume Commitment (Thousands of Barrels Daily)(1) | Phillips 66 Capacity Reservation (Thousands of Barrels Daily) | ||||

Transportation Services Agreements | ||||||

Clifton Ridge Transportation Services Agreement | ||||||

Clifton Ridge to Lake Charles refinery pipeline | 190 | — | ||||

Sweeny to Pasadena Transportation Services Agreement | ||||||

Sweeny to Pasadena pipelines | 200 | — | ||||

Hartford Connector Throughput and Deficiency Agreement | ||||||

Wood River refinery to Hartford pipeline(2) | 43 | 12.2 | ||||

Hartford to Explorer pipeline(2) | 16 | 39.2 | ||||

Gold Line Transportation Services Agreement | ||||||

Borger refinery to Wichita pipeline | 54 | — | ||||

Wichita to Kansas City pipeline | 45 | — | ||||

Wichita to Jefferson City pipeline | 7 | — | ||||

Wichita to East St. Louis Pipeline | 10 | — | ||||

Terminal and Storage Services Agreements | ||||||

Clifton Ridge Terminal Services Agreement | ||||||

Clifton Ridge terminal storage | 190 | — | ||||

Clifton Ridge ship dock / Pecan Grove barge dock | 150 | — | ||||

Hartford and Pasadena Terminal Services Agreement | ||||||

Pasadena terminal | 135 | — | ||||

Pasadena and Hartford terminal truck racks | 55 | — | ||||

Gold Line Terminal Services Agreement | ||||||

Wichita North, Kansas City, Jefferson City and East St. Louis terminals truck racks | 80 | — | ||||

Gold Line Storage Services Agreement | ||||||

Wichita North, Kansas City and East St. Louis terminals(3) | 1,010 | — | ||||

Medford Spheres Storage Services Agreement | ||||||

Medford Spheres(3) | 70 | — | ||||

Bayway Terminal Services Agreement | ||||||

Bayway Rail Rack(3) | 75 | — | ||||

Ferndale Terminal Services Agreement | ||||||

Ferndale Rail Rack(3) | 30 | — | ||||

(1)Includes capacity-based monthly fee arrangements.

(2)Total volume commitment includes both Phillips 66 minimum volume commitment and Phillips 66 capacity reservation.

(3)Capacity upon which minimum monthly fee is calculated.

11

See the “Commercial Agreements,” “Amended Operational Services Agreement,” “Amended Omnibus Agreement” and “Tax Sharing Agreement” sections of Note 18—Related Party Transactions, in the Notes to Consolidated Financial Statements, for summaries of the terms of these and other agreements with Phillips 66.

COMPETITION

As a result of our contractual relationship with Phillips 66 under our commercial agreements and our direct connections to Phillips 66’s owned or operated refineries, we believe that our crude oil and refined petroleum product pipelines, terminals and storage facilities will not face significant competition from other pipelines, terminals and storage facilities for Phillips 66’s crude oil or refined petroleum product transportation requirements to and from the refineries we support. If Phillips 66’s customers were to reduce their purchases of refined petroleum products from Phillips 66, Phillips 66 might only ship the minimum volumes through our pipelines (or pay the shortfall payment if it does not ship the minimum volumes), which would cause a decrease in our revenue. Phillips 66 competes with integrated petroleum companies, which have their own crude oil supplies and distribution and marketing systems, as well as with independent refiners, many of which also have their own distribution and marketing systems. Phillips 66 also competes with other suppliers that purchase refined petroleum products for resale. Competition in any particular geographic area is affected significantly by the volume of products produced by refineries in that area and by the availability of products and the cost of transportation to that area from distant locations.

RATES AND OTHER REGULATIONS

Our common carrier pipeline systems are subject to regulation by various federal, state and local agencies. The Federal Energy Regulatory Commission (FERC) regulates interstate transportation on our common carrier pipeline systems under the Interstate Commerce Act (ICA), the Energy Policy Act of 1992 (EPAct 1992) and the rules and regulations promulgated under those laws. FERC regulations require that rates for interstate service pipelines that transport crude oil and refined petroleum products (collectively referred to as “petroleum pipelines”) and certain other liquids be just and reasonable and must not be unduly discriminatory or confer any undue preference upon any shipper. FERC regulations also require interstate common carrier petroleum pipelines to file with FERC and publicly post tariffs stating their interstate transportation rates and terms and conditions of service. Under the ICA, FERC or interested persons may challenge existing or changed rates or services. FERC is authorized to investigate such charges and may suspend the effectiveness of a new rate for up to seven months. A successful rate challenge could result in a common carrier paying refunds together with interest for the period that the rate was in effect. FERC may also order a pipeline to change its rates, and may require a common carrier to pay shippers reparations for damages sustained for a period up to two years prior to the filing of a complaint. EPAct 1992 deemed certain interstate petroleum pipeline rates then in effect to be just and reasonable under the ICA. These rates are commonly referred to as “grandfathered rates.” Our rates in effect at the time of the passage of EPAct 1992 for interstate transportation service were deemed just and reasonable and therefore are grandfathered. New rates have since been established after EPAct 1992 for certain pipeline systems. FERC may change grandfathered rates upon complaint only after it is shown that:

• | A substantial change has occurred since enactment in either the economic circumstances or the nature of the services that were a basis for the rate. |

• | The complainant was contractually barred from challenging the rate prior to enactment of EPAct 1992 and filed the complaint within 30 days of the expiration of the contractual bar. |

• | A provision of the tariff is unduly discriminatory or preferential. |

EPAct 1992 required FERC to establish a simplified and generally applicable methodology to adjust tariff rates for inflation for interstate petroleum pipelines. As a result, FERC adopted an indexing rate methodology which, as currently in effect, allows common carriers to change their rates within prescribed ceiling levels that are tied to changes in the Producer Price Index (PPI) for finished goods. FERC’s indexing methodology is subject to review every five years. During the five-year period commencing July 1, 2011, and ending June 30, 2016, common carriers charging indexed rates are permitted to adjust their indexed ceilings annually by PPI plus 2.65 percent. The indexing methodology is applicable to existing rates, including grandfathered rates, with the exclusion of market-based rates. A pipeline is not

12

required to raise its rates up to the index ceiling, but it is permitted to do so and rate increases made under the index are presumed to be just and reasonable unless a protesting party can demonstrate that the portion of the rate increase resulting from application of the index is substantially in excess of the pipeline’s increase in costs. Under the indexing rate methodology, in any year in which the index is negative, pipelines must file to lower their rates if those rates would otherwise be above the rate ceiling.

While common carriers often use the indexing methodology to change their rates, they may elect to support proposed rates by using other methodologies such as cost-of-service rate making, market-based rates and settlement rates. A pipeline can follow a cost-of-service approach when seeking to increase its rates above the rate ceiling (or when seeking to avoid lowering rates to the reduced rate ceiling). A common carrier can charge market-based rates if it establishes that it lacks significant market power in the affected markets. In addition, a common carrier can establish rates under settlement if agreed upon by all current shippers. We have used indexed rates and settlement rates for our different pipeline systems. If we used cost-of-service rate making to establish or support our rates, the issue of the proper allowance for federal and state income taxes could arise. In 2005, FERC issued a policy statement stating that it would permit common carriers, among others, to include an income tax allowance in cost-of-service rates to reflect actual or potential tax liability attributable to a regulated entity’s operating income, regardless of the form of ownership. Under FERC’s policy, a tax pass-through entity seeking such an income tax allowance must establish that its partners or members have an actual or potential income tax liability on the regulated entity’s income. Whether a pipeline’s owners have such actual or potential income tax liability is subject to review by FERC on a case-by-case basis. Although this policy is generally favorable for common carriers that are organized as pass-through entities, it still entails rate risk due to the FERC’s case-by-case review approach. The application of this policy, as well as any decision by FERC regarding our cost of service, may also be subject to review in the courts. Intrastate services provided by certain of our pipeline systems are subject to regulation by state regulatory authorities. These state regulatory authorities use a complaint-based system of regulation, both as to matters involving rates and priority of access. State regulatory authorities could limit our ability to increase our rates or to set rates based on our costs or order us to reduce our rates and require the payment of refunds to shippers. FERC and state regulatory authorities generally have not investigated rates, unless the rates are the subject of a protest or a complaint. Phillips 66 has agreed not to contest our tariff rates applicable for our transportation services agreements entered into in connection with the Offering and the Acquisitions for the term of those agreements. However, FERC or a state regulatory authority could investigate our rates on its own initiative or at the urging of a third party, and this could lead to a refund of previously collected revenue.

Pipeline Safety

Our assets are subject to increasingly strict safety laws and regulations. The transportation and storage of crude oil and refined petroleum products involves a risk that hazardous liquids may be released into the environment, potentially causing harm to the public or the environment. In turn, any such incidents may result in substantial expenditures for response actions, significant government penalties, liability to government agencies for natural resources damages, and significant business interruption. The United States Department of Transportation (DOT) has adopted safety regulations with respect to the design, construction, operation, maintenance, inspection and management of our assets. These regulations contain requirements for the development and implementation of pipeline integrity management programs, which include the inspection and testing of pipelines and necessary maintenance or repairs. These regulations also require that pipeline operation and maintenance personnel meet certain qualifications and that pipeline operators develop comprehensive spill response plans. We are subject to regulation by the DOT under the Hazardous Liquid Pipeline Safety Act of 1979 (the HLPSA). The HLPSA delegated to DOT the authority to develop, prescribe, and enforce minimum federal safety standards for the transportation of hazardous liquids by pipeline. Congress also enacted the Pipeline Safety Act of 1992 (the PSA), which added the environment to the list of statutory factors that must be considered in establishing safety standards for hazardous liquid pipelines, required regulations be issued to define the term “gathering line” and establish safety standards for certain “regulated gathering lines,” and mandated that regulations be issued to establish criteria for operators to use in identifying and inspecting pipelines located in High Consequence Areas (HCAs), defined as those areas that are unusually sensitive to environmental damage, that cross a navigable waterway, or that have a high population density. In 1996, Congress enacted the Accountable Pipeline Safety and Partnership Act (the APSPA), which limited the operator identification requirement mandate to pipelines that cross a waterway where a substantial likelihood of commercial navigation exists, required that certain areas where a pipeline rupture would likely cause permanent or long-term environmental damage be considered in determining whether an area is unusually sensitive to environmental damage, and mandated that regulations be issued for the qualification and testing of certain pipeline personnel. In the Pipeline Inspection, Protection, Enforcement, and Safety Act of 2006 (the PIPES Act), Congress required mandatory inspections for certain U.S. crude oil and natural gas transmission pipelines in HCAs

13

and mandated that regulations be issued for low-stress hazardous liquid pipelines and pipeline control room management. We are also subject to the Pipeline Safety, Regulatory Certainty and Job Creation Act of 2011, which reauthorized funding for federal pipeline safety programs through 2015, increased penalties for safety violations, established additional safety requirements for newly constructed pipelines, and required studies of certain safety issues that could result in the adoption of new regulatory requirements for existing pipelines.

DOT’s Pipeline and Hazardous Materials Safety Administration (PHMSA) administers compliance with these statutes and has promulgated comprehensive safety standards and regulations for the transportation of hazardous liquid by pipeline, including regulations for the design and construction of new pipeline systems or those that have been relocated, replaced, or otherwise changed; pressure testing of new pipelines; operation and maintenance of pipeline systems, including inspecting and reburying pipelines in the Gulf of Mexico and its inlets, establishing programs for public awareness and damage prevention, managing the integrity of pipelines in HCAs, and managing the operation of pipeline control rooms; protection of steel pipelines from the adverse effects of internal and external corrosion; and integrity management requirements for pipelines in HCAs. In addition, in 2010, PHMSA issued an advance notice of proposed rulemaking on a range of topics relating to the safety of crude oil and other hazardous liquids pipelines. Among other items, the advance notice of proposed rulemaking requested comment on whether to extend regulation to certain pipelines currently exempt from federal safety regulations; whether to extend integrity management regulations to additional pipelines outside of HCAs; and whether to require leak detection outside of HCAs. PHMSA has not yet taken further action on the issues raised in the advance notice of proposed rulemaking. We do not anticipate that we would be impacted by these regulatory initiatives to any greater degree than other similarly situated competitors. In addition, PHMSA has published an advisory bulletin providing guidance on verification of records related to pipeline maximum operating pressure. PHMSA is considering a rulemaking on this topic referred to as the Integrity Verification Process. We have performed hydrostatic tests of our facilities to confirm the maximum operating pressure and do not expect that any final rulemaking by PHMSA regarding verification of maximum operating pressure would materially affect our operations or revenue.

We monitor the structural integrity of our pipelines through a program of periodic internal assessments using high resolution internal inspection tools, as well as hydrostatic testing and direct assessment that conforms to federal standards. We accompany these assessments with a review of the data and repair anomalies, as required, to ensure the integrity of the pipeline. We then utilize sophisticated risk algorithms and a comprehensive data integration effort to ensure that the highest-risk pipelines receive the highest priority for scheduling subsequent integrity assessments. We use external coatings and impressed-current cathodic protection systems to protect against external corrosion. We conduct all cathodic protection work in accordance with National Association of Corrosion Engineers standards. We continually monitor, test, and record the effectiveness of these corrosion inhibiting systems.

Product Quality Standards

Refined petroleum products that we transport are generally sold by our customers for use by the public. Various federal, state and local agencies have the authority to prescribe product quality specifications for products. Changes in product quality specifications or blending requirements could reduce our throughput volumes, require us to incur additional handling costs or require capital expenditures. For example, different product specifications for different markets affect the fungibility of the products in our system and could require the construction of additional storage. If we are unable to recover these costs through increased revenue, our cash flows and ability to pay cash distributions could be adversely affected. In addition, changes in the product quality of the products we receive on our product pipeline systems could reduce or eliminate our ability to blend products.

Terminal Safety

Our operations are subject to regulations promulgated by the U.S. Occupational Safety and Health Administration (OSHA), DOT and comparable state and local regulations. For each of our terminal facilities, we have identified which assets are subject to the jurisdiction of OSHA or DOT. Certain of our terminals are under the dual jurisdiction of DOT and OSHA, whereby certain portions of the terminal are subject to OSHA regulation and other assets at the terminal are subject to DOT regulation due to the type of asset and the configuration of the terminal. Our terminal facilities are operated in a manner consistent with industry safe practices and standards. The tanks designed for crude oil and refined product storage at our terminals are equipped with appropriate emission controls to promote safety. Our terminal facilities have response plans, spill prevention and control plans, and other programs to respond to emergencies.

14

Rail Safety

Our rail operations are currently limited to crude oil unloading and receiving activities. Generally, rail operations are subject to regulations promulgated by the U.S. Department of Transportation Federal Railroad Administration, PHMSA and comparable state and local regulations. We believe our rail operations are in material compliance with all applicable regulations and meet or exceed current industry standards and practices.

Security

We are also subject to Department of Homeland Security Chemical Facility Anti-Terrorism Standards, which are designed to regulate the security of high-risk chemical facilities, to the Transportation Security Administration’s Pipeline Security Guidelines, and other comparable state and local regulations. We have an internal program of inspection designed to monitor and provide for compliance with all of these requirements. We believe that we are in material compliance with all applicable laws and regulations regarding the security of our facilities. However, these laws and regulations are subject to changes, or to changes in their interpretation, by the regulatory authorities, and continued and future compliance with such laws and regulations may require us to incur significant expenditures. In addition, any incidents may result in substantial expenditures for response actions, government penalties, and business interruption.

While we are not currently subject to governmental standards for the protection of computer-based systems and technology from cyber threats and attacks, proposals to establish such standards are being considered in the U.S. Congress and by U.S. Executive Branch departments and agencies, including the Department of Homeland Security, and we may become subject to such standards in the future. We currently are implementing our own cyber security programs and protocols; however, we cannot guarantee their effectiveness. A significant cyber attack could have a material effect on operations and those of our customers.

ENVIRONMENTAL REGULATIONS

General

Our operations are subject to extensive and frequently changing federal, state and local laws, regulations and ordinances relating to the protection of the environment. Among other things, these laws and regulations govern the emission or discharge of pollutants into or onto the land, air and water, the handling and disposal of solid and hazardous wastes and the remediation of contamination. As with the industry generally, compliance with existing and anticipated environmental laws and regulations increases our overall cost of business, including our capital costs to construct, maintain, operate and upgrade equipment and facilities. While these laws and regulations affect our maintenance capital expenditures and net income, we believe they do not affect our competitive position, as the operations of our competitors are similarly affected. We believe our facilities are in substantial compliance with applicable environmental laws and regulations. However, these laws and regulations are subject to changes, or to changes in their interpretation, by regulatory authorities, and continued and future compliance with such laws and regulations may require us to incur significant expenditures. Additionally, violation of environmental laws, regulations, and permits can result in the imposition of significant administrative, civil and criminal penalties, injunctions limiting our operations, investigatory or remedial liabilities or construction bans or delays in the construction of additional facilities or equipment. Further, a release of hydrocarbons or hazardous substances into the environment could, to the extent the event is not insured, subject us to substantial expenses, including costs to comply with applicable laws and regulations and to resolve claims by third parties for personal injury or property damage, or by the U.S. federal government or state governments for natural resources damages. These impacts could directly and indirectly affect our business and have an adverse impact on our financial position, results of operations and liquidity. We cannot currently determine the amounts of such future impacts.

Expensed environmental costs were $1.0 million in 2014 and are expected to be approximately $4.6 million in 2015 and $0.5 million in 2016. The majority of the environmental expenses forecasted for 2015 and 2016 relate to environmental matters attributable to ownership of our current assets prior to our acquisition of these assets from Phillips 66. Phillips 66 has agreed to retain responsibility for these liabilities. Accordingly, although these amounts would be expensed by us, there would be no required cash outflow from us. See the “Indemnification” and “Excluded Liabilities of the Acquired Assets” sections to follow for additional information on Phillips 66-retained liabilities. Capitalized environmental costs were $23.9 million in 2014 and are expected to be approximately $25 million in 2015 and $26 million in 2016. These amounts do not include capital expenditures made for other purposes that have an indirect benefit on environmental compliance.

15

Air Emissions and Climate Change

We are subject to the Clean Air Act (CAA) and its regulations and comparable state and local statutes and regulations in connection with air emissions from our operations. Under these laws, permits may be required before construction can commence on a new source of potentially significant air emissions, and operating permits may be required for sources that are already constructed. These permits may require controls on our air emission sources, and we may become subject to more stringent regulations requiring the installation of additional emission control technologies.

Future expenditures may be required to comply with the CAA and other federal, state and local requirements for our various sites, including our pipeline and storage facilities. The impact of future legislative and regulatory developments, if enacted or adopted, could result in increased compliance costs and additional operating restrictions on our business, all of which could have an adverse impact on our financial position, results of operations and liquidity.

These air emissions requirements also affect Phillips 66’s domestic refineries from which we directly or indirectly receive substantially all of our revenue. Phillips 66 has been required in the past, and will likely be required in the future, to incur significant capital expenditures to comply with new legislative and regulatory requirements relating to its operations. To the extent these capital expenditures have a material effect on Phillips 66, they could have a material effect on our business and results of operations.

In December 2007, Congress passed the Energy Independence and Security Act (EISA) that created a second Renewable Fuels Standard (RFS2). This standard requires the total volume of renewable transportation fuels (including ethanol and advanced biofuels) sold or introduced annually in the United States to rise to 36 billion gallons by 2022. The requirements could reduce future demand for petroleum products and thereby have an indirect effect on certain aspects of our business. For compliance year 2014, the U.S. Environmental Protection Agency (EPA) proposed to reduce the statutory volumes of advanced and total renewable fuels using authority granted to it under the EISA. We do not know whether this reduction will be finalized as proposed and/or whether the EPA will utilize its authority to reduce statutory volumes in future compliance years.

Currently, various legislative and regulatory measures to address greenhouse gas (GHG) emissions (including carbon dioxide, methane and other gases) are in various phases of discussion or implementation. These include requirements effective in January 2010 to report emissions of GHGs to the EPA beginning in 2011, and proposed federal legislation and regulation as well as state actions to develop statewide or regional programs, each of which require or could require reductions in our GHG emissions or those of Phillips 66. Requiring reductions in GHG emissions could result in increased costs to (1) operate and maintain our facilities, (2) install new emission controls at our facilities and (3) administer and manage any GHG emissions programs, including acquiring emission credits or allotments. These requirements may also impact Phillips 66’s domestic refinery operations and may have an indirect effect on our business, financial condition and results of operations.

In addition, the EPA has proposed and may adopt further regulations under the CAA addressing GHGs, to which some of our facilities may become subject. Congress continues to consider legislation on GHG emissions, which may include a delay in the implementation of GHG regulations by the EPA or a limitation on the EPA’s authority to regulate GHGs, although the ultimate adoption and form of any federal legislation cannot presently be predicted. The impact of future regulatory and legislative developments, if adopted or enacted, including any cap-and-trade program, is likely to result in increased compliance costs, increased utility costs, additional operating restrictions on our business, and an increase in the cost of products generally. Although such costs may impact our business directly or indirectly by impacting Phillips 66’s facilities or operations, the extent and magnitude of that impact cannot be reliably or accurately estimated due to the present uncertainty regarding the additional measures and how they will be implemented.

Waste Management and Related Liabilities

To a large extent, the environmental laws and regulations affecting our operations relate to the release of hazardous substances or solid wastes into soils, groundwater, and surface water, and include measures to control pollution of the environment. These laws generally regulate the generation, storage, treatment, transportation, and disposal of solid and hazardous waste. They also require corrective action, including investigation and remediation, at a facility where such waste may have been released or disposed.

16

The Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA), which is also known as Superfund, and comparable state laws impose liability, without regard to fault or to the legality of the original conduct, on certain classes of persons that contributed to the release of a “hazardous substance” into the environment. These persons include the former and present owner or operator of the site where the release occurred and the transporters and generators of the hazardous substances found at the site. Under CERCLA, these persons may be subject to joint and several liabilities for the costs of cleaning up the hazardous substances that have been released into the environment, for damages to natural resources, and for the costs of certain health studies. CERCLA also authorizes the EPA and, in some instances, third parties to act in response to threats to the public health or the environment and to seek to recover from the responsible classes of persons the costs they incur. It is not uncommon for neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by hazardous substances or other pollutants released into the environment. In the course of our ordinary operations, we generate waste that falls within CERCLA’s definition of a “hazardous substance” and, as a result, may be jointly and severally liable under CERCLA for all or part of the costs required to clean up sites.

We also generate solid wastes, including hazardous wastes, that are subject to the requirements of the Resource Conservation and Recovery Act (RCRA) and comparable state statutes. From time to time, the EPA considers the adoption of stricter disposal standards for non-hazardous wastes. Hazardous wastes are subject to more rigorous and costly disposal requirements than are non-hazardous wastes. Any changes in the regulations could increase our maintenance capital expenditures and operating expenses. We continue to seek methods to minimize the generation of hazardous wastes in our operations.

We currently own and lease, and Phillips 66 has in the past owned and leased, properties where hydrocarbons are being or for many years have been handled. Although we have utilized operating and disposal practices that were standard in the industry at the time, hydrocarbons or other waste may have been disposed of or released on or under the properties owned or leased by us or on or under other locations where these wastes have been taken for disposal. In addition, many of these properties have been operated by third parties whose treatment and disposal or release of hydrocarbons or other wastes were not under our control. These properties and wastes disposed thereon may be subject to CERCLA, RCRA and analogous state laws. Under these laws, we could be required to remove or remediate previously disposed wastes (including wastes disposed of or released by prior owners or operators), to clean up contaminated property (including contaminated groundwater), or to perform remedial operations to prevent further contamination.

Water

Our operations can result in the discharge of pollutants, including crude oil and petroleum products. Regulations under the Water Pollution Control Act of 1972 (Clean Water Act), Oil Pollution Act of 1990 (OPA 90) and comparable state laws impose regulatory burdens on our operations. Spill Prevention Control and Countermeasure (SPCC) requirements of federal laws and some state laws require containment to mitigate or prevent contamination of navigable waters in the event of an oil overflow, rupture, or leak. For example, the Clean Water Act requires us to maintain SPCC plans at many of our facilities. We maintain numerous discharge permits as required under the National Pollutant Discharge Elimination System program of the Clean Water Act and have implemented systems to oversee our compliance efforts.

In addition, the transportation and storage of crude oil and petroleum products over and adjacent to water involves risk and subjects us to the provisions of OPA 90 and related state requirements. Among other requirements, OPA 90 requires the owner or operator of a tank vessel or a facility to maintain an emergency plan to respond to releases of oil or hazardous substances. Also, in case of any such release, OPA 90 requires the responsible company to pay resulting removal costs and damages. OPA 90 also provides for civil penalties and imposes criminal sanctions for violations of its provisions. We operate facilities at which releases of oil and hazardous substances could occur. We have implemented emergency oil response plans for all of our components and facilities covered by OPA 90 and we have established SPCC plans for facilities subject to Clean Water Act SPCC requirements. Construction or maintenance of our pipelines, terminals and storage facilities may impact wetlands, which are also regulated under the Clean Water Act by the EPA and the United States Army Corps of Engineers. Regulatory requirements governing wetlands (including associated mitigation projects) may result in the delay of our projects while we obtain necessary permits and may increase the cost of new projects and maintenance activities.

17

Employee Safety

We are subject to requirements promulgated by OSHA and comparable state statutes that regulate the protection of the health and safety of workers. In addition, the OSHA hazard communication standard requires that information be maintained about hazardous materials used or produced in operations and that this information be provided to employees, state and local government authorities and citizens. We believe that our operations are in substantial compliance with OSHA requirements, including general industry standards, record keeping requirements, and monitoring of occupational exposure to regulated substances.

Endangered Species Act

The Endangered Species Act restricts activities that may affect endangered species or their habitats. While some of our facilities are in areas that may be designated as habitats for endangered species, we believe that we are in substantial compliance with the Endangered Species Act. However, the discovery of previously unidentified endangered species could cause us to incur additional costs or become subject to operating restrictions or bans in the affected area.

Hazardous Materials Transportation Requirements

The DOT regulations affecting pipeline safety require pipeline operators to implement measures designed to reduce the environmental impact of crude oil and petroleum products discharge from onshore crude oil and petroleum product pipelines. These regulations require operators to maintain comprehensive spill response plans, including extensive spill response training for pipeline personnel. In addition, the DOT regulations contain detailed specifications for pipeline operation and maintenance. We believe our operations are in substantial compliance with these regulations. The DOT also has a pipeline integrity management rule, with which we are in substantial compliance.

Indemnification

Under our amended omnibus agreement, Phillips 66 indemnifies us for certain environmental liabilities, tax liabilities, and litigation and other matters attributable to the assets contributed by Phillips 66 in connection with the Offering (the Initial Assets) and which arose prior to the closing of the Offering. Indemnification for any unknown environmental liabilities is limited to liabilities due to occurrences prior to the closing of the Offering and that are identified before the fifth anniversary of the closing of the Offering, subject to an aggregate deductible of $0.1 million before we are entitled to indemnification. Indemnification for litigation matters provided therein (other than legal actions pending as of the Offering) is subject to an aggregate deductible of $0.2 million before we are entitled to indemnification. Phillips 66 also indemnifies us under our amended omnibus agreement for failure to obtain certain consents, licenses and permits necessary to conduct our business, including the cost of curing any such condition, in each case that is identified prior to the fifth anniversary of the closing of the Offering, subject to an aggregate deductible of $0.2 million before we are entitled to indemnification. We have agreed to indemnify Phillips 66 for events and conditions associated with the ownership or operation of the Initial Assets that occur on or after the closing of the Offering and for certain environmental liabilities related to the Initial Assets to the extent Phillips 66 is not required to indemnify us.

Excluded Liabilities of the Acquired Assets

Pursuant to the terms of the various agreements under which we acquired assets from Phillips 66 since the Offering, Phillips 66 assumed the responsibility for any liabilities arising out of or attributable to the ownership or operation of the Acquired Assets, or other activities occurring in connection with and attributable to the ownership or operation of the Acquired Assets, prior to the effective date of each acquisition. We have assumed, and have agreed to pay, discharge and perform as and when due, all liabilities arising out of or attributable to the ownership or operation of the Acquired Assets or other activities occurring in connection with and attributable to the ownership or operation of the Acquired Assets, from and after the effective date of each acquisition.

18

GENERAL

Major Customer

Phillips 66 accounted for 95 percent, 94 percent and 95 percent of our total revenues in the years ended December 31, 2014, 2013 and 2012, respectively. We provide crude oil and refined petroleum product pipeline transportation, terminaling, storage and rail-unloading services to Phillips 66.

Seasonality

The crude oil and refined petroleum products transported in our pipelines and stored in our terminals, rail racks and storage facilities are directly affected by the level of supply and demand for crude oil and refined petroleum products in the markets served directly or indirectly by our assets. However, many effects of seasonality on our revenue should be substantially mitigated through the use of our fee-based commercial agreements with Phillips 66 that include minimum volume commitments.

Pipeline Control Operations

Our pipeline systems are operated from a central control room owned and operated by Phillips 66, located in Bartlesville, Oklahoma. The control center operates with a supervisory control and data acquisition system equipped with computer systems designed to continuously monitor operational data. Monitored data includes pressures, temperatures, gravities, flow rates and alarm conditions. The control center operates remote pumps, motors, and valves associated with the receipt and delivery of crude oil and refined petroleum products, and provides for the remote-controlled shutdown of pump stations on the pipeline systems. A fully functional back-up operations center is also maintained and routinely operated throughout the year to ensure safe and reliable operations.

Employees

We are managed and operated by the executive officers of our General Partner with oversight provided by its Board of Directors. Neither we nor our subsidiaries have any employees. Our General Partner has the sole responsibility for providing the employees and other personnel necessary to conduct our operations. All of the employees that conduct our business are employed by affiliates of our General Partner. Our General Partner and its affiliates have approximately 130 employees who spend a significant amount of their time performing services for our operations. We believe that our General Partner and its affiliates have a satisfactory relationship with those employees.

Website Access to SEC Reports

Our Internet website address is http://www.phillips66partners.com. Information contained on our Internet website is not part of this Annual Report on Form 10-K.