Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Armada Hoffler Properties, Inc. | d870492d8k.htm |

| EX-99.1 - EX-99.1 - Armada Hoffler Properties, Inc. | d870492dex991.htm |

Armada

Hoffler Properties, Inc. Fourth Quarter 2014 Supplemental Information

1

Exhibit 99.2 |

Table of

Contents 2

Forward Looking Statements

3

Corporate Profile

4

Quarter Results and Financial Summary

5

Highlights

6

2015 Outlook

7

Summary Information

8

Summary Balance Sheet

9

Summary Income Statement

10

Normalized FFO, Core FFO & AFFO

11

Summary of Outstanding Debt

12

Core Debt to Core EBITDA

13

Debt Information

14

Portfolio Summary & Business Segment Overview

15

Stabilized Portfolio Summary

16

Stabilized Portfolio Summary Footnotes

17

Development Pipeline

18

Acquisitions & Dispositions

19

Construction Business Summary

20

Operating Results & Property-Type Segment Analysis

21

Same Store NOI by Segment

22

Top 10 Tenants by Annual Base Rent

23

Office Lease Summary

24

Retail Lease Summary

26

Historical Occupancy

28

Net Asset Value Component Data

31

Appendix - Definitions & Reconciliations

32

Definitions

33

Reconciliations

38 |

Forward

Looking Statements 3

This

Supplemental

Information

should

be

read

in

conjunction

with

our

Annual

Report

on

Form

10-K

for

the

year ended December 31, 2014, and the unaudited consolidated financial statements

appearing in our press release dated February 12, 2015, which has been furnished

as Exhibit 99.1 to our Form 8-K filed on February

12,

2015.

The

Company

makes

statements

in

this

Supplemental

Information

that

are

forward-

looking statements within the meaning of the Private Securities Litigation Reform Act

of 1995 (set forth in Section 27A of the Securities Act of 1933, as amended (the

“Securities Act”), and Section 21E of the Securities

Exchange

Act

of

1934,

as

amended

(the

“Exchange

Act”)).

In

particular,

statements

pertaining

to our capital resources, portfolio performance and results of operations contain

forward-looking statements. Likewise, all of our statements regarding

anticipated growth in our funds from operations, normalized funds from

operations, core funds from operations, adjusted funds from operations, funds

available for distribution and net operating income are forward-looking

statements. You can identify forward-looking statements by the use of

forward-looking terminology such as “believes,”

“expects,”

“may,”

“will,”

“should,”

“seeks,”

“approximately,”

“intends,”

“plans,”

“estimates”

or “anticipates”

or

the negative of these words and phrases or similar words or phrases which are

predictions of or indicate future events or trends and which do not relate

solely to historical matters. You can also identify forward- looking

statements by discussions of strategy, plans or intentions. Forward-looking

statements involve numerous risks and uncertainties and you should not rely on them as

predictions of future events. Forward-looking statements depend on assumptions,

data or methods which may

be

incorrect

or

imprecise

and

the

Company

may

not

be

able

to

realize

them.

The

Company

does

not

guarantee

that

the

transactions

and

events

described

will

happen

as

described

(or

that

they

will

happen

at all). For further discussion of risk factors and other events that could

impact our future results, please refer to the section entitled “Risk

Factors” in our most recent Annual Report on Form 10-K filed with the

Securities and Exchange Commission (the “SEC”), and the documents

subsequently filed by us from time to time with the SEC.

|

Corporate Profile

4

Corporate Information

Management & Board

Board of Directors

Corporate Officers

Daniel A. Hoffler

Executive Chairman of the Board

Louis S. Haddad

President and Chief Executive Officer

A. Russell Kirk

Vice Chairman of the Board

Anthony P. Nero

President of Development

Louis S. Haddad

Director

Shelly R. Hampton

President of Asset Management

John W. Snow

Lead Independent Director

Eric E. Apperson

President of Construction

George F. Allen

Independent Director

Michael P. O’Hara

Chief Financial Officer and Treasurer

James A. Carroll

Independent Director

Eric L. Smith

Vice President of Operations and Corporate Secretary

James C. Cherry

Independent Director

Joseph W. Prueher

Independent Director

Analyst Coverage

Raymond James & Associates

Robert W. Baird & Co.

Stifel, Nicolaus & Company, Inc.

Wunderlich Securities

Bill Crow

David Rodgers

John Guinee

Craig Kucera

(727) 567-2594

(216) 737-7341

(443) 224-1307

(540) 277-3366

bill.crow@raymondjames.com

drodgers@rwbaird.com

jwguinee@stifel.com

ckucera@wundernet.com

Investor Relations Contact

Julie Loftus Trudell

Vice President of Investor Relations

(757) 366-6692

jtrudell@armadahoffler.com

Armada Hoffler Properties, Inc. (NYSE: AHH)

is a full service real estate company that develops, constructs, and owns institutional grade

office, retail, and multifamily properties in the Mid-Atlantic United States.

The Company also provides general contracting and development services to third-party clients

throughout the Mid-Atlantic and Southeastern regions. Armada Hoffler Properties,

Inc. was founded in 1979 and is headquartered in Virginia Beach, VA. The Company

has elected to be taxed as a real estate investment trust (REIT) for U.S. federal income tax purposes. |

Fourth

Quarter Results and Financial Summary |

Highlights

•

Funds From Operations (“FFO”) of $8.0 million, or $0.20 per diluted share,

for the quarter ended December 31, 2014. FFO of $28.1 million, or $0.80

per diluted share, for the full-year 2014. •

Core FFO of $7.9 million, or $0.20 per diluted share, for the quarter ended December

31, 2014. Core FFO of $29.4 million, or $0.84 per diluted share, for the

full-year 2014. •

Occupancy up to 95.7%, compared to 95.1 % as of September 30, 2014 and 94.4% as of

December 31, 2013. •

Increased quarterly GAAP and Cash Same Store Net Operating Income (“NOI”)

2.9% and 3.0%, respectively, compared to the fourth quarter of 2013.

•

Increased annual GAAP and Cash Same Store NOI 2.0% and 0.7%, respectively, compared to

the full-year 2013. •

In the fourth quarter, completed the sale of the Virginia Natural Gas office building

for approximately $8.9 million, representing a cap rate of 6.25%.

•

In January 2015, completed the sale of the Sentara Williamsburg office building for

approximately $15.4 million, representing a cap rate of 6.3%.

•

Entered into agreements to acquire two grocery anchored retail centers located in

Maryland. These pending

acquisitions will add over 185,000 square feet to the Company’s portfolio with a

combined occupancy of approximately 90%.

The Company intends to acquire 100% interests in these centers in exchange for a

combination of common stock and cash including the net proceeds from the Sentara

Williamsburg sale. These acquisitions are expected to be accretive to 2015

FFO per diluted share and are expected to close by the end of the first quarter of 2015.

Both

transactions are subject to customary closing conditions.

•

Entered into a commitment with a syndicate of banks co-led by Bank of America and

Regions Bank for a new, expanded and unsecured $200 million senior credit

facility that includes a $50 million term loan. •

Declared a cash dividend of $0.17 per common share for the first

quarter of 2015, representing a 6.3% increase over the

prior quarter’s cash dividend. The first quarter dividend will be payable on

April 9, 2015 to stockholders of record on April 1, 2015.

•

Introduces 2015 Normalized FFO guidance in the range of $0.85 to

$0.90 per diluted share.

6 |

2015

Outlook 7

Full-year 2015 Guidance

Total GAAP NOI

$52.3M

$53.3M

Construction company annual segment gross profit

$4.5M

$5.0M

General and administrative expenses

$8.3M

$8.6M

Interest expense

$14.0M

$15.0M

Normalized FFO per diluted share

$0.85

$0.90

Expected Ranges |

Summary

Information 8

$ in thousands, except per share

Market Capitalization

Key Financials

12/31/2014

Financial Information:

12/31/2014

% of Total

Equity

Total Market

Capitalization

Rental revenues

$17,521

Market Data

General contracting and real estate services revenues

32,060

Total Common Shares Outstanding

63%

25,023

Rental properties Net Operating Income

(NOI) 11,572

Operating Partnership ("OP") Units

Outstanding 37%

14,776

General contracting and real estate services

gross profit 1,113

Common shares and OP units

outstanding 100%

39,799

Net income

5,226

Market price per common

share $9.49

Funds From Operations (FFO)

7,991

Equity market

capitalization $377,689

FFO per diluted share

$0.20

Total debt

359,229

Normalized FFO

8,156

Total market capitalization

$736,918

Normalized FFO per diluted share

$0.20

Less: cash

(30,107)

Core FFO

7,938

Total enterprise

value $706,811

Core FFO per diluted share

$0.20

Weighted Average Shares/Units Outstanding

39,796

Stable Portfolio Metrics

Debt Metrics

12/31/2014

Rentable square feet or number of units:

12/31/2014

Office

(1)

918,162

Key Metrics

Retail

(2)

1,200,738

Core debt/enterprise value

34.6%

Multifamily

(3)

626

Fixed

charge coverage ratio: EBITDA

(7)

$10,597

Occupancy:

Interest

2,671

Office

(4)

95.2%

Principal

800

Retail

(4)

96.4%

Total Fixed Charges

3,471

Multifamily

(5)

95.7%

Fixed charge coverage ratio

3.05x

Weighted Average

(6)

95.7%

Core Debt/Annualized Core EBITDA

6.1x

Three months ended

Three months ended

(1) Excludes 4525 Main Street

(2) Excludes Greentree Shopping Center

(3) Excludes Liberty, Encore, and Whetstone Apartments

(4) Office

and

retail

occupancy

based

on

leased

square

feet

as

a

%

of

respective

total

(5) Multifamily occupancy based on occupied units as a % of respective total

(6) Total occupancy weighted by annualized base rent

(7) Excludes $2.2M gain on disposition |

Summary

Balance Sheet 9

$ in thousands

12/31/2014

12/31/2013

Assets

(Unaudited)

Real estate investments:

Income producing property

$513,918

$406,239

Construction in progress

81,082

56,737

Accumulated depreciation

(116,099)

(105,228)

Net real estate investments

478,901

357,748

Real estate investments held-for-sale

8,538

-

Cash and cash equivalents

25,883

18,882

Restricted cash

4,224

2,160

Accounts receivable, net

20,548

18,272

Construction receivables, including retentions

19,432

12,633

Costs and estimated earnings in excess of billings

272

1,178

Other assets

33,108

24,409

Total Assets

$590,906

$435,282

Liabilities and Equity

Indebtedness

$359,229

$277,745

Accounts payable and accrued liabilities

8,358

6,463

Construction payables, including retentions

42,399

28,139

Billings in excess of costs and estimated earnings

1,053

1,541

Other liabilities

17,961

15,873

Total Liabilities

429,000

329,761

Total Equity

161,906

105,521

Total Liabilities and Equity

$590,906

$435,282

As of |

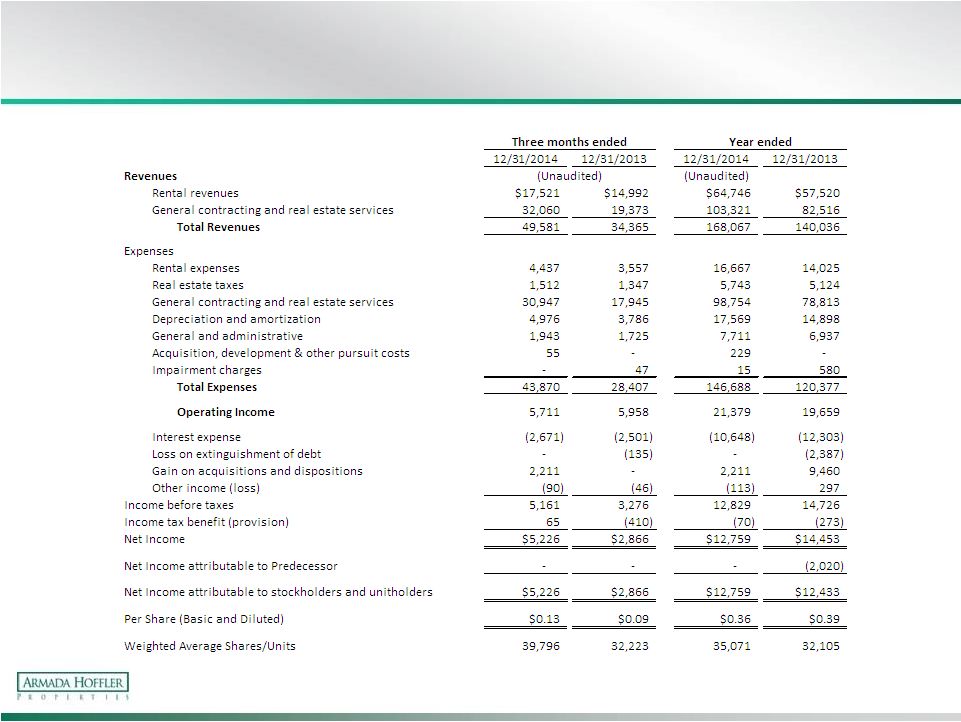

Summary

Income Statement 10

$ in thousands |

Normalized FFO, Core FFO & AFFO

11

$ in thousands, except per share

(1) Excludes tenant improvements and leasing commissions on first generation rental

space. Three months ended

Year ended

12/31/2014

12/31/2014

(Unaudited)

Net income

$5,226

$12,759

Depreciation and amortization

4,976

17,569

Gain on acquisitions

(2,211)

(2,211)

FFO

7,991

28,117

FFO per weighted average share

$0.20

$0.80

Normalized FFO

Acquisition costs

55

229

Loss on extinguishment of debt

-

-

Impairment charges

-

15

Derivative (income) losses

110

233

Normalized FFO

8,156

28,594

Normalized FFO per weighted average share

$0.20

$0.82

Core FFO

Derivative income (losses)

(110)

(233)

Non-cash stock compensation

197

917

Non-stabilized development pipeline adjustments

(305)

79

Core FFO

7,938

29,357

Core FFO per weighted average share

$0.20

$0.84

AFFO

Non-Stabilized development pipeline adjustments

305

(79)

Acquisition costs

(55)

(229)

Tenant improvements, leasing commissions

(3,114)

(5,311)

Leasing incentives

(334)

(462)

Property related capital expenditures

(583)

(1,479)

Non cash interest expense

104

514

GAAP Adjustments

Net effect of straight-line rents

(394)

(1,887)

Amortization of lease incentives and above (below) market rents

172

633

Derivative (income) losses

110

233

Government development grants

-

300

AFFO

4,149

21,590

AFFO per weighted average share

$0.10

$0.62

(1) |

Summary

of Outstanding Debt 12

$ in thousands

(1) LIBOR rate is determined by individual lenders.

(2) Subject to an interest rate swap lock.

(3) Principal balance excluding any fair value

adjustment recognized upon acquisition.

(4) Excludes fair value adjustment

Weighted Average Fixed Interest Rate

5.3%

Weighted Average Variable Interest Rate

2.1%

Total Weighted Average Interest Rate

(4)

3.4%

Variable Interest Rate as a % of Total (excluding interest rate caps)

(4)

59.7%

Weighted Average Maturity (years)

(4)

8.3

Debt

Amount

Outstanding

Interest Rate

(1)

Effective Rate as of

December 31, 2014

Maturity Date

Balance at

Maturity

Virginia Beach Town Center

249 Central Park Retail

$15,566

5.99%

September 8, 2016

$15,084

South Retail

6,867

5.99%

September 8, 2016

6,655

Studio 56 Retail

2,618

3.75%

May 7, 2015

2,592

Commerce Street Retail

5,549

LIBOR +2.25%

2.40%

October 31, 2018

5,264

Fountain Plaza Retail

7,783

5.99%

September 8, 2016

7,542

Dick's at Town Center

8,216

LIBOR+2.75%

2.90%

October 31, 2017

7,889

The Cosmopolitan

47,132

3.75%

July 1, 2051

-

Diversified Portfolio

Oyster Point

6,274

5.41%

December 1, 2015

6,089

Broad Creek Shopping Center

Note 1

4,452

LIBOR +2.25%

2.40%

October 31, 2018

4,223

Note 2

8,173

LIBOR +2.25%

2.40%

October 31, 2018

7,752

Note 3

3,422

LIBOR +2.25%

2.40%

October 31, 2018

3,246

Hanbury Village

Note 1

21,218

6.67%

October 11, 2017

20,499

Note 2

4,090

LIBOR +2.25%

2.40%

October 31, 2018

3,777

Harrisonburg Regal

3,659

6.06%

June 8, 2017

3,165

North Point Center

Note 1

10,149

6.45%

February 5, 2019

9,333

Note 2

2,753

7.25%

September 15, 2025

1,344

Note 5

685

LIBOR+2.00%

3.57%

(2)

February 1, 2017

641

Tyre Neck Harris Teeter

2,437

LIBOR +2.25%

2.40%

October 31, 2018

2,235

Smith's Landing

24,470

LIBOR+2.15%

2.30%

January 31, 2017

23,793

185,513

131,123

Credit Facility

59,000

LIBOR + 1.60% - 2.20%

1.90%

May 13, 2016

59,000

Total including Credit Facility

$244,513

$190,123

Development Pipeline

4525 Main Street

$30,870

LIBOR+1.95%

2.10%

January 30, 2017

30,870

Encore Apartments

22,215

LIBOR+1.95%

2.10%

January 30, 2017

22,215

Whetstone Apartments

16,019

LIBOR+1.90%

2.05%

October 8, 2016

16,019

Sandbridge Commons

5,892

LIBOR+1.85%

2.00%

January 17, 2018

5,892

Liberty Apartments

20,603

(3)

5.66%

November 1, 2043

-

Oceaneering

13,490

LIBOR+1.75%

1.90%

February 28, 2018

13,490

Commonwealth of Virginia - Chesapeake

3,585

LIBOR+1.90%

2.05%

August 28, 2017

3,585

Lightfoot Marketplace

3,484

LIBOR+1.90%

2.05%

November 14, 2017

3,484

Total Notes Payable - Development

Pipeline 116,158

95,555

Unamortized fair value adjustments

(1,442)

-

Total Notes Payable

$359,229

$285,678

4Q 2014

Year to Date

Capitalized Interest

$794

$2,752 |

Core

Debt to Core EBITDA 13

Three months ended

12/31/2014

12/31/2014

(Unaudited)

(Unaudited)

Net Income

$5,226

Total Debt

$359,229

Excluding:

Excluding:

Interest Expense

2,671

Development

Pipeline Unstabilized Debt (114,716)

Income Tax

(65)

Depreciation and amortization

4,976

Core Debt

$244,513

EBITDA

12,808

Additional Adjustments:

Gain on dispositions

(2,211)

Early extinguishment of

debt -

Core Debt/Annualized Core EBITDA

6.1x

Derivative (income) losses

110

Non-cash stock compensation

197

Development Pipeline

(802)

Total Other Adjustments

(2,706)

Core EBITDA

$10,102

Annualized Core EBITDA

$40,408

$ in thousands |

Debt

Information 14

$ in thousands

Interest Rate Cap Agreements At or Below 1.50%

Effective Date

Maturity Date

Strike Rate

Notional Amount

May 31, 2012

May 29, 2015

1.09%

$8,888

September 1, 2013

March 1, 2016

1.50%

40,000

October 4, 2013

April 1, 2016

1.50%

18,500

March 14, 2014

March 1, 2017

1.25%

50,000

Total Interest Rate Caps at or Below 1.50%

$117,388

Fixed Debt Outstanding (excludes fair value adjustment)

145,307

Total Fixed Interest Rate Debt (including caps)

$262,695

Fixed Interest Rate Debt as a % of Total

73%

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

2015

2017

2019 and

thereafter

Debt Maturity as of

12/31/2014

2016

2018 |

Portfolio Summary & Business

Segment Overview |

Stabilized Portfolio Summary

16

As of 12/31/14

Property

Location

Year Built

Net Rentable

Square Feet

(1)

Occupied Sq. Ft.

% Leased

(2)

Annualized

Base Rent

(3)

Annualized

Base Rent per

Leased Sq. Ft.

(3)

Average Net

Effective

Annual Base

Rent per

Leased Sq. Ft.

(4)

Office Properties

Armada Hoffler Tower

(5)

Virginia Beach, VA

2002

323,966

312,415

96.4%

$8,320,174

$26.63

$27.46

One Columbus

Virginia Beach, VA

1984

129,424

129,424

100.0%

3,018,331

23.32

23.34

Two Columbus

Virginia Beach, VA

2009

108,464

98,938

91.2%

2,528,923

25.56

25.75

Richmond Tower

Richmond, VA

2010

206,969

204,083

98.6%

7,569,747

37.09

41.81

Oyster Point

Newport News, VA

1989

100,139

80,128

80.0%

1,767,387

22.06

21.12

Sentara Williamsburg

(6)

Williamsburg, VA

2008

49,200

49,200

100.0%

1,006,140

20.45

20.50

Subtotal / Weighted Average Office Portfolio

(7)

918,162

874,188

95.2%

$24,210,702

$27.70

$29.04

Retail Properties Not Subject to Ground Lease

Bermuda Crossroads

Chester, VA

2001

111,566

109,966

98.6%

1,522,001

13.84

14.03

Broad Creek Shopping Center

Norfolk, VA

1997-2001

227,691

221,576

97.3%

3,091,636

13.95

12.66

Courthouse 7-Eleven

Virginia Beach, VA

2011

3,177

3,177

100.0%

125,000

39.35

43.81

Gainsborough Square

Chesapeake, VA

1999

88,862

85,782

96.5%

1,346,126

15.69

15.16

Hanbury Village

Chesapeake, VA

2006-2009

61,049

52,716

86.4%

1,278,659

24.26

24.46

North Point Center

Durham, NC

1998-2009

215,690

200,890

93.1%

2,383,713

11.87

11.91

Parkway Marketplace

Virginia Beach, VA

1998

37,804

37,804

100.0%

737,456

19.51

19.44

Harrisonburg Regal

Harrisonburg, VA

1999

49,000

49,000

100.0%

683,550

13.95

13.95

Dick's at Town Center

Virginia Beach, VA

2002

103,335

103,335

100.0%

1,179,866

11.42

11.72

249 Central Park Retail

(8)

Virginia Beach, VA

2004

91,171

83,481

91.6%

2,424,086

29.04

28.29

Studio 56 Retail

Virginia Beach, VA

2007

11,600

9,832

84.8%

371,200

37.75

37.58

Commerce Street Retail

(9)

Virginia Beach, VA

2008

19,173

19,173

100.0%

781,588

40.77

37.06

Fountain Plaza Retail

Virginia Beach, VA

2004

35,961

35,961

100.0%

970,230

26.98

26.79

South Retail

Virginia Beach, VA

2002

38,493

38,493

100.0%

921,559

23.94

24.31

Dimmock Square

Colonial Heights, VA

1998

106,166

106,166

100.0%

1,769,435

16.67

16.76

Subtotal / Weighted Avg Retail Portfolio not Subject to Ground Leases

(10)

1,200,738

1,157,352

96.4%

$19,586,105

$16.92

$16.61

Retail Properties Subject to Ground Lease

Bermuda Crossroads

(11)

Chester, VA

2001

(13)

100.0%

163,350

Broad Creek Shopping Center

(12)

Norfolk, VA

1997-2001

(14)

100.0%

588,126

Hanbury Village

(11)

Chesapeake, VA

2006-2009

(15)

100.0%

1,067,598

North Point Center

(11)

Durham, NC

1998-2009

(16)

100.0%

1,062,784

Tyre Neck Harris Teeter

(12)

Portsmouth, VA

2011

(17)

100.0%

508,134

Subtotal / Weighted Avg Retail Portfolio Subject to Ground Leases

100.0%

$3,389,992

Total / Weighted Avg Retail Portfolio

1,200,738

(18)

1,157,352

96.4%

$22,976,097

$16.92

$16.61

Total / Weighted Average Retail and Office Portfolio

2,118,900

2,031,540

95.9%

$47,186,799

$21.56

$21.95

Property

Location

Year Built

Units

(19)

% Leased

(2)

Annualized

Base Rent

(20)

Average

Monthly Base

Rent per

Leased Unit

(21)

Multifamily

Smith's Landing

(22)

Blacksburg, VA

2009

284

97.9%

$3,472,020

$1,040.77

The Cosmopolitan

Virginia Beach, VA

2006

342

93.9%

6,937,078

1,571.26

Total / Weighted Avg Multifamily Portfolio

626

95.7%

$10,409,098

$1,325.06 |

Stabilized Portfolio Summary Footnotes

17

1)

The net rentable square footage for each of our office properties is the sum of (a) the square

footages of existing leases, plus (b) for available space, management’s estimate of net rentable square footage

based, in part, on past leases. The net rentable square footage included in office leases is

generally determined consistently with the Building Owners and Managers Association, or BOMA, 1996

measurement guidelines. The net rentable square footage for each of our retail properties is

the sum of (a) the square footages of existing leases, plus (b) for available space, the field verified square

footage.

2)

Percentage leased for each of our office and retail properties is calculated as (a) square

footage under executed leases as of December 31, 2014, divided by (b) net rentable square feet, expressed as a

percentage. Percentage leased for our multifamily properties is calculated as (a) total units

occupied as of December 31, 2014, divided by (b) total units available, expressed as a percentage.

3)

For the properties in our office and retail portfolios, annualized base rent is calculated by

multiplying (a) base rental payments for executed leases as of December 31, 2014 (defined as cash base rents

(before abatements) excluding tenant reimbursements for expenses paid by the landlord), by (b)

12. Annualized base rent per leased square foot is calculated by dividing (a) annualized base rent, by (b)

square footage under commenced leases as of December 31, 2014. In the case of triple net or

modified gross leases, annualized base rent does not include tenant reimbursements for real estate taxes,

insurance, common area or other operating expenses. 4)

Average net effective annual base rent per leased square foot represents (a) the contractual

base rent for leases in place as of December 31, 2014, calculated on a straight-line basis to amortize free rent

periods and abatements, but without regard to tenant improvement allowances and leasing

commissions, divided by (b) square footage under commenced leases as of December 31, 2014.

5)

As of December 31,2014, the Company occupied 18,984 square feet at this property at an

annualized base rent of $529,746 or $27.90 per leased square foot, which amounts are reflected in the % leased,

annualized base rent and annualized base rent per square foot columns in the table above. The

rent paid by us is eliminated from our revenues in consolidation. In addition, effective March 1, 2013, the

Company sublease approximately 5,000 square feet of space from a tenant at this property. 6)

This property is subject to a triple net lease pursuant to which the tenant pays operating

expenses, insurance and real estate taxes.

7)

Includes square footage and annualized base rent pursuant to leases for space occupied by us. 8)

As of December 31, 2014, the Company occupied 8,995 square feet at this property at an

annualized base rent of $287,300, or $31.94 per leased square foot, which amounts are reflected in the % leased,

annualized base rent and annualized base rent per square foot columns in the table above. The

rent paid by us is eliminated from our revenues in consolidation.

9)

Includes $32,460 of annualized base rent pursuant to a rooftop lease. 10)

Reflects square footage and annualized base rent pursuant to leases for space occupied by AHH.

11)

For this ground lease, the Company own the land and the tenant owns the improvements

thereto. The Company will succeed to the ownership of the improvements to the land upon the termination of

the ground lease.

12)

The Company lease the land underlying this property from the owner of the land pursuant to a

ground lease. The Company re-lease the land to our tenant under a separate ground lease pursuant to which

our tenant owns the improvements on the land. 13)

Tenants collectively lease approximately 139,356 square feet of land from us pursuant to

ground leases. 14)

Tenants collectively lease approximately 299,170 square feet of land from us pursuant to

ground leases. 15)

Tenants collectively lease approximately 105,988 square feet of land from us pursuant to

ground leases. 16)

Tenants collectively lease approximately 1,443,985 square feet of land from us pursuant to

ground leases. 17)

Tenant leases approximately 200,073 square feet of land from us pursuant to a ground lease. 18)

The total square footage of our retail portfolio excludes the square footage of land subject

to ground leases. 19)

Units represent the total number of apartment units available for rent at December 31,

2014. 20)

For the properties in our multifamily portfolio, annualized base rent is calculated by

multiplying (a) base rental payments for the month ended December 31, 2014 by (b) 12.

21)

Average monthly base rent per leased unit represents the average monthly rent for all leased

units for the month ended December 31, 2014.

22)

The Company lease the land underlying this property from the owner of the land pursuant to a

ground lease. 23)

The annualized base rent for The Cosmopolitan includes $885,000 of annualized rent from 15

retail leases at the property. |

Development Pipeline

18

$ in thousands

(1) Represents estimates that may change as the development process proceeds

(2) Estimated square footage includes land subject to ground lease and will be excluded

from the portfolio square footage upon stabilization. (3) AHH earns a preferred

return on equity prior to any distributions to JV partners (4) This property is

located within the Virginia Beach Town Center (5) Approximately 83,000 square

feet is leased to Clark Nexsen, an architectural firm and

approximately 23,000 square feet is leased to the

Development Authority of Virginia Beach Schedule

(1)

Development, Not Delivered

Location

Estimated

(1)

Estimated

Cost

(1)

Cost Incurred

through

12/31/2014

Start

Initial

Occupancy

Stabilized

Operation

AHH

Ownership %

Property Type

%leased

Anchor Tenants

Oceaneering

Chesapeake, VA

155,000 sf

$26,000

$22,000

4Q13

1Q15

1Q15

100%

Office

100%

Oceaneering

Sandbridge Commons

Virginia Beach, VA

70,000 sf

(2)

13,000

9,000

4Q13

1Q15

4Q15

100%

Retail

86%

Harris Teeter

Commonwealth of VA -

Chesapeake

Chesapeake, VA

36,000 sf

7,000

7,000

2Q14

1Q15

1Q15

100%

Office

100%

Commonwealth of Virginia

Commonwealth of VA -

Virginia Beach

Virginia Beach, VA

11,000 sf

3,000

3,000

2Q14

1Q15

1Q15

100%

Office

100%

Commonwealth of Virginia

Lightfoot Marketplace

Williamsburg, VA

88,000 sf

(2)

24,000

11,000

3Q14

1Q16

2Q17

60%

(3)

Retail

60%

Harris Teeter

Johns Hopkins Village

Baltimore, MD

157 units

65,000

2,000

1Q15

3Q16

4Q16

80%

Multifamily

NA

NA

138,000

54,000

Schedule

(1)

Development, Delivered Not Stabilized

Location

Estimated

(1)

Estimated

Cost

(1)

Cost Incurred

through

12/31/2014

Start

Initial

Occupancy

Stabilized

Operation

AHH

Ownership %

(1)

Property Type

%leased

Anchor Tenants

4525 Main Street

(4)

Virginia Beach, VA

239,000 sf

(3)

$50,000

$44,000

1Q13

3Q14

1Q16

100%

Office

56%

(5)

Clark Nexsen, Development Authority

of Virginia Beach

, Anthropologie

Greentree Shopping Center

Chesapeake, VA

18,000 sf

(2)

6,000

5,000

4Q13

3Q14

3Q15

100%

Retail

73%

Wawa

Encore Apartments

(4)

Virginia Beach, VA

286 units

34,000

31,000

1Q13

3Q14

4Q15

100%

Multifamily

NA

NA

Whetstone Apartments

Durham, NC

203 units

29,000

27,000

2Q13

3Q14

4Q15

100%

Multifamily

NA

NA

119,000

107,000

Schedule

Re-Development

Location

Estimated

Estimated Cost

Cost Incurred

through

12/31/2014

Start

Complete

Property Type

%leased

Anchor Tenants

Dick's at Town Center

Virginia Beach, VA

20,000 sf

$2,000

$2,000

1Q14

4Q14

Retail

100%

USI

Total

$259,000

$163,000 |

Acquisitions & Dispositions

19

$ in thousands

(1) Closed on 1/5/2015

Estimated

Pending Acquisitions

Location

Approximately

Purchase Price

Purchase Date

AHH

Ownership %

Property Type

%leased

Anchor Tenants

2 Grocery Anchor Shopping Centers

MD

185,000 sf

$39,500

1Q15

100%

Retail

90%

Grocery

Dispositions

Location

Approximately

Sale Price

Disposition

Date

AHH

Ownership %

Property Type

%leased

Anchor Tenants

Sentara Williamsburg

Williamsburg, VA

49,200 sf

$15,450

1Q15

(1)

100%

Office

100%

Sentara |

Construction Business Summary

20

$ in thousands

Gross Profit Summary

Q4 2014

YTD 2014

(Unaudited)

Revenue

$32,060

$103,321

Expense

(30,947)

(98,754)

Gross Profit

$1,113

$4,567

Location

Total Contract

Value

Work in Place as

of 12/31/2014

Backlog

Estimated Date

of Completion

Projects Greater than $5.0M

Exelon

Baltimore, MD

$168,764

$42,785

$125,979

1Q 2016

City of Suffolk Municipal Center

Suffolk, VA

25,375

23,221

2,154

2Q 2015

Four Seasons Condominium Expansion

Baltimore, MD

24,053

3,073

20,980

4Q 2015

Sub Total

218,192

69,079

149,113

Projects Less than $5.0M

144,666

134,640

10,026

Total

$362,858

$203,719

$159,139

|

Operating Results & Property-

Type Segment Analysis |

Same

Store NOI by Segment 22

(Reconciliation to GAAP located in appendix pg. 38)

$ in thousands

Three months ended 12/31

Year ended 12/31

2014

2013

$ Change

% Change

2014

2013

$ Change

% Change

Office

(1)

(Unaudited)

(Unaudited)

Revenue

$6,499

$6,353

$146

2%

$25,640

$25,117

$523

2%

Expenses

2,036

1,903

133

7%

8,208

7,816

392

5%

Net Operating Income

4,463

4,450

13

0%

17,432

17,301

131

1%

Retail

(1)

Revenue

5,780

5,684

96

2%

20,874

20,474

400

2%

Expenses

1,712

1,725

(13)

-1%

6,487

6,525

(38)

-1%

Net Operating Income

4,068

3,959

109

3%

14,387

13,949

438

3%

Multifamily

(1)

Revenue

2,974

2,784

190

7%

7,758

7,494

264

4%

Expenses

1,277

1,254

23

2%

3,555

3,441

114

3%

Net Operating Income

1,697

1,530

167

11%

4,203

4,053

150

4%

Same Store Net Operating Income (NOI), GAAP basis

$10,228

$9,939

$289

3%

$36,022

$35,303

$719

2%

Net effect of straight-line rents

(198)

(187)

(11)

6%

(1,022)

(571)

(451)

79%

Amortization of lease incentives and above (below) market rents

159

142

17

12%

716

738

(22)

-3%

Same store portfolio NOI, cash basis

$10,189

$9,894

$295

3%

$35,716

$35,470

$246

1%

Cash Basis:

Office

$4,232

$4,131

$101

2%

$16,075

$16,257

($182)

-1%

Retail

4,229

4,205

24

1%

15,422

15,140

282

2%

Multifamily

1,728

1,558

170

11%

4,219

4,073

146

4%

$10,189

$9,894

$295

3%

$35,716

$35,470

$246

1%

GAAP Basis:

Office

$4,463

$4,450

$13

0%

$17,432

$17,301

$131

1%

Retail

4,068

3,959

109

3%

14,387

13,949

438

3%

Multifamily

1,697

1,530

167

11%

4,203

4,053

150

4%

$10,228

$9,939

$289

3%

$36,022

$35,303

$719

2%

(1) See page 37 for Same Store vs. Non - Same Store Properties

|

Top 10

Tenants by Annual Base Rent 23

As of December 31, 2014

Office

Tenant

Number

of Leases

Number

of

Properties

Properties

Lease

Expiration

Annualized

Base Rent

% of Office

Portfolio

Annualized

Base Rent

% of Total

Portfolio

Annualized

Base Rent

Williams Mullen

3

2

Armada Hoffler Tower, Richmond Tower

3/22/2026

$7,978,920

33.0%

13.9%

Clark Nexsen

1

1

4525 Main Street

9/30/2029

2,390,656

9.9%

4.2%

Sentara Medical Group

1

1

Sentara Williamsburg

(1)

3/31/2023

1,006,140

4.2%

1.7%

Cherry Bekaert

3

3

Armada Hoffler Tower, Richmond Tower, Oyster Point

1/31/2025

958,984

4.0%

1.7%

Hampton University

2

1

Armada Hoffler Tower

2/28/2023

891,087

3.7%

1.5%

GSA

1

1

Oyster Point

4/26/2017

856,448

3.5%

1.5%

Troutman Sanders

1

1

Armada Hoffler Tower

1/31/2025

805,605

3.3%

1.4%

The Art Institute

1

1

Two Columbus

12/31/2019

787,226

3.3%

1.4%

Pender & Coward

1

1

Armada Hoffler Tower

1/31/2030

781,536

3.2%

1.4%

Kimley Horn

1

1

Two Columbus

12/31/2018

682,162

2.8%

1.2%

Top 10 Total

$17,138,764

70.8%

29.8%

Retail

Tenant

Number

of Leases

Number

of

Properties

Properties

Lease

Expiration

Annualized

Base Rent

% of Retail

Portfolio

Annualized

Base Rent

% of Total

Portfolio

Annualized

Base Rent

Home Depot

2

2

Broad Creek Shopping Center, North Point Center

12/3/2019

$2,189,900

9.5%

3.8%

Harris Teeter

2

2

Tyre Neck Harris Teeter, Hanbury Village

10/16/2028

1,430,532

6.2%

2.5%

Food Lion

3

3

Broad Creek Shopping Center, Bermuda Crossroads,

Gainsborough Square

3/19/2020

1,282,568

5.6%

2.2%

Dick's Sporting Goods

1

1

Dick's at Town Center

1/31/2020

798,000

3.5%

1.4%

Regal Cinemas

1

1

Harrisonburg Regal

4/23/2019

683,550

3.0%

1.2%

PetSmart

2

2

Broad Creek Shopping Center, North Point Center

7/21/2018

618,704

2.7%

1.1%

Kroger

1

1

North Point Center

8/31/2018

552,864

2.4%

1.0%

Yard House

1

1

Commerce Street Retail

11/30/2023

538,000

2.3%

0.9%

Rite Aid

2

2

Gainsborough Square, Parkway Marketplace

5/29/2019

484,193

2.1%

0.8%

Walgreens

1

1

Hanbury Village

12/31/2083

447,564

1.9%

0.8%

Top 10 Total

$9,025,875

39.3%

15.7%

(1) Sold 1/5/15 |

Office

Lease Summary 24

Renewal Lease Summary

(1)

GAAP

Cash

Quarter

Number of

Leases

Signed

Net rentable

SF Signed

Leases

Expiring

Net rentable

SF Expiring

Contractual

Rent per SF

Prior Rent

per SF

Annual

Change in

Rent per SF

Contractual

Rent per SF

Prior Rent

per SF

Annual Change

in Rent per SF

Weighted

Average Lease

Term

TI, LC, &

Incentives

TI, LC, &

Incentives

per SF

4th Quarter 2014

6

26,386

3

5,726

$21.08

$21.23

($0.15)

$20.50

$22.14

($1.65)

3.65

$182,728

$6.93

3rd Quarter 2014

3

6,859

2

6,082

18.50

19.63

(1.13)

18.48

19.85

(1.36)

2.62

68,913

10.05

2nd Quarter 2014

2

18,824

1

8,452

25.12

24.33

0.79

25.37

27.55

(2.18)

7.75

204,718

10.88

1st Quarter 2014

1

25,506

2

5,430

32.28

26.66

5.63

29.95

29.25

0.70

10.00

1,315,127

51.56

New Lease Summary

(1)

Quarter

Number of

Leases

Signed

Net rentable

SF Signed

Contractual

Rent per SF

Weighted

Average

Lease Term

TI, LC, &

Incentives

TI, LC, &

Incentives

per SF

4th Quarter 2014

1

4,754

$17.50

10.00

$103,266

$21.72

3rd Quarter 2014

2

2,853

22.65

2.56

55,892

19.59

2nd Quarter 2014

4

6,948

20.18

4.28

190,255

27.38

1st Quarter 2014

2

5,430

24.12

1.00

5,239

0.96

(1) Excludes leases for space occupied by AHH. |

Office

Lease Expirations 25

1.8%

4.0%

6.5%

18.3%

9.4%

4.9%

4.0%

5.4%

10.6%

35.2%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Year of Lease Expiration

Number of

Leases

Expiring

Square

Footage of

Leases

Expiring

% Portfolio

Net Rentable

Square Feet

Annualized

Base Rent

% of Portfolio

Annualized

Base Rent

Annualized Base

Rent per Leased

Square Foot

Available

-

43,974

4.8%

$0

-

$0.00

2015

12

17,012

1.9%

424,967

1.8%

24.98

2016

15

41,197

4.5%

977,367

4.0%

23.72

2017

6

65,186

7.1%

1,564,421

6.5%

24.00

2018

19

162,718

17.7%

4,435,761

18.3%

27.26

2019

10

95,977

10.5%

2,268,983

9.4%

23.64

2020

5

43,731

4.8%

1,176,453

4.9%

26.90

2021

4

41,363

4.5%

973,852

4.0%

23.54

2022

3

48,117

5.2%

1,295,525

5.4%

26.92

2023

4

115,889

12.6%

2,578,196

10.6%

22.25

Thereafter

8

242,998

26.5%

8,515,178

35.2%

35.04

Total / Weighted Average

86

918,162

100.0%

24,210,702

$

100.0%

$27.70 |

Retail

Lease Summary 26

Renewal Lease Summary

(1)

GAAP

Cash

Quarter

Number of

Leases

Signed

Net rentable

SF Signed

Leases

Expiring

Net

rentable SF

Expiring

Contractual

Rent per SF

Prior Rent

per SF

Annual Change

in Rent per SF

Contractual

Rent per SF

Prior Rent

per SF

Annual Change

in Rent per SF

Weighted

Average Lease

Term

TI, LC, &

Incentives

TI, LC, &

Incentives

per SF

4th Quarter 2014

6

17,361

2

2,991

$24.91

$21.35

$3.57

$24.80

$23.10

$1.71

4.37

$18,858

$1.09

3rd Quarter 2014

6

26,900

3

6,012

17.64

16.19

1.45

17.76

16.98

0.78

5.11

44,109

1.64

2nd Quarter 2014

6

12,916

2

3,842

20.47

19.66

0.81

20.20

20.65

(0.46)

1.87

5,730

0.44

1st Quarter 2014

5

23,857

3

6,540

20.84

20.41

0.43

21.18

21.82

(0.64)

4.55

63,339

2.65

New Lease Summary

(1)

Quarter

Number of

Leases

Signed

Net rentable

SF Signed

Contractual

Rent per SF

Weighted

Average

Lease Term

TI, LC, &

Incentives

TI, LC, &

Incentives

per SF

4th Quarter 2014

1

2,140

$16.00

5.00

$2,140

$1.00

3rd Quarter 2014

7

35,574

20.30

6.83

522,738

14.69

2nd Quarter 2014

4

10,574

25.73

7.78

1,071,485

101.33

1st Quarter 2014

1

3,160

16.25

10.50

126,558

40.05

(1) Excludes leases from space occupied by AHH |

Retail

Lease Expiration 27

Year of Lease Expiration

Number of

Leases

Expiring

Square

Footage of

Leases

Expiring

% Portfolio

Net Rentable

Square Feet

Annualized

Base Rent

% of Portfolio

Annualized

Base Rent

Annualized Base

Rent per Leased

Square Foot

Available

-

43,386

3.6%

$0

-

$0.00

2015

16

51,906

4.3%

1,063,979

5.4%

20.50

2016

23

73,259

6.1%

1,651,561

8.4%

22.54

2017

25

152,603

12.7%

2,223,266

11.4%

14.57

2018

23

136,687

11.4%

2,034,025

10.4%

14.88

2019

25

327,441

27.3%

4,795,310

24.5%

14.64

2020

18

200,877

16.7%

2,770,104

14.1%

13.79

2021

5

25,204

2.1%

740,832

3.8%

29.39

2022

6

83,588

7.0%

1,216,663

6.2%

14.56

2023

6

49,460

4.1%

1,331,093

6.8%

26.91

Thereafter

11

56,327

4.7%

1,759,270

9.0%

31.23

Total / Weighted Average

158

1,200,738

100.0%

19,586,105

$

100.0%

$16.92

5.4%

8.4%

11.4%

10.4%

24.5%

14.1%

3.8%

6.2%

6.8%

9.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0% |

Historical

Occupancy 28

(1) Office and retail occupancy based on occupied square feet as a % of respective

total (2) Multifamily occupancy based on occupied units as a % of respective total

(3) Total occupancy weighted by annualized base rent

Occupancy -

All Properties

as of

Sector

12/31/2014

9/30/2014

6/30/2014

3/31/2014

12/31/2013

Office

(1)

95.2%

94.8%

95.3%

95.4%

95.2%

Retail

(1)

96.4%

94.7%

93.5%

93.4%

93.4%

Multifamily

(2)

95.7%

96.6%

94.9%

94.2%

94.2%

Weighted Average

(3)

95.7%

95.1%

94.6%

94.5%

94.4% |

Multifamily Occupancy

29

Occupancy Summary - Smiths Landing (284 available units)

Quarter Ended

Number of Units

Occupied

Percentage

Occupied

(1)

Annualized Base

Rent

(2)

Average Monthly Rent

per Occupied Unit

12/31/2014

278

97.9%

$3,472,020

$1,041

9/30/2014

274

96.5%

3,379,428

1,028

6/30/2014

273

96.1%

3,321,096

1,014

3/31/2014

283

99.6%

3,430,260

1,010

12/31/2013

282

99.3%

3,382,380

1,000

Occupancy

Summary - The Cosmopolitan (342 available units) Quarter Ended

Number of Units

Occupied

Percentage

Occupied

(1)

Annualized Base

Rent

(2)(4)

Average Monthly Rent

per Occupied Unit

(3)

12/31/2014

321

93.9%

$6,052,488

$1,571

9/30/2014

331

96.8%

6,218,892

1,566

6/30/2014

321

93.9%

6,042,132

1,569

3/31/2014

307

89.8%

5,799,564

1,574

12/31/2013

308

90.1%

5,721,144

1,548

(1) Total units occupied as of each respective date

(2)

Annualized base rent is calculated by multiplying (a) contractual rent due from our tenants

for the last month of the respective quarter by (b) 12 (3)

Average Monthly Rent per Occupied Unit is calculated as (a) annualized base

rent divided by (b) the number of occupied units as of the end of the respective date.

(4)

Excludes annualized base rent from retail leases

|

30

Components of NAV

Stabilized Portfolio NOI x Market Cap Rate = Stabilized Portfolio Value

Investment in Unstabilized Development Pipeline

Stabilized

Development

Pipeline

NOI

x

Market

Cap

Rate

=

Stabilized

Development

Portfolio

Value

Annualized General Contracting and Real Estate Services x Appropriate Multiple = TRS

Value Other Assets

Liabilities

NAV |

Net

Asset Value Component Data 31

$ in thousands

(1) Includes leases for space occupied by Armada Hoffler which are eliminated for GAAP

purposes (2) Completed Not Stabilized properties are presented in our Consolidated

Balance Sheet as Income Producing Property Stabilized Portfolio NOI (Cash)

Other Assets

Three months

ended

Annualized

As of 12/31/2014

12/31/2014

12/31/2014

Other Assets

Diversified

Portfolio

Cash and Cash Equivalents

$25,883

Office

$2,050

$8,200

Restricted Cash

4,224

Retail

3,493

13,972

Accounts Receivable

20,548

Multifamily

613

2,452

Construction receivables, including retentions

19,432

Total Diversified Portfolio NOI

$6,156

$24,624

Other Assets

33,380

Total Other Assets

$103,467

Virginia

Beach

Town Center

Office

(1)

$2,338

$9,352

Liabilities & Share Count

Retail

(1)

1,252

5,008

As of 12/31/2014

Multifamily

1,115

4,460

Liabilities

Total Virginia Beach Town Center NOI

$4,705

$18,820

Mortgages and notes payable

$359,229

Accounts payable and accrued liabilities

8,358

Stabilized Portfolio NOI (Cash)

$10,861

$43,444

Construction payables, including retentions

42,399

Other Liabilities

19,014

Development Pipeline

Total Liabilities

$429,000

12/31/2014

Construction in Progress: (pg. 9 balance sheet)

$81,082

Three months

ended

99,115

Share Count

12/31/2014

Weighted Average Common Shares Outstanding

25,020

Taxable REIT Subsidiary (TRS)

Weighted Average Operating Partnership ("OP") Units Outstanding

14,776

Full Year

Total Weighted Average Common shares and OP units outstanding

39,796

12/31/2014

General Contracting and Real Estate Services

$4,567

Development Pipeline Completed Not Stabilized at Cost

(2)

|

Appendix –

Definitions & Reconciliations |

Definitions

Net Operating Income:

Funds From Operations:

33

We calculate Net Operating Income (“NOI”) as property revenues (base rent,

expense reimbursements and other revenue) less property expenses (rental

expenses and real estate taxes). For our office, retail and multifamily

segments, NOI excludes general contracting and real estate services expenses,

depreciation and amortization, general and administrative expenses, and

impairment charges. Other REITs may use different methodologies for calculating

NOI, and accordingly, our NOI may not be comparable to such other REITs’

NOI. NOI is not a measure of operating income or cash flows from operating

activities as measured by GAAP and is not indicative of cash available to fund

cash needs. As a result, net operating income should not be considered an alternative

to cash flows as a measure of liquidity. We consider NOI to be an

appropriate supplemental measure to net income because it assists both investors

and management in understanding the core operations of our real estate business.

(Reconciliation to GAAP located in appendix pg. 40)

We calculate Funds From Operations (“FFO”) in accordance with the standards

established by the National Association of Real Estate Investment Trusts

(“NAREIT”). NAREIT defines FFO as net income (loss) (calculated in accordance with

accounting principles generally accepted in the United States (“GAAP”)),

excluding gains (or losses) from sales of depreciable operating property, real

estate related depreciation and amortization (excluding amortization of deferred

financing costs) and after adjustments for unconsolidated partnerships and joint

ventures. FFO is a supplemental non-GAAP financial measure. Management uses FFO as a

supplemental performance measure because it believes that FFO is beneficial to

investors as a starting point in measuring our operational performance.

Specifically, in excluding real estate related depreciation and amortization and gains

and losses from property dispositions, which do not relate to or are not

indicative of operating performance, FFO provides a performance measure that,

when compared year over year, captures trends in occupancy rates, rental rates and operating costs.

Other equity REITs may not calculate FFO in accordance with the NAREIT definition as we

do, and, accordingly, our FFO may not be comparable to such other REITs’

FFO. |

Definitions

Normalized Funds From Operations:

Core Funds From Operations:

34

We calculate Core Funds From Operations ("Core FFO") as Normalized FFO adjusted

for mark-to-market adjustments on interest rate derivatives, noncash

stock compensation expense and the impact of development pipeline projects that

are still in lease-up. We generally consider a property to be in lease-up

until the earlier of (i) the quarter after which the property reaches 80%

occupancy or (ii) the thirteenth quarter after the property receives its certificate of

occupancy.

Management believes that the computation of FFO in accordance to NAREIT’s

definition includes certain items that are not indicative of the results

provided by the Company’s operating portfolio and affect the comparability of the

Company’s period-over-period performance. Our calculation of Core

FFO differs from NAREIT's definition of FFO. Other equity REITs may not

calculate Core FFO in the same manner as us, and, accordingly, our Core FFO may not be

comparable to other REITs' Core FFO.

We calculate Normalized Funds From Operations (“Normalized FFO") as FFO

calculated in accordance with the standards established by NAREIT, adjusted for

acquisition, development and other pursuit costs, gains or losses from the early

extinguishment of debt, impairment charges, mark-to-market adjustments on interest rate derivatives and

other nonrecurring or noncomparable items.

Management believes that the computation of FFO in accordance to NAREIT’s

definition includes certain items that are not indicative of the results

provided by the Company’s operating portfolio and affect the comparability of the

Company’s period-over-period performance. Our calculation of

Normalized FFO differs from NAREIT's definition of FFO Other equity REITs may not

calculate Normalized FFO in the same manner as us, and, accordingly, our Normalized FFO

may not be comparable to other REITs' Normalized FFO.

|

Definitions

Adjusted Funds From Operations:

EBITDA:

35

We calculate Adjusted Funds From Operations (“AFFO”) as Core FFO, (i)

excluding the impact of tenant improvement and leasing commission costs, capital

expenditures, the amortization of deferred financing fees, derivative (income)

loss, the net effect of straight-line rents and the amortization of lease

incentives and net above (below) market rents and (ii) adding back the impact of

development pipeline projects that are still in lease-up and government

development grants that are not included in FFO.

Management believes that AFFO provides useful supplemental information to investors

regarding our operating performance as it provides a consistent comparison of

our operating performance across time periods and allows investors to more

easily compare our operating results with other REITs. However, other REITs may use different

methodologies for calculating AFFO or similarly entitled FFO measures and, accordingly,

our AFFO may not always be comparable to AFFO or other similarly entitled FFO

measures of other REITs. We calculate EBITDA as net income (loss) (calculated in accordance with GAAP),

excluding interest expense, income taxes and depreciation and amortization.

Management believes EBITDA is useful to investors in evaluating and facilitating

comparisons of our operating performance between periods and between REITs by removing the impact of

our capital structure (primarily interest expense) and asset base (primarily

depreciation and amortization) from our operating results. |

Definitions

Core EBITDA:

We calculate Core EBITDA as EBITDA, excluding certain items, including, but not limited

to, non-recurring or extraordinary gains (losses), early extinguishment of

debt, derivative (income) losses, acquisition costs and the impact of

development pipeline projects that are still in lease-up. We generally consider a property to be in lease-up until the

earlier of (i) the quarter after which the property reaches 80% occupancy or (ii) the

thirteenth quarter after the property receives its certificate of occupancy.

Management believes that Core EBITDA provides useful supplemental information to

investors regarding our ongoing operating performance as it provides a consistent comparison of our

operating performance across time periods and allows investors to more easily compare

our operating results with other REITs. However, other REITs may use different

methodologies for calculating Core EBITDA or similarly entitled measures and,

accordingly, our Core EBITDA may not always be comparable to Core EBITDA or other similarly entitled measures

of other REITs.

Core Debt:

We calculate Core Debt as our total debt, excluding any construction loans associated

with our development pipeline. Same Store Portfolio:

We define same store properties as including those properties that were owned and

operated for the entirety of the period being presented and excluding properties

that were in lease-up during the period present. We generally

consider

a

property

to

be

in

lease-up

until

the

earlier

of

(i)

the

quarter

after

which

the

property

reaches

80%

occupancy

or (ii) the thirteenth quarter after the property receives its certificate of

occupancy. The following table shows the properties included in the same

store and non-same store portfolio for the comparative periods presented.

36 |

Same

Store vs. Non-Same Store Properties 37

Same Store

Non-Same Store

Same Store

Non-Same Store

Office Properties

Armada Hoffler Tower

X

X

One Columbus

X

X

Two Columbus

X

X

Richmond Tower

X

X

Oyster Point

X

X

Sentara Williamsburg

X

X

4525 Main Street

X

X

Virginia Natural Gas

X

X

Retail Properties

Bermuda Crossroads

X

X

Broad Creek Shopping Center

X

X

Courthouse 7-Eleven

X

X

Dimmock Square

X

X

Gainsborough Square

X

X

Hanbury Village

X

X

North Point Center

X

X

Parkway Marketplace

X

X

Harrisonburg Regal

X

X

Dick’s at Town Center

X

X

249 Central Park Retail

X

X

Studio 56 Retail

X

X

Commerce Street Retail

X

X

Fountain Plaza Retail

X

X

South Retail

X

X

Tyre Neck Harris Teeter

X

X

Greentree Shopping Center

X

X

Multifamily Properties

Encore Apartments

X

X

Smith’s Landing

X

X

The Cosmopolitan

X

X

Liberty Apartments

X

X

Whetstone Apartments

X

X

Comparison of Year Ended

December 31, 2014 to 2013

Comparison of Three Months Ended

December 31, 2014 to 2013 |

Reconciliation to GAAP -

Segment Portfolio NOI

38

$ in thousands

(1) See page 37 for Same Store vs. Non-Same Store Properties

Three months ended 12/31

Year ended 12/31

2014

2013

2014

2013

Office Same Store

(1)

Rental revenues

$6,499

$6,353

$25,640

$25,117

Property expenses

2,036

1,903

8,208

7,816

NOI

4,463

4,450

17,432

17,301

Non-Same Store NOI

744

149

1,685

601

Segment NOI

$5,207

$4,599

$19,117

$17,902

Retail Same Store

(1)

Rental revenues

$5,780

$5,684

$20,874

$20,474

Property expenses

1,712

1,725

6,487

6,525

NOI

4,068

3,959

14,387

13,949

Non-Same Store NOI

531

-

2,461

1,027

Segment NOI

$4,599

$3,959

$16,848

$14,976

Multifamily Same Store

(1)

Rental revenues

$2,974

$2,784

$7,758

$7,494

Property expenses

1,277

1,254

3,555

3,441

NOI

1,697

1,530

4,203

4,053

Non-Same Store NOI

69

-

2,168

1,440

Segment NOI

1,766

1,530

$6,371

$5,493

Total Segment Portfolio NOI

$11,572

$10,088

$42,336

$38,371 |

Reconciliation to GAAP -

Segment Portfolio NOI

39

$ in thousands

Three months ended 12/31/2014

Diversified Portfolio

Office

Retail

Multifamily

Total

Cash NOI

$2,050

$3,493

$613

$6,156

Net effect of straight-line rents

192

(100)

(13)

79

Amortization of lease incentives and (above) below market rents

(12)

46

(13)

21

GAAP NOI

$2,230

$3,439

$587

$6,256

Town Center of Virginia Beach

Office

Retail

Multifamily

Total

Cash NOI

$2,338

$1,252

$1,115

$4,705

Net effect of straight-line rents

79

53

(5)

127

Amortization of lease incentives and (above) below market rents

(28)

(145)

-

(173)

Elimination of AHH rent

(156)

(74)

-

(230)

GAAP NOI

$2,233

$1,086

$1,110

$4,429

GAAP NOI

Office

Retail

Multifamily

Total

Diversified Portfolio

$2,230

$3,439

$587

$6,256

Town Center of Virginia Beach

2,233

1,086

1,110

4,429

Unstabilized Properties

744

74

69

887

Total Segment Portfolio GAAP NOI

$5,207

$4,599

$1,766

$11,572 |

Reconciliation to GAAP -

Segment Portfolio NOI

$ in thousands

40

Office

Retail

Multifamily

Total Rental

Properties

General Contracting &

Real Estate Services

Total

Segment revenues

7,464

$

6,397

$

3,660

$

17,521

$

32,060

$

49,581

$

Segment expenses

2,257

1,798

1,894

5,949

30,947

36,896

Net operating income

5,207

$

4,599

$

1,766

$

11,572

$

1,113

$

12,685

$

Depreciation and amortization

(4,976)

General and administrative expenses

(1,943)

Acquisition, development and other pursuit costs

(55)

Impairment charges

-

Interest expense

(2,671)

Gain on dispositions

2,211

Other expense

(90)

Income tax benefit

65

Net income

5,226

$

Office

Retail

Multifamily

Total Rental

Properties

General Contracting &

Real Estate Services

Total

Segment revenues

27,827

$

23,956

$

12,963

$

64,746

$

103,321

$

168,067

$

Segment expenses

8,710

7,108

6,592

22,410

98,754

121,164

Net operating income

19,117

$

16,848

$

6,371

$

42,336

$

4,567

$

46,903

$

Depreciation and amortization

(17,569)

General and administrative expenses

(7,711)

Acquisition, development and other pursuit costs

(229)

Impairment charges

(15)

Interest expense

(10,648)

Gain on dispositions

2,211

Other expense

(113)

Income tax provision

(70)

Net income

12,759

$

Three months ended 12/31/2014

Year ended 12/31/2014 |