Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - US BANCORP \DE\ | d869270d8k.htm |

Credit

Suisse Financial Services Forum 2015

February 11, 2015

Kathy Rogers

Vice Chairman and CFO

P.W. (Bill) Parker

Vice Chairman, Chief Risk Officer

EXTENDING

THE ADVANTAGE

Exhibit 99.1

1 |

EXTENDING

THE

ADVANTAGE

2

Forward-looking Statements and Additional Information

The

following

information

appears

in

accordance

with

the

Private

Securities

Litigation

Reform

Act

of

1995:

This

presentation

contains

forward-looking

statements

about

U.S.

Bancorp.

Statements

that

are

not

historical

or

current

facts,

including

statements

about beliefs and expectations, are forward-looking statements and are based on

the information available to, and assumptions and estimates made by,

management

as

of

the

date

made.

These

forward-looking

statements

cover,

among

other

things,

anticipated

future

revenue

and

expenses

and

the

future

plans

and

prospects

of

U.S.

Bancorp.

Forward-looking

statements

involve

inherent

risks

and

uncertainties,

and

important

factors

could

cause

actual

results

to

differ

materially

from

those

anticipated.

A

reversal

or

slowing

of

the

current

economic

recovery

or

another

severe

contraction

could

adversely

affect

U.S.

Bancorp’s

revenues

and

the

values

of

its

assets

and

liabilities.

Global

financial

markets

could

experience

a

recurrence

of significant turbulence, which could reduce the availability of funding to

certain financial institutions and lead to a tightening of credit, a reduction of

business activity, and increased market volatility. Stress in the commercial

real estate markets, as well as a downturn in the residential real estate

markets, could cause credit losses and deterioration in asset values. In

addition, U.S. Bancorp’s business and financial performance is likely to be

negatively

impacted

by

recently

enacted

and

future

legislation

and

regulation.

U.S.

Bancorp’s

results

could

also

be

adversely

affected

by

deterioration

in

general

business

and

economic

conditions;

changes

in

interest

rates;

deterioration

in

the

credit

quality

of

its

loan

portfolios

or

in

the

value of the collateral securing those loans; deterioration in the value of

securities held in its investment securities portfolio; legal and regulatory

developments;

increased

competition

from

both

banks

and

non-banks;

changes

in

customer

behavior

and

preferences;

breaches

in

data

security;

effects of mergers and acquisitions and related integration; effects of critical

accounting policies and judgments; and management’s ability to

effectively manage credit risk, residual value risk, market risk, operational risk,

interest rate risk and liquidity risk. For

discussion

of

these

and

other

risks

that

may

cause

actual

results

to

differ

from

expectations,

refer

to

U.S.

Bancorp’s

Annual

Report

on

Form 10-K for the year ended December 31, 2013, on file with the Securities and

Exchange Commission, including the sections entitled “Risk

Factors”

and “Corporate Risk Profile”

contained in Exhibit 13, and all subsequent filings with the Securities and

Exchange Commission under Sections 13(a), 13(c), 14 or 15(d) of the

Securities Exchange Act of 1934. Forward-looking statements speak only as of the date they are made, and

U.S. Bancorp undertakes no obligation to update them in light of

new information or future events.

This

presentation

includes

non-GAAP

financial

measures

to

describe

U.S.

Bancorp’s

performance.

The

calculations

of

these

measures

are

provided

within

or

in

the

appendix

of

the

presentation.

These

disclosures

should

not

be

viewed

as

a

substitute

for

operating

results

determined

in

accordance with GAAP, nor are they necessarily comparable to non-GAAP

performance measures that may be presented by other companies. |

EXTENDING

THE

ADVANTAGE

3

Agenda

Overview

Financial Management

Capital Management

Loan Growth / Credit Quality

1Q15 Update

Long-term Goals |

EXTENDING

THE

ADVANTAGE

4

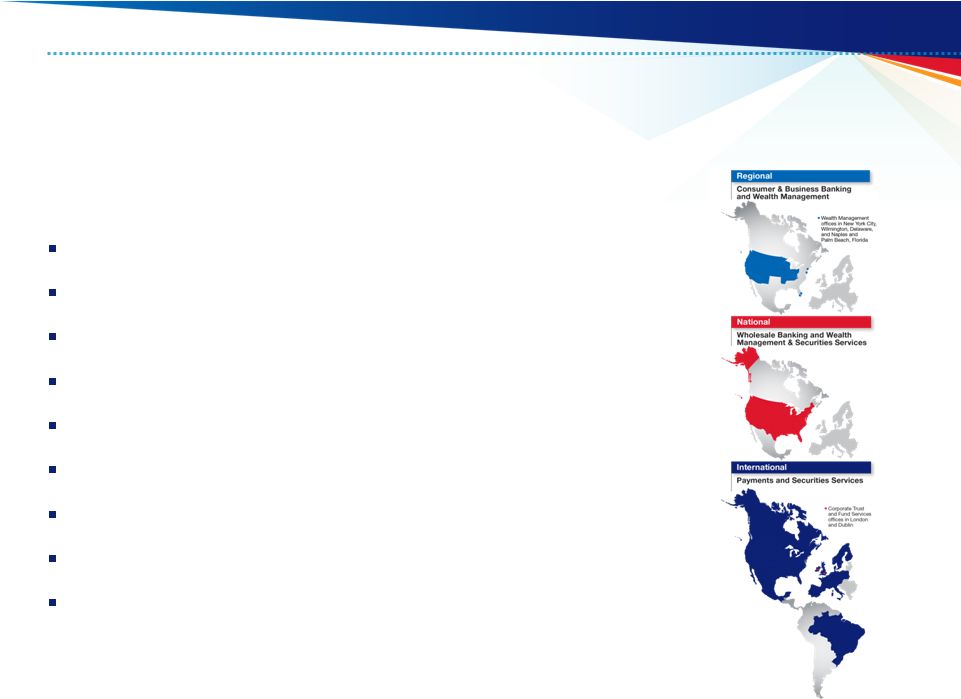

U.S. Bancorp Dimensions

Asset Size

$403 billion

Deposits

$283 billion

Loans

$248 billion

Customers

18.5 million

NYSE Traded

USB

Market Capitalization*

$75 billion

Founded

1863

Bank Branches

3,176

ATMs

5,022

4Q14 Dimensions

* As of 1/30/15 |

EXTENDING

THE

ADVANTAGE

5

Industry Positions

Source: company reports, SNL and FactSet

Assets and deposits as of 12/31/14, market value as of 1/30/15

U.S.

U.S.

U.S.

Rank

Company

$ Billions

Rank

Company

$ Billions

Rank

Company

$ Billions

1

J.P. Morgan

$2,527

1

J.P. Morgan

$1,363

1

Wells Fargo

$268

2

Bank of America

2,105

2

Wells Fargo

1,168

2

J.P. Morgan

202

3

Citigroup

1,843

3

Bank of America

1,119

3

Bank of America

159

4

Wells Fargo

1,687

4

Citigroup

899

4

Citigroup

142

5

U.S. Bancorp

403

5

U.S. Bancorp

283

5

U.S. Bancorp

75

6

PNC

345

6

PNC

232

6

PNC

44

7

SunTrust

190

7

SunTrust

141

7

BB&T

25

8

BB&T

187

8

BB&T

129

8

SunTrust

20

9

Fifth Third

139

9

Fifth Third

102

9

Fifth Third

14

10

Regions

120

10

Regions

94

10

Regions

12

Assets

Deposits

Market Value |

EXTENDING

THE

ADVANTAGE

6

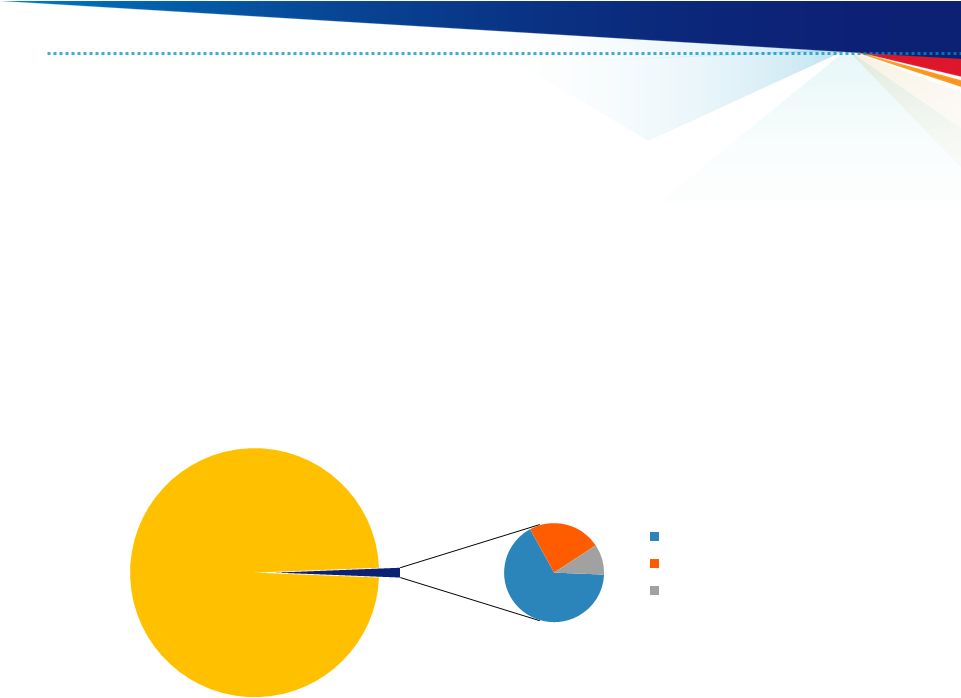

Revenue Mix

By Business Line

Consumer and

Small Business

Banking

41%

Payment Services

30%

Wealth Mgmt and

Securities Services

11%

Wholesale

Banking and

Commercial

Real Estate

18%

Fee Income / Total Revenue

Full year 2014, taxable-equivalent basis, excluding securities gains (losses)

net 2014

fee

income

excludes

$214

million

Visa

gain

and

$124

million

Nuveen

gain

Revenue percentages exclude Treasury and Corporate Support, see Appendix for

calculation Diversified Business Mix |

EXTENDING

THE

ADVANTAGE

7

Agenda

Overview

Financial Management

Capital Management

Loan Growth / Credit Quality

1Q15 Update

Long-term Goals |

EXTENDING

THE ADVANTAGE

8

Peer Banks

Peer Bank Ticker Symbols

BAC

Bank of America

PNC

PNC

BBT

BB&T

RF

Regions

FITB

Fifth Third

STI

SunTrust

JPM

J.P. Morgan

USB

U.S. Bancorp

KEY

KeyCorp

WFC

Wells Fargo

Bank of America

SunTrust

Wells Fargo

KeyCorp

BBT

Fifth Third

Regions

PNC

J.P. Morgan

U.S. Bancorp |

EXTENDING

THE ADVANTAGE

9

Source: SNL and company reports; Peer banks: BAC, BBT, FITB, JPM, KEY, PNC, RF, STI

and WFC Efficiency ratio computed as noninterest expense divided by the sum

of net interest income on a taxable-equivalent basis and noninterest income excluding securities gains (losses)

Industry Leading Returns

Return on

Average Assets

Return on Average

Common Equity

Efficiency Ratio

Full Year 2014

4Q14 |

EXTENDING

THE

ADVANTAGE

10

Efficient Expense Platform

Single processing platforms

Full consolidation of acquisitions

Operating scale in all significant

businesses

Business line monthly review

process

2014 Efficiency Ratio

Source of

Competitive Advantage

Source: SNL and company reports; Peer banks: BAC, BBT, FITB, JPM, KEY, PNC, RF, STI

and WFC Efficiency ratio computed as noninterest expense divided by the sum

of net interest income on a taxable-equivalent basis and noninterest income excluding securities gains (losses) |

EXTENDING

THE

ADVANTAGE

11

Debt ratings: holding company as of 1/30/15

op=outlook positive

on=outlook negative

s=outlook stable

wn=watch negative

wp=watch positive

Flight to quality

Funding advantage

Advantages

Peer Debt Ratings

Top of Class Debt Ratings

Rating

Outlook

Rating

Outlook

Rating

Outlook

Rating

Outlook

USB

A1

s

A+

s

AA-

s

AA

s

WFC

A2

s

A+

on

AA-

s

AA

s

BBT

A2

on

A-

s

A+

s

A (high)

s

JPM

A3

s

A

on

A+

s

A (high)

s

PNC

A3

s

A-

s

A+

s

A (high)

s

FITB

Baa1

s

BBB+

s

A

s

A (low)

s

BAC

Baa2

s

A-

on

A

on

A (low)

s

STI

Baa1

s

BBB+

s

BBB+

op

A (low)

s

KEY

Baa1

s

BBB+

s

A-

s

BBB (high)

s

RF

Ba1

op

BBB

s

BBB

s

BBB

s

Moody's

S&P

Fitch

DBRS |

EXTENDING

THE

ADVANTAGE

12

Agenda

Overview

Financial Management

Capital Management

Loan Growth / Credit Quality

1Q15 Update

Long-term Goals |

EXTENDING

THE

ADVANTAGE

13

Capital Requirement

* Based on the final rules for the Basel III fully implemented standardized

approach Earnings Distribution Target

8.0%

Internal

Buffer

1.0%

2.5%

Capital

Conservation

Buffer

4.5%

Minimum

Capital

Requirement

9.0%*

Common Equity Tier 1

Basel III Target

USB 4Q14

Reported

Capital Management

Reinvest and

Acquisitions

Dividends

Share

Repurchases

20 -

40%

30 -

40%

30 -

40%

Dividends

30%

Reinvestment

30%

Share Repurchases

40%

Assumed ROTCE

20%

Discretionary Distributions

70%

Balance Sheet Growth

6%

Hypothetical Earnings Distribution Example |

EXTENDING

THE

ADVANTAGE

14

62%

11%

32%

Payout Ratio

71%

Capital Distributions

72%

Comprehensive Capital Analysis

and Review (CCAR) capital plan

was submitted in January

CCAR results expected to be

published by March 31, 2015

PPNR = Pre-Provision Net Revenue

Source: Federal Reserve, estimates in the severely adverse scenario

|

EXTENDING

THE

ADVANTAGE

15

Agenda

Overview

Financial Management

Capital Management

Loan Growth / Credit Quality

1Q15 Update

Long-term Goals |

EXTENDING

THE

ADVANTAGE

16

$ in millions

Prior 5 Years

Average Balances

Year-Over-Year Growth

3.9%

4.4%

6.9%

5.6%

6.3%

Prior 5 Quarters

Average Balances

Year-Over-Year Growth

5.7%

6.0%

6.8%

6.3%

5.9%

Loan Growth |

EXTENDING

THE

ADVANTAGE

17

$ in millions

Net Charge-offs

Net Charge-offs (Left Scale)

NCOs to Avg Loans (Right Scale)

Credit Quality

Nonperforming Assets

Nonperforming Assets (Left Scale)

NPAs to Loans plus ORE (Right Scale) |

EXTENDING

THE

ADVANTAGE

18

Credit Quality

Source: SNL and company reports

Strong credit culture

•

Lowest net charge-off volatility in peer group from 1Q03 –

4Q14

Minimum/Maximum

NCO%

4Q14 NCO%

NCO Volatility |

EXTENDING

THE

ADVANTAGE

19

Credit Quality

Source: company reports, reserve release is calculated as net charge-offs less

provision for credit losses Strong credit culture

•

Reserve build was less than peers –

now have modest releases

Reserve Release / Net Income

(Full Year 2014) |

EXTENDING

THE

ADVANTAGE

20

Small Business

Card Growth

Ongoing benefit of

2009+ Originations

Net Charge-offs -

USB Normalized

•

Overall normalized loss rate 0.95% -

1.00%

•

Actual losses now well below normalized

Credit Risk Management

* Includes commercial and commercial real estate

Normalized

Normalized

Loan Portfolio

NCO%

Loan Portfolio

NCO%

Commercial

0.45%

Commercial

0.45%

Commercial Real Estate

0.50%

Commercial Real Estate

0.50%

Small Business*

1.75%

Small Business*

1.85%

Residential Mortgages

0.60%

Residential Mortgages

0.50%

Credit Cards

5.00%

Credit Cards

5.00%

Other Retail

1.00%

Other Retail

1.00%

Covered Assets

0.25%

Covered Assets

0.25%

Total

1.00%

Total

Investor Day 2Q13

Current |

EXTENDING

THE

ADVANTAGE

21

Energy Lending

A limited, managed exposure

•

$11.5

billion

in

commitments,

$3.1

billion

funded

(1.3%

of

total

loans)

•

~70% of commitments rated investment grade or equivalent

•

Low energy prices are expected to help consumer spending in areas such

as services and restaurants

Exploration and Production

Midstream

Oil Field Service

Providers and Refiners

Total Loans

($247.9B)

Energy Loans

($3.1B)

66%

24%

10%

Energy |

EXTENDING

THE

ADVANTAGE

22

Overview

Financial Management

Capital Management

Loan Growth / Credit Quality

1Q15 Update

Long-term Goals

Agenda |

EXTENDING

THE

ADVANTAGE

23

1Q15 Update

Business Climate

Loan Growth

Net Interest Margin

Credit Quality

Noninterest Income / Expense |

EXTENDING

THE

ADVANTAGE

24

Overview

Financial Management

Capital Management

Loan Growth / Credit Quality

1Q15 Update

Long-term Goals

Agenda |

EXTENDING

THE

ADVANTAGE

25

Long-term Goals

Optimal business line mix

Investments generating

positive returns

Profitability:

•

ROE 16-19%

•

ROA 1.60-1.90%

•

Efficiency Ratio low 50s

Capital distributions:

•

Earnings distribution 60-80%

Current Status

Four simple and stable business lines

Mortgage, wealth management, corporate

banking, international payments, branch

technology, internet and mobile channels,

and select acquisitions

2014 Profitability:

•

ROE 14.7%

•

ROA 1.54%

•

Efficiency Ratio 53.2%

2014 Capital distributions:

•

Distributed 72% of earnings

(dividends 31%, share repurchases 41%)

Long-term Goals |

EXTENDING

THE

ADVANTAGE

26

Appendix |

EXTENDING

THE

ADVANTAGE

27

Non-GAAP Financial Measures

$ in millions

4Q14

3Q14

2Q14

1Q14

4Q13

Total equity

44,168

$

43,829

$

43,386

$

42,743

$

41,807

$

Preferred stock

(4,756)

(4,756)

(4,756)

(4,756)

(4,756)

Noncontrolling interests

(689)

(688)

(686)

(689)

(694)

Goodwill (net of deferred tax liability) (1)

(8,403)

(8,503)

(8,548)

(8,352)

(8,343)

Intangible assets, other than mortgage servicing rights

(824)

(877)

(925)

(804)

(849)

Tangible common equity (a)

29,496

29,005

28,471

28,142

27,165

Tangible common equity (as calculated above)

29,496

29,005

28,471

28,142

27,165

Adjustments (2)

172

187

224

239

224

Common equity tier 1 capital estimated for the Basel III fully

implemented standardized and advanced approaches (b)

29,668

29,192

28,695

28,381

27,389

Tier 1 capital, determined in accordance with prescribed

regulatory requirements using Basel I definition

33,386

Preferred stock

(4,756)

Noncontrolling interests, less preferred stock not eligible for Tier 1 capital

(688)

Tier 1 common equity using Basel I definition (c)

27,942

(1)

Includes goodwill related to certain investments in unconsolidated financial institutions per

prescribed regulatory requirements beginning March 31, 2014. (2)

Includes net losses on cash flow hedges included in accumulated other comprehensive income and other

adjustments. (3)

2014 amounts calculated under the Basel III transitional standardized approach; December 31, 2013

calculated under Basel I. (4)

Includes higher risk-weighting for unfunded loan commitments, investment securities, residential

mortgages, mortgage servicing rights and other adjustments. (5)

Primarily reflects higher risk-weighting for mortgage servicing rights.

|

EXTENDING

THE

ADVANTAGE

28

Non-GAAP Financial Measures

$ in millions

4Q14

3Q14

2Q14

1Q14

4Q13

Total assets

402,529

$

391,284

$

389,065

$

371,289

$

364,021

$

Goodwill (net of deferred tax liability) (1)

(8,403)

(8,503)

(8,548)

(8,352)

(8,343)

Intangible assets, other than mortgage servicing rights

(824)

(877)

(925)

(804)

(849)

Tangible assets (d)

393,302

381,904

379,592

362,133

354,829

Risk-weighted assets, determined in accordance with prescribed

regulatory requirements (3)(e)

317,398

*

311,914

309,929

302,841

297,919

Adjustments (4)

11,110

*

12,837

12,753

13,238

13,712

Risk-weighted assets estimated for the Basel III fully implemented

standardized approach (f)

328,508

*

324,751

322,682

316,079

311,631

Risk-weighted assets, determined in accordance with prescribed

transitional advanced approaches regulatory requirements

248,596

*

243,909

241,929

Adjustments (5)

3,270

*

3,443

3,383

Risk-weighted assets estimated for the Basel III fully implemented

251,866

*

247,352

245,312

advanced approaches (g)

Ratios

Tangible common equity to tangible assets (a)/(d)

7.5

%

7.6

%

7.5

%

7.8

%

7.7

%

Tangible common equity to risk-weighted assets (a)/(e)

9.3

9.3

9.2

9.3

9.1

Tier 1 common equity to risk-weighted assets using Basel I definition (c)/(e)

--

--

--

--

9.4

Common equity tier 1 capital to risk-weighted assets estimated for the

Basel III fully implemented standardized approach (b)/(f)

9.0

9.0

8.9

9.0

8.8

Common equity tier 1 capital to risk-weighted assets estimated for the

Basel III fully implemented advanced approaches (b)/(g)

11.8

11.8

11.7

* Preliminary data. Subject to change prior to filings with applicable regulatory

agencies. (1)

Includes goodwill related to certain investments in unconsolidated financial institutions per

prescribed regulatory requirements beginning March 31, 2014. (2)

Includes net losses on cash flow hedges included in accumulated other comprehensive income and other

adjustments. (3)

2014 amounts calculated under the Basel III transitional standardized approach; December 31, 2013

calculated under Basel I. (4)

Includes higher risk-weighting for unfunded loan commitments, investment securities, residential

mortgages, mortgage servicing rights and other adjustments. (5)

Primarily reflects higher risk-weighting for mortgage servicing rights.

|

EXTENDING

THE

ADVANTAGE

29

Taxable-equivalent basis, excluding securities gains (losses) net

Line of Business Financial Performance

Non-GAAP Financial Measures

$ in millions

Revenue

Line of Business Financial Performance

FY 2014

Wholesale Banking and Commercial Real Estate

3,037

$

Consumer and Small Business Banking

6,915

Wealth Management and Securities Services

1,765

Payment Services

5,032

Treasury and Corporate Support

3,412

Consolidated Company

20,161

Less Treasury and Corporate Support

3,412

Consolidated Company excluding Treasury and Corporate Support

16,749

$

Percent of Total

Wholesale Banking and Commercial Real Estate

15%

Consumer and Small Business Banking

34%

Wealth Management and Securities Services

9%

Payment Services

25%

Treasury and Corporate Support

17%

Total

100%

Percent of Total excluding Treasury and Corporate Support

Wholesale Banking and Commercial Real Estate

18%

Consumer and Small Business Banking

41%

Wealth Management and Securities Services

11%

Payment Services

30%

Total

100% |

EXTENDING

THE ADVANTAGE

30

Credit Suisse Financial

Services Forum 2015

February 11, 2015 |