Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - Truett-Hurst, Inc. | v401014_ex99-1.htm |

| 8-K - FORM 8-K - Truett-Hurst, Inc. | v401014_8k.htm |

Exhibit 99.2

Truett - Hurst, Inc. FY15Q2 Earnings Call February 11, 2015 NASDAQ: THST 1

2 Safe Harbor Statement This presentation (including the presentation and any subsequent questions and answers) contains statements that are forward - looking within the meaning of Section 27 A of the Securities Act of 1933 and Section 21 E of the Securities Exchange Act of 1934 . Such forward - looking statements are only predictions and are not guarantees of future performance . Any such forward - looking statements are and will be, as the case may be, subject to many risks, uncertainties, certain assumptions and factors relating to the operations and business environments of Truett - Hurst, Inc . and its subsidiaries that may cause the actual results of the companies to be materially different from any future results expressed or implied in such forward - looking statements . These risk factors, include, but are not limited to, a reduction in the supply of grapes and bulk wine available to us ; significant competition ; any change in our relationships with retailers could harm our business ; we may not achieve or maintain profitability in the future ; the loss of key employees ; a reduction in our access to, or an increase in the cost of, the third - party services we use to produce our wine could harm our business ; credit facility restrictions on our current and future operations ; failure to protect, or infringement of, trademarks and proprietary rights ; these factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this report or detailed in our periodic filings (including Forms 8 - K, 10 - K and 10 - Q) or other documents filed with the Securities and Exchange Commission . For more detailed information on us, please refer to our filings with the Securities and Exchange Commission, which are readily available at http : //www . sec . gov, or through the our Investor Relations website at http : //www . truetthurstinc . com . For additional information, see our annual report for the period ended June 30 , 2014 on Form 10 - K filed on September 29 , 2014 , or our other reports currently on file with the Securities and Exchange Commission, which contain a more detailed discussion of risks and uncertainties that may affect future results . We do not undertake to update any forward - looking statements unless otherwise required by law .

Agenda • Paper Boy Update • FY15Q2 vs. FY14Q2 • First Half FY15 vs. First Half FY14 • Out - of - date Paper Boy Product • FY15Q2 Financial Details • Business Update • Q&A • Appendix

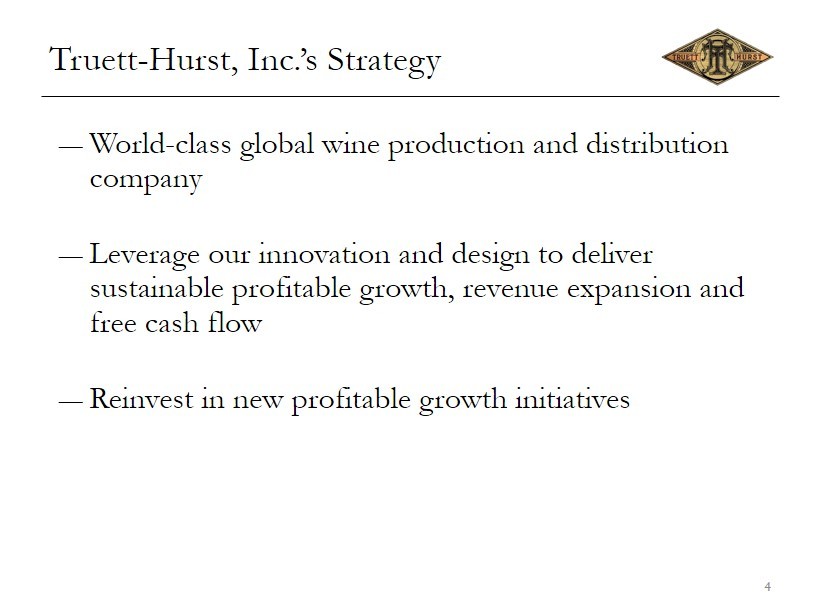

Truett - Hurst, Inc.’s Strategy ― W orld - class global wine production and distribution company ― Leverage our innovation and design to deliver sustainable profitable growth, revenue expansion and free cash flow ― Reinvest in new profitable growth initiatives 4

Out - of - Date Paper Boy Product • Paper Boy has a more limited shelf life than our other products; in January we were notified that certain Paper Boy wines were past their shelf life and had partially oxidized (not a health hazard) • We notified distributors that unsold Paper Boy stock was past its recommended shelf life and should be destroyed • We have taken a $0.6 million loss contingency accrual in connection with our efforts to assist with addressing out - of - date inventory • We have reviewed our inventory and have written off the expired Paper Boy finished goods inventory in our warehouse in the amount of $0.2 million • Subsequent to this issue, but unrelated to the shelf life expiration, we have determined that the latest generation paper bottle does not meet our quality standards. Until the manufacturer can consistently produce bottles that meet our standards we are not able to produce new Paper Boy inventory • Sales of Paper Boy represented less than 8% of net sales in FY14 and less than 1% of year to date net sales in FY15 5

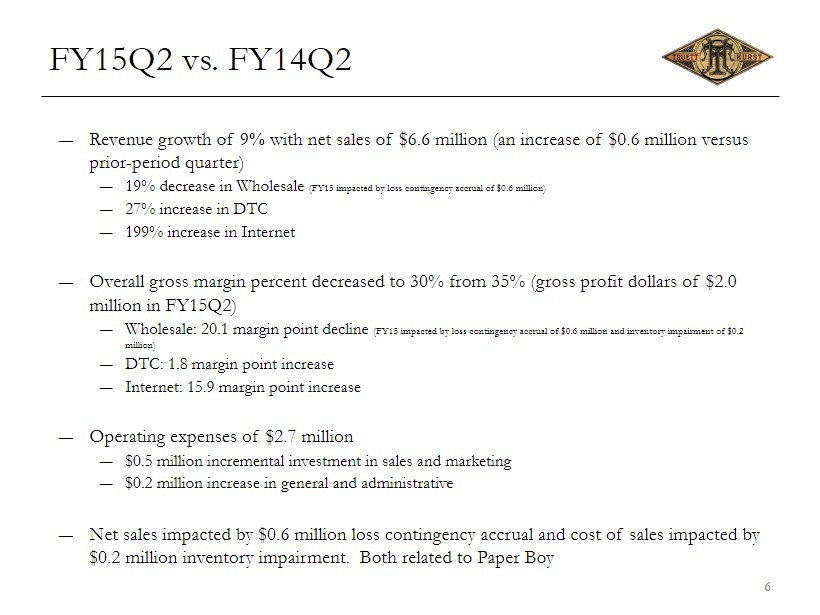

FY15Q2 vs. FY14Q2 ― Revenue growth of 9 % with net sales of $6.6 million (an increase of $0.6 million versus prior - period quarter) ― 19% decrease in Wholesale (FY15 impacted by loss contingency accrual of $0.6 million) ― 27% increase in DTC ― 199% increase in Internet ― Overall gross margin percent decreased to 30% from 35% (gross profit dollars of $2.0 million in FY15Q2) ― Wholesale: 20.1 margin point decline (FY15 impacted by loss contingency accrual of $0.6 million and inventory impairment of $0.2 million) ― DTC: 1.8 margin point increase ― Internet: 15.9 margin point increase ― Operating expenses of $2.7 million ― $0.5 million incremental investment in sales and marketing ― $0.2 million increase in general and administrative ― Net sales impacted by $0.6 million loss contingency accrual and cost of sales impacted by $0.2 million inventory impairment. Both related to Paper Boy 6

First Half FY15 vs. First Half FY14 ― Revenue growth of 15 % with net sales of $13.0 million (an increase of $1.6 million versus prior - period quarter) ― 8% decline in Wholesale (FY15 impacted by loss contingency accrual of $0.6 million) ― 21% increase in DTC ― 197% increase in Internet ― Overall gross margin percent flat at 34%. Gross profit dollars grew 13.4% to $4.4 million (an increase of $0.5 million versus prior year) ― Wholesale: 8.8 margin point decline (FY15 impacted by loss contingency accrual of $0.6 million and inventory impairment of $0.2 million) ― DTC: 3.1 margin point increase ― Internet: 12.0 margin point increase ― Operating expenses of $5.2 million ― $0.9 million incremental investment in sales and marketing ― $0.4 million increase in general and administrative ― Net sales impacted by $0.6 million loss contingency accrual and cost of sales impacted by $0.2 million inventory impairment. Both related to Paper Boy 7

FY15Q2 FINANCIAL HIGHLIGHTS

FY15Q2 Financial Details 9 FY 14 FY 15 FH 15 v 14 Q1 Q2 Q3 Q4 Q1 Q2 B / (W) % Net sales (1) 5,386 5,996 5,160 5,515 6,482 6,564 1,664 14.6% Gross profit (1) 1,789 2,121 1,752 1,767 2,435 1,999 524 13.4% Gross Margin % 33.2% 35.4% 34.0% 32.0% 37.6% 30.5% Sales and marketing 1,154 1,399 1,377 1,551 1,565 1,858 (870) 34.1% General and administrative 736 588 613 763 943 812 (431) 32.6% Other - (1) 400 88 2 - (3) Total operating expenses (2), (3) 1,890 1,986 2,390 2,402 2,510 2,670 (1,304) 33.6% (Loss) income from operations (101) 135 (638) (635) (75) (671) (780) Net (loss) income before non-controlling interests (139) 111 (625) (631) (150) (817) (939) (1) Loss contingency accrual & inventory impairment: Accrual for sales return - included in net sales 582 (582) Inventory Impairment (Paper Boy)- included in cost of goods 209 (209) Total Gross Margin Impact 791 (791) (2) Non-cash stock compenstion expense: Sales and marketing 106 78 40 117 83 100 1 General and administrative 8 9 11 67 55 105 (143) 114 87 51 184 138 205 (142) (3) Operating expenses as a percentage of Net Sales Sales and marketing 21.4% 23.3% 26.7% 28.1% 24.1% 28.3% General and administrative 13.7% 9.8% 11.9% 13.8% 14.5% 12.4%

10 FY15Q2 Financial Details Gross profit contribution growth for DTC and Internet segments exceed sales growth due to margin expansion Wholesale impacted by $0.6 million loss contingency accrual Continued strong growth in tasting room and wine club sales driving DTC Second consecutive quarter of triple digit growth for the Internet segment Q2 2014 2015 B / (W) % D Net Sales Wholesale 4,357 3,544 (813) -18.7% Direct to Consumer 1,091 1,382 291 26.7% Internet 548 1,638 1,090 198.9% 5,996 6,564 568 9.5% Gross Profit Wholesale 1,279 330 (949) -74.2% Direct to Consumer 658 858 200 30.4% Internet 184 811 627 340.8% 2,121 1,999 (122) -5.8% Gross Margin Wholesale 29.4% 9.3% -20.0% Direct to Consumer 60.3% 62.1% 1.8% Internet 33.6% 49.5% 15.9% 35.4% 30.5% -4.9% Wholesale gross margin, adjusting for impact of Paper Boy related loss contingency accrual ($0.6 million) and inventory impairment ($0.2 million), was 27.2%.

11 FY15Q2 Financial Details • Wholesale segment, before the impact of Paper Boy related charges, had net sales of $4.1 million . $0.2 million lower than Q2FY14 • We anticipate variability in quarterly comparisons for the wholesale segment due to timing of brining on new customers and product launches • Consolidated net sales, before the impact of Paper Boy related charges, grew 19.2% with 31.5% growth in gross margin contribution (overall gross margin percent increased 370 basis points) Q2 FY 15 vs.Q2FY14 As Reported Adjustments (1) As Adjusted B / (W) Wholesale Net Sales 3,544 582 4,126 (231) Gross Profit 330 791 1,121 (158) Gross Margin 9.3% 27.2% -2.2% Q2 FY 15 vs.Q2FY14 As Reported Adjustments (1) As Adjusted B / (W) % vs Consolidated Q2FY14 Net Sales 6,564 582 7,146 1,150 19.2% Gross Profit 1,999 791 2,790 669 31.5% Gross Margin 30.5% 39.0% 3.7% (1) Loss contingency accrual & inventory impairment:Loss contingency accrual & inventory impairment: Accrual for sales return - included in net sales 582 Inventory Impairment (Paper Boy)- included in cost of goods 209 Gross Profit Impact 791

12 FY15Q2 Financial Details Q-O-Q 2015 2015 in Q1 Q2 WC Total Assets 39,517 34,557 Total Liabilities 21,112 16,762 Total Equity 18,405 17,795 39,517 34,557 Cash and cash equivalents 4,752 2,913 Property & equipment, net 5,845 5,931 Major Working Capital Accounts A/R 3,959 2,294 1,665 Inventories 23,660 21,952 1,708 AP & Accrueds 7,758 3,474 (4,284) (911) Interest Bearing Debt Credit facilities 9,055 8,457 Other Interest Bearing Debt 3,826 3,849 12,881 12,306

BUSINESS UPDATE

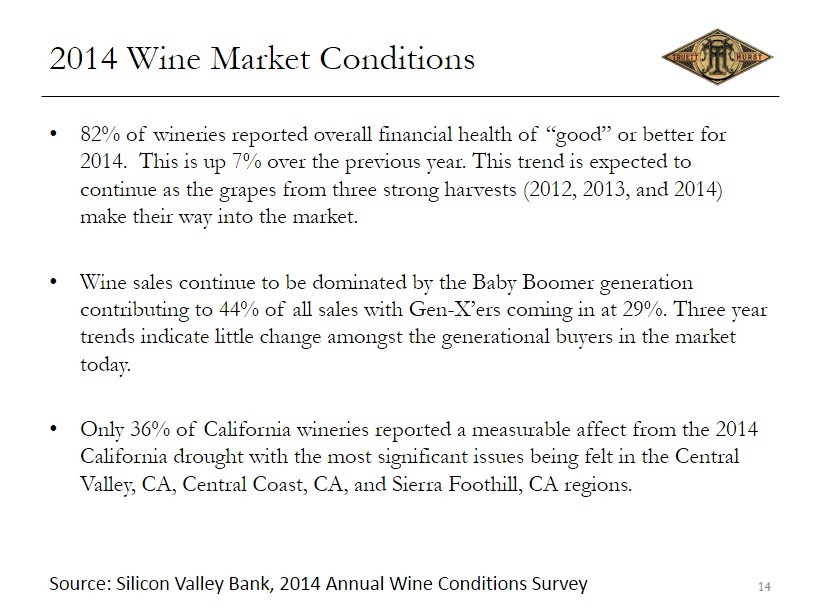

2014 Wine Market Conditions 14 • 82% of wineries reported overall financial health of “good” or better for 2014 . This is up 7% over the previous year . This trend is expected to continue as the grapes from three strong harvests (2012 , 2013 , and 2014) make their way into the market. • Wine sales continue to be dominated by the Baby Boomer generation contributing to 44% of all sales with Gen - X’ers coming in at 29%. Three year trends indicate little change amongst the generational buyers in the market today . • Only 36 % of California wineries reported a measurable affect from the 2014 California drought with the most significant issues being felt in the Central Valley , CA , Central Coast , CA , and Sierra Foothill , CA regions. Source : Silicon Valley Bank, 2014 Annual Wine Conditions Survey

Innovation/Experimentation 15 Source: EJ Gallo Top 10 Snapshots of the American Wine Consumer, 2014

Overall Channel Growth 16

17 Direct to Consumer Volumes Achieve Critical Mass

Robert Parker December 2014 18 December 2014 issue: 2012 TH Burning Man Petite Sirah, 95 Points 2012 TH Rattler Rock Zinfandel, 93 Points 2012 TH Red Rooster Zinfandel, 94 Points 2012 VML Moon Pinot Noir, 90 Points 2012 VML Earth Pinot Noir, 89 Points 2012 VML Stars Pinot Noir, 89 Points 2013 VML RRV Chardonnay, 89 Points 2012 VML RRV Pinot Noir, 87 Points 2013 VML RRV SB, 87 Points

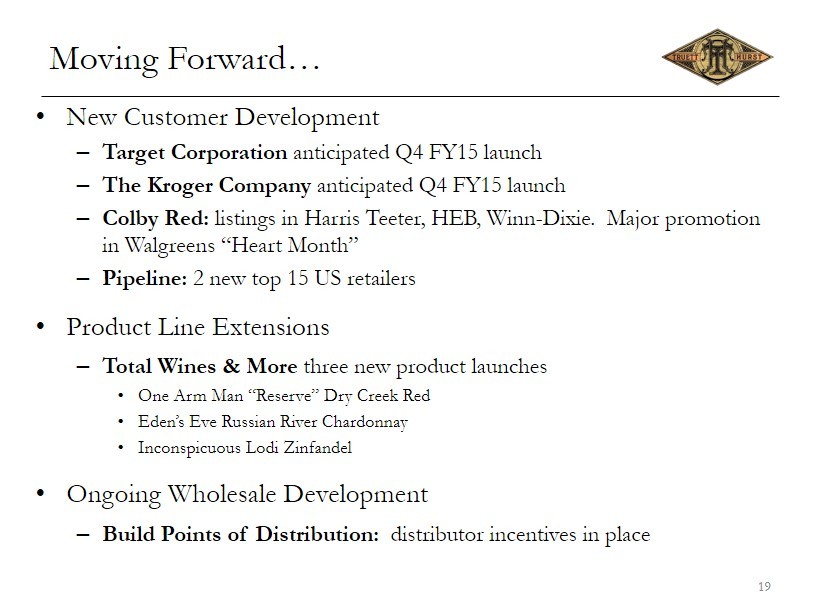

Moving Forward… • New Customer Development – Target Corporation anticipated Q4 FY15 launch – The Kroger Company anticipated Q4 FY15 launch – Colby Red: listings in Harris Teeter, HEB, Winn - Dixie. Major promotion in Walgreens “Heart Month” – Pipeline: 2 new top 15 US retailers • Product Line Extensions – Total Wines & More three new product launches • One Arm Man “Reserve” Dry Creek Red • Eden’s Eve Russian River Chardonnay • Inconspicuous Lodi Zinfandel • Ongoing Wholesale Development – Build Points of Distribution: distributor incentives in place 19

Q & A 20

21 APPENDIX I. Contact Information II. Conference Call Playback Information III. Ownership Structure IV. Second Quarter and Six - Month Fiscal 2015 Pro forma Diluted EPS & Market Cap

Appendix I - Contact Information 22 Phillip L. Hurst Chief Executive Officer, President Email: phil@truetthurst.com T: 707.433.4408 M: 707.318.7480 Paul A. Forgue Chief Financial Officer & Chief Operations Officer Email: paul@truetthurst.com T: 707.431.4423 M: 707.494.3452 www.truetthurstinc.com ir@truetthurstinc.com

Appendix II – Call Playback Information Transcript, when available, at: www.truetthurstinc.com Webcast/PowerPoint / Replay available at: www.truetthurstinc.com/investors Transcript available until February 18, 2015. 23

Appendix III Ownership Structure 24 HDD LLC Ownership Class A Shares (Fully Diluted) Members THI Total Outstanding Unconverted LLC Units Equity Incentives Total As of Initial Public Offering 4,102,644 2,700,000 6,802,644 2,700,000 4,102,644 252,000 7,054,644 60.3% 39.7% 100.0% 38.3% 58.2% 3.6% 100.0% Changes through 12/31/14: LLC Conversions (1,019,184) 1,019,184 0 1,019,184 (1,019,184) 0 0 Vesting of Equity Incentives Outstanding @ IPO Date 0 0 0 112,000 0 (112,000) 0 Post IPO Equity Incentives Equity Incentives Granted - RSA / RSU 0 0 0 0 0 131,629 131,629 Equity Incentives Granted - Options 0 0 0 0 0 150,000 150,000 Equity Incentives Vested 0 0 0 16,802 0 (16,802) 0 0 0 0 16,802 0 264,827 281,629 As of 12/31/14 3,083,460 3,719,184 6,802,644 3,847,986 3,083,460 404,827 7,336,273 45.3% 54.7% 100.0% 52.5% 42.0% 5.5% 100.0% Increase in Class A Shares (excluding unvested equity incentives) 1.9% Increase in Class A Shares (fully diluted) 4.0%

Appendix IV Adjusted Pro Forma EPS & Market Cap December 31, 2014 Net loss attributable to Truett-Hurst, Inc. and H.D.D. LLC (474)$ Adjusted Pro Forma Basic & Diluted Loss Per Share Weighted average Class A common stock 3,786,712 LLC units assuming 100% LLC membership conversion 3,083,460 Total weighted average basic pro forma shares outstanding 6,870,172 Adjusted Pro Forma Basic Loss Per Share Calculation (0.07)$ Adjusted Market Capital based on December 31, 2014 Class A common stock closing price of $3.97 27,274,583$ TRUETT-HURST, INC. AND SUBSIDIARIES Adjusted Pro Forma Basic Loss Per Share & Market Cap For the Three-month Period Ended December 31, 2014 (assumes 100% conversion of LLC units to THST Class A stock ) 25

Appendix IV Adjusted Pro Forma EPS & Market Cap December 31, 2014 Net loss attributable to Truett-Hurst, Inc. and H.D.D. LLC (574)$ Adjusted Pro Forma Basic & Diluted Loss Per Share Weighted average Class A common stock 3,768,592 LLC units assuming 100% LLC membership conversion 3,083,460 Total weighted average basic pro forma shares outstanding 6,852,052 Adjusted Pro Forma Basic Loss Per Share Calculation (0.08)$ Adjusted Market Capital based on December 31, 2014 Class A common stock closing price of $3.97 27,202,646$ TRUETT-HURST, INC. AND SUBSIDIARIES Adjusted Pro Forma Basic Loss Per Share & Market Cap For the Six-month Period Ended December 31, 2014 (assumes 100% conversion of LLC units to THST Class A stock ) 26