Attached files

| file | filename |

|---|---|

| EX-4.3 - EX-4.3 - MaxPoint Interactive, Inc. | a2222730zex-4_3.htm |

| EX-3.3 - EX-3.3 - MaxPoint Interactive, Inc. | a2222730zex-3_3.htm |

| EX-3.1 - EX-3.1 - MaxPoint Interactive, Inc. | a2222730zex-3_1.htm |

| EX-4.2 - EX-4.2 - MaxPoint Interactive, Inc. | a2222730zex-4_2.htm |

| EX-10.2 - EX-10.2 - MaxPoint Interactive, Inc. | a2222730zex-10_2.htm |

| EX-10.7 - EX-10.7 - MaxPoint Interactive, Inc. | a2222730zex-10_7.htm |

| EX-21.1 - EX-21.1 - MaxPoint Interactive, Inc. | a2222730zex-21_1.htm |

| EX-23.1 - EX-23.1 - MaxPoint Interactive, Inc. | a2222730zex-23_1.htm |

| EX-10.5 - EX-10.5 - MaxPoint Interactive, Inc. | a2222730zex-10_5.htm |

| EX-10.6 - EX-10.6 - MaxPoint Interactive, Inc. | a2222730zex-10_6.htm |

As filed with the Securities and Exchange Commission on February 3, 2015.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form S-1

REGISTRATION STATEMENT

Under

The Securities Act of 1933

MAXPOINT INTERACTIVE, INC.

(Exact Name of Registrant as Specified in its Charter)

| Delaware (State or Other Jurisdiction of Incorporation or Organization) |

7370 (Primary Standard Industrial Classification Code Number) |

20-5530657 (I.R.S. Employer Identification Number) |

MaxPoint Interactive, Inc.

3020 Carrington Mill Blvd., Suite 300

Morrisville, North Carolina 27560

(800) 916-9960

(Address, including zip code and telephone number, including area code, of registrant's principal executive offices)

Joseph Epperson

Chief Executive Officer

MaxPoint Interactive, Inc.

3020 Carrington Mill Blvd., Suite 300

Morrisville, North Carolina 27560

(800) 916-9960

(Name, address, including zip code and telephone number, including area code, of agent for service)

| Copies to: | ||||

Robert V. Gunderson, Jr., Esq. Glen R. Van Ligten, Esq. Richard C. Blake, Esq. Gunderson Dettmer Stough Villeneuve Franklin & Hachigian, LLP 1200 Seaport Blvd. Redwood City, California 94063 (650) 321-2400 |

Brad R. Schomber Chief Financial Officer MaxPoint Interactive, Inc. 3020 Carrington Mill Blvd., Suite 300 Morrisville, North Carolina 27560 (800) 916-9960 |

Mark G. Borden, Esq. Erika L. Robinson, Esq. Wilmer Cutler Pickering Hale and Dorr LLP 7 World Trade Center, 250 Greenwich Street New York, New York 10007 (212) 230-8800 |

||

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

|

||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee |

||

|---|---|---|---|---|

Common Stock, $0.00005 par value |

$75,000,000 | $8,715 | ||

|

||||

- (1)

- Estimated pursuant to Rule 457(o) under the Securities Act of 1933, as amended.

- (2)

- Includes the aggregate offering price of additional shares that the underwriters have the option to purchase to cover over-allotments, if any.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to such Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion. Dated , 2015.

Shares

Common Stock

This is an initial public offering of shares of common stock of MaxPoint Interactive, Inc. All of the shares of common stock are being sold by us.

Prior to this offering, there has been no public market for the common stock. It is currently estimated that the initial public offering price per share will be between $ and $ . We are applying to list our common stock on the New York Stock Exchange under the symbol "MXPT."

We are an "emerging growth company" as that term is used in the Jumpstart Our Business Startups Act of 2012 and, as such, have elected to comply with certain reduced public company reporting requirements.

See "Risk Factors" on page 13 to read about factors you should consider before buying shares of the common stock.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| |

Per Share | Total | |||||

|---|---|---|---|---|---|---|---|

Initial public offering price |

$ | $ | |||||

Underwriting discount(1) |

$ | $ | |||||

Proceeds, before expenses, to MaxPoint |

$ | $ | |||||

- (1)

- See "Underwriting" for a description of the compensation payable to the underwriters.

To the extent that the underwriters sell more than shares of common stock, the underwriters have the option to purchase up to an additional shares from MaxPoint at the initial price to public less the underwriting discount.

The underwriters expect to deliver the shares against payment in New York, New York on , 2015.

| Goldman, Sachs & Co. | Deutsche Bank Securities | Pacific Crest Securities |

| Needham & Company | William Blair |

Prospectus dated , 2015.

TABLE OF CONTENTS

Neither we nor any of the underwriters have authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we have prepared. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

Through and including , 2015 (25 days after the commencement of this offering), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This delivery is in addition to a dealer's obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

For investors outside the United States: Neither we nor any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of our common stock and the distribution of this prospectus outside of the United States.

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. You should read the following summary together with the more detailed information appearing in this prospectus, including our consolidated financial statements and related notes, and in the sections titled "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations," before deciding whether to purchase shares of our common stock. Unless the context otherwise requires, we use the terms "MaxPoint," the "company," "we," "us" and "our" in this prospectus to refer to MaxPoint Interactive, Inc. and its subsidiary.

Overview

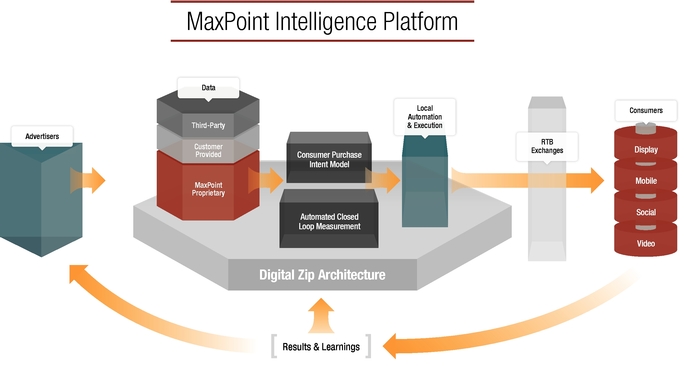

MaxPoint provides a leading business intelligence and marketing automation software service, which we refer to as our solution, that enables national brands to drive local, in-store sales. National brands use our MaxPoint Intelligence Platform to predict the most likely local buyers of a specific product at a particular retail location and then execute cross-channel digital marketing campaigns to reach these buyers. Business intelligence is at the core of our solution, which leverages high-velocity data processing and proprietary statistical models to continuously analyze more than 10 billion daily data attributes to delineate consumers' real-time purchase intent. By identifying and reaching only the most likely local buyers with digital customized product offers for local stores, national brands can more efficiently and effectively run local marketing campaigns, thereby increasing in-store sales and reducing wasted marketing spend associated with traditional approaches. We provide a technology-driven alternative to traditional local marketing methods for national brands across a number of industries where transactions take place predominantly offline, such as consumer products, retail, automotive, healthcare, telecommunications and entertainment.

The primary marketing methods traditionally utilized to engage local consumers are print media, direct mail and radio. We believe these methods have become outdated as media consumption moves online and national brands increasingly seek digital solutions to make effective local marketing decisions to drive in-store sales. Approximately 88% of total U.S. retail purchases in 2014 occurred at physical locations, according to Euromonitor. The challenges associated with the promotion of local, in-store purchasing include predicting a consumer's purchase intent and matching that consumer with the appropriate local store that currently has the desired product in stock. We believe these challenges are more pronounced for national brands because they generally operate on a centralized or regional basis, which limits their visibility into the purchase intent of local consumers.

The MaxPoint Intelligence Platform is a software service that enables national brands to predict local demand based on consumers' purchase power and intent and manage customized digital advertisements containing in-store offers and promotions to reach consumers at a local level across display, mobile, social and video channels. The MaxPoint Intelligence Platform matches the most likely communities of local buyers with a specific product at a particular retail location within a given timeframe. Through marketing automation and direct integration with real-time bidding, or RTB, exchanges, our platform delivers customized digital advertisements containing product and store-specific promotions to local consumers. National brands can then measure the offline sales impact of those digital marketing campaigns to optimize future campaigns and budgets and manage in-store supply levels. We introduced the MaxPoint Intelligence Platform in 2011 as a service primarily run by us on behalf of our customers. Since 2013, our customers have also had the ability to directly interface with the MaxPoint Intelligence Platform software service.

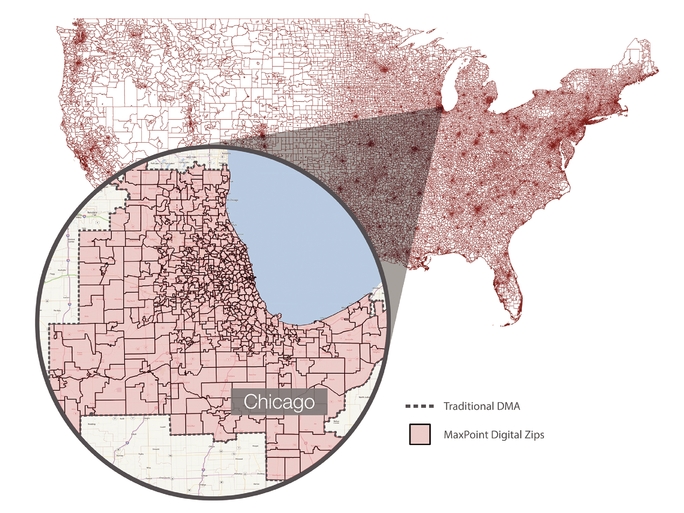

The foundation for our local targeting is our proprietary Digital Zip architecture, a digital grid of households organized into over 44,000 specific neighborhoods, or Digital Zips, which can be as small as a couple of city blocks. Through a combination of our proprietary and third-party data, we

1

create a profile for each Digital Zip based on shared demographic and financial traits, such as family size, income level, education, age and historical purchasing behavior.

We use our consumer purchase intent model to determine which products consumers in a particular Digital Zip are most likely to purchase. Our consumer purchase intent model uses proprietary algorithms that take into account demographic and financial characteristics of potential consumers, historical purchase patterns of potential consumers and recent consumption of online media content by consumers, each aggregated at the Digital Zip level, which relate to targeted product characteristics or brand attributes. We analyze the aggregated consumption of online media content in each Digital Zip through the use of our proprietary search-based technology. This technology crawls, indexes and analyzes webpages around-the clock to interpret the meaning of text on webpages and catalogue each webpage by key topics. We then match the Digital Zips with the highest number of views of webpages that pertain to a key topic associated with a targeted product or product category. Based on these results, we can then match a targeted product offer to specific Digital Zips that exhibit an online behavior that correlates most strongly with the likely purchase of such products at the local level. We define "local," in terms of both retail locations and buyers or consumers, as the close proximity of a targeted consumer to a targeted retail location, typically within a specific Digital Zip.

Our diverse customer base consists primarily of enterprises with national brands in the consumer products, retail, automotive, healthcare, telecommunications and entertainment industries. We sell our solution either directly to our customers or through advertising agencies that act on behalf of our customers. We have worked with each of the top 20 leading national advertisers and each of the top 10 advertising agencies in the United States as ranked in 2014 by Advertising Age. As of September 30, 2014, we had 431 enterprise customers. We define an enterprise customer to be any customer from which we have generated more than $10,000 of revenue during any trailing twelve-month period. Our customers typically pay us on a cost per thousand impression, or CPM, model based on the number of impressions we deliver through our platform for each marketing campaign.

We generated revenue of $14.7 million, $35.1 million and $66.1 million for the years ended December 31, 2011, 2012 and 2013, respectively, representing year-over-year increases of 139% and 88%, respectively. We generated revenue of $41.8 million and $67.9 million for the nine months ended September 30, 2013 and 2014, respectively, representing a period-over-period increase of 62%. Revenue less traffic acquisition costs, which we refer to as Revenue ex-TAC, was $6.9 million, $18.6 million and $38.4 million for the years ended December 31, 2011, 2012 and 2013, respectively, representing year-over-year increases of 169% and 106%, respectively. Our Revenue ex-TAC was $24.7 million and $40.3 million for the nine months ended September 30, 2013 and 2014, respectively, representing a period-over-period increase of 63%. We recorded a net loss of $5.5 million, $6.8 million and $0.2 million for the years ended December 31, 2011, 2012 and 2013, respectively. We recorded a net loss of $1.4 million and $11.5 million for the nine months ended September 30, 2013 and 2014, respectively. Our Adjusted EBITDA was $(4.6) million, $(5.1) million and $2.6 million for the years ended December 31, 2011, 2012 and 2013, respectively. Our Adjusted EBITDA was $0.6 million and $(6.9) million for the nine months ended September 30, 2013 and 2014, respectively. Revenue ex-TAC and Adjusted EBITDA are financial measures not calculated in accordance with U.S. generally accepted accounting principles, or GAAP. Please refer to "—Summary Consolidated Financial Data" for information on Revenue ex-TAC and Adjusted EBITDA and for a reconciliation of Revenue ex-TAC to revenue and Adjusted EBITDA to net income (loss), respectively, the most directly comparable GAAP financial measures.

Industry Background

Despite the growth of e-commerce over the past decade, the vast majority of consumer purchases currently is and, in the foreseeable future, is expected to be made locally in physical

2

retail stores. Approximately 88% of total U.S. retail purchases in 2014 occurred at physical store locations, representing over $2 trillion of spending, and approximately 12% of total U.S. retail purchases occurred at non-physical store locations (including e-commerce), representing over $300 billion of spending, according to Euromonitor. We believe the vast majority of these retail purchases at physical store locations are made at retail stores in close proximity to the consumer's home. By 2019, retail purchases at physical retail store locations will continue to represent approximately 85%, or nearly $3 trillion, and retail purchases at non-physical store locations (including e-commerce) will represent approximately 15%, or approximately $500 billion, of total U.S. retail spending according to Euromonitor.

National brands employ a variety of offline and online local marketing channels in an effort to target and reach consumers to promote sales of their products at physical retail locations. According to BIA/Kelsey, the U.S. marketing industry spent approximately $137 billion in 2014 and is projected to spend approximately $159 billion in 2019 on local media marketing, which includes both traditional and digital forms of marketing.

- •

- Traditional Local Marketing. Local

marketing is still predominantly conducted through traditional marketing channels, which include television, newspaper, magazine and radio advertising, as well as mailers, free-standing inserts and

coupons. According to BIA/Kelsey, spending for traditional local marketing was approximately $106 billion in 2014 and is projected to be approximately $104 billion in 2019, which would

represent a decline from approximately 77% to approximately 65% of total local marketing spend during that period.

- •

- Online/Digital Local Marketing. As consumers continue to shift their media consumption online, national brands continue to increase their digital marketing efforts. According to BIA/Kelsey, digital local marketing spending was approximately $31 billion in 2014 and is projected to be approximately $55 billion in 2019, which would represent an increase from approximately 23% to approximately 35% of total local marketing spend during that period.

National brands seeking to drive in-store sales face the following challenges with current local marketing channels:

- •

- Limited ability to predict and target the most likely

buyers. Traditional marketing methods typically lack sophisticated technology while online methods generally rely on cookies that are not

optimized for local consumer targeting and are frequently deleted.

- •

- Limited ability to efficiently reach the most likely buyers at scale and at the right

time. Many traditional methods for local marketing have shrinking audiences and lack the ability to connect consumers to a particular

product. Also, as lead times of up to eight weeks are generally required to plan and execute marketing campaigns, national brands often miss opportunities to reach consumers at the point in time when

they desire to purchase a product.

- •

- Inability to capture and analyze massive amounts of unstructured and disparate data in real

time. Most local marketing methods are unable to programmatically capture, process and analyze in real time the massive amounts of

disparate data that reflect the current purchase intent of consumers and store-level supply of products.

- •

- Inability to measure and optimize local marketing based on in-store

sales. Both offline and online media typically lack measurement and attribution tools that, at the individual store level, demonstrate

return on investment for national brands and help them determine where to allocate marketing budgets.

- •

- Inability to automate offline methods of marketing. Traditional local marketing campaigns typically have long lead times, require a significant amount of effort to manage across multiple markets and involve numerous small media purchases across multiple channels and geographies.

3

The Benefits of Our Solution

Our solution presents significant benefits to our customers, including the ability to:

- •

- predict and target the most likely local buyers for specific products based on consumers' purchase intent in real time;

- •

- reach the most likely consumers of a product efficiently, at scale, and at the right time by programmatically delivering

targeted and timely advertisements to the most likely buyers;

- •

- capture and analyze massive amounts of unstructured and disparate data in real time using our integrated proprietary

software and customized hardware platform to make 450,000 decisions per second and run more than a thousand simultaneous campaigns;

- •

- measure the impact of local, online marketing campaigns on the in-store sales of specific locations; and

- •

- automate and streamline the execution of local marketing with minimal lead time and human intervention.

Our Competitive Strengths

We believe we have the following competitive strengths:

- •

- Pioneering solution with compelling value

proposition. Our proprietary, predictive business intelligence engine identifies, in real time, consumers likely to be receptive to our

customers' advertisements, thereby focusing marketing spend on the most efficient and effective channel.

- •

- Virtuous cycle of data

aggregation. As our business intelligence engine analyzes and makes millions of predictions about consumer intent, our solution learns from

each action, enabling us to programmatically improve our algorithms and the results we deliver to our customers.

- •

- Proprietary, data-driven understanding of consumer intent and

behavior. We have developed a proprietary business intelligence engine that predicts consumer purchase intent for products generally

purchased offline.

- •

- Deep relationships with national brands across key industries. Leading national brands trust us to help them automate and execute local marketing campaigns.

Our Growth Strategies

The core elements of our growth strategy include:

- •

- Increase share of spend from existing

customers. Our goal is to capture an increasing share of our existing customers' marketing budgets by working with more of their national

brands, growing the number of physical store locations of retailers through which they sell their products, and broadening the number of regions and geographies covered by our solution.

- •

- Acquire new customers. We believe

that many national brands can benefit from our proprietary, technology-driven local marketing solution, and we plan to invest in growing our sales organization and marketing efforts in order to reach

these potential customers.

- •

- Further penetrate new industries. Historically, we have focused primarily on serving national brands in three industries—consumer products, retail and automotive—and have recently expanded into three new industries—healthcare, telecommunications and entertainment. Our plan is to continue to penetrate these new industries and pursue opportunities in additional industries.

4

- •

- Continue to innovate and invest in our

technology. We plan to continue to make substantial investments in our technology and product development to enhance the effectiveness of

our solution in an effort to deliver increasing value to our customers.

- •

- Expand internationally. We believe that our technology and solution can be adapted to other countries where national brands face similar local marketing challenges. We recently established a presence in the United Kingdom and expect to explore additional international expansion opportunities.

Key Financial and Operating Performance Metrics

The following metrics aid us in developing and refining our growth strategies and making strategic decisions:

| |

Year Ended December 31, | Nine Months Ended September 30, |

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2011 | 2012 | 2013 | 2013 | 2014 | |||||||||||

| |

(in thousands, except number of enterprise customers) |

|||||||||||||||

Revenue |

$ | 14,679 | $ | 35,072 | $ | 66,068 | $ | 41,817 | $ | 67,864 | ||||||

Revenue ex-TAC |

$ | 6,917 | $ | 18,587 | $ | 38,356 | $ | 24,657 | $ | 40,312 | ||||||

Adjusted EBITDA |

$ | (4,648 | ) | $ | (5,116 | ) | $ | 2,631 | $ | 621 | $ | (6,859 | ) | |||

Number of enterprise customers |

106 | 225 | 304 | 292 | 431 | |||||||||||

- •

- Revenue ex-TAC is a non-GAAP financial measure defined by us as revenue less traffic acquisition costs, which consist of

purchases of advertising impressions from RTB exchanges. This metric is meaningful because it is frequently used for internal management purposes and combines the important factors of our ability to

sustain pricing with our customers, purchase inventory at reasonable and expected prices, and to scale our business. See "—Summary Consolidated Financial Data."

- •

- Adjusted EBITDA represents our net loss before income taxes, interest expense, and depreciation and amortization, adjusted

to eliminate stock-based compensation expense and the change in the fair value of convertible preferred stock warrant liability. We evaluate Adjusted EBITDA because we believe it provides a useful

measure for period-to-period comparisons of our core business. See "—Summary Consolidated Financial Data."

- •

- We believe our ability to attract new customers onto our MaxPoint Intelligence Platform is an important component of our growth strategy. We also believe that those customers from which we have generated more than $10,000 of revenue during any trailing twelve-month period best identifies customers that are actively using our solution and contribute more meaningfully to revenue. We refer to these customers as our enterprise customers. As of December 31, 2011, 2012 and 2013 and September 30, 2014, customers from which we have generated less than $10,000 of revenue during the previous trailing twelve-month period have accounted for less than 2% of our revenue.

Risks Related to Our Business

Our business is subject to numerous risks of which you should be aware before making an investment decision, described more fully in the "Risk Factors" section immediately following this prospectus summary. These risks represent challenges to the successful implementation of our strategy and to the growth and future profitability of our business. These risks include the following:

- •

- Our limited operating history makes it difficult to evaluate our business and prospects and may increase the risks

associated with your investment.

- •

- We have a history of losses, we expect our operating expenses to continue to increase substantially and we may not achieve or sustain profitability in the future.

5

- •

- If the MaxPoint Intelligence Platform does not accurately predict the most likely local buyers for specific products, we

could lose revenue, which would have a material adverse impact on our operating results and financial condition.

- •

- Our operating results fluctuate, which make our future results difficult to predict and could cause our operating results

to fall below analysts' and investors' expectations.

- •

- If we are unable to attract new customers or our existing customers do not allocate a greater portion of their marketing

spend to us, our revenue growth will be adversely affected.

- •

- If we fail to develop new solutions and services or enhance our existing solution and services, we may not attract and

retain customers, and our revenue and results of operations may decline.

- •

- If we do not manage our growth effectively, the quality of our solution may suffer, and our operating results may be

negatively affected.

- •

- We may not be able to compete successfully against current and future competitors, which may result in declining revenue

or inability to grow our business.

- •

- We have historically relied, and expect to continue to rely, on a small number of customers for a significant portion of

our revenue, and the loss of any of these customers may significantly harm our business, results of operations and financial condition.

- •

- We rely on advertising agencies that act on behalf of our customers for a substantial majority of our revenue. Multiple

advertising agencies operating within three global advertising networks represented numerous customers accounting for approximately 18%, 13% and 10% of our revenue, respectively, for the year ended

December 31, 2013. For the nine months ended September 30, 2014, multiple advertising agencies operating within one global advertising network represented numerous customers accounting

for approximately 15% of our revenue. The loss of any such relationships or increased competition from such advertising agencies or agency trading desks could materially harm our business.

- •

- Legislation and regulation of online businesses, including privacy and data protection regimes, could create unexpected

costs, subject us to enforcement actions for compliance failures or cause us to change our technology platform or business model, which may have a material adverse effect on our business.

- •

- Our ability to generate revenue depends on our collection of significant amounts of data from various sources.

Corporate Information

We were incorporated in the state of Delaware in September 2006. Our principal executive offices are located at 3020 Carrington Mill Blvd., Suite 300, Morrisville, North Carolina 27560. Our telephone number is (800) 916-9960. Our website address is www.maxpoint.com. Information contained on our website is not incorporated by reference into this prospectus, and you should not consider information contained on our website to be part of this prospectus or in deciding whether to purchase shares of our common stock.

MaxPoint, the MaxPoint logo, MaxPoint Interactive, Digital Zip and other trademarks or service marks of MaxPoint appearing in this prospectus are the property of MaxPoint. This prospectus contains additional trade names, trademarks and service marks of ours and of other companies. We do not intend our use or display of other companies' trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, these other companies.

6

Common stock offered |

shares | |

Common stock to be outstanding after this offering |

shares |

|

Over-allotment option |

shares |

|

Use of proceeds |

We expect to receive net proceeds from this offering of approximately $ million, after deducting the underwriting discount and commissions and estimated offering expenses payable by us. We intend to use the net proceeds from this offering for general corporate purposes, including working capital, sales and marketing activities, engineering initiatives including enhancement of our solution, investment in technology and development and capital expenditures. We also may use a portion of the net proceeds from this offering to acquire or invest in technologies, solutions or businesses that complement our business, although we have no present commitments, and have not allocated specific amounts of net proceeds, to complete any such transactions or plans. See "Use of Proceeds." |

|

Risk factors |

You should read the "Risk Factors" section of this prospectus beginning on page 13 for a discussion of factors to consider carefully before deciding to invest in shares of our common stock. |

|

Proposed symbol |

"MXPT" |

The number of shares of our common stock to be outstanding after this offering is based on 37,689,073 shares of our common stock outstanding as of September 30, 2014, and excludes:

- •

- 6,695,951 shares of common stock issuable upon the exercise of options outstanding as of September 30, 2014 under

our 2010 Equity Incentive Plan, with a weighted average exercise price of $3.23 per share;

- •

- 990,850 shares of common stock issuable upon the exercise of options granted after September 30, 2014 under our

2010 Equity Incentive Plan, with a weighted average exercise price of $7.27 per share;

- •

- 200,000 shares of common stock issuable upon the exercise of lender warrants outstanding as of September 30, 2014

with an exercise price of $5.68 per share;

- •

- 100,000 shares of common stock issuable upon the exercise of lender warrants outstanding issued after September 30, 2014

with an exercise price of $5.68 per share; and

- •

- shares of our common stock reserved for future issuance under our equity compensation plans, consisting of 974,894 shares of our common stock that were reserved for issuance under our 2010 Equity Incentive Plan as of September 30, 2014, and shares of our common stock reserved for issuance under our 2015 Equity Incentive Plan. On

7

the date immediately prior to the date of this prospectus, any remaining shares available for issuance under our 2010 Equity Incentive Plan were added to the shares reserved under our 2015 Equity Incentive Plan and we ceased granting awards under the 2010 Equity Incentive Plan. Our 2015 Equity Incentive Plan also provides for automatic annual increases in the number of shares reserved thereunder, as more fully described in "Executive Compensation—Equity Plans."

Except as otherwise indicated, all information in this prospectus assumes:

- •

- the effectiveness of our amended and restated certificate of incorporation and the adoption of our amended and restated

bylaws in connection with the completion of this offering;

- •

- the automatic conversion of our outstanding convertible preferred stock into an aggregate of 29,697,650 shares of our

common stock, the conversion of which will occur immediately prior to the completion of this offering;

- •

- no exercise of outstanding options described above; and

- •

- no exercise by the underwriters of their right to purchase up to an additional shares of common stock to cover over-allotments.

8

Summary Consolidated Financial Data

The following tables summarize our consolidated financial data. You should read this summary consolidated financial data together with the sections entitled "Selected Consolidated Financial Data," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and related notes that are included elsewhere in this prospectus.

The consolidated statements of operations data for the years ended December 31, 2011, 2012 and 2013, and the consolidated balance sheet data as of December 31, 2011, 2012 and 2013 are derived from our audited consolidated financial statements that are included elsewhere in this prospectus. The condensed consolidated statements of operations data for the nine months ended September 30, 2013 and 2014 and the condensed consolidated balance sheet data as of September 30, 2014 are derived from our unaudited consolidated financial statements that are included elsewhere in this prospectus. The unaudited consolidated financial statements were prepared on a basis consistent with our audited consolidated financial statements and include, in management's opinion, all adjustments, consisting only of normal recurring adjustments that we consider necessary for a fair presentation of the financial information set forth in those statements. Our historical results are not necessarily indicative of the results that may be expected in the future, and our interim results are not necessarily indicative of the results to be expected for the full year or any other period.

| |

Year Ended December 31, | Nine Months Ended September 30, |

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2011 | 2012 | 2013 | 2013 | 2014 | |||||||||||

| |

(in thousands, except share and per share data) |

|||||||||||||||

Consolidated Statements of Operations Data: |

||||||||||||||||

Revenue |

$ | 14,679 | $ | 35,072 | $ | 66,068 | $ | 41,817 | $ | 67,864 | ||||||

Traffic acquisition costs |

7,762 | 16,485 | 27,712 | 17,160 | 27,552 | |||||||||||

Other cost of revenue |

1,295 | 2,982 | 3,904 | 2,721 | 5,360 | |||||||||||

| | | | | | | | | | | | | | | | | |

Gross profit |

5,622 | 15,605 | 34,452 | 21,936 | 34,952 | |||||||||||

Operating expenses: |

||||||||||||||||

Sales and marketing |

6,325 | 12,938 | 20,475 | 13,771 | 26,905 | |||||||||||

Research and development |

2,555 | 5,376 | 8,666 | 6,014 | 10,102 | |||||||||||

General and administrative |

2,117 | 4,043 | 5,217 | 3,342 | 8,440 | |||||||||||

| | | | | | | | | | | | | | | | | |

Total operating expenses |

10,997 | 22,357 | 34,358 | 23,127 | 45,447 | |||||||||||

(Loss) income from operations |

(5,375 | ) | (6,752 | ) | 94 | (1,191 | ) | (10,495 | ) | |||||||

Other expense (income): |

||||||||||||||||

Interest expense |

88 | 27 | 283 | 187 | 1,005 | |||||||||||

Other expense (income) |

31 | (19 | ) | (2 | ) | (2 | ) | (2 | ) | |||||||

| | | | | | | | | | | | | | | | | |

Total other expense (income) |

119 | 8 | 281 | 185 | 1,003 | |||||||||||

Loss before income taxes |

(5,494 | ) | (6,760 | ) | (187 | ) | (1,376 | ) | (11,498 | ) | ||||||

Provision for income taxes |

— | — | — | — | — | |||||||||||

| | | | | | | | | | | | | | | | | |

Net loss |

$ | (5,494 | ) | $ | (6,760 | ) | $ | (187 | ) | $ | (1,376 | ) | $ | (11,498 | ) | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

Net loss per share of common stock—basic and diluted |

$ | (1.11 | ) | $ | (1.07 | ) | $ | (0.03 | ) | $ | (0.19 | ) | $ | (1.49 | ) | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

Pro forma net loss per share of common stock—basic and diluted(1): |

$ | (0.01 | ) | $ | (0.31 | ) | ||||||||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

Weighted average shares of common stock used in computing net loss per share—basic and diluted |

4,965,155 |

6,340,942 |

7,417,068 |

7,398,718 |

7,737,968 |

|||||||||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

Weighted average shares of common stock used in computing pro forma net loss per share—basic and diluted(1): |

37,114,718 | 37,435,618 | ||||||||||||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

9

| |

Year Ended December 31, | Nine Months Ended September 30, |

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2011 | 2012 | 2013 | 2013 | 2014 | |||||||||||

| |

(in thousands) |

|||||||||||||||

Stock-based compensation expense included above: |

||||||||||||||||

Other cost of revenue |

$ | 1 | $ | 2 | $ | 6 | $ | 4 | $ | 11 | ||||||

Sales and marketing |

32 | 137 | 212 | 152 | 331 | |||||||||||

Research and development |

21 | 155 | 276 | 188 | 461 | |||||||||||

General and administrative |

230 | 259 | 85 | 64 | 651 | |||||||||||

Other financial data: |

||||||||||||||||

Revenue ex-TAC(2) |

$ | 6,917 | $ | 18,587 | $ | 38,356 | $ | 24,657 | $ | 40,312 | ||||||

Adjusted EBITDA(3) |

$ | (4,648 | ) | $ | (5,116 | ) | $ | 2,631 | $ | 621 | $ | (6,859 | ) | |||

- (1)

- Pro forma basic and diluted net loss per share of common stock have been calculated assuming the conversion of all outstanding shares of convertible preferred stock into 29,697,650 shares of common stock as of the beginning of the applicable period or at the time of issuance, if later.

- (2)

- Revenue ex-TAC is not a financial measure prepared in accordance with GAAP. We define Revenue ex-TAC as revenue less traffic acquisition costs. Traffic acquisition costs consist of purchases of advertising impressions from RTB exchanges on a CPM basis. See "—Non-GAAP Financial Measures" for more information and for a reconciliation of Revenue ex-TAC to revenue, the most directly comparable financial measure calculated in accordance with GAAP.

- (3)

- Adjusted EBITDA is not a financial measure prepared in accordance with GAAP. We define Adjusted EBITDA as net loss before income taxes, interest expense, and depreciation and amortization, adjusted to eliminate stock-based compensation expense and change in fair value of convertible preferred stock warrant liability. See "—Non-GAAP Financial Measures" for more information and for a reconciliation of Adjusted EBITDA to net loss, the most directly comparable financial measure calculated in accordance with GAAP.

| |

As of September 30, 2014 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

Actual | Pro forma(1) | Pro forma as adjusted(2) |

|||||||

| |

(in thousands) |

|||||||||

Consolidated Balance Sheet Data: |

||||||||||

Cash and cash equivalents |

$ | 12,480 | $ | 12,480 | $ | |||||

Accounts receivable, net |

29,443 | 29,443 | ||||||||

Working capital |

22,586 | 22,586 | ||||||||

Total assets |

54,702 | 54,702 | ||||||||

Long-term debt, net |

30,862 | 30,862 | ||||||||

Total liabilities |

52,645 | 52,645 | ||||||||

Total convertible preferred stock |

25,476 | — | ||||||||

Total stockholders' (deficit) equity |

(23,419 | ) | 2,057 | |||||||

- (1)

- The pro forma column reflects the conversion of all outstanding shares of convertible preferred stock into 29,697,650 shares of common stock immediately prior to the closing of this offering.

- (2)

- The pro forma as adjusted column reflects the pro forma adjustment described in footnote (1) above and the sale by us of shares of common stock in this offering at an assumed initial public offering price of $ per share, the midpoint of the price range set forth on the cover page of this prospectus, after deducting the underwriting discount and commissions and estimated offering expenses payable by us. A $1.00 increase (decrease) in the assumed initial public offering price of $ per share would increase (decrease) each of pro forma as adjusted cash and cash equivalents, working capital and total assets by $ and decrease (increase) pro forma as adjusted total stockholders' (deficit) equity by approximately $ , assuming the number of shares we are offering, as set forth on the cover page of this prospectus, remains the same, after deducting the underwriting discount and commissions and estimated offering expenses payable by us. The pro forma as adjusted information is illustrative only, and we will adjust this information based on the actual initial public offering price, number of shares offered and other terms of this offering determined at pricing.

10

Non-GAAP Financial Measures

Revenue ex-TAC

We believe that Revenue ex-TAC is a meaningful measure of operating performance because it is frequently used for internal management purposes, indicates the effectiveness of delivering results to advertisers and facilitates a more complete period-to-period understanding of factors and trends affecting our underlying revenue performance. A limitation of Revenue ex-TAC is that it is a measure that other companies, including companies in our industry that have similar business arrangements, either may not use or may calculate differently, which reduces its usefulness as a comparative measure. Because of these and other limitations, we consider, and you should consider, Revenue ex-TAC alongside other GAAP financial measures, such as revenue, gross profit and total operating expenses. The following table presents a reconciliation of Revenue ex-TAC to revenue for each of the periods indicated:

| |

Year Ended December 31, | Nine Months Ended September 30, |

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2011 | 2012 | 2013 | 2013 | 2014 | |||||||||||

| |

(in thousands) |

|||||||||||||||

Revenue |

$ | 14,679 | $ | 35,072 | $ | 66,068 | $ | 41,817 | $ | 67,864 | ||||||

Less: traffic acquisition costs |

(7,762 | ) | (16,485 | ) | (27,712 | ) | (17,160 | ) | (27,552 | ) | ||||||

| | | | | | | | | | | | | | | | | |

Revenue ex-TAC |

$ | 6,917 | $ | 18,587 | $ | 38,356 | $ | 24,657 | $ | 40,312 | ||||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

Adjusted EBITDA

We have included Adjusted EBITDA in this prospectus because it is a key measure used by our management and board of directors to understand and evaluate our core operating performance and trends, to prepare and approve our annual budget and to develop short- and long-term operating plans. In particular, we believe the exclusion of certain items in calculating Adjusted EBITDA can provide a useful measure for period-to-period comparisons of our business. Accordingly, we believe that Adjusted EBITDA provides useful information to investors in understanding and evaluating our operating results.

Our use of Adjusted EBITDA has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our results as reported under GAAP. Some of these limitations are:

- •

- although depreciation and amortization are non-cash charges, the assets being depreciated and amortized may have to be

replaced in the future, and Adjusted EBITDA does not reflect cash capital expenditure requirements for such replacements or for new capital expenditure requirements;

- •

- Adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs;

- •

- Adjusted EBITDA does not reflect the potentially dilutive impact of equity-based compensation;

- •

- Adjusted EBITDA does not reflect interest or tax payments that may represent a reduction in cash available to us; and

- •

- other companies, including companies in our industry, may calculate Adjusted EBITDA differently, which reduces its usefulness as a comparative measure.

11

Because of these and other limitations, we consider, and you should consider, Adjusted EBITDA together with other GAAP-based financial performance measures, including various cash flow metrics, net loss and our other GAAP results. The following table presents a reconciliation of net loss to Adjusted EBITDA for each of the periods indicated:

| |

Year Ended December 31, | Nine Months Ended September 30, |

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2011 | 2012 | 2013 | 2013 | 2014 | |||||||||||

| |

(in thousands) |

|||||||||||||||

Net loss |

$ | (5,494 | ) | $ | (6,760 | ) | $ | (187 | ) | $ | (1,376 | ) | $ | (11,498 | ) | |

Adjustments: |

||||||||||||||||

Interest expense |

88 | 27 | 283 | 187 | 1,005 | |||||||||||

Provision for income taxes |

— | — | — | — | — | |||||||||||

Depreciation and amortization |

443 | 1,063 | 1,956 | 1,402 | 2,180 | |||||||||||

Stock-based compensation |

284 | 553 | 579 | 408 | 1,454 | |||||||||||

Change in fair value of warrant to purchase Series A convertible preferred stock |

31 | 1 | — | — | — | |||||||||||

| | | | | | | | | | | | | | | | | |

Adjusted EBITDA |

$ | (4,648 | ) | $ | (5,116 | ) | $ | 2,631 | $ | 621 | $ | (6,859 | ) | |||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

12

Investing in our common stock involves a high degree of risk. You should consider carefully the risks and uncertainties described below, together with all of the other information in this prospectus, including the section titled "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and related notes, before deciding whether to purchase shares of our common stock. If any of the following risks actually occurs, our business, financial condition, results of operations and prospects could be materially and adversely affected. In that event, the price of our common stock could decline and you could lose part or all of your investment.

Risks Related to Our Business and Industry

Our limited operating history makes it difficult to evaluate our business and prospects and may increase the risks associated with your investment.

We commenced operations in 2006 and, as a result, have only a limited operating history upon which our business and future prospects may be evaluated. Although we have experienced substantial revenue growth in recent years, we may not be able to sustain this rate of growth or even maintain our current revenue levels. We have encountered and will continue to encounter risks and difficulties frequently experienced by growing companies in rapidly developing and changing industries. Our and our business prospects will depend in large part on our ability to:

- •

- build a reputation for a superior solution and create trust and long-term relationships with customers and advertising

agencies;

- •

- distinguish ourselves from competitors in our industry;

- •

- develop and offer a competitive technology platform and offerings that meet our customers' evolving needs;

- •

- maintain and expand our relationships with the real-time bidding, or RTB, exchanges through which we execute our

customers' digital marketing campaigns;

- •

- respond to evolving industry standards and government regulations that impact our business, particularly in the areas of

data collection and consumer privacy;

- •

- prevent or otherwise mitigate failures or breaches of security or privacy;

- •

- expand our business internationally; and

- •

- attract, hire, integrate and retain qualified and motivated employees.

We may need to adapt our current operations to scale our business and achieve long-term profitability. If we are unable to meet one or more of these objectives or fail to implement these changes effectively and on a timely basis, or if we are unable to implement them at all, our revenue may decline, we may not be able to achieve further growth or long-term profitability and our business may suffer.

We have a history of losses, we expect our operating expenses to continue to increase substantially and we may not achieve or sustain profitability in the future.

We incurred net losses of $5.5 million, $6.8 million and $0.2 million in 2011, 2012 and 2013, respectively, and a net loss of $11.5 million for the nine months ended September 30, 2014. As of September 30, 2014, we had an accumulated deficit of $27.4 million. Although our revenue has increased significantly in recent periods, we may not be able to achieve or sustain profitability or this revenue growth rate. In addition, our operating expenses have increased with our revenue

13

growth and we expect our traffic acquisition costs and operating expenses to continue to increase substantially as we expand our business, including adding sales, marketing and related support employees in existing and new territories, engineering employees to support continued investments in our technology platform and general and administrative employees to support our growth and expansion as well as our transition to being a public company. If we do not achieve and sustain profitability, our revenue growth rate declines or our expenses exceed expectations, our financial performance will be adversely affected.

If the MaxPoint Intelligence Platform does not accurately predict the most likely local buyers for specific products, we could lose revenue, which would have a material adverse impact on our operating results and financial condition.

Our solution depends on the ability of the MaxPoint Intelligence Platform to accurately predict the most likely communities of local buyers for specific products and to serve advertisements for those products to those communities. We do not have long-term commitments from our customers and it is relatively easy for our customers or the advertising agencies acting on their behalf to seek alternative providers of digital marketing solutions, as there are no significant switching costs. Thus, we must continuously deliver satisfactory results for our customers to maintain and increase revenue, which depends in part on the continued performance of the MaxPoint Intelligence Platform. Our failure to continuously innovate and improve on the algorithms underlying the MaxPoint Intelligence Platform could result in poor performance, which could in turn result in our customers ceasing to use our solution, which would have a material adverse impact on our operating results and financial condition.

Our operating results fluctuate, which make our future results difficult to predict and could cause our operating results to fall below analysts' and investors' expectations.

Our quarterly and annual operating results have fluctuated in the past, and we expect this to continue for the foreseeable future. These fluctuations could cause our performance to fall below the expectations of securities analysts and investors, and adversely affect the price of our common stock. Because our business is evolving rapidly, our historical operating results may not be useful in predicting our future operating results. Factors that may increase the volatility of our operating results include the factors set forth in this "Risk Factors" section, as well as the following:

- •

- changes in the economic prospects of our customers or the economy generally, which could alter current or prospective

customers' spending priorities, or increase the time or costs required to complete sales;

- •

- changes in demand for and pricing of our MaxPoint Intelligence Platform;

- •

- the impact of macroeconomic factors and seasonality on our customers' businesses and budgets for digital marketing

campaigns, particularly our consumer product and retail customers;

- •

- unpredictable sales cycles;

- •

- changes in our pricing policies, or the pricing policies of our competitors, RTB exchanges or other third-party service

providers;

- •

- the addition or loss of customers;

- •

- the growth or reduction of business with current customers or advertising agencies that act on their behalf;

14

- •

- changes in our customers' advertising budget allocations, agency affiliations or marketing strategies;

- •

- changes and uncertainty in the regulatory environment for us or our customers;

- •

- changes in the availability of media inventory through RTB exchanges;

- •

- the introduction of new technologies, products or service offerings by our competitors;

- •

- changes in our operating expenses and capital expenditures; and

- •

- costs related to acquisitions of people, businesses or technologies.

Based upon all of the factors described above, many of which are beyond our control, and others that we may not anticipate, we have a limited ability to forecast our future revenue, costs and expenses, and as a result, our operating results may fall below our estimates or the expectations of securities analysts and investors.

If we are unable to attract new customers or our existing customers do not allocate a greater portion of their marketing spend to us, our revenue growth will be adversely affected.

To sustain or increase our revenue, we must add new customers and encourage existing customers to allocate a greater portion of their marketing spend to us. As the digital advertising industry matures and competitors introduce lower cost or differentiated products or services, our ability to sell our solution could be impaired. Even after a successful digital marketing campaign or series of campaigns with an existing customer, we frequently must compete to win further business from that customer. We may reach a point of saturation where we cannot continue to grow our revenue from existing customers because of, among other things, internal limits that they may place on their advertising budgets for digital media, particular digital marketing campaigns, local advertising or a particular provider. If we are unable to attract new customers or obtain new business from existing customers, our revenue, growth and business will be adversely affected.

If we fail to develop new solutions and services or enhance our existing solution and services, we may not attract and retain customers, and our revenue and results of operations may decline.

We compete for customers that want to execute digital marketing campaigns. Our industry is subject to rapid changes in standards, technologies, products and service offerings, as well as advertiser expectations. We continuously need to develop new solutions and services and enhance our existing solution and services to meet advertiser demands and respond to industry changes. New customer demands, superior competitive offerings or new industry standards could render our existing solution unattractive, unmarketable or obsolete and require us to make substantial changes to our technology platform or business model. Our failure to adapt to a rapidly changing market or to anticipate customer demand could harm our business and our financial performance.

If we do not manage our growth effectively, the quality of our solution may suffer, and our operating results may be negatively affected.

We continue to experience rapid growth in our headcount and operations, which will continue to place significant demands on our management, operational and financial infrastructure. To manage our growth effectively, we must continue to improve and expand our infrastructure, including our IT systems, financial and administrative systems and controls. We must also continue to manage our employees, operations, finances, research and development and capital investments efficiently. Our productivity and the quality of our solution may be adversely affected if we do not integrate and train our new employees, particularly our sales and account management personnel,

15

quickly and effectively. If we continue our rapid growth, we may incur significant additional expenses, and our growth may continue to strain our management, resources, infrastructure and ability to maintain the quality of our solution. If the current and future members of our management team do not effectively scale with our growth, the quality of our solution may suffer and our corporate culture may be harmed. Failure to manage our future growth effectively could cause our business to suffer, which, in turn, could have an adverse impact on our results of operations and financial condition.

We may not be able to compete successfully against current and future competitors, which may result in declining revenue or inability to grow our business.

Competition for our customers' advertising budgets is intense, and we expect competition to increase in the future with more advertising occurring online. Our principal competition includes traditional advertising and direct marketing companies, such as Gannett Company, Inc., The McClatchey Company, News America Marketing, Valassis Communications, Inc. and Valpak Direct Marketing Systems, Inc. In addition, we compete or may compete with:

- •

- companies that offer demand-side platforms that allow customers to purchase inventory directly from RTB exchanges or other

third parties;

- •

- advertising networks and advertising agencies;

- •

- traditional advertising channels, such as television, radio and print;

- •

- services offered through large online portals, such as Yahoo! Inc. and Google Inc.;

- •

- companies providing online search advertising, for which we do not offer a solution;

and

- •

- technology companies providing online marketing platforms focused on local businesses.

Many current and potential competitors have advantages, such as longer operating histories, greater name recognition, larger customer bases, greater access to media inventory, more access to Internet user data and significantly greater financial, technical, sales and marketing resources. Increased competition may result in reduced pricing for our solution, longer sales cycles or a decrease of our market share, any of which could negatively affect our revenue and future operating results and our ability to grow our business.

We have historically relied, and expect to continue to rely, on a small number of customers for a substantial majority of our revenue, and the loss of any of these customers may significantly harm our business, results of operations and financial condition.

Our customers are primarily enterprises with national brands in a number of industries. We sell our solution either directly to our customers or through advertising agencies that act on behalf of our customers. A relatively small number of customers have historically accounted for a substantial majority of our revenue. For the years ended December 31, 2011, 2012 and 2013, our top ten customers accounted for approximately 57%, 31% and 36% of our revenue, respectively. For the year ended December 31, 2011, one customer accounted for approximately 28% of our revenue, and for the years ended December 31, 2012 and 2013, no single customer represented more than 10% of our revenue. For the nine months ended September 30, 2014, no single customer represented more than 10% of our revenue. We expect that we will continue to depend upon a relatively small number of customers for a substantial majority of our revenue for the foreseeable future while we continue to broaden our customer base. As a result, if we fail to successfully attract or retain customers, or if existing customers reduce or delay their marketing spend with us, our business, results of operations and financial condition would be harmed. Moreover, a significant portion of our customers' products are purchased at a limited number of large national retailers.

16

Any material decline in these customers' sales at the physical retail locations of these large national retailers may adversely impact our business.

We rely on advertising agencies that act on behalf of our customers for a substantial majority of our revenue. The loss of any such relationships or increased competition from such advertising agencies or agency trading desks could materially harm our business.

We rely on advertising agencies that act on behalf of our customers for a substantial majority of our revenue. Multiple advertising agencies operating within three global advertising networks represented numerous customers accounting for approximately 18%, 13% and 10% of our revenue, respectively, for the year ended December 31, 2013. For the nine months ended September 30, 2014, multiple advertising agencies operating within one global advertising network represented numerous customers accounting for approximately 15% of our revenue. In addition, for reasons specific to individual agencies, some agencies may not recommend us to the national brands they represent, even if our solution is more effective than alternative solutions. Certain of those agencies are creating their own competitive solutions, referred to as agency trading desks. If the agency trading desks are successful in leveraging agency relationships with our customers, we may be unable to compete successfully even if our solution is more effective.

Potential "Do Not Track" standards or government regulation could negatively impact our business by limiting our access to the anonymous user data that the MaxPoint Intelligence Platform uses to predict local purchase demand and execute the digital marketing campaigns we run, and as a result may degrade our performance for our customers, which, in turn, may have a material adverse effect on our business.

As the use of cookies and other tracking mechanisms has received ongoing media attention, and some government regulators and privacy advocates have suggested creating a "Do Not Track" standard that would allow Internet users to express a preference, independent of cookie settings in their browser, not to have website browsing recorded. In 2010, the Federal Trade Commission, or FTC, issued a staff report criticizing the advertising industry's self-regulatory efforts as too slow and lacking adequate consumer protections. The FTC emphasized a need for simplified notice, choice and transparency to consumers regarding collection, use and sharing of data, and it suggested implementing a "Do Not Track" browser setting that allows consumers to choose whether to allow "tracking" of their online browsing activities. For example, in a 2012 report, the FTC encouraged continued improvements in consumer choice with respect to behavioral advertising and full implementation of a "Do Not Track" mechanism. All of the major Internet browsers have implemented some version of a "Do Not Track" setting. Microsoft's Internet Explorer 10 includes a "Do Not Track" setting that is selected by default. However, there is no definition of "tracking," no clarity as to the specific technologies or practices that would be affected, no consensus regarding what message is conveyed by a "Do Not Track" setting and no industry standards regarding how to respond to a "Do Not Track" preference. The World Wide Web Consortium chartered a "Tracking Protection Working Group" in 2011 to convene a multi-stakeholder group of academics, thought leaders, companies, industry groups and consumer advocacy organizations, to create a voluntary "Do Not Track" standard for the web. The group has yet to agree upon a standard. The FTC has stated that it will pursue a legislative solution if the industry cannot agree upon a standard. The "Do-Not-Track Online Act of 2013" was introduced in the United States Senate in February 2013, and similar legislation has been and could be introduced at the federal and state levels. If a "Do Not Track" browser setting is adopted by many Internet users, and the standard either imposed by state or federal legislation, or agreed upon by standard setting groups, prohibits us from using non-personal data as we currently do, then that could hinder growth of advertising and content production on the web generally, cause us to change our business practices and have a material adverse effect on our business.

17

Furthermore, in the European Union, or E.U., Directive 2009/136/EC, commonly referred to as the "Cookie Directive," directs E.U. member states to ensure that accessing information on an Internet user's computer, such as through a cookie or other tracking mechanism, is allowed only if the Internet user has given his or her consent. In response, member states have adopted and implemented, and may continue to adopt and implement further legislation that negatively impacts the use of cookies and other tracking mechanisms for online advertising. Limitations on the use or effectiveness of cookies, whether imposed by E.U. member state implementation of the Cookie Directive or otherwise, may impact the performance of our solution, cause us to change our business practices and have an adverse effect on our business.

Legislation and regulation of online businesses, including privacy and data protection regimes, could create unexpected costs, subject us to enforcement actions for compliance failures, or cause us to change our technology platform or business model, which may have a material adverse effect on our business.

Legislation and government regulation, including laws and regulations that limit our ability to collect and analyze the data we use in our MaxPoint Intelligence Platform, could adversely affect our business and operating results. U.S. and foreign governments have enacted or are considering legislation related to online advertising, and we expect to see an increase in legislation and regulation related to advertising online, the use of geolocation data to inform advertising, the collection and use of anonymous Internet user data and unique device or other identifiers (such as IP addresses or mobile device identifiers), and other data protection and privacy regulation. Such legislation or regulation could affect the costs of doing business online, and may adversely affect the demand for our solution or otherwise harm our business, results of operations, and financial condition. For example, a wide variety of provincial, state, national, and international laws and regulations apply to the collection, use, retention, protection, disclosure, transfer, and other processing of personal data. While we do not collect data that traditionally has been considered personal data by U.S. regulators (such as name, email address, address, phone numbers, social security numbers, credit card numbers or individualized financial or health data), we typically do collect and store IP addresses, device identifiers, geolocation information, cookie data and other data that are or may be considered personal data in some jurisdictions or otherwise may be the subject of legislation or regulation. Evolving and changing definitions of personal data, within the European Union, the United States, and elsewhere, especially relating to classification of IP addresses, machine or device identifiers, location data, and other information, have in the past, and may cause us in the future, to change our business practices, or may limit or inhibit our ability to operate or expand our business. Similarly, the law is unsettled concerning the definition and permissible uses of "sensitive" data, including with respect to certain financial, geolocation and health data. Regulators and legislators have proposed additional limitations on the collection and use of such data, which could have a material adverse effect on our business. More generally, data protection and privacy-related laws and regulations are evolving and may result in ever-increasing regulatory and public scrutiny and escalating levels of enforcement and sanctions.

In addition, data security is of increasing concern to U.S., state and foreign regulators and, as a result, the legal standards for data security and the consequences for violating those standards continue to evolve. And the threat posed by cyber-attacks and data breaches continues to grow. While we take measures to protect the security of information that we collect, use, and disclose in the operation of our business, and to offer certain privacy protections with respect to such information, such measures may not always be effective. In addition, while we take steps to avoid collecting personally identifiable data about consumers, we may inadvertently receive this information from customers or from the advertising agencies that act on their behalf or through the process of delivering advertising.

18

In the United States, our privacy, data security and handling practices are subject to regulation at both the federal and state level, and the FTC and many states actively enforce against unfair and deceptive trade practices, including the violation of privacy policies and representations. Outside of the United States, our privacy and data handling practices are subject to regulation by data protection authorities and other regulators in the countries in which we do business. Our failure to comply with applicable laws and regulations concerning privacy or data security, or to protect personal data, could result in enforcement action against us, including fines, imprisonment of our officers, and public censure; claims for damages by consumers and other affected individuals; damage to our reputation; and loss of goodwill, any of which could have a material adverse impact on our results of operations, financial performance, and business. Moreover, even the perception of privacy or security concerns, whether or not valid, may harm our reputation and inhibit adoption of our solution by current and future customers or the advertising agencies that act on their behalf.

Our ability to generate revenue depends on our collection of significant amounts of data from various sources.

Our ability to deliver our business intelligence and marketing automation software solution depends on our ability to successfully leverage significant amounts of data, including data that we collect from our customers and acquire from third parties, as well as raw data captured by our proprietary consumer purchase intent model. The foundation of our local targeting is our proprietary Digital Zip architecture, a digital grid of households organized into over 44,000 specific neighborhoods, or Digital Zips. We create a profile for each Digital Zip by using third party data and proprietary data captured by our consumer purchase intent model, including IP addresses and consumer online browsing data, and any limit to our access or use of these types of data could impact our ability to match the most likely community of local buyers with specific products, which could have an adverse effect on our ability to successfully execute our customers' digital marketing campaigns on a real-time basis. Our customers often share with us enterprise data, such as point of sale and spending information, and certain customers provide us with supply chain management and customer relationship management, or CRM, data. If our enterprise customers do not share their data, our ability to scale and provide our solution could be adversely affected. In addition, our ability to successfully leverage vast amounts of data is dependent upon our continued ability to access and utilize up-to-date data. Our ability to access and use such data could be restricted by a number of factors, including consumer choice, restrictions imposed by our customers, changes in technology and new developments in laws, regulations and industry standards. If the data we utilize is out-of-date or stale, our predictions, recommendations and business intelligence will be ineffective and our reputation will suffer. Further, we sometimes use cookies and other tracking mechanisms to deliver our solution, and certain web browsers, including Safari, currently block or are planning to block some or all third-party cookies by default. As a result, we could be blocked from serving advertisements on the basis of cookies to users that utilize web browsers that block third-party cookies. Any limitation on our ability to collect data would make it more difficult for us to deliver effective solutions that meet the needs of national brands. This, in turn, could adversely affect our business and operating results.

We may experience outages and disruptions of our services or experience data security incidents if we fail to maintain adequate security and supporting infrastructure our systems, which may harm our brand and reputation, result in regulatory enforcement, actions or litigation and negatively impact our revenue and results of operations.

Creating the appropriate support for our technology platform, including storing large amounts of data and managing our computational infrastructure, is expensive and complex, and our failure to create and maintain such support, particularly as we scale our system to support the growth in our business, could result in operational inefficiencies, disruptions or failures and increased

19