Attached files

| file | filename |

|---|---|

| EX-21 - EXHIBIT 21 - BROADCOM CORP | a20141231-10k_ex21.htm |

| EX-23.1 - EXHIBIT 23.1 - BROADCOM CORP | a20141231-10k_ex231.htm |

| EX-10.41 - EXHIBIT 10.41 - BROADCOM CORP | a20141231-10k_ex1041.htm |

| EX-10.48 - EXHIBIT 10.48 - BROADCOM CORP | a20141231-10k_ex1048.htm |

| EX-10.20 - EXHIBIT 10.20 - BROADCOM CORP | a20141231-10k_ex1020.htm |

| EXCEL - IDEA: XBRL DOCUMENT - BROADCOM CORP | Financial_Report.xls |

| EX-31.2 - EXHIBIT 31.2 - BROADCOM CORP | a20141231-10k_ex312.htm |

| EX-31.1 - EXHIBIT 31.1 - BROADCOM CORP | a20141231-10k_ex311.htm |

| EX-32 - EXHIBIT 32 - BROADCOM CORP | a20141231-10k_ex32.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2014

or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number: 000-23993

Broadcom Corporation

(Exact Name of Registrant as Specified in Its Charter)

California | 33-0480482 |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

5300 California Avenue

Irvine, California 92617-3038

(Address of Principal Executive Offices) (Zip Code)

(Registrant’s telephone number, including area code): (949) 926-5000

Securities registered pursuant to Section 12(b) of the Act:

Title of Class | Name of Exchange on Which Registered |

Class A Common Stock, $0.0001 par value | The Nasdaq Stock Market LLC (Nasdaq Global Select Market) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

(Check one): | |||

Large accelerated filer þ | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ |

(Do not check if a smaller reporting company) | |||

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2). Yes ¨ No þ

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant on June 30, 2014, was $20.00 billion (based on the closing sales price of the registrant’s common stock on the Nasdaq Global Select Market on that date). As of December 31, 2014 there were 550 million shares of Class A common stock and 49 million shares of Class B common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III incorporates by reference certain information from the registrant’s definitive proxy statement for the 2015 Annual Meeting of Shareholders to be filed on or before April 30, 2015.

Broadcom®, the pulse logo, and BroadR-Reach® are among the trademarks of Broadcom Corporation and/or its affiliates in the United States, certain other countries and/or the EU. Any other trademarks or trade names mentioned are the property of their respective owners.

©2015 Broadcom Corporation. All rights reserved. | This Annual Report on Form 10-K is printed on recycled paper. |

BROADCOM CORPORATION

ANNUAL REPORT ON FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2014

TABLE OF CONTENTS

Page | |

PART I | |

PART II | |

PART III | |

PART IV | |

Cautionary Statement

All statements included or incorporated by reference in this Annual Report on Form 10-K, other than statements or characterizations of historical fact, are forward-looking statements within the meaning of the federal securities laws, including the Private Securities Litigation Reform Act of 1995. Examples of forward-looking statements include, but are not limited to, statements concerning projected total net revenue, costs and expenses and gross margin; our accounting estimates, assumptions and judgments; the demand for our products; our dependence on a few key customers and/or design wins for a substantial portion of our revenue; our commitment to research and development efforts; the characteristics of our patents; the accuracy of our estimates and forecasts; estimates related to the amount and/or timing of the expensing of unearned stock-based compensation expense and stock-based compensation as a percentage of revenue; manufacturing, assembly and test capacity; the effect that economic conditions, seasonality and volume fluctuations in the demand for our customers’ consumer-oriented products will have on our quarterly operating results; our ability to adjust operations in response to changes in demand for existing products and services or the demand for new products requested by our customers; the competitive nature of and anticipated growth in our markets; our ability to consummate acquisitions and integrate their operations successfully; our ability to migrate to smaller process geometries; our success in pending intellectual property litigation matters; our potential needs for additional capital; inventory and accounts receivable levels; our ability to permanently reinvest our foreign earnings; the effect of potential changes in U.S. or foreign tax laws and regulations or the interpretation thereof; the level of accrued rebates; and our intention to continue to pay dividends. These forward-looking statements are based on our current expectations, estimates and projections about our industry and business, management’s beliefs, and certain assumptions made by us, all of which are subject to change. Forward-looking statements can often be identified by words such as “anticipates,” “expects,” “intends,” “plans,” “predicts,” “believes,” “seeks,” “estimates,” “may,” “will,” “should,” “would,” “could,” “potential,” “continue,” “ongoing,” similar expressions, and variations or negatives of these words. These statements are not guarantees of future performance and are subject to risks, uncertainties and assumptions that are difficult to predict. Therefore, our actual results could differ materially and adversely from those expressed in any forward-looking statements as a result of various factors, some of which are listed under the section entitled “Risk Factors” in Part I, Item 1A of this Report. These forward-looking statements speak only as of the date of this Report. We undertake no obligation to revise or update publicly any forward-looking statement to reflect future events or circumstances.

PART I

Item 1. Business

Overview

Broadcom Corporation (including our subsidiaries, referred to collectively in this Annual Report as “Broadcom,” “we,” “our” and “us”) is a global leader and innovator in semiconductor solutions for wired and wireless communications. Broadcom was incorporated in California in August 1991. Our Class A common stock trades on the Nasdaq Global Select Market® under the symbol BRCM. Our principal executive offices are located at 5300 California Avenue, Irvine, California 92617-3038, and our telephone number at that location is 949.926.5000. Our Internet address is www.broadcom.com. The inclusion of our Internet address in this Report does not include or incorporate by reference into this Report any information on our website. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and other U.S. Securities and Exchange Commission (SEC) filings are available free of charge through the Investor Relations section of our website as soon as reasonably practicable after such reports are electronically filed with, or furnished to, the SEC. The SEC also maintains a web site, www.sec.gov, which contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

Communications technologies continue to evolve rapidly due to growth in the number of connected devices, continual increased demand for faster speeds across wired and wireless networks, the emergence of new communications standards, and the introduction of new technologies and features. Success in this field is influenced by the strength of a supplier’s intellectual property, or IP, portfolio and the ability to integrate that IP into complex, single-chip solutions. We have one of the strongest IP portfolios among global fabless semiconductor suppliers, as

1

ranked by the Institute of Electrical and Electronics Engineers (IEEE). Our strategy centers on designing highly-complex and highly-integrated semiconductor solutions that leverage our leading IP portfolio and target a broad range of wired and wireless communications markets. We provide one of the industry’s broadest portfolio of highly-integrated system-on-a-chip solutions, or SoCs, that seamlessly deliver voice, video, data and multimedia connectivity in the home, office and mobile environments. This focus on integration enables Broadcom to provide products that deliver leading performance, consume relatively low power and take up a minimal amount of space within our customers’ products. Our strong and growing IP portfolio and solid track record in designing highly-integrated SoCs enables us to quickly and efficiently respond to a rapidly evolving marketplace for communication solutions.

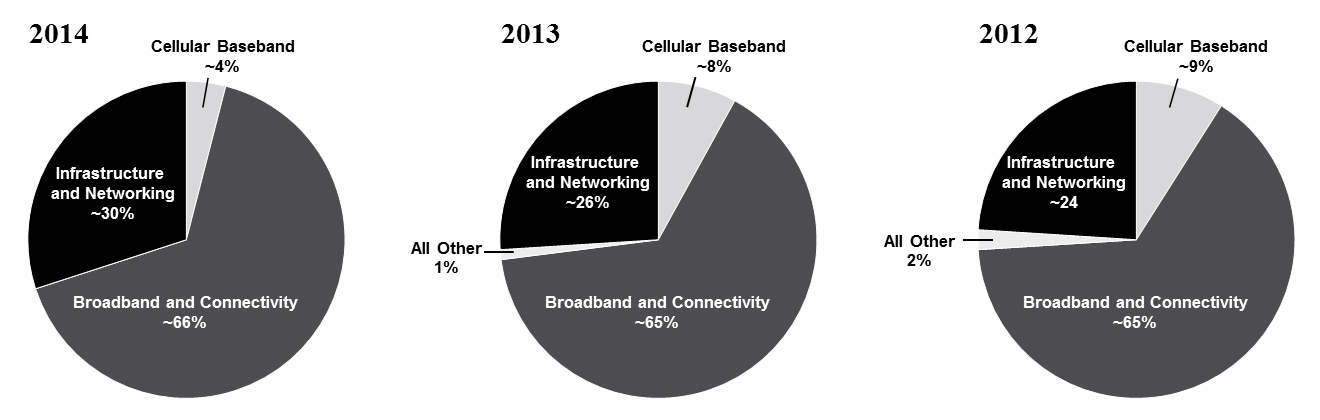

Reportable Segments

Our business is structured around two reportable segments: (i) Broadband and Connectivity; and (ii) Infrastructure and Networking.

Net revenue for these reportable segments is presented below. “Cellular Baseband” represents the operations of the cellular baseband business that is currently winding down. “All Other” is comprised of income from our April 2009 agreement with Qualcomm Incorporated, or the Qualcomm Agreement. See detailed discussion in the “Overview” section in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Percentage of Net Revenue

Net Revenue: $8.43 billion | Net Revenue: $8.31 billion | Net Revenue: $8.01 billion | ||

Broadband and Connectivity Reportable Segment

Our solutions in this reportable segment include: set-top box solutions, broadband modem solutions, connectivity solutions, and a range of other technologies. Customer products incorporating our solutions in this reportable segment include: set-top boxes, or STBs, central office broadband access equipment, residential gateways, stand-alone broadband access modems, and a range of consumer devices, including smartphones and tablets, wearable devices, PCs, laptops, access points, and others.

Set-Top Box Solutions

Global service providers are increasingly introducing new and enhanced technologies and services in STBs, including transcoding, digital video recording functionality, higher definition, increased networking capabilities, and more tuners to enable faster channel change and more simultaneous recordings. Service providers are also deploying High Efficiency Video Coding, or HEVC, a video compression format that is a successor to the H.264/MPEG-4 format. HEVC enables Ultra HD services by effectively doubling the capacity of existing networks to deploy new or existing content.

2

We offer complete platform solutions for cable, satellite, Internet Protocol, over-the-top and terrestrial STBs. Our families of STB solutions support the complete range of resolutions, from standard definition, to high definition, and Ultra HD. We also provide a family of related mixed-signal and digital RF tuner front-ends. Our latest generation of digital tuners leverages our Full-Band Capture (FBC) technology, which digitizes the entire downstream spectrum, replacing multiple tuners with a single FBC digital tuner. Our FBC technology is integrated into a range of gateways and STB platforms.

Broadband Modem Solutions

Global service providers continue to deploy next generation broadband access technologies across multiple standards, including DSL, cable and fiber, to provide more bandwidth and faster speeds to consumers. Over the coming years, we see global service providers moving toward DOCSIS 3.1 for cable modem technologies, G.Fast for DSL, and deploying more fiber-based solutions to increase speeds and bandwidth for customers.

We offer complete platform solutions for DSL, cable and fiber for both central office deployments and consumer premise equipment (CPE). For CPE deployments, we see continued transitions toward residential gateway solutions, which are frequently powered by Broadcom. For the central office, our solutions include cable modem termination systems for cable, optical line termination for fiber, and DSLAM’s for DSL.

Connectivity Technologies

Our connectivity solutions include integrated and discrete Wi-Fi, Bluetooth and near field communication, or NFC, solutions. Devices incorporating our wireless connectivity solutions include: smartphones; tablets; laptops, and related peripherals; wireless home routers and gateways; printers; handheld media devices; home gaming systems; smart TVs and connected STBs; as well as a range of wearable and connected devices, including watches and glasses, smoke alarms and thermostats.

Wi-Fi allows devices on a local area network to communicate wirelessly. It adds the convenience of mobility to the utility of high-speed data networks. We offer a family of high performance, low power Wi-Fi chipsets. We support a broad range of value added features on top of our WiFi solutions, including Wi-Fi Direct, WiFi Display and Miracast.

Bluetooth is a low power technology that enables direct connectivity between devices. We offer a complete family of Bluetooth silicon and software solutions that enable manufacturers to easily and cost-effectively add Bluetooth functionality to virtually any device. We continue to drive the evolution of Bluetooth with support of the Bluetooth Low Energy (BLE) standard, or Bluetooth Smart, for supporting low power applications such as health and fitness, medical devices, and wearable devices.

NFC, an ultra short-range wireless standard that enables simple pairing between devices, has been adopted for contactless payment systems and can also be implemented to facilitate simple pairing between a variety of devices, including smartphones, tablets, TVs, remote controls, wireless mice, and Bluetooth headsets. We offer a family of low-power NFC solutions for a range of consumer devices.

Other Broadband and Connectivity Technologies

Our other broadband and connectivity technologies include small cell/femtocell solutions, location (GPS) and touch controllers.

Small-cell: We offer complete 3G/4G platform solutions for femtocells and small and residential cells. We see service providers continuing to deploy small cells to add capacity and coverage to their cellular network topology. Femtocells are deployed primarily in residences to enhance cellular coverage in the home. Small cells are low-powered radio access nodes that operate in licensed and unlicensed spectrum with a range of 10 meters to 2 kilometers. Service providers are deploying small cells to enable data offload, which will enable them to more

3

efficiently utilize their limited spectrum.

Location (GPS): We also offer a family of GPS, assisted GPS (A-GPS) and GNSS semiconductor products, software and data services. Our location-based services technology delivers data to our GNSS devices, further enhancing performance and reliability. These GPS solutions are part of a broader location platform that leverages a broad range of communications technologies, including WiFi, Bluetooth, MEMS sensors and GPS, to provide more accurate location, navigation and more functionality indoors, including indoor location and navigation.

Touch controllers: We also offer touch controllers targeted to one customer, which are integrated circuits designed to process signals from touch screens on mobile devices. Our touch controllers can be found in smartphones and tablets.

Infrastructure and Networking Reportable Segment

Our solutions in this reportable segment include: Ethernet switches and PHYs, which includes switches and fabrics; copper and optical transceivers; backplane and optical front-end physical layer devices; processors (including multicore processors); and other Infrastructure and Networking technologies (including knowledge-based processors, VoIP solutions, microwave backhaul solutions and radio head digital front ends). We also offer a family of Ethernet controllers.

Customer products incorporating our solutions in this reportable segment include: service provider metro equipment; edge and core routers, wireless infrastructure and wireless access points; switches and routers; servers and workstations; network interface cards; LAN on motherboard applications; optical networks and dense wave division multiplexing applications; security appliances; storage controllers; microwave links for wireless backhaul; cellular remote radio heads; automobile Ethernet networks; point-of-sale equipment; and other embedded SoC subsystems.

Ethernet Switches and PHYs

Ethernet is a ubiquitous interconnection technology that enables high performance and cost effective networking infrastructure across the enterprise, service provider, data center and small and medium business spaces.

Ethernet Switch. We offer a broad set of Ethernet switching products that are optimized for service provider networks, data center implementations, and enterprise and small-and-medium businesses. These solutions range from low-cost five port switch chips to complete solutions enabling in excess of 400 terabits per second of switching capacity in a multi-chassis configuration. More specifically:

• | Data center - High capacity, low latency switching silicon that supports advanced protocols around virtualization and multi-pathing. Our Ethernet switching fabric technologies provide the ability to build highly scalable flat networks supporting tens of thousands of servers and supporting 100 gigabits per second (Gbps) Ethernet. |

• | Service provider - Our service provider switch portfolio enables carrier/service provider networks to support a large number of services in the wireless backhaul, access, aggregation and core of their networks. In addition, we also offer a full duplex 100 Gbps fully programmable packet processor. |

• | Enterprise and small-and-medium businesses (SMB) - For enterprise applications, we offer product families that combine multi-layer switching capabilities and wire-speed Gigabit, 10, 40 and 100 Gbps Ethernet switching performance for unified wired and wireless enterprise business networks. Our family of SMB Ethernet switch products are designed to support lower power modes and comply with industry standards around energy efficient Ethernet. |

4

Ethernet Copper Transceivers. Our high performance Ethernet transceivers are built upon a proprietary digital signal processing communication architecture optimized for high-speed network connections and support the latest standards and advanced features, such as energy efficient Ethernet, data encryption and time synchronization at one or 10 Gbps.

Automotive Ethernet. As consumer demand for in-vehicle connectivity continues to grow, automotive manufacturers are under pressure to deliver competitive, innovative features while minimizing cost. Broadcom’s BroadR-Reach® automotive solutions allow multiple in-vehicle systems (such as infotainment, on-board diagnostics and automated driver assistance) to simultaneously access information over unshielded single twisted pair cable. Our automotive Ethernet product portfolio consists of five devices (including three highly integrated switches with embedded PHYs and two stand-alone PHY solutions) that deliver high-performance bandwidth of 100Mbps and beyond while dramatically reducing connectivity costs and cabling weight, as well as increasing energy efficiency.

Backplane and Optical Front-End Physical Layer Devices. To address increasing volumes of data traffic both in data centers and service provider networks, we offer a portfolio of 10G and 40G Ethernet transceivers, 100 Gbps gear boxes, forward error correction solutions, and chips for backplanes and optical interconnect. These devices are low-power solutions for very high density 10, 40 and 100 Gbps switching and transport solutions. We also offer 2.5 Gbps and 10 Gbps SONET/SDH/OTN transceivers that enable the development of low-cost, high-density optical transport equipment, enabling telecommunications and service providers to efficiently deliver data and voice traffic over existing fiber networks.

Processors

Multicore Communication Processor. Used in building current and next-generation server, storage, data networking and wireless equipment, our multicore solutions include high performance quad-issue, quad-threaded central processing units (CPUs) that are coupled with high performance on-chip fabric and accelerators, enabling multi-chip cache coherent configurations. Broadcom’s high-speed communications processors support complex networking applications, such as deep content switching, routing and load balancing at wireline speed. In addition to our multicore processors, we provide a line of highly integrated processor and networking solutions based on ARM processors.

Ethernet Controllers

We offer Ethernet controllers for servers, workstations, and desktop and notebook computers, supporting multiple generations of Ethernet technology. We also supply ASIC controllers through a relationship with QLogic Corporation.

Other Infrastructure and Networking Technologies

Knowledge-Based Processors (KBP). Broadcom’s knowledge-based processors enable high-performance decision-making for packet processing in a variety of advanced devices in the enterprise, metro, access, edge and core networking spaces. This family features the ability to process packets at wire-speed while consuming relatively little power.

Microwave Modems and RF. Our family of microwave and millimeter modems and RF chip sets allows our customers to build high performance wireless backhaul and LAN extension products for service providers. They include features such as dual polarization for increased throughput, integrated networking functionality and full path protection.

VoIP solutions. Our family of VoIP solutions allows our customers to build VoIP-enabled telephony products primarily for the enterprise environment.

Digital Front-End Processors (DFE). We offer a family of Remote Radio Head DFE products that can be found in wireless infrastructure deployments around the globe.

5

Custom Silicon Products

We offer customers a range of custom application-specific integrated circuit, or ASIC, products that integrate customer-specific intellectual property into larger, more highly integrated solutions. This approach enables our customers to leverage their own intellectual property while still benefiting from the cost, power and performance benefits of a more integrated single-chip solution.

Reference Platforms

To assist our customers in developing products, we develop reference platforms designed around our integrated circuit products that represent prototypical system-level applications. These reference platforms generally include an extensive suite of software drivers, as well as protocol and application layer software. By providing reference platforms that may ultimately be incorporated into our customers’ end products, we believe we enable our customers to achieve easier and faster transitions from the initial prototype designs through final production releases. We believe these reference platform designs also significantly enhance customers’ confidence that our products will meet their market requirements and product introduction schedules.

Customers and Strategic Relationships

We sell our products to leading wired and wireless communications manufacturers. We have also established strategic relationships with multiservice operators that provide wired and wireless communications services to consumers and businesses. Our leading customers currently shipping wired and/or wireless communications equipment and devices incorporating our products include:

• Alcatel-Lucent | • Humax |

• Apple | • Pace |

• Arris | • Samsung |

• Cisco | • Technicolor |

• Huawei Technologies | • ZTE |

A small number of customers have historically accounted for a substantial portion of our net revenue. Contributions to our net revenue by these customers have increased in the last several years. Sales to our five largest customers represented 44.1%, 48.3% and 46.9% of our net revenue in 2014, 2013 and 2012, respectively. In 2014, 2013 and 2012 sales to Samsung represented 14.2%, 21.3%, and 17.3% of our net revenue, respectively. In 2014, 2013 and 2012 sales to Apple represented 14.0%, 13.3%, and 14.6% of our net revenue, respectively. See Note 11 of Notes to Consolidated Financial Statements, included in Part IV, Item 15 of this Report. We expect that our key customers will continue to account for a substantial portion of our net revenue in 2015 and in the foreseeable future. We typically sell products pursuant to purchase orders that customers can generally cancel, change or defer on short notice without incurring a significant penalty.

Research and Development

We have assembled a large team of experienced engineers and technologists, many of whom are leaders in their particular field or discipline. As of December 31, 2014 we had approximately 8,000 research and development employees (or approximately 75% of our total employees), including over 800 employees with Ph.D.s. These key employees are involved in advancing our core technologies, as well as product development. We believe that increased intellectual property integration and the timely introduction of new products are essential to our growth. Because SoC solutions benefit from the same underlying core technologies, we are able to address a wide range of communications markets with a relatively focused investment in research and development. Our research and development expense was $2.37 billion, $2.49 billion and $2.32 billion in 2014, 2013 and 2012, respectively. These amounts included stock-based compensation expense for employees engaged in research and development of $304 million, $363 million and $368 million in 2014, 2013 and 2012, respectively. We have design centers throughout the United States, including our principal design facilities in Irvine, California and Santa Clara County, California, as well as Asia, Europe and the Middle East.

6

Our revenue and our research and development costs as a percentage of revenue are subject to the cyclicality and seasonality of our industry. Our research and development costs on an absolute dollar basis are not, however, meaningfully affected by these patterns. We endeavor to manage our cost structure to attain long-term business objectives, rather than focusing on short-term profit targets.

Manufacturing

Wafer Fabrication

We depend on multiple foundry subcontractors located in Asia to manufacture a majority of our products. Our key silicon foundries are:

• | Taiwan Semiconductor Manufacturing Corporation, or TSMC, in Taiwan; |

• | United Microelectronics Corporation in Singapore and Taiwan; |

• | Semiconductor Manufacturing International Corporation in China; and |

• | GlobalFoundries, Inc. (formerly Chartered Semiconductor Manufacturing) in Singapore and Germany. |

By subcontracting manufacturing, we focus resources on design and test applications where we believe we have greater competitive advantages. This strategy also avoids the high capital cost of owning and operating semiconductor wafer fabrication facilities. See “Risk Factors” under Item 1A of this Report for a discussion of the risks associated with our dependence on independent foundry subcontractors.

Most of our products are manufactured using complementary metal oxide semiconductor, or CMOS, process technology. Our products are currently fabricated on a variety of processes ranging from 500 nanometers to 28 nanometers. We generally evaluate the benefits of migrating to smaller geometry process technologies based on the benefits in performance, power and/or cost. In 2014, approximately 50% of our products were manufactured in 40 nanometers and 30% in 65 nanometers. We are designing most new products in 40 nanometers and 28 nanometers, and are beginning to evaluate FinFET technologies. As we move to smaller geometries, we have become increasingly reliant on Taiwan Semiconductor Manufacturing Company (TSMC) for the manufacture of product at and below 40 nanometers. See “Risk Factors” under Item 1A of this Report for a discussion of the risks associated with transitioning to smaller geometry process technologies.

Assembly and Test

Our products are tested at either the wafer level and/or the packaged finished products level. Our product testing is conducted by independent foundries, and independent test subcontractors. The die are assembled into finished products by independent assembly and package subcontractors. A majority of our test and assembly is performed by the following independent subcontractors:

• | Advanced Semiconductor Engineering (ASE) in Singapore, China and Taiwan (test, assembly and packaging); |

• | Siliconware Precision in Taiwan (test, assembly and packaging); |

• | United Test and Assembly Center in Singapore, China and Thailand (test, assembly and packaging); |

• | Amkor in Korea, Philippines, Taiwan and China (assembly and packaging only); and |

• | STATSChipPAC in Singapore, Korea, Malaysia and China (test, assembly and packaging). |

See “Risk Factors” under Item 1A of this Report for a discussion of the risks associated with our dependence on third party assembly and test subcontractors.

7

Quality Assurance

We consider product reliability from the initial stage of the design cycle through each specific design process, from layout through testing. Our operations and quality engineering teams closely manage the interface between manufacturing and design engineering. We evaluate each assembly and foundry subcontractor. We also participate in quality and reliability monitoring by reviewing electrical and parametric data from our wafer foundry and assembly subcontractors. We closely monitor wafer foundry production to ensure consistent overall quality, reliability and yield levels. All of our principal independent foundries and package assembly facilities are currently ISO 9001 certified, a comprehensive International Standards Organization specified quality system acknowledgment. As part of our total quality program, we received ISO 9001 certification for our Singapore distribution facility.

Environmental Management

We assess the environmental impact of our products to international standards. Our manufacturing subcontractors have registered our manufacturing flow to ISO 14000, the international standard related to environmental management. Lead-free solutions in electronic components and systems are receiving increasing attention within the semiconductor industry. Our products are compliant with the Restriction of Hazardous Substances Directive, or RoHS, the European legislation that restricts the use of a number of substances, including lead, and current European REACH (Regulation, Evaluation and Authorization of Chemicals) laws.

Product Distribution

Due largely to the location of our customers and their fabrication facilities, the majority of our products are shipped outside of the United States to customers through our distribution center in Singapore and a smaller portion within the United States via an operations and distribution center in Irvine, California. Net product revenue derived from actual shipments to international destinations, primarily in Asia represented 95.7%, 96.4% and 96.4% of our net revenue in 2014, 2013 and 2012, respectively.

Sales and Marketing

Our sales and marketing strategy is to achieve design wins with industry leaders by providing quality, state-of-the-art products and superior technical support. We market and sell our products in the United States through a direct sales force, but we also use distributors and manufacturers’ representatives. The majority of our domestic sales occur through our direct sales force, which is located in offices throughout the United States. We market and sell our products internationally through regional offices in Asia and Europe, as well as through a network of independent distributors and representatives in Asia, Australia, Europe, South Africa and South America. We or our customers select these independent entities based largely on their ability to provide effective sales and technical support to our customers. All international sales to date have been in U.S. dollars. We present revenue from independent customers by geographic area in Note 11 of Notes to Consolidated Financial Statements, included in Part IV, Item 15 of this Report.

Backlog

Our sales are primarily made through standard purchase orders for delivery of products. We follow industry practice that allows customers to cancel, change or defer orders with limited advance notice prior to shipment. Given this practice, we do not believe that backlog, by itself, is a reliable indicator of future revenue levels.

Competition

The semiconductor industry in general, and wired and wireless communications markets in particular, are intensely competitive and are characterized by constant innovation, rapid change, rapid cadence through technology standards, short product life cycles and steady price erosion. We believe that the principal factors of competition for integrated circuit providers in general, or their product offerings in particular, include:

8

• product quality and reputation | • market presence |

• product capabilities | • standards compliance |

• level of integration | • system cost |

• engineering execution and scale | • breadth of intellectual property |

• reliability | • customer interface and support |

• power efficiency | • time-to-market |

• circuit board footprint | • security |

We believe that we currently compete favorably with respect to each of these factors.

We compete with a number of major domestic and international suppliers of integrated circuits and related applications, including, but not limited to the following:

Broadband and Connectivity | Infrastructure and Networking |

• Intel Corporation | • Cavium, Inc. |

• Marvell Technology Group Ltd. | • Freescale Semiconductor,Ltd. |

• Mediatek Inc. | • Intel Corporation |

• Qualcomm Incorporation | • Marvell Technology Group Ltd. |

• STMicroelectronics NV | • Mellanox |

We also compete with suppliers of system-level and motherboard-level solutions incorporating integrated circuits that are proprietary or sourced from manufacturers other than Broadcom. This competition, along with Moore’s law, has resulted and may continue to result in declining average selling prices for our products in certain markets. We also may face competition from newly established competitors, suppliers of products based on new or emerging technologies, and customers that choose to develop their own silicon solutions.

Some of our competitors operate their own fabrication facilities and have longer operating histories and presence in key markets, greater name recognition, larger customer bases and significantly greater financial, sales and marketing, manufacturing, distribution and other resources than we do. As a result, these competitors may be able to adapt more quickly to new or emerging technologies and changes in customer requirements or devote greater resources to the promotion and sale of their products. Current and potential competitors have established or may establish financial or strategic relationships among themselves or with existing or potential customers, resellers or other third parties, and may refuse to provide us with information necessary to permit the interoperability of our products with theirs. Accordingly, it is possible that new competitors or alliances among competitors could emerge and rapidly acquire significant market share. In addition, competitors may develop technologies that more effectively address our markets with products that offer enhanced features, lower power requirements or lower costs. Increased competition could result in pricing pressures, decreased gross margins and loss of market share and may materially and adversely affect our business, financial condition and results of operations. See “Risk Factors” under Item 1A of this Report for further discussion of the risks associated with competition.

Seasonality

Our revenue, at both the consolidated and reportable segment level, is subject to some seasonal variation. Our revenue tends to be weaker in the first and fourth quarters of the calendar year and stronger in the middle of the calendar year. This trend is driven by multiple factors, including manufacturers preparing for the major holiday selling seasons. Our seasonality has varied significantly over time, which ultimately limits the usefulness of this metric as a predictive indicator of our revenue trend on a quarterly basis.

Intellectual Property

Our success and future product revenue growth depend, in part, on our ability to protect our intellectual property. We rely primarily on patents, copyrights, trademarks and trade secrets, as well as nondisclosure agreements and other methods, to protect our proprietary technologies and processes. However, these may not provide

9

meaningful or adequate protection for our intellectual property.

We currently hold more than 10,350 U.S. patents (up from more than 9,000 U.S. patents from the prior year) and more than 3,550 foreign patents and have more than 6,550 additional U.S. and foreign pending patent applications. We believe that no single patent is solely responsible for protecting our products and that the duration of our patents is adequate relative to the expected lives of our products.

We generally enter into confidentiality agreements with our employees and strategic partners, and typically control access to and distribution of product documentation and other proprietary information. Despite these precautions, it is possible that competitors or other unauthorized third parties may obtain, copy, use or disclose our technologies and processes, develop similar technology independently, or design around our patents. As such, any rights granted under our patents may not provide us with meaningful protection. In addition, we may not be able to successfully enforce our patents against infringing products in every jurisdiction. See “Risk Factors” under Item 1A of this Report for further discussion of the risks associated with patents and intellectual property.

Some or all of our patents have in the past been licensed and may in the future be licensed to certain of our competitors through cross-license agreements. Moreover, because we have participated and continue to participate in developing various industry standards, we may be required to license some of our patents to others, including competitors, who develop products based on those standards.

Companies in the semiconductor industry, particularly in the wired and wireless communications markets, often aggressively protect and pursue their intellectual property rights. We are currently engaged in litigation and may need to engage in future litigation to enforce or protect our intellectual property rights or the rights of our customers, to protect our trade secrets, or to determine the validity and scope of proprietary rights of others, including our customers. Such litigation could result in substantial costs and diversion of our resources and could materially and adversely affect our business, financial condition and results of operations. For a detailed description of various outstanding intellectual property litigation matters, see Note 8 of Notes to Consolidated Financial Statements, included in Part IV, Item 15 of this Report.

Employees

As of December 31, 2014 we had approximately 10,650 employees, including 8,000 individuals engaged in research and development, 1,000 engaged in sales and marketing, 700 engaged in manufacturing operations, and 950 engaged in general and administrative activities. Although we have works council or employee representatives in certain countries, our U.S. employees are not represented by a labor union.

Additional Information

Investors and others should note that we announce material financial information using our company website (www.broadcom.com), our investor relations website (investors.broadcom.com), SEC filings, press releases, public conference calls and webcasts. Information about Broadcom and our business may also be communicated in posts on the following social media channels:

• | B-Connected Blog (blog.broadcom.com) |

• | Broadcom’s Twitter feed (www.twitter.com/Broadcom) |

• | Broadcom’s Facebook page (www.facebook.com/Broadcom) |

The information that we post on these social media channels could be deemed to be material information. As a result, we encourage investors, the media, and others interested in Broadcom to review the information that we post on these social media channels. These channels may be updated from time to time on our website. The information on or accessible through our websites and social media channels is not incorporated by reference in this Annual Report on Form 10-K.

10

Item 1A. Risk Factors

Before deciding to purchase, hold or sell our common stock, you should carefully consider the risks described below in addition to the other information contained in this Report and in our other filings with the SEC, including subsequent reports on Forms 10-Q and 8-K. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also affect our business. If any of these known or unknown risks or uncertainties actually occurs with material adverse effects on Broadcom, our business, financial condition, results of operations and/or liquidity could be seriously harmed. In that event, the market price for our Class A common stock will likely decline, and you may lose all or part of your investment.

Our quarterly operating results may fluctuate significantly.

Our quarterly net revenue and operating results have fluctuated significantly in the past and may vary from quarter to quarter. Variability in the nature of our operating results may be attributed to the factors identified throughout this “Risk Factors” section, many of which may be outside our control, including:

• | changes in economic conditions in the markets we address, including the continuing volatility in the technology sector and semiconductor industry; |

• | our dependence on a few significant customers and/or design wins for a substantial portion of our revenue; |

• | our exit or entry into various markets and our ability to align our resources to areas of strategic focus; |

• | changes in customer product needs and market acceptance of our products; |

• | seasonality in sales of consumer and enterprise products in which our products are incorporated; |

• | timing, rescheduling or cancellation of significant customer orders and our ability, as well as the ability of our customers, to manage inventory; |

• | competitive pressures and other factors such as the qualification, availability and pricing of competing products and technologies and the resulting effects on sales and pricing of our products; |

• | goodwill and other purchased intangible impairment charges; |

• | the impact of a significant natural disaster, such as an earthquake, severe weather, tsunami or other flooding, or a nuclear crisis, as well as interruptions or shortages in the supply of utilities such as water and electricity, in a key location such as our corporate headquarters or our Northern California facilities, both of which are located near major earthquake fault lines, in our Singapore distribution center or in a key location of one of our suppliers, foundries or customers; |

• | the impact of enterprise system failures or network disruptions, the lack of system redundancies, and the potential failure of our disaster recovery planning to cover various unanticipated occurrences; and |

• | the impact of tax examinations. |

We depend on a few significant customers for a substantial portion of our revenue.

We derive a substantial portion of our revenue from sales to a relatively small number of customers. Contributions to our net revenue by these customers have increased in the last several years. Sales to our five largest customers represented 44.1%, 48.3% and 46.9% of our total net revenue in 2014, 2013 and 2012, respectively. Sales to two significant customers, those representing 10% or more of total net revenue, represented 28.2%, 34.6% and 31.9% of our total net revenue in 2014, 2013 and 2012, respectively. We expect that our largest customers will continue to account for a substantial portion of our total net revenue for the foreseeable future. The loss of any significant customer could materially and adversely affect our financial condition and results of operations. Also, as our significant customers become larger relative to our business and the industry, they may be able to leverage pricing pressure through the supply chain, vertical integration or other avenues, thereby adversely affecting our gross margins.

A significant portion of our revenue in any period may also depend on a single product design win with a large customer. As a result, the loss of any such key design win or any significant delay in the ramp of volume production of the customer’s products into which our product is designed could materially and adversely affect our financial

11

condition and results of operations. We may not be able to maintain sales to certain of our key customers or continue to secure key design wins for a variety of reasons, including:

• | agreements with our customers typically do not require them to purchase a minimum quantity of our products; and |

• | our customers can stop incorporating our products into their own products with limited notice to us and suffer little or no penalty. |

Additionally, in markets where we have a strong presence, our future growth will not necessarily be dependent on or correlate to our technical or design win success, but rather, may be dependent on (and may be constrained by) the growth rate of the overall market for the end product devices.

The loss of a key customer or design win, a reduction in sales to any key customer, a significant delay or negative development in our customers’ product development plans, or our inability to attract new significant customers or secure new key design wins could seriously impact our revenue and materially and adversely affect our results of operations.

We may fail to appropriately adjust our operations in response to changes in our strategy or market demand.

We significantly modified the scope of our operations and workforce in recent years. In response to changes in industry and market conditions, we may from time to time strategically realign our resources. These circumstances could cause the need to implement restructuring actions and other cost saving measures. Our operations are characterized by a high percentage of costs that are fixed or difficult to reduce in the short term, such as research and development expenses related to our highly skilled workforce.

During other periods, our growth has placed a significant strain on our management personnel, systems and resources. To respond to such periods of increased demand, we would need to expand, train, manage and motivate our workforce, and to upgrade or enhance our existing IT systems. For example, in response to prior periods of growth we began upgrading our enterprise resource planning system and expect to continue to do so during 2015. We may not be successful in implementing new systems, which could involve business disruptions, including impeding the shipment of our products. If we are unable to effectively manage expanding operations during growth periods, we may be unable to adjust our business quickly enough to meet competitive challenges or exploit potential market opportunities.

Any of these circumstances could materially and adversely affect our current or future business.

We face intense competition.

The semiconductor industry and the wired and wireless communications markets are intensely competitive. We expect competition to continue to increase as new markets develop, as industry standards become well known and as other competitors enter our business. We also expect to encounter further consolidation in the markets in which we compete.

Some of our competitors have longer operating histories and presences in key markets, greater name recognition, larger customer bases, and significantly greater financial, research and development, sales and marketing, manufacturing, distribution, technical and other resources than we do, and in some cases operate their own fabrication facilities. These competitors may be able to adapt more quickly to new or emerging technologies and changes in customer requirements. They may also be able to devote greater resources to the promotion and sale of their products. We also face competition from newly established competitors, suppliers of products, and customers who choose to develop their own semiconductor solutions.

Existing or new competitors may develop technologies that more effectively address our markets with products that offer enhanced features and functionality, lower power requirements, lower cost or greater levels of integration. The trend of increasingly integrated SoCs and chipset solutions in particular could pose a risk to various

12

lines of our business, especially with respect to our connectivity products, as customers may opt for a solution that includes functionality that was previously sourced from us on a standalone basis.

Increased competition also has resulted in and is likely to continue to result in increased expenditures on research and development, a decline in average selling prices, reduced gross margins and loss of market share in certain markets. These factors in turn create increased pressure to consolidate. We cannot provide assurance that we will be able to continue to compete successfully against current or new competitors. If we do not compete successfully, we may lose market share in our existing markets and our revenues may fail to increase or may decline.

We manufacture and sell complex products and may be unable to successfully develop and introduce new products.

We expect that a high percentage of our future sales will come from sales of new products. We sell products in markets that are characterized by rapid technological change, evolving industry standards, frequent new product introductions and sometimes short product life cycles. The markets for some of these products are new to us and may be immature and/or unpredictable. These markets may not develop into profitable opportunities and we have in the past invested substantial resources in emerging technologies that did not achieve the market acceptance or commercial success that we had expected. As a result, it is difficult to anticipate our future revenue streams from, or the sustainability of, our new products.

Our industry is dynamic and we are required to devote significant resources to research and development to remain competitive. Such costs increase with the advancement of technologies and manufacturing in smaller geometry processes, which can adversely affect our operating margin. The development of new silicon devices is highly complex, and due to supply chain cross-dependencies and other issues, we may experience delays in completing the development, production and introduction of our new products. We may choose to discontinue one or more products or product development programs to dedicate more resources to other products. The discontinuation of an existing or planned product may adversely affect our relationship with one or more of our customers and/or cause other negative consequences.

Our ability to successfully develop and deliver new products will depend on various factors, including our ability to:

•effectively identify and capitalize upon opportunities in new markets;

•timely complete and introduce new integrated products;

•transition our semiconductor products to increasingly smaller line width geometries;

•obtain sufficient foundry capacity (including at smaller geometry processes) and packaging materials;

•license any desired third party technology or intellectual property rights; and

•qualify and obtain industry interoperability certification of our products.

If we are not able to develop and introduce new products in a cost effective and timely manner, we will be unable to attract new customers or to retain our existing customers which would materially and adversely affect our results of operations.

We have experienced hardware and software defects and bugs associated with the introduction of our highly complex products. If any of our products contain defects or bugs, or have reliability, quality, security or compatibility problems, our reputation may be damaged and customers may be reluctant to buy our products. These problems could interrupt or delay sales and shipments of our products to customers. To alleviate these problems, we may have to divert our resources from other development efforts. In addition, these problems could result in claims against us by our customers or others, including possible claims for consequential damages and/or lost profits. As we transition to manufacturing our products in smaller geometry processes, such as 28 nanometers and below, these risks are enhanced.

13

We are exposed to risks associated with our international operations.

We currently obtain substantially all of our manufacturing, assembly and testing services from suppliers located outside the United States. Products shipped to international destinations, primarily in Asia, represented 95.7%, 96.4% and 96.4% of our product revenue in 2014, 2013 and 2012, respectively. Substantially all of our products are shipped through our logistical facilities in Singapore. An increasing portion of our product sales is made through international distributors, which increases our exposure to the risks described below. In addition, we undertake various sales and marketing activities through regional offices in a number of countries. We intend to continue expanding our international business activities and to open other design and operational centers abroad.

International operations are subject to many inherent risks, including but not limited to:

• | political, social and economic instability; |

• | exposure to different business practices and legal and compliance standards; |

• | continuation of overseas conflicts and the risk of terrorist attacks and resulting heightened security; |

• | the imposition of governmental controls and restrictions and unexpected changes in regulatory requirements; |

• | nationalization of business and blocking of cash flows; |

• | logistical delays or disruptions; |

• | changes in taxation and tariffs; and |

• | difficulties in staffing and managing international operations. |

Our international operations are subject to increasingly complex foreign and U.S. laws and regulations, including but not limited to anti-corruption laws, such as the Foreign Corrupt Practices Act and the UK Bribery Act and equivalent laws in other jurisdictions, antitrust or competition laws, and data privacy laws, among others. Violations of these laws and regulations could result in fines and penalties, criminal sanctions against us, our officers, or our employees, prohibitions on the conduct of our business and on our ability to offer our products and services in one or more countries, and could also materially affect our reputation, our international expansion efforts, our ability to attract and retain employees, our business, and our operating results. Although we have implemented policies, procedures and training designed to ensure compliance with these laws and regulations, there can be no complete assurance that any individual employee, contractor, or agent will not violate our policies. Additionally, the costs of complying with these laws (including the costs of investigations, auditing and monitoring) could also adversely affect our current or future business.

Economic conditions in our primary markets, particularly in Asia, may negatively impact the demand for our products in those geographies. Also, all of our international sales to date have been denominated in U.S. dollars. Accordingly, an increase in the value of the U.S. dollar relative to foreign currencies could make our products less competitive in international markets or require us to assume the risk of denominating certain sales in foreign currencies. We anticipate that these factors will impact our business to a greater degree as we further expand our international business activities.

Our operating results may be adversely impacted by worldwide economic uncertainties and specific conditions in the markets we address.

We operate primarily in the semiconductor industry, which is cyclical and subject to rapid change and evolving industry standards. From time to time, the semiconductor industry has experienced significant downturns characterized by decreases in product demand, excess customer inventories and accelerated erosion of prices. The semiconductor industry also periodically experiences increased demand and production capacity constraints, which may affect our ability to ship products. Economic volatility can cause extreme difficulties for our customers and vendors in accurately forecasting and planning future business activities. This unpredictability could cause our customers to reduce spending on our products and services, which would delay and lengthen sales cycles. Furthermore, during challenging economic times our customers and vendors may face challenges in gaining timely access to sufficient credit, which could impact their ability to make timely payments to us. As a result, we may experience growth patterns that are different than the demand for our customers’ products, particularly during

14

periods of high volatility.

We cannot predict the timing, strength or duration of any economic slowdown or recovery or the impact of such events on our customers, our vendors or us. The combination of our lengthy sales cycle coupled with challenging macroeconomic conditions and supply chain cross-dependencies could have a compound impact on our business. The impact of market volatility is not limited to revenue but may also affect our gross margins and other financial metrics. Any downturn in the semiconductor industry may be severe and prolonged, and any failure of the industry or wired and wireless communications markets to fully recover from downturns could seriously impact our revenue and harm our business, financial condition and results of operations.

We may be unable to attract, retain or motivate key personnel.

Our future success depends on our ability to attract, retain and motivate senior management and qualified technical personnel. Competition for these employees is intense. If we are unable to attract, retain and motivate such personnel in sufficient numbers and on a timely basis, we will experience difficulty in implementing our current business and product plans. In that event, we may be unable to successfully meet competitive challenges or to exploit potential market opportunities, which could adversely affect our business and results of operations. Our recent and any future restructuring plans may adversely impact our ability to attract and retain key employees.

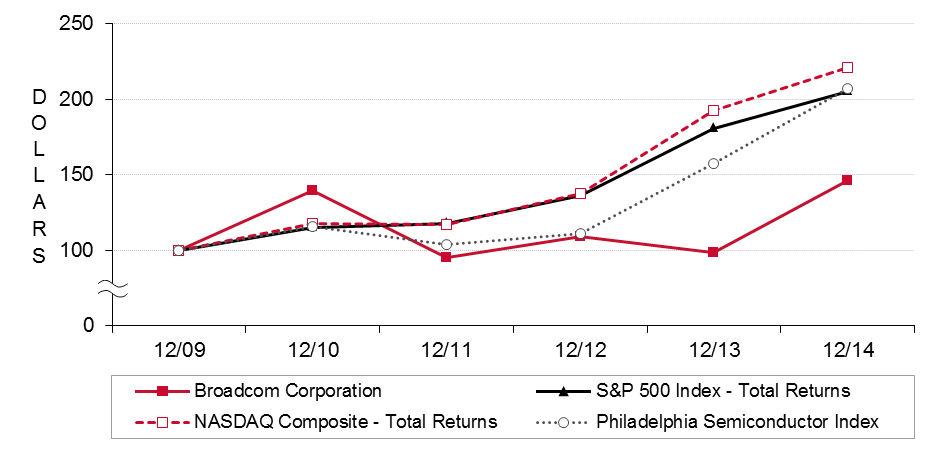

Our stock price is highly volatile.

The market price of our Class A common stock has fluctuated substantially in the past and is likely to continue to be highly volatile and subject to wide fluctuations. From January 1, 2012 through December 31, 2014 our Class A common stock has traded at prices as low as $23.25 and as high as $44.33 per share. Fluctuations have occurred and may continue to occur in response to various factors, many of which we cannot control.

In addition, the market prices of securities of semiconductor and other technology companies have been and remain volatile. This volatility has significantly affected the market prices of securities of many technology companies for reasons frequently unrelated to the operating performance of the specific companies. If our operating results do not meet the expectations of securities analysts or investors, who may derive their expectations by extrapolating data from recent historical operating results, our financial forecasts, or company presentations, then the market price of our Class A common stock will likely decline. Accordingly, you may not be able to resell your shares of common stock at or above the price you paid. In the past, we, and other companies that have experienced volatility in the market price of their securities, have been the subject of securities class action litigation.

Due to the nature of our compensation programs, most of our executive officers sell shares of our common stock periodically, often pursuant to trading plans established under Rule 10b5-1 of the Exchange Act. As a result, sales of shares by our executive officers may not be indicative of their respective opinions of Broadcom’s performance at the time of sale or of our potential future performance. Nonetheless, the market price of our stock may be affected by sales of shares by our executive officers.

Our business is subject to potential tax liabilities.

We are subject to income taxes in the United States and various foreign jurisdictions. The amount of income taxes we pay is subject to our interpretation and application of tax laws in jurisdictions in which we file. Changes in current or future laws or regulations, the imposition of new or changed tax laws or regulations or new related interpretations by taxing authorities in the U.S. or foreign jurisdictions, or changes in our tax planning strategies could adversely affect our results of operations and could lead to volatility with respect to tax expenses and liabilities from period to period. We are subject to examinations and tax audits. There can be no assurance that the outcomes from these audits will not have an adverse effect on our net operating loss and research and development tax credit carryforwards, our financial position, or our operating results.

15

We may be required to defend against alleged infringement of intellectual property rights of others and/or may be unable to adequately protect or enforce our own intellectual property rights.

Companies in the semiconductor industry, particularly those in the wired and wireless communications markets, aggressively protect and pursue their intellectual property rights. From time to time, we receive notices from competitors and other operating companies, as well as notices from “non-practicing entities,” or NPEs, that claim we have infringed upon, misappropriated or misused other parties’ proprietary rights. We may also be required to indemnify some customers and strategic partners under our agreements if a third party alleges or if a court finds that our products or activities have infringed upon, misappropriated or misused another party’s proprietary rights. We have received requests from certain customers and strategic partners to include increasingly broad indemnification provisions in our agreements with them. Additionally, our products may contain technology provided to us by other parties such as contractors, suppliers or customers. We may have little or no ability to determine in advance whether such technology infringes the intellectual property rights of a third party. Our contractors, suppliers and licensors may not be required to indemnify us in the event that a claim of infringement is asserted against us, or they may be required to indemnify us only up to a maximum amount, above which we would be responsible for any further costs or damages.

Furthermore, our success and future revenue growth will depend, in part, on our ability to protect our intellectual property. It is possible that competitors or other unauthorized third parties may obtain, copy, use or disclose our technologies and processes, or confidential employee, customer or supplier data. Any of our existing or future patents may be challenged, invalidated or circumvented. We engage in litigation to enforce or defend our intellectual property rights, protect our trade secrets, or determine the validity and scope of the proprietary rights of others, including our customers. We also enter into confidentiality agreements with our employees, consultants and strategic partners and control access to and distribution of our technologies, documentation and other proprietary information. Despite these efforts, internal or external parties may attempt to copy, disclose, obtain or use our products, services or technology without our authorization. If we cannot adequately protect our technology, our competitors may be able to offer products similar to ours.

Intellectual property litigation can be expensive, time consuming and distracting to management. An adverse determination in any of these types of disputes could prevent us from manufacturing or selling some of our products or could prevent us from enforcing our intellectual property rights. Settlements can involve royalty or other payments that could reduce our profit margins and adversely affect our financial results. Additionally, identifying unauthorized use of our products and technologies is difficult and time consuming. The initiation of litigation may adversely affect our relationships and agreements with certain customers that have a stake in the outcome of the litigation proceedings.

We face risks associated with our acquisition strategy.

An important element of our business strategy involves expansion through the acquisition of businesses, assets, products or technologies. The expansion of our business through acquisitions allows us to complement our existing product offerings, expand our market coverage, increase our engineering workforce and/or enhance our technological capabilities. We may not be able to identify or consummate future acquisitions or realize the desired benefit from these acquisitions.

We face a number of challenges associated with our acquisition strategy that could disrupt our ongoing business and distract our management team, including:

• | lower revenue, gross margins and operating income than originally anticipated at the time of acquisition and other financial challenges; |

• | delays in the timing and successful integration of an acquired company’s technologies and/or launch of products; |

• | the loss of key personnel; |

• | challenges in obtaining necessary transition services; and |

• | becoming subject to intellectual property or other litigation. |

16

Acquisitions can result in increased debt or contingent liabilities. While we believe we will be able to service any additional debt issued in connection with acquisitions, our ability to make principal and interest payments when due depends upon our future performance, which is subject to general economic conditions, industry cycles, and business and other factors affecting our operations, including the other risk factors described in this section, many of which are beyond our control. Acquisitions can also result in adverse tax consequences, warranty or product liability exposure related to acquired assets, additional stock-based compensation expense, write up of acquired inventory to fair value, and the recording and later amortization of amounts related to certain purchased intangible assets, all of which can adversely affect our reported results on a GAAP basis. Furthermore, we have in the past and may in the future record goodwill and other purchased intangible assets in connection with an acquisition and incur impairment charges.

We are subject to order and shipment uncertainties.

It is difficult to accurately predict demand for our semiconductor products. We typically sell products pursuant to purchase orders rather than long-term purchase commitments. Customers can generally cancel, change or defer purchase orders on short notice without incurring a significant penalty. Our ability to accurately forecast customer demand is further impaired by delays inherent in our lengthy sales cycle. We operate in a dynamic industry and use significant resources to develop new products for existing and new markets. After we have developed a product, there is no guarantee that our customers will integrate our product into their equipment or devices and, ultimately, bring those equipment and devices incorporating our product to market. In these situations, we may never produce or deliver a significant number of our products, even after incurring substantial development expenses. From the time a customer elects to integrate our solution into their product, it is typically six to 24 months before high volume production of that product commences. After volume production begins, we cannot be assured that the equipment or devices incorporating our product will gain market acceptance.

Our products are incorporated into complex devices and systems, creating supply chain cross-dependencies. Accordingly, supply chain disruptions affecting components of our customers’ devices and/or systems could negatively impact the demand for our products, even if the supply of our products is not directly affected.

Our product demand forecasts are based on multiple assumptions, each of which may introduce error into our estimates. In the event we overestimate customer demand, we may allocate resources to manufacturing products that we may not be able to sell. As a result, we could hold excess or obsolete inventory, which would reduce our profit margins and adversely affect our financial results. Conversely, if we underestimate customer demand or if insufficient manufacturing capacity is available, we could forego revenue opportunities and potentially lose market share and damage our customer relationships. Also, due to our industry’s use of “just-in-time” inventory management, any disruption in the supply chain could lead to more immediate shortages in product or component supply. Additionally, any enterprise system failures, including in connection with implementing new systems, could impact our ability to fulfill orders and interrupt other processes.

A portion of our inventory is maintained under hubbing and distribution arrangements whereby products are delivered to a customer or third party warehouse based upon the customer’s projected needs. Under these arrangements, we do not recognize product revenue until the customer reports that it has removed our product from the warehouse to incorporate into its end products. Our ability to effectively manage inventory levels may be impaired under such arrangements, which could increase expenses associated with insurance costs, excess and obsolete product inventory and negatively impact our cash flow.

We depend on third parties to fabricate, assemble and test our products.

As a fabless semiconductor company, we do not own or operate fabrication, assembly or test facilities. As a result, we face competition for manufacturing capacity in the open market. We rely on third parties to manufacture, assemble and test substantially all of our semiconductor devices. Accordingly, we cannot directly control our product delivery schedules and quality assurance. This lack of control could result in product shortages or quality assurance problems. These issues could delay shipments of our products or increase our assembly or testing costs. In

17

addition, the consolidation of foundry subcontractors, as well as the increasing capital intensity and complexity associated with fabrication in smaller process geometries has limited our diversity of suppliers and increased our risk of a “single point of failure.” Specifically, as we move to smaller geometries, we have become increasingly reliant on TSMC (Taiwan Semiconductor Manufacturing Company) for the manufacture of product at and below 40 nanometers. The lack of diversity of suppliers could also drive increased wafer prices, adversely affect our results of operations, including our gross margins.

We do not have long-term agreements with any of our direct or indirect suppliers, including our manufacturing, assembly or test subcontractors. We typically procure services from these suppliers on a per order basis. In the event our third-party foundry subcontractors experience a disruption or limitation of manufacturing, assembly or testing capacity, we may not be able to obtain alternative manufacturing, assembly and testing services in a timely manner, or at all. Furthermore, our foundries must have new manufacturing processes qualified if there is a disruption in an existing process, which could be time-consuming. We could experience significant delays in product shipments if we are required to find alternative manufacturers, assemblers or testers for our products. We are continuing to develop relationships with additional third-party subcontractors to assemble and test our products.

Because we rely on outside foundries and other third party suppliers, we face several significant risks in addition to those discussed above, including:

• | a lack of guaranteed supply of wafers and other components and potential higher wafer and component prices due to supply constraints; |

• | the limited availability of, or potential delays in obtaining access to, key process technologies; and |

• | the location of foundries and other suppliers in regions that are subject to earthquakes, tsunamis and other natural disasters. |

The manufacture of integrated circuits is a highly complex and technologically demanding process. Our foundries have from time to time experienced lower than anticipated manufacturing yields. This often occurs during the production of new products or the installation and start-up of new process technologies. In addition, we are dependent on our foundry subcontractors to successfully transition to smaller geometry processes.

Our systems are subject to security breaches and other cybersecurity incidents.

We experience cyber attacks of varying degrees on a regular basis, and as a result, unauthorized parties have obtained, and may in the future obtain, access to our computer systems and networks. Such cyber attacks could result in the misappropriation of our proprietary information and technology or interrupt our business. The reliability and security of our information technology infrastructure and software and our ability to expand and continually update technologies in response to our changing needs is critical to our business. To the extent that any disruptions or security breaches result in significant loss or damage to our data, or inappropriate disclosure of significant proprietary information, it could cause damage to our reputation and affect our relationships with our customers and ultimately harm our business.

Government regulation may adversely affect our business.

The effects of regulation on our customers or the industries in which they operate may materially and adversely impact our business. For example, regulatory policies of the Federal Communications Commission that affect the ability of cable or satellite operators or telephone companies to offer certain services to their customers could impede sales of our products in the United States. We and our customers are also subject to various import and export laws and regulations that apply to the encryption or other features contained in some of our products. If we fail to continue to comply with these regulations, we may be unable to manufacture the affected products at foreign foundries or ship these products to certain customers, or we may incur penalties or fines.

As described above under the risk factor entitled “We are exposed to risks associated with our international operations,” our business is also increasingly subject to complex foreign and U.S. laws and regulations, including but not limited to, anti-corruption laws, such as the Foreign Corrupt Practices Act and the UK Bribery Act and

18